8-1 Lecture #6 Hedging foreign currency risk: Issues in and out of China.

38

8-1 Lecture #6 Hedging foreign currency risk: Issues in and out of China

-

Upload

claribel-mclaughlin -

Category

Documents

-

view

219 -

download

1

Transcript of 8-1 Lecture #6 Hedging foreign currency risk: Issues in and out of China.

8-1

Lecture #6

Hedging foreign currency risk: Issues in and out of

China

8-2

Currency Risk Management Forward Market Hedge (Not yet available) Money Market Hedge Options Market Hedge (Not yet available) Cross-Hedging Minor Currency Exposure Hedging Contingent Exposure Hedging Through Invoice Currency Hedging via Lead and Lag Exposure Netting Should the Firm Hedge?

8-3

Forward Market Hedge: Imports If you expect to owe foreign currency in the

future, you can hedge by agreeing today to buy the foreign currency in the future at a set price by entering into a long position in a forward contract.

Forward Contract

Counterparty

Importer

Foreign Supplier

Foreign

currencyGoods or

Services

Forei

gn

curr

ency

Domes

tic

Curre

ncy

8-4

Forward Market Hedge: Exports If you are going to receive foreign currency in

the future, agree to sell the foreign currency in the future at a set price by entering into short position in a forward contract.

Forward Contract

Counterparty

Exporter

Foreign Custome

r

Goods or

Services Foreign

CurrencyDom

estic

Curre

ncy

Forei

gn

Curre

ncy

8-5

Importer’s Forward Market Hedge

Forward Contract

Counterparty

U.S. Import

er

Italian Supplie

r

Shoes

$1,3

69,5

00

A U.S.-based importer of Italian shoes has just ordered next year’s inventory. Payment of €1M is due in one year. If the importer buys €1M at the forward exchange rate of $1.3695/€, the cash flows at maturity look like this:

8-6

Exporter’s Forward Market Cross-Currency Hedge

A firm is a U.K.-based exporter of bicycles. They have sold €750,000 worth of bicycles to an Italian retailer. Payment (in euros) is due in six months. The firm wants to hedge the receivable into pounds.

CountryU.S. $ equiv.

Currency per U.S. $

Britain $1.5905 £0.6287

1 Month Forward $1.5901 £0.6289

3 Months Forward $1.5894 £0.6292

6 Months Forward $1.5882 £0.6296

Euro $1.3435 €0.7433

1 Month Forward $1.3439 €0.7441

3 Months Forward $1.3444 €0.7438

6 Months Forward $1.3452 €0.7434

8-7

The exporter has to convert the €750,000 receivable first into pounds.

The forward six-month rate of $1.3452/€, can be used along with rate of $1.5882/£ to figure the forward euro price of the pound.

Selling the €750,000 forward at the six-month forward rate of ($1.3452/€)/($1.5882/£)=£0.846997/€ generates:

£635,247.45 = €750,000 × €1

£0.846997

At the six-month forward exchange rate €750,000 will buy £635,247.45. We can secure this trade with a LONG position in six-month pound forward contracts:

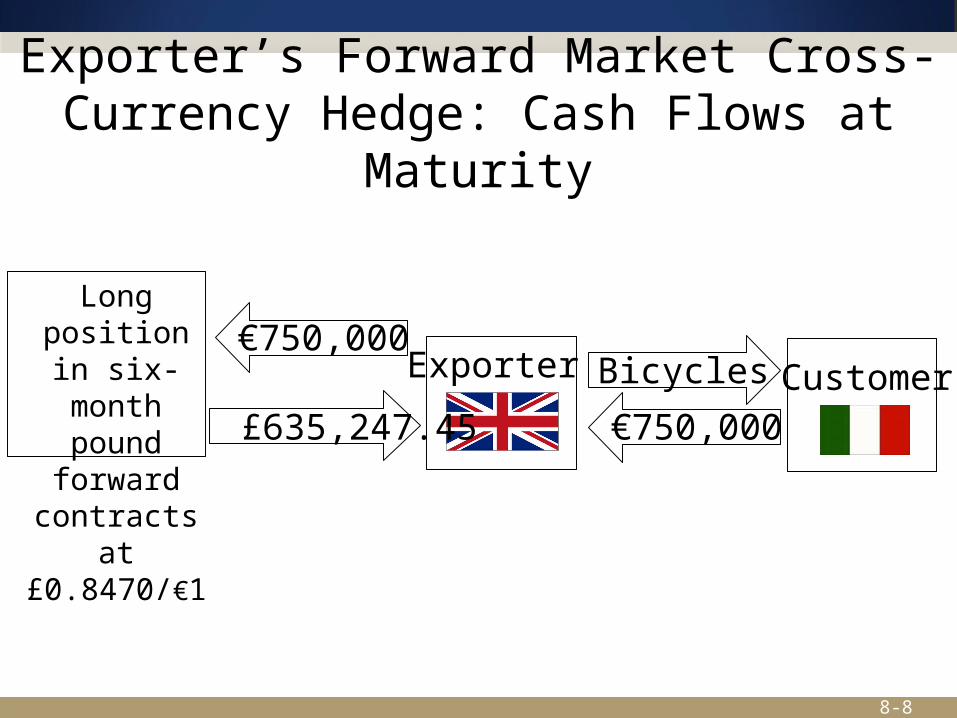

Exporter’s Forward Market Cross-Currency Hedge

8-8

Exporter’s Forward Market Cross-Currency Hedge: Cash Flows at

Maturity

Exporter Customer

€750,000

€750,000 Long position in six-month

pound forward contracts at £0.8470/€1

Bicycles

£635,247.45

8-9

Importer’s Money Market Hedge This is the same idea as covered interest

arbitrage. To hedge a foreign currency payable, buy the

present value of that foreign currency payable today and put it in the bank at interest.– Buy the present value of the foreign

currency payable today at the spot exchange rate.

– Invest that amount at the foreign rate.– At maturity your investment will have

grown enough to cover your foreign currency payable.

8-10

Importer’s Money Market HedgeA Chinese–based importer of Italian bicycles owes €100,000 to an Italian supplier in one year.– The spot exchange rate is ¥8.2344 = €1.00.– The one-year interest rate in Italy is i€ = 4%.– The importer can hedge this payable by

buying

and investing €96,153.85 at 4% in Italy for one year. At maturity, she will have €100,000 = €96,153.85 × (1.04).

¥8.2344€1.00RMB cost today = ¥791,769.23 = €96,153.85 ×

€100,0001.04€96,153.85 =

8-11

Importer’s Money Market Hedge

¥831,357.69 = ¥791,769.723 × (1.05)

With this money market hedge, we have redenominated a one-year €100,000 payable into a ¥791,769.23 payable due today.

If the Chinese interest rate is i¥ = 5%, we could borrow the ¥791,769.23 today and owe ¥831,357.69 in one year.

¥831,357.69=€100,000(1+ i€)T (1+ i¥)T×S(¥/€)×

8-12

Importer’s Money Market Hedge: Cash Flows Now and at Maturity

Importer

Supplier

bicycles

Spot Foreign Exchange

Market

€100,000

¥791,769.23

€96,153.85

CNY Bank¥8

31,3

57.6

9

Italia Bank

€100,000

T= 1 cash

flows

deposit i€ = 4%

€96,153.85

8-13

Exporter’s Money Market Hedge

Exporter

Customer

shoes

Spot Foreign Exchange

Market€100,000

$119,047.62

€95,238.10

U.S Bank$1

27,5

00.0

0

Crédit Agricole

€100,000

T= 1 cash

flows

deposit i$ = 7.10%

€95,238.10Borrow i€ = 5%

An American exporter has just sold €100,000 worth of shoes to a French customer. Payment is due in one year.Interest rates in dollars are 7.10 percent in the U.S. and 5 percent in the euro zone.The spot exchange rate is $1.25/€1.00. Use a money market hedge to eliminate the exporter’s exchange rate risk.

8-14

Examples outside of China A US firm learns in November that it will

receive £500,000 in March 2014. The firm is very concerned with exchange rate risk.– What to do? (For reference, on November

20, $ price of the pound is 1.6150)• Nothing• Sell a forward contract• Sell a futures contract• Purchase a put option.• Money market hedge as just considered

8-15

Options Contracts: Preliminaries

An option gives the holder the right, but not the obligation, to buy or sell a given quantity of an asset (in our case a currency) in the future at prices agreed upon today.

Calls vs. Puts:– Call options give the holder the right, but not the

obligation, to buy a given quantity of some asset at some time in the future at prices agreed upon today.

– Put options give the holder the right, but not the obligation, to sell a given quantity of some asset at some time in the future at prices agreed upon today.

8-16

Options Contracts: Preliminaries European versus American options:

– European options can only be exercised on the expiration date while American options can be exercised at any time up to and including the expiration date.

– American options are usually worth more than European options, other things equal.

Money– If immediate exercise is profitable, an option is

“in the money.”– Out of the money options can still have value.

7-17

PHLX Currency Option Specifications

Currency Contract Size

Australian dollar AUD 10,000

British pound GBP 10,000

Canadian dollar CAD 10,000

Euro EUR 10,000

Japanese yen JPY 1,000,000

Mexican peso MXN 100,000

New Zealand dollar

NZD 10,000

Norwegian krone NOK 100,000

South African rand

ZAR 100,000

Swedish krona SEK 100,000

Swiss franc CHF 10,000

8-18

Options Call and put options, summary

– Call gives the option to buy– Put gives the option to sell

The price at which an option would be exercised is known as the “strike price.”– If the future exchange rate exceeds the strike price:

• Call option is exercised (prefer to buy at the lower price).• Put option is not exercised (prefer to sell at the higher

price)

A premium must be paid no matter what.– Notice for the puts, premium increases with the

strike price (better chance of being exercised)… Opposite is true for a call.

8-19

OPTIONSPremium Strike Last

March 22 0.45 152.00

March 22 0.55 153.0

March 22 0.67 154.0

March 22 0.80 155.0

March 22 0.98 156.0

March 22 1.18 157.0

March 22 1.43 158.0

March 22 1.73 159.0

March 22 2.09 160.0

March 22 2.50 161.0

March 22 2.95 162.0

March 22 3.70 163.0

March 22 4.40 164.0

8-20

Possibilities The premium must be paid no matter what. Suppose we select an option with a strike price

of 160. Premium is 2.09 cents per pound: 3 possibilities (written before the start of class).

– On March 22, 2014, dollar price of the pound is less than $1.5791.

– On March 22, 2014, spot dollar price of the pound is between $1.5791 and $1.60

– On March 22, 2014, spot dollar price of the pound is greater than $1.60

8-21

In the money Scenario 1: Suppose S($/£)=$1.50:

– Pay 0.0209*500,000=$10,450 upfront– Sell pounds at $1.60 in spot: $800,000– Total Proceeds: $789,550– Without an option: $500,000 *1.50=$750,000

Scenario 2: Suppose S($/£)=$1.58– Pay 0.0209*500,000=$10,450 upfront– Sell pounds at $1.60 in spot: $800,000– Total Proceeds: $789,550– Without an option: $790,000

8-22

Out of the money. Anytime the future spot rate exceeds $1.60, the

option expires worthless. We always pay the premium of $10,450 regardless.

Summary:– Exchange rate less than $1.5791: the option is

exercised. Total benefit, ignoring lost interest (of $10,450) is highest for the option.

– Exchange rate between $1.5791 and $1.60. The option is exercised, but we would have been better off without one.

– Exchange rate greater than $1.60. Options expires worthless. Better off without and option.

8-23

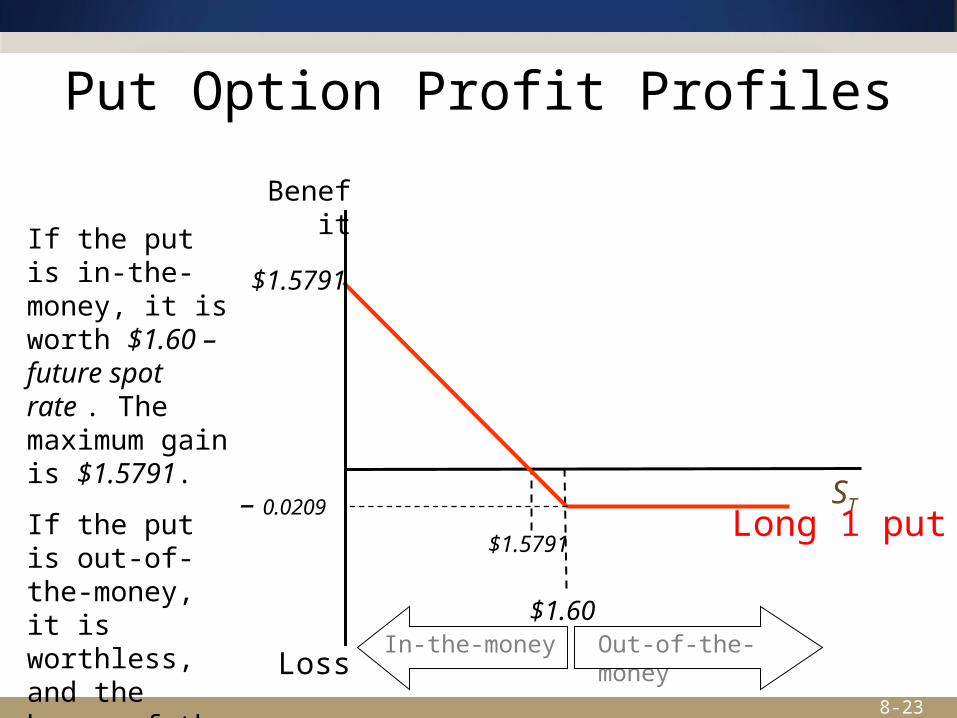

Put Option Profit Profiles

$1.60

ST

Benefit

Loss

– 0.0209

$1.5791Long 1 put

$1.5791

If the put is in-the-money, it is worth $1.60 – future spot rate . The maximum gain is $1.5791.

If the put is out-of-the-money, it is worthless, and the buyer of the put loses her entire investment of $0.0209.

Out-of-the-moneyIn-the-money

8-24

Futures Contracts: Preliminaries

Standardizing features:– Contract size– Delivery month– Daily resettlement

Initial performance bond (about 2 percent of contract value, cash or T-bills)

8-25

Currency Futures Markets The CME Group (formerly Chicago Mercantile Exchange) is

by far the largest currency futures market. CME hours are 7:20 a.m. to 2:00 p.m. CST Monday-Friday. Extended-hours trading takes place Sunday through

Thursday (local) on GLOBEX i.e. from 5:00 p.m. to 4:00 p.m. CST the next day.

The Singapore Exchange offers interchangeable contracts. There are other markets, but none are close to CME and

SIMEX trading volume. Expiry cycle: March, June, September, December. The delivery date is the third Wednesday of delivery month. The last trading day is the second business day preceding

the delivery day.

8-26

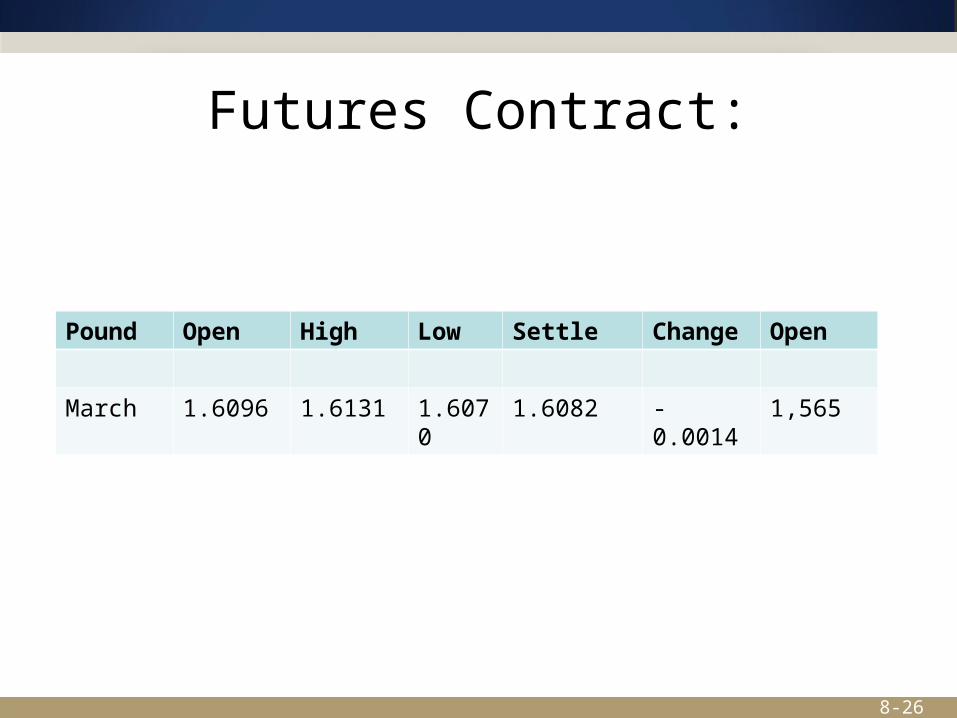

Futures Contract:

Pound Open High Low Settle Change

Open

March 1.6096 1.6131 1.6070

1.6082 -0.0014 1,565

8-27

Details An initial deposit of usually 2% or more is required. Recall, the contract is marked to market every day. Futures contract are not very convenient for

hedging purposes, but can be used nonetheless. Suppose the future’s contract is purchased at the

settlement price of $1.6082.

– Two possibilities: In March $ price of the pound:• $1.55• $1.65

8-28

Scenarios First scenario:

– Settlement price will converge to the spot rate at the moment the contract matures:

– Because we are selling pounds, and the dollar price of the pound drops, money is added to the trader’s account:• ($1.6082-1.55)*500,000= $29,100• Sell pounds at $1.55: $775,000• TOTAL: $804,100 = 500,000 * 1.6082

8-29

Second scenario If future spot rate ends up being $1.65…

– Over the life of the contract, ($1.65-$1.6082)*500,000 = $20,900 is subtracted.

– Will require potentially costly funds to be deposited if the position remains open.

In March, sell pounds for 1.65:– 500,000*1.65 = $825,000– TOTAL proceeds: 825,000 – 20,900 =

$804,100.

8-30

Yuan non-deliverables Example: In November a Chinese firm

wrote a contract so that they will receive $1,000,000 for exported goods in 6 months.

But, the yuan may continue appreciating. What to do?

– While potentially costly, a yuan NDF is available. How do they work?

8-31

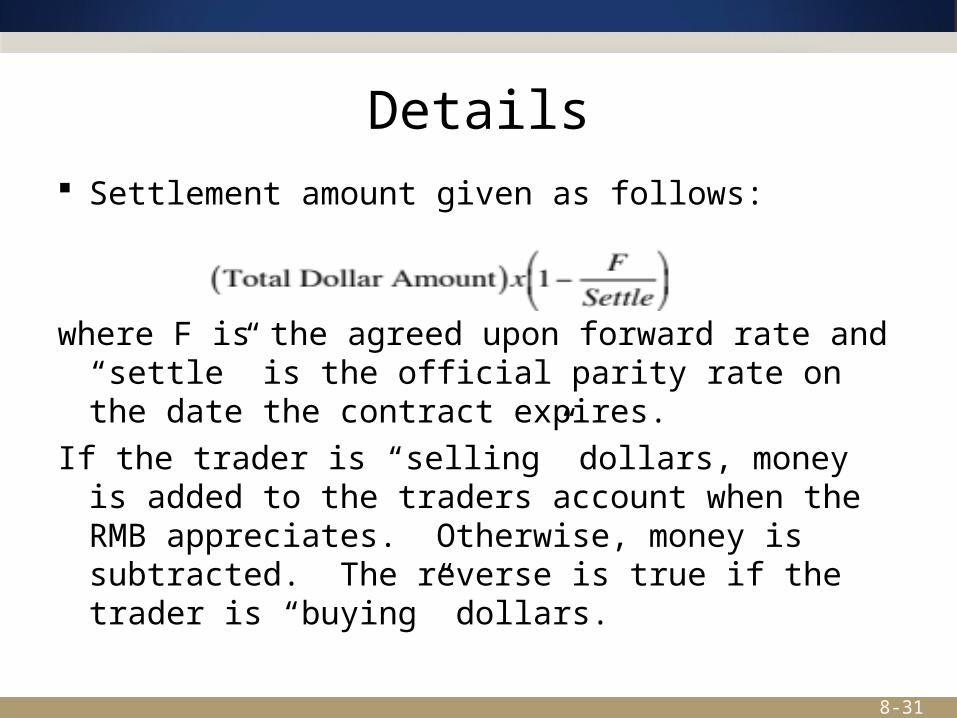

Details Settlement amount given as follows:

where F is the agreed upon forward rate and “settle” is the official parity rate on the date the contract expires.

If the trader is “selling” dollars, money is added to the traders account when the RMB appreciates. Otherwise, money is subtracted. The reverse is true if the trader is “buying” dollars.

8-32

Example continued On November 23, 2013, the 6 month NDF

rate was 6.1440. Suppose in 6 months, the RMB price of the

dollar is RMB 5.98. The hedge would be quite useful.

Note, the trader will still be required to sell dollars in the spot market: – Proceeds: 5.98 * $1,000,000 = RMB

5,980,000 But, the trader will have a dollar payment of:

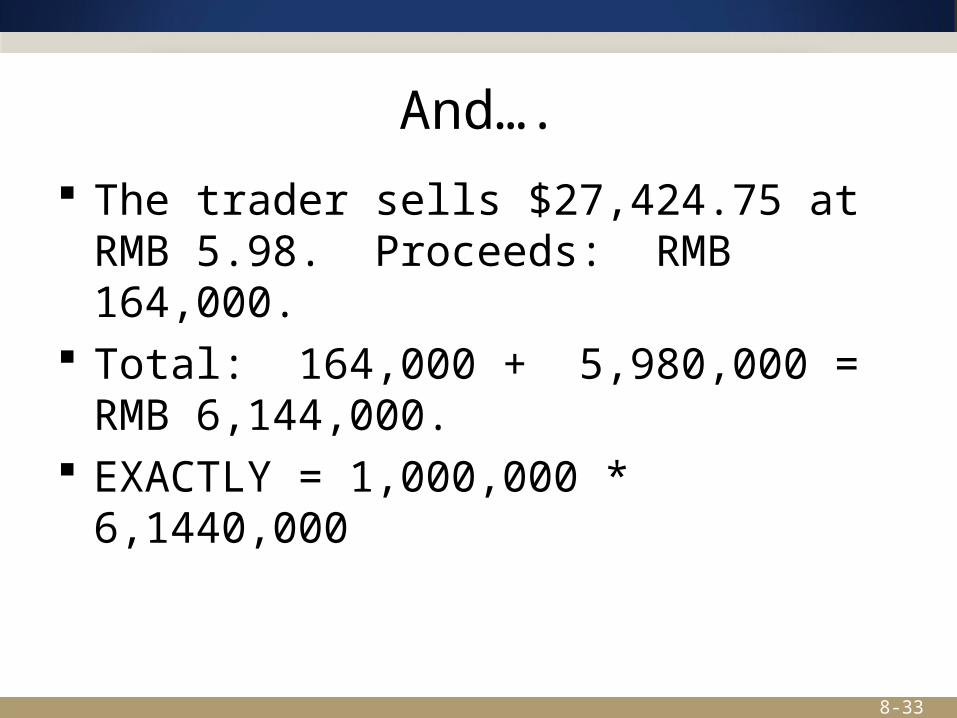

8-33

And….

The trader sells $27,424.75 at RMB 5.98. Proceeds: RMB 164,000.

Total: 164,000 + 5,980,000 = RMB 6,144,000.

EXACTLY = 1,000,000 * 6,1440,000

8-34

Cross-Hedging Minor Currency Exposure

The major world currencies are the U.S. dollar, Canadian dollar, British pound, euro, Swiss franc, Mexican peso, and Japanese yen… (and maybe soon to be the yuan).

Other currencies may be minor (for example, the Swedish krona).

It is difficult, expensive, and sometimes even impossible to use financial contracts to hedge exposure to minor currencies.

8-35

Cross-Hedging Minor Currency Exposure

Cross-hedging involves hedging a position in one asset by taking a position in another asset.

The effectiveness of cross-hedging depends upon how well the assets are correlated.– An example would be a U.S. importer with

liabilities in Swedish krona hedging with long or short forward contracts on the euro. If the krona is expensive when the euro is expensive, or even if the krona is cheap when the euro is expensive, it can be a good hedge. But they need to co-vary in a predictable way.

8-36

Exposure Netting A multinational firm should not consider deals in

isolation, but should focus on hedging the firm as a portfolio of currency positions.

Once the residual exposure is determined, we hedge that. Multilateral netting is an efficient and cost-effective

mechanism for settling foreign exchange transactions and thus determining the firm’s residual exposure.

Illustration:– For imported goods, a Chinese firm must pay

€1,000,000 in 6 months.– A different division of the same Chinese firm will

receive payment of €750,000 for exported goods in 6 months.

• The Chinese firm is only exposed to a net short position of €250,000.

8-37

Other Hedging Strategies Hedging through invoice currency.

– The firm can shift, share, or diversify:• Shift exchange rate risk by invoicing foreign sales in home

currency• Share exchange rate risk by pro-rating the currency of the

invoice between foreign and home currencies• Diversify exchange rate risk by using a market basket index

Hedging via lead and lag.– If a currency is appreciating, pay those bills denominated in

that currency early; let customers in that country pay late as long as they are paying in that currency.

– If a currency is depreciating, give incentives to customers who owe you in that currency to pay early; pay your obligations denominated in that currency as late as your contracts will allow.

8-38

What Risk Management Products do Firms Use?

Most U.S. firms meet their exchange risk management needs with forward, swap, and options contracts.

The greater the degree of international involvement, the greater the firm’s use of foreign exchange risk management.