A Digital Edition of a Single-entry Bookkeeping System in ...

41

A Digital Edition of a Single-entry Bookkeeping System in Spreadsheet Databases – The case of the Portuguese Silk Factory Company’s First Administration (1734-1745) Introduction This paper is about accounting history digital editing (AHDE), a subarea of digital history editing, designed in spreadsheet databases. It is a first early attempt to digitally edit the whole single-entry bookkeeping system of the Portuguese Joint-Stock Silk Factory Company’s First Administration (1734-1745), throughout its nine accounting books. The project intends to create an Excel workbook with nine sheets, one for each accounting book, making first from the original document the digital transcription of records (digital document) and then create spreadsheet databases (digital data). The choice of the fields to create is critical and will need the collaboration of other relevant knowledge areas (e. g. computer scientists). This project will have as reference the George Washington Financial Papers Project (GWFPP) and Carvalho (2017). The first makes available in its site (http://www.financial.gwpapers.org/) account records digital editing (ARDE) of three general ledgers (1750 - 1799) and a cash book (1811 - 1816), using the Drupal database software in the PHP language. It is an innovative digital editing (DE) with very much quality, following the best practices. Its responsible, Jennifer Stertzer, found many new and complex problems and has created solutions for them. This project can be a good benchmarking tool. Carvalho (2017) follows the same database approach but with a different and simpler software, a spreadsheet database (Microsoft® Excel®) to represent the Journal records of

Transcript of A Digital Edition of a Single-entry Bookkeeping System in ...

A Digital Edition of a Single-entry Bookkeeping System in

Spreadsheet Databases – The case of the Portuguese Silk

Factory Company’s First Administration (1734-1745)

Introduction

This paper is about accounting history digital editing (AHDE), a subarea of digital history

editing, designed in spreadsheet databases. It is a first early attempt to digitally edit the

whole single-entry bookkeeping system of the Portuguese Joint-Stock Silk Factory

Company’s First Administration (1734-1745), throughout its nine accounting books. The

project intends to create an Excel workbook with nine sheets, one for each accounting

book, making first from the original document the digital transcription of records (digital

document) and then create spreadsheet databases (digital data). The choice of the fields

to create is critical and will need the collaboration of other relevant knowledge areas (e.

g. computer scientists).

This project will have as reference the George Washington Financial Papers Project

(GWFPP) and Carvalho (2017). The first makes available in its site

(http://www.financial.gwpapers.org/) account records digital editing (ARDE) of three

general ledgers (1750 - 1799) and a cash book (1811 - 1816), using the Drupal database

software in the PHP language. It is an innovative digital editing (DE) with very much

quality, following the best practices. Its responsible, Jennifer Stertzer, found many new

and complex problems and has created solutions for them. This project can be a good

benchmarking tool.

Carvalho (2017) follows the same database approach but with a different and simpler

software, a spreadsheet database (Microsoft® Excel®) to represent the Journal records of

Silk Factory Company (SFC) in its Second Administration, a double-entry (partidas

dobradas, in Portuguese) bookkeeping system, in order to obtain the Ledger records.

Although some outputs of the spreadsheet databases were displayed, the workbooks were

not publicly presented.

Comparing with GWFPP, this spreadsheet project is more centered in the accounting

knowledge related to the bookkeeping of that age (18th century). So, it is interesting to

have the brief reference to stewardship bookkeeping (charge and discharge system) and

to the differences between single-entry bookkeeping (SEB) and double-entry

bookkeeping (DEB). A simple reference to the triple-entry and quadruple-entry are also

made, because of the reliability of accounting information.

ARDE projects produce information to be used by others whose major formation is not

History (e. g. accountants, economists). And so, it is important to know what outputs they

need and what are the contributions they can give to the project, namely the accountants.

This paper makes a first attempt in AHDE, in a similar way to that of Carvalho (2017),

to represent the whole accounting system of the SFC’s First Administration (1734-1745),

in Excel spreadsheet databases. Instead of digitally representing a book, this paper intends

to represent a larger reality, an accounting system. So, it is possible to consider three

levels of DE: Documentary editing, ARDE and AHDE.

The remainder of this paper is structured in six parts: (1) DE, that includes three sections,

(2) research design, (3) contributions of accounting knowledge, that includes three

sections, (4) the SFC’s bookkeeping system, that includes three sections, (5) the Excel

AHDE project, and (6) the final part, discussion and conclusions and suggestions.

The first section of DE part compares the evolution of the research teams stages, in Digital

Accounting History (DAH) and Digital History of Accounts (DHoA) and suggests the

designation of “tribes”, in a similar way to that of Domingos (2015), the second explains

what DE consists of and the third deals with the state of the art of DE in DHoA, presenting

the case of the GWFPP.

The second part (section) explains briefly the research design framework, following

basically Bernal Torres (2000).

The third part, about contributions of the accounting knowledge, presents three issues:

“Charge and discharge accounting versus double-entry accounting?”, showing that they

are not incompatible, “Single, double, triple and quadruple-entry bookkeeping”, to show

that double-entry is more reliable than single-entry, and “The Accounting Entity of a

bookkeeping system”, that shows the impact of changing the entity in the bookkeeping

system.

The fourth part of the SFC’s bookkeeping system has three sections. The first is “The

case of the Silk Factory Company’s First Administration”, in which the history of SFC is

told, particularly the First Administration. The second is “The importance of First

Administration bookkeeping system”, in which seven issues of importance are identified.

The third is about the bookkeeping system of the First Administration, in which the

organization of the accounting books is presented and the most important books are

described.

Finally, in the last two parts, it is treated the AHDE Excel project, in which clues for what

the system is intended are presented, and the (1) discussion and (2) conclusions and

suggestions sections, where challenges are indicated (e. g. new problems to solve) and

suggestions presented.

Digital Accounting History (DAH) and Digital History of Accounts (DHoA)

According to Carvalho (2017: 5), in the Accounting History research (AHR) evolution of

the research teams four phases can be considered:

1 – Primordial research: The research teams are composed only by accountants;

2 – Traditional research: The teams are composed by accountants and historians;

3 – Digital research: The teams include accountants, historians and computer scientists;

4 – Holistic research: The teams include all relevant specialists (e. g. economic historians

or philosophers).

This paper considers that AHR is in the second phase and it is important to proceed to

another stage, the digital research. In terms of accounts research, the historian teams

evolution is different. They are doing digital history of accounts (DHoA) research. It is

possible to consider three phases in the DHoA:

1 – Traditional research: The research teams are composed only by historians;

2 – Digital research: The teams are composed by historians and computer scientists;

3 – Holistic research: The teams include all relevant specialists (e. g. accountants,

economists or philosophers).

The accountants should be considered in the DHoA third phase because they are relevant

to the accounts study. So, like Domingos (2015) considers five “tribes” in Machine

Learning1, it is possible to identify two “tribes” of researchers in the study of the history

of accounts in the digital way, the digital historians (tribe H) and the digital accountants

(tribe A). There are other “tribes” that are relevant for the history of accounts, for instance,

the digital economists (Tribe E) or the digital linguists (tribe L). Similar to the DAH

should be considered the DEH, i. e., digital economic history. All the “tribes” that are

relevant to the study of digital history of accounts would form the “society” of digital

1 The five “tribes” of Machine Learning are: Symbolists, Connectionists, Evolutionaries, Bayesians and Analogizers.

historians of accounts (DHoA) or later the digital accounting history (DAH). Normally,

the papers presented in DHoA are in phase 2.

What is Digital Editing (DE)?

This paper deals with the DE of an accounting system with nine books that are in AN /

TT (Lisbon). Each book has dozens or even hundreds of pages and they are handwritten.

To know the books contents, it is necessary to understand the language and the

handwriting.

In the past, it was very difficult to access a book or a document that could be in another

continent. It was possible to go there, buy it or borrow it. Another possibility was to ask

for photocopies and receive them by mail. Nowadays, it possible to receive by email the

photos of each page of a book, paying or not. Each photo is a digital document that

reproduces the original document. Today the great effort that is done is to digitize all

documents with interest to research and turn them accessible to everyone.

The next stage to improve the understandability of the document was to transcribe it and

to print it in press letters (e. g. in a book). So, it was easy to translate it in other languages.

A better way to transcribe it can be a digital device, like Word, Excel, or another software

language (e. g. xml). This is digital editing. It is easy to copy a part of a document to

another digital document. A digital document was created, but it is still a document. The

Association for Documentary Editing (The ADE) was created in 1978. So, in terms of

DE there is a gap of four decades between the tribes H and A.

The new level was to create data from the set of documents that constitutes a book or

several books when their information is organized in a certain way (e. g. database) and

joining the maximum information related to each document. It is necessary to create a

digital device where it can work. For instance, Carvalho (2017) selected the Excel

application and Stertzer’s team selected Drupal databases. Stertzer (2014) clearly traces

the difference between digital document and digital data. This turns an original “dead

document” into a “living document” that “talks”. With this organized information it is

possible to extract new information, comparing it with similar situations in other

countries, and create new knowledge, allowing to propose new theories. So, five phases

can be considered in the DE process: (1) Book digitization (a folder of files), (2)

Document transcription, (3) Translation into English (or other language), (4) Databases

and (5) Extraction of information (e. g. tables obtained from the databases).

The State of the Art of Digital Editing in Digital History of Accounts (DHoA)

There is no Digital History of Accounts without Digital Editing (DE). Stertzer (2014) is

a fundamental article, based on the GWFPP, to understand the state of the art of DE in

DHoA. It starts in 1980s, when several pages from the ledgers were published, in print.

Over the years Jennifer Stertzer thinks about accessibility solutions for the financial

papers and in 2009 decides the financial papers should be a digital-only edition. It was

possible digitize the documents (e. g. photos). The initial approach was XML-based to

describe the financial documents, but later the Stertzer’s team selected the relational

database / Doc Tracker solution, that began in July 2012, in a funded project. This tool

transcribes documents and creates data. The final output appeared in 2017.

A visit to the GWFPP’s site is interesting. It has eight groups of issues (The Financial

Papers, About, Documents, Search, Explore, Learning Center, Resources and Contacts)

and allows us to have an idea of the state of the art of DE in DHoA. The first group is

divided into three parts (About the Project; What are Financial Documents? and Explore

the Financial Papers. In the second group (About), it is presented the Project Background

and Project. The GWFPP's two main objectives were to develop a freely accessible digital

editing and an open-source editorial platform. In the Document group, one of the four

accounting books should be chosen. Search group permits advanced search. Explore is

for doing advanced search by People, Places, Ships, Occupations & Titles, Services,

Foods & Beverages, Agriculture and Place Types. Learning Center presents Articles &

Blog Posts, Visualizations and Presentations & Posters. Resources include Editorial

Methodology, Glossary, Bibliography and Site Manual. Editorial Methodology treats

information about Transcription, Format, Annotation, Contents Types, Taxonomies,

Bibliography, Platform Design, Documents and Data and How to cite the Edition.

With the path Documents and the ledger A, page 10 is obtained the account Cash, both

debit and credit (http://financial.gwpapers.org/?q=content/ledger-1750-1772-pg10). It

presents the edition and images 1 and 2, and also information of this folio about people,

place, occupations & titles, services and book. It also indicates a glossary of terms and a

money calculator. Very relevant are the annotations. For instance, in this editing page the

metadata about John Carlyle give much information. He was a merchant and military

(colonel), born in 1720 and died in 1780. There is much information related with him (e.

g. places). It clearly remembers digital augmented reality, the so-called intelligence

augmented (IA). It is an outstanding project. A possible criticism is some lack of

accounting knowledge. This paper presents three issues of accounting knowledge.

Stertzer creates a Center for Digital Editing (CDE). It concentrates the resources and

expertise necessary to advance the practice of editing and growth of innovative digital

project solutions.

Carvalho (2017) presents a paper with the case of SFC’s Second Administration, with a

double-entry bookkeeping system, using Excel application for AHDE and transforming

the Journal database in a Ledger database.

A brief Research Design

Bernal Torres (2000, p. 74) suggests for the research process framework the first

following phases: subject, problem, objectives, justification and delimitation and type of

research. So, in this paper the phases are the following:

• Subject – AHDE

• Problem – How to improve the research quality through AHDE, creating a

database template, as all-purpose as possible.

• Main objective – Creating an AHDE database template in Excel.

• Specific objectives – Create innovative fields in the database. Identify and solve

problems raised by the accounting books (e. g. measures, arithmetical errors).

• Justification and delimitation – AHDE is a powerful tool to improve AHR and

uses intelligence augmented (IA). This paper looks for a solution among several.

It does not want to determine the best solution to the problem.

• Type of research – Case study in historical research. The case is the bookkeeping

system of SFC’s First Administration.

According to Phillips and Pugh, (1994, p. 50), the basic type of research is a problem-

solving research. But it is also an exploratory research. In fact, Stertzer (2014) shows a

long journey with new challenges and barriers and finding new solutions to the problems,

a pioneer work that includes a diversified and expert team, with a funded project. This

project of editing books of accounts in single entry reached an output of great quality.

The present paper tries to find a solution to a whole accounting system using databases

in an Excel environment. So, in this case, it is necessary to create different databases to

different accounting books, which is a more complex problem. The biggest difficulty is

for each database to define the relevant databases fields. So, the suitable type of research

should be also exploratory.

Charge and discharge accounting versus double-entry accounting?

This paper suggests that the accounting knowledge is needed to obtain better spreadsheet

databases, through new accounting fields and the table of each field. In order to improve

the database design, choosing the more suitable database fields, it is very important the

discussion of questions like these: “Is double-entry accounting the opposite system of

charge and discharge accounting?” or “Is double-entry accounting a more reliable system

of charge and discharge than single-entry accounting?”. The study of the charge and

discharge accounting and the discussion of the number of entries (e. g. single vs double)

can contribute to the better quality of the databases. To address these issues, the first

question is treated in this section and the second in the next. Another question even more

important is about the identification of the accounting entity, treated later.

The charge and discharge accounting is linked to the agency relationship between the

principal and the agent. This one acts on behalf of the principal, but there is asymmetry

of information because the former has all information needed. So, what is the best way to

render the accounts of what has been done on behalf of the principal? The solution was

the creation of an accountability process in which he was charged by the money he had

received and discharged by the payments he has made in order to ascertain the final

balance. The registration process is called the charge and discharge accounting or

stewardship accounting or agency bookkeeping.

The first medieval charge and discharge system can be identified in the English

Exchequer about 1110. This system was gradually diffused to other European

Exchequers, to monasteries and bishoprics, to lay estates, to manorial accounting, to

guilds, boroughs, universities and parishes (Jones, 2008a: 355). From the Royal

Exchequer, the practices gradually spread to the monasteries and bishoprics, to lay estates

and then down to the manors (p. 356). The English Exchequer system was devised by

Roger of Salisbury, in Henry I’s reign (1100–1135). There was an upper Exchequer (an

auditing chamber), which met formally twice a year and a lower Exchequer (the treasury).

Seventeen royal officials sat round the Exchequer table and watched the treasurer

interview the sheriff, the King’s official. The system basic principle was ‘charging’ the

sheriff with the King’s revenue and ‘discharging’ the sheriff when he had successfully

rendered his account (p.357).

Stone (1993) presents several accounts (Exchequer, abbey, guild, manorial and

household) to trace the development of charge and discharge accounting. This had always

the primary objective of accountability (p. 6). Profit and loss account was not determined

(idem, p. 6). It was an accounting about persons, not things. In the 17th century, in

England, farm accounting had changed the emphasis from accountability and innovations

were made in profit determination (ibidem, p.6). These changes resulted from new needs

of management.

The charge and discharge accounting, that has a vast literature (e. g. Littleton, 1933, Lee,

1975, Edwards, 1989, Mills, 1986, Hernández Esteve, 1993), precedes the double-entry

bookkeeping (DEB), known after the Pacioli’s Summa (1494). Pacioli was not the

inventor of double-entry, but the main promotor, a changing agent. Sangster (2016: 305)

considers that origins of double-entry occurred in Florence in the ledger banks in the early

13th century. Gradually DEB substitutes the charge and discharge accounting. DEB use

became widespread in the first half of the nineteenth century (Lemarchand (1994: 140).

This article makes a comparison of accounting records in French companies, in the 17th

and 18th centuries, in the use of the charge and discharge accounting and DEB, and

concludes that it depends on the activity sector, financiers and types of professions. For

instance, double-entry was the merchant’s model and was used in the textile industry,

where the capital came from trade. On the other hand, charge and discharge accounting

was the accounting model of mining and metallurgical enterprises, where the capital was

from the nobility and financiers (p. 119). It presents three cases of simultaneous use of

charge and discharge and double entry (p. 123 and 127). Clearly, these systems are not in

opposition, they coexist.

Normally, the charge and discharge accounting was recorded in single-entry, because it

was enough to solve the accountability problem. The double entry was also possible. This

permits a better control of accounts and a change of the accounting entity: the enterprise.

To improve the database, it is interesting to create a group of two fields for the agency

relationship, based on an agency table. These should be: Code of agency type and agency

type.

Single, double, triple and quadruple-entry bookkeeping

Nowadays, the accounting systems are in double-entry. It is possible to consider, in terms

of numbers of entries by each operation, other accounting systems: single-entry, triple-

entry, quadruple-entry and multidimensional system. The last is possible in databases in

which the accounting phenomena are represented. The case in which there is no

accounting, it is possible to consider: (1) current records of accounts and (2) accounting

records in books with debit and credit, but do not form an accounting system.

Currently, accounting historians prefer ancient accounting records in double-entry to

single, because the former is more evolved. But there is much relevant information in

single-entry, mainly associated with the charge and discharge accounting and can present

much information useful for DE.

To analyze an accounting system it is necessary to know the accounting books available,

the interconnection among them and the number of entries for each operation. Concerning

the latter, it is important to know whether it is an accounting system or isolated records.

The enterprises use the double-entry accounting system, i. e., for each operation, there are

normally two entries, one at debit, and another at credit, for the same value.

Clearly, double-entry is considered more reliable, because of the balancing game that

supports it. Theoretically triple-entry should be more reliable than double-entry.

The triple-entry bookkeeping was invented in Russia by Fedor V. Ezersky (Platonova,

2015 and Sá, 1983: 312). He wrote in the book: “The frauds, losses and errors in balance

sheets as a part of the double-entry system of bookkeeping and detected by the indicators

to the accuracy of the accounts offered by the Russian triple-entry”, in 1876 (apud

Platonova, 2015). It was translated in French in 1878. He was a critic to the double-entry.

More than a century later Iuji Ijiri published two books about triple-entry accounting (Ijiri,

1982 and Ijiri, 1989). None of these three books had success in promoting the method.

Currently, Portuguese firms had to report to the Tax Administration (AT) the annual

inventory in quantities and next year (January 2020) they have to report the inventory of

2019, in quantities and values. They have also to report all the invoices processed and the

accounting records produced. As AT has all the accounting external information, it is

possible that some Portuguese accounting firms (gabinetes de contabilidade) can

download all the accounting information of each client from the AT databases. In this

case, there is a significant time reduction in the record of the accounting documents

processing. This information technology, using the blockchain, increases very much the

reliability of the system. It is not possible to create new documents and records related to

the past, which reduces the fraud. This system is clearly more reliable than the traditional

double-entry. Today, is the so-called triple-entry accounting (e. g. Wiatt, 2019). There is

a lot of information and discussion about triple-entry.

Wiatt (2019: 29) in an article about the blockchain technology shows a figure presenting

the triple entry movements, including the distributed ledger

(https://sfmagazine.com/issue/january-2019/). This paper disagrees with this article,

because each accounting operation has four records. There are three operations and twelve

records. Eventually, it was more suitable to call it quadruple-entry. A more accurate

designation to the figure in the review’s page 29 would be triple-entities accounting.

This triple-entry (or quadruple-entry) accounting does not change the accounting

technique, that continues to be double-entry in each firm with the same output documents.

There is also a reduction of errors (e. g. two intervenient firms in the same operation

cannot report it with different values), namely from the blockchain technology. What

changes is the accuracy of the accounting systems, that clearly are more reliable, and the

significant time reduction in the introduction of documental information in the computers.

What changes is a better reliability of the accounting system and a reduction of cost

processing.

To improve the spreadsheet database, a field with the number of entries should be created.

.

The Accounting Entity of a bookkeeping system

One of the most important principles in accounting practice is the Business Entity. There

is a clear separation between the enterprise and owner. If there is a different accounting

entity, then the accounting records are completely different and the outputs of the

accounting systems are quite different.

The design of the accountability process depends on the problems to solve (e. g.

embezzlement, theft or profit). It is necessary to create suitable accounting system and

audit system and also to define the rules and procedures, more or less formal, to render

the accounts. Normally, accounting systems tend to contribute to the solution of the

problems faced in the accountability process. When the problems change, then it is tried

to improve the system with innovations or create different new systems in order to solve

the problems faced.

The English Exchequer accountability process creates an accounting system (charge and

discharge) to support that process, in which the sheriff renders accounts to the King

through the Treasure. This is an agency relationship. The bookkeeping records can be

registered in the first name (e. g. I received this rent or I paid this work). The books are

recorded in single-entry. The accounting entity is the accountant / cashier / sheriff.

A merchant in the 17th century can register their accounts in double-entry. He himself

does the accounting registrations. He wants to solve the problem like to know the profit

or the business, or what is owed to a supplier. The accounting entity is his wealth, which

has a mixture of business and personal expenses.

In the first case, the Exchequer system was people-oriented, with personal accountability

being at its heart. There was a personal accountability (Jones, 2008b). In the second case,

it was a mixture of persons and things (e. g. inventory), also with the objective to know

how well the business runs, i. e. whether he has profit.

When the accounting entity is the enterprise, the final documents of accounts were totally

different. It is an accounting system of person and things. The profit and loss account is

very important in the new accounting system. The accountability continues to exist and

the rendering of accounts continues to be necessary for the approval of accounts by the

partners.

The accounting entity is a very important group database field. When it is changed, the

accounting outputs are totally different. It should be created a table with the Code of

Accounting entities and the Accounting entities. It is relevant to consider the accounting

entities not only for the study of the case, but also for all other situations, like other kinds

of firms, other ages, other sectors, other countries, etc..

The case of Silk Factory Company’s First Administration

Silk Factory Company (Companhia da Fábrica das Sedas) was a joint-stock company

and was created on October 5, 1734 (B797: s. 2, i. 27)2 by nine partners (shareholders).

The Frenchman Robert Godin was the expert, had no capital and he was called

“Mercenary”. Silk Factory Company (SFC) was private until June 15, 1750, when it

became the property of the Royal Treasury (Real Fazenda) and was called Royal Silk

Factory (Real Fábrica das Sedas). The company ends in 1835.

The private and joint-stock had three administrations: First (1734 – 1745), Second (1745

– 1747) and Third (1747 – 1750). The First Administration of the Company was

constituted by three directors, Manoel Nunes da Silva Tojal, Francisco Xavier Ferraz de

Oliveira and Domingos da Silva Vieira. When the last two were missing, on the death of

2 Reference B797: s. 2, i. 27 means that it is in book 797, on sheet 2 and the photographic image is the 27.

It is also used page (p.) and folio (f.).

the first and the second being useless, Tojal became the sole director (Almeida, 1989-90:

9). The first had an annual salary of 600$000, for the brassage of the cash (B797: s. 37, i.

97). He was the only director to receive a salary. In the Second Administration no longer

received any salary (Carvalho, forthcoming: 6).

This paper studies the First Administration and tries to understand the transition to the

Second Administration’s bookkeeping system. The bookkeeping registration was quite

different in each Administration. The Second Administration has a double-entry

bookkeeping system and it was studied by Carvalho, Rodrigues and Craig (2007). This

article traces a brief history of the SFC (p. 66 – 70). Both administrations have a charge

and discharge accountability system.

Carvalho (forthcoming: 10) considers that the activity of the First Administration can be

divided into three periods:

• Start-up of the activity and construction of the new Rato factory (1734 - 1737);

• Exploration of the factory in the new facilities and completion of the building and the

annexed constructions (1738 - 1740);

• Normality - The Company at cruising speed (1741 - 1745).

The delimiting facts of these periods are the change of facilities from the factory to the

new Rato building, which occurred at Christmas 1737, and then worked with all the

necessary conditions and the completion of the building and other annexed buildings were

only completed at the end of 1740.

In the National Archives (AN / TT) there are 34 accounting books of Silk Factory

Company, of which nine are from the First Administration. The study of these books will

allow to understand the accountability system (charge and discharge) and the

bookkeeping records. The digital accounting history (DAH) approach, similar to

Carvalho (2017), with spreadsheet databases that permits more data and more control

over the data bookkeeping, resulting in deeper analyses, useful to a better understanding

of the different sort of the company’s problems.

The importance of the First Administration’s bookkeeping system

In this section, seven relevant issues about First Administration’s bookkeeping system

are identified:

1 – Differences in the bookkeeping systems of the First and Second Administrations;

2 – Accounting books more ancient than those of the First Administration;

3 – Inventory at the end of the First Administration (Balance Sheet);

4 – Identification of different accounting entities in the First and Second Administrations;

5 – Is First Administration’s bookkeeping really an accounting system?

6 – Better understanding of the Second Administration’s bookkeeping with the study of

the First Administration’s bookkeeping.

7 – Reasons for the interest of analysing SFC’s bookkeeping systems.

Silk Factory Company has an accountability system of charge and discharge in both

administrations supported by a single-entry bookkeeping system in the First

Administration and a double-entry in the Second Administration. It is the oldest

Portuguese bookkeeping system of a Manufacture and that of the Second Administration

is the oldest in double-entry. It is worth understanding that evolution.

Gonçalves (2018, p. 32 and 33) refers three ledgers books of Portuguese merchants that

are older than SFC’s accounting books: Francisco da Gama (1619-1621), Manuel de

Sousa de Meneses (1660-1715) and António Coelho Guerreiro (1653-1717). Analysing

the books under accounting lens, that paper concludes that the two first have records in

single-entry of a current accounts ledger. More interesting could be the third, which was

studied by Rau (1956) and Rocha and Gomes (2002). It was raised the question whether

it was written in double-entry, but the latter article concluded that it was a single-entry

bookkeeping. Besides, 19 sheets were torn from the initial 48 folios (p. 622).

Manoel Tojal, Administrator and Cashier, presented at the end of First Administration, in

the Inventory book (B214), the SFC Balance Sheet. It is an admirable document that

presents the assets, liabilities and equities. He was the accountant and the accounting

system permitted to obtain that Balance Sheet. Lemarchand (1994: 129) indicates that the

author has found a bilan en doit et avoir (debit and credit balance sheet). It adds that as a

matter of fact, this is just a trial balance signed and certified by the head of accounting.

Probably, Tojal’s balance sheet is better than that one.

The bookkeeping systems of the First and Second Administrations and Closing Inventory

above have three different accounting entities. In the First Administration’s bookkeeping,

the accounting entity is the accountant, Manoel Tojal, also being Administrator, Cashier

and Shareholder. In the Closing Inventory, the accounting entity is the company (SFC).

Finally, in the Second Administration’s bookkeeping, the accounting entity is the Second

Administration itself, i. e., the set of three administrators (Manoel de Sande de

Vasconcelos, Christian Stockler and Manoel Nunes da Silva Tojal). The comparison

between the Tojal’s closing inventory (B214) and the Beginning Inventory of the Second

Administration (February, 1, 1745) is rather different. The debts considered in both cases

are also different and a particular debt was split in two, the Second Administration had to

bear one part and the First Administration the remainder.

The bookkeeping system tries to solve problems of accountability, has an articulated set

of books, with the current accounts ledger as the main accounting book and was able to

produce at the end of the First Administration a balance sheet of great quality. So, this

paper considers that is a complete accounting system.

The reason for a better understanding of the Second Administration’s bookkeeping with

the study of the First Administration’s bookkeeping will be analysed later (p. 20).

Finally, there are relevant reasons for analysing the bookkeeping system, because it was

used in (1) an ancient age, prior to the British Industrial Revolution, to the first book

written in Portuguese about bookkeeping (1758) and to the Lisbon’s earthquake/tsunami

(1755); in (2) a complex organization, a private joint stock company and also a large

manufacture; and (3) trying to respond to accountability problems.

The reality of trade is less complex than that of the manufacture and the joint-stock

company. In this case, the accountability process, it is more difficult and the administrator

has an agency relationship with the shareholders, from type principal - agent.

The bookkeeping system of the First Administration

The First Administration’s bookkeeping has the following available nine books (AN /

TT, 1995: 43):

- Current accounts of partners (Contas correntes de sócios), Book 797 (1734 - 1745);

- Inventory (Inventário), Book 214 (January 31, 1745);

- Account of what the house costs (Conta do que custou a casa), Book 536 (1735 -

1744);

- Partners entry (Entrada de sócios), Book 980 (1734 - 1742);

- Interest sheets belonging to the partners (Folhas de juros pertencentes aos

interessados), Book 306 (1738 - 1745);

- Shipments (Carregações), Book 712 (1735 - 1745);

- Draft debtors (Borrador de devedores), Book 520 (1735 - 1749);

- Entry and exit of silk and more goods (Entrada e saída de seda e mais géneros), Book

1054 (1734 - 1745);

- Entry and exit of silk clothes (Entrada e saída das fazendas de seda), Book 1020

(1734 - 1745).

These are a set of nine available accounting books. However, there are references to other

books, like draft expenses (borrador de gastos), daily draft (borrador diário) and draft

accounts (borrador de contas) that are not available. A cash book would make sense, but

there is no reference to it. In the bookkeeping system there is a main book, “current

accounts of partners”, and a complementary book, “Inventory”. The other seven books

are auxiliary, because all their information should be transferred into the main book.

Although being an auxiliary book, the “Account of what the house costs” deserves a

special note, because they have diverse information to know better the society of that age

and useful for economic historians. The inventory book is also amazing, with the

Company's Balance Sheet, at the date of January 31, 1745, recorded in the Inventory Book

(B214). It is a remarkable accounting item for the age, since it involves the tangible fixed

assets, liabilities and capital and profit / loss of the period.

The indication made by AN / TT (1995: 43) as “Current accounts of partners” is not

correct, because there are also accounting operations with the stakeholders. The book

cover has the following indication (B797, cover book, i. 1), in three lines: 1ª

Administração; Contas correntes; desde 1734 athe 1745 (1st Administration; Current

Accounts; from 1734 until 1745). The paper prefers to indicate it as "Current Accounts

Ledger Book" (B797).

According to Carvalho (forthcoming), the nuclear account of "Current Accounts Ledger

Book" (B797) is "Interested in the Company" (“Interessados na Companhia”), i.e. the

partners (shareholders). It registers the charges and discharges of the Cashier and

Administrator, Manoel Tojal (the agent) with the set of the partners (the principal) and

the balance of the account represented the value that he has to be or to pay to the partners.

In the Ledger, the debit and credit records are made under the rule "who receives owes,

who delivers has to be," (“quem recebe deve, quem entrega tem a haver”) should be

followed. In the account "Interested in the Company", when the Cashier receives

something, he is charged and the account “Interested in the Company” is registered in the

creditor side of the folio (Has to be or "Há de haver"). When he pays, he is discharged

and the account is registered in the debitor side (Owes or "Deve"). The perspective of this

account is the opposite of the Cashier, like a mirror, an account reflection. The absence

of cash account can be intriguing, but there are similarities with Sangster (2016: 302),

that says: “The absence of a cash account was a consequence of the Catholic Church’s

prohibition of usury”. But the account “Interested in the Company” does not control daily

the movements of cash, because, for instance, the sales are registered every three years

and at the closing of the First Administration there are accounting operations not

concerned with cash.

The book “Account of what the house costs” (B536) has the original title “Conta do qve

cvstov a caza em qve se estabeleceo a Fabrica e ovtras moradas a ella pertencentes”

("Account of what costs the house in which establishes the Factory and other dwellings

to it belonging") and joins the period of "1735 until 1740". It has two parts, the first related

to the factory building and the annexed constructions (65 pages) and second with its

financing (50 pages), only with outside capital. The files have 124 images. The final cost

of the house is 31:037$875 (B536: p.65, i.69). A summary is presented on pages 63 and

64 (i. 67 and 68). The borrowed capital was 30:632$320, with a summary on p. 89 (i. 93).

A summary of interests paid (5:021$193) is presented on p. 88 (i. 92), with the indications

of annual interests, on the left of the page, and the borrowed capital on the right. The

lenders accounts have a ledger format: the debit, “Owes”, on the left side of the folio and

the credit, “Have to be”, on the right side. Costs of the house (B536) were only transferred

to the master book 797 (Ledger) when all the works were completed (January 2, 1741).

The Book of Shareholders Entry (B980) registered the 153 subscriptions of shares of

400$000 each, but two (no. 95 and 96) were not paid. So, the total social capital was

60:400$000 and there were 27 shareholders at the end of the Administration (1745). The

first share was signed on October 8, 1734, and the last on May 28, 1742.

It does not seem interesting to continue detailing the other accounting auxiliary books,

except the book “Interest sheets belonging to the shareholders” (B306). This book shows

that total loans were 12 and the amount was 40:400$000 (B306: 4 - 25, 5a and 5b). But

the debit loans considered in the beginning of Second Administration were 18:910$525

(B720: p. 1-8; i. 7-14). Why? Carvalho (forthcoming: 25) explains:

“The logic of the Second Administration's assumption of responsibility was to pay the

inventories (including debtors' debts) it received and to be committed to pay the same

amount of debt borrowed by the company. Thus, he did not have to pay anything to the

shareholders. The remaining debts were assumed by the shareholders of the First

Administration and were considered as referring to the Factory House (Casa da Fábrica).

These debts and their interest were recorded in Book 303 and those in Book 304. It is

interesting to see the description of Book 303 (p. 6: i. 14) in which administrators state

that they have paid the inventories they have received because of an error in the weight

of the dyed silks, of hair and weft, and thus are lenders of those interested of that

difference.”

The responsibility of paying to the remaining lenders is from the First Administration.

There was even a debt (Father Jozé Dias) that had to be split up, being part of the

responsibility of the new administration and the other part of the shareholders. It is

necessary to study the First Administration to understand better the Second.

The organization of the accounting books is well understood with the example of a

"Money Charge and Discharge Account", in manorial accounting, presented by Edwards

(1989: 35), also referred by Carvalho (forthcoming). It says that, on the charge group,

there are four types of revenues that with the beginning balance of what he owes to the

"lord of the manor" gives the total revenue. On the discharge side, there are three types

of payments that give the total of payments. The difference between the charge and the

discharge gives the final balance of what he owes to the "lord". This paper agrees with

Carvalho (forthcoming) when it says:

“In this charge and discharge accounting, two revenue groups and two expenses groups

were created, depending on the construction of the Rato building or the fabric business.

Thus, it was decided to finance the construction of the building with interest-bearing

loans, registering in the cost of the house book (B536), both its payments and the receipts

obtained by the borrowing. In the current accounts book (B797) the expenses and

revenues of industrial activity were recorded. When the building construction and the

annexed constructions were finished, at the end of 1740, expenses (house cost) and

revenues (loans contracted) were transferred to the current accounts book and recorded

in the " Interested in the Company" account, the first on the side of the "owes" (B797:

s.79, i.181) and the second on the "Have to be" side (B797: s.75, i.173)”.

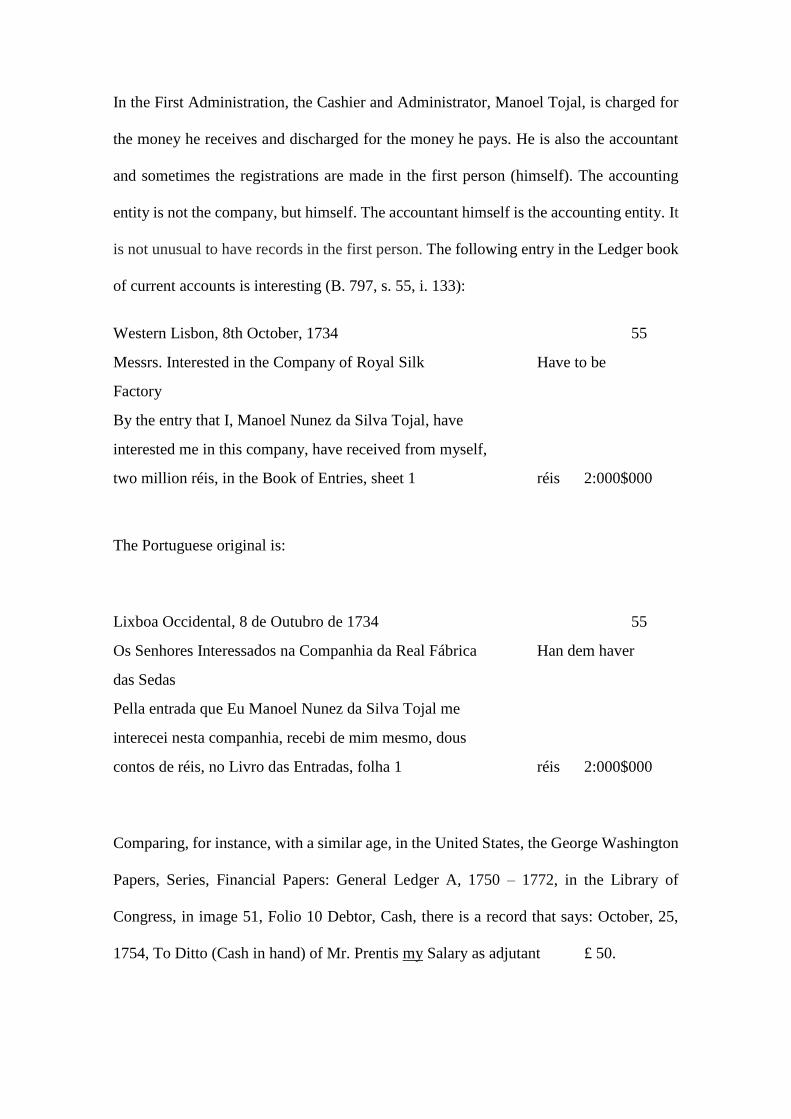

In the First Administration, the Cashier and Administrator, Manoel Tojal, is charged for

the money he receives and discharged for the money he pays. He is also the accountant

and sometimes the registrations are made in the first person (himself). The accounting

entity is not the company, but himself. The accountant himself is the accounting entity. It

is not unusual to have records in the first person. The following entry in the Ledger book

of current accounts is interesting (B. 797, s. 55, i. 133):

Western Lisbon, 8th October, 1734 55

Messrs. Interested in the Company of Royal Silk Have to be

Factory

By the entry that I, Manoel Nunez da Silva Tojal, have

interested me in this company, have received from myself,

two million réis, in the Book of Entries, sheet 1 réis 2:000$000

The Portuguese original is:

Lixboa Occidental, 8 de Outubro de 1734 55

Os Senhores Interessados na Companhia da Real Fábrica Han dem haver

das Sedas

Pella entrada que Eu Manoel Nunez da Silva Tojal me

interecei nesta companhia, recebi de mim mesmo, dous

contos de réis, no Livro das Entradas, folha 1 réis 2:000$000

Comparing, for instance, with a similar age, in the United States, the George Washington

Papers, Series, Financial Papers: General Ledger A, 1750 – 1772, in the Library of

Congress, in image 51, Folio 10 Debtor, Cash, there is a record that says: October, 25,

1754, To Ditto (Cash in hand) of Mr. Prentis my Salary as adjutant £ 50.

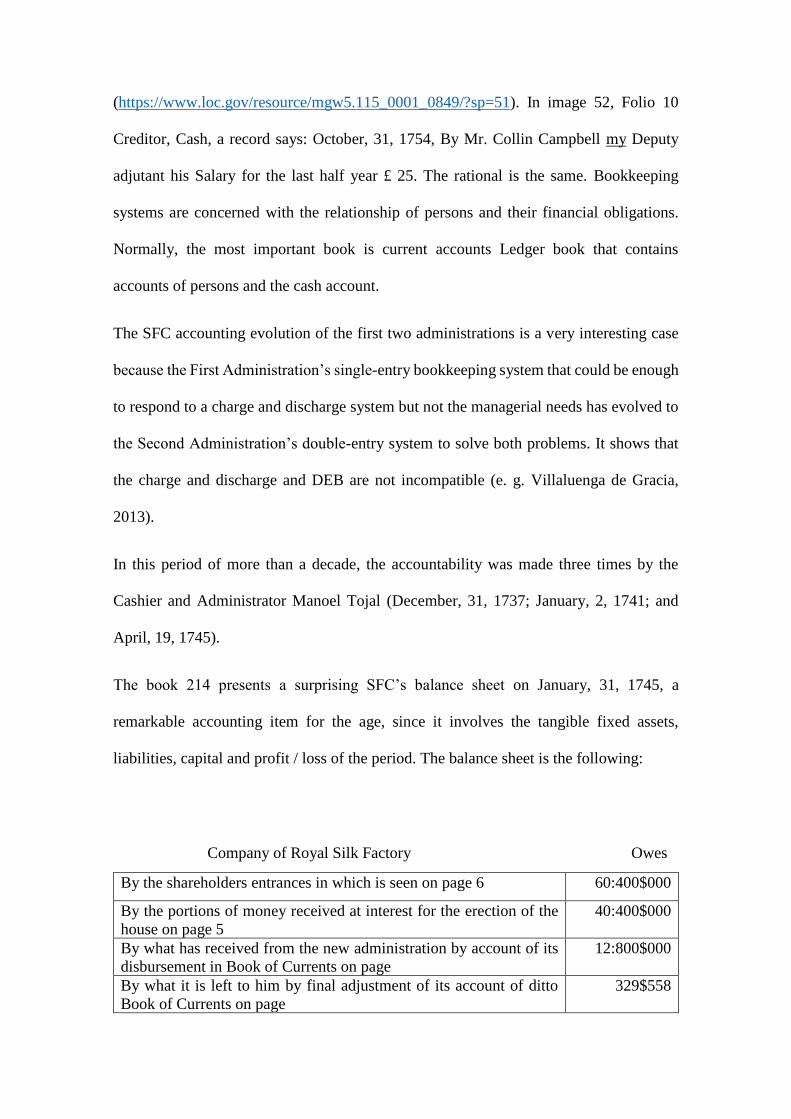

(https://www.loc.gov/resource/mgw5.115_0001_0849/?sp=51). In image 52, Folio 10

Creditor, Cash, a record says: October, 31, 1754, By Mr. Collin Campbell my Deputy

adjutant his Salary for the last half year £ 25. The rational is the same. Bookkeeping

systems are concerned with the relationship of persons and their financial obligations.

Normally, the most important book is current accounts Ledger book that contains

accounts of persons and the cash account.

The SFC accounting evolution of the first two administrations is a very interesting case

because the First Administration’s single-entry bookkeeping system that could be enough

to respond to a charge and discharge system but not the managerial needs has evolved to

the Second Administration’s double-entry system to solve both problems. It shows that

the charge and discharge and DEB are not incompatible (e. g. Villaluenga de Gracia,

2013).

In this period of more than a decade, the accountability was made three times by the

Cashier and Administrator Manoel Tojal (December, 31, 1737; January, 2, 1741; and

April, 19, 1745).

The book 214 presents a surprising SFC’s balance sheet on January, 31, 1745, a

remarkable accounting item for the age, since it involves the tangible fixed assets,

liabilities, capital and profit / loss of the period. The balance sheet is the following:

Company of Royal Silk Factory Owes

By the shareholders entrances in which is seen on page 6 60:400$000

By the portions of money received at interest for the erection of the

house on page 5

40:400$000

By what has received from the new administration by account of its

disbursement in Book of Currents on page

12:800$000

By what it is left to him by final adjustment of its account of ditto

Book of Currents on page

329$558

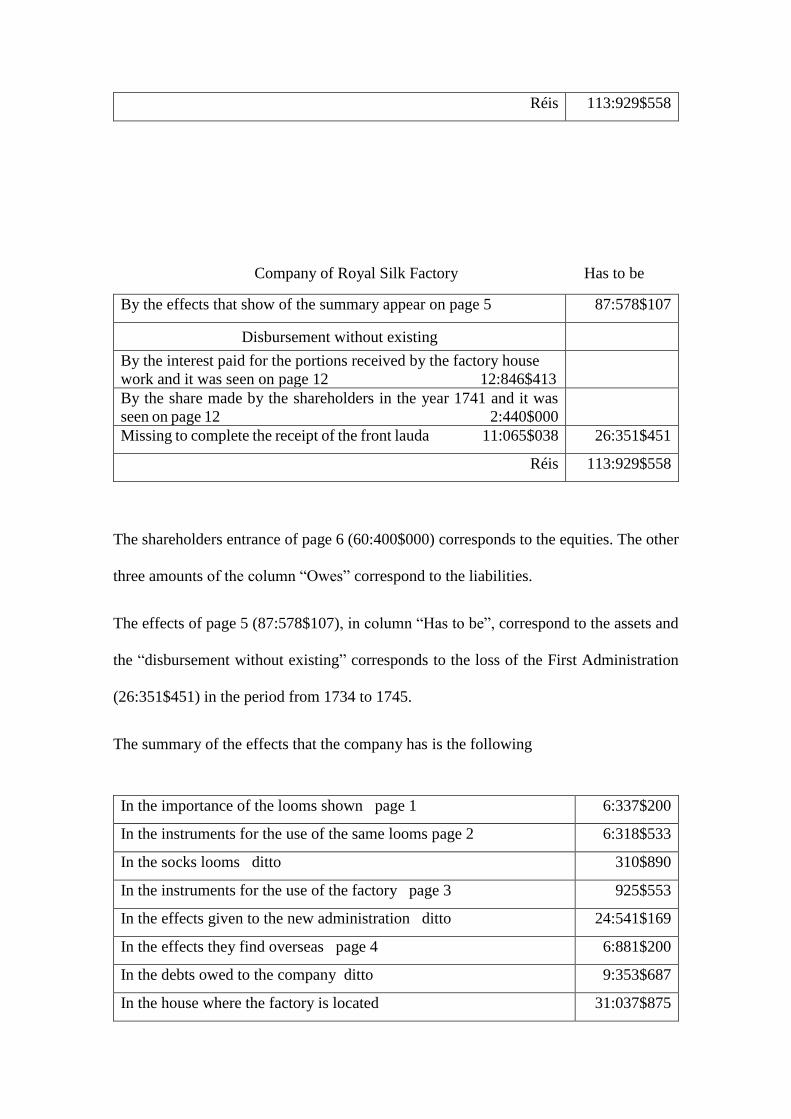

Réis 113:929$558

Company of Royal Silk Factory Has to be

By the effects that show of the summary appear on page 5 87:578$107

Disbursement without existing

By the interest paid for the portions received by the factory house

work and it was seen on page 12 12:846$413

By the share made by the shareholders in the year 1741 and it was

seen on page 12 2:440$000

Missing to complete the receipt of the front lauda 11:065$038 26:351$451

Réis 113:929$558

The shareholders entrance of page 6 (60:400$000) corresponds to the equities. The other

three amounts of the column “Owes” correspond to the liabilities.

The effects of page 5 (87:578$107), in column “Has to be”, correspond to the assets and

the “disbursement without existing” corresponds to the loss of the First Administration

(26:351$451) in the period from 1734 to 1745.

The summary of the effects that the company has is the following

In the importance of the looms shown page 1 6:337$200

In the instruments for the use of the same looms page 2 6:318$533

In the socks looms ditto 310$890

In the instruments for the use of the factory page 3 925$553

In the effects given to the new administration ditto 24:541$169

In the effects they find overseas page 4 6:881$200

In the debts owed to the company ditto 9:353$687

In the house where the factory is located 31:037$875

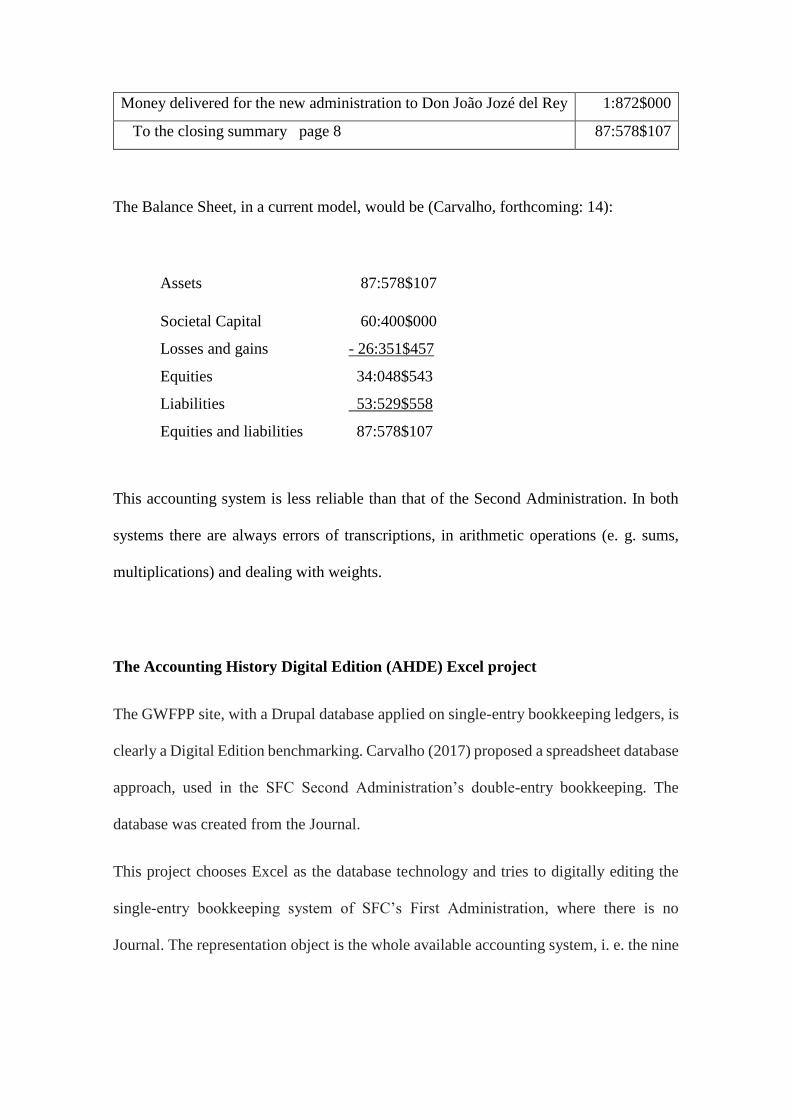

Money delivered for the new administration to Don João Jozé del Rey 1:872$000

To the closing summary page 8 87:578$107

The Balance Sheet, in a current model, would be (Carvalho, forthcoming: 14):

Assets 87:578$107

Societal Capital 60:400$000

Losses and gains - 26:351$457

Equities 34:048$543

Liabilities 53:529$558

Equities and liabilities 87:578$107

This accounting system is less reliable than that of the Second Administration. In both

systems there are always errors of transcriptions, in arithmetic operations (e. g. sums,

multiplications) and dealing with weights.

The Accounting History Digital Edition (AHDE) Excel project

The GWFPP site, with a Drupal database applied on single-entry bookkeeping ledgers, is

clearly a Digital Edition benchmarking. Carvalho (2017) proposed a spreadsheet database

approach, used in the SFC Second Administration’s double-entry bookkeeping. The

database was created from the Journal.

This project chooses Excel as the database technology and tries to digitally editing the

single-entry bookkeeping system of SFC’s First Administration, where there is no

Journal. The representation object is the whole available accounting system, i. e. the nine

books. Why was the First Administration system chosen? There are two reasons, it is the

first, i. e., is older, and helps to understand the Second Administration system.

It is possible to conceive five levels of documents aggregation in DE, from a single

document to all accounting records in the world. The five levels are: (1) Single document;

(2) Single accounting book; (3) Single accounting system; (4) All accounting systems of

a country; and (5) All accounting systems in the World. The objective is not to have all

systems digitally edited, but have created common rules and procedures that facilitate the

aggregation of different accounting systems.

Probably the workbook will have nine sheets, one for each accounting book. It is an early

attempt to create the databases and it is necessary a long journey, mainly in the creation

of fields, to achieve a good and final stage. The most difficult book to work is Current

accounts ledger (B797).

This Excel project tries to have GWFPP as a benchmark. To improve it is necessary to

join some accounting knowledge (e. g. charge and discharge accounting, accounting

entity or single and double-entry). So, it is possible to create new and relevant database

fields. It is necessary to divide the system into accounting books and each one in

documents (pages of the books or photographic images). Two different pages could put

very difficult problems. It is necessary to study and find suitable solutions. Each

spreadsheet should have two different areas, one for the digital transcription of what is

written in the accounting book and the other to create the database with all possible fields.

It is necessary to treat both the documents and the data.

In order to get better databases with new relevant fields, it is necessary to identify other

“tribes” with potential interest. For instance, Palma & Reis (2019) have a research work

on studying Portuguese accounting books from 16th to 19th century, during ten years, to

study prices, wages, in different periods and regions of Portugal and get information to

ascertain the values of GDP (gross domestic product) along centuries. It could be

interesting that “tribe” A (Accounting historians) joined with “tribe” E (Economic

historians) to make suggestions of database fields related to this area. The study of the

book “Accounts of what costs the house” could be a very interesting base to study

economic matters. This dual “tribal” conference could deal with matters like DE, charge

and discharge accounting, SFC bookkeeping, issues of economic history and database

technology. The result of this conference could be suggestions of database fields to create,

better databases and the creation of digital customized outputs.

This project should result in an interdisciplinary team work, with much volunteer work

to introduce data. Eventually, it is interesting to have two teams, one working on book

797 and another on book 536.

What has been done so far?

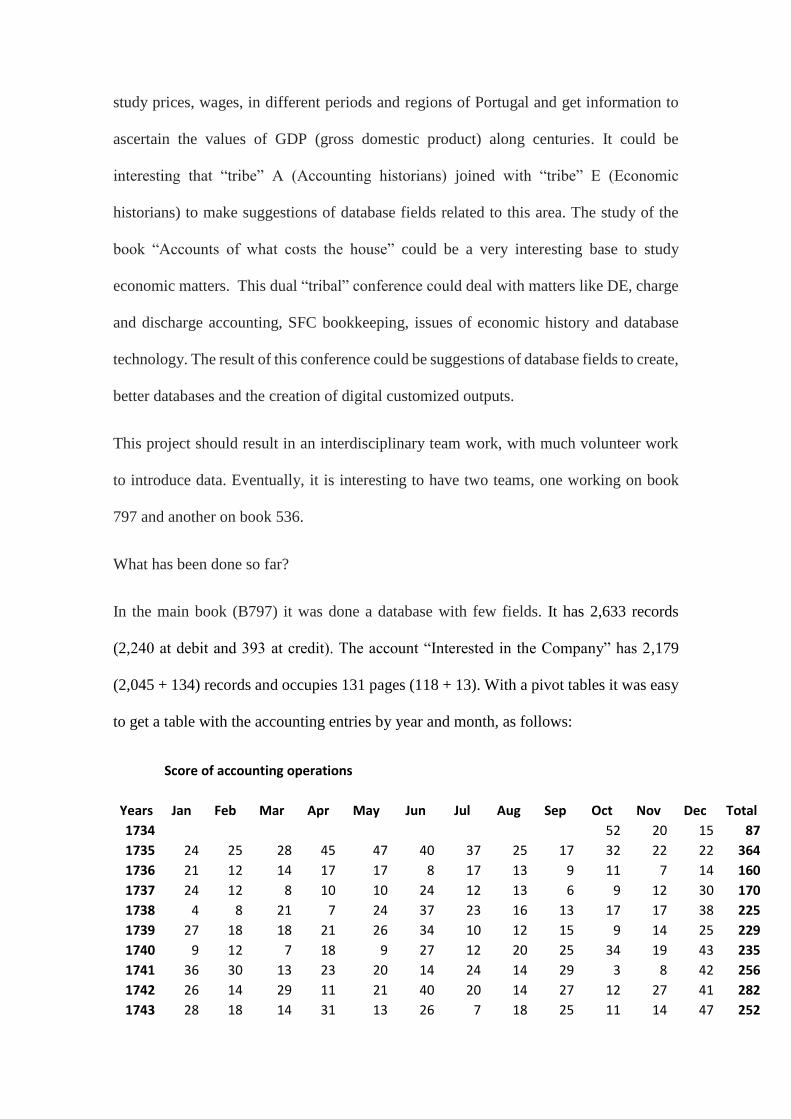

In the main book (B797) it was done a database with few fields. It has 2,633 records

(2,240 at debit and 393 at credit). The account “Interested in the Company” has 2,179

(2,045 + 134) records and occupies 131 pages (118 + 13). With a pivot tables it was easy

to get a table with the accounting entries by year and month, as follows:

Score of accounting operations

Years Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Total

1734 52 20 15 87

1735 24 25 28 45 47 40 37 25 17 32 22 22 364

1736 21 12 14 17 17 8 17 13 9 11 7 14 160

1737 24 12 8 10 10 24 12 13 6 9 12 30 170

1738 4 8 21 7 24 37 23 16 13 17 17 38 225

1739 27 18 18 21 26 34 10 12 15 9 14 25 229

1740 9 12 7 18 9 27 12 20 25 34 19 43 235

1741 36 30 13 23 20 14 24 14 29 3 8 42 256

1742 26 14 29 11 21 40 20 14 27 12 27 41 282

1743 28 18 14 31 13 26 7 18 25 11 14 47 252

1744 16 43 29 22 19 32 22 25 16 10 11 52 297

1745 20 5 5 46 76

Total 235 197 186 251 206 282 184 170 182 200 171 369 2633

The system has a weak reliability because it can happen mistakes of transcription or

arithmetic. On sheet 24 (i. 71) there is a mistake of sum of 36$000 (36,000 réis). Probably,

there was an inversion of digits in the value, it was considered the amount of the sum

13:326$303 instead of 13:362$303. It could be interesting to classify the amount by

operations, sums, balances, and so on. The spreadsheet technology is a good device to

better see the mistakes. It is easy to get a trial balance. This is a continuous improvement

process with new ideas in the DE process.

The number of registered shareholders was 39, but it was possible to sell the shares and

at the end of the First Administration there were 27. There are 19 stakeholders accounts,

being 6 from Spain, 5 from France, 3 from Portugal and 2 from Netherlands. There is also

1 from Italy, 1 from England and another without geographical identification (brigantine).

Related to towns, there are 3 stakeholders each from Lion, Madrid and Valencia, 2 each

from Amsterdam and Lisbon, and 1 from Bragança, Genoa, London, Marseille and

Rouen.

The book 536 (Account of what cost the house) has several mistakes of transcription and

arithmetic errors. The accuracy is not total to calculate the cost of the house. For instance,

on page 35 (i. 39) there is an error of transcription. It was considered 261$000 instead of

261$600.

In the book 214 (Inventory) there are no mistakes, but the values are different from the

beginning inventory of the Second Administration.

The Excel technology has some advantages because it is a low-cost solution, easy to use

and to create new databases fields, flexible, use of hyperlinks, has calculator ability and

so good to find mistakes and it is easy to learn. It has the disadvantage of not being so

powerful as other databases.

Discussion

This paper is focused on constructing an multidisciplinary AHDE Excel project that

should represent a whole accounting system, i. e., a set of books, instead of a sole

accounting book, from the first half of the 18th century (1734 – 1745), being in an early

stage, and based on holistic research with other relevant areas of knowledge. The state of

art of AHDE is based on the GWFPP, a benchmark in ARDE, and Carvalho (2017) that

digitally edited the double-entry bookkeeping system of the SFC’s Second

Administration, using Excel spreadsheet databases, for the first time.

The selected case study was the accounting system of the SFC’s First Administration

because it is older and helps to understand the Second Administration system. More six

reasons are indicated about its importance (p.14). It is a complete bookkeeping system

working in SEB. Unlike that of the Second Administration, it has no Journal and the main

book is the Current accounts ledger (B797). This is the first database that was created.

Each spreadsheet should be divided in the transcription area (contents of the accounting

book) and a database with all possible fields. It is the separation between document and

data.

In this accounting system, three books stand out: the referred B797, the B536 (Cost of the

house) and the B214 (Inventory). The first has 2,633 records and its main account

“Interested in the Company” has 2,179 records. The second book has two parts: the

factory building and the financing (only outside capital). The data about wages and prices

at that age and place could be interesting for digital economic historians. The inventory

book presents the balance sheet of the Company on January, 31, 1745, involving the

tangible assets, liabilities, capital and profit / loss of the period. It is possible to present

the balance sheet in a modern way. This balance sheet is quite different from the

beginning inventory of Second Administration and also the accounting records of the First

Administration, because the perspective (accounting entity) is different. In the First

Administration, it is the perspective of the Cashier and Administrator and in the Second

Administration it is that of itself. In the Second Administration, the Administrators are

responsible for the liabilities amount until the assets amount. So, it was not possible to

consider all the loans. The remaining amount should be supported by the Administrators

of the First Administration. It was necessary to split up a loan (Father Jozé Dias) in two

parts, one supported by the Second Administration and the remaining by the First.

To create a database template, it is important to consider some accounting knowledge in

the selection of fields. Three issues were considered: charge and discharge system,

double-entry vs. single entry and accounting entity. It is possible to have at the same time

a DEB system and charge and discharge system (e. g. Second Administration).

The charge and discharge system is based on the agency relationship. In the First

Administration the Cashier and Administrator, Manoel Tojal, is the agent and the partners

(shareholders) are the principal. The account “Interested in the Company” registers the

charge and discharge of the Cashier. The rule “who receives owes, who delivers has to

be” is used to determine the debit and the credit of that account. When he receives, he is

charged and when he pays, he is discharged. That account should reflect the account of

cash but in an opposite way. In the system, there is no account of cash.

This charge and discharge system has two revenues groups, i. e., fabric business and

financing the construction of the Rato building and two expenses group, i. e., fabric

business and the costs of the construction of the Rato building. When all constructions

where finished (end of 1740), the costs of the house and the loans contracted were

transferred to the current account book (“Interested in the Company” account).

There are some problems to solve in the introduction of data in the database. For instance,

the weight measurement units (e. g. arrátel, ounce, heights) should occupy several

columns (fields) in the database, including one in a decimal mode. Other problems like

the transcription of sentences with abbreviations or the words with spelling errors should

be treated. Here it is important the contribution of a linguist. How to treat errors of

transcription or errors of sum, multiplication, division or others? Perhaps, it seems more

suitable to have a photo of each page (digitized document) and write the sentences without

abbreviations or spelling errors. It is important to reproduce what the writer wanted to

say.

An important aim of this project is to improve the databases, creating new innovative

fields, with good tables for the fields and to produce suitable and customized outputs. The

amounts can be classified by operation type, sums, balances, etc..

It is possible to consider, in terms of complexity, three DE levels: Documentary editing,

ARDE and AHDE. But currently, the great effort is made in digitization of documents.

Stertzer’s team identified and solved many problems in ARDE. But with the inclusion of

accounting knowledge issues, certainly ARDE will be turned into AHDE.

Excel is easy to use, it is a low-cost solution, has calculator ability and is good to find

mistakes and is flexible, but it is not so powerful as other databases.

Conclusions and suggestions

AHDE is an area of growing interest, although it is only starting. It is an innovative digital

issue, a strategical powerful productivity tool in terms of AHR. It is concerned with the

accessibility, the digital rendition and searchable transcription. DE applies to the

Intelligence Augmented (IA). It is a must the creation and the availability of AHDE.

The GWFPP is a middle and end project, using a Drupal database and also the best

practices of ARDE. It edits ledgers and a cash book, but has some lack of accounting

knowledge. The information is free and publicly available. Carvalho (2017) edits

information from the DEB Ledger book of the SFC’s Second Administration in a

spreadsheet database, in Excel, for the first time. This workbook is not publicly available.

The AHDE of the bookkeeping system of the SFC’s First Administration (Excel), is a

first attempt to edit it, in a database. The first spreadsheet database edits the Current

accounts book (B797) because there is no Journal. It is important the use of different

platforms, so that the best ones will be selected. It is also important the comparison of the

editing problems identified and the choices of the best solutions.

The accounting systems of the SFC, in the First and Second Administrations, are very

interesting and relevant cases to understand the development of accounting in that age.

They are the most ancient, in Portugal, in single and double-entry accounting system used

in the industry. The information covers all period of those two administrations. The

accounting system of the Second Administration has, at the same time, a charge and

discharge system and a DEB. In the system of the First Administration, it clearly shows

the charge and discharge system, using the registration of some entries in the first person.

In these two administrations, it is possible to see that there are different accounting

entities: The Cashier (First Administration), the Company (in the Inventory book) and

Administrators (Second Administration).

To understand well the accounting system of the SFC’s Second Administration, it is only

possible after the study of the First Administration, namely the beginning inventory of

the Second Administration, because the Administrators of the Second Administration

assume responsibilities of liabilities until the amount of the assets received which do not

include the tangible fixed assets. It is a different sight of the responsibilities of the

Administrators comparing with the First Administration.

In the First Administration there are three more interesting books: Current accounts book

(B797), Cost of the house (B536) and Inventory (B214). The first allows to understand

better and feel the charge and discharge system. The second gives much information

about the price of the things at the age. Finally, the last presents a surprising balance sheet

of the Company. It is similar to a modern balance sheet.

In terms of suggestions, the first is about the GWFPP, an outstanding project but with

some lack of accounting knowledge. It could be improved with the contribution of

American accounting historians.

This paper suggests dual “tribal” conferences, like accountants / economists or

accountants / historians, for joining different lens to exchange “tribal” knowledge and

analyze the digital representations of the accounting records and to contribute to better

solutions of AHDE. It is good that historians learn accounting, reading some articles (e.

g. about charge and discharge accounting or DEB) and accountants learn AHDE.

The several dual “tribal” conferences will address problem of each “tribe”. Each of them

will tell what is important for them, what are the critical issues and what are the

customized outputs they want. There are many new problems to solve, many challenges.

It is difficult to work with “tribes” with so different interests. A final multi “tribal”

conference would be recommended. All this is innovation in the accounting history.

Portugal and other countries need to make a strong effort of digitization of accounting

documents. It is the first step for the digital editing of these documents. It is an interesting

idea to create a multidisciplinary team, with funded projects, to digitally edit the digitized

documents of the SFC (three administrations).

It is possible to think in grandiose projects, like the Pacioli’s Summa (Particularis de

computis et scripturis). It is an endless DE job, because there is too much information

about it and too many issues of discussion. It is a long journey in a continuous

improvement process.

References

Almeida, Luís Ferrand de (1989-90) A Fabrica das Sedas de Lisboa no Tempo de D. João

V. Revista Portuguesa de História., Vol. 25: p. 1-48.

AN / TT - Arquivos Nacionais / Torre do Tombo (1995) Real Fábrica das Sedas e Fábricas

Anexas – Inventário. Lisboa, Divisão de Publicações. ISBN 972-8107-17-X.

Bernal Torres, César Augusto (2000) Metodología de la Investigación para

Administración y Economía. Prentice Hall. Pearson Educación de Colombia, Ltda. Santa

Fé de Colombia.

Carnegie, Garry D. & Wolnizer, Peter W. Editors (1996) Accounting History Newsletter

1980 – 1989 and Accounting History 1989 – 1994 A Tribute to Robert William Gibson.

Garland Publishing, Inc. New York and London.

Carvalho, José M., Rodrigues, Lúcia L. & Craig, Russel (2007) Early cost accounting

practices and private ownership: The silk factory company of Portugal, 1745-1747.

Accounting Historians Journal, 34 (1), 57-89. USA, Birmingham, The Academy of

Accounting Historians.

Carvalho, José Manuel de Matos (2017) From Traditional Accounting History to Digital

Accounting History: An Eighteenth-Century Double-Entry Bookkeeping System

represented in Spreadsheet Databases. XVI International Congress of Accounting and

Auditing. Aveiro. https://www.occ.pt/dtrab/trabalhos/xviicica//finais_site/92.pdf (Digital

Format: ISBN:978-989-98660-8-9).

Carvalho, José Manuel de Matos (forthcoming) O sistema de escrituração de carga e

descarga da Primeira Administração da Companhia da Fábrica das Sedas (1734 – 1745)

in História da Contabilidade em Portugal, 3 vols., Coordenação Geral de Fernando de

Sousa; 1º A história da contabilidade nos séculos XII-XVII (coordenação de António

Castro Henriques); 2º A História da Contabilidade dos inícios do século XVIII a 1926

(coordenação de Maria de Fátima Brandão) and 3º A História da Contabilidade de 1926

a 2016 (coordenação de Fernando de Sousa). Lisboa/Porto: Ordem dos Contabilistas

Certificados/CEPESE.

Domingos, Pedro (2015) The Master Algoritm: How the Quest for the Ultimate Machine

Learning Will Remake Our World. Basisc Books.

Edwards, John Richard (1989) A History of Financial Accounting. Routledge. London.

Ezersky, Fedor V. (1876) The frauds, losses and errors in balance sheets as a part of the

double-entry system of bookkeeping and detected by the indicators to the accuracy of the

accounts offered by the Russian triple-entry. (Written in Russian).

Gonçalves, Miguel (2018) As partidas dobradas como método de registo contabilístico,

com especial referência aos aspectos pedagógicos e técnico científicos, à sua

institucionalização em Portugal e ao seu primeiro livro impresso em português: síntese,

análise histórico- contabilística e apresentação de dados inéditos. Lição no âmbito de

provas públicas. Instituto Superior de Contabilidade e Administração. Instituto

Politécnico de Coimbra.

Jones, Michael John (2008a) The role of change agents and imitation in the diffusion of

an idea: charge and discharge accounting. Accounting and Business Research, Vol. 38.

No. 5. pp. 355-371.

Jones, Michael John (2008b) The role of change agents and imitation in the diffusion of

an idea: charge and discharge accounting. Abacus A Journal of Accounting, Finance and

Business Studies, Vol. 44. No. 4. p. 443-474. doi: 10.1111/j.1467-6281.2008.00272.x.

Jones, Michael John (2009) Origins of medieval Exchequer accounting’. Accounting,

Business and Financial History,19 (1)

Hernández Esteve, Esteban. (1993). Problemática General de una Historia de la

Contabilidade en España. Revisión genérica de las modernas corrientes epistemológicas

y metodológicas, y cuestiones especificas. Contaduría Universidad de Antioquia, n. 21-

22, 26-92. Medellín.

Ijiri, Yuji (1982) Triple-Entry Bookkeeping and Income Momentum. Studies in

Accounting Research #18. American Accounting Association.

Ijiri, Yuji (1989) Momentum Accounting and Triple-Entry Bookkeeping: Exploring the

Dynamic Structure of Accounting Measurements. Studies in Accounting Research #31.

American Accounting Association.

Lee, G. A. (1975) The Concept of Profit in British Accounting, 1760-1900. British

History Review, Vol. XLIV (Spring), p. 6-36.

Lemarchand, Yannick (1994) Double entry versus charge and discharge accounting in

eighteenth-century France. Accounting, Business & Financial History. Volume 4. Issue

1. p. 119-145.

Mann, Harvey (1979) Accounting for Les forges de Saint-Maurice 1730-1736.

Accounting Historians Journal, Vol. 6, No. 1, p. 63-82.

Mills, Patti A. (1986) Financial Reporting and Stewardship Accounting in Sixteenth-

century Spain. The Accounting Historians Journal, 13 (2) Fall, 65-76. USA, Birmingham:

The Academy of Accounting Historians.

Palma, Nuno & Reis, Jaime (2019) From Convergence to Divergence: Portuguese

Economic Growth, 1527 – 1850. The Journal of Economic History. Volume 79, Issue 2,

June, p. 477 – 506. DOI: https://doi.org/10.1017/S0022050719000056.

Phillips, Estelle M. & Pugh, D. S. (1994) How to Get a PhD: A handbook for students

and their supervisors. 2nd edition. Open University Press.

Platonova, Natalia V. (2015) F. V. Ezersky and the Development of Accounting Thought

and Practices in Russia (https://www.hse.ru/data/2015/11/08/.../Platonova-Doklad.docx)

Rau, Virgínia (1956) Livro de Rezão de António Coelho Guerreiro. Lisboa. Companhia

de Diamantes de Angola.

Rocha, Armandino & Gomes, Delfina (2002) Um contributo para a história da

contabilidade em Portugal (séculos XIV a XVII). Revista de Contabilidade e Comércio

231, p. 591 – 634.

Sá, Antônio Lopes de & Sá, Ana Maria Lopes de (1983) Dicionário de Contabilidade.

Atlas. S. Paulo. Brasil.

Sangster, Alan (2016) The genesis of double entry bookkeeping. The Accounting Review.

91 (1) p. 299 – 315.

Stertzer, Jennifer (2014). Working with the Financial Records of George Washington:

Document vs. Data. Digital Studies / Le Champ Numérique. DOI:

http://doi.org/10.16995/dscn.57

Stone, Williard (1993). The development of charge and discharge accounting: 1183 to

1660. Accounting History, 5 (2), p. 41-61.

The George Washington Financial Papers Project, ed. Jennifer E. Stertzer, et al,

Charlottesville: Washington Papers, 2017

Villaluenga de Gracia, Susana (2013) La partida doble y el cargo y data como instrumento

de un sistema de información contable y de responsabilidade jurídica integral, según se

manifiesta en fuentes documentales de la Catedral de Toledo (1533 – 1613). Revista de

Contabilidad / Spanish Accounting Review, vol. 16, núm. 2, p. 126-135. Barcelona:

ASEPUC.

Wiatt, R. G. 2019. From the mainframe to the blockchain: With its triple-entry approach

and use of distributed ledgers, blockchain technology not only has the potential to

redefine accounting and auditing, but it could also create greater confidence in all sorts

of transactions and data exchanges. Strategic Finance (January): p. 26-35.

(https://sfmagazine.com/issue/january-2019/).

Acronyms

AHDE – accounting history digital editing

AHR – accounting history research

ANTT – Arquivos Nacionais / Torre do Tombo (Portuguese National Archives)

ARDE – accounting records digital editing

AT – Autoridade Tributária e Aduaneira (Tax and Customs Authority)

DAH – Digital Accounting History

DE – digital editing

DEB – double-entry bookkeeping

DH – Digital History

DHoA – Digital History of Accounts

GWFPP – George Washington Financial Papers Project

SEB – single-entry bookkeeping

SFC – Silk Factory Company (Companhia da Fábrica das Sedas)