4. MGARCH - economics.utoronto.ca. MGARCH.pdf · Intro VEC and BEKK Example Factor Models Cond Var...

27

Intro VEC and BEKK Example Factor Models Cond Var and Cor Application Ref 4. MGARCH JEM 140: Quantitative Multivariate Finance IES, Charles University, Prague Summer 2018 JEM 140 () 4. MGARCH Summer 2018 1 / 26

Transcript of 4. MGARCH - economics.utoronto.ca. MGARCH.pdf · Intro VEC and BEKK Example Factor Models Cond Var...

Intro VEC and BEKK Example Factor Models Cond Var and Cor Application Ref

4. MGARCH

JEM 140: Quantitative Multivariate FinanceIES, Charles University, Prague

Summer 2018

JEM 140 () 4. MGARCH Summer 2018 1 / 26

Intro VEC and BEKK Example Factor Models Cond Var and Cor Application Ref

Motivation

I Multivatiate volatility models add cross-covariances of asset pricemovements in a portfolio to univariate modeling

I Covariances are important for potfolio analysisI Asset allocation and risk managementI Asset pricingI Volatility transition and spill-over e¤ects

I Drawback: number of parameters increases rapidly with portfolio size

I We need to trade o¤ exibility and accuracy vs parsimony andimplementation feasibility

JEM 140 (IES) 4. MGARCH Summer 2018 1 / 26

Intro VEC and BEKK Example Factor Models Cond Var and Cor Application Ref

Notation Framework

I Consider an (N 1) stochastic vector process frtg of asset returns,with E [rt ] = 0

I Denote by Ft1 the information set at t 1

I Letrt = H1/2

t ηt jFt1where:

I Ht = [hij ] is the (N N) covariance matrix of rtI ηt is an (N 1) iid vector error process s.t.

Eηtη

0t= I

JEM 140 (IES) 4. MGARCH Summer 2018 2 / 26

Intro VEC and BEKK Example Factor Models Cond Var and Cor Application Ref

Model Overview

1. The covariance matrix Ht is modeled directly: VEC and BEKK typemodels

2. Factor models

3. Model conditional variances and correlations: CCC type models

JEM 140 (IES) 4. MGARCH Summer 2018 3 / 26

Intro VEC and BEKK Example Factor Models Cond Var and Cor Application Ref

Models of Conditional Covariance MatrixI The VEC-GARCH model (Bollerslev et al, 1998):

vech(Ht ) = c+q

∑j=1Ajvech(rtj r0tj ) +

p

∑j=1Bjvech(Htj )

I Straightforward generalization of the univariate GARCH model

I Dimensionality: c is N(N + 1)/2, Aj and Bj areN(N + 1)/2N(N + 1)/2

I Every conditional covariance is a function of all lagged:I variancesI covariancesI squared returnsI cross-products of returns

JEM 140 (IES) 4. MGARCH Summer 2018 4 / 26

Intro VEC and BEKK Example Factor Models Cond Var and Cor Application Ref

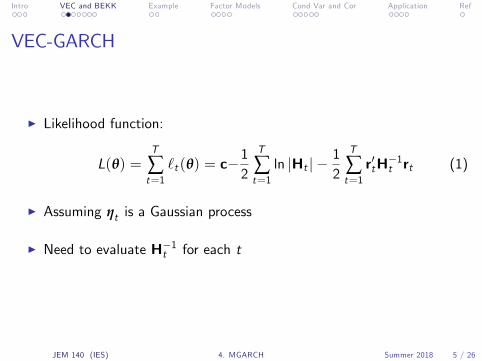

VEC-GARCH

I Likelihood function:

L(θ) =T

∑t=1`t (θ) = c

12

T

∑t=1ln jHt j

12

T

∑t=1r0tH

1t rt (1)

I Assuming ηt is a Gaussian process

I Need to evaluate H1t for each t

JEM 140 (IES) 4. MGARCH Summer 2018 5 / 26

Intro VEC and BEKK Example Factor Models Cond Var and Cor Application Ref

VEC-GARCH

I AdvantagesI Very exibleI Potentially very accurate

I DisadvantagesI Curse of dimensionality (e.g. when p = 1, q = 1, N = 10, the modelhas 3080 parameters)

I Computationally very demandingI Potentially unstable numerical inversion of Ht in likelihood evaluationI Di¢ cult to ensure Ht stays positive denite

JEM 140 (IES) 4. MGARCH Summer 2018 6 / 26

Intro VEC and BEKK Example Factor Models Cond Var and Cor Application Ref

Diagonal VEC

I Simplied version: Aj and Bj are diagonal

I Only (p + q + 1)N(N + 1)/2 parameters (e.g. when p = q = 1,N = 10, the model has 55 parameters)

I Disadvantage:I Very restrictive modelI No interaction allowed between conditional variances and covariances

JEM 140 (IES) 4. MGARCH Summer 2018 7 / 26

Intro VEC and BEKK Example Factor Models Cond Var and Cor Application Ref

BEKK

I BEKK (Engle and Kroner, 1995):

Ht = CC0 +q

∑j=1

K

∑k=1

A0kj rtj r0tjAkj +

p

∑j=1

K

∑k=1

B0kjHtjBkj

where:I C,A,B are (N N) parameter matricesI C is lower-triangular

I The constant term CC0 ensures positive deniteness of Ht

JEM 140 (IES) 4. MGARCH Summer 2018 8 / 26

Intro VEC and BEKK Example Factor Models Cond Var and Cor Application Ref

BEKK

I AdvantagesI Still quite exibleI Potentially accurateI Positive deniteness of Ht automatically satised

I DisadvantagesI N(N + 1)/2+ (p + q)K (N N) parameters (e.g. whenp = q = K = 1, N = 10, the model has 255 parameters)

I Fewer parameters than VEC but still many overallI Matrix inversion of Ht required at each t for likelihood evaluation

JEM 140 (IES) 4. MGARCH Summer 2018 9 / 26

Intro VEC and BEKK Example Factor Models Cond Var and Cor Application Ref

Diagonal and Scalar BEKK

I Diagonal BEKK: A,B are diagonal matricesI Advantage: parsimonious (N(N + 1)/2+ (p + q)KN parameters)I Disadvantage: restrictive - no covariance dynamics

I Scalar BEKK: A = aI, B = bI, where a, b 2 R

I Advantage: very parsimonious (N(N + 1)/2+ (p + q)K parameters)I Disadvantage: very restrictive - no variance or covariance dynamics

I Both are special cases of VEC and BEKK

JEM 140 (IES) 4. MGARCH Summer 2018 10 / 26

Intro VEC and BEKK Example Factor Models Cond Var and Cor Application Ref

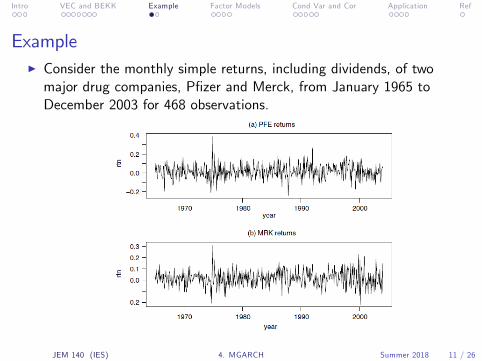

ExampleI Consider the monthly simple returns, including dividends, of twomajor drug companies, Pzer and Merck, from January 1965 toDecember 2003 for 468 observations.

JEM 140 (IES) 4. MGARCH Summer 2018 11 / 26

Intro VEC and BEKK Example Factor Models Cond Var and Cor Application Ref

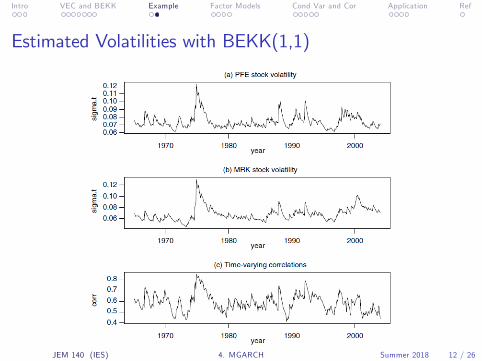

Estimated Volatilities with BEKK(1,1)

JEM 140 (IES) 4. MGARCH Summer 2018 12 / 26

Intro VEC and BEKK Example Factor Models Cond Var and Cor Application Ref

Factor GARCHI Assumption: returns are generated by a (relatively small) number of"factors" with a GARCH-type structure

I Advantage: dimensionality reduction whenK dim(factors) < dim(rt ) = N

I Engle (1990):

Ht = Ω+K

∑k=1

wkw0k fk ,t

k = 1, . . . ,K , where:I Ω is an (N N) PSD matrixI wk are (N 1) linearly independent vectors of factor weightsI fk ,t are factors with the GARCH structure

fk ,t = ωk + αk (γ0k rt1)

2 + βk fk ,t1

with ωk , αk , βk 2 R

JEM 140 (IES) 4. MGARCH Summer 2018 13 / 26

Intro VEC and BEKK Example Factor Models Cond Var and Cor Application Ref

Factor GARCH

I Engle (1990) applicationI Factor 1: value-weighted stock index returnsI Factor 2: average T-bill returns

I Disadvantage: possible correlation among factors leads to loss ofe¢ ciency

I Follow-up papers: uncorrelated factor structure

rt =Wtzt

where:I zt is an unobservable vector of uncorrelated factors estimated from dataI Wt is a linear transformation matrix

JEM 140 (IES) 4. MGARCH Summer 2018 14 / 26

Intro VEC and BEKK Example Factor Models Cond Var and Cor Application Ref

GO-GARCHI Generalized Orthogonal (GO-)GARCH (van der Weide, 2002):

Hzt = (IAB) + A (zt1z0t1) +BHzt1where:

I E [ztz0t ] = I (normalization)I A,B are (N N) diagonal parameter matricesI denotes Hadamard (i.e. elementwise) product

I Then,

Ht =WHztW0 =

N

∑k=1

w(k )w0(k )h

zk ,t

where:I w(k ) are the columns of the matrix WI hzk ,t are the diagonal elements of the matrix H

zt

I Disadvantage: in the GO-GARCH K dim(factors) = dim(rt ) = NJEM 140 (IES) 4. MGARCH Summer 2018 15 / 26

Intro VEC and BEKK Example Factor Models Cond Var and Cor Application Ref

GOF-GARCHI Generalized Orthogonal Factor (GOF-) GARCH (Lanne andSaikkonen, 2007):

W = CV

obtained via the polar decomposition, where:I C is SPD (N N) matrixI V is an orthogonal (N N) matrix

I SinceE [rt r0t ] =WW

0 = CC0

the matrix C is estimated using the spectral decomposition

C = UΛ1/2U0

where the columns of U are the eigenvectors of E [rt r0t ] and thediagonal matrix Λ contains its eigenvalues.

I Combines advantages of both factor models (reduced number offactors) and orthogonal models (ease of estimation)

JEM 140 (IES) 4. MGARCH Summer 2018 16 / 26

Intro VEC and BEKK Example Factor Models Cond Var and Cor Application Ref

CCC

I Based on the decomposition of Ht into conditional standarddeviations and correlations

I Constant Conditional Correlation (CCC-) GARCH (Bollerslev, 1990):

Ht = DtPDt (2)

where:I Dt = diag(h1/2

1t , . . . , h1/2Nt )

I P = [ρij ], PD with ρii = 1 for i = 1, . . . ,N (CCC matrix)

I For the o¤-diagonal elements of Ht this implies

[Ht ]ij = h1/2it h1/2

jt ρij , i 6= j

JEM 140 (IES) 4. MGARCH Summer 2018 17 / 26

Intro VEC and BEKK Example Factor Models Cond Var and Cor Application Ref

CCC

I Each rt follows a univariate GARCH model, yielding

ht = ω+q

∑j=1Aj r

(2)tj +

p

∑j=1Bjhtj

where:I ht is an (N 1) vector of conditional variancesI ω is an (N 1) vector of parametersI A,B are diagonal (N N) matricesI r(2)t = rt rt

JEM 140 (IES) 4. MGARCH Summer 2018 18 / 26

Intro VEC and BEKK Example Factor Models Cond Var and Cor Application Ref

ECCC

I Extended CCC (ECCC-) GARCH (Jeantheanu, 1998)I A,B are full (N N) matrices (no longer diagonal)

I Thus,

hit = ωi + a11r21,t1 + . . .+ a1N r2N ,t1 + b11h1,t1 + . . .+ b1NhN ,t1

I Advantages:I Past squared returns and variances of all series enter individual varianceequations

I Richer autocorrelation structure than CCC

JEM 140 (IES) 4. MGARCH Summer 2018 19 / 26

Intro VEC and BEKK Example Factor Models Cond Var and Cor Application Ref

CCC EstimationI The CCC structure greatly simplies estimation

I Due to the decomposition (2) the likelihood (1) has the followingsimple structure:

T

∑t=1`t (θ) = c

12

T

∑t=1

N

∑i=1ln jhit j

12

T

∑t=1ln jPj 1

2

T

∑t=1r0tD

1t P

1D1t rt

I Advantages:I P has to be inverted only once per maximization iterationI D1t = diag(1/h1/2

1t , . . . , 1/h1/2Nt )

I Easy numerical estimation

I Disadvantages:I The assumption of constant conditional correlations is too restrictive inmany applications

JEM 140 (IES) 4. MGARCH Summer 2018 20 / 26

Intro VEC and BEKK Example Factor Models Cond Var and Cor Application Ref

DCC

I Dynamic Conditional Correlation (DCC) GARCH (Engle, 2002):

Qt = (1 a b)S+ aεt1ε0t1 + bQt1

Pt = (IQt )1/2Qt (IQt )1/2 (rescaling)

where:I a, b 2 R, s.t. a+ b < 1I S is the unconditional correlation matrix of the standardized errors εt

I Advantage:I Dynamics in correlations relative to CCC

I Disadvantage:I All correlations are restricted to have the same dynamic structure

JEM 140 (IES) 4. MGARCH Summer 2018 21 / 26

Intro VEC and BEKK Example Factor Models Cond Var and Cor Application Ref

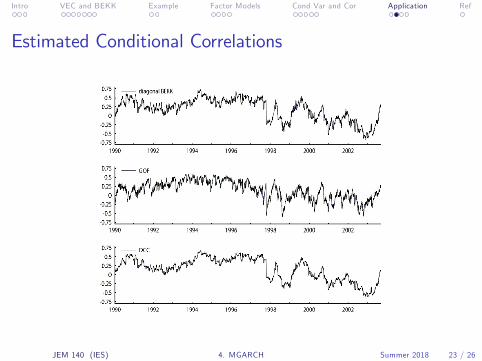

Application

I Model comparison of several (bivariate) MGARCH modelsI diag BEKK, GOF, DCC

I Data: daily returns of S&P 500 index futures and 10-year bondfutures, January 1990 - August 2003

I No theoretical consensus on how stocks and long-term bonds arerelated

I The long-run correlation is state-dependent and varies with othermacro-economic variables

JEM 140 (IES) 4. MGARCH Summer 2018 22 / 26

Intro VEC and BEKK Example Factor Models Cond Var and Cor Application Ref

Estimated Conditional Correlations

JEM 140 (IES) 4. MGARCH Summer 2018 23 / 26

Intro VEC and BEKK Example Factor Models Cond Var and Cor Application Ref

Estimates

I Sample Correlations of the Estimated Conditional Correlations

JEM 140 (IES) 4. MGARCH Summer 2018 24 / 26

Intro VEC and BEKK Example Factor Models Cond Var and Cor Application Ref

Comparison

I Assess model t by likelihood value at the parameter estimates

I Models that are relatively easy to estimate t the data less well thanthe other models

I Models with more complicated structure attain higher likelihoodvalues

JEM 140 (IES) 4. MGARCH Summer 2018 25 / 26

Intro VEC and BEKK Example Factor Models Cond Var and Cor Application Ref

Reference

I Reference: Silvennoinen, A. and Teräsvirta, T. "Multivariate GARCHModels", in Hanbook of Financial Time Series, Andersen et al (Eds.),Springer, 2009.

JEM 140 (IES) 4. MGARCH Summer 2018 26 / 26