A desynchronised recovery: Global economic outlook · Schroders Insurance Asset Management...

43

November 2014 | For professional investors only. This material is not suitable for retail clients Schroders Insurance Asset Management Investment Seminar 2014 A desynchronised recovery: Global economic outlook Keith Wade | Chief Economist and Strategist

Transcript of A desynchronised recovery: Global economic outlook · Schroders Insurance Asset Management...

November 2014 | For professional investors only. This material is not suitable for retail clients

Schroders Insurance Asset Management

Investment Seminar 2014

A desynchronised

recovery: Global

economic outlook

Keith Wade | Chief Economist and Strategist

Global recovery – can the world resynchronise?

US – recovery and Fed on track?

Eurozone – turning Japanese?

UK – how long will the boom last?

Japan – is “Abenomics” working?

Emerging markets – will China crash?

Markets in 2015

Asset allocation – the return of “irrational exuberance”?

Key issues Macro and market outlook?

1

Outline

Global recovery What happened?

Recovery recap – real GDP since the crisis began US bounces back, but Japan and Germany falter in Q2 and Q3

UK

US

Spa

EZ

Ger

Ita

Jap

90

92

94

96

98

100

102

104

106

108

110

2008 2009 2010 2011 2012 2013 2014 2015

Index (100 = 2007 Q4)

3

Source: Thomson Datastream, Schroders at 14 November 2014

01/12/2014 17:49:02

Emerging markets not sharing in developed world recovery

EM beta to global growth has fallen

4

Source: Thomson Datastream at 19 November 2014

Global trade has not recovered from the crisis Trade-orientated emerging markets are struggling

-40

-20

0

20

40

60

1970 1975 1980 1985 1990 1995 2000 2005 2010

Recession World exports y/y%, LHS Average trade growth, RHS

5

Source: Thomson Datastream, Schroders at 4 November 2014

y/y%

An era of USD strength? The return of currency wars?

6

Source: Thomson Datastream, Schroders at 19 November 2014

USD trade-weighted index: breakdown JPY since Abenomics

G7 headline CPI and GS commodity prices

Fall in commodity prices will drive inflation lower

Should we worry?

7

Source: Thomson Datastream, Schroders at 19 November 2014

US Recovery and Fed on

track?

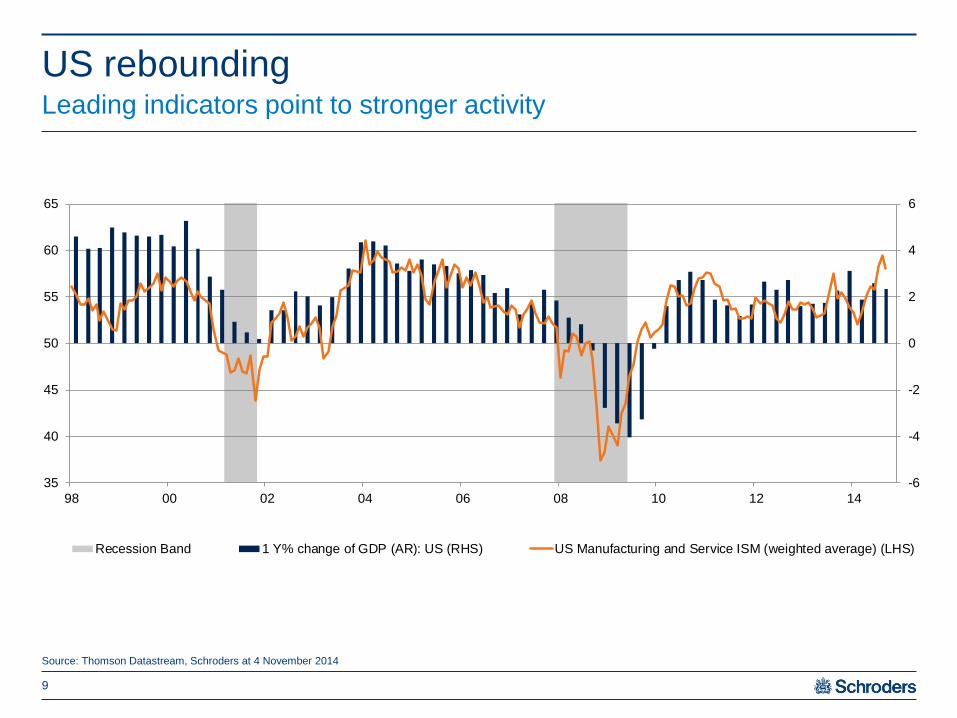

US rebounding Leading indicators point to stronger activity

9

Source: Thomson Datastream, Schroders at 4 November 2014

-6

-4

-2

0

2

4

6

35

40

45

50

55

60

65

98 00 02 04 06 08 10 12 14

Recession Band 1 Y% change of GDP (AR): US (RHS) US Manufacturing and Service ISM (weighted average) (LHS)

1.5

2.0

2.5

3.0

3.5

2010 2011 2012 2013 2014 2015

2011 2012 2013 2014 2015

%

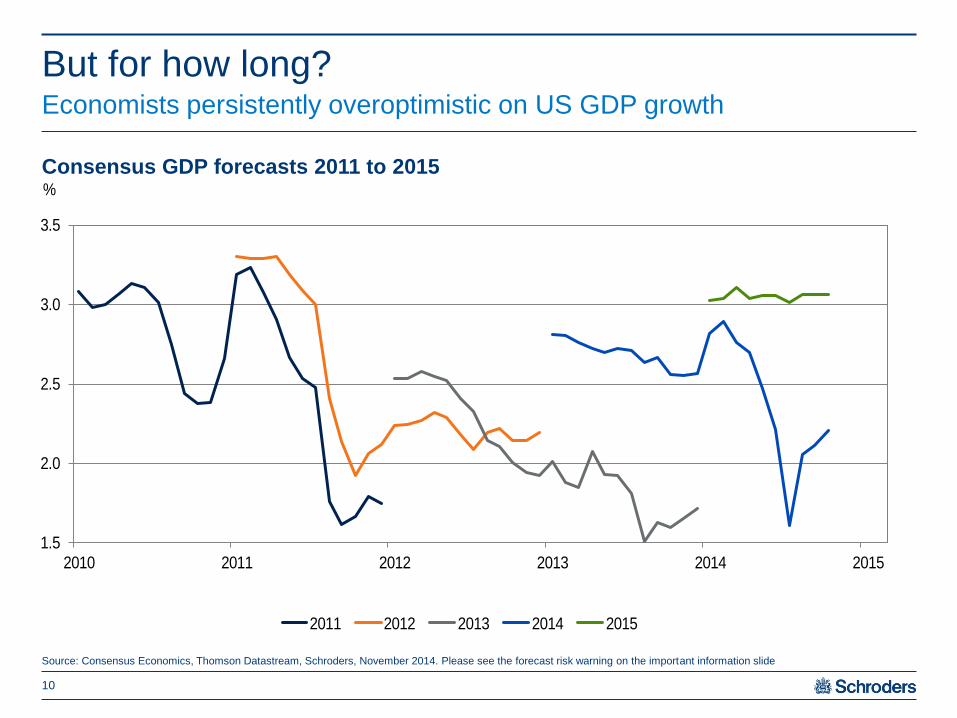

Consensus GDP forecasts 2011 to 2015

But for how long? Economists persistently overoptimistic on US GDP growth

10

Source: Consensus Economics, Thomson Datastream, Schroders, November 2014. Please see the forecast risk warning on the important information slide

US debt levels – deleveraging to continue Households continue to de-lever, but corporate and public debt has increased

11

Source: Thomson Datastream, Schroders at 8 September 2014

30

40

50

60

70

80

90

100

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010

Households Corporates (Non Financial) Government

% of GDP

Sign of secular stagnation?

Trend productivity slows after boost from internet

12

Source: Thomson Datastream, Schroders at 19 November 2014

01/12/2014 17:49:03

y/y%

48

50

52

54

56

58

60

62

64

66

68

70

0

2

4

6

8

10

12

14

16

18

20

22

55 60 65 70 75 80 85 90 95 00 05 10 15

NBER defined US recessions Unemployment rate (%), lhs

Participation rate (%), rhs

4.5% 5.0% 5.5% 5.8%*

62.0%* 118k 56k -5k -42k

62.5%* 213k 151k 89k 51k

62.8%* 270k 207k 145k 107k

63.0%* 307k 245k 182k 145k

Participation

rate

Unemployment rate

Unemployment to fall faster than Fed expects Fall in participation rate is more structural than cyclical

13

1Source: Thomson Datastream, Schroders at 11 November 2014 2Source: Atlanta Federal Reserve, Schroders at 9 October 2014 3Denotes current participation and unemployment rate. NBER – The National Bureau of Economic Research

Change in payrolls needed to achieve U/E

rate in 1year2

The Federal Open Market Committee (FOMC) projects the

unemployment rate to be between 5.4 and 5.6% in Q4 2015 and 5.1 –

5.4% in Q4 2016 (September 2014 projections). The current 3 month

average payroll print is 224k

Fall in the participation rate key to fall in

U/E rate1

US wages rise as labour market tightens Another prop to consumer spending, but concern for the Fed

14

Source: Thomson Datastream, Schroders at 19 November 2014

y/y % %

Eurozone –

turning Japanese?

“They make a desert and

call it peace” – Tacitus

Eurozone outlook Not a lot to smile about

16

Eurozone recovery shows signs of fatigue Eurozone GDP vs BNB survey

17

Source: Thomson Datastream, Markit, Belgian National Bank, Eurostat, Schroders at 4 November 2014

-30

-25

-20

-15

-10

-5

0

5

10

-6

-4

-2

0

2

4

6

2002 2004 2006 2008 2010 2012 2014

Eurozone GDP growth, Y/Y % (lhs) Belgian National bank survey (rhs)

y/y %

Key difference between US and Europe US banking sector is lending again, Eurozone yet to turn positive

-15

-10

-5

0

5

10

15

92 94 96 98 00 02 04 06 08 10 12 14

US Commercial bank lending y/y% Eurozone bank lending y/y%

18

Source: Thomson Datastream, Schroders at 4 November 2014

y/y%

Out of the woods? Eurozone needs to pull clear of deflation

19

Source: Thomson Datastream, Eurostat, Schroders at 4 November 2014

-1.5%

-1.0%

-0.5%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Y/Y

Core Energy Food incl. alcohol & tobacco Headline

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Minimal Low Moderate High CPI, Y/Y% (lhs)

IMF deflation vulnerability

indicator reconstructed and

updated to flag risk of deflation

Currently estimates a 14%

chance of deflation two years

from the point of entering the

moderate risk category (down

from 25% in the high risk

category)

ECB responded in June with

cut in deposit rate and

announced new bank funding

(TLTROs). Then cut again in

September, and announced

asset-backed security

purchases

Market inflation expectations

remain very low

Eurozone deflation Risk moderates after fall in EUR

20

Source: IMF, Thomson Reuters Datastream, Schroders Economic Group at 9 September 2014. Vulnerability indicator at Q2 2014

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

04 05 06 07 08 09 10 11 12 13 14

Eurozone CPI %YoY and Deflation Vulnerability Indicator

Minimal Low Moderate High CPI %YoY (LHS)

Eurozone CPI % Y/Y and Deflation Vulnerability Indicator

UK

How long will the boom

last?

UK economic growth close to peak GDP growth vs Schroders Activity Index

-3.0%

-2.5%

-2.0%

-1.5%

-1.0%

-0.5%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14

Q/Q

GDP Growth Schroders Activity Index

22

Source: ONS, Markit, CBI, Schroders at 4 November 2014

01/12/2014 17:49:03

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

05 06 07 08 09 10 11 12 13 14 15

Halifax 3m/3m (AR)

New buyers - New instructions (6m lead)

-20%

-15%

-10%

-5%

0%

5%

10%

15%

05 06 07 08 09 10 11 12 13 14

House prices (Y/Y)

Range of houseprices Average of surveys

House price growth appears to be peaking Leading indicators softening

23

Source: Thomson Datastream, Halifax, Nationwide, Rightmove Hometrack, LSL/Acadametrics, ONS, Schroders at 29 September 2014

01/12/2014 17:49:03

UK fiscal policy will continue to weigh on activity Policy to tighten further to meet government targets

24

Source: OBR, Schroders at 2 April 2014. Forecast risk warning: Please refer to the important information slide at the end of the presentation

-4

-3

-2

-1

0

1

2

3

4

97

/98

98

/99

99

/00

00

/01

01

/02

02

/03

03

/04

04

/05

05

/06

06

/07

07

/08

08

/09

09

/10

10

/11

11

/12

12

/13

13

/14

14

/15

15

/16

16

/17

17

/18

18

/19

Forecast Change in cyclically adjusted primary balance

% of GDP

Fiscal tightening

Fiscal stimulus

In years

Japan

Is Abenomics working?

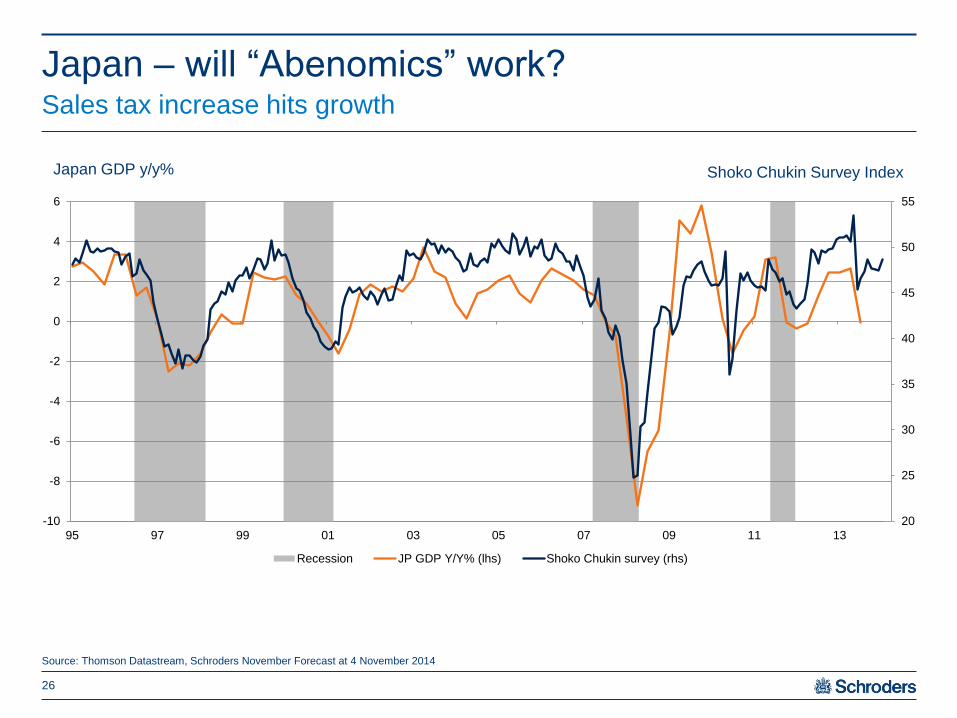

Japan – will “Abenomics” work? Sales tax increase hits growth

26

Source: Thomson Datastream, Schroders November Forecast at 4 November 2014

20

25

30

35

40

45

50

55

-10

-8

-6

-4

-2

0

2

4

6

95 97 99 01 03 05 07 09 11 13

Recession JP GDP Y/Y% (lhs) Shoko Chukin survey (rhs)

Japan GDP y/y% Shoko Chukin Survey Index

Pick up in worker earnings offset by higher inflation Lower real wages will slow consumption

27

Earnings are calculated by summing the six month moving average y/y% changes of wages per hour, hours per worker and the number of workers

Wage inflation shows the Y/Y% change in contract cash earnings

Source: Thomson Datastream, Morgan Stanley, Schroders at 4 November 2014

-6

-4

-2

0

2

4

6

8

10

1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013

CPI inflation Contracted wage inflation Earnings inflation (incl. bonuses)

y/y%

Emerging

markets

Will China crash?

China slowdown to continue Expect China to lower the growth target in 2015

29

Source: Thomson Datastream, Schroders at 4 November 2014

4

6

8

10

12

14

16

-20

0

20

40

60

80

100

02/06 02/07 02/08 02/09 02/10 02/11 02/12 02/13 02/14

Casino revenue - Macau, LHS Chinese GDP Y/Y%, RHS

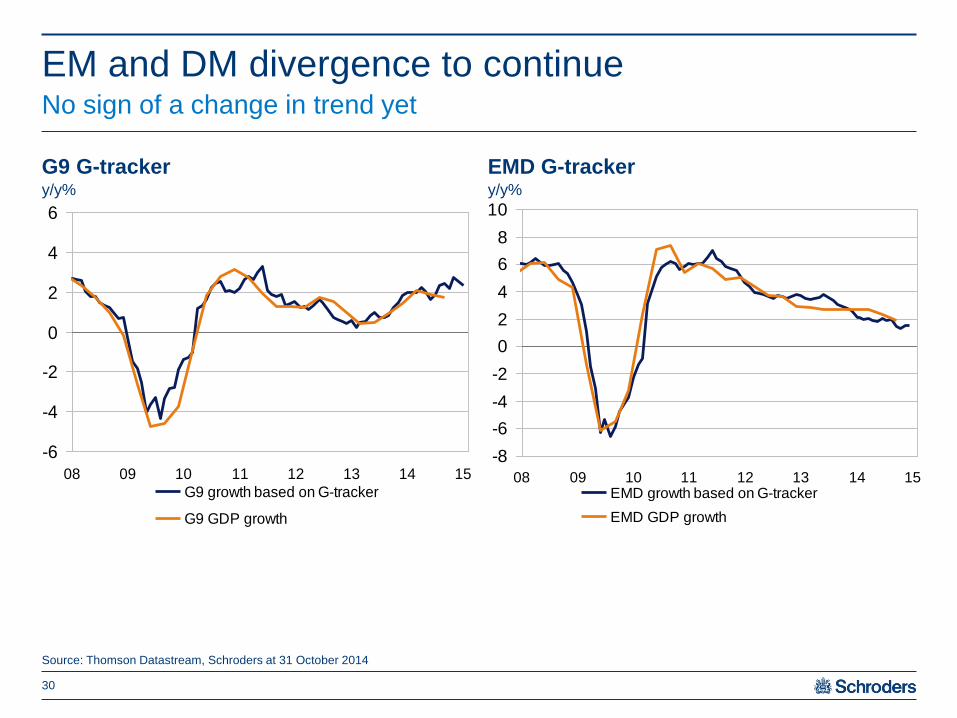

EM and DM divergence to continue No sign of a change in trend yet

30

Source: Thomson Datastream, Schroders at 31 October 2014

G9 G-tracker EMD G-tracker

01/12/2014 17:49:03

y/y%

-6

-4

-2

0

2

4

6

08 09 10 11 12 13 14 15

G9 growth based on G-tracker

G9 GDP growth

-8

-6

-4

-2

0

2

4

6

8

10

08 09 10 11 12 13 14 15EMD growth based on G-tracker

EMD GDP growth

y/y%

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0 0.05 0.1 0.15 0.2 0.25

Competition index

Exports to Japan as share of total

Philippines

Indonesia

Malaysia

Thailand

Vietnam

Chile

China

South Korea

Peru

Russia

India

Brazil

Germany

US

EMEAColombia

Mex

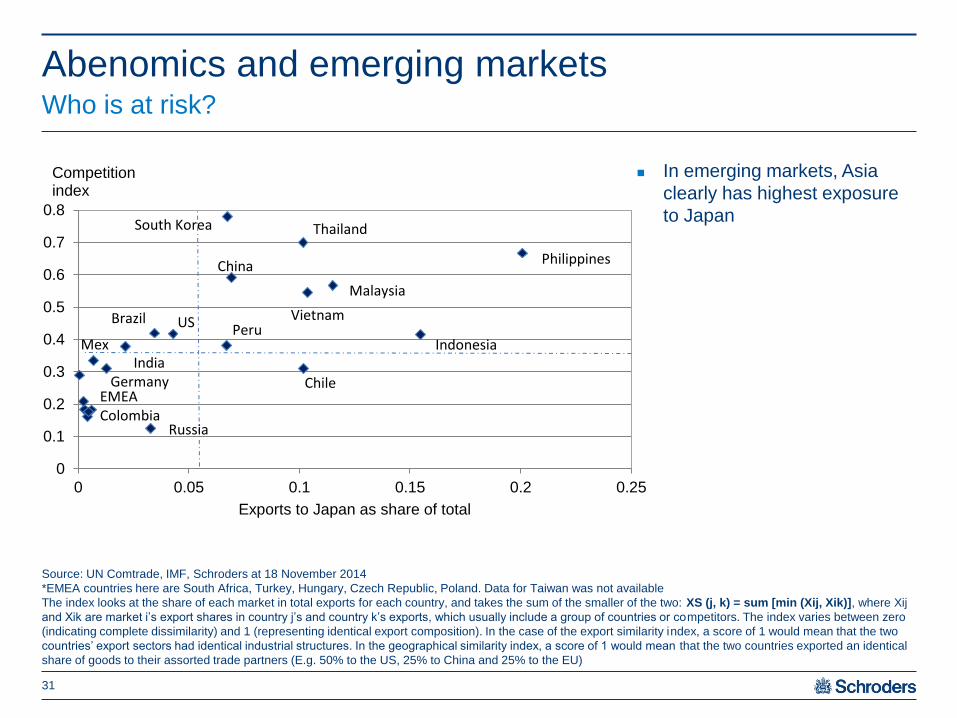

Abenomics and emerging markets Who is at risk?

In emerging markets, Asia

clearly has highest exposure

to Japan

31

Source: UN Comtrade, IMF, Schroders at 18 November 2014

*EMEA countries here are South Africa, Turkey, Hungary, Czech Republic, Poland. Data for Taiwan was not available

The index looks at the share of each market in total exports for each country, and takes the sum of the smaller of the two: XS (j, k) = sum [min (Xij, Xik)], where Xij

and Xik are market i’s export shares in country j’s and country k’s exports, which usually include a group of countries or competitors. The index varies between zero

(indicating complete dissimilarity) and 1 (representing identical export composition). In the case of the export similarity index, a score of 1 would mean that the two

countries’ export sectors had identical industrial structures. In the geographical similarity index, a score of 1 would mean that the two countries exported an identical

share of goods to their assorted trade partners (E.g. 50% to the US, 25% to China and 25% to the EU)

01/12/2014 17:49:03

Fed tightening and emerging markets Problems remain despite adjustments

Source: IMF, Bank for International Settlements (BIS), World Bank Joint External Debt Hub (JEDH), Bloomberg, Schroders, September 2014

0

100

200

300

400

500

600

2013 Q3 2013 Q4 2014 Q1

32

Gross external financing requirement (GEFR) as % reserves

Markets in 2015

Liquidity is everywhere What price? Napoleon’s hat, the stars and stripes, Elvis

34

Source: BBC, The Telegraph, The Guardian

Thanks to central banks How much money has been printed?

0

2

4

6

8

10

12

14

16

18

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Value of assets in central banks' balance sheets (Trillions of USD)

Eurozone Japan Switzerland China US UK

35

Source: Thomson Datastream, Schroders at 7 November 2014

01/12/2014 17:49:03

$9.7

Trillion

Equity and bond markets have parted company Higher equity markets and lower bond yields since 2012

36

Source: Thomson Datastream, Schroders at 19 November 2014

Index

Rally begins to stretch some markets Equity market valuations (10-year history)

0

5

10

15

20

25

30

35

40

Russia(Micex)

China (Hshares)

MSCI EM Brazil(Bovespa)

UK (FTSE) Korea(Kospi)

Germany(DAX)

Japan(Topix)

MSCI DM France(CAC)

India(Nifty)

US (S&P) Eurostoxx

Current PE Mean Last year

PE ratio

Based on a 10 year history

37

The “box” in the box and whisker plot represents the interquartile range of data points and the “whisker” represents the maximum and minimum range over the past 10 years

Source: Thomson Datastream, Schroders at 6 November 2014

01/12/2014 17:49:03

Dollar strength creates emerging markets trouble The stronger USD will weigh on emerging vs developed equity performance

38

Source: Thomson Datastream, Schroders at 19 November 2014

01/12/2014 17:49:03

2015 surprise? USD strength may hold the Fed back US$ will weigh on inflation in the US

-15

-10

-5

0

5

10

15

20-10

-8

-6

-4

-2

0

2

4

6

8

10

96 98 00 04 06 08 10 12 14

Recession Import Prices exc Oil USD Broad Index 3m lead (rhs, inverted)

39

Source: Thomson Datastream, Schroders at 4 November 2014

01/12/2014 17:49:04

y/y, % y/y, %

-15

-10

-5

0

5

10

15

20-10

-8

-6

-4

-2

0

2

4

6

8

10

'96 '98 '00 '02 '04 '06 '08 '10 '12 '14

Import Prices exc Oil USD Broad Index 3m lead (rhs, inverted) Recession

y/y, % y/y, %

Asia crisisAsia crisis

Asset allocation views November 2014

40

Key: +/- market expected to outperform/ underperform (maximum +++ minimum ---) 0 indicates a neutral position

The above asset allocation is for illustrative purposes only. Actual client portfolios will vary according to mandate, benchmark, risk profile and the availability and riskiness of individual

asset classes in different regions. Source: Schroders Global Market Perspective Q4 2014

Equity + Bonds 0 Alternatives 0 Cash - Currency

By region By Sector By Sector USD +

US + Government 0 Commodities 0 JPY --

Europe ex UK 0 Inflation-linked 0 UK Property + EUR -

UK 0 Investment

grade

- GBP 0

Pacific ex Japan

(Australia, New

Zealand, Hong

Kong and

Singapore)

0 Emerging

market debt

0 AUD -

Japan + High yield - CHF 0

Emerging

Markets

0 EM 0

Gold 0

Global recovery remains de-synchronised reflecting policy

differences and structural headwinds

Lower commodity prices driven by supply as much as demand, will

support growth in 2015

US: most advanced in cycle, growth on a sustainable path, policy

rates to rise in 2015. USD to strengthen further

Eurozone: sluggish growth, but deflation should be avoided. ECB

will keep monetary policy loose

UK: the boom is fading, political risk will hamper growth in H1 2015

delaying Bank of England rate rise until H2

Emerging markets: vulnerable to tighter Fed policy. China growth

to remain tepid, but hard landing should be avoided

Macro risks skewed to downside/deflation

Back to “irrational exuberance” for markets?

Summary Global outlook and risks

41

For professional investors only. This material is not suitable for retail clients

The views and opinions contained herein are those of the Schroders Economics Group, and may not necessarily represent views expressed or reflected

in other Schroders communications, strategies or funds

This presentation is intended to be for information purposes only and it is not intended as promotional material in any respect. The material is not intended as an offer

or solicitation for the purchase or sale of any financial instrument. The material is not intended to provide, and should not be relied on for, accounting, legal or tax

advice, or investment recommendations. Information herein is believed to be reliable but Schroders does not warrant its completeness or accuracy. No responsibility

can be accepted for errors of fact or opinion. Reliance should not be placed on the views and information in the document when taking individual investment and/or

strategic decisions

Third party data is owned or licensed by the data provider and may not be reproduced or extracted and used for any other purpose without the data provider's

consent. Third party data is provided without any warranties of any kind. The data provider and issuer of the document shall have no liability in connection with the

third party data. The Prospectus and/or www.schroders.com contains additional disclaimers which apply to the third party data

Past performance is not a reliable indicator of future results, prices of shares and the income from them may fall as well as rise and investors may not get back the

amount originally invested

Forecast risk warning: The forecasts included in this presentation should not be relied upon, are not guaranteed and are provided only as at the date of issue. Our

forecasts are based on our own assumptions which may change. We accept no responsibility for any errors of fact or opinion and assume no obligation to provide

you with any changes to our assumptions or forecasts. Forecasts and assumptions may be affected by external economic or other factors.

Issued in November 2014 by Schroder Investment Management Limited, 31 Gresham Street, London EC2V 7QA. Registered No: 1893220 England. Authorised and

regulated by the Financial Conduct Authority. UK08460

Important information

42