9 January 2015, Holland FinTech Meet Up - Innopay

17

tomorrow’s transac,ons today Digital iden,ty The mother of all transac,ons Douwe Lycklama– meetup 9 January 2015

-

Upload

holland-fintech -

Category

Economy & Finance

-

view

96 -

download

1

Transcript of 9 January 2015, Holland FinTech Meet Up - Innopay

tomorrow’s transac,ons today

R 255 G 135 B 0

R 135 G 204 B 0

R 0 G 135 B 255

Digital iden,ty The mother of all transac,ons

Douwe Lycklama– meetup 9 January 2015

R 255 G 135 B 0

R 135 G 204 B 0

R 0 G 135 B 255

2 OTA – ‘Coali,on of the willing’. Douwe Lycklama, Mounaim Cortet, Nick Smaling – 8 April. © Innopay BV. All rights reserved.

3 Digital iden,ty – Holland Fintech meetup. Mounaim Cortet. January 2015. © Innopay BV. All rights reserved.

R 255 G 135 B 0

R 135 G 204 B 0

R 0 G 135 B 255

4 Digital iden,ty – Holland Fintech meetup. Mounaim Cortet. January 2015. © Innopay BV. All rights reserved.

R 255 G 135 B 0

R 135 G 204 B 0

R 0 G 135 B 255

Dimensions of Digital Iden,ty: Func,ons, Applica,ons, Requirements

1. Func;ons: user ac,ons to access or make use of an online (self-‐) service offered by relying party

2. Applica;ons: outcomes or experience of using digital iden,y solu,ons

3. Requirements: defines key successfactors for digital iden,ty solu,ons

1. Func;ons

• Iden,fica,on • Authen,ca,on • Authoriza,on

5 Digital iden,ty – Holland Fintech meetup. Mounaim Cortet. January 2015. © Innopay BV. All rights reserved.

R 255 G 135 B 0

R 135 G 204 B 0

R 0 G 135 B 255

Three key digital iden,ty func,ons: Iden,fica,on, Authen,ca,on and Authoriza,on

Government, Business Relying party User

Consumer, Ci0zen, Business

3 func;ons

1. Iden;fica;on - This is me - This is more about

me (a7ribute x)

2. Authen;ca;on - This is really me

(iden0ty creden0als)

3. Authoriza;on - I am allowed or - I allow somebody

Name Age Address

Preferences

Balance

PIN

Place of birth

Mandates

Geoloca,on Credit ra,ng

AJributes

…

Credit card nr.

6 Digital iden,ty – Holland Fintech meetup. Mounaim Cortet. January 2015. © Innopay BV. All rights reserved.

R 255 G 135 B 0

R 135 G 204 B 0

R 0 G 135 B 255

0 140 204 140 204 0 255 140 0

Func'on

Applica;on Iden0fica0on Authen0ca0on Authoriza0on

1. Trust

2. Convenience

3. Compliance

Three key digital iden,ty applica,ons: Trust, Convenience and Compliance

Opera;ons

Legal

Digital signing

Single Sign On

Login (e.g. government, bank)

AJribute verifica;on (age check, KYC, AML)

PSD2 (‘consent’)

Data protec;on

Cookies, profiling

Sign-‐up process

Strong customer authen;ca;on

(Secure Pay)

Strong customer authen;ca;on

(Secure Pay)

7 Digital iden,ty – Holland Fintech meetup. Mounaim Cortet. January 2015. © Innopay BV. All rights reserved.

R 255 G 135 B 0

R 135 G 204 B 0

R 0 G 135 B 255

0 140 204 140 204 0 255 140 0

Three key digital iden,ty requirements: Reach, Conversion and Cost

Reach

Cost

1.

2.

3.

Conversion

Relying party:

1. Reach

Capture as many of target audience

2. Conversion

Enable trust, fast and easy use

3. Cost

Digital iden,ty solu,ons that are economical and reduce fraud

User:

1. Reach

Widely accepted solu,ons

2. Conversion

Fast and easy solu,on

3. Cost

Typically free, for businesses this may differ

8 Digital iden,ty – Holland Fintech meetup. Mounaim Cortet. January 2015. © Innopay BV. All rights reserved.

R 255 G 135 B 0

R 135 G 204 B 0

R 0 G 135 B 255

Value of digital iden,ty solu,ons is primarily determined by the ‘breadth’ and ‘depth’

Value of digital iden,ty solu,ons depend on: -‐ Breadth: number of afributes -‐ Depth: ‘level of assurance’ or certainty of single afributes

Government

Iden;ty Specialists

Banks

# AJributes (breath)

Level of Assurance (depth)

Social Media Merchants

Value

Value of digital iden;ty services

Indica;ve Non-‐exhaus;ve

Source: Innopay analysis

9 Digital iden,ty – Holland Fintech meetup. Mounaim Cortet. January 2015. © Innopay BV. All rights reserved.

R 255 G 135 B 0

R 135 G 204 B 0

R 0 G 135 B 255

Legend: Digital Idenity models (incl. roles*)

DISP

Relying party User

Iden,ty provider Broker

Processing Processing

AJribute provider

Name Address Age …

Preferences Ra,ng Bank balance

…

DISP

Trust Framework

Pladorm

‘Digital Iden,ty Solu,on’

Digital Iden,ty: ‘End-‐to-‐end trust’ is established in various models through different roles

Direct model

Plahorm model

Digital Iden,ty Service Provider

Trust Framework

Afribute provider

End-‐to-‐end trust 1.

2. 3.

4.

5.

Governance/ Business

Applica,on

Technology Level of Assurance

1.

2.

3.

4.

5.

Directory

Source: Innopay analysis

10 Digital iden,ty – Holland Fintech meetup. Mounaim Cortet. January 2015. © Innopay BV. All rights reserved.

R 255 G 135 B 0

R 135 G 204 B 0

R 0 G 135 B 255

The payment role models apply in Digital Iden,ty Iden,ty Payment Equivalent

Two sided market theory and prac,ces apply!

Direct Model

Plahorm

Network

User

User

User

Relying Party

Relying Party

Relying Party

Digital ID Provider

Digital ID Provider

Digital ID Provider

Re-‐using iden,,es of relying par,es

Digital iden,ty providers collabora,ng under a ‘trust framework’

Merchants issuing own payment method

Bank offering their own payment methods

Banks collabora,ng in offering a universal user experience for both sides of the market

Relying par,es offer own passwords and access tokens. High burden of many passwords

11 Digital iden,ty – Holland Fintech meetup. Mounaim Cortet. January 2015. © Innopay BV. All rights reserved.

R 255 G 135 B 0

R 135 G 204 B 0

R 0 G 135 B 255

DISPs reduce market fragmenta,on and increase reach of co-‐exis,ng solu,on genera,ons

3rd genera;on: Trust Framework

2000 2010 2020

Digital Iden;ty Service Providers (DISP)

2nd genera;on: Pladorm

1st genera;on: Direct model

I. ‘Open-‐up’

II. ‘interoperability’

III. ‘Simplify’

12 Digital iden,ty – Holland Fintech meetup. Mounaim Cortet. January 2015. © Innopay BV. All rights reserved.

R 255 G 135 B 0

R 135 G 204 B 0

R 0 G 135 B 255

Fragmented European digital iden,ty landscape with many government driven ini,a,ves

Observa;ons • Many government ini,a,ves

• Driven by ‘digital by default strategy’

• Banks established a strong posi,on (in Nordics)

• MNOs seek to enter the market

• Emergence of many innova,ve iden,ty providers

• DISPs connect fragmented landscape

Digital iden;ty ini;a;ves in Europe (non-‐exhaus;ve) (public and private sector providers)

Tupas

FineID

Estonian ID card

QiybankID NL

13 Digital iden,ty – Holland Fintech meetup. Mounaim Cortet. January 2015. © Innopay BV. All rights reserved.

R 255 G 135 B 0

R 135 G 204 B 0

R 0 G 135 B 255

Five (upcoming) regula,ons expected to further drive relevance of digital iden,ty

14 Digital iden,ty – Holland Fintech meetup. Mounaim Cortet. January 2015. © Innopay BV. All rights reserved.

R 255 G 135 B 0

R 135 G 204 B 0

R 0 G 135 B 255

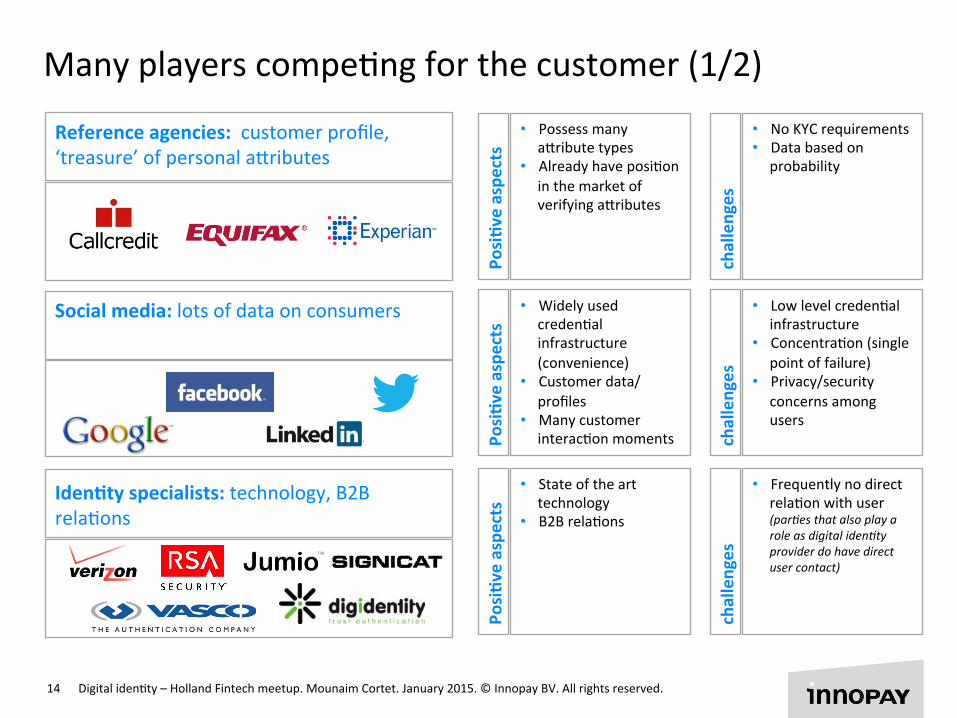

Social media: lots of data on consumers

Iden;ty specialists: technology, B2B rela,ons

Many players compe,ng for the customer (1/2)

• Low level creden,al infrastructure

• Concentra,on (single point of failure)

• Privacy/security concerns among users

challenges

• Widely used creden,al infrastructure (convenience)

• Customer data/profiles

• Many customer interac,on moments Po

si;v

e aspe

cts

• Frequently no direct rela,on with user (par0es that also play a role as digital iden0ty provider do have direct user contact)

challenges

• State of the art technology

• B2B rela,ons

Posi;v

e aspe

cts

Reference agencies: customer profile, ‘treasure’ of personal afributes

• No KYC requirements • Data based on

probability

challenges

• Possess many afribute types

• Already have posi,on in the market of verifying afributes

Posi;v

e aspe

cts

15 Digital iden,ty – Holland Fintech meetup. Mounaim Cortet. January 2015. © Innopay BV. All rights reserved.

R 255 G 135 B 0

R 135 G 204 B 0

R 0 G 135 B 255

Telco’s: customer ownership, access to trusted device

Postal services: leverage physical network, brand

Merchants: customer knowledge, brand, shopping experience

• Limited KYC requirements

challenges

• Customer ownership • Access to trusted

device (of users mobile phone and SIM card)

• Issuing process (face-‐2-‐face seong)

Posi;v

e aspe

cts

• Lack online experience and technical capabili,es (frequently partner to speed up market entrance)

challenges

• Brand • Customer

rela,onship • Leverage physical

network to issue creden,als to users directly

Posi;v

e aspe

cts

• Expensive to create proprietary creden,al infrastructure

challenges

• Customer knowledge and rela,onship

• Brand • Shopping experience

Posi;v

e aspe

cts

Many players compe,ng for the customer (2/2)

16 Digital iden,ty – Holland Fintech meetup. Mounaim Cortet. January 2015. © Innopay BV. All rights reserved.

R 255 G 135 B 0

R 135 G 204 B 0

R 0 G 135 B 255

Digital iden,ty: the mother of all transac,ons?!

tomorrow’s transac,ons today

R 255 G 135 B 0

R 135 G 204 B 0

R 0 G 135 B 255

Thank you!