3rd LNG SUPPLY, STORAGE AND TRANSPORTATION PHILLIPINES ... · 3rd LNG SUPPLY, STORAGE AND...

10

3 rd LNG SUPPLY, STORAGE AND TRANSPORTATION PHILLIPINES FORUM 2016 – SMX AURA, MANILA “Growing the market for “LNG to Power (L2P)” Projects through the Conversion of Existing LNG Carriers” Nor Aslam Khan Director newGAS Pte. Ltd. [email protected]

Transcript of 3rd LNG SUPPLY, STORAGE AND TRANSPORTATION PHILLIPINES ... · 3rd LNG SUPPLY, STORAGE AND...

LNG PHILIPPINES 2016

3rd LNG SUPPLY, STORAGE AND TRANSPORTATION PHILLIPINES FORUM 2016 – SMX AURA, MANILA

“Growing the market for “LNG to Power (L2P)” Projects through the Conversion of Existing LNG Carriers”

Nor Aslam KhanDirectornewGAS Pte. [email protected]

LNG PHILIPPINES 2016

LNG is enabling gas to become the fuel of choice for power generation

• Gas market share of primary energyhas been increasing steadily.

Shares of Primary Energy* Includes Biofuels

Inputs to power as a share of total primary energy

Shares of global gas consumption

• Power is the main driver for totalprimary energy consumption.

• LNG has become the preferred gastransportation technology in globalconsumption.

BP Energy Outlook 2016

2

LNG PHILIPPINES 2016

Growth in LNG regas projects in ASEAN fueled by development of new gas power plants

LNG Supply from Australia and Papua New Guinea

LNG Supply from Qatar/ME

A no of mini gas power plant projectsto be fueled by LNG

LNG Regasification Projects linked toPower markets/customers

LNG Supply - Liquefaction Plants

Existing LNG Regas Terminal - reloads

3

LNG PHILIPPINES 2016

Powering with LNG via pipelines is well established – Buyer’s Market

LiquefactionStandard Sized

Shipping

Oversupplied Oversupplied

Regasification

• Asia Pacific has 75% of

demand market share

• LNG - 11% of all gas use

Buyer’s Market

Upstream Gas Supply

Abundance

USA Annual Proved Reserves (1964 – 2014) Source : The Economist

Source : Forbes (EIA, JTC)

Source : SSY 4

LNG PHILIPPINES 2016

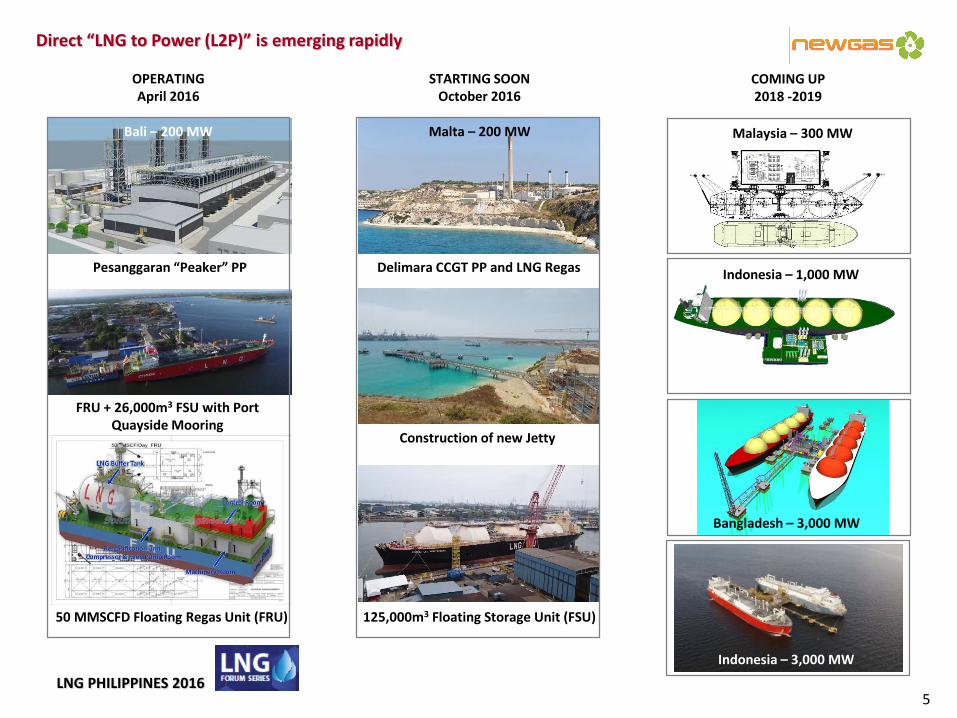

Direct “LNG to Power (L2P)” is emerging rapidly

5

OPERATING April 2016

STARTING SOON October 2016

COMING UP 2018 -2019

Bali – 200 MW Malta – 200 MW Malaysia – 300 MW

Indonesia – 1,000 MW

Bangladesh – 3,000 MW

Indonesia – 3,000 MW

Pesanggaran “Peaker” PP Delimara CCGT PP and LNG Regas

FRU + 26,000m3 FSU with Port Quayside Mooring

50 MMSCFD Floating Regas Unit (FRU)

Construction of new Jetty

125,000m3 Floating Storage Unit (FSU)

LNG PHILIPPINES 2016

Where are the bottlenecks for growth in small scale L2P?

6

Pre - 2000 Post 2010 – Multi Carriers 24 Month Delivery – LNG Carrier

1 - 2 Nos - < 20,000 m3

Controlled by 1 company

6 Nos – 10,000 – 12,000 m3

Controlled by 1 company. Available for niche usage such as

cool-down, short term charter, etc.

1 - 2 Nos – 6,000 – 30,000 m3

1 company dedicated to LNG. Ready designs and firm price from

shipyards.

2 Nos – 45,000 m3

1 company. Possibly targeting private Chinese inland market.

2015 – 2019 Chinese LNGC

5 Nos – 14,000 - 30,000 m3

Controlled by 3 companies for inland transportation. Available

for 1 to 2 year charter.

• Main bottleneck for small scale L2P is in Logistics – availability of ships, right size, price.

• Challenges related to new entrants in L2P projects are,

Procurement Strategy for shipping and FSRU is rigid – does not allow to “mixand match” between EPCC (direct purchase) and Time Charter.

Insufficient company size for L2P projects – procurement on long term LNGcontract to fuel power plant is a challenge. Right sized parcels allow projectcashflow optimization.

Where to start and how to develop the project - lacking information, knowledgeand expertise in LNG.

LNG PHILIPPINES 2016

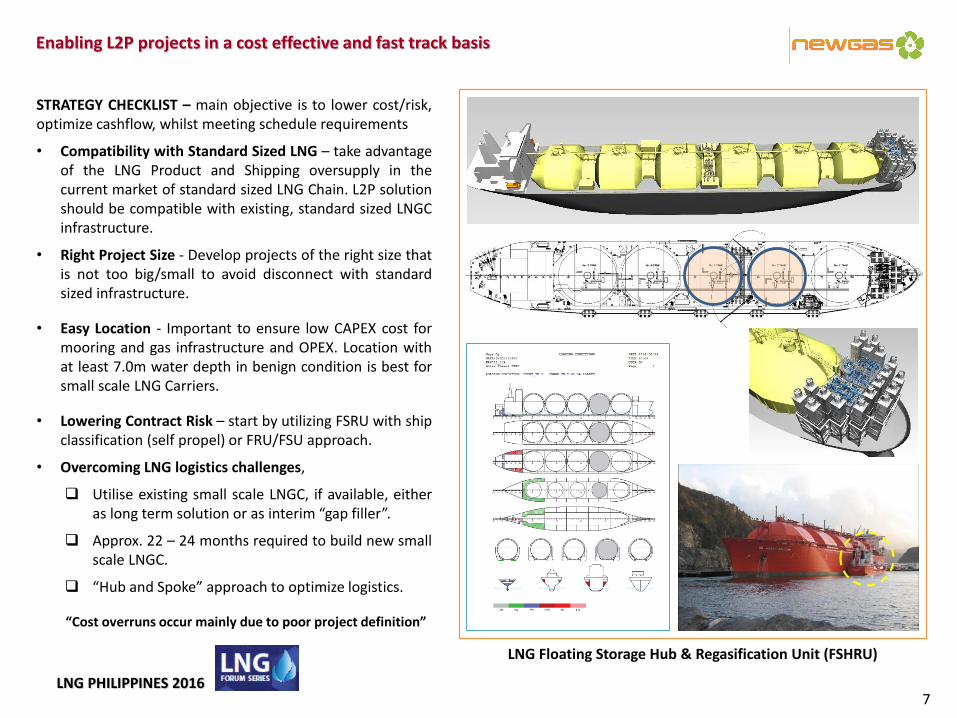

Enabling L2P projects in a cost effective and fast track basis

7

STRATEGY CHECKLIST – main objective is to lower cost/risk,optimize cashflow, whilst meeting schedule requirements

• Compatibility with Standard Sized LNG – take advantageof the LNG Product and Shipping oversupply in thecurrent market of standard sized LNG Chain. L2P solutionshould be compatible with existing, standard sized LNGCinfrastructure.

• Right Project Size - Develop projects of the right size thatis not too big/small to avoid disconnect with standardsized infrastructure.

• Easy Location - Important to ensure low CAPEX cost formooring and gas infrastructure and OPEX. Location withat least 7.0m water depth in benign condition is best forsmall scale LNG Carriers.

• Lowering Contract Risk – start by utilizing FSRU with shipclassification (self propel) or FRU/FSU approach.

• Overcoming LNG logistics challenges,

Utilise existing small scale LNGC, if available, eitheras long term solution or as interim “gap filler”.

Approx. 22 – 24 months required to build new smallscale LNGC.

“Hub and Spoke” approach to optimize logistics.

LNG Floating Storage Hub & Regasification Unit (FSHRU)

“Cost overruns occur mainly due to poor project definition”

LNG PHILIPPINES 2016

Example of sustainable L2P project – overcome tight schedule, yet allow for growth

8

1st Phase – start project

LNG FSHRT utilized to store and regas LNG to fuel power plant - < 15 months

Gas Fuel

Gas Fuel

Gas Fuel

2nd Phase – maintain and grow

LNG FSHRT utilized for trans-shipment of LNG cargo for other terminals

Small Scale LNGC

Either build new or charter-in if available

FSU

Utilise existing LNGC as interim until new FSU is delivered

Newbuilding FRU

Can be delivered in 12 to 15 months

LNG

LNG Shuttle Tanker – standard LNG Carrier

Compatible for Ship-to-Ship (STS) transfer to deliver partial LNG cargo

LNG PHILIPPINES 2016

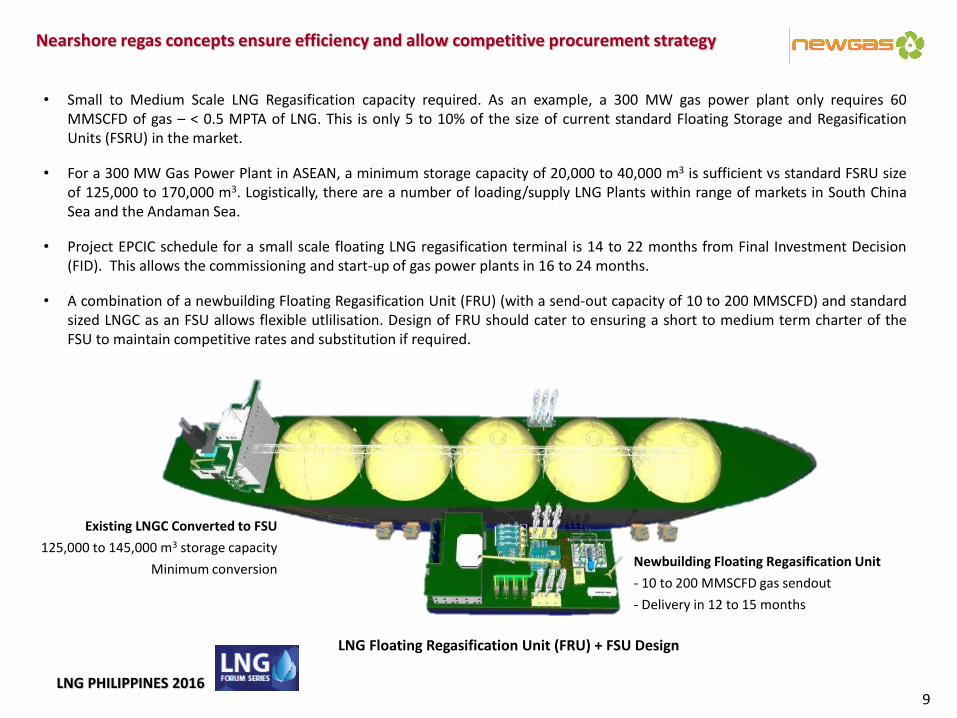

Nearshore regas concepts ensure efficiency and allow competitive procurement strategy

• Small to Medium Scale LNG Regasification capacity required. As an example, a 300 MW gas power plant only requires 60MMSCFD of gas – < 0.5 MPTA of LNG. This is only 5 to 10% of the size of current standard Floating Storage and RegasificationUnits (FSRU) in the market.

• For a 300 MW Gas Power Plant in ASEAN, a minimum storage capacity of 20,000 to 40,000 m3 is sufficient vs standard FSRU sizeof 125,000 to 170,000 m3. Logistically, there are a number of loading/supply LNG Plants within range of markets in South ChinaSea and the Andaman Sea.

• Project EPCIC schedule for a small scale floating LNG regasification terminal is 14 to 22 months from Final Investment Decision(FID). This allows the commissioning and start-up of gas power plants in 16 to 24 months.

• A combination of a newbuilding Floating Regasification Unit (FRU) (with a send-out capacity of 10 to 200 MMSCFD) and standardsized LNGC as an FSU allows flexible utlilisation. Design of FRU should cater to ensuring a short to medium term charter of theFSU to maintain competitive rates and substitution if required.

LNG Floating Regasification Unit (FRU) + FSU Design

9

Newbuilding Floating Regasification Unit

- 10 to 200 MMSCFD gas sendout

- Delivery in 12 to 15 months

Existing LNGC Converted to FSU

125,000 to 145,000 m3 storage capacity

Minimum conversion

LNG PHILIPPINES 2016

How can we help you?

END

THANK YOU

www.newgas.com.sg

Project Definition

Hit the ground running

Competitive Concepts and Solutions

Fit for Purpose

Decision Making Facilitation

Focus on what matters

Leverage Partners

Turnkey EPCC, Shipyards, O&M Services

LNG Shipping

Tie down the logistics