A Comparative Study of OECD's Principles of Corporate...

63

MSc Finance & International Business Author: Leena Ronkainen (280786) Academic Advisor: Morten Balling A Comparative Study of OECD's Principles of Corporate Governance of 2004 and Finnish Corporate Governance Code of 2008 Department of Business Studies Aarhus School of Business University of Aarhus May 2010

Transcript of A Comparative Study of OECD's Principles of Corporate...

MSc Finance & International Business Author:

Leena Ronkainen (280786)

Academic Advisor:

Morten Balling

A Comparative Study of

OECD's Principles of Corporate Governance of 2004

and Finnish Corporate Governance Code of 2008

Department of Business Studies

Aarhus School of Business

University of Aarhus

May 2010

ABSTRACT

Importance of corporate governance is increasing as a result of recent financial

crisis and corporate failures. Global organizations like Organisation of Economic

Development (OEDC) and national governments are working together with market

players to review and promote best practices of corporate governance. OECD

published revised principles of corporate governance (Revised Principles) in 2004.

Finland revised Finnish corporate governance code (FCGC) in 2008 and is again in

process of amending the code. FCGC is incorporated into statutory legislation on

listed companies and takes the ‘comply or explain’ –approach. This thesis aims to

contribute to the knowledge of Finland’s corporate governance landscape for listed

companies. Firstly, existing theory concerning corporate governance is surveyed

and an agency theory perspective is taken for the analysis. From agency theory

perspective, separation of ownership and management has resulted in a situation

where owner ‘principal’ delegates the decision making power to management

‘agent’. In the analysis, Finnish corporate governance code and also related

statutory regulation are compared to OECD’s Revised Principles. The thesis seeks

answers to the following research questions: (i) How Revised Principles have been

taken into consideration in FCGC? and (ii) How FCGC approaches the issues with

information asymmetry and agency costs? The analysis shows that Finnish

corporate governance code aligns well with Revised Principles. Detailed disclosure

recommendations are emphasized in FCGC, reducing information asymmetry

when enforced efficiently. As a result, agency cost issues such as monitoring costs

will decrease. Taken aside the agency perspective, Revised Principles go in more

depth into roles and importance of stakeholders in corporate governance, whereas

stakeholders are not soundly incorporated in the FCGC. Further research could be

done to increase the empirical knowledge of corporate governance practices in

Finland.

KEY WORDS: Corporate governance, agency theory, Information asymmetry,

OECD, Finland.

3

1 Introduction ................................................................................................... 4 1.1 Problem Statement ................................................................................ 6 1.2 Structure of the Thesis ........................................................................... 7

2 Literature Review .......................................................................................... 8 2.1 Corporate Governance........................................................................... 8 2.2 Agency Theory..................................................................................... 10 2.3 Transaction Cost Theory...................................................................... 13 2.4 Stakeholder Theory.............................................................................. 14 2.5 Institutional Investors ........................................................................... 17 2.6 Remuneration of the Management....................................................... 18 2.7 Role of Board ....................................................................................... 19 2.8 Disclosure ............................................................................................ 21 2.9 Enforcement of Corporate Governance ............................................... 23

3 OECD and Revised Principles .................................................................... 24 4 Finland and Corporate Governance ............................................................ 27

4.1.1 Regulatory Environment in Finland ............................................... 27 4.1.2 Corporate Governance Code........................................................ 30

5 Analysis of Revised Principles and FCGC .................................................. 33 5.1 Basis for an Effective Corporate Governance Framework ................... 33 5.2 Rights of Shareholders and Key Ownership Functions ........................ 35

5.2.1 General Meeting ........................................................................... 36 5.3 The Equitable Treatment of Shareholders ........................................... 38 5.4 The Role of Stakeholders in Corporate Governance............................ 40 5.5 Disclosure and Transparency .............................................................. 42 5.6 The Responsibilities of the Board......................................................... 44

6 Agency Perspective on FCGC .................................................................... 47 6.1 Information Asymmetry ........................................................................ 47 6.2 Agency Costs ....................................................................................... 50

6.2.1 Bonding Costs............................................................................... 50 6.2.2 Monitoring Costs ........................................................................... 51 6.2.3 Residual Loss ............................................................................... 52

7 Discussion................................................................................................... 55 BIBLIOGRAPHY................................................................................................. 59

Appendix 1: Finnish Corporate Governance Code - Summary of Recommendations

List of Tables: Table 1: Revised Principles summarized Table 2: Summarized Finnish corporate governance on information asymmetry Table 3: Summarized Finnish corporate governance on agency costs List of Figures: Figure 1: The firm as the nexus of contracts Figure 2: General governance structure of Finnish companies Figure 3: Compliance to FCGC in Helsinki Stock Exchange

4

1 Introduction

Importance of corporate governance codes and interest on the discipline are

increasing. Companies like Enron have collapsed because of unsustainable

management or governance scandals. Also, the recent economical crisis and

downfall of financial institutions all over the world have raised interest of the

general public on enforcement and best practices of corporate governance.

Global organizations, like Organisation of Economic Co-operation and

Development (hereinafter OECD), World Bank, International Monetary Fund, and

national governments have been active on setting frameworks and best practices.

In United Kingdom, corporate governance was influenced largely by the Cadbury

Report1 and several other committee reports2. Sarbanes Oxley Act was introduced

in United States in 2002. Both UK and Sarbanes Oxley Act have had an impact on

the corporate governance landscape in Europe. Many large multinational

companies are listed both in some stock exchange in Europe and in United States.

There is a debate whether corporate governance practices are globally converging

or not. World’s capital markets have become more integrated on a global scale and

cross-listing in stock-exchanges is more common. Companies have access to

foreign capital and foreign shareholders have become common in major stock

exchanges. Due to wide variety of company ownership structures and corporate

cultures in the world, local governments and stock exchanges are in the root of the

practical enforcement of corporate governance. OECD published the Principles of

Corporate Governance in 1999. Before making the principles, it had consulted

national governments, private corporations and international organizations. OECD

updated the principles in 2004 and these are referred hereinafter as Revised

Principles. OECD (2004, p. 13) emphasizes that principles should be considered

as more of a reference point than a prescription national legislation. 1 Sir Adrian Cadbury published Report of the Committee on the Financial Aspects of Corporate Governance in the year 1992 2 To mention the most important reports: Greenbury (1995), Hampel (1998), Turnbull (1999, and revised in 2005), Myners (2001), Higgs (2003) and Smith (2003)

5

The aim of this thesis is to compare Revised Principles and Finnish Corporate

Governance Code (hereinafter FCGC). In this thesis, the corporate governance

discussion is limited to publicly listed companies. Taking into consideration the

comparative nature of the thesis, it is important to explore how OECD and Finnish

Securities Market Association, which published FCGC, define corporate

governance.

OECD (2004, p11) defines corporate governance Revised Principles as follows:

“Corporate governance involves a set of relationships between a company’s

management, its board, its shareholders and other stakeholders. Corporate

governance also provides the structure through which the objectives of the

company are set, and the means of attaining those objectives and monitoring

performance are determined.”

Securities Market Association3 notes there is no clear definition of corporate

governance available and takes their view on corporate governance system as

follows: “In general it means a corporate governance system which defines the

corporate executive, that is, the role of the board of directors and hired directors,

duties and their relations to the shareholders. Simply, Corporate Governance

means a system which helps managing and controlling the enterprise.”

As a starting point, the both definitions mostly agree that corporate governance

system is built on relationships between the board, managers and the

shareholders. In addition, both emphasize systems importance as a means of

managing and monitoring the company. Both of the parties also mention that good

corporate governance practice enhance company’s success. OECD mentions

stakeholders in the definition, whereas FCGC does not.

3 Securities Market Association web page (2009) viewed on 17.12.2009, Source: http://www.cgfinland.fi/content/blogcategory/15/142/lang,en/

6

1.1 Problem Statement

Currently, limited amount of research is available concerning Finnish corporate

governance landscape. FCGC, applied to companies listed in Helsinki Stock

Exchange, has increased the access to information on Finnish corporate

governance practices. Listed companies in Finland were required to issue a

corporate governance statement for a financial period commencing on September

2008 or later. In practice, this means that the most of year 2009 annual financial

disclosures have included a corporate governance statement on compliance (and

explanations on departures) of FCGC. Extensive literature, at least in Finnish,

exists on Finland’s statutory regulation on company activities, and the goal of this

thesis is to contribute on this topic on the general level of the corporate governance

code. Due to ‘comply or explain’ –approach adopted in the FCGC, the thesis will

focus on FCGC as a complement of the statutory legislation, and will not go into

detail on corporate governance practices in individual listed companies or

departures from the Finnish Corporate Governance Code published in 2008.

The thesis takes a deductive approach to the subject; theory is surveyed and

applied in analysis of the Revised Principles and FCGC. There are many

perspectives that can be chosen to explore corporate governance in practice. The

thesis aims to discuss how Revised Principles and FCGC encounter the corporate

governance issues that are emphasized in agency theory. Agency theory will be

discussed in more details in the literature view. The below research questions

abridge the main ideas of the thesis:

(i) How Revised Principles have been taken into consideration in FCGC?

(ii) How FCGC approaches the issues with information asymmetry and agency

costs (i.e. monitoring and bonding costs, and residual loss)?

7

1.2 Structure of the Thesis

The thesis structure is summarized in the brief descriptions of chapters below. The

thesis is a broad comparative case study built in an essay form.

Chapter 2: Theory is surveyed from existing academic literature. After considering

general definitions of corporate governance, following topics are discussed in more

detail: agency theory, transaction cost theory, stakeholder theory, institutional

investors in corporate governance, management compensation, board of director’s

role and disclosure. In addition, enforcement of corporate governance is

considered.

Chapter 3: OECD’s Principles of Corporate Governance are discussed and the

main structure of the Revised Principles is summarized in a table.

Chapter 4: The chapter gives a general picture of Finland’s company law

concerned with corporate governance and describes corporate governance

landscape in Finland. The actual recommendations of FCGC are summarized in

Appendix 1.

Chapter 5: The analysis uses primary and secondary data: Revised Principles and

FCGC are used as primary material for the comparison, but also available research

on the topic is considered. Important component in the comparison is also

Finland’s Limited Liability Companies Act because it does form the basis for the

corporate governance in Finland.

Chapter 6: Next, key areas of the analysis from an agency theory perspective are

considered especially concerning the Finnish Corporate Governance Code. The

statutory law and recommendations essential in reducing information asymmetry

and agency costs are summarized in tables.

Chapter 7: The main results and limitations of the thesis are discussed and further

suggestion for future research.

8

2 Literature Review

2.1 Corporate Governance

There is a wide range of definitions for corporate governance. According to Shleifer

and Vishny (1997, p. 737), corporate governance deals with the way in which

suppliers of finance to corporations assure themselves of getting a return on their

investment. Shleifer and Vishny (1997, p. 738) note that understanding corporate

governance can help major institutional changes in developing economies. Jensen

(1993, p. 850) noted there are only four control forces operating on the company to

resolve issues resulting from a divergence between managers’ decisions and those

that are optimal for society: (1) capital markets, (2) legal/political/regulatory system,

(3) product and factor markets, and (4) internal control system headed by the

board of directors. In other words, the groups that assure company is operating

optimally in its corporate landscape are investors, stakeholders like government,

employees, customers, suppliers and board of directors.

Solomon (2007, p. 12) notes that definitions of corporate governance fall along a

spectrum. The agency theory concentrates to relationships between the company

and its shareholders, whereas broader definition of stakeholder theory considers

the relationships of other stakeholders as well. Solomon adds that accountability

has become an essential part on the corporate governance discipline. Solomon’s

(2007, p. 14) view on corporate governance can be placed on the broader end of

the spectrum: “the system of checks and balances, both internal and external to

companies, which ensures that companies discharge their accountability to all their

stakeholders and act in a socially responsible way in all areas of their business

activity”. Solomon assumes that companies maximize shareholder value in long

term taking into account the other stakeholders. Nowadays, social responsibility is

closely connected with this view.

9

Corporate governance discussion is tightly connected with corporate law discipline.

All companies from sole proprietorship to the limited liability have been given a

legal framework from which they can form their company structure and activities.

Until the introduction of Limited Liability Acts, the shareholders had unlimited

liability of their company’s debt. The reduced risk with limited liability created the

basis of today’s capitalism and corporate financing markets. Mallin (2007, p. 11)

describes that corporate governance area is complex as it includes aspects like

legal structure and culture differences.

Van der Berghe (Cornelius and Kogut [eds] 2003, p. 489) recommends a double

track for development of corporate governance: while basic corporate governance

are universal, their translation and practical implementation needs to be

differentiated according to firm type and the relevant governance challenges and

problems associated with that type. Cornelius and Kogut (2003, p. 2) make a

difference between corporate governance and corporate governance system: A

system of corporate governance consist of those formal and informal institutions,

laws, values, and rules that generate the menu of legal and organizational forms

available in a country and which in turn determine the distribution of power – how

ownership is assigned, managerial decisions are made and monitored, information

is audited and released, and profits and benefits are allocated and distributed.

In the following chapters of the literature view, the theoretical base and research on

corporate governance will be introduced: agency theory, transaction cost and

stakeholder theory, role of boards, institutional investors, management

compensation, enforcement of corporate governance, the role of board of directors

and disclosure.

10

2.2 Agency Theory

The issues related to separation of owning and managing the company were

discussed already long time ago. Widely quoted pioneer in corporate governance

research, and especially agency theory, is Adam Smith4 cited by Jensen and

Meckling (1976, p. 305): “The directors, - - being manager of other people’s money

than their own, it cannot well be expected that they should watch over it with the

same anxious vigilance which the partners in private copartnery frequently watch

over their own.” The empirical research for the separation of ownership was

continued further by Berle and Means (1932, p. 129) who confirmed directors have

considerable power over the company, while shareholders have limited means to

remove directors before next election. They also raised their concern on the proxy

voting of shareholders that may lead to separating the power even further from the

principal, when management or committee seeking control has chosen the proxy.

The shareholder as ‘principal’ delegates the decision making power to company

directors who act as ‘agent’ of the owner. Assuming that company’s goal is

maximizing shareholder’s wealth, agents may in practice drive their own goals like

ensuring high performance incentives, perquisites and taking unnecessary risk

instead of making strategically sound decisions for the maximization of long term

shareholder wealth. Agency perspective in corporate governance is to minimize

these conflicts of interest and their costs. Agent may be shirking which can lead to

moral hazards where principal does not have complete information on the actions

of the manager. In other words, there are hidden actions by the agent. Solomon

(2007, p. 144) explains that the information asymmetry leads to situation where

managers know more about company’s activities and financial situation than

investors do. The role of information disclosure is discussed further in its own

chapter. Also adverse selection exists because principal cannot fully evaluate the

agent’s abilities and qualities when delegating the decision making power. In other

words, there is hidden information inaccessible by the principal.

4 Original quote is from Adam Smith’s (1776) book ‘The Wealth of Nations’ p. 192.

11

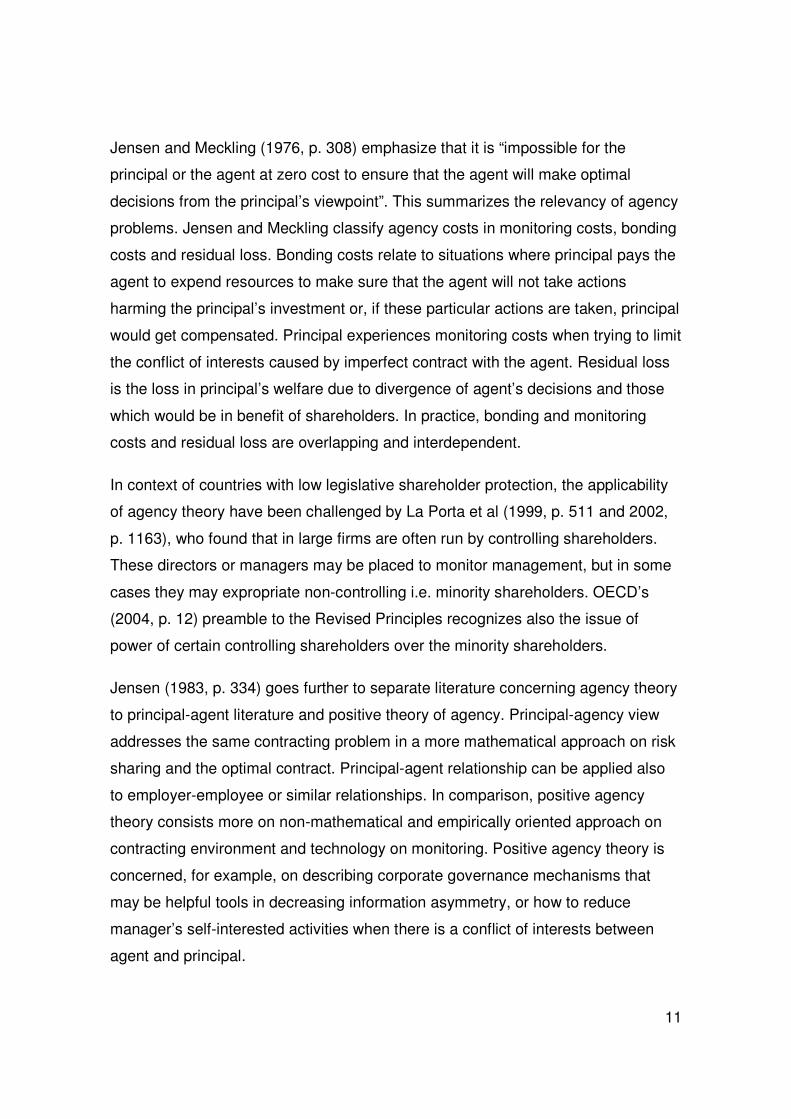

Jensen and Meckling (1976, p. 308) emphasize that it is “impossible for the

principal or the agent at zero cost to ensure that the agent will make optimal

decisions from the principal’s viewpoint”. This summarizes the relevancy of agency

problems. Jensen and Meckling classify agency costs in monitoring costs, bonding

costs and residual loss. Bonding costs relate to situations where principal pays the

agent to expend resources to make sure that the agent will not take actions

harming the principal’s investment or, if these particular actions are taken, principal

would get compensated. Principal experiences monitoring costs when trying to limit

the conflict of interests caused by imperfect contract with the agent. Residual loss

is the loss in principal’s welfare due to divergence of agent’s decisions and those

which would be in benefit of shareholders. In practice, bonding and monitoring

costs and residual loss are overlapping and interdependent.

In context of countries with low legislative shareholder protection, the applicability

of agency theory have been challenged by La Porta et al (1999, p. 511 and 2002,

p. 1163), who found that in large firms are often run by controlling shareholders.

These directors or managers may be placed to monitor management, but in some

cases they may expropriate non-controlling i.e. minority shareholders. OECD’s

(2004, p. 12) preamble to the Revised Principles recognizes also the issue of

power of certain controlling shareholders over the minority shareholders.

Jensen (1983, p. 334) goes further to separate literature concerning agency theory

to principal-agent literature and positive theory of agency. Principal-agency view

addresses the same contracting problem in a more mathematical approach on risk

sharing and the optimal contract. Principal-agent relationship can be applied also

to employer-employee or similar relationships. In comparison, positive agency

theory consists more on non-mathematical and empirically oriented approach on

contracting environment and technology on monitoring. Positive agency theory is

concerned, for example, on describing corporate governance mechanisms that

may be helpful tools in decreasing information asymmetry, or how to reduce

manager’s self-interested activities when there is a conflict of interests between

agent and principal.

12

Tricker (2009, p. 218) describes how in practice the complexity of ownership from

holding a share in a company directly has extended to mutual funds and proxies

which may add another level of conflicting objectives to the simple principal-agent

modeling. Clarke (2007, p. 24) considers agency problems further and suggests

that agency theory underestimates the complexity of relationships between

shareholder, board and management. These result in a double agency dilemma.

Research by La Porta et al (1999, p. 511) and Becht and Röell (1999, p. 1055)

conclude that there may be conflict between the interests of large controlling

shareholders and the minority shareholders. They agree that in United States the

main agency problem is between managers and dispersed shareholders, whereas

in continental Europe large block holders exercise control over the management.

Van der Berghe (Cornelius and Kogut [eds] 2003, p. 484) points out that managing

corporations in a global networked economy is far more complex than managing a

single company with one principal and one agent.

Taking the perspective of shareholders who diversify their risk in investing to a

portfolio of securities, the principal’s willingness to take risk may be larger than for

the agent. Portfolio investors have diversified at least the variation of the short-term

value of the stock, whereas managing director’s remuneration and future service

contract is much more dependent on the success of the company. Wiseman and

Gomez-Mejia (1998, p. 133) suggest that agents may show signs of risk-seeking

as well as risk-averse behavior. Manager may have variety of risk preferences,

depending on the situation and the decision to be made.

Hill and Jones (1992, p. 135) discuss the power shifts between principal an agent

when the contracting opportunities are limited. If agents experience substantial

losses when exiting from the relationship, the principal has the power. However, if

the principals have a shortage of agents to choose from, the power shifts to the

agent. This is an important aspect of principal-agent relationship, as business

environment is dynamic in reality and there may be inefficiencies in the short run in

managerial labor market. In long run, success of the firm is considered as

affirmative information of manager’s talent.

13

2.3 Transaction Cost Theory

Transaction cost theory is based on the idea that companies can internally

undertake activities more economically rather than contracting them externally.

Ronald Coase and Oliver Williamson have contributed greatly to development of

transaction cost theory. According to Solomon (2007, p. 21), the theory

incorporates human behavior on how company organizes its activities. It is based

on the fact that companies are nowadays so large that they substitute the market in

determining allocation of resources. Companies internalize transactions to reduce

risks and to protect their competitive advantage. Instruments used in transactions

can be called governance mechanisms. As firm grows in size and experience

diseconomies of scale, some activities are more cost efficient when outsourced.

Also small firms may consider outsourcing book-keeping, payroll or other activities

which are not adding value if kept internal.

Transaction theory assumes bounded rationality, in other words limitations in

human cognitive abilities. The contracts made can never be perfect as there is

always unpredictability in future outcomes. Williamson (1985, p. 181) notes also

that human behavior can be self-interest seeking or opportunistic: Economic

agents make calculated efforts to mislead and disclose information in selective and

distorted manner. Williamson summarizes issues in world of governance as

follows: Planning is necessarily incomplete (bounded rationality), unguarded

promise may break down (opportunism), and the pair-wise identity of the parties

matter because of asset specifity.

Eisenhardt (1989, p. 64) notes that transaction cost theory is more concerned with

the boundaries of the company, variables of asset specificity and small numbers

bargaining. In comparison, agency theory is interested in cooperation of different

parties regardless of organizational boundaries and independent variables of risk

attitudes, outcome uncertainty and information systems.

14

Limited Liability

CompanyCreditors

CommunitiesOther contractual parties

CustomersShareholders

Employees

Management

Auditors

2.4 Stakeholder Theory

Stakeholder theory is concerned with broader definition of corporate governance:

Business activities influence the surrounding society, not only the owners of

company shares. Stakeholders like banks, customers, suppliers, employees and

municipalities have established contracts with the company or are affected by the

company’s activities. Van der Berghe notes (Cornelius and Kogut [eds] 2003,

p. 486) that, in modern business environment, corporations need to increasingly

cope with other critical stakeholders and board members have included the duty of

balancing the interests of all stakeholders. John and Senbet (1998, p. 372) note

that corporate governance deals with mechanisms by which stakeholders of a

corporation exercise control over corporate insiders and management in such way

that their interests are protected. Managers are in a special position as they have

direct control over the company, in comparison for example to creditors who have

indirect control.

According to Fama (1980, p. 290) managers are “coordinating the activities of

inputs and carrying the contracts agreed among inputs”. In this way, transaction

cost theory and incomplete contract theory of the firm5 link the agency theory and

stakeholder theory. Quoting Jensen (1983, p. 327): “The behaviour of organization

is the equilibrium behaviour of a complex contractual system made up of

maximizing agents with diverse and conflicting objectives.” The nexus of contracts

is illustrated in the following Figure 1.

Figure 1: The firm as the nexus of contracts [adapted from Timonen (2000, p. 36)]

5 Coase (1937) “The Nature of the firm” and Williamson (1975) “Markets and hierarchies”

15

Mallin (2007, p. 49) describes how shareholder wealth increases from the residual

cash flow which means profits remaining after the other stakeholders like loan

creditors have been paid. In other words, maximizing the use of resources should

in fact benefit other stakeholders as well. Jensen and Meckling (1976, p. 319) refer

to residual loss when they explain the other side of the coin: Agents’ decisions may

reduce the principals’ residual cash flow. Also Blair (Cornelius and Kogut [eds]

2003, p. 57) notes that shareholders are indeed residual claimants: whereas

stakeholders receive fixed amounts specified in contracts, shareholders get what is

left over. In addition, other stakeholders are protected by their contract, in

comparison to shareholders who have limited liability in total of the amount they

have invested to the shares.

According to Shleifer and Vishny (1997, pp. 751-752), the courts in OECD have

generally accepted the idea that managers have a duty of loyalty to shareholders.

They justify the idea on the fact that shareholders investments are sunk, whereas

stakeholders like employees are paid immediately for their efforts and can threaten

to quit if their investment is in danger of expropriation. In other words, many

stakeholders, other than shareholders, are better assured that they get a return for

their investment. In comparison to shareholders, creditors have a better legal

protection in case of default due to contractual nature of the investment. It is good

to keep in mind that shareholders of listed companies have limited liability. In case

of default, the amount of losses is limited to the investment of the shares, whereas

some stakeholders like chief executive officer may even face criminal prosecution

on intentional misconduct. For example the 2002 Sarbanes-Oxley Act in United

States is known from the imposed criminal penalties to chief executive officer and

chief financial officer. Tirole (2001, p. 23) mentions that also regular employees

have sunk investments: For instance in form of housing arrangements and

foregone alternative opportunities. Van der Berghe (Cornelius and Kogut [eds]

2003, p. 486) states that “corporate governance should aim at optimizing the (long-

term) return to shareholders while satisfying the legitimate expectations of

stakeholders.”

16

Agency theory is more profit-seeking compared to stakeholder theory’s perspective

of social responsibility. Agency theory is not primarily concerned with, for example,

the relationship between employees and the company. Bainbridge (2008, p. 51)

explains that maximizing shareholder value is also in the benefit of the board: “If

management fails to maximize the shareholders residual claim, an outsider can

profit by purchasing a majority of the shares and voting out the incumbent board of

directors”. Bainbridge also notes that the contractual relationship of employees and

shareholders is different: employee relationship with the company is often subject

to periodic renegotiation, whereas shareholders have indefinite relationship – until

the shareholder transfers the relationship by for example selling the share.

Often the agency theory and stakeholder theory are considered opposite views, but

Solomon (2007, p. 27) points out that there are similarities between the two

theories. Asymmetric information is a disadvantage to all stakeholders including

the shareholders. Managers are also a stakeholder group and have the most

power to affect allocation of resources. Stakeholder theory emphasizes that

managers interest should align also with other stakeholders, not only with

shareholders.

17

2.5 Institutional Investors

La Porta et al (1999, p. 474) note that when ownership of stocks is more

concentrated to others and minority shareholders exist, control rights of the

company are not distributed evenly. They encourage research to focus on the

incentives and the opportunities of these controlling shareholders to both benefit

and expropriate the minority owners. La Porta et al (1999, p. 491) added that

controlling shareholders can be also families or the state.

Jensen (1993, p. 867) does not limit the investor activism to only large

shareholders: active investors hold large debt and/or equity stakes in the company

and actively participate in its strategic direction. Jensen’s point links closely the

stakeholder theory as creditors do not attend for example board meetings, but still

often affect to governance of the corporation. This chapter will concentrate more on

shareholdings of institutional investors which as themselves are a heterogeneous

group.

According to Gillian and Starks (2003, p. 4), the emergence of institutional

investors as shareholders has become an important external control mechanism

that affects governance. In diffused or dispersed ownership, individual shareholder

would need to bear large monitoring costs, when simultaneously rest of the

shareholders would free-ride on the benefits of monitoring the management.

Institutional investors often standardize the monitoring activities to achieve

economies of scale. This may also lead to free-riding of monitoring, as monitoring

will benefit also those shareholders who are not sharing costs of the monitoring

activities.

Gillian and Starks (2003, p. 10) describe that in 1980’s public pension and union

funds began submitting shareholder proposals to companies, later they negotiated

directly with the management and pressured companies through media. These are

not the only way institutional investors can influence the company, they can simply

buy shares or sell them. They also point out the ongoing debate on the

appropriateness and the effectiveness on the activism by institutional investors.

18

2.6 Remuneration of the Management

Agency theory pointed out the need for monitoring of management. Another way to

bring into line the interests of shareholders and management is incentive

alignment. According to Chan (2008, p. 129), executive compensation packages

consist generally from four parts: base fixed salary, annual bonus, stock options

and restricted stock grants, and long term incentive plan. These can be described

also as explicit incentives. Managers may also enjoy perquisites, like company

cars or golf club memberships, which may not always be so visible to

shareholders.

Chan (2008, p. 131) notes that, as principal does not have all the needed

information about agent’s activities, an outcome-based contract is called for.

Agent’s behavior is however not the only factor that affects outcome: economy,

legislation and competition among other macro-environmental factors influence the

performance of the corporation. Chan simplifies that the risk is moved to the risk-

averse agent with the performance-based contract and, due to agent’s self-

monitoring, agency costs are reduced. Chan (2008, p. 133) summarizes also that

researchers6 have found only “little support for the alignment of executive and

shareholder interests with optimal contracting focus of agency theory”. However,

Hartzell and Starks (2003, p. 2372) find a strong positive relation between

institutional concentration and the pay-for-performance sensitivity of managerial

compensation. The optimal contracting view is also challenged by Bebchuk and

Fried (2003, p. 73) who argue that board of directors favor high remuneration for

executive management because the latter can influence director’s compensation

and nomination. Managers wish to perform will in order to keep their post as CEO.

Poor management performance can bring about proxy fights or even take-over.

Managers of other firms may consider that they can manage the firm’s assets more

profitably and seek to take over the company. Managers also aim to maintain their

own reputation and ensure their human capital is still competitive in the managerial

labor market. 6 For example: Gomez-Mejia and Wiseman 1997; Tosi et al. 2000

19

2.7 Role of Board

Board of directors is very important point to consider as it monitors the

management of the company and should consider the benefit of shareholders in

company’s strategic decisions. The role of board is to act as a mediator between

the shareholders (principal) and the everyday managing of the company (agent).

Bainbridge (2008, p. 161) recaps the essence of board as follows: “the modern

board - - is properly understood as a production team whose product consists of a

unique combination of advice giving, ongoing supervision, and crisis management”.

The general classification for board types is unitary and two-tier board. Unitary

board is defined as a single governing body whereas two-tier boards have

managing board for operational management decisions and a supervisory board

for strategic decisions and supervising the management board. Shareholders

usually select the directors to the unitary board and two-tier board system’s

supervisory board. In turn, supervisory board selects the members of the

management board. As an exception, for instance German companies’ employees

select the supervisory board. Solomon (2007, p. 79) states that unitary boards are

common in Anglo-Saxon style of corporate governance.

Jensen (1993, p. 866) criticizes the common practice in US for CEO to hold the

position of board chairman: “Without the direction of an independent leader, it is

much more difficult for the board to perform its critical function.” By this function he

means hiring, monitoring, compensating and removing the managing director/CEO.

Indeed, if the board chairman is also the CEO, it is possible that he or she tries to

negotiate better compensation package. CEO should not be involved in the

decision making process that involves hiring or firing himself or herself. However,

the involvement on decisions concerning directors own interest is usually tightly

regulated in the Limited Liability Acts. Jensen (1993, p. 864) argues that boards

are motivated more on minimizing downside risk rather than maximizing value – in

fear of class action suits or other legal liabilities. Jensen also mentions that board

may base their decisions partly on avoiding adverse publicity from media.

20

According to Mallin (2007, p. 128), board may delegate various activities by

appointing sub-committees. However, board cannot delegate its responsibility as a

whole. Already in Cadbury report in 1992, it was recommended for board to

establish audit and nomination committees. Higgs (2003, p. 19) reported that audit

and remuneration committees are very common in listed companies: One firm of

FTSE 100 did not have audit or remuneration committee, and 15 percent of FTSE

350 did not have audit committee7. Mallin (2007, pp. 128-131) defines roles of

audit, remuneration, nomination and risk committees. Audit committee reviews the

audit scope and ensures that auditors are objective. It is considered the most

important subcommittee. Remuneration committee reviews and recommends,

within agreed terms of reference, the cost and framework of executive

remuneration. Remuneration is a relevant topic in the recent financial crisis as loss

making banks or corporations pay high management bonuses. Nomination

committee evaluates the balance of competences of board members (or

candidates). Risk committee assesses the risk like use of derivatives and level of

risk monitoring internally. In UK, Turnbull report in 1999 emphasized the

responsibility of board concerning internal controls of the company.

Coming back to the role of board and its responsibilities, Clarke (2007, p. 37)

explains the importance of business judgment rule. Business judgment rule

provides directors more discretion to make decisions in good faith: “As long as

there is not evidence of fraud, gross negligence or other misconduct, directors will

not be held responsible for a business judgement if it proves to be mistaken.” The

decision-making of the company is complex and the element of risk-taking in

business activity is important when looking for long-term growth opportunities.

7 Please note that the snapshot data was drawn in July 17, 2002 for Higgs Review.

21

2.8 Disclosure

According to Solomon (2007, p. 66), disclosure covers accountability to

shareholders, several descriptions concerning board, training, induction and

directors’ evaluation. It is more related to qualitative information on the way the

company is managed. It can also be voluntary corporate communication like web

pages and management forecasts. Publicly listed companies often need to

disclose more information to the potential investors than small family owned

companies.

Healy and Palepu (2001, p. 410) summarize the issues on information and agency

frame work as follows: “(i) role of disclosure and financial reporting regulation in

mitigating information and agency problems, (ii) the effectiveness of auditors and

information intermediaries as a means of increasing the credibility of management

disclosure and uncovering new information, (iii) factors affecting management

decisions by managers on financial reporting and disclosure, and (iv) the economic

consequences of disclosure.”

According to Solomon (2007, p. 145), frequent and relevant disclosure of

information narrows the information asymmetry gap and gives a better position for

shareholders. However, the information is also available to potential investors who

can free-ride on this information. In turn, annual general meetings of shareholders

are often accessible only to current shareholders. Disclosure of standardized

information reduces the transaction costs of searching information for monitoring

and evaluating company performance.

Solomon emphasizes (2007, p. 171) that external auditing, as a corporate

governance mechanism, helps shareholders to monitor and control the company

activities from distance. In other words, it may decrease issues with information

asymmetry. On the other hand, auditing company often offers consultancy services

to the company. This may compromise the independence or objectivity of the

auditors. According to Solomon (2007, p. 172), the regular audit activities often

lead to close relationships between the auditor and the management.

22

Information asymmetry played a big role in collapse of Enron and auditors did take

part in the creative financial reporting of the financial condition. Suppliers of finance

like banks rely on the assurance of the auditors that published information

describes the state of company’s financial position. Financial media provides their

part of the investor information by analyzing the disclosures and information on the

market. Financial analysts collect data from public and private sources and make

forecasts or recommendations on the stock.

Richardson (2000, p. 325) notes that, due to information asymmetry between

principal and agent, managers may be able to manage earnings. He suggests

reasons for earnings management: avoiding violation of debt covenants and

maximizing management bonus. In large corporations, managers often withdraw

considerable benefits via perquisites and may avoid disclosing the complete

picture to shareholders.

Boards can be driven to consider the remuneration policies carefully by requiring

corporations to disclose their remuneration decision making process and policies.

This indeed narrows the information asymmetry and monitoring costs on

managerial compensation, and allows shareholder’s to take action if incentive

packages are evaluated excessive.

Miller (2002, p. 189) found substantial and pervasive increase in disclosure during

periods of increased earnings. Miller’s sample was 80 listed US companies, and he

considered voluntary disclosures. He argues that when the earnings increases

cease, the magnitude of voluntary disclosure returns to the same level as in flat

earnings period. Study on Monitoring and Enforcement Practices in Corporate

Governance in the [European Union] Member States by RiskMetrics Group (2009,

p. 59) notes that transparency requirements on disclosure can lead to competitive

disadvantage. Very detailed information allows for example competitors to analyze

company strategies and competitive advantages too much in depth.

23

2.9 Enforcement of Corporate Governance

Building blocks of corporate governance framework need to be enforced

effectively. Otherwise corporate governance code, or even legislation, does not

have desired effect on corporations’ overall practices. Market environment, where

company operates, is regulated and supervised by authorities and also stakeholder

relations are controlled by laws. Private enforcement is also important as individual

parties make sure their contracts are enforced in an agreed way. From legal point

of view, principal has delegated agent the management of principal’s property.

Company’s operations are organized in form of contractual relations. Stakeholder

theory refers to a wide range of contracts between the company and bank,

employees, customers or suppliers. These regulations and contractual

relationships create the framework in which company operates. Corporate

governance is a part of this framework: There are both obligatory and voluntary

elements involved. Enforcement should be efficient in order to achieve the goals of

the set codes or recommendations.

Corporate governance can be enforced by law or by more voluntary approach.

Common voluntary approach is ‘comply or explain’. Legislation on disclosure of

information usually covers financial information, audit function and, for example,

annual general meetings. Agency theory point of view on corporate governance

enforcement is to enhance monitoring, reduce asymmetry of information and the

conflicts of interest between the principal and agent. This in turn reduces agency

costs. From stakeholder perspective, it guarantees that mechanisms for control

and operative management are in place. Solomon describes (2007, p. 186) that

particular country’s legal framework dictates how corporate governance

enforcement is set. Common law systems prefer often voluntary initiatives whereas

countries with codified legal system choose government-led corporate or

commercial law framework changes. The comprehensible allocation of roles and

power among the authorities are essential for implementation of corporate

governance in practice. In addition, enough resources need to exist for the

authorities to monitor the implementation.

24

3 OECD and Revised Principles

OECD published Principles of Corporate Governance for the first time in 1999. It

has raised awareness of corporate governance practices in OECD member

countries and as well as among non-members. With a new mandate by OECD

Ministers in 2002, a review of the principles was carried out including surveys

directed to member countries, comments from Regional Corporate Governance

Roundtables including also non-member countries and help of World Bank and

other sponsors. Prior to making the Revised Principles, OECD consulted many

international bodies such as World Bank and governments of member states in

order to gain a converged view on the governance guidelines and suggestions for

improvement. Revised Principles were published in the year of 2004.

OECD also recognizes that principles may not fit all the countries due to variety of

corporate, social and cultural structures. Revised Principles take voluntary

approach to corporate governance and many OECD member and non-member

countries over the world have used in building and evaluating their legal

frameworks and best practices. In the preamble of the Revised Principles,

corporate governance practices are seen as one key element in improving

economic efficiency and growth and also enhance investors’ confidence. Revised

Principles (2004, p. 12) “focus on governance problems that result from separation

of ownership and control.” Without under-estimating the relevance of other

stakeholder parties in sustainable business operations, the focus of Revised

Principles supports the agency theory approach that this thesis has taken. OECD

emphasizes that other issues relevant to company activities, like environmental,

anti-corruption or ethical concerns, have been included more soundly in different

OECD and other international organizations’ instruments.

25

Solomon (2007, p. 189) mentions a weakness of OECD principles: They have no

legal or regulatory power by itself. Kirkpatrick and Jesover (2005, p. 127) note that

the principles have a focus on publicly traded companies. However, other

companies are also encouraged to apply the principles. From global perspective, it

is important that OECD principles are adaptable to various types of corporate

structures. According to Mallin (2007, p. 33), World Bank and International

Monetary Fund use OECD principles to prepare assessments of corporate

governance in individual countries. Through world wide application of the

principles, the framework is influential in global scale.

OECD emphasizes the responsibility of national governments in shaping effective

regulatory frameworks that provide also flexibility for markets to respond to

continuously evolving business environment and expectations of shareholders and

other stakeholders. Revised Principles were chosen to form a framework for the

analysis of the Finnish Corporate Governance Code, because they allow better to

account for country specific business environment’s characteristics, and the

statutory regulation that are rooted in the Finnish corporate governance landscape.

26

Table 1 summarizes the Revised Principles key areas. The principles are

complemented by the separate annotation part which includes explanation and

more details on each principle.

The areas of Revised Principles: The corporate governance framework should: I. Ensuring the basis for an effective corporate governance framework

“- - promote transparent and efficient markets, be consistent with the rule of law and clearly articulate the division of responsibilities among different supervisory, regulatory and enforcement authorities”

II. The rights of shareholders and key ownership functions

“- - protect and facilitate the exercise of shareholders’ rights.”

III. The equitable treatment of shareholders

“- - ensure the equitable treatment of all shareholders, including minority and foreign shareholders. All shareholders should have the opportunity to obtain effective redress for violation of their rights.”

IV. The role of stakeholders in corporate governance

“- - recognize the rights of stakeholders established by law or through mutual agreements and encourage active cooperation between corporations and stakeholders in creating wealth, jobs, and the sustainability of financially sound enterprises. “

V. Disclosure and transparency “- - ensure that timely and accurate disclosure is made on all material matters regarding the corporation, including the financial situation, performance, ownership, and governance of the company“

VI. The responsibilities of the board “- - ensure the strategic guidance of the company, the effective monitoring of management by the board, and the board’s accountability to the company and the shareholders“

Table 1: Revised Principles summarized (adapted from Jesover and Kirkpatrick

(2005, p. 130))

27

4 Finland and Corporate Governance

4.1.1 Regulatory Environment in Finland

Finnish legislation is based on civil law system. Legislation concerning Finnish

listed companies is the Limited Liability Companies Act (624/2006 as amended,

hereinafter FLLCA) and Securities Markets Act (495/1989 as amended, hereinafter

SMA). Companies listed in NASDAQ OMX Helsinki Ltd (hereinafter Helsinki Stock

Exchange) should follow with Rules of the Stock Exchange8, which are compliant

with the aforementioned Finnish law. According to the study on corporate

governance in European Union by RiskMetrics Group (2009, p. 96 of Appendix 1),

the Finnish market is very heterogeneous with big global players like Nokia

governed by the same framework as many more small domestic companies listed

in the Helsinki stock exchange. Same study (2009, p. 26) notes that stock

ownership is concentrated in the hands of foreign investors. According to OMX

Nordic Exchange web pages9, 128 companies were listed in Helsinki Stock

Exchange in 2009.

According to a decree by Ministry of Finance (393/2008), company shall provide an

explanation if departing from the applicable10 governance code. Internal control of

the company is referred in FLLCA (§6, item 2) as board of directors is responsible

on the control of company’s accounts and finances. The general manager shall

handle the compliance with law on the accounts and financial affairs. It should be

mentioned at this point that Finnish Ministry of Justice Working Group on FLLCA

left in purpose the corporate governance issues to self-regulation of businesses:

Best practices can change faster than it’s feasible to change legislation.

8 Rules of the Stock Exchange entered into force 16.03.2009. Original Finnish document used to familiarize with the rules and the unofficial translation of the document by NASDAQ OMX Helsinki was used for referencing in the text. 9 Yearly Nordic Statistics 2000-2009 in an Excel form, 2010, Source (viewed 5 March 2010): http://nordic.nasdaqomxtrader.com/digitalAssets/67/67432_yearly_nordic_statistics_2000_2009.xls 10 FCGC applies providing it does not conflict with statutory regulation in the company’s domicile

28

reporting

appointment

Shareholders

Auditors Supervisory Board

Employees

Board of Directors

Management

SuppliersCustomers Creditors

In agency theory, the purpose of a company is to maximize shareholder value,

whereas Finnish law (FLLCA §1, item 5) allows the articles of association to define

other purpose for the company. FLLCA (§1, item 8) states that managers shall act

with due care and promote the interest of the company. Generally this means

fiduciary duty to shareholders, but it may allow interpretations. In the analysis, it is

assumed that listed companies’ purpose is to maximize shareholder value. Figure

2 illustrates the general governance model in Finnish companies.

Figure 2: General governance structure of Finnish companies [adapted from

Laitinen & Ruuhela (1997, p. 319)]

Articles of Association have an important role in forming the governance practices

and basis for corporate operations in Finland. Articles of Association are obligatory

for a limited liability company. In general, shares in Finland contain both of the

following rights:

1) Property rights (e.g. dividend, pre-emptive rights and registering of shares)

2) Administrative rights (e.g. right to receive information, using right to put item

on agenda of general meeting, right to speak and to make questions, and to

contest decisions)

29

Before going more in detail on corporate governance in Finland, a brief description

of general meeting and extraordinary general meeting is given. These will be

further discussed in the analysis of corporate governance codes. FLLCA states

that general meeting is to be held within six months of the financial period’s end. In

addition, FLLCA require that at least one statutory auditor is appointed by the

annual general meeting. Auditors are regulated by the Finnish Auditing Act. FLLCA

(§3, item 2) also lists items that fall within scope of ordinary general meeting and

extraordinary general meeting. Ordinary General meeting shall include decisions

on the following items: (1) adoption of the financial statements; (2) the use of profit

shown on the balance sheet; (3) the discharge of board of directors and managing

director from liability; (4) the appointment of the board; (5) other matters that shall

be decided in the general meeting according to articles of association.

An extraordinary general meeting shall be held if (1) articles of association require;

(2) board considers it necessary; (3) shareholder or auditor demands; or (4)

supervisory board considers it necessary and it is competent under articles of

association, decide on the holding of extraordinary meeting. Referring to the third

point, an extraordinary meeting is held if a total of tenth of shareholders (or less if

company’s article of association states so) demand so in writing. This enhances

also the rights of minority shareholders, if they succeed to gather 10 percent of the

shareholders to demand extraordinary meeting. (see FLLCA §3, item 3-4)

30

4.1.2 Corporate Governance Code

The adoption of euro and reduction of barriers of capital flows have increased the

amount of potential investors and access to funds also in Finland. These have

increased pressure on enhancement corporate governance system, and changed

the business environment. Investors’ access to information about Finnish corporate

culture and financial information has been an important target in building the

corporate governance code in Finland. According to statistics from Euroclear

(2010), the foreign and nominee-registered11 portion of the shares issued has been

47-53 percent in the last 10 years and 45.7 percent in March 2010.

European Commission requires annual statement on structure and practice of

corporate governance on comply or explain -basis. This disclosure requirement

applies to stock listed companies. They released also directives aiming to

harmonize transparency and disclosures. Directive 2006/46/EC require listed

companies to publish a corporate governance statement and it has been applied in

Finland. European Union in itself and European Commission’s directives

harmonizing the company law evidently converge the corporate governance in the

member states.

Finland’s first corporate governance guidelines, published in 1997, were based on

voluntary application for listed companies. Corporate governance recommendation

for listed companies was published in 2003. The current revised FCGC issued by

Securities Market Association12 came into force on 1.1.2009 and additional

corporate governance statement guidelines were published in 200913. Revising the

code was driven by private actors having public support due to European

Commission Directive to be harmonized in Finland. The code is a complement to

the Finnish statutory legislation.

11 Custodial nominee account: Book-entry securities owned by a foreign individual, corporation or foundation may be entered in a special book-entry account. (not available for Finnish-owned share) 12 Central Chamber of Commerce of Finland, Confederation of Finnish Industries EK and NASDAQ OMX Helsinki Ltd established Securities Market Association in 2006. 13 Remuneration Statement Guideline in October 23, 2009 and Corporate Governance Statement Guideline in November 2, 2009 available in Securities Market Association’s web pages.

31

In brief, FCGC framework consists of recommendations in the areas of general

meeting (recommendations 1-4), board (5-17), board committees (18-33),

managing director (34-36), other executives (37-38), remuneration (39-44), internal

control, risk management and internal audit (45-47), insider administration (48),

audit (49-50) and communications (51-52). The recommendations are stated in

Appendix 1. FCGC includes an explanatory section under each recommendation.

The introductory part of FCGC includes general description on the corporate

governance in Finland, also a brief description on shareholder’s rights based on

the statutory regulation. According to FCGC (2008, p. 6), ownership structures and

governance practices vary among the listed companies. In international terms,

most of the companies listed in Helsinki Stock Exchange are medium or small-

sized companies.

Introductory chapter of FCGC further explains the comply or explain principle as

follows:

“The company may depart from an individual recommendation of the Code due to,

e.g. the ownership or company structure or the special characteristics of its area of

business. A clear and comprehensive explanation will consolidate the trust in the

decision made by the company and make it easier for the shareholders and

investors to evaluate the departure.” (see FCGC 2008, p. 6)

Interestingly, OECD’s Revised Principles are based on non-binding, voluntary

adaptation in member countries, but they do not particularly emphasize to adopt

this comply or explain –approach. They do mention it, but only on annotation

concerning their recommendation on disclosure and transparency:

“In several countries, companies must implement corporate governance principles

set, or endorsed, by the listing authority with mandatory reporting on a “comply or

explain” basis. Disclosure of the governance structures and policies of the

company - - is important for the assessment of a company’s governance.” (see

OECD 2004, pp. 53-54)

32

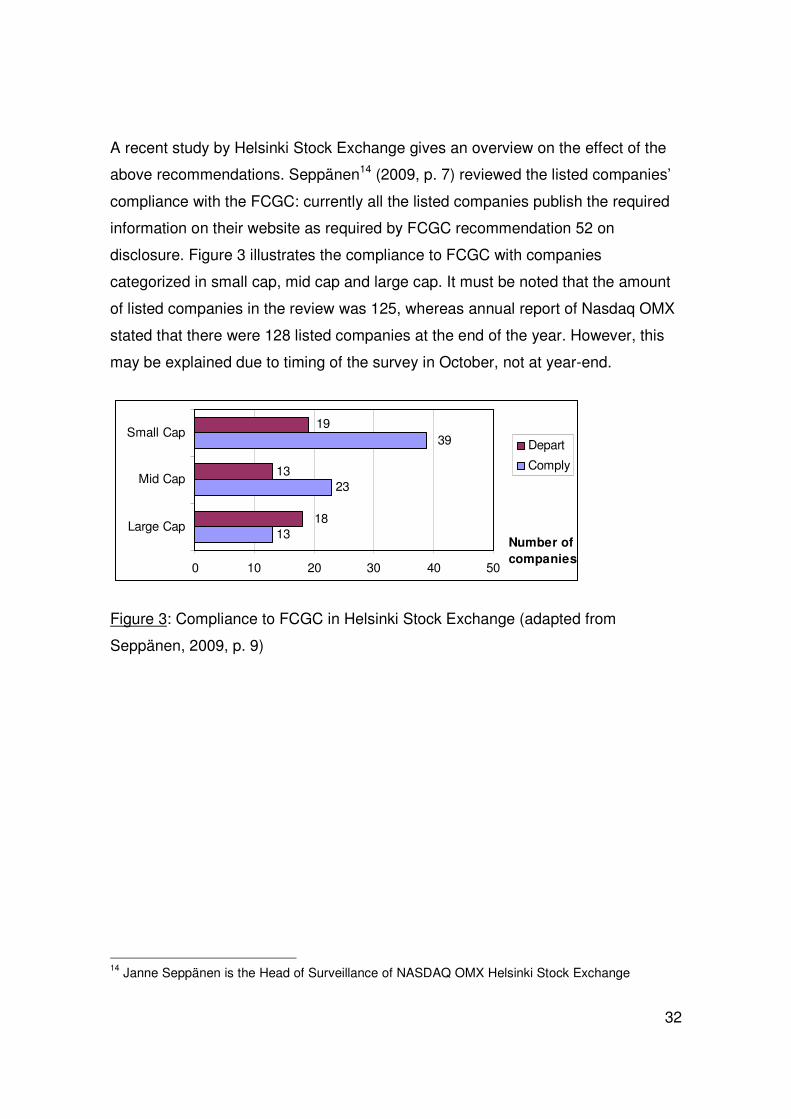

A recent study by Helsinki Stock Exchange gives an overview on the effect of the

above recommendations. Seppänen14 (2009, p. 7) reviewed the listed companies’

compliance with the FCGC: currently all the listed companies publish the required

information on their website as required by FCGC recommendation 52 on

disclosure. Figure 3 illustrates the compliance to FCGC with companies

categorized in small cap, mid cap and large cap. It must be noted that the amount

of listed companies in the review was 125, whereas annual report of Nasdaq OMX

stated that there were 128 listed companies at the end of the year. However, this

may be explained due to timing of the survey in October, not at year-end.

13

2313

39

18

19

0 10 20 30 40 50

Large Cap

Mid Cap

Small Cap

Number of companies

Depart

Comply

Figure 3: Compliance to FCGC in Helsinki Stock Exchange (adapted from

Seppänen, 2009, p. 9)

14 Janne Seppänen is the Head of Surveillance of NASDAQ OMX Helsinki Stock Exchange

33

5 Analysis of Revised Principles and FCGC

5.1 Basis for an Effective Corporate Governance Framework

According to OECD’s Principals, framework should promote transparent and

efficient markets, be consistent with rule of law and clarify the responsibilities of

authorities involved. In addition to making recommendations, FCGC has taken task

to give foreign investors a general view on the Finnish corporate governance

system. OECD explains the basis of the framework in the annotation and notes

that framework may need to be adjusted as new experiences accrue and business

circumstances change. As already mentioned before, Finnish legislators have

deliberately left corporate governance for self regulation, providing it does not

conflict with FLLCA or other compelling legislation. The FCGC applies to

companies listed in Helsinki exchange, given it is not conflicting with statutory

regulation in the domicile of the company.

Revised Principles encourage authorities building the framework to consult with

corporations and other stakeholders. Securities Market Association has duty to

administer the code. For example, following European Commission’s

recommendation on remuneration of directors of listed companies15, Securities

Market Association set up a working group, consisting of lawyers, representatives

from chamber of commerce, investors, corporations e.g. Nokia and from stock

exchange, to investigate a need for changes in the FCGC. The working group is

currently waiting for comments on their proposal and the goal is to publish the

updated corporate governance code in June 2010.

Revised Principles annotation describes that division of the responsibilities among

authorities should be clear. However, some recommendations of FCGC are based

on law or other compelling regulation. Company may not depart from these

statutory items.

15 30.4.2009 dated Commission Recommendation complementing Recommendations 2004/913/EC and 2005/162/EC as regards the regime for the remuneration of directors of listed companies

34

The mandatory implementation of corporate governance code is a recent adoption

to statutory law, and as a result the distribution of responsibilities among authorities

is slightly unclear. Finnish Financial Supervisory Authority (hereinafter FFSA) does

refer in their web pages16 to the corporate governance code for listed companies

and considers some areas of FCGC of particular relevance: competence and

independence and remuneration of board members, internal control and risk

management. Keeping in mind that FFSA has jurisdiction over the issue, it has not

established major monitoring system on the compliance of the code. Therefore, the

responsibility so far has remained with the Helsinki Stock Exchange to monitor that

the listed companies follow their rules of the exchange. As Helsinki Stock

Exchange is a private body, it does not have the formal legal authority and

enforcement. However, sanctions from Helsinki stock exchange apply. FCGC

Recommendation 51 states that the law [Securities Market Act 392/2008] requires

the company to present corporate governance statement either in the annual report

by the board of directors or as a separate report. FCGC (2008, p. 6) refers also to

the Rules of Helsinki stock exchange which include obligations related to good

corporate governance practices and disclosure.

Non-binding nature of OECD Principles is also reflected in FCGC. The FCGC

follows the ‘comply and explain’ –principle. This principle does not necessarily

increase convergence of corporate governance practices: Alternative of not

complying is available for the company, as long as they explain the departure. In

addition, company may choose a very general explanation on the departure.

Revised Principles note that flexibility of the corporate governance framework

allows companies to operate in broadly different circumstances. FFSA published a

report on regulatory outlines of corporate governance in 2005. The report stated

that the Finnish corporate governance framework builds on Revised Principles,

guidelines issued by Basel Committee on Banking Supervision and the

Recommendation for Corporate Governance of Listed companies.

16 Finnish Financial Supervisory Authority [in Finnish Finanssivalvonta] 2005, Source (viewed 2 December 2009): http://www.finanssivalvonta.fi/en/Listed_companies/Listing/Corporate_Governance/

35

5.2 Rights of Shareholders and Key Ownership Functions

According to Revised Principles’ annotations (2004, p. 32), the “section can be

seen as a statement of the most basic rights of shareholders, which are recognized

by law in virtually all OECD countries.” In Finland the basic shareholder rights are

covered in FLLCA. OECD’s Principles’ CG framework should protect and facilitate

shareholder rights including registration and transfer shares. FLLCA has provisions

on rights related to shares and on annual general meeting. Companies are

required to maintain a register of shares and the register shall be available in

company’s head office to access for everyone.

Revised Principles state that capital structures and arrangements that enable

shareholders to obtain a degree of control disproportional to their ownership shall

be disclosed. European Commission Directive 2004/109/EC states that investors

should notify no later than 4 days if they exceed the threshold of holding 5 percent

of shares. Finnish Securities Market Act (§2, item 9) has more strict legislation on

notifying with flagging announcement on the threshold of holdings without undue

delay. In the articles of association, the company can set even a lower threshold of

holdings that need to be notified. In Finland, shareholders can require a minority

dividend if one tenth of shareholders do so. FLLCA (§13, item 7) states that articles

of association may restrict the right to minority dividend to be decided only on the

consent of all shareholders.

Concerning institutional investors, Revised Principles (2004, pp. 36-37) do not

advocate particular investment strategies for institutional investors, and state that

they should disclose their voting policies in respect to their investments. FCGC

(2008, p. 7) notes that it may be interest of the company and the shareholders if

“the board is aware of the opinion of shareholders with significant voting rights on a

matter under preparation for the general meeting”. They also emphasize that

insider regulations of Helsinki Stock Exchange must be considered. In addition,

shareholders are allowed to communicate with each other on issues concerning

shareholder rights – except cases that may result on abuse.

36

5.2.1 General Meeting

Revised Principles (2004, p. 18) state that shareholders should be able to

participate effectively and vote in general meetings and should also be informed of

the rules. In Finland, shareholders entered into the share register before ten days

of the general meeting have the right to attend. Articles of Associations may

contain a clause of need to notify of attendance not to be later than ten days before

the meeting. Shareholders may exercise their rights via proxy and if required,

shareholder or proxy may also have an assistant at the general meeting. FLLCA

(§5, item 8) states that proxy document or otherwise reliable evidence shall be

produced by the representative. This means in practice also that the company

cannot limit the selection of proxy to their preferences.

Shareholders have the right to be timely informed on corporate changes and

should have an opportunity to participate in general meetings. FCGC

recommendation 1 on general meeting contains some obligations by the EU

directive (2007/36/EC) on the exercise of certain rights of shareholders. The aim of

the directive is to improve access to take part in voting in general meeting. The

directive has been applied in Finland; most of it was already included in the

statutory regulation. Recommendation 1 concerning general meeting includes

notion that company should make every effort to ensure possibility to participate in

the decision making of general meeting (e.g. arranging simultaneous translation in

general meeting for foreign investors). In FCGC recommendation 3, it is explained

that, by exercising shareholders right to present questions in general meeting,

owners can get detailed information on the items on the general meeting agenda.

Furthermore, recommendation 3 mentions that the presence of the auditor at the

general meeting allows shareholders to ask details on the financial statements.

37

FCGC recommendation 1 includes very detailed description on what information

should be included in the notice of the general meeting. Invitation to the annual

general meeting shall be delivered no earlier than two months and no later than

one week before the meeting. Shareholders have the right to request information

on an item on general meeting agenda or suggest a relevant item on the agenda, if

shareholder notifies the board well in advance. According to the Helsinki exchange

rules (2009, p. 39), any board’s proposals for general meeting that have a material

effect on the security’s value need to be disclosed. The proposals of board of

directors and other relevant information like annual report and auditor’s report shall

be available in the head quarters of the company or in their website. The same

information shall be sent without delay to shareholder if requested. (FLLCA §5,

item 19 and §5, item 21)

Revised Principles (2004, p. 58) do not contain exclusive recommendations of

board composition, but they take an approach of describing best practices. FLLCA

(§6, item 9 and §6, item 21) states that majority of board’s directors are appointed

by the general meeting, however company’s articles of associations may state on

another way of appointing the remaining minority. In turn, FCGC recommendation

8 emphasizes that the complete board of directors is appointed by general

meeting. For instance, the general meeting does not select the board of directors,

when there is a supervisory board that appoints the board of directors. According

to the RiskMetrics Group (2009, p. 94 of Appendix 1), it is unusual among Finnish

companies that board of directors would be appointed by anyone else than annual

general meeting. RiskMetrics Group (2009, p. 100) describe that in general the

board directors election is conducted as bundle election. Shareholders present in

the general meeting, may ask to conduct election of board of directors individually.

However, the ability to influence the result is limited unless there are alternative

director candidates. FCGC recommendation 11 advises that shareholders shall be

informed about new director candidates and their biographical details on the

company website. As a result, informed owners have a possibility to evaluate the

candidate before making decisions in the general meeting.

38

5.3 The Equitable Treatment of Shareholders

OECD’s Revised Principles emphasize that all shareholders should be treated

equally according to the share classifications, insider trading and abusive self-

dealing should not be allowed and top management and board members should

disclose to the board if they have a material interest on the matters affecting to the

corporation.

Revised Principles describe that all shares should carry the same rights, within any

series of a class. On the rule of law level, FLLCA (§3, item 3) includes

requirements on equal treatment of shareholders, unless otherwise provided in the

company’s articles of association – referring to classification of shares. FCGC

(2008, p7) notes that principle of equal shareholder rights does not prevent using

of majority rule. However, decisions favoring majority of shareholders at cost of

other shareholders is forbidden by law (see FLLCA §1, item 7). Referring to the