A GENERALIZED THEIL-TORNQVIST INDEX FOR … · Comparisons Project of the Statistical Offices of...

28

A GENERALIZED THEIL-TORNQVIST INDEX FOR MULTILATERAL COMPARISONS D.S. Prasada Rao and E.A. Selvanathan No. 49 - November 1990 ISSN ISBN 0 157-0188 0 85834 904 3

Transcript of A GENERALIZED THEIL-TORNQVIST INDEX FOR … · Comparisons Project of the Statistical Offices of...

A GENERALIZED THEIL-TORNQVIST INDEX

FOR MULTILATERAL COMPARISONS

D.S. Prasada Rao and E.A. Selvanathan

No. 49 - November 1990

ISSN

ISBN

0 157-0188

0 85834 904 3

ABSTRACT

The Theil-Tornqvist index is a well-known index for binary

comparisons of cost-of-living. Properties of the Theil-Tornqvist index

are discussed in Diewert (1976, 1981) and recommended strongly for use in

comparisons of prices, real output and productivity (see Caves,

Christensen and Diewert, 1982). However the index, when applied in a

framework of multilateral comparisons, does not possess the property of

transitivity. The main purpose of this paper is to generalize the

Theil-Tornqvist index and derive a formula which is consistent and

base-invariant. The generalization makes use of a simple least-squares

interpretation of the Theil-Tornqvist index. This paper shows that the

resulting index uses the matrix of binary Theil-Tornqvist indices as

building blocks. The proposed method is illustrated using data from the

International Comparisons Project (ICP) of the United Nations. A further

generalization, which accounts for the economic distance between regions

or countries involved in the multilateral comparisons, and the resulting

index numbers are also discussed in the paper.

A GENERALIZED THEIL-TORNOVIST INDEX FOR MULTILATERAL COMPARISONS

D.S. Prasada Rao and E.A. Selvanathan

1. Introduction

The Theil-Tornqvist index is an essential element in the economic

theoretic approach to the construction of price and quantity index numbers.

This index, discussed in Tornqvist (1936), featured prominently in the

literature over the last two decades. Theil (1965) and Kloek and Theil (1965)

discuss various statistical properties of the index and attempt an

international comparisons exercise using the index. Eichorn and Voeller

(1983) establishes that the index satisfies a number of Fisher’s tests. In

the recent past, this index has been examined using the stochastic approach to

index numbers in Clements and Izan (1987) and Selvanathan (1989). The main

economic theoretic properties are expounded in a number of papers by Diewert.

Diewert (1976, 1981) and Caves, Christensen and Diewert (1982a, 1982b)

establish the "exact" and "superlative" nature of the index, and consequently

it is strongly recommended for use in the comparisons of prices, output,

inputs and productivity.

The Theil-Tornqvist index is essentially a binary index for use in the

comparisons of prices and quantities involving two sets of prices. Despite

its prominence and elegant statistical and economic theoretic properties, this

index has not played any role in the context of international comparisons

which involve multilateral comparisons of prices and quantities. This is

essentially due to the fact that this index does not satisfy the crucial

property of transitivity and symmetry [for details see Kravis et al. (1975,

1978 and 1982)].

In this paper we provide two generalizations of the Theil-Tornqvist

binary index and derive multilateral index number formulae that satisfy the

transitivity and symmetry requirements. A number of properties of the

formulae derived here are also discussed along with numerical illustrations

based on aggregated data from the Phase IV exercise of the International

Comparisons Project of the Statistical Offices of the United Nations and the

European Economic Community (U.N., 1987).

2

A brief outline of the paper is as follows: Section 2 discusses the

problem of multilateral comparisons and describes the transitivity and

symmetry requirements. Section 3 provides a brief description of the

Theil-Tornqvist index for binary comparisons and its properties. An

alternative interpretation of the index is provided using the stochastic

approach in Clements and Izan (1987). In Section 4, a generalized

Theil-Tornqvist index for multilateral comparisons is derived using the

stochastic approach. A number of properties of the new index are also

discussed in the section. A numerical illustration providing a comparison of

binary and generalized multilateral Theil-Tornqvist indices is included.

Section 5 proposes a further generalization which leads to another

multilateral system of index numbers. The last section provides some

concluding remarks and points towards possible future research in this area.

2. The Problem of Multilateral Comparisons

Let (~i’ ~I)’ (~2’ ~2) ..... (~M’ ~M) denote M pairs of price and

quantity vectors of dimension N, where M may typically refer to regions within

a country or countries or time periods and N represents the number of

commodities. The case where M = 2 refers to binary comparisons and M z 3

refers to multilateral comparisons.

The basic assumptions made in the paper are: (i) ~pj > 0 for all j;

(ii) q~j -~ 0 for all j; and (iii) for each i, there is at least one j such

that ql] > O.

The main problem is to construct price and quantity index numbers Ikj’

index for j with k as base, such that the transitivity and symmetry conditions

are satisfied. These conditions are defined below.

Definition: An index number formula I is said to be transitive if and only

if all pairwise comparisons I (k,j = 1,2 ..... M), are such thatkj

Ikj = Ik~ . l~j (I)

for all triplets k, j and ~.

Definition: An index I is symmetric if all countries are treatedkj

symmetrically and a comparison of two countries is invariant to any

permutations in which the rest of the countries are considered.

The index I discussed above is essentially in multiplicative form.kJ

However bulk of Theil’s work is in terms of log-change index numbers, [I kj’

where ~[ = ~n I Then the transitivity condition may be stated askJ k J"

in terms of log-change index numbers.

In Sections 4 and 5 two index number formulae for multilateral

comparisons are proposed that satisfy the requirements in stated in (i) and

C2).

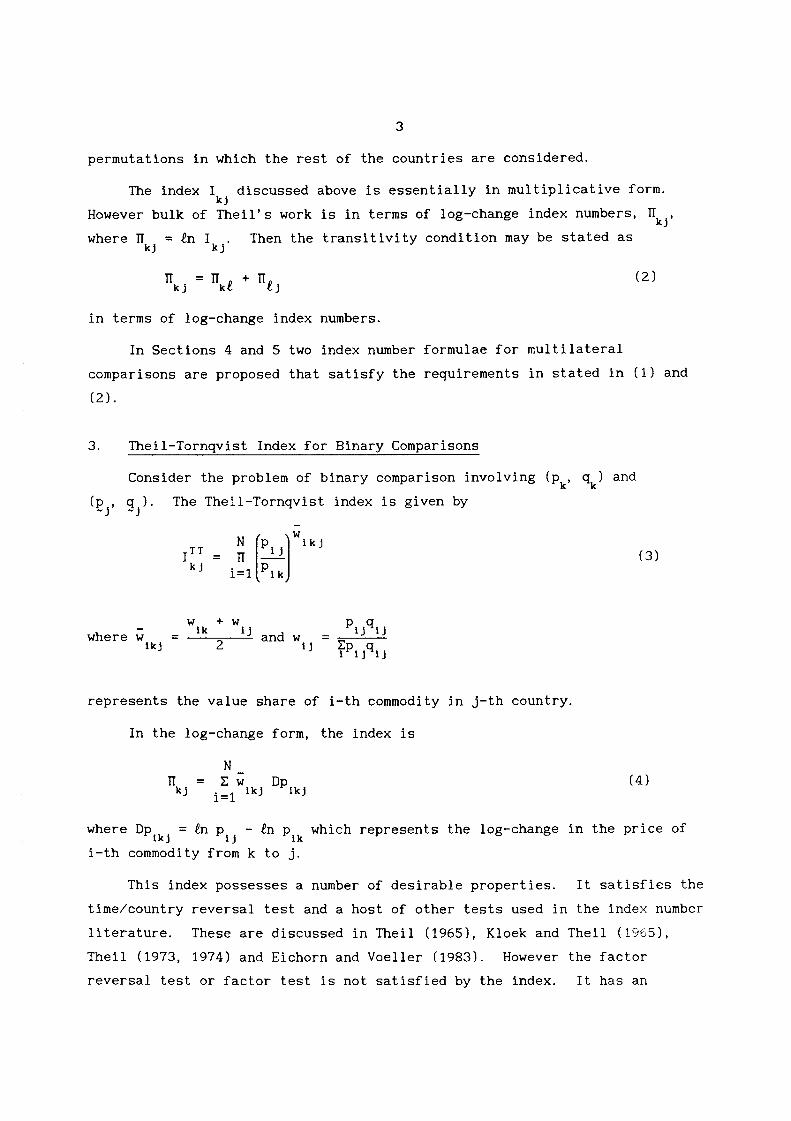

3. Theil-Tornqvist Index for Binary Comparisons

Consider the problem of binary comparison involving (Pk’ qk) and

(~pj, q~j). The Theil-Tornqvist index is given by

N PIj ikj

(3)

W + Wpljqljwhere w ik tJ and wtkj 2 tJ l~pi jqij

represents the value share of i-th commodity in j-th country.

In the log-change form, the index is

N= E w DPlkjUkJ i=1 Ikj

(4)

where DPlkj = tn Plj - gn Plk which represents the log-change in the price of

i-th commodity from k to j.

This index possesses a number of desirable properties. It satisfies the

time/country reversal test and a host of other tests used in the index number

literature. These are discussed in Theil (1965), Kloek and Theil (1965),

Theil (1973, 1974) and Eichorn and Voeller (1983). However the factor

reversal test or factor test is not satisfied by the index. It has an

4

impressive array of economic theoretic properties, and for a discussion of

these the reader is referred to Diewert (1976 and 1981).

Stochastic approach

The Theil-Tornqvist index can be derived using a regression model based

on price differences for each commodity.

Consider the log-change in price of commodity i from k to j, DPlkj.

Following Clements and Izan (1987), for a pair k and j, we write

DPlkJ = ]’[kj + UikJ i = 1,2 ..... N (5)

The parameter [I may be interpreted as a measure of the common trend ink]

prices of all N commodities. The disturbances u are assumed to have the

following properties:

2

(i) E(Ulkj) = O; (ii) V(Ulkj) --0"

W

and cov (u Ikj’ Ui’k’ J’ ) = 0 for all i ~ i’, k ~ k’

(6)

The generalized least squares estimator of ~kJ

]’[kj = i~ Wikj DPlkJ

in (5) is given by

which is a weighted arithmetic average of DPlkj (i = 1,2 ..... N). This is

identical to the log-change index in equation (4).

However, the main problem in using the Theil-Tornqvist index in (3) and

(4) for multilateral comparisons is that the indices based on this formula for

all pairs k and j do not satisfy transitivity conditions. This makes this

index inapplicable for comparisons involving a set of three or more regions or

countries. In the following section we derive a generalization of the index

for multilateral comparisons.

4. A Generalization of the Theil-Tornqvist Index

In this section the alternative interpretation of the Theil-Tornqvist

index, as a generalized least squares estimator from the regression model,

based on the stochastic approach is pursued further to obtain a

generalization.

Suppose we postulate the model

DPlkJ = 11kJ + Ulkj i = 1,2 ..... N

for all pairs of regions k and j (k,j = 1,2 ..... M). However the resulting

II would not satisfy transitivity. Then transitivity may be imposed on the

model above in the form of a set of homogeneous linear restrictions of the

form,

for all k, j and ~

But it is simpler to substitute the restrictions into the regression model

and use the restricted model for parameter estimation. The following result

is useful in obtaining a workable form for the restricted model.

Result: An index number formula ]’[kj’ for all k and j, satisfies transitivity

in log-change form if and only if there exist real numbers 111’ 112 ..... 11M

such that II = II - II .

Proof: If part is straightforward. To establish the only if part suppose

II is transitive then define,kj

= 11 ; II = II .... 1I = 11 .Ill 11 2 12 M IM

Obviously 11 = O. Using these numbers 11 and transitivity, everyjexpressed as II - II .

can be

Based on this result, the restricted regression model incorporating all

the restrictions is given by

+ u (7)DPlkj = gj - 11k IkJ

i = 1,2 ..... N; k = 1,2 ..... M; j = k+l ..... M

6

and the disturbance term u has the same properties outlined in (6).

generalized least squares estimators of HI,H2 ..... HM may be obtained by

applying ordinary least squares to the transformed model below.

The

Transformed Model:

This may be expressed in the form of a linear regression model as

Y=XII + u~ (8)

where ~ = [~~’~2 ..... UM]’ is a vector of unknown parameters.

Application of least squares to the transformed model yields the normal

equations:

^

X’X]] = X’¥ (9)

using the symmetry w = wik] iJk’

(M-l) -I . .. -1

-I (M-l) ... -1

-I -I ... (M-I)

it can be shown that

and X’Y =M×I

M N _E Z w log --

j=1 i=l i~] P~]

M N _ PiMZ Z w log --

j=l i=1 ~M] P~]

^

Solution of U from (9) depends on rank of X’X. It can be seen that X’X is

singular and Rank (X’X) = M-I. This indicates presence of multicollinearity

and implies that original parameter vector U in (8) is not identified.

The following results are useful in deriving the best linear unbiased

estimator of ~ - N.j k

Result I: All linear combinations of the form H - H are estimable.] k

~ - ~ may be expressed as w’H where w’ = [0 0 .. I j o.. k -i 0 .. O] with 1

and -I in j-th and k-th places respectively and following Schmidt (1986)

7

is estimable since there exists a vector k such that X’XA = w.

may use 2% = [0 0 .. I/M -I/M 0 .. 0]’

For this w, we

^ ^

Result 2: The BLUE of N - N is given by U - ~ where ~ is any solution ofj k J k

the normal equations (9) and the resulting estimator is unique.

^

Result 3: Since rank of X’X is M-l, we set ~ = 0 and solve for

~M-I uniquely.

Using Results 1, 2 and 3 the required estimators are given by

= Z ~. ~ log ik -If] = IIj - IIMk=l i=l I Mk P~M +k=lY" i=lZ w

^

and :[ = O. (I0)M

The solution ~ may be interpreted essentially as a log-change index forJ

j with base M. Expressing this in a multiplicative form, the index may be

expressed in general, for any j and k, as

M N Pi~ Wik~ ].[ PlJ Wi~j ~I~ = F[

__I/ ---- (II)

kJ ~=I i 1 Plk i=l P~

The index number formula, I* is the generalized Theil-Tornqvist index whichkj’

provides a multivariate generalization of the Theil-Tornqvist index.

Properties of the New Index

The following properties can be easily established for the generalized

Theil-Tornqvist index in equation (II).

Property 1: The index I* satisfies the transitivity condition.kj

This can be proved by simply using (II) in conjunction with transitivity

condition defined in (I).

Property 2: I~ satisfies the country symmetry or base invariance, property.kj

As I~ uses all the countries in the simple geometric mean defined in (ii),kj

any permutation of countries would not alter I~kj"

8

Property 3: Using the formula for the binary Theil-Tornqvist index, ITT inkj’

equation (3), I~ may be written askJ

Equation (12) provides a very useful interpretation of the generalized index

derived here. I~ is a simple geometric mean of M indirect comparisonskJbetween k and j, where each indirect comparison is made through a country ~

(~ = 1,2 ..... M) using the binary formula. Incidentally indirect comparisons

based on chains of more than one country lead to the same index I~ in (12).kJ

Property 4: I* (for k,j = 1,2 ..... M) provides a multilateral index that iskJ

transitive and has minimum distance from the binary indices. That is, if we

consider the problem of finding I such thatkJ

7~ Z log I - logk=l j=l k]

is minimum subject to the restriction Ikj = Ik~.I~], then I*kj is the solution

to this problem.

Proof of this follows from a similar result in Prasada Rao and Banerjee

(1986).

Property 5: As I* is obtained from a regresion model, it would be possiblekJ

to compute the standard errors associated with I* which can be used in

constructing confidence intervals for the indices obtained.

Among the properties of I~ discussed above, the most important is

Property 4 which establishes that I* deviates least from the binary index

IIT. This implies that any other multilateral index would deviate from ITT

more than I* . In view of the many statistical and, more importantly,kj

economic theoretic properties of the binary Theil-Tornqvist index, the

multilateral index derived here retains the essential features of the binary

index.

A numerical illustration

The following illustration uses the price and quantity data for eight

broadly defined commodity groups for 60 countries included in the Phase IV -

1980 of the International Comparisons Project of the U.N. Statistical Office.

The Table below shows the results from the binary and generalized multilateral

versions of the Theil-Tornqvist index for all the countries with the United

States as the base country. The official exchange rates are also presented

for purposes of comparison.

The results show, firstly, that the Theil-Tornqvist indices deviate

substantially from the official exchange rates. Second, there is no

appreciable difference between binary and the generalized Theil-Tornqvist

indices which demonstrates the minimum distance property of I~ derived here.kj

Table 1

Theil-Tornqvist Exchange Rates, Purchasing Power Parities and

Official Exchange Rates, 1980

CountryCurrency

Theil-Tornqvist IndexOfficial

Unit Exchange RatesBinary Generalized

I. USA2. Belgium3. Denmark4. France5. Germany6. Greece7. Ireland8. Italy9. LuxembourgI0. NetherlandsII. United Kingdom12. Austria13. Finland1415161718192021

HungaryNorwayPolandPortugalSpainYugoslaviaBotswanaCameroon

US DollarsFrancsKronerFrancsD. MarkDrachmaeIr PoundsLifeFrancsGuildersPoundsSchillingsMarkkaaForintKronerZlotychEscudosPesetasDinarsPulaFrancs

I 000037 1513

7 75125 32872 4580

36 17450.4747

752.661634.2014

2.45130.4843

15.20334.4228

12.37186.6225

17.529332.647065.317318.41790.6171

201.3285

1.0000 1.0037.3132 29.243

7.9555 5.63595.3769 4.22602.4459 1.8177

35.3057 42.6170.4866 0.4859

759.1463 856.5034.0850 29.243

2.4590 1.98810.4923 0.4303

15.4664 12.9384.5979 3.7301

13.2421 32.7336.8146 4.9392

18.3362 31.05132.4902 50.06263.7134 71.7719.2265 24.9110.5968 0.7769

199.9959 211.30

10

Table 1 (cont.)

CountryCurrency

Unit

Theil-Tornqvist Index

Binary Generalized

OfficialExchange Rates

22. Ethiopia23. Cote d’ivoire24. Kenya25. Madagascar26. Malawi27. Mall28. Morocco29. Nigeria30. Senegal31. Tanzania32. Tunisia33. Zambia34. Zimbabwe35. Israel36. Hong Kong37. India38. Indonesia39. Japan40. Korea41. Pakistan42. Philippines43. Sri Lanka44. Argentina45. Bolivia46. Brazil47. Chile48. Colombia49. Costa Rica50. Dominican Rep.51. Ecuador52. E1 Salvador53. Guatemala54. Honduras55. Panama56. Paraguay57. Peru58. Uruguay59. Venezuela60. Canada

BirrFrancsShillingsFrancsKwachaFrancsDirhamsNairaFrancsShillingsDinarsKwachaDollarsShekelsHK DollarsRupeesRupiahsYenWonRupeesPesosRupeesPesosPesosCruzeirosPesosPesosColonesDollarsSucresColonesQuetzalesLempirasBalboasGuaraniesSolesNew PesosBolivaresDollars

1.0842 1.0421229.4047 217.0487

4.8078 4.7044150.3823 143.4935

0.4607 0.4164294.9225 271.7350

2.9622 2.85290.6794 0.6570

185.2384 171.19136.4799 6.45490.2744 0.26750.8242 0.77210.5292 0.50264.1781 4.27583.4736 3.49813.3975 3.4152

286.8827 284.8610241.8619 257.8033418.7953 416.6591

3.0183 3.07822.8837 2.97473.4541 3.7341

2695.6340 2544.751017.6344 16.882632.4467 30.991830.7376 30.754820.6466 20.9612

5.4415 5.75300.5724 0.5856

14.8215 14.66651.2779 1.34410.4263 0.46111.0730 1.08420.6482 0.6404

83.8193 81.0953132.2637 133.2354

7.9802 7.90893.0240 3.25641.0184 1.0655

7.

O.422.

3.O.

8.O.O.O.557

626226607

97

161837

24.5239478

2521

083.

129.7.3.

0730420230812160936754653019540578856425124O08639974439O51145342O517139O02857O0O05OO012564876O5814169

II

5. A Further Generalization of the Theil-Tornqvist Index

The generalization considered in this section is prompted by the fact

that I~ in the previous section, in equations (11) and (12), is a simplekJ

geometric mean of all indirect comparisons between k and j. However,

intuition suggests that some indirect comparisons would be instrinsically

more reliable than others. For example, if k refers to USA and j refers to

the UK, then an indirect comparison between the USA and the UK through France

would be more reliable than a comparison through India.

To achieve this, the basic regression model is postulated with

disturbances exhibiting a more general form of heteroscedasticity. This uses

the concept of economic distance between j and k based on the tea! per capita

incomes associated with j and k. Let E be the nominal income in j then

E /I would convert j-th per capita income into the currency unit of I.

Then the distance 82 between j and k may be defined as

kj [ ( l J) ( IkJJ

-2= log Ej log l~j log Ek Ik

= log Ej - ]’[j log Ek - Ilk (13)

the last equality following from the transitivity of I

Based on this concept of economic distance, we postulate a regression

model

DPtkj + u (14)= ]’[j - ]’[k Ikj

with2

E(u ) = 0 V(u ) - ¢ 82ikj ikj - kJ

WIkJ

E(Ulkj Ul,k,j,) = 0for i ~ i’, k ~ k’ and j # j’.

As 62 depends upon r[ - II we may use the fol!owing two step procedure:j k’

12

Step I: Obtain initial estimate of I[ - [[ from the model in the previous

section and obtain^ 82 as

;~3 -- (log ~3- log ~.k) - (n3 - ~ ~

Step 2: Using ~2 k3’ apply ordinary least squares method to the transformedmodel:

= - + u~ (15)

Least squares method then leads to the normal equations

^

X’X[I = X’Y (16)

where X’X =M

-1/~2 E 1/8^2 ... -1/~212 j=1 23 2M

~2M

-IA~ -I/~~ ... z i/?IM 2M MJj:l

~M

(17)

Again it can be seen that X’X is singular and Rank(X’X) = M-I which implies

that components of H are not identifiable.

Following a procedure similar to that employed in Section 3, it is

feasible to obtain the best linear unbiased estimator of any linearA ^

combination of the form (~ - n ). This is given by (H - ~ ) where^ J k j k

(~I’ ~2 ..... ~M) is any solution to the normal equation (16). In view of

the form of (X’X), no useful explicit formula could be derived. However, for

the simple case of M=3, the indices in the multiplicative form with base 3

are given by

13

This can be expressed in terms of binary Theil-Tornqvist indices ITT askJ

I*" =r IITT ITT rlTT (is)

As ~2 is a direct distance between 1 and 3 and from the triangular13

inequality ~2 + ~2 is greater than or equal to ~2 . This means that I~* is12 23 13 3 1

a weighted geometric mean of the direct comparison ITT and indirect

[ITT ITT] 31comparison [ 32 " 21j’ and the direct comparison is accorded a larger weight

which is consistent with intuition.

However we have been unable to derive expressions similar to (18) in the

most general case but work is in progress in this direction.

6. Conclusions

In this paper two new sets of index numbers for multilateral comparisons

have been proposed. These formulae are derived using the regression model

underlying the well-known Theil-Tornqvist index. The indices discussed here

are transitive and base invariant and possess the usual least squares

properties. Further these indices are shown to use the Theil-Tornqvist

binary indices as building blocks. The new indices are illustrated using

aggregated data from the International Comparisons Project. From this paper

it appears that the indices proposed here could provide viable alternative

aggregation procedures for multilateral comparisons with attractive

properties. It is evident from Section 5 that a further examination of the

regression model could yield more meaningful index number formulae.

14

REFERENCES

Caves, D.W., L.R. Christensen and W.E. Diewert (1982a). "Multilateral

Comparisons of Output, Input and Productivity Using Superlative Index

Numbers", Economic Journal, Voi.92, 73-86.

Caves, D.W., L.R. Christensen and W.E. Diewert (1982b). "The Economic Theory

of Index Numbers and the Measurement of Input, Output and Productivity",

Econometrica, Vol.50, 1393-1414.

Clements, K.W. and H.Y. Izan (1987). "The Measurement of Inflation: A

Stochastic Approach", Journal of Business and Economic Statistics, Vol.5,

339-350.

Diewert, W.E. (1976). "Exact and Superlative Index Numbers", Journal of

Econometrics, Vol.4, 115-145.

Diewert, W.E. (1981). "The Economic Theory of Index Numbers: A Survey", in

Essays in the Theory and Measurement of Consumer Behaviour, Deaton, A.

(Ed.), 163-208.

Eichhorn, W. and J. Voeller (1983). "Axiomatic Foundations of Price Indexes

and Purchasing Power Parities", in Price Level Measurement, Eds.

W.E. Diewert and C. Montamarquette, Statistics Canada, Ottawa.

Kloek, J. and H. Theil (1965). "International Comparisons of Prices and

Quantities Consumed", Econometrica, Voi. 33, No.4, 535-556.

Prasada Rao, D.S. and K.S. Banerjee (1986). "A Multilateral System of Index

Numbers Based on Factorial Approach", Statistiche Hefte, Voi.27, 297-312.

Selvanathan, E.A. (1989). "A Note on the Stochastic Approach to Index

Numbers", Journal of Business and Economic Statistics, Vol.7, 471-474.

Theil, H. (1965). "The Information Approach to Demand Analysis",

Econometrica, Voi.33, 67-87.

Theil, H. (1973). "A New Index Number Formula", Review of Economics and

Statistics, Voi.53, 498-502.

15

Theil, H. (1974). "More on Log-change Index Numbers", Review of Economics

and Statistics, Voi.54, 552-554.

Tornqvist, L. (1936). "The Bank of Finland’s Consumption Price Index", Bank

of Finland Monthly Bulletin, No. lO, 1-8.

United Nations (1987). World Comparisons of Purchasing Power and Real Product

for 1980. Part 2. New York.

WORKING PAPERS IN ECONOMETRICS AND APPLIED STATISTICS

~o2.~ir_~ ~ia2.o~ A~o~. Lung-Fei Lee and William E. Griffiths,No. I - March 1979.

Howard E. Doran and Rozany R. Deen, No. 2 - March 1979.

HaZe on ~ Za~ @atiznaZon ~n aa ~ @anon 2~ade/.William Griffiths and Dan Dao, No. 3 - April 1979.

~eirda:. G.E. Battese and W.E. Griffiths, No. 4 - April 1979.

D.S. Prasada Rao, No. 5 - April 1979.

H~ Req~ ~edega. George E. Battese andBruce P. Bonyhady, No. 7 - September 1979.

Howard E. Doran and David F. Williams, No. 8 - September 1979.

D.S. Prasada Rao, No. 9 - October 1980.

~ Do/~ - 1979. W.F. Shepherd and D.S. Prasada Rao,No. 10 - October 1980.

a~2A ~o~aad HeqA~.Lb~~ R~o/ca. W.E. Griffiths andJ.R. Anderson, No. II - December 1980.

£0~-0~-~ Yeai~n ~he ~aeaeaceo~ ~~. Howard E. Doranand Jan Kmenta, No. 12 - April 1981.

~irva£ Oadea ~/~£oz~eg~~g~. H.E. Doran and W.E. Griffiths,No. 13 - June 1981.

Pauline Beesley, No. 14 - July 1981.

Yoia~ Dola. George E. Battese and Wayne A. Fuller, No. 15 - February1982.

~~. H.I. Toft and P.A. Cassidy, No. 16 - February 1985.

H.E. Doran, No. 17 - February 1985.

J.W.B. Guise and P.A.A. Beesley, No. 18 - February 1985.

W.E. Griffiths and K. Surekha, No. 19- August 1985.

~~ ~aZce~. D.S. Prasada Rao, No. 20 - October 1985.

H.E. Doran, No. 21- November 1985.

~e-~emi ~~Nm~ ~ZAe ~,u~ ~ed2/. William E. Griffiths,R. Carter Hill and Peter J. Pope, No. 22 - November 1985.

~~o~ ~a~ ~9inn. William E. Griffiths, No. 23 - February1986.

~ Doi~ #ndu~7~. T.J. Coelli and G.E. Battese. No. 24 -February 1986.

~a~ ~u~ ~aing ~DoJ~. George E. Battese andSohail J. Malik, No. 25 - April 1986.

George E. Battese and Sohail J. Malik, No. 26 - April 1986.

~~. George E. Battese and Sohail J. Malik, No. 27 - May 1986.

George E. Battese, No. 28- June 1986.

~u~. D.S. Prasada Rao and J. Salazar-Carrillo, No. 29 - August1986.

WIE. Griffiths and P.A. Beesley, No. 30 - August 1987.

William E. Griffiths, No. 31 - November 1987.

H.E. Doran,

3

Chris M. Alaouze, No. 32 - September, 1988.

G.E. Battese, T.J. Coelli and T.C. Colby, No. 33- January, 1989.

~OA~g~. Tim J. Coelli, No. 34- February, 1989.

No. 35 - February, 1989.Colin P. Hargreaves,

William Griffiths and George Judge, No. 36 - February, 1989,

~Pp~~ Woie~ ~ ~ao/sI2_n~. Chris M. Alaouze, No. 38 -July, 1989.

Chris M. Alaouze and Campbell R. Fitzpatrick, No. 39 - August, 1989.

Doi~. Guang H. Wan, William E. Griffiths and Jock R. Anderson, No. 40 -September 1989.

o~ ~~m~ed ~ea~ Op~’u:zZian. Chris M. Alaouze, No. 41 - November,1989.

~ ~Aeo~ ~ £g~ Mp~. William Griffiths andHelmut Lfitkepohl, No. 42 - March 1990.

Howard E. Doran, No. 43 - March 1990.

~ain~ Yhe XoInu~n 5igtea ~a ga~£aA-~ap~. Howard E. Doran,No. 44 - March 1990.

~e~. Howard Doran, No. 45 - May, 1990.

Howard Doran and Jan Kmenta, No. 46 - May, 1990.

~~ ~~and ~nZan/~Zena2 ~aice~. D.S. Prasada Rao andE.A. Selvanathan, No. 47 - September, 1990.

~c_anx:uni~ YZudieaoiZAe~~ ~:~e!~ @agIand. D.M. Dancer andH.E. Doran, No. 48 - September, 1990.

D.S. Prasada Rao and E.A. Selvanathan, No. 49 - November, 1990.