65-6514 FASSBERG, Harold Edward, 1919- CONTRIBUTIONS TO A ...

103

65-6514 FASSBERG, Harold Edward, 1919- CONTRIBUTIONS TO A CAPITAL MODEL WITH EFFICIENT PATHS OF CAPITAL ACCUMULATION BY USE OF THE CALCULUS OF VARIATIONS. The American University, Ph. D ., 1965 Economics, theory University Microfilms, Inc., Ann Arbor, Michigan

Transcript of 65-6514 FASSBERG, Harold Edward, 1919- CONTRIBUTIONS TO A ...

65-6514

FASSBERG, Harold Edward, 1919- CONTRIBUTIONS TO A CAPITAL MODEL WITH EFFICIENT PATHS OF CAPITAL ACCUMULATION BY USE OF THE CALCULUS OF VARIATIONS.

The American University, Ph. D ., 1965 Economics, theory

University Microfilms, Inc., Ann Arbor, Michigan

CONTRIBUTIONS TO A CAPITAL MODEL WITH EFFICIENT PATHS OF

CAPITAL ACCUMULATION BY USE OF THE CALCULUS OF VARIATIONS

A Dissertation

Presented to

the Faculty of the Graduate School

The American University

In Partial Fulfillment

of the Requirements for the Degree

Doctor of Philosophy

in Economics

byHarold E,-' Fassberg

December 1964

CONTRIBUTIONS TO A CAPITAL MODEL WITH EFFICIENT PATHS OFCAPITAL ACCUMULATION BY USE OF THE CALCULUS OF VARIATIONS

byHarold E. Fassberg

Submitted to the

Faculty of the Graduate School

of The American University in Partial Fulfillment of

the Requirements for the Degree

of

Doctor of Philosophy

In

Economics

Graduate Dean: /~\ ,

2 / Lf

Signatures of Committee:

t:Chairman:

Q(y / __

Date: Disc, / O / y / <y

December 1964

The American University Washington, D. C.

AMERICAN UNlVr.RSiT.1LldKKiv EF * 8 1 1965

WASHINGTON. 0 . C.

*

V

PREFACE

There has been increasing acceptance of the role of mathematics

in economic analysis over the past two decades. This has been brought

about by several factors including a recognition of the importance of

measuring the quantitative impact of alternative economic policies.

The advent of electronic computers has made possible the necessary

computation for handling a large number of relationships involving

many factors or variables. What is now called for is the recognition

of existing methods of mathematical formulation and the development of

new forms of analysis by and for economists.

This study has twin goals: to make some meaningful contributions

to the current concept of a capital model, and to bring into proper

focus the role of the Calculus of Variations in this kind of analysis.

To take advantage of the opportunities offered by this branch of mathe

matics it will be necessary to employ reasonably abstract forms of

analysis. Indeed, there are indications that economists will be using

the Calculus of Variations to an increasing extent in the near future.

It is hoped that this study will be useful on both counts.

The study is organized into four chapters. In the first chapter

a brief survey of previous attempts to apply the Calculus of Variations

is undertaken and the necessary mathematical preliminaries for the main

part of the study are set forth. These latter are concerned with the

nature of homogeneous production functions, transformation loci and the

conditions which must be met to achieve constrained maximum of such

functions. The material will be recognized as that necessary for work

in the field of mathematical economics.

The second chapter is concerned with a description of several

models of economic growth which are the subject of considerable interest

in the current economic literature. These include aggregate as well as

multisector economic growth models with the latter being the main focus

of attention in this study.

In the third chapter the main theoretical development of efficient

paths of capital accumulation is undertaken. Both methodologically and

substantively the current capital model is extended by the use of the

Hamilton-Jacobi formulation of the Calculus of Variations. The following

results which go beyond the current concept of a capital model are obtained:

1. There are important differences when the model is independent of time compared with the situation when time is an explicit variable.

2. In the time independent or conservative case there exists a set of prices, a discount rate, and an own rate of interest or growth which take the form of an additional constraint.This constraint says that the discounted value of all new investment is constant.

3. Maximization of capital accumulation with these prices is equivalent to the maximization without the specific incorporation of such prices.

Looking1 toward the time when such a model can be used for planning

and decision-making the study concludes with an examination of a number of

computational methods to obtain optimal paths of capital accumulation.

Two principal methods, the use of generating functions and direct methods,

are discussed and the possible economic implications are indicated.

In view of the interrelated economic and mathematical considerations

which are involved in this study my debt of gratitude to my dissertation

committee is particularly heavy. To Dr. Naidel, Dr. Smith, Dr. Jacobs,

Dr. Caplan and Dr. Wolozin, I wish to express my thanks for their aid andiii

encouragement. In many ways too numerous to mention the help of the

Research Analysis Corporation must be acknowledged. And finally, no words

could adequately describe the extent of my thanks to my wife and children

for their patience and encouragement over the years.

iv

TABLE OF CONTENTS

CHAPTER PAGE

PREFACE...............................................................ii

I. PRELIMINARY CONSIDERATIONS FOR THE DEVELOPMENT OF A

CAPITAL MODEL INVOLVING THE USE OF THE CALCULUS OF

VARIATIONS .................................................. 1

A. Introduction ................................... 1

B. Historical Developments ............................... 2

C. Nature of the Calculus of Variations . . . . . . . . . 7

D. The Transformation Function or L o c u s ...................11

1. Role in Economic Analysis.................... 11

2. Capital Stocks . . .......................... . 15

3. First Order Homogeneous Production Function . . . . 16

II. MODELS OF ECONOMIC GROWTH IN THE RECENT HISTORY OF

ECONOMIC I D E A S ..................................... 18A. General Vie w s............................................18

B. Aggregate Economic Model and Economic Growth ......... 22

1. Harrod-Domar M o d e l .......................... 24

2. Hicks-Samuelson Model........................ 27

C. Multisector Economic Growth Models .................. 29

1. Ramsey M o d e l .................... 30

2. Generalization of the Ramsey M o d e l ..........32

3. Efficient Paths of Capital Growth.................. 36

4. Economic Growth in Activity Analysis . . . . . . . 39

III. EXTENSIONS OF THE CURRENT CONCEPT OF A COMPLETE

CAPITAL MODEL ........................................... 42

CHAPTER PAGE

A. Preliminary Discussion . . . . . . . . . 42

B. Economic Analysis in Higher Dimensional Space . . . . 50

1. Role of Constraints.................... 51

2. Durrent Capital Model Considered in this Space . . 53

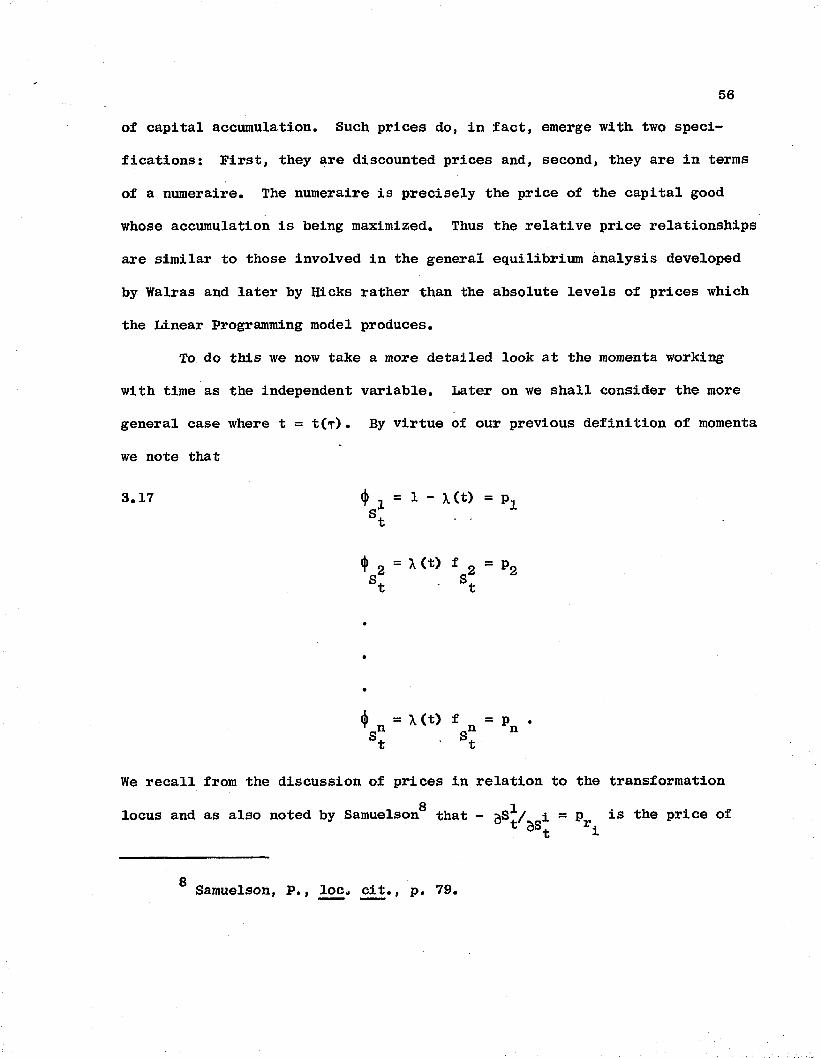

C. Nature of Prices..................................... 55

D. Implicit Fundamental Constraint .................... 58

E. Efficient Paths in N Space and in the Extended

Phase Space ..................................... 63

F. -Transversal Surfaces and the E n v e l o p e .............. 67

G. Economic Significance of the Analysis .............. 69

IV. IMPLICATIONS OF COMPUTATIONAL METHODS FOR ECONOMIC GROWTH . 73

A. An Overall V i e w .............................. 73

B. Methods of Solution ............. 74

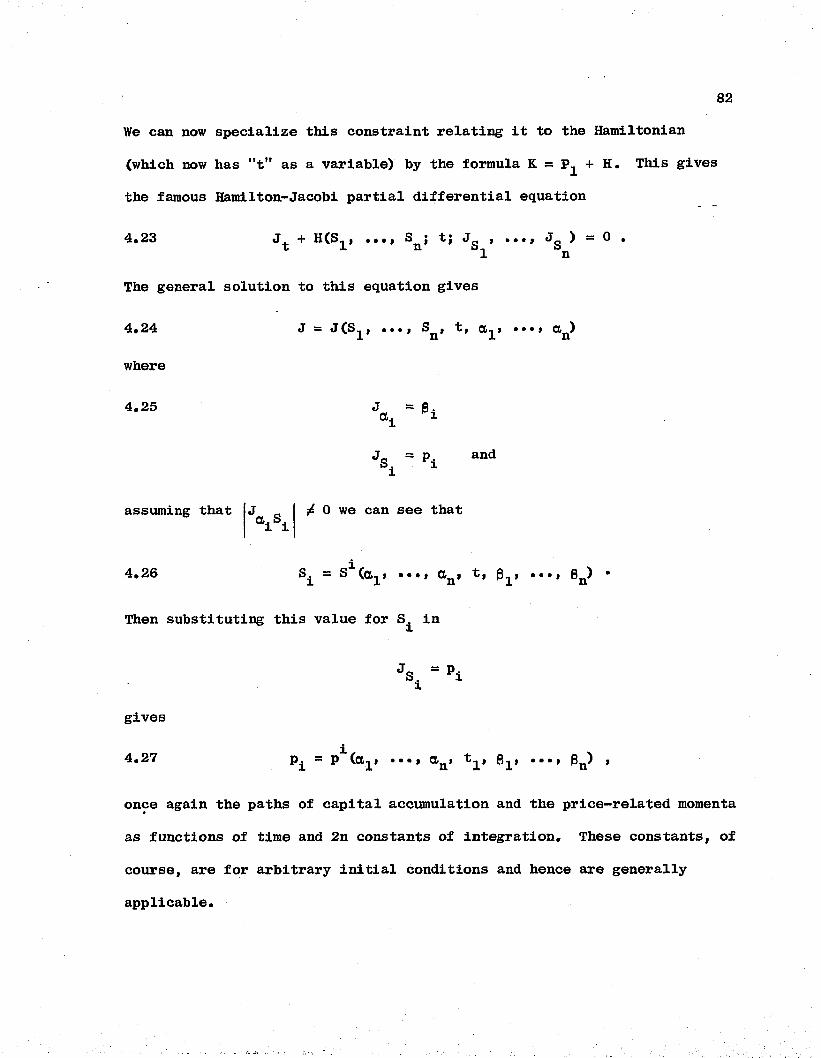

1. Use of Generating Functions.............. 75

a. Hamilton's Principle Function ............ . 75

b. Jacobi's Generating Function Approach . . . . 79

2. Direct Methods.................. 83

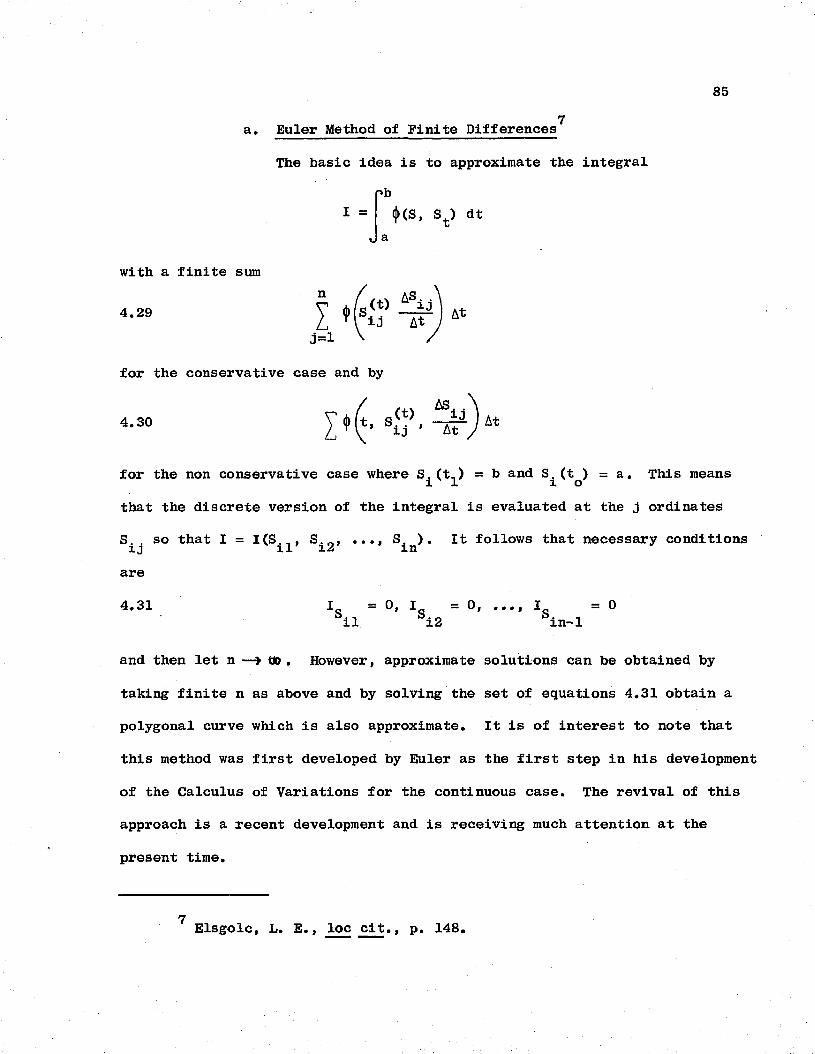

a. Euler Method of Finite Differences .......... 85

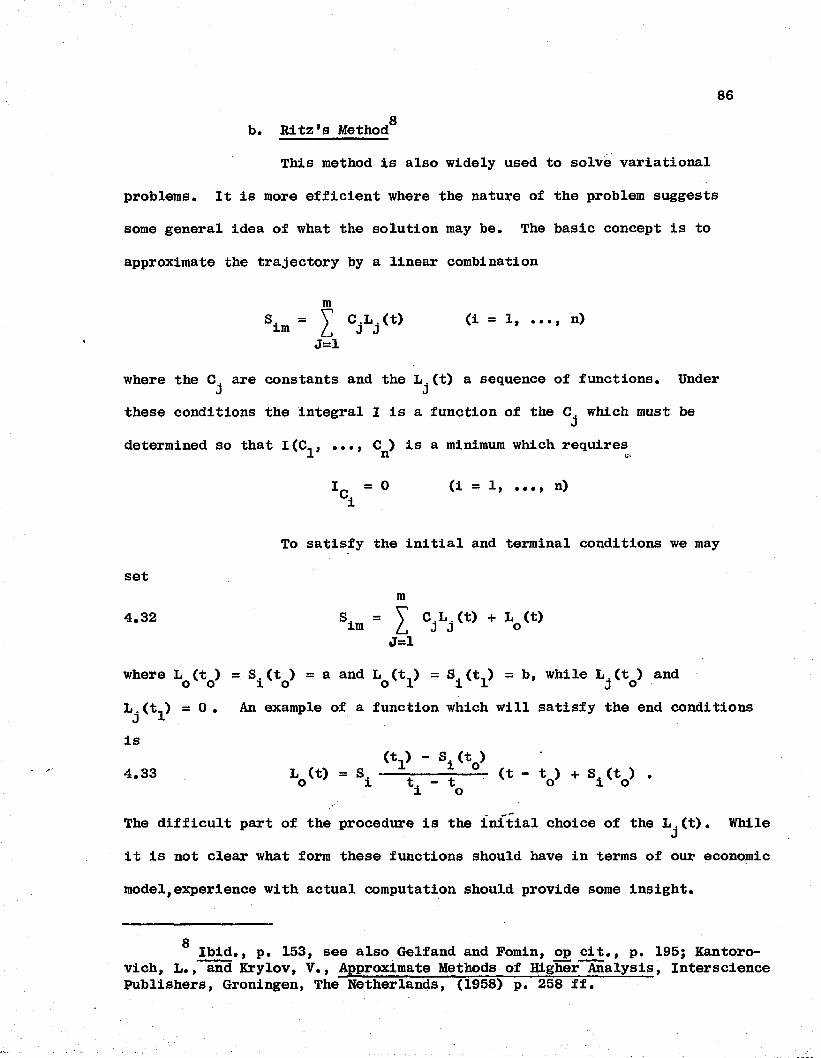

b. Ritz's M e t h o d ............................... 86

BIBLIOGRAPHY . ......................... 87

APPENDIX ........................................................ 91

Vi

CHAPTER I

PRELIMINARY CONSIDERATIONS FOR THE DEVELOPMENT OF A

CAPITAL MODEL INVOLVING THE USE

OF THE CALCULUS OF VARIATIONS

A. INTRODUCTION

This is a purely theoretical study to investigate a general

Capital Model of heterogeneous capital goods by use of the Calculus of

Variations. It has as its aim extending the results achieved by

Professors Samuelson, Solow and others, and will bring to bear in this

field powerful mathematical insights which the use of the Calculus of

Variations makes possible. The new employment of an old tool in

theoretical economics has a relatively short history going back some

40 years and we shall make a cursory examination of these developments

as well as describe in very brief compass the nature of the mathematical

tool in the first chapter.

To expand further the theoretical results for a Capital Model we

shall develop the framework of the analysis at an abstract level,

specializing it to cover both the time independent and the time dependent

cases. This will be accomplished by parametrizing the problem and then

working in a space of higher dimension. It will then be possible to

employ the Hamilton-Jacobi formulation with significant advantages over

current capital models by bringing into the picture the role of prices and

their relationship to the momenta of classical mechanics. Moreover, we

shall show that by carrying out the analysis in the larger space and

utilizing the Hamiltonian there exists a constraint on the system with

interesting economic content. These results are presented in Chapter III.

To indicate that a capital model has potential usefulness beyond

its purely theoretical interest we shall survey some of the methods which

may be employed to solve Calculus of Variations problems. Some of these

methods have economic content which is of interest; other methods are purely numerical in character but are capable of computer solution. Much

attention and a lot of resources are being concentrated in this difficult

mathematical field and economists should be made aware of these developments

and their prospective usefulness. This survey is presented in Chapter IV,

and as far as can be determined from the literature this has not been done

before.

B. HISTORICAL DEVELOPMENTS

During the decade of the 1920's the first substantial interest in

the use of the Calculus of Variations as a tool in Economics is discernible

even though the tool itself has been developed over the past several

centuries. In an important article, "A General Mathematical Theory of

Depreciation," which appeared in the Journal of the American Statistical

Association (1925), Professor Hotelling wrote:

...But the problem here transcends the questions of depreciation and useful life, and belongs to the dawning economic theory based upon considerations of maximum and minimum which bears to the older theories the relations which the Hamilton dynamics and the thermodynamics of entropy bear to their predecessors...

...A thorough working knowledge of the Calculus of Variations is a prerequisite to the development of this type of economic theory— which doubtless explains why it has not developed further.

During this period a number of articles appeared by Hotelling,

Evans and Roos in which the Calculus of Variations was employed in the

Analysis of depreciation as well as in more general problems of monopoly

and competition. In retrospect, this burst of analytical activity does

not appear to have had much impact on subsequent theoretical developments.

In 1928, Frank Ramsey, a protege of the late .Lord Keynes, wrote a

pioneering article in the Economic Journal, 1928, "A Mathematical Theory

of Saving," which alluded to the use of Variational Analysis in the field

of capital growth and which has become the starting point for current

theoretical analysis to be described below.

The period of the 1930's saw some further development of this

earlier work by Hotelling, Evans and Roos but still without much impact.

However, an interesting point of view was presented by F. Creedy in two

articles in Econometrica in 1934 and 1935;

(1) "On Equations of Motion of Business Activity"

(2) "An Economic Interpretation of the Principle of LeastAction and Other Dynamical Theorems."

In these two articles Creedy attempted to utilize in economic

analysis the wealth of results which came from the use of the Calculus

of Variations in Classical Mechanics. In order to bring the economic

concepts within the requirements of Classical Mechanics rather strained

definitions were used which no economist has been willing to accept.

However, the basic idea of utilizing the results of the Calculus of

Variations which have been developed in Classical Mechanics has

persisted to the present time. Professor Harold Davis in his The

Theory of Econometrics wrote:

...the Calculus of Variations appears destined to play an important role in the theory of economics, as it has in mechanics...

It is worthy of note that up to the outbreak of World War II all

the work cited above was done by mathematicians rather than economists,

for it was not yet generally agreed that mathematics was an important tool

for the economist and the Calculus of Variations represents an advanced

part of mathematics.The war and immediate post-war years represented a hiatus in the

attempts to use the Calculus of Variations in economic analysis, however

renewed interest has arisen during the decade of the 1950's. There are

multiple motivations for further use of the Calculus of Variations.

First of all, the advent of the high-speed electronic computer has made

it possible to obtain numerical results whereas formerly only those

problems which could be solved in closed form could be evaluated numerically

and very few variational problems fall within this category. Second, in

a real sense the Calculus of Variations may be looked upon as a generaliza

tion of Linear Programming which has experienced a phenomenal development

during the last ten years. Linear Programming, or more generally mathe

matical programming, is a technique for optimizing a functional (not

necessarily linear) subject to simultaneous inequality constraints.

Using matrix notation the linear programming problem may be presented in

the following way:

MaximizeT1.1 c x

subject toAx < b

where

°T - ■ 1 V ik=l

and

is

Ax < b

\' a ,x ^ b, (i — 1, .«., in j j — lj > ■ • j n)L i «J J _ id=i

In the Calculus of Variations formulation we wish to maximize

I

1.2 * [* < « • 1 r ] d t + I * i ( t ) t ± wi=l

where the (J) (x) = 0 are the constraints and the (t) are the Lagrangian

multipliers.

Third, increased interest in economic development has focused

attention on the growth of capital which is an area in which the

Calculus of Variations has been applied. Paths of capital accumulation

within the constraints inherent in the economic system such as the

availabilities of domestic resources, foreign exchange and other factors

are being studied.

In the post-war period Professors Paul Samuelson and Robert Solow

have been the chief, if not the only, ones engaged in the application of

the Calculus of Variations to economic theory and entirely in the area

of capital growth. In the Quarterly Journal of Economics, November 1956,

these authors jointly published "A Complete Capital Model Involving

Heterogeneous Capital Goods” which attempted to generalize the results

developed by Ramsey thirty years earlier. This article is a straight

forward application of some of the formalisms of the Calculus of

Variations which apply to the so-called “type-one" problem.1 For the

first time the Hamiltonian canonical equations are introduced into economic

analysis in a purely formal way in addition to the Euler equations which

represent necessary conditions for an optimal relationship.

In 1958 both authors, with the help of Professor Dorfman, published

their Linear Programming and Economic Analysis in which the problem of

efficient paths of capital accumulation was analyzed by means of Linear

Programming. It was stated that "the case of continuously flowing time

can be handled by the more sophisticated methods of the Calculus of

Variations in terms of n commodities and capital stocks, but we do not

give this extension here.1' This extension was originally written as an2appendix for this book but appeared as a separate article in a book

edited by Professor Arrow. In a footnote Samuelson states, "The mathe

matics of this paper bears a striking similarity to that of classical

mechanics."

1 It is convenient to classify Calculus of Variations problems into two groups: type one in which the variables to be determined areall functions of one independent variable; in type two problems the variable or variables are functions of more than one independent variable.

2 Mathematical Methods in the Social Sciences 1959 Proceedings of the First Stanford Symposium, Stanford Mathematical Studies of the Social Sciences.

7

C. NATURE OF THE CALCULUS OF VARIATIONS

Economists have long been familiar with the concept of finding the

maximum or minimum values of a given function or relationship. This

application of the calculus has been used to obtain a wide variety of

results in economic theory, which until the past decade was consigned to

the mathematical appendices of most books. Two notable examples are

Marshall's Principles of Economics and Hick's Value and Capital. In

more recent years, as questions of economic optimization requiring quanti

tative answers have arisen, other mathematical tools have been used. At

the present time much work in economics is being done utilizing a wide

variety of mathematical tools. In many instances they have been known

for a long time although there has been a very considerable development

of new mathematical methods of analysis which appear to offer opportunities

for employment in economics.

The Calculus of Variations which is sometimes referred to as

Variational Analysis has long been considered a part of classical mathe

matics and in recent years there has been a renewed interest in this

mathematical area. This has been brought about in large part by the need

to obtain best solutions where best is defined in some minimum or maximum

manner and by the advent of high-speed digital computers which provide a

means to obtain numerical answers to a wider range of problems.

Essentially, Variational Analysis is concerned with finding that

particular functional relationship or path along which another relationship

is a maximum or minimum. This is in sharp contrast with the ordinary task

of finding a value or values for which a known relationship is optimum.

Stated in relatively simple mathematics the problem is to find out of a

family of possible paths

1.3 y = y(x)

that one for which

nxi1.4 PCxjy.y') dx y* = dy/dx

x

is an optimum.For use in economic analysis where we shall have to deal with a

number of relationships simultaneously it will be necessary to handle

problems where we shall be looking for "n" different paths

1.5 y± = y^x) i = 1, ..., n

where

1.6 y = (y1} y2, yQ) ; y' = (y^ y2, • ••* y )

such that

■>x11.7 F(x,y,y') dx y ^ x 1) = y^ yj.(x°) = y°

o*Jx

is a maximum.

It will be observed that each of the relationships sought have the

same independent variable and specified limits of integration. For the

general problem of the Calculus of Variations, this latter limitation can

be removed where the nature of the analysis requires a more general context.

This means that a method of analysis is available for obtaining optimal

paths where the initial and terminal points each lie on its own locus of3points, h(y) and g(y), for example. It is therefore possible that alterna

tive initial and terminal points can be taken into account in obtaining the

optimum paths. The conditions which must be met are known as the "trans-

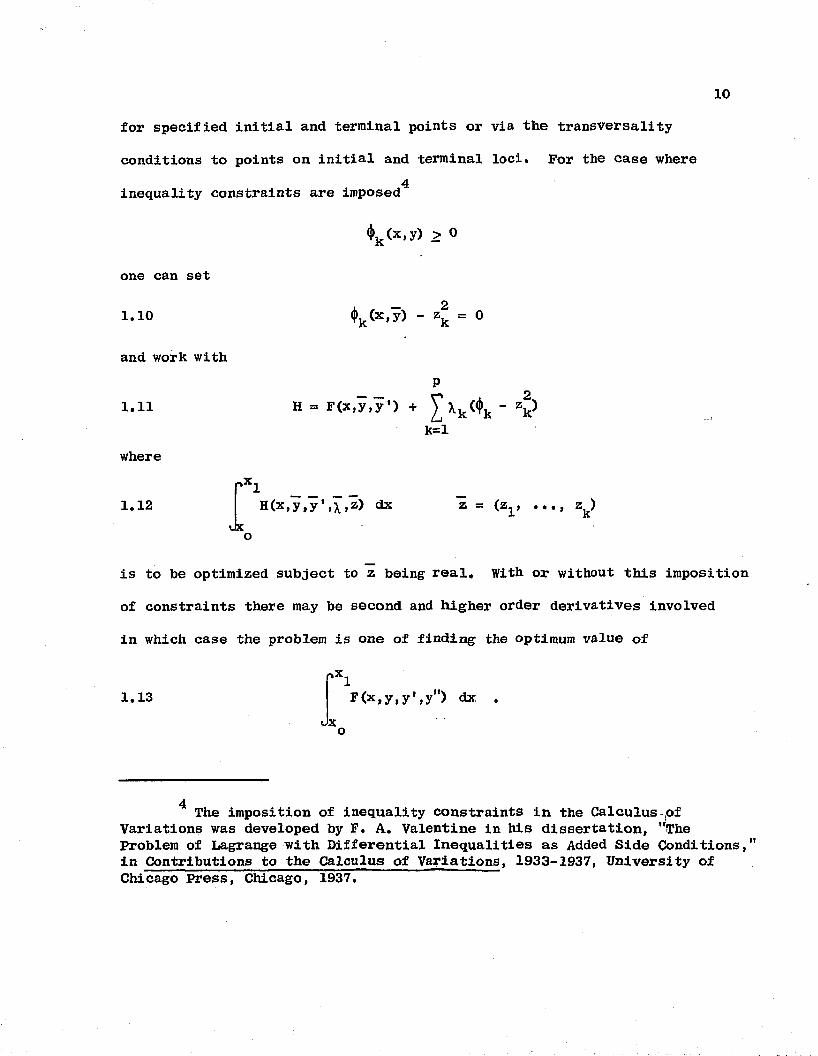

versality11 conditions.Other variations of the basic model can be carried out as specialized

applications of the Calculus of Variations. The paths can be subjected to

certain equality as well as inequality constraints. Given the equality

constraints

♦fc(x,y> = 0 > (k = 1, P)

which are to be imposed on y^ = y^(x) we form the new function

P1.8

k=l

and optimize

1.9 G(x,y,y\\) dx X = (Xx

3 If there were alternative initial levels of capital to be investigated then these possibilities would be described by the locus h(y). We do not go into this matter in the investigation.

10

for specified initial and terminal points or via the transversality

conditions to points on initial and terminal loci. For the case where4inequality constraints are imposed

‘Lcx.y) > 0

one can set

1.10

and work with

^k(x,y) " Zk = 0

1.11

where

1.12rxi

H = F(x,y,y’) +k=l

H(x,y,y',x,z) dx Z - (Zj i . • • , Z )Ox

is to be optimized subject to z being real. With or without this imposition

of constraints there may be second and higher order derivatives involved

in which case the problem is one of finding the optimum value of

r>x.

1.13 F<x»y>y’»yn) dx .Ox

The imposition of inequality constraints in the Calculus -sof Variations was developed by F. A. Valentine in his dissertation, "The Problem of Lagrange with Differential Inequalities as Added Side Conditions," in Contributions to the Calculus of Variations, 1933-1937, University of Chicago Press, Chicago, 1937.

11

While it is possible that in the field of economics derivatives higher than

the first might be involved we shall not treat them.

From a purely mathematical standpoint there are a number of strong

requirements on the functions involved particularly regarding continuity

and differentiability which we shall assume. Necessary conditions to obtain

the optimal paths are well understood;, the use of the Weierstrass conditions

to determine sufficiency are more difficult and we shall not be concerned

with them.

In order to determine optimal paths of "n” simultaneous relationships

it will be necessary to work in "n" dimensional space. On occasion by

doubling the size of the space to 2n it will be possible to exhibit funda

mental relationships which are otherwise not obvious. This is accomplished

at the expense of adding to the computational burden. This more powerful

method of mathematical analysis, which came from the genius of W. R. Hamilton,

has a special significance for economic analysis which we shall utilize to

obtain our main results.

D. THE TRANSFORMATION FUNCTION OR LOCUS5

1. Role in Economic Analysis

For a number of years mathematical economists have utilized

the concept of a transformation locus in the theoretical analysis of the

firm. In this type of analysis it is assumed that the firm can produce two

g This discussion borrows from R. G. D. Allen's two books, Mathematical Analysis for Economists, Macmillan, 1938, and Mathematical Economics, St. Martins Press, 1956.

or more products X , X , . X with given supplies of factors of production.l a nAt this stage of the discussion we shall limit the number of products which

can be produced by a firm to two, X,Y, for purposes of easier exposition.

The results can be generalized to n products in a straightforward manner.

With the production of an amount x of X the fixed resources can be used for

the production of the greatest amount y of Y compatible with the production

of X. It is taken as normal that at higher levels of output of X the output

of Y will decrease at a faster rate and the reverse arguments would also

hold. Thus we may symbolize these relations in the following manner:

1.14 y = f (x) , x = g(y)

where both are single valued and monotonic decreasing functions. The two

functions are inverse to each other and we may write

1.15 F(x,y) = 0

which is what we call the transformation function or locus (sometimes

referred to as an efficiency locus). It represents a menu of the production

possibilities where the maximum amount of product or product mix is desired.

By the very nature of the concept lesser amounts of one or both products are

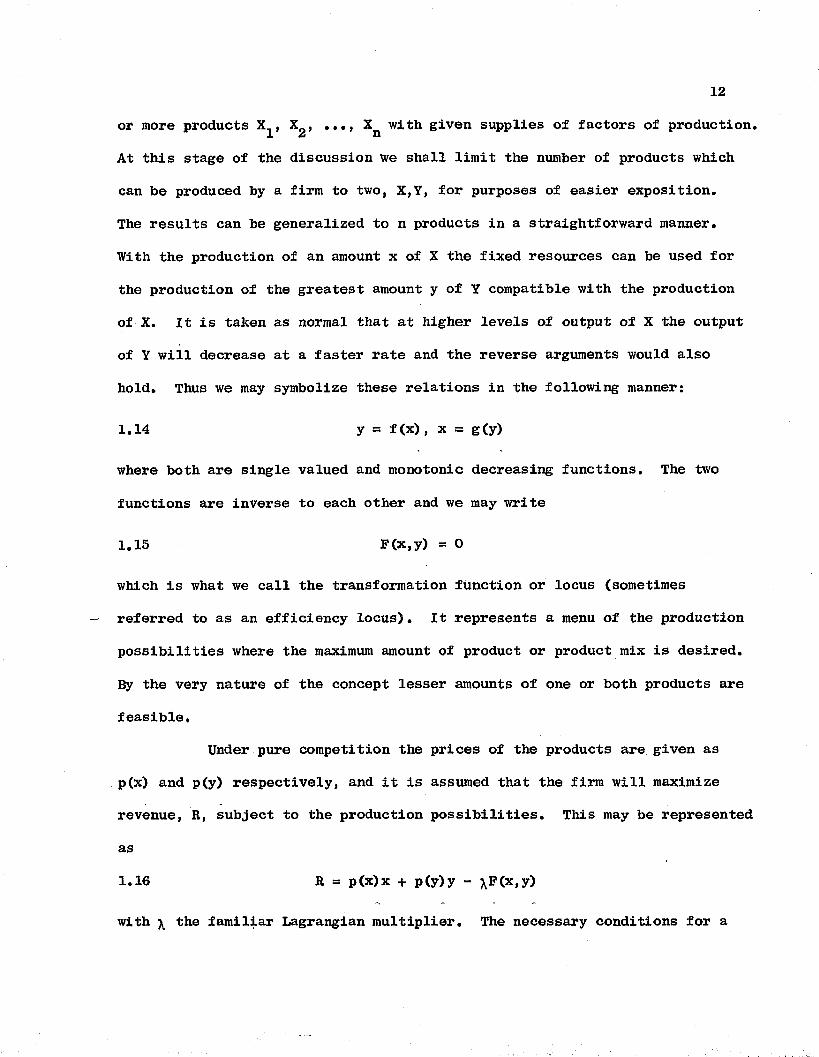

feasible.Under pure competition the prices of the products are given as

p(x) and p(y) respectively, and it is assumed that the firm will maximize

revenue, R, subject to the production possibilities. This may be represented

as

1.16 R = p(x)x + p(y)y - \F(x,y)

with \ the familiar Lagrangian multiplier. The necessary conditions for a

maximum are

1.17 = 0 = p(x) - xFx (x,y)

so that

= ° = P(y) - XFy(x,y)

p(x)/p = X = p(y)/jX

and that

1.18 _y _ p(y) .f x p(x)

This can be generalized immediately to n products X^, X^,

and we may state the conditions as follows:

1.19 _a!L

is a negative definite matrix. This means that the bordered Hessian

1.20 x.

X1X1

X X Xn n 1

n

x,x 1 n

X Xn n

must have the proper sign. The signs of the determinants under these

circumstances alternate in the following manner:

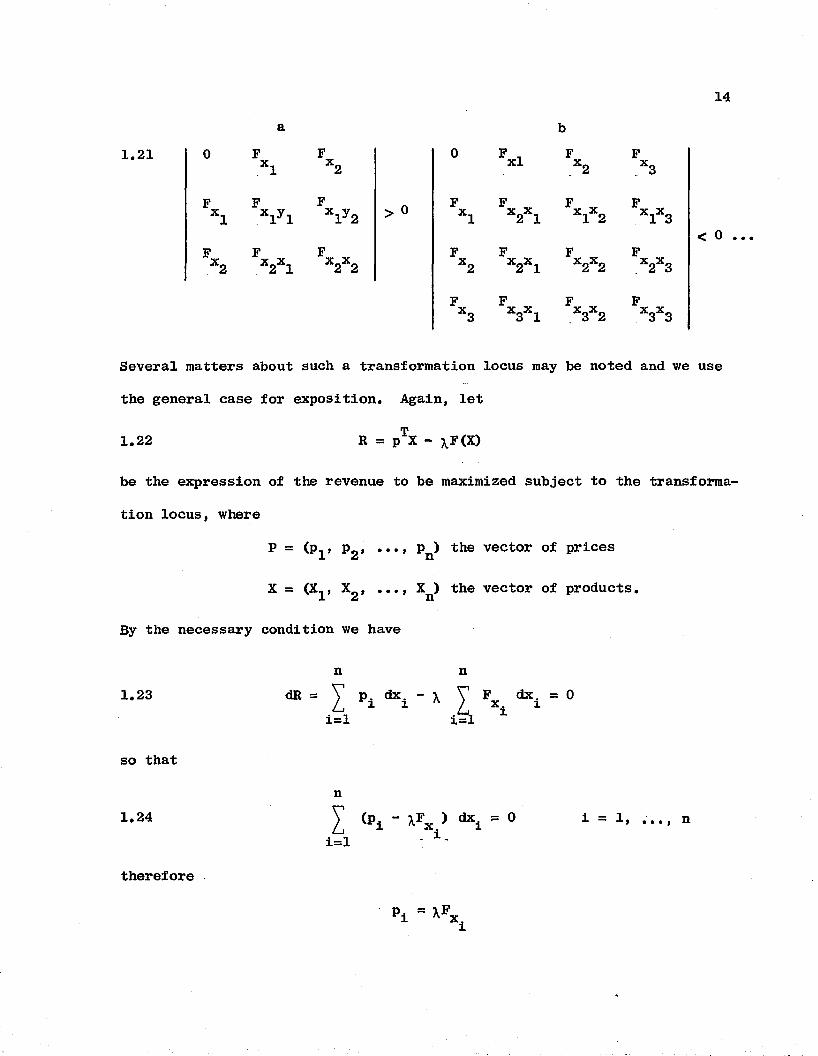

Several matters about such a transformation locus may be noted and we use

the general case for exposition. Again, let

be the expression of the revenue to be maximized subject to the transforma

tion locus, where

P = (P-. > P m •••» P ) the vector of prices l & n

X = (X , X2, ..., Xn) the vector of products.

By the necessary condition we have

1.22 R = pTX - xF(X)

n n1.23

i=lP dx. = 0x. 1ii=l

so that

n1.24

i=JL

therefore

so that

This means that pair-wise the ratio of prices must equal the marginal rate

of substitution of product j for product i. These are the well known

tangency conditions of the transformation locus and the hyperplane repre

senting the value of production.

For the two product case we have for any jj, such that 0 < jj, < 1 .

1.26 uPOCjYj) + (1 - (J.) F(X2Y2) < F + (1 - |i) X2> ^ + (1 - ji) Y2]

in view of the concavity of the transformation locus. This means that any

convex linear combination of maximum outputs is also a feasible or attainable

level of output for the two products although it is not itself a maximum

achievable level of output.

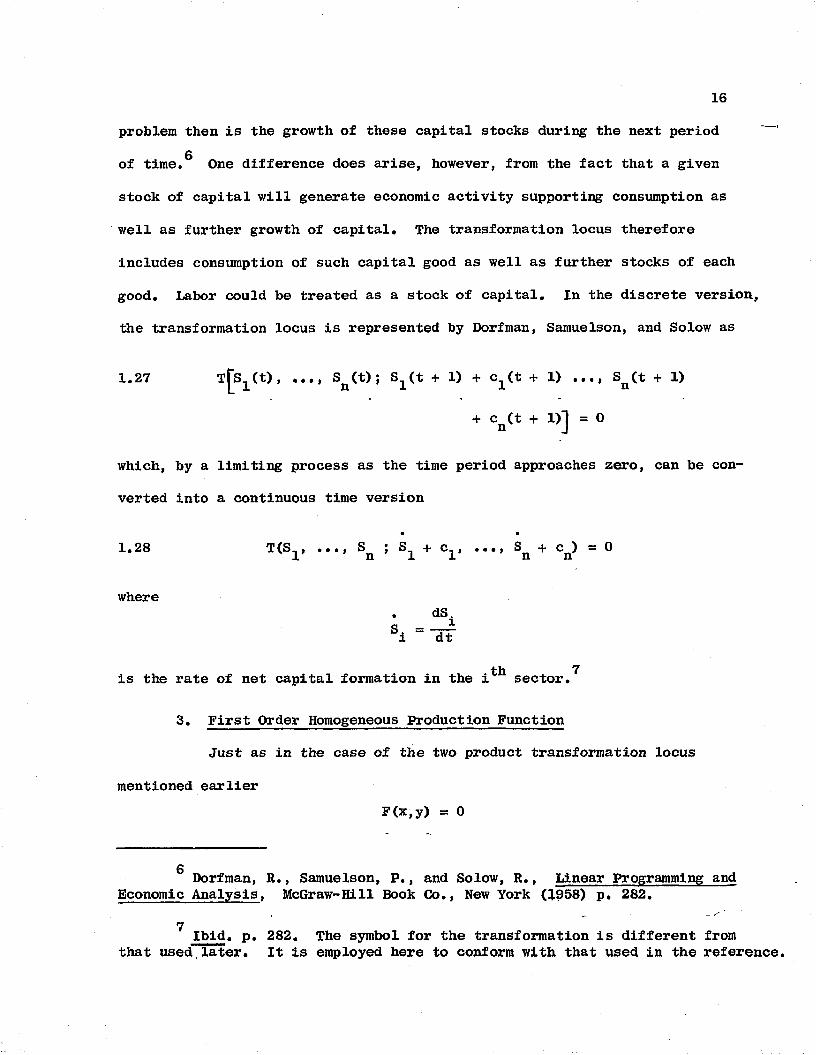

2. Capital Stocks

It is only a short step from the concept of a transformation locus

involving multiple products of a firm to the idea of one involving alterna

tive levels of capital stock accumulation in the economy at large. In the

former case, it is the factors of production available to the firm which

are considered fixed. In the latter case, it is the stocks of all of the

factors or commodities which are considered fixed at any given time. The

16

problem then is the growth of these capital stocks during the next periodg

of time. One difference does arise, however, from the fact that a given

stock of capital will generate economic activity supporting consumption as

well as further growth of capital. The transformation locus therefore

includes consumption of such capital good as well as further stocks of each

good. Labor could be treated as a stock of capital. In the discrete version,

the transformation locus is represented by Dorfman, Samuelson, and Solow as

1.27 Tfs. (t), ..., S (t); S (t + 1) + c (t + 1) ..., S (t + 1)1 n l l n+ cfl(t + l)j = 0

which, by a limiting process as the time period approaches zero, can be con

verted into a continuous time version

• •

1.28 T(S^, ..., Sn i S1 + c^i i•.i Sn + c^) = 0

wheredS

S, = -rf i dt

th 7is the rate of net capital formation in the i sector.

3. First Order Homogeneous Production Function

Just as in the case of the two product transformation locus

mentioned earlierF(x,y) = 0

gDorfman, R., Samuelson, P., and Solow, R., Linear Programming and

Economic Analysis, McGraw-Hill Book Co., New York (1958) p. 282.7 Ibid. p. 282. The symbol for the transformation is different from

that used.later. It is employed here to conform with that used in the reference.

where it was possible to solve for y = f(x) so we may solve for one of the

variables, say S^t), in terms of the other variables to give

In this form the relationship may be considered as a production function

since there are underlying production functions for each S^(t). Moreover, we

may assume the production function to be homogeneous of the first degree, i.e.

for production functions is often made in economic theory. Its reasonableness

is based upon the contention that under perfect competition in the long run

and at the most efficient levels of output, marginal and average costs tend

to be the same. Its pertinency in the Calculus of Variations lies in the

fact that the necessary and sufficient condition to utilize a parametric

representation of the functional is that the integral be a homogeneous

function of the first degree. With such a representation it becomes possible,

as is shown below, to obtain analytical results not otherwise attainable.

1.29 • • • 9

1.30

s1(t), ..., sn(t))

and

1.31

The assumption of a homogeneous relationship of the first order

CHAPTER XI

MODELS1 OF ECONOMIC GROWTH IN THE

RECENT HISTORY OF ECONOMIC IDEAS

A. GENERAL VIEWS

In this chapter we shall investigate the role which capital accumula

tion has played in recent years in the formulation of models of economic

growth and place the concept of efficient paths of capital accumulation in

perspective. We shall be able to show the tradition out of which this

latter concept has grown and therefore place our analysis in its proper

historical setting. While the question of the nature and role of capital

has been a subject of investigation at least since the days of Adam Smith,

we shall confine our attention primarily to the period since World War II

with one or two notable exceptions, but we must recognize that the question

of economic growth and the role of capital was one of the principal concerns

of Ricardo.... The extension of the classical analysis by Marx is too familiar

to need any elaboration. Toward the end of the 19th century the subject of

capital was again an object of investigation by BHhm-Bawerk and J. B. Clark.

Since we are dealing with efficient paths of capital accumulation

and much of the economic literature is in terms of growth models we must be

clear about the meanings we ascribe to these concepts. In the literature,

growth is generally taken to mean the rise in national income (or one of the

related magnitudes such as Gross National Product) but it could just as well

1 The word model is used to indicate a formal framework within which to carry out the economic analysis.

19

be represented by the rise of the total output of the economy. Moreover,

it can be on a total value basis, a per man basis or even on a per hour

basis, although the latter is frequently a measure of productivity. When a

total value basis is used it is generally in real terms or constant dollars

so that monetary considerations do not enter into the analysis. By carrying

out the analysis in terms of a per man basis the growth in the population

or labor force is brought into the analysis. But what is of particular

interest is the fact that growth as it has been used is an aggregate concept

covering the entire economy rather than growth of an industry or particular

sector such as steel, automobile, weaving or textiles. The nature of growth

is also subject to varying interpretations. From one point of view it could

be understood to mean the most rapid rate of growth possible although this

would have to be subject to certain types of constraints otherwise consumption,

the government sector and the foreign trade sectors would be called upon to

undergo unacceptable deprivations. Other yardsticks for measuring growth

could involve the question of maintaining full employment of capital resources

as well as labor. Still another concept might be that rate of growth which

is consistent with the saving and investing patterns of activity of the

entrepreneurial class. Regardless of which concept is of interest the

determinants of the growth rate are inherent in the economic structure and

are in a sense market oriented although it is of course true that the govern

ment is not without resources to exert direct or indirect influence over

economic growth.

On the other hand efficient paths of capital accumulation will be

understood to refer to investment, on a net basis, in one or more specified

industrial sectors, in contrast to the path through time of some measure of

20

overall economic activity such as total production, indicated in the above

paragraph. How the sector or sectors are selected is not the critical

issue but the fact that there is some central control involved is what is

required. The objective might be the build-up of the fertilizer industry

as an example and the goal to be achieved would be to reach some specified

level of capacity in the particular industry. Of course, as is true for

the aggregate analysis referred to previously, resources are limited for

the case under consideration. Resources devoted -to the build-up of a given

industry or industries must be obtained at the expense of other industries,

consumption, government activities or such other economic activities as

might be involved.

What we are concerned with is known in the literature as a multi

sector model of the economy in which all the relevant sectors are included

in the analysis. This is in sharp contrast to the aggregate type models

where total levels of production, consumption, investment and government

spending are involved. It is the maximization of investment in a particular

sector which is to be achieved with the other sectors a central part of

the analysis. Within such a framework efficient paths of capital accumula

tion will not only involve the sector whose path is to be maximized but

also the paths of the other sectors of the economy. Their pattern of growth

is such that the necessary conditions of the Euler-Lagrange equations are

satisfied. Moreover, all the paths including the one which is maximized

must satisfy the fundamental relationship between the various own rates of

interest, which we shall briefly consider in the next chapter although it

is not the main focus of attention in this study.

21

The kind of problem to which this analysis addresses itself is

similar to what a developing country faces after having decided what sectors

must be developed first. The model with which we are concerned, however,

presents an idealized pattern of what could be accomplished within the

constraints imposed; it does not purport to represent a realistic situation

that one might find in an economy. As in so much of economic theorizing it

has the possibility of giving some added insights into the growth problem.

We shall see that the kind of analysis to be undertaken springs from

two separate but related traditions in the development of economic ideas,

both of relatively recent origin. In both traditions it is recognized that

economic growth, however defined, can be brought about or at least influenced

by many factors including institutional arrangements, development of tech

nology, productivity of labor, changes in consumers preferences, monetary

factors and changes in expectations. However, it is the essence of economic

theory to be able to select out from the welter of detail those factors which

can be identified as being the main motors in providing the thrust of the

economy. This is especially true in the macro-economic field although it

brings with it problems involving the degree of aggregation, measurement,

errors in the data, comparability of information and a host of other diffi

culties which make the testing of hypotheses about economic activity

troublesome. But all this is nothing new in either the micro or macro

economic theories which economists have expounded to bring about greater

understanding of the nature of economic activity.

22

B. a g g r e g a t e e c o n o m i c m o d e l a n d ec o n o m i c g r o w t h

The post World War II period has witnessed an unprecedented amount

of theoretical analysis in the formulation of economic models describing

paths and levels of economic activity. The pioneering work was done by2Harrod in an article published just prior to the outbreak of the war and

slightly recast and enlarged in a series of lectures which appeared in book

form in 1948 under the title, Towards A Dynamic Economics. There have been3 4a number of suggested modifications associated with Domar , Baumol ,

5 6 7 8 9 10Alexander , Hicks , Duesenberry , Phillips , Goodwin , and Samuelson .

2 Harrod, Roy F., "An Essay in Dynamic Theory," Economic Journal,1939. See also Towards A Dynamic Economics, Macmillan, 1949.

Domar, Evsey D., "Capital Expansion, Rate of Growth and Employment,"Econometrica, Vol. 14, p. 137-147. See also his Essays in the Theory of Economic Growth.

^ Baumol, William J., "Formalization of Mr. Harrod's Model," Economic Journal, Vol. 59 (1949). See.also Economic Dynamics, Macmillan, 1951.

g Alexander, Sydney, "Mr. Harrod's Dynamic Model," Economic Journal Vol. 60 (1950).

0 Hicks, J. R., A Contribution to the Theory of the Trade Cycle,Oxford Clarendon Press, 1959.

7 Duesenberry, James J., "Hicks on the Trade Qycle," Quarterly Journal of Economics, Vol. 64 (1950).

Phillips, W. A., "Stabilization Policy in a Closed Economy," Economic Journal, Vol. 64 (1950).

9 Goodwin, R. M., The Non-Linear Accelerator and the Persistence of Business Cycles," Econometrica, Vol. 19.

10 „Samuelson, Paul A., Interactions between the Multiplier Analysisand the Principle of Acceleration," Review of Economic Statistics, Vol. 21.

By and large the differences or modifications described in the literature

tend to be matters of detail in terms of our main interest. They involve

such issues as continuous versus period analysis, the number of time lags

to be incorporated in the consumption, savings and investment relationships,

the expected path of autonomous investment, and the linearity of such

relationships. It is of particular interest to note that in none of these

articles is there any attempt to identify their theoretical developments

with the work of such eminent economic theorists as Schumpeter’1-'1' or Joan 12Robinson even though the latter two had been active in the field of

economic development as early as the decade of the '30's. If there was

any real source it was Keynes and the "General Theory" but mainly as a point

of departure, for his is essentially a static equilibrium model with no

attempt at analyzing the paths of economic activity through time. One of

his basic conclusions that there can be equilibrium at less than full

utilization of labor typifies his general approach. However, the focus of

his attention on the role of investment and the consumption relationship

had a profound impact on the work of Harrod, Domar and others. But Keynes

never had a concept involving the accelerator which relates induced invest

ment to changes in income levels and it was therefore not to be expected

that his model would be dynamic in the sense that the growth in income would

Schumpeter, Joseph, The Theory of Economic Development, Harvard University Press, Cambridge, Mass., 1934.

12 Robinson, Joan, Accumulation of Capital

be related to investment and at the same time influence the levels of such

investment. We must look to Harrod for this development and its logical

extension.

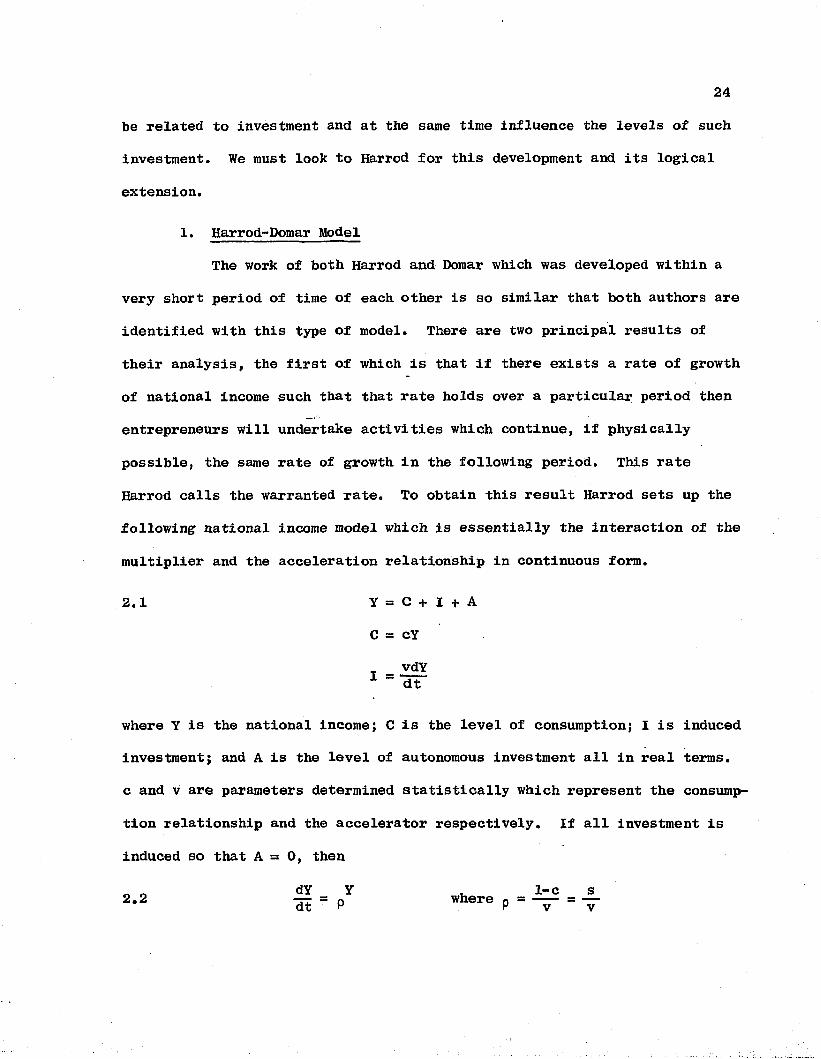

1. Harrod-Domar ModelThe work of both Harrod and Domar which was developed within a

very short period of time of each other is so similar that both authors are

identified with this type of model. There are two principal results of

their analysis, the first of which is that if there exists a rate of growth

of national income such that that rate holds over a particular period then

entrepreneurs will undertake activities which continue, if physically

possible, the same rate of growth in the following period. This rate

Harrod calls the warranted rate. To obtain this result Harrod sets up the

following national income model which is essentially the interaction of the

multiplier and the acceleration relationship in continuous form.

2.1 Y = C + I A

C = cY

vdYdt

where Y is the national income; C is the level of consumption; 1 is induced

investment; and A is the level of autonomous investment all in real terms,

c and v are parameters determined statistically which represent the consump

tion relationship and the accelerator respectively. If all investment is

induced so that A = 0, then

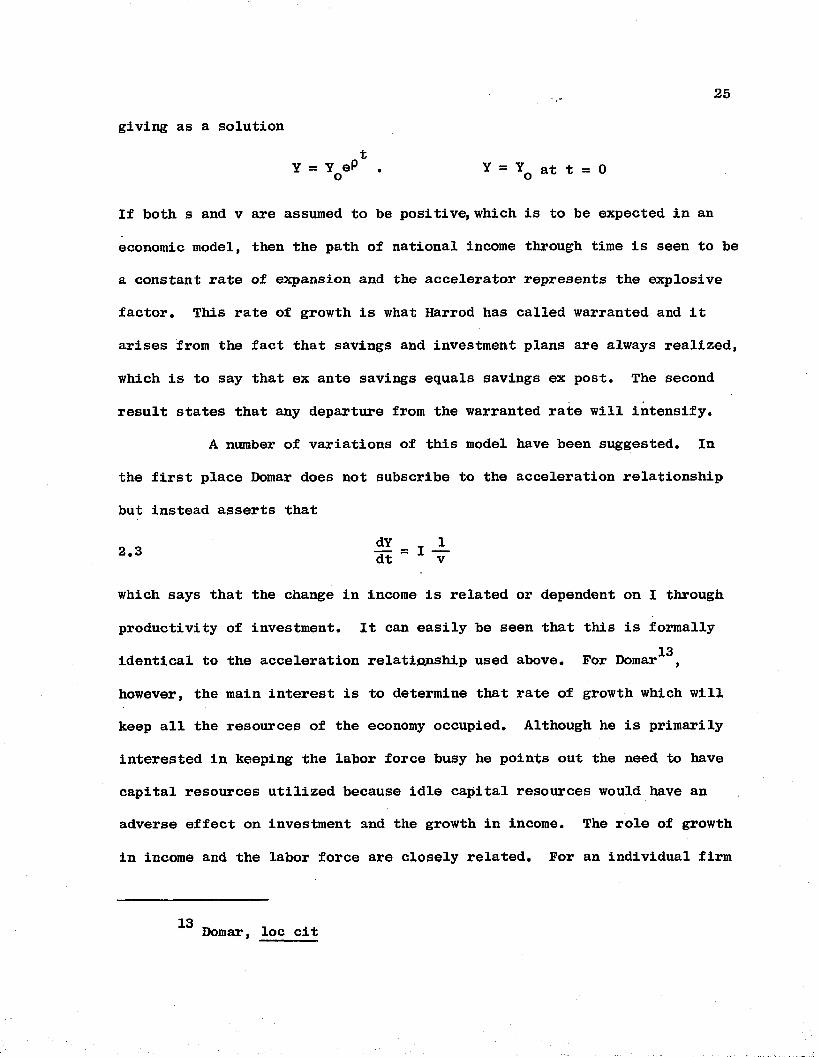

giving as a solutiont

Y = YQeP . Y = Yq at t = 0

If both s and v are assumed to be positive, which is to be expected in an

economic model, then the path of national income through time is seen to be

a constant rate of expansion and the accelerator represents the explosive

factor. This rate of growth is what Harrod has called warranted and it

arises from the fact that savings and investment plans are always realized,

which is to say that ex ante savings equals savings ex post. The second

result states that any departure from the warranted rate will intensify.

A number of variations of this model have been suggested. In

the first place Domar does not subscribe to the acceleration relationship

but instead asserts that

which says that the change in income is related or dependent on I through

productivity of investment. It can easily be seen that this is formally13identical to the acceleration relationship used above. For Domar ,

however, the main interest is to determine that rate of growth which will

keep all the resources of the economy occupied. Although he is primarily

interested in keeping the labor force busy he points out the need to have

capital resources utilized because idle capital resources would have an

adverse effect on investment and the growth in income. The role of growth

in income and the labor force are closely related. For an individual firm

13 Domar, loc cit

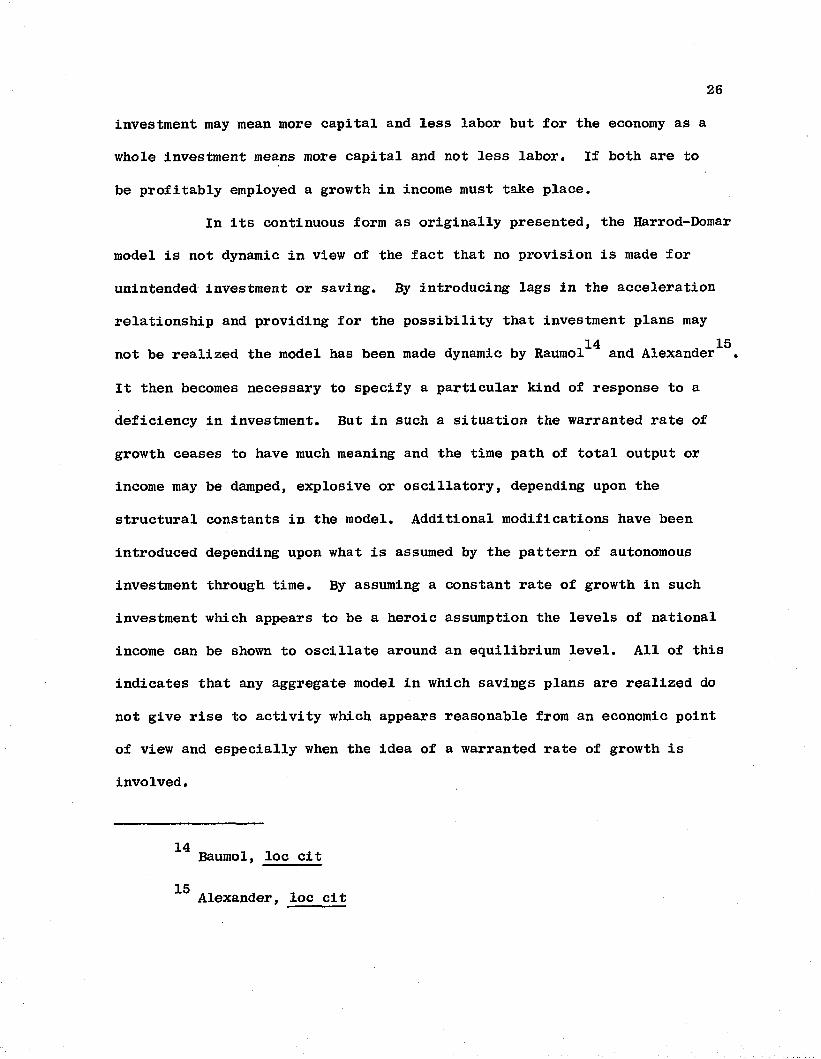

26

investment may mean more capital and less labor but for the economy as a

whole investment means more capital and not less labor. If both are to

be profitably employed a growth in income must take place.

In its continuous form as originally presented, the Harrod-Domar

model is not dynamic in view of the fact that no provision is made for

unintended investment or saving. By introducing lags in the acceleration

relationship and providing for the possibility that investment plans may14 15not be realized the model has been made dynamic by Raumol and Alexander .

It then becomes necessary to specify a particular kind of response to a

deficiency in investment. But in such a situation the warranted rate of

growth ceases to have much meaning and the time path of total output or

income may be damped, explosive or oscillatory, depending upon the

structural constants in the model. Additional modifications have been

introduced depending upon what is assumed by the pattern of autonomous

investment through time. By assuming a constant rate of growth in such

investment which appears to be a heroic assumption the levels of national

income can be shown to oscillate around an equilibrium level. All of this

indicates that any aggregate model in which savings plans are realized do

not give rise to activity which appears reasonable from an economic point

of view and especially when the idea of a warranted rate of growth is

involved.

^ Baumol, loc cit

Alexander, loc cit

27

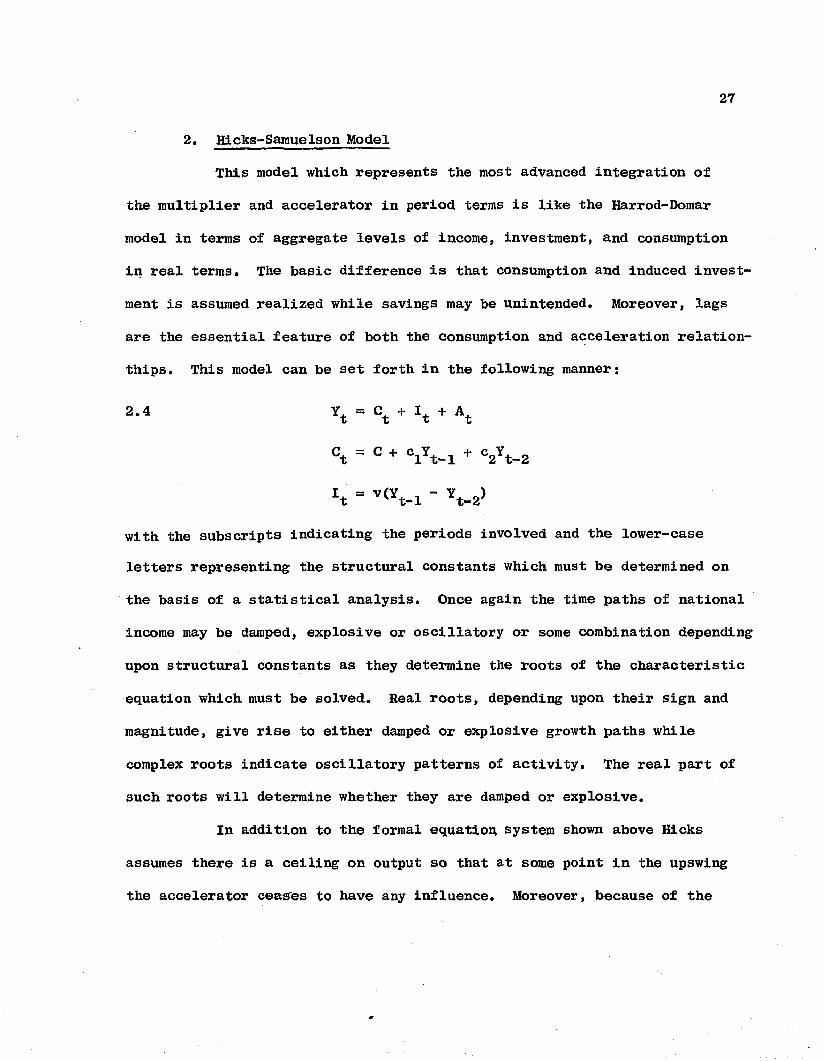

2. Hicks-Samuelson Model

This model which represents the most advanced integration of

the multiplier and accelerator in period terms is like the Harrod-Domar

model in terms of aggregate levels of income, investment, and consumption

in real terms. The basic difference is that consumption and induced invest

ment is assumed realized while savings may be unintended. Moreover, lags

are the essential feature of both the consumption and acceleration relation-

thips. This model can be set forth in the following manner;

2.4 Yt = ct + It + At

Ct = C + ClYt-l + C2Yt-2

't = V<Yt-X - Yt-2>

with the subscripts indicating the periods involved and the lower-case

letters representing the structural constants which must be determined on

the basis of a statistical analysis. Once again the time paths of national

income may be damped, explosive or oscillatory or some combination depending

upon structural constants as they determine the roots of the characteristic

equation which must be solved. Real roots, depending upon their sign and

magnitude, give rise to either damped or explosive growth paths while

complex roots indicate oscillatory patterns of activity. The real part of

such roots will determine whether they are damped or explosive.

In addition to the formal equation system shown above Hicks

assumes there is a ceiling on output so that at some point in the upswing

the accelerator ceases to have any influence. Moreover, because of the

existence of excess capital on the downswing the value of the accelerator

is assumed to be smaller during that part of the cycle. This model has

been subjected to constructive criticism by Duesenberry who argues that

disinvestment is limited by size of depreciation allowances. At the bottom

there are new initial conditions for the start of the upswing. With the

existence of excess capacity the accelerator will not be effective. In

fact, each cycle starts with the elimination of excess capacity. The

ceiling is called into question because a steady cyclic pattern can be

maintained even if the multiplier and accelerator coefficients imply

explosive oscillatory cycles. Finally, Duesenberry suggests the replace

ment of a rising trend of autonomous investment with an irreversible

consumption function which keeps the income in a depression from falling

back to the level of a previous depression.

In the search for more adequate models to describe both the growth

of the economy and its cyclical behaviour, many variations of the basic

relationships described in the above two models have been developed. The

most notable have been those due to Phillips and Goodwin, with the former

introducing lags in the continuous version while the latter makes use of a

non-linear accelerator. There has been much interest in these models not

only because of the people associated with them but also because the

question of growth has become more important. However, there is dissatis

faction with the idea that a warranted rate of growth rests upon a razor's

edge and once off will depart farther and farther from such a rate. More

over, the statistical evidence of the existence of the accelerator is not

too convincing even with the modifications introduced by Duesenberry and

others. The question that arises is how useful is the aggregated model in

explaining the pattern of growth for individual sectors of the economy. It

seems reasonably clear that the total value of output is a resultant of many

diverse movements in the individual industries, and the level of aggregation

may mask the important movements. For planning purposes the disadvantages

are even greater. Not everything is equally important in any development

program: services and agriculture may not be in the proper relationship to

the industrial sectors. For a partial answer to this type of question we

shall consider more recent developments in the area of growth models.

C. MULTISECTOR ECONOMIC GROWTH MODELS

The adaptation and further development of the concept of economic

growth to many sectors of the economy has been the subject of much recent

analysis. While it represents in one sense a logical extension of the work

done for aggregate analysis, a considerable part of the motivation has come

from a different tradition in which the pioneering work was done by Ramsey

as indicated earlier. This work, interestingly enough, was also couched in

aggregate terms with its main focus the question of how much an economy

should save. With this determined, at least conceptually, the question was

then raised as to how to distribute these resources among the different

sectors of the economy to achieve economic growth. The Calculus of Variations

has played an increasingly important role in this kind of analysis.

30

1. Ramsey Model^

In his original article Ramsey attempted to determine how much

a nation should save by constructing a capital model consisting of a single

homogeneous capital good. His conclusion was that the proper criterion is

that the

rate of savings multiplied by marginal utility of consumption should always equal bliss minus the actual rate of utility enjoyed,

where bliss is defined as the maximum obtainable rate of enjoyment or utility.

While Ramsey alluded to the use of variational analysis in his

study, it was R. G. D. Allen who obtained the main result with a straight-17forward application of the Calculus of Variations . He took a given

production function f(b,c) which represents the total income of the community

in which amounts b and c of the factors labor "b " and capital MCM are employed, dcWith b(t), c(t), representing the employment of labor, capital and theQX

rate of growth of capital respectively, consumption is then

2.5 a(t) = f(b,c) - de/dt .

If now it is assumed that utility of consumption is measurable, u = <j>(a) and analogously the disutility of labor is v = y(b). The total amount of net

utility between time periods tQ and ^ is then

f l2.6 F(b,c,c’) dt

to

10 Ramsey, F., ,rA Mathematical Theory of Savings," Economic Journal,1928.

17 Allen, R. G. D., Mathematical Analysis for Economists, Macmillan, 1938, p. 537 ff.

31

where

F(b,c,c') = <jl(a) - y(b) •

The first Euler equation necessary for a maximum is

2.7 Fb = <Fb,)t . 0

= (f)» (a) — - v» (b) = 0 — = f.V w db * v ' db b

so thaty(b)

b (f>' (a) *

The second equation is

2.8 Fc = (Fo,)t

♦ '<“>*, = <-+'(a))t

so that

These second order partial differential equations can be solved for a(t),

b(t) and c(t). While we are chiefly interested in obtaining the rate of

capital formation, we may note in passing that the marginal products of labor

and capital, f^,fc> which under conditions of competition can be considered

the wage rate and the rate of interest, are expressed in terms of meaningful

economic relationships. For example, the wage rate equals the ratio of the

marginal disutility of labor to the marginal utility of consumption and the

rate of interest is equal to the negative of the derivative of the logarithm

of the marginal utility of consumption. In other words, the latter is the

proportional rate of decrease of the marginal utility of consumption. As

Allen states, "consumption, rises over time until its marginal utility or

32

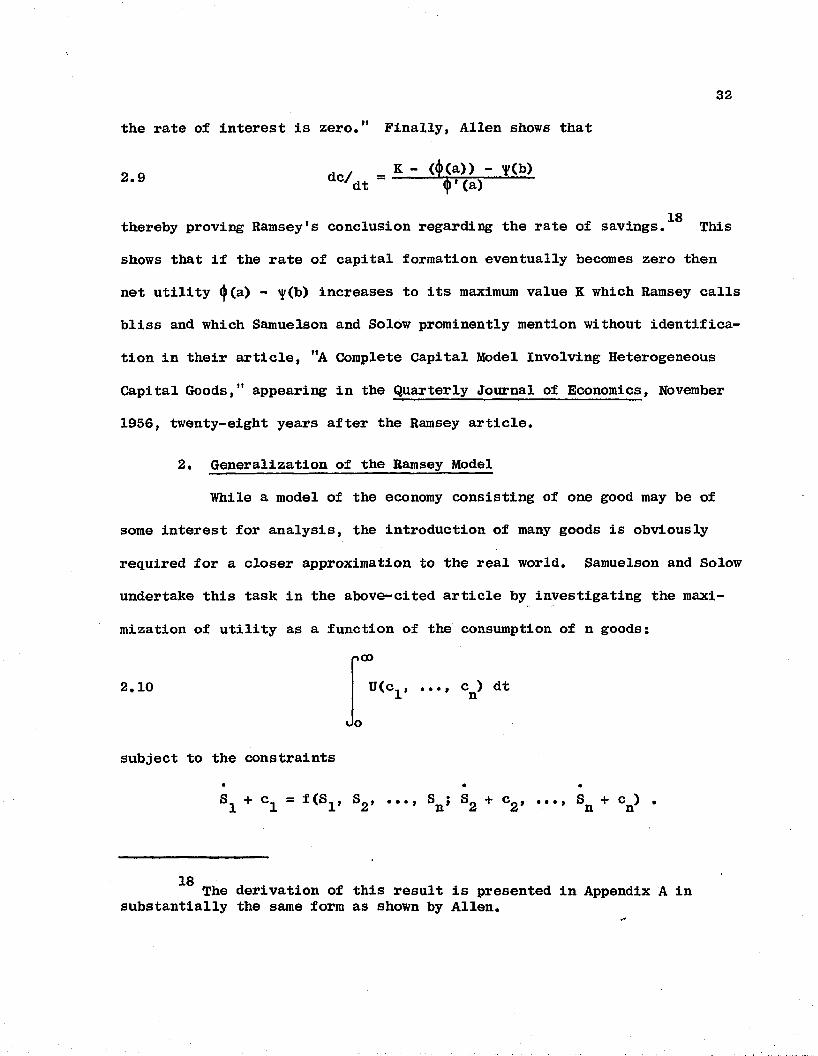

the rate of interest is zero." Finally, Allen shows that

2.9 dc/dt_ K - <<!» (a)) - y(b)"ip—

thereby proving Ramsey’s conclusion regarding the rate of savings 18 This

shows that if the rate of capital formation eventually becomes zero then

net utility <|)(a) - increases to its maximum value K which Ramsey calls

bliss and which Samuelson and Solow prominently mention without identifica

tion in their article, "A Complete Capital Model Involving Heterogeneous

Capital Goods," appearing in the Quarterly Journal of Economics, November

1956, twenty-eight years after the Ramsey article.

2. Generalization of the Ramsey Model

some interest for analysis, the introduction of many goods is obviously

required for a closer approximation to the real world. Samuelson and Solow

undertake this task in the above-cited article by investigating the maxi

mization of utility as a function of the consumption of n goods:

While a model of the economy consisting of one good may be of

2.10 U(c,, ..., c ) dt 1 n«Jo

subject to the constraints

18 The derivation of this result is presented in Appendix A in substantially the same form as shown by Allen.

33

As in the referenced article, we adopt the convention that• • • *

c ss (c-» C2 * ; S = (S^, S^j •••» Sn) } S = (S^i Sg, • • •, sn) •

In some instances the context will indicate that

s = (Sg, •••, Sn) j

where confusion is possible the explicit vector coordinates will be used.

Like Ramsey, the analysis is carried out for two different bliss

points: the one where further increment of capital would not give rise to

an increase of income or leisure; the second, where the maximum conceivable

rate of enjoyment has been reached so that there would be no use for more

income or leisure. Samuelson and Solow refer to these cases as ’’production

satiation" and "utility satiation" and carry out their analyses along these

lines. Thus, the heterogeneous capital structure of the "n" paths of

capital formation which emerge through time are those which give rise to a

maximum level of utility.

Much of the exposition is concerned with stating a number of the

results from the Calculus of Variations which are well known in the field.

The generalization of the Ramsey model to "n” capital goods and the

corresponding categories of consumption.is carried out in a straightforward

manner giving rise to paths of capital accumulation in n dimensional space.

The principal result which appears to emerge aside from the generalization

is that there is a unique end point or bliss point which is independent of

the initial point in the utility satiation case as well as in the production

satiation case. This unique end point lies on a locus of possible end points

which represent final attainable levels of capital. Which of the points on

34

the locus is the desired bliss point is determined by the transversality

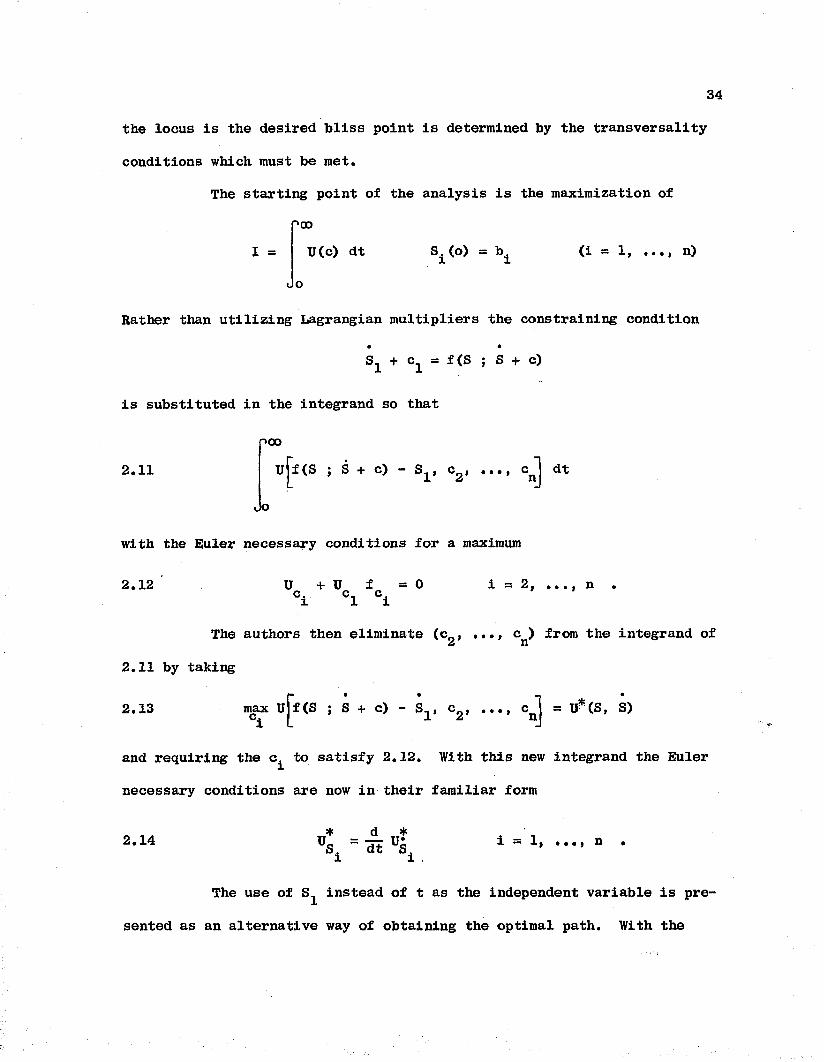

conditions which must be met.The starting point of the analysis is the maximization of

oooI = U(c) dt si<°> - \ (i = 11 ... i n)

do

Rather than utilizing Lagrangian multipliers the constraining condition

S1 + c = f(S ; S + c)

is substituted in the integrand so that

poo2.11 ujf(S j S + c) — S^, c^j •••» dt

Jo

with the Euler necessary conditions for a maximum

2.12 U + U f = 0 °i C1 °i

i — 2 j • • • y n •

The authors then eliminate (coJ . c ) from the integrand ofa n2.11 by taking

2.13 f. . — •

f(S ; S + c) - c2> ..., cnj = U*(S, S)

and requiring the c^ to satisfy 2.12. With this new integrand the Euler

necessary conditions are now in their familiar form

2.14 . * d * US± " dt \

The use of instead of t as the independent variable is pre

sented as an alternative way of obtaining the optimal path. With the

35

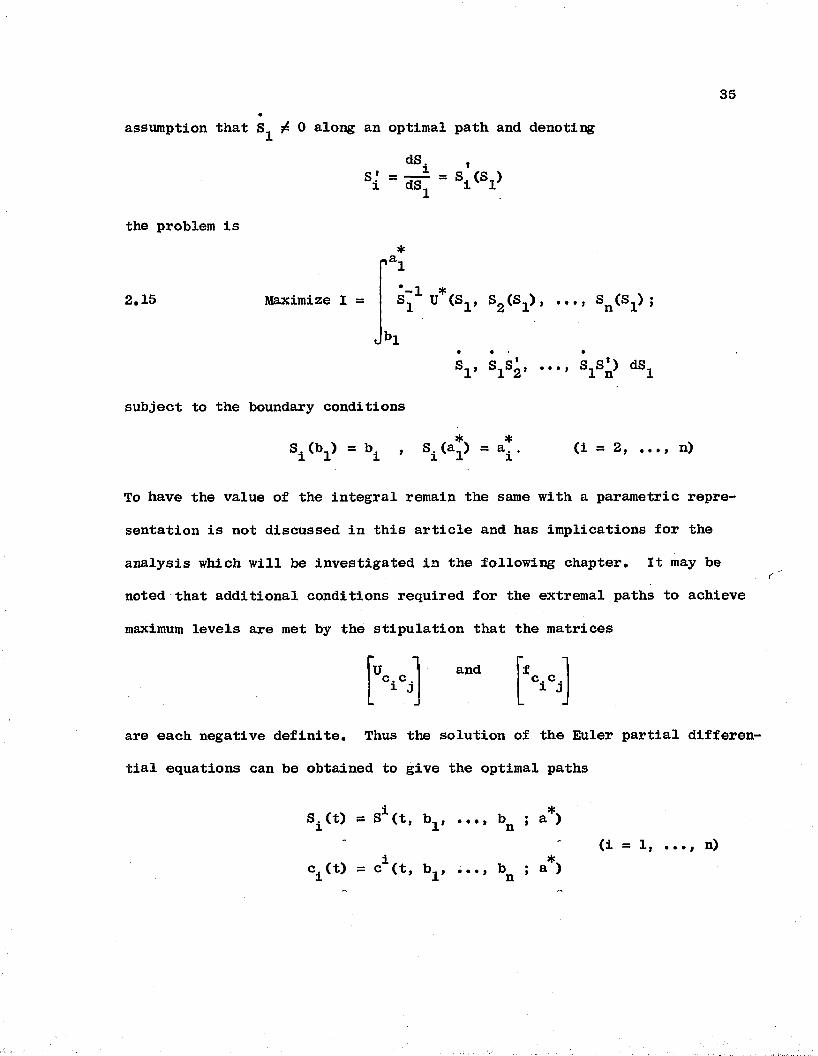

assumption that ^ 0 along an optimal path and denoting

dS

the problem is

2.15ra!

Maximize 1 = S11 U*(S1’ S2 (Sl)f V * 3!* 5

*>1• •

sl> sis2...... SlS'n> dsl

subject to the boundary conditions

Si*bl* = bi * ^i(a*) = a*. (i = 2, n)

To have the value of the integral remain the same with a parametric repre

sentation is not discussed in this article and has implications for the

analysis which will be investigated in the following chapter. It may bec

noted that additional conditions required for the extremal paths to achieve

maximum levels are met by the stipulation that the matrices

1Uc. c . i 3and c. c . i J

are each negative definite. Thus the solution of the Euler partial differen

tial equations can be obtained to give the optimal paths

S^t) = Si(t, b ^ ..., bn ; a*)

i *^(t) = c (t, bj, ..., b ; a )(i = 1, ..., n)

36

Some discussion of the model is devoted to (1) setting forth in

a purely mathematical manner some of the Hamiltonian equations which can

be obtained by working in a 2n dimensional space in which first order

partial differential equations are obtained, although these equations are

not used in the analysis, and (2) a very brief exposition of the famous_ rHamilton-Jacobi partial differential equation which can be used to get the

optimal paths of the problem. We shall go into these matters in some detail

in the following two chapters ascribing economic content to the results.

3. Efficient Paths of Capital Growth

The most recent contribution to the development of a Capital

Model using the Calculus of Variations as the principal means of analysis

is Professor Samuelson's article, "Efficient Paths of Capital Accumulation

in Terms of the Calculus of Variations,” which appeared as a chapter in

Mathematical Methods in the Social Sciences referred to earlier. It builds

on the earlier generalized Ramsey model and is at the same time a continuous

version of the discrete time analysis of Chapter 12, "Efficient Programs of

Capital Accumulation," of Linear Programming and Economic Analysis published

in 1958 by Dorfman, Samuelson and Solow. Rather than maximizing the utility

as in the generalized Ramsey case, the direct optimization of capital stocks

is undertaken subject, however, to the production function relationship as

in the earlier version.^

19 The authors point out that this formulation can be derived from the utility model previously described. See equations in Samuelson, P., and Solow, R., "A Complete Capital Model Involving Heterogeneous Capital Goods," Quarterly Journal of Economics, 70, (1956) p. 541.

37

Formally, the problem is to maximize

:1rt’t-2.16 S,(t) dt

subject to

S^t) = f ^ C t ) , Sn (t) ; S2(t) + cg(t), Sn (t) + cn (t)j - ^(t)

which is considered to be a first degree homogeneous production function.20This is then represented as

pt.2.17

m •Sg, • •«> Sn j Slf ..., Sn j X) dt

where

<|> = Sx(t) + X(t) p c s 1> •••> j Sg + c

with the Euler equations

2.18 — ()>• = d)dt V , YS. (i — 1, ..., n)

being necessary conditions for a maximum.

The three principal results obtained by: Samuelson are

(a) the equivalence of flow and stock prices,

(b) the conditions required to maintain consumption levels,

(c) the efficiency of maximum balanced growth,

all of which are continuous versions of results achieved in the referenced

The variable "t" has been dropped merely for convenience.

38

work on Linear Programming and Economic Analysis. The first of the results

is obtained by the application of the transversal!ty conditions but in a

manner which is more restrictive than will be used later on and consequently

without the additional results which we shall derive in the next chapter.

Result (b) is obtained by simple straightforward specialization of the Euler

equations given in 2.18 above by setting all net additions to capital,•S. = 0 .l

The third principal result shows that the Von Neumann maximum

balanced growth rate exists and is efficient. To demonstrate the efficiency

of the maximum balanced growth rate set•

Sic. = 0 for all i, —— = msi

by the definition of balanced growth and substitute into the constraint of

2.16 above, giving

2.19 m = f(S1, ..., ; m S^, ..., m S^)

Since V S. - S, < 0, m can be obtained as a function of all the capitalL s. j 1stocks

2.20 m — m(Sn, ..., S )1 nand a maximum rate will satisfy

2.21 -22- = 0 . (i = 1, ..., n)

Using 2.19, 2.20 and 2a21 it can be shown that

2.22 f + f f = 0 (i = 2, ..., n)i i 1

and that this satisfies the efficiency conditions represented by the Euler equations.

39

4. Economic Growth in Activity Analysis21Several years after the Ramsey article Von Neumann developed

a discrete time period model of an expanding economy in which the emphasis

was on uniform expansion. By this is meant that the output of each sector

of the economy would increase at the same constant rate and it was shown

that for this multisectored model such a rate would be equal to the rate of

interest. It was necessary to assume that (1) basic factors such as labor

and capital are available in unlimited amounts, (2) each sector has an input

from every other sector, and (3) that all the production or proceeds from

production above that required for inputs into the production activities in

the following period are invested. This means that consumption is one of

the sectors in the model. It has been shown that this basic model can be

formulated in terms of a Linear Programming model or more accurately as a

series of Linear Programmes. More recently there have been attempts to

further develop the concept of balanced growth of a multisectored model in

the same sense used by Von Neumann.

During the past several years increased interest has been given

to the analysis of capital development programs along similar lines. This

has been done by using a Linear Programming formulation in which the

Leontief input-output system has been embedded. Specifically, the model

is designed to maximize the levels of capital accumulation over a number of

time periods in one or a positive linear combination of sectors subject to

21 Von Neumann, J., "Uber ein okonomisches Gleichungssystem und line Verallgemeinerung des Brouwerschen Fixpunktsatzes," Ergebnisse eines mathematischen Kolloquiums, No. 8 (1938), pp. 73-83, translated as, "A Model of General Economic Equilibrium,1* Review of Economic Studies, Vol. 13, No. 33 (1945-46) pp. 1-9.

40

capacity restraints. The variables for this formulation represent levels of

capital in the various sectors by time period.

It can be seen that this approach represents a significant

departure from what has been described above in connection with aggregate

analysis. First of all it is non-market-oriented by which is meant that the

interplay of prices, consumption, and the levels of income do not have an

impact on investment activities. Levels of investment are determined on the

basis of technological considerations involving the individual sector input-

output relations and the capital-output ratios. Consumption of sector output

by consumers by time periods generally is stipulated.

The solution of such a Linear Programming model generates levels

of capital accumulation in quantity terms which maximize one sector or some

positive combination of sectors. The question naturally arises as to the role

of prices in such a formulation. It is well known that there is a dual

solution to every regular or primal solution to a Linear Programming model,

the variables of which are prices of the resources employed in the model.

Such prices are variously described as shadow prices or accounting prices

associated with the resources utilized. The prices of resources which are

not fully utilized are zero, the prices of fully utilized resources being

positive. A set of such prices may not be unique. They can be interpreted

as rates of substitution and in competitive markets may be thought of as

market prices. In non-competitive situations they serve as guides to effi

cient allocation of resources.

This kind of model represents a discrete time approach to the

continuous formulation described in 3. above. It has the advantage of having

available efficient algorithms for obtaining solutions of electronic

computers. It has the disadvantage of being forced into a mold with linear

relations or at best being able to handle a small class of non-linear

relations.

CHAPTER III

EXTENSIONS OF THE CURRENT CONCEPT OF A COMPLETE CAPITAL MODEL

A. PRELIMINARY DISCUSSION

As a general method of theoretical analysis there is usually much

to be gained by undertaking an abstract formulation of the subject matter

and then specializing the relationships to achieve and reveal particularly

interesting results. This is especially true for the analysis of a capital

model by means of the Calculus of Variations for it opens up new method

ological approaches to this type of economic analysis as well as revealing

analytical results. The analysis is best carried out at a level of mathe

matical abstraction necessary to achieve the desired results.

We are concerned with a disaggregated analysis of individual sectors

of the economy with respect to investment, on a net basis, over a specific

period of time. Capital accumulation in this sense refers to the growth of

the stocks of the individual sectors. By making the units of time short

enough, both fixed and circulating capital can be covered provided that

joint products are permitted. Thus we may include stocks of commodities

covering various types of capital formation from inventories to plant and

equipment. We are talking about industrial sectors of the economy generally,

although agricultural and trade sectors could be included. In fact we

include households as a sector by stipulating the levels of consumption

throughout the time period involved. It is clear therefore that we are

talking about an idealized model which has as a goal the theoretical

achievement of the maximum amount of capital accumulation by a certain

period of time in the future.

In order to make the mathematico-economic development easier to

follow it will be helpful to state the assumptions upon which the ensuing

analysis is based. Much of the discussion in Chapter I was concerned with

the kind of abstract economic analysis so frequently employed in economic

theory. This was done to show that essentially the same kind of concepts

are used in the Capital Model with which we are concerned. The transforma

tion function in which alternative levels of stocks of capital can be

obtained is presented in the form of a restraint on the growth of one

sector whose capital is maximized. This use of a transformation locus

has been frequently employed in the theoretical analysis of consumer

behavior in which utilities are associated with particular consumption

goods and the production function operates as a constraint limiting the

availabilities of such goods.

We also assume that the rate of production of capital goods in one

sector can be represented by a production function which is homogeneous of

the first degree and independent of time although this latter restriction

is partially removed later on. The independent variables are the levels

of capital and their rates of change. By having the production function

"conservative" or independent of time the production possibilities are

assumed not to change over the period considered. The first degree

homogeneity assumption means that there are constant returns to scale

which is frequently employed in economic analysis. In addition to the

"conservative" case we shall consider production functions which are time

dependent so that changes in production capabilities can be covered. For

this latter case it is assumed that the production function is again first

44

order homogeneous although the production function depends upon time in

addition to the levels of capital and their rates of change. In both the

time independent and dependent cases the substitution of capital is taken

to be smooth and continuous.

The representation of some economic activities by sufficiently smooth

and continuous curves is frequently made as a first order approximation in

theoretical economic analysis. In making such assumptions we shall satisfy

the mathematical requirements of the Calculus of Variations. This is

particularly pertinent to the paths of capital accumulation over the period

of time considered and to the rates of change of capital or investment,

which we shall obtain. The levels of capital at the end of the period are

stipulated except for the sector in which capital is maximized. The same

continuity assumptions hold true for prices of capital goods which are

introduced into the model. These prices are taken to be the marginal rates

of substitution embodied in the transformation function and may or may not

be in line with actual prices prevailing in the economy. However, the

concept of technologically determined prices has played an important role in

economic analysis.

Finally, the assumption is made that consumption is specified over

the time period as was done in the Samuelson model. This is not to say

that it is constant but rather that it may change but in a stipulated way.

We shall derive the following results, all of which are new for the

current concepts of a disaggregated capital model. Moreover, the power

and usefulness in economic analysis of the Calculus of Variations, and

particularly the Hamilton-Jacobi formulation will be evident. Indeed

45

it is diffucult to see how these results could be obtained in any other

way.

1. Prices are incorporated into the model and are shown to

arise naturally from the model by using the Calculus of

Variations as the principal tool of analysis. The special

nature of these prices is described.2. An overall constraint inherent in a Capital Model and its

economic significance are described and further developed.

3. Demonstration of equivalence of maximization of capital

accumulation with and without prices explicitly in the

model is undertaken.

4. The interrelationships of transversality, the transformation

locus, and the paths of maximum capital accumulation are

made more explicit and in some measure simplified.

Our task is to determine the implications of obtaining efficient

paths of capital accumulation for all sectors under consideration when the

objective is to maximize the investment in one particular sector. Such a

maximization is subject to the constraint inherent in the transformation

loci which appear over the time period concerned. To begin with, the

maximization starts at a particular period in time and continues to a

terminal point in time. During each point in time the transformation locus

represents the technical possibilities for having more or less of invest

ment in the sector to be maximized in relation to the other sectors. This

is exactly what a transformation locus represents in other areas of economic

analysis described previously.

46To maximize the investment in one sector, say the first, we shall

make a maximum

"i" sector. The levels of capital for the other sector (t) are affected

in the maximization through the relationship in the production function

which is assumed by Samuelson to be homogeneous of the first degree. It is

obvious that we have assumed away many practical problems.

To begin with there is the question of the availability of data to

develop a production function and the question of its being homogeneous of

the first degree. Then, there are questions of the definition of a sector

which is difficult, the proper units of measurements, and the level of

aggregation. Finally, we must be able to determine the level of capital

S^(t°) at the starting point in time t°.

^ -J-11

3.1

in which c (-t) are specified levels of consumption for the output of each

3.2 • • • > S^(t) j

In the previous discussion

3.3 I • • • f Sn(t) j Sg(t) + c2(t), ...,

47

so that we wish to maximize

r't1

3.4 (j)(S1(t), S2(2), Sn (t) ; S2(t>, Sn (t) ; \(t)) dt .ot

The solution of the Euler differential equations which are necessary condi

tions for a maximum

3-5 = 0 = 1 ”)i 8s!

are

3.6 S;L(t) = S (Sr • • •, Sn ; Sg, • «•, ; c ; t — t )

foro 1t < t < t

Samuelson has shown that \ is related to a discounting function which we

shall have occasion to make use of below.^

There are several important things to be noted about the capital

accumulation time paths. First, they are idealized growth curves for the

various sectors of the economy and can be realized only if all the condi

tions of the model are met. This would require centralized direction over

j|( For one way to obtain the solution involving the use of canonical transformations and the Hamilton-Jaeobi partial differential equation, see Chapter IV.

1 Samuelson, P., "Efficient Paths of Capital Accumulation in Terms of the Calculus of Variations," Mathematical Methods in the Social Sciences, 1959; edited by Arrow, K., Karlin, S., and Suppes, P., Stanford University Press, Stanford, California, 1960, p. 79, equation (5').

48

the allocation of resources and realism in the economic relationships which

the equations describe. Realistically, they are goals or benchmarks against

which to measure actual growth in an investment plan. Second, while it is

only investment in the first sector which is maximized, all the investment

paths are efficient. However, for the sectors other than the first, the

efficiency of their investment growth through time is in the sense that such2paths are consistent with the first sector’s investment to be maximized.

This can be seen in view of the fact that all of them satisfy the Euler

differential equations.

A further word is required about the production function. We shall

not insist that the production be homogeneous of the first degree but rather

the parametrization of the model t = t(T) will convert the production

relationship into one which does meet this requirement. This would of course

make the time, "t", an explicit independent variable and its introduction

could inject the idea of technological growth into the production process.

This will also facilitate the development of price relationships within the

model.

At times we shall keep the parameter in general terms although it

could be other magnitudes of economic interest. For example, another

variable representing the accumulation of capital in a different sector might

be of interest or some positive linear combination of the other variables

where r^ is the own rate of interest and p^ the price ratio in terms of thefirst good as numeraire. See the paragraph following equation (5 1) in the above footnote.

2 The fundamental relationship which must hold is r. = r^ + P± dt

might be used. In particular the latter could be the square root of the

sum of squares of the other variables which would from a mathematical point

of view make the variable of integration an arc length, while from an

economic standpoint the levels of capital accumulation would be in terms of

such a metric. Of course, we retain the flexibility of keeping the variables

as functions of time. Finally, regardless of the parametrization relative

prices remain the same which, of course, is what is required, for we do not

wish the basic structural relationships to be affected by the change in the

mathematical representation.

In order to make the mathematical development easier to follow, the