A Competitive Realities Report for the Evansville Metro ...ftpcontent4.worldnow.com/wfie/Images/EVV...

84

1 E April 1, 2011 A Competitive Realities Report for the Evansville Metro and Southwest Indiana Region Prepared especially for the:

Transcript of A Competitive Realities Report for the Evansville Metro ...ftpcontent4.worldnow.com/wfie/Images/EVV...

1

E

April 1, 2011

A Competitive Realities Report for the Evansville Metro and Southwest Indiana Region

Prepared especially for the:

2

TABLE OF CONTENTS

ABOUT OUR COMPANIES ................................................................................................................ 3

INTRODUCTION AND METHODOLOGY ............................................................................................ 3

SECTION 1: ASSETS AND CHALLENGES ASSESSMENT ...................................................................... 5

SECTION 2: DASHBOARD INDICATORS SUMMARY ........................................................................ 15

SECTION 3: DEMOGRAPHIC & LABOR DYNAMICS ......................................................................... 17

SECTION 4: ECONOMIC DYNAMICS ............................................................................................... 34

SECTION 5: LOCAL SPECIALIZATION, COMPETITIVENESS & GROWTH .......................................... 51

CONCLUSION ................................................................................................................................. 70

APPENDICES ................................................................................................................................... 71

3

ABOUT OUR COMPANIES

INTRODUCTION AND METHODOLOGY

The Economic Development Coalition of Southwest Indiana

(EDC) retained Garner Economics, LLC, a nationally known

economic development and site location consulting firm based

in Atlanta to develop a regional economic development

strategy for the four county service area of the EDC consisting of Vanderburgh, Warrick, Gibson and

Posey Counties. Garner Economics has collaborated with Newmark Knight Frank of Chicago to assist in

this project related to key deliverables utilizing their expertise.

Our firms have assisted many local, regional and statewide

economic development organizations in creating proactive

business and community development strategies and

implementation guidance with the ultimate goal of quality jobs creation and capital investment. Our

combined companies’ site selection consulting experience has assisted volumes of corporate clients in

their expansion and relocation needs with a truly global reach. We are able to apply that knowledge of

what corporate investors consider important in their location search to our work with community

clients in devising “solutions that work”.

he Economic Development Coalition of Southwest

Indiana (EDC) retained Garner Economics, LLC in late

January of 2011 to conduct a regional economic

development strategy for the four county service area of the

EDC. The scope of services included analyzing the regional

economy, conduct an assets and challenges assessment of the

region from the eyes of a site location consultant, recommend

industry clusters suitable for the region based on our research

and analysis, and finally provide a set of implementable

recommendations that the stakeholders in the region can

utilize to enhance the economic well being of the region. Jay

Garner, President of Garner Economics, served as the lead

consultant with this project for the region. Tom Tveidt, research

economist for Garner Economics, provided the analytical analysis

and business target recommendations. Robert Hess and Tim Walden of Newmark Knight Frank (NKF)

were involved in analyzing the region’s assets and challenges and in recommendations for the EDC to

help in gaining a competitive advantage in business development and economic growth opportunities.

T

Map courtesy by the EDC of Southwest Indiana

4

This Competitive Realities Report is the first of three reports we are providing to the EDC. The second

report will consist of our industry cluster recommendations and the third and final report will be a

consolidation of all of the reports along with our conclusions and recommendations in how the region

can enhance its global competitiveness.

Our approach began with the Garner Economics team conducting an Assets and Challenges

assessment of the region. We have conducted hundreds of Assets and Challenges assessments (also

referred to as a SWOT analysis) on behalf of our economic development and corporate clients

throughout the United States. We apply many of the same criteria to assess a community that we use

when a corporate client engages us to evaluate communities on their behalf for possible corporate

investment. Our assessment, which follows in this report, is both an objective and subjective

evaluation of the community from the eyes of a site location consultant. Our Assets and Challenges

assessment allows us to document what problems exist in the region that constitutes barriers for

successfully achieving the vision of its leadership.

The objectives of this assessment are to:

● Identify key strengths to emphasize in economic development marketing efforts, and;

● Identify key weaknesses that may limit investment in the region so that remediation of these local challenges may occur.

A multi-day windshield tour was provided by representatives of the EDC to review those items that

were necessary for us to evaluate as outlined in our assets and challenges below. This research then

supplemented the economic analysis we conducted to identify the best possible opportunities for

business targets.

We then conducted focus groups and interviews with key stakeholders in the region. This gave us an

overview of how local businesses and residents evaluate the business climate of the area. We

facilitated eight focus groups over a two day period with seventy participants. Focus group categories

included large employers, small to midsized employers, elected/government officials,

entrepreneurs/start-ups, financing/banking, academia/career development, and design/engineering

(see the appendix for a summary of the focus groups).

Finally, as it relates to the completion of this Competitive Realities Report, we evaluated key

demographic and economic indicators for the region as compared to state and national trends as well

as the comparison of the Chattanooga, TN MSA and the Davenport-Moline-Rock Island, IA-IL MSA,

which were selected as benchmark communities by the EDC. These areas both have or had a high

concentration of similar industry specialization to the Evansville region, and all three MSA’s have

multiple states in their geography.

To enable readers a summary overview of the report’s main findings, a set of dashboard icons is

presented. Each finding has an accompanying icon to assist with interpretation. Readers are

encouraged to review the supporting data to gain a more complete understanding in those areas of

interest in the full report.

5

The Garner Economics team analyzed sixty five (65)

community factors as part of the assessment for the region. These

are many of the same factors that are used when we conduct a

site/community evaluation for a company that is considering a

new location, expansion, consolidation or closure.

SECTION 1: ASSETS AND CHALLENGES ASSESSMENT

he Garner Economics team analyzed sixty five (65) community

factors as part of the assessment for the region. These are

many of the same factors that are used when we conduct

a site/community evaluation for a company that is considering

a new location, expansion, consolidation or closure. Our

methodology was both objective - using published statistical

sources such as crime rate data and wage data, and

subjective - based on our many years of working in the

economic development profession and in representing

companies evaluating communities for investment. Tours of

the region took place in February and March as part of our

asset mapping methodology.

We define an Asset as a positive feature of the region that would

be evaluated and rated by the Garner Economics team as normal or

better. A challenge is considered by us as a deficiency that should be

addressed for future remediation and may be an impediment for economic

development if not resolved over time. Neutral is considered normal in the realm of economic

development opportunity and competitiveness.

T

REPORT DASHBOARD

Indicates the region is better (more positive) compared to a majority of the benchmark geographies, or points to a positive trend or asset within the region.

Indicates the region is neutral, neither positive nor negative. Indicator may represent an observation, or be in the middle of the benchmark geographies.

Indicates the region is worse compared to a majority of the benchmark geographies, or points to a negative trend or challenge within the region.

6

he Evansville region is

well positioned

geographically for access

to regional, national and in some

aspects, international markets.

The area is within a one day

drive of more than two-thirds of

the U.S. population. It has good

east/west access with I-64, but

its north/south access is

contingent on the successful

completion of I-69. Four rail

lines serve the area and the Port

of Indiana at Mount Vernon in

Posey County has a 30ft. river

depth. Companies like Shoe

Carnival however use a rail/truck

land bridge system to transport

imports from the Port of Long

Beach or other west coast ports

to area distribution centers. The

Port of Indiana’s focus is bulk commodities.

High speed internet service is slow. On multiple trips to Evansville, we experienced very slow

download times from various locations, including different hotels in the area. According to the

National Broadband Map, Evansville ranks 368 of 370 metros in the U.S. on upload and download

speeds (see endnote 8). This is a serious impediment for the attraction of certain IT types of

companies, and to mobile entrepreneurs that rely on the internet for their work.

The Evansville Regional Airport provides good air service for a region of its size. However, the schedule

is not necessarily business friendly. For example, it is difficult to do a day trip to and from Atlanta.

Currently, the first flight from ATL to EVV which is nonstop arrives in EVV at 10:25am. The last

departure from EVV back to ATL (non stop) is at 3:45pm. This only leaves a four hour window of work.

This provides a challenge for companies that are engaged in office/shared services and in some sales

positions.

ACCESS TO MARKETS RATING

Centrally located for major regional market 1

Centrally located for national market 2

Well positioned to serve international markets 3

Interstate highways 4

Rail service 5

Port facilities 6

Scheduled airfreight services

Within 1 hour of commercial air passenger service

7

General aviation airport capable of handling corporate aircraft

High speed internet services 8

Connection of local telephone company to national fiber optics network

9

T

7

During our focus group sessions,

many of the respondents who

are either employers, or who

serve as a resource to help train

employees for employers, cited

the difficulty to find and retain

skilled industrial, technical and

managerial talent. There was

near unanimity of that opinion

from most if not all of the 70

focus groups participants we

interviewed. The cost of labor is

comparable to the benchmark

regions we analyzed, except for

certain counties that are skewed

because of a dominate

employer. Southwest Indiana is

the home of the University of

Evansville, the University of

Southern Indiana and Oakland City University. Ivy Tech Community College and Vincennes University

both do a good job of providing a curriculum to meet the demands and needs of employers.

U of E offers civil, computer, electrical and mechanical engineering degrees and is a valuable asset to

the region with its degreed offerings. USI offers a BS degree in industrial supervision.

Many regions around the U.S. are experiencing the same challenges Southwest Indiana faces in finding

and retaining skilled talent. Those that are able to differentiate their regions with a method to attract

and retain people will flourish in a highly competitive global marketplace.

LABOR RATING

Availability of skilled industrial workers 10

Availability of skilled clerical workers

Availability of technicians and scientists

Availability of managerial personnel

Cost of labor 11

Quality of labor-management relations 12

Availability of post-secondary vocational training 13

Availability of free on-the-job training assistance 14

Within 1/2 hour of four year university/college and post graduate degrees

15

Availability of engineering program 16

8

Agricultural production is an

unsung asset in the region.

Posey and Gibson counties are

large growers of corn, soybean,

wheat, melons and sorghum

(see endnote 17). With a

movement by many food

processing manufacturers to

locate closer to the food

commodity, Southwest Indiana

can potentially position itself as a

suitable location for food

processing manufactures.

Coal production is dominant in

the region. We believe that

there is potential for energy research related to coal to be more of a factor in the area. This would

typically be done in cooperation with an academic institution, e.g. Indiana Center for Coal and

Technology Research at Purdue University.

Southwest Indiana has a high per capita ratio of both manufacturing employment and manufactures’

shipments compared to many other regions in the U.S. Shipments from the region are in excess of

$3.6 billion annually.

ACCESS TO RESOURCES RATING

Availability of agricultural products for food processing

17

Availability of minerals 18

Availability of manufacturing processes 19

Availability of business and professional services

Cost of electricity for industrial use 20

Availability of high quality electric service

Availability of uninterruptible natural gas

Availability of water/cost of water/sewer Varies by county

9

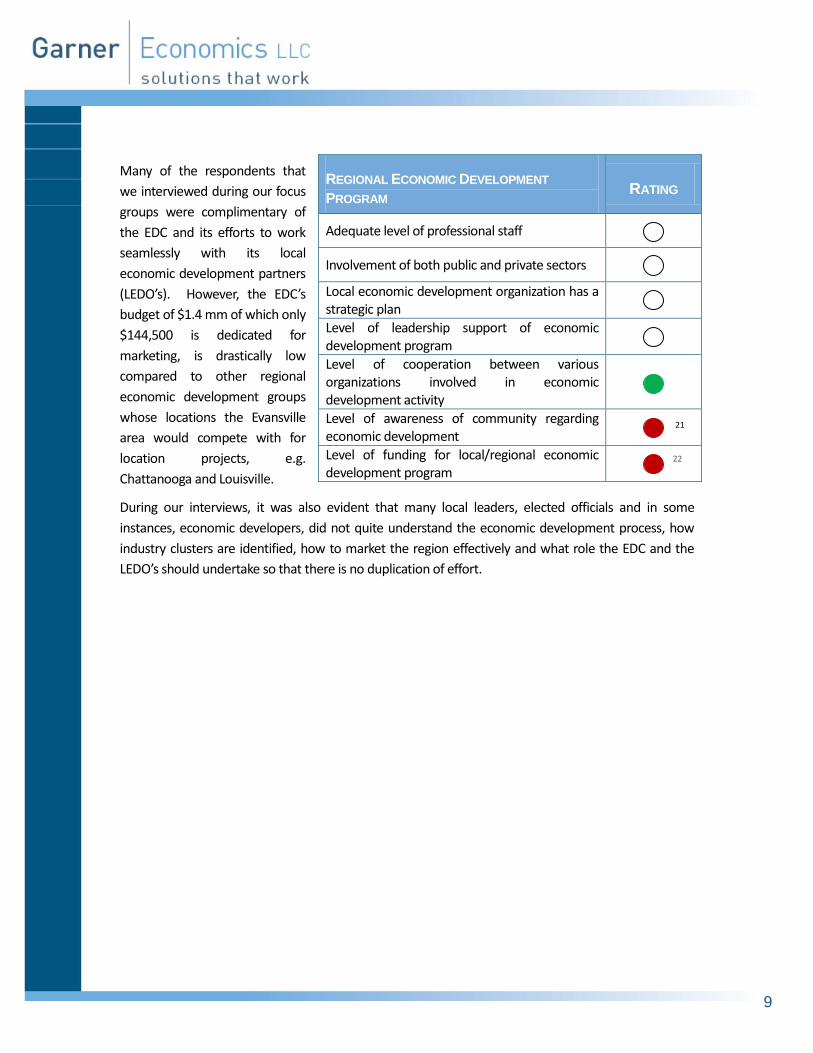

Many of the respondents that

we interviewed during our focus

groups were complimentary of

the EDC and its efforts to work

seamlessly with its local

economic development partners

(LEDO’s). However, the EDC’s

budget of $1.4 mm of which only

$144,500 is dedicated for

marketing, is drastically low

compared to other regional

economic development groups

whose locations the Evansville

area would compete with for

location projects, e.g.

Chattanooga and Louisville.

During our interviews, it was also evident that many local leaders, elected officials and in some

instances, economic developers, did not quite understand the economic development process, how

industry clusters are identified, how to market the region effectively and what role the EDC and the

LEDO’s should undertake so that there is no duplication of effort.

REGIONAL ECONOMIC DEVELOPMENT

PROGRAM RATING

Adequate level of professional staff

Involvement of both public and private sectors

Local economic development organization has a strategic plan

Level of leadership support of economic development program

Level of cooperation between various organizations involved in economic development activity

Level of awareness of community regarding economic development

21

Level of funding for local/regional economic development program

22

10

Clearly, one of the most

significant challenges in the

region is the lack of suitable and

available industrial and office

space related to industrial parks,

industrial sites and available,

quality class A office space.

There are available industrial

parks in Warrick County, but

most of what we saw during our

tour of the region was land that

may be for sale and with little to no infrastructure already to the location. It is not defined as a site

until there is an agreed to price on the property with infrastructure in place. As such, the region is site

deficient and our focus group participants said the same.

The availability of venture or

angel capital for entrepreneurs

and start up ventures related to

non retail enterprises is virtually

nonexistent in the region.

Entrepreneurial growth and the

need to attract and retain early-

stage, high-growth, innovative

companies is important for the region to grow economically. Many analysts and economists believe

that up to 70% of the net new jobs in this decade will be created by high potential entrepreneurial

companies in a variety of industries and niches.

ACCESS TO SPACE RATING

Availability of fully served and attractive industrial sites

23

Availability of fully served and attractive office sites

Reasonably priced sites

Availability of suitable industrial space

Availability of suitable office space

ACCESS TO CAPITAL RATING

Availability of tax-exempt financing for new industrial facilities

Availability of low interest loans for small business

Availability of venture capital from local sources for business startups

24

11

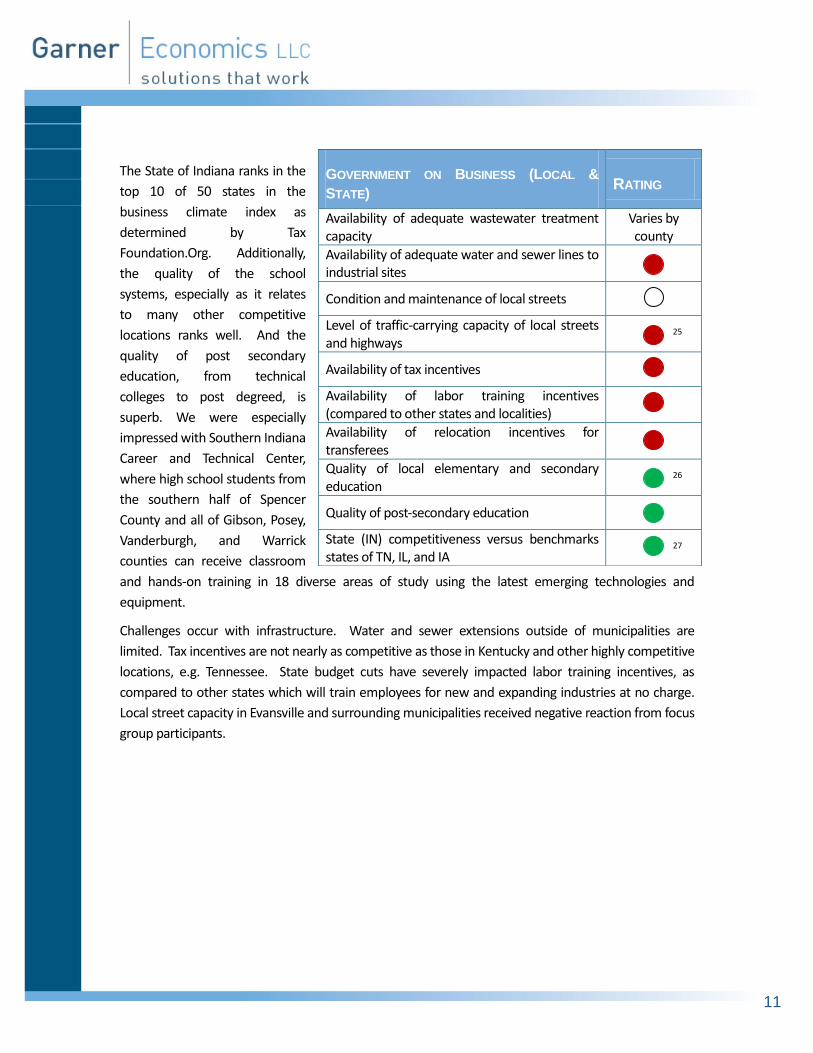

The State of Indiana ranks in the

top 10 of 50 states in the

business climate index as

determined by Tax

Foundation.Org. Additionally,

the quality of the school

systems, especially as it relates

to many other competitive

locations ranks well. And the

quality of post secondary

education, from technical

colleges to post degreed, is

superb. We were especially

impressed with Southern Indiana

Career and Technical Center,

where high school students from

the southern half of Spencer

County and all of Gibson, Posey,

Vanderburgh, and Warrick

counties can receive classroom

and hands-on training in 18 diverse areas of study using the latest emerging technologies and

equipment.

Challenges occur with infrastructure. Water and sewer extensions outside of municipalities are

limited. Tax incentives are not nearly as competitive as those in Kentucky and other highly competitive

locations, e.g. Tennessee. State budget cuts have severely impacted labor training incentives, as

compared to other states which will train employees for new and expanding industries at no charge.

Local street capacity in Evansville and surrounding municipalities received negative reaction from focus

group participants.

GOVERNMENT ON BUSINESS (LOCAL &

STATE) RATING

Availability of adequate wastewater treatment capacity

Varies by county

Availability of adequate water and sewer lines to industrial sites

Condition and maintenance of local streets

Level of traffic-carrying capacity of local streets and highways

25

Availability of tax incentives

Availability of labor training incentives (compared to other states and localities)

Availability of relocation incentives for transferees

Quality of local elementary and secondary education

26

Quality of post-secondary education

State (IN) competitiveness versus benchmarks states of TN, IL, and IA

27

12

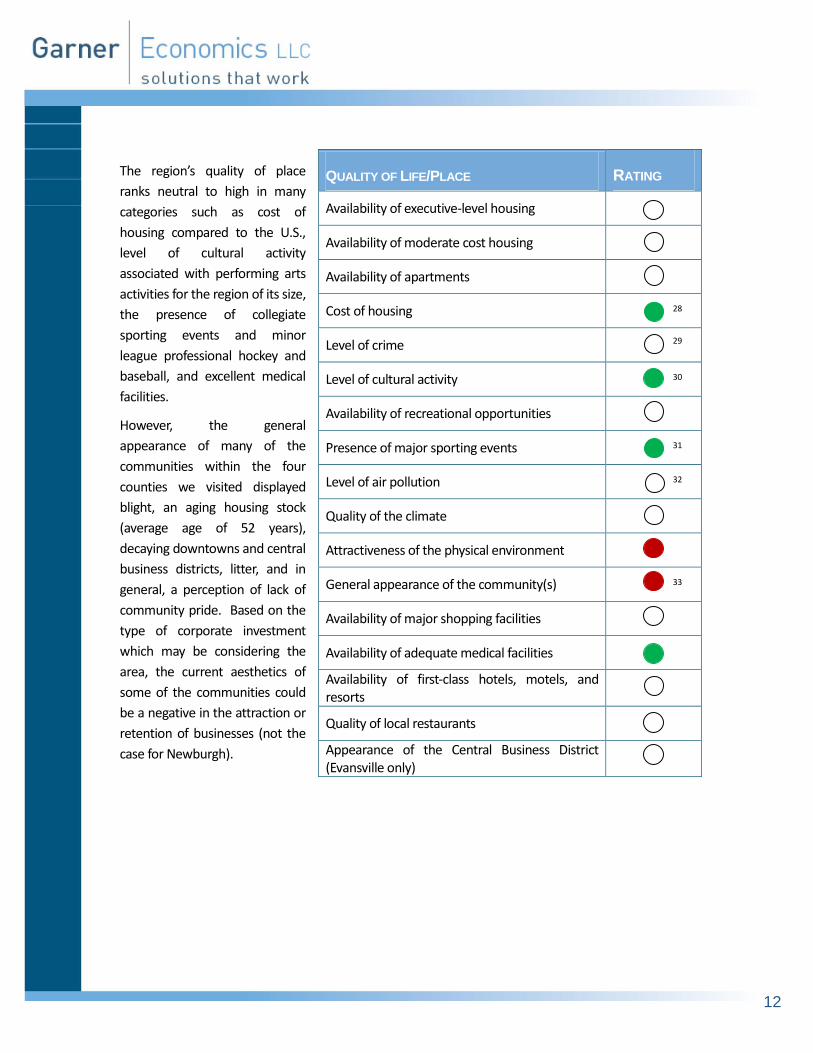

The region’s quality of place

ranks neutral to high in many

categories such as cost of

housing compared to the U.S.,

level of cultural activity

associated with performing arts

activities for the region of its size,

the presence of collegiate

sporting events and minor

league professional hockey and

baseball, and excellent medical

facilities.

However, the general

appearance of many of the

communities within the four

counties we visited displayed

blight, an aging housing stock

(average age of 52 years),

decaying downtowns and central

business districts, litter, and in

general, a perception of lack of

community pride. Based on the

type of corporate investment

which may be considering the

area, the current aesthetics of

some of the communities could

be a negative in the attraction or

retention of businesses (not the

case for Newburgh).

QUALITY OF LIFE/PLACE RATING

Availability of executive-level housing

Availability of moderate cost housing

Availability of apartments

Cost of housing 28

Level of crime 29

Level of cultural activity 30

Availability of recreational opportunities

Presence of major sporting events 31

Level of air pollution 32

Quality of the climate

Attractiveness of the physical environment

General appearance of the community(s) 33

Availability of major shopping facilities

Availability of adequate medical facilities

Availability of first-class hotels, motels, and resorts

Quality of local restaurants

Appearance of the Central Business District (Evansville only)

13

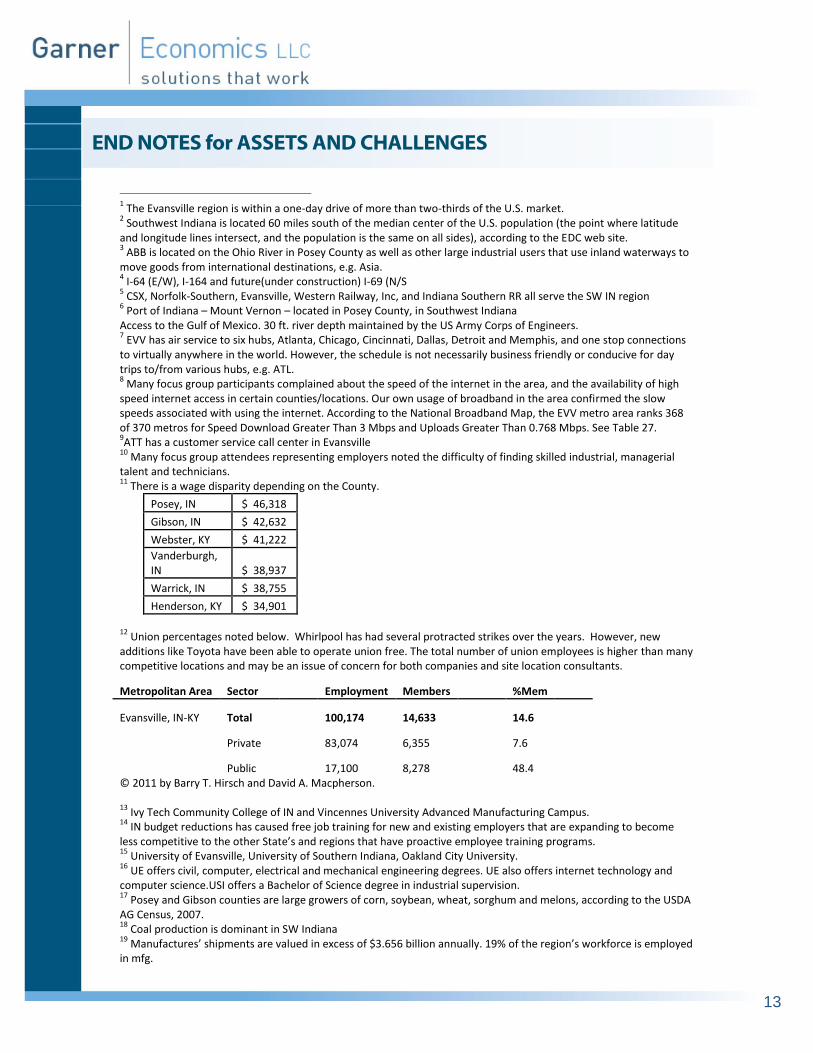

END NOTES for ASSETS AND CHALLENGES

1 The Evansville region is within a one-day drive of more than two-thirds of the U.S. market.

2 Southwest Indiana is located 60 miles south of the median center of the U.S. population (the point where latitude

and longitude lines intersect, and the population is the same on all sides), according to the EDC web site. 3 ABB is located on the Ohio River in Posey County as well as other large industrial users that use inland waterways to

move goods from international destinations, e.g. Asia. 4 I-64 (E/W), I-164 and future(under construction) I-69 (N/S

5 CSX, Norfolk-Southern, Evansville, Western Railway, Inc, and Indiana Southern RR all serve the SW IN region

6 Port of Indiana – Mount Vernon – located in Posey County, in Southwest Indiana

Access to the Gulf of Mexico. 30 ft. river depth maintained by the US Army Corps of Engineers. 7 EVV has air service to six hubs, Atlanta, Chicago, Cincinnati, Dallas, Detroit and Memphis, and one stop connections

to virtually anywhere in the world. However, the schedule is not necessarily business friendly or conducive for day trips to/from various hubs, e.g. ATL. 8 Many focus group participants complained about the speed of the internet in the area, and the availability of high

speed internet access in certain counties/locations. Our own usage of broadband in the area confirmed the slow speeds associated with using the internet. According to the National Broadband Map, the EVV metro area ranks 368 of 370 metros for Speed Download Greater Than 3 Mbps and Uploads Greater Than 0.768 Mbps. See Table 27. 9ATT has a customer service call center in Evansville

10 Many focus group attendees representing employers noted the difficulty of finding skilled industrial, managerial

talent and technicians. 11

There is a wage disparity depending on the County.

Posey, IN $ 46,318

Gibson, IN $ 42,632

Webster, KY $ 41,222

Vanderburgh, IN $ 38,937

Warrick, IN $ 38,755

Henderson, KY $ 34,901

12

Union percentages noted below. Whirlpool has had several protracted strikes over the years. However, new additions like Toyota have been able to operate union free. The total number of union employees is higher than many competitive locations and may be an issue of concern for both companies and site location consultants.

Metropolitan Area Sector

Employment Members

%Mem

Evansville, IN-KY Total

100,174 14,633

14.6

Private

83,074 6,355

7.6

Public

17,100 8,278

48.4

© 2011 by Barry T. Hirsch and David A. Macpherson. 13

Ivy Tech Community College of IN and Vincennes University Advanced Manufacturing Campus. 14

IN budget reductions has caused free job training for new and existing employers that are expanding to become less competitive to the other State’s and regions that have proactive employee training programs. 15

University of Evansville, University of Southern Indiana, Oakland City University. 16

UE offers civil, computer, electrical and mechanical engineering degrees. UE also offers internet technology and computer science.USI offers a Bachelor of Science degree in industrial supervision. 17

Posey and Gibson counties are large growers of corn, soybean, wheat, sorghum and melons, according to the USDA AG Census, 2007. 18

Coal production is dominant in SW Indiana 19

Manufactures’ shipments are valued in excess of $3.656 billion annually. 19% of the region’s workforce is employed in mfg.

14

20

Average Retail Price of Electricity to Ultimate Customers by End-Use Sector, by State, Year-to-Date through November 2010, U.S. Energy Information Administration, for industrial users:

East North Central 6.52

Illinois 6.72

Indiana (includes Duke and Vectren)

5.96

Michigan 7.19

Ohio 6.32

21

Some focus group participants noted that there is a disconnect between local elected officials and a better understanding of the economic development process. We too observed that as a challenge during the focus groups. 22

The EDC’s annual budget is $1.4mm, of which $144,500 is designated for marketing and external outreach. Based on our analysis of best practice regional economic development programs, the EDC’s marketing budget is drastically low. 23

There are two industrial parks in Warrick County. 24 Venture capital and a formal angel network are nonexistent in the region 25

Many focus group participants complained about the conditions and traffic flow of local streets 26

http://www.evscschools.com/AdminDefault.aspx?portalId=c45369af-1b9a-4929-a2a1-446af4fcbf7d&pid=65744905-4419-4c19-81ae-03f1440d3d4d 27

Indiana ranks number 10 of the 50 states in the State rankings business climate index, as determined by the Tax Foundation, 2011 http://www.taxfoundation.org/research/show/22658.html 28

*For Evansville (Sperling’s 2011): Housing Evansville, IN United States

Median Home Age

52 33

Median Home Cost

$97,020 $183,450

Home Appreciation

1.91% -5.21%

Homes Owned

53.10% 60.14%

Housing Vacant

10.91% 10.50%

Homes Rented

35.99% 29.36%

Property Tax Rate

$7.85 $11.20

29 See Table 10.

30 For the size of the region’s population, there are a number of documented performing arts activities that give the

area a good rating. However, most focus group participants did not feel that there were many cultural assets in the region. 31

UE, USI and Oakland City University both offer NCAA Div I and II college sports. There is minor league hockey and baseball team. 32

Vanderburgh and Warrick Counties are both attainment areas with a maintenance plan. Posey and Gibson counties are attainment. Air quality in Evansville, IN is 38 on a scale to 100 (higher is better). This is based on ozone alert days and number of pollutants in the air, as reported by the EPA. 33

Newburgh shows exceptionally well. Evansville, which is the dominant city in the region, does not. Princeton and Oakland City do not present itself well either. An aged housing stock and what appears to be lack of community pride in the aesthetes of the community is evident. The median age of Evansville real estate is 52 years (Sperling’s, 2011).

15

SECTION 2: DASHBOARD INDICATORS SUMMARY

he following analysis examines the economic position and competitiveness of the six county

Evansville metropolitan economy. Throughout the report, references to Evansville imply the

entire metropolitan area, unless otherwise noted. Besides the nation and state of Indiana, the

report also compares Evansville to two benchmark communities, which are Chattanooga TN, and

Davenport-Moline-Rock Island IA-IL.

The analysis relies heavily on raw objective data collected by impartial governmental or impartial

agencies. In all cases the original and most current available data as of March 31, 2011 is used. All

unique calculations and computations from the original data were conducted by Garner Economics,

who will gladly share methodology to clients upon request.

Population growth, while positive at a rate of 4.6 percent over the last decade, is below both the nation, state and one benchmark community.

Over the period of 2000-2009, natural growth accounted for an estimated 83 percent of net new residents. Over the same period, Evansville lost a net of 657 residents due to domestic out-migration. Growth from natural and international sources, while positive, is less likely to satisfy immediate workforce demands.

o With 89.9 percent of the population categorizing themselves as white, the population of Evansville is less diverse relative to the state, nation, and benchmark communities.

At 38.5 years, the median age in Evansville is very close to the medians in both benchmark communities, and approximately two years above the state and nation.

Relative to the state and nation, Evansville has a lower proportion of its population ages 5-24, and 35-44. Conversely, the area has a higher relative proportion of population ages 45 and older.

Evansville has a higher relative proportion of residents whose highest level of educational attainment is “High school diploma”, compared to the nation, state and both benchmark communities. Likewise, the area has a lower relative proportion of residents whose highest level of attainment is “Bachelor’s Degree” and above.

At eight percent, or 3,952 of all bachelor degree holders, Evansville has a relatively high proportion of residents with degrees in Engineering.

Average ACT scores for Evansville schools within the four metro Indiana counties are notably above the nation, and both benchmark communities, across all subjects tested.

o A total of 8 percent of the population age 18 and over are enrolled in college or graduate school in Evansville, a percentage that is slightly less than the nation, state, and one benchmark community.

T

16

Violent and Property crime rates in Evansville are below the nation, state and the one benchmark community for which rates were available.

The percentage and number of persons who both work and live in the four Evansville metro Indiana counties has declined over the last five years.

Per capita real GDP has been declining in Evansville since 2003. Although still higher than the state, and benchmark communities, Evansville fell below the nation in 2004.

As of 2009, Evansville had exports totaling $2 billion, up nearly 40 percent above 2008. In per capita terms, at $5,724, Evansville exports are above the state, nation, and one benchmark community.

The five and ten-year pace of growth of Evansville’s average wage per job is below the nation and both benchmark communities.

The five and ten-year pace of growth of Evansville’s per capita income is below the nation and one benchmark communities.

Through February 2011, Evansville has experienced 12 straight months of year-to-year employment growth. The current rate of job growth averages 1.6 percent, outpacing the nation, state and both benchmark communities.

Since the end of the recession, Evansville’s unemployment rate has averaged 8.5 percent, a rate below the averages for the state, nation, and benchmark communities.

o Evansville has a relatively higher proportion of employment in Construction, Manufacturing, Private Education and Health Services. Conversely, the area has a lower relative proportion of employment in Financial Activities, and Federal, State and Local Government.

Evansville has experienced a decline in the total number of private establishments, down by 2 percent over the last nine years, and up just 0.5 percent over the last five year. The rates are below the nation, state, and one benchmark community.

As of 2008, proprietors accounted for 14.3 percent of total employment in Evansville, proportionally less than in the nation, state or both benchmark communities.

Evansville’s 2010 composite Cost of Living score of 96.1 demonstrates a low relative rate cost for residents. The two benchmark communities also enjoy scores below 100. Utility prices appear the exception in Evansville, scoring at 120.3.

Relative to the benchmark community airports, Evansville Dress Regional Airport has significantly less passenger activity and scheduled fights, ranging from 40 to 60 percent lower.

Evansville’s broadband coverage ranks in the lowest 50 to 10 percent of rankings among all U.S. metros for four key measures, and is also below the benchmark communities in most areas.

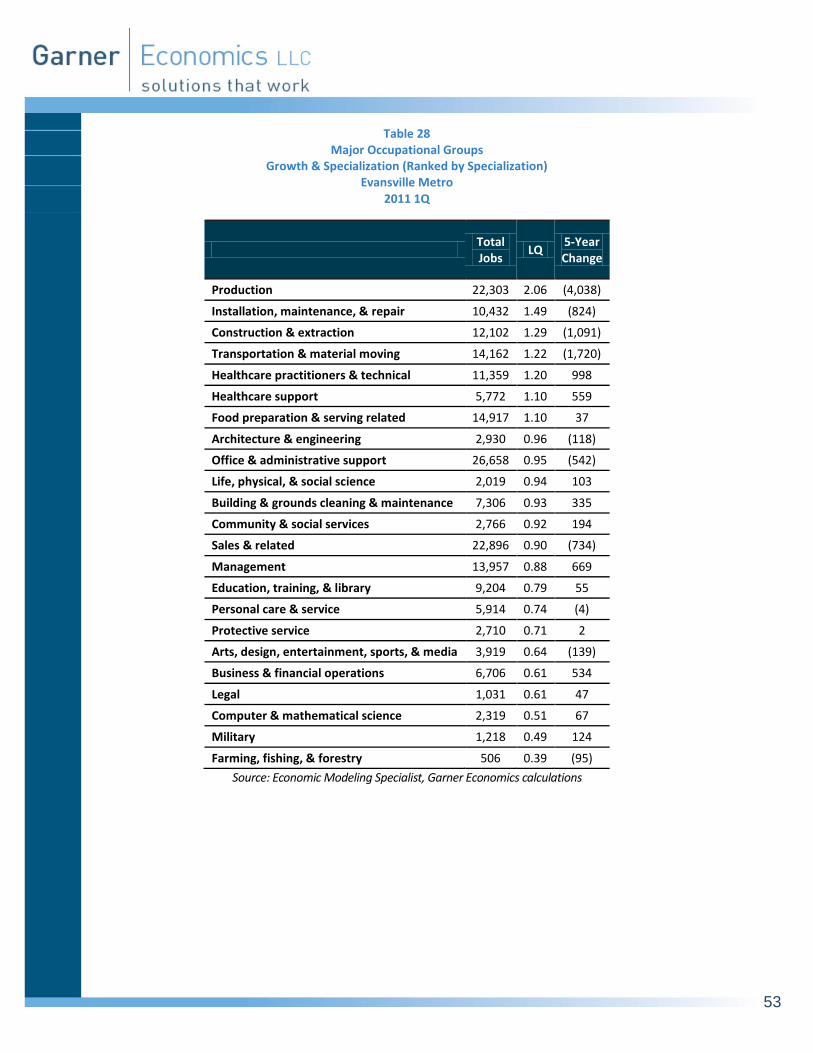

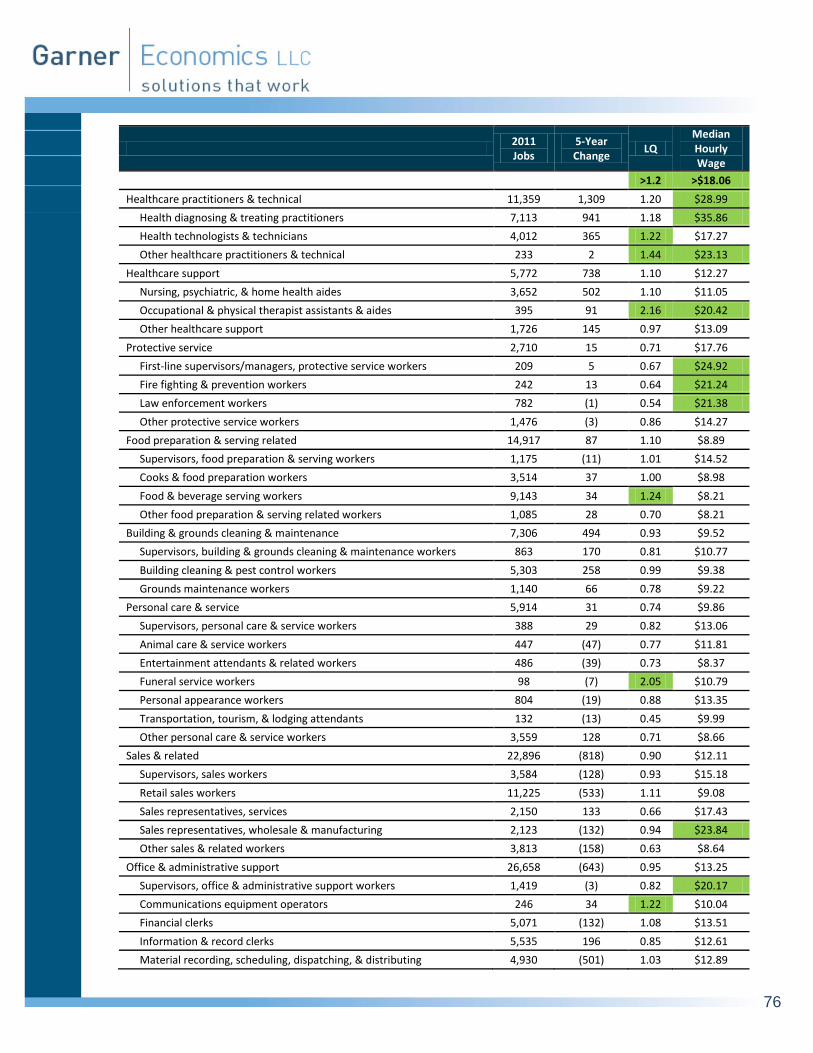

o Evansville’s most highly specialized occupational group is Production. Other local highly specialized occupational groups are Installation, maintenance & repair, Construction & extraction, and Transportation & material moving.

17

SECTION 3: DEMOGRAPHIC & LABOR DYNAMICS

o Several occupational groups in Evansville have experienced growth exceeding national trends, implying a local competitive edge; the leaders are Construction & extraction, Office & administrative support, and Production.

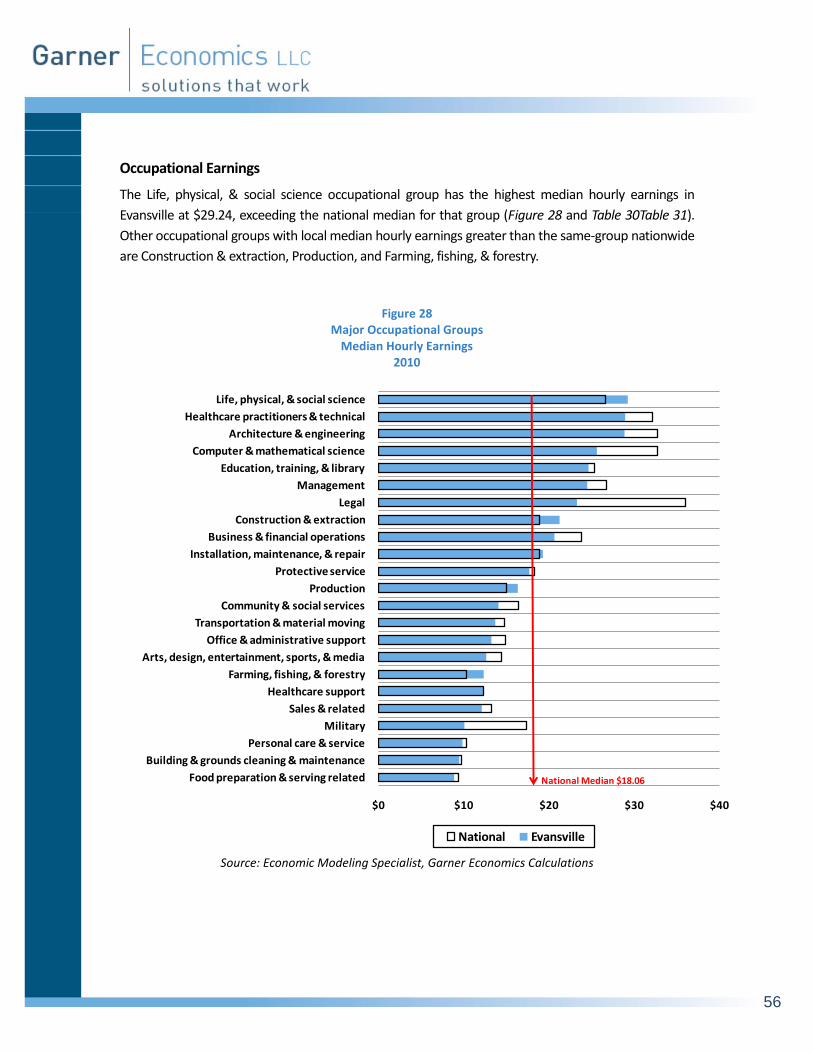

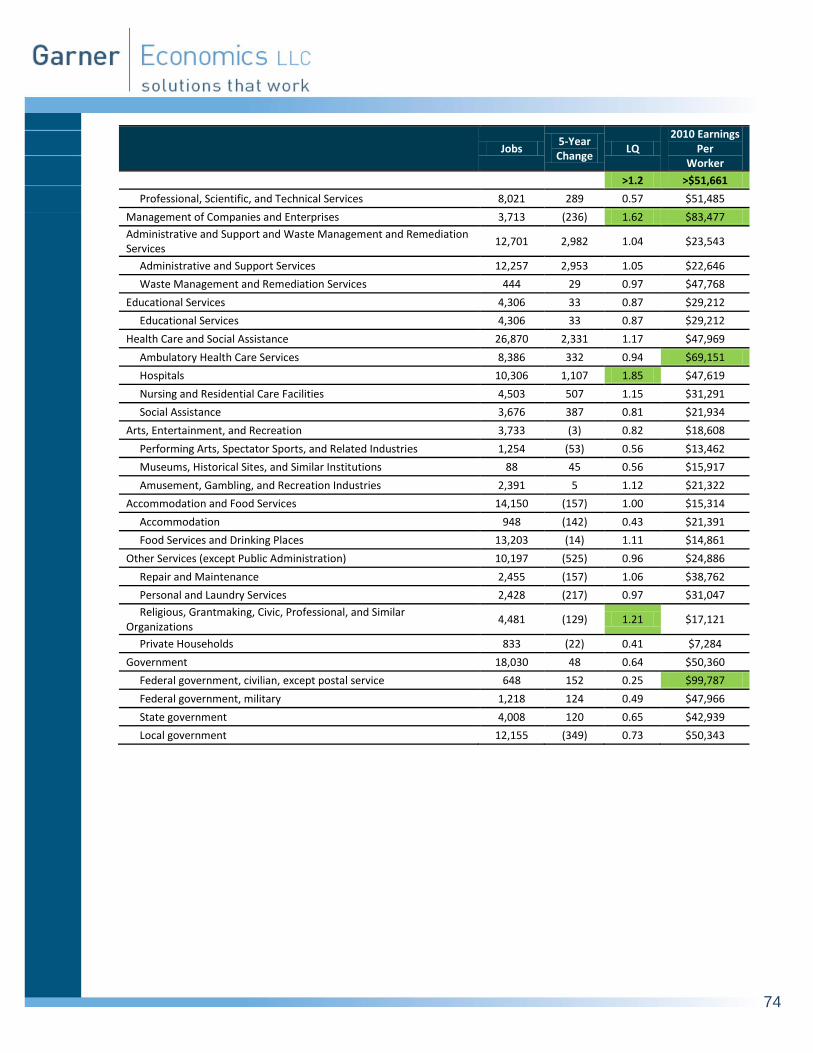

o The Life, physical & social science occupational group has the highest median hourly earnings in Evansville at $29.24, exceeding the national median for that group. Other occupational groups with local median hourly earnings greater than the same-group nationwide are Construction & extraction, Production, and Farming, fishing, & forestry.

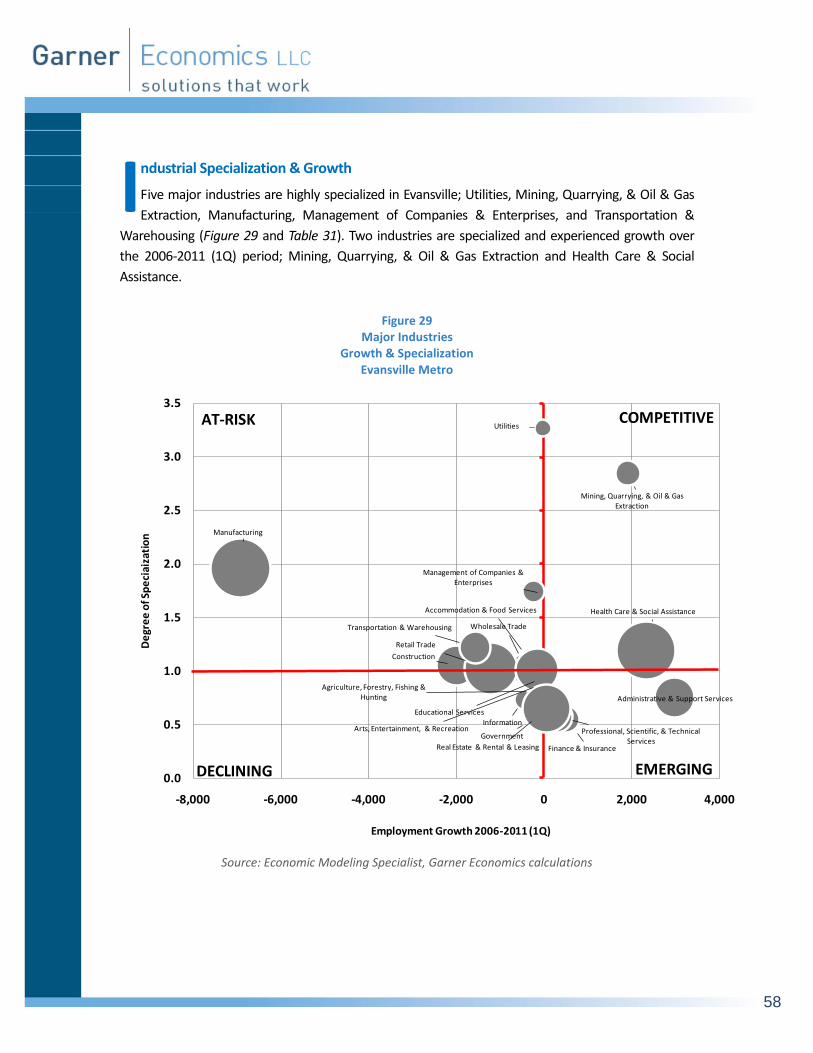

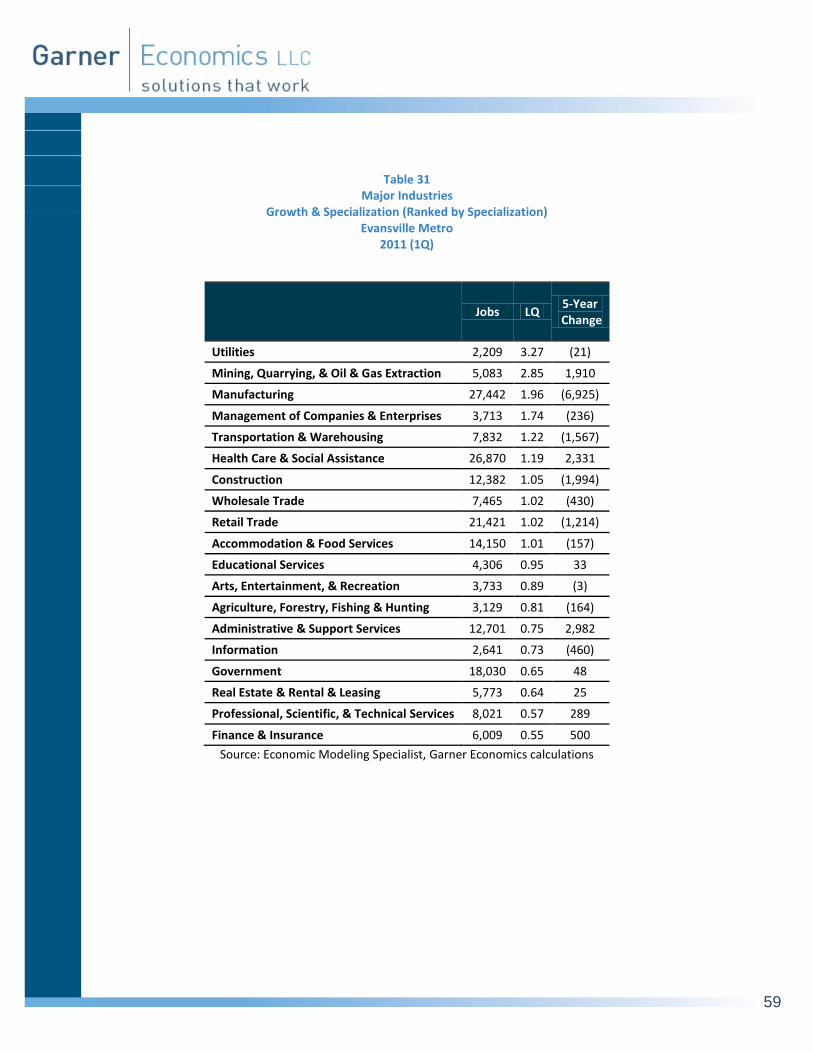

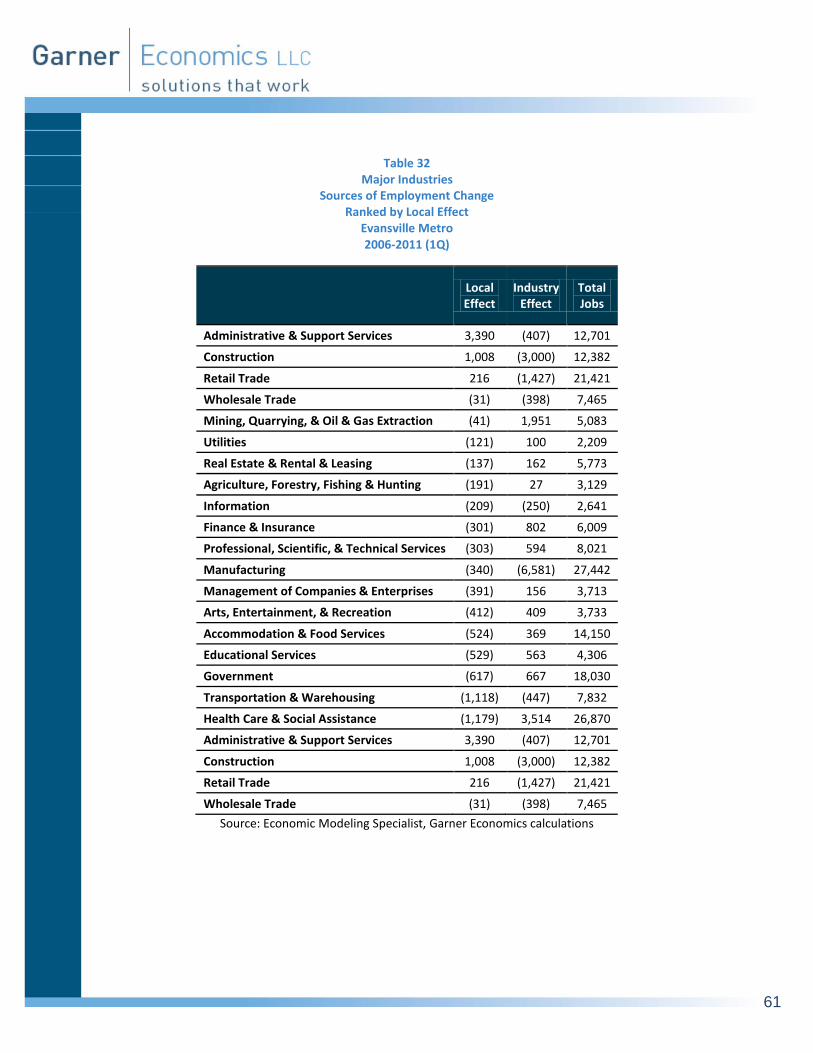

o Five major industries are highly specialized in Evansville; Utilities, Mining, Quarrying, & Oil & Gas Extraction, Manufacturing, Management of Companies & Enterprises, and Transportation & Warehousing.

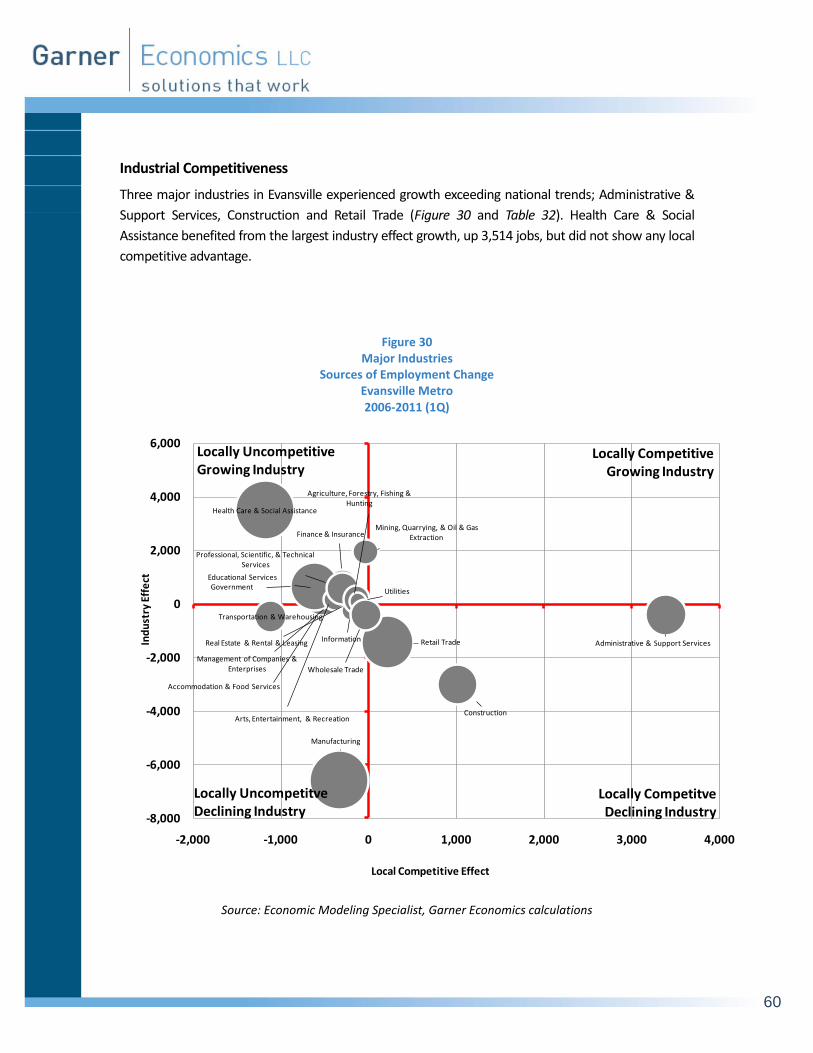

o Three major industries in Evansville experienced growth exceeding same-industry national trends; Administrative & Support Services, Construction and Retail Trade.

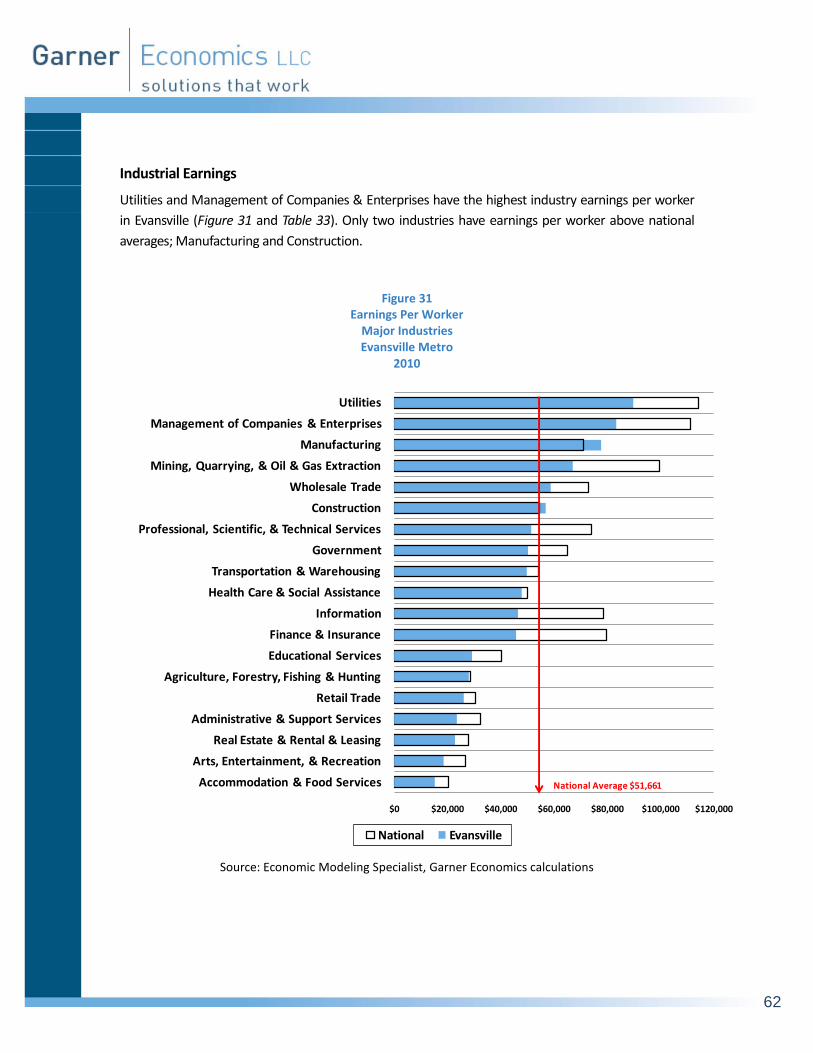

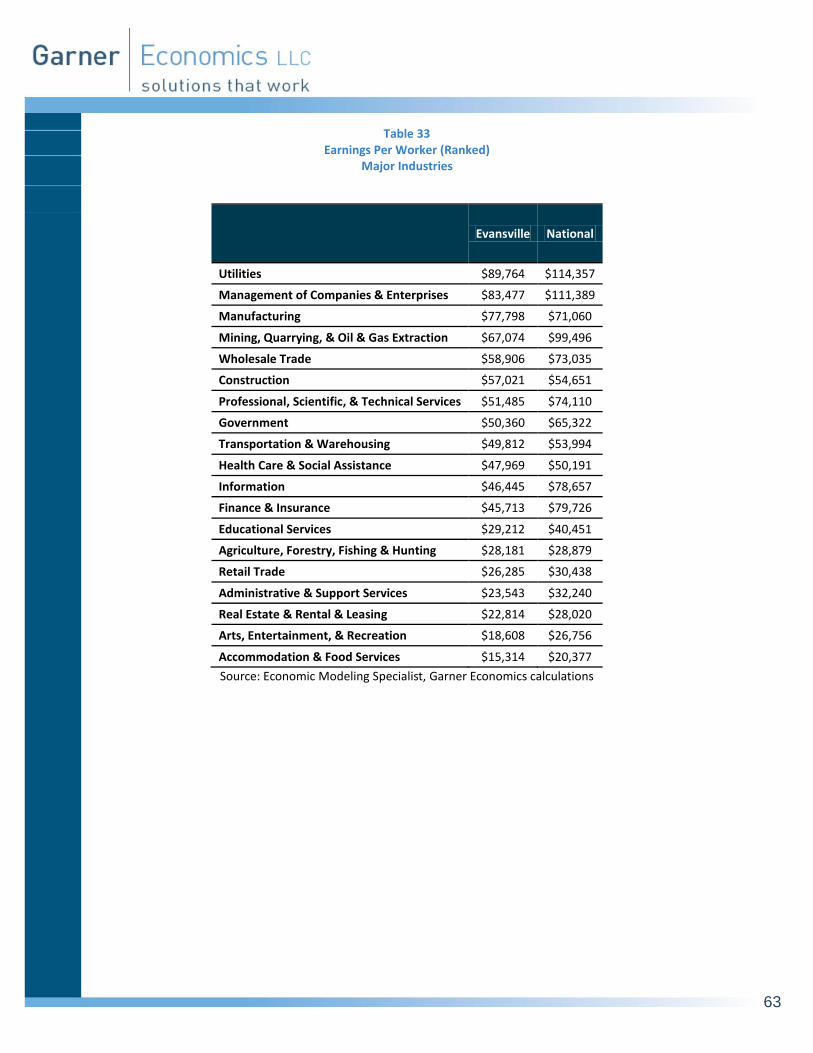

o Utilities and Management of Companies & Enterprises have the highest industry earnings per worker in Evansville. Only two industries have earnings per worker above national same-industry averages; Manufacturing and Construction.

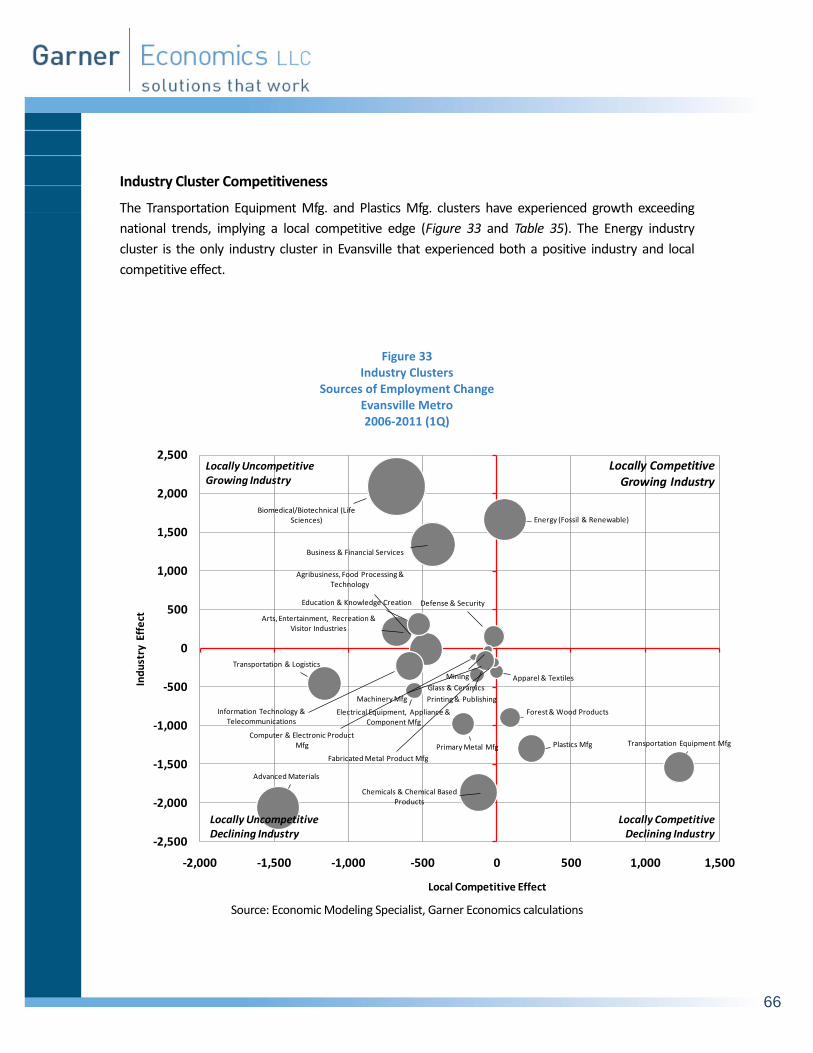

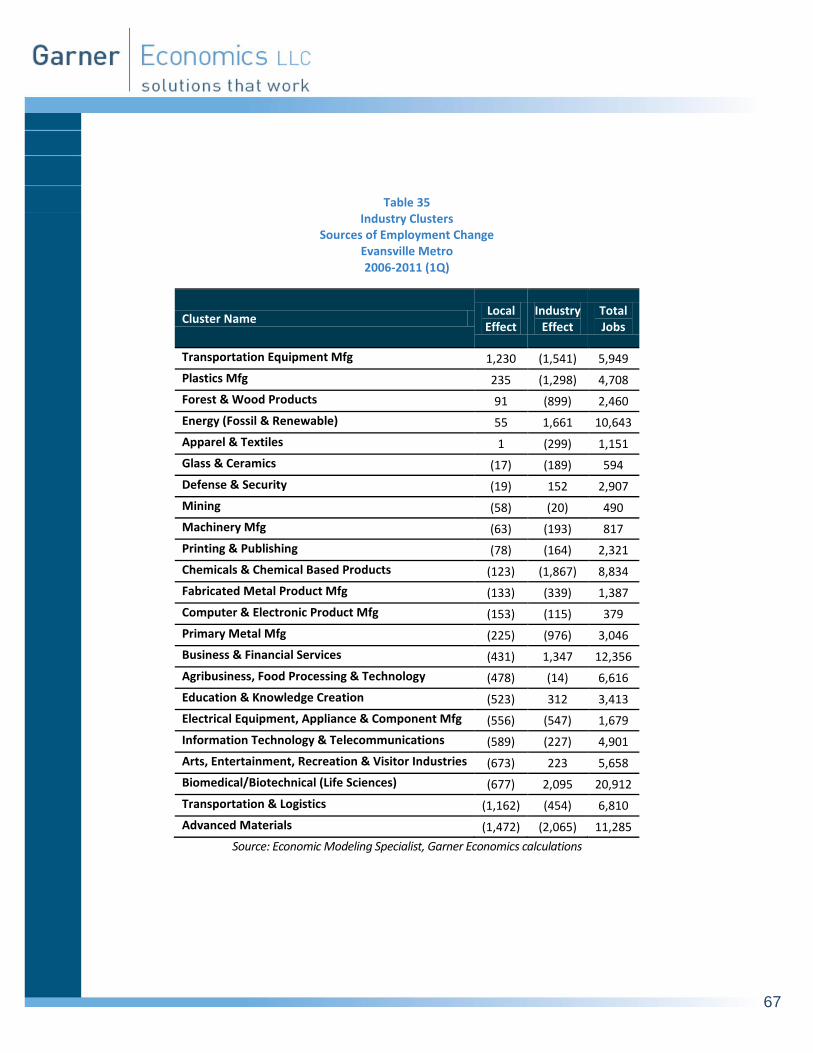

o Evansville has two industry clusters which display local specialization and positive employment growth; Biomedical/Biotechnical (Life Sciences) and Energy. The two most highly specialized industry clusters in Evansville are Primary Metal Mfg., and Plastics Mfg.

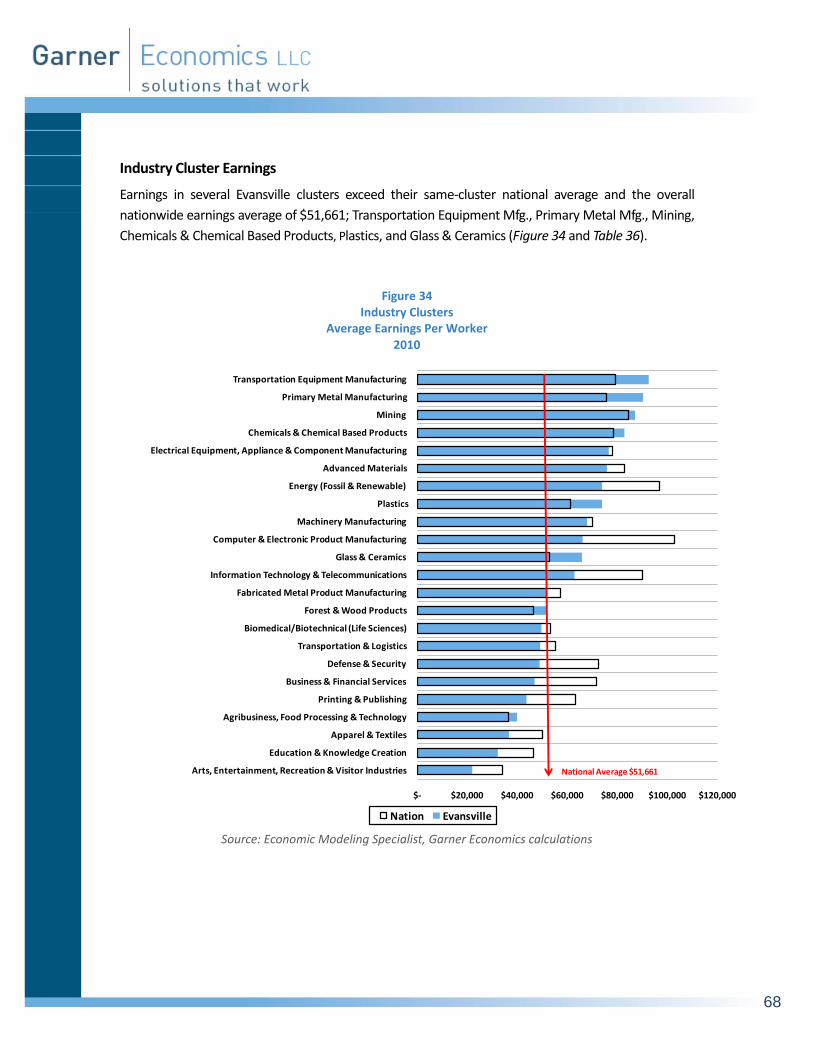

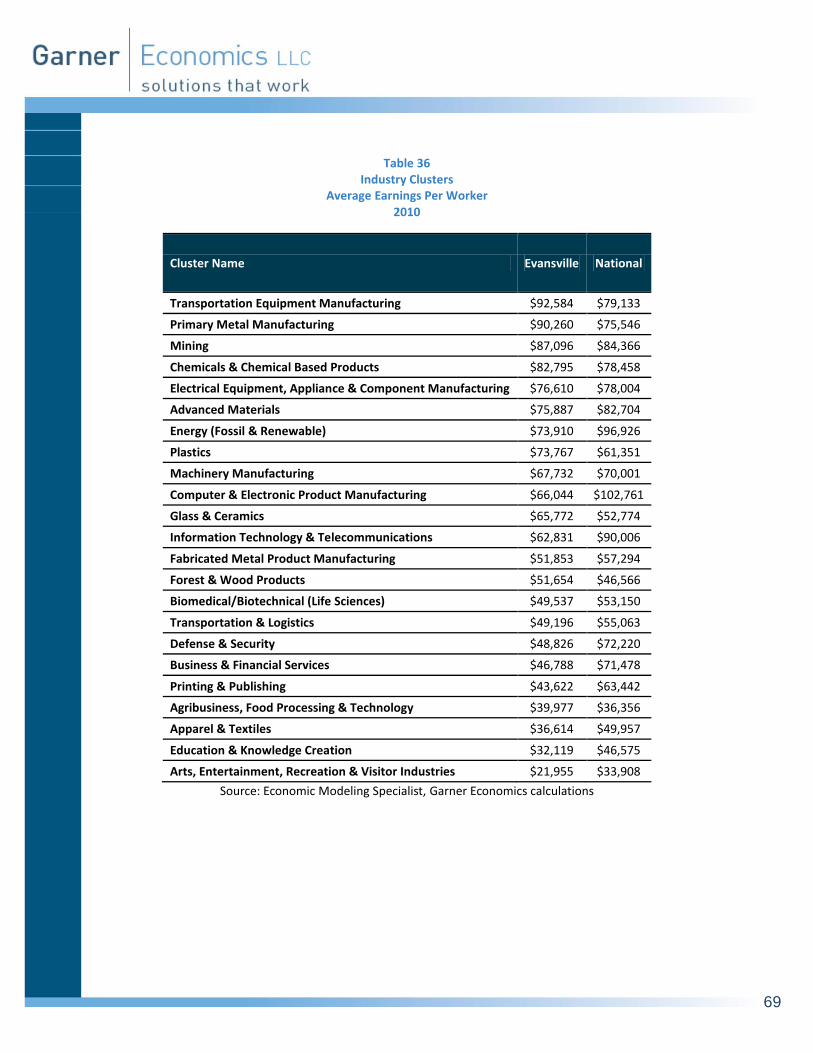

o Earnings in several Evansville clusters exceed their same-cluster national average and the overall nationwide earnings average of $51,661; Transportation Equipment Mfg., Primary Metal Mfg., Mining, Chemicals & Chemical Based Products, Plastics, and Glass & Ceramics.

opulation Growth

The rate of population growth can be a significant factor in local economic health, and is often

a key consideration in business expansion and site selection decisions. Most firms are wary of

areas with population declines, very slow growth rates, or significant amounts of domestic out-

migration

According to the just released 2010 decennial Census figures, the total population of the Evansville

metro equals 358,676. This marks an increase of 4.6 percent, or 15,861 over the last decade, a tepid

rate below the state, nation, and one benchmark community (Figure 1 and Table 1). Only the

Davenport-Moline-Rock Island metro has a lesser growth rate, equaling a mere one percent over the

decade.

P

18

Figure 1 2000-2010 Population Change

Source: US Census Bureau

Table 1 2000-2010 Population Change

2000 2010 Change Change %

Evansville 342,815 358,676 15,861 4.6%

Chattanooga 476,531 528,143 51,612 10.8%

Davenport-Moline—Rock Island 376,019 379,690 3,671 1.0%

Indiana 6,080,485 6,483,802 403,317 6.6%

US 281,421,906 308,745,538 27,323,632 9.7%

Source: US Census Bureau

ources of Population Change

Population change has three major sources: 1) natural (births minus deaths), 2) domestic

migration, and, 3) international migration1. The leading contributor to changes in Evansville

population is natural (Figure 1 andTable 1). Over the period of 2000-2009, natural growth accounted

1 Migration of the foreign born; lawful permanent residents (immigrants), temporary migrants (such as students), people illegally present in the United States, and additionally net movements of the Armed Forces population between the United States and overseas.

4.6%

10.8%

1.0%

6.6%

9.7%

0% 2% 4% 6% 8% 10% 12%

Evansville

Chattanooga

Davenport--Moline--Rock Island

Indiana

US

S

19

for an estimated 83 percent of net new residents. International in-migration was responsible for the

remaining 17 percent of net new residents. Over the same period, Evansville lost a net of 657 residents

due to domestic out-migration. Growth from natural and international sources, while positive, is less

likely to satisfy immediate workforce demands.

Compared to the benchmark communities, the contribution to net the population increase in

Chattanooga has been due overwhelmingly to domestic in-migration, while Davenport-Moline-Rock

Island’s slow growth is due to strong out-migration (Figure 3).

Figure 2 Annual Sources of Population Change

Evansville Metro

Source: US Census Bureau

-1,500

-1,000

-500

0

500

1,000

1,500

2,000

2,500

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Natural International Domestic

20

Table 2 Annual Sources of Population Change

Evansville Metro

Year Natural International Domestic

2000 193 38 (69)

2001 960 260 (891)

2002 747 249 154

2003 997 224 810

2004 1,102 221 347

2005 1,083 226 (62)

2006 1,082 228 34

2007 1,355 204 (185)

2008 1,159 198 (796)

2009 1,091 203 1

Components do not total exactly due to inter-year residual adjustments made by the Census Bureau.

Source: US Census Bureau

Figure 3 Net Source of Population Change

2000-2009 Estimate

Source: US Census Bureau

-20,000

-10,000

0

10,000

20,000

30,000

40,000

Evansville Chattanooga Davenport-Moline-Rock Island

Natural International Domestic

21

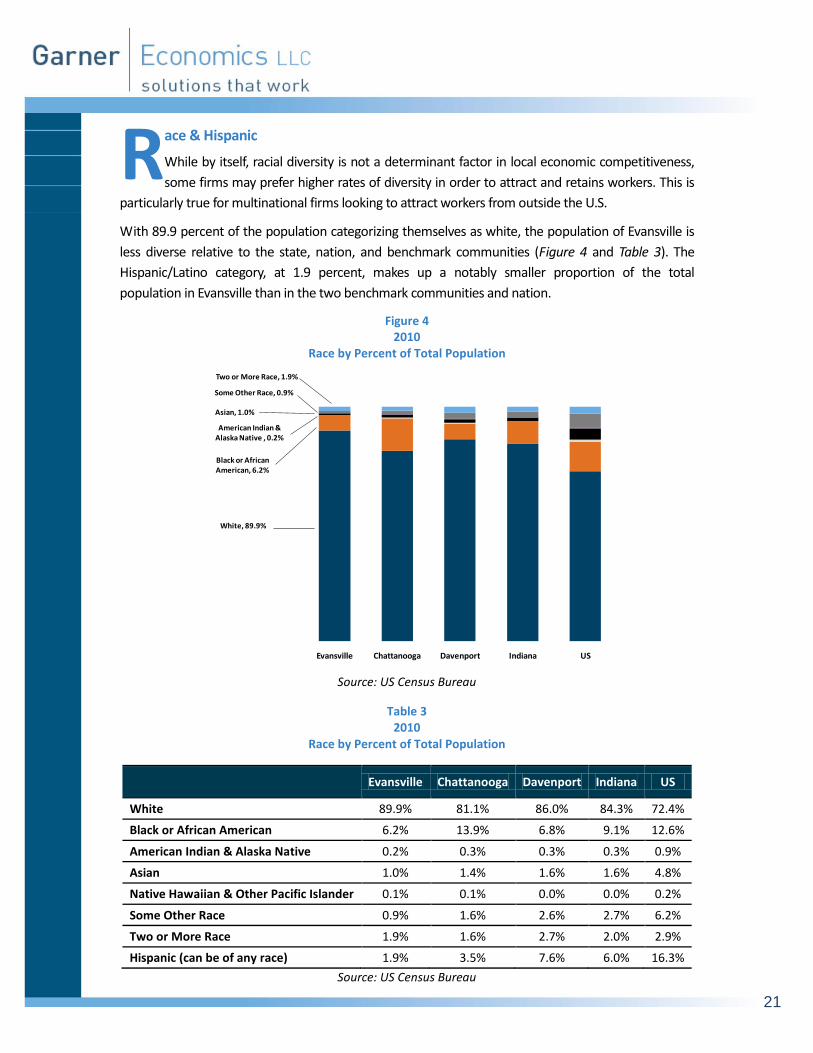

ace & Hispanic

While by itself, racial diversity is not a determinant factor in local economic competitiveness,

some firms may prefer higher rates of diversity in order to attract and retains workers. This is

particularly true for multinational firms looking to attract workers from outside the U.S.

With 89.9 percent of the population categorizing themselves as white, the population of Evansville is

less diverse relative to the state, nation, and benchmark communities (Figure 4 and Table 3). The

Hispanic/Latino category, at 1.9 percent, makes up a notably smaller proportion of the total

population in Evansville than in the two benchmark communities and nation.

Figure 4 2010

Race by Percent of Total Population

Source: US Census Bureau

Table 3 2010

Race by Percent of Total Population

Evansville Chattanooga Davenport Indiana US

White 89.9% 81.1% 86.0% 84.3% 72.4%

Black or African American 6.2% 13.9% 6.8% 9.1% 12.6%

American Indian & Alaska Native 0.2% 0.3% 0.3% 0.3% 0.9%

Asian 1.0% 1.4% 1.6% 1.6% 4.8%

Native Hawaiian & Other Pacific Islander 0.1% 0.1% 0.0% 0.0% 0.2%

Some Other Race 0.9% 1.6% 2.6% 2.7% 6.2%

Two or More Race 1.9% 1.6% 2.7% 2.0% 2.9%

Hispanic (can be of any race) 1.9% 3.5% 7.6% 6.0% 16.3%

Source: US Census Bureau

White, 89.9%

Black or African American, 6.2%

American Indian & Alaska Native , 0.2%

Asian, 1.0%

Some Other Race, 0.9%

Two or More Race, 1.9%

Evansville Chattanooga Davenport Indiana US

R

22

ge

The age composition of a local population can be an important determinant in business

decisions and competitiveness. The lack or underrepresentation of younger workers may

defer some firms from considering some communities for their long term plans. Low proportions of

middle age workers may prevent firms from initiating expansions requiring quick start-up operations.

The presence of older workers may indicate certain incumbent skills or the need to replace soon-to-

retire workers.

Median Age

At 38.5 years, the median age in Evansville is very close to the medians in both benchmark

communities, but approximately two years above the state and nation. (Figure 5 and Table 4).

Figure 5 Median Age 2005-2009

Source: US Census Bureau

Table 4

Median Age 2005-2009

Evansville 38.5

Chattanooga 38.6

Davenport-Moline—Rock Island 38.6

Indiana 36.4

US 36.5

Source: US Census Bureau

38.538.6 38.6

36.436.5

35

36

37

38

39

Evansville Chattanooga Davenport-Moline Rock Island

Indiana US

A

23

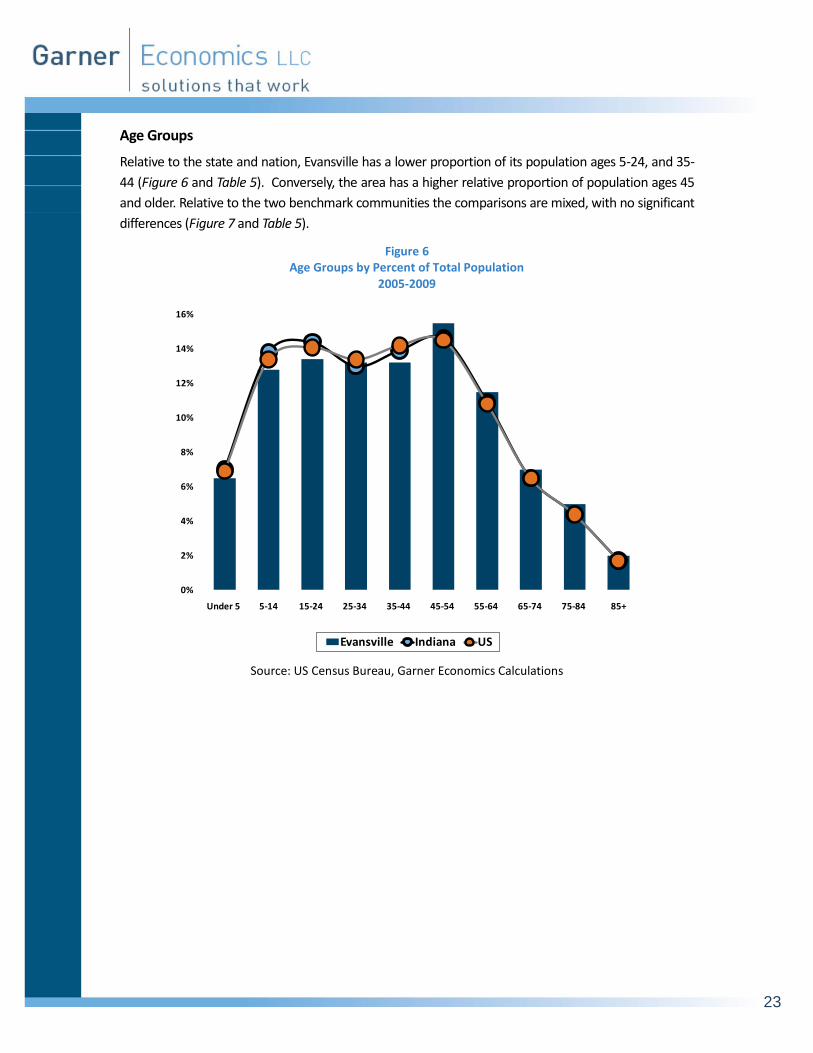

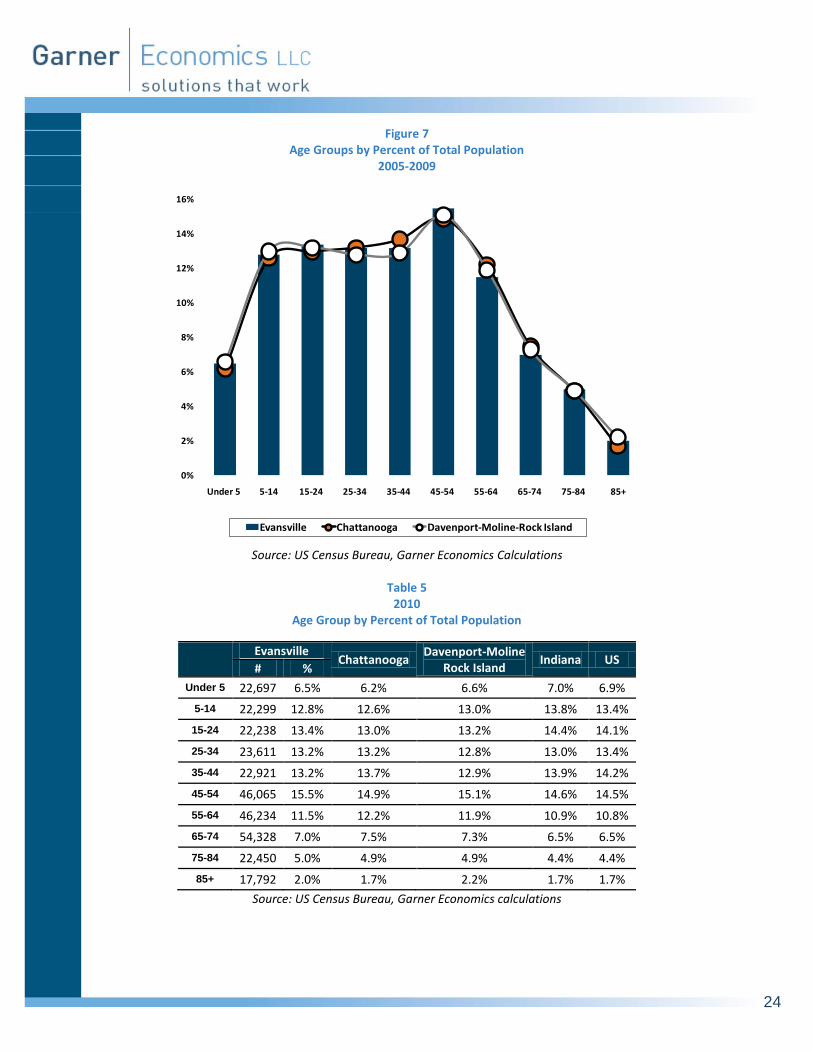

Age Groups

Relative to the state and nation, Evansville has a lower proportion of its population ages 5-24, and 35-

44 (Figure 6 and Table 5). Conversely, the area has a higher relative proportion of population ages 45

and older. Relative to the two benchmark communities the comparisons are mixed, with no significant

differences (Figure 7 and Table 5).

Figure 6 Age Groups by Percent of Total Population

2005-2009

Source: US Census Bureau, Garner Economics Calculations

0%

2%

4%

6%

8%

10%

12%

14%

16%

Under 5 5-14 15-24 25-34 35-44 45-54 55-64 65-74 75-84 85+

Evansville Indiana US

24

Figure 7 Age Groups by Percent of Total Population

2005-2009

Source: US Census Bureau, Garner Economics Calculations

Table 5 2010

Age Group by Percent of Total Population

Evansville

Chattanooga Davenport-Moline

Rock Island Indiana US

# %

Under 5 22,697 6.5% 6.2% 6.6% 7.0% 6.9%

5-14 22,299 12.8% 12.6% 13.0% 13.8% 13.4%

15-24 22,238 13.4% 13.0% 13.2% 14.4% 14.1%

25-34 23,611 13.2% 13.2% 12.8% 13.0% 13.4%

35-44 22,921 13.2% 13.7% 12.9% 13.9% 14.2%

45-54 46,065 15.5% 14.9% 15.1% 14.6% 14.5%

55-64 46,234 11.5% 12.2% 11.9% 10.9% 10.8%

65-74 54,328 7.0% 7.5% 7.3% 6.5% 6.5%

75-84 22,450 5.0% 4.9% 4.9% 4.4% 4.4%

85+ 17,792 2.0% 1.7% 2.2% 1.7% 1.7%

Source: US Census Bureau, Garner Economics calculations

0%

2%

4%

6%

8%

10%

12%

14%

16%

Under 5 5-14 15-24 25-34 35-44 45-54 55-64 65-74 75-84 85+

Evansville Chattanooga Davenport-Moline-Rock Island

25

ducation

Increasingly, the level of education of a communities’ population is becoming a decisive factor

in economic competitiveness. Firms understand the need to operate in economies that offer a

sufficient supply of workers that meet or exceed their demands. They also know that the lack of an

educated workforce can significantly affect business performance.

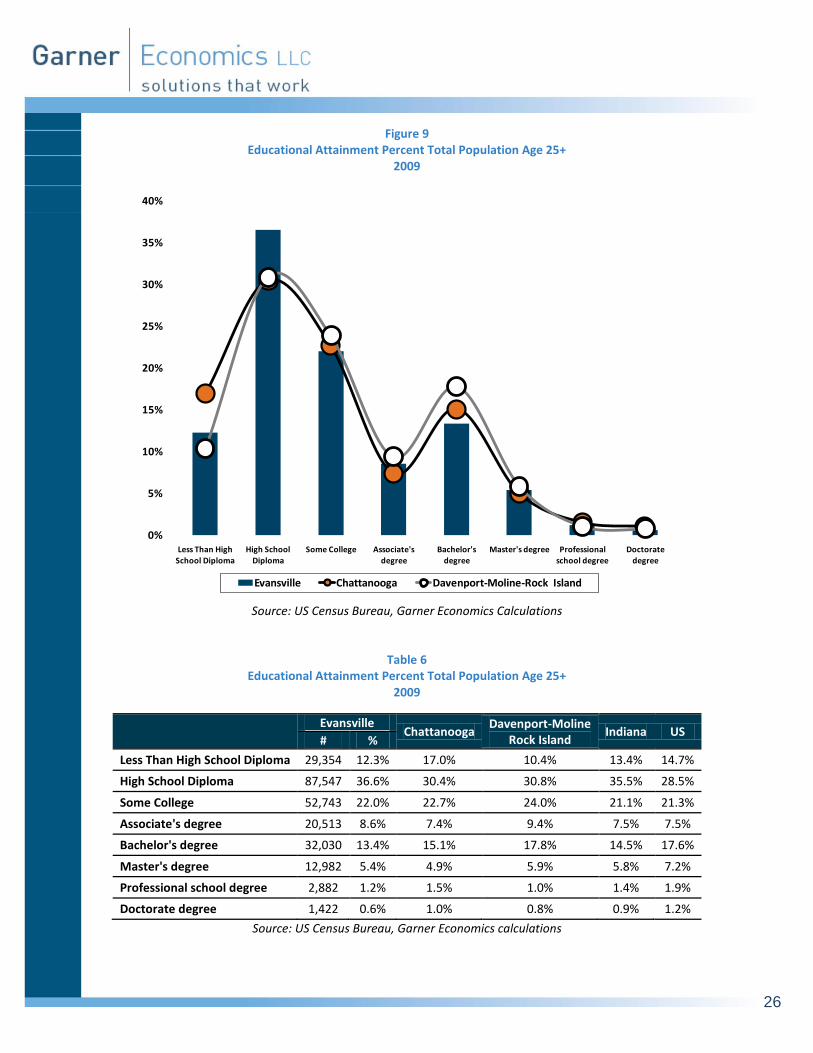

Educational Attainment

Comparing levels of educational attainment reveals several distinct characteristics among Evansville’s

residents ages 25 and over. Evansville has a higher relative proportion of residents whose highest level

of educational attainment is “High school diploma”, compared to the nation, state and both

benchmark communities. Likewise, Evansville has a lower relative proportion of residents whose

highest level of attainment is “Bachelor’s Degree” and above (Figure 8, Figure 9 and Table 6).

While the differences are not entirely striking, they may influence the attraction of firms demanding a

sizeable pool of highly educated workers, or cause firms to reconsider Evansville for large scale

research and development type operations.

Figure 8 Educational Attainment Percent Total Population Age 25+

2009

Source: US Census Bureau, Garner Economics calculations

0%

5%

10%

15%

20%

25%

30%

35%

40%

Less Than High School Diploma

High School Diploma

Some College Associate's degree

Bachelor's degree

Master's degree Professional school degree

Doctorate degree

Evansville Indiana US

E

26

Figure 9 Educational Attainment Percent Total Population Age 25+

2009

Source: US Census Bureau, Garner Economics Calculations

Table 6 Educational Attainment Percent Total Population Age 25+

2009

Evansville

Chattanooga Davenport-Moline

Rock Island Indiana US

# %

Less Than High School Diploma 29,354 12.3% 17.0% 10.4% 13.4% 14.7%

High School Diploma 87,547 36.6% 30.4% 30.8% 35.5% 28.5%

Some College 52,743 22.0% 22.7% 24.0% 21.1% 21.3%

Associate's degree 20,513 8.6% 7.4% 9.4% 7.5% 7.5%

Bachelor's degree 32,030 13.4% 15.1% 17.8% 14.5% 17.6%

Master's degree 12,982 5.4% 4.9% 5.9% 5.8% 7.2%

Professional school degree 2,882 1.2% 1.5% 1.0% 1.4% 1.9%

Doctorate degree 1,422 0.6% 1.0% 0.8% 0.9% 1.2%

Source: US Census Bureau, Garner Economics calculations

0%

5%

10%

15%

20%

25%

30%

35%

40%

Less Than High School Diploma

High School Diploma

Some College Associate's degree

Bachelor's degree

Master's degree Professional school degree

Doctorate degree

Evansville Chattanooga Davenport-Moline-Rock Island

27

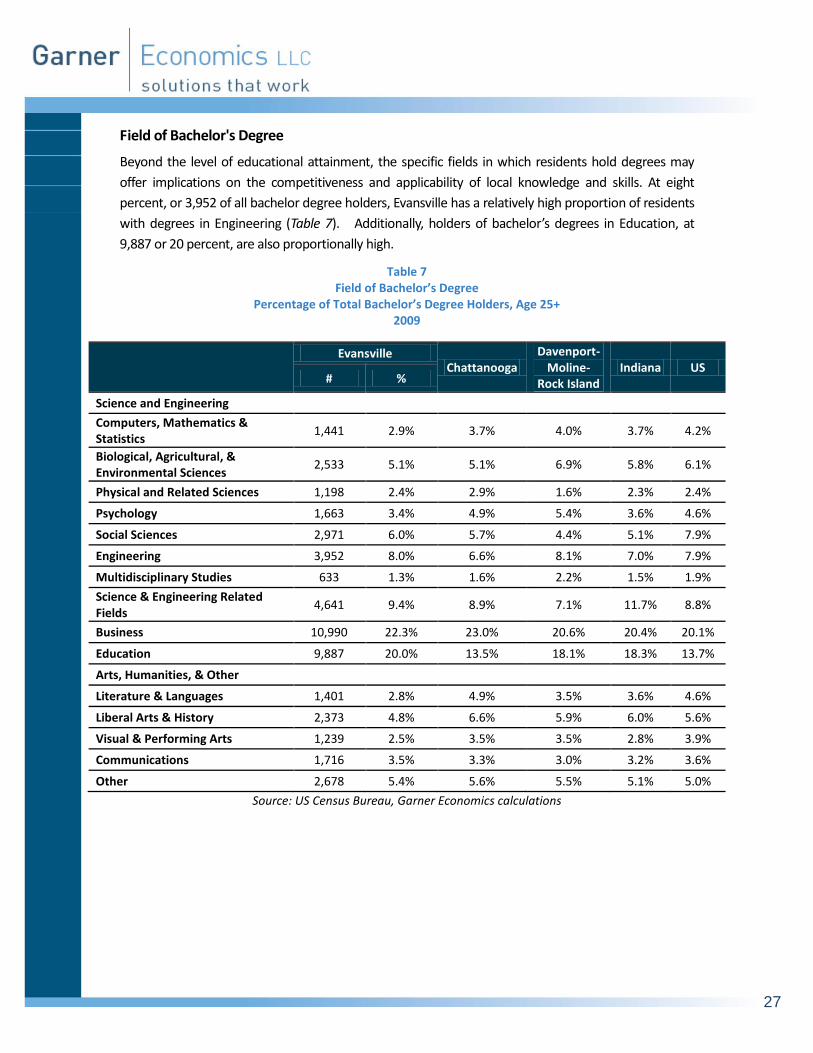

Field of Bachelor's Degree

Beyond the level of educational attainment, the specific fields in which residents hold degrees may

offer implications on the competitiveness and applicability of local knowledge and skills. At eight

percent, or 3,952 of all bachelor degree holders, Evansville has a relatively high proportion of residents

with degrees in Engineering (Table 7). Additionally, holders of bachelor’s degrees in Education, at

9,887 or 20 percent, are also proportionally high.

Table 7 Field of Bachelor’s Degree

Percentage of Total Bachelor’s Degree Holders, Age 25+ 2009

Evansville Chattanooga

Davenport-Moline-

Rock Island Indiana US

# %

Science and Engineering

Computers, Mathematics & Statistics

1,441 2.9% 3.7% 4.0% 3.7% 4.2%

Biological, Agricultural, & Environmental Sciences

2,533 5.1% 5.1% 6.9% 5.8% 6.1%

Physical and Related Sciences 1,198 2.4% 2.9% 1.6% 2.3% 2.4%

Psychology 1,663 3.4% 4.9% 5.4% 3.6% 4.6%

Social Sciences 2,971 6.0% 5.7% 4.4% 5.1% 7.9%

Engineering 3,952 8.0% 6.6% 8.1% 7.0% 7.9%

Multidisciplinary Studies 633 1.3% 1.6% 2.2% 1.5% 1.9%

Science & Engineering Related Fields

4,641 9.4% 8.9% 7.1% 11.7% 8.8%

Business 10,990 22.3% 23.0% 20.6% 20.4% 20.1%

Education 9,887 20.0% 13.5% 18.1% 18.3% 13.7%

Arts, Humanities, & Other

Literature & Languages 1,401 2.8% 4.9% 3.5% 3.6% 4.6%

Liberal Arts & History 2,373 4.8% 6.6% 5.9% 6.0% 5.6%

Visual & Performing Arts 1,239 2.5% 3.5% 3.5% 2.8% 3.9%

Communications 1,716 3.5% 3.3% 3.0% 3.2% 3.6%

Other 2,678 5.4% 5.6% 5.5% 5.1% 5.0%

Source: US Census Bureau, Garner Economics calculations

28

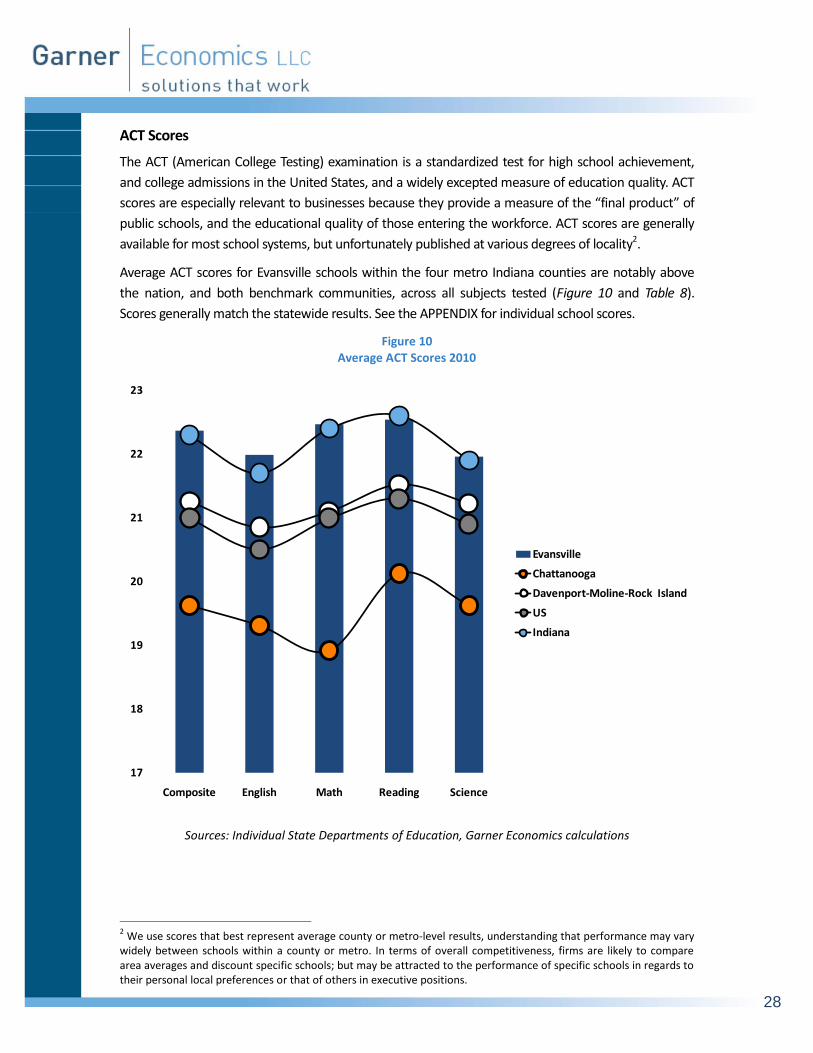

ACT Scores

The ACT (American College Testing) examination is a standardized test for high school achievement,

and college admissions in the United States, and a widely excepted measure of education quality. ACT

scores are especially relevant to businesses because they provide a measure of the “final product” of

public schools, and the educational quality of those entering the workforce. ACT scores are generally

available for most school systems, but unfortunately published at various degrees of locality2.

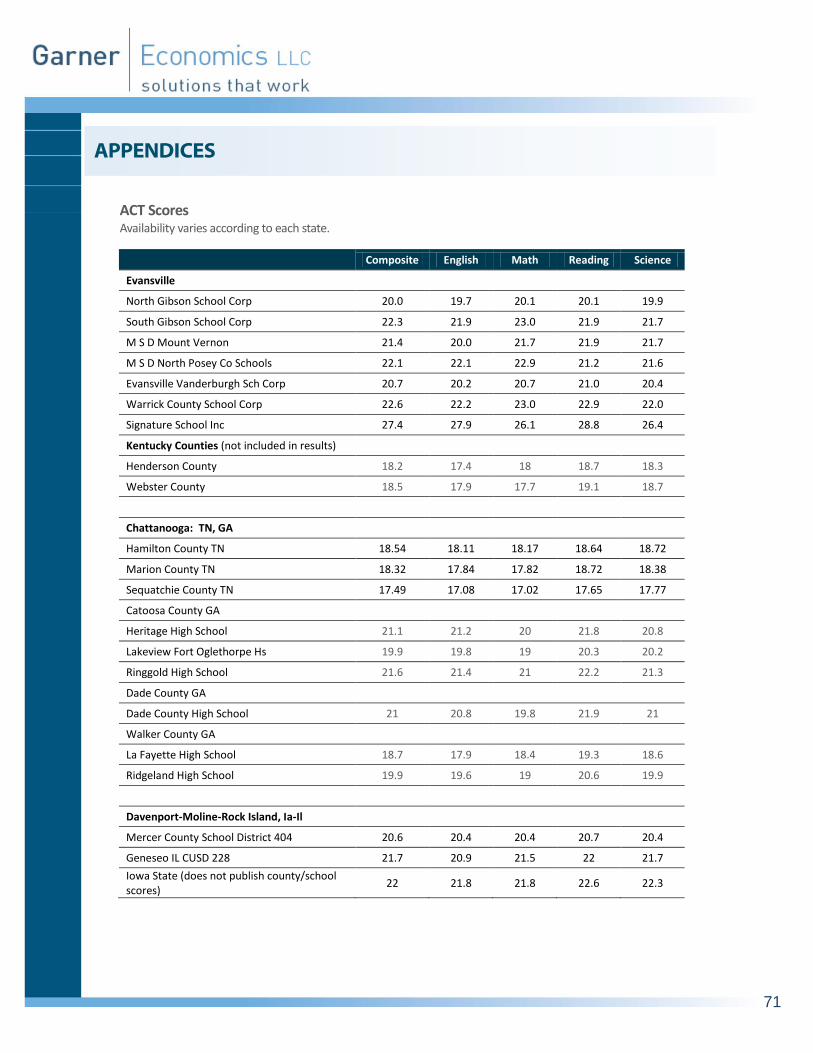

Average ACT scores for Evansville schools within the four metro Indiana counties are notably above

the nation, and both benchmark communities, across all subjects tested (Figure 10 and Table 8).

Scores generally match the statewide results. See the APPENDIX for individual school scores.

Figure 10 Average ACT Scores 2010

Sources: Individual State Departments of Education, Garner Economics calculations

2 We use scores that best represent average county or metro-level results, understanding that performance may vary

widely between schools within a county or metro. In terms of overall competitiveness, firms are likely to compare area averages and discount specific schools; but may be attracted to the performance of specific schools in regards to their personal local preferences or that of others in executive positions.

17

18

19

20

21

22

23

Composite English Math Reading Science

Evansville

Chattanooga

Davenport-Moline-Rock Island

US

Indiana

29

Table 8 Average ACT Scores 2010

Composite English Math Reading Science

Evansville (Indiana counties) 22.4 22.0 22.5 22.5 22.0

Chattanooga 19.6 19.3 18.9 20.1 19.6

Davenport-Moline-Rock Island 21.3 20.9 21.1 21.5 21.2

Indiana 22.3 21.7 22.4 22.6 21.9

US 21 20.5 21 21.3 20.9

Sources: Individual State Departments of Education, Garner Economics calculations

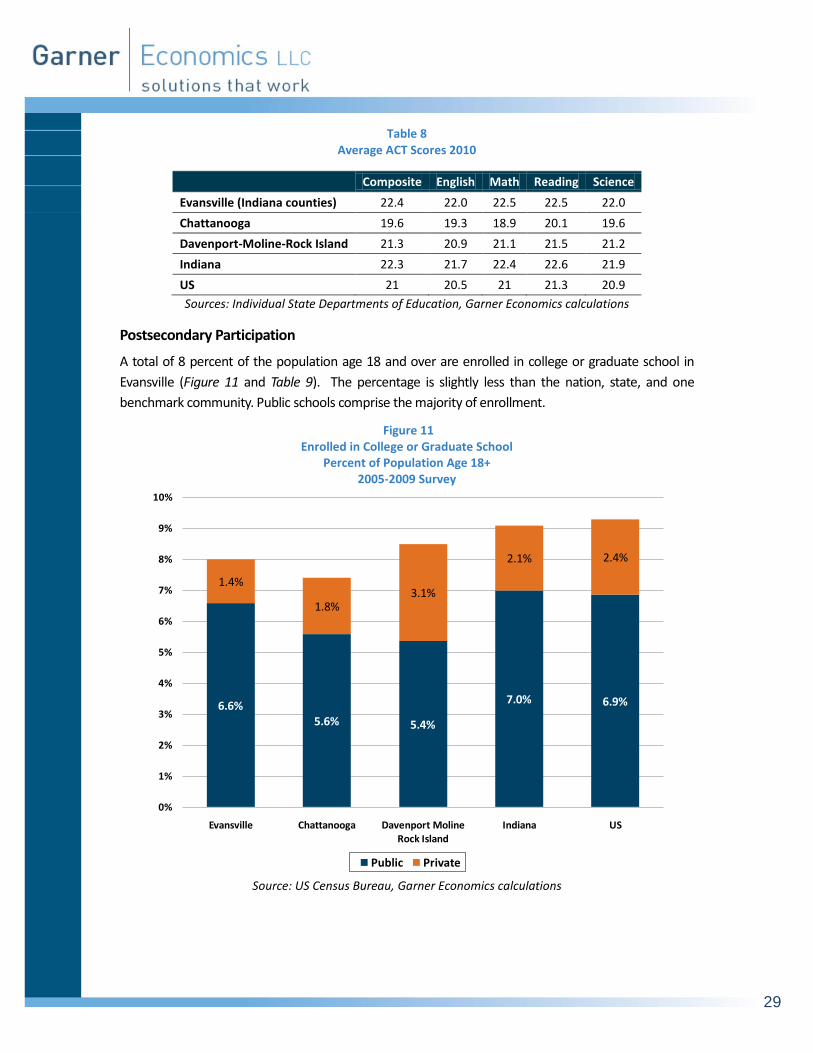

Postsecondary Participation

A total of 8 percent of the population age 18 and over are enrolled in college or graduate school in

Evansville (Figure 11 and Table 9). The percentage is slightly less than the nation, state, and one

benchmark community. Public schools comprise the majority of enrollment.

Figure 11 Enrolled in College or Graduate School

Percent of Population Age 18+ 2005-2009 Survey

Source: US Census Bureau, Garner Economics calculations

6.6%5.6% 5.4%

7.0% 6.9%

1.4%

1.8%3.1%

2.1% 2.4%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

Evansville Chattanooga Davenport Moline Rock Island

Indiana US

Public Private

30

Table 9 Enrolled in College or Graduate School

Percent of Population Age 18+ 2005-2009 Survey

Total Public Private

21,459 17,682 3,777

Evansville 8.0% 6.6% 1.4%

Chattanooga 7.4% 5.6% 1.8%

Davenport-Moline-Rock Island 8.5% 5.4% 3.1%

Indiana 9.1% 7.0% 2.1%

US 9.3% 6.9% 2.4%

Source: US Census Bureau, Garner Economics calculations

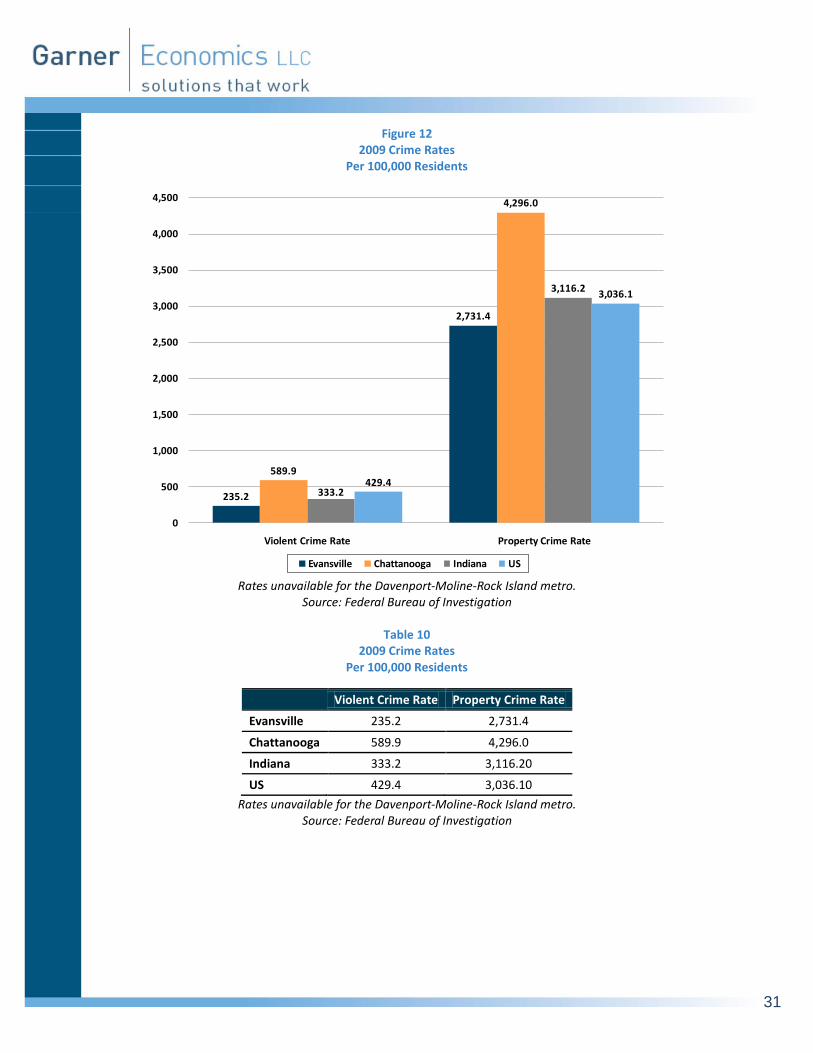

rime Rate

Crime rates may seem outside the typical measures of economic competitiveness, but they

represent a widely-accepted objective gauge used by firms. Crime rates generally reflect

underlying economic conditions, and may signal deeper systemic problems better than standard

economic measures.

According to the most current FBI data, 2009 Violent and Property crime rates in Evansville are below

the nation, state and one benchmark community (Figure 12 and Table 10). The FBI does not publish

rates for the Davenport-Moline-Rock Island metro.

C

31

Figure 12 2009 Crime Rates

Per 100,000 Residents

Rates unavailable for the Davenport-Moline-Rock Island metro.

Source: Federal Bureau of Investigation

Table 10 2009 Crime Rates

Per 100,000 Residents

Violent Crime Rate Property Crime Rate

Evansville 235.2 2,731.4

Chattanooga 589.9 4,296.0

Indiana 333.2 3,116.20

US 429.4 3,036.10

Rates unavailable for the Davenport-Moline-Rock Island metro. Source: Federal Bureau of Investigation

235.2

2,731.4

589.9

4,296.0

333.2

3,116.2

429.4

3,036.1

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

Violent Crime Rate Property Crime Rate

Evansville Chattanooga Indiana US

32

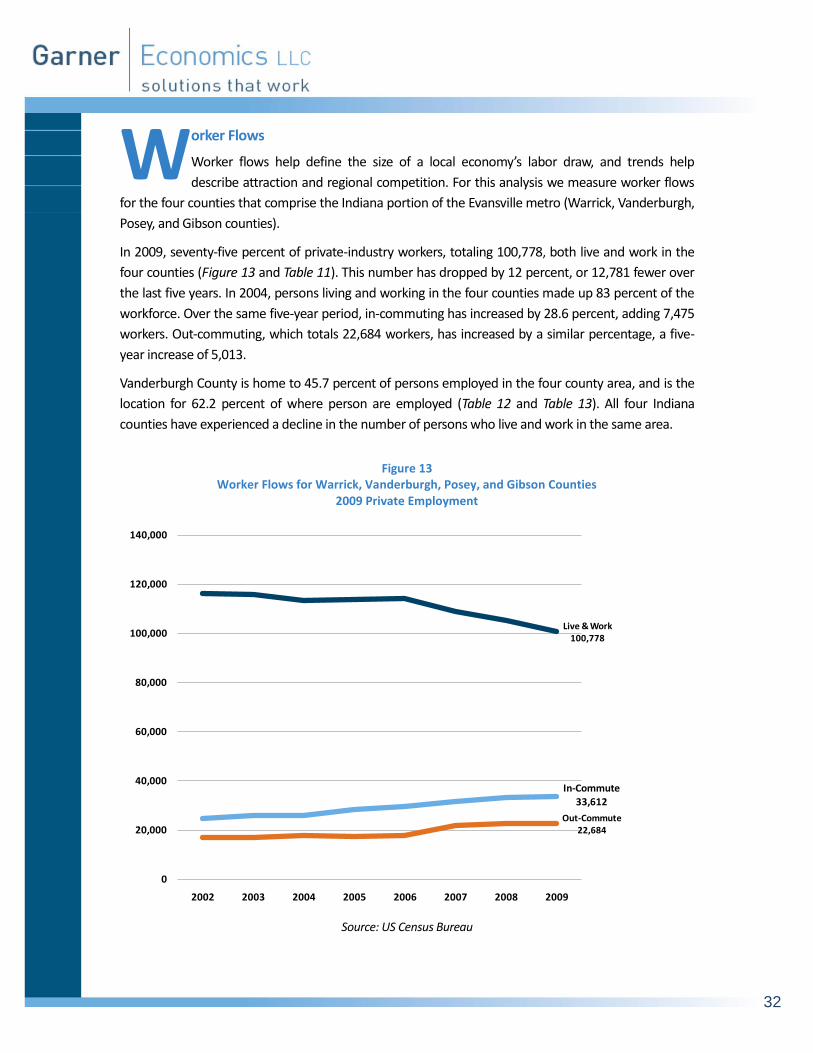

orker Flows

Worker flows help define the size of a local economy’s labor draw, and trends help

describe attraction and regional competition. For this analysis we measure worker flows

for the four counties that comprise the Indiana portion of the Evansville metro (Warrick, Vanderburgh,

Posey, and Gibson counties).

In 2009, seventy-five percent of private-industry workers, totaling 100,778, both live and work in the

four counties (Figure 13 and Table 11). This number has dropped by 12 percent, or 12,781 fewer over

the last five years. In 2004, persons living and working in the four counties made up 83 percent of the

workforce. Over the same five-year period, in-commuting has increased by 28.6 percent, adding 7,475

workers. Out-commuting, which totals 22,684 workers, has increased by a similar percentage, a five-

year increase of 5,013.

Vanderburgh County is home to 45.7 percent of persons employed in the four county area, and is the

location for 62.2 percent of where person are employed (Table 12 and Table 13). All four Indiana

counties have experienced a decline in the number of persons who live and work in the same area.

Figure 13

Worker Flows for Warrick, Vanderburgh, Posey, and Gibson Counties 2009 Private Employment

Source: US Census Bureau

Live & Work100,778

Out-Commute22,684

In-Commute33,612

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

2002 2003 2004 2005 2006 2007 2008 2009

W

33

Table 11 Worker Flows for Warrick, Vanderburgh, Posey, and Gibson Counties

Private Employment

2004 2009

5-Year Net

Change

5-Year Percent Change

Live & Work 113,559 100,778 (12,781) -11.3%

Out-Commute 17,671 22,684 5,013 28.4%

In-Commute 26,137 33,612 7,475 28.6%

Source: US Census Bureau, Garner Economics calculations

Table 12 Where Workers Live Who are Employed

in Warrick, Vanderburgh, Posey, and Gibson Counties 2009 Private Employment

Home

County Percent of

Total 5-Year Change

Vanderburgh IN 61,411 45.7% (11,056)

Warrick IN 20,037 14.9% (798)

Posey IN 9,681 7.2% (494)

Gibson IN 9,649 7.2% (433)

Henderson KY 3,792 2.8% (210)

Marion IN 2,679 2.0% 524

Spencer IN 2,056 1.5% 187

Dubois IN 1,783 1.3% 550

Pike IN 1,348 1.0% 322

Daviess KY 1,258 0.9% (30)

All Other Locations 20,696 15.4% 6,132

Source: US Census Bureau, Garner Economics calculations

34

SECTION 4: ECONOMIC DYNAMICS

Table 13 Where Workers are Employed Who Live in

Warrick, Vanderburgh, Posey, and Gibson Counties 2009 Private Employment

Source: US Census Bureau, Garner Economics calculations

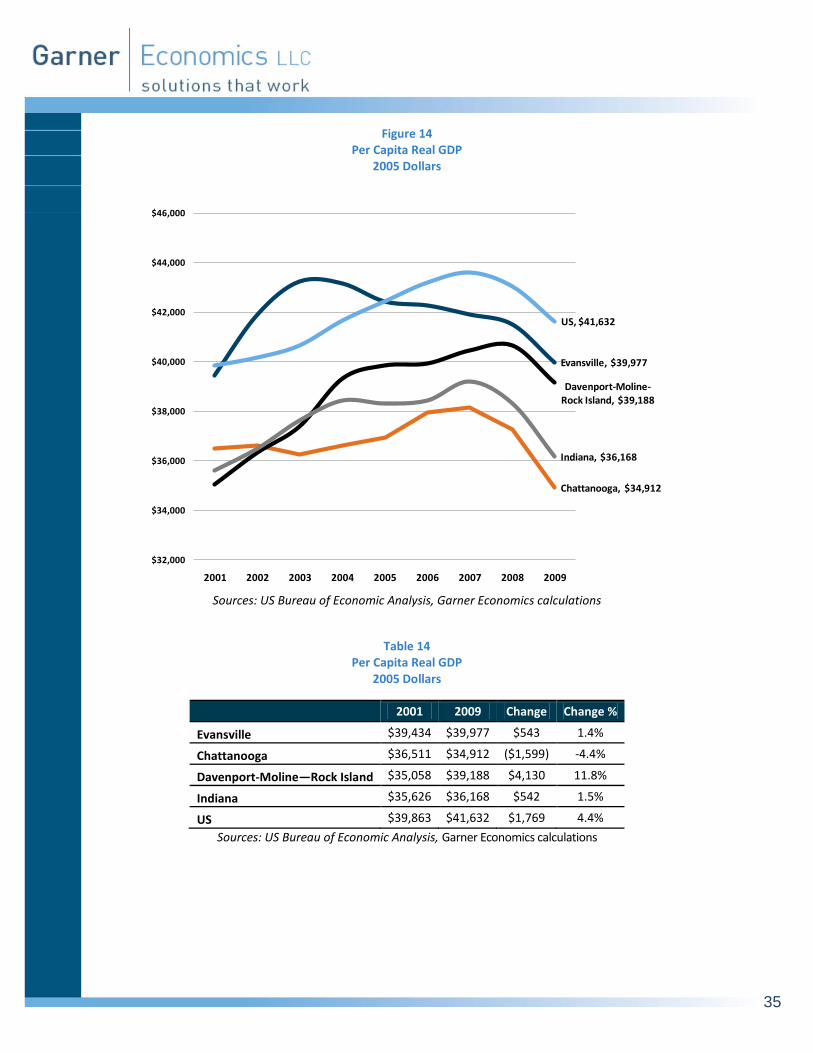

ross Domestic Product

Gross Domestic Product (GDP) is the most comprehensive measure of economic activity. GDP

for metro areas is derived as the sum of the GDP originating in all the industries in the area.

GDP for metro areas is only available for the years 2001-2009. In 2009, the inflation adjusted real GDP

for Evansville was $14,068 million. The figure was 3.3 percent below 2008, and mirrors a decline

experienced by 80 percent of all U.S. metros. Per capita real GDP has been declining in Evansville since

2003.

Measured in per capita terms, at $39,977 Evansville has a higher amount of economic activity than the

state, and the two benchmark communities. However, since 2004 per capita GDP in Evansville has

fallen below the nation (Figure 14 and Table 14).

Work

County Percent of

Total 5-Year Change

Vanderburgh IN 76,758 62.2% (9,787)

Warrick IN 9,376 7.6% (998)

Gibson IN 8,797 7.1% (1,162)

Posey IN 5,847 4.7% (834)

Marion IN 4,526 3.7% 1,739

Henderson KY 1,445 1.2% (301)

Dubois IN 1,279 1.0% (26)

Knox IN 959 0.8% 159

Hamilton IN 810 0.7% 433

Vigo IN 747 0.6% 26

All Other Locations 12,918 10.5% 2,983

G

35

Figure 14 Per Capita Real GDP

2005 Dollars

Sources: US Bureau of Economic Analysis, Garner Economics calculations

Table 14 Per Capita Real GDP

2005 Dollars

2001 2009 Change Change %

Evansville $39,434 $39,977 $543 1.4%

Chattanooga $36,511 $34,912 ($1,599) -4.4%

Davenport-Moline—Rock Island $35,058 $39,188 $4,130 11.8%

Indiana $35,626 $36,168 $542 1.5%

US $39,863 $41,632 $1,769 4.4%

Sources: US Bureau of Economic Analysis, Garner Economics calculations

Evansville, $39,977

Chattanooga, $34,912

Davenport-Moline-Rock Island, $39,188

Indiana, $36,168

US, $41,632

$32,000

$34,000

$36,000

$38,000

$40,000

$42,000

$44,000

$46,000

2001 2002 2003 2004 2005 2006 2007 2008 2009

36

xports

In a global economy, exports are playing a more critical role in local economic competitiveness.

Exporting has proven to be a powerful means to generate wealth, and provides evidence of an

area’s capacity to compete with firms outside the U.S.

As of 2009, Evansville had exports totaling $2,014,256,564. The figure is nearly 40 percent above 2008,

and marks a significant jump in export value over the last four years. Transportation equipment and

chemicals make up for the major exports from the area. In per capita terms, at $5,724, Evansville

exports are above the state, nation and one benchmark community (Figure 15 and Table 15).

Figure 15 Per Capita Exports

Sources: International Trade Administration, US Census Bureau, Garner Economics calculations

Table 15

Per Capita Exports

2005 2006 2007 2008 2009

Evansville $3,602 $3,318 $4,023 $4,112 $5,724

Chattanooga $1,074 $1,390 $1,569 $2,025 $1,260

Davenport-Moline—Rock Island $8,431 $9,116 $11,036 $13,940 $9,346

Indiana $3,453 $3,597 $4,090 $4,149 $3,566

US $3,047 $3,436 $3,807 $4,230 $3,440

Sources: International Trade Administration, US Census Bureau, Garner Economics calculations

Evansville, $5,724

Chattanooga, $1,260.22

Davenport-Moline-Rock Island, $9,346

Indiana, $3,566

US, $3,440

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

2005 2006 2007 2008 2009

E

37

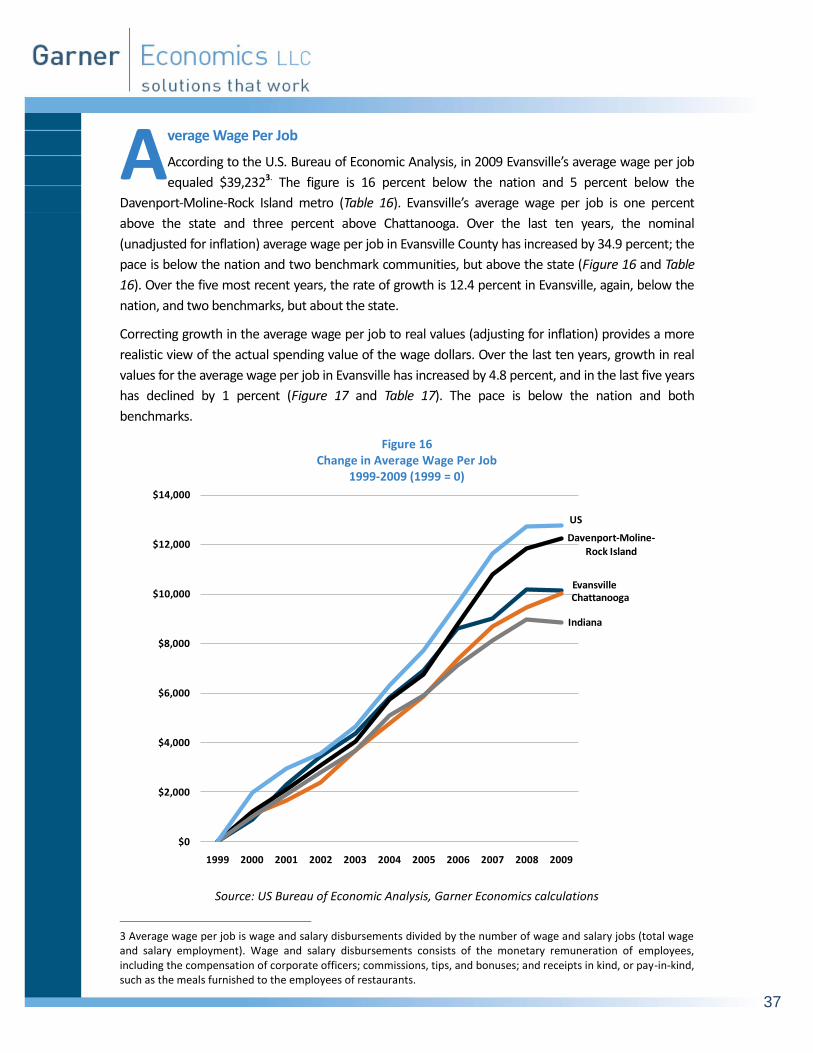

verage Wage Per Job

According to the U.S. Bureau of Economic Analysis, in 2009 Evansville’s average wage per job

equaled $39,2323. The figure is 16 percent below the nation and 5 percent below the

Davenport-Moline-Rock Island metro (Table 16). Evansville’s average wage per job is one percent

above the state and three percent above Chattanooga. Over the last ten years, the nominal

(unadjusted for inflation) average wage per job in Evansville County has increased by 34.9 percent; the

pace is below the nation and two benchmark communities, but above the state (Figure 16 and Table

16). Over the five most recent years, the rate of growth is 12.4 percent in Evansville, again, below the

nation, and two benchmarks, but about the state.

Correcting growth in the average wage per job to real values (adjusting for inflation) provides a more

realistic view of the actual spending value of the wage dollars. Over the last ten years, growth in real

values for the average wage per job in Evansville has increased by 4.8 percent, and in the last five years

has declined by 1 percent (Figure 17 and Table 17). The pace is below the nation and both

benchmarks.

Figure 16 Change in Average Wage Per Job

1999-2009 (1999 = 0)

Source: US Bureau of Economic Analysis, Garner Economics calculations

3 Average wage per job is wage and salary disbursements divided by the number of wage and salary jobs (total wage and salary employment). Wage and salary disbursements consists of the monetary remuneration of employees, including the compensation of corporate officers; commissions, tips, and bonuses; and receipts in kind, or pay-in-kind, such as the meals furnished to the employees of restaurants.

EvansvilleChattanooga

Davenport-Moline-Rock Island

Indiana

US

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

A

38

Table 16 Average Wage Per Job

2009

10-Year Net Change

10-Year Percent Change

5-Year Net Change

5-Year Percent Change

Evansville $39,232 $10,159 34.9% $4,340 12.4%

Chattanooga $38,017 $10,049 35.9% $5,271 16.1%

Davenport-Moline-Rock Island $41,265 $12,240 42.2% $6,495 18.7%

Indiana $38,809 $8,878 29.7% $3,778 10.8%

US $45,831 $12,760 38.6% $6,442 16.4%

Source: US Bureau of Economic Analysis, Garner Economics calculations

Figure 17 Change in Average Wage Per Job (Adjusted for Inflation)

1999-2009 (1999 = 0)

Source: US Bureau of Economic Analysis, Garner Economics calculations

Evansville

Chattanooga

Davenport-Moline-Rock Island

Indiana

US

-$500

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

39

Table 17 Average Wage Per Job Trends

Adjusted for Inflation (1999 = 0)

10-Year

Net Change

10-Year Percent Change

5-Year Net Change

5-Year Percent Change

Evansville $1,393 4.8% ($307) -1.0%

Chattanooga $1,554 5.6% $642 2.2%

Davenport-Moline-Rock Island $3,020 10.4% $1,379 4.5%

Indiana $206 0.7% ($758) -2.5%

US $2,519 7.6% $851 2.5%

Source: US Bureau of Economic Analysis, Garner Economics calculations

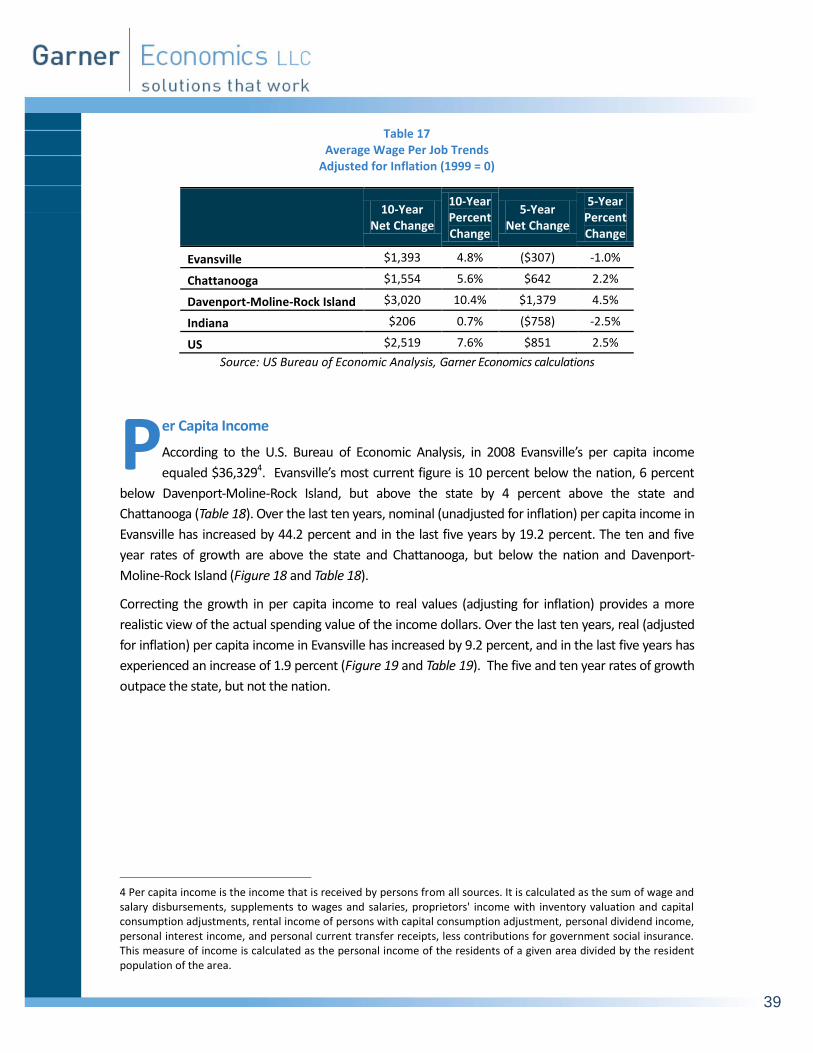

er Capita Income

According to the U.S. Bureau of Economic Analysis, in 2008 Evansville’s per capita income

equaled $36,3294. Evansville’s most current figure is 10 percent below the nation, 6 percent

below Davenport-Moline-Rock Island, but above the state by 4 percent above the state and

Chattanooga (Table 18). Over the last ten years, nominal (unadjusted for inflation) per capita income in

Evansville has increased by 44.2 percent and in the last five years by 19.2 percent. The ten and five

year rates of growth are above the state and Chattanooga, but below the nation and Davenport-

Moline-Rock Island (Figure 18 and Table 18).

Correcting the growth in per capita income to real values (adjusting for inflation) provides a more

realistic view of the actual spending value of the income dollars. Over the last ten years, real (adjusted

for inflation) per capita income in Evansville has increased by 9.2 percent, and in the last five years has

experienced an increase of 1.9 percent (Figure 19 and Table 19). The five and ten year rates of growth

outpace the state, but not the nation.

4 Per capita income is the income that is received by persons from all sources. It is calculated as the sum of wage and salary disbursements, supplements to wages and salaries, proprietors' income with inventory valuation and capital consumption adjustments, rental income of persons with capital consumption adjustment, personal dividend income, personal interest income, and personal current transfer receipts, less contributions for government social insurance. This measure of income is calculated as the personal income of the residents of a given area divided by the resident population of the area.

P

40

Figure 18 Change in Per Capita Income

1998-2008 (1998 = 0)

Source: US Bureau of Economic Analysis, Garner Economics calculations

Table 18

Per Capita Income

2008

10-Year Net Change

10-Year Percent Change

5-Year Net Change

5-Year Percent Change

Evansville $36,329 $11,134 44.2% $5,850 19.2%

Chattanooga $34,784 $10,189 41.4% $5,613 19.2%

Davenport-Moline-Rock Island $38,571 $12,588 48.4% $8,276 27.3%

Indiana $34,543 $9,374 37.2% $4,970 16.8%

US $40,166 $12,908 47.4% $7,895 24.5%

Source: US Bureau of Economic Analysis, Garner Economics calculations

Evansville

Chattanooga

Davenport-Moline-Rock Island

Indiana

US

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

41

Figure 19 Change in Per Capita Income (Adjusted for Inflation)

1998-2008 (1998 = 0)

Source: US Bureau of Economic Analysis, Garner Economics calculations

Table 19 Per Capita Income Trends

Adjusted for Inflation (1998 = 0)

10-Year

Net Change

10-Year Percent Change

5-Year Net Change

5-Year Percent Change

Evansville $2,309 9.2% $503 1.9%

Chattanooga $1,739 7.1% $492 1.9%

Davenport-Moline-Rock Island $3,218 12.4% $2,364 8.8%

Indiana $983 3.9% ($46) -0.2%

US $3,151 11.6% $1,821 6.4%

Source: US Bureau of Economic Analysis, Garner Economics calculations

Evansville

Chattanooga

Davenport-Moline-Rock Island

Indiana

US

-$500

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

$4,000

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

42

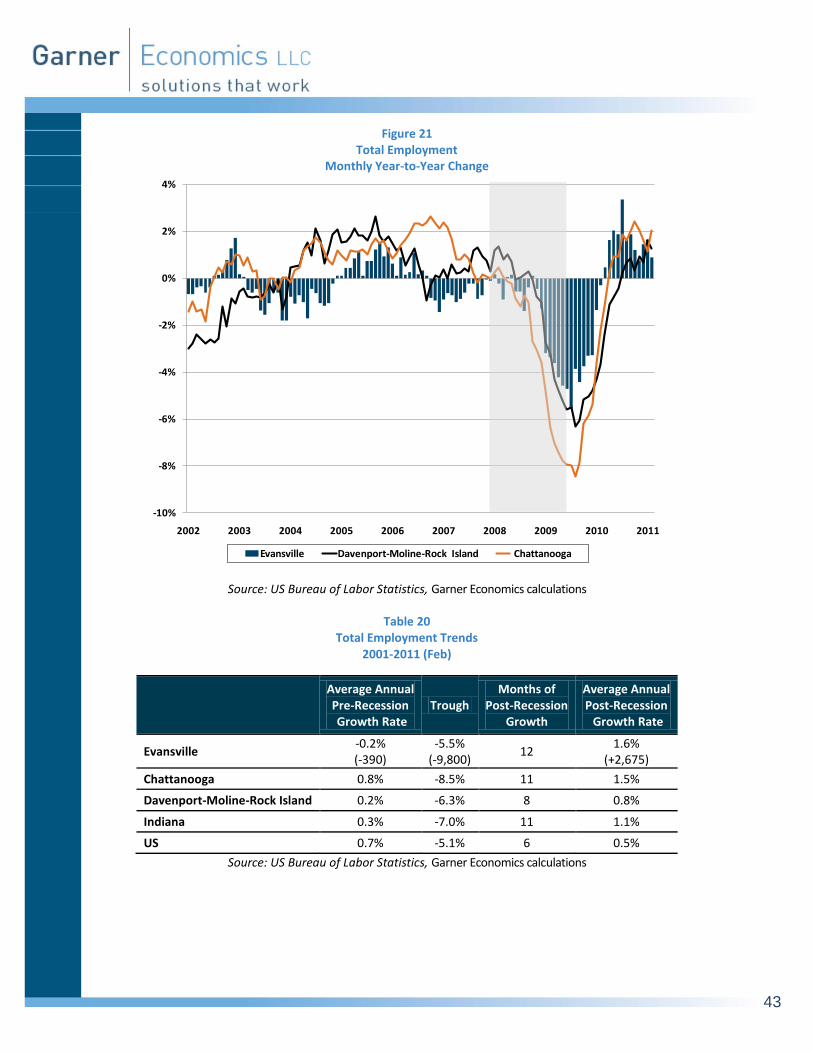

otal Employment

Through February 2011, Evansville has experienced 12 straight months of year-to-year

employment growth (Figure 20, Figure 21 and Table 20). The current pace of job growth is

averaging 1.6 percent, or an annual increase of 2,675 net new jobs. Evansville current pace of growth

is greater than the nation, state and both benchmark communities. At its lowest point, Evansville was

down 9,800 jobs, or -5.5 percent, just one month past the official end of the recent recession.5

Figure 20 Total Employment

Monthly Year-to-Year Change

Source: US Bureau of Labor Statistics, Garner Economics calculations

5 The recession is officially dated as beginning December 2007 and ending June 2009.

-8%

-6%

-4%

-2%

0%

2%

4%

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Evansville Indiana US

T

43

Figure 21 Total Employment

Monthly Year-to-Year Change

Source: US Bureau of Labor Statistics, Garner Economics calculations

Table 20 Total Employment Trends

2001-2011 (Feb)

Average Annual Pre-Recession Growth Rate

Trough Months of

Post-Recession Growth

Average Annual Post-Recession Growth Rate

Evansville -0.2% (-390)

-5.5% (-9,800)

12 1.6%

(+2,675)

Chattanooga 0.8% -8.5% 11 1.5%

Davenport-Moline-Rock Island 0.2% -6.3% 8 0.8%

Indiana 0.3% -7.0% 11 1.1%

US 0.7% -5.1% 6 0.5%

Source: US Bureau of Labor Statistics, Garner Economics calculations

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Evansville Davenport-Moline-Rock Island Chattanooga

44

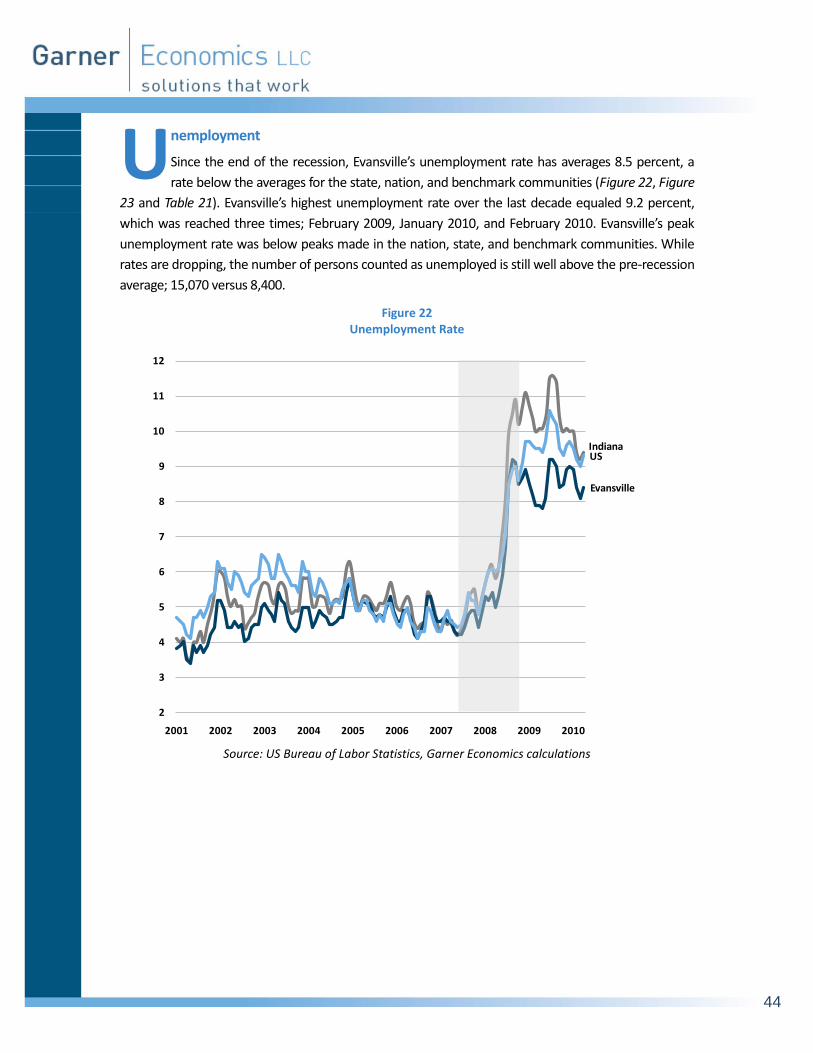

nemployment

Since the end of the recession, Evansville’s unemployment rate has averages 8.5 percent, a

rate below the averages for the state, nation, and benchmark communities (Figure 22, Figure

23 and Table 21). Evansville’s highest unemployment rate over the last decade equaled 9.2 percent,

which was reached three times; February 2009, January 2010, and February 2010. Evansville’s peak

unemployment rate was below peaks made in the nation, state, and benchmark communities. While

rates are dropping, the number of persons counted as unemployed is still well above the pre-recession

average; 15,070 versus 8,400.

Figure 22 Unemployment Rate

Source: US Bureau of Labor Statistics, Garner Economics calculations

Indiana

Evansville

US

2

3

4

5

6

7

8

9

10

11

12

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

U

45

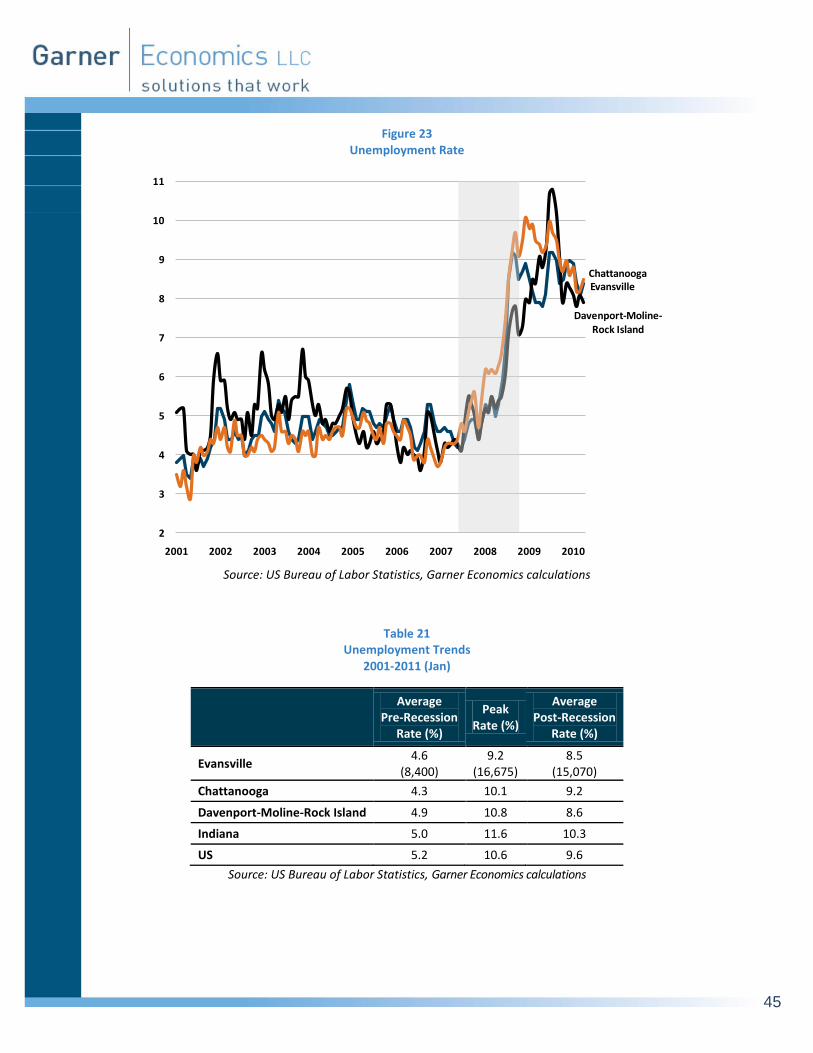

Figure 23 Unemployment Rate

Source: US Bureau of Labor Statistics, Garner Economics calculations

Table 21 Unemployment Trends

2001-2011 (Jan)

Average Pre-Recession

Rate (%)

Peak Rate (%)

Average Post-Recession

Rate (%)

Evansville 4.6

(8,400) 9.2

(16,675) 8.5

(15,070)

Chattanooga 4.3 10.1 9.2

Davenport-Moline-Rock Island 4.9 10.8 8.6

Indiana 5.0 11.6 10.3

US 5.2 10.6 9.6

Source: US Bureau of Labor Statistics, Garner Economics calculations

Evansville

Davenport-Moline-Rock Island

Chattanooga

2

3

4

5

6

7

8

9

10

11

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

46

ajor Industry Sector Composition

A comparison of major industry composition provides a broad relative assessment of

differences among economies, and may help indicate areas of uniqueness. Generally,

Evansville has a relatively higher proportion of employment in Construction, Manufacturing, Private

Education and Health Services (Table 22). Conversely, the area has a lower relative proportion of

employment in Financial Activities, and Federal, State and Local Government. A much more detailed

analysis of Evansville’s industrial, occupational, and cluster specialization relative to the nation can be

found in Section 5.

Table 22 Percentage of Employment by Sector

September 2010

Evansville Chattanooga

Davenport-Moline

Rock Island Indiana US

# %

Natural Resources & Mining 2,063 1.2% 0.1% 0.7% 0.8% 1.5%

Construction 10,459 6.3% 4.0% 5.7% 4.4% 4.4%

Manufacturing 27,575 16.6% 13.1% 15.3% 16.6% 9.0%

Information 2,320 1.4% 1.5% 1.8% 1.3% 2.1%

Financial Activities 5,556 3.3% 7.4% 5.3% 4.5% 5.7%

Professional & Business Services 18,732 11.3% 9.2% 14.1% 10.2% 13.1%

Leisure & Hospitality 16,707 10.0% 10.9% 11.8% 10.2% 10.3%

Trade, Transportation, & Utilities 32,440 19.5% 21.5% 24.5% 19.6% 19.0%

Private Education & Health Services 27,576 16.6% 13.4% 16.8% 14.5% 14.5%

Total Private 148,780 89.4% 84.2% na 85.1% 83.3%

Total Government 17,575 10.6% 15.8% na 14.9% 16.7%

Federal Government 1,336 0.8% 2.8% na 1.4% 2.2%

State Government 3,249 2.0% 2.2% na 3.3% 3.6%

Local Government 12,990 7.8% 10.8% na 10.2% 10.8%

Source: US Bureau of Labor Statistics, Garner Economics calculations

M

47

rivate Business Establishments

Tracking the growth and decline in the number of private business establishments is a broad

indicator of economic vitality and dynamism. Over the nine most current years of data

available, Evansville has experienced subpar establishment activity, down over the entire 9 year period

by 2 percent, and up just 0.5 percent over the last five years (Figure 24 and Table 23). The rates are

below the nation, state, and one benchmark community.

Figure 24 Change in the Number of Private Business Establishments

2001 (3Q) - 2010 (3Q)

Source: US Bureau of Labor Statistics, Garner Economics calculations

Table 23 Private Business Establishments

2010 (3Q)

9-Year Net

Change

9-Year %

Change

5-Year Net

Change

5-Year %

Change

Evansville 8,228 (147) -1.8% 40 0.5%

Chattanooga 10,649 801 8.1% (82) -0.8%

Davenport-Moline-Rock Island 9,736 457 4.9% 189 2.0%

Indiana 151,190 4,744 3.2% 2,783 1.9%

US 8,746,332 997,988 12.9% 409,355 4.9%

Source: US Bureau of Labor Statistics, Garner Economics calculations

13%

3%

5%

8%

-2%

5%

2%

2%

-1%

0%

-2% 0% 2% 4% 6% 8% 10% 12% 14%

US

Indiana

Davenport-Moline-Rock Island

Chattanooga

Evansville

5-Year 9-Year

P

48

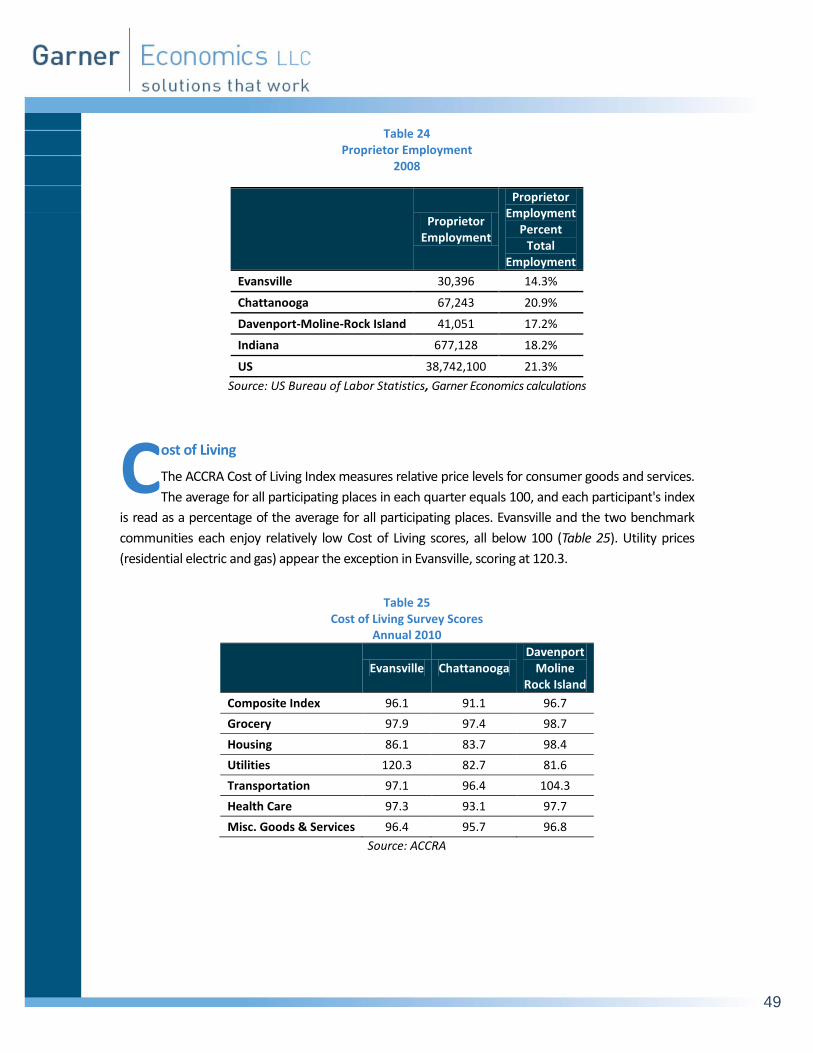

roprietor Employment

Measuring the relative proportion of proprietor employment is a means to gauge

entrepreneurial activity, which in turn provides a view of local risk-taking and dynamism.

According to the U.S. Bureau of Economic Analysis, as of 2008, proprietors accounted for 14.3 percent

of total employment in Evansville (Figure 25 and Table 24). The percentage is less than in the nation,

state or both benchmark communities.

Figure 25 Proprietor Employment as a Percent of Total Employment

2008

Source: US Bureau of Economic Analysis, Garner Economics calculations

14.3%

20.9%

17.2%18.2%

21.3%

0%

5%

10%

15%

20%

25%

Evansville Chattanooga Davenport-Moline Rock Island

Indiana US

P

49

Table 24 Proprietor Employment

2008

Proprietor

Employment

Proprietor Employment

Percent Total

Employment

Evansville 30,396 14.3%

Chattanooga 67,243 20.9%

Davenport-Moline-Rock Island 41,051 17.2%

Indiana 677,128 18.2%

US 38,742,100 21.3%

Source: US Bureau of Labor Statistics, Garner Economics calculations

ost of Living

The ACCRA Cost of Living Index measures relative price levels for consumer goods and services.

The average for all participating places in each quarter equals 100, and each participant's index

is read as a percentage of the average for all participating places. Evansville and the two benchmark

communities each enjoy relatively low Cost of Living scores, all below 100 (Table 25). Utility prices

(residential electric and gas) appear the exception in Evansville, scoring at 120.3.

Table 25

Cost of Living Survey Scores Annual 2010

Evansville Chattanooga

Davenport Moline

Rock Island

Composite Index 96.1 91.1 96.7

Grocery 97.9 97.4 98.7

Housing 86.1 83.7 98.4

Utilities 120.3 82.7 81.6

Transportation 97.1 96.4 104.3

Health Care 97.3 93.1 97.7

Misc. Goods & Services 96.4 95.7 96.8

Source: ACCRA

C

50

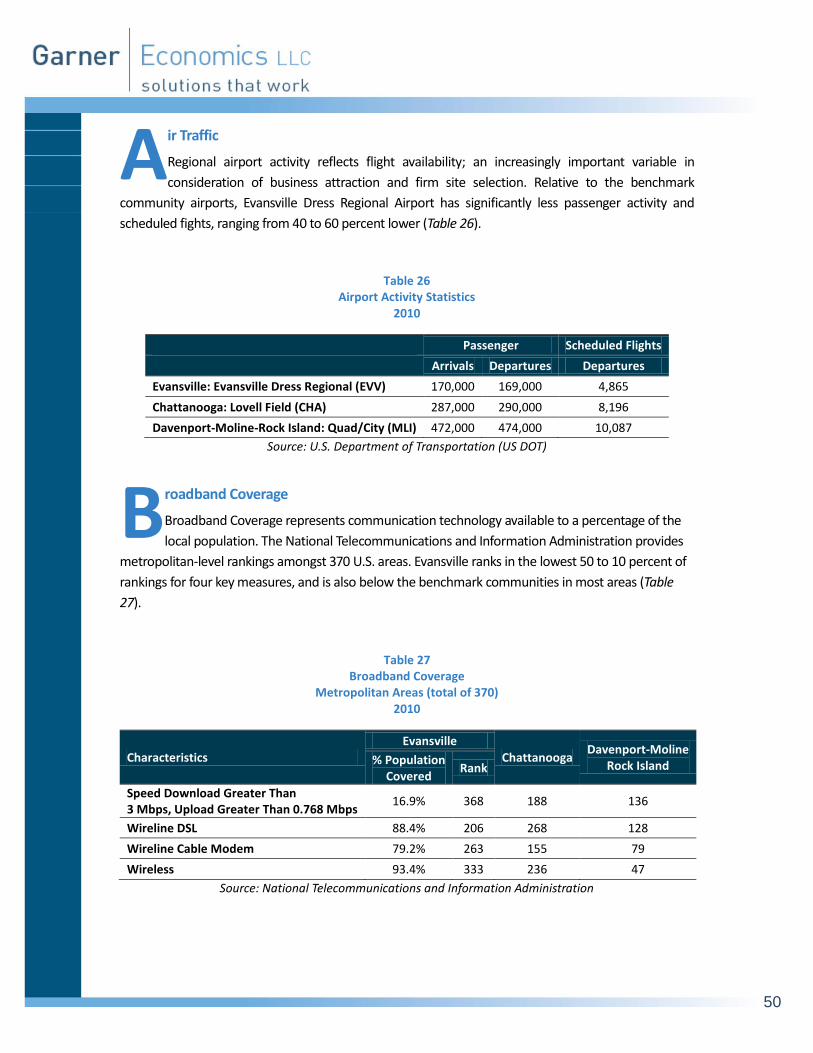

ir Traffic

Regional airport activity reflects flight availability; an increasingly important variable in

consideration of business attraction and firm site selection. Relative to the benchmark

community airports, Evansville Dress Regional Airport has significantly less passenger activity and

scheduled fights, ranging from 40 to 60 percent lower (Table 26).

Table 26 Airport Activity Statistics

2010

Passenger Scheduled Flights

Arrivals Departures Departures

Evansville: Evansville Dress Regional (EVV) 170,000 169,000 4,865

Chattanooga: Lovell Field (CHA) 287,000 290,000 8,196

Davenport-Moline-Rock Island: Quad/City (MLI) 472,000 474,000 10,087

Source: U.S. Department of Transportation (US DOT)

roadband Coverage

Broadband Coverage represents communication technology available to a percentage of the

local population. The National Telecommunications and Information Administration provides

metropolitan-level rankings amongst 370 U.S. areas. Evansville ranks in the lowest 50 to 10 percent of

rankings for four key measures, and is also below the benchmark communities in most areas (Table

27).

Table 27 Broadband Coverage

Metropolitan Areas (total of 370) 2010

Characteristics

Evansville

Chattanooga Davenport-Moline

Rock Island % Population Covered

Rank

Speed Download Greater Than 3 Mbps, Upload Greater Than 0.768 Mbps

16.9% 368 188 136

Wireline DSL 88.4% 206 268 128

Wireline Cable Modem 79.2% 263 155 79

Wireless 93.4% 333 236 47

Source: National Telecommunications and Information Administration

A

B

51

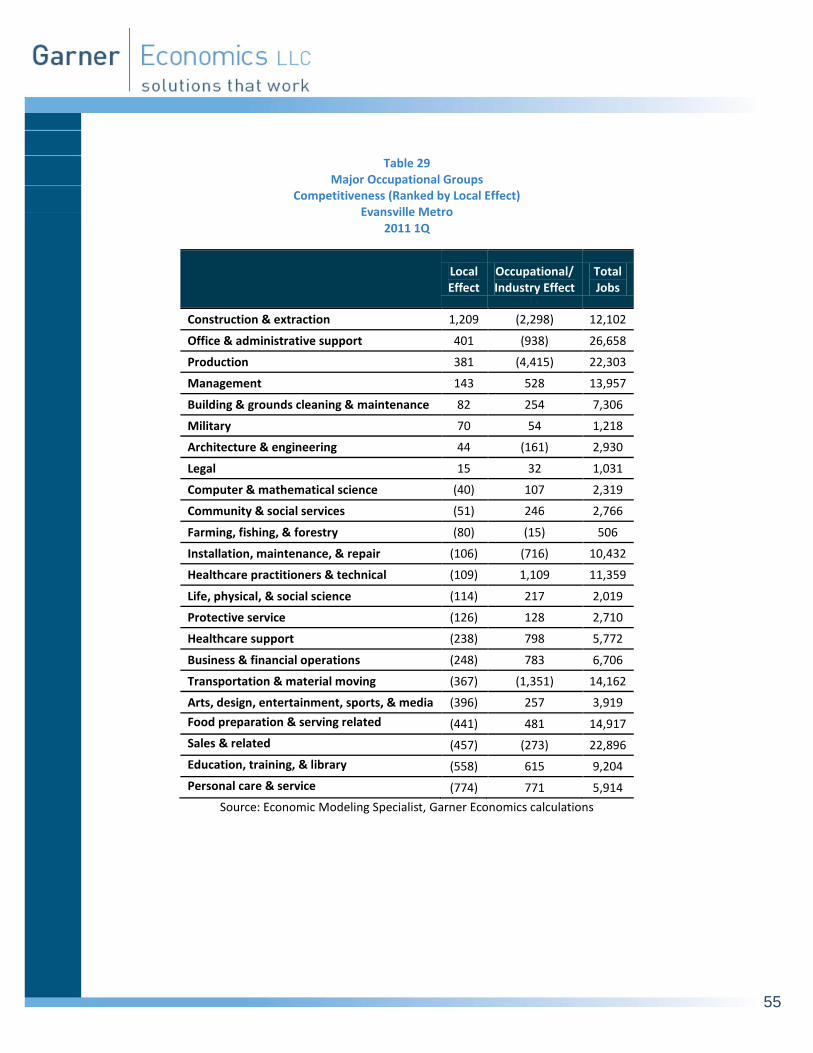

SECTION 5: LOCAL SPECIALIZATION, COMPETITIVENESS & GROWTH

he following section provides a detailed and objective assessment of the Evansville economy.

The analysis examines the local economy from several different perspectives, each adding a

supporting layer of information. The assessment’s main goals are to provide historic context,

reveal areas of unique specialization, gauge competitiveness, and help uncover emerging trends and

opportunities.

The three main subjects of analysis are: occupations, major industries, and industry clusters. For each

area there are relative measures of specialization, growth, local competitiveness, and earnings.

The presentation tools of the assessment are bubble/scatter charts, ranking charts and tables.

Definitions:

Specialization: measured using location quotient (LQ).6 Reflects the level of relative

concentration of a particular occupation/industry/cluster in Evansville to the nation. In