6.1 Key considerations - Royal Commission

23

{ STYLEREF "Title" } Westpac Group confidential 1 May 2013 Business Credit Manual Page { SEQ Chapter\c \* Arabic \* MERGEFORMAT }- 1 6.1 Key considerations Table of contents Policy .....................................................{ SEQ Chapter _Toc462651371 \* ARABIC }-101 Guidelines .............................................{ SEQ Chapter _Toc462651372 \* ARABIC }-201 Additional Information .........................{ SEQ Chapter _Toc462651373 \* ARABIC }-301 WBC.400.043.6461

Transcript of 6.1 Key considerations - Royal Commission

{ STYLEREF "Title" }

Westpac Group confidential1 May 2013 Business Credit Manual Page { SEQ Chapter\c \*

Arabic \* MERGEFORMAT }-1

6.1 Key considerations

Table of contents

Policy.....................................................{ SEQ Chapter _Toc462651371 \* ARABIC }-101

Guidelines .............................................{ SEQ Chapter _Toc462651372 \* ARABIC }-201

Additional Information .........................{ SEQ Chapter _Toc462651373 \* ARABIC }-301

WBC.400.043.6461

WBC.400.043.6462

{ STYLEREF "Title" }

Westpac Group confidential16 November 2012 Business Credit Manual Page { SEQ Chapter\c \*

Arabic \* MERGEFORMAT }-101

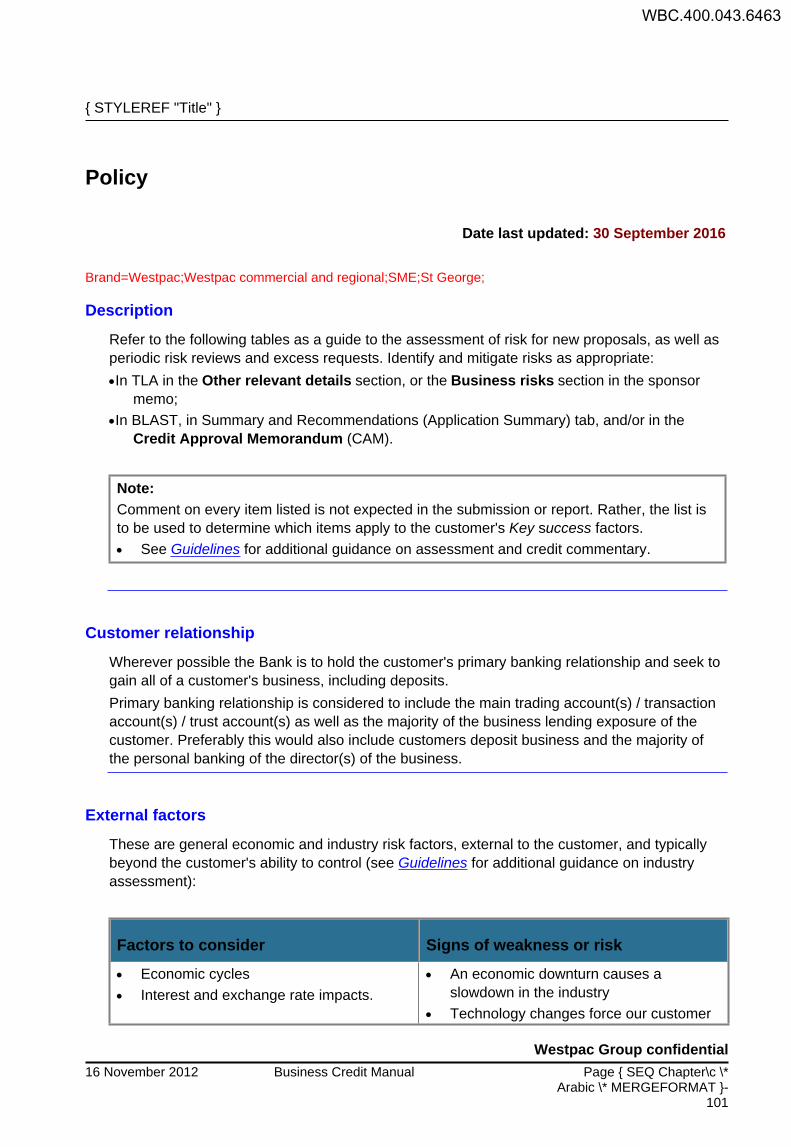

Policy

Date last updated: 30 September 2016

Brand=Westpac;Westpac commercial and regional;SME;St George;

Description

Refer to the following tables as a guide to the assessment of risk for new proposals, as well as periodic risk reviews and excess requests. Identify and mitigate risks as appropriate:In TLA in the Other relevant details section, or the Business risks section in the sponsor

memo;In BLAST, in Summary and Recommendations (Application Summary) tab, and/or in the

Credit Approval Memorandum (CAM).

Note: Comment on every item listed is not expected in the submission or report. Rather, the list is to be used to determine which items apply to the customer's Key success factors. See Guidelines for additional guidance on assessment and credit commentary.

Customer relationship

Wherever possible the Bank is to hold the customer's primary banking relationship and seek to gain all of a customer's business, including deposits.Primary banking relationship is considered to include the main trading account(s) / transaction account(s) / trust account(s) as well as the majority of the business lending exposure of the customer. Preferably this would also include customers deposit business and the majority of the personal banking of the director(s) of the business.

External factors

These are general economic and industry risk factors, external to the customer, and typically beyond the customer's ability to control (see Guidelines for additional guidance on industry assessment):

Factors to consider Signs of weakness or risk Economic cycles Interest and exchange rate impacts.

An economic downturn causes a slowdown in the industry

Technology changes force our customer

WBC.400.043.6463

{styleref "Title" }

Westpac Group confidentialPage { SEQ Chapter\c \* Arabic \* MERGEFORMAT }-102

Business Credit Manual 16 November 2012

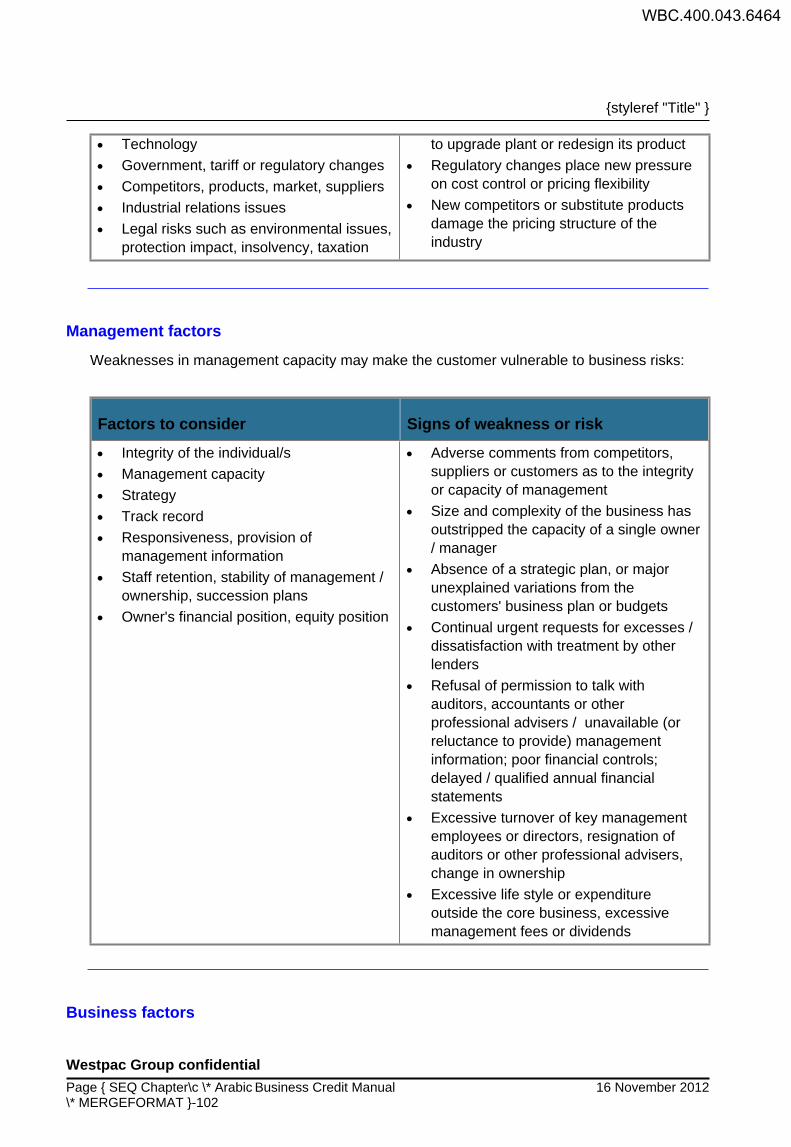

Technology Government, tariff or regulatory changes Competitors, products, market, suppliers Industrial relations issues Legal risks such as environmental issues,

protection impact, insolvency, taxation

to upgrade plant or redesign its product Regulatory changes place new pressure

on cost control or pricing flexibility New competitors or substitute products

damage the pricing structure of the industry

Management factors

Weaknesses in management capacity may make the customer vulnerable to business risks:

Factors to consider Signs of weakness or risk Integrity of the individual/s Management capacity Strategy Track record Responsiveness, provision of

management information Staff retention, stability of management /

ownership, succession plans Owner's financial position, equity position

Adverse comments from competitors, suppliers or customers as to the integrity or capacity of management

Size and complexity of the business has outstripped the capacity of a single owner / manager

Absence of a strategic plan, or major unexplained variations from the customers' business plan or budgets

Continual urgent requests for excesses / dissatisfaction with treatment by other lenders

Refusal of permission to talk with auditors, accountants or other professional advisers / unavailable (or reluctance to provide) management information; poor financial controls; delayed / qualified annual financial statements

Excessive turnover of key management employees or directors, resignation of auditors or other professional advisers, change in ownership

Excessive life style or expenditure outside the core business, excessive management fees or dividends

Business factors

WBC.400.043.6464

{ STYLEREF "Title" }

Westpac Group confidential16 November 2012 Business Credit Manual Page { SEQ Chapter\c \*

Arabic \* MERGEFORMAT }-103

Weaknesses in business factors can ultimately threaten the viability of the business if faced with adversity.

Factors to consider Signs of weakness or risk Products Pricing strategies Contracts Premises, equipment Leases Contingency Plans

Over-diversification at the expense of concentration on a core product

Inability to respond to customer and competitive demands and external factors.

Reliance on one or few key customers or suppliers

Idle, surplus or ageing equipment and premises

Actual or planned business growth above and beyond historical trends or industry averages

Strengths and susceptibilities in its business operating cycle;

Business strategy - will it lessen or increase the risks identified under Industry Analysis?

Infornation Technology Security

Is there appropriate information technology (IT) risk management in place, including consideration of risks of outsourcing data and cybercrime if applicable?

Agricultural considerations

Key considerations for agricultural deals can be found in the Sector policy - Agriculture section.

Financial factors

These are financial measures which may highlight weak management or adverse business factors:

Factors to consider Signs of weakness or risk Credit Terms Cost Structure

Our customer relies on longer supplier credit terms

Suppliers tighten trade credit terms

WBC.400.043.6465

{styleref "Title" }

Westpac Group confidentialPage { SEQ Chapter\c \* Arabic \* MERGEFORMAT }-104

Business Credit Manual 16 November 2012

High fixed cost structure (including excessive fixed asset capacity and / or vertical integration)

Efficiency ratios Unexplained or excessive increase in debtors days

Unexplained or excessive increase in inventory days

Sales volumes Profit margins Liquidity ratios

Reduction in sales volumes or revenues Reduced profit margins or a reported

trading loss Working capital and liquidity Difficulty in settling tax liability payments,

or undue delay in remitting employee or company tax withholding

Ability to generate a sustained cashflow to repay debt

Requests to postpone principal repayments

Shortening debt maturities and continual hard core excesses

Run of account, account conduct Cash balances down; run of account confirms less liquidity

Casual overdrafts and / or excesses over facility limits

Structural financing

Structural finance is finance for business expansion (including the purchase of an additional 'same business') that cannot be repaid from current cash available for debt service (CAFDS) or be justified by current performance levels shown in the customer's balance sheet. It includes diversification into new business areas or geographies or stand-alone projects such as property development, or where adverse trends are evident that might indicate historical income levels might not be maintained.

WBC.400.043.6466

{ STYLEREF "Title" }

Westpac Group confidential16 November 2012 Business Credit Manual Page { SEQ Chapter\c \*

Arabic \* MERGEFORMAT }-201

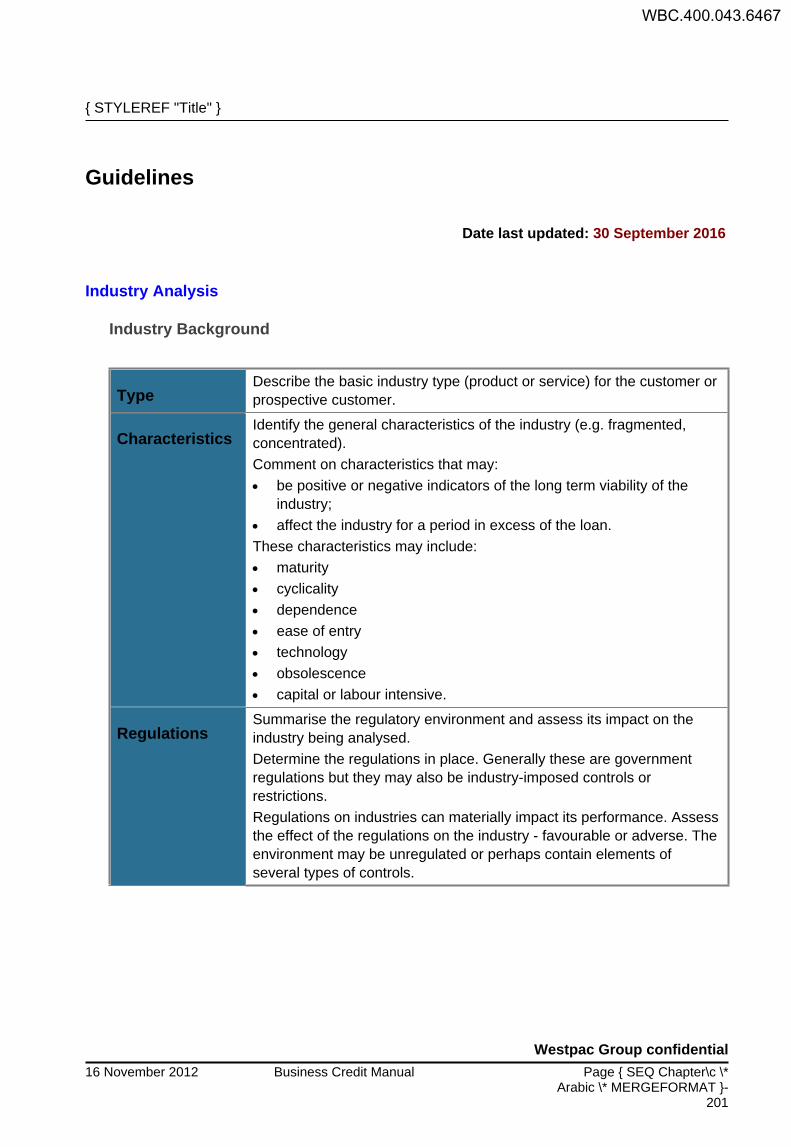

Guidelines

Date last updated: 30 September 2016

Industry Analysis

Industry Background

TypeDescribe the basic industry type (product or service) for the customer or prospective customer.

CharacteristicsIdentify the general characteristics of the industry (e.g. fragmented, concentrated).Comment on characteristics that may: be positive or negative indicators of the long term viability of the

industry; affect the industry for a period in excess of the loan.These characteristics may include: maturity cyclicality dependence ease of entry technology obsolescence capital or labour intensive.

RegulationsSummarise the regulatory environment and assess its impact on the industry being analysed.Determine the regulations in place. Generally these are government regulations but they may also be industry-imposed controls or restrictions.Regulations on industries can materially impact its performance. Assess the effect of the regulations on the industry - favourable or adverse. The environment may be unregulated or perhaps contain elements of several types of controls.

WBC.400.043.6467

{styleref "Title" }

Westpac Group confidentialPage { SEQ Chapter\c \* Arabic \* MERGEFORMAT }-202

Business Credit Manual 16 November 2012

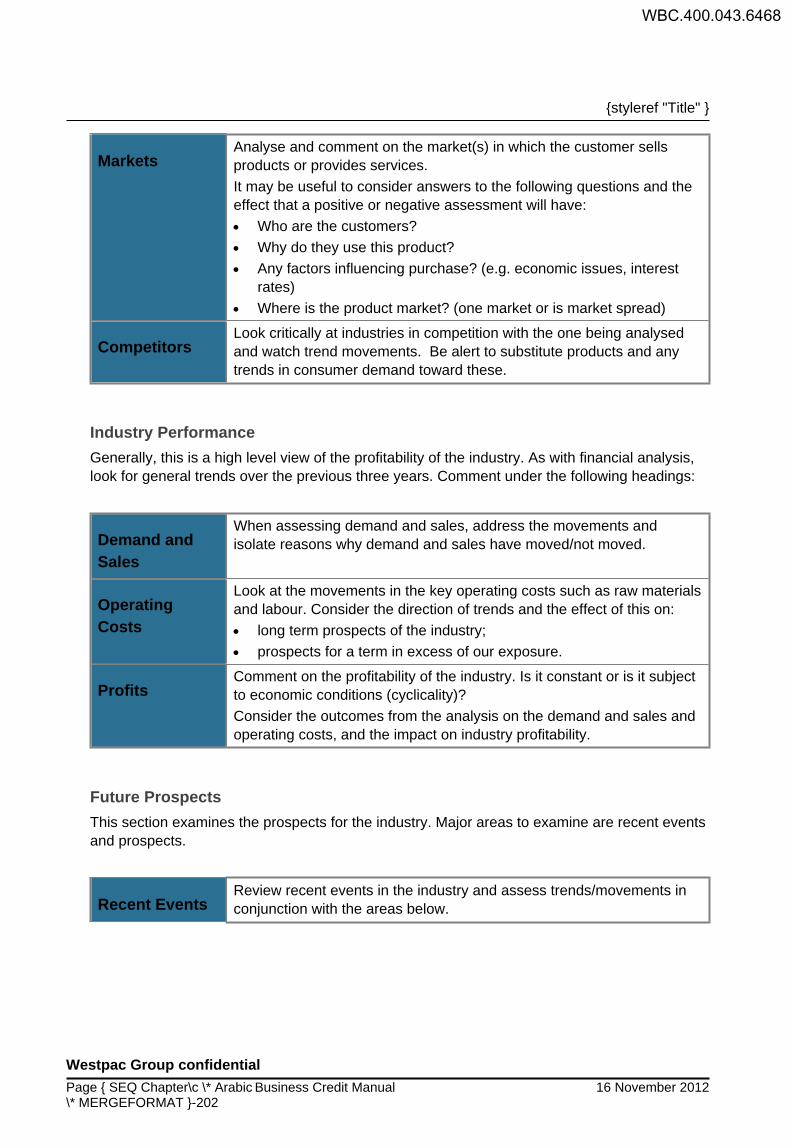

MarketsAnalyse and comment on the market(s) in which the customer sells products or provides services.It may be useful to consider answers to the following questions and the effect that a positive or negative assessment will have: Who are the customers? Why do they use this product? Any factors influencing purchase? (e.g. economic issues, interest

rates) Where is the product market? (one market or is market spread)

CompetitorsLook critically at industries in competition with the one being analysed and watch trend movements. Be alert to substitute products and any trends in consumer demand toward these.

Industry PerformanceGenerally, this is a high level view of the profitability of the industry. As with financial analysis, look for general trends over the previous three years. Comment under the following headings:

Demand and Sales

When assessing demand and sales, address the movements and isolate reasons why demand and sales have moved/not moved.

Operating Costs

Look at the movements in the key operating costs such as raw materials and labour. Consider the direction of trends and the effect of this on: long term prospects of the industry; prospects for a term in excess of our exposure.

ProfitsComment on the profitability of the industry. Is it constant or is it subject to economic conditions (cyclicality)?Consider the outcomes from the analysis on the demand and sales and operating costs, and the impact on industry profitability.

Future Prospects This section examines the prospects for the industry. Major areas to examine are recent events and prospects.

Recent EventsReview recent events in the industry and assess trends/movements in conjunction with the areas below.

WBC.400.043.6468

{ STYLEREF "Title" }

Westpac Group confidential16 November 2012 Business Credit Manual Page { SEQ Chapter\c \*

Arabic \* MERGEFORMAT }-203

Prospects Demand and sales - comment on the forecast direction of demand

and sales and the underlying reasons/assumptions. Operating cycle costs - the historical performance of the industry

has been analysed from the industry performance section above. Assess the future direction of operating costs in comparison to business cycles. Comment on the expected direction and why this trend is expected.

Profits - comment on the forecasted future probability for the industry derived from comments made above.

Business Analysis

The following are additional guidance notes on credit assessment and commentary.

Customer BackgroundAs part of the preliminary screening of a loan request, we must learn about the borrower's business, and determine:

General Characteristics

Provide general characteristics of the customer/proposed customer.Issues that would normally be expected to be commented upon include: size (turnover, profit, market share etc.); history (when it was formed); product; maturity cycle; Diversification of products and services offered. Legal/ownership structure. Organisational structure. Geographic dispersion and ownership of assets, licences,

franchises, etc. Product distribution and receivables collection channels.Consider this information in terms of the results of the industry analysis previously undertaken.

WBC.400.043.6469

{styleref "Title" }

Westpac Group confidentialPage { SEQ Chapter\c \* Arabic \* MERGEFORMAT }-204

Business Credit Manual 16 November 2012

Goals and Strategies

Strategies are the plans by which the customer proposes to meet its goals or objectives.Analyse the goals and strategies of the customer in terms of a variable that is able to be measured, such as: market share growth return on equity profitability.Examine and discuss the implications of the strategy for the company, and how it fits with the industry trends and expected direction.

Products/CompetitionThe management decisions related to the Product/Market mix are vital elements of the likely success of a company.

Product / Market Match

Assessment of Product/Market match falls into two primary categories.The first is analysis of the importance of the product/service to customers. Is the product an essential or luxury item?The second factor is the differentiation of products. Is there anything that makes the customer's product stand out from others in the range? (E.g. price, terms, packaging etc.).Consider these factors and check compatibility with Goals and Objectives and the company and the view of the industry.

OperationsThe analysis of Operations focuses on three primary areas. Assess and comment on any risks involved in the areas as it relates to the safety of our lending. Examine the following areas of Operations and ensure consideration is given to the outcomes of the Industry Analysis.

Supply Analysis

Assess the supply of raw materials, labour, personnel, product etc. to suit the industry type (product or service) and ascertain the source and depth of the resource along with the cost, availability and continuity of supply

Production Analysis

Concentrate the analysis of this section on the products or services capable of being delivered in a timely manner at a competitive price.There are three main areas to be addressed in Production Analysis. They are: consistency (production/performance); vulnerability (technology, natural disasters etc.); labour relations.

WBC.400.043.6470

{ STYLEREF "Title" }

Westpac Group confidential16 November 2012 Business Credit Manual Page { SEQ Chapter\c \*

Arabic \* MERGEFORMAT }-205

Distribution Analysis

Distribution Analysis is the sequential step following production. It involves all steps from making the product or service available to consumers up to delivery following purchase.The primary areas to analyse are: the networks in place to reach target markets; quality control over the product image throughout the sales cycle; flexibility to respond quickly to alternative distribution methods and

systems; vulnerability to changes in overseas risks.

Sales AnalysisThe assessment of sales is broken down into four primary areas. Focus Sales Analysis comments on the following areas and relate them to the Industry Analysis:

CompetitionDiscuss competition and the expected impact on our customer's products. Also, consider substitute products.

Bargaining Power

Ascertain if the customer is able to exert any leverage over sale prices and demand, and comment accordingly.

DemandAssess demand for the customer's products and comment if they are able to exert any influence.

ConcentrationAnalyse sales and look for any concentrations. Be wary when concentration of products or services exceeds 10%. Identify concentrations and any possible impact on the safety of our lending.

Management EvaluationManagement is a key element to the safety of our lending. Good management with sound techniques will be better placed to weather adversity than others. Comment on management under the following headings:

ExperienceAssess and comment on the management experience in the industry.

QualificationsAssess technical expertise and other skills required.

TrainingAssess adequacy given the rate and type of change that has occurred, plus the type of challenges facing the business and the industry.

Historical Performance

Consider and comment on the previous record of meeting goals and objectives of the management. This is always a good indicator of performance capability.

WBC.400.043.6471

{styleref "Title" }

Westpac Group confidentialPage { SEQ Chapter\c \* Arabic \* MERGEFORMAT }-206

Business Credit Manual 16 November 2012

IntegrityConsider the integrity of management as this is a critical safety indicator—a demonstration of their willingness to repay advances.

DepthLook at the depth of the management (capacities, numbers, succession planning) and identify any possible risk areas.

BreadthComment on the breadth of management. Pay particular attention to the Customer's Organisation structure and look for identification and clear separation of functions.

Board of Directors

Check and comment on the composition, strength and independence of the Board of Directors. Does an Audit Committee exist?

WBC.400.043.6472

Business Credit Manual{ STYLEREF "Heading 1" \* MERGEFORMAT }

16 November 2012 { StyleRef "Heading 1" \* MERGEFORMAT }

Additional Information

Date last updated: 30 September 2016

Industry profiles (IBIS World) intranet page

Credit Structuring

Clear recognition and understanding of the various components of a credit are pre-requisites to the optimum structuring of the transaction. This leads in turn to:Increased efficiency and productivity of the credit process.A loan which becomes to some degree self-monitoring, with repayments aligned to anticipated

events.A loan facility tailored more closely to the customer's needs and the Bank's portfolio and profit

objectives.Credit Structuring fundamentally depends on the identification of the proposed borrower vis-a-vis its legal capacity and relationships and the extent to which its credit worthiness may involve the support of any surrounding group of companies or other entities.The next fundamentals to understand are the reason for borrowing and the purpose to which the requested credit is to be applied. This can be a fairly simple task in Consumer credit, whereas normal operations of a Business credit can involve:Increase in assets:

current: receivables and inventory;fixed: plant and equipment.

Decrease in other liabilities:payment of creditors, expenses or accruals;refinance of existing debt.

Distribution of dividends/profits.The critical element in determining the type of credit product to be provided, however, is the source of repayment. We use Credit Analysis to determine the borrower's sources and capacities of repayment, and align these to the appropriate type of credit product(s) from the Bank.Therefore Credit Structuring moves in parallel with Credit Analysis in determining how the credit transaction is to be best shaped to meet the Bank's objectives and the needs of the borrower.

Business CreditThese borrowers primarily use credit for purposes which generate business income and thus there is generally a close relationship between borrowing purpose and repayment source (although the latter may also include sale of non-operating assets and infusion of further capital).Credit analysis focuses principally on the capacity to repay from business operations, be they conversion of short-term assets or cashflow retentions in the medium-term, and will use both

WBC.400.043.6473

{styleref "Title" }

Westpac Group confidentialPage { SEQ Chapter\c \* Arabic \* MERGEFORMAT }-302

Business Credit Manual 16 November 2012

historical financial performance and forward projections to assess both repayment capacity and satisfactory financial stability. Borrowers are likely to use any or all of the borrowing types listed in Credit Structuring section above and thus facility mechanisms will be aligned to meet their particular purposes and repayment modes. Security should include charges over the assets being financed and supporting cash flows, but will also require appropriate linkage between borrowers and other entities supporting the credit supported by a GSA and/or SSA, company legislation again becoming a determinant. Loan conditioning to monitor and control compliance with repayment and safety expectations, and periodic relationship visits are necessary.

Institutional Credit This area includes banks, finance companies, securities firms, governmental and semi-governmental entities, and other types of financial institutions. The facility types and the purposes to which they are put are quite separate and distinct from those in other borrower types.

Specialised Credit Other borrowers, because of the intrinsic risk of their industry or the nature or structure of their requirements are also segregated for specialised handling. They are usually larger corporations or entities handled on a relationship basis by appropriately experienced officers, although similar general channelling of credit assessment and decision for some risk-prone industries (such as agriculture, mining, property developers) may also be established.Similarly, certain types of credit are separately channelled for specialised handling; project finance, structured finance, loan participation/syndication.

Types of Credit Product

Once Credit Analysis processes have identified the reason(s) for borrowing and the purpose(s) to which the intended credit is to be put, the appropriateness and nature of Bank assistance is examined by reference to the source(s) of repayment evident in the borrower's projections.

Business Credit

Repayment Source Type of Credit1 Committed Refinance Yes

No2 Arranged sale proceeds non- current

assetsYes Bridging Loan

No3 Assured equity infusion Yes

No4 Conversion of seasonal assets Yes Seasonal Credit

WBC.400.043.6474

Business Credit Manual{ STYLEREF "Heading 1" \* MERGEFORMAT }

16 November 2012 { StyleRef "Heading 1" \* MERGEFORMAT }

No5 Surplus cash flow Yes Medium Term Credit

No6 Maintainable borrowing base Yes Revolving Credit

No7 Subordinated debt

Equity infusion Sell/Merge business

Note

Note Comment1/2/3 Can a portion of the borrowing need be provided by way of short-term bridging

finance pending the assured inflow of repayment funds from any of these sources?

4 Does analysis identify portion of the need will be removed once a seasonal build-up of current assets is converted to cash - the repayment source for a seasonal loan?

5 Does a surplus of annual cashflow after funding: capital expenditure working capital increases existing debt servicing/repayment distribution of profit provide an adequate basis to service and repay some new medium term lending?

6 Is there a sufficient maintainable level of prudently valued current assets under charge to support extension of revolving credit at levels geared to the time-to-time value of such assets? Or is there a fixed asset of sufficient enduring value under charge to support revolving credit up to a stipulated limit?

7 If the request cannot be based satisfactorily upon repayment sources 1-6 above, it is unsuitable for Bank credit and external capital (or quasi-capital) or business restructure is required.

Sources of repayment and their relationship to the main types of borrowing needs provided

Bridging Loans

PurposesTo provide interim only finance until the occurrence of a specific event which pays the loan. Three main clearance avenues:

WBC.400.043.6475

{styleref "Title" }

Westpac Group confidentialPage { SEQ Chapter\c \* Arabic \* MERGEFORMAT }-304

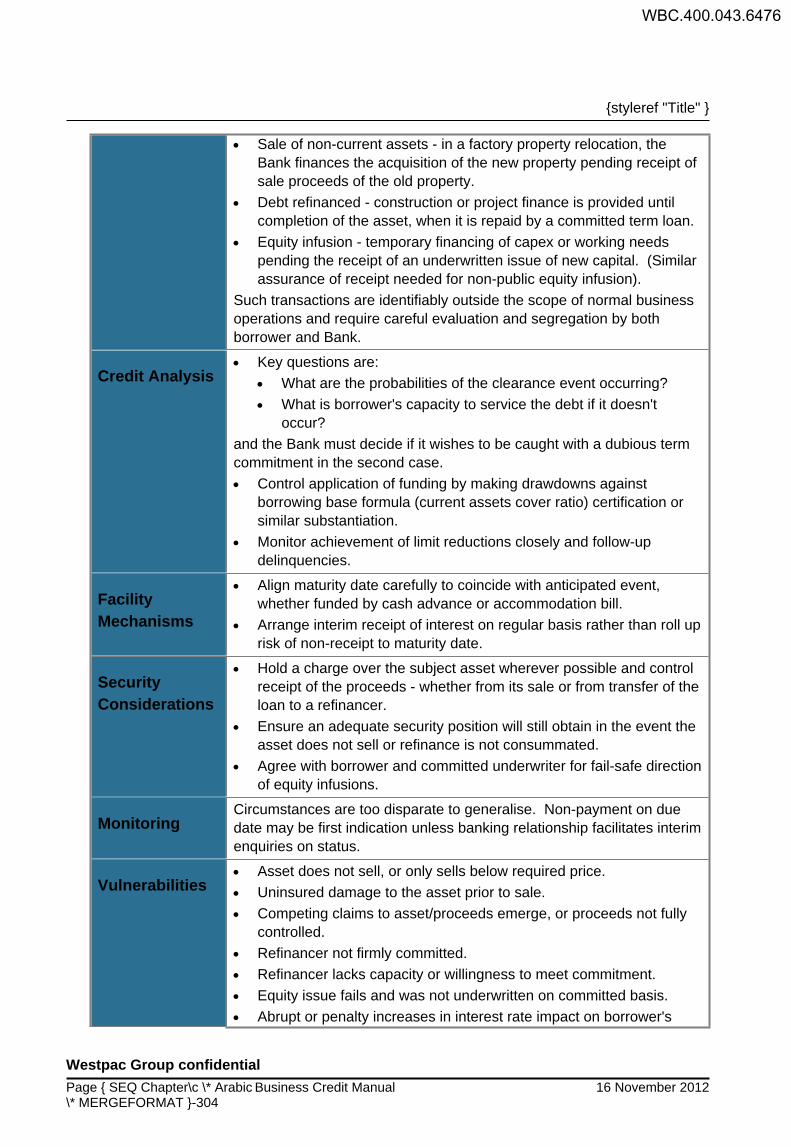

Business Credit Manual 16 November 2012

Sale of non-current assets - in a factory property relocation, the Bank finances the acquisition of the new property pending receipt of sale proceeds of the old property.

Debt refinanced - construction or project finance is provided until completion of the asset, when it is repaid by a committed term loan.

Equity infusion - temporary financing of capex or working needs pending the receipt of an underwritten issue of new capital. (Similar assurance of receipt needed for non-public equity infusion).

Such transactions are identifiably outside the scope of normal business operations and require careful evaluation and segregation by both borrower and Bank.

Credit Analysis Key questions are:

What are the probabilities of the clearance event occurring? What is borrower's capacity to service the debt if it doesn't

occur?and the Bank must decide if it wishes to be caught with a dubious term commitment in the second case. Control application of funding by making drawdowns against

borrowing base formula (current assets cover ratio) certification or similar substantiation.

Monitor achievement of limit reductions closely and follow-up delinquencies.

Facility Mechanisms

Align maturity date carefully to coincide with anticipated event, whether funded by cash advance or accommodation bill.

Arrange interim receipt of interest on regular basis rather than roll up risk of non-receipt to maturity date.

Security Considerations

Hold a charge over the subject asset wherever possible and control receipt of the proceeds - whether from its sale or from transfer of the loan to a refinancer.

Ensure an adequate security position will still obtain in the event the asset does not sell or refinance is not consummated.

Agree with borrower and committed underwriter for fail-safe direction of equity infusions.

MonitoringCircumstances are too disparate to generalise. Non-payment on due date may be first indication unless banking relationship facilitates interim enquiries on status.

Vulnerabilities Asset does not sell, or only sells below required price. Uninsured damage to the asset prior to sale. Competing claims to asset/proceeds emerge, or proceeds not fully

controlled. Refinancer not firmly committed. Refinancer lacks capacity or willingness to meet commitment. Equity issue fails and was not underwritten on committed basis. Abrupt or penalty increases in interest rate impact on borrower's

WBC.400.043.6476

Business Credit Manual{ STYLEREF "Heading 1" \* MERGEFORMAT }

16 November 2012 { StyleRef "Heading 1" \* MERGEFORMAT }

ability to service loan. Expected event does not occur, borrower lacks ability to service

debt and no valid second way out of loan is available.

Traps for Lenders

Failure to identify and consider all contingencies that could prevent repayment.

Imputing too high a value to asset to be sold so that loan is only partly cleared.

Borrower will not "meet the market", asset remains unsold and interest accumulates.

Underestimating required refinance amount in areas of cost escalations, cost over-runs, excessive accumulation of interest, etc.

Not identifying and confirming an adequate and secondary source of repayment.

Under-pricing the loan in relation to its risks.

Short-Term Seasonal Credit

PurposesWorking capital needs which are self-liquidating from conversion of accumulated inventory and/or receivables within the defined "season".

Credit Analysis

Must identify peak current assets/liabilities relationship in expansion stage and their base relationship at end of contraction stage.

Cashflow projections should be provided by borrower on monthly (perhaps weekly) periods which identify cash and credit sales receipts, direct costs and operating expenses, capex / tax payments / dividends / debt repayment, starting / ending bank balances and starting / ending balances of inventories, trade debtors and trade creditors.

If borrower cannot provide such projections (which are fundamental for proper monitoring of actual cashflows and borrowing base security), examine carefully the adequacy of its financial and operational management.

to develop our own projections - which will need further analysis to isolate the borrowing base factors. Remember that historical, end-of-period financials are unlikely to reflect interim seasonal positions.

Credit Analysis

All cashflow assumptions - particularly quantum and timing - should be confirmed with borrower and sensitised by Bank.

Bank-developed projections particularly need exhaustive discussion with, confirmation and acceptance by the borrower as achievable, realistic performance expectations if we are obliged to resort to preparing such projections. Recognise the lender liability implications in these circumstances.

Satisfaction with borrower's financial condition on macro/year on year analysis is pre-requisite to seasonal finance.

WBC.400.043.6477

{styleref "Title" }

Westpac Group confidentialPage { SEQ Chapter\c \* Arabic \* MERGEFORMAT }-306

Business Credit Manual 16 November 2012

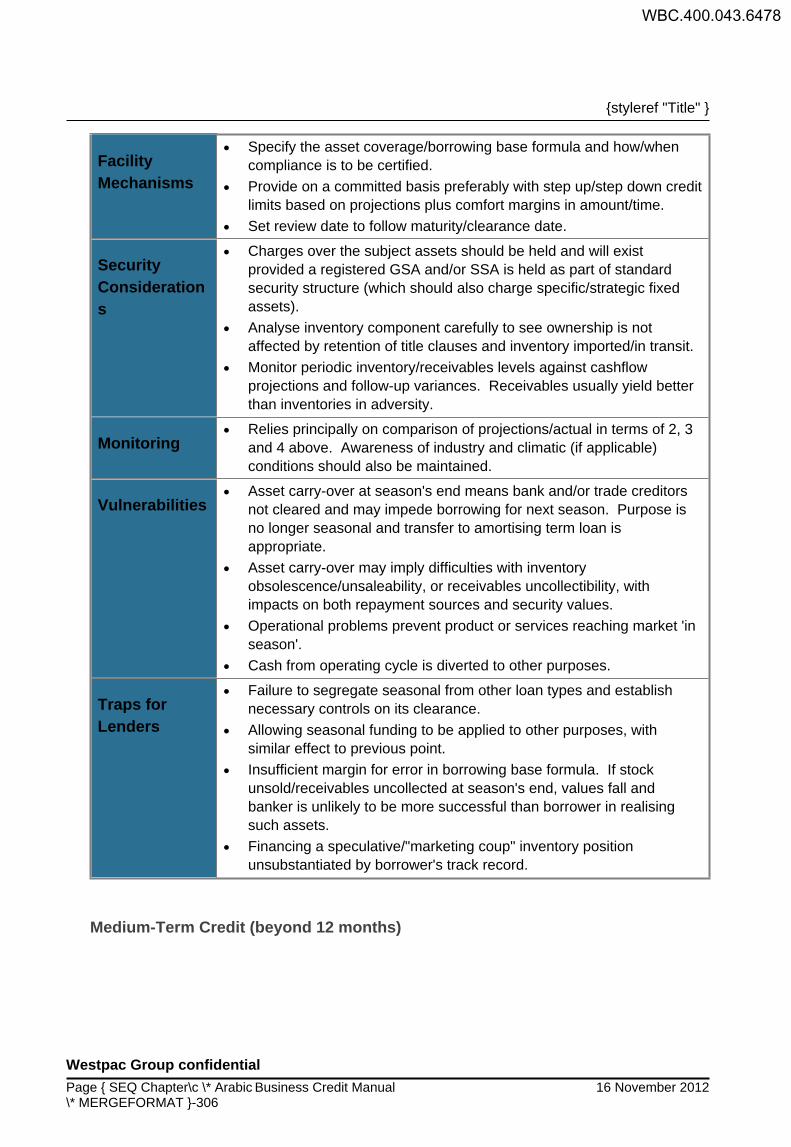

Facility Mechanisms

Specify the asset coverage/borrowing base formula and how/when compliance is to be certified.

Provide on a committed basis preferably with step up/step down credit limits based on projections plus comfort margins in amount/time.

Set review date to follow maturity/clearance date.

Security Considerations

Charges over the subject assets should be held and will exist provided a registered GSA and/or SSA is held as part of standard security structure (which should also charge specific/strategic fixed assets).

Analyse inventory component carefully to see ownership is not affected by retention of title clauses and inventory imported/in transit.

Monitor periodic inventory/receivables levels against cashflow projections and follow-up variances. Receivables usually yield better than inventories in adversity.

Monitoring Relies principally on comparison of projections/actual in terms of 2, 3

and 4 above. Awareness of industry and climatic (if applicable) conditions should also be maintained.

Vulnerabilities Asset carry-over at season's end means bank and/or trade creditors

not cleared and may impede borrowing for next season. Purpose is no longer seasonal and transfer to amortising term loan is appropriate.

Asset carry-over may imply difficulties with inventory obsolescence/unsaleability, or receivables uncollectibility, with impacts on both repayment sources and security values.

Operational problems prevent product or services reaching market 'in season'.

Cash from operating cycle is diverted to other purposes.

Traps for Lenders

Failure to segregate seasonal from other loan types and establish necessary controls on its clearance.

Allowing seasonal funding to be applied to other purposes, with similar effect to previous point.

Insufficient margin for error in borrowing base formula. If stock unsold/receivables uncollected at season's end, values fall and banker is unlikely to be more successful than borrower in realising such assets.

Financing a speculative/"marketing coup" inventory position unsubstantiated by borrower's track record.

Medium-Term Credit (beyond 12 months)

WBC.400.043.6478

Business Credit Manual{ STYLEREF "Heading 1" \* MERGEFORMAT }

16 November 2012 { StyleRef "Heading 1" \* MERGEFORMAT }

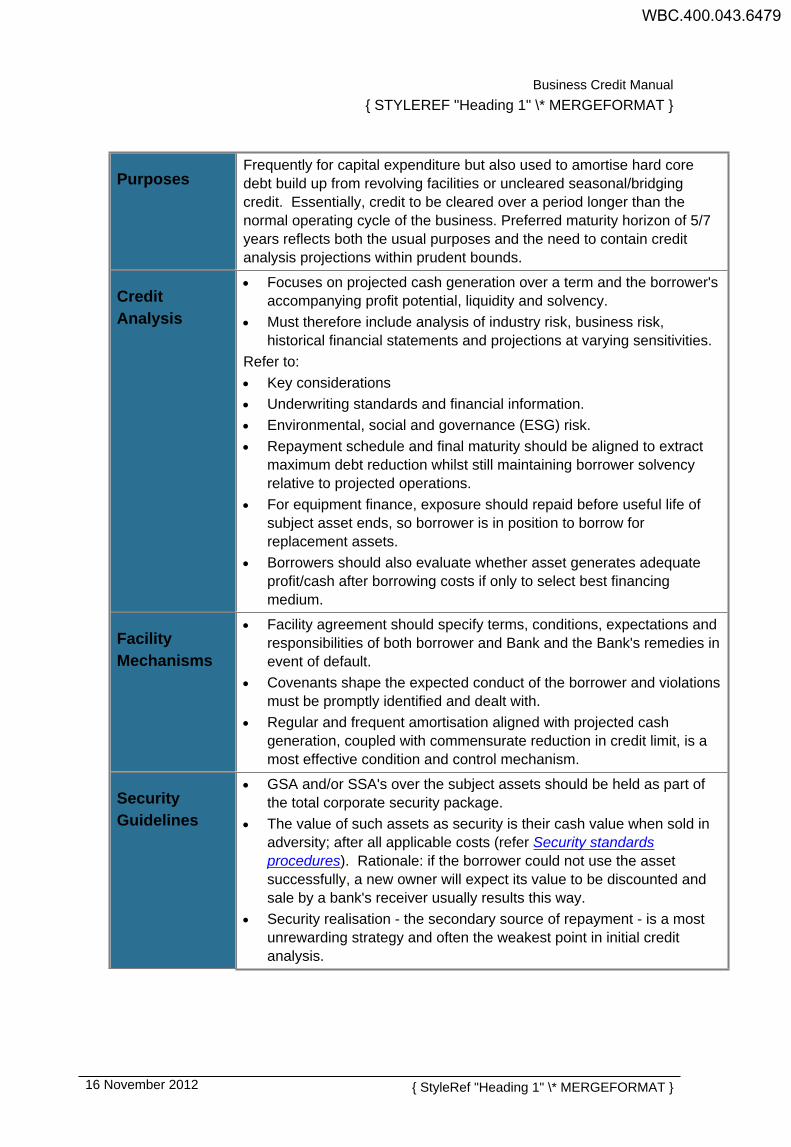

PurposesFrequently for capital expenditure but also used to amortise hard core debt build up from revolving facilities or uncleared seasonal/bridging credit. Essentially, credit to be cleared over a period longer than the normal operating cycle of the business. Preferred maturity horizon of 5/7 years reflects both the usual purposes and the need to contain credit analysis projections within prudent bounds.

Credit Analysis

Focuses on projected cash generation over a term and the borrower's accompanying profit potential, liquidity and solvency.

Must therefore include analysis of industry risk, business risk, historical financial statements and projections at varying sensitivities.

Refer to: Key considerations Underwriting standards and financial information. Environmental, social and governance (ESG) risk. Repayment schedule and final maturity should be aligned to extract

maximum debt reduction whilst still maintaining borrower solvency relative to projected operations.

For equipment finance, exposure should repaid before useful life of subject asset ends, so borrower is in position to borrow for replacement assets.

Borrowers should also evaluate whether asset generates adequate profit/cash after borrowing costs if only to select best financing medium.

Facility Mechanisms

Facility agreement should specify terms, conditions, expectations and responsibilities of both borrower and Bank and the Bank's remedies in event of default.

Covenants shape the expected conduct of the borrower and violations must be promptly identified and dealt with.

Regular and frequent amortisation aligned with projected cash generation, coupled with commensurate reduction in credit limit, is a most effective condition and control mechanism.

Security Guidelines

GSA and/or SSA's over the subject assets should be held as part of the total corporate security package.

The value of such assets as security is their cash value when sold in adversity; after all applicable costs (refer Security standards procedures). Rationale: if the borrower could not use the asset successfully, a new owner will expect its value to be discounted and sale by a bank's receiver usually results this way.

Security realisation - the secondary source of repayment - is a most unrewarding strategy and often the weakest point in initial credit analysis.

WBC.400.043.6479

{styleref "Title" }

Westpac Group confidentialPage { SEQ Chapter\c \* Arabic \* MERGEFORMAT }-308

Business Credit Manual 16 November 2012

Monitoring Working account excesses and/or delinquencies under a set

amortisation schedule are liquidity warning signals and require immediate investigation.

Compliance with well-constructed covenants - financial ratio and non-financial triggers - should be followed up regularly and all due certifications, etc. checked.

A maintained awareness of developments in borrower's industry and their implications on the credit is essential to ensure correct grading of risk.

Periodic visits to borrower's operations allow insights into many relevant aspects - management calibre, workforce quality and morale, current marketplace, current trading, value of security, etc. A visit should follow analysis of latest annual/six monthly financials.

Vulnerabilities Sales volume not achieved and insufficient cash generated for debt

reduction. Gross profit margins not achieved, to same effect. Higher volumes/lower margins sees cash absorbed into current

assets. Operating expenses cannot be reduced to counter such current asset

increase. Current asset turn ratios slow down, payables ratio accelerates and

absorb cash. Capex budgets exceeded and/or excessive dividends /drawings /fees/

salaries paid (in absence of controlling covenants). Liquidity streamed beyond security ambit by shareholder /

intercompany loans (ditto).

Traps for Lenders

Failure to understand nature of industry and borrower's position in same.

Failure to assess management's ability to handle change. Failure to identify and assess all factors affecting earnings. Projecting past track record indefinitely into the future (refer first

point). Projecting optimistically or without substantiation. Failing to leave adequate financial flexibility in borrowing structure,

leaving no scope for additional needs. Over-estimating value of security. Committing term of loan too long vis-a-vis industry and projection

uncertainties.

Revolving Credit (renewable by review)

WBC.400.043.6480

Business Credit Manual{ STYLEREF "Heading 1" \* MERGEFORMAT }

16 November 2012 { StyleRef "Heading 1" \* MERGEFORMAT }

Purposes Recurrent working capital needs to a peak level assessed over a

forward period of maximum twelve months, when renewal is subject to review.

Usually justified by slower turning current assets and faster turning current liabilities.

Drawings either increase current assets or decrease other current liabilities. Not suitable for capex, term debt repayment, etc.

Debt should be able to fluctuate up and down as current assets/collections expand and contract.

Credit Analysis

Absence of a specific repayment source (credit is really substitute for owners' equity) requires borrower to have: Sound/stable financial position and ongoing profitability. Well controlled and predictable operating cycle (clear cut

purchasing and collections policies carried through). Capable and consistent operational and financial management.

Bank must have: Sound understanding of industry and borrower's position in same. Confidence in existence and valuation of current assets. Knowledge of any working capital facilities from other sources. Awareness that this riskiest form of lending is often put to

inappropriate purposes, disbursement is usually at borrower's discretion, increased use may mask operating losses, and security in asset backing may either not exist or its dilution not be detected for some time.

Adequate financial projections to establish both adequacy of revolving credit limit vis-a-vis recurrent peak needs and also the likelihood that adequate fluctuation in limit usage will occur. It may be necessary to apportion a part of the limit to amortising term loan to achieve these objectives.

Facility Mechanisms

Facility commitment should stipulate peak limit available, required style of usage in term of fluctuations, manner of disbursement and repayment (if not on ODR), any applicable borrowing base formula and its application, and other terms and conditions including the essential "renewal subject to (annual) review" of such criteria and account conduct.

Security Considerations

Because of the various inherent risks, it is imprudent to rely on charges over the related current assets alone. The requisite financial attributes (see above) should be accompanied by not only standard fixed and floating charge but also specific charge (s) over fixed assets of some enduring value.

Realisation of inventories may be impacted by reservation of title by suppliers, distant locations, obsolescence, warranties, storage and transportation costs or (at worst) simply their non-existence (having been absorbed into operating losses or elsewhere).

Realisation of receivables is similarly hazardous.

WBC.400.043.6481

{styleref "Title" }

Westpac Group confidentialPage { SEQ Chapter\c \* Arabic \* MERGEFORMAT }-310

Business Credit Manual 16 November 2012

Monitoring Frequent specific financial reporting to analyse receivables by size

concentration, ageing and past due amounts, and inventories by raw materials, work in progress, finished goods and obsolescent stock, stock in transit, etc. should accompany usual balance sheet and operating statement analysis.

Conduct of account statistics should be watched to see fluctuation/usage criteria is met and to identify any development of hard core debt at an early stage.

Security valuations should be regularly confirmed, particularly to the degree they relate to current assets.

A current awareness of developments in the borrower's industry and their impacts on the credit should be maintained and supplemented by frequent client contact and inspection of operations.

Vulnerabilities Mis-application of drawings to non-cash-cycle purposes. Deterioration in quality of receivables and/or inventories and their

convertibility to cash. Potential for fraudulent operation of the credit by a borrower in

financial distress.

Traps for Lenders

Failure to set ground rules for facility conduct and maintenance of adequate security.

Over-estimation of realisable value of security. Book value means nothing in a liquidation scenario.

Failure to monitor account trends and financial signals closely enough to implement remedies to reduce/repay exposure.

Tendency to let things ride in the hope they will self-remedy.

WBC.400.043.6482

Business Credit Manual{ STYLEREF "Heading 1" \* MERGEFORMAT }

16 November 2012 { StyleRef "Heading 1" \* MERGEFORMAT }

Document information

Date last updated: 30 September 2016

Document control information

Manual titleBusiness Credit Manual

Chapter title6.1 Key considerations

OwnerSee footer

Contact nameSee footer

Contact phone number

See footer

Change history

Amendment number

Amendment issue date

Description of changes

1 16 November 2012

First issue online.

2 1 May 2013 Policy Alignment.3 31 May 2013 Update to correct links.4 2 October 2015 Transfer of 'Structural Financing' from Credit submission

standards.5 30 September

2016Inclusion of Information technology consideration.

WBC.400.043.6483