3rd Astana M&M International Congress -...

17

3 rd Astana M&M International Congress William Husband Head of Metals and Mining Russia and CIS

Transcript of 3rd Astana M&M International Congress -...

3rd Astana M&M International Congress

William Husband

Head of Metals and Mining

Russia and CIS

Kazakhstan is Well Positioned to Continue M&M Industry Growth

One of the most promising Metals & Mining geographies globally

- 2nd largest uranium reserves in the world

- More than 10% of global copper and iron reserves

- More than 13% of global lead and zinc reserves

- About 30% and 25% of global reserves of chromium and manganese respectively

Kazakhstan‟s Metals & Mining industry produces more than 20% of the country‟s overall industrial output

Higher than 5% real GDP growth is expected over the next 5 years

Kazakhstan‟s Metals & Mining sector has established national champions with the global scale:

- ENRC, the leading producer of marketable iron ore, ferrous alloys, pellets and aluminium

- Kazakhmys, the major copper producer with more than 90% of Kazakhstan‟s copper production

- Kazzinc, the leading zinc producer in Kazakhstan

- KazAtomProm, the leading global producer of uranium and rare metals

The largest foreign companies including Rio Tinto, Glencore, Vale, Mechel and Ivanhoe have been operating in

Kazakhstan for years

1

Kazakhstan Metals & Mining Landscape Having a lot of world class deposits of various metals already in operation, Kazakhstan has enormous exploration

potential through existing and not yet discovered greenfield deposits.

Gold Copper / Zinc Coal Ferroaloys Iron Ore Aluminium Uranium

2

Astana

Akzhal

Aksu Bestobe

Zholymbet

Varvarinskoye

Komarovskoye Elevatornoye Raigorodok Novodneprovskoye

Suzdal Maleevsky

Central Mukur

Ridder-Sokolny Tishinsky Shubinsky

Shaimerden

Kyzyl

Zhomart

South Annensky East North

Stepnoy

Orlovsky Artemyevsky

Mizek

Shatyrkul

Sayak

Abyz

Akbastau

Nurkazgan Molodezhny

Kusheki

Donskoy

Zhairem

Sokolov-Sarbai

Turgai

Shubarkol

Uvanas

Kanzhugan Moinkum

Northern Karamurun Southern Karamurun

Vostok

Voskhod

Irtyshsky

Nikolayevsky

Yubileyno-Snegirikhinsky

Almaty

Bogatyr

Severny Vostochny Vasilkovskoye

Zarechnoe

Akbastau

Akbastau Akdala South Inkai

Karatau

Polymetal CAMMEX Polyus Nordgold

Kazzinc (Glencore) Altynalmas (Ivanhoe) Kazakhmys ENRC Kazatomprom

Mechel

Samruk-Energy / Rusal

Uranium one Cameco

Inkai

‟s Dedicated Global Metals and Mining Team

Australia

South Africa

Russia & CIS

Strib Koster

Managing Director

Chairman of Global Industrials Group

Head of Global Metals & Mining Sector

Japan

India

Europe

North America

Nick Pagden

Managing Director

Asia / China

Richard Zhang

Managing Director

Irackly Mtibelishvily

Managing Director

Brennan Smith

Managing Director

Pramit Jhaveri

Managing Director

Shun Uchikawa

Managing Director

Tom Massey

Managing Director

Jason Johnson

Managing Director

Paul Harris

Managing Director

Citi has an established, highly connected global network of relationship bankers and product specialists to access

decision makers in the Metals & Mining industry and investment community in relevant geographies.

John Messina

Director

Ivan Leung

Director – M&A

Nathan Eldridge

Managing Director – M&A

Sean Wegerhoff

Director

Mark Doller

Director

Eugene Qian

Managing Director

James Hu

Director

Sukbong Kim

Director

Korea

Sumit Parikh

Vice President

Arash Mahdaviani

Director

Mike Cramer

Managing & Senior

Technical Director

Mining Specialist

Jason Hutchings

Managing Director

Christian Hoessrich

Director

Richy Xie

Director

William Husband

Director

Asif Zaidi

Managing Director

3

Citi‟s Commitment and Insight into Kazakhstan Long standing commitment to Kazakhstan Major Transactions in Kazakhstan

Citi is the most committed foreign bank in Kazakhstan as evidenced by:

our history of on the ground presence since 1994;

over 120 full time employees in Kazakhstan;

a branch in Astana since 2006;

continuous support to our clients during the economic downturn, and

expansion in Kazakhstan during the Global economic downturn with hiring

new bankers, increasing capitalization of Citibank Kazakhstan to over

US$150mn as of end 2010 and opening of 2 new Representative Offices in

the Caspian region in 2009,

Citi has proven to be the leading arranger of debt financing for Kazakh issuers - Citi

arranged in total more than US$20bn financing for Kazakh clients during 2005-

2011

Citibank Kazakhstan offers a wide range of products and services: from lending,

transaction services, trade finance and foreign exchange – to derivatives, hedging,

capital markets and custody services

Citibank Kazakhstan takes full advantage of Citi‟s unique banking platforms and

global reach and delivers the best-in-class banking service to its clients in

Kazakhstan with a wide range of comprehensive, most innovative and client-

focused financial solutions

Citi has an in-depth market knowledge of Kazakhstan and well-balanced customer

base with over 380 clients

Citibank Kazakhstan has a banking team of 11 Relationship Managers on the

ground in Kazakhstan, who closely cooperate with London-based Investment

Banking, Debt/ Equity Capital Markets, Treasury and other product and industry

teams

Joint Acquisition of

MangistauMunayGas

Advisor to CNPCI

US$2.6bn

2009

CNPC/ KazMunayGas

Development Bank of

Kazakhstan

Lead Arranger, Lender and

Agent

JBIC Buyer‟s Credit Facility

JPY 3.4bn

2009

Halyk Bank

7.25% due 2021

Joint Bookrunner

US$500mn

2011

Samruk-Energy

Balkhash Thermal

Power Plant Project

Financial Advisor

2011

Kazmunaygas

Kazakhstan Caspian

Transportation System Project

Financial Advisor

2009

Zhaikmunai

10.5% due 2015

Joint Bookrunner

US$450mn

2010

Kazmunaygas

7.0% due 2020

Joint Bookrunner

Eurobond

US$1.5bn

2010

Samruk-Kazyna

“People‟s IPO” Project

Lead Financial

Advisor & Coordinator

2011

Acquisition of 50% of CCPL

(formerly Nations Energy)

from CITIC Group

Advisor to KazMunaiGas EP

US$930mn

2007

Acquisition of

Nations Energy

Adviser to CNOOC

US$2.0bn

2006

Kegoc

“People‟s IPO” Project

Financial

Advisor

2012

Zhaikmunai

10.5% due 2015

Consent Solicitation

2012

4

Key Themes in Global Metals and Mining Industry

Current Macro Uncertainty Has Not Diminished Long-term Views

Theme Comments

Increasing Uncertainty

Rising Price Volatility

Macroeconomic uncertainty / heightened market volatility have impacted real commodity demand

Some indication customers have sought to delay shipments of iron ore and copper in response to falling spot prices

Weakening demand has translated into price declines across commodities

Equity prices seem to be leading commodity prices down although some recent bounce-back

Capex Efficiency /

Shareholder Needs

Long dated projects create significant capex requirements

Shareholders want cash returned in short term vs. significant capex needs of miners

Capital deployment to create shareholder value not just volume

Political Risks Growing as

Focus Increases on

Developing Countries

A significant percentage of the growth pipeline is increasingly reliant on higher political risk jurisdictions

Resource nationalism has been on the rise around the world, resulting in increased threats of both taxation and

incremental nationalisations

Supply Chain /

Procurement Issues

Remain Challenging

Demand for equipment / labour has re-created supply shortages

Key suppliers are remaining cautious in outlook

Increasingly sensitive to customer credit profiles, less inclined to supply smaller or weaker customers

Cost Inflation Will Intensify

Pressure on Projects and

Sponsors

Shortages of key inputs, elevated fuel costs and declining grades drive declining efficiency of capital expenditure

Despite capex levels estimated to be ~70% higher than pre-GFC actual mine output still declining given rising input

costs

Rising input costs likely to continue given supply chain lead times and continued megaproject development

Long-Term Outlook

Remains Strong,

Particularly for Supply-

Challenged Commodities

Chinese demand remains strong

Market conviction on long-term strength remains: copper, aluminium, iron ore demand to double over 15-20 years

Confidence in the supercycle remains largely intact

1

2

3

4

5

6

5

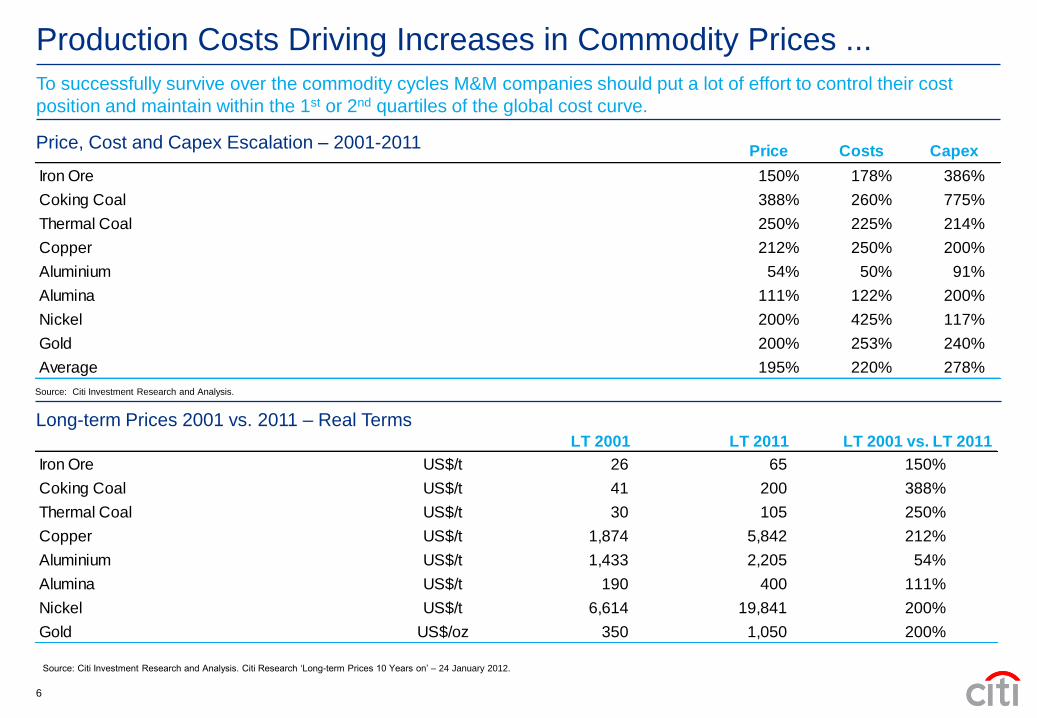

Production Costs Driving Increases in Commodity Prices ...

Price, Cost and Capex Escalation – 2001-2011 Price Costs Capex

Iron Ore 150% 178% 386%

Coking Coal 388% 260% 775%

Thermal Coal 250% 225% 214%

Copper 212% 250% 200%

Aluminium 54% 50% 91%

Alumina 111% 122% 200%

Nickel 200% 425% 117%

Gold 200% 253% 240%

Average 195% 220% 278%

Long-term Prices 2001 vs. 2011 – Real Terms LT 2001 LT 2011 LT 2001 vs. LT 2011

Iron Ore US$/t 26 65 150%

Coking Coal US$/t 41 200 388%

Thermal Coal US$/t 30 105 250%

Copper US$/t 1,874 5,842 212%

Aluminium US$/t 1,433 2,205 54%

Alumina US$/t 190 400 111%

Nickel US$/t 6,614 19,841 200%

Gold US$/oz 350 1,050 200%

Source: Citi Investment Research and Analysis.

Source: Citi Investment Research and Analysis. Citi Research „Long-term Prices 10 Years on‟ – 24 January 2012.

To successfully survive over the commodity cycles M&M companies should put a lot of effort to control their cost

position and maintain within the 1st or 2nd quartiles of the global cost curve.

6

… Without Corresponding Increases in Returns

Project IRR – 2001 vs. 2011

Source: Citi Investment Research and Analysis.

0%

5%

10%

15%

20%

25%

30%

35%

40%

Iron Ore Coking Coal Thermal Coal Copper Aluminium Alumina Nickel Gold

2001 2011

The Long Term commodity prices have on average risen by almost 200% over 2001-2011 period, but IRR for projects

have actually declined on average from 18% to 16%.

7

… and with Significantly Higher Capex Requirements

Going forward, the mining companies are expected to spend more on capex over the next five years then they have

in the past twenty years.

Global capex – Metals and Mining Citi coverage

According to Citi Research calculations, the Return on Incremental Invested Capital (ROIIC) will be significantly below vs. the currently enjoyed by the mining

sector

The mining sector bought earnings momentum through M&A from the period between 2006 and 2008, and the mining sector is now buying earnings

momentum through unprecedented capex spend

Source: Citi Investment Research and Analysis.

0

50,000

100,000

150,000

200,000

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011E 2012E 2013E 2014E

North America Australia Latin America EMEA Asia Europe

8

Company 2009 2010 2011

38.2% 48.4% 44.3%

n/a 43.9% 38.1%

50.4% 59.7% 55.0%

EBITDA margins

Stable Margins but Significant Challenges to Sustain Them Margins for the mining industry peaked around 2006 and have subsequently fallen but have remained relatively

stable. M&M Companies estimate that the returns will continue to be at the current levels in the years to come,

however there are significant factors that might challenge / compress the margins.

Global metals and mining sector margins

Going forward we expect further margin compression coming from higher depreciation costs, higher operating costs, higher oil

prices, higher exchange rates, higher capex costs and higher salaries, all this suggests that margins will continue to come under

pressure

Significant downward

pressure

Source: Citi Investment Research and Analysis.

0%

5%

10%

15%

20%

25%

30%

35%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012E2013E2014E

EBITDA Margins EBIT Margins

9

Resource Funding of Global M&M Universe

Capital Structure Evolution

Ready Access / Execution Intermediate Access /

Execution

No Access

Life-Cycle Stage Exploration Development Emerging

Producer

Established

Producer

By Market

Equity

Hybrid Capital

Convertible Bond

Bond

Bank - Project

Finance

Bank - Revolving

Credit Facility

Commodity Finance

Transaction Services

10

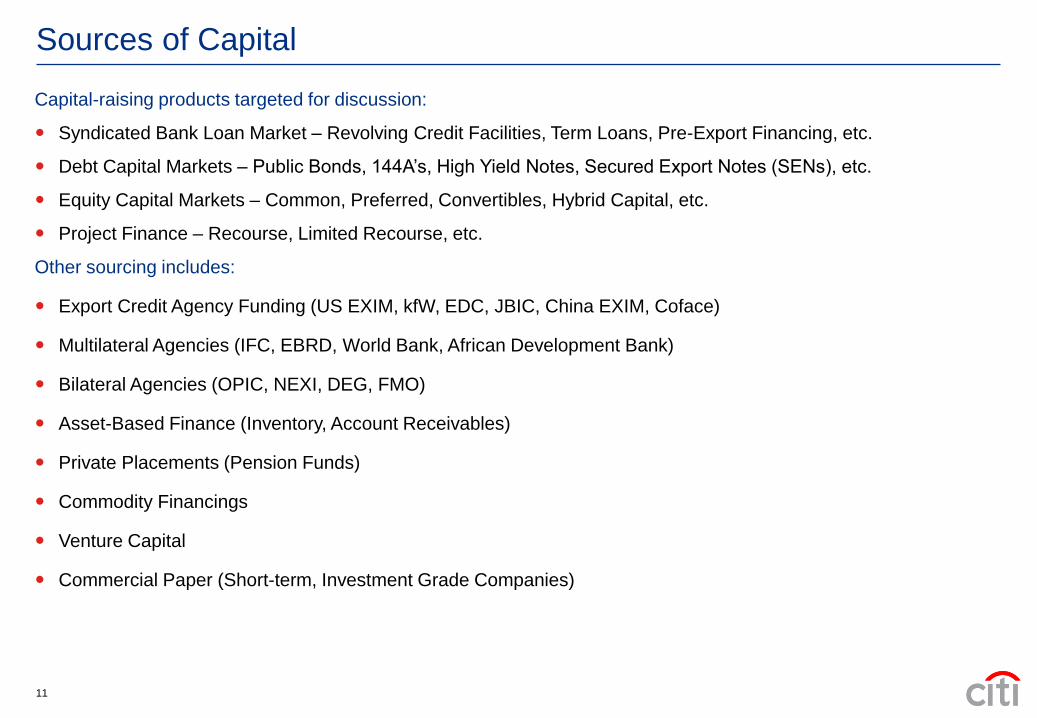

Sources of Capital

Capital-raising products targeted for discussion:

Syndicated Bank Loan Market – Revolving Credit Facilities, Term Loans, Pre-Export Financing, etc.

Debt Capital Markets – Public Bonds, 144A‟s, High Yield Notes, Secured Export Notes (SENs), etc.

Equity Capital Markets – Common, Preferred, Convertibles, Hybrid Capital, etc.

Project Finance – Recourse, Limited Recourse, etc.

Other sourcing includes:

Export Credit Agency Funding (US EXIM, kfW, EDC, JBIC, China EXIM, Coface)

Multilateral Agencies (IFC, EBRD, World Bank, African Development Bank)

Bilateral Agencies (OPIC, NEXI, DEG, FMO)

Asset-Based Finance (Inventory, Account Receivables)

Private Placements (Pension Funds)

Commodity Financings

Venture Capital

Commercial Paper (Short-term, Investment Grade Companies)

11

Situation in The European Banking System

Significant Risk of Global Contagion

682

519

374

189139

9967 53

0

100

200

300

400

500

600

700

800

FRAN GER UK US SPN JPN SWTZ ITLY

Ban

k E

xp

osu

re t

o G

IIP

S, $B

n

Greece

Portugal

Ireland

Spain

Italy

Current Eurozone stress is believed to be putting tremendous funding pressure on European banks, especially those

domiciled in impaired sovereigns

Even in non-breakup scenarios, European banks may need incremental capital of €100-330Bn(1)

In the event of a Eurozone break-up, the impact of incremental FX-linked asset write downs as well as broader economic

spillover effects could cause global financial market distress comparable to the post-Lehman period

A number of European banks could find USD funding challenging – and worse in the event of a break-up

Significant Capital Needs for European Banks

0

70

140

210

280

€350

GRC, IRE,

PORT Banks

ITLY and SPN

Banks

GER, AUS, FIN,

NETHS

Other EM U Banks of

Europe ex EM U

All European

Banks

A. EBA Oct 26 M ark to M arket of sov'n debt

B. Case A + 10% writedown for private exposure to GRC, 5% in IRE and PORT

C. Case B + 1% writedown on exposure to EU private sector ex GRC, IRE, PORT

D. Case C + 10% writedown on sov'n debt of GRC, PORT, IRE, FRAN, ITLY, SPN, BELG

Source: BIS. The data is reported on consolidated foreign claims that are not adjusted for risk mitigants

(guarantees and collateral) vis-à-vis individual countries by nationality of reporting banks. Data as of 06/2011. Source: Source: CIRA, EBA.

(1) Capital estimates are based on the target Core Tier 1 Ratio of 9%.

Historically European banks have been very active in funding of Metals & Mining industry across CIS. However they

now face funding pressure on the back of Eurozone crisis.

12

Russian and Chinese Banks Advancing in Kazakhstan

On the back of European banks‟ problems as well as troubling quality of Kazakh banks‟ assets, Chinese and Russian

banks become more aggressive and increase their presence in Kazakhstan.

Quality of assets in Kazakhstan‟s banking sector, %

0

10

20

30

40

50

60

70

80

90

100

Jan2007

Jan2008

Jan2009

Jan2010

Jan2011

Jan2012

May2012

Standard Doubtful Loss

Kazakhstan‟s banking system faces difficulties with the asset

quality and decreased profitability

Moody‟s outlook on Kazakhstan's banking system remains

negative. The agency says that most of problematic loans are

unlikely to recover and will have to be written off

Kazakh banks' total provisions for loan-loss reserves stood at

32% of gross loans at year-end 2011 and these reserves are

insufficient to cover all expected losses

Kazakhstan‟s authorities are trying to provide support for its

lenders to compete with the local units of foreign banks that

receive funding and balance sheet support from their parent

institutions.

“Foreign banks shouldn‟t control over 30 percent of the

financial services in Kazakhstan”, Mr. Nazarbayev said recently

On the back of Kazakh banks difficulties as well as problems in

Eurozone, Chinese and Russian banks become more

aggressive and increase their presence in Kazakhstan

Russian state-run Sberbank‟s unit became the 6th largest

lender by assets in Kazakhstan with market share of 4.8% as

of May 2012, while it was the 8th largest a year earlier

23.4%

76.6%

Total assets split in Kazakhstan‟s banking system, %

Jan 2010

30.8%

69.2%

Jan 2012

Source: Committee for The Control and Supervision of The Financial Organizations of

The National Bank of The Republic of Kazakhstan. 13

Domestic banks Foreign banks

Disclaimer

© 2012 Citigroup Global Markets Limited. Authorized and regulated by the Financial Services Authority. All rights reserved. Citi and Citi and Arc Design are trademarks and service marks of Citigroup Inc. or its affiliates and are used

and registered throughout the world.

IRS Circular 230 Disclosure: Citigroup Inc. and its affiliates do not provide tax or legal advice. Any discussion of tax matters in these materials (i) is not intended or written to be used, and cannot be used or relied

upon, by you for the purpose of avoiding any tax penalties and ( ii) may have been written in connection with the "promotion or m arketing" of any transaction contemplated hereby ("Transaction") . Accordingly, you

should seek advice based on your particular circumstances from an independent tax advisor.

Any terms set forth herein are intended for discussion purposes only and are subject to the final terms as set forth in separate definitive written agreements. This presentation is not a comm itment to lend, syndicate a financing,

underwrite or purchase securities, or commit capital nor does it obligate us to enter into such a commitment, nor are we acting as a fiduciary to you. By accepting this presentation, subject t o applicable law or regulation, you agree to

keep confidential the information contained herein and the exist ence of and proposed terms for any Transaction.

Prior to entering into any Transaction, you should determine, wi thout reliance upon us or our affiliates, the economic risks and merits (and independently determine that you are able to assume these risks) as well as the legal, tax and

accounting characterizations and consequences of any such Transa ction. In this regard, by accepting this presentation, you ackn owledge that (a) we are not in the business of providing (and yo u are not relying on us for) legal, tax or

accounting advice, (b) there may be legal, tax or accounting ris ks associated with any Transaction, (c) you should receive (and rely on) separate and qualified legal, tax and accounting advice and (d) you should apprise senior

management in your organization as to such legal, tax and accoun ting advice (and any risks associated with any Transaction) and our disclaimer as to these matters. By acceptance of these mate rials, you and we hereby agree that

from the commencement of discussions with respect to any Transac tion, and notwithstanding any other provision in this presentati on, we hereby confirm that no participant in any Transaction sha ll be limited from disclosing the U.S. tax

treatment or U.S. tax structure of such Transaction.

We are required to obtain, verify and record certain information that identifies each entity that enters into a formal business relationship with us. We will ask for your complete name, stree t address, and taxpayer ID number. We may

also request corporate formation documents, or other forms of id entification, to verify information provided.

Any prices or levels contained herein are preliminary and indica tive only and do not represent bids or offers. These indications are provided solely for your information and consideration, ar e subject to change at any time without notice

and are not intended as a solicitation with respect to the purch ase or sale of any instrument. The information contained in thi s presentation may include results of analyses from a quantitati ve model which represent potential future

events that may or may not be realized, and is not a complete an alysis of every material fact representing any product. Any est imates included herein constitute our judgment as of the date he reof and are subject to change without

any notice. We and/or our affiliates may make a market in these instruments for our customers and for our own account. Accordi ngly, we may have a position in any such instrument at any time.

Although this material may contain publicly available informatio n about Citi corporate bond research, fixed income strategy or e conomic and market analysis, Citi policy (i) prohibits employees from offering, directly or indirectly, a

favorable or negative research opinion or offering to change an opinion a s consideration or inducement for the receipt of business or for compensation; and (ii) prohibits analysts from being compensate d for specific recommendations

or views contained in research reports. So as to reduce the pot ential for conflicts of interest, as well as to reduce any appea rance of conflicts of interest, Citi has enacted policies and procedures designed to limit communications

between its investment banking and research personnel to specifi cally prescribed circumstances.

![New E-Books January 2016 - European University Institute · # 59 The burdens of empire [electronic resource] : 1539 to the present / Anthony Pagden Pagden, Anthony Cambridge : Cambridge](https://static.fdocuments.net/doc/165x107/5ec0d2bb16a9b179cf12bf2d/new-e-books-january-2016-european-university-institute-59-the-burdens-of-empire.jpg)

![[Anthony Pagden (Ed.)] the Languages of Political](https://static.fdocuments.net/doc/165x107/54509996af795903098b4dba/anthony-pagden-ed-the-languages-of-political.jpg)