9th Annual Itaú BBA LatAm CEO Conference

25

1 9th Annual Itaú BBA LatAm CEO Conference in New York May, 2014

-

Upload

direcionalri -

Category

Investor Relations

-

view

141 -

download

0

Transcript of 9th Annual Itaú BBA LatAm CEO Conference

1

9th Annual Itaú BBA LatAm CEO Conference in New York May, 2014

History and Business Model

3

More Than 30 Years of History

47%

Filadélphia

Participações S.A.1 Others

53%

155,298,749 ordinary shares

1. Holding owned by Ricardo Valadares Gontijo and family

2. Data: 06/30/2013

Industrial projects acting

as contractor to third

parties

Important geographic

expansion: Brasília, Rio de

Janeiro and Campinas

Development of projects

focused on the low-income

segment

Beginning of large scale

projects for the low-income

segment

Consolidation of a leading

position in Manaus and

Brasilia

Operations expansion to

PA, RO and ES

IPO 36% annual growth

in PSV launched

(CAGR)

69% annual growth

in net revenue

(CAGR)

Follow-on

MCMV 2

Establishment of

own sales team

1981 - 2005 2006-2007 2008 2009 2010-2011 2012

Record net

revenue of R$ 1.4

Billion, a 28% YoY

growth

More than R$

1 billion on

projects delivered

during 2012

Increasing stock

liquidity

The most relevant

player in the MCMV

2nd phase Level 1

Focus on Cash

Generation and

Construction

Service business

2013

Latin American

Asia 13.8%

North American

4.1%

Europe

15.8%

Brazil

17.2%

49.1%

Free Floating ( others 53%)2

Unique Footprint Strong footprint in markets with high growth potential, low

competition and high barriers to entry Low competition in

profitable markets

Track Record in

Operating in the low-

Income segment

Over 30 years of experience

Solid track record in MCMV Level 1 projects

Low equity commitment,

solid margins and high

ROIC

Focus on Large

Scale Projects

Verticalized

Business Model

Strong expertise in large scale ventures

Own work force

Performance-based compensation

Standardized and industrialized production on-site

Large scale operations in

the low-income segments,

with strict cost control and

high margins

4

Direcional: A Unique Business Model

The most profitable

and efficient player in

the low-income sector

‘’’’

High efficiency and profitability

ROE¹ among the highest in the sector LTM ROE¹: 15%

1. LTM ROE: Net Income in the Last Twelve Months / Average Shareholders’ Equity in the Last Twelve Months (net of non-controlling interest in silent partnerships and SPEs)

The best low-income player in Brazil

Industrialization Aluminum panels and concrete walls technology

45 days to develop a five floors building

1

2

3

5

4

Focus on the Low-Income Segment

6

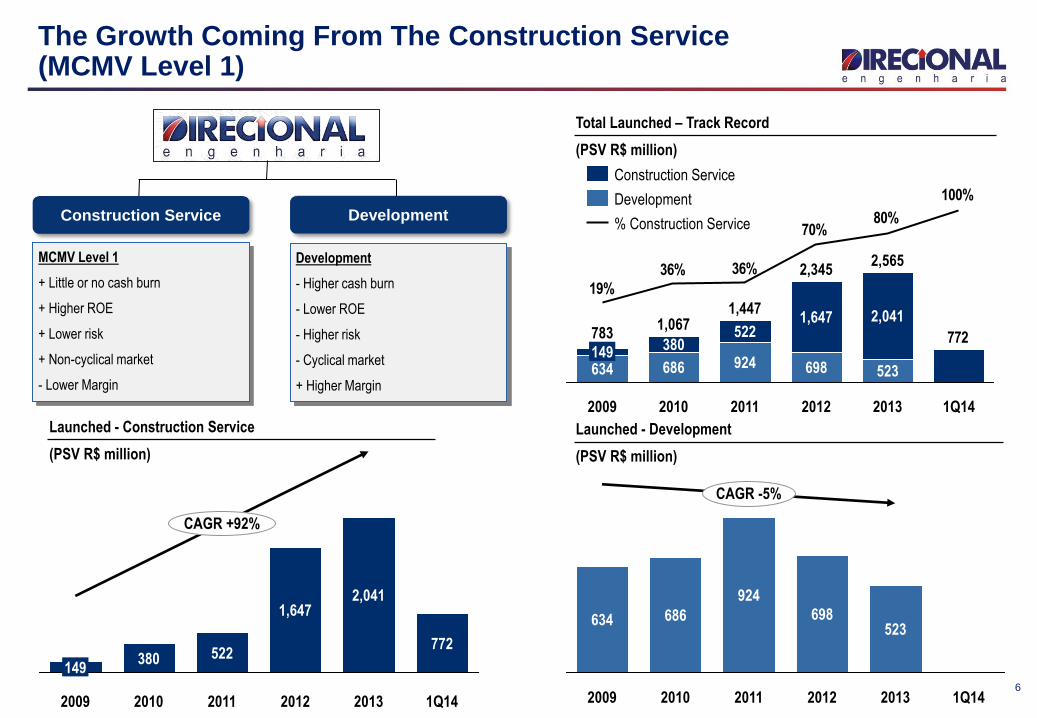

Launched - Construction Service

(PSV R$ million)

CAGR -5%

1Q14 2013

523

2012

698

2011

924

2010

686

2009

634

Launched - Development

(PSV R$ million)

CAGR +92%

1Q14

772

2013

2,041

2012

1,647

2011

522

2010

380

2009

149

Construction Service Development

MCMV Level 1

+ Little or no cash burn

+ Higher ROE

+ Lower risk

+ Non-cyclical market

- Lower Margin

Development

- Higher cash burn

- Lower ROE

- Higher risk

- Cyclical market

+ Higher Margin

Total Launched – Track Record

(PSV R$ million)

772

100%

80%70%

36%36%

19%

2013 1Q14

698

2,565

523

2,041

2012

2,345

1,647

2011

1,447

924

522

2010

1,067

686

380

2009

783

634 149

% Construction Service

Development

Construction Service

The Growth Coming From The Construction Service (MCMV Level 1)

Total Hired % Balance Concluded % %(A) (B) (C) (C/A) (C/B)

Level 1 2,000,000 1,527,379 76% 472,621 459,647 23% 30%

Level 2 1,200,000 1,294,889 100% - 935,370 78% 72%

Level 3 400,000 417,361 100% - 139,208 35% 33%

Total 3,600,000 3,239,629 472,621 1,534,225

Results MCMV (Phase 1 & 2) - Up - to Date

7

MCMV Focus Moving Towards Level 1

Program Challenges ("Ministério das Cidades")

• Hire 470k units in 2014; (ii) Quality assurance and delivery; (iii) Investments on projects sustainability; (iv) Improvements in the

construction process

Source : Ministério do Planejamento, Orçamento e Gestão 12/31/2013

Lauch Date Jul/2011 Aug/2012

Level 1 R$48 k - R$65 k R$57 k - R$76 k 17%

Level 2 and 3 R$65 k - R$170 k R$76 k - R$190 k 12%

MCMV 2MCMV 2

(after review)Unit Price D%

2,600,000

+300%

MCMV2

1,600,000

800,000

200,000

MCMV1

1,000,000

400,000

400,000

200,000

Level 1

Level 2

Level 3 The Government increased the price cap of 17% for the units within

the first level of the MCMV Program.

4x

2x

1x

• Brazil’s Federal Government has already shown that its focusing the Level 1 of MCMV, where the BZ housing deficit is heavily

concentrated.

• Such focus is clear when looking the breakdown of the Level 1 from MCMV 1 compared to MCVM 2 and its subsequent update.

8

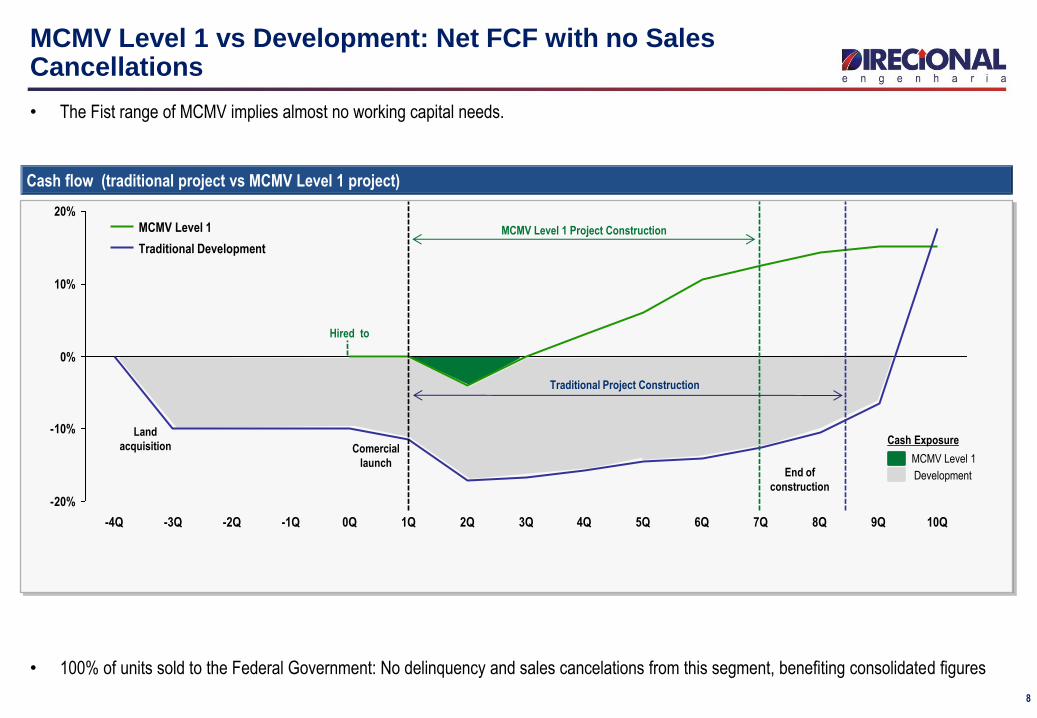

MCMV Level 1 vs Development: Net FCF with no Sales Cancellations

Cash flow (traditional project vs MCMV Level 1 project)

-20%

-10%

0%

10%

20%

0Q -1Q 10Q 9Q 8Q 7Q 6Q 5Q 4Q 3Q 2Q 1Q -2Q -3Q -4Q

Traditional Development

MCMV Level 1 MCMV Level 1 Project Construction

• 100% of units sold to the Federal Government: No delinquency and sales cancelations from this segment, benefiting consolidated figures

• The Fist range of MCMV implies almost no working capital needs.

Land

acquisition Comercial

launch End of

construction

Hired to

Traditional Project Construction

Cash Exposure

MCMV Level 1

Development

Level 1 Contracted Units Direcional Share %

MCMV 1 & 2 1,527,379 73,869 5%

MCMV 1 482,741 7,391 2%

MCMV 2 1,044,638 66,478 6%

9

MCMV: Risk of Discontinuation?

Even considering a potential reduction in the MCMV Level 1 program with a change in political parties, there should be little effect on Direcional.

There are few companies that can deliver high volumes of construction in MCMV Level 1:

MCMV 1: 23% of units launched in MCMV Level 1 were delivered

100% 76%

23%

78%

35% 100%

100%

100%

100%

Delivered Contracted Program

Level 1

Level 2

Level 3

MCMV Program Phase 1 & 2: Status

(% of Units)

Low Share: Direcional represents 5% of MCMV Level 1 as a whole

Opportunity to increase its share

+400 bps

Source : Ministério do Planejamento, Orçamento e Gestão 07/15/2013

Very Low Income Projects:

# of projects: 34

# of Units: 84,065

Total PSV: R$ 5,363.2 MM

Average PSV: R$ 157.7 MM

Average Units: 2,472

10

Direcional’s Contracted MCMV Level 1

1st Phase MCMV 2nd Phase MCMV

# of projects: 3

# of Units: 7,391

Total PSV: R$ 380.3 million

# of projects: 31

# of Units: 76,674

Total PSV: R$ 4,983.2MM

+

Direcional`s Contracted MCMV – Level 1

(PSV million)

Direcional`s Contracted MCMV – Level 1

(Units)

+437%

1Q14

772

2013

2,041

2012

1,647

2011

522

2010

380

+365%

1Q14

10,196

2013

34,372

2012

23,234

2011

8,872

2010

7,391

Focus on Industrialization

11

12

Focus on Performance

6% 5%5%

4Q13

45%

49%

7%

1Q14

4% 8%

88% 85%

10%

3Q13

84%

11%

2Q13

78%

16%

1Q13

75%

18% 7%

4Q12

70%

23%

7%

3Q12

60%

31%

9%

2Q12

56%

36%

9%

1Q12

50%

41%

8%

4Q11

49%

43%

7%

3Q11

Units Under Construction by Construction Method

(% of Units)

1 Aluminum mold and concrete walls method

Industrial Construction¹ Concrete Blocks Conventional Structure (Concrete Pillars)

1Q14 1Q13 D %

Units Under Construction 77.291 55.583 39%

% of Industrialization (# of units) 88% 75% 13 p.p.

Construction Sites 56 50 12%

Average # of Units by Construction Sites 1.380 1.112 24%

# of Cities 18 13 38%

Construction Technology

45 days to develop 2 buildings with 5 floors and 4 apartments per floor

Video: http://www.direcional.com.br/ri

Aluminum Panels and Concrete Walls

13

14

Construction Inflation (INCC) Track Record

Brazilian construction cost index, base 100 = Jan/2003

100

110

120

130

140

150

160

170

180

190

200

210

220

230

240

250

260

jan/03 jan/04 jan/05 jan/06 jan/07 jan/08 jan/09 jan/10 jan/11 jan/12 jan/13

Labor

INCC

(Aggregated Index)

Materials

Source: BACEN and IBGE

Operating and Financial Highlights

15

16

Launches

20% 14%

2012

60%

20%

2013

82%

4%

Launches by Region - Development

(% PSV)

16%43%

27%

2013

24%

30%

3%

2012

33%

24%

Launches by Region - MCMV Level 1

(% PSV)

2013:

MCMV Level 1 represented 80% of the PSV launched;

82% of the launches in the development segment were in the

southeast region.

+9%

2,565

+24%

2013

2,041

523

2012

2,346

1,647

698

Launched PSV

(R$ million)

MCMV Level 1

Development

Southeast North Northeast Midwest

Launches 1Q14

MG

RS

681,595PSV (R$'000)

Units

Granja Werneck

8,896

89,909PSV (R$'000)

Units

Irmãos Maristas

1,300

17

Net Sales and Inventory

Inventory by Region – 1Q14

(% PSV)

Inventory

(PSV - R$ million)

882

+66%

1Q14

772

110

1Q13

530

405

125

Contracted Net Sales

(PSV - R$ million)

MCMV Level 1

Development

1Q14

55.3%

14.0%

4Q13

55.1%

21.1%

3Q13

46.9%

15.4%

2Q13

49.6%

21.2%

1Q13

40.7%

15.2%

With MCMV Level 1 project

Without MCMV Level 1 project

Sales-over-supply ratio (VSO)¹

(% Total PSV)

1 - VSO ratio = Sales for the period / (Opening Inventory + Launches in the Period)

43%

20%

North

37% Southeast

Midweast

-9%

1Q14

631

452

179

2013

725

571

154

2012

800

670

130

-13.0%

Under Construction

Finished Units

18

Deliveries – 1Q14

Deliveries

(PSV Launched - R$ million)

Units

6.217 13.556

1Q14

601

2013

1.237

Delivered PSV

30%

Commercial

18%

MCMV Level 1

46%

Medium

6% Low-Income

Residencial Macapaba

Parque Carioca

Deliveries reached a record of R$ 601

million PSV in 1Q14

19

Land Bank

73% are large scale projects (over 1,000 units)

58% are eligible for the MCMV Program

82% were acquired by physical or financial Swap

Average acquisition price of 12% over PSV

R$ 7.8 Billion

52.115 units

Land Bank by Segment

(% PSV)

Land Bank Track Record in 2013

(R$ million in PSV) 194

1Q14

7,820

Review of

Assumptions

/ Traded and

Cancellation

Acquired

Land Bank

632

4Q13

7,382

Land Bank by Region

(% PSV)

Type of Payment

(1Q14 – % PSV)

Swap 81.8% Cash 18.2%

9%

Upper-Middle

2%

RET

31% Low-Income

Medium

53%

Commercial

5%

ES1%

AM10%

MG40%

RO1%

SP6%

PA7%

DF18%

GO2%

RJ15%

250

60%47%

31%24%

14%

1Q14 2013

836

2012

457

2011

269

2010

117

% of Gross Revenue

Revenue from Services

(R$ million)

Cash Generation with Growth

1 - Cash Burn: measured by the change in net debt adjusted for dividend payments and shares buyback

2 – Numbers prior to 2012 are not adjusted in accordance with the new consolidation accounting practices (IFRS 11).

1Q14

82

2013

76

2012

-183

2011

-176

2010

-283

2009

-95

Cash Burn¹,²

(R$ million)

Net Revenues - Track Record²

(R$ million)

397

2012

1,744

2012

1,449

2011

1,072

2010

782

2009

378

CAGR +66%

1Q14

Financing Pass-through (“Repasses”)

(R$ million)

633

+39%

2013

273

360

2012

455

233

222

"Associativo"

SFH Service

87%

Development 13%

Revenue to be Recognized

(% Total)

Services

R$ 4,2 Billion

Development

21

Financial Results

1. Adjusted for (non-cash) expenses with the stock option program

Adjusted¹ G&A

(R$ million)

2013

101

5.8%

2012

96

6.6%

1Q14

30

7.5%

4Q13

26

5.9%

+5%

+15%

1Q13

26

6.6%

Adjusted¹ G&A

% Net revenue

Selling Expenses

(R$ million)

+2%

-27%

2013

41

2.4%

2012

40

2.8%

1Q14

11

2.7%

4Q13

14

3.3%

1Q13

6

1.6%

Selling Expenses % Net revenue

585

4,214

+61%

1Q14

3,660

555

1Q13

2,620

2,035

MCMV Level 1

Development

Revenues to be Recognized

(R$ million)

Gross Revenue

(R$ million)

1,024

457

1Q14

414

164

250

4Q13

452

214

238

1Q13

396

+21%

-8%

2013

1,792

956

836

2012

1,482

246

150

Development

MCMV Level 1

22

Capital Structure

(R$ million)

Loans and Financing – 1Q14

(% of Debt)

1Q14

603

869

4Q13

543

890

1Q13

434

807

Cash

Gross Debt 374

Net Debt

25% 22% 16%

Net Debt / Shareholder's Equity

22

348 266

Capital Structure

Debt

(R$ million)

CRI

4%

Working Capital

2%

SFH

66%

FINAME and Leasing 5%

Debentures

23%

Net Debt

Without SFH

-310

Net Debt

266

Cash and

Cash

Equivalent

603

Debt

869

SFH

576

293

23

Improvement on DIRR3 Float

-13%

Apr.14

1.370

847

523

Mar.14

1.571

675

896

Pessoas Jurídicas

Pessoas Físicas

Number of Investors

(#)

6.043

11.789

-49%

1Q14 1Q13

Average Trading Volume

(R$ 000)

Average Trading Volume

(# of Transactions)

1.359

+52%

1Q14

2.072

1Q13

2.069

3

24

Benchmarking 2013 – Outstanding Results

Direcional: Adjusted for non-cash expenses (Stock-Options Program)

BISA3; -10%

CYRE3; 13%

EVEN3; 15%

EZTC3; 30%

GFSA3; 1%

HBOR3; 26%

MRVE3; 11%

PDGR3; -6%

DIRR3 16%

RDNI3; 12%

RSID3; 2%

TCSA3; 16%

VIVR3; -63%

SETOR; 7%

TRIS3; 6%

22%

27%

32%

37%

42%

47%

52%

-55% -35% -15% 5% 25% 45%

Net

Rev

enu

e LT

M/T

ota

l Ass

ets

Net Margin¹

Slow turnover and margin above averageSlow turnover and margin below average

Fast turnover and margin below average Fast turnover and margin above average

Company; ROE LTMSize: Leverage (Assets/Equity)

Color: Average Prince - Launched Units Last 24 months

Low - up to R$ 200k per unit

Medium - between R$ 200k and R$ 400k per unit

High - above R$ 400k per unit

Setor

18%

25

Contacts

Carlos Wollenweber CFO | IR Officer

Paulo Sousa IR Coordenador

Luiz Felipe Almeida IR Analyst

www.direcional.com.br

(55 31) 3214-6200

(55 31) 3214-6450