8.3.4 Probabilistic Characterization of the Put Price Presenter: Chih-tai,Shen Jan,05 2012 Stat,NCU.

12

8.3.4 Probabilistic Characterization of the Put Price Presenter: Chih-tai ,Shen Jan,05 2012 Stat,NCU

-

Upload

zackery-danforth -

Category

Documents

-

view

219 -

download

0

Transcript of 8.3.4 Probabilistic Characterization of the Put Price Presenter: Chih-tai,Shen Jan,05 2012 Stat,NCU.

8.3.4 Probabilistic Characterization of the Put Price

Presenter: Chih-tai ,ShenJan,05 2012

Stat,NCU

Outline

Theorem 8.3.5Corollary 8.3.6

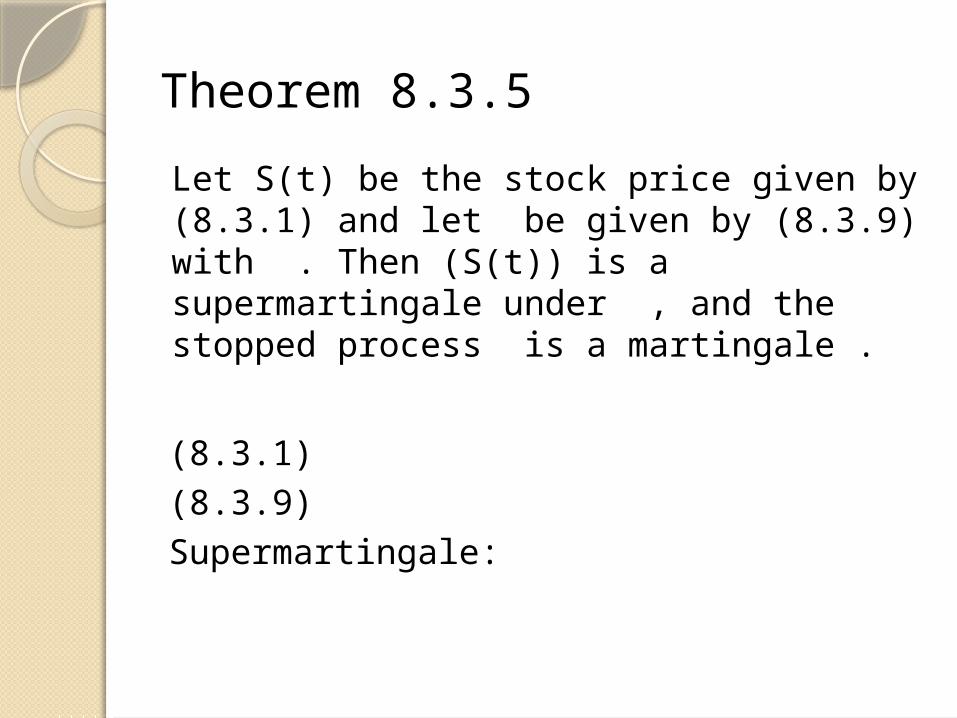

Theorem 8.3.5

Let S(t) be the stock price given by (8.3.1) and let be given by (8.3.9) with . Then (S(t)) is a supermartingale under , and the stopped process is a martingale .

(8.3.1) (8.3.9) Supermartingale:

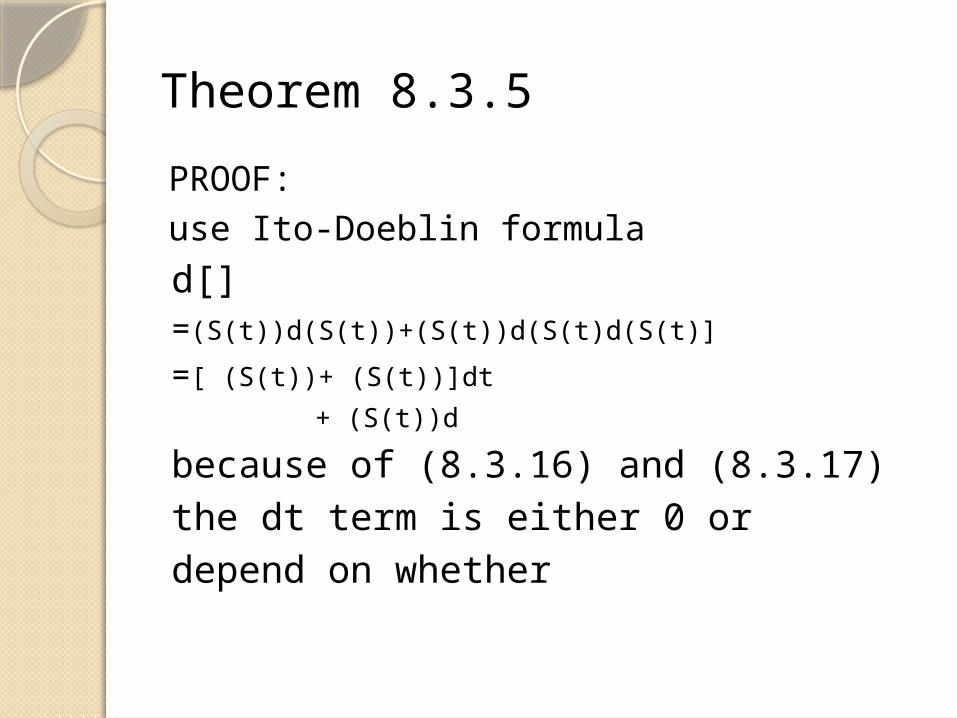

Theorem 8.3.5

PROOF:use Ito-Doeblin formula

d[]=(S(t))d(S(t))+(S(t))d(S(t)d(S(t)]

=[ (S(t))+ (S(t))]dt

+ (S(t))d

because of (8.3.16) and (8.3.17)the dt term is either 0 or depend on whether

Theorem 8.3.5Then we can get

by dt term is less than or equal to zero , is a supermartingale .

Theorem 8.3.5

When it has the downward tendency. If the initial stock price above ,then prior to the time when the stock price first reaches , the dt term in is zero and hence ) is a martingale.

Corollary 8.3.6

Recall that the set of all stopping times ,not just those of the (8.3.9) . we have

where is the initial stock price . In other words ,s the perpetual American put price of Definition 8.3.1

Corollary 8.3.6

PROOF: (i)because is a supermartingale under , we have from Theorem 8.2.4 (optional sampling) for every stopping time

Supermartingale:

*( ) max [ ( ( ))]r

Lv x E e K S

T

*

* *

( ) ( )

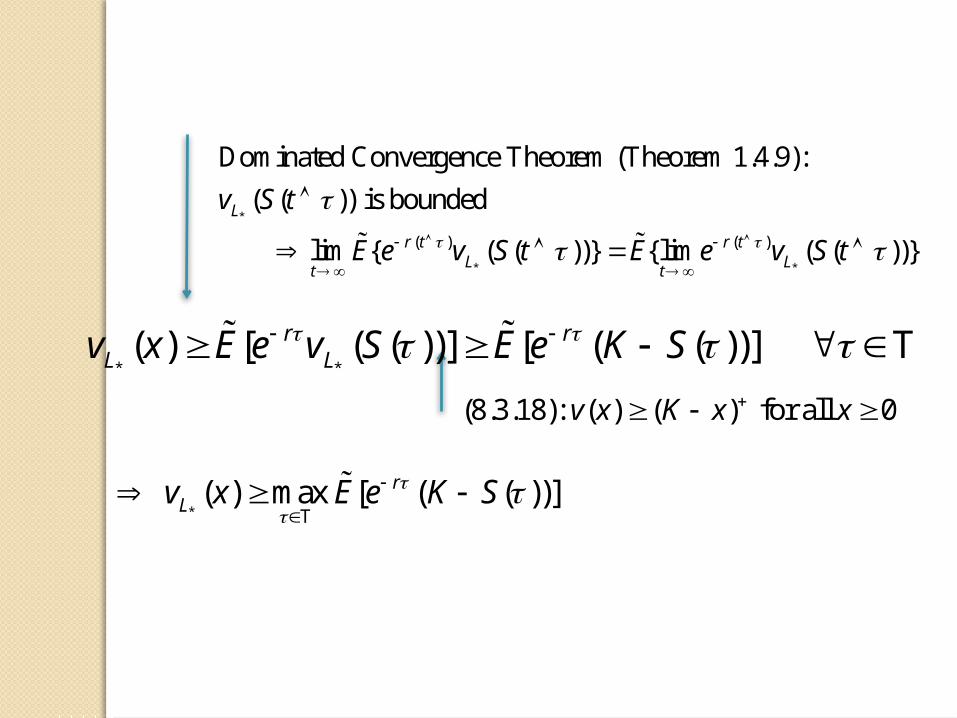

Dominated Convergence Theorem (Theorem 1.4.9):

( ( )) is bounded

lim { ( ( ))} {lim ( ( ))}

L

r t r tL L

t t

v S t

E e v S t E e v S t

* *( ) [ ( ( ))] [ ( ( ))] r r

L Lv x E e v S E e K S T

(8.3.18): ( ) ( ) for all 0 v x K x x

* ( ) max [ ( ( ))]rLv x E e K S

T

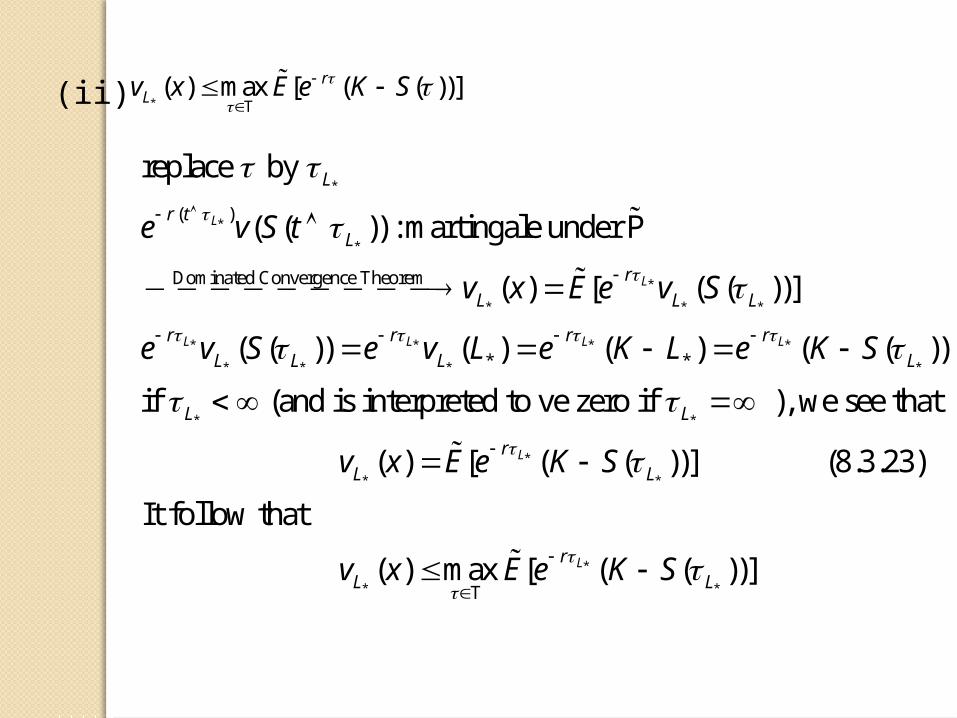

(ii)

*

*

*

*

* * *

* * * *

* * * *

*

( )

Dominated Convergence Theorem

* *

replace by

( ( )) : martingale under P

( ) [ ( ( ))]

( ( )) ( ) ( ) ( ( ))

if (and i

L

L

L L L L

L

r t

L

r

L L L

r r r r

L L L L

L

e v S t

v x E e v S

e v S e v L e K L e K S

*

*

* *

*

* *

s interpreted to ve zero if ), we see that

( ) [ ( ( ))] (8.3.23)

It follow that

( ) max [ ( ( ))]

L

L

L

r

L L

r

L L

v x E e K S

v x E e K S

T

*( ) max [ ( ( ))]r

Lv x E e K S

T

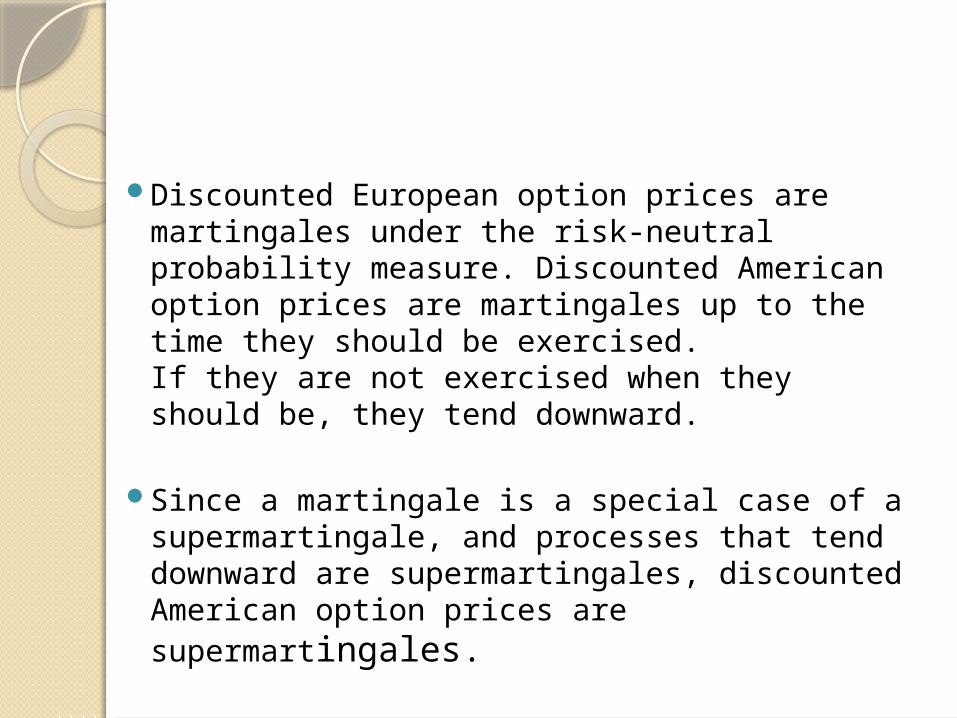

Discounted European option prices are martingales under the risk-neutral probability measure. Discounted American option prices are martingales up to the time they should be exercised. If they are not exercised when they should be, they tend downward.

Since a martingale is a special case of a supermartingale, and processes that tend downward are supermartingales, discounted American option prices are supermartingales.

THANKS YOUR ATTENTION