3 May 2011 Asia Equities Daily Focus Periodicalimg.jrjimg.cn/2011/05/20110504152417139.pdf · 3 May...

44

Asia Pan-Asia Strategy 3 May 2011 Asia Equities Daily Focus Today's research headlines Asian Edition Deutsche Bank AG/Hong Kong All prices are those current at the end of the previous trading session unless otherwise indicated. Prices are sourced from local exchanges via Reuters, Bloomberg and other vendors. Data is sourced from Deutsche Bank and subject companies. Deutsche Bank does and seeks to do business with companies covered in its research reports. Thus, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. DISCLOSURES AND ANALYST CERTIFICATIONS ARE LOCATED IN APPENDIX 1. MICA(P) 007/05/2010 Periodical Asian Index Closings EQUITIES Close 1D Chg %Chg SHSZ300 3192.72 0.98 2.06 HSCEI 13208.71 -0.84 4.07 HSI 23720.81 -0.36 2.98 TWSE 9007.87 -0.36 0.39 KOSPI 2228.96 1.67 8.68 FSSTI 3179.86 -0.16 -0.32 KLCI 1534.95 -0.02 1.06 SENSEX 18998.02 -0.72 -7.37 NIFTY 5701.30 -0.84 -7.06 SET 1093.56 0.11 5.89 JCI 3849.30 0.78 3.94 PCOMP 4326.76 0.17 2.99 ASX200 4825.30 0.04 1.69 FOREX (vs US$) Close 1D Chg YTD %Chg Rmb 6.49 -0.01 1.76 HK$ 7.77 0.01 0.09 NT$ 28.57 0.15 2.57 Won 1065.23 0.59 5.70 S$ 1.22 0.21 5.04 M$ 2.96 -0.07 3.39 Rupee 44.34 -0.26 0.83 Baht 29.90 -0.07 0.54 Rupiah 8543.00 0.23 5.30 Peso 42.62 0.28 2.78 A$ 1.10 -0.14 7.07 Source: Bloomberg Finance LP Latest Commodity Prices COMMODITIES Close 1D %Chg YTD %Chg West Texas 113.70 -0.20 24.43 Brent 124.88 -0.63 32.43 CRB 368.17 -0.65 10.63 Copper 418.25 0.41 -5.79 Gold (Spot) 1554.28 -0.60 9.40 Alum. (LME) 2767.50 0.86 12.05 Baltic Dry 1269.00 0.79 -28.43 Source: Bloomberg Finance LP DB CORPORATE ACCESS DB Access Asia Conference 2011 - Singapore 5/23 - 26 DB Access Taiwan Conference 2011 - Taipei 11/7 - 8 DB Access Korea Conference 2011 - Seoul 11/10 - 11 DB Access Indonesia Conference 2011 - Jakarta 11/29 - 12/1 Research Team Carissa Szeto Equity Focus (+852) 2203 6171 [email protected] Ching-Li Teo, CFA Equity Focus (+852) 2203 6206 [email protected] Company Global Markets Research Nodita_ TOP STORIES Digital China (0861.HK),HKD14.86 Buy Price Target HKD19.00 A re-rating story; Initiating with Buy Lorraine Kuo Page 7 China Macro Strategy Update Positive macro outlook intact Jun Ma Page 8 ESTIMATE & TARGET PRICE CHANGES Esprit Holdings Ltd (0330.HK),HKD32.30 Buy Price Target HKD49.30 Cutting target price on weak wholesale; maintaining Buy Anne Ling Page 9 Lianhua Supermarket (0980.HK),HKD31.60 Hold Price Target HKD32.70 Investing in food safety system for future growth; Hold Anne Ling Page 10 Taiwan Cement (1101.TW),TWD41.95 Buy Price Target TWD45.00 Growth momentum continues; raising price target to NT$45 Yvonne Tsai Page 11 HDS (069960.KS),KRW166,500. 00 Buy Price Target KRW198,000.00 SSS growth to accelerate in 2Q11; maintaining Buy Jihyun Song Page 12 Hyundai Mobis (012330.KS),KRW366,000. 00 Buy Price Target KRW470,000.00 1Q11 results strong; target price raised to W470,000 Sanjeev Rana Page 13 STRATEGY/ECONOMICS Asia Economics Daily Mixed news on inflation in April Michael Spencer Page 14 Global Commodities Daily Gas prices not dangerous yet Adam Sieminski Page 18

Transcript of 3 May 2011 Asia Equities Daily Focus Periodicalimg.jrjimg.cn/2011/05/20110504152417139.pdf · 3 May...

Asia Pan-Asia Strategy

3 May 2011

Asia Equities Daily Focus Today's research headlines Asian Edition

Deutsche Bank AG/Hong Kong

All prices are those current at the end of the previous trading session unless otherwise indicated. Prices are sourced from local exchanges via Reuters, Bloomberg and other vendors. Data is sourced from Deutsche Bank and subject companies. Deutsche Bank does and seeks to do business with companies covered in its research reports. Thus, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. DISCLOSURES AND ANALYST CERTIFICATIONS ARE LOCATED IN APPENDIX 1. MICA(P) 007/05/2010

Periodical

Asian Index Closings EQUITIES Close 1D Chg %Chg

SHSZ300 3192.72 0.98 2.06 HSCEI 13208.71 -0.84 4.07 HSI 23720.81 -0.36 2.98 TWSE 9007.87 -0.36 0.39 KOSPI 2228.96 1.67 8.68 FSSTI 3179.86 -0.16 -0.32 KLCI 1534.95 -0.02 1.06 SENSEX 18998.02 -0.72 -7.37 NIFTY 5701.30 -0.84 -7.06 SET 1093.56 0.11 5.89 JCI 3849.30 0.78 3.94 PCOMP 4326.76 0.17 2.99 ASX200 4825.30 0.04 1.69 FOREX (vs US$) Close 1D Chg YTD %Chg Rmb 6.49 -0.01 1.76 HK$ 7.77 0.01 0.09 NT$ 28.57 0.15 2.57 Won 1065.23 0.59 5.70 S$ 1.22 0.21 5.04 M$ 2.96 -0.07 3.39 Rupee 44.34 -0.26 0.83 Baht 29.90 -0.07 0.54 Rupiah 8543.00 0.23 5.30 Peso 42.62 0.28 2.78 A$ 1.10 -0.14 7.07

Source: Bloomberg Finance LP

Latest Commodity Prices COMMODITIES Close 1D %Chg YTD %Chg West Texas 113.70 -0.20 24.43 Brent 124.88 -0.63 32.43 CRB 368.17 -0.65 10.63 Copper 418.25 0.41 -5.79 Gold (Spot) 1554.28 -0.60 9.40 Alum. (LME) 2767.50 0.86 12.05 Baltic Dry 1269.00 0.79 -28.43

Source: Bloomberg Finance LP

DB CORPORATE ACCESS DB Access Asia Conference 2011 - Singapore 5/23 - 26 DB Access Taiwan Conference 2011 - Taipei 11/7 - 8 DB Access Korea Conference 2011 - Seoul 11/10 - 11 DB Access Indonesia Conference 2011 - Jakarta 11/29 - 12/1

Research Team

Carissa Szeto Equity Focus (+852) 2203 6171 [email protected] Ching-Li Teo, CFA Equity Focus (+852) 2203 6206 [email protected]

Co

mp

any

Glo

bal

Mar

kets

Res

earc

h

Nodita_ 1. 2.

TOP STORIES Digital China (0861.HK),HKD14.86 Buy Price Target HKD19.00

A re-rating story; Initiating with Buy Lorraine Kuo Page 7

China Macro Strategy Update Positive macro outlook intact Jun Ma Page 8

ESTIMATE & TARGET PRICE CHANGES

Esprit Holdings Ltd (0330.HK),HKD32.30 Buy Price Target HKD49.30

Cutting target price on weak wholesale; maintaining Buy

Anne LingPage 9

Lianhua Supermarket (0980.HK),HKD31.60 Hold Price Target HKD32.70

Investing in food safety system for future growth; Hold

Anne LingPage 10

Taiwan Cement (1101.TW),TWD41.95 Buy Price Target TWD45.00

Growth momentum continues; raising price target to NT$45

Yvonne TsaiPage 11

HDS (069960.KS),KRW166,500.00 Buy Price Target KRW198,000.00

SSS growth to accelerate in 2Q11; maintaining Buy

Jihyun Song

Page 12

Hyundai Mobis (012330.KS),KRW366,000.00 Buy Price Target KRW470,000.00

1Q11 results strong; target price raised to W470,000

Sanjeev Rana

Page 13

STRATEGY/ECONOMICS

Asia Economics Daily Mixed news on inflation in April Michael Spencer Page 14

Global Commodities Daily Gas prices not dangerous yet Adam

Sieminski Page 18

3 May 2011 Strategy Asia Equities Daily Focus

Page 2 Deutsche Bank AG/Hong Kong

ADDITIONAL RESEARCH DB CONFERENCE/CORPORATE DAY

AsiaInfo-Linkage (ASIA.OQ),USD18.90 Buy Price Target USD24.75

1Q11 Preview Eva LeungPage 20 DB Access Asia Conference 2011 - Singapore 5/23 - 26

DB Access Taiwan Conference 2011 - Taipei 11/7 - 8 DB Access Korea Conference 2011 - Seoul 11/10 - 11

China Shenhua Energy (1088.HK),HKD36.25 Buy Price Target HKD40.00

1Q results in line with DB forecasts James KanPage 21

DB Access Indonesia Conference 2011 - Jakarta 11/29 - 2/1 1

NDRs Dongfang Electric

(1072.HK),HKD25.55 Buy Price Target HKD32.00

Record 1Q performance; Buy Michael TongPage 22 DBS Group Holdings (DBS SP) - SG 5/3

PT Bank Tabungan Negara (Persero), Tbk (BBTN IJ) - SG 5/3 - 4, HK 5/5 - 6 Sands China (1928 HK) - HK 5/4 Indofood CBP Sukes Makmur (ICBP IJ) & PT Indofood Sukses Makmur (INDF IJ) - HK 5/18 - 19 PT Adaro Energy Tbk (ADRO IJ) - HK 5/23

Little Sheep Group Limited (0968.HK),HKD5.00 Buy Price Target HKD6.15

Resume trading on 3 May; consideration yet to be announced

Anne Ling

Page 23LG Chem (051910 KS) - HK 5/23 - 24 H TC Corporation (2498 TT) - SG 6/21 - 22, HK 6/23 - 24

DB ANALYST/SALES ROADSHOWS

Korean autos Carmakers' domestic sales up 3%, global sales up 11% YoY

Sanjeev RanaPage 24

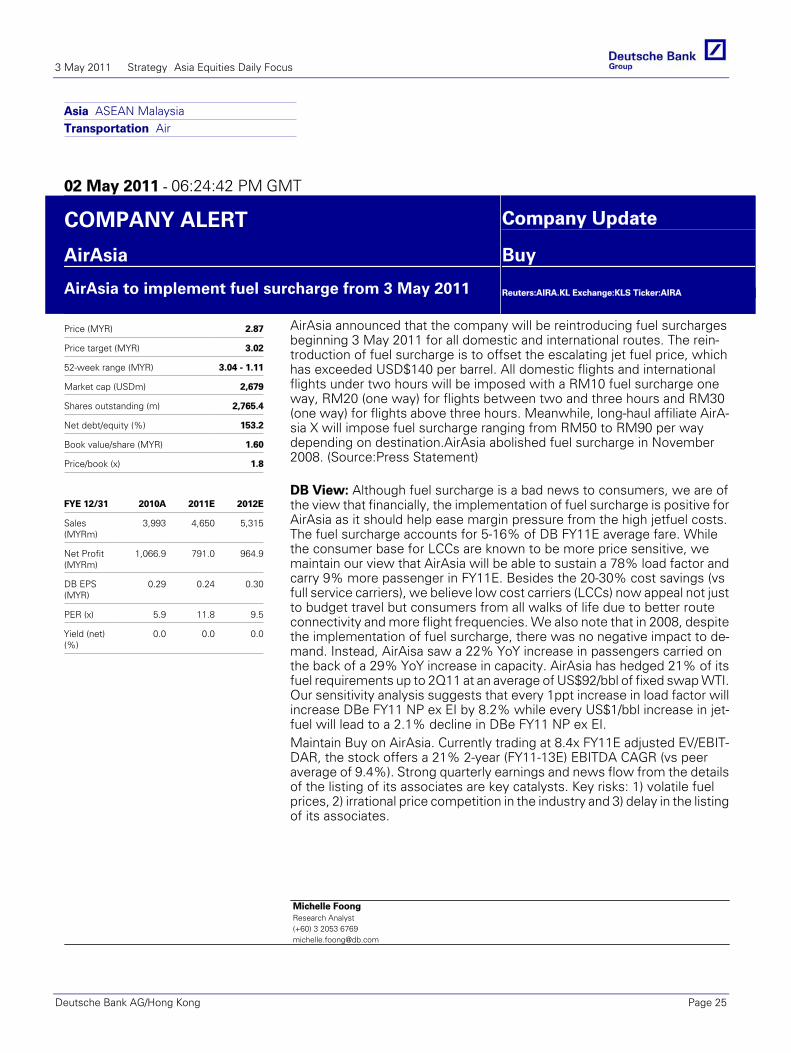

AirAsia (AIRA.KL) AirAsia to implement fuel surcharge from 3 May 2011

Michelle Foong Page 25

Soozhana Choi: Commodities - HK 5/5 - 6 KC Kao: Buy Selective PC Stocks: Neutralize on Smartphone - SG 6/21, HK 6/23

DB INTERNATIONAL PRODUCT Asian Palm Oil Industry Demand strength to offset near-term

price weakness Eltricia Foong

Page 26ROADSHOWS

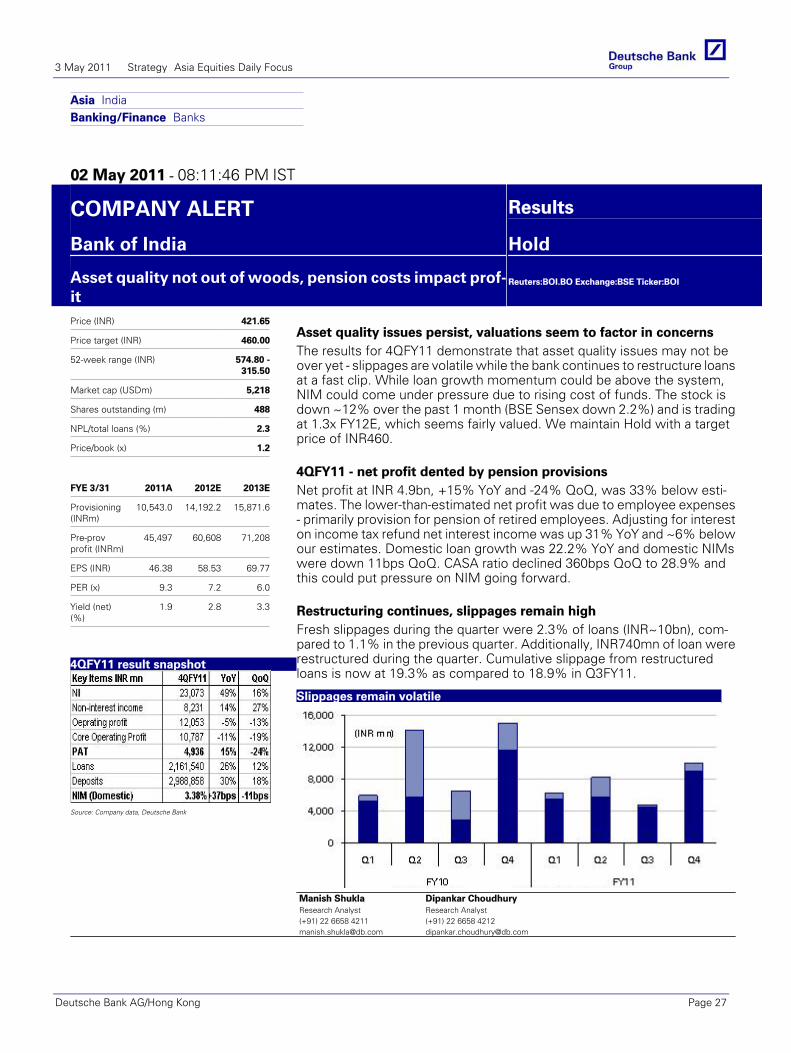

Bank of India (BOI.BO),INR421.65 Hold Price Target INR460.00

Asset quality not out of woods, pension costs impact profit

Manish ShuklaPage 27

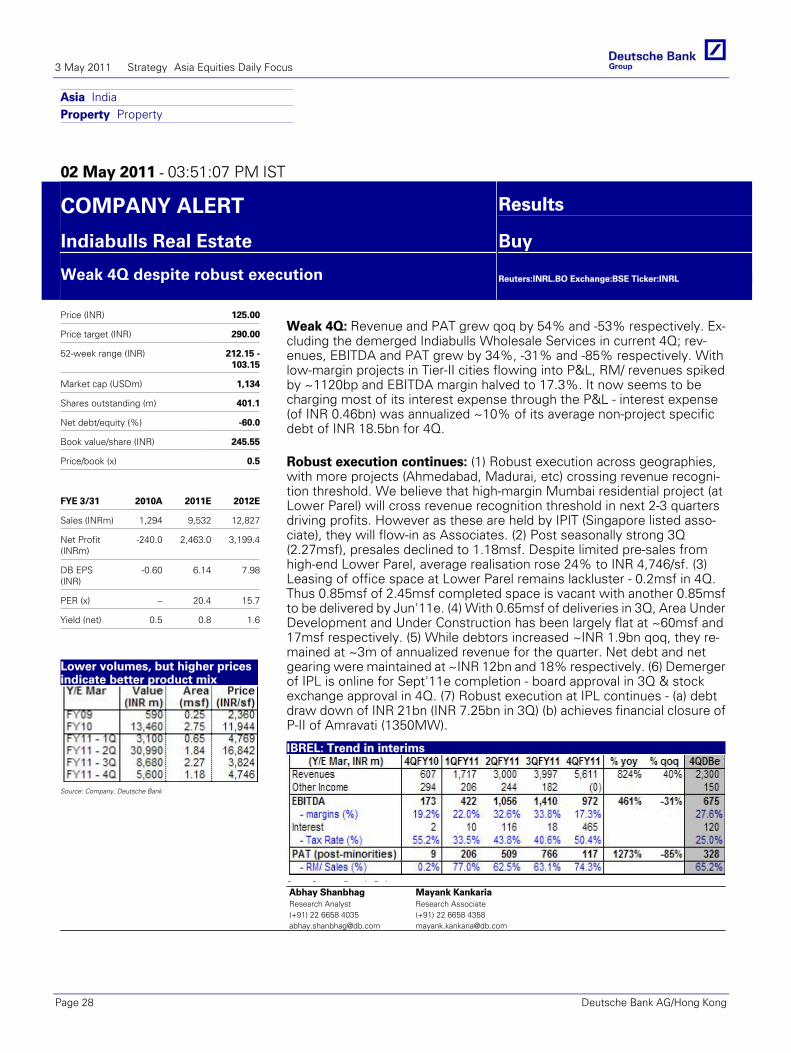

Fedex Corp. (FDX US) - HK 5/5, SG 5/6 Diageo (DGE LN) - HK 5/9, SG 5/10, PEK 5/11 Tom Ernst: Cloud Computing & Software - KL 5/18, HK 5/19, PEK 5/20, SG 5/23 Indiabulls Real Estate

(INRL.BO),INR125.75 Buy Price Target INR290.00

Weak 4Q despite robust execution Abhay Shanbhag Page 28

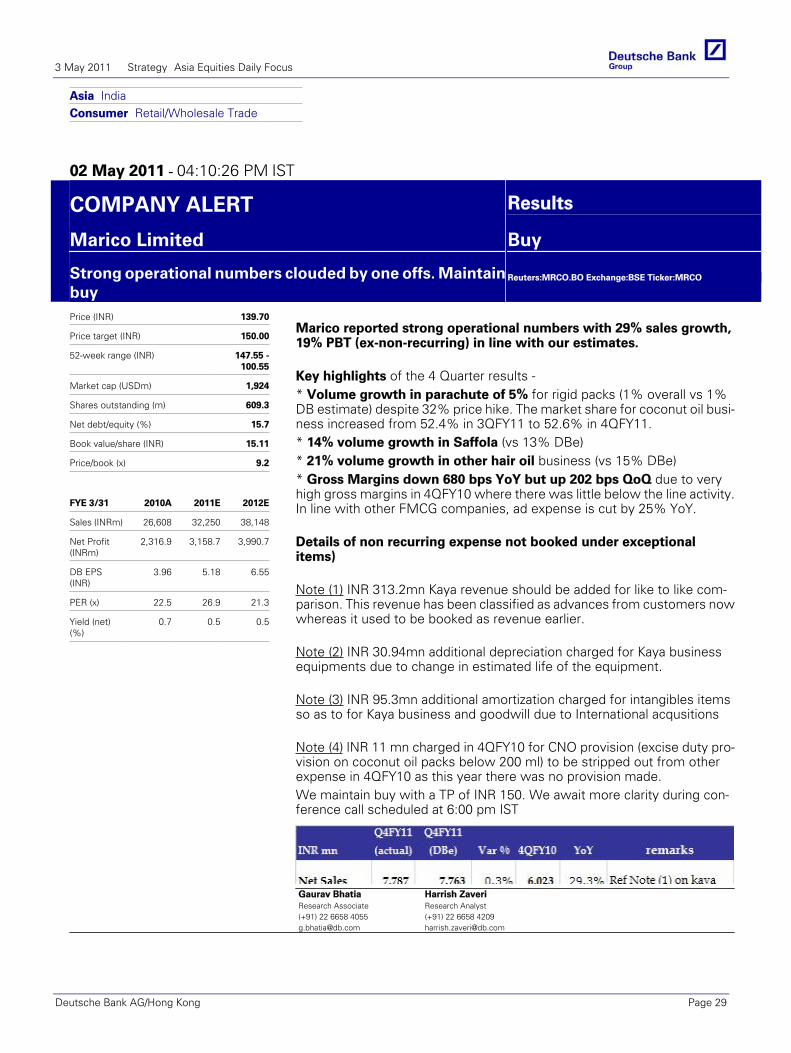

Marico Limited (MRCO.BO),INR136.45 Buy Price Target INR150.00

Strong operational numbers clouded by one offs. Maintain buy

Visa Inc. (V US) - PEK 5/23, HK 5/24 L'Oreal (OR EP) - PEK 5/23, SHA 5/24 Daimler AG (DAI GR) - HK 5/26 Equinix, Inc (EQIX US) - HK 5/27

Gaurav Bhatia

Page 29

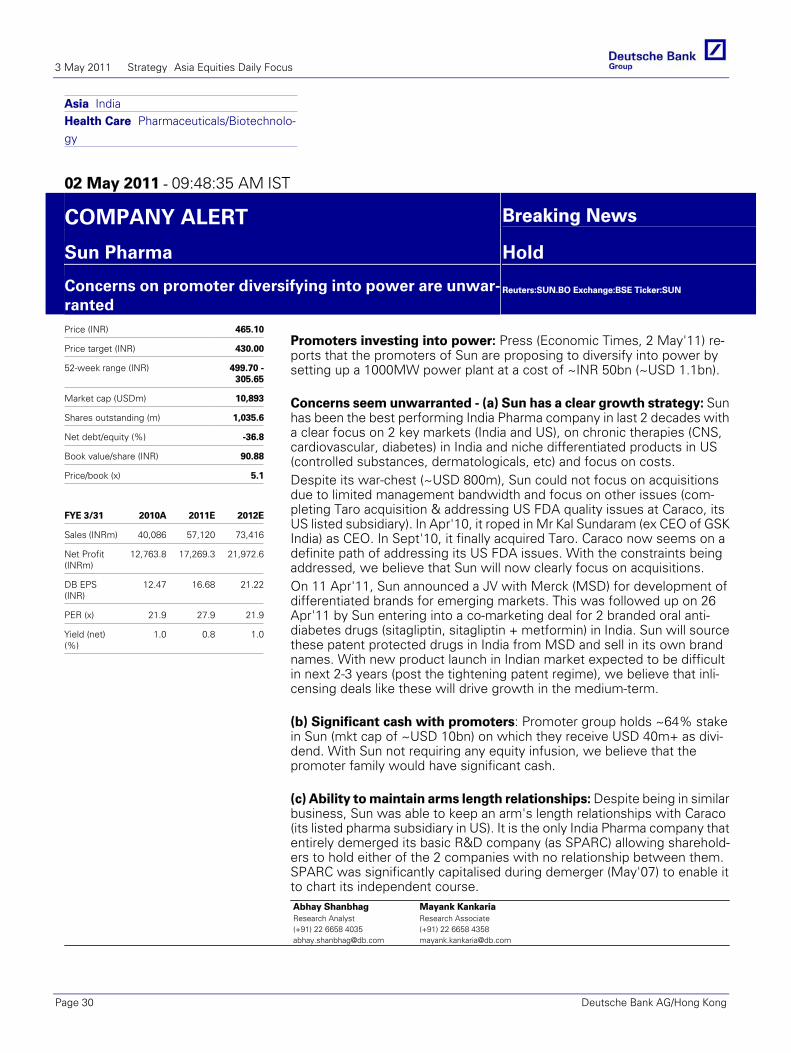

Sun Pharma (SUN.BO),INR465.30 Hold Price Target INR430.00

Concerns on promoter diversifying into power are unwarranted

Justin Yageman: Transportation & Shipping - SG 5/30, HK 5/31, PEK 6/2 SEL 6/3 RWE AG (RWE GR) - PEK 6/30, SG 7/1

Abhay Shanbhag Page 30

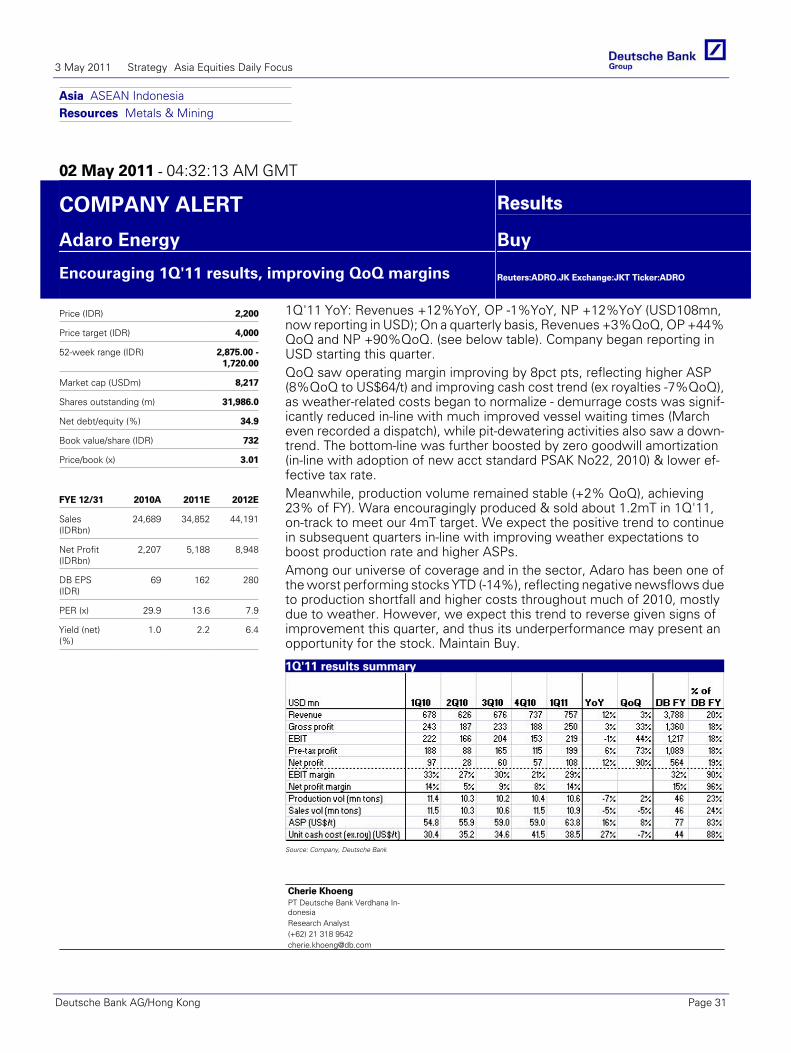

Adaro Energy (ADRO.JK),IDR2,225.00 Buy Price Target IDR4,000.00

Encouraging 1Q'11 results, improving QoQ margins

Cherie Khoeng

Page 31

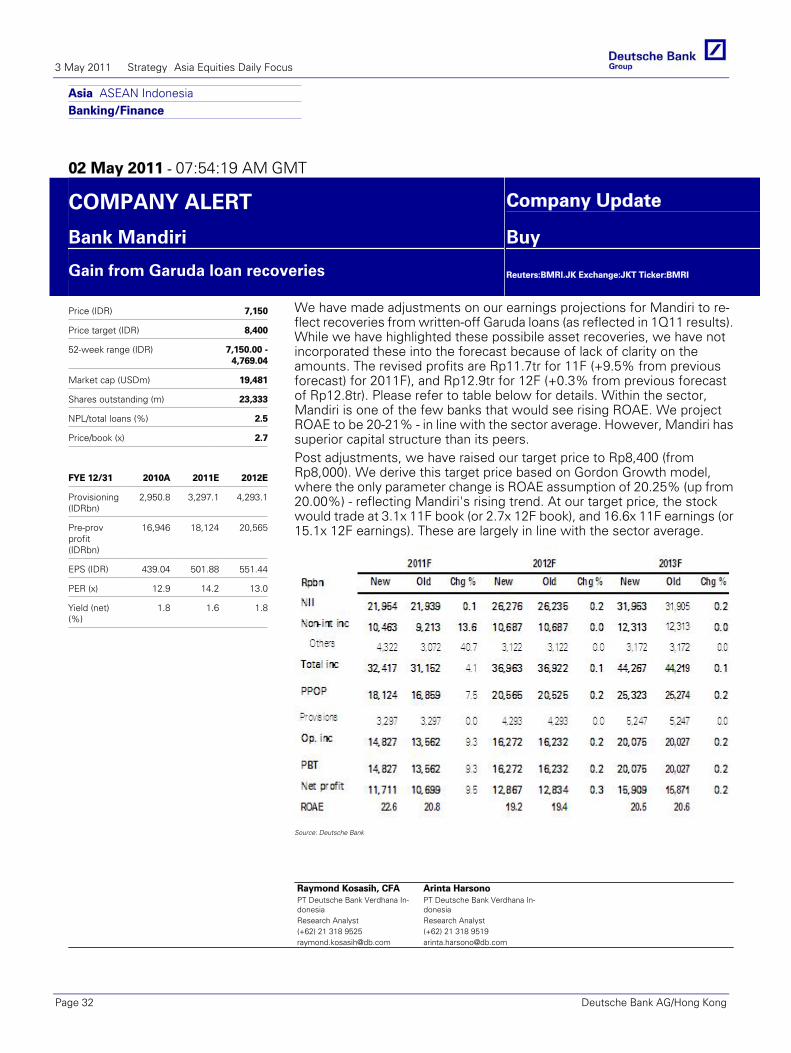

Bank Mandiri (BMRI.JK),IDR7,350.00 Buy Price Target IDR8,400.00

Gain from Garuda loan recoveries Raymond Kosasih Page 32

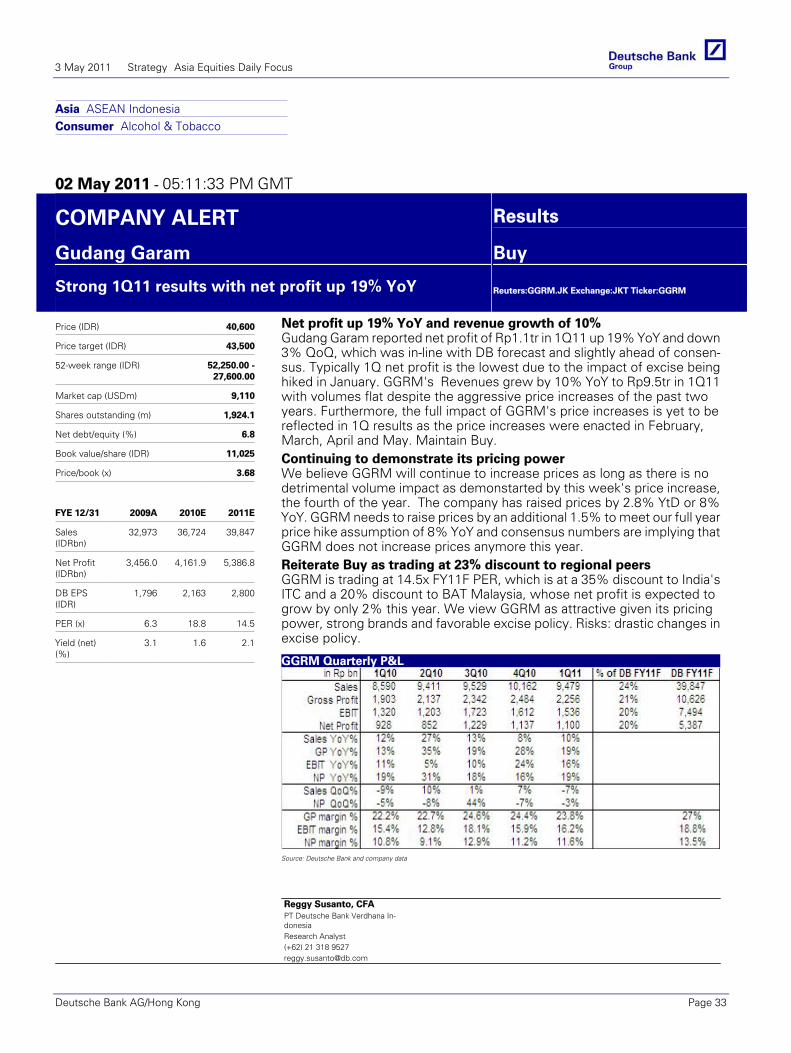

Gudang Garam (GGRM.JK) IDR40,600 Buy Price Target IDR43,500

Strong 1Q11 results with net profit up 19% YoY

Reggy Susanto

Page 33

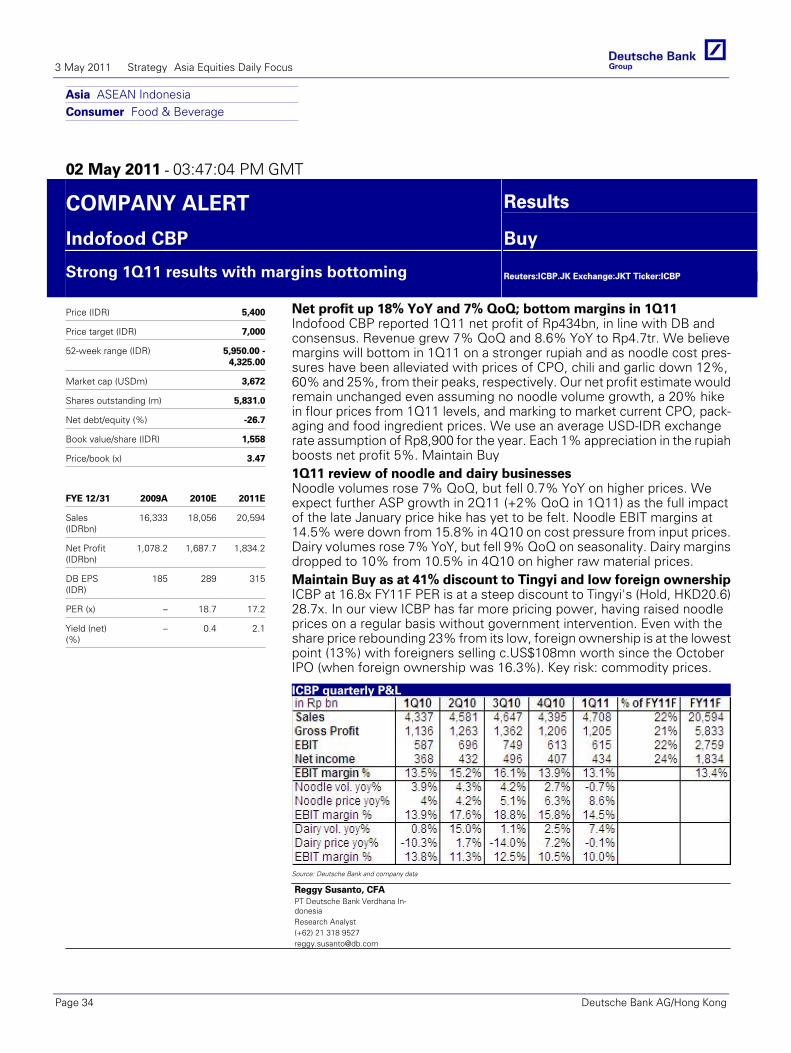

Indofood CBP (ICBP.JK),IDR5,300.00 Buy Price Target IDR7,000.00

Strong 1Q11 results with margins bottoming

Reggy Susanto

Page 34

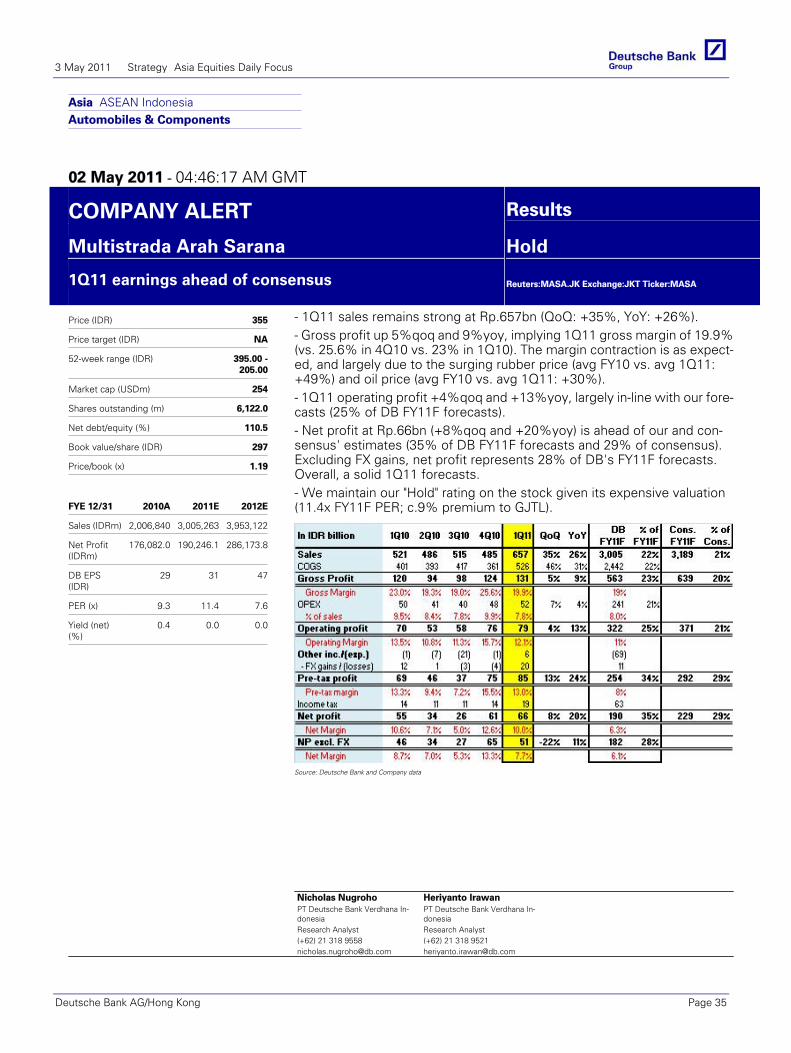

Multistrada Arah Sarana (MASA.JK),IDR350.00 Hold NA

NicholasNugroho

1Q11 earnings ahead of consensus Page 35

3 May 2011 Strategy Asia Equities Daily Focus

Deutsche Bank AG/Hong Kong Page 3

Summarecon (SMRA.JK),IDR1,260.00 Buy Price Target IDR1,400.00

1Q11 results below expectations Fiky Silvia

Page 36

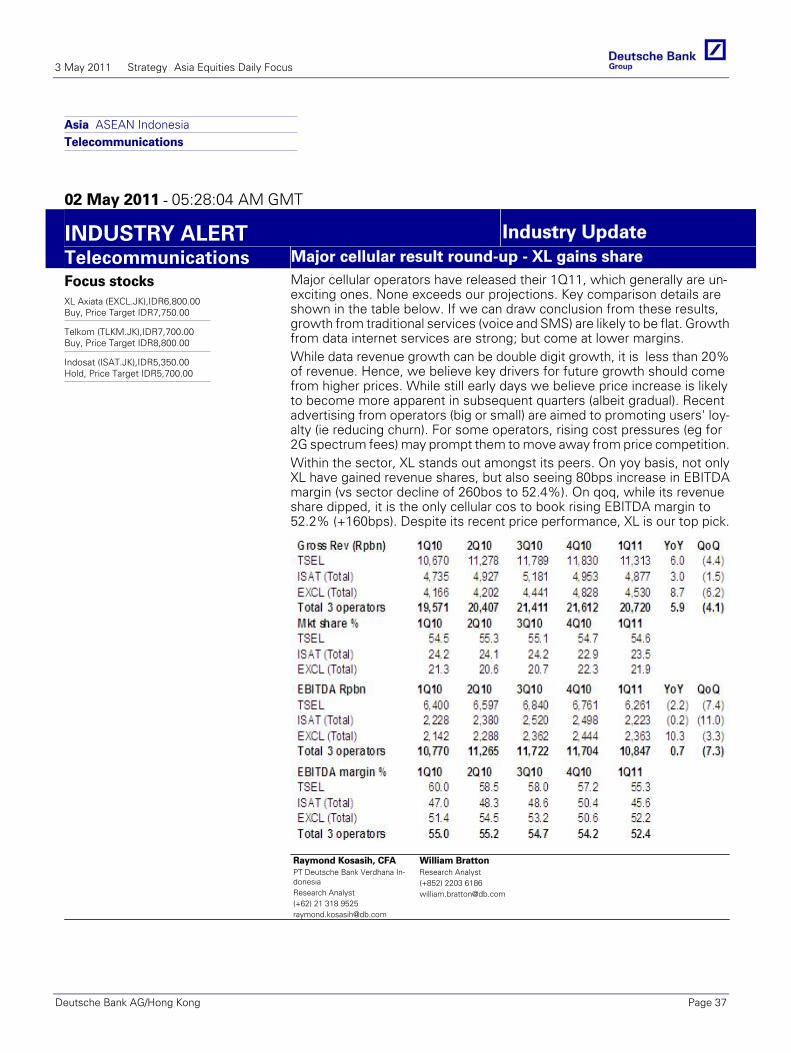

Telecommunications Major cellular result round-up - XL gains share

Raymond Kosasih Page 37

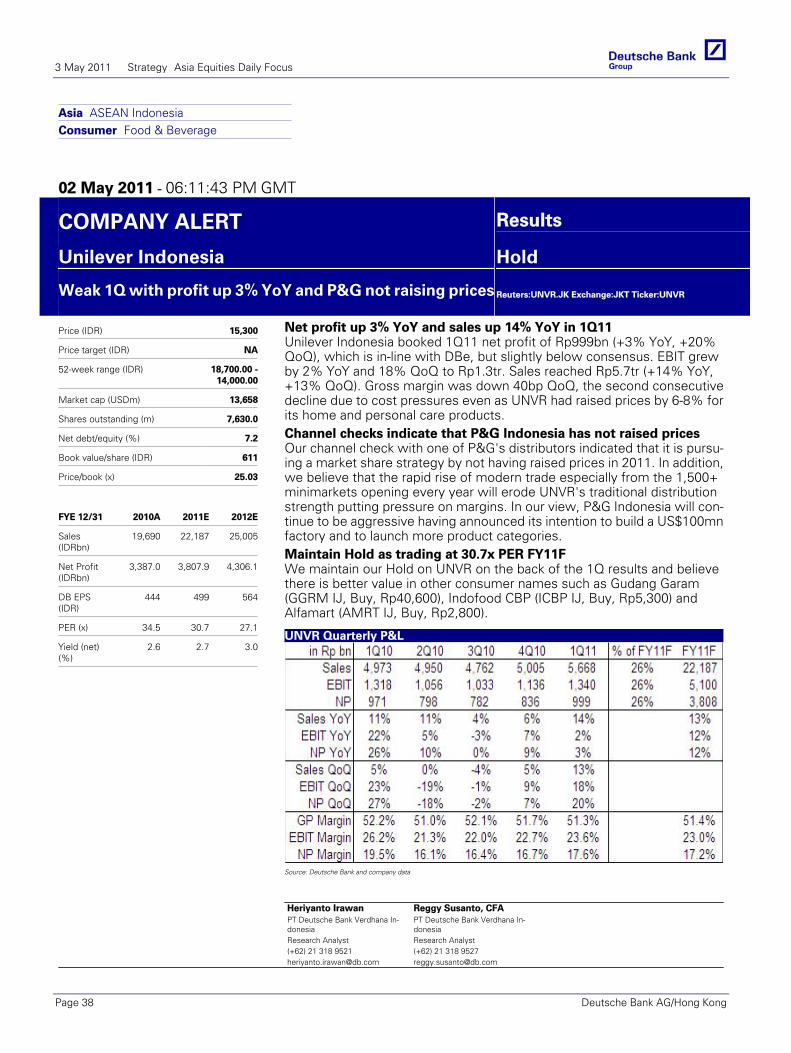

Unilever Indonesia (UNVR.JK) IDR15,300 Hold NA

Weak 1Q with profit up 3% YoY and P&G not raising prices

Heriyanto Irawan Page 38

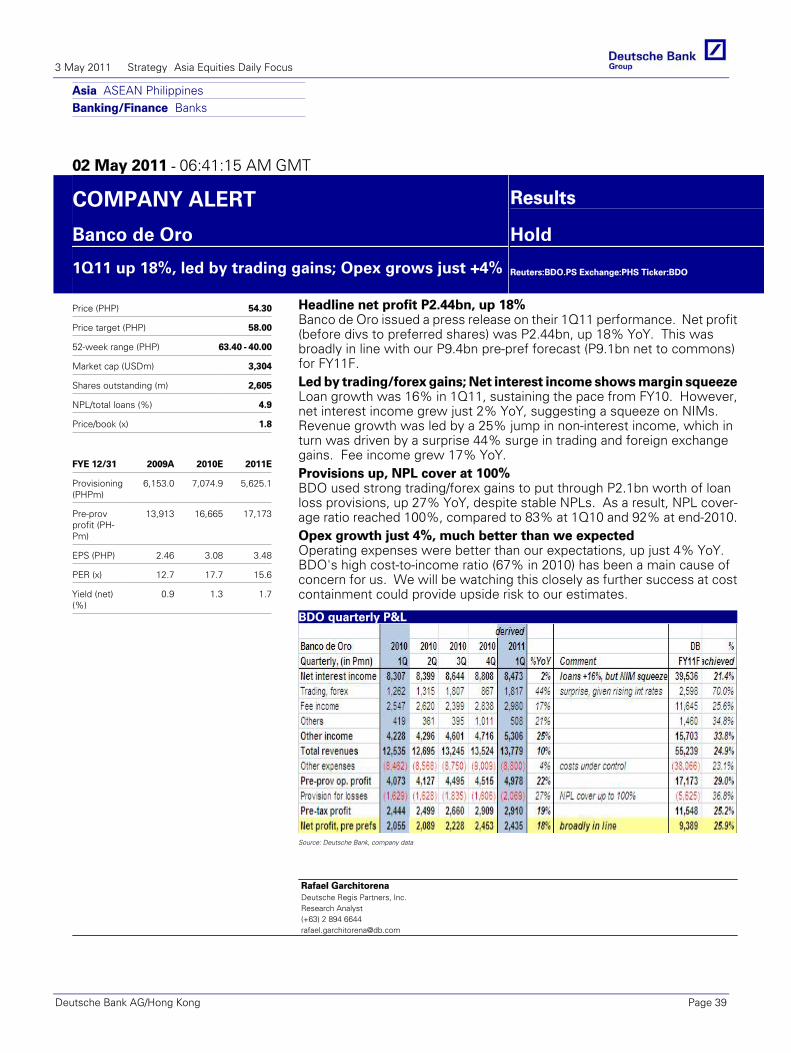

Banco de Oro (BDO.PS),PHP54.50 Hold Price Target PHP58.00

1Q11 up 18%, led by trading gains; Opex grows just +4%

Rafael Garchitorena Page 39

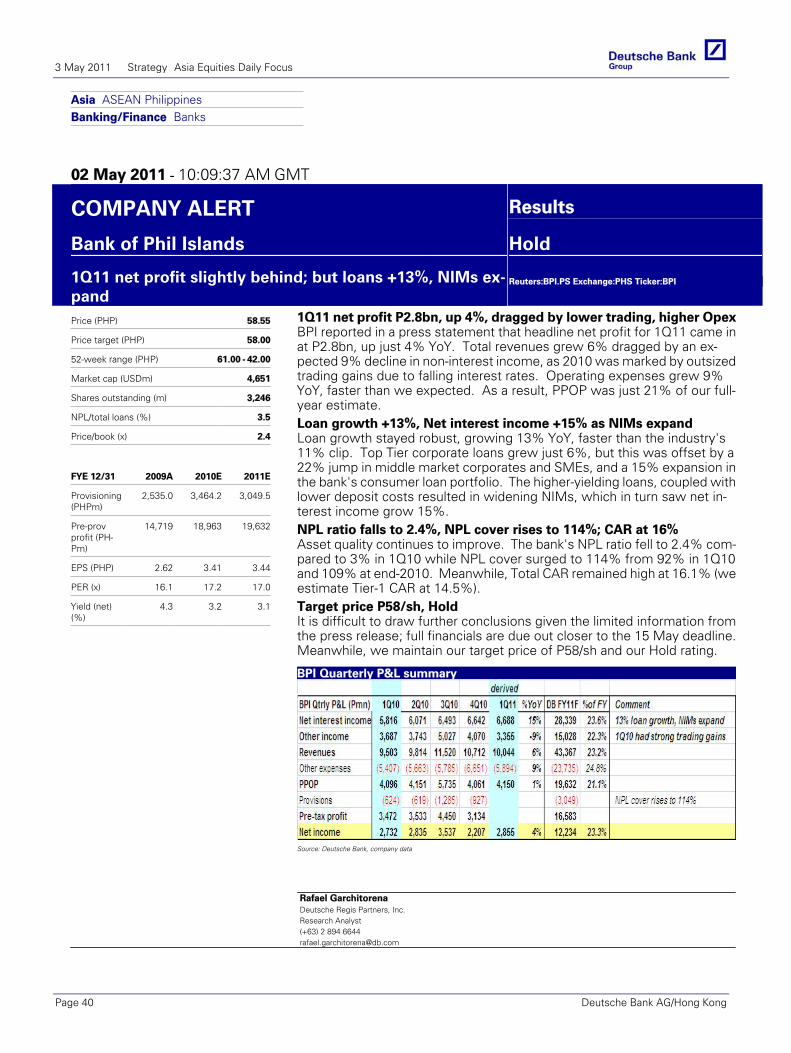

Bank of Phil Islands (BPI.PS),PHP58.55 Hold Price Target PHP58.00

1Q11 net profit slightly behind; but loans +13%, NIMs expand

Rafael Garchitorena Page 40

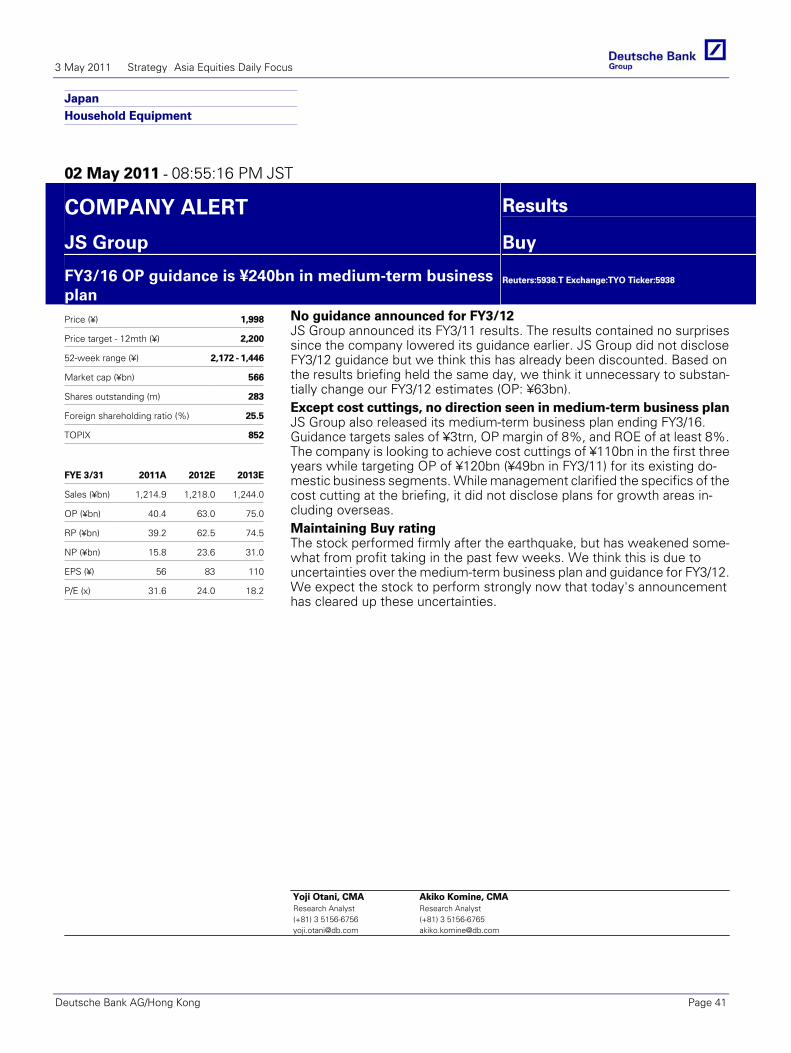

GLOBAL RESEARCH JS Group (5938.T),¥1,998 Buy Price Target ¥2,200 FY3/16 OP guidance is ¥240bn in

medium-term business plan Yoji Otani

Page 41

The notes and reports contained in this Daily are all excerpts of previously published documents. Please refer to the published notes on our web site for details on risks, valuations and earnings changes

3 May 2011 Strategy Asia Equities Daily Focus

Page 4 Deutsche Bank AG/Hong Kong

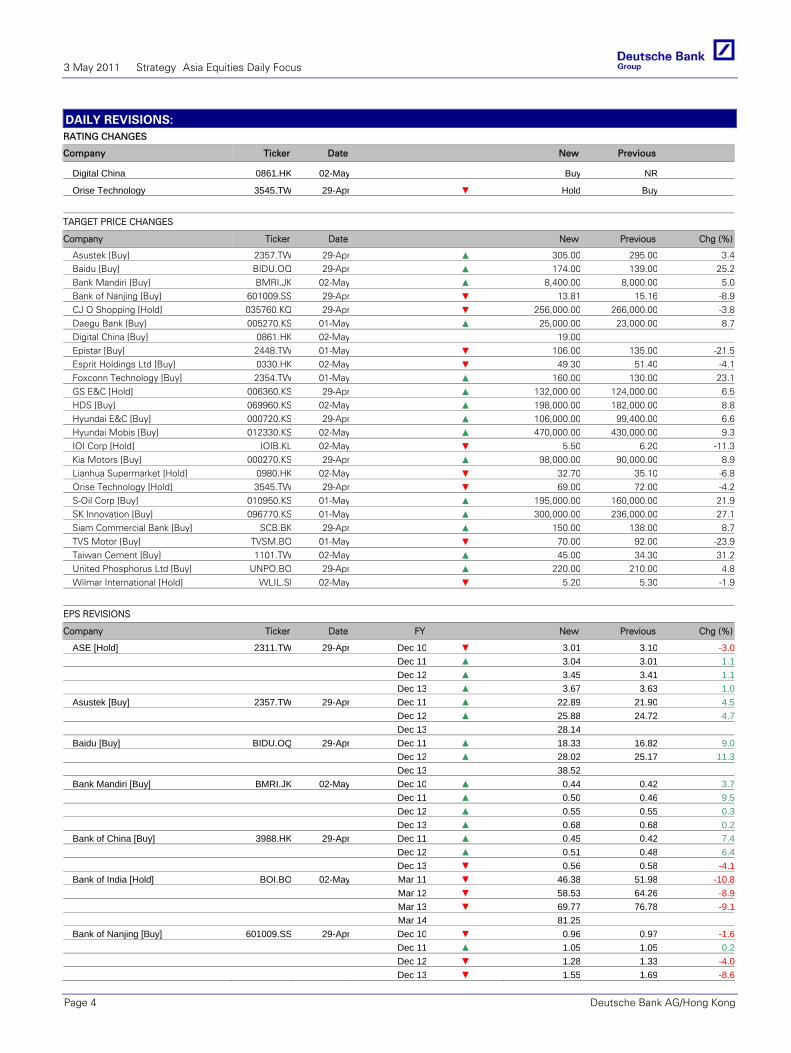

DAILY REVISIONS: RATING CHANGES

Company Ticker Date New Previous

Digital China 0861.HK 02-May Buy NR

Orise Technology 3545.TW 29-Apr ▼ Hold Buy

TARGET PRICE CHANGES

Company Ticker Date New Previous Chg (%)

Asustek [Buy] 2357.TW 29-Apr ▲ 305.00 295.00 3.4Baidu [Buy] BIDU.OQ 29-Apr ▲ 174.00 139.00 25.2Bank Mandiri [Buy] BMRI.JK 02-May ▲ 8,400.00 8,000.00 5.0Bank of Nanjing [Buy] 601009.SS 29-Apr ▼ 13.81 15.16 -8.9CJ O Shopping [Hold] 035760.KQ 29-Apr ▼ 256,000.00 266,000.00 -3.8Daegu Bank [Buy] 005270.KS 01-May ▲ 25,000.00 23,000.00 8.7Digital China [Buy] 0861.HK 02-May 19.00 Epistar [Buy] 2448.TW 01-May ▼ 106.00 135.00 -21.5Esprit Holdings Ltd [Buy] 0330.HK 02-May ▼ 49.30 51.40 -4.1Foxconn Technology [Buy] 2354.TW 01-May ▲ 160.00 130.00 23.1GS E&C [Hold] 006360.KS 29-Apr ▲ 132,000.00 124,000.00 6.5HDS [Buy] 069960.KS 02-May ▲ 198,000.00 182,000.00 8.8Hyundai E&C [Buy] 000720.KS 29-Apr ▲ 106,000.00 99,400.00 6.6Hyundai Mobis [Buy] 012330.KS 02-May ▲ 470,000.00 430,000.00 9.3IOI Corp [Hold] IOIB.KL 02-May ▼ 5.50 6.20 -11.3Kia Motors [Buy] 000270.KS 29-Apr ▲ 98,000.00 90,000.00 8.9Lianhua Supermarket [Hold] 0980.HK 02-May ▼ 32.70 35.10 -6.8Orise Technology [Hold] 3545.TW 29-Apr ▼ 69.00 72.00 -4.2S-Oil Corp [Buy] 010950.KS 01-May ▲ 195,000.00 160,000.00 21.9SK Innovation [Buy] 096770.KS 01-May ▲ 300,000.00 236,000.00 27.1Siam Commercial Bank [Buy] SCB.BK 29-Apr ▲ 150.00 138.00 8.7TVS Motor [Buy] TVSM.BO 01-May ▼ 70.00 92.00 -23.9Taiwan Cement [Buy] 1101.TW 02-May ▲ 45.00 34.30 31.2United Phosphorus Ltd [Buy] UNPO.BO 29-Apr ▲ 220.00 210.00 4.8Wilmar International [Hold] WLIL.SI 02-May ▼ 5.20 5.30 -1.9

EPS REVISIONS

Company Ticker Date FY New Previous Chg (%)

ASE [Hold] 2311.TW 29-Apr Dec 10 ▼ 3.01 3.10 -3.0 Dec 11 ▲ 3.04 3.01 1.1 Dec 12 ▲ 3.45 3.41 1.1 Dec 13 ▲ 3.67 3.63 1.0Asustek [Buy] 2357.TW 29-Apr Dec 11 ▲ 22.89 21.90 4.5 Dec 12 ▲ 25.88 24.72 4.7 Dec 13 28.14 Baidu [Buy] BIDU.OQ 29-Apr Dec 11 ▲ 18.33 16.82 9.0 Dec 12 ▲ 28.02 25.17 11.3 Dec 13 38.52 Bank Mandiri [Buy] BMRI.JK 02-May Dec 10 ▲ 0.44 0.42 3.7 Dec 11 ▲ 0.50 0.46 9.5 Dec 12 ▲ 0.55 0.55 0.3 Dec 13 ▲ 0.68 0.68 0.2Bank of China [Buy] 3988.HK 29-Apr Dec 11 ▲ 0.45 0.42 7.4 Dec 12 ▲ 0.51 0.48 6.4 Dec 13 ▼ 0.56 0.58 -4.1Bank of India [Hold] BOI.BO 02-May Mar 11 ▼ 46.38 51.98 -10.8 Mar 12 ▼ 58.53 64.26 -8.9 Mar 13 ▼ 69.77 76.78 -9.1 Mar 14 81.25 Bank of Nanjing [Buy] 601009.SS 29-Apr Dec 10 ▼ 0.96 0.97 -1.6 Dec 11 ▲ 1.05 1.05 0.2 Dec 12 ▼ 1.28 1.33 -4.0 Dec 13 ▼ 1.55 1.69 -8.6

3 May 2011 Strategy Asia Equities Daily Focus

Deutsche Bank AG/Hong Kong Page 5

DAILY REVISIONS: Company Ticker Date New Previous Chg (%)

Bank of Ningbo [Sell] 002142.SZ 29-Apr Dec 11 ▼ 0.97 0.98 -1.2 Dec 12 ▲ 1.23 1.19 3.3 Dec 13 ▼ 1.53 1.56 -2.3CJ O Shopping [Hold] 035760.KQ 29-Apr Dec 10 ▼ 8,588.16 9,217.37 -6.8 Dec 11 ▼ 15,764.72 18,558.95 -15.1 Dec 12 ▼ 17,116.30 21,313.83 -19.7 Dec 13 19,111.26 China Construction Bank [Buy] 0939.HK 29-Apr Dec 11 ▲ 0.65 0.62 5.5 Dec 12 ▼ 0.74 0.74 -0.1 Dec 13 ▲ 0.85 0.78 7.9China Minsheng [Hold] 1988.HK 29-Apr Dec 11 ▲ 0.78 0.67 16.1 Dec 12 ▲ 0.80 0.69 16.6 Dec 13 ▲ 0.92 0.75 22.0DBS Group Holdings Ltd [Buy] DBSM.SI 29-Apr Dec 11 ▼ 1.33 1.38 -3.1 Dec 12 ▼ 1.51 1.53 -1.2 Dec 13 ▲ 1.70 1.69 0.8Daegu Bank [Buy] 005270.KS 01-May Dec 10 0.00 nm Dec 11 0.00 nm Dec 12 0.00 nm Dec 13 0.00 Digital China [Buy] 0861.HK 02-May Mar 09 0.86 Mar 10 0.84 Mar 11 0.93 Mar 12 1.16 Dongfang Electric [Buy] 1072.HK 02-May Dec 10 ▼ 1.30 1.39 -6.6 Dec 11 ▼ 1.61 1.70 -5.2 Dec 12 ▲ 1.74 1.74 0.2 Dec 13 1.75 Epistar [Buy] 2448.TW 01-May Dec 11 ▼ 4.33 6.38 -32.1 Dec 12 ▼ 6.97 8.31 -16.1 Dec 13 8.26 Esprit Holdings Ltd [Buy] 0330.HK 02-May Jun 11 ▼ 2.80 2.89 -3.0 Jun 12 ▼ 3.07 3.29 -6.4 Jun 13 ▼ 3.55 3.75 -5.4Foxconn Technology [Buy] 2354.TW 01-May Dec 10 ▲ 6.84 6.48 5.6 Dec 11 ▲ 9.30 8.58 8.4 Dec 12 ▲ 10.94 9.83 11.4 Dec 13 12.62 GS E&C [Hold] 006360.KS 29-Apr Dec 10 ▼ 8,220.31 8,666.52 -5.1 Dec 11 ▼ 8,858.99 9,165.60 -3.3 Dec 12 ▼ 10,376.63 10,909.24 -4.9 Dec 13 12,200.83 Golden Agri-Resources [Buy] GAGR.SI 02-May Dec 10 ▲ 0.03 0.03 15.1 Dec 11 ▲ 0.04 0.04 0.0 Dec 12 ▲ 0.04 0.04 0.0 Dec 13 0.04 HDS [Buy] 069960.KS 02-May Dec 11 ▲ 14,151.67 13,662.34 3.6 Dec 12 ▲ 16,918.17 16,104.40 5.1 Dec 13 ▲ 19,401.09 18,382.69 5.5Hyundai E&C [Buy] 000720.KS 29-Apr Dec 10 ▼ 4,859.41 5,006.78 -2.9 Dec 11 ▲ 6,470.42 6,436.49 0.5 Dec 12 ▼ 7,747.77 7,852.20 -1.3 Dec 13 ▼ 9,366.84 9,458.62 -1.0Hyundai Mobis [Buy] 012330.KS 02-May Dec 11 ▲ 34,002.73 33,298.77 2.1 Dec 12 ▲ 36,988.31 35,999.63 2.7 Dec 13 41,779.60 IOI Corp [Hold] IOIB.KL 02-May Jun 13 ▲ 0.40 0.37 8.0Industrial Bank [Buy] 601166.SS 29-Apr Dec 11 ▲ 3.66 3.38 8.2 Dec 12 ▲ 4.38 3.91 12.1 Dec 13 ▲ 5.18 4.48 15.5

3 May 2011 Strategy Asia Equities Daily Focus

Page 6 Deutsche Bank AG/Hong Kong

DAILY REVISIONS: Company Ticker Date New Previous Chg (%)

Kia Motors [Buy] 000270.KS 29-Apr Dec 11 ▲ 8,891.52 8,177.60 8.7 Dec 12 ▲ 9,444.86 8,689.00 8.7 Dec 13 9,996.16 Kuala Lumpur Kepong [Buy] KLKK.KL 02-May Sep 11 ▼ 1.20 1.20 0.0 Sep 12 ▲ 1.27 1.22 3.8 Sep 13 ▲ 1.31 1.16 13.1Lianhua Supermarket [Hold] 0980.HK 02-May Dec 11 ▼ 1.17 1.23 -4.7 Dec 12 ▼ 1.40 1.46 -4.4 Dec 13 ▼ 1.68 1.75 -4.1MediaTek [Sell] 2454.TW 29-Apr Dec 10 ▲ 28.44 28.44 0.0 Dec 11 ▼ 15.37 15.52 -1.0 Dec 12 ▼ 16.89 16.89 0.0Orise Technology [Hold] 3545.TW 29-Apr Dec 10 ▲ 3.57 3.56 0.1 Dec 11 ▼ 4.06 4.25 -4.4 Dec 12 ▼ 5.10 5.12 -0.6S-Oil Corp [Buy] 010950.KS 01-May Dec 10 ▲ 5,849.21 5,683.53 2.9 Dec 11 ▲ 16,685.43 12,430.01 34.2 Dec 12 ▲ 18,121.77 13,492.25 34.3 Dec 13 ▲ 18,920.77 14,561.50 29.9SEC [Buy] 005930.KS 29-Apr Dec 11 ▼ 89,427.64 91,641.61 -2.4 Dec 12 ▼ 104,654.23 109,099.02 -4.1SK Innovation [Buy] 096770.KS 01-May Dec 10 ▼ 15,212.74 16,260.19 -6.4 Dec 11 ▲ 27,613.04 18,939.87 45.8 Dec 12 ▲ 28,282.85 21,615.30 30.8 Dec 13 ▲ 32,852.22 13,878.31 136.7SMRT Corporation [Hold] SMRT.SI 29-Apr Mar 11 ▲ 0.11 0.10 2.6 Mar 14 0.14 Shanghai Pudong Bank [Hold] 600000.SS 29-Apr Dec 11 ▲ 1.93 1.85 3.9 Dec 12 ▲ 2.06 2.00 2.8 Dec 13 ▼ 2.40 2.99 -19.7Shriram Transport Finance [Buy] SRTR.BO 01-May Mar 11 ▲ 57.88 56.96 1.6 Mar 12 ▼ 72.66 73.02 -0.5 Mar 13 ▼ 87.27 88.17 -1.0 Mar 14 104.42 Siam Commercial Bank [Buy] SCB.BK 29-Apr Dec 10 ▼ 7.12 7.12 0.0 Dec 11 ▲ 10.84 8.53 27.1 Dec 12 ▲ 10.62 9.73 9.1 Dec 13 11.58 nmTVS Motor [Buy] TVSM.BO 01-May Mar 11 ▼ 4.05 4.18 -2.9 Mar 12 ▼ 5.21 5.93 -12.2 Mar 13 ▼ 6.60 7.13 -7.5Taiwan Cement [Buy] 1101.TW 02-May Dec 10 ▲ 2.38 2.30 3.8 Dec 11 ▲ 2.64 2.63 0.6 Dec 12 ▲ 3.21 3.02 6.4 Dec 13 3.75 Unilever Indonesia [Hold] UNVR.JK 02-May Dec 10 ▼ 443.86 489.05 -9.2 Dec 11 ▼ 499.03 565.32 -11.7 Dec 12 ▼ 564.33 722.17 -21.9 Dec 13 ▼ 620.95 867.21 -28.4United Phosphorus Ltd [Buy] UNPO.BO 29-Apr Mar 11 ▼ 12.56 12.89 -2.6 Mar 12 ▲ 18.24 17.17 6.2 Mar 13 ▲ 20.58 18.86 9.1 Mar 14 24.00 Wilmar International [Hold] WLIL.SI 02-May Dec 10 ▼ 0.20 0.22 -8.8 Dec 11 ▼ 0.26 0.27 -4.3 Dec 12 ▼ 0.29 0.31 -5.3 Dec 13 0.33

Source: Deutsche Bank

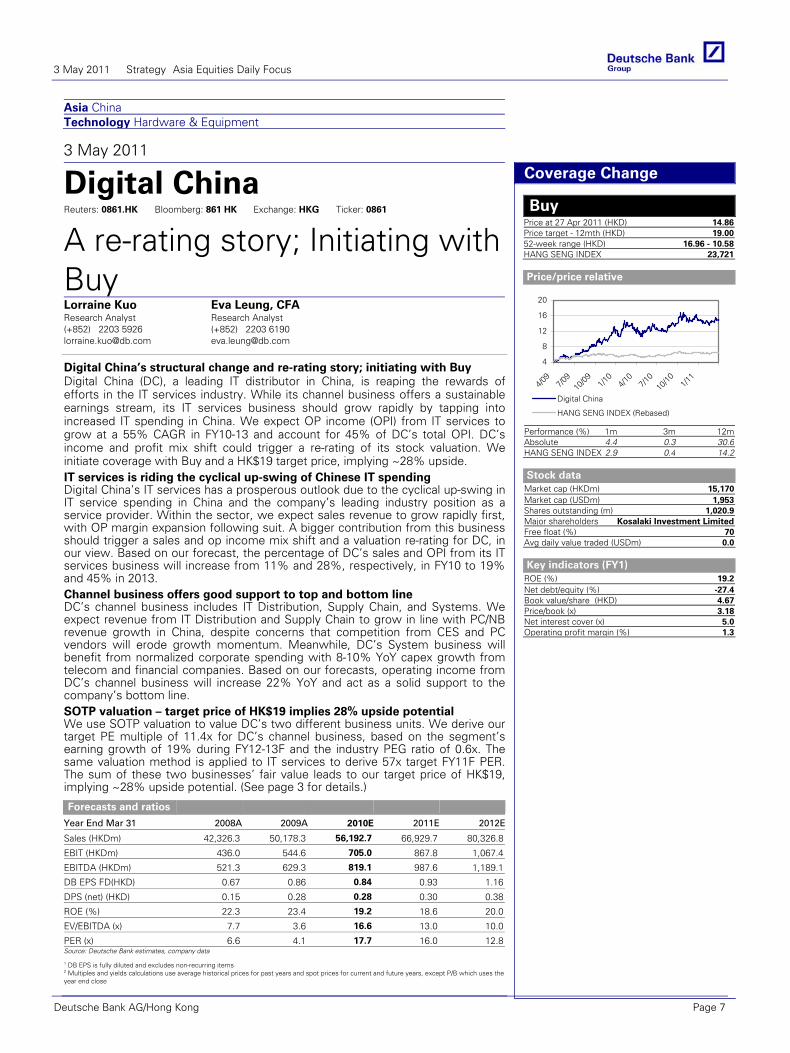

Asia China Technology Hardware & Equipment

3 May 2011

Digital China Reuters: 0861.HK Bloomberg: 861 HK Exchange: HKG Ticker: 0861

A re-rating story; Initiating with Buy Lorraine Kuo Research Analyst (+852) 2203 5926 [email protected]

Eva Leung, CFA Research Analyst (+852) 2203 6190 [email protected]

Digital China’s structural change and re-rating story; initiating with Buy Digital China (DC), a leading IT distributor in China, is reaping the rewards of efforts in the IT services industry. While its channel business offers a sustainable earnings stream, its IT services business should grow rapidly by tapping into increased IT spending in China. We expect OP income (OPI) from IT services to grow at a 55% CAGR in FY10-13 and account for 45% of DC’s total OPI. DC’s income and profit mix shift could trigger a re-rating of its stock valuation. We initiate coverage with Buy and a HK$19 target price, implying ~28% upside.

Forecasts and ratios

Year End Mar 31 2008A 2009A 2010E 2011E 2012E

Sales (HKDm) 42,326.3 50,178.3 56,192.7 66,929.7 80,326.8

EBIT (HKDm) 436.0 544.6 705.0 867.8 1,067.4

EBITDA (HKDm) 521.3 629.3 819.1 987.6 1,189.1

DB EPS FD(HKD) 0.67 0.86 0.84 0.93 1.16

DPS (net) (HKD) 0.15 0.28 0.28 0.30 0.38

ROE (%) 22.3 23.4 19.2 18.6 20.0

EV/EBITDA (x) 7.7 3.6 16.6 13.0 10.0

PER (x) 6.6 4.1 17.7 16.0 12.8Source: Deutsche Bank estimates, company data

1 DB EPS is fully diluted and excludes non-recurring items 2 Multiples and yields calculations use average historical prices for past years and spot prices for current and future years, except P/B which uses the year end close

Deutsche Bank AG/Hong Kong

Coverage Change

Buy Price at 27 Apr 2011 (HKD) 14.86Price target - 12mth (HKD) 19.0052-week range (HKD) 16.96 - 10.58HANG SENG INDEX 23,721

Price/price relative

4

8

12

16

20

4/09

7/09

10/09 1/1

04/1

07/1

010

/10 1/11

Digital China

HANG SENG INDEX (Rebased)

Performance (%) 1m 3m 12mAbsolute 4.4 0.3 30.6HANG SENG INDEX 2.9 0.4 14.2

Stock data

Market cap (HKDm) 15,170Market cap (USDm) 1,953Shares outstanding (m) 1,020.9Major shareholders Kosalaki Investment Limited Free float (%) 70Avg daily value traded (USDm) 0.0

Key indicators (FY1)

ROE (%) 19.2Net debt/equity (%) -27.4Book value/share (HKD) 4.67Price/book (x) 3.18Net interest cover (x) 5.0Operating profit margin (%) 1.3

IT services is riding the cyclical up-swing of Chinese IT spending Digital China’s IT services has a prosperous outlook due to the cyclical up-swing in IT service spending in China and the company’s leading industry position as a service provider. Within the sector, we expect sales revenue to grow rapidly first, with OP margin expansion following suit. A bigger contribution from this business should trigger a sales and op income mix shift and a valuation re-rating for DC, in our view. Based on our forecast, the percentage of DC’s sales and OPI from its IT services business will increase from 11% and 28%, respectively, in FY10 to 19% and 45% in 2013. Channel business offers good support to top and bottom line DC’s channel business includes IT Distribution, Supply Chain, and Systems. We expect revenue from IT Distribution and Supply Chain to grow in line with PC/NB revenue growth in China, despite concerns that competition from CES and PC vendors will erode growth momentum. Meanwhile, DC’s System business will benefit from normalized corporate spending with 8-10% YoY capex growth from telecom and financial companies. Based on our forecasts, operating income from DC’s channel business will increase 22% YoY and act as a solid support to the company’s bottom line. SOTP valuation – target price of HK$19 implies 28% upside potential We use SOTP valuation to value DC’s two different business units. We derive our target PE multiple of 11.4x for DC’s channel business, based on the segment’s earning growth of 19% during FY12-13F and the industry PEG ratio of 0.6x. The same valuation method is applied to IT services to derive 57x target FY11F PER. The sum of these two businesses’ fair value leads to our target price of HK$19, implying ~28% upside potential. (See page 3 for details.)

3 May 2011 Strategy Asia Equities Daily Focus

Deutsche Bank AG/Hong Kong Page 7

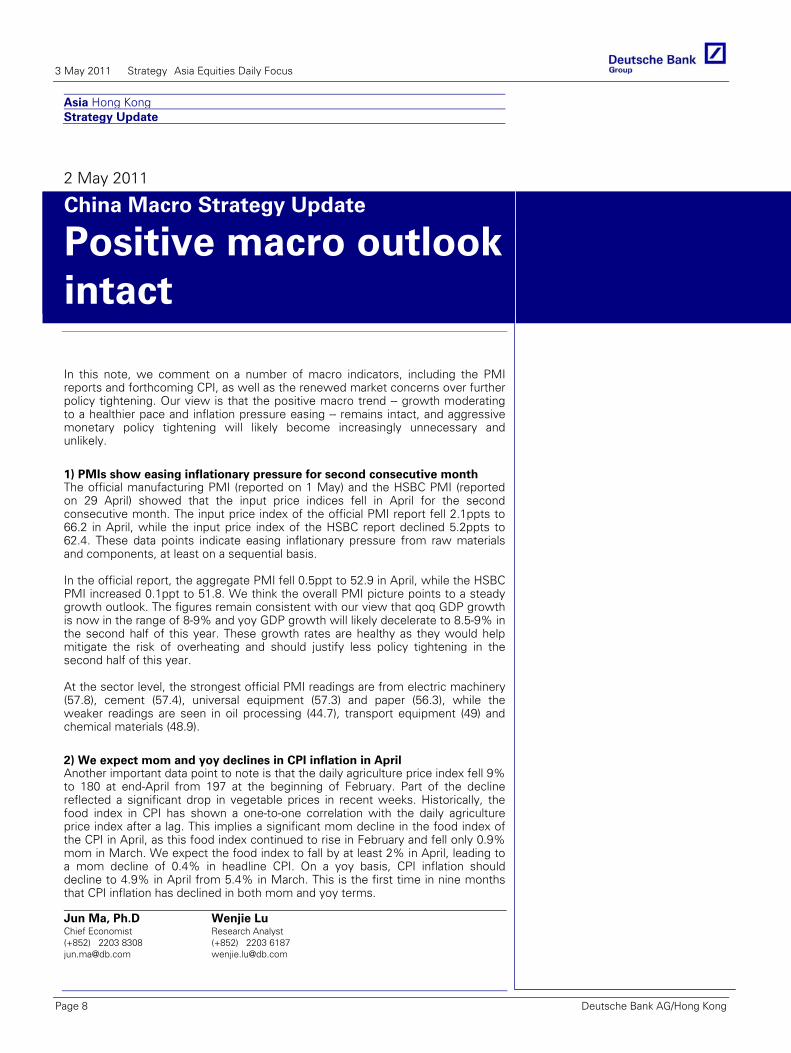

Asia Hong Kong Strategy Update

2 May 2011

China Macro Strategy Update

Positive macro outlook intact

Jun Ma, Ph.D Chief Economist (+852) 2203 8308 [email protected]

Wenjie Lu Research Analyst (+852) 2203 6187 [email protected]

In this note, we comment on a number of macro indicators, including the PMI reports and forthcoming CPI, as well as the renewed market concerns over further policy tightening. Our view is that the positive macro trend -- growth moderating to a healthier pace and inflation pressure easing -- remains intact, and aggressive monetary policy tightening will likely become increasingly unnecessary and unlikely.

1) PMIs show easing inflationary pressure for second consecutive month The official manufacturing PMI (reported on 1 May) and the HSBC PMI (reported on 29 April) showed that the input price indices fell in April for the second consecutive month. The input price index of the official PMI report fell 2.1ppts to 66.2 in April, while the input price index of the HSBC report declined 5.2ppts to 62.4. These data points indicate easing inflationary pressure from raw materials and components, at least on a sequential basis. In the official report, the aggregate PMI fell 0.5ppt to 52.9 in April, while the HSBC PMI increased 0.1ppt to 51.8. We think the overall PMI picture points to a steady growth outlook. The figures remain consistent with our view that qoq GDP growth is now in the range of 8-9% and yoy GDP growth will likely decelerate to 8.5-9% in the second half of this year. These growth rates are healthy as they would help mitigate the risk of overheating and should justify less policy tightening in the second half of this year. At the sector level, the strongest official PMI readings are from electric machinery (57.8), cement (57.4), universal equipment (57.3) and paper (56.3), while the weaker readings are seen in oil processing (44.7), transport equipment (49) and chemical materials (48.9).

2) We expect mom and yoy declines in CPI inflation in April Another important data point to note is that the daily agriculture price index fell 9% to 180 at end-April from 197 at the beginning of February. Part of the decline reflected a significant drop in vegetable prices in recent weeks. Historically, the food index in CPI has shown a one-to-one correlation with the daily agriculture price index after a lag. This implies a significant mom decline in the food index of the CPI in April, as this food index continued to rise in February and fell only 0.9% mom in March. We expect the food index to fall by at least 2% in April, leading to a mom decline of 0.4% in headline CPI. On a yoy basis, CPI inflation should decline to 4.9% in April from 5.4% in March. This is the first time in nine months that CPI inflation has declined in both mom and yoy terms.

3 May 2011 Strategy Asia Equities Daily Focus

Page 8 Deutsche Bank AG/Hong Kong

Asia Hong Kong Consumer Retail/Wholesale Trade

2 May 2011

Esprit Holdings Ltd Reuters: 0330.HK Bloomberg: 330 HK Exchange: HKG Ticker: 0330

Cutting target price on weak wholesale; maintaining BuyAnne Ling Research Analyst (+852) 2203 6177 [email protected]

3Q11 wholesale performance weaker than expected The trend shows that the business is close to bottoming out. Retail performance has been stable and is showing signs of bottoming, with flat SSSG. We maintain our Buy rating despite lowering our EPS forecast for FY11-13 by 3-6% and target price to HK$49.3 because we believe the current share price reflects market expectations that the brand is unlikely to recover. However, we believe that any small improvement in rebranding in 1H12 would result in an improvement in valuation. We thus maintain our Buy rating on Esprit.

Forecasts and ratios

Year End Jun 30 2009A 2010A 2011E 2012E 2013E

Sales (HKDm) 34,485.0 33,734.0 34,267.3 37,107.2 40,160.4

EBITDA (HKDm) 6,505.0 5,766.0 5,464.8 5,992.7 6,872.3

Reported NPAT (HKDm) 4,745.0 4,226.0 3,645.2 4,012.3 4,646.2

Reported EPS FD(HKD) 3.81 3.34 2.80 3.07 3.55

DB EPS FD(HKD) 3.81 2.95 2.80 3.07 3.55

OLD DB EPS FD(HKD) 3.81 2.95 2.89 3.29 3.75

% Change 0.0% 0.0% -3.0% -6.4% -5.4%

DB EPS growth (%) -26.9 -22.6 -5.1 9.9 15.5

PER (x) 13.3 18.0 11.5 10.5 9.1

EV/EBITDA (x) 9.0 10.9 6.5 5.8 5.0

DPS (net) (HKD) 2.84 1.40 1.70 1.87 2.16

Yield (net) (%) 5.6 2.6 5.3 5.8 6.7Source: Deutsche Bank estimates, company data

1 DB EPS is fully diluted and excludes non-recurring items 2 Multiples and yields calculations use average historical prices for past years and spot prices for current and future years, except P/B which uses the year end close

Deutsche Bank AG/Hong Kong

Forecast Change

Buy Price at 29 Apr 2011 (HKD) 32.30Price target - 12mth (HKD) 49.3052-week range (HKD) 56.70 - 32.30HANG SENG INDEX 23,721

Key changes

Price target 51.40 to 49.30 -4.1%Sales (FYE) 33,993 to 34,267 0.8%Op prof margin (FYE) 13.9 to 13.3 -3.9%Net profit (FYE) 3,761.6 to 3,645.2 -3.1%

Price/price relative

30

40

50

60

70

80

4/09 7/09 10/09 1/10 4/10 7/10 10/10 1/11Esprit Holdings Ltd

HANG SENG INDEX (Rebased)

Performance (%) 1m 3m 12mAbsolute -5.8 -13.4 -41.3HANG SENG INDEX 2.9 0.4 14.2

Stock data

Market cap (HKDm) 39,427Market cap (USDm) 5,076Shares outstanding (m) 1,220.6Major shareholders Jurgen, FRIEDRICH (5.18%)Free float (%) 91Avg daily value traded (USDm) 36.255

Key indicators (FY1)

ROE (%) 23.4Net debt/equity (%) -22.6Book value/share (HKD) 12.94Price/book (x) 2.5Net interest cover (x) –Operating profit margin (%) 13.3

Comparatives

Hennes & Mauritz (HMb.ST),SEK213.50 Hold2010A 2011E 2012E

DB EPS (SEK) 11.29 9.95 11.98P/E (x) 20.1 21.5 17.8EV/EBITA (x) 14.2 15.3 12.7Inditex (ITX.MC),EUR60.54 Buy

2011A 2012E 2013EDB EPS (EUR) 2.78 2.98 3.37P/E (x) 18.7 20.3 18.0EV/EBITA (x) 12.4 13.5 11.6

Weak 3Q wholesale performance as short-term orders did not materialize Overall sales declined 3% in Hong Kong dollar terms, but increased 0.7% in LCY for 9MFY11. Retail sales increased 4.8% (8.1% in LCY), and retail SSSG was down 1% (flat for 3Q11). Wholesale sales declined 11.4% (-7.1% in LCY). Wholesale orders fell 8.9% for 3Q11 (vs. a 3% increase in 2Q11) due to the short-term order book not fully materializing during the period.

Lowering our EPS forecast by 3-6% for FY11-13E We lowered our EPS forecast due to weaker 3QFY11 retail space growth and a cotton price hike. A cotton price hike is likely to affect GPM and EBITM for wholesale and retail performance for 2H11 and 1H12, based on the current cotton price trend. We also lowered our yearend retail-space growth from 8%, 6% and 6% to 5%, 6% and 6% for FY11-13, respectively, based on 9MFY11 retail space growth of 2.2%.

Lowering target price to HK$49.3 from HK$51.4; maintaining Buy Our target price is based on a DCF model (we also use DCF for H&M and Inditex), using a WACC of 8.92%, including a country WACC of 7.3% and beta of 1.3. Our target price translates into 16.8x CY11E P/E and 14.9x CY12E P/E. Key risks: new management’s unproven track record, operating performance weaker than the market recovery, product risk and euro volatility.

3 May 2011 Strategy Asia Equities Daily Focus

Deutsche Bank AG/Hong Kong Page 9

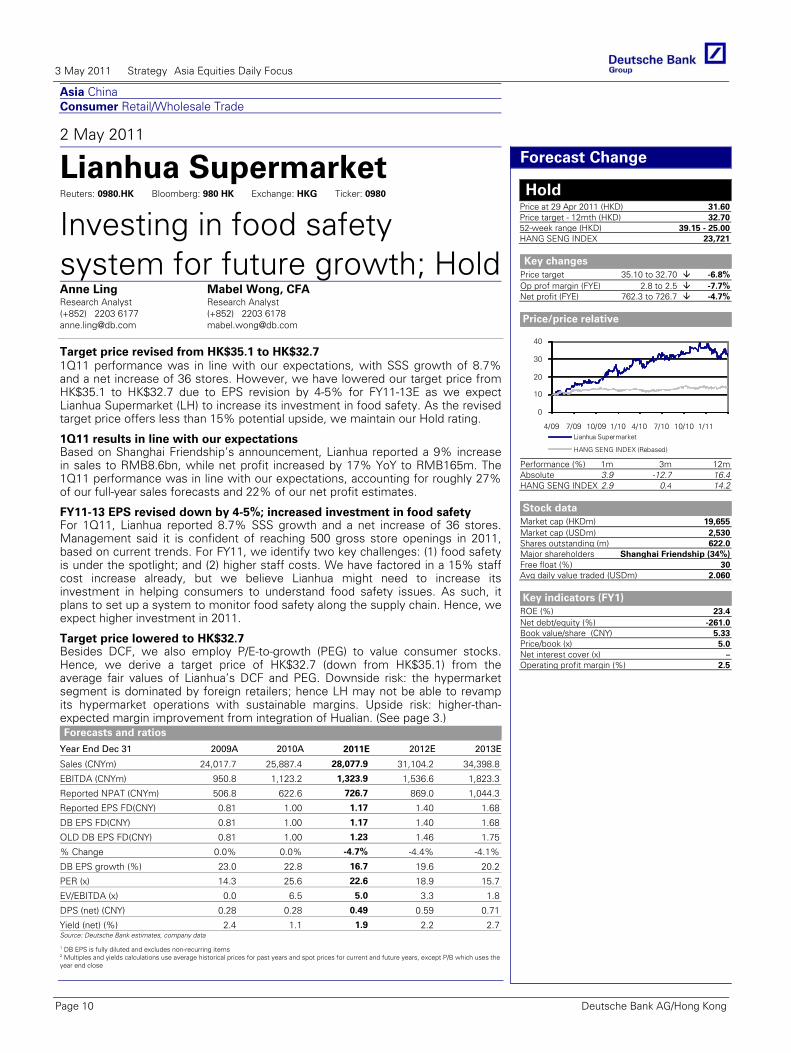

Asia China Consumer Retail/Wholesale Trade

2 May 2011

Lianhua Supermarket Reuters: 0980.HK Bloomberg: 980 HK Exchange: HKG Ticker: 0980

Investing in food safety system for future growth; HoldAnne Ling Research Analyst (+852) 2203 6177 [email protected]

Mabel Wong, CFA Research Analyst (+852) 2203 6178 [email protected]

Target price revised from HK$35.1 to HK$32.7 1Q11 performance was in line with our expectations, with SSS growth of 8.7% and a net increase of 36 stores. However, we have lowered our target price from HK$35.1 to HK$32.7 due to EPS revision by 4-5% for FY11-13E as we expect Lianhua Supermarket (LH) to increase its investment in food safety. As the revised target price offers less than 15% potential upside, we maintain our Hold rating.

Forecasts and ratios

Year End Dec 31 2009A 2010A 2011E 2012E 2013E

Sales (CNYm) 24,017.7 25,887.4 28,077.9 31,104.2 34,398.8

EBITDA (CNYm) 950.8 1,123.2 1,323.9 1,536.6 1,823.3

Reported NPAT (CNYm) 506.8 622.6 726.7 869.0 1,044.3

Reported EPS FD(CNY) 0.81 1.00 1.17 1.40 1.68

DB EPS FD(CNY) 0.81 1.00 1.17 1.40 1.68

OLD DB EPS FD(CNY) 0.81 1.00 1.23 1.46 1.75

% Change 0.0% 0.0% -4.7% -4.4% -4.1%

DB EPS growth (%) 23.0 22.8 16.7 19.6 20.2

PER (x) 14.3 25.6 22.6 18.9 15.7

EV/EBITDA (x) 0.0 6.5 5.0 3.3 1.8

DPS (net) (CNY) 0.28 0.28 0.49 0.59 0.71

Yield (net) (%) 2.4 1.1 1.9 2.2 2.7Source: Deutsche Bank estimates, company data

1 DB EPS is fully diluted and excludes non-recurring items 2 Multiples and yields calculations use average historical prices for past years and spot prices for current and future years, except P/B which uses the year end close

Deutsche Bank AG/Hong Kong

Forecast Change

Hold Price at 29 Apr 2011 (HKD) 31.60Price target - 12mth (HKD) 32.7052-week range (HKD) 39.15 - 25.00HANG SENG INDEX 23,721

Key changes

Price target 35.10 to 32.70 -6.8%Op prof margin (FYE) 2.8 to 2.5 -7.7%Net profit (FYE) 762.3 to 726.7 -4.7%

Price/price relative

0

10

20

30

40

4/09 7/09 10/09 1/10 4/10 7/10 10/10 1/11Lianhua Supermarket

HANG SENG INDEX (Rebased)

Performance (%) 1m 3m 12mAbsolute 3.9 -12.7 16.4HANG SENG INDEX 2.9 0.4 14.2

Stock data

Market cap (HKDm) 19,655Market cap (USDm) 2,530Shares outstanding (m) 622.0Major shareholders Shanghai Friendship (34%)Free float (%) 30Avg daily value traded (USDm) 2.060

Key indicators (FY1)

ROE (%) 23.4Net debt/equity (%) -261.0Book value/share (CNY) 5.33Price/book (x) 5.0Net interest cover (x) –Operating profit margin (%) 2.5

1Q11 results in line with our expectations Based on Shanghai Friendship’s announcement, Lianhua reported a 9% increase in sales to RMB8.6bn, while net profit increased by 17% YoY to RMB165m. The 1Q11 performance was in line with our expectations, accounting for roughly 27% of our full-year sales forecasts and 22% of our net profit estimates.

FY11-13 EPS revised down by 4-5%; increased investment in food safety For 1Q11, Lianhua reported 8.7% SSS growth and a net increase of 36 stores. Management said it is confident of reaching 500 gross store openings in 2011, based on current trends. For FY11, we identify two key challenges: (1) food safety is under the spotlight; and (2) higher staff costs. We have factored in a 15% staff cost increase already, but we believe Lianhua might need to increase its investment in helping consumers to understand food safety issues. As such, it plans to set up a system to monitor food safety along the supply chain. Hence, we expect higher investment in 2011.

Target price lowered to HK$32.7 Besides DCF, we also employ P/E-to-growth (PEG) to value consumer stocks. Hence, we derive a target price of HK$32.7 (down from HK$35.1) from the average fair values of Lianhua’s DCF and PEG. Downside risk: the hypermarket segment is dominated by foreign retailers; hence LH may not be able to revamp its hypermarket operations with sustainable margins. Upside risk: higher-than-expected margin improvement from integration of Hualian. (See page 3.)

3 May 2011 Strategy Asia Equities Daily Focus

Page 10 Deutsche Bank AG/Hong Kong

Asia Taiwan Resources Construction Materials

2 May 2011

Taiwan Cement Reuters: 1101.TW Bloomberg: 1101 TT Exchange: TAI Ticker: 1101

Growth momentum continues; raising price target to NT$45Yvonne Tsai Research Analyst (+886) 2 2192 2824 [email protected]

James Kan Research Analyst (+852) 2203 6146 [email protected]

Factoring in mid- to long-term growth profile We are raising Taiwan Cement's PT from NT$34.4 to NT$45. In response to 1Q11 results, we have increased its 2011 OP (domestic cement operations) by 45% and earnings contribution from its Chinese cement operations by 20%. Together with a rollover of the valuation to 2H11-1H12 earnings, this leads to an upgrade in our cement business valuation of c.50% or ~NT$6/share. Mark-to-market for other listed equity investments and decreased net debt also boost the PT by another NT$4/share. With a solid outlook for the cement operations, we maintain Buy.

Forecasts and ratios

Year End Dec 31 2009A 2010A 2011E 2012E 2013E

Sales (TWDm) 20,904.1 22,097.1 24,800.1 27,295.8 27,748.6

Reported NPAT (TWDm) 7,424.5 8,031.3 9,764.5 11,853.3 13,842.2

DB EPS FD(TWD) 2.26 2.38 2.64 3.21 3.75

OLD DB EPS FD(TWD) 2.26 2.30 2.63 3.02 –

% Change 0.0% 3.8% 0.6% 6.4% –

DB EPS growth (%) 28.6 5.7 10.9 21.4 16.8

PER (x) 14.4 12.8 15.9 13.1 11.2

Yield (net) (%) 5.6 6.6 5.0 6.1 7.1Source: Deutsche Bank estimates, company data

1 DB EPS is fully diluted and excludes non-recurring items 2 Multiples and yields calculations use average historical prices for past years and spot prices for current and future years, except P/B which uses the year end close

Deutsche Bank AG/Hong Kong

Forecast Change

Buy Price at 29 Apr 2011 (TWD) 41.95Price target - 12mth (TWD) 45.0052-week range (TWD) 42.60 - 25.40TWSE 9,008

Key changes

Price target 34.30 to 45.00 31.2%Sales (FYE) 25,032 to 24,800 -0.9%Op prof margin (FYE) 2.5 to 3.7 46.5%Net profit (FYE) 9,704.7 to 9,764.5 0.6%

Price/price relative

2428323640444852

4/09 7/09 10/09 1/10 4/10 7/10 10/10 1/11Taiwan Cement

TWSE (Rebased)

Performance (%) 1m 3m 12mAbsolute 18.2 33.8 48.2TWSE 4.8 -1.5 11.8

Stock data

Market cap (TWDm) 154,887Market cap (USDm) 5,408Shares outstanding (m) 3,692.2Major shareholders Koo family (10%)Free float (%) 86Avg daily value traded (USDm) 25.1

Key indicators (FY1)

ROE (%) 10.2Net debt/equity (%) 0.9Book value/share (TWD) 26.35Price/book (x) 1.59Net interest cover (x) 4.9Operating profit margin (%) 3.7

1Q11 results reinforce our view on robust cement profitability TCC reported solid results for cement operations in 1Q11, though its bottom line was dragged down by one-off losses and Hoping Power's weak earnings in the quarter. However, we maintain our FY11 profit forecast as we believe the strong 1Q momentum in cement could continue in the coming quarters and offset the weakness at Hoping Power. We raise our 2012 net profit forecast by 6%. We are 4% and 13% above consensus for 2011 and 2012 NP estimates, respectively.

Cement in China to stay favourable in the mid-to-long term We remain positive on the demand-supply outlook in the greater Guangdong market in the mid-to-long term. We expect net cement capacity growth in China to be moderate, with gross new additions offset by phase-outs. Guangdong will likely have new capacity addition of ~7mt p.a. in 2011-12, while total phase-out from 2011 to 2015 should be 37mtpa (average 7-7.5mt p.a.). We also believe cement demand in Guangdong has not yet reached saturation. The social housing program and infrastructure projects should continue to boost demand.

SOTP valuation with cement business valued on 2H11-1H12 earnings We believe a mid- to long-term growth profile in the cement industry justifies valuing TCC's cement business on 2H11-1H12 rolling earnings. We adopt regional cement peers’ average P/E at 13.2x and derive a price target of NT$45 via a SOTP valuation, with our 10% non-core discount maintained. TCC is now trading at 1.6x 2011 BVPS, slightly above its historical average of 1.57x P/B. Yet, with a cement industry upcycle and TCC's close-to-peak ROE, we believe the valuation is not stretched. Key risks: China government loosening its curb on cement capacity.

3 May 2011 Strategy Asia Equities Daily Focus

Deutsche Bank AG/Hong Kong Page 11

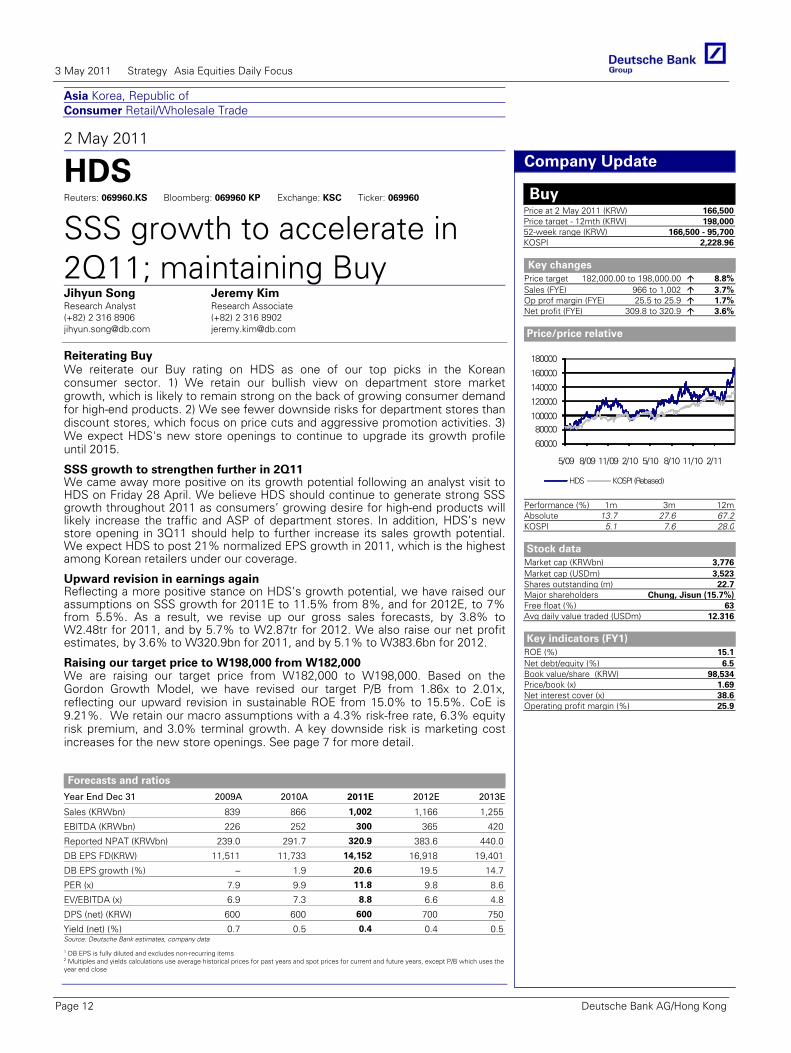

Asia Korea, Republic of Consumer Retail/Wholesale Trade

2 May 2011

HDS Reuters: 069960.KS Bloomberg: 069960 KP Exchange: KSC Ticker: 069960

SSS growth to accelerate in 2Q11; maintaining BuyJihyun Song Research Analyst (+82) 2 316 8906 [email protected]

Jeremy Kim Research Associate (+82) 2 316 8902 [email protected]

Reiterating Buy We reiterate our Buy rating on HDS as one of our top picks in the Korean consumer sector. 1) We retain our bullish view on department store market growth, which is likely to remain strong on the back of growing consumer demand for high-end products. 2) We see fewer downside risks for department stores than discount stores, which focus on price cuts and aggressive promotion activities. 3) We expect HDS's new store openings to continue to upgrade its growth profile until 2015.

Forecasts and ratios

Year End Dec 31 2009A 2010A 2011E 2012E 2013E

Sales (KRWbn) 839 866 1,002 1,166 1,255

EBITDA (KRWbn) 226 252 300 365 420

Reported NPAT (KRWbn) 239.0 291.7 320.9 383.6 440.0

DB EPS FD(KRW) 11,511 11,733 14,152 16,918 19,401

DB EPS growth (%) – 1.9 20.6 19.5 14.7

PER (x) 7.9 9.9 11.8 9.8 8.6

EV/EBITDA (x) 6.9 7.3 8.8 6.6 4.8

DPS (net) (KRW) 600 600 600 700 750

Yield (net) (%) 0.7 0.5 0.4 0.4 0.5Source: Deutsche Bank estimates, company data

1 DB EPS is fully diluted and excludes non-recurring items 2 Multiples and yields calculations use average historical prices for past years and spot prices for current and future years, except P/B which uses the year end close

Deutsche Bank AG/Hong Kong

Company Update

Buy Price at 2 May 2011 (KRW) 166,500Price target - 12mth (KRW) 198,00052-week range (KRW) 166,500 - 95,700KOSPI 2,228.96

Key changes

Price target 182,000.00 to 198,000.00 8.8%Sales (FYE) 966 to 1,002 3.7%Op prof margin (FYE) 25.5 to 25.9 1.7%Net profit (FYE) 309.8 to 320.9 3.6%

Price/price relative

60000

80000100000

120000

140000

160000

180000

5/09 8/09 11/09 2/10 5/10 8/10 11/10 2/11

HDS KOSPI (Rebased)

Performance (%) 1m 3m 12mAbsolute 13.7 27.6 67.2KOSPI 5.1 7.6 28.0

Stock data

Market cap (KRWbn) 3,776Market cap (USDm) 3,523Shares outstanding (m) 22.7Major shareholders Chung, Jisun (15.7%)Free float (%) 63Avg daily value traded (USDm) 12.316

Key indicators (FY1)

ROE (%) 15.1Net debt/equity (%) 6.5Book value/share (KRW) 98,534Price/book (x) 1.69Net interest cover (x) 38.6Operating profit margin (%) 25.9

Glo

bal

Mar

kets

Res

earc

h

SSS growth to strengthen further in 2Q11 We came away more positive on its growth potential following an analyst visit to HDS on Friday 28 April. We believe HDS should continue to generate strong SSS growth throughout 2011 as consumers’ growing desire for high-end products will likely increase the traffic and ASP of department stores. In addition, HDS’s new store opening in 3Q11 should help to further increase its sales growth potential. We expect HDS to post 21% normalized EPS growth in 2011, which is the highest among Korean retailers under our coverage.

Upward revision in earnings again Reflecting a more positive stance on HDS’s growth potential, we have raised our assumptions on SSS growth for 2011E to 11.5% from 8%, and for 2012E, to 7% from 5.5%. As a result, we revise up our gross sales forecasts, by 3.8% to W2.48tr for 2011, and by 5.7% to W2.87tr for 2012. We also raise our net profit estimates, by 3.6% to W320.9bn for 2011, and by 5.1% to W383.6bn for 2012.

Raising our target price to W198,000 from W182,000 We are raising our target price from W182,000 to W198,000. Based on the Gordon Growth Model, we have revised our target P/B from 1.86x to 2.01x, reflecting our upward revision in sustainable ROE from 15.0% to 15.5%. CoE is 9.21%. We retain our macro assumptions with a 4.3% risk-free rate, 6.3% equity risk premium, and 3.0% terminal growth. A key downside risk is marketing cost increases for the new store openings. See page 7 for more detail.

3 May 2011 Strategy Asia Equities Daily Focus

Page 12 Deutsche Bank AG/Hong Kong

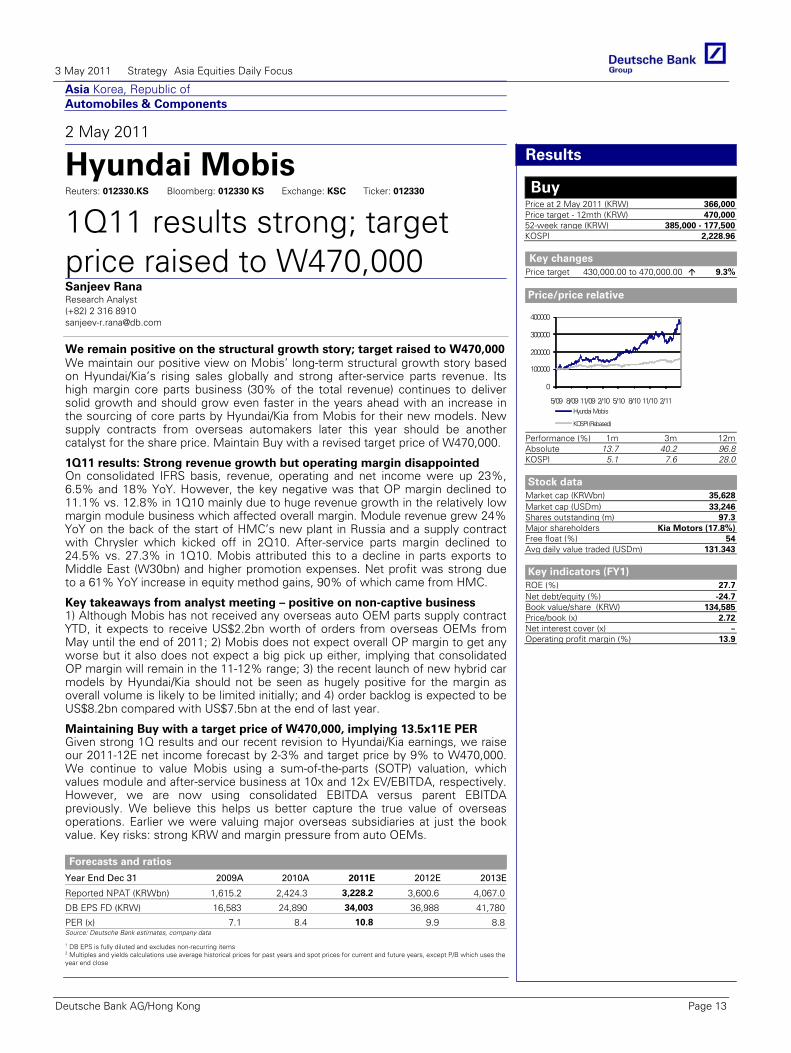

Asia Korea, Republic of Automobiles & Components

2 May 2011

Hyundai Mobis Reuters: 012330.KS Bloomberg: 012330 KS Exchange: KSC Ticker: 012330

1Q11 results strong; target price raised to W470,000Sanjeev Rana Research Analyst (+82) 2 316 8910 [email protected]

We remain positive on the structural growth story; target raised to W470,000 We maintain our positive view on Mobis’ long-term structural growth story based on Hyundai/Kia’s rising sales globally and strong after-service parts revenue. Its high margin core parts business (30% of the total revenue) continues to deliver solid growth and should grow even faster in the years ahead with an increase in the sourcing of core parts by Hyundai/Kia from Mobis for their new models. New supply contracts from overseas automakers later this year should be another catalyst for the share price. Maintain Buy with a revised target price of W470,000.

Forecasts and ratios

Year End Dec 31 2009A 2010A 2011E 2012E 2013E

Reported NPAT (KRWbn) 1,615.2 2,424.3 3,228.2 3,600.6 4,067.0

DB EPS FD (KRW) 16,583 24,890 34,003 36,988 41,780

PER (x) 7.1 8.4 10.8 9.9 8.8Source: Deutsche Bank estimates, company data

1 DB EPS is fully diluted and excludes non-recurring items 2 Multiples and yields calculations use average historical prices for past years and spot prices for current and future years, except P/B which uses the year end close

Deutsche Bank AG/Hong Kong

Results

Buy Price at 2 May 2011 (KRW) 366,000Price target - 12mth (KRW) 470,00052-week range (KRW) 385,000 - 177,500KOSPI 2,228.96

Key changes

Price target 430,000.00 to 470,000.00 9.3%

Price/price relative

0

100000

200000

300000

400000

5/09 8/09 11/09 2/10 5/10 8/10 11/10 2/11Hyundai Mobis

KOSPI (Rebased)

Performance (%) 1m 3m 12mAbsolute 13.7 40.2 96.8KOSPI 5.1 7.6 28.0

Stock data

Market cap (KRWbn) 35,628Market cap (USDm) 33,246Shares outstanding (m) 97.3Major shareholders Kia Motors (17.8%)Free float (%) 54Avg daily value traded (USDm) 131.343

Key indicators (FY1)

ROE (%) 27.7Net debt/equity (%) -24.7Book value/share (KRW) 134,585Price/book (x) 2.72Net interest cover (x) –Operating profit margin (%) 13.9

1Q11 results: Strong revenue growth but operating margin disappointed On consolidated IFRS basis, revenue, operating and net income were up 23%, 6.5% and 18% YoY. However, the key negative was that OP margin declined to 11.1% vs. 12.8% in 1Q10 mainly due to huge revenue growth in the relatively low margin module business which affected overall margin. Module revenue grew 24% YoY on the back of the start of HMC’s new plant in Russia and a supply contract with Chrysler which kicked off in 2Q10. After-service parts margin declined to 24.5% vs. 27.3% in 1Q10. Mobis attributed this to a decline in parts exports to Middle East (W30bn) and higher promotion expenses. Net profit was strong due to a 61% YoY increase in equity method gains, 90% of which came from HMC.

Key takeaways from analyst meeting – positive on non-captive business 1) Although Mobis has not received any overseas auto OEM parts supply contract YTD, it expects to receive US$2.2bn worth of orders from overseas OEMs from May until the end of 2011; 2) Mobis does not expect overall OP margin to get any worse but it also does not expect a big pick up either, implying that consolidated OP margin will remain in the 11-12% range; 3) the recent launch of new hybrid car models by Hyundai/Kia should not be seen as hugely positive for the margin as overall volume is likely to be limited initially; and 4) order backlog is expected to be US$8.2bn compared with US$7.5bn at the end of last year.

Maintaining Buy with a target price of W470,000, implying 13.5x11E PER Given strong 1Q results and our recent revision to Hyundai/Kia earnings, we raise our 2011-12E net income forecast by 2-3% and target price by 9% to W470,000. We continue to value Mobis using a sum-of-the-parts (SOTP) valuation, which values module and after-service business at 10x and 12x EV/EBITDA, respectively. However, we are now using consolidated EBITDA versus parent EBITDA previously. We believe this helps us better capture the true value of overseas operations. Earlier we were valuing major overseas subsidiaries at just the book value. Key risks: strong KRW and margin pressure from auto OEMs.

3 May 2011 Strategy Asia Equities Daily Focus

Deutsche Bank AG/Hong Kong Page 13

Asia

2 May 2011

Asia Economics Daily

Mixed news on inflation in April

Deutsche Bank AG/Hong Kong

Michael Spencer, Ph.D Chief Economist, Asia (+852) 2203 8303 [email protected]

Jun Ma, Ph.D Chief Economist, Greater China (+852) 2203 8308 [email protected]

Taimur Baig, Ph.D Chief Economist, India (+65) 6423 8681 [email protected]

Juliana Lee Senior Economist (+852) 2203 8312 [email protected]

Kaushik Das Economist (+91) 22 6658 4909 [email protected]

Mac

ro

Eco

no

mic

s

HIGHLIGHTS

Indonesia - Inflation eases further in April, led by lower food prices; Trade surplus narrows to USD1.8bn in March, on high import growth

India - Trade deficit narrows to USD 5.6bn on lower imports growth South Korea - Inflation surprise to the downside in April; Exports rise by 26.6%yoy in April, above expectations Thailand - Inflation reached 4% mark in April, well above expectations Sri Lanka - CPI inflation touches 9.8%yoy in April, rate hike ahead; Exports growth eases to 36.8%yoy in February, well

below our expectation UPCOMING RELEASES

Hong Kong – Retail sales (vol) (Mar) DB forecast 14.5% (5.1% in Feb) India – We expect the RBI to raise policy rates by 25bps in response to rising inflation.

NEWS IN BRIEF

INDONESIA CPI inflation (Apr). Lower food prices brought headline CPI inflation down further in April, to 6.2%yoy from 6.7% in March, well below our (6.7%) as well as consensus (6.4%) forecasts. Food inflation slowed for the third straight month to 11.1% from a peak of 16.2% in January-2011. But core inflation edged up to 4.6% from 4.5% suggesting still robust demand-side pressures. Inflation was stable in the transportation (2.93% vs. 2.90%), housing (4.72% vs. 4.61%) and education (3.91% vs. 3.84%) categories. Today's data show that inflation is returning to a stable state for now as administrative prices remain frozen. When and as petrol, LPG, electricity, toll, and transportation tariffs are adjusted, inflation would rise by another 200bps, in our view. This risk plus the rising core inflation should keep Bank Indonesia on alert, but we don’t expect them to act aggressively unless it appears that inflation is at risk of getting out of control. Hence, we expect a continued moderate pace of rate hikes. We expect BI to pause this month but see the central bank hiking rates by 25bps next month. External trade (Mar). Export growth slowed to 27.5%yoy in March from 29.1% in February. This was better than our as well as consensus expectations of 22.5% and 25.4% respectively. Oil exports rose 36.9%, up from 20.1% in February, reflecting rising international oil prices. On the other hand, non-oil exports growth slowed to 25.6% in March, from 31.3% in February. Meanwhile, imports outpaced expectations, expanding by 32.0% in March up from 23.7% in February, suggesting buoyant domestic demand. This brought down the trade surplus to USD1.8bn from USD2.7bn in February. We expect rising international energy/commodity prices and strong demand from G2 countries as well as other emerging nations will continue to support export growth in the months ahead.

3 May 2011 Strategy Asia Equities Daily Focus

Page 14 Deutsche Bank AG/Hong Kong

INDIA External trade (Mar). As expected, export growth slowed to 43.9%yoy in March, from 49.7% in February. With import growth also moderating -- to 17.3% from 21.2% in February -- the trade deficit narrowed to USD5.6bn in March from USD8.1bn in February. Within imports, non-oil imports growth slowed to 21.0% in March from. 31.0% in February. However, reflecting mostly higher prices we think, oil imports increased sharply to 8.2%yoy in March against a decline of 0.3% in February.

SOUTH KOREA CPI inflation (Apr). After reaching a 29-month high of 4.7%yoy in March, CPI inflation eased to 4.2% in April and was below the consensus (4.6%) as well as our (4.4%) expectation. By category, this downward surprise was led by lower food prices, which slowed to 7.6% in April down sharply from 10.9% in March. Also, transport inflation eased somewhat last month, to 7.0% from 7.9% in March. In contrast, housing inflation rose to 4.3% in April, up from 4.1% and 3.7% respectively in the last two months. So core inflation, which excludes volatile food and energy components, slowed to 3.2% in April from 3.3% in March. Although we see a modest slowdown in inflation ahead we still expect it to stay above the 4% mark for the coming few months primed by high energy/commodity and housing costs. Given that inflation has already breached the central bank’s target and growth momentum seems intact, we expect the BoK to deliver 25bps rate hike in its policy meeting next week. But for rest of the year beyond that we expect only one more 25bps rate hike as debt concerns weigh on policy and the won is expected to appreciate further.

External trade (Apr). Exports rose by 26.6%yoy in April, albeit slightly lower than 28.9% (revised) growth reported in March but above the consensus (23.7%) as well as our (20.0%) forecasts. The slowdown was led by volatile vessel exports, which fell 20.2% in April, following 67% growth in March. On the other hand, electric/electronics (7.5% in Apr vs. 6.9% in Mar), steel (39.7% vs. 39.1%) and chemical products (29.3% vs. 28.5%) all witnessed strong growth during April. By destination, exports to China and Europe, slowed to 9.3% and 4.5% respectively in April, from 18.1% and 23.6% in March. However, exports to Japan and US rose at a faster pace of 70.1% and 23.0% during the month vs. 53.8% and 14.4% in March. It’s hard to see an impact from Japan’s earthquake in these data. With imports rising at a relatively slower pace of 23.7% in April vs. 27.3% in March, the trade surplus widened from USD2.8bn to USD5.8bn in April. We expect strong demand from G2 and regional countries will continue to drive high exports growth ahead, also we see high import bill led by rising international oil prices

THAILAND CPI inflation (Apr). Headline inflation rose to a 30-month high of 4.0%yoy in April, up sharply from 3.1% reported in March and was significantly higher than our (3.5%) as well as consensus (3.2%) expectations. Unlike Korea and Indonesia, food inflation in Thailand rose in April, to 8.6% from 5.9% in March, reflecting higher prices in vegetables (20.6%) and meat/poultry/fish (8.9%). In the non-food segment, transport inflation remained broadly stable at 2.5%, while housing inflation slowed from 1.2% to 0.6% in April. Meanwhile, reflecting robust expansion in domestic demand, the core inflation rate rose in April, to 2.1% from 1.6% in March. This upside surprise further cements our view of another 25bps rate hike at the next MPC and two more thereafter as inflationary pressure rises amid sustained growth..

SRI LANKA CPI inflation (Apr). Headline inflation rose to a 29-month high of 9.8%yoy in April, 120bps higher than March's reading and was broadly in line with our expectation of 9.9%. Almost all sub-segments reported an acceleration in inflation in April. Food inflation rose 14.3% in April up from 13.9% in March, due to the unfortunate flooding incident in Sri Lanka in early 2011 as well as a sharp spike in global food prices. Also, transport and housing inflation jumped to 5.3% and 6.8% respectively in April, from 2.4% and 3.6% in March. We expect CPI inflation to rise to double-digits in the coming months as the ongoing surge in international food/fuel inflation continue to put pressure on the overall price index. Given rising inflation pressure and strong growth momentum we expect the CBSL to deliver 100bps rate hike in rest of the year with the first 25bps hike to be expected in June.

External trade (Feb). As base effect drops out from the data, export growth slowed to 36.8%yoy in February, sharply down from 72.4% in January and was weaker than our forecast of 55.0%. Industrial (45.4% in Feb vs. 92.5% in Jan), Agri (11.6% vs. 28.9%) and minerals (13.6% vs. 49.5%) exports all witnessed slowdown in growth during February. With imports rising by 27.0% in February vs. 21.3% in January, the trade deficit narrowed from USD0.7bn to USD0.4bn in April.

3 May 2011 Strategy Asia Equities Daily Focus

Deutsche Bank AG/Hong Kong Page 15

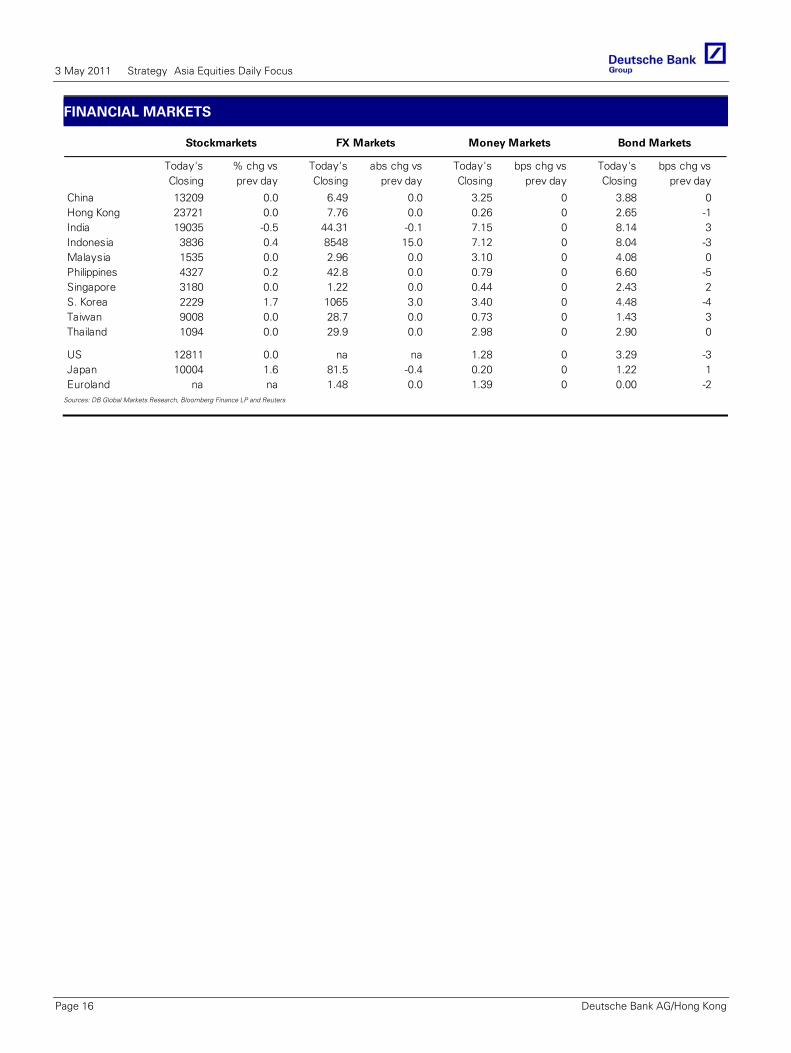

FINANCIAL MARKETS

Today's % chg vs Today's abs chg vs Today's bps chg vs Today's bps chg vsClosing prev day Closing prev day Closing prev day Closing prev day

China 13209 0.0 6.49 0.0 3.25 0 3.88 0Hong Kong 23721 0.0 7.76 0.0 0.26 0 2.65 -1India 19035 -0.5 44.31 -0.1 7.15 0 8.14 3Indonesia 3836 0.4 8548 15.0 7.12 0 8.04 -3Malaysia 1535 0.0 2.96 0.0 3.10 0 4.08 0Philippines 4327 0.2 42.8 0.0 0.79 0 6.60 -5Singapore 3180 0.0 1.22 0.0 0.44 0 2.43 2S. Korea 2229 1.7 1065 3.0 3.40 0 4.48 -4Taiwan 9008 0.0 28.7 0.0 0.73 0 1.43 3Thailand 1094 0.0 29.9 0.0 2.98 0 2.90 0

US 12811 0.0 na na 1.28 0 3.29 -3Japan 10004 1.6 81.5 -0.4 0.20 0 1.22 1Euroland na na 1.48 0.0 1.39 0 0.00 -2

Stockmarkets FX Markets Money Markets Bond Markets

Sources: DB Global Markets Research, Bloomberg Finance LP and Reuters

3 May 2011 Strategy Asia Equities Daily Focus

Page 16 Deutsche Bank AG/Hong Kong

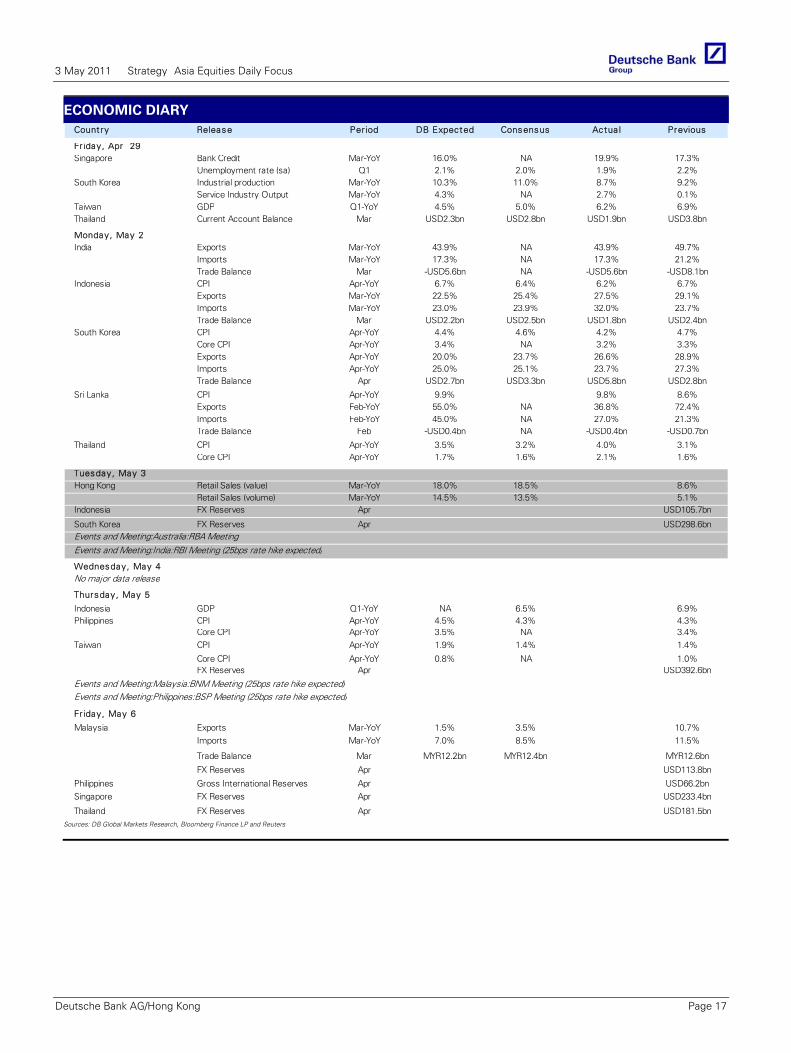

ECONOMIC DIARY Country Release Period DB Expected Consensus Actua l Previous

Fr iday, Apr 29Singapore Bank Credit Mar-YoY 16.0% NA 19.9% 17.3%

Unemployment rate (sa) Q1 2.1% 2.0% 1.9% 2.2%South Korea Industrial production Mar-YoY 10.3% 11.0% 8.7% 9.2%

Service Industry Output Mar-YoY 4.3% NA 2.7% 0.1%Taiwan GDP Q1-YoY 4.5% 5.0% 6.2% 6.9%Thailand Current Account Balance Mar USD2.3bn USD2.8bn USD1.9bn USD3.8bn

Monday, May 2India Exports Mar-YoY 43.9% NA 43.9% 49.7%

Imports Mar-YoY 17.3% NA 17.3% 21.2%Trade Balance Mar -USD5.6bn NA -USD5.6bn -USD8.1bn

Indonesia CPI Apr-YoY 6.7% 6.4% 6.2% 6.7%Exports Mar-YoY 22.5% 25.4% 27.5% 29.1%Imports Mar-YoY 23.0% 23.9% 32.0% 23.7%Trade Balance Mar USD2.2bn USD2.5bn USD1.8bn USD2.4bn

South Korea CPI Apr-YoY 4.4% 4.6% 4.2% 4.7%Core CPI Apr-YoY 3.4% NA 3.2% 3.3%Exports Apr-YoY 20.0% 23.7% 26.6% 28.9%Imports Apr-YoY 25.0% 25.1% 23.7% 27.3%Trade Balance Apr USD2.7bn USD3.3bn USD5.8bn USD2.8bn

Sri Lanka CPI Apr-YoY 9.9% 9.8% 8.6%Exports Feb-YoY 55.0% NA 36.8% 72.4%Imports Feb-YoY 45.0% NA 27.0% 21.3%Trade Balance Feb -USD0.4bn NA -USD0.4bn -USD0.7bn

Thailand CPI Apr-YoY 3.5% 3.2% 4.0% 3.1%Core CPI Apr-YoY 1.7% 1.6% 2.1% 1.6%

Tuesday, May 3Hong Kong Retail Sales (value) Mar-YoY 18.0% 18.5% 8.6%

Retail Sales (volume) Mar-YoY 14.5% 13.5% 5.1%Indonesia FX Reserves Apr USD105.7bn

South Korea FX Reserves Apr USD298.6bnEvents and Meeting:Australia:RBA MeetingEvents and Meeting:India:RBI Meeting (25bps rate hike expected)

Wednesday, May 4No major data release

Thursday, May 5

Indonesia GDP Q1-YoY NA 6.5% 6.9%Philippines CPI Apr-YoY 4.5% 4.3% 4.3%

Core CPI Apr-YoY 3.5% NA 3.4%Taiwan CPI Apr-YoY 1.9% 1.4% 1.4%

Core CPI Apr-YoY 0.8% NA 1.0%FX Reserves Apr USD392.6bn

Events and Meeting:Malaysia:BNM Meeting (25bps rate hike expected)Events and Meeting:Philippines:BSP Meeting (25bps rate hike expected)

Fr iday, May 6

Malaysia Exports Mar-YoY 1.5% 3.5% 10.7%Imports Mar-YoY 7.0% 8.5% 11.5%

Trade Balance Mar MYR12.2bn MYR12.4bn MYR12.6bn

FX Reserves Apr USD113.8bn

Philippines Gross International Reserves Apr USD66.2bnSingapore FX Reserves Apr USD233.4bn

Thailand FX Reserves Apr USD181.5bnSources: DB Global Markets Research, Bloomberg Finance LP and Reuters

3 May 2011 Strategy Asia Equities Daily Focus

Deutsche Bank AG/Hong Kong Page 17

Global

2 May 2011

Global Commodities DailyGas prices not dangerous yet

Deutsche Bank AG/London

Co

mm

od

itie

s

The Day Ahead

Time(EST) Country Event Previous Market View

03:55 Germany PMI Manufacturing (Apr) 61.7

04:00 EZ PMI Manufacturing (Apr) 57.7 57.7

10:00 US ISM Manufacturing (Apr) 61.2 59.6

16:00 US USDA crop progress report

21:00 China China Non-manufacturing PMI (Apr) 60.2

Overview

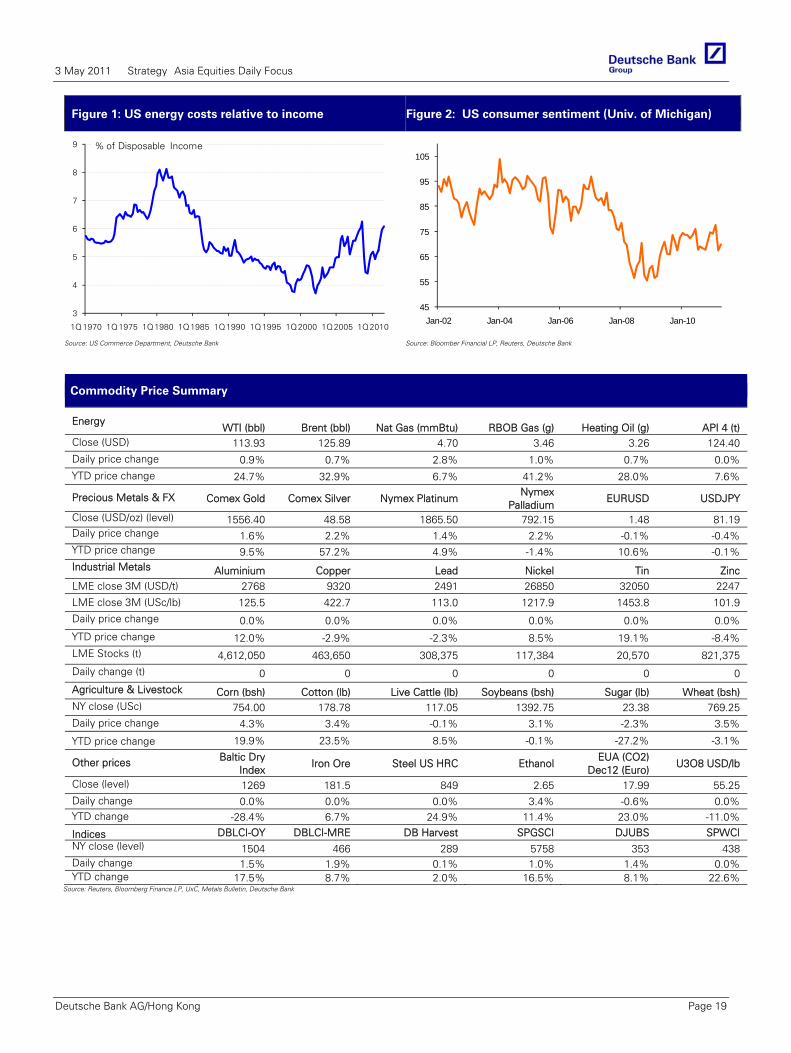

Gasoline prices continue to rise, with the latest weekly data (April 25) showing the average for all grades now at USD3.93/gallon. We estimate that prices will average USD4/gal during Q2 2011, but are unlikely to exceed USD4.25/gal over the summer unless another geopolitical event disrupts supplies. Energy costs for US consumers are tracked by the US Department of Commerce. Energy goods and services (consisting of gasoline and other energy goods – and of electricity and natural gas) are now up to 5.6% of disposable personal income, Figure 1.

The relationship between the total consumer energy costs and gasoline is very strong. If gasoline averages USD4.25/gal in Q3 2011, we estimate that energy’s share of disposable income will rise to 6.1%- still slightly below the 6.3% reached three years ago in Q3 2008. The good news for consumers is that natural gas and electricity prices have remained relatively “affordable” and it appears unlikely that the 8% energy cost peak hit in 1980 will be seen this year without some further major geopolitical event.

Our US economic team is encouraged by the fact consumer confidence appears to be stabilizing despite continued gasoline price increases, and believes March retail sales showed impressive momentum outside of autos and gasoline. The most recent Thomson Reuters/University of Michigan consumer sentiment data shows the final index for April rising to 69.8 from 67.5 in March, Figure 2. Monthly volatility in the data series has been high, but the “tops” have continued to edge higher and the index bottoms remain well about the 2008-09 lows.

Looking ahead at this week’s economic indicator releases, today we have the April manufacturing ISM for the US and China’s non-manufacturing PMI. Following last week’s Chicago PMI reading, which was slightly lower than we expected, our economics team looks for the US ISM survey to come in at 59.5 vs. 61.2 in March. On Wednesday, we expect a flat reading for the April US non-manufacturing ISM survey (57.0 vs. 57.3). Thursday brings the Q1 nonfarm productivity and unit labour cost data, which we expect to show increases of 1.3% and 1.1% respectively. The gain in the latter will push its y-o-y rate from -0.1% to +1.4% assuming there are no revisions, and would represent the first positive reading on the year-over-year rate since Q4 2008. Last but not least, we are forecasting April nonfarm payrolls at +200k, with private employment up a stronger +225k. We expect the unemployment rate to edge lower (8.7% vs. 8.8%), and look for a long overdue but slight rise in average hourly earnings.

Commodities & Global Markets

Commodities News In Brief

• China’s total steel capacity will hit 768 mn tonnes by the end of this year, and controlling excess capacity will be one of the big tasks facing the sector, the China Iron & Steel Association (CISA) said.

• Growth in Chinese demand for steel may ease to 2.6% to 4.6% annually through 2015 as the economy slows, the China Iron and Steel Association said.

• India, Asia’s second-biggest energy consumer pumped 3.3 mn tonnes of oil last month, a 12% increase from a year earlier, the oil ministry said.

• China’s stainless steel output rose 26% in the first quarter from a year earlier to 3.08 mn tonnes, the country’s stainless steel council said.

• Russia’s top steelmaker Severstal said its crude steel output rose to 3.65 mn tonnes in the first quarter 2011, up 5% from the same period last year.

Global Markets News In Brief

• Germany retail sales (MoM) declined to -2.1% from -0.3% in Mar; YoY down to -3.5 from 1.1%.

• EZ Consumer Confidence deteriorated to -11.6 in Apr from vs -10.6 in Mar.

• EZ Unemployment rate (MoM) (Mar) remains stable at 9.9%.

• US Chicago PMI (MoM) (Apr) fell to 67.6 from 70.6 the prior month.

• US personal spending increased by 0.6% in March after a 0.9% rise in February.

• U. of Michigan confidence rose to 69.8.

• China PMI Manufacturing fell to 52.9 in April from 53.4 in March.

Event Risks

• US ADP employment change on May 4.

• EZ PMI services on May 4.

• China HSBC services PMI on May 4.

• US Nonfarm productivity on May 5.

• ECB interest rate decision on May5.

• Germany factory orders on May 5.

• US unemployment rate on May6.

Research Team Adam Sieminski Soozhana Choi Research Analyst Research Analyst (1) 202 662 1624 (65) 6423 5261 [email protected] [email protected]

3 May 2011 Strategy Asia Equities Daily Focus

Page 18 Deutsche Bank AG/Hong Kong

Figure 1: US energy costs relative to income Figure 2: US consumer sentiment (Univ. of Michigan)

3

4

5

6

7

8

9

1Q 1970 1Q 1975 1Q 1980 1Q 1985 1Q 1990 1Q 1995 1Q 2000 1Q 2005 1Q 2010

% of Disposable Income

45

55

65

75

85

95

105

Jan-02 Jan-04 Jan-06 Jan-08 Jan-10

Source: US Commerce Department, Deutsche Bank

Source: Bloomber Financial LP, Reuters, Deutsche Bank

Commodity Price Summary

Energy WTI (bbl) Brent (bbl) Nat Gas (mmBtu) RBOB Gas (g) Heating Oil (g) API 4 (t)

Close (USD) 113.93 125.89 4.70 3.46 3.26 124.40 Daily price change 0.9% 0.7% 2.8% 1.0% 0.7% 0.0% YTD price change 24.7% 32.9% 6.7% 41.2% 28.0% 7.6%

Precious Metals & FX Comex Gold Comex Silver Nymex Platinum Nymex

Palladium EURUSD USDJPY

Close (USD/oz) (level) 1556.40 48.58 1865.50 792.15 1.48 81.19 Daily price change 1.6% 2.2% 1.4% 2.2% -0.1% -0.4% YTD price change 9.5% 57.2% 4.9% -1.4% 10.6% -0.1% Industrial Metals Aluminium Copper Lead Nickel Tin Zinc LME close 3M (USD/t) 2768 9320 2491 26850 32050 2247

LME close 3M (USc/lb) 125.5 422.7 113.0 1217.9 1453.8 101.9

Daily price change 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

YTD price change 12.0% -2.9% -2.3% 8.5% 19.1% -8.4% LME Stocks (t) 4,612,050 463,650 308,375 117,384 20,570 821,375

Daily change (t) 0 0 0 0 0 0

Agriculture & Livestock Corn (bsh) Cotton (lb) Live Cattle (lb) Soybeans (bsh) Sugar (lb) Wheat (bsh) NY close (USc) 754.00 178.78 117.05 1392.75 23.38 769.25 Daily price change 4.3% 3.4% -0.1% 3.1% -2.3% 3.5%

YTD price change 19.9% 23.5% 8.5% -0.1% -27.2% -3.1%

Other prices Baltic Dry Index

Iron Ore Steel US HRC Ethanol EUA (CO2)

Dec12 (Euro) U3O8 USD/lb

Close (level) 1269 181.5 849 2.65 17.99 55.25 Daily change 0.0% 0.0% 0.0% 3.4% -0.6% 0.0% YTD change -28.4% 6.7% 24.9% 11.4% 23.0% -11.0%

Indices DBLCI-OY DBLCI-MRE DB Harvest SPGSCI DJUBS SPWCI NY close (level) 1504 466 289 5758 353 438 Daily change 1.5% 1.9% 0.1% 1.0% 1.4% 0.0% YTD change 17.5% 8.7% 2.0% 16.5% 8.1% 22.6%

Source: Reuters, Bloomberg Finance LP, UxC, Metals Bulletin, Deutsche Bank

3 May 2011 Strategy Asia Equities Daily Focus

Deutsche Bank AG/Hong Kong Page 19

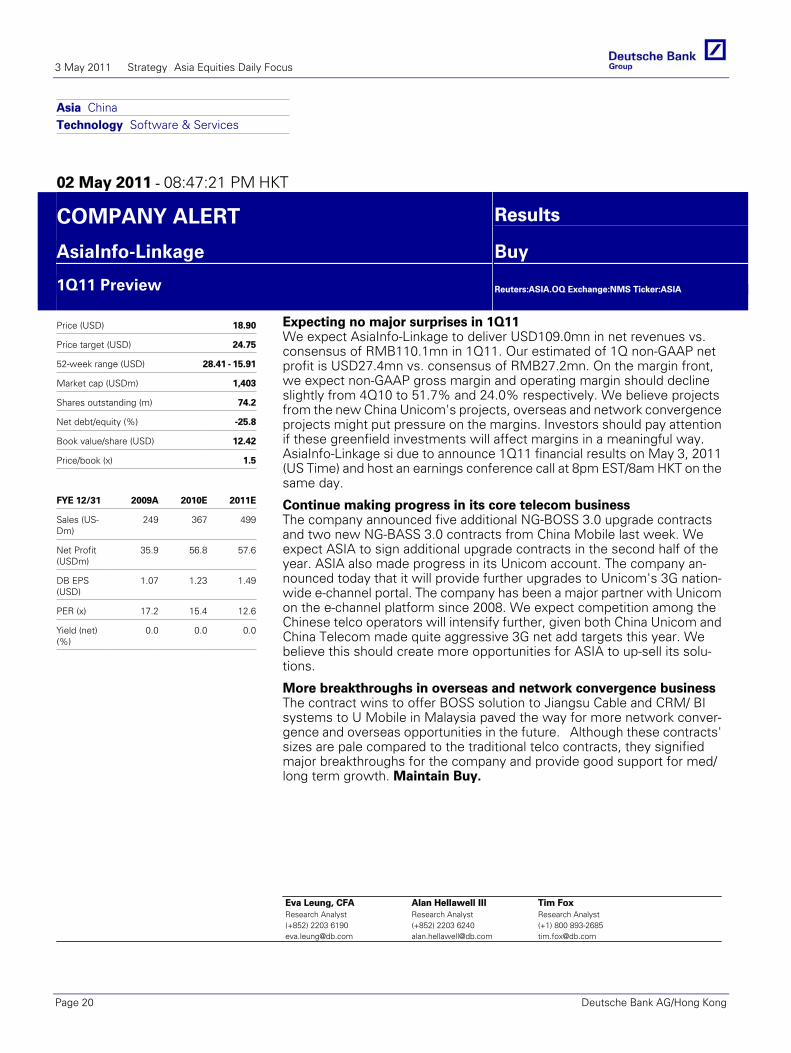

Asia ChinaTechnology Software & Services

02 May 2011 - 08:47:21 PM HKT

COMPANY ALERT Results

AsiaInfo-Linkage Buy

1Q11 Preview

Reuters:ASIA.OQ Exchange:NMS Ticker:ASIA

Price (USD) 18.90

Price target (USD) 24.75

52-week range (USD) 28.41 - 15.91

Market cap (USDm) 1,403

Shares outstanding (m) 74.2

Net debt/equity (%) -25.8

Book value/share (USD) 12.42

Price/book (x) 1.5

FYE 12/31 2009A 2010E 2011E

Sales (US-Dm)

249 367 499

Net Profit(USDm)

35.9 56.8 57.6

DB EPS(USD)

1.07 1.23 1.49

PER (x) 17.2 15.4 12.6

Yield (net)(%)

0.0 0.0 0.0

Expecting no major surprises in 1Q11We expect AsiaInfo-Linkage to deliver USD109.0mn in net revenues vs.consensus of RMB110.1mn in 1Q11. Our estimated of 1Q non-GAAP netprofit is USD27.4mn vs. consensus of RMB27.2mn. On the margin front,we expect non-GAAP gross margin and operating margin should declineslightly from 4Q10 to 51.7% and 24.0% respectively. We believe projectsfrom the new China Unicom's projects, overseas and network convergenceprojects might put pressure on the margins. Investors should pay attentionif these greenfield investments will affect margins in a meaningful way.AsiaInfo-Linkage si due to announce 1Q11 financial results on May 3, 2011(US Time) and host an earnings conference call at 8pm EST/8am HKT on thesame day.

Continue making progress in its core telecom businessThe company announced five additional NG-BOSS 3.0 upgrade contractsand two new NG-BASS 3.0 contracts from China Mobile last week. Weexpect ASIA to sign additional upgrade contracts in the second half of theyear. ASIA also made progress in its Unicom account. The company an-nounced today that it will provide further upgrades to Unicom's 3G nation-wide e-channel portal. The company has been a major partner with Unicomon the e-channel platform since 2008. We expect competition among theChinese telco operators will intensify further, given both China Unicom andChina Telecom made quite aggressive 3G net add targets this year. Webelieve this should create more opportunities for ASIA to up-sell its solu-tions.

More breakthroughs in overseas and network convergence businessThe contract wins to offer BOSS solution to Jiangsu Cable and CRM/ BIsystems to U Mobile in Malaysia paved the way for more network conver-gence and overseas opportunities in the future. Although these contracts'sizes are pale compared to the traditional telco contracts, they signifiedmajor breakthroughs for the company and provide good support for med/long term growth. Maintain Buy.

Eva Leung, CFAResearch Analyst(+852) 2203 [email protected]

Alan Hellawell IIIResearch Analyst(+852) 2203 [email protected]

Tim FoxResearch Analyst(+1) 800 [email protected]

3 May 2011 Strategy Asia Equities Daily Focus

Page 20 Deutsche Bank AG/Hong Kong

Co

mp

any Asia China

Resources Metals & Mining

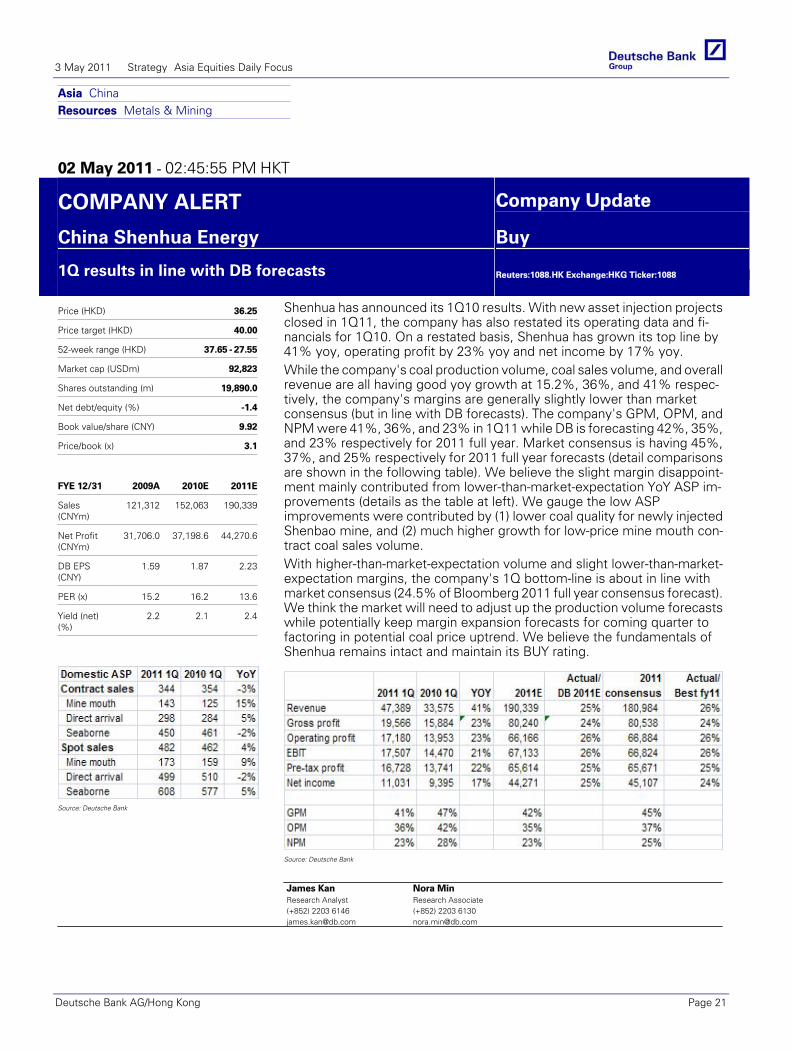

02 May 2011 - 02:45:55 PM HKT

COMPANY ALERT Company Update

China Shenhua Energy Buy

1Q results in line with DB forecasts

Reuters:1088.HK Exchange:HKG Ticker:1088

Price (HKD) 36.25

Price target (HKD) 40.00

52-week range (HKD) 37.65 - 27.55

Market cap (USDm) 92,823

Shares outstanding (m) 19,890.0

Net debt/equity (%) -1.4

Book value/share (CNY) 9.92

Price/book (x) 3.1

FYE 12/31 2009A 2010E 2011E

Sales(CNYm)

121,312 152,063 190,339

Net Profit(CNYm)

31,706.0 37,198.6 44,270.6

DB EPS(CNY)

1.59 1.87 2.23

PER (x) 15.2 16.2 13.6

Yield (net)(%)

2.2 2.1 2.4

Source: Deutsche Bank

Shenhua has announced its 1Q10 results. With new asset injection projectsclosed in 1Q11, the company has also restated its operating data and fi-nancials for 1Q10. On a restated basis, Shenhua has grown its top line by41% yoy, operating profit by 23% yoy and net income by 17% yoy.While the company's coal production volume, coal sales volume, and overallrevenue are all having good yoy growth at 15.2%, 36%, and 41% respec-tively, the company's margins are generally slightly lower than marketconsensus (but in line with DB forecasts). The company's GPM, OPM, andNPM were 41%, 36%, and 23% in 1Q11 while DB is forecasting 42%, 35%,and 23% respectively for 2011 full year. Market consensus is having 45%,37%, and 25% respectively for 2011 full year forecasts (detail comparisonsare shown in the following table). We believe the slight margin disappoint-ment mainly contributed from lower-than-market-expectation YoY ASP im-provements (details as the table at left). We gauge the low ASPimprovements were contributed by (1) lower coal quality for newly injectedShenbao mine, and (2) much higher growth for low-price mine mouth con-tract coal sales volume.With higher-than-market-expectation volume and slight lower-than-market-expectation margins, the company's 1Q bottom-line is about in line withmarket consensus (24.5% of Bloomberg 2011 full year consensus forecast).We think the market will need to adjust up the production volume forecastswhile potentially keep margin expansion forecasts for coming quarter tofactoring in potential coal price uptrend. We believe the fundamentals ofShenhua remains intact and maintain its BUY rating.

Source: Deutsche Bank

James KanResearch Analyst(+852) 2203 [email protected]

Nora MinResearch Associate(+852) 2203 [email protected]

3 May 2011 Strategy Asia Equities Daily Focus

Deutsche Bank AG/Hong Kong Page 21

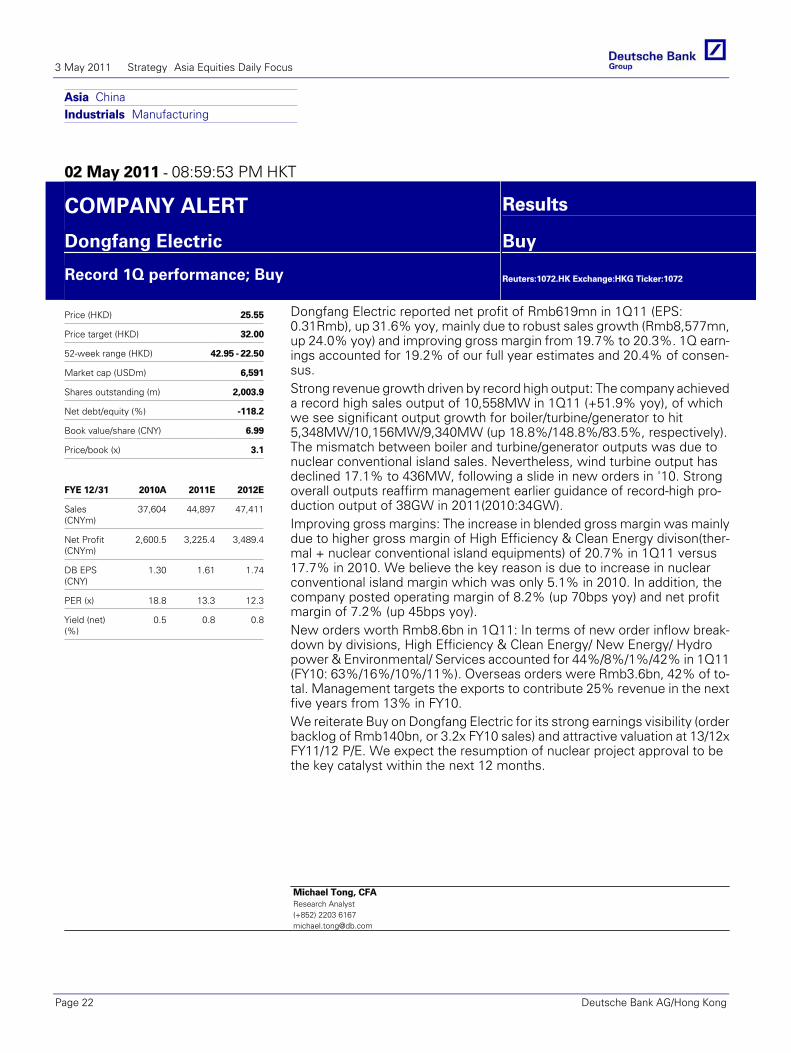

Asia ChinaIndustrials Manufacturing

02 May 2011 - 08:59:53 PM HKT

COMPANY ALERT Results

Dongfang Electric Buy

Record 1Q performance; Buy

Reuters:1072.HK Exchange:HKG Ticker:1072

Price (HKD) 25.55

Price target (HKD) 32.00

52-week range (HKD) 42.95 - 22.50

Market cap (USDm) 6,591

Shares outstanding (m) 2,003.9

Net debt/equity (%) -118.2

Book value/share (CNY) 6.99

Price/book (x) 3.1

FYE 12/31 2010A 2011E 2012E

Sales(CNYm)

37,604 44,897 47,411

Net Profit(CNYm)

2,600.5 3,225.4 3,489.4

DB EPS(CNY)

1.30 1.61 1.74

PER (x) 18.8 13.3 12.3

Yield (net)(%)

0.5 0.8 0.8

Dongfang Electric reported net profit of Rmb619mn in 1Q11 (EPS:0.31Rmb), up 31.6% yoy, mainly due to robust sales growth (Rmb8,577mn,up 24.0% yoy) and improving gross margin from 19.7% to 20.3%. 1Q earn-ings accounted for 19.2% of our full year estimates and 20.4% of consen-sus.Strong revenue growth driven by record high output: The company achieveda record high sales output of 10,558MW in 1Q11 (+51.9% yoy), of whichwe see significant output growth for boiler/turbine/generator to hit5,348MW/10,156MW/9,340MW (up 18.8%/148.8%/83.5%, respectively).The mismatch between boiler and turbine/generator outputs was due tonuclear conventional island sales. Nevertheless, wind turbine output hasdeclined 17.1% to 436MW, following a slide in new orders in '10. Strongoverall outputs reaffirm management earlier guidance of record-high pro-duction output of 38GW in 2011(2010:34GW).Improving gross margins: The increase in blended gross margin was mainlydue to higher gross margin of High Efficiency & Clean Energy divison(ther-mal + nuclear conventional island equipments) of 20.7% in 1Q11 versus17.7% in 2010. We believe the key reason is due to increase in nuclearconventional island margin which was only 5.1% in 2010. In addition, thecompany posted operating margin of 8.2% (up 70bps yoy) and net profitmargin of 7.2% (up 45bps yoy).New orders worth Rmb8.6bn in 1Q11: In terms of new order inflow break-down by divisions, High Efficiency & Clean Energy/ New Energy/ Hydropower & Environmental/ Services accounted for 44%/8%/1%/42% in 1Q11(FY10: 63%/16%/10%/11%). Overseas orders were Rmb3.6bn, 42% of to-tal. Management targets the exports to contribute 25% revenue in the nextfive years from 13% in FY10.We reiterate Buy on Dongfang Electric for its strong earnings visibility (orderbacklog of Rmb140bn, or 3.2x FY10 sales) and attractive valuation at 13/12xFY11/12 P/E. We expect the resumption of nuclear project approval to bethe key catalyst within the next 12 months.

Michael Tong, CFAResearch Analyst(+852) 2203 [email protected]

3 May 2011 Strategy Asia Equities Daily Focus

Page 22 Deutsche Bank AG/Hong Kong

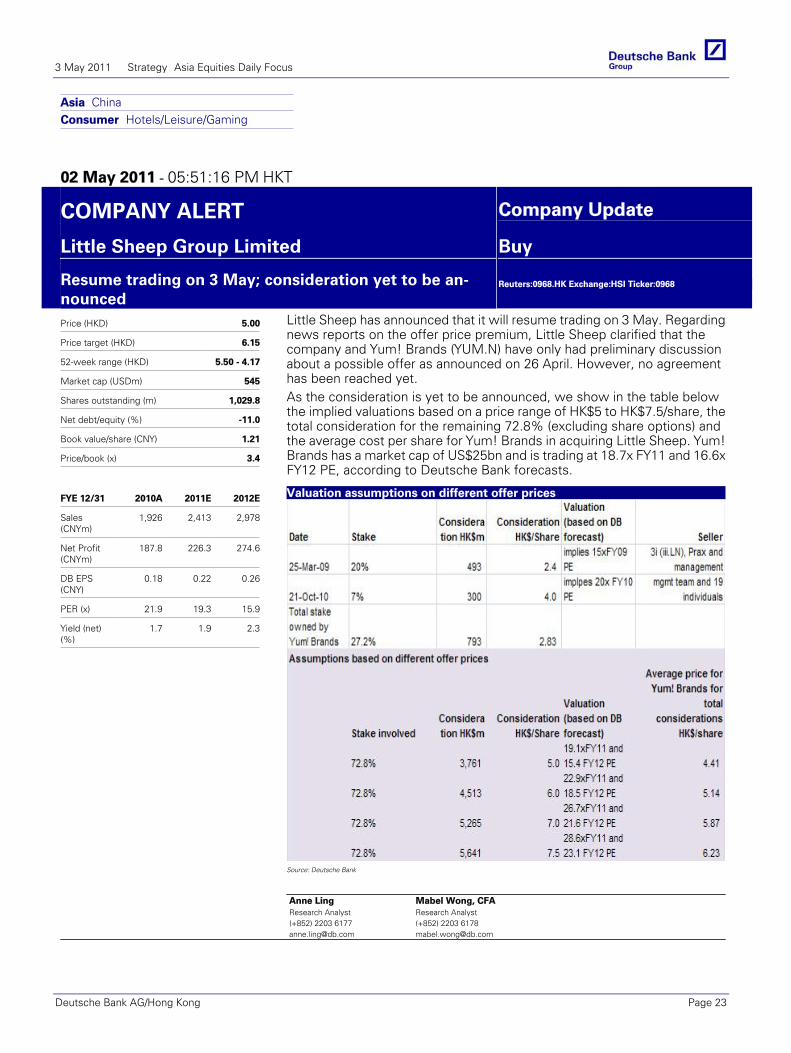

Asia ChinaConsumer Hotels/Leisure/Gaming

02 May 2011 - 05:51:16 PM HKT

COMPANY ALERT Company Update

Little Sheep Group Limited Buy

Resume trading on 3 May; consideration yet to be an‐nounced

Reuters:0968.HK Exchange:HSI Ticker:0968

Price (HKD) 5.00

Price target (HKD) 6.15

52-week range (HKD) 5.50 ‐ 4.17

Market cap (USDm) 545

Shares outstanding (m) 1,029.8

Net debt/equity (%) ‐11.0

Book value/share (CNY) 1.21

Price/book (x) 3.4

FYE 12/31 2010A 2011E 2012E

Sales(CNYm)

1,926 2,413 2,978

Net Profit(CNYm)

187.8 226.3 274.6

DB EPS(CNY)

0.18 0.22 0.26

PER (x) 21.9 19.3 15.9

Yield (net)(%)

1.7 1.9 2.3

Little Sheep has announced that it will resume trading on 3 May. Regardingnews reports on the offer price premium, Little Sheep clarified that thecompany and Yum! Brands (YUM.N) have only had preliminary discussionabout a possible offer as announced on 26 April. However, no agreementhas been reached yet.As the consideration is yet to be announced, we show in the table belowthe implied valuations based on a price range of HK$5 to HK$7.5/share, thetotal consideration for the remaining 72.8% (excluding share options) andthe average cost per share for Yum! Brands in acquiring Little Sheep. Yum!Brands has a market cap of US$25bn and is trading at 18.7x FY11 and 16.6xFY12 PE, according to Deutsche Bank forecasts.

Valuation assumptions on different offer prices

Source: Deutsche Bank

Anne LingResearch Analyst(+852) 2203 [email protected]

Mabel Wong, CFAResearch Analyst(+852) 2203 [email protected]

3 May 2011 Strategy Asia Equities Daily Focus

Deutsche Bank AG/Hong Kong Page 23

Asia Korea, Republic of Automobiles & Components

2 May 2011

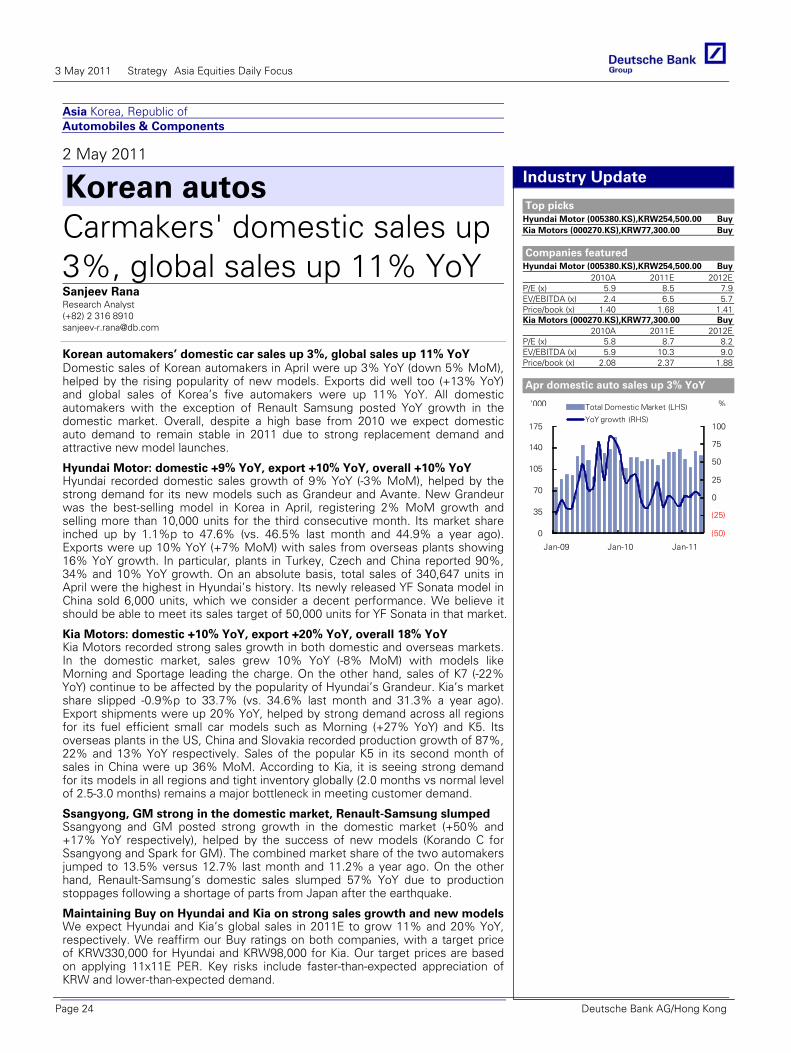

Korean autos Carmakers' domestic sales up 3%, global sales up 11% YoYSanjeev Rana Research Analyst (+82) 2 316 8910 [email protected]

Korean automakers’ domestic car sales up 3%, global sales up 11% YoY Domestic sales of Korean automakers in April were up 3% YoY (down 5% MoM), helped by the rising popularity of new models. Exports did well too (+13% YoY) and global sales of Korea’s five automakers were up 11% YoY. All domestic automakers with the exception of Renault Samsung posted YoY growth in the domestic market. Overall, despite a high base from 2010 we expect domestic auto demand to remain stable in 2011 due to strong replacement demand and attractive new model launches.

Deutsche Bank AG/Hong Kong

Industry Update

Top picks Hyundai Motor (005380.KS),KRW254,500.00 BuyKia Motors (000270.KS),KRW77,300.00 Buy

Companies featured

Hyundai Motor (005380.KS),KRW254,500.00 Buy2010A 2011E 2012E

P/E (x) 5.9 8.5 7.9EV/EBITDA (x) 2.4 6.5 5.7Price/book (x) 1.40 1.68 1.41Kia Motors (000270.KS),KRW77,300.00 Buy

2010A 2011E 2012EP/E (x) 5.8 8.7 8.2EV/EBITDA (x) 5.9 10.3 9.0Price/book (x) 2.08 2.37 1.88

Apr domestic auto sales up 3% YoY

(50)

(25)

0

25

50

75

100

0

35

70

105

140

175

Jan-09 Jan-10 Jan-11

Total Domestic Market (LHS)

YoY growth (RHS)

'000 %

Glo

bal

Mar

kets

Res

earc

h