3 - 1 Cost-Volume-Profit Analysis Chapter 3 3 - 2 Learning Objective 1 Understand the assumptions...

60

3 - 1 Cost-Volume-Profit Analysis Chapter 3

-

date post

21-Dec-2015 -

Category

Documents

-

view

236 -

download

4

Transcript of 3 - 1 Cost-Volume-Profit Analysis Chapter 3 3 - 2 Learning Objective 1 Understand the assumptions...

3 - 1

Cost-Volume-Profit AnalysisCost-Volume-Profit Analysis

Chapter 3

3 - 2

Learning Objective 1Learning Objective 1

Understand the assumptions

underlying cost-volume-profit

(CVP) analysis.

3 - 3

Cost-Volume-Profit Assumptionsand Terminology

Cost-Volume-Profit Assumptionsand Terminology

1. Changes in the level of revenues and costs arise only because of changes in the number of product (or service) units produced and sold.

2. Total costs can be divided into a fixed component and a component that is variable with respect to the level of output.

3 - 4

Cost-Volume-Profit Assumptionsand Terminology

Cost-Volume-Profit Assumptionsand Terminology

3. When graphed, the behavior of total revenues and total costs is linear (straight-line) in relation to output units within the relevant range (and time period).

4. The unit selling price, unit variable costs, and fixed costs are known and constant.

3 - 5

Cost-Volume-Profit Assumptionsand Terminology

Cost-Volume-Profit Assumptionsand Terminology

5. The analysis either covers a single product or assumes that the sales mix when multiple products are sold will remain constant as the level of total units sold changes.

6. All revenues and costs can be added and compared without taking into account the time value of money.

3 - 6

Cost-Volume-Profit Assumptionsand Terminology

Cost-Volume-Profit Assumptionsand Terminology

Operating income= Total revenues from operations– Cost of goods sold and operating costs (excluding income taxes)

Net income = Operating income – Income taxes

3 - 7

Learning Objective 2Learning Objective 2

Explain the features

of CVP analysis.

3 - 8

Essentials of Cost-Volume-Profit(CVP) Analysis Example

Essentials of Cost-Volume-Profit(CVP) Analysis Example

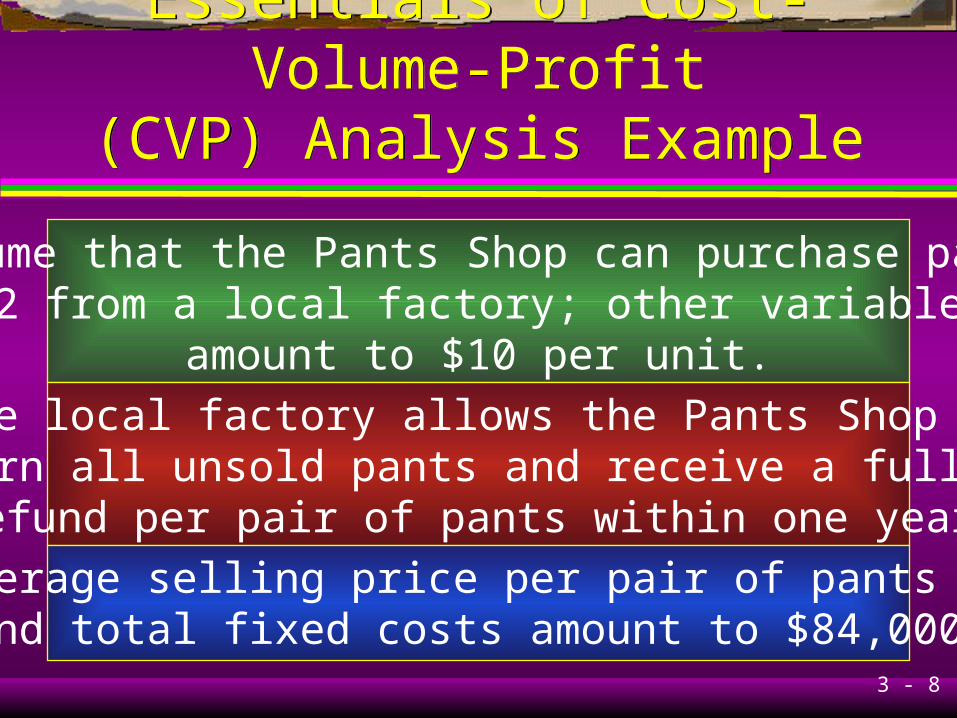

Assume that the Pants Shop can purchase pantsfor $32 from a local factory; other variable costs

amount to $10 per unit.

The local factory allows the Pants Shop toreturn all unsold pants and receive a full $32

refund per pair of pants within one year.

The average selling price per pair of pants is $70and total fixed costs amount to $84,000.

3 - 9

Essentials of Cost-Volume-Profit(CVP) Analysis Example

Essentials of Cost-Volume-Profit(CVP) Analysis Example

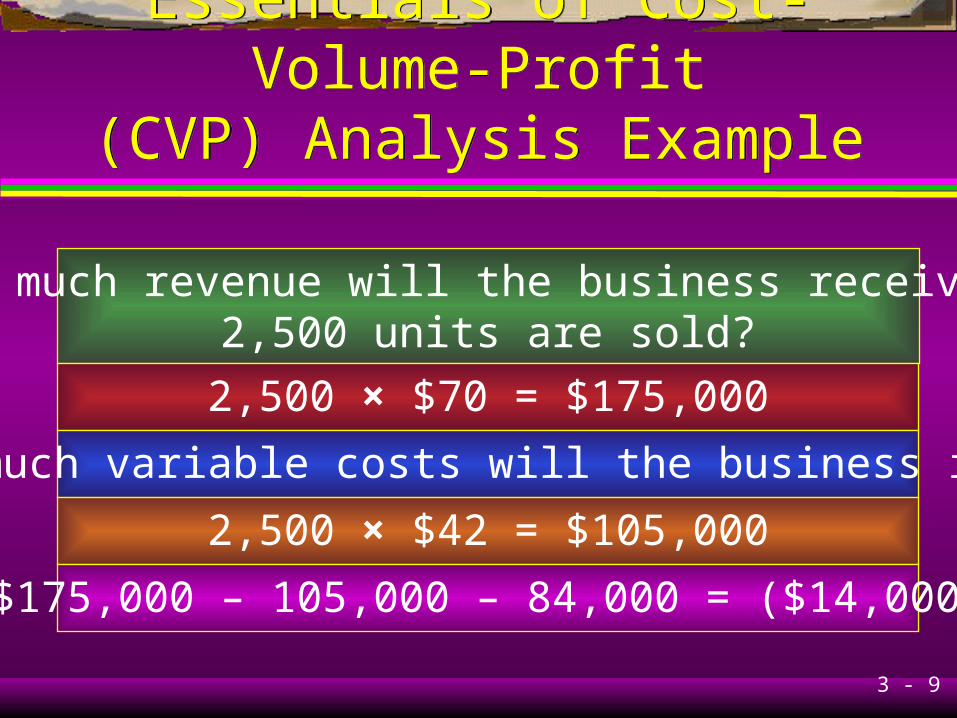

How much revenue will the business receive if2,500 units are sold?

2,500 × $70 = $175,000

How much variable costs will the business incur?

2,500 × $42 = $105,000

$175,000 – 105,000 – 84,000 = ($14,000)

3 - 10

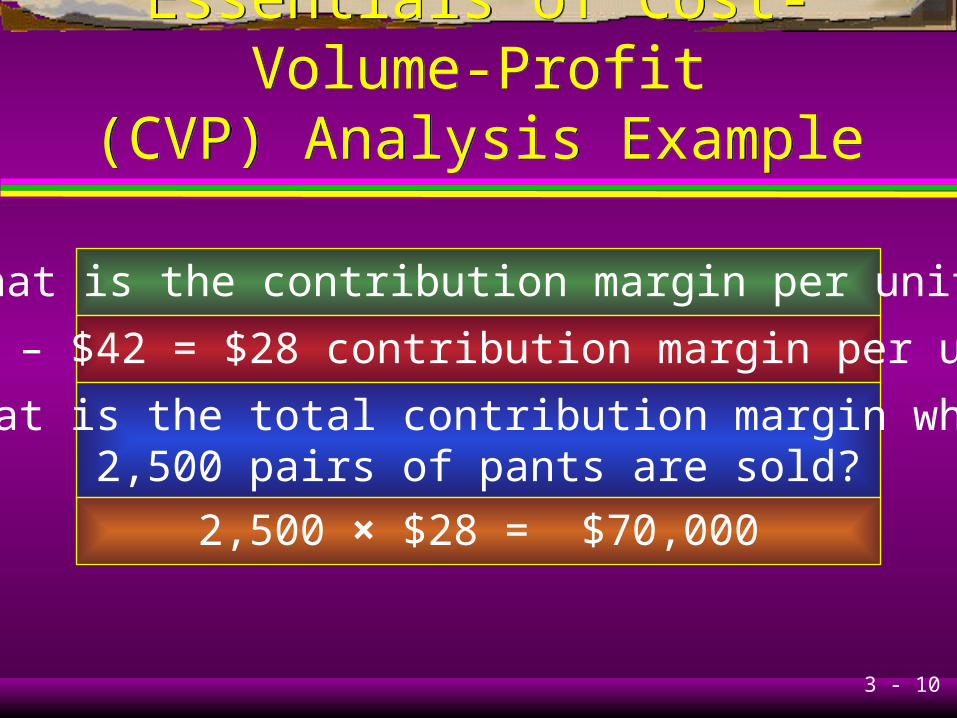

Essentials of Cost-Volume-Profit(CVP) Analysis Example

Essentials of Cost-Volume-Profit(CVP) Analysis Example

What is the contribution margin per unit?

$70 – $42 = $28 contribution margin per unit

What is the total contribution margin when2,500 pairs of pants are sold?

2,500 × $28 = $70,000

3 - 11

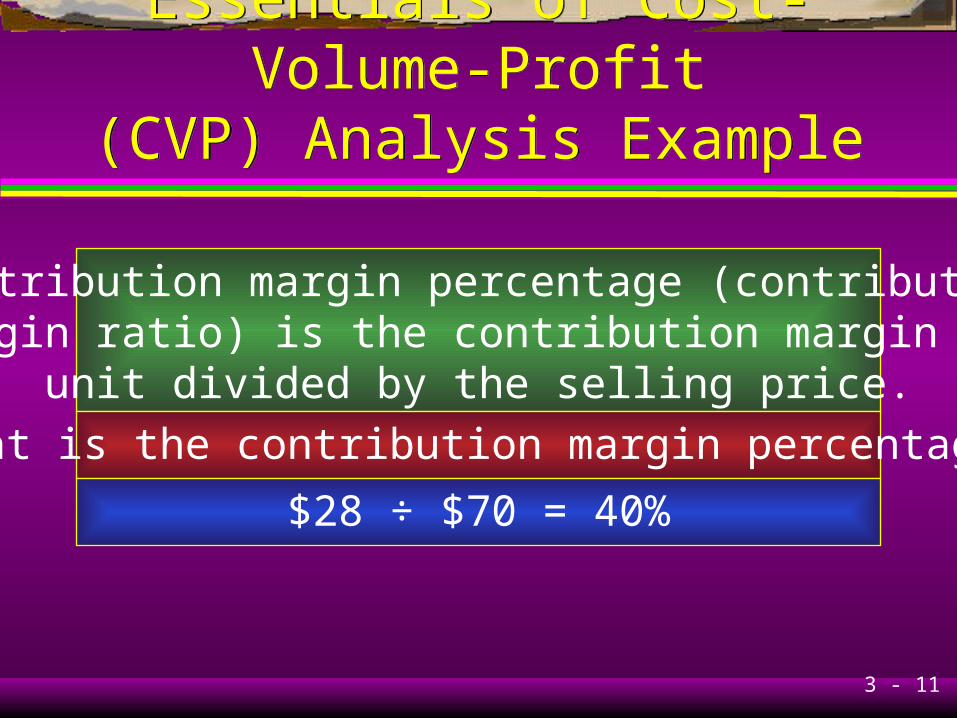

Essentials of Cost-Volume-Profit(CVP) Analysis Example

Essentials of Cost-Volume-Profit(CVP) Analysis Example

Contribution margin percentage (contributionmargin ratio) is the contribution margin per

unit divided by the selling price.

What is the contribution margin percentage?

$28 ÷ $70 = 40%

3 - 12

Essentials of Cost-Volume-Profit(CVP) Analysis Example

Essentials of Cost-Volume-Profit(CVP) Analysis Example

If the business sells 3,000 pairs of pants,revenues will be $210,000 and contribution

margin would equal 40% × $210,000 = $84,000.

A

FEDERAL RESERVE NOTE

THE UNITED STATES OF AMERICATHE UNITED STATES OF AMERICA

L70744629F

12

1212

12

L70744629F

ONE DOLLARONE DOLLAR

WA SHINGTON, D.C.

TH IS N O TE IS LE GA L TE N DE R

FOR A LL D E B TS , P UB LIC AN D P RIV A TE

S E RIES

19 85

H 293

3 - 13

Learning Objective 3Learning Objective 3

Determine the breakeven point

and output level needed to achieve

a target operating income using

the equation, contribution margin,

and graph methods.

3 - 14

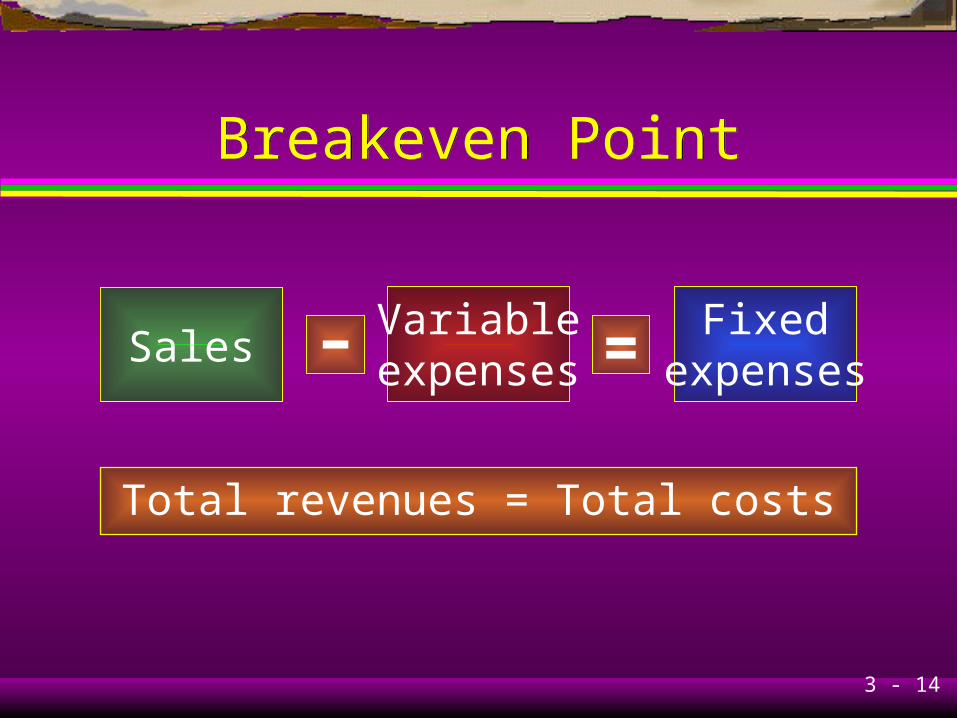

Breakeven PointBreakeven Point

SalesVariableexpenses

Fixedexpenses

– =

Total revenues = Total costs

3 - 15

AbbreviationsAbbreviations

SP = Selling price

VCU = Variable cost per unit

CMU = Contribution margin per unit

CM% = Contribution margin percentage

FC = Fixed costs

3 - 16

AbbreviationsAbbreviations

Q = Quantity of output units sold(and manufactured)

OI = Operating income

TOI = Target operating income

TNI = Target net income

3 - 17

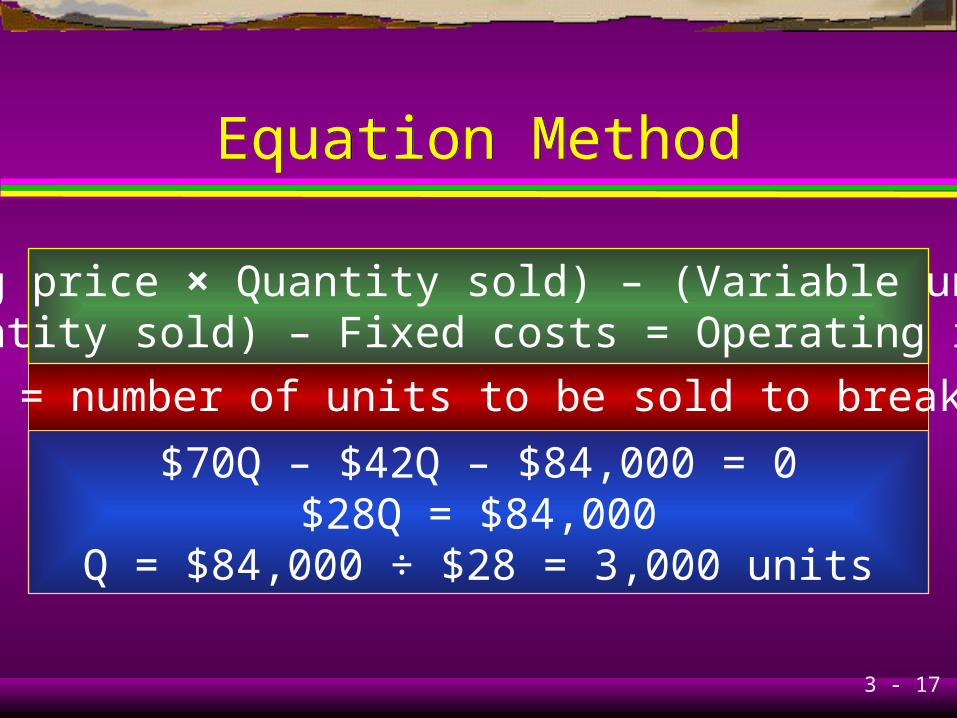

Equation MethodEquation Method

$70Q – $42Q – $84,000 = 0$28Q = $84,000

Q = $84,000 ÷ $28 = 3,000 units

Let Q = number of units to be sold to break even

(Selling price × Quantity sold) – (Variable unit cost× Quantity sold) – Fixed costs = Operating income

3 - 18

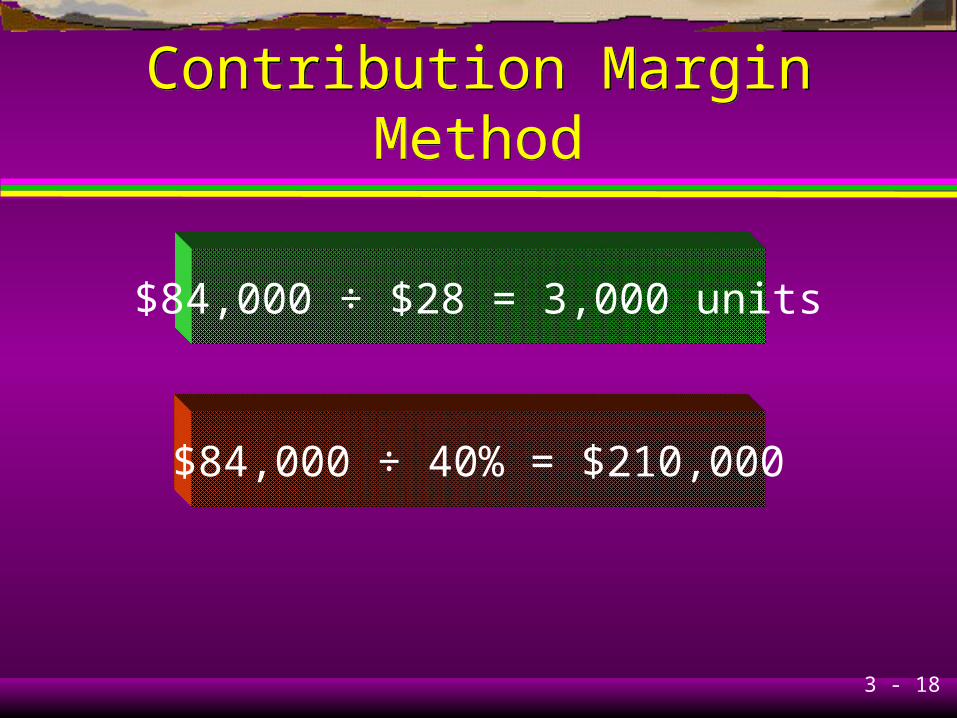

Contribution Margin MethodContribution Margin Method

$84,000 ÷ $28 = 3,000 units

$84,000 ÷ 40% = $210,000

3 - 19

Graph MethodGraph Method

04284

126168210252294336378

0 1000 2000 3000 4000 5000

Units

$(00

0)

Revenue

Total costs

Breakeven

Fixed costs

3 - 20

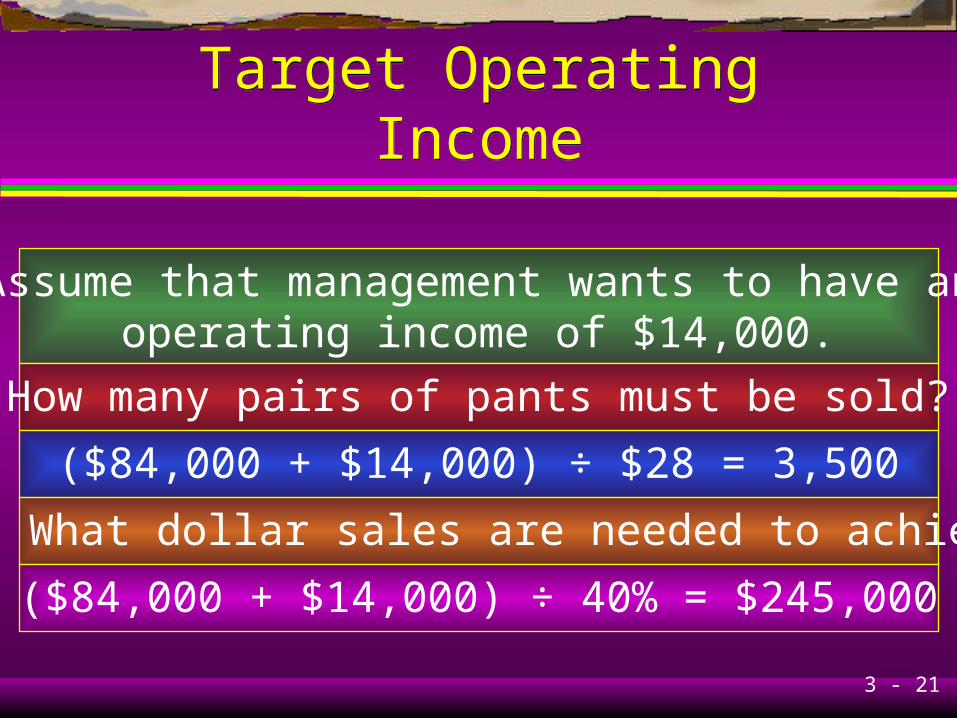

Target Operating IncomeTarget Operating Income

(Fixed costs + Target operating income)divided either by Contribution margin

percentage or Contribution margin per unit

3 - 21

Target Operating IncomeTarget Operating Income

Assume that management wants to have anoperating income of $14,000.

How many pairs of pants must be sold?

($84,000 + $14,000) ÷ $28 = 3,500

What dollar sales are needed to achieve this income?

($84,000 + $14,000) ÷ 40% = $245,000

3 - 22

Learning Objective 4Learning Objective 4

Understand how income

taxes affect CVP analysis.

3 - 23

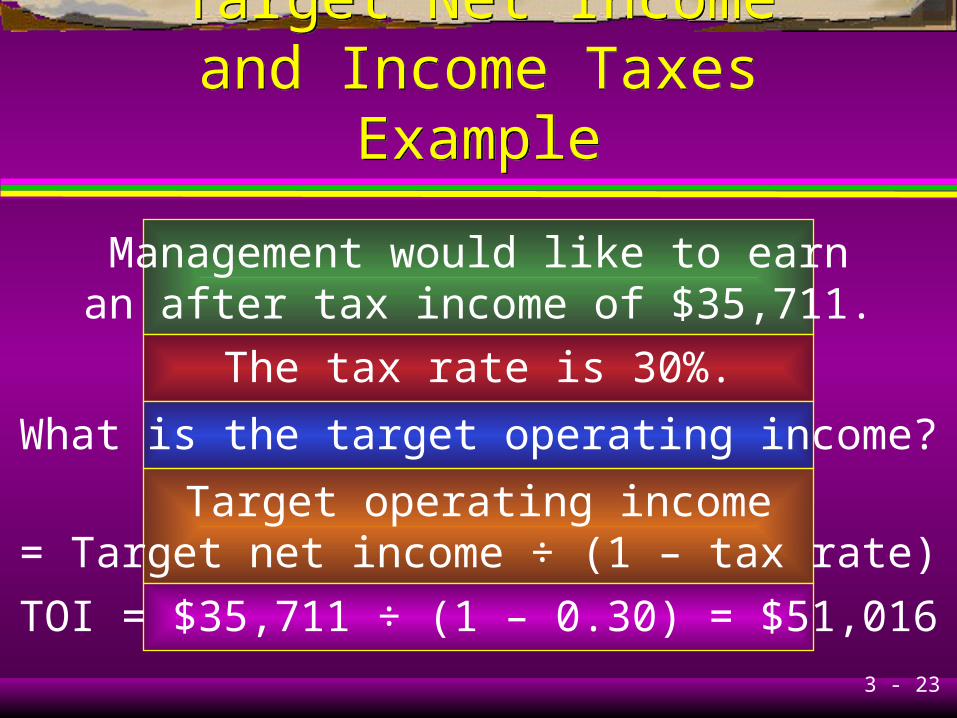

Target Net Incomeand Income Taxes Example

Target Net Incomeand Income Taxes Example

Management would like to earnan after tax income of $35,711.

The tax rate is 30%.

What is the target operating income?

Target operating income= Target net income ÷ (1 – tax rate)

TOI = $35,711 ÷ (1 – 0.30) = $51,016

3 - 24

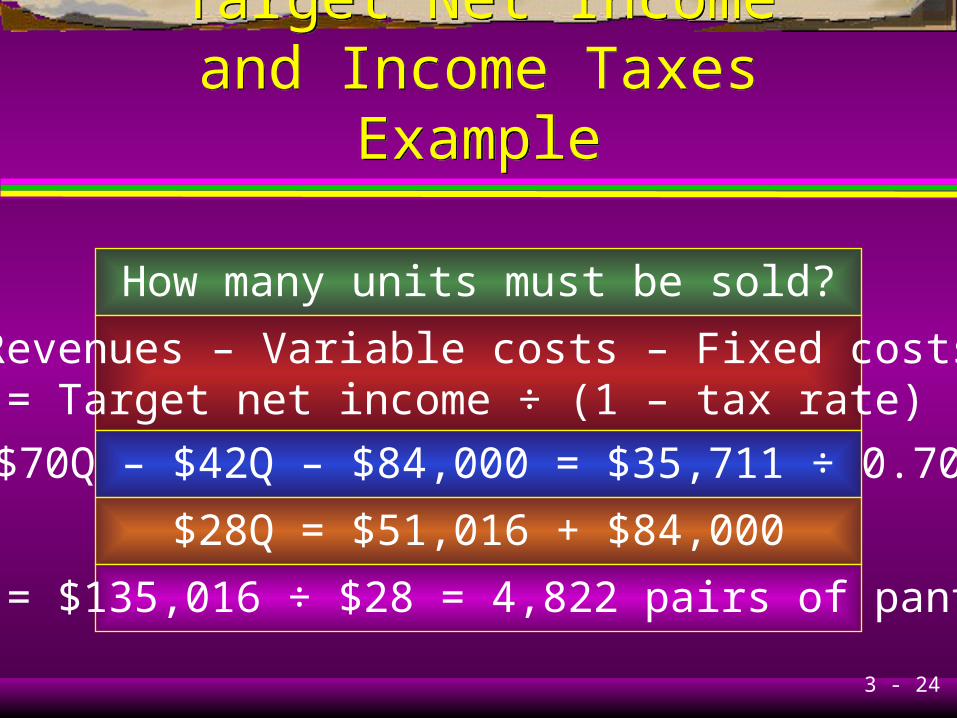

Target Net Incomeand Income Taxes Example

Target Net Incomeand Income Taxes Example

How many units must be sold?

Revenues – Variable costs – Fixed costs= Target net income ÷ (1 – tax rate)

$70Q – $42Q – $84,000 = $35,711 ÷ 0.70

$28Q = $51,016 + $84,000

Q = $135,016 ÷ $28 = 4,822 pairs of pants

3 - 25

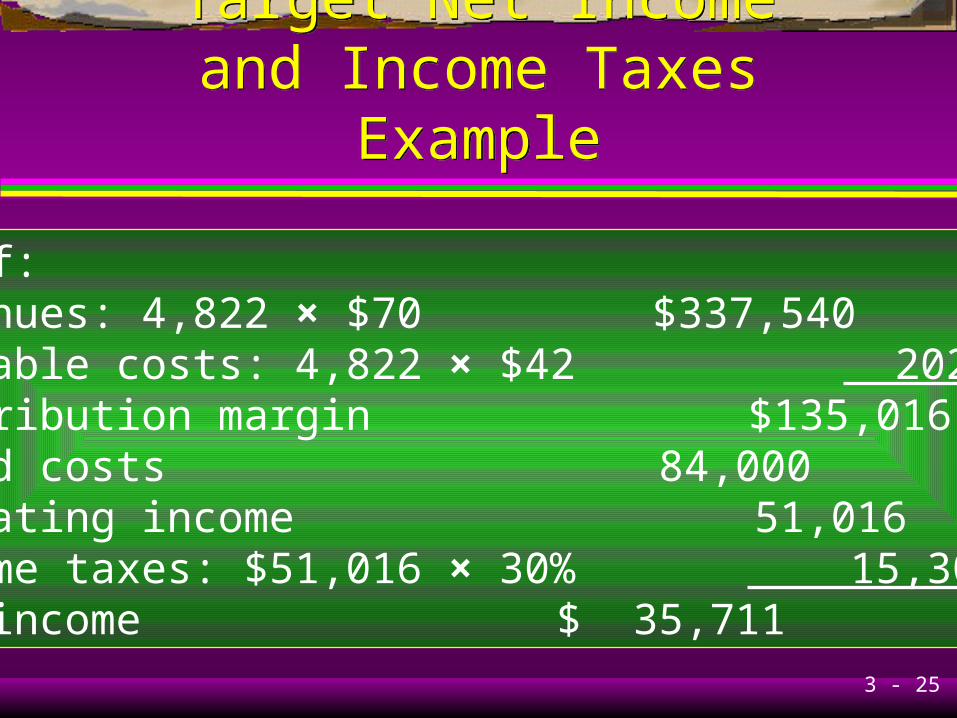

Target Net Incomeand Income Taxes Example

Target Net Incomeand Income Taxes Example

Proof:Revenues: 4,822 × $70 $337,540Variable costs: 4,822 × $42 202,524Contribution margin $135,016Fixed costs 84,000Operating income 51,016Income taxes: $51,016 × 30% 15,305Net income $ 35,711

3 - 26

Learning Objective 5Learning Objective 5

Explain CVP analysis

in decision making and

how sensitivity analysis helps

managers cope with uncertainty.

3 - 27

Using CVP Analysis ExampleUsing CVP Analysis Example

Suppose the management anticipatesselling 3,200 pairs of pants.

Management is considering an advertisingcampaign that would cost $10,000.

It is anticipated that the advertising willincrease sales to 4,000 units.

Should the business advertise?

3 - 28

Using CVP Analysis ExampleUsing CVP Analysis Example

3,200 pairs of pants sold with no advertising:

Contribution margin $89,600Fixed costs 84,000Operating income $ 5,600

4,000 pairs of pants sold with advertising:

Contribution margin $112,000Fixed costs 94,000Operating income $ 18,000

3 - 29

Using CVP Analysis ExampleUsing CVP Analysis Example

Instead of advertising, management isconsidering reducing the selling price

to $61 per pair of pants.

It is anticipated that this will increasesales to 4,500 units.

Should management decrease the sellingprice per pair of pants to $61?

3 - 30

Using CVP Analysis ExampleUsing CVP Analysis Example

3,200 pairs of pants sold with no changein the selling price:

Operating income = $5,600

4,500 pairs of pants sold at a reduced selling price:

Contribution margin: (4,500 × $19) $85,500Fixed costs 84,000Operating income $ 1,500

3 - 31

Sensitivity Analysis andUncertainty Example

Sensitivity Analysis andUncertainty Example

Assume that the Pants Shop can sell4,000 pairs of pants.

Fixed costs are $84,000.

Contribution margin ratio is 40%.

At the present time the business cannothandle more than 3,500 pairs of pants.

3 - 32

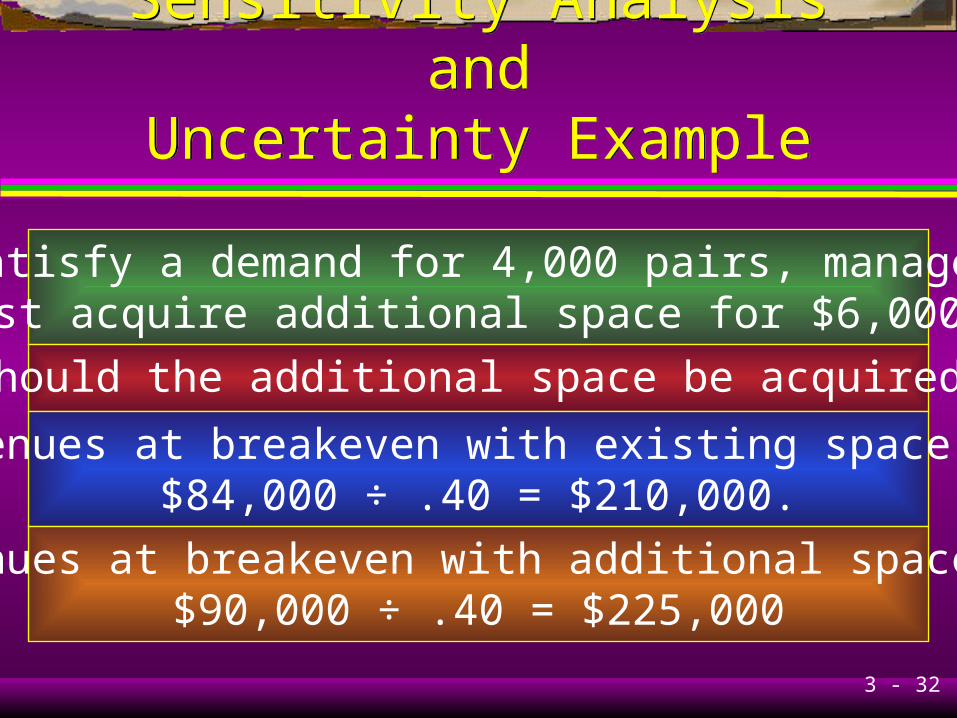

Sensitivity Analysis andUncertainty Example

Sensitivity Analysis andUncertainty Example

To satisfy a demand for 4,000 pairs, managementmust acquire additional space for $6,000.

Should the additional space be acquired?

Revenues at breakeven with existing space are$84,000 ÷ .40 = $210,000.

Revenues at breakeven with additional space are$90,000 ÷ .40 = $225,000

3 - 33

Sensitivity Analysis andUncertainty Example

Sensitivity Analysis andUncertainty Example

Operating income at $245,000 revenues withexisting space = ($245,000 × .40)

– $84,000 = $14,000.

(3,500 pairs of pants × $28) – $84,000 = $14,000

3 - 34

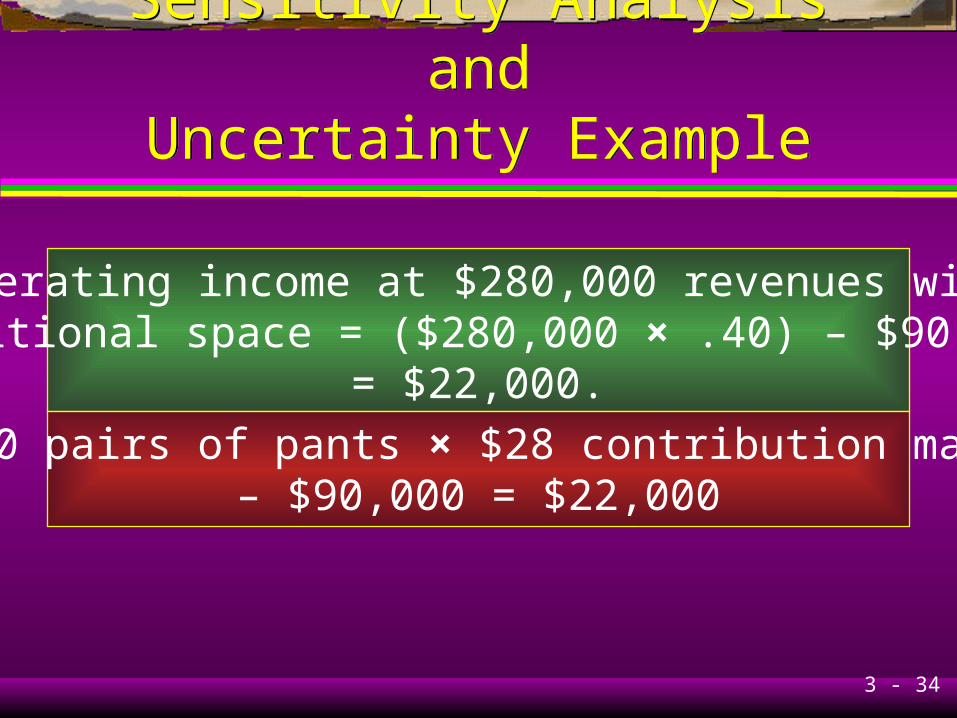

Sensitivity Analysis andUncertainty Example

Sensitivity Analysis andUncertainty Example

Operating income at $280,000 revenues withadditional space = ($280,000 × .40) – $90,000

= $22,000.

(4,000 pairs of pants × $28 contribution margin)– $90,000 = $22,000

3 - 35

Learning Objective 6Learning Objective 6

Use CVP analysis to plan

fixed and variable costs.

3 - 36

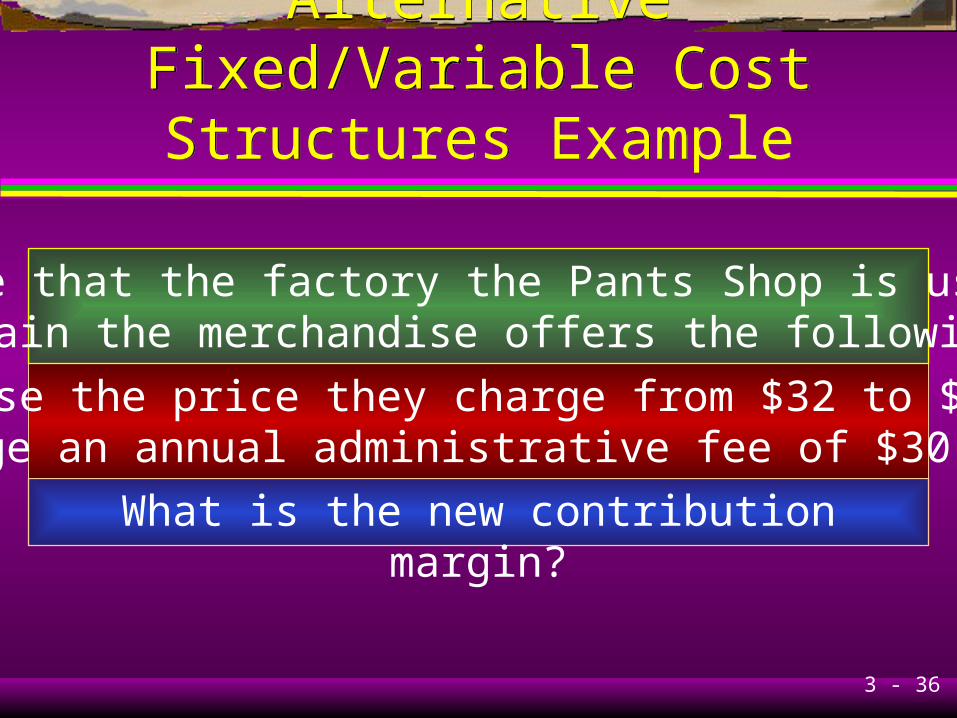

Alternative Fixed/Variable CostStructures Example

Alternative Fixed/Variable CostStructures Example

What is the new contribution margin?

Decrease the price they charge from $32 to $25 andcharge an annual administrative fee of $30,000.

Suppose that the factory the Pants Shop is using toobtain the merchandise offers the following:

3 - 37

Alternative Fixed/Variable Cost Structures Example

Alternative Fixed/Variable Cost Structures Example

$70 – ($25 + $10) = $35

Contribution margin increases from $28 to $35.

What is the contribution margin percentage?

$35 ÷ $70 = 50%

What are the new fixed costs?

$84,000 + $30,000 = $114,000

3 - 38

Alternative Fixed/Variable Cost Structures Example

Alternative Fixed/Variable Cost Structures Example

Management questions what sales volumewould yield an identical operating income

regardless of the arrangement.

28x – 84,000 = 35x – 114,000

114,000 – 84,000 = 35x – 28x

7x = 30,000

x = 4,286 pairs of pants

3 - 39

Alternative Fixed/Variable Cost Structures Example

Alternative Fixed/Variable Cost Structures Example

Cost with existing arrangement= Cost with new arrangement

.60x + 84,000 = .50x + 114,000

.10x = $30,000 x = $300,000

($300,000 × .40) – $ 84,000 = $36,000

($300,000 × .50) – $114,000 = $36,000

3 - 40

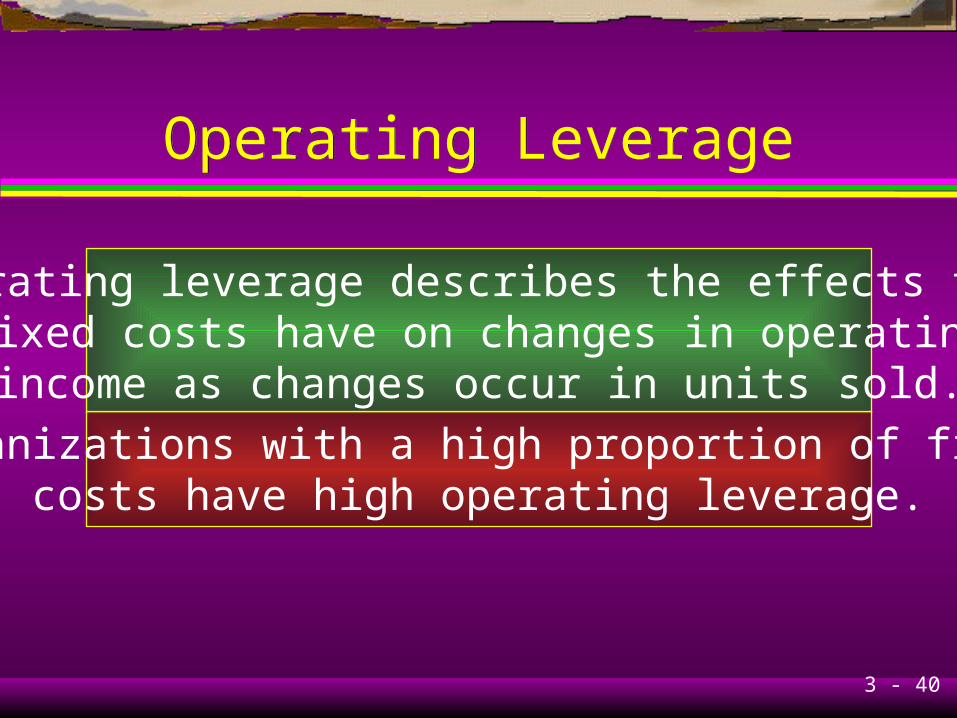

Operating LeverageOperating Leverage

Operating leverage describes the effects thatfixed costs have on changes in operatingincome as changes occur in units sold.

Organizations with a high proportion of fixedcosts have high operating leverage.

3 - 41

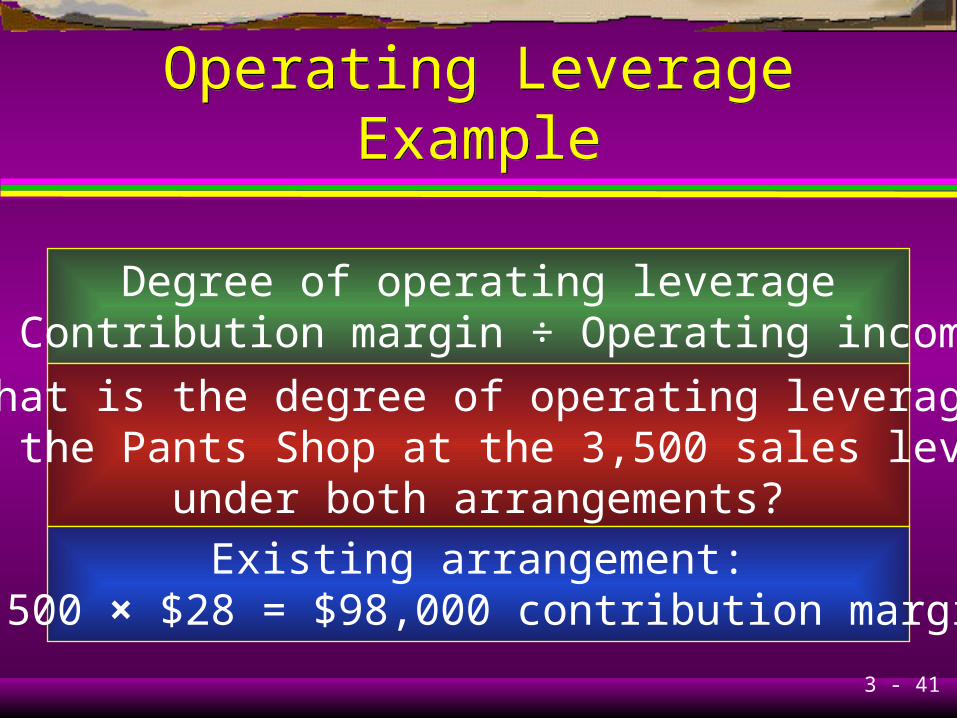

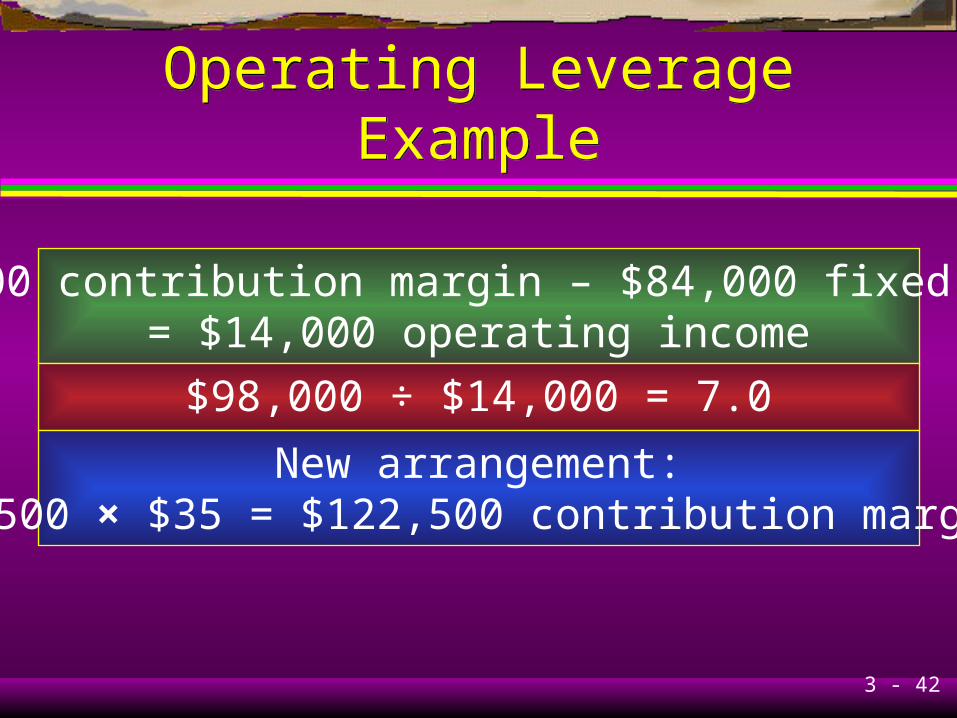

Operating Leverage ExampleOperating Leverage Example

Degree of operating leverage= Contribution margin ÷ Operating income

What is the degree of operating leverageof the Pants Shop at the 3,500 sales level

under both arrangements?

Existing arrangement:3,500 × $28 = $98,000 contribution margin

3 - 42

Operating Leverage ExampleOperating Leverage Example

$98,000 contribution margin – $84,000 fixed costs= $14,000 operating income

$98,000 ÷ $14,000 = 7.0

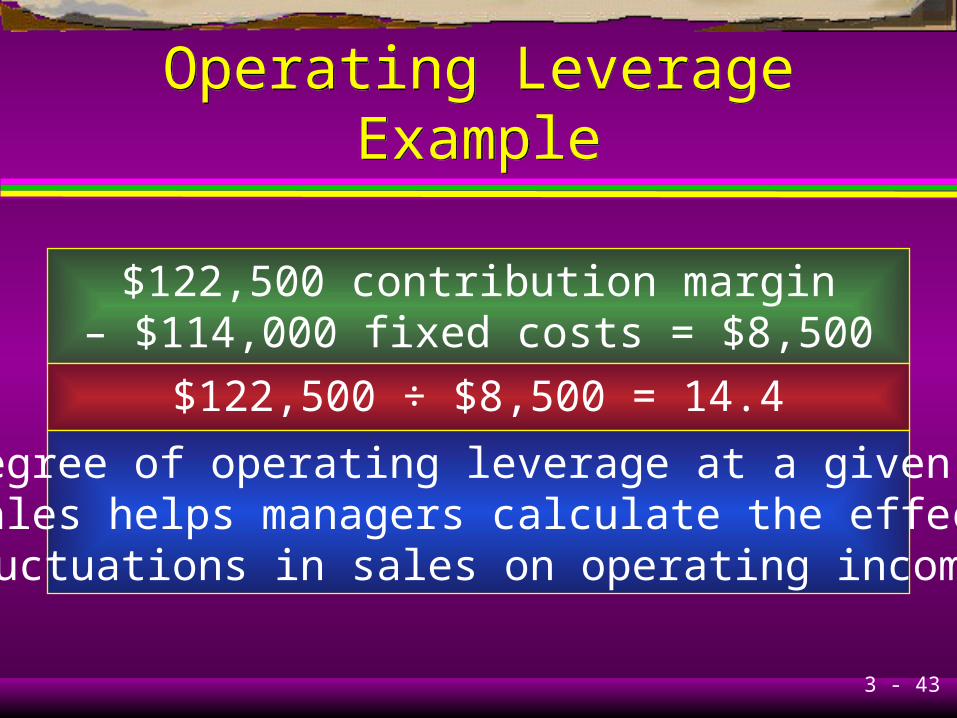

New arrangement:3,500 × $35 = $122,500 contribution margin

3 - 43

Operating Leverage ExampleOperating Leverage Example

$122,500 contribution margin– $114,000 fixed costs = $8,500

$122,500 ÷ $8,500 = 14.4

The degree of operating leverage at a given levelof sales helps managers calculate the effect of

fluctuations in sales on operating income.

3 - 44

Learning Objective 7Learning Objective 7

Apply CVP analysis to a company

producing different products.

3 - 45

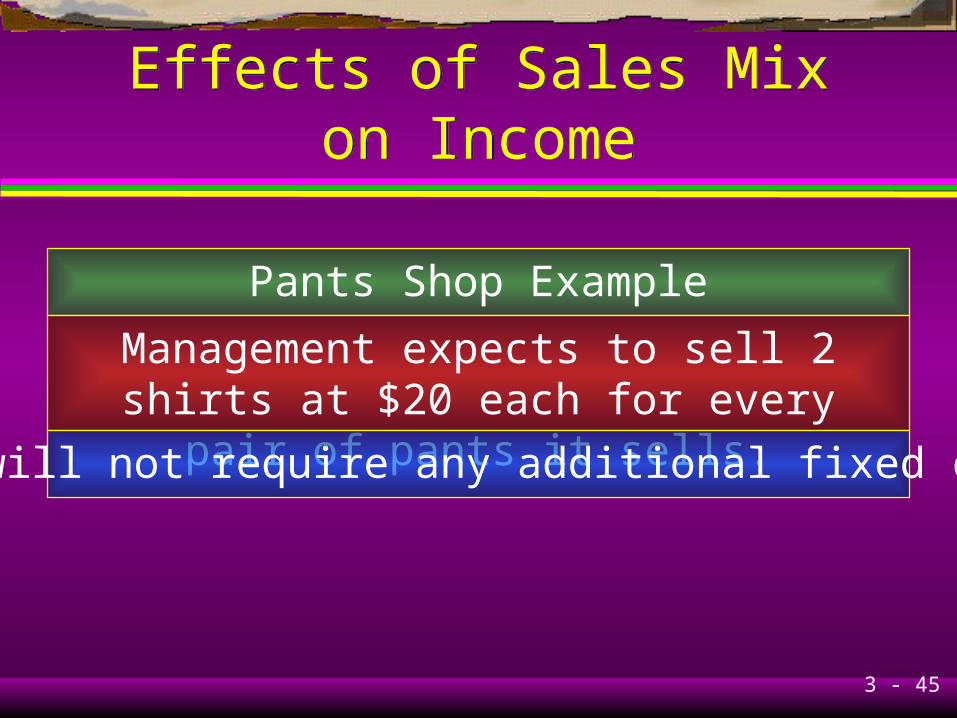

Effects of Sales Mix on IncomeEffects of Sales Mix on Income

Pants Shop Example

Management expects to sell 2 shirts at $20 each for every pair of pants it sells.

This will not require any additional fixed costs.

3 - 46

Effects of Sales Mix on IncomeEffects of Sales Mix on Income

What is the contribution margin of the mix?

Contribution margin per shirt: $20 – $9 = $11

$28 + (2 × $11) = $28 + $22 = $50

3 - 47

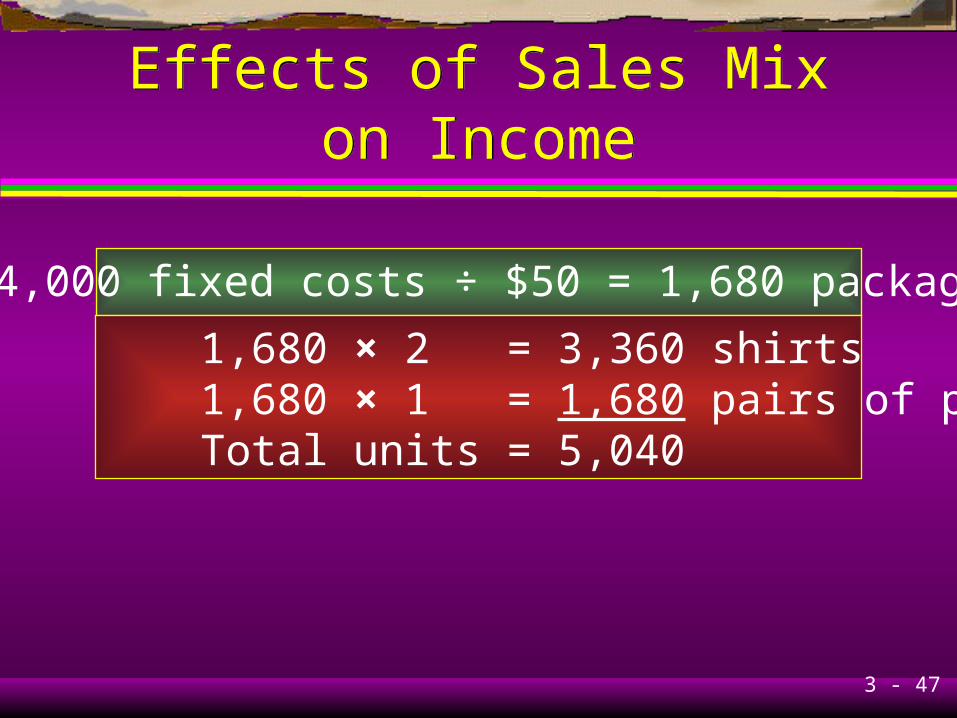

Effects of Sales Mix on IncomeEffects of Sales Mix on Income

$84,000 fixed costs ÷ $50 = 1,680 packages

1,680 × 2 = 3,360 shirts1,680 × 1 = 1,680 pairs of pantsTotal units = 5,040

3 - 48

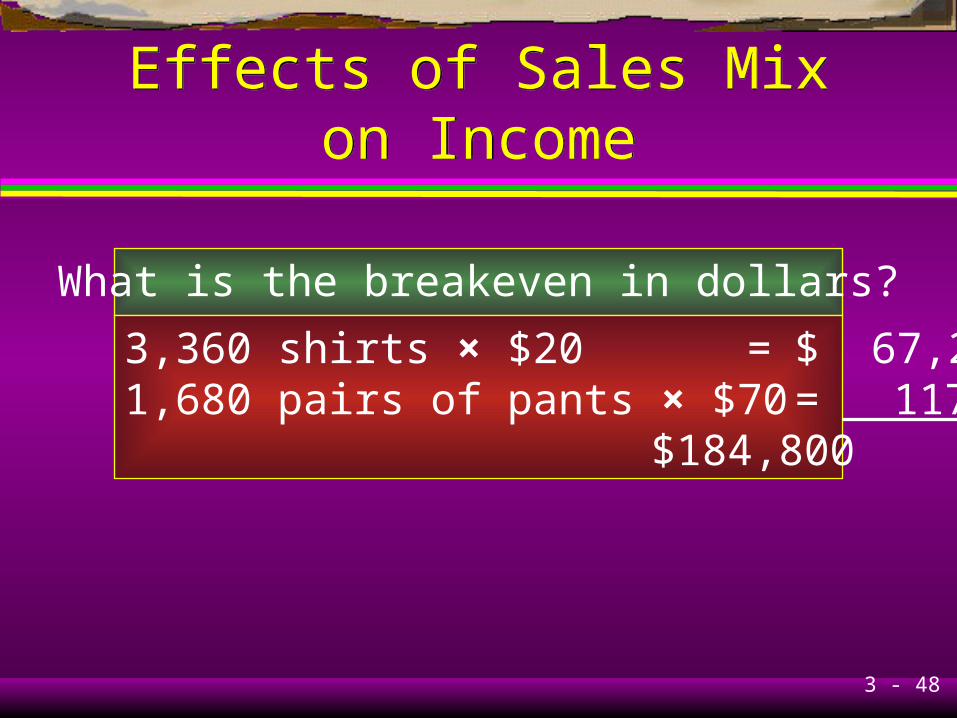

Effects of Sales Mix on IncomeEffects of Sales Mix on Income

What is the breakeven in dollars?

3,360 shirts × $20 = $ 67,2001,680 pairs of pants × $70 = 117,600

$184,800

3 - 49

Effects of Sales Mix on IncomeEffects of Sales Mix on Income

What is the weighted-average budgeted contribution margin?

Pants: 1 × $28 + Shirts: 2 × $11

= $50 ÷ 3 = $16.667

3 - 50

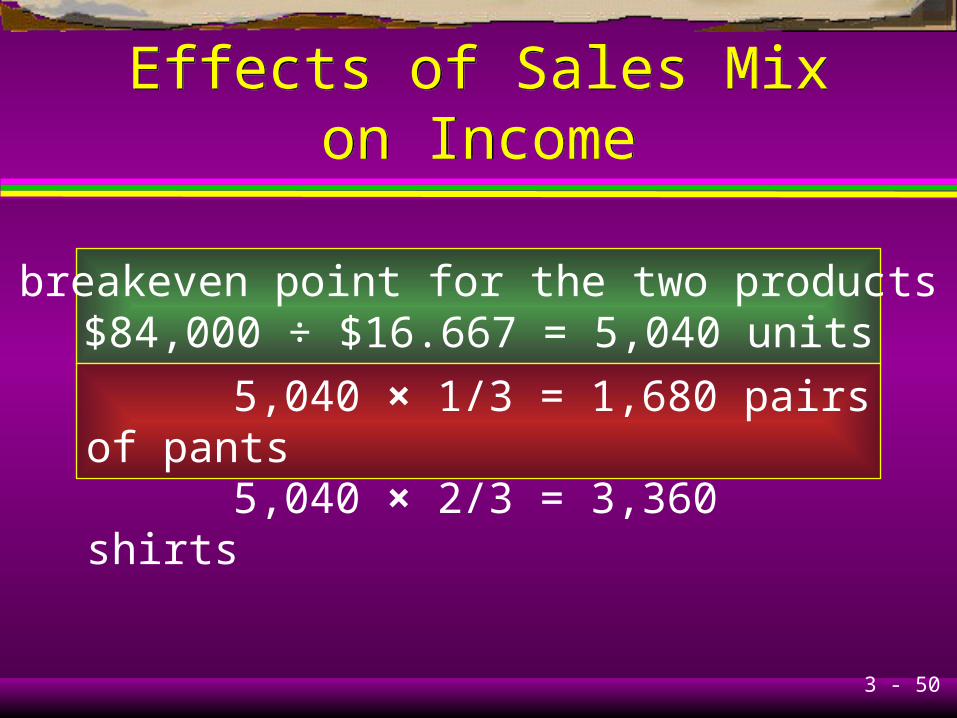

Effects of Sales Mix on IncomeEffects of Sales Mix on Income

The breakeven point for the two products is:$84,000 ÷ $16.667 = 5,040 units

5,040 × 1/3 = 1,680 pairs of pants 5,040 × 2/3 = 3,360 shirts

3 - 51

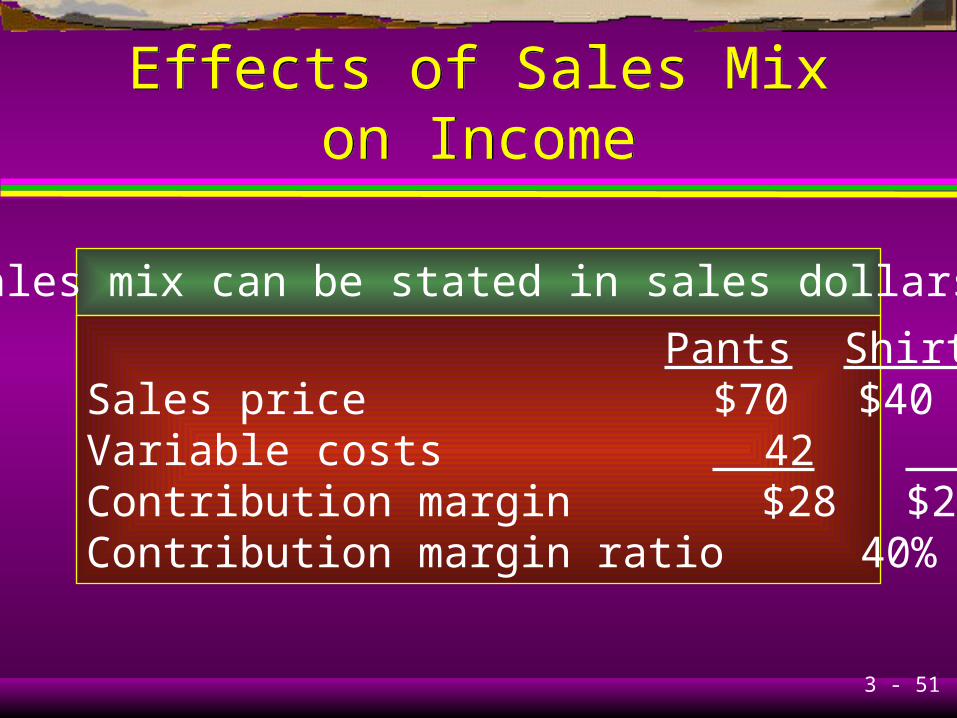

Effects of Sales Mix on IncomeEffects of Sales Mix on Income

Sales mix can be stated in sales dollars:

Pants ShirtsSales price $70 $40Variable costs 42 18Contribution margin $28 $22Contribution margin ratio 40% 55%

3 - 52

Effects of Sales Mix on IncomeEffects of Sales Mix on Income

Assume the sales mix in dollarsis 63.6% pants and 36.4% shirts.

Weighted contribution would be:40% × 63.6% = 25.44% pants55% × 36.4% = 20.02% shirts

45.46%

3 - 53

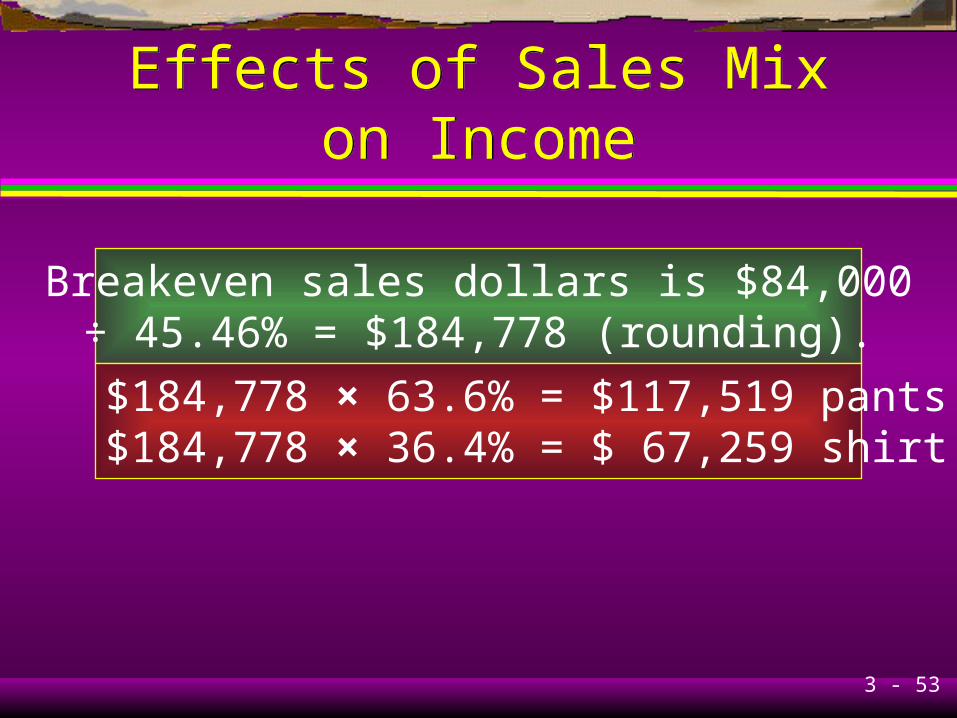

Effects of Sales Mix on IncomeEffects of Sales Mix on Income

Breakeven sales dollars is $84,000÷ 45.46% = $184,778 (rounding).

$184,778 × 63.6% = $117,519 pants sales$184,778 × 36.4% = $ 67,259 shirt sales

3 - 54

Learning Objective 8Learning Objective 8

Adapt CVP analysis to situations

in which a product has more

than one cost driver.

3 - 55

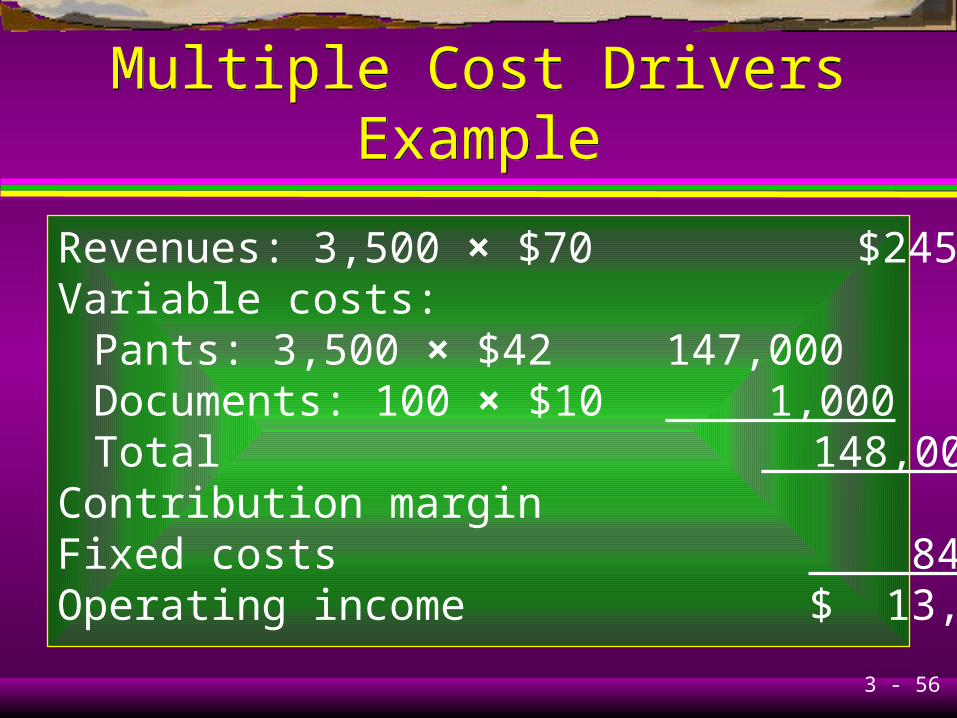

Multiple Cost Drivers ExampleMultiple Cost Drivers Example

Suppose that the business will incur an additionalcost of $10 for preparing documents associated

with the sale of pants to various customers.

Assume that the business sells 3,500pants to 100 different customers.

What is the operating income from this sale?

3 - 56

Multiple Cost Drivers ExampleMultiple Cost Drivers Example

Revenues: 3,500 × $70 $245,000Variable costs:

Pants: 3,500 × $42 147,000Documents: 100 × $10 1,000Total 148,000

Contribution margin 97,000Fixed costs 84,000Operating income $ 13,000

3 - 57

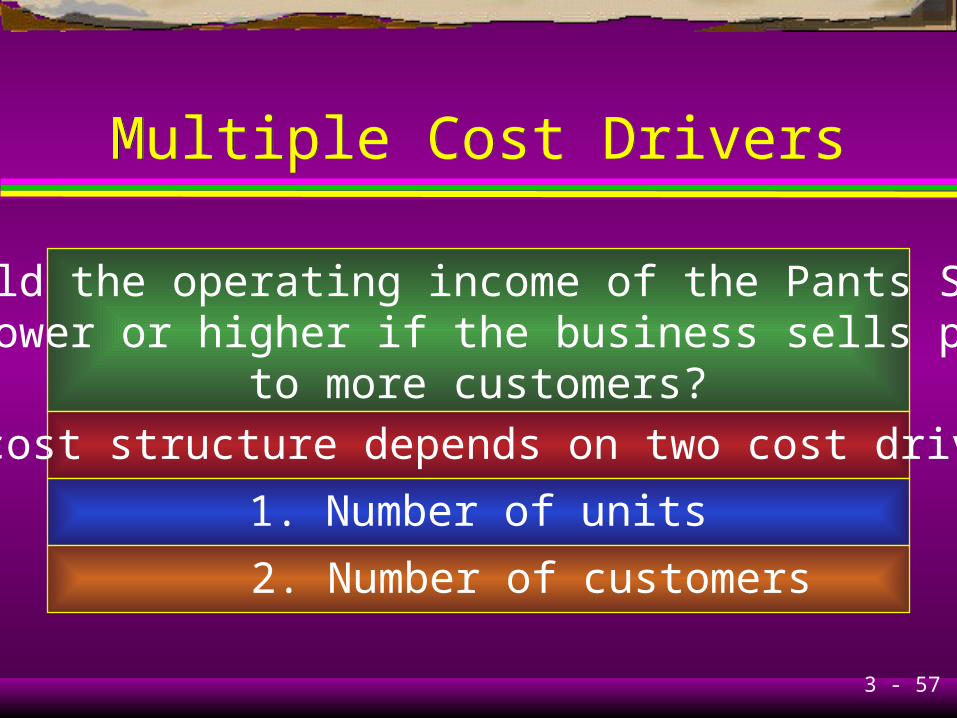

Multiple Cost DriversMultiple Cost Drivers

Would the operating income of the Pants Shopbe lower or higher if the business sells pants

to more customers?

The cost structure depends on two cost drivers:

1. Number of units

2. Number of customers

3 - 58

Learning Objective 9Learning Objective 9

Distinguish between

contribution margin

and gross margin.

3 - 59

Contribution Margin versusGross Margin

Contribution Margin versusGross Margin

Contribution income statement emphasizescontribution margin.

Financial accounting income statementemphasizes gross margin.

3 - 60

End of Chapter 3End of Chapter 3