McGraw-Hill/Irwin © 2005 The McGraw-Hill Companies, Inc. All ...

Upload

lesley-knightCategory

view

213download

0

4- 1

McGraw Hill/Irwin Copyright © 2009 by The McGraw-Hill Companies, Inc. All rights reserved

Fundamentals of Corporate

Finance

Sixth Edition

Richard A. Brealey

Stewart C. Myers

Alan J. Marcus

Slides by

Matthew Will

Chapter 4

McGraw Hill/Irwin Copyright © 2009 by The McGraw-Hill Companies, Inc. All rights reserved

Measuring Corporate Performance

4- 2

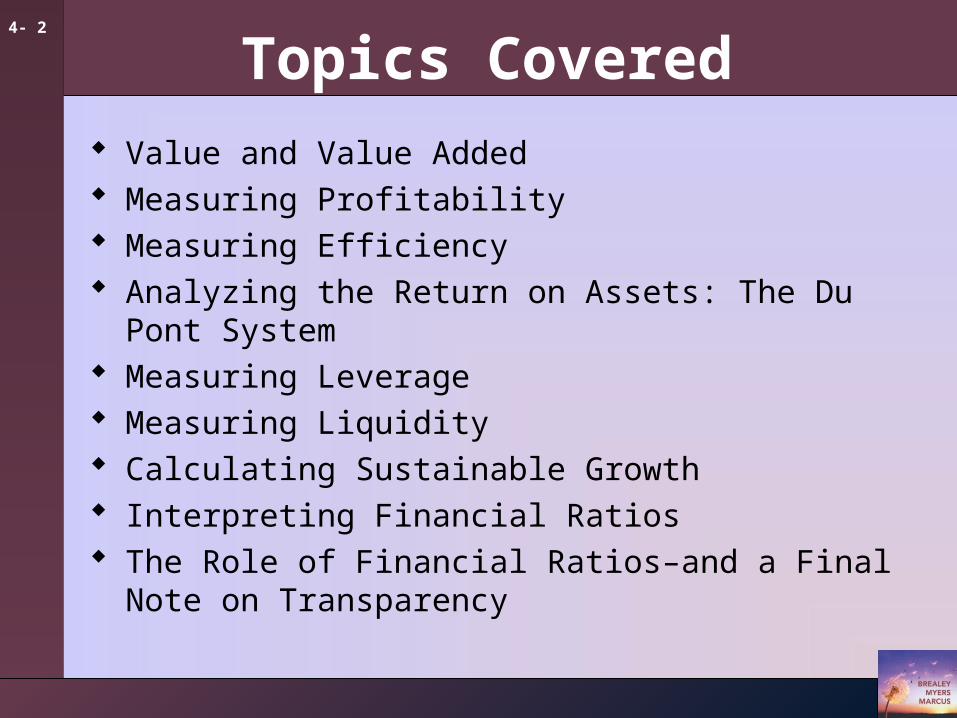

Topics Covered Value and Value Added Measuring Profitability Measuring Efficiency Analyzing the Return on Assets: The Du Pont System Measuring Leverage Measuring Liquidity Calculating Sustainable Growth Interpreting Financial Ratios The Role of Financial Ratios–and a Final Note on

Transparency

4- 3

Value and Value AddedPepsiCo Balance Sheet (December 31, 2006) $Millions

4- 4

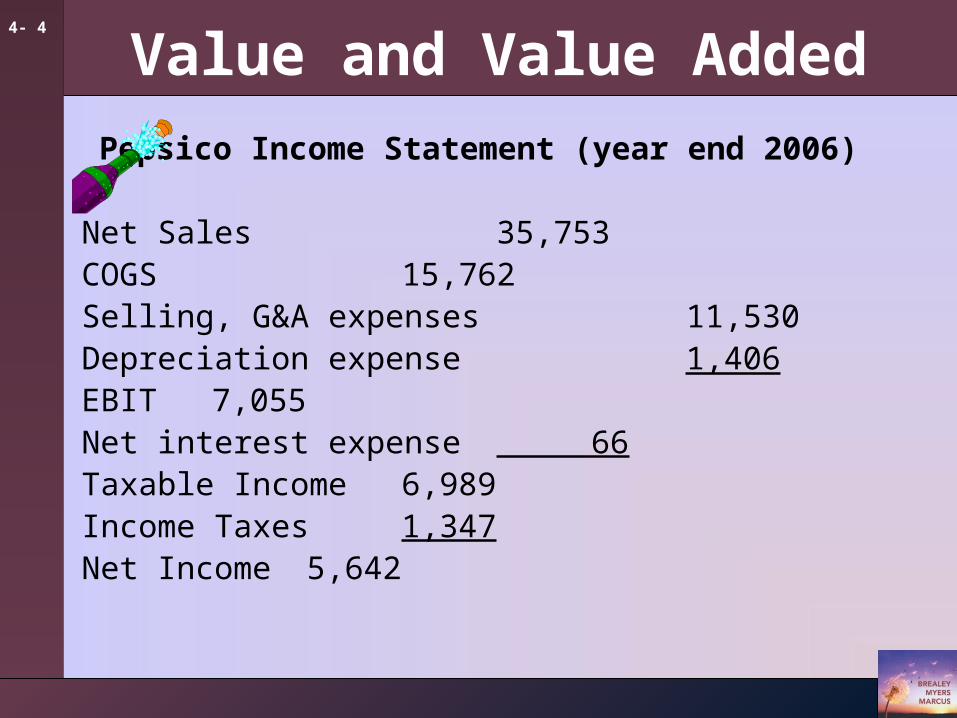

Value and Value Added

Pepsico Income Statement (year end 2006)

Net Sales 35,753COGS 15,762Selling, G&A expenses 11,530Depreciation expense 1,406EBIT 7,055Net interest expense 66Taxable Income 6,989Income Taxes 1,347Net Income 5,642

4- 5

Value and Value Added

Market Capitalization Total market value of equity, equal to share price

times number of shares outstanding.

Market Value Added Market capitalization minus book value of equity.

share)per (priceshares) (# tion CapitalizaMarket

ValueBook Equity -tion CapitalizaMarket MVA

4- 6

Value and Value Added

Stock market measures of company performance, 2006. Companies are ranked by market value added. (dollar values in millions)

4- 7

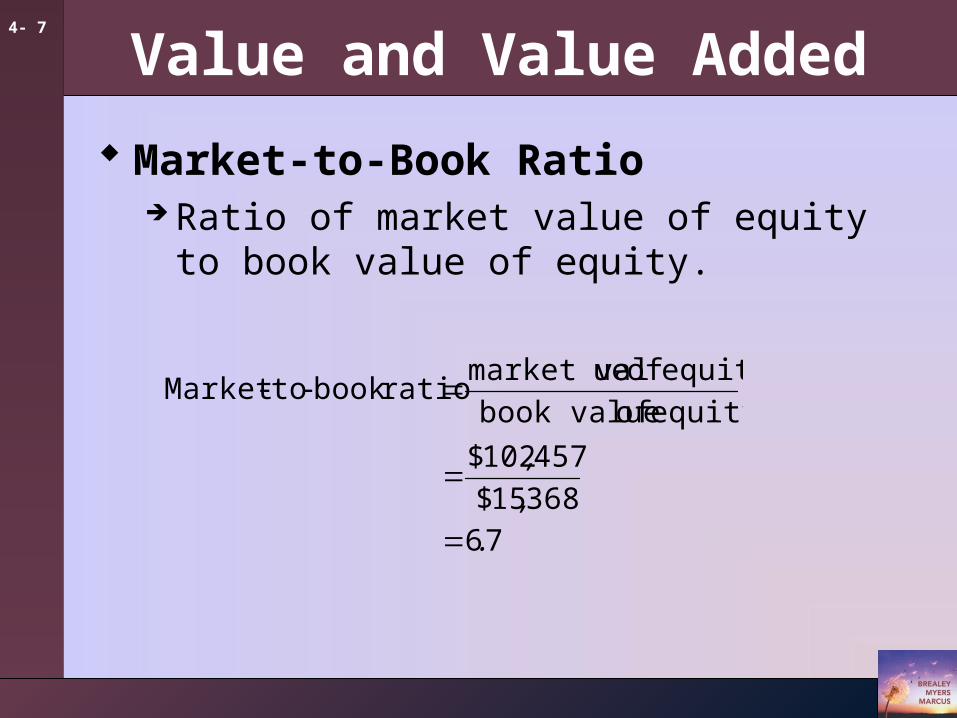

Value and Value Added

Market-to-Book Ratio Ratio of market value of equity to book value of

equity.

76

36815$

457102$

equity of book value

equity of uemarket valratiobook -to-Market

.

,

,

4- 8

Measuring Profitability

Economic Value Added (EVA) Net income minus a charge for the cost of capital

employed. Also called residual income.

Residual Income Net Dollar return after deducting the cost of

capital

Equity Equity ofCost - IncomeNet

Income Residual

EVA

4- 9

Measuring Profitability

Economic Value Added (EVA) of PepsiCo

Equity Equity ofCost - IncomeNet

Income Residual

EVA

million $4,527

14,251.095 - 5,642

Income Residual

EVA

4- 10

Measuring Profitability

Accounting measures of company performance, 2006. Companies are ranked by return on equity.

4- 11

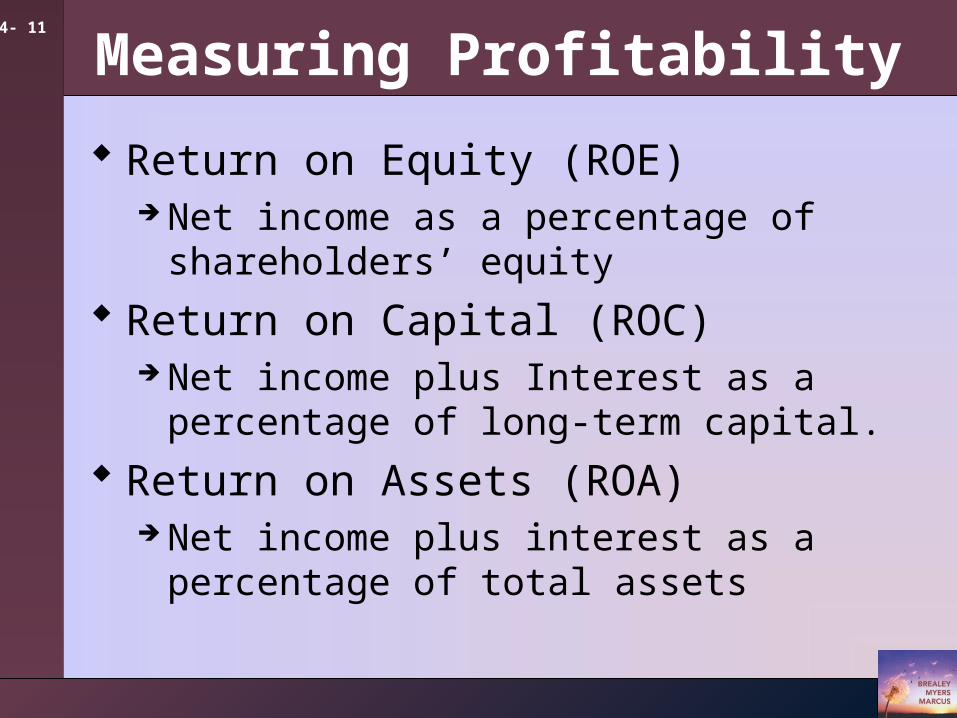

Measuring Profitability

Return on Equity (ROE) Net income as a percentage of shareholders’

equity

Return on Capital (ROC) Net income plus Interest as a percentage of long-

term capital.

Return on Assets (ROA) Net income plus interest as a percentage of total

assets

4- 12

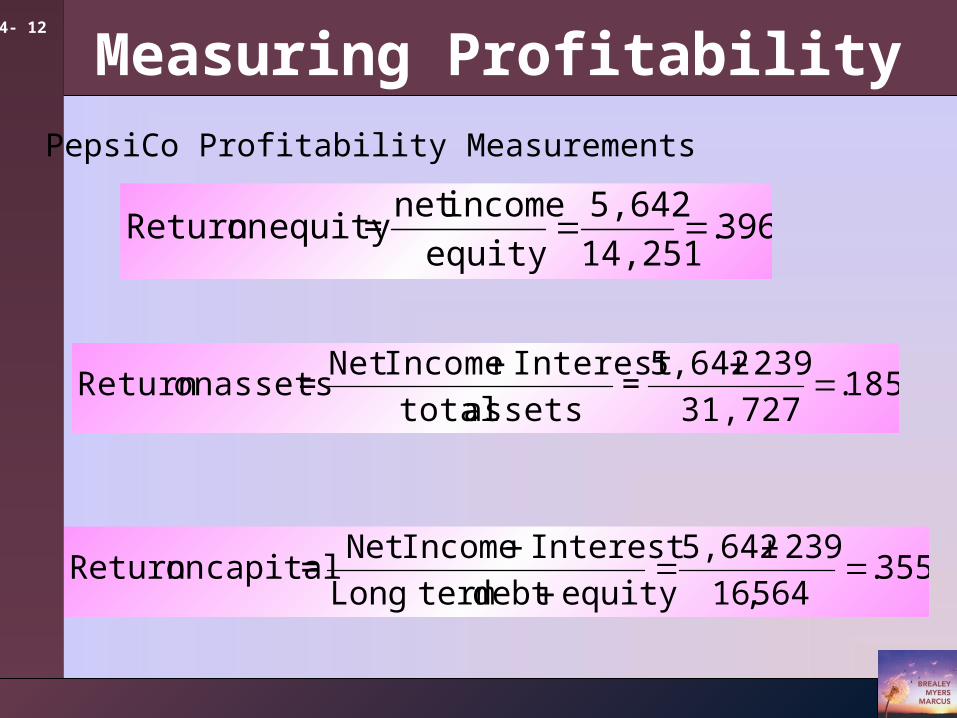

Measuring Profitability

396.14,251

5,642

equity

incomenet =equityon Return

185.31,727

2395,642=

assets total

Interest IncomeNet =assetson Return

355.564,16

2395,642

equity debt termLong

Interest IncomeNet =capitalon Return

PepsiCo Profitability Measurements

4- 13

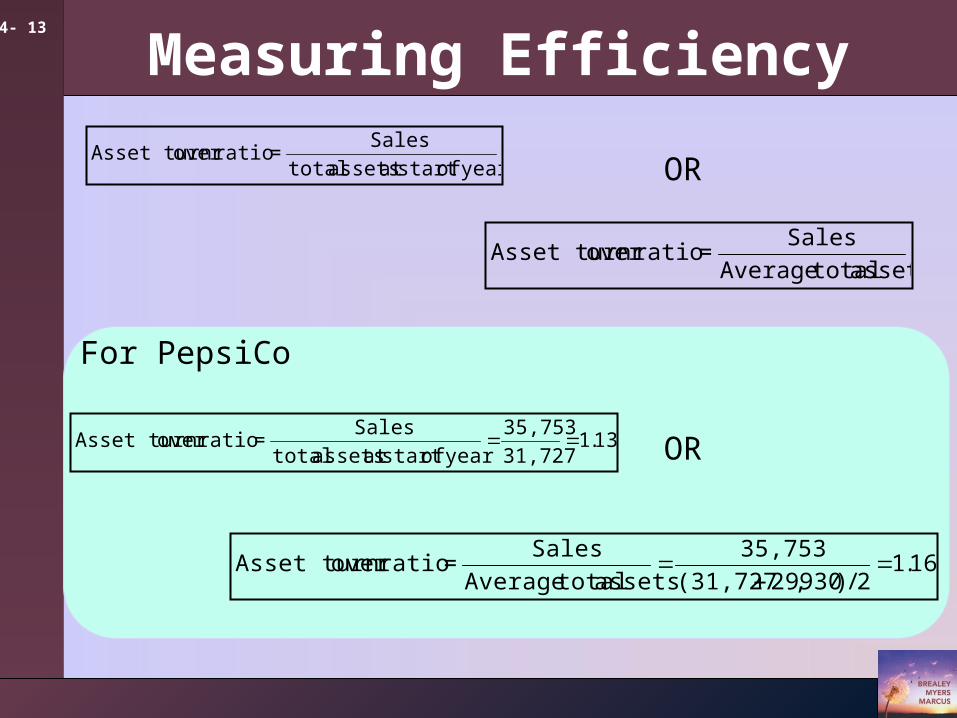

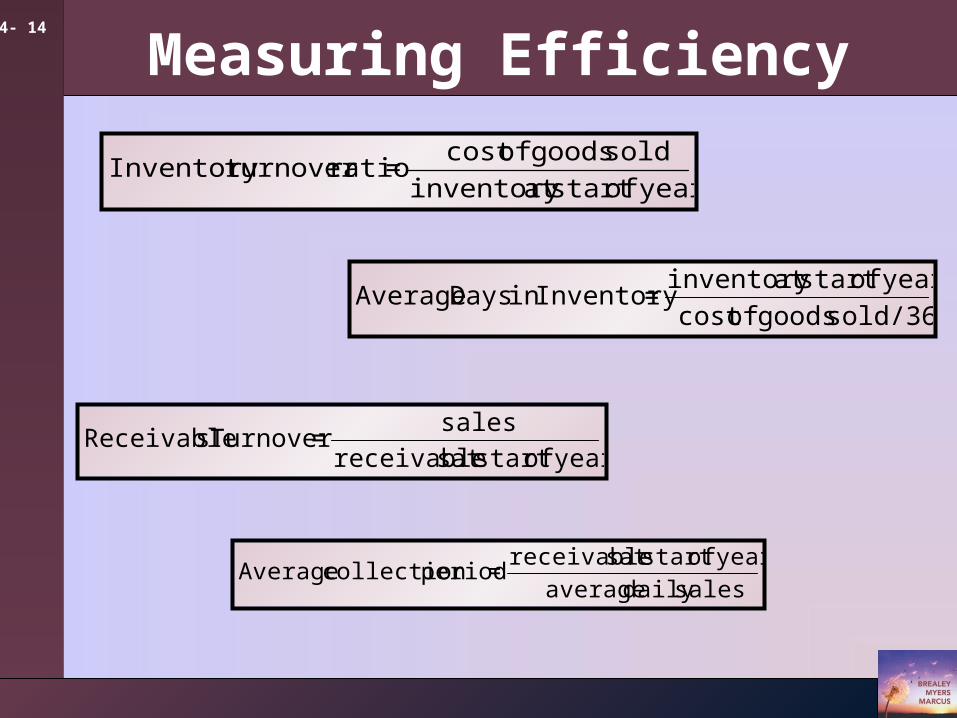

Measuring Efficiency

year ofstart at assets total

Sales=ratioover Asset turn

assets totalAverage

Sales=ratioover Asset turn

OR

13.131,727

35,753

year ofstart at assets total

Sales=ratioover Asset turn

16.12/)930,29(31,727

35,753

assets totalAverage

Sales=ratioover Asset turn

OR

For PepsiCo

4- 14

Measuring Efficiency

sold/365 goods ofcost

year ofstart at inventory =Inventoryin Days Average

year ofstart at inventory

sold goods ofcost =ratioturnover Inventory

salesdaily average

year ofstart at sreceivable=period collection Average

year ofstart at sreceivable

sales=Turnover sReceivable

4- 15

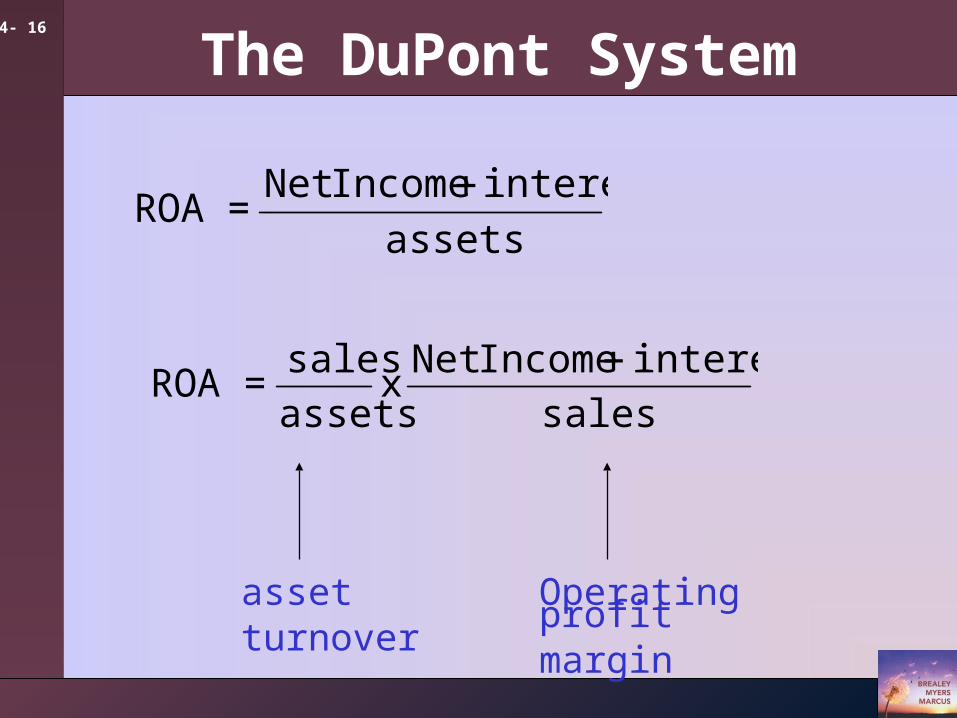

The DuPont System

A breakdown of ROE and ROA into component ratios

sales

Interest IncomeNet =MarginProfit Operating

sales

IncomeNet =MarginProfit

4- 16

The DuPont System

sales

interestIncomeNet x

assets

sales=ROA

assetturnover

Operating profitmargin

assets

interest IncomeNet =ROA

4- 17

Measuring Leverage

equity+debt termlong

debt termlong=ratiodebt termLong

equity

debt termlong=ratioequity Debt

4- 18

Measuring Leverage

Total debt ratio =total liabilities

total assets

Times interest earned =EBIT

interest payments

Cash coverage ratio =EBIT + depreciation

interest payments

4- 19

Measuring Leverage

interestIncomeNet

IncomeNet x

sales

interestIncomeNet x

assets

salesx

equity

assets=ROE

leverageratio

assetturnover

Operating profitmargin

debtburden

4- 20

Measuring Liquidity

Net working capital

to total assets ratio=

Net working capital

Total assets

Current ratio =current assets

current liabilities

4- 21

Liquidity Ratios

Cash ratio =cash + marketable securities

current liabilities

Quick ratio =cash + marketable securities + receivables

current liabilities

4- 22

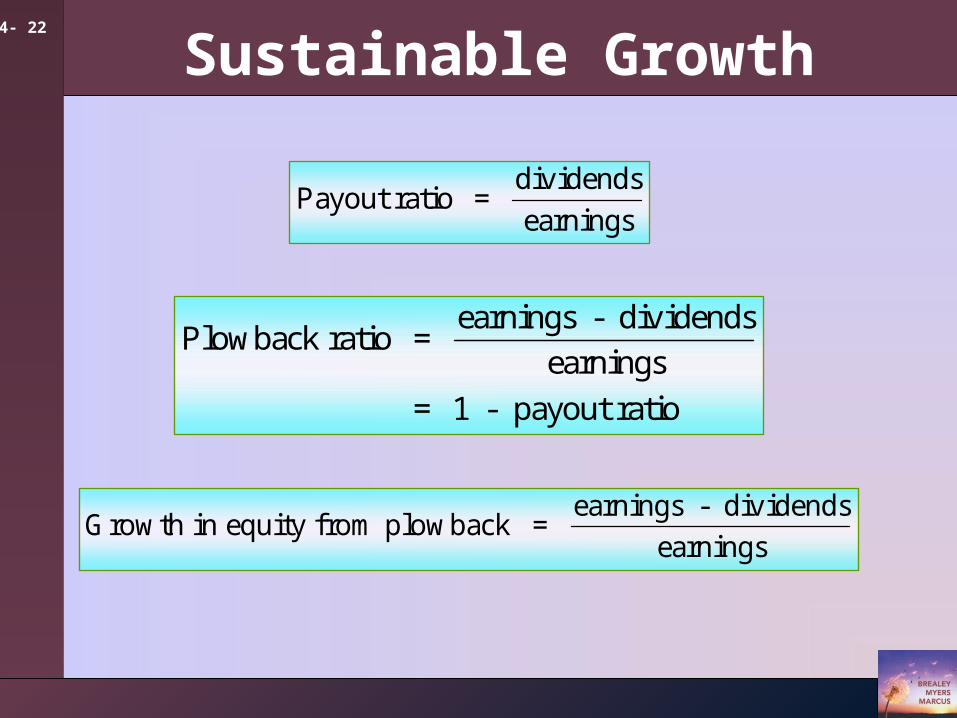

Sustainable Growth

Plowback ratio =earnings - dividends

earnings

= 1 - payout ratio

Payout ratio =dividends

earnings

Growth in equity from plowback =earnings - dividends

earnings

4- 23

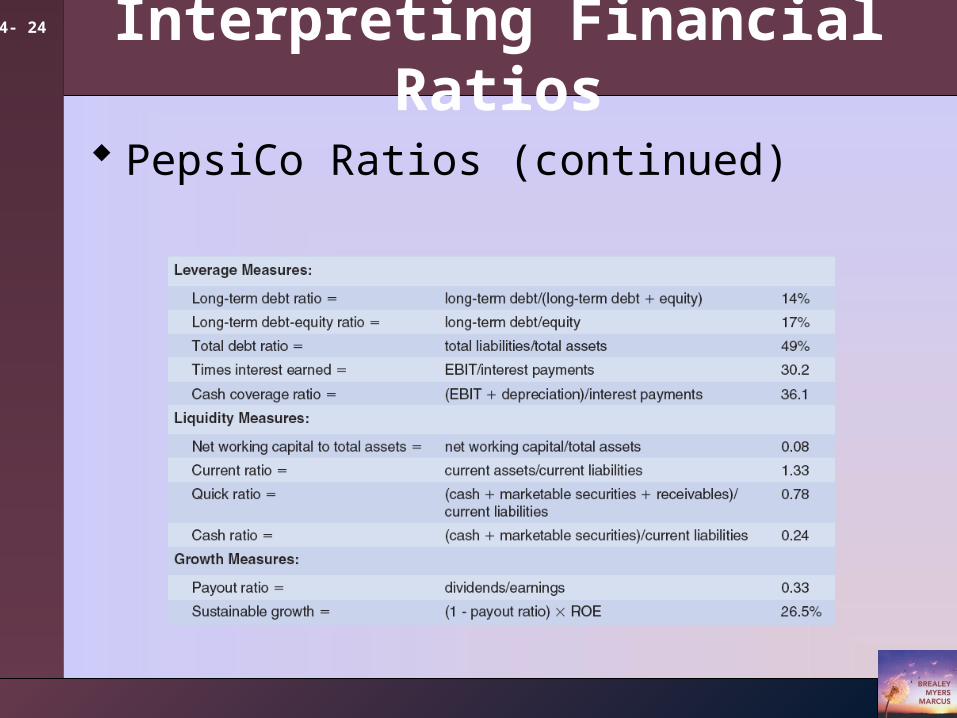

Interpreting Financial Ratios

PepsiCo Ratios

4- 24

Interpreting Financial Ratios

PepsiCo Ratios (continued)

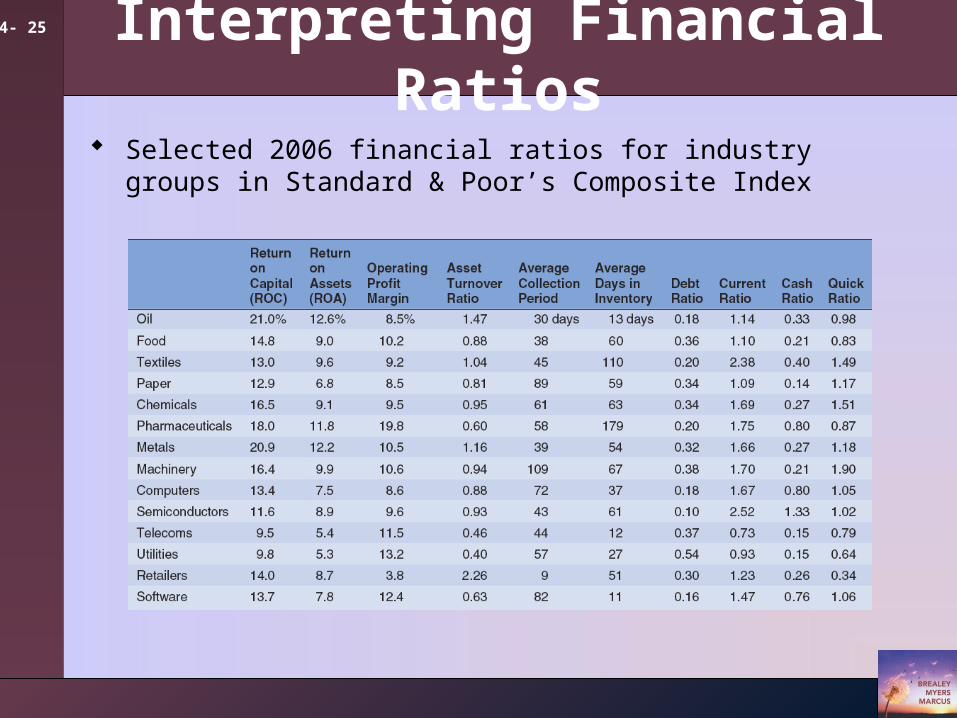

4- 25

Interpreting Financial Ratios Selected 2006 financial ratios for industry groups in Standard & Poor’s

Composite Index

4- 26

The Role of Financial Ratios

4- 27

Web Resources