3. planning feb 2014

24

BY Atta-ur-Rahman Arif

-

Upload

syed-osama-rizvi -

Category

Education

-

view

49 -

download

0

Transcript of 3. planning feb 2014

BY

Atta-ur-Rahman Arif

MEANINGAction to be taken by an auditor, inrespect of any particular field ofverification and reporting, shouldbe so design that it may enable himto conduct an audit moreeffectively.

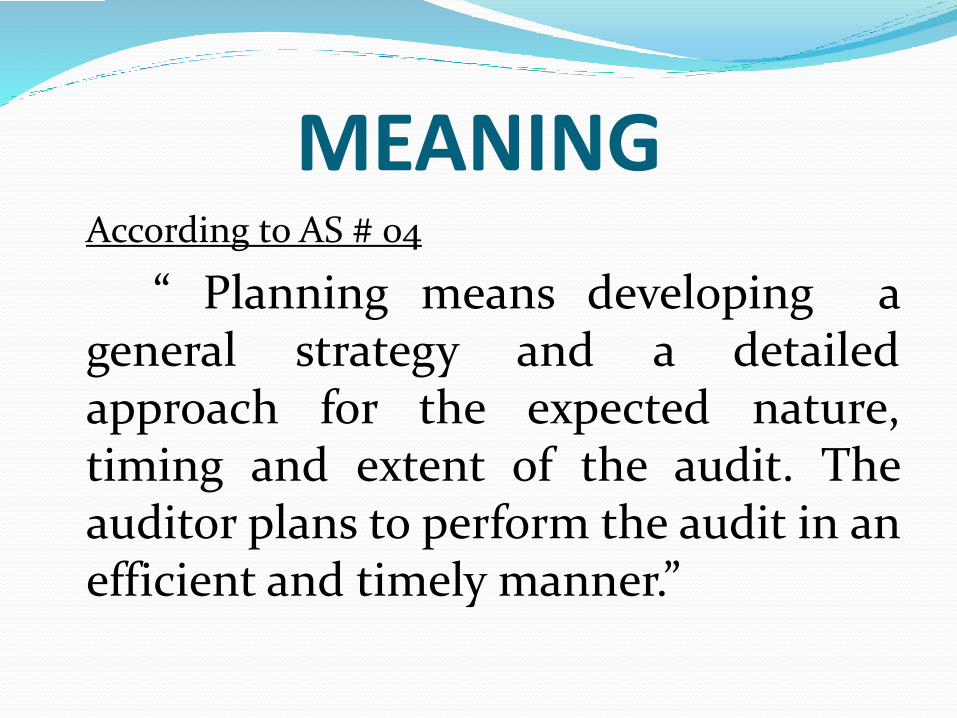

MEANINGAccording to AS # 04

“ Planning means developing ageneral strategy and a detailedapproach for the expected nature,timing and extent of the audit. Theauditor plans to perform the audit in anefficient and timely manner.”

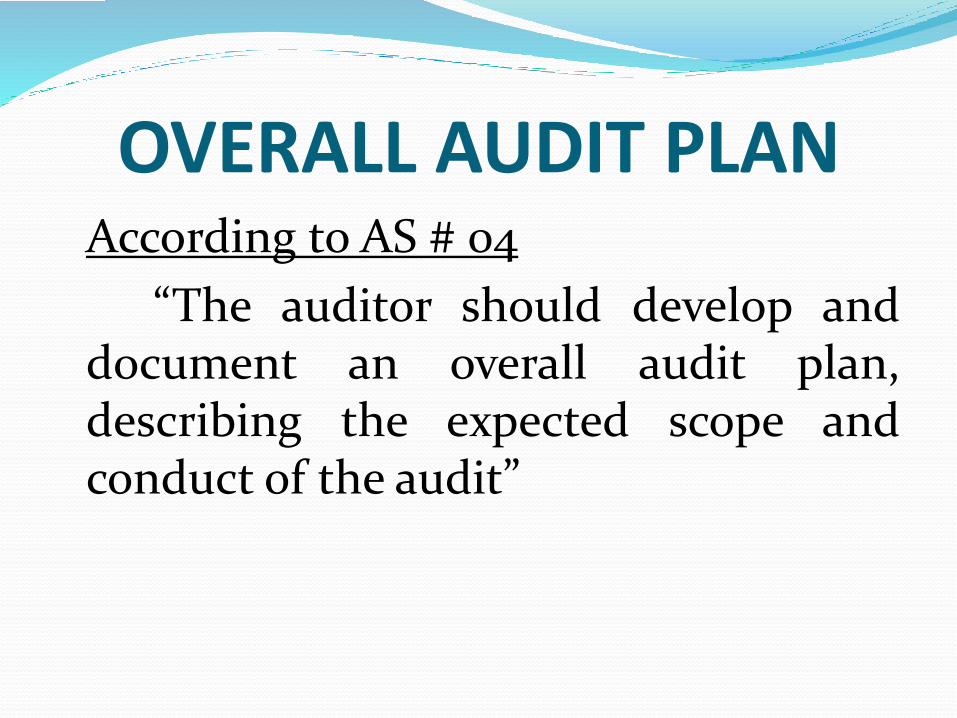

OVERALL AUDIT PLANAccording to AS # 04

“The auditor should develop anddocument an overall audit plan,describing the expected scope andconduct of the audit”

6-5

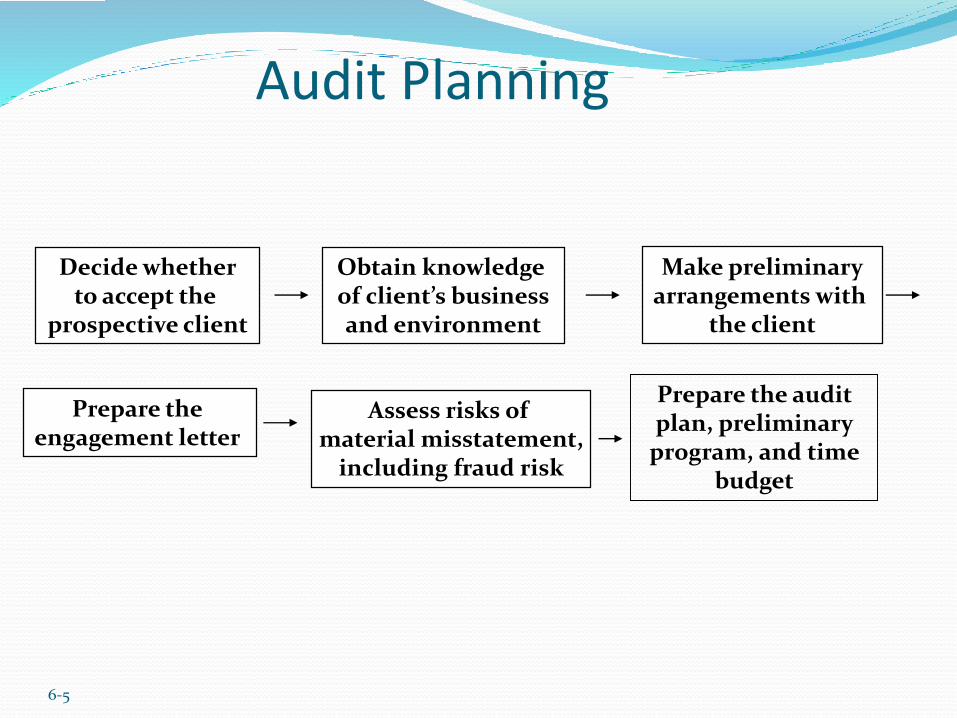

Audit Planning

Decide whetherto accept the

prospective client

Obtain knowledge of client’s businessand environment

Make preliminaryarrangements with

the client

Prepare the engagement letter

Assess risks of material misstatement,

including fraud risk

Prepare the audit plan, preliminary

program, and time budget

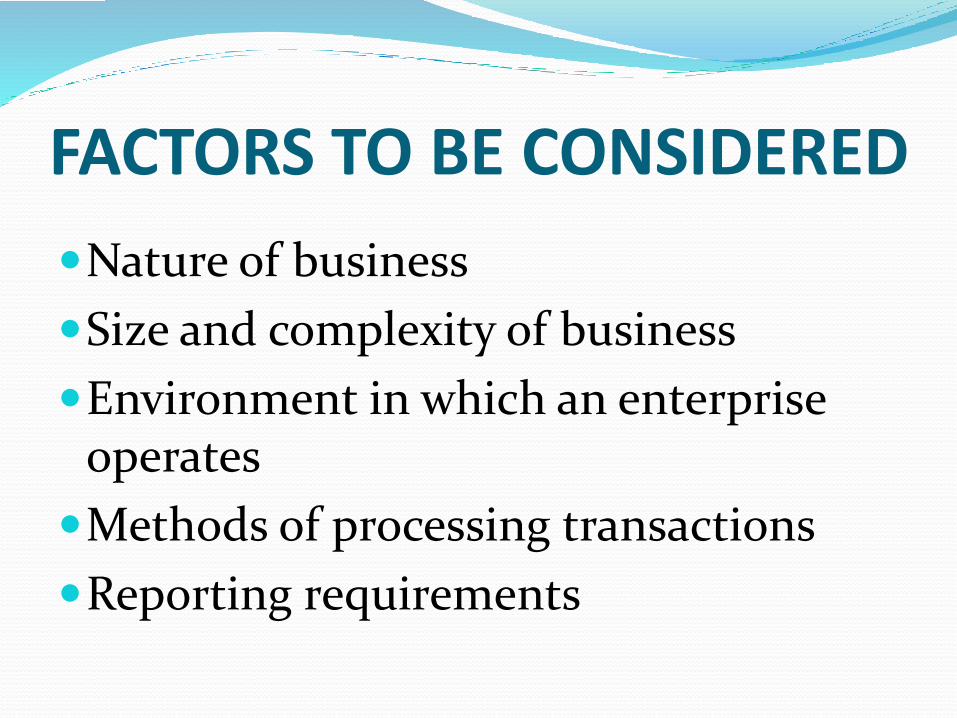

FACTORS TO BE CONSIDERED

Nature of business

Size and complexity of business

Environment in which an enterprise operates

Methods of processing transactions

Reporting requirements

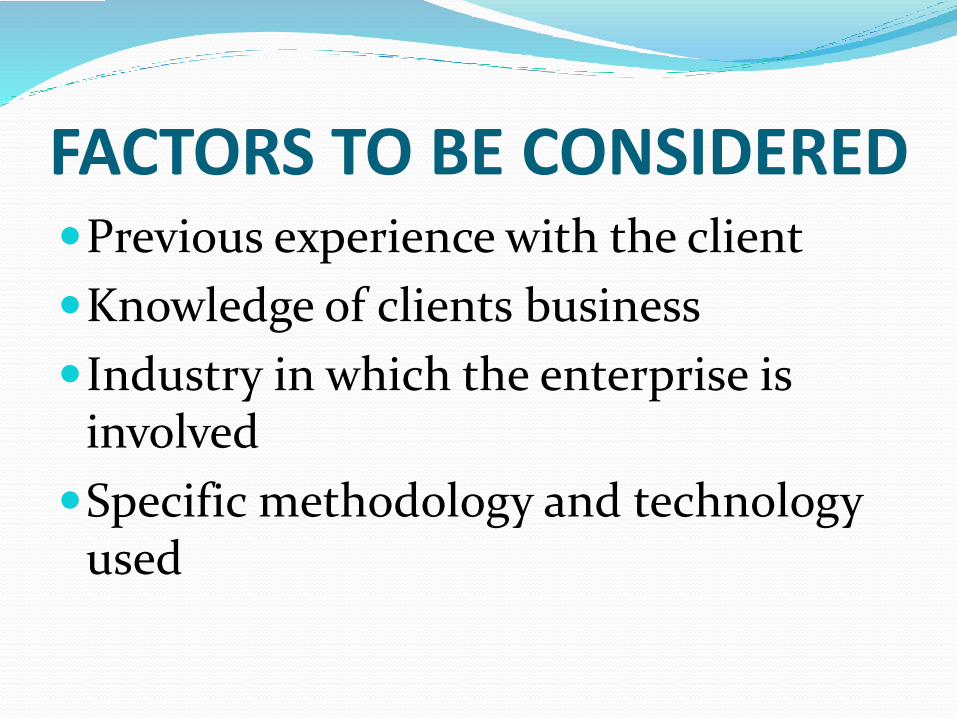

Previous experience with the client

Knowledge of clients business

Industry in which the enterprise is involved

Specific methodology and technology used

FACTORS TO BE CONSIDERED

6-8

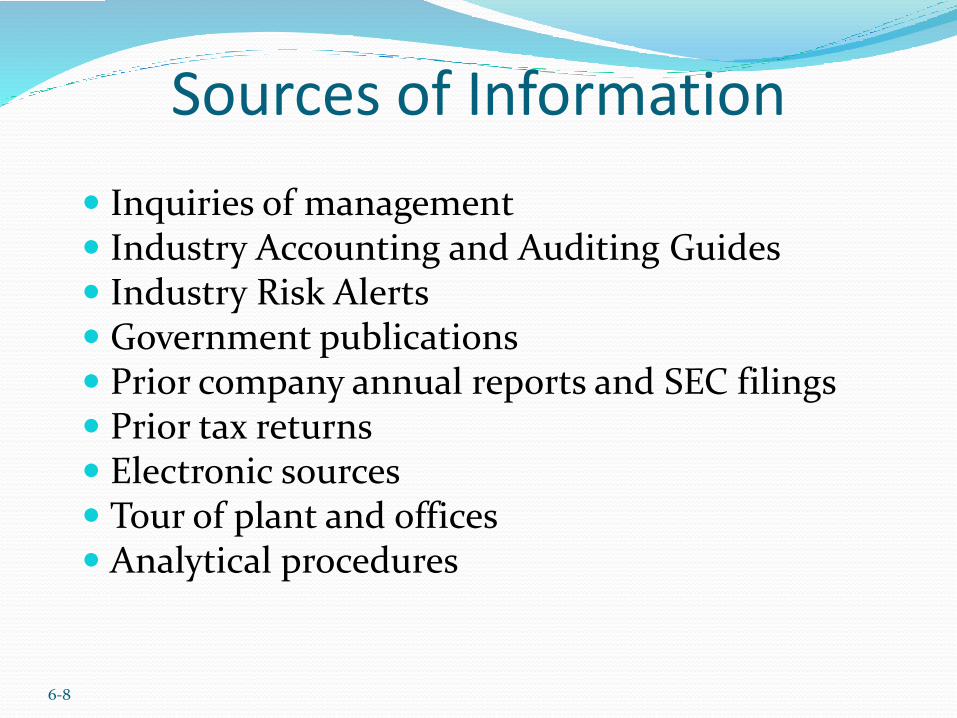

Sources of Information

Inquiries of management Industry Accounting and Auditing Guides Industry Risk Alerts Government publications Prior company annual reports and SEC filings Prior tax returns Electronic sources Tour of plant and offices Analytical procedures

6-9

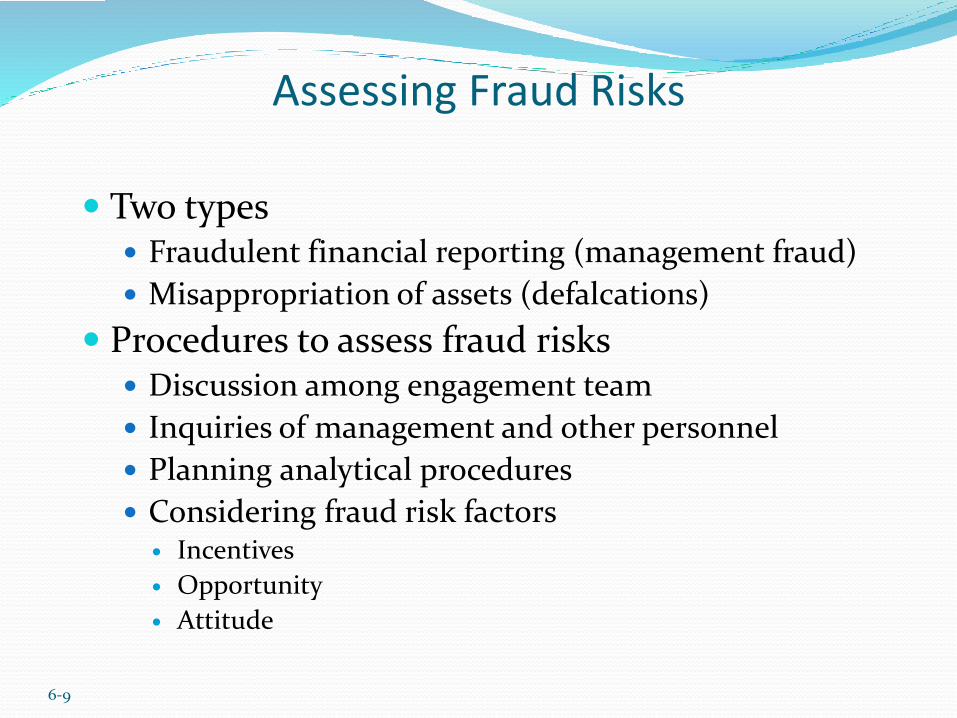

Assessing Fraud Risks

Two types Fraudulent financial reporting (management fraud)

Misappropriation of assets (defalcations)

Procedures to assess fraud risks Discussion among engagement team

Inquiries of management and other personnel

Planning analytical procedures

Considering fraud risk factors Incentives

Opportunity

Attitude

PLANNING PROCEDUREAudit planning is a continuous process and can be classified into following stages:

1. Sound knowledge regarding business of client

2. Developing an overall audit plan

3. Implementation the audit plan through audit programme

4. Updating the audit plan according to the changes

5. Post audit planning review in form of suggestions

KEY MATTERS KNOWLEDGE OF THE BUSINESS

General economic factors and industryaffecting the entity’s business.

Important characteristics of entity likebusiness, financial performance andreporting requirements including changessince the last audit.

General level of competence ofmanagement

KNOWLEDGE OF THE BUSINESS Auditor should obtain knowledge of

Annual accounts to shareholders

Minutes of Shareholders, directors and Committees

Internal financial reports

Previous year’s working papers

Discussion with client’s management and staff

Policy, accounting and management manuals

Government policies and their impact on business

Visits of client premises and plants

Overall Audit StrategyACCOUNTING AND INETRNAL CONTROL SYSTEM

Understanding the accounting policies and changes in those policies.

The effect of new auditing or accounting pronouncements.

Sound knowledge of internal control system especially on test of control and substantive procedures.

Overall Audit StrategyRISK AND MATERIALITY

Expected assessment of inherent andcontrol risks.

Identification of significant audit areas.

Setting of materiality level for auditpurposes.

Possibility of material misstatement,including the experience of past periodsor fraud.

Overall Audit StrategyNATURE, TIMING AND EXTENT OF PROCEDURE

Possible changes of emphasis on specificaudit areas.

Effect of information technology on theaudit.

Work of internal auditing and itsexpected effect on external auditing.

Overall Audit StrategyCOORDINATION AND REVIEW

Involvement of other auditors in the audit of components for example subsidiaries, branches and divisions.

Involvement of experts.

Staffing requirements.

Number of locations.

Overall Audit StrategyOTHER MATTERS

Possibility that the going concernassumption may be subject to question.

Conditions requiring special attention,such as the existence of related parties.

The terms of engagement and thestatutory responsibilities.

The nature and timing of reports.

DOCUMENTATION OF PLANAuditor should document his plan in

the end of the first stage of planning.

Form and extent of document dependupon the size of each individual audit.

Auditor should follow time tableshowing allocated hours for each auditprocedures.

AUDIT TIMETABLEAuditor should document an overall audit

timetable setting out the dates agreed withthe client for the commencement and thecompletion of audit.

Make provision for phasing the audit overthe year instead of carrying out the entireaudit work at year end.

ADJUSTMENT OF PLANNING Auditor should be continuously amendable to

circumstances with which he is confrontedduring audit.

The errors noticed, should be given dueconsideration as all these greatly influence theaudit plan.

Should extend the scope of audit by increasingthe number of samples in the test if the errorsor fraud has been found

Specific Planning Area Time Budgeting

Staff Planning

Client’s work Support

Extent of reliance over internal control

Meetings with tax and finance department

Joint audit of sectional audit

Work performed by distant offices

BENEFITS OF PLANNING Appropriate attention to important areas of

audit.

Prompt identification of potential problems.

Expeditious completion of task by exercisingproper control and timing.

Proper utilization of audit force available.

Effective coordination of audit assignment.

Review of field work by seniors becomessimplified and speedy.

Advantages of Planning1. Progress monitor is easy

2. Uniformity in audit work

3. Division of work made easy

4. Responsibility can easily be fixed when divided properly

5. Final review made easy

Disadvantages of Planning Audit staff loose their initiative and interest

Audit program may not cover each and every aspect

Audit became too mechanical

Rigidity in audit work unless the program not frequently reviewed and modified