3 May 2013 Jet Airways (India) Limited Extra-ordinary ...India)Ltd-EGM-24May13... · Voting...

12

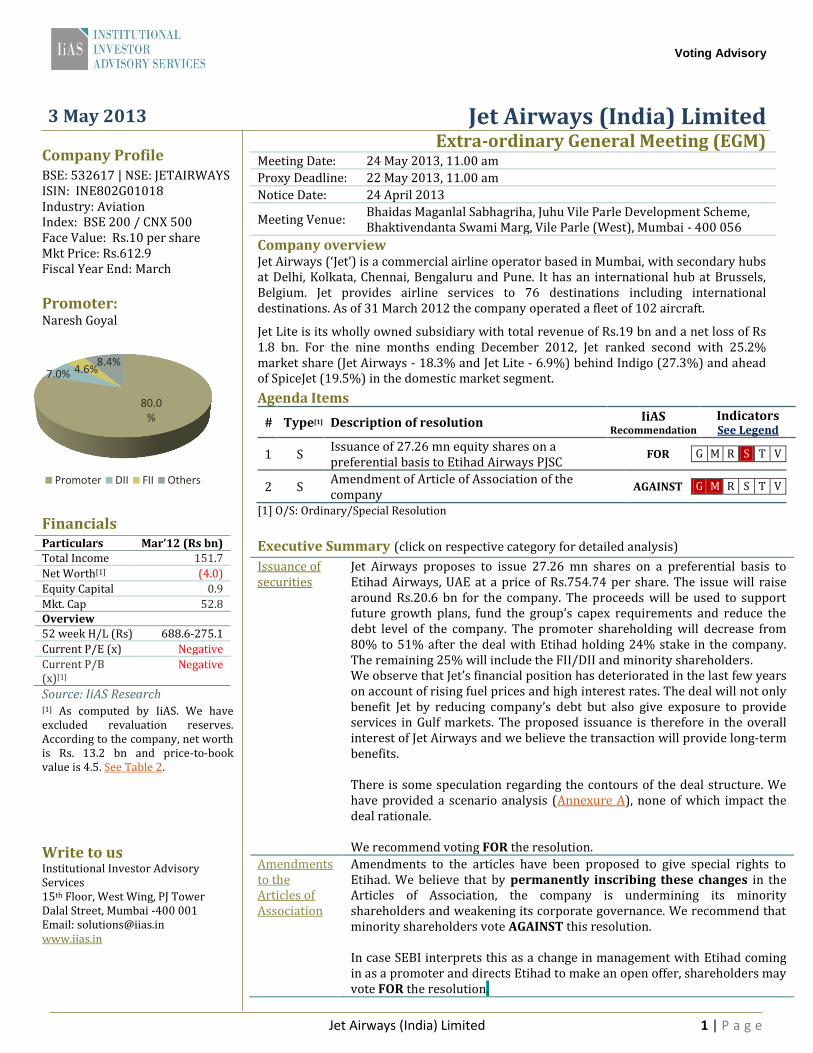

Voting Advisory Jet Airways (India) Limited 1 | Page 3 May 2013 Jet Airways (India) Limited Company Profile BSE: 532617 | NSE: JETAIRWAYS ISIN: INE802G01018 Industry: Aviation Index: BSE 200 / CNX 500 Face Value: Rs.10 per share Mkt Price: Rs.612.9 Fiscal Year End: March Promoter: Naresh Goyal Financials Particulars Mar’12 (Rs bn) Total Income 151.7 Net Worth [1] (4.0) Equity Capital 0.9 Mkt. Cap 52.8 Overview 52 week H/L (Rs) 688.6-275.1 Current P/E (x) Negative Current P/B (x) [1] Negative Source: IiAS Research [1] As computed by IiAS. We have excluded revaluation reserves. According to the company, net worth is Rs. 13.2 bn and price-to-book value is 4.5. See Table 2. Write to us Institutional Investor Advisory Services 15 th Floor, West Wing, PJ Tower Dalal Street, Mumbai -400 001 Email: [email protected] www.iias.in Extra-ordinary General Meeting (EGM) Meeting Date: 24 May 2013, 11.00 am Proxy Deadline: 22 May 2013, 11.00 am Notice Date: 24 April 2013 Meeting Venue: Bhaidas Maganlal Sabhagriha, Juhu Vile Parle Development Scheme, Bhaktivendanta Swami Marg, Vile Parle (West), Mumbai - 400 056 Company overview Jet Airways (‘Jet’) is a commercial airline operator based in Mumbai, with secondary hubs at Delhi, Kolkata, Chennai, Bengaluru and Pune. It has an international hub at Brussels, Belgium. Jet provides airline services to 76 destinations including international destinations. As of 31 March 2012 the company operated a fleet of 102 aircraft. Jet Lite is its wholly owned subsidiary with total revenue of Rs.19 bn and a net loss of Rs 1.8 bn. For the nine months ending December 2012, Jet ranked second with 25.2% market share (Jet Airways - 18.3% and Jet Lite - 6.9%) behind Indigo (27.3%) and ahead of SpiceJet (19.5%) in the domestic market segment. Agenda Items # Type [1] Description of resolution IiAS Recommendation Indicators See Legend 1 S Issuance of 27.26 mn equity shares on a preferential basis to Etihad Airways PJSC FOR G M R S T V 2 S Amendment of Article of Association of the company AGAINST G M R S T V [1] O/S: Ordinary/Special Resolution Executive Summary (click on respective category for detailed analysis) Issuance of securities Jet Airways proposes to issue 27.26 mn shares on a preferential basis to Etihad Airways, UAE at a price of Rs.754.74 per share. The issue will raise around Rs.20.6 bn for the company. The proceeds will be used to support future growth plans, fund the group’s capex requirements and reduce the debt level of the company. The promoter shareholding will decrease from 80% to 51% after the deal with Etihad holding 24% stake in the company. The remaining 25% will include the FII/DII and minority shareholders. We observe that Jet’s financial position has deteriorated in the last few years on account of rising fuel prices and high interest rates. The deal will not only benefit Jet by reducing company’s debt but also give exposure to provide services in Gulf markets. The proposed issuance is therefore in the overall interest of Jet Airways and we believe the transaction will provide long-term benefits. There is some speculation regarding the contours of the deal structure. We have provided a scenario analysis (Annexure A), none of which impact the deal rationale. We recommend voting FOR the resolution. Amendments to the Articles of Association Amendments to the articles have been proposed to give special rights to Etihad. We believe that by permanently inscribing these changes in the Articles of Association, the company is undermining its minority shareholders and weakening its corporate governance. We recommend that minority shareholders vote AGAINST this resolution. In case SEBI interprets this as a change in management with Etihad coming in as a promoter and directs Etihad to make an open offer, shareholders may vote FOR the resolution. 80.0 % 7.0% 4.6% 8.4% Promoter DII FII Others

Transcript of 3 May 2013 Jet Airways (India) Limited Extra-ordinary ...India)Ltd-EGM-24May13... · Voting...

Voting Advisory

Jet Airways (India) Limited 1 | P a g e

3 May 2013 Jet Airways (India) Limited

Company Profile BSE: 532617 | NSE: JETAIRWAYS ISIN: INE802G01018 Industry: Aviation Index: BSE 200 / CNX 500 Face Value: Rs.10 per share Mkt Price: Rs.612.9 Fiscal Year End: March

Promoter: Naresh Goyal

Financials Particulars Mar’12 (Rs bn) Total Income 151.7

Net Worth[1] (4.0)

Equity Capital 0.9

Mkt. Cap 52.8 Overview 52 week H/L (Rs) 688.6-275.1

Current P/E (x) Negative

Current P/B (x)[1]

Negative

Source: IiAS Research [1] As computed by IiAS. We have excluded revaluation reserves. According to the company, net worth is Rs. 13.2 bn and price-to-book value is 4.5. See Table 2.

Write to us Institutional Investor Advisory Services 15th Floor, West Wing, PJ Tower Dalal Street, Mumbai -400 001 Email: [email protected] www.iias.in

Extra-ordinary General Meeting (EGM) Meeting Date: 24 May 2013, 11.00 am

Proxy Deadline: 22 May 2013, 11.00 am

Notice Date: 24 April 2013

Meeting Venue: Bhaidas Maganlal Sabhagriha, Juhu Vile Parle Development Scheme, Bhaktivendanta Swami Marg, Vile Parle (West), Mumbai - 400 056

Company overview Jet Airways (‘Jet’) is a commercial airline operator based in Mumbai, with secondary hubs at Delhi, Kolkata, Chennai, Bengaluru and Pune. It has an international hub at Brussels, Belgium. Jet provides airline services to 76 destinations including international destinations. As of 31 March 2012 the company operated a fleet of 102 aircraft.

Jet Lite is its wholly owned subsidiary with total revenue of Rs.19 bn and a net loss of Rs 1.8 bn. For the nine months ending December 2012, Jet ranked second with 25.2% market share (Jet Airways - 18.3% and Jet Lite - 6.9%) behind Indigo (27.3%) and ahead of SpiceJet (19.5%) in the domestic market segment.

Agenda Items

# Type[1] Description of resolution IiAS Recommendation

Indicators See Legend

1 S Issuance of 27.26 mn equity shares on a preferential basis to Etihad Airways PJSC

FOR G M R S T V

2 S Amendment of Article of Association of the company

AGAINST G M R S T V

[1] O/S: Ordinary/Special Resolution

Executive Summary (click on respective category for detailed analysis) Issuance of securities

Jet Airways proposes to issue 27.26 mn shares on a preferential basis to Etihad Airways, UAE at a price of Rs.754.74 per share. The issue will raise around Rs.20.6 bn for the company. The proceeds will be used to support future growth plans, fund the group’s capex requirements and reduce the debt level of the company. The promoter shareholding will decrease from 80% to 51% after the deal with Etihad holding 24% stake in the company. The remaining 25% will include the FII/DII and minority shareholders. We observe that Jet’s financial position has deteriorated in the last few years on account of rising fuel prices and high interest rates. The deal will not only benefit Jet by reducing company’s debt but also give exposure to provide services in Gulf markets. The proposed issuance is therefore in the overall interest of Jet Airways and we believe the transaction will provide long-term benefits. There is some speculation regarding the contours of the deal structure. We have provided a scenario analysis (Annexure A), none of which impact the deal rationale. We recommend voting FOR the resolution.

Amendments to the Articles of Association

Amendments to the articles have been proposed to give special rights to Etihad. We believe that by permanently inscribing these changes in the Articles of Association, the company is undermining its minority shareholders and weakening its corporate governance. We recommend that minority shareholders vote AGAINST this resolution. In case SEBI interprets this as a change in management with Etihad coming in as a promoter and directs Etihad to make an open offer, shareholders may vote FOR the resolution.

80.0%

7.0% 4.6% 8.4%

Promoter DII FII Others

Voting Advisory

Jet Airways (India) Limited 2 | P a g e

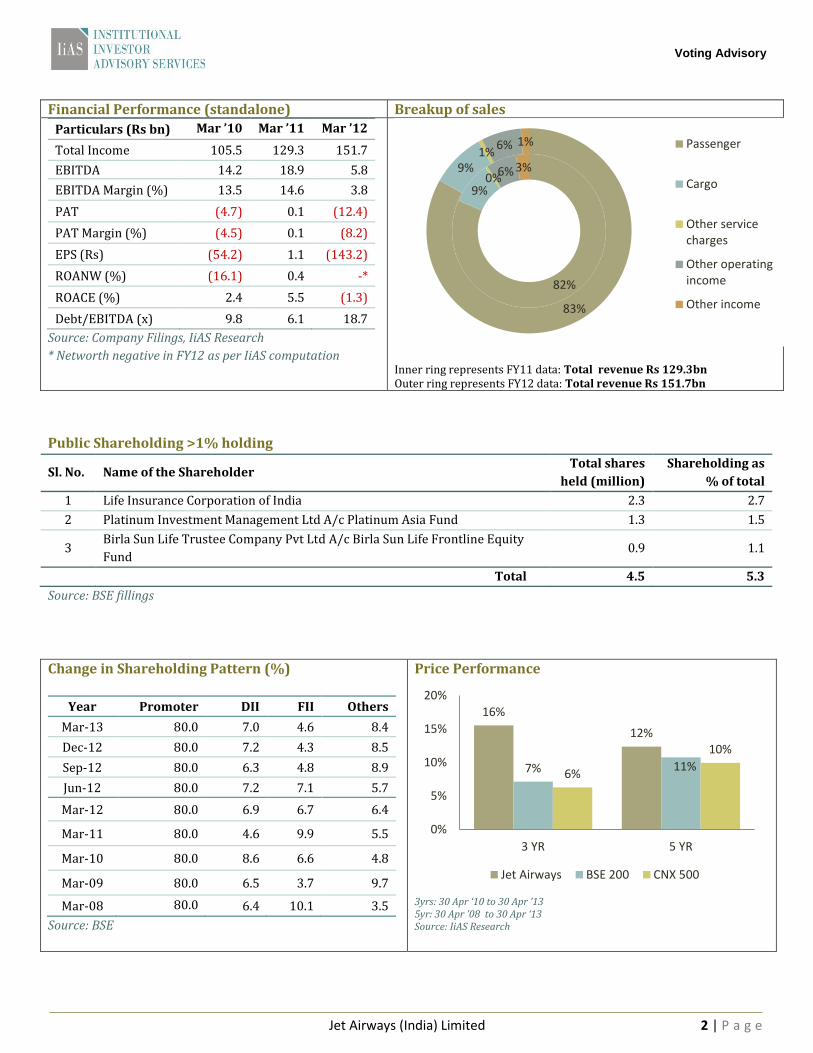

Financial Performance (standalone) Breakup of sales

Particulars (Rs bn) Mar ’10 Mar ’11 Mar ’12

Total Income 105.5 129.3 151.7

EBITDA 14.2 18.9 5.8

EBITDA Margin (%) 13.5 14.6 3.8

PAT (4.7) 0.1 (12.4)

PAT Margin (%) (4.5) 0.1 (8.2)

EPS (Rs) (54.2) 1.1 (143.2)

ROANW (%) (16.1) 0.4 -*

ROACE (%) 2.4 5.5 (1.3)

Debt/EBITDA (x) 9.8 6.1 18.7

Source: Company Filings, IiAS Research

* Networth negative in FY12 as per IiAS computation

Inner ring represents FY11 data: Total revenue Rs 129.3bn Outer ring represents FY12 data: Total revenue Rs 151.7bn

Public Shareholding >1% holding

Sl. No. Name of the Shareholder Total shares

held (million)

Shareholding as

% of total

1 Life Insurance Corporation of India 2.3 2.7

2 Platinum Investment Management Ltd A/c Platinum Asia Fund 1.3 1.5

3 Birla Sun Life Trustee Company Pvt Ltd A/c Birla Sun Life Frontline Equity

Fund 0.9 1.1

Total 4.5 5.3

Source: BSE fillings

Change in Shareholding Pattern (%)

Year Promoter DII FII Others

Mar-13 80.0 7.0 4.6 8.4

Dec-12 80.0 7.2 4.3 8.5

Sep-12 80.0 6.3 4.8 8.9

Jun-12 80.0 7.2 7.1 5.7

Mar-12 80.0 6.9 6.7 6.4

Mar-11 80.0 4.6 9.9 5.5

Mar-10 80.0 8.6 6.6 4.8

Mar-09 80.0 6.5 3.7 9.7

Mar-08 80.0 6.4 10.1 3.5

Source: BSE

Price Performance

3yrs: 30 Apr ‘10 to 30 Apr ‘13 5yr: 30 Apr ’08 to 30 Apr ‘13 Source: IiAS Research

82%

9% 0% 6% 3%

83%

9% 1%

6% 1% Passenger

Cargo

Other servicecharges

Other operatingincome

Other income

16%

12%

7% 11% 6%

10%

0%

5%

10%

15%

20%

3 YR 5 YR

Jet Airways BSE 200 CNX 500

There are two possibilities

depending on the interpretation of

control

• Option 1: No Open Offer. Control of Jet Airways is

deemed to be unchanged. Etihad need not have to make an open offer.

• Option 2: Open offer. Etihad is interpreted to gain

significant control. It is forced to make an open offer.

Voting Advisory

Jet Airways (India) Limited 3 | P a g e

Category: Issuance of securities

IiAS Evaluation Parameters for Issuance of Securities Parameter Result Risk Level Details

Are these being issued to the promoter? No -

Is the allottee a current shareholder/stakeholder in the company? No -

What is the dilution for minority shareholders? - -

Have the reasons for fund-raising been clearly disclosed? Yes -

IiAS Recommendation FOR

Discussion

In order to raise additional capital to fund the operations of the company, Jet Airways seeks to issue upto 27.3 mn equity shares, each having a face value of Rs.10, on a preferential basis to Etihad Airways PJSC (see Box1). The relevant date fixed was 24 April 2013 and accordingly the issue will be priced at around Rs.754.7 per share. The company is therefore expected to raise an aggregate amount of Rs.20.6 bn from the issue.

Box1: Details of Jet Airways’ strategic partnership with Etihad

Etihad, the national carrier of UAE, has agreed to subscribe to 27.2 bn new shares in Jet Airways at a price of Rs.754.74 per share. The value of this equity investment is $379 mn (Rs 20.6 bn) and will result in Etihad Airways holding 24 % of the expanded share capital of Jet Airways. Over the span of 18-20 months ending April 2013, Etihad invested not just in Jet, but also in other international carriers (Air Berlin (nearly 30%), Air Seychelles (40%) and Virgin Australia (10%)).

According to media reports, Etihad has also committed to inject $220 mn to create and strengthen an extended partnership between the two carriers. As part of the deal, Etihad will invest an additional $150m in Jet's frequent flyer program “Jet Privilege’. It has already spent $70m to buy Jet's three pairs of Heathrow slots through a sale and leaseback agreement announced earlier this year (FY13).

Under the strategic partnership, the airlines will gradually expand existing operations and introduce new routes between India and Abu Dhabi. They will combine their network of 140 destinations, with Jet Airways, establishing a Gulf gateway in Abu Dhabi and expanding its reach through Etihad Airways’ growing global network. The deal is expected to take at least three months to obtain regulatory approvals.

In addition to the allotment of shares as stated above, Etihad will also be eligible for additional rights including

three seats on the board of the company (one of whom may be elected as vice chairman of the board).

The two governments have also increased weekly seats between India and Abu Dhabi from 13,300 to 50,000 seats

over the next three years.

Investors should note: In the airline industry, seat capacities between two countries are decided through bilateral

agreements with each country then apportioning its share to different airlines registered there.

Resolution 1: Issuance of securities To issue upto 27.26 mn equity shares of face value Rs.10 each on a preferential basis to Etihad Airways PJSC IiAS Recommendation: FOR

Voting Advisory

Jet Airways (India) Limited 4 | P a g e

Reasons for fund raising, as stated by the company, are general in nature and broadly include:

i. Supporting the growth and operations of the company and/or it subsidiaries ii. Funding the capex requirements of the company and/or it subsidiaries

iii. Repaying the loans which have prefunded the capex requirements so far

The company’s debt reduced from Rs.115.1 bn in FY11 to Rs 108.7 bn in FY12. Despite this reduction, the debt to

EBIDTA ratio has increased from 6.1x in FY11 to 18.7 in FY12 (refer Table 1) primarily on account of increased

operating expenses. The high debt level is hurting the company in the form of high interest charges.

The company expects that the above deal will not only benefit in reducing its debt but will also help in reduction

of expenses, given the synergies in operation of both the airlines.

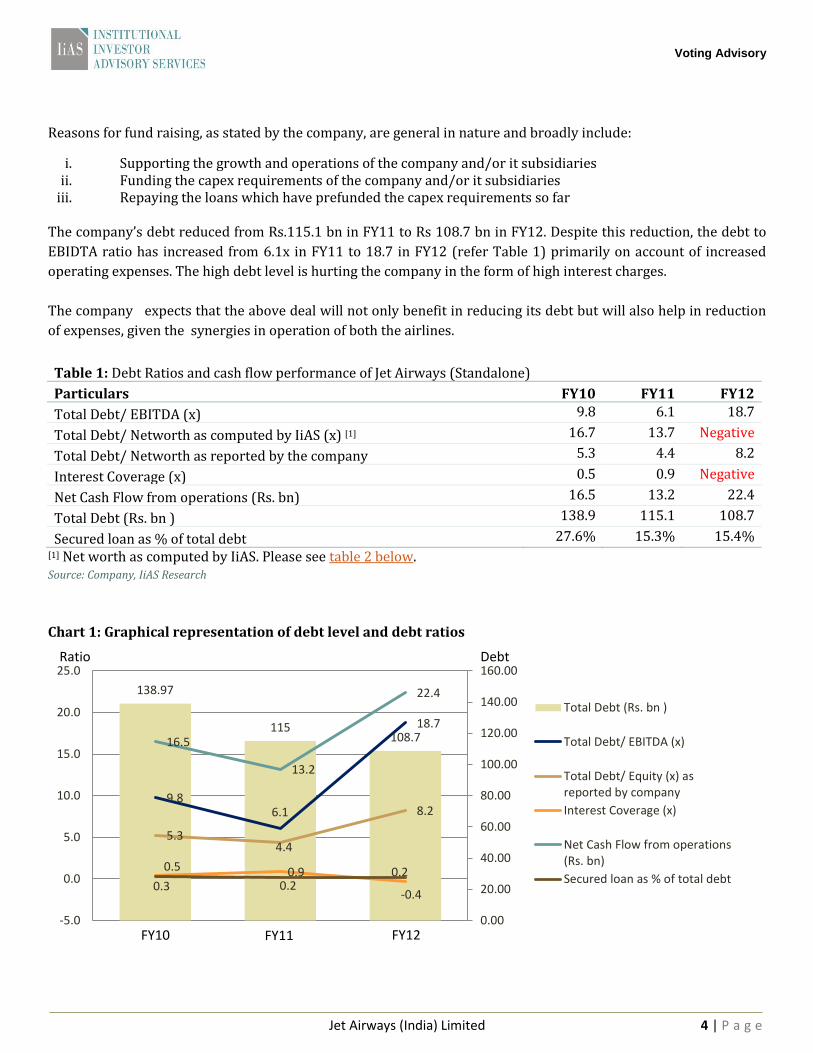

Table 1: Debt Ratios and cash flow performance of Jet Airways (Standalone)

Particulars FY10 FY11 FY12

Total Debt/ EBITDA (x) 9.8 6.1 18.7

Total Debt/ Networth as computed by IiAS (x) [1] 16.7 13.7 Negative

Total Debt/ Networth as reported by the company 5.3 4.4 8.2

Interest Coverage (x) 0.5 0.9 Negative

Net Cash Flow from operations (Rs. bn) 16.5 13.2 22.4

Total Debt (Rs. bn ) 138.9 115.1 108.7

Secured loan as % of total debt 27.6% 15.3% 15.4% [1] Net worth as computed by IiAS. Please see table 2 below. Source: Company, IiAS Research

Chart 1: Graphical representation of debt level and debt ratios

138.97

115 108.7

9.8 6.1

18.7

5.3 4.4

8.2

0.5 0.9

-0.4

16.5

13.2

22.4

0.3 0.2 0.2

0.00

20.00

40.00

60.00

80.00

100.00

120.00

140.00

160.00

-5.0

0.0

5.0

10.0

15.0

20.0

25.0

Total Debt (Rs. bn )

Total Debt/ EBITDA (x)

Total Debt/ Equity (x) asreported by company

Interest Coverage (x)

Net Cash Flow from operations(Rs. bn)

Secured loan as % of total debt

FY10 FY11 FY12

Debt Ratio

Voting Advisory

Jet Airways (India) Limited 5 | P a g e

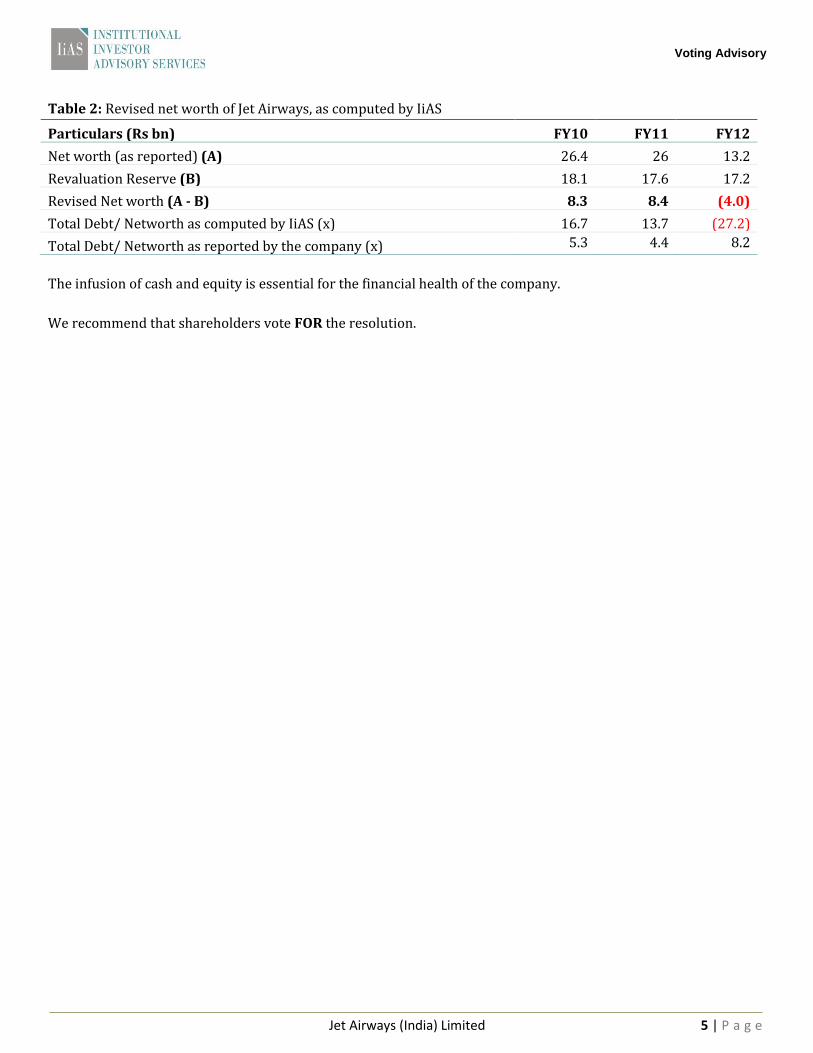

Table 2: Revised net worth of Jet Airways, as computed by IiAS

Particulars (Rs bn) FY10 FY11 FY12

Net worth (as reported) (A) 26.4 26 13.2

Revaluation Reserve (B) 18.1 17.6 17.2

Revised Net worth (A - B) 8.3 8.4 (4.0)

Total Debt/ Networth as computed by IiAS (x) 16.7 13.7 (27.2)

Total Debt/ Networth as reported by the company (x) 5.3 4.4 8.2

The infusion of cash and equity is essential for the financial health of the company.

We recommend that shareholders vote FOR the resolution.

Voting Advisory

Jet Airways (India) Limited 6 | P a g e

Category: Alteration to charter documents

Resolution 2: Amendment to Articles of Association (AoA) of the company

IiAS Recommendation: AGAINST

Discussion

The company is seeking shareholders’ approval for modifying the existing Articles of Association of the company reflecting its shareholders agreement (signed between the promoters and Etihad Airways).

The company proposes to amend the Articles of Association. We have listed the important changes below, classifying them into two categories viz. 1) Newly introduced special changes made keeping in mind the promoter and Etihad and 2) Modifications to existing Articles of Association of the company.

Category 1: Newly introduced conditions in the Articles of Association Special rights given to the Etihad Airways as an investor

Transaction related: o Right of first refusal: The clause stipulates that both the Promoter and Etihad possess the right of

first refusal in case of transfer of shares to a third party. For instance, if the promoter plans to sell a certain number of shares to a third party at a determined price, he would be obligated to offer Etihad the option to pre-emptively buy all or part of these shares at the same price. The details of the transferee, number of shares transferred and the selling price would be sent to Etihad by a Right of First Refusal Notice (RFR). Etihad would have sixty days from receipt of the notice to decide on exercising the option, and in case it decides to buy the offered shares, it would have to pay within thirty days of having sent its confirmation.

o Tag along rights: In case the promoter plans to transfer/sell his shares to a third party, this article gives Etihad the right to ‘tag along’ with the promoter and sell or transfer its own stake to the same third party.

Control related: o Right to appoint vice Chairman of Jet Airways o Right to appoint 3 board members (nominees), including the vice chairman, out of 14 o Right to get Etihad nominees appointed on all board committees, all subsidiaries and all board

committees of subsidiaries

Special restrictions on Etihad Airways as an investor Lock-in: Etihad’s shareholding will remain locked-in for three years unless they sell less than 3% stake in a

12 month period, through a market sale

Special restrictions on promoter Naresh Goyal and affiliates

Restriction on promoters: Promoters must hold at least 51% and cannot transfer these shares without the approval of Etihad

Restriction on Naresh Goyal: Naresh Goyal must hold at least 26% and cannot transfer these shares without the approval of Etihad

Voting Advisory

Jet Airways (India) Limited 7 | P a g e

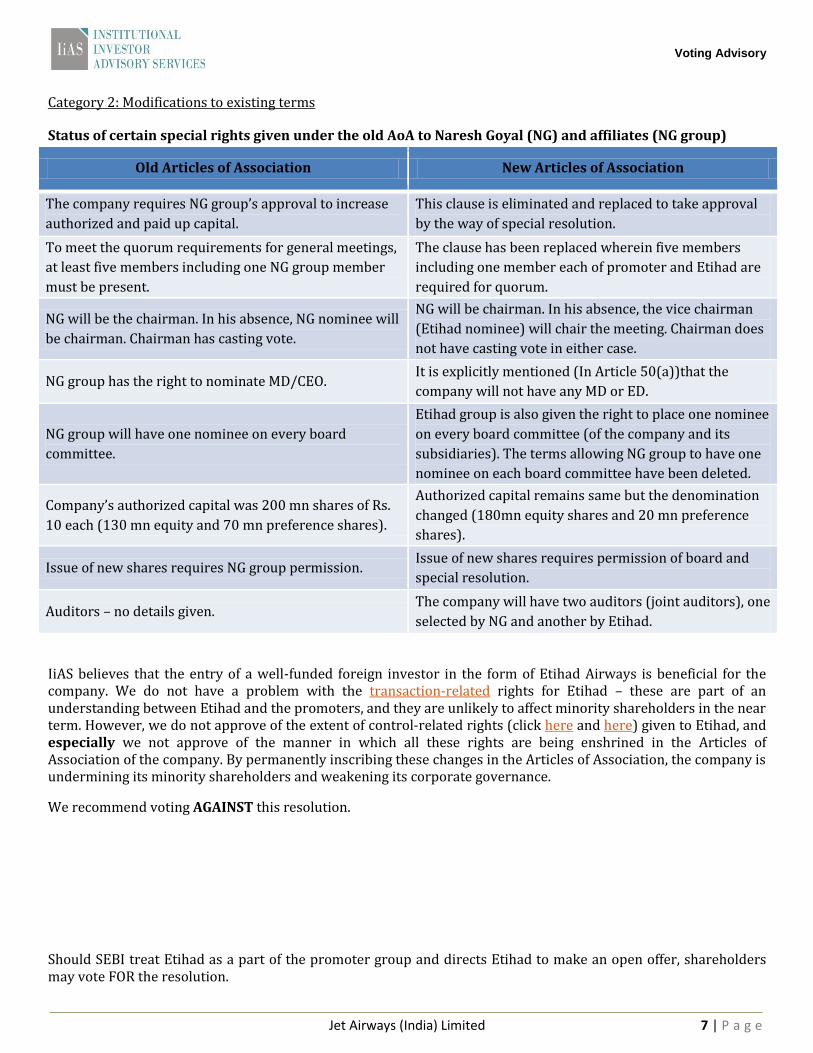

Category 2: Modifications to existing terms

Status of certain special rights given under the old AoA to Naresh Goyal (NG) and affiliates (NG group)

Old Articles of Association New Articles of Association

The company requires NG group’s approval to increase

authorized and paid up capital.

This clause is eliminated and replaced to take approval

by the way of special resolution.

To meet the quorum requirements for general meetings,

at least five members including one NG group member

must be present.

The clause has been replaced wherein five members

including one member each of promoter and Etihad are

required for quorum.

NG will be the chairman. In his absence, NG nominee will

be chairman. Chairman has casting vote.

NG will be chairman. In his absence, the vice chairman

(Etihad nominee) will chair the meeting. Chairman does

not have casting vote in either case.

NG group has the right to nominate MD/CEO. It is explicitly mentioned (In Article 50(a))that the

company will not have any MD or ED.

NG group will have one nominee on every board

committee.

Etihad group is also given the right to place one nominee

on every board committee (of the company and its

subsidiaries). The terms allowing NG group to have one

nominee on each board committee have been deleted.

Company’s authorized capital was 200 mn shares of Rs.

10 each (130 mn equity and 70 mn preference shares).

Authorized capital remains same but the denomination

changed (180mn equity shares and 20 mn preference

shares).

Issue of new shares requires NG group permission. Issue of new shares requires permission of board and

special resolution.

Auditors – no details given. The company will have two auditors (joint auditors), one

selected by NG and another by Etihad.

IiAS believes that the entry of a well-funded foreign investor in the form of Etihad Airways is beneficial for the company. We do not have a problem with the transaction-related rights for Etihad – these are part of an understanding between Etihad and the promoters, and they are unlikely to affect minority shareholders in the near term. However, we do not approve of the extent of control-related rights (click here and here) given to Etihad, and especially we not approve of the manner in which all these rights are being enshrined in the Articles of Association of the company. By permanently inscribing these changes in the Articles of Association, the company is undermining its minority shareholders and weakening its corporate governance.

We recommend voting AGAINST this resolution.

Should SEBI treat Etihad as a part of the promoter group and directs Etihad to make an open offer, shareholders may vote FOR the resolution.

Voting Advisory

Jet Airways (India) Limited 8 | P a g e

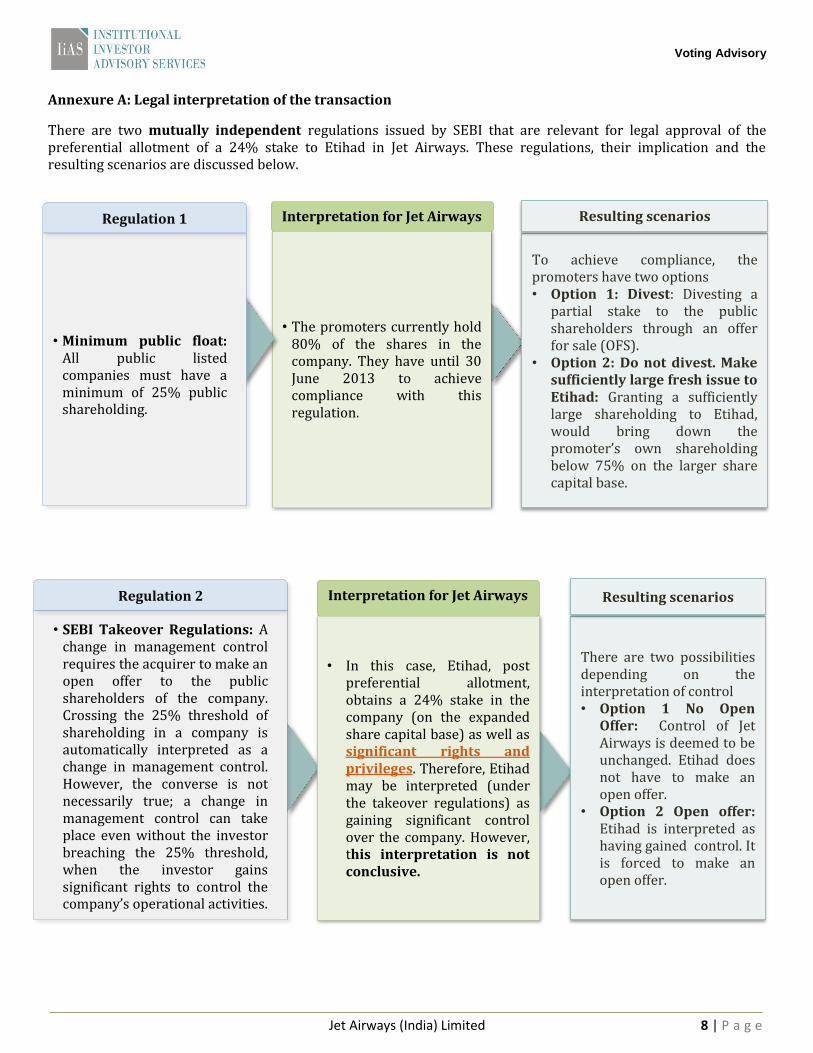

Annexure A: Legal interpretation of the transaction

There are two mutually independent regulations issued by SEBI that are relevant for legal approval of the preferential allotment of a 24% stake to Etihad in Jet Airways. These regulations, their implication and the resulting scenarios are discussed below.

To achieve compliance, the promoters have two options • Option 1: Divest: Divesting a

partial stake to the public shareholders through an offer for sale (OFS).

• Option 2: Do not divest. Make sufficiently large fresh issue to Etihad: Granting a sufficiently large shareholding to Etihad, would bring down the promoter’s own shareholding below 75% on the larger share capital base.

• The promoters currently hold 80% of the shares in the company. They have until 30 June 2013 to achieve compliance with this regulation.

• Minimum public float: All public listed companies must have a minimum of 25% public shareholding.

Interpretation for Jet Airways Resulting scenarios

• SEBI Takeover Regulations: A change in management control requires the acquirer to make an open offer to the public shareholders of the company. Crossing the 25% threshold of shareholding in a company is automatically interpreted as a change in management control. However, the converse is not necessarily true; a change in management control can take place even without the investor breaching the 25% threshold, when the investor gains significant rights to control the company’s operational activities.

• In this case, Etihad, post preferential allotment, obtains a 24% stake in the company (on the expanded share capital base) as well as significant rights and privileges. Therefore, Etihad may be interpreted (under the takeover regulations) as gaining significant control over the company. However, this interpretation is not conclusive.

There are two possibilities depending on the interpretation of control • Option 1 No Open

Offer: Control of Jet Airways is deemed to be unchanged. Etihad does not have to make an open offer.

• Option 2 Open offer: Etihad is interpreted as having gained control. It is forced to make an open offer.

Regulation 2 Interpretation for Jet Airways Resulting scenarios

Regulation 1

Voting Advisory

Jet Airways (India) Limited 9 | P a g e

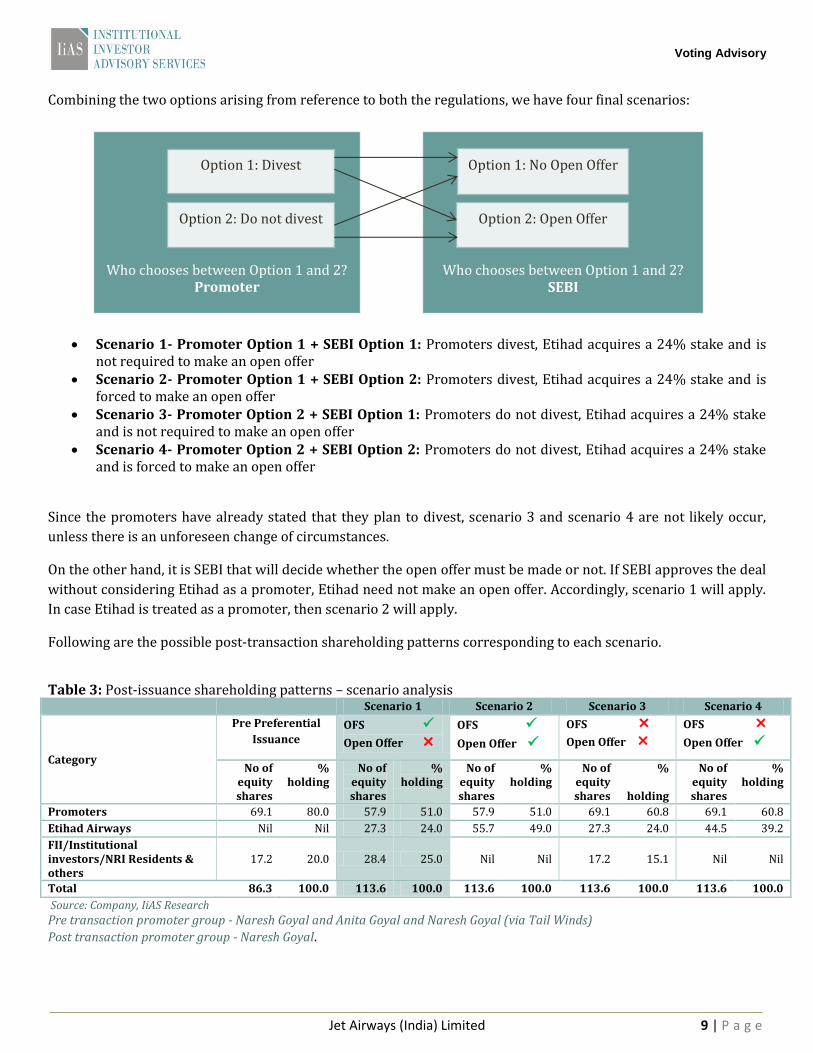

Combining the two options arising from reference to both the regulations, we have four final scenarios:

Scenario 1- Promoter Option 1 + SEBI Option 1: Promoters divest, Etihad acquires a 24% stake and is not required to make an open offer

Scenario 2- Promoter Option 1 + SEBI Option 2: Promoters divest, Etihad acquires a 24% stake and is forced to make an open offer

Scenario 3- Promoter Option 2 + SEBI Option 1: Promoters do not divest, Etihad acquires a 24% stake and is not required to make an open offer

Scenario 4- Promoter Option 2 + SEBI Option 2: Promoters do not divest, Etihad acquires a 24% stake and is forced to make an open offer

Since the promoters have already stated that they plan to divest, scenario 3 and scenario 4 are not likely occur,

unless there is an unforeseen change of circumstances.

On the other hand, it is SEBI that will decide whether the open offer must be made or not. If SEBI approves the deal

without considering Etihad as a promoter, Etihad need not make an open offer. Accordingly, scenario 1 will apply.

In case Etihad is treated as a promoter, then scenario 2 will apply.

Following are the possible post-transaction shareholding patterns corresponding to each scenario.

Table 3: Post-issuance shareholding patterns – scenario analysis Scenario 1 Scenario 2 Scenario 3 Scenario 4

Category

Pre Preferential

Issuance OFS

Open Offer

OFS

Open Offer

OFS

Open Offer

OFS

Open Offer

No of equity shares

% holding

No of equity shares

% holding

No of equity shares

% holding

No of equity shares

%

holding

No of equity shares

% holding

Promoters 69.1 80.0 57.9 51.0 57.9 51.0 69.1 60.8 69.1 60.8

Etihad Airways Nil Nil 27.3 24.0 55.7 49.0 27.3 24.0 44.5 39.2

FII/Institutional investors/NRI Residents & others

17.2 20.0 28.4 25.0 Nil Nil 17.2 15.1 Nil Nil

Total 86.3 100.0 113.6 100.0 113.6 100.0 113.6 100.0 113.6 100.0

Source: Company, IiAS Research

Pre transaction promoter group - Naresh Goyal and Anita Goyal and Naresh Goyal (via Tail Winds)

Post transaction promoter group - Naresh Goyal.

Who chooses between Option 1 and 2? Promoter

Option 2: Do not divest

Option 1: Divest

Who chooses between Option 1 and 2? SEBI

Option 2: Open Offer

Option 1: No Open Offer

Voting Advisory

Jet Airways (India) Limited 10 | P a g e

Scenario 1: Promoters divest through Offer for Sale (OFS), Etihad acquires a 24% stake and is not required make an open offer The deal has been constructed in two phases. In first phase, the company plans to bring down its shareholding to 67.1% by selling 1.1 mn equity shares through OFS and in second phase it will bring down its shareholding to 51% by issuing fresh equity to Etihad.

Hence, post allotment, the promoter stake will decrease from 80.0% to 51.0% and Etihad’s stake will be 24%, technically complying with both the aviation sector norms – wherein the control (51% stake) should be in the hands of an Indian company and SEBI’s norms- of a minimum requirement of 25% public float, by stipulated June 2013 deadline.

Scenario 2: Promoters divest through Offer for Sale (OFS), Etihad acquires a 24% stake and is forced to make an open offer Jet and Etihad are entering into a strategic alliance operationally. Hence, as part of the deal, Etihad obtains significant influence over the operations of Jet Airways, as reflected in the amendments to the charter documents. This aspect of the transaction is under review by the regulatory authorities and SEBI may consider the transaction to be a change in management control – which will trigger open offer under SEBI Takeover code. Etihad will then have to make an open offer for the remaining 25% stake which is currently with the public.

In case the open offer is done, and in case all public shareholders subscribe, this would take Etihad’s overall stake to 49%. However this is in violation of SEBI norms of a minimum requirement of 25% public float. In that case, the promoter (current + Etihad) will have to dilute their stake through another new issue or OFS.

Scenario 3: Promoters do not divest, Etihad acquires a 24% stake and is not required make an open offer

At present the company’s public shareholding is 20%. Hence, theoretically, if the company does not offer an OFS

and goes ahead with only the preferential allotment of a 24% shareholding on the expanded share capital base to

Etihad, then the promoters stake post allotment will come down to 61%. Etihad’s stake will be 24% and public

shareholding will come down to 15 %. If Etihad is treated as a public shareholder, the company will be in

compliance with the minimum public float requirement.

Scenario 4: Promoters do not divest, Etihad acquires a 24% stake and is required to make an open offer This case follows from Scenario 3. Immediately after the transaction, the promoter would hold 61%, and Etihad would hold 24% of the expanded share capital base of Jet Airways. In case Etihad is treated as a promoter, it will have to make an open offer for 26% of the company’s shareholding, where the public shareholding is only 15%. Thus, Etihad could end up with a 39% stake in the company. The company will be in violation of the minimum public float requirement.

Shareholders should note that Scenarios 3 and 4 are just for academic purpose as we have already conveyed these scenarios are not possible.

Voting Advisory

Jet Airways (India) Limited 11 | P a g e

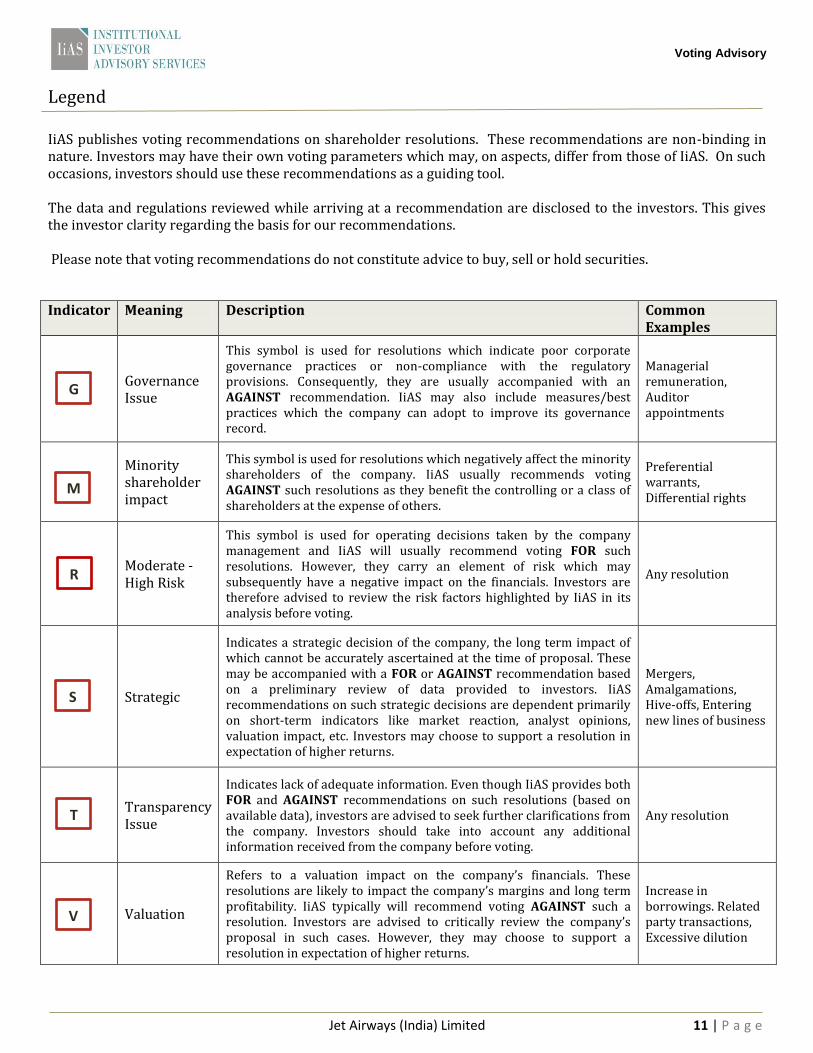

Legend

IiAS publishes voting recommendations on shareholder resolutions. These recommendations are non-binding in nature. Investors may have their own voting parameters which may, on aspects, differ from those of IiAS. On such occasions, investors should use these recommendations as a guiding tool. The data and regulations reviewed while arriving at a recommendation are disclosed to the investors. This gives the investor clarity regarding the basis for our recommendations. Please note that voting recommendations do not constitute advice to buy, sell or hold securities.

Indicator Meaning Description Common Examples

Governance Issue

This symbol is used for resolutions which indicate poor corporate governance practices or non-compliance with the regulatory provisions. Consequently, they are usually accompanied with an AGAINST recommendation. IiAS may also include measures/best practices which the company can adopt to improve its governance record.

Managerial remuneration, Auditor appointments

Minority shareholder impact

This symbol is used for resolutions which negatively affect the minority shareholders of the company. IiAS usually recommends voting AGAINST such resolutions as they benefit the controlling or a class of shareholders at the expense of others.

Preferential warrants, Differential rights

Moderate - High Risk

This symbol is used for operating decisions taken by the company management and IiAS will usually recommend voting FOR such resolutions. However, they carry an element of risk which may subsequently have a negative impact on the financials. Investors are therefore advised to review the risk factors highlighted by IiAS in its analysis before voting.

Any resolution

Strategic

Indicates a strategic decision of the company, the long term impact of which cannot be accurately ascertained at the time of proposal. These may be accompanied with a FOR or AGAINST recommendation based on a preliminary review of data provided to investors. IiAS recommendations on such strategic decisions are dependent primarily on short-term indicators like market reaction, analyst opinions, valuation impact, etc. Investors may choose to support a resolution in expectation of higher returns.

Mergers, Amalgamations, Hive-offs, Entering new lines of business

Transparency Issue

Indicates lack of adequate information. Even though IiAS provides both FOR and AGAINST recommendations on such resolutions (based on available data), investors are advised to seek further clarifications from the company. Investors should take into account any additional information received from the company before voting.

Any resolution

Valuation

Refers to a valuation impact on the company’s financials. These resolutions are likely to impact the company’s margins and long term profitability. IiAS typically will recommend voting AGAINST such a resolution. Investors are advised to critically review the company’s proposal in such cases. However, they may choose to support a resolution in expectation of higher returns.

Increase in borrowings. Related party transactions, Excessive dilution

G

M

S

V

T

R

Voting Advisory

Jet Airways (India) Limited 12 | P a g e

Disclaimer

This document has been prepared by Institutional Investor Advisory Services India Limited (IiAS). IiAS is a full service Institutional

Shareholder Advisory Service Company. The information contained herein is from publicly available data or other sources believed to be

reliable, but we do not represent that it is accurate or complete and it should not be relied on as such. IiAS shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report. This

document is provided for assistance only and is not intended to be and must not alone be taken as the basis for any Voting or investment

decision. The user assumes the entire risk of any use made of this information. Each recipient of this document should make such

investigation as it deems necessary to arrive at an independent evaluation of the individual resolutions which may affect their investment in

the securities of companies referred to in this document (including the merits and risks involved). The discussions or views expressed may

not be suitable for all investors. This information is strictly confidential and is being furnished to you solely for your information. This

information should not be reproduced or redistributed or passed on directly or indirectly in any form to any other person or published,

copied, in whole or in part, for any purpose. This report is not directed or intended for distribution to, or use by, any person or entity who is

a citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution, publication, availability or use

would be contrary to law, regulation or which would subject IiAS to any registration or licensing requirements within such jurisdiction. The

distribution of this document in certain jurisdictions may be restricted by law, and persons in whose possession this document comes,

should inform themselves about and observe, any such restrictions. The information given in this document is as of the date of this report

and there can be no assurance that future results or events will be consistent with this information. This information is subject to change

without any prior notice. IiAS reserves the right to make modifications and alterations to this statement as may be required from time to

time. However, IiAS is under no obligation to update or keep the information current. Nevertheless, IiAS is committed to providing

independent and transparent recommendation to its client and would be happy to provide any information in response to specific client

queries. Neither IiAS nor any of its affiliates, group companies, directors, employees, agents or representatives shall be liable for any

damages whether direct, indirect, special or consequential including lost revenue or lost profits that may arise from or in connection with

the use of the information. . The disclosures of interest statements incorporated in this document are provided solely to enhance the

transparency and should not be treated as endorsement of the views expressed in the report. The analyst for this report certifies that all of

the views expressed in this report accurately reflect his or her personal views about the subject company or companies and its or their

securities, and no part of his or her compensation was, is or will be, directly or indirectly related to specific recommendations or views

expressed in this report. The information provided in these reports remains, unless otherwise stated, the copyright of IiAS. All layout, design,

original artwork, concepts and other Intellectual Properties, remains the property and copyright of IiAS and may not be used in any form or

for any purpose whatsoever by any party without the express written permission of the copyright holders.