![[Albania] New Albania I.pdf](https://static.fdocuments.net/doc/165x107/544cfeb4b1af9f710c8b499e/albania-new-albania-ipdf.jpg)

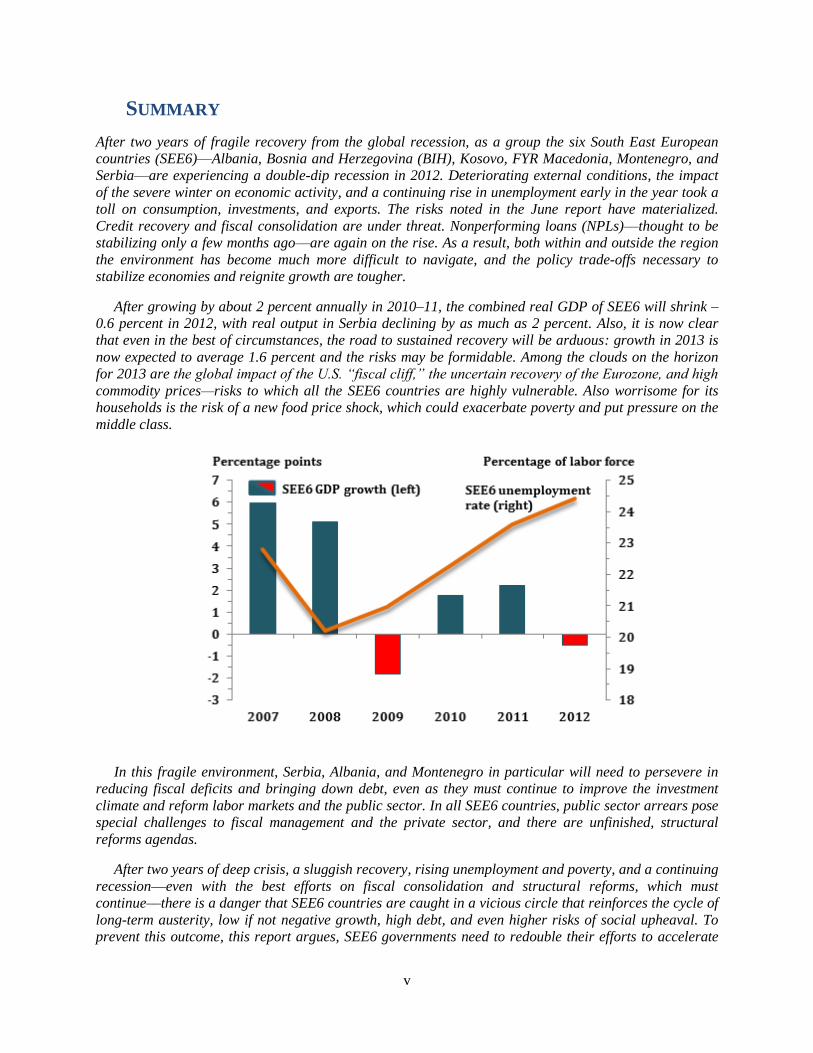

67 SEE6 GDP growth (left) SEE6 unemployment 25 24 ... SUMMARY After two years of fragile recovery...

59

South East Europe Regular Economic Report No.3 From Double-Dip Recession to Accelerated Reforms Pre-launch copy; December 15, 2012 Launch: December 18, 2012 www.worldbank.org/eca/seerer 18 19 20 21 22 23 24 25 -3 -2 -1 0 1 2 3 4 5 6 7 2007 2008 2009 2010 2011 2012 Percentage points Percentage of labor force SEE6 GDP growth (left) SEE6 unemployment rate (right) Poverty Reduction and Economic Management Unit Europe and Central Asia Region

Transcript of 67 SEE6 GDP growth (left) SEE6 unemployment 25 24 ... SUMMARY After two years of fragile recovery...

South East Europe Regular

Economic Report

No.3

From Double-Dip Recession to

Accelerated Reforms

Pre-launch copy; December 15, 2012

Launch: December 18, 2012

www.worldbank.org/eca/seerer

18

19

20

21

22

23

24

25

-3

-2

-1

0

1

2

3

4

5

6

7

2007 2008 2009 2010 2011 2012

Percentage points Percentage of labor force

SEE6 GDP growth (left) SEE6 unemploymentrate (right)

Poverty Reduction and Economic Management Unit

Europe and Central Asia Region

SOUTH EAST EUROPE:

REGULAR ECONOMIC REPORT No. 3

From Double-Dip Recession

to Accelerated Reforms

December 18, 2012

i

TABLE OF CONTENTS

RECENT ECONOMIC DEVELOPMENTS, OUTLOOK, AND POLICY CHALLENGES

MANAGING VULNERABILITY TO NEW FOOD PRICE SHOCKS IN SEE6 COUNTRIES

1. RECENT DEVELOPMENTS, OUTLOOK, AND POLICY CHALLENGES ...................... 1

A. EUROZONE IN RECESSION, NEW GLOBAL RISKS ................................................................. 1

B. GROWTH IN SEE6—A DOUBLE-DIP RECESSION ................................................................... 3

C. LABOR MARKETS––A CONTINUING CRISIS ........................................................................... 6

D. TRADE AND EXTERNAL DEBT—WORSENING .................................................................... 15

E. FISCAL POLICY––RISING DEFICITS, DEBT, AND ARREARS ............................................. 20

F. FINANCIAL SECTOR––CONTINUED VULNERABILITY ...................................................... 25

G. STRUCTURAL ISSUES: THE SEE6 ENVIRONMENT FOR DOING BUSINESS ................... 28

H. STRUCTURAL ISSUES: THE SECOND WAVE OF PRIVATIZATION? ................................. 30

I. STRUCTURAL ISSUES: ENERGY INFRASTRUCTURE DEFICIT ......................................... 32

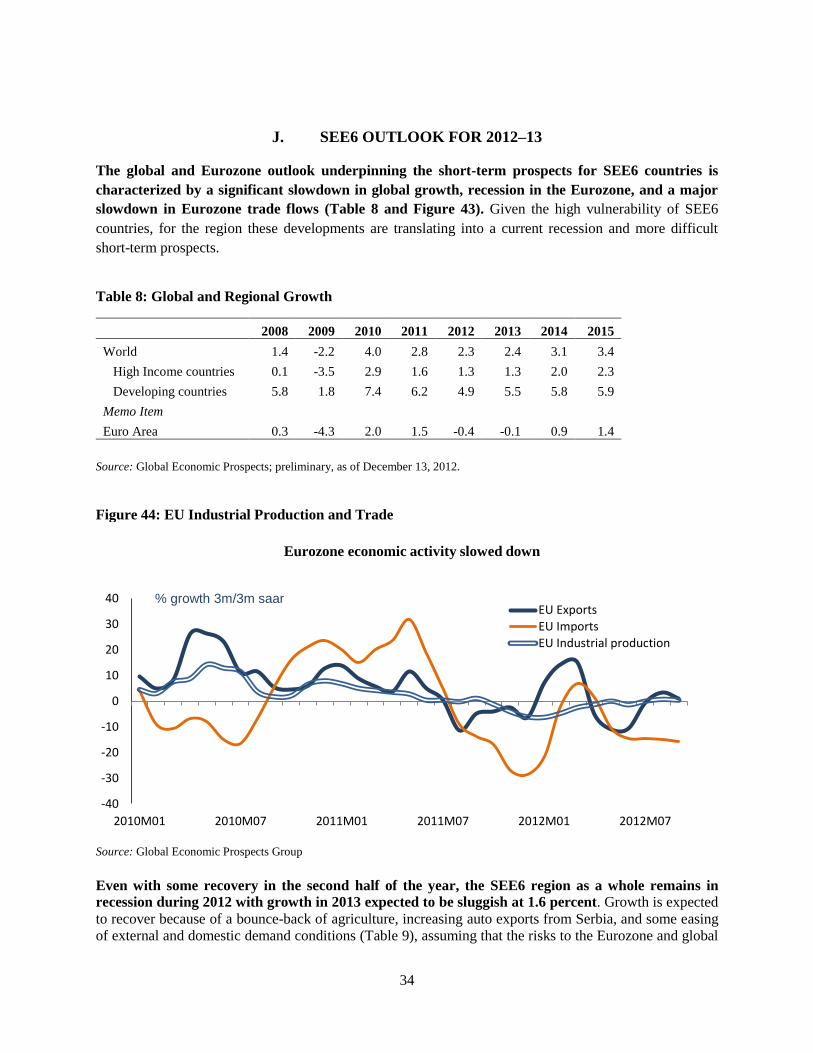

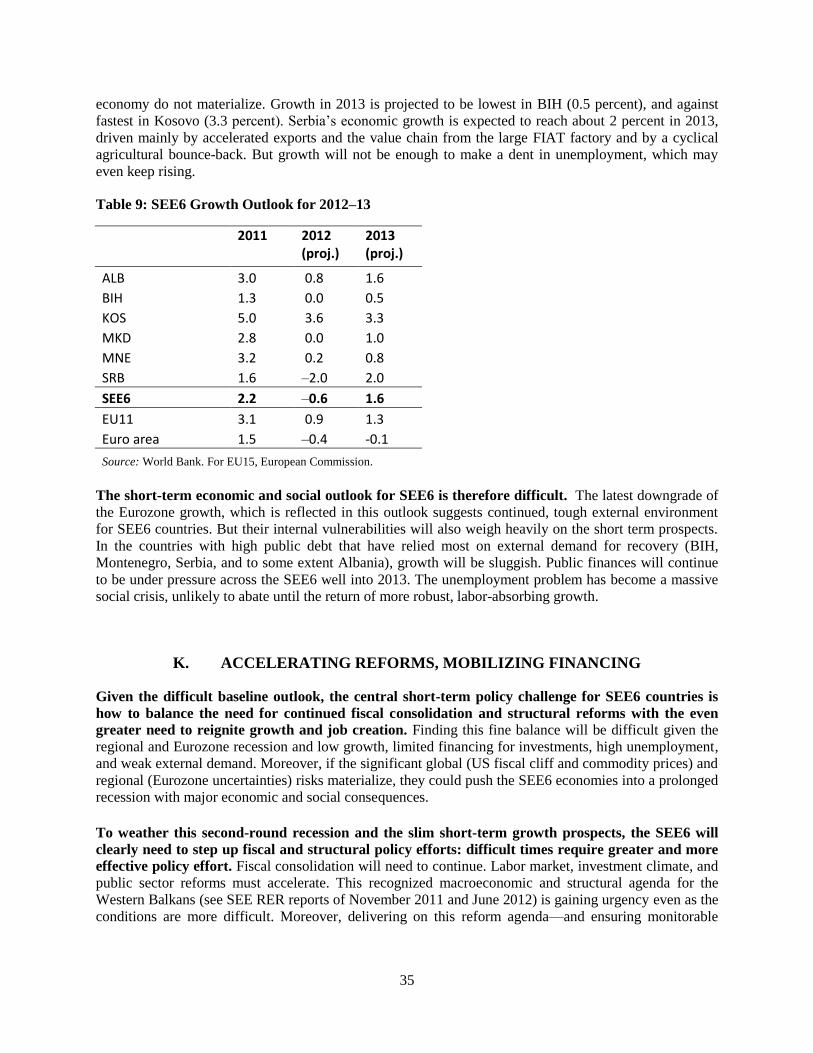

J. SEE6 OUTLOOK FOR 2012–13 ................................................................................................... 34

K. ACCELERATING REFORMS, MOBILIZING FINANCING ...................................................... 35

2. MANAGING VULNERABILITY TO FOOD PRICE SHOCKS IN THE SEE6 ................ 37

A. INTRODUCTION .......................................................................................................................... 37

REFERENCES ............................................................................................................................. 49

Figures

Figure 1: Financial Markets Developments .................................................................................................. 2

Figure 2: Global Industrial Production ......................................................................................................... 2

Figure 3: Global Growth Assumptions ......................................................................................................... 3

Figure 4: SEE6: Inflation––CPI and Food (Percent) .................................................................................... 6

Figure 5: Change in SEE6 Unemployment Rates, 2008 and 2012 (Percentage points)* ............................. 7

Figure 6: Unemployment Rates, SEE6 and EU10 ........................................................................................ 7

Figure 7: Registered Unemployed in 2011 (January 2011 = 100) ................................................................ 8

Figure 8: Employment Rates in SEE6 (2011–2012), in percent ................................................................... 9

Figure 9: Gross Average Nominal Wage Changes (January 2011 = 100) .................................................. 10

Figure 10: Employment and Real Wage Index (December 2010 = 100) .................................................... 10

Figure 11: SEE6 Difficulty of Hiring Workers ........................................................................................... 13

ii

Figure 12: SEE6 Premiums on Night Shift and Work on Rest Days .......................................................... 13

Figure 13: Redundancy Costs and Notification Requirements ................................................................... 14

Figure 14: The WEF Labor Efficiency Index, 2012–13 ............................................................................. 14

Figure 15: Exports (% of GDP) .................................................................................................................. 15

Figure 16: Growth in Exports to SEE6 (%) ................................................................................................ 16

Figure 17: Export Growth, SEE6 and EU (%) ............................................................................................ 16

Figure 18: Exports and Economic Growth (%)........................................................................................... 16

Figure 19: Import Growth (%) .................................................................................................................... 16

Figure 20: Export and Import Growth (% y-o-y) ........................................................................................ 17

Figure 21: CAD and Trade Balance (% of GDP) ....................................................................................... 17

Figure 22: CAD by Country (% of GDP) ................................................................................................... 17

Figure 23: Worker Remittances 2008–2011 (% of GDP) ........................................................................... 18

Figure 24: Foreign Direct Investment (net, % GDP) .................................................................................. 19

Figure 25: FDI per Capita (net, US$) ......................................................................................................... 19

Figure 26: SEE6 External Debt (Average, percent of GDP) ...................................................................... 19

Figure 27: Total International Bonds Outstanding, Select SEE6 Countries (US$ million) ........................ 19

Figure 28: Total Public and Private External Debt Through June 2012 (% of GDP) ................................. 20

Figure 29: Growth and Structural Balance (unweighted; percent of GDP) ................................................ 21

Figure 30: Structural Balance, 2005–11, (percent of GDP) ........................................................................ 21

Figure 31: SEE6 Real Revenues, 2008–12 ................................................................................................. 22

Figure 32: SEE6 Real Expenditures, 2008-12 ............................................................................................ 22

Figure 33: Public Debt and Guarantees (percent of GDP) .......................................................................... 24

Figure 34: International Claims (% of GDP, 2012Q2) ............................................................................... 25

Figure 35: Foreign Currency Loans (% of total, 2012Q3) .......................................................................... 25

Figure 36: Credit Growth (% change, Q-on-Q) .......................................................................................... 26

Figure 37: NPLs (% of Total Loans) and Provisioning (% of NPLs, 2012Q3) .......................................... 26

Figure 38: Capital Adequacy Ratios and Return ........................................................................................ 27

Figure 39: Loan-to-Deposit Ratios (%, 2012Q3) ........................................................................................ 27

Figure 40: SEE6 Ease of Doing Business, 2011-13 .................................................................................... 29

Figure 41: SEE6 Weak Areas in the Business Environment 2012 ............................................................. 30

Figure 42: Current and forecast power imports (GWh) .............................................................................. 33

Figure 43: EU Industrial Production and Trade .......................................................................................... 34

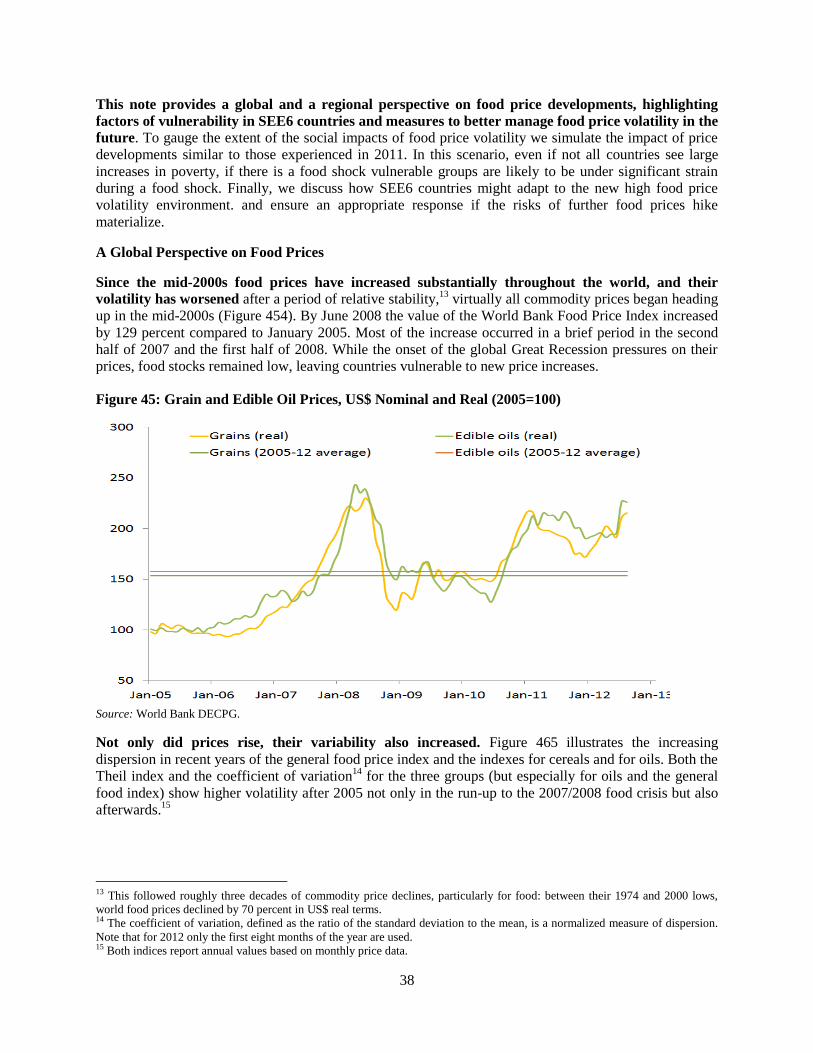

Figure 44: Grain and Edible Oil Prices, US$ Nominal and Real (2005=100) ............................................ 38

Figure 45: Price Volatility: Annual Coefficient of Variation and Theil Index of Food Prices, 1990–201239

Figure 46: Prices of Maize and Wheat Future (US cents per bushel) ......................................................... 40

Figure 47: Food price indices for SEE countries, y-o-y .............................................................................. 41

Figure 48: Household Vulnerability to Global Food Price Shocks, EU and Europe and Central Asia ...... 43

Figure 49: Food Budget Shares by Consumption Decile ............................................................................ 44

Figure 50: Change in the Budget Share of food due to a 5 percent Increase in the Food Price Index

(percentage points) ...................................................................................................................................... 46

Figure 51: Targeting, coverage and generosity of social assistance in the Western Balkans ..................... 47

iii

Tables

Table 1: South East Europe Six: Real Economic Growth, 2009–12 ............................................................. 4

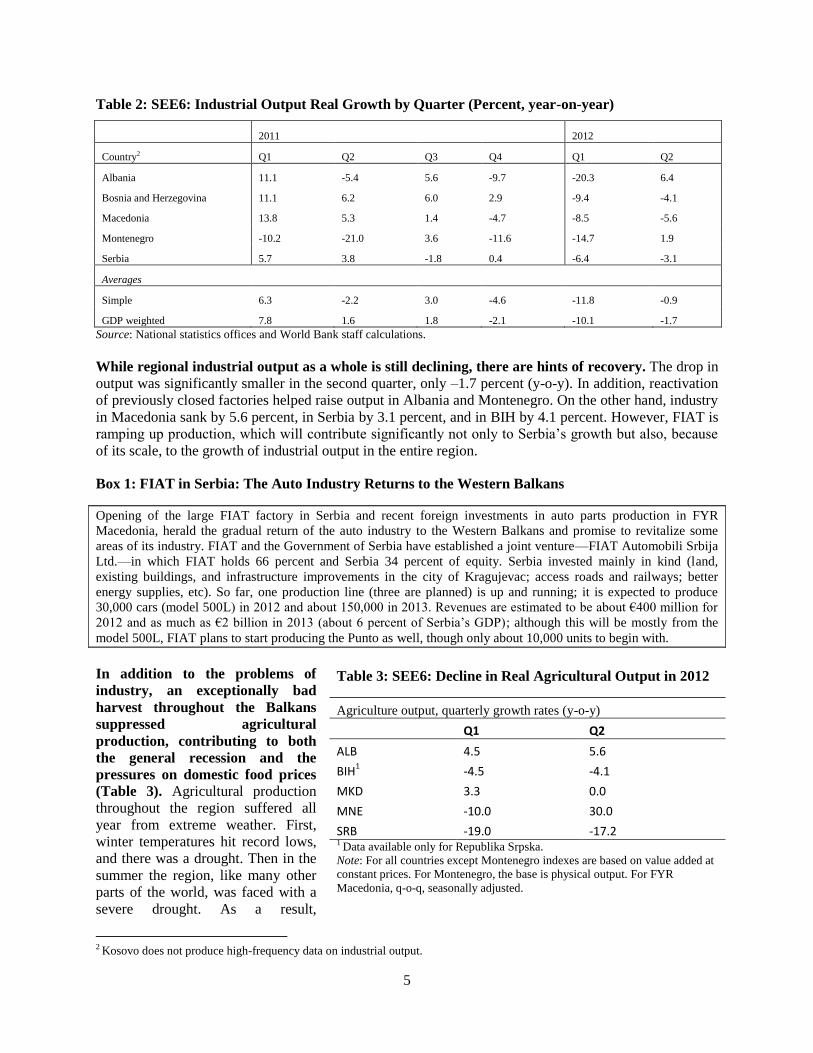

Table 2: SEE6: Industrial Output Real Growth by Quarter (Percent, year-on-year) .................................... 5

Table 3: SEE6: Decline in Real Agricultural Output in 2012 ....................................................................... 5

Table 4: SEE6 Fiscal Balances, 2008–12 (% GDP) ................................................................................... 20

Table 5: SEE6: Sovereign Credit Ratings1.................................................................................................. 24

Table 6: Key Macro Indicators (2012 projections, % of GDP) and Financial Safety Net Issues ............... 27

Table 7: Announced Privatizations in the Western Balkans ....................................................................... 31

Table 8: Global and Regional Growth ........................................................................................................ 34

Table 9: SEE6 Growth Outlook for 2012–13 ............................................................................................. 35

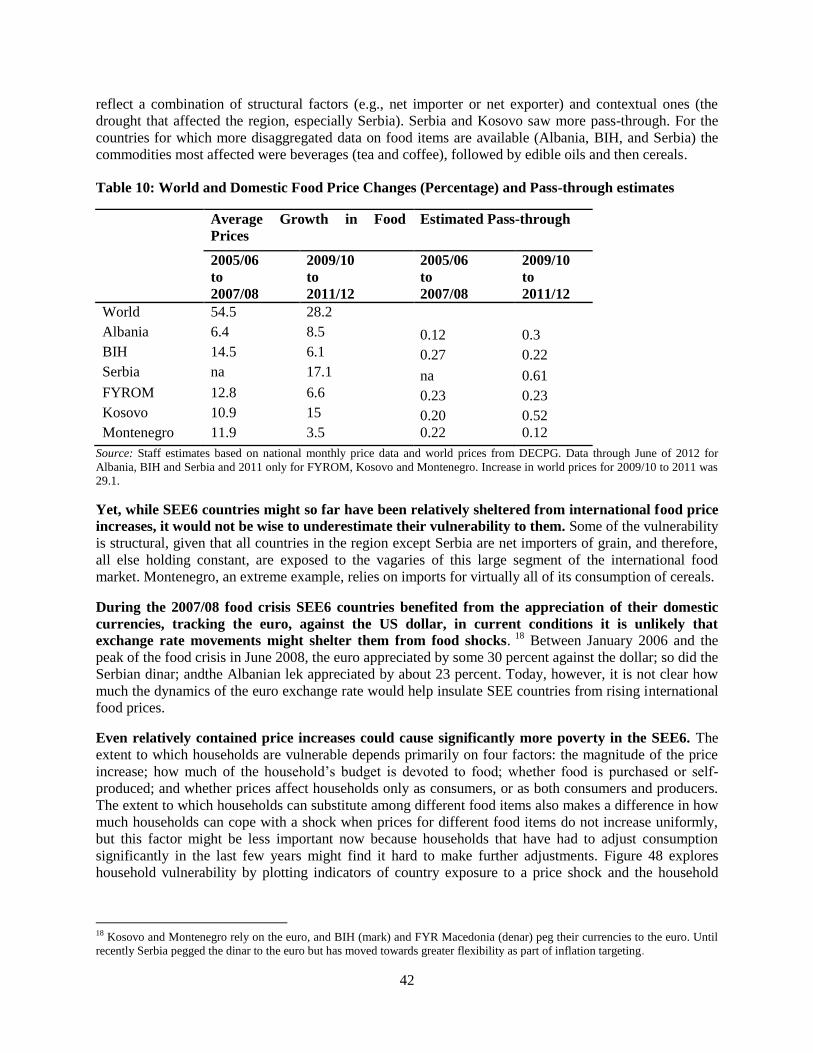

Table 10: World and Domestic Food Price Changes (Percentage) and Pass-through estimates ................ 42

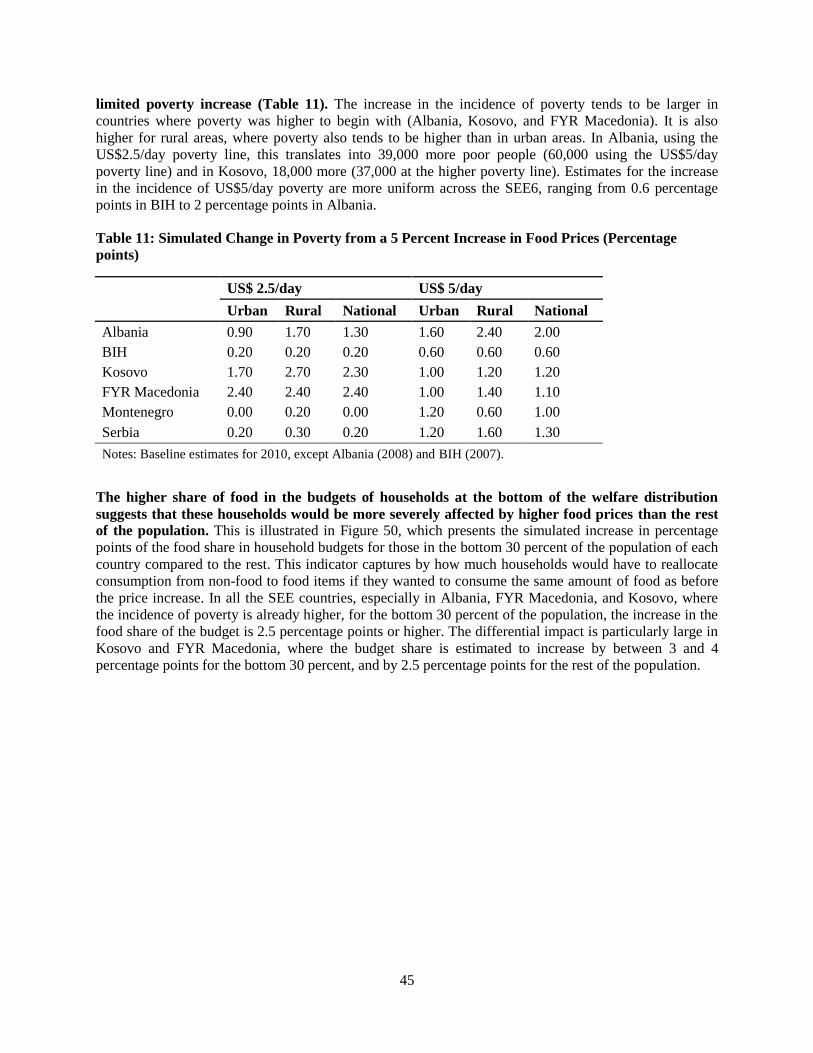

Table 11: Simulated Change in Poverty from a 5 Percent Increase in Food Prices (Percentage points) .... 45

Boxes

Box 1: FIAT in Serbia: The Auto Industry Returns to the Western Balkans ................................................ 5

Box 2: Soaring Unemployment in Serbia ..................................................................................................... 8

Box 3: World Development Report on Jobs: Implications for Labor Market Policies ............................... 12

Box 4: Tax and Expenditure Arrears: A Growing Cause for Concern ....................................................... 23

Box 5: Assumptions Underlying Estimated Poverty Impacts ..................................................................... 44

iv

This report is produced twice a year by staff economists at the World Bank Europe and Central Asia region Poverty

Reduction and Economic Management Department (ECA PREM). This and previous reports may be found at the

www.worldbank.org/eca/seerer website. The authors’ team is led by Željko Bogetić ([email protected]) and

includes the following team members with thematic assignments: Dilek Aykut (global developments and outlook);

Alexandru Cojocaru (special topic note on food prices); Damir Ćosić (financial sector; Bosnia and Herzegovina);

Simon Davies (fiscal and debt); Mike Edwards (financial sector); Agim Demukaj (external sector, Kosovo); Borko

Handjiski (labor markets, Bosnia and Herzegovina); Caterina Ruggeri Laderchi (special topic note on food prices);

Erjon Luci (SEE6 countries database manager, Albania); Sanja Madzarević-Sujster (Montenegro and SEE6

structural reforms); Lazar Sestović (real economy, Serbia); Bojan Shimbov (privatization, doing business, FYR

Macedonia); and Kenneth Simler (special topic on food prices). Carolina Sanchez-Paramo and Indhira Vanessa

Santos contributed to the section on labor markets. Arturo Rivera prepared the box on energy infrastructure and

Javier Suarez contributed to the box on lessons of privatizations. Maria Andreina Clower and Mismake Galatis

provided team assistance.

Dissemination of the report and external and media relations is managed by an EXR team including Lundrim Aliu,

Denis Boskovski, Ana Gjokutaj, Jasmina Hadzić, Andrew Kircher, Vesna Kostić, Mirjana Popovć, John Mackedon,

Krystin Schrader, and Dragana Varezić.

The team benefitted from guidance and advice from Satu Kähkönen (sector manager, ECA PREM2) and Yvonne

Tsikata (director, ECA PREM). Discussions with Abebe Adugna (ECSPE) and Juan Zalduendo (ECAVP) are

gratefully acknowledged.

In this report, “South East Europe” refers to the six countries of the Western Balkans (SEE6): Albania, Bosnia and

Herzegovina, Kosovo, FYR Macedonia, Montenegro, and Serbia.

v

SUMMARY

After two years of fragile recovery from the global recession, as a group the six South East European

countries (SEE6)––Albania, Bosnia and Herzegovina (BIH), Kosovo, FYR Macedonia, Montenegro, and

Serbia––are experiencing a double-dip recession in 2012. Deteriorating external conditions, the impact

of the severe winter on economic activity, and a continuing rise in unemployment early in the year took a

toll on consumption, investments, and exports. The risks noted in the June report have materialized.

Credit recovery and fiscal consolidation are under threat. Nonperforming loans (NPLs)––thought to be

stabilizing only a few months ago––are again on the rise. As a result, both within and outside the region

the environment has become much more difficult to navigate, and the policy trade-offs necessary to

stabilize economies and reignite growth are tougher.

After growing by about 2 percent annually in 2010–11, the combined real GDP of SEE6 will shrink –

0.6 percent in 2012, with real output in Serbia declining by as much as 2 percent. Also, it is now clear

that even in the best of circumstances, the road to sustained recovery will be arduous: growth in 2013 is

now expected to average 1.6 percent and the risks may be formidable. Among the clouds on the horizon

for 2013 are the global impact of the U.S. “fiscal cliff,” the uncertain recovery of the Eurozone, and high

commodity prices—risks to which all the SEE6 countries are highly vulnerable. Also worrisome for its

households is the risk of a new food price shock, which could exacerbate poverty and put pressure on the

middle class.

In this fragile environment, Serbia, Albania, and Montenegro in particular will need to persevere in

reducing fiscal deficits and bringing down debt, even as they must continue to improve the investment

climate and reform labor markets and the public sector. In all SEE6 countries, public sector arrears pose

special challenges to fiscal management and the private sector, and there are unfinished, structural

reforms agendas.

After two years of deep crisis, a sluggish recovery, rising unemployment and poverty, and a continuing

recession––even with the best efforts on fiscal consolidation and structural reforms, which must

continue––there is a danger that SEE6 countries are caught in a vicious circle that reinforces the cycle of

long-term austerity, low if not negative growth, high debt, and even higher risks of social upheaval. To

prevent this outcome, this report argues, SEE6 governments need to redouble their efforts to accelerate

vi

fiscal and structural reforms. These countries have largely exhausted their fiscal space and reduced

public investment (except Kosovo, an outlier) to a fraction of what is needed to maintain public capital

stock in critical infrastructure. Private investment is suppressed by the lack of productive, complementary

public investments, slow credit recovery, and depressed domestic demand. External demand is minimal,

and exports are not only too few, they are prevented from becoming an immediate, new engine of growth

by infrastructure, finance, and other deficiencies.

What is needed first and foremost, this report argues, is more intensive policy reform to reduce public

debt and accelerate structural reforms, especially in public sector governance, the investment climate,

and labor markets. Given their vulnerabilities, the SEE6 countries could also better prepare for new food

price shocks.

If such accelerated reforms materialize, external support—well-coordinated and targeting the region

as a whole, not just individual countries––from the EU and global international financial institutions

(IFIs) could help ease the transition to a more sustained growth in medium term.

In November 2012, the European Investment Bank, the European Bank for Reconstruction and

Development, and the World Bank announced €30 billion in financing for Central and South East

European countries over the next two years. In SEE6 countries, this timely initiative would likely be

delivered via the Western Balkans Investment Framework (WBIF) and other IFI resources. IPA resources

will also be important, especially in supporting institutional reform and rural development. By focusing

on major infrastructure of regional significance (rail, highways, energy, and gas) and on jobs and small

and medium enterprises, the efficiency of investments, growth, and employment could be substantially

heightened. However, additional financing for growth and jobs could prove effective only if accompanied

by intensified fiscal and structural reforms, especially in the areas of investment climate, labor markets,

and governance.

1

1. RECENT DEVELOPMENTS, OUTLOOK, AND POLICY

CHALLENGES

A. EUROZONE IN RECESSION, NEW GLOBAL RISKS

After months of decelerating economic activity following turbulence in financial markets in the second

quarter, global economic activity is slowly picking up once again — most notably in developing

countries. But the modest rebound is tenuous. The latest data show growth in industrial production in the

world’s two largest economies, USA and Japan, is on the decline. Due to mid-year weakness, calendar

year global GDP growth projections are tentatively being downgraded by about 0.2 percentage points to

2.3 percent in 2012 and by 0.6 percentage points in 2013 to 2.4 percent, mainly because of the recession

in the Eurozone. Threats to the recovery lie in the difficulties of implementing Eurozone fiscal

consolidation; remaining global uncertainty, and the risk of an uncontrolled unwinding of China’s high

investment rates. To further complicate the situation, low stocks of maize and wheat could result in even

higher food prices with serious consequences for the poor.

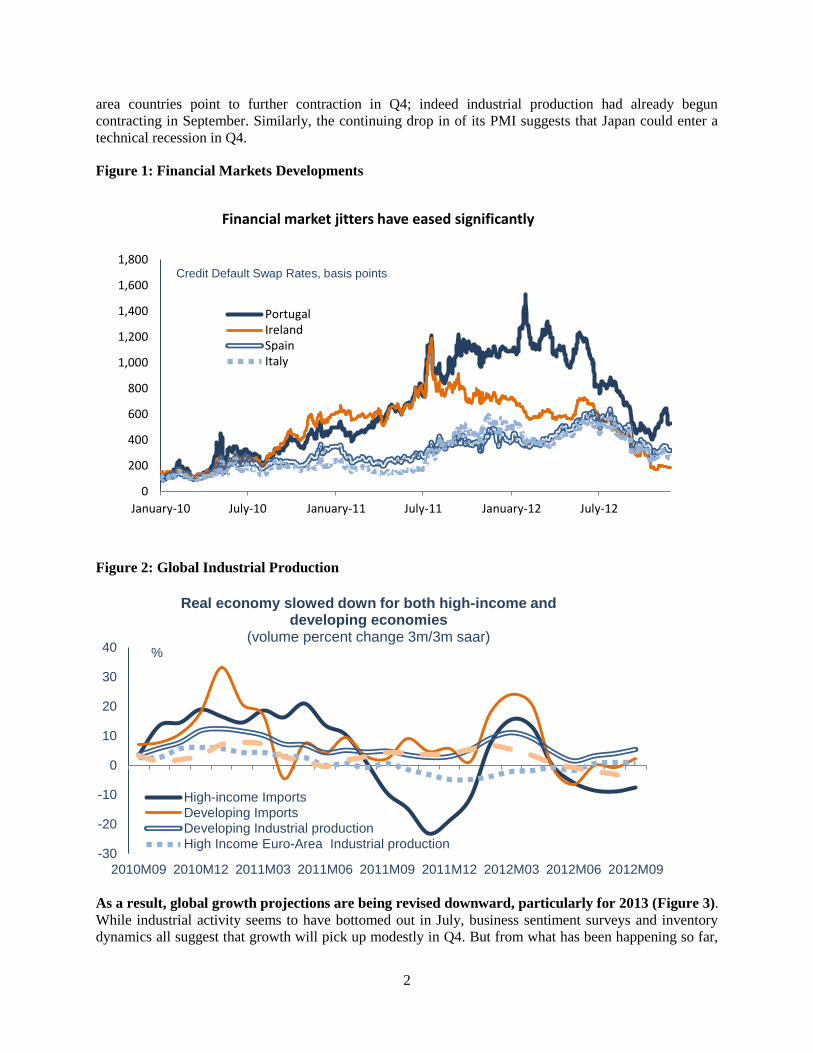

Since the highly volatile second quarter of 2012 ended, global financial market tensions have eased

significantly, thanks mainly to the announcement of European Central Bank (ECB) measures to

defend the Eurozone, but significant risks remain in the global economy. In early September, with the

actual launch of ECB’s bond-buying program and the favorable German Constitutional Court ruling on

the European Stability Mechanism (ESM), the risk of an acute crisis subsided considerably, and

borrowing costs for high-spread countries like Italy and Spain fell steeply (Figure 1). Emerging markets

bond spreads (EMBIG) have declined by 80 basis points (bps) since June to their long-term averages

(about 310 bps). Since early June global equity markets have also rebounded: stocks in high-income

countries are up 10.7 percent so far for 2012 and in developing countries by 8.1 percent.

Similarly, gross capital flows seem to be recovering. All capital flows to developing countries

(international bond issues, cross-border syndicated bank loans, and equity placements), which fell by 30–

40 percent toward the end of the second quarter in June, returned to first-quarter levels in the third

quarter. As the Eurozone deleveraging unwound, syndicated bank lending to developing countries nearly

doubled in August, though it is still more than 30 percent below 2011 levels. After capital flows eased in

August—a normal seasonal lull— gross flows in September outdid every other month since 2007 totaling

$408 billion, a slight increase over 2011. The surge in bond issues by developing countries compensated

for the declines in syndicated bank lending and equity issues.

Developing countries have been leading the upswing in economic activity (Figure 2). Industrial

production grew at a 5.8 percent annualized pace in Q3. China’s GDP expanded by 9.1 percent (q/q,

annualized), up from 8.2 percent in Q2, led by the services sector. Among high-income countries the

situation is more nuanced. There was an acceleration in the United States in Q2 (2.7 percent q/q

annualized ) supported by solid growth in residential investment, but it was followed by an abrupt

contraction in Q3 (-3 percent q/q annualized). In the Eurozone industrial production picked up in Q3 but

not enough to avert a contraction for the quarter in GDP (–0.1, q/q).

But leading indicators suggest a mixed picture for the last quarter of 2012. Recent Purchasing

Managers Indexes (PMIs) suggest that manufacturing is looking healthier in Q4 for the United States (but

note that the PMI was carried out before Hurricane Sandy) and for developing countries like China,

Brazil, Indonesia, India, Russia, and Turkey, many of which have benefitted from a recent easing of

policy rates. Although Eurozone industrial activity stabilized in Q3, PMI for both core and periphery Euro

2

area countries point to further contraction in Q4; indeed industrial production had already begun

contracting in September. Similarly, the continuing drop in of its PMI suggests that Japan could enter a

technical recession in Q4.

Figure 1: Financial Markets Developments

Figure 2: Global Industrial Production

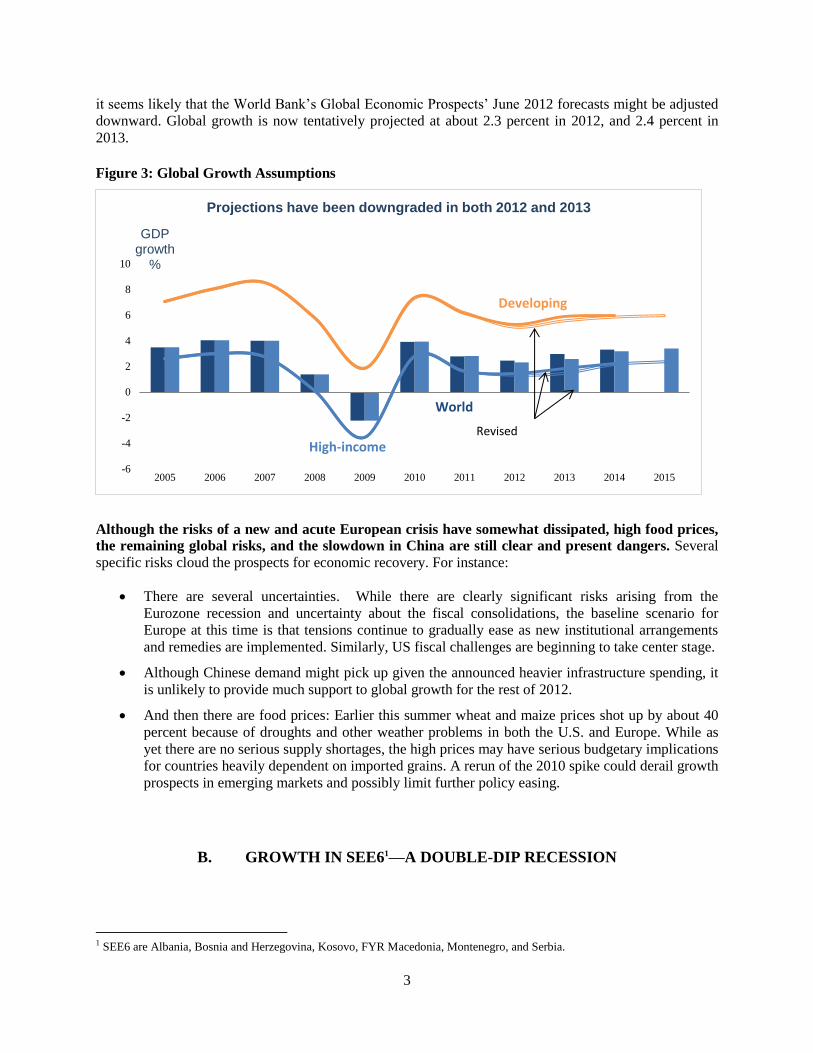

As a result, global growth projections are being revised downward, particularly for 2013 (Figure 3).

While industrial activity seems to have bottomed out in July, business sentiment surveys and inventory

dynamics all suggest that growth will pick up modestly in Q4. But from what has been happening so far,

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

January-10 July-10 January-11 July-11 January-12 July-12

Financial market jitters have eased significantly

PortugalIrelandSpainItaly

Credit Default Swap Rates, basis points

-30

-20

-10

0

10

20

30

40

2010M09 2010M12 2011M03 2011M06 2011M09 2011M12 2012M03 2012M06 2012M09

Real economy slowed down for both high-income and developing economies

(volume percent change 3m/3m saar)

High-income Imports

Developing Imports

Developing Industrial production

High Income Euro-Area Industrial production

%

3

it seems likely that the World Bank’s Global Economic Prospects’ June 2012 forecasts might be adjusted

downward. Global growth is now tentatively projected at about 2.3 percent in 2012, and 2.4 percent in

2013.

Figure 3: Global Growth Assumptions

Although the risks of a new and acute European crisis have somewhat dissipated, high food prices,

the remaining global risks, and the slowdown in China are still clear and present dangers. Several

specific risks cloud the prospects for economic recovery. For instance:

There are several uncertainties. While there are clearly significant risks arising from the

Eurozone recession and uncertainty about the fiscal consolidations, the baseline scenario for

Europe at this time is that tensions continue to gradually ease as new institutional arrangements

and remedies are implemented. Similarly, US fiscal challenges are beginning to take center stage.

Although Chinese demand might pick up given the announced heavier infrastructure spending, it

is unlikely to provide much support to global growth for the rest of 2012.

And then there are food prices: Earlier this summer wheat and maize prices shot up by about 40

percent because of droughts and other weather problems in both the U.S. and Europe. While as

yet there are no serious supply shortages, the high prices may have serious budgetary implications

for countries heavily dependent on imported grains. A rerun of the 2010 spike could derail growth

prospects in emerging markets and possibly limit further policy easing.

B. GROWTH IN SEE61—A DOUBLE-DIP RECESSION

1 SEE6 are Albania, Bosnia and Herzegovina, Kosovo, FYR Macedonia, Montenegro, and Serbia.

-6

-4

-2

0

2

4

6

8

10

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Projections have been downgraded in both 2012 and 2013

World

Developing

High-income Revised

GDP growth

%

4

After average annual growth of just 2 percent in 2010 and 2011, and mirroring Eurozone

developments, in the first half of 2012 SEE6 countries again entered recession. Led by Serbia, which

accounts for almost half of SEE6 GDP, regional economic activity faltered in part because of the severe

winter but also because of severely shrinking demand, both external and domestic (Table 1).

Table 1: South East Europe Six: Real Economic Growth, 2009–12

Source: SEE6 country statistics offices and World Bank staff (2013). Averages are GDP weighted.

General recession notwithstanding, growth in individual SEE6 countries varied widely. Serbia and

FYR Macedonia contracted most, by about 1.6 and 1.1 percent, respectively, in the first half of 2012.

Kosovo is an outlier whose real output continues to be propelled by remittances from the diaspora as well

as high public investments, and Albania’s economy grew 1 percent on the heels of domestic demand.

Lower exports and investments drove these developments; high unemployment keeps the lid on

consumption. Even with the expected gradual recovery in the second half of the year, the SEE6 as a group

will remain in recession for the year as a whole. Unemployment––the highest regional unemployment in

Europe, averaging about 25 percent (excluding Kosovo whose unemployment exceeds 40 percent, partly

offset by informal employment)––will keep rising.

The recovery was slowed by poor industrial performance. Across the region industrial output has been

sliding downhill for three consecutive quarters, from Q4 2011 through Q2 2012. The drop was most

severe in Q1 2012, when many factories had to shut down for weeks because of an unusually cold winter;

winter drought and associated hydropower shortages; and a drop in demand for industrial exports. As a

result, the weighted average growth of industrial output in the first quarter was –10.1 percent. The most

significant decline was in Albania (–20.3), followed by Montenegro (–14.7 percent) (Table 2)

2009 2010 2011 2012 H1 2012 H2

(proj.)

2012

(proj.)

ALB 3.3 3.5 3.0 1.0 0.6 0.8

BIH -2.9 0.7 1.3 -0.2 0.2 0.0

KOS 2.9 3.9 5.0 3.6 3.6 3.6

MKD -0.9 2.9 2.8 -1.1 1.0 0.0

MNE -5.7 2.5 3.2 -0.9 1.0 0.2

SRB -3.5 1.0 1.6 -1.6 -2.3 -2.0

SEE6 -1.8 1.8 2.2 -0.6 -0.5 -0.6

EU11 … 2.0 3.1 1.3 … 0.9

5

Table 2: SEE6: Industrial Output Real Growth by Quarter (Percent, year-on-year)

2011 2012

Country2 Q1 Q2 Q3 Q4 Q1 Q2

Albania 11.1 -5.4 5.6 -9.7 -20.3 6.4

Bosnia and Herzegovina 11.1 6.2 6.0 2.9 -9.4 -4.1

Macedonia 13.8 5.3 1.4 -4.7 -8.5 -5.6

Montenegro -10.2 -21.0 3.6 -11.6 -14.7 1.9

Serbia 5.7 3.8 -1.8 0.4 -6.4 -3.1

Averages

Simple 6.3 -2.2 3.0 -4.6 -11.8 -0.9

GDP weighted 7.8 1.6 1.8 -2.1 -10.1 -1.7

Source: National statistics offices and World Bank staff calculations.

While regional industrial output as a whole is still declining, there are hints of recovery. The drop in

output was significantly smaller in the second quarter, only –1.7 percent (y-o-y). In addition, reactivation

of previously closed factories helped raise output in Albania and Montenegro. On the other hand, industry

in Macedonia sank by 5.6 percent, in Serbia by 3.1 percent, and in BIH by 4.1 percent. However, FIAT is

ramping up production, which will contribute significantly not only to Serbia’s growth but also, because

of its scale, to the growth of industrial output in the entire region.

Box 1: FIAT in Serbia: The Auto Industry Returns to the Western Balkans

Opening of the large FIAT factory in Serbia and recent foreign investments in auto parts production in FYR

Macedonia, herald the gradual return of the auto industry to the Western Balkans and promise to revitalize some

areas of its industry. FIAT and the Government of Serbia have established a joint venture––FIAT Automobili Srbija

Ltd.––in which FIAT holds 66 percent and Serbia 34 percent of equity. Serbia invested mainly in kind (land,

existing buildings, and infrastructure improvements in the city of Kragujevac; access roads and railways; better

energy supplies, etc). So far, one production line (three are planned) is up and running; it is expected to produce

30,000 cars (model 500L) in 2012 and about 150,000 in 2013. Revenues are estimated to be about €400 million for

2012 and as much as €2 billion in 2013 (about 6 percent of Serbia’s GDP); although this will be mostly from the

model 500L, FIAT plans to start producing the Punto as well, though only about 10,000 units to begin with.

In addition to the problems of

industry, an exceptionally bad

harvest throughout the Balkans

suppressed agricultural

production, contributing to both

the general recession and the

pressures on domestic food prices

(Table 3). Agricultural production

throughout the region suffered all

year from extreme weather. First,

winter temperatures hit record lows,

and there was a drought. Then in the

summer the region, like many other

parts of the world, was faced with a

severe drought. As a result,

2 Kosovo does not produce high-frequency data on industrial output.

Table 3: SEE6: Decline in Real Agricultural Output in 2012

Agriculture output, quarterly growth rates (y-o-y)

Q1 Q2

ALB 4.5 5.6

BIH1 -4.5 -4.1

MKD 3.3 0.0

MNE -10.0 30.0

SRB -19.0 -17.2 1 Data available only for Republika Srpska.

Note: For all countries except Montenegro indexes are based on value added at

constant prices. For Montenegro, the base is physical output. For FYR

Macedonia, q-o-q, seasonally adjusted.

6

agricultural output plunged. And the results for the third quarter might be particularly bad for countries

that have concentrated their agricultural activities in cereals and fruit production. Serbia, and to some

extent BIH, were hit hardest. In the first half of the year alone Serbia saw value-added in agriculture drop

by 18 percent. As a result, food and general CPI inflation in SEE6 reversed the downward trend that had

begun in March 2012 (Figure 4).

Figure 4: SEE6: Inflation––CPI and Food (Percent)

Source: SEE6 national statistics offices.

C. LABOR MARKETS––A CONTINUING CRISIS

With a double-dip recession, unemployment in the SEE6 continues to rise. Three years after the

global crisis hit the region, labor markets in most of its economies are still deteriorating. Unemployment

in Serbia and BIH, is much higher in 2012 than it was in 2008 (Figure 5). Serbia’s unemployment rate

soared by 11 percentage points—an unprecedented loss of jobs (Box 2)—and in BIH the rate went up by

almost 5 percentage points. Among Europe and Central Asian developing countries only the three Baltic

States had seen unemployment rate hikes as high as 11–12 percentage points during the global crisis, but

by 2011 all three countries had pushed the rates down 2.5–4.5 percentage points. Moreover, the job losses

in the Baltics resulted from the sharp economic recession and double-digit declines in output. In contrast,

the output contraction in Serbia and BIH has been much milder, but the labor market deterioration has

been much more protracted. Montenegro’s unemployment rate is also higher than it was before the crisis,

though the impact has been less stark. Albania is probably in the same group, with a return of some

migrants from Greece, adding to the unemployment problem, but labor force survey data are not

available. FYR Macedonia and Kosovo performed better because these economies have been growing

moderately in recent years.

-4

-2

0

2

4

6

8

10

12

14

16

1 2 3 4 5 6 7 8 9 10 11 12 1 2 3 4 5 6 7 8 9 10 11 12 1 2 3 4 5 6 7 8 9 10 11

2010 2011 2012

Inflation (y-o-y)

Food inflation (y-o-y)

7

Figure 5: Change in SEE6 Unemployment Rates, 2008 and 2012 (Percentage points)*

Source: Labor force surveys (LFS) of national statistical offices.

* Latest 2011 LFS data not available for Kosovo and Albania.

High unemployment is still a major economic and social challenge for the region (Figure 6). Kosovo,

with unemployment at 43.5 percent, FYR Macedonia, 31 percent, and BIH and Serbia, at about 28

percent are outliers in Europe as a whole and also rank high globally. According to the World Bank’s

World Development Indicators, few countries in the world have unemployment rates higher than 25

percent. As mentioned in previous issues of this report, youth and long-term unemployment are

particularly daunting problems for the region. A prolonged economic downturn would add to the already

chronic problem of long-term unemployment.

Figure 6: Unemployment Rates, SEE6 and EU10

Source: Labor Force Surveys of National Statistical Offices.

Note: Data for Kosovo for 2010–11 are not available; data for Albania from administrative sources. EU10 countries

encompass Bulgaria, Czech Republic, Estonia, Hungary, Latvia, Lithuania, Poland, Romania, Slovak Republic, and

Slovenia. EU11 also includes Croatia.

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

10.0

12.0

Macedonia, FYR Montenegro BiH Serbia

8

Box 2: Soaring Unemployment in Serbia

Unemployment rocketed up in Serbia as a result of the 2008-9 economic crisis and continued to head upward

in 2010–2011 even though the economy returned to mildly positive growth; with return to recession in 2012, it

is likely to get worse before it gets better. Estimates from the Labor Force Survey (LFS) panel suggest that the

share of unemployed in the total active population (age 15+) increased from 15.8 percent in April 2009 to 19.5

percent in April 2010, 22.5 percent in April 2011, and 23.7 percent in November 2011.

Inactivity is also on the rise. In 2009–11 not only did the number of unemployed increase by more than 250,000

but the economically active population decreased by over 340,000. Estimates based on the LFS panel suggest that

labor inactivity was particularly high when the global crisis began, and a quarter of those employed informally

transitioned to inactivity between April 2008 and April 2009. Of those unemployed in April of 2008 more than 20

percent had dropped out of the labor market by April 2009.

Finding work for the unemployed is extremely difficult. Of those unemployed in April 2009, 85 percent still had

no jobs in April 2010, and only 9 percent had managed to transition into employment, most commonly in the formal

sector. Similarly, of those unemployed in April 2010, 83 percent were still unemployed in April 2011, while the

share of those moving to employment was still less than 10 percent.

Source: World Bank (2012c), based on Serbia Labor Force Survey panel data.

Administrative source data on the registered unemployed support the above analysis and allow for

monitoring of 2012 trends in all SEE6 countries (Figure 7). Data on registered unemployed persons

from administrative sources (typically Bureaus of Employment) are less reliable than LFS data and are

not comparable across countries. Nevertheless, these data show a divergence in performance similar to

what the LFS data illustrate. The number of registered job seekers in 2012 is higher than in 2011 in BIH

and Albania. However, the number of registered job seekers in FYR Macedonia, Montenegro, and

Kosovo has come down in 2012—although changes in labor regulation in FYR Macedonia and Kosovo

may explain part of the difference.3

Figure 7: Registered Unemployed in 2011 (January 2011 = 100)

Source: National statistics offices.

3 In FYR Macedonia the provision of free health insurance was delinked from the labor market status of individuals, and the

authorities are introducing additional measures to streamline the unemployment registry. Kosovo introduced a digital database of

job seekers which allowed to clean up the outdated paper records.

7580859095

100105110

De

c-1

0

Jan

-11

Feb

-11

Mar

-11

Ap

r-1

1

May

-11

Jun

-11

Jul-

11

Au

g-1

1

Sep

-11

Oct

-11

No

v-1

1

De

c-1

1

Jan

-12

Feb

-12

Mar

-12

Ap

r-1

2

May

-12

Jun

-12

Jul-

12

Au

g-1

2

Sep

-12

Oct

-12

BiH Macedonia, FYR Montenegro Serbia Kosovo Albania

9

The labor market participation rate in SEE6 countries has traditionally been lower than in EU

countries, ranging from 44 percent in BIH to 56 percent in FYR Macedonia.4 The participation rate held

relatively steady between 2011 and 2012. The largest change was in Montenegro: an increase of 0.5

percentage points, mirrored by the rise in the employment rate. Serbia, on the other hand, has seen labor

participation decrease over the last three years. This pull-out of the labor force represents additional,

“hidden unemployment” beyond the official figures.

The LFS employment data available for 2012 show a mixed picture at best (Figure 8). Regionally,

employment rates are highest in Montenegro and lowest in BIH. Employment continues to slide in Serbia

and in BIH. Serbia has lost about 680,000 jobs since 2008––a staggering 30 percent of total employment

in 2012. These losses seem to be concentrated in agriculture, finance, and construction—sectors that are

particularly hard hit by cyclical and structural factors. On the other hand, after losing jobs in the first

quarter of 2012 Montenegro made the biggest gain in employment in the second quarter, though this

comes partly from preparation for tourism, and annualized data show continued headwinds.

Figure 8: Employment Rates in SEE6 (2011–2012), in percent

Source: Labor force surveys of national statistical offices.

Wage movements in the region reflect labor market performance. With unemployment high, wages

in the SEE6 were mostly either stagnant (BIH) or declining (FYR Macedonia and Montenegro) with

inflation in the latter group causing an even greater drop in real wages (Figure 9 and Figure 10). The

exception is Serbia, where nominal wages have been on the rise (excluding the typical drop in January

after the hike in December caused by payment of the 13th month in salary).

4 Using “age 15 and above” to define the active population.

30

32

34

36

38

40

42

FYR Macedonia Montenegro Serbia BiH

10

Figure 9: Gross Average Nominal Wage Changes (January 2011 = 100)

Source: National statistics offices.

Figure 10: Employment and Real Wage Index (December 2010 = 100)

Source: National statistics offices and World Bank staff estimates.

The jobs challenge in the region is also a social inclusion challenge: Low labor force participation

masks huge inequalities to the disadvantage of women, youth, those who are less educated, and ethnic

minorities. The share of women employed or actively seeking a job is relatively low in SEE6, which

could be interpreted as hidden unemployment. For example, in Kosovo female employment stands at a

mere 9.2 percent, less than one fourth the employment of males. Labor market outcomes also vary

90

95

100

105

110

115

120

125

130Ja

n-1

1

Feb

-11

Mar

-11

Ap

r-1

1

May

-11

Jun

-11

Jul-

11

Au

g-1

1

Sep

-11

Oct

-11

No

v-1

1

De

c-1

1

Jan

-12

Feb

-12

Mar

-12

Ap

r-1

2

May

-12

Jun

-12

Jul-

12

Au

g-1

2

Sep

-12

Oct

-12

BiH Macedonia, FYR Montenegro Serbia

11

substantially across ethnic groups; for example, Roma are much more likely to be unemployed than

individuals from other ethnic groups, and the labor force participation rate among Albanian women is

almost negligible compared to that of other ethnicities.

Addressing the job creation challenge will require governments to move beyond reforms of labor

market institutions and active labor market policies. As discussed in the World Bank report Jobs in

Eastern Europe and Central Asia and the World Development Report 2013 on Jobs, poor labor market

and social inclusion outcomes are the result of multiple, highly interconnected factors, such as labor

demand patterns, skills mismatches, impediments to labor mobility, limited effectiveness of labor market

intermediation mechanisms, poorly aligned higher education systems. The economic crisis facing most of

the countries continues to compound pre-existing structural weaknesses, with labor force participation

falling and unemployment and poverty on the rise. Moreover, as populations in most countries in the

region age, the number of retirees in comparison to the working age population is rapidly growing, adding

stress to labor markets and the entire social model. Without swift policy action, the situation is likely to

deteriorate. Meeting these challenges through an array of measures for fostering growth, competitiveness,

and job creation could boost living standards, productivity, and social cohesion (Box 3). More productive

and well-paying jobs, as the World Development Report 2013 demonstrates, can improve living standards

by providing earnings, lift people out of poverty and raise their consumption; and raise productivity. They

can also strengthen social cohesion when economic opportunities open for all socio-economic and

demographic groups.

Are labor regulations to blame for the poor performance of SEE6 labor markets? The answer seems

to be: partly, yes. In countries where the majority of jobs are created by the private sector, labor

regulations can facilitate or impede job creation and wage earnings. Labor markets need to be regulated to

protect workers from unfair treatment and ensure efficient contracting between employers and workers.

Excessive regulations, however, may go beyond addressing market distortions and constrain job creation.

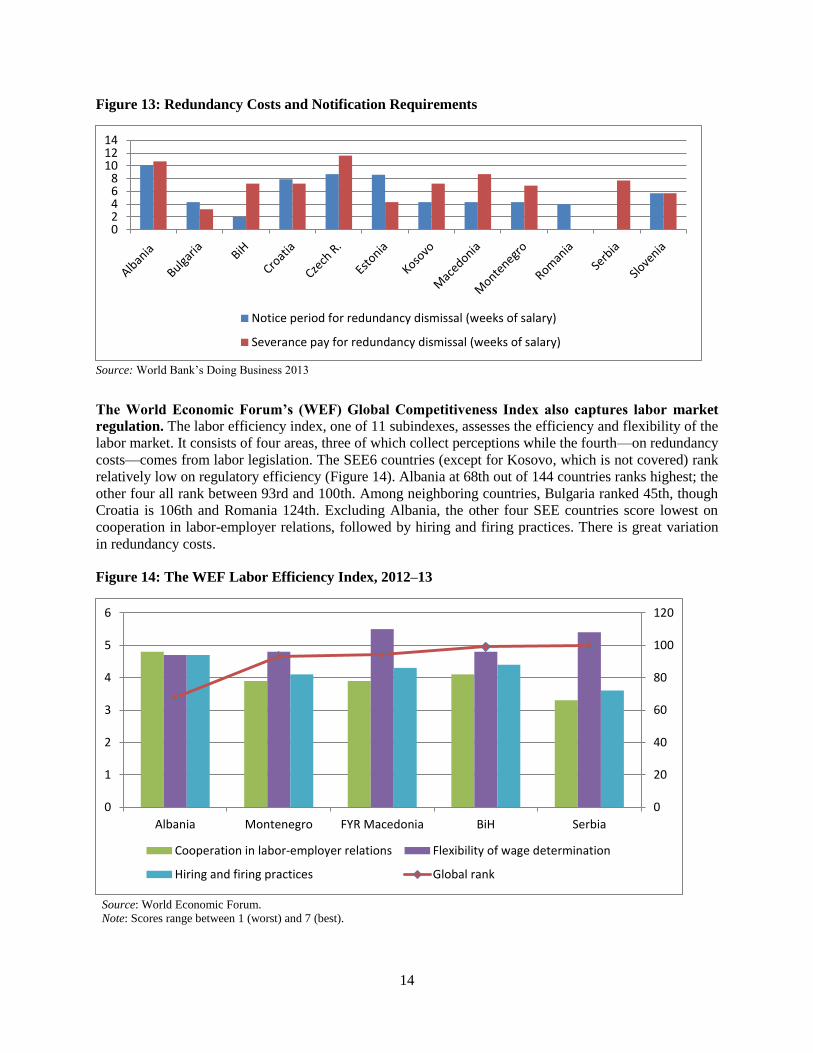

So where are the SEE6 countries on the regulatory spectrum? Two global indexes help answer this

question: the World Bank Doing Business “employing workers” index5 and the “labor efficiency” index

of the World Economic Forum (WEF). The Doing Business index looks at indicators that measure

flexibility in the regulation of hiring, working hours, and redundancy. These three aspects of labor

regulations are measured using 21 sub-indicators (Figure 11Figure 12: contains the 12 that have the most

heterogeneity in the SEE6).

5 www.doingbusiness.org.

12

Box 3: World Development Report on Jobs: Implications for Labor Market Policies

With the global spotlight on jobs following the global economic crisis, the World Bank’s World Development

Report 2013 (WDR 2013) suggests a comprehensive approach to public policies for creating not just any jobs

but jobs that are good for development. The latter are jobs that boost living standards, raise productivity, and

foster social cohesion. The WDR 2013 proposes a three-layer approach to creating jobs good for development:

First, policy fundamentals—including macroeconomic stability, an enabling business environment, investments in

human capital, and the rule of law—are essential for both growth and job creation. Second, well-designed labor

policies can help ensure that growth translates into employment opportunities, but they need to be complemented by

a broader approach to job creation that looks beyond the labor market. Third, governments should strategically

identify which jobs would do the most for

development given their specific country context, and

remove or offset the obstacles that prevent the private

sector from creating more of those jobs.

Hence, the WDR 2013 moves the discussion of job

creation beyond labor market policies. It finds that

labor market policies are not always the binding

constraint on creating jobs good for development,

except when they are either excessive or minimal.

Labor market policies, including labor regulations,

collective bargaining, active labor market programs,

and social protection may deter formal employment

and productivity when excessive, or when inadequate

regulation allows harmful forms of work. If labor

market policies are kept within reasonable bounds,

their aggregate effects are more on redistribution than

employment. For example, employment protection

legislation tends to have only modest effects on

aggregate employment, but it favors prime-age males, over youth, women and the low-skilled. On the other hand,

active labor market programs and social protection policies have been shown to promote greater employment and

wage equality. In Western Balkans, however, there remains important scope for improving labor market flexibility.

Regulation of the SEE6 labor markets varies substantially across countries in each area of

regulation, but there is scope to make labor markets more flexible. In terms of flexibility of hiring,

Albania and Serbia prohibit use of fixed-term contracts for permanent tasks, and the other four countries

set maximum length for fixed-term contracts. The minimum wage for workers or apprentices is more

than twice as high in BIH than in Kosovo—the other countries fall somewhere in between. Albania and

Macedonia stipulate the highest premiums for work on rest days and night shifts. In the easiest place to

fire workers, Albania, employers must pay the highest redundancy cost. In terms of flexibility of hiring,

there is a wide variety of approaches of flexibility in hiring throughout in the SEE6 region and in Europe

(Figure 11). A high minimum wage can be a disincentive for employers to hire young workers, and here

BIH is an outlier in a negative sense. Albania and Serbia prohibit use of fixed-term contracts for

permanent tasks, but this is also the practice in several EU-11 countries. Four SEE6 countries set

maximum length of fixed-term contracts, and in Serbia, BIH, and Montenegro the period is shorter than in

benchmark EU-11 countries. Overall, Kosovo has the most flexible regulations for hiring workers—but it

also has the highest unemployment rate in Europe. Finally, regulations also vary in terms of how difficult

and costly it is to fire workers (Figure 13). While there is clearly scope to further improve labor market

flexibility in the SEE6, the largely structural unemployment problem will require first and foremost

restoration of robust economic growth as well as other structural reforms (e.g. investment climate).

13

Figure 11: SEE6 Difficulty of Hiring Workers

Source: Doing Business report 2013.

Notes: Size of bubble depicts minimum wage of a 19-year-old worker. Blue color countries allow the use of fixed-term contracts

for permanent tasks.

*Albania and Kosovo have no limit on the maximum length of fixed-term contracts.

Figure 12: SEE6 Premiums on Night Shift and Work on Rest Days

Source: World Bank’s Doing Business 2013.

Albania

Bulgaria

BIH

Croatia

Czech R. Estonia

Kosovo

Macedonia

Montenegro

Romania Serbia

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0 20 40 60 80 100 120 140

Rat

io o

f m

inim

um

wag

e t

o v

alu

e a

dd

ed

pe

r w

ork

er

Maximum length of fixed-term contracts (months)*

0

20

40

60

80

100

120

Premium for night work (% of hourly pay)

Premium for work on weekly rest day (% of hourly pay)

14

Figure 13: Redundancy Costs and Notification Requirements

Source: World Bank’s Doing Business 2013

The World Economic Forum’s (WEF) Global Competitiveness Index also captures labor market

regulation. The labor efficiency index, one of 11 subindexes, assesses the efficiency and flexibility of the

labor market. It consists of four areas, three of which collect perceptions while the fourth—on redundancy

costs—comes from labor legislation. The SEE6 countries (except for Kosovo, which is not covered) rank

relatively low on regulatory efficiency (Figure 14). Albania at 68th out of 144 countries ranks highest; the

other four all rank between 93rd and 100th. Among neighboring countries, Bulgaria ranked 45th, though

Croatia is 106th and Romania 124th. Excluding Albania, the other four SEE countries score lowest on

cooperation in labor-employer relations, followed by hiring and firing practices. There is great variation

in redundancy costs.

Figure 14: The WEF Labor Efficiency Index, 2012–13

Source: World Economic Forum.

Note: Scores range between 1 (worst) and 7 (best).

02468

101214

Notice period for redundancy dismissal (weeks of salary)

Severance pay for redundancy dismissal (weeks of salary)

0

20

40

60

80

100

120

0

1

2

3

4

5

6

Albania Montenegro FYR Macedonia BiH Serbia

Cooperation in labor-employer relations Flexibility of wage determination

Hiring and firing practices Global rank

15

In a nutshell, given high unemployment SEE6 countries still have a considerable distance to go to

improve labor market institutions and regulations. But it is true that factors outside labor market, such

as slow growth, weak investment and consumption, investment climate deficiencies, and economic

bottlenecks are also contributing to the exceptionally bad SEE6 labor market outcomes. Job creation is

determined by numerous factors, labor regulations being a major determinant. SEE6 countries suffer from

low levels of employment partly because of the legacy of economic transformation in the 1990s, when a

substantial share of capital was rendered obsolete. Labor regulations to promote job creation could to

some extent make up for the slack demand for workers. The above analysis shows that even though the

SEE6 are similar to the EU-11 countries, they have ample opportunities to promote job creation by

simplifying labor regulations. Areas for reform differ by country, but the results will likely depend on

factors such as the robustness and structure of economic growth and the quality of the investment climate,

especially for small and medium size businesses that are incubators of job creation.

D. TRADE AND EXTERNAL DEBT—WORSENING

The SEE6 countries are closely linked economically with the EU, so what happens in the SEE6

external sector is highly correlated to what is happening in the EU. The linkage was obvious in the

deterioration throughout the SEE6 in trade, current account deficits (CADs), FDI, and transfers in the first

half of 2012. The outlier this time was Albania, whose trade and external developments have

outperformed the rest of the region, partly because of higher oil and mineral exports.

Exports and Imports

Progressive integration of SEE6 economies into

the EU means that EU trade is central to SEE6

export performance and economic growth

generally. Even with demand subdued, the EU

still accounted for 58 percent of all SEE6 exports

in the first half of 2012 (down slightly from 58.8

percent in 2011). The lion’s share, 27.6 percent

(down from 28.7 percent in 2011), goes to Italy

and Germany (Figure 15).

Intraregional trade remains very important in

SEE6 countries. This is especially so for FYR

Macedonia, BIH, Serbia, Montenegro, and

Kosovo, while a large share of Albania’s exports

are directed toward Italy and other EU countries.

The share in GDP of intraregional exports

increased from 28.3 percent in 2011 to 30.6

percent in 2012, mainly because exports to other

countries fell. Albania had the largest real growth of exports to the SEE6 in 2012, followed by Kosovo

and Montenegro. The export shifts to the latter were also affected by a steep drop in their exports to EU

when prices of metals dropped (Figure 16 and Figure 17).

Figure 15: Exports (% of GDP)

Source: SEE6 central banks and UNCTAD.

16

Figure 16: Growth in Exports to SEE6 (%)

Figure 17: Export Growth, SEE6 and EU (%)

Source: SEE6 central banks and Eurostat.

Source: SEE6 central banks and Eurostat.

SEE6 exports slowed in the second half of 2011 and the first half of 2012 because of both weak

demand in the Eurozone and bad weather. In 2011 SEE6 exports grew by 14.0 percent, compared to

14.4 percent for the EU10, but they began to decline toward year-end. Besides an exceptionally harsh

winter, the main cause of falling exports across the region is the adverse economic climate in the EU,

which is resulting in lower import demand and especially lower metal prices. As a result, the weighted

average decline in the first half of 2012 was not marginal at –2.7 percent. Exports in some SEE6 countries

declined more than in others because EU demand fell (Figure 18 and Figure 19).

Figure 18: Exports and Economic Growth (%)

Figure 19: Import Growth (%)

Source: SEE6 central banks and Eurostat.

Note: Export growth is in bars, real GDP growth in lines.

Source: SEE6 central banks and Eurostat.

The dynamics of SEE6 imports reflected the recent weakening of domestic demand and the overall

economic activity. Imports strengthened in 2011 across the region, growing 13.8 percent thanks to

domestic demand and FDI. However, in the first half of 2012 imports moderated to about 1.6 percent

growth y-o-y as domestic demand weakened and industrial production declined (Figure 20). The value of

imports in Albania in the first half of 2012, for instance, declined by –1.8 percent, mainly because of

lower domestic demand for food and raw materials and lower imports of energy in the second quarter as

weather conditions eased.

17

Figure 20: Export and Import Growth (% y-o-y)

Source: SEE6 central banks.

Note: Data for 2012 are for the first half of the year

Current Account Deficits and Trade Balances

Although current account deficits (CAD) and trade balances improved significantly after the crisis,

both have since deteriorated across the region. The slide began in 2011 (Figure 21), most visibly in

Kosovo, where current account and trade balances are deeply affected by construction of the highway to

Albania and the associated imports. In the first half of 2012 the problem accelerated in Serbia, BIH, and

Montenegro, mainly because trade deficits widened with the decline in exports and only moderate growth

in imports. The negative trend in both current account and trade balances is a corollary of the decline in

EU demand for SEE6 commodities. The other negative impact on current account balance came from a

drop of net transfers in Serbia (Figure 22).

Figure 21: CAD and Trade Balance (% of GDP)

Figure 22: CAD by Country (% of GDP)

-30

-20

-10

0

10

20

30

40

Exp Imp Exp Imp Exp Imp Exp Imp Exp Imp Exp Imp

ALB BIH KOS MKD MNE SRB

2010 2011 H1:2012

18

Source: Central banks, IMF WEO, and World Bank

staff calculations.

Source: SEE6 Central Banks.

Remittances and FDI

Though remittances have declined somewhat in the past two years, overall, they remained relatively

resilient to the Eurozone crisis. Serbia’s remittances sank from 9.5 percent in 2009 to 6.8 percent in

2011 and then to 5.8 percent in 2012, but

those of other countries were relatively flat

in 2012 (Figure 23). Surprisingly,

remittances to Albania have not declined

even though most of their migrants went to

Greece and Italy (probably for cultural and

demographic reasons). Otherwise, the

decline in remittances in SEE6 countries

seems to have been mitigated because their

migrants are working in better-performing

countries, such as Germany, Switzerland,

and Sweden. Also, contributing factors

were the repatriation of savings of

returning migrants (Albania), and labor

policies in many EU countries which

protect well-established migrants from

SEE6 countries.

FDI––which is important to financing, investment, and growth in the SEE6––saw a robust increase

of 20 percent in 2011 but has since fallen off noticeably (Figure 24 and Figure 25). FDI more than

doubled in Serbia and FYR Macedonia in 2011; car parts for industry and finance (FYR Macedonia) were

among the most successful sectors. But in the first half of 2012 FDI moderated in FYR Macedonia,

Kosovo, and even declined in Montenegro and Serbia, mainly because of the negative impact of EU

crisis, the high 2011 base in Serbia and FYR Macedonia, and significant outflows from Serbia. But

Albania received 30 percent more FDI, concentrated in financial intermediation, services, and industry;

and privatization of four small hydropower plants could result in additional revenues. By September, FDI

in Montenegro well recovered, rising by almost 12 percent on annual basis.

Figure 23: Worker Remittances 2008–2011 (% of GDP)

Source: SEE6 Central Banks.

ALB and BIH define remittances as including compensation of

employees; KOS, SRB, MK and MNE use narrower definitions.

19

Figure 24: Foreign Direct Investment (net, %

GDP)

Figure 25: FDI per Capita (net, US$)

Source: SEE6 central banks. Source: SEE6 central banks.

External Debt

With rapid deleveraging of the private sector, in 2012 total external debt declined in SEE6, but

public external debt continued to head upward as a result of governments’ external borrowing in

the context of weak recovery and government revenues. After peaking at 64.1 percent of GDP in 2010,

external debt declined to 60.7 percent in 2011. From June 2009 to September 2012 four countries

accessed international commercial markets by issuing Eurobonds (FYR Macedonia in 2009, Albania in

2010, Montenegro in 2010 and 2011, and Serbia in 2011 and 2012 (Figure 27) or tapping loan markets

with an IBRD guarantee (Serbia, FYR Macedonia, Montenegro) (Figure 28). In the SEE6 total external

debt varies widely, with Montenegro and Serbia not only having the highest debt but well above the

regional average, and Kosovo6 having the lowest (Figure 26).

Figure 27: SEE6 External Debt (Average,

percent of GDP)

Figure 28: Total International Bonds

Outstanding, Select SEE6 Countries (US$

million)

Source: Central banks and Ministries of Finance (MoF)

of SEE6.

Source: MoFs of SEE6 countries.

6 Unlike other SEE6 countries, Kosovo has very limited access to international financial markets and consequently little external

debt.

869

341 284 285 232 225

77

0

200

400

600

800

1,000

1,200

1,400

MNE SRB KOS SEE6 ALB MKD BIH

2010 2011

20

Figure 29: Total Public and Private External Debt Through

June 2012 (% of GDP)

Source: Central Banks and MoFs of SEE6; IMF; World Bank.

E. FISCAL POLICY––RISING DEFICITS, DEBT, AND ARREARS

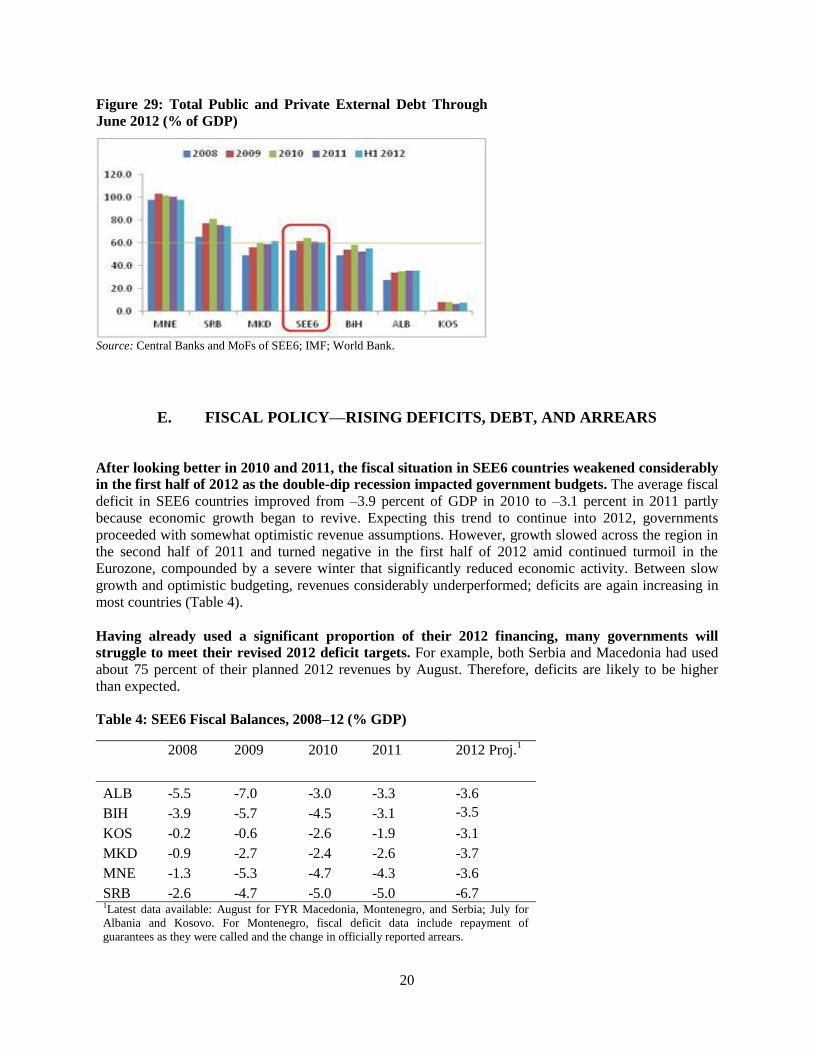

After looking better in 2010 and 2011, the fiscal situation in SEE6 countries weakened considerably

in the first half of 2012 as the double-dip recession impacted government budgets. The average fiscal

deficit in SEE6 countries improved from –3.9 percent of GDP in 2010 to –3.1 percent in 2011 partly

because economic growth began to revive. Expecting this trend to continue into 2012, governments

proceeded with somewhat optimistic revenue assumptions. However, growth slowed across the region in

the second half of 2011 and turned negative in the first half of 2012 amid continued turmoil in the

Eurozone, compounded by a severe winter that significantly reduced economic activity. Between slow

growth and optimistic budgeting, revenues considerably underperformed; deficits are again increasing in

most countries (Table 4).

Having already used a significant proportion of their 2012 financing, many governments will

struggle to meet their revised 2012 deficit targets. For example, both Serbia and Macedonia had used

about 75 percent of their planned 2012 revenues by August. Therefore, deficits are likely to be higher

than expected.

Table 4: SEE6 Fiscal Balances, 2008–12 (% GDP)

2008 2009 2010 2011 2012 Proj.1

ALB -5.5 -7.0 -3.0 -3.3 -3.6

BIH -3.9 -5.7 -4.5 -3.1 -3.5

KOS -0.2 -0.6 -2.6 -1.9 -3.1

MKD -0.9 -2.7 -2.4 -2.6 -3.7

MNE -1.3 -5.3 -4.7 -4.3 -3.6

SRB

-2.6 -4.7 -5.0 -5.0 -6.7 1Latest data available: August for FYR Macedonia, Montenegro, and Serbia; July for

Albania and Kosovo. For Montenegro, fiscal deficit data include repayment of

guarantees as they were called and the change in officially reported arrears.

21

Interestingly, over a longer period SEE6 countries seem on average to have run countercyclical

fiscal policies, but the surpluses were too small to provide much room for maneuver during a

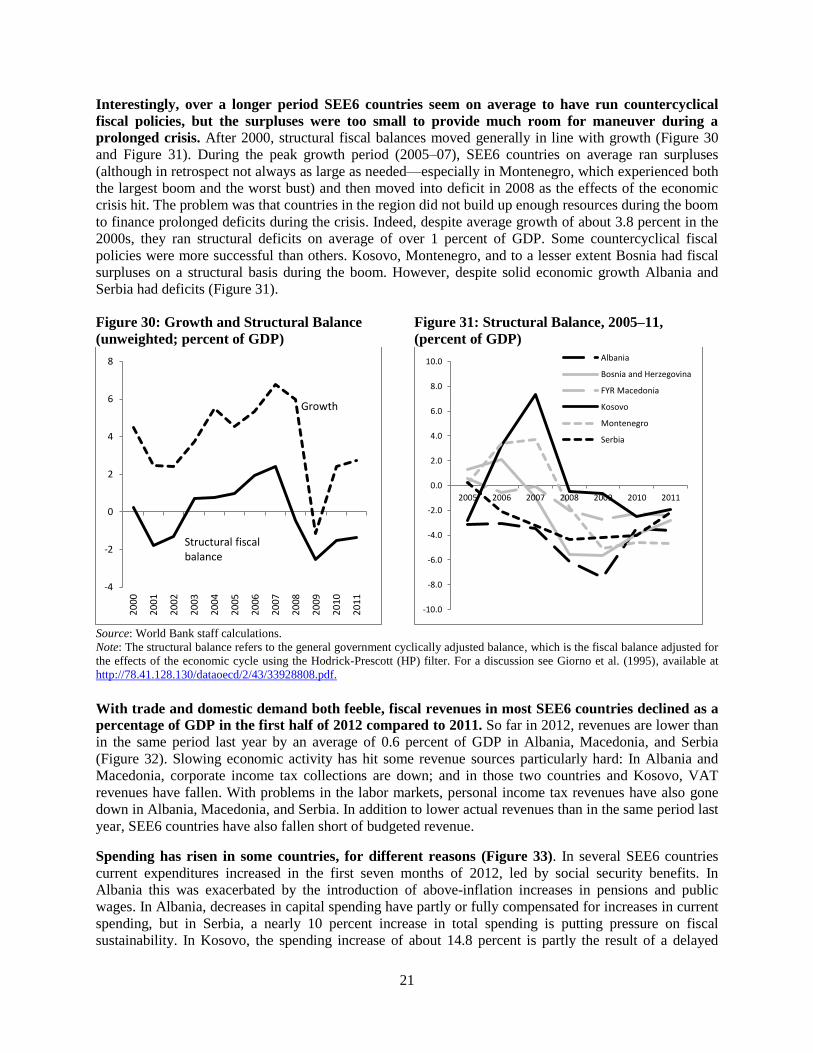

prolonged crisis. After 2000, structural fiscal balances moved generally in line with growth (Figure 30

and Figure 31). During the peak growth period (2005–07), SEE6 countries on average ran surpluses

(although in retrospect not always as large as needed—especially in Montenegro, which experienced both

the largest boom and the worst bust) and then moved into deficit in 2008 as the effects of the economic

crisis hit. The problem was that countries in the region did not build up enough resources during the boom

to finance prolonged deficits during the crisis. Indeed, despite average growth of about 3.8 percent in the

2000s, they ran structural deficits on average of over 1 percent of GDP. Some countercyclical fiscal

policies were more successful than others. Kosovo, Montenegro, and to a lesser extent Bosnia had fiscal

surpluses on a structural basis during the boom. However, despite solid economic growth Albania and

Serbia had deficits (Figure 31).

Figure 30: Growth and Structural Balance

(unweighted; percent of GDP)

Figure 31: Structural Balance, 2005–11,

(percent of GDP)

Source: World Bank staff calculations.

Note: The structural balance refers to the general government cyclically adjusted balance, which is the fiscal balance adjusted for

the effects of the economic cycle using the Hodrick-Prescott (HP) filter. For a discussion see Giorno et al. (1995), available at

http://78.41.128.130/dataoecd/2/43/33928808.pdf.

With trade and domestic demand both feeble, fiscal revenues in most SEE6 countries declined as a

percentage of GDP in the first half of 2012 compared to 2011. So far in 2012, revenues are lower than

in the same period last year by an average of 0.6 percent of GDP in Albania, Macedonia, and Serbia

(Figure 32). Slowing economic activity has hit some revenue sources particularly hard: In Albania and

Macedonia, corporate income tax collections are down; and in those two countries and Kosovo, VAT

revenues have fallen. With problems in the labor markets, personal income tax revenues have also gone

down in Albania, Macedonia, and Serbia. In addition to lower actual revenues than in the same period last

year, SEE6 countries have also fallen short of budgeted revenue.

Spending has risen in some countries, for different reasons (Figure 33). In several SEE6 countries

current expenditures increased in the first seven months of 2012, led by social security benefits. In

Albania this was exacerbated by the introduction of above-inflation increases in pensions and public

wages. In Albania, decreases in capital spending have partly or fully compensated for increases in current

spending, but in Serbia, a nearly 10 percent increase in total spending is putting pressure on fiscal

sustainability. In Kosovo, the spending increase of about 14.8 percent is partly the result of a delayed

-4

-2

0

2

4

6

8

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

Growth

Structural fiscal balance

-10.0

-8.0

-6.0

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

10.0

2005 2006 2007 2008 2009 2010 2011

Albania

Bosnia and Herzegovina

FYR Macedonia

Kosovo

Montenegro

Serbia

22

budget in 2011. However, unlike the other SEE6 countries, Kosovo’s capital spending also shot up, by

nearly 25 percent, mainly for transport projects to better connect with neighboring countries.

Figure 32: SEE6 Real Revenues, 2008–12

Figure 33: SEE6 Real Expenditures, 2008-12

Most SEE6 countries have, though at different paces, recognized the need to address the problems

head-on with attempts to increase revenues and curtail expenditures. Some SEE6 countries raised

excises (Montenegro) and VAT and the corporate income tax (Serbia) and moved to cut spending (FYR

Macedonia, Montenegro). But others, facing slow revenue collection combined with limited financing

options (BIH and Kosovo) sought financing from international financial institutions (IFIs). While other

SEE6 countries have been trying to control spending, despite the above-inflation raises in pensions and

salaries, Albania has chosen to wait to see if planned privatizations materialize first, an approach that

markets may penalize through higher yields if the expected revenues underperform.

50

60

70

80

90

100

110

120

130

140

150

2008 2009 2010 2011 2012

ALB BIH KOS

MKD MNE SRB50

60

70

80

90

100

110

120

130

140

2008 2009 2010 2011 2012

ALB BIH KOS

MKD MNE SRB

23

Box 4: Tax and Expenditure Arrears: A Growing Cause for Concern

With weak activity and budgets under pressure, most countries in the region have seen growth in arrears for

tax refunds and overdue government payments since 2008. Arrears are created when payments are not made

within a reasonable grace period after their due dates. However, the definition of arrears can change depending upon

the country and the type of bill. For example, in Montenegro, VAT refunds fall into arrears 60 days after the refund

request submission but wages do so if they are not paid on time. In Kosovo, for goods and services, any bill not paid

for 30 days after it has been entered into the treasury system is considered in arrears. The stock of arrears is difficult

to measure precisely but in the Western Balkans is estimated to average 1–3.5 percent of combined GDP.

The causes of arrears are complex and differ by country, but their impact on financial discipline, liquidity,

and economic activity can be detrimental. One of the main reasons for arrears has been overly optimistic revenue

forecasts that led to spending that cannot be covered by the revenue collected. This has been exacerbated by the

uncertainty about economic and trade conditions in Europe. Thus revenue shortfalls and tight cash flow have

prompted governments to extend payment periods and delay payments, which naturally sets in motion a chain

reaction of nonpayment by private suppliers and thus a major liquidity squeeze on an already struggling economy. In

some cases businesses have been encouraged to delay submission of invoices for work completed, or governments

have relaxed requirements for recording commitments, so that the full extent of payment obligations is obscured.

Incentives have been affected, too: some private companies that are owed by the public sector are forced to evade

taxes to stay afloat. In extreme cases, arrears can escalate into a total collapse of payment discipline, as happened,

for example, in the early 1990s in Ukraine and the former Yugoslavia in the run-up to hyperinflation in 1992.

The expansion of arrears may provide temporary cash flow relief for governments, but the impacts are far-

reaching and the payments will eventually have to be made. Delays in government payments have a direct

negative effect on consumption, employment, and investment because people who have supplied goods and services

are denied the funds they need to pay their bills and keep their businesses going. The economic situation makes it

even more difficult because businesses cannot borrow to get the cash needed to pay their own wages and suppliers.

Unpaid invoices also affect their willingness and ability to invest in growth and expansion. In the medium term,

suppliers to government will raise prices or demand payment in advance if they expect they will not be paid within a

reasonable time. Some firms will stop bidding for government contracts, which will reduce competition and value

for money.

It is vital that governments act quickly to address arrears while they are still manageable. If they are allowed

to grow unchecked, arrears can threaten fiscal sustainability and even national creditworthiness irreparably.

Concerted action on arrears requires careful revenue and cash flow management and firm procedures for controlling

expenditure commitments and processing tax refunds: accurate recording of invoices and tax refund requests,

monitoring the amount and timing of payments, and budgeting sufficient resources to pay obligations within a

defined period. A crucial element of the action plan is to prevent new arrears from being created while implementing

a schedule for eliminating the stock of arrears. Some increases in the deficit—if financeable—would be justified if

they include a time-bound plan for eliminating payment arrears. Ministries of Finance need to monitor commitments

and payments closely to ensure that budget units comply with payment deadlines and do not offset reduction in

arrears by incurring unmanageable new commitments.

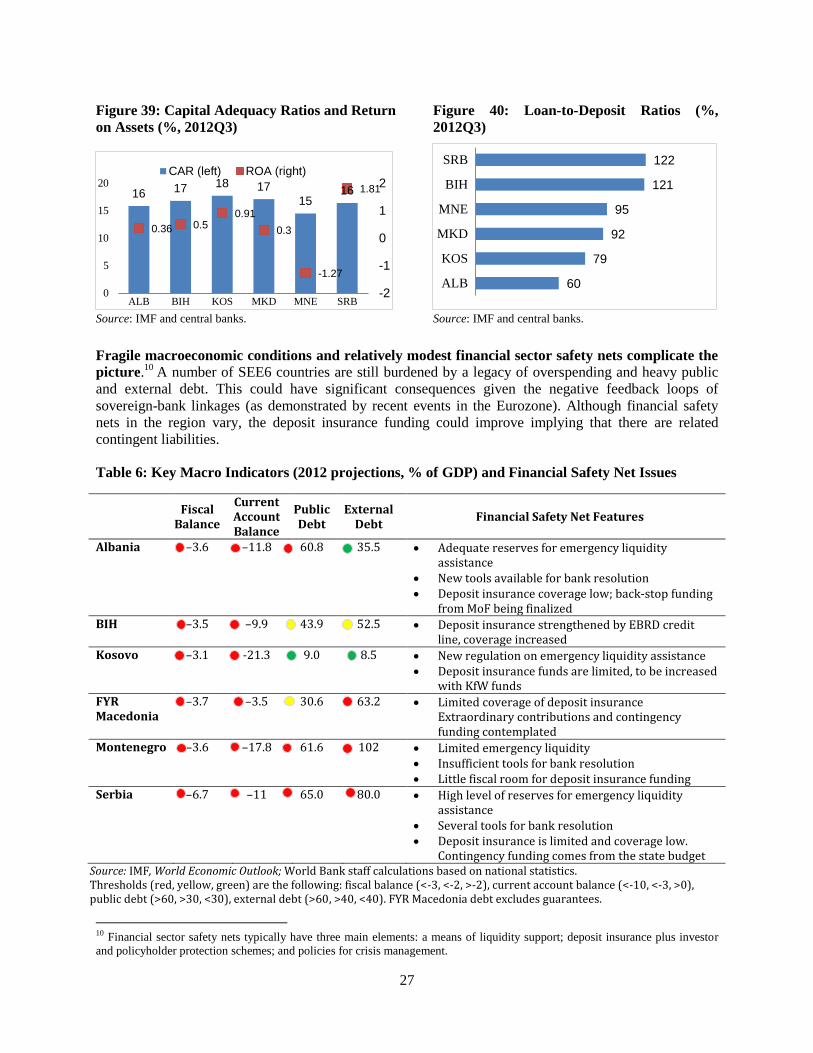

In Serbia, Albania, and Montenegro public debt is too high (Figure 34). In August, Serbian public

debt stood at 57.6 percent, well above the 45 percent ceiling set by the Law on Fiscal Responsibility.

Albania also has breached its public debt threshold of 60 percent of GDP. Montenegro’s public debt has

risen significantly, above 59 percent of GDP, in large part because of the deficits during and after the

global crisis and state guarantees. These countries will need to make special efforts to implement fiscal

consolidation and ensure that they keep the confidence of lenders. BIH, Kosovo, and FYR Macedonia all

seem to be well within sustainable levels of public debt. BIH debt was about 40 percent of GDP at the end

of 2011, but given the vulnerabilities, BIH debt levels should also be reduced in medium term. Kosovar

public debt is now about 9 percent of GDP, although attempts to build up a domestic credit market may

push this up slightly in 2013. Public debt in Macedonia is moderate.

24

Figure 34: Public Debt and Guarantees (percent of GDP)

Source: National authorities and World Bank estimates based on the latest data available.

In several countries debt refinancing—especially of short-term issues—will contribute considerably

to gross financing requirements. So far, SEE6 countries have been able to roll over their debt, but

whether they can continue to do so depends on market confidence. Some countries also have large

amounts for long-term bonds due in late 2012 and early 2013.

Unfavorable public debt dynamics have resulted in sovereign debt rating downgrades in two SEE6

countries since June. In the face of increasingly unfavorable public debt dynamics, Standard and Poor

(S&P) has downgraded sovereign debt ratings of Montenegro and Serbia (Table 5). These downgrades

may hinder access to markets to fund deficits. Further downgrades may follow if current risks to fiscal

and debt sustainability are realized.

Table 5: SEE6: Sovereign Credit Ratings1

Dec

2010

Dec

2011

Mar

2012

Jun

2012

Sep

*2012

ALB B+ B+ B+ B+ B+

BIH B+ B B B B

MKD BB BB BB BB BB

MNE BB BB BB BB- BB-

SRB BB- BB BB BB BB- Source: Standard & Poor’s. * No change as of December 12, 2012. 1Long-term foreign currency debt as of October 19, 2012. Kosovo does not have a sovereign rating.

Finally, over the short to medium term SEE6 countries face major risks, both internal and external,

that could undermine fiscal sustainability. External risks are rooted in anemic growth in Europe and

financial sector uncertainty worldwide. Continued spillover (through export demand or erosion in

business confidence) from a poorly performing Eurozone economy will likely put further downward

pressure on revenues and require equivalent adjustments in spending. Financial market jitters could make

0%

10%

20%

30%

40%

50%

60%

70%

MNE ALB SRB BIH MKD KOS

External Domestic Guarantees

25

it difficult or costly for governments to raise the financing they need to fund their deficits. High debt-to-

GDP ratios put Serbia, Albania, and Montenegro most at risk, but a general loss of confidence in

emerging markets (a “flight to safety”) could affect all SEE6 countries. Internal (“homegrown”) risks are

largely political. They boil down to keeping control of spending during the election cycles in FYR

Macedonia and Albania.

F. FINANCIAL SECTOR––CONTINUED VULNERABILITY