A F S Arrowsmith Fund, Ltd. Year Ended December 31, 2014 ... Fund... · Independent Auditors’...

42

AUDITED FINANCIAL STATEMENTS Arrowsmith Fund, Ltd. Year Ended December 31, 2014 With Independent Auditors’ Report

Transcript of A F S Arrowsmith Fund, Ltd. Year Ended December 31, 2014 ... Fund... · Independent Auditors’...

AUDITED FINANCIAL STATEMENTS Arrowsmith Fund, Ltd. Year Ended December 31, 2014 With Independent Auditors’ Report

Arrowsmith Fund, Ltd.

Audited Financial Statements

Year Ended December 31, 2014

Contents Independent Auditors’ Report ..................................................................................................... 1 Statement of Financial Position ................................................................................................... 3 Statement of Comprehensive Income .......................................................................................... 4 Statement of Changes in Net Assets Attributable to Holders of Redeemable Participating Shares ................................................................................................................. 5 Statement of Cash Flows ............................................................................................................. 6 Condensed Schedule of Investments ............................................................................................ 7 Notes to Financial Statements ................................................................................................... 15

1

Independent Auditors’ Report

The Directors Arrowsmith Fund, Ltd.

We have audited the accompanying financial statements of Arrowsmith Fund, Ltd. (the Fund) which comprise the statement of financial position, including the condensed schedule of investments as at December 31, 2014, and the related statement of comprehensive income, statement of changes in net assets attributable to holders of redeemable participating shares and statement of cash flows for the year then ended, and a summary of significant accounting policies and other explanatory information.

Management’s Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these financial statements in accordance with International Financial Reporting Standards, and for such internal control as management determines is necessary to enable the preparation of financial statements that are free from material misstatement, whether due to fraud or error.

Auditors’ Responsibility

Our responsibility is to express an opinion on these financial statements based on our audit. We conducted our audit in accordance with International Standards on Auditing. Those standards require that we comply with ethical requirements and plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditors’ judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made by management, as well as evaluating the overall presentation of the financial statements.

Ernst & Young One Montague Place East Bay Street P.O. Box N-3231 Nassau Bahamas

Tel: +242 502 6000 Fax: +242 502 6090 ey.com

2

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

Opinion

In our opinion, the accompanying financial statements present fairly, in all material respects, the financial position of the Arrowsmith Fund, Ltd. as at December 31, 2014, and of its financial performance and cash flows for the year then ended in accordance with International Financial Reporting Standards.

September 2, 2015

Arrowsmith Fund, Ltd.

Statement of Financial Position (Expressed in United States Dollars)

3

December 31 2014 2013 Assets Cash at bank and brokers (Note 3) $ 14,957,626 $ 15,469,222 Investments at fair value (cost – $44,368,159; 2013 – $38,683,521) (Note 4) 47,945,549 41,957,980 Receivables for investments sold 666,848 1,034,353 Investments made in advance 6,010,000 1,000,000 Other receivables 212,616 426,705 Total assets $ 69,792,639 $ 59,888,260 Liabilities Due to Portfolio Manager (Note 5) $ 48,393 $ 248,846 Long term borrowings (Note 6) 2,000,000 2,000,000 Interest payable 10,000 10,000 Payable for investments purchased 1,000 588,839 Proceeds from sale of participating preferred shares received in advance – 1,150,000 Redemptions payable 2,371,259 2,809,797 Net assets attributable to holders of redeemable participating preferred shares – Class A (Note 7) 64,720,351 48,805,208 Net assets attributable to holders of redeemable participating preferred shares – Class B (Note 7) 641,536 4,275,470 Total liabilities 69,792,539 59,888,160 Shareholder’s equity (Note 7) Attributable to common shares 100 100 Total liabilities and shareholder’s equity $ 69,792,639 $ 59,888,260 Redeemable participating preferred shares outstanding and net asset value per share (Note 7) Class A shares outstanding 3,903 2,866 Class B shares outstanding 471 3,073 Net asset value per share Class A $ 16,582.23 $ 17,029.07 Net asset value per share Class B $ 1,362.07 $ 1,391.30 See accompanying notes.

Arrowsmith Fund, Ltd.

Statement of Comprehensive Income (Expressed in United States Dollars)

4

Year Ended December 31 2014 2013 Investment income Dividends and distributions (net of withholding taxes of $34,527; 2013 – $35,892) (Note 9) $ 198,937 $ 205,410 Interest 40,078 455,548 Fee rebate income – 1,957 Total investment income 239,015 662,915 Expenses Management fees (Note 5) 555,642 531,358 Interest (Note 6) 142,880 129,028 Performance fees (Note 5) 32,849 861,585 Miscellaneous expense 2,908 11,248 Dividends – 7,275 Total expenses 734,279 1,540,494 Net investment loss (495,264) (877,579) Realized and change in unrealized (loss) gain from investment activities and foreign currencies Net realized (loss) gain on investments and foreign currencies (1,003,167) 4,296,030 Net change in unrealized appreciation of investments and foreign currencies 289,901 3,222,748 Net realized and change in unrealized (loss) gain on investments and foreign currencies (713,266) 7,518,778 Net (decrease) increase in net assets attributable to holders of redeemable participating shares from operations $ (1,208,530) $ 6,641,199 See accompanying notes.

Arrowsmith Fund, Ltd.

Statement of Changes in Net Assets Attributable to Holders of Redeemable Participating Shares

(Expressed in United States Dollars)

5

Year Ended December 31 2014 2013 Net (decrease) increase in net assets attributable to holders of redeemable participating shares from operations Net investment loss $ (495,264) $ (877,579) Net realized (loss) gain on investments and foreign currencies (1,003,167) 4,296,030 Net change in unrealized appreciation of investments and foreign currencies 289,901 3,222,748 Net (decrease) increase in net assets attributable to holders of redeemable participating shares from operations (1,208,530) 6,641,199 Share capital transactions Sale of participating preferred shares – Class A 24,138,274 6,338,035 Redemptions of participating preferred shares – Class A (7,057,411) (9,179,843) Redemptions of participating preferred shares – Class B (3,591,124) (177,139) Net increase (decrease) in net assets from share capital transactions 13,489,739 (3,018,947) Net increase in net assets attributable to holders of redeemable participating preferred shares during the year 12,281,209 3,622,252 Net assets attributable to holders of redeemable participating preferred shares at beginning of year 53,080,678 49,458,426 Net assets attributable to holders of redeemable participating preferred shares at end of year $ 65,361,887 $ 53,080,678 See accompanying notes.

Arrowsmith Fund, Ltd.

Statement of Cash Flows (Expressed in United States Dollars)

6

Year Ended December 31 2014 2013 Operating activities Net (decrease) increase in net assets attributable to holders of redeemable participating shares from operations $ (1,208,530) $ 6,641,199 Adjustments to reconcile net (decrease) increase in net assets attributable to holders of redeemable participating shares from operations to net cash (used in) provided by operating activities: Changes in operating assets and liabilities: Investments, at fair value (5,987,569) 1,519,786 Receivables for investments sold 367,505 1,130,772 Investments made in advance (5,010,000) (1,000,000) Other receivables 214,089 (170,648) Due to Portfolio Manager (200,453) 206,889 Payable for investments purchased (587,839) 171,031 Net cash (used in) provided by operating activities (12,412,797) 8,499,029 Financing activities Proceeds from sales of redeemable participating preferred shares 22,988,274 3,338,035 Proceeds from sale of redeemable participating preferred shares received in advance – 1,150,000 Payments for redemptions of redeemable participating preferred shares (11,087,073) (7,682,351) Net cash provided by (used in) financing activities 11,901,201 (3,194,316) Net change in cash balances at bank and brokers (511,596) 5,304,713 Cash balances at bank and brokers at beginning of year 15,469,222 10,164,509 Cash balances at bank and brokers at end of year $ 14,957,626 $ 15,469,222 Supplemental cash flow information Cash received during the year for dividends $ 249,104 $ 192,699 Cash received during the year for interest $ 40,078 $ 698,862 Cash paid during the year for interest $ 142,880 $ 129,028 Cash paid during the year for dividends $ – $ 7,275 See accompanying notes.

Arrowsmith Fund, Ltd.

Condensed Schedule of Investments (Expressed in United States Dollars)

December 31, 2014

7

Shares Description Cost Fair Value

Investments – (73.35%)* Common and preferred stocks – (23.71%):

32,500.00 AISI Realty Public Ltd. $ 80,742 $ 28,093 100,000.00 Atlantis Japan Growth Fund Ltd. 192,372 184,564

6,400.00 Avex Group Holdings, Inc. 100,009 105,762 10,000.00 Baker Hughes, Inc. 575,506 560,700 63,500.00 China Auto Rental, Inc. 92,733 85,336 98,000.00 CIBanco, S.A. Institución de Banca Múltiple 194,714 205,113 12,500.00 Citigroup, Inc. 635,850 676,375

3,215.00 DB ETC Index PLC 356,401 371,509 10,000.00 eBay, Inc. 543,909 561,200 50,000.00 Federal Home Loan Mortgage Corporation 209,730 103,000 50,000.00 Federal National Mortgage Corporation 212,925 102,750 25,000.00 General Motors Corporation 882,558 872,750 10,000.00 Genworth Financial, Inc. 94,180 85,000 15,000.00 GlaxoSmithKline PLC 688,136 641,100 65,730.00 Gozde Girisim Sermayesi Yatiri 99,564 81,371 30,000.00 Hertz Global Holdings, Inc. 827,616 748,200 20,000.00 Hewlett Packard Co. 606,358 802,600 30,000.00 Internap Corporation 235,526 238,800 59,000.00 Intesa Sanpaolo SpA 197,643 172,885

4,400.00 Itochu Techno-Solutions Corporation 200,693 156,966 17,800.00 Kuraray Co. Ltd. 202,038 204,924 16,320.00 Maple Leaf Foods, Inc. 302,075 273,440 12,500.00 Microsoft Corporation 501,731 580,625

3,613,200.00 Modern Internasional Tbk Pt 200,102 196,925 195,890.00 Monitise PLC 205,600 77,037 200,000.00 Niko Resources Ltd. 412,277 42,000

14,000.00 Nippon Ceramic Company Ltd. 202,008 209,132 28,000.00 Opt, Inc. 207,089 171,937 18,930.00 Orange SA 298,646 324,070 22,530.00 Orkla ASA 185,279 154,192 13,391.00 Partners Group Global Opportunities 54,322 156,984 59,524.00 Peugeot SA 287,004 277,615 30,000.00 Pfizer, Inc. 913,536 934,500

4,000.00 Pharmacyclics, Inc. 537,148 489,040

Arrowsmith Fund, Ltd.

Condensed Schedule of Investments (continued) (Expressed in United States Dollars)

8

Shares Description Cost Fair Value

Investments – (73.35%) (continued)* Common and preferred stocks – (23.71%):

21,000.00 Ping An Insurance Group Co. $ 202,049 $ 214,232 10,000.00 Proshares Trust II 702,620 893,000 52,631.00 Quotient Ltd. 499,995 947,358 60,000.00 Sirius XM Holdings, Inc. 209,842 210,000 20,000.00 Sunesis Pharmaceuticals, Inc. 99,993 51,000

271,590.00 Telecom Italia SpA 297,778 289,810 15,000.00 The Spectranetics Corporation 463,975 518,700 44,118.00 Third Point Offshore Investors 492,508 737,212 26,932.00 Uchiyama Holdings Co. Ltd. 187,429 135,678 22,600.00 UCS Co. Ltd. 212,621 164,645

8,025.00 Ulker Biskuvi Sanayi AS 50,362 63,767 50,000.00 Vivus Inc. 265,482 144,000 10,000.00 Weight Watchers International 266,427 248,400

Other 499,201 – Total common and preferred stocks 15,986,302 15,494,297

Advisor investment funds – (49.45%): 250.00 Andean Capital Investment Ltd. 250,000 229,395

0.46 Apollo Value Investment Offshore 340 382 514.61 Autonomy Fund II C Ltd. 51,460 98,486

5,233.95 Autonomy Fund II D Ltd. 654,203 748,660 531.50 Autonomy Global Macro Fund Ltd. 79,547 155,268

2,594.77 Bluecrest Special Situations Fund 257,934 12,844 5,000.00 Camox Fund 500,000 531,750

121.53 Canyon Value Realization Fund 144,705 951,975 27,158.63 Caxton Global Investments Ltd. 738,455 1,107,738

7,717.18 Egerton Euro Dollar Fund Ltd. 447,308 1,154,639 – Firebird Fund, L.P.*** 1,500,000 1,096,188 – Firstmark Healthcare Venture*** 1,695 6,792

4.24 Galleon Special Opportunities Crossover 299,248 80,074 – Gavea Investment Fund II C, L.P.*** 79,720 151,493

Arrowsmith Fund, Ltd.

Condensed Schedule of Investments (continued) (Expressed in United States Dollars)

9

Shares Description Cost Fair Value

Investments – (73.35%) (continued)* Advisor investment funds – (49.45%) (continued):

10,000.00 Gavea Investment Fund Ltd. $ 398,940 $ 98,497 – Gavea Investment IV D, L.P.*** 861,005 889,100 – Gavea Jus Brazilian Government*** 680,000 564,256

28,057.05 Harbour Holdings Ltd. 1,100,013 1,138,866 165.33 Hermitage Global Fund 16,530 6,035

4,210.17 HFS Discover Fund Ltd. 421,017 492,159 238.62 HITE Hedge Offshore Ltd. 454,759 885,026

1,001.30 HITE MLP Caymans Ltd. 1,000,000 2,104,565 1,395.23 IIG Trade Opportunities Fund 223,711 360,469

– India Asset Recovery Fund, L.P.*** 92,386 62,602 250.00 Iraq Investment Partners I Ltd. 250,000 170,672

5,000.00 Kylin Offshore Long Fund Ltd. 500,000 474,739 – Lawrence Offshore Partners, L.P.*** 500,000 479,724

767.14 Lone Monterey Ltd. 855,574 2,544,573 80.00 MCT Berlin Residential SCA 751,307 34,844

5,413.00 MGHY Liquidation SPV 245,956 9,216 24.33 Moore Global Investments Ltd. 896,366 1,382,973

– Morgan Stanley Real Estate Fund, L.P.*** 423,659 555,036 – MPM Bioventures III QP, L.P.*** 226,669 157,320 – NCH Agribusiness Partners, L.P.*** 1,017,435 1,076,863

9,855.61 Nomura Investment Solutions PL 1,000,000 997,398 252.18 Pacificor Offshore Fund Ltd. 499,212 335,267

1,000,000.00 Pinetree Capital Ltd. 950,348 986,835 – Pomona Capital III Fund, L.P.*** 9,936 41,349

540,859.28 Protege Partners Fund Ltd. 399,183 635,490 163.54 Raptor Private Holdings Ltd. 93,484 80,676

1,000.00 Shellback Offshore Fund Ltd. 1,000,000 1,129,539 5,300.47 Simplex Value Up Trust 1,000,000 984,351

574.92 SIO Partners Offshore Ltd. 1,000,000 1,276,493 500.00 Spottail Fund Ltd. 500,000 532,072

1,159.91 Square Meal Investments 160,913 277,977 6,788.61 Tal China Focus Fund 1,000,000 1,114,079

Arrowsmith Fund, Ltd.

Condensed Schedule of Investments (continued) (Expressed in United States Dollars)

10

Shares Description Cost Fair Value

Investments – (73.35%) (continued)* Advisor investment funds – (49.45%) (continued):

– Technikos LLP*** $ 486,386 $ 244,694 202.37 Thai Focused Equity Fund Ltd. 250,000 239,706 507.80 The Fine Wine Investment Fund 1,077,504 670,898

1,000.00 Touradji Private Equity Offshore Fund Ltd.** 470,000 782,380

114.79 Tudor BVI Global Fund Ltd. 129,261 172,413 413.87 VPL-I Trust 500,000 516,439

5,144.97 WF Asian Reconnaissance Fund Ltd. 904,839 1,494,459 Other 1 1 Total advisor investment funds 27,351,009 32,325,734

Other investments – 0.19%** – Mockernstrassee 70 GM*** 253,702 125,515

Other 777,146 3 Total other investments 1,030,848 125,518 Total investments $ 44,368,159 $ 47,945,549

* Percentage (%) represents percentage of net assets attributable to holders of redeemable participating

shares. ** Investments within this classification are valued at fair value as determined in good faith by the

Portfolio Manager under the supervision of the Board of Directors. *** Investment is not unitized. See accompanying notes.

Arrowsmith Fund, Ltd.

Condensed Schedule of Investments (continued) (Expressed in United States Dollars)

December 31, 2013

11

Shares/Par Description Cost Fair Value

Investments – (79.05%)* Bonds – (3.65%):

$ 10,010,000.00 Argentine Republic 0%, 12/15/2035 $ 1,623,470 $ 894,890

$ 1,401,000.00 Sorenson Communications 10.5%, 02/01/2015 1,009,614 1,043,745 Total bonds 2,633,084 1,938,635

Common and preferred stocks – (9.16%): 42,500.00 AISI Realty Public Ltd. 118,972 47,853 14,550.00 CMIC Holdings Co. Ltd. 200,658 188,032 22,500.00 Federal Home Loan Mortgage Corporation 189,440 201,825

289,583.00 Hirco PLC 237,872 97,097 100,000.00 Niko Resources Ltd. 147,240 235,200

14,000.00 Nippon Ceramic Company Ltd. 197,694 218,544 18,500.00 Opt, Inc. 154,633 175,488 22,368.20 Partners Group Global Opportunities 90,573 278,878 17,500.00 Proshares Ultrashort 1,393,787 1,386,000

1,500,000.00 Radicle Projects PLC 73,297 – 84,680.00 Third Point Offshore Investors 949,941 1,342,178 57,000.00 Toko, Inc. 202,547 193,762

113,050.00 Transatlantic Petroleum Ltd. 121,764 96,093 26,932.00 Uchiyama Holdings Co. Ltd. 187,429 173,128 25,000.00 Vivus Inc. 247,125 227,000

657,895.00 Windimurra Vanadium Ltd. 973,702 – Other 964,586 – Total common and preferred stocks 6,451,260 4,861,078

Arrowsmith Fund, Ltd.

Condensed Schedule of Investments (continued) (Expressed in United States Dollars)

12

Shares Description Cost Fair Value

Investments – (79.05%) (continued)* Advisor investment funds – (66.10%):

8.43 Apollo Value Investment Offshore $ 6,233 $ 11,684 43.16 Artis Clean Tech Partners Ltd. 45,413 4,514

259.72 Artis Partners 2x Ltd. 27,307 2,347 198.62 Autonomy Capital Fund Ltd. 19,539 76,671

1,143.35 Autonomy Fund II C Ltd. 114,335 169,324 5,233.95 Autonomy Fund II D Ltd. 654,203 920,042

369.85 Autonomy Global Macro Fund Ltd. 65,540 103,357 3,110.90 Bluecrest Special Situations Fund 309,240 39,975

121.53 Canyon Value Realization Fund 144,705 906,002 27,158.63 Caxton Global Investments Ltd. 738,455 1,397,333

– Cedar Hill Offshore Mortgage, L.P.*** 1,096,107 1,315,253 6,517,212.50 China Commodities Absolute Return 100,137 37,148

43.74 CSL Energy Offshore Fund Ltd. 49,825 33,593 7,717.18 Egerton Euro Dollar Fund Ltd. 447,308 1,119,351

– Firebird Fund L.P. *** 1,000,000 1,062,832 – Firebird New Mongolia Fund, L.P.*** 446,260 277,840 – Firstmark Healthcare Venture L.P.*** 1,695 5,470

4.24 Galleon Special Opportunities Crossover 299,248 135,769 – Gavea Investment Fund II C, L.P.*** 101,942 100,249

10,000.00 Gavea Investment Fund Ltd. 398,940 147,671 – Gavea Investment IV D, L.P.*** 799,753 698,819 – Gavea Jus Brazilian Government*** 430,000 350,231

17,117.00 Hamon Asian Market Leaders Fund 499,302 444,871 165.33 Hermitage Global Fund 16,533 6,165

– HFIC Offshore Fund Ltd.*** 334 29,622 4,210.17 HFS Discover Fund Ltd. 421,017 499,576

524.73 HITE Hedge Offshore Ltd. 1,000,000 1,833,146 1,001.30 HITE MLP Caymans Ltd. 1,000,000 1,884,913 1,395.23 IIG Trade Opportunities Fund 223,711 446,012

– India Asset Recovery Fund, L.P.*** 87,386 62,042 250.00 Iraq Investment Partners I Ltd. 250,000 252,551 742.56 Joho Fund Ltd. 444,932 1,392,587

Arrowsmith Fund, Ltd.

Condensed Schedule of Investments (continued) (Expressed in United States Dollars)

13

Shares Description Cost Fair Value

Investments – (79.05%) (continued)* Advisor investment funds – (66.10%) (continued):

857.13 Lone Monterey Ltd. $ 1,000,000 $ 2,922,977 80.00 MCT Berlin Residential SCA 751,307 934,198

– Merlin Nexus I, L.P.*** 33 9,252 5,413.00 MGHY Liquidation SPY 245,956 44,441 3,903.39 Mission Investment Partners LLC 3,903 2,277

772.34 Monarch Debt Recovery Fund Ltd. 1,000,000 1,231,688 5,736.89 Montpelier Global Funds Ltd. 57,369 66,950

24.33 Moore Global Investments Ltd. 896,366 1,354,415 – Morgan Stanley Real Estate Fund, L.P.*** 520,382 617,364 – MPM Bioventures III QP, L.P.*** 275,146 142,097 – NCH Agribusiness Partners, L.P.*** 1,044,798 1,127,556

271.74 Pacificor Offshore Fund Ltd. 537,927 309,566 409.45 Permal Japan Holding N.V. 1,027,546 1,128,970

1,000,000.00 Pinetree Capital Ltd. 1,000,000 1,219,832 – Pomona Capital III Fund, L.P.*** 11,633 63,584

542,371.44 Protege Partners Fund Ltd. 399,183 617,446 209.47 Raptor Private Holdings Ltd. 117,841 107,488

– SG Perimeter LLC*** 250,000 354,954 5,193.19 Simplex Value Up Trust 1,000,000 988,367 1,000.00 SIO Partners Offshore Ltd. 1,000,000 1,062,517 1,159.91 Square Meal Investments 160,913 372,237

– SRPE Investment Fund One Mini LLP*** 246,732 96,399 6,567.28 Tal China Focus Fund 1,000,000 1,061,601

– Technikos LLP*** 985,219 477,794 970.64 The Fine Wine Investment Fund 1,077,504 790,039

1,000.00 Touradji Private Equity Offshore Fund Ltd.** 470,000 650,000

157.28 Tudor BVI Global Fund Ltd. 176,224 237,461 5,282.11 WF Asian Reconnaissance Fund Ltd. 913,555 1,321,444

– YCAB Offshore Coinvest (A) LLC*** 818 899 – YCAB Offshore Coinvest (B) LLC*** 1,514 2,287

Other 812 1 Total advisor investment funds 27,412,081 35,083,061

Arrowsmith Fund, Ltd.

Condensed Schedule of Investments (continued) (Expressed in United States Dollars)

14

Shares Description Cost Fair Value

Investments – (79.05%) (continued)* Other investments – (0.14%):**

– Mendell Davis Gas Partners LLC*** $ 35,000 $ – – Mockernstrasse 70 GmbH*** 253,702 75,201

Other 1,898,394 5 Total other investments 2,187,096 75,206 Total investments $ 38,683,521 $ 41,957,980

* Percentage (%) represents percentage of net assets attributable to holders of redeemable participating

shares. ** Investments within this classification are valued at fair value as determined in good faith by the

Portfolio Manager under the supervision of the Board of Directors. *** Investment is not unitized. See accompanying notes.

Arrowsmith Fund, Ltd.

Notes to Financial Statements (Expressed in United States Dollars)

December 31, 2014

15

1. Corporate Information

Arrowsmith Fund, Ltd. (the Fund) was incorporated on January 4, 1989 under the International Business Companies Act of the British Virgin Islands and commenced operations on July 13, 1989. The Fund is an open-ended investment company. The primary objective of the Fund is to achieve superior long-term results by investing in other open-ended funds. The Fund will also invest and trade in stocks, stock options, bonds and collectibles as well as in the shares of closed-ended funds located within and outside the United States (U.S.).

The address of the Fund’s registered office is Palm Grove House, Road Town, Tortola, British Virgin Islands.

The Fund’s shares are listed on the Cayman Islands Stock Exchange.

These financial statements were authorized for issue by the directors of the Fund on September 2, 2015.

2. Summary of Significant Accounting Policies

Statement of Compliance

These financial statements have been prepared in accordance with International Financial Reporting Standards (IFRS) as issued by the International Accounting Standards Board (IASB).

Basis of Preparation

These financial statements have been prepared on an historical cost basis, except for investments classified as at fair value through profit or loss and other financial assets and financial liabilities that have been measured at fair value. These financial statements are expressed in U.S. dollars. The preparation of financial statements in conformity with IFRS requires management to make estimates and assumptions that affect the reported amounts and disclosures in the financial statements and accompanying notes. Management believes that the estimates utilized in preparing its financial statements are reasonable and prudent. Actual results could differ from those estimates.

Arrowsmith Fund, Ltd.

Notes to Financial Statements (continued) (Expressed in United States Dollars)

16

2. Summary of Significant Accounting Policies (continued)

Going Concern

The Fund’s management has made an assessment of the Fund’s ability to continue as a going concern and is satisfied that the Fund has the resources to continue in business for the foreseeable future. Furthermore, the Fund’s management is not aware of any material uncertainties that may cast significant doubt upon the Fund’s ability to continue as a going concern. Therefore the financial statements continue to be prepared on the going concern basis.

Critical Accounting Judgments and Key Sources of Estimation Uncertainty

In the application of the Fund’s accounting policies, management is required to make judgments, estimates and assumptions about the carrying amount of assets and liabilities that are not readily apparent from other sources. The estimates and associated assumptions are based on historical experience and other factors that are considered relevant. Actual results may differ from these estimates.

The estimates and underlying assumptions are reviewed on an ongoing basis. Revisions to accounting estimates are recognized in the period in which the estimates are revised if the revision affects only that period or in the period of the revision and future periods if the revision affects both current and future periods.

The following are critical judgments and key assumptions concerning the future that management has made in the process of applying the Fund’s accounting policies and that have the most significant effect on the amounts recognized in the financial statements. These judgments may have significant risk of causing a material adjustment in the carrying amounts of assets and liabilities in the future periods.

Fair Value of Investments and Derivative Contracts Traded Over-the-Counter

The Fund’s financial instruments could include investments and derivative contracts traded over-the-counter, which are not quoted in an active public market. The fair value of these instruments is established by using valuation techniques. Valuation techniques include using recent arm’s length market transactions, if available, reference to current fair value of other instruments that are substantially the same, discounted cash flow analysis, pricing models and other valuation techniques commonly used by market participants that have been demonstrated to provide reliable estimates of prices obtained in actual market transactions. Techniques used incorporate observable market data about the market conditions and other factors that are likely to affect these instruments’ fair value.

Arrowsmith Fund, Ltd.

Notes to Financial Statements (continued) (Expressed in United States Dollars)

17

2. Summary of Significant Accounting Policies (continued)

Financial Assets and Liabilities at Fair Value Through Profit or Loss

Financial Assets and Liabilities Held for Trading

Financial assets and liabilities include certain securities and securities sold short. These instruments are acquired or incurred principally for the purpose of generating a profit from short-term fluctuation in price. Derivatives are categorized as held for trading, as the Fund does not designate any derivative as hedging instruments for hedge accounting purposes as defined by IAS 39. The Fund did not hold derivative contracts during the year ended December 31, 2014 and 2013.

Financial Instruments Designated as at Fair Value Through Profit or Loss Upon Initial Recognition

Investments designated as at fair value through profit or loss upon initial recognition include financial assets such as investment funds and other investments that are not held for trading. These financial assets are designated on the basis that their fair value can be reliably measured and their performance has been evaluated on a fair value basis in accordance with the investment strategy as set out in the Fund’s offering documents.

Recognition

The Fund recognizes a financial asset or a financial liability when, and only when, it becomes a party to the contractual provisions of the instrument.

A purchase or sale of financial assets is recognized using trade date accounting. From the purchase date, any gains and losses arising from changes in fair value of the financial assets or financial liabilities are recorded through the Statement of Comprehensive Income.

Derecognition

The Fund derecognizes a financial asset when the contractual rights to the cash flows from the financial asset expire or it transfers the financial asset and the transfer qualifies for derecognition in accordance with IAS 39. The Fund derecognizes a financial liability when the obligation specified in the contract is discharged, cancelled or expires.

Arrowsmith Fund, Ltd.

Notes to Financial Statements (continued) (Expressed in United States Dollars)

18

2. Summary of Significant Accounting Policies (continued)

Initial Measurement

Financial instruments categorized at fair value through profit or loss are recognized initially at fair value. All transaction costs for such instruments are recognized directly in the Statement of Comprehensive Income.

Subsequent Measurement

After initial measurement, the Fund measures financial instruments which are classified as fair value through profit or loss, at their fair values.

Investments in shares of open-ended investment funds are valued at their net asset values as indicated by the management of such investment funds. If net asset value calculations of an investment fund are not consistently available for timely calculations of the Fund’s net asset value, the Fund may, on a consistent basis, use the last previously reported net asset value of such investment fund for purposes of calculating the Fund’s net asset value.

The Fund also invests in managed funds which are not quoted in an active market. Investments in managed funds are valued based on the Net Assets Value (NAV) per unit published by the administrator of those funds, adjusted to reflect the effect of the time passed since the calculation date, liquidity risk, limitations on redemptions, bid prices observed in the secondary market and other factors when necessary.

None of the investment funds at December 31, 2014 and 2013 had a readily available market value. Due to the inherent uncertainty of valuation, the value of the investments held by the Fund may differ significantly from the values that would have been used had a ready market for the investment existed, and the differences could be material.

Investments in securities that are classified as held-for-trading are valued at the last reported sales price in the principal market where such securities trade or, if no sales are reported, the mean between representative bid and ask quotations obtained from a quotation reporting system or from established market makers or dealers. If an asset or a liability measured at fair value has a bid price and an ask price, IFRS 13 “Fair value measurement” standard requires valuation to be based on a price within the bid-ask spread that is more representative of fair value and allows the use of mid-market pricing or other pricing conventions that are used by market participants as a practical expedient of fair value measurement within a bid-ask spread. At December 31, 2014 and 2013, there were no material differences between the reported values by the Fund and the valuation required by IFRS.

Arrowsmith Fund, Ltd.

Notes to Financial Statements (continued) (Expressed in United States Dollars)

19

2. Summary of Significant Accounting Policies (continued)

If a quoted market price is not available on a recognized stock exchange or from a reputable broker/counterparty, the fair value of the financial instruments may be estimated by the Board of Directors using valuation techniques, including use of recent arm’s length market transactions, reference to the current fair value of another instrument that is substantially the same, discounted cash flow techniques, option pricing models or any other valuation technique that provides a reliable estimate of prices obtained in actual market transactions.

The Board of Directors is ultimately responsible for valuations of financial instruments. Investments in securities of $907,895 or 1.39% (2013 – $725,201 or 1.37%) of net assets attributable to holders of redeemable participating preferred shares have been valued in good faith on the basis of the valuations provided by Arrowsmith, LLC (the Portfolio Manager) as at December 31, 2014, using the principles laid down by the Board of Directors. Because of the inherent uncertainty of valuation of securities, these estimated fair values may differ significantly from values that will eventually be realized upon an actual liquidation of the portfolio, and such differences could be material.

Loans and Receivables

Loans and receivables are non-derivative financial assets with fixed or determinable payments that are not quoted in an active market. The Fund includes in this category amounts relating to receivable for investments sold, investments made in advance and other receivables.

Other Financial Liabilities

This category includes all financial liabilities, other than those classified as held for trading. The Fund includes in this category amounts relating to due to Portfolio Manager, long term borrowings, interest payable, payable for investment purchased and dividends payable.

Derivative Financial Instruments

The Fund, in its normal course of investing and trading activities, may enter into transactions in derivative financial instruments based on expectations of future market movements and conditions. The fair value of derivative financial instruments at the reporting date generally reflects the amount that the Fund would receive or pay to terminate the contract at the reporting date. Many derivative financial instruments are exchange traded or traded in the over-the-counter market where market values are readily obtainable. These transactions have market and off-balance sheet risk and may have credit and liquidity risk.

Arrowsmith Fund, Ltd.

Notes to Financial Statements (continued) (Expressed in United States Dollars)

20

2. Summary of Significant Accounting Policies (continued)

Derivative Financial Instruments (continued)

All derivative financial instruments are classified in assets when amounts are receivable by the Fund and in liabilities when amounts are payable by the Fund. Changes in the fair values of derivatives are included in the Statement of Comprehensive Income. During the period a contract is open, changes in the value of the contract are recognized as unrealized appreciation or depreciation to reflect the fair value of the contract at the last day of the valuation period. When the contract is closed, the Fund records a realized gain or loss equal to the difference between the proceeds from (or cost of) the closing transaction and the Fund’s basis in the contract. The Fund did not hold derivative financial instruments during the year ended December 31, 2014 and 2013.

Accounting for Investments and Related Income

Investment transactions are accounted for on the trade date (date the order to buy or sell is executed). Investments purchased not yet received represent prepayments for investments. Receivables for investments sold are recorded at the redemption value on the relevant redemption date. Dividend income and expense are recorded on the ex-dividend date. Interest is recorded on the accrual basis as earned. The first in first out method is used to calculate gains and losses on investments sold. Gains and losses on all investments are recognized in the Statement of Comprehensive Income.

Cash Flows

For the purpose of the Statement of Cash Flows, cash is comprised of cash at banks, money market balances, and cash on deposit with custodians and brokers for initial and variation margin on securities sold short.

Dividends and Distributions

The Board of Directors of the Fund is empowered to declare and pay dividends and distributions. Since the Fund’s primary objective is capital appreciation, the Fund has not paid any dividends nor is it anticipated that the Fund will pay dividends in the future.

Arrowsmith Fund, Ltd.

Notes to Financial Statements (continued) (Expressed in United States Dollars)

21

2. Summary of Significant Accounting Policies (continued)

Foreign Currency Translation

The Fund’s functional currency is the U.S. dollar (capital raising currency); however, it transacts business in currencies other than U.S. dollars. Monetary assets and liabilities denominated in currencies other than the U.S. dollar are translated into U.S. dollars at the rate in effect at the date of the Statement of Financial Position. Income and expense items denominated in currencies other than the U.S. dollar are translated into U.S. dollars at the month end rate for the month that the transaction occurred. Gains and losses resulting from translation to the U.S. dollar are reported in the Statement of Comprehensive Income within the net change in unrealized appreciation (depreciation) balance.

The Fund does not isolate that portion of gains and losses on investments which is due to changes in foreign exchange rates from that which is due to changes in market prices of the investments. Such fluctuations are included with the net realized and unrealized gains and losses from investments.

Borrowing Cost

Borrowing costs are recognized as an expense when incurred.

Redeemable Participating Preferred Shares

Redeemable participating preferred shares are redeemable at the shareholder’s option and are classified as financial liabilities (unless they meet all conditions to be classified as equity in accordance with IAS 32). These shares can be put back to the Fund as described in Note 7 for cash equal to a proportionate share of the Fund’s net asset value attributable to holders of participating shares.

Share Capital

Common shares are classified as equity as these shares cannot be put back to the Fund at the holder’s option. These shares do not participate in profits of the Fund.

Arrowsmith Fund, Ltd.

Notes to Financial Statements (continued) (Expressed in United States Dollars)

22

2. Summary of Significant Accounting Policies (continued)

Impairment of Financial Assets

An assessment is made at each balance sheet date to determine whether there is objective evidence that a financial asset or group of financial assets may be impaired. If such evidence exists, the estimated recoverable amount of that asset is determined and any impairment loss recognized for the difference between the recoverable amount and the carrying amount is included in the Statement of Comprehensive Income. The Fund did not record any impairment adjustments at December 31, 2014 and 2013.

Interest Income and Expenses

Interest income and expenses are recognized in the Statement of Comprehensive Income on a time-proportionate basis using the effective interest rate method. The effective interest rate method is a method of calculating the amortized cost of a financial asset or financial liability and of allocating the interest income or interest expense over the relevant year. The effective interest rate is the rate that exactly discounts estimated future cash payments or receipts throughout the expected life of the financial instrument, or, when appropriate, a shorter period, to the net carrying amount of the financial assets or financial liability. When calculating the effective interest rate, the Fund estimates cash flows considering all contractual terms of the financial instrument but does not consider future credit losses. The calculation includes all fees and points paid or received between parties to the contract that are an integral part of the effective interest rate, transaction costs and all other premiums or discounts.

Dividend Income and Expenses

Dividend income and expenses are recorded in the Statement of Comprehensive Income on an ex-dividend date (when the right to receive payment is established), gross of withholding taxes. Withholding tax is recorded on an accrual basis.

Standards, Interpretations, and Amendments

New Standards, Interpretations and Amendments Adopted by the Fund The accounting policies adopted in the preparation of the financial statements are consistent with those followed in the preparation of the Fund’s financial statements for the year ended December 31, 2015, except for the adoption of new standards and interpretations effective on the dates described below.

Arrowsmith Fund, Ltd.

Notes to Financial Statements (continued) (Expressed in United States Dollars)

23

2. Summary of Significant Accounting Policies (continued)

Standards, Interpretations, and Amendments (continued)

IFRS 10 - Consolidated Financial Statements – Investment Entities IFRS 10 replaces the portion of IAS 27 Consolidated and Separate Financial Statements that addresses the accounting for consolidated financial statements. It also replaces SIC-12 Consolidation – Special Purpose Entities. This amendment establishes a single control model that applies to all entities including ‘special purpose entities’. The changes introduced by IFRS 10 will require management to exercise significant judgment to determine which entities are controlled, and therefore required to be consolidated by a parent, compared with the requirements that were in IAS 27. This amendment became effective as of January 1, 2014. The adoption of this standard had no impact on the Fund’s financial position or performance.

IFRS 12 - Disclosure of Involvement with Other Entities – Investment Entities Amendment IFRS 12 includes all of the disclosures that were previously in IAS 27 related to consolidated financial statements, as well as all of the disclosures that were previously included in IAS 31 and IAS 28. These disclosures relate to an entity’s interests in subsidiaries, joint arrangements, associates and structured entities. A number of new disclosures are also required. The investment entities amendment became effective for annual periods beginning on or after January 1, 2014. The adoption of this standard had no impact on the Fund’s financial position or performance.

IAS 32 – Offsetting Financial Assets and Financial Liabilities This amendment clarifies the meaning of “currently has a legally enforceable right to set-off”. The amendment also clarifies the application of the IAS 32 offsetting criteria to settlement systems (such as central clearing house systems) which apply gross settlement mechanisms that are not simultaneous. This amendment became effective as of January 1, 2014. The adoption of this standard had no impact on the measurement techniques employed by the Fund.

Arrowsmith Fund, Ltd.

Notes to Financial Statements (continued) (Expressed in United States Dollars)

24

2. Summary of Significant Accounting Policies (continued)

Standards Issued But Not Yet Effective

IFRS 9 – Financial Instruments: Classification and Measurement IFRS 9 as issued reflects the first phase of the IASB’s work on the replacement of IAS 39 and applies to classification and measurement of financial assets and financial liabilities as defined in IAS 39. The standard is effective for annual periods beginning on or after January 1, 2018. In subsequent phases, the IASB will address hedge accounting and impairment of financial assets. The adoption of the first phase of IFRS 9 is not expected to have an effect on the classification and measurement of the Fund’s financial assets and financial liabilities. The Fund will quantify the effect in conjunction with the other phases, when issued, to present a comprehensive picture.

3. Cash at Bank and Brokers

At December 31, 2014, the cash at bank and brokers totaling $14,957,626 (2013 – $15,469,222 represented primarily cash at the Fund’s brokers held on deposit. Margin and short sales requirements are satisfied by the deposits of cash with the brokers. The Fund earns interest income on its cash deposited with banks and brokers.

Investments and cash are held by the Fund’s principal brokers and custodians and, as required, are used as collateral for margin transactions conducted for the Fund. The Fund is liable for its obligations and indebtedness to its principal brokers upon demand. The Fund’s investments and cash have a general lien to the extent of indebtedness of the Fund to its brokers.

4. Fair Value Measurement

The Fund classifies fair value measurements using a fair value hierarchy that reflects the significance of the inputs used in determining the measurements in line with IFRS 13.

The fair value hierarchy has the following levels:

Level I Quoted market price in an active market for an identical instrument.

Level II Valuation techniques based on observable inputs. This category includes instruments valued using: quoted market prices in active markets for similar instruments; quoted prices for similar instruments in markets that are considered less than active; or other valuation techniques where all significant inputs are directly or indirectly observable from market data.

Arrowsmith Fund, Ltd.

Notes to Financial Statements (continued) (Expressed in United States Dollars)

25

4. Fair Value Measurement (continued)

Level III Valuation techniques using significant unobservable inputs. This category includes all instruments where the valuation technique includes inputs not based on observable data and the unobservable inputs could have a significant impact on the instrument’s valuation. This category includes instruments that are valued based on quoted prices for similar instruments where significant unobservable adjustments or assumptions are required to reflect differences between the instruments.

When fair values of any listed equity (including listed investments in managed funds) and debt securities at the reporting date, as well as publicly traded derivatives, are based on quoted market prices or binding dealer price quotations, without any deduction for transaction costs, the instruments are included within Level I of the hierarchy.

Depending on adjustments needed to the NAV per unit published by advisor investment funds, the Fund classifies the fair value of that investment as either Level II or Level III. An individual advisor investment fund’s level within the fair value hierarchy is based on the lowest level of any input that is significant to the fair value measurement. Pursuant to the above mentioned guidance, advisor investment funds with the following criteria are classified as Level II:

• Quarterly liquidity or more frequent • No hard or soft lock-up that is effective as the measurement date • No gates or suspension of redemptions/withdrawals as of the measurement date

The Portfolio Funds that do not meet the above criteria are classified as Level III.

The residential real estate is in Mockernstrasse 70 GmbH, a private company which is a private placement in an apartment building complex in Germany. Mockernstrasse 70 GmbH is valued based on sales and other activities of the apartment units. This investment is included as part of “Other Investments”.

Arrowsmith Fund, Ltd.

Notes to Financial Statements (continued) (Expressed in United States Dollars)

26

4. Fair Value Measurement (continued)

The following table presents the financial instruments carried on the Statement of Financial Position by caption and by level within the fair valuation hierarchy as of December 31, 2014:

Level I Level II Level III Total Investments Advisor Investment Funds $ – $ 23,609,135 $ 8,716,599 $ 32,325,734 Common and Preferred Stocks 15,337,313 156,984 – 15,494,297 Other Investments – – 125,518 125,518 Total investments $ 15,337,313 $ 23,766,119 $ 8,842,117 $ 47,945,549 There were no transfers between Level I and Level II during the year.

The table below sets out information about significant unobservable inputs used at December 31, 2014 in measuring financial instruments categorized as Level III in the fair value hierarchy.

Description

Fair Value at

December 31, 2014

Valuation Technique

Unobservable Input

Range (Weighted Average)

Sensitivity to Changes in Significant

Unobservable Inputs

Advisor Investment Funds

$ 7,934,219

Unadjusted net asset

value

N/A

N/A

Restrictions would result in a lower fair

value Advisor Investment Fund

$ 782,380

Adjusted net asset value

Discount for lack

of marketability

30%-35%

Sale(s) to industry participants should

eliminate the discount(s)

Other Investments

$ 125,518

Sales/ activities of

the units

N/A

N/A

Sale(s) to industry participants should

eliminate the discount(s)

Arrowsmith Fund, Ltd.

Notes to Financial Statements (continued) (Expressed in United States Dollars)

27

4. Fair Value Measurement (continued)

Changes in Level III assets measured at fair value for the year ended December 31, 2014:

Investments in Advisor

Investment Funds

Investments in Other

Investments Balance as of December 31, 2013 $ 7,447,822 $ 75,206 Realized gain (loss) 12,921 (469,954) Change in unrealized appreciation (372,049) 520,266 Purchases 2,543,586 – Sales (2,294,870) – Transfers in 1,379,189 – Balance as of December 31, 2014 $ 8,716,599 $ 125,518 Net change in unrealized appreciation (depreciation) from investments still held as of December 31, 2014 $ (221,729) $ 50,314 All transfers are recorded at beginning of year fair values. For year ended December 31, 2014, there were no transfers noted in/out of Level III.

The following table presents the financial instruments carried on the Statement of Financial Position by caption and by level within the fair valuation hierarchy as of December 31, 2013:

Level I Level II Level III Total Investments Advisor Investment Funds $ – $ 27,635,239 $ 7,447,822 $ 35,083,061 Bonds – 1,938,635 – 1,938,635 Common and Preferred Stocks 4,582,200 278,878 – 4,861,078 Other Investments – – 75,206 75,206 Total investments $ 4,582,200 $ 29,852,752 $ 7,523,028 $ 41,957,980

Arrowsmith Fund, Ltd.

Notes to Financial Statements (continued) (Expressed in United States Dollars)

28

4. Fair Value Measurement (continued)

The table below sets out information about significant unobservable inputs used at December 31, 2013 in measuring financial instruments categorized as Level III in the fair value hierarchy.

Description

Fair value at December 31,

2013 Valuation Technique Unobservable Input

Range (Weighted Average)

Sensitivity to Changes in Significant

Unobservable Inputs

Advisor Investment Funds

$ 6,797,821

Unadjusted net asset

value

N/A

N/A

Restrictions would result in a lower fair

value Advisor Investment Fund

$ 650,000

Adjusted net asset value

Discount for lack of marketability

30%-35%

Sale(s) to industry participants should

eliminate the discount(s)

Other Investment

$ 75,206

Comparable market prices

N/A

N/A

Sale(s) to industry participants should

eliminate the discount(s)

Changes in Level III assets measured at fair value for the year ended December 31, 2013:

Investments in Advisor

Investment Funds

Investments in Other

Investments Balance as of December 31, 2012 $ 6,979,360 $ 6 Realized gain (loss) 113,897 (707,894) Change in unrealized appreciation 70,289 836,721 Purchases 2,212,204 – Sales (1,927,929) (53,627) Balance as of December 31, 2013 $ 7,447,822 $ 75,206 Net change in unrealized appreciation from investments still held as of December 31, 2013 $ 70,107 $ 1,016,721

Arrowsmith Fund, Ltd.

Notes to Financial Statements (continued) (Expressed in United States Dollars)

29

5. Investment Management Agreement

The Fund has a portfolio management agreement with the Portfolio Manager, the managing member of which is James R. Hodge, wherein the Fund agreed to place its investment portfolio under the supervision of the Portfolio Manager. For these services, the Fund pays to the Portfolio Manager a monthly fee (the Fixed Fee or Management Fee) equal to 1/12 of 1.0% of the net assets of Class A and 1/12 of 0.5% of the net assets of Class B.

The Fund also pays a monthly performance fee (the Performance Fee) to the Portfolio Manager. The Performance Fee for Class A and Class B is an amount equal to 15% and 5%, respectively, of each class portion of the net profits of the Fund, if any, resulting from investment activities during each month.

Net profits are reduced by any cumulative loss carryforward resulting from losses in prior months since the Portfolio Manager first began managing the Fund’s investments. Any cumulative loss carryforward is reduced pro rata through distributions by or redemptions from the Fund. For purposes of calculating the Performance Fee, profits and losses include both realized and unrealized gains.

The Management Fees are payable to the Portfolio Manager net of other operating expenses. Interest expense and standard acquisition and disposition costs such as brokerage commissions are not considered operating expenses. The Portfolio Manager retrocedes a substantial portion of its fees to institutions that introduce clients to the Fund based on ownership positions in the Fund by those clients.

6. Borrowings

Long-Term Facility

In prior years, the Fund entered into an unsecured promissory note with a Distributor of the Fund for $2,000,000 (the terms allow payment before maturity) of which $Nil were made in 2014 (2013 - $Nil). The following table represents the promissory note related to the loan facility provided to the Fund as of December 31, 2014 and 2013.

December 31, 2014 and 2013

Loan Date Principal Amount Maturity Date Interest Rate November 1, 2007 $ 2,000,000 October 31, 2027 6%

Arrowsmith Fund, Ltd.

Notes to Financial Statements (continued) (Expressed in United States Dollars)

30

6. Borrowings (continued)

Long-Term Facility (continued)

For the year ended December 31, 2014, the Fund incurred $120,000 (2013 – $129,028) in interest relating to the promissory note which is included in interest on the Statement of Comprehensive Income.

7. Share Capital and Redeemable Participating Shares

The Fund has authorized share capital of $40,100, divided into 100 common shares at $1.00 par value per share, 2,000,000 shares of Class A shares and 2,000,000 shares of Class B shares of redeemable participating preferred shares (preferred shares) at $.01 par value per share. Common shares have voting rights, but no rights to participate in the profits or losses of the Fund. No dividends may be declared on common shares. Class B shares are subject to a two year lock-up period before they may be redeemed.

Preferred shares have no voting rights, except that they will have one vote per share for resolutions to (a) dissolve the Fund, (b) amend the rights of preferred shareholders defined in the Articles of Association, (c) sell all or a substantial part of the assets of the Fund, or (d) approve investments not in conformity with the safeguards described in the offering circular.

Preferred shares are available for issue by the Fund to investors as of the last calendar day of each month (a Valuation Date), except when determination of net asset value and redemption rights have been temporarily suspended in accordance with the provisions outlined in the Fund’s offering circular. Preferred shares are being issued at the offering price, which will be the net asset value per preferred share computed as of the close of business on the relevant Valuation Date plus a sales charge of up to 5.5%. Such sales charge will be computed as a percentage of the aggregate net asset value of the preferred shares being purchased. The sales charge may be paid to third parties or may be waived, in whole or in part, in certain cases, at the sole discretion of the Fund.

The redemption price of the preferred shares will be the net asset value as of the close of business on the applicable Valuation Date. All redemptions must be executed by a written notice at least forty-five days prior to the redemption date. The redemption price may be more or less than the offering price paid by the shareholder, depending on the value of the assets of the Fund at the time of the redemption. Payment of proceeds of redemption of preferred shares will be made in U.S. dollars in accordance with the shareholder’s instructions within thirty business days following the Valuation Date as of which the preferred shares are redeemed.

Arrowsmith Fund, Ltd.

Notes to Financial Statements (continued) (Expressed in United States Dollars)

31

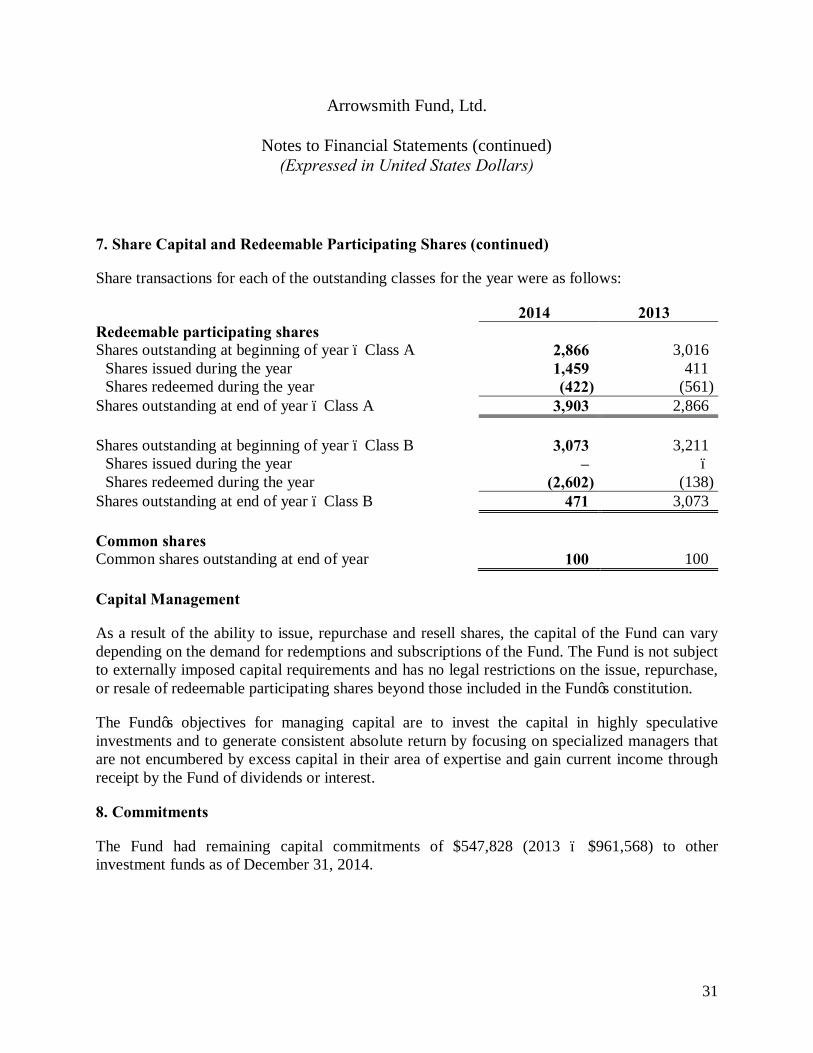

7. Share Capital and Redeemable Participating Shares (continued)

Share transactions for each of the outstanding classes for the year were as follows:

2014 2013 Redeemable participating shares Shares outstanding at beginning of year – Class A 2,866 3,016 Shares issued during the year 1,459 411 Shares redeemed during the year (422) (561) Shares outstanding at end of year – Class A 3,903 2,866 Shares outstanding at beginning of year – Class B 3,073 3,211 Shares issued during the year – – Shares redeemed during the year (2,602) (138) Shares outstanding at end of year – Class B 471 3,073 Common shares Common shares outstanding at end of year 100 100 Capital Management

As a result of the ability to issue, repurchase and resell shares, the capital of the Fund can vary depending on the demand for redemptions and subscriptions of the Fund. The Fund is not subject to externally imposed capital requirements and has no legal restrictions on the issue, repurchase, or resale of redeemable participating shares beyond those included in the Fund’s constitution.

The Fund’s objectives for managing capital are to invest the capital in highly speculative investments and to generate consistent absolute return by focusing on specialized managers that are not encumbered by excess capital in their area of expertise and gain current income through receipt by the Fund of dividends or interest.

8. Commitments

The Fund had remaining capital commitments of $547,828 (2013 – $961,568) to other investment funds as of December 31, 2014.

Arrowsmith Fund, Ltd.

Notes to Financial Statements (continued) (Expressed in United States Dollars)

32

9. Taxation

The Fund is exempt from all forms of taxation in the British Virgin Islands, including income, capital gains and withholding taxes. The Fund is also not subject to capital gains tax in the U.S. However, dividends and interest with respect to certain securities of U.S. issuers are subject to a U.S. withholding tax of 30% of the gross amount. No other taxes are applicable to the Fund.

10. Administrator, Registrar and Transfer Agent

The Fund has entered an administration agreement dated March 1, 2005, with Citco Fund Services (Curaçao) N.V. (the Administrator) to provide administrative, registrar and transfer agent services to the Fund. For its services the Administrator is paid a fee at a rate of 3 basis points per annum of the month-end net assets of the Fund. The fee is calculated and payable monthly in arrears.

The Fund has also contracted with W & P Fund Services Ltd. (the Sub-Administrator) to provide Sub-Administrative services to the Fund. Fees paid to the Sub-Administrator are commensurate with customary fees for the performance of such services. A director of the Fund is also an employee of the Sub-Administrator.

11. Financial Instruments and Associated Risks

The Fund maintains positions in a variety of financial instruments as dictated by its investment management strategy. The Fund’s investment portfolio consists primarily of investments in other private investment funds that it intends to hold for an indefinite period of time. The Fund also has investments in common and preferred stock.

The Fund’s investing activities expose it to various types of risk that are associated with the financial instruments and markets in which it invests. The most important types of financial risk to which the Fund is exposed are market risk, credit risk and liquidity risk.

Asset allocation is determined by the Fund’s Portfolio Manager who manages the distribution of the assets to achieve the investment objective. Divergence from target asset allocations and the composition of the portfolio is monitored by the Fund’s Portfolio Manager.

The nature and extent of the risks associated with the financial instruments outstanding at the balance sheet date are discussed below.

Details of the Fund’s investment portfolio at the Statement of Financial Position date are disclosed in the Condensed Schedule of Investments herein.

Arrowsmith Fund, Ltd.

Notes to Financial Statements (continued) (Expressed in United States Dollars)

33

11. Financial Instruments and Associated Risks (continued)

Market Risk

Market risk is the risk that the value of the Fund’s investments will fluctuate due to changes in security prices, stock indices and other market factors. Market risk embodies the potential for both losses and gains and includes currency risk, interest rate risk and price risk. The Fund’s strategy on the management of investment risk is driven by the Fund’s investment objective of long term capital appreciation through investments in publicly and privately traded securities. The Fund’s market risk is managed on an ongoing basis by the Portfolio Manager in accordance with policies and procedures in place. The Portfolio Manager invests in strategies that it believes differ from those followed by traditional asset managers. The foremost concern of the Fund is achieving the total compound return on assets with particular emphasis on the safeguarding of these assets. In doing so, it applies techniques more fully defined in the Fund’s Offering Circular.

All investments in securities present a risk of loss of capital. Underlying investment funds in which the Fund may invest may utilize such investment techniques as option transactions, limited diversification, margin transactions, short sales, futures and forward contracts and other leveraged or derivative transactions which can, in certain circumstances, significantly exacerbate any losses.

All individual investments in equity instruments are disclosed separately. All of the Fund’s investments are designated as at fair value through profit or loss and the fair values at December 31, 2014 and 2013 were fair valued as described in Note 2.

Price Risk

Price risk is the risk that the value of the instrument will fluctuate as a result of changes in market prices, whether caused by factors specific to an individual investment, its issuer or all factors affecting all instruments traded in the market.

As the majority of the Fund’s financial instruments are carried at fair value with fair value changes recognized in the Statement of Comprehensive Income, all changes in market conditions will directly affect the Fund’s results from operations.

Price risk is mitigated by the Fund’s Portfolio Manager by constructing a diversified portfolio of investments. In addition, price risk may be hedged using derivative financial instruments such as options or futures.

Arrowsmith Fund, Ltd.

Notes to Financial Statements (continued) (Expressed in United States Dollars)

34

11. Financial Instruments and Associated Risks (continued)

Price Risk (continued)

For the years ended December 31, 2014 and 2013, the Fund can be benchmarked against the S&P 500 Index as a point of reference to its correlation with price movements in the market.

The following details the Fund’s sensitivity to a 5.00% increase and decrease in the S&P 500 Index, with 5.00% being the sensitivity rate used when reporting market risk internally and representing management’s assessment of the possible change in market prices.

At December 31, 2014, had the S&P 500 Index been 5.00% higher with all other variables held constant, the increase in net assets attributable to holders of redeemable shares would have been $1,608,840 (2013 – $1,777,068). If the S&P 500 Index been 5.00% lower with all other variables held constant, the decrease in net assets attributable to holders of redeemable shares would have had an equal but opposite effect. The sensitivity is generally lower in 2014 than in 2013 because of a decrease in the net financial assets and liabilities at fair value through profit or loss at balance sheet date.

The sensitivity analysis above is based on management’s best estimate of the sensitivity to a reasonably possible change in price movements in the market. In practice, the actual trading results could differ from the sensitivity analysis and the differences could be material.

Currency Risk

Currency risk is the risk that the value of a financial instrument will fluctuate due to changes in foreign exchange rates. The Fund and the underlying investment funds in which it invests may invest a substantial portion of their assets in investments and/or assets denominated in currencies other than U.S. dollars, the base currency of the Fund, the price of which is determined with reference to currencies other than U.S. dollars. However, the Fund values, and such investment funds may value, investments and other assets in U.S. dollars. To the extent these investments are not hedged, the value of the Fund and any such investment fund’s assets is likely to fluctuate with U.S. dollars exchange rates as well as with price changes of the Fund and any such investment fund’s investments in the various local markets and currencies. The Fund and/or the relevant investment fund may utilize options to manage the risk against currency fluctuations, but there can be no assurance that such hedging transactions will be conducted and, if conducted, will be effective.

Arrowsmith Fund, Ltd.

Notes to Financial Statements (continued) (Expressed in United States Dollars)

35

11. Financial Instruments and Associated Risks (continued)

The Fund’s total net exposure to fluctuations in foreign currency exchange rates at year end was as follows:

Fair Value Fair Value 2014 2013 Assets Brazilian Real $ 748,661 $ 920,041 Canadian Dollar 273,861 – Euro 1,412,994 1,345,842 Hong Kong Dollar 299,568 – Indonesian Rupiah 196,925 – Japanese Yen 1,181,084 958,876 Mexican Peso 205,113 – Norwegian Krone 154,192 – Pound Sterling 1,250,976 731,014 Turkish Lira 145,138 – United States Dollar 63,924,127 55,932,487 Total $ 69,792,639 $ 59,888,260 Liabilities and shareholders’ equity United States Dollar $ 69,792,639 $ 59,888,260 Total $ 69,792,639 $ 59,888,260 At December 31, 2014, had the U.S. Dollar strengthened by 5.00% in relation to all other currencies, with all other variables held constant, net assets attributable to holders of redeemable shares and the change in net assets attributable to holders of redeemable shares per the Statement of Comprehensive Income would have increased by $293,424 (2013 – $197,790). A 5.00% weakening of the U.S. dollar in relation to all other currencies would have resulted in an equal but opposite effect on the above financial statement amounts to the amounts shown above, on the basis that all other variables remain constant.

The sensitivity analysis above is based on management’s best estimate of the sensitivity to a reasonably possible change in price movements in the market. In practice, the actual trading results could differ from the sensitivity analysis and the differences could be material.

Arrowsmith Fund, Ltd.

Notes to Financial Statements (continued) (Expressed in United States Dollars)

36

11. Financial Instruments and Associated Risks (continued)

Interest Rate Risk

Interest rate risk arises from the possibility that changes in interest rates will affect future cash flows or the fair values of financial instruments. The majority of the Fund’s financial assets are non-interest-bearing. Interest-bearing financial assets and interest-bearing financial liabilities mature or re-price in the short term, no longer than twelve months. As a result, the Fund is subject to limited exposure to interest rate risk due to fluctuations in the prevailing levels of market interest rates.

The Fund or the underlying investment funds in which the Fund invests may be empowered to borrow funds from brokerage firms, banks or other financial institutions in order to increase the amount of capital available for investment and or to fund redemptions. Consequently, the level of interest rates at which such borrowing can be made will affect the operating results of the funds. In addition, the Fund and or the relevant investment fund may in effect borrow funds through entry into repurchase agreements and may leverage its investment return with options, commodity futures contracts, swaps, forwards and other derivative instruments. As discussed in Note 6, at December 31, 2014 and 2013, the Fund had a note payable which is not subject to interest rate risk as it has a fixed interest rate.

The sensitivity analysis below has been determined based on the Fund’s exposure to interest rates for interest bearing assets and liabilities at the balance sheet date. The analysis assumes that the stipulated change takes place at the beginning of the financial year and is held constant throughout the reporting period in the case of instruments that have floating rates. A 100 basis point increase or decrease is used when reporting interest rate risk internally and represents management’s assessment of the possible change in interest rates.

For the year ended December 31, 2014 and 2013, an increase of 100 basis points in an annualized effective interest rate would have decreased the net assets attributable to holders of redeemable shares by $20,000 (2013 – $20,000). A decrease of 100 basis points would have an equal but opposite effect.

The sensitivity analysis above is based on management’s best estimate of the sensitivity to a reasonably possible change in price movements in the market. In practice, the actual trading results could differ from the sensitivity analysis and the differences could be material.

Arrowsmith Fund, Ltd.

Notes to Financial Statements (continued) (Expressed in United States Dollars)

37

11. Financial Instruments and Associated Risks (continued)

Credit Risk

Credit risk is the risk that a counterparty to a financial instrument will fail to discharge an obligation or commitment that it has entered into with the Fund. Concentrations of credit risk exist when changes in economic, industry or geographic factors affect counterparties whose aggregate credit exposure is significant in relation to the Fund’s total credit exposure. Predominantly all financial instruments are cleared through and held in custody by one institution. The Fund is subject to credit risk to the extent that this institution may be unable to fulfill its obligations either to return the Fund’s securities or repay amounts owed. The Fund does not anticipate any losses as a result of this concentration.

At December 31, 2014, the following financial assets were exposed to credit risk: investments in investment funds, cash at banks and other receivables. The carrying amounts of financial assets best represent the maximum credit risk exposure at the balance sheet date. This relates also to financial assets carried at amortized cost, as they have a short-term to maturity. Total carrying amount of financial assets exposed to credit risk amounted to $69.8 million (2013 – $59.9 million).

Credit Quality of Financial Assets

The following table contains an analysis of the Fund’s portfolio of debt securities by rating agency category.

% of Debt Securities

December 31,

2014 December 31,

2013 Credit rating BB –% –% B –% –% B- –% 46% NR –% 54% Total –% 100% The Fund did not hold debt securities as of December 31, 2014.

Arrowsmith Fund, Ltd.

Notes to Financial Statements (continued) (Expressed in United States Dollars)

38

11. Financial Instruments and Associated Risks (continued)

Liquidity Risk

Liquidity risk is the risk that a given investment cannot be traded quickly enough in the market to prevent or minimize a loss. The Fund’s financial instruments include investments in unlisted equity investments, which are not traded on an organized public market and which generally may be illiquid. As a result, the Fund may not be able to quickly liquidate some of its investments in these instruments at an amount close to its fair value in order to meet its liquidity requirements, or to respond to specific events such as deterioration in the creditworthiness of any particular issuer.

The Fund has the ability to liquidate its investments periodically in other funds, generally ranging from monthly to annually, depending on the provisions of the respective underlying fund’s agreements. The Fund’s investments include unlisted funds, which are not traded in any organized public market and which generally may be illiquid if not redeemable. These funds may have to apply redemption limitations such as gates and side-pockets or may even suspend their usual redemption process for a significant time (lock-up). At December 31, 2014, the underlying fund does not have any investments with a lock-up period greater than one year. Certain underlying funds may charge a redemption fee to the Fund should the Fund redeem its holdings prior to a specified lock-up period.

The following tables detail the Fund’s liquidity analysis for its financial assets and financial liabilities:

As at December 31, 2014

Less Than One Month

One Month to One Year

Over One Year Total

Financial assets Cash at bank and brokers $ 14,957,626 $ – $ – $ 14,957,626 Investments, at fair value 15,337,313 23,766,119 8,842,117 47,945,549 Investments made in advance – 6,010,000 – 6,010,000 Other receivables 212,616 – – 212,616 Receivables for investments sold 666,848 – – 666,848 Total financial assets $31,174,403 $ 29,776,119 $ 8,842,117 $ 69,792,639

Arrowsmith Fund, Ltd.

Notes to Financial Statements (continued) (Expressed in United States Dollars)

39

11. Financial Instruments and Associated Risks (continued)

The following tables detail the Fund’s liquidity analysis for its financial assets and financial liabilities:

As at December 31, 2014

Less Than One Month

One Month to One Year

Over One Year Total

Financial liabilities Due to portfolio manager $ 48,393 $ – $ – $ 48,393 Interest payable – 10,000 – 10,000 Long term borrowings – – 2,000,000 2,000,000 Payable for investments purchased 1,000 – – 1,000 Payable redemptions of funds 2,371,259 – – 2,371,259 Net assets attributable to holders of redeemable participating preferred shares – 65,361,987 – 65,361,987 Total financial liabilities $ 2,420,652 $ 65,371,987 $ 2,000,000 $ 69,792,639 As at December 31, 2013

Less Than One Month

One Month to One Year

Over One Year Total

Financial assets Cash at bank and brokers $ 15,469,222 $ – $ – $ 15,469,222 Investments, at fair value 4,582,200 29,852,752 7,523,028 41,957,980 Investments made in advance – 1,000,000 – 1,000,000 Other receivables 426,705 – – 426,705 Receivables for investments sold 1,034,353 – – 1,034,353 Total financial assets $21,512,480 $ 30,852,752 $ 7,523,028 $ 59,888,260

Arrowsmith Fund, Ltd.

Notes to Financial Statements (continued) (Expressed in United States Dollars)

40

11. Financial Instruments and Associated Risks (continued)

As at December 31, 2013

Less Than One Month

One Month to One Year

Over One Year Total

Financial liabilities Due to portfolio manager $ 248,846 $ – $ – $ 248,846 Interest payable – 10,000 – 10,000 Long term borrowings – – 2,000,000 2,000,000 Payable for investments purchased 588,839 – – 588,839 Contribution received in advance 1,150,000 – – 1,150,000 Payable redemptions of funds 2,809,797 – – 2,809,797 Net assets attributable to holders of redeemable participating preferred shares – 53,080,778 – 53,080,778 Total financial liabilities $ 4,797,482 $ 53,090,778 $ 2,000,000 $ 59,888,260 12. Subsequent Events

Subsequent to year end, the Fund recorded $5,272,520 of subscriptions for Class A. Additionally, the Fund recorded $6,542,052 of redemptions from Class A and $395,902 of redemptions from Class B, of which $2,371,259 was payable on December 31, 2014.

![Nietzsche notes for ''we philologists'' [arrowsmith]](https://static.fdocuments.net/doc/165x107/5790563a1a28ab900c985b6e/nietzsche-notes-for-we-philologists-arrowsmith.jpg)