29 February 2016 DAVID KERLY'S GOLD-SILVER-SHARES and MARKETS

11

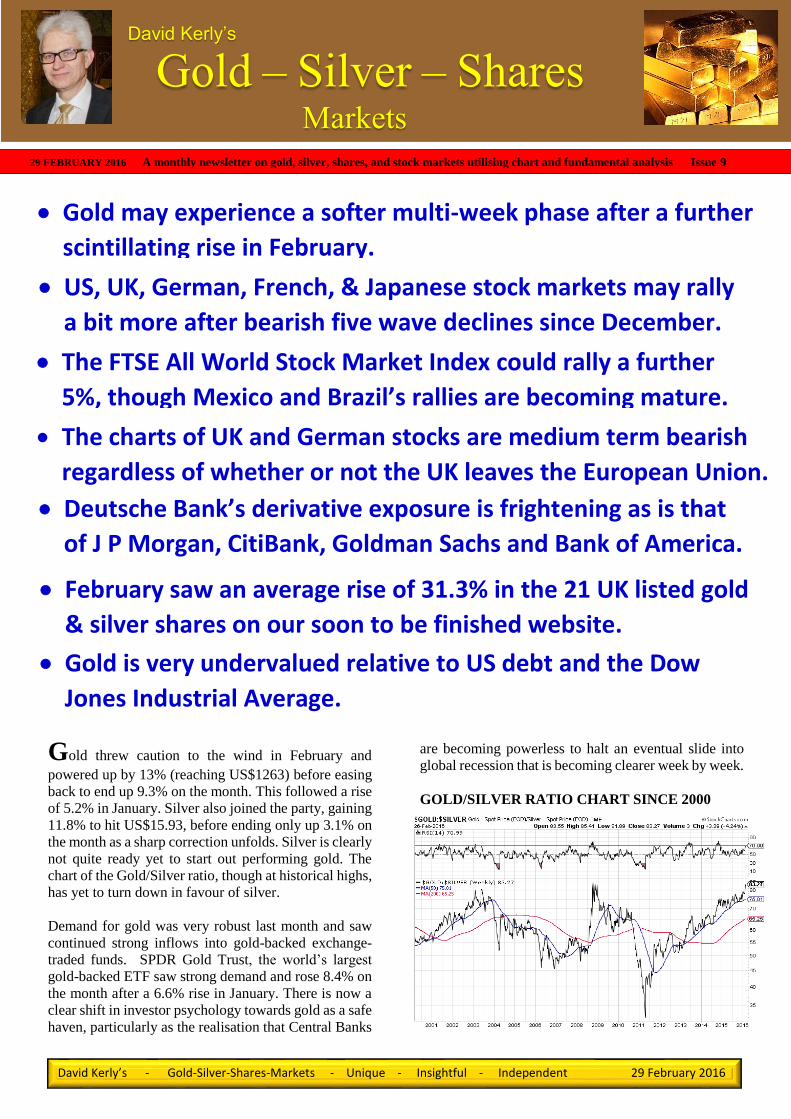

Gold – Silver – Shares Markets David Kerly’s David Kerly’s - Gold-Silver-Shares-Markets - Unique - Insightful - Independent 29 February 2016 Gold threw caution to the wind in February and powered up by 13% (reaching US$1263) before easing back to end up 9.3% on the month. This followed a rise of 5.2% in January. Silver also joined the party, gaining 11.8% to hit US$15.93, before ending only up 3.1% on the month as a sharp correction unfolds. Silver is clearly not quite ready yet to start out performing gold. The chart of the Gold/Silver ratio, though at historical highs, has yet to turn down in favour of silver. Demand for gold was very robust last month and saw continued strong inflows into gold-backed exchange- traded funds. SPDR Gold Trust, the world’s largest gold-backed ETF saw strong demand and rose 8.4% on the month after a 6.6% rise in January. There is now a clear shift in investor psychology towards gold as a safe haven, particularly as the realisation that Central Banks are becoming powerless to halt an eventual slide into global recession that is becoming clearer week by week. GOLD/SILVER RATIO CHART SINCE 2000 29 FEBRUARY 2016 A monthly newsletter on gold, silver, shares, and stock markets utilising chart and fundamental analysis Issue 9 The charts of UK and German stocks are medium term bearish regardless of whether or not the UK leaves the European Union. February saw an average rise of 31.3% in the 21 UK listed gold & silver shares on our soon to be finished website. US, UK, German, French, & Japanese stock markets may rally a bit more after bearish five wave declines since December. Deutsche Bank’s derivative exposure is frightening as is that of J P Morgan, CitiBank, Goldman Sachs and Bank of America. Gold may experience a softer multi-week phase after a further scintillating rise in February. Gold is very undervalued relative to US debt and the Dow Jones Industrial Average. The FTSE All World Stock Market Index could rally a further 5%, though Mexico and Brazil’s rallies are becoming mature.

-

Upload

david-kerly -

Category

Documents

-

view

116 -

download

0

Transcript of 29 February 2016 DAVID KERLY'S GOLD-SILVER-SHARES and MARKETS

’s

Gold – Silver – Shares Markets

David Kerly’s

David Kerly’s - Gold-Silver-Shares-Markets - Unique - Insightful - Independent 29 February 2016

Gold threw caution to the wind in February and

powered up by 13% (reaching US$1263) before easing

back to end up 9.3% on the month. This followed a rise

of 5.2% in January. Silver also joined the party, gaining

11.8% to hit US$15.93, before ending only up 3.1% on

the month as a sharp correction unfolds. Silver is clearly

not quite ready yet to start out performing gold. The

chart of the Gold/Silver ratio, though at historical highs,

has yet to turn down in favour of silver.

Demand for gold was very robust last month and saw

continued strong inflows into gold-backed exchange-

traded funds. SPDR Gold Trust, the world’s largest

gold-backed ETF saw strong demand and rose 8.4% on

the month after a 6.6% rise in January. There is now a

clear shift in investor psychology towards gold as a safe

haven, particularly as the realisation that Central Banks

are becoming powerless to halt an eventual slide into

global recession that is becoming clearer week by week.

GOLD/SILVER RATIO CHART SINCE 2000

29 FEBRUARY 2016 A monthly newsletter on gold, silver, shares, and stock markets utilising chart and fundamental analysis Issue 9

The charts of UK and German stocks are medium term bearish

regardless of whether or not the UK leaves the European Union.

or not.

February saw an average rise of 31.3% in the 21 UK listed gold

& silver shares on our soon to be finished website.

US, UK, German, French, & Japanese stock markets may rally

a bit more after bearish five wave declines since December.

Deutsche Bank’s derivative exposure is frightening as is that

of J P Morgan, CitiBank, Goldman Sachs and Bank of America.

Gold may experience a softer multi-week phase after a further

scintillating rise in February.

Gold is very undervalued relative to US debt and the Dow

Jones Industrial Average.

The FTSE All World Stock Market Index could rally a further

5%, though Mexico and Brazil’s rallies are becoming mature.

David Kerly’s - Gold-Silver-Shares-Markets - Unique - Insightful - Independent 29 February 2016

FINANCE OFFICIALS FROM G20 MEMBER

COUNTRIES MET IN SHANGHAI ON 26th-27th

FEBRUARY

As we suspected finance ministers and central bankers

of the G20 nations tried to reassure jittery financial

markets over this weekend that the global economy is

healthy. However, they acknowledged in a statement

that they "need to do more" to boost growth. It is our

view at Gold-Silver-Shares-Markets that they are going

to find it very difficult, to sustain growth, let alone

“boost it” given the downtrends that are developing in

the charts of global stock markets and economic data.

They promised on Saturday to use "all tools" to shore

up sagging global growth and to avoid devaluing their

currencies to boost exports, but made no pledges of joint

action. Such a comment reminds us of Mario Draghi’s

2012 comment that the ECB will do “whatever it takes”

to save the Eurozone from collapse. So far a policy of

Q/E and now negative interest rates is not working. We

note the German bank Commerzbank commented in its

2015 interim report last August that “companies

unwillingness to invest, which is reflected in low

demand for credit, is lessening only very gradually”.

Global growth is at its lowest in two years and

forecasters say the danger of recession is rising. The

International Monetary Fund cut this year's global

growth forecast by 0.2 percentage points last month to

3.4 percent. It said another downgrade is likely in April.

On Friday, Germany's finance minister said his

government would refuse to take part in any new joint

stimulus in the event of falling global growth. He

insisted governments had to embrace reforms instead.

The Shanghai meeting concluded that a possible vote to

withdraw from the Eurozone "is among the biggest

economic dangers this year," Osborne said. "If that's

their assessment of the impact on the world economy,

imagine what it would do to the U.K." We have also

noted the surprising openness displayed by George

Osborn recently in TV appearances and in the press

about the difficulties facing the UK economy.

Other gold exposed funds such as the UK based

BlackRock Gold & General Fund which invests in gold

and silver mining shares (77.4%) and precious metals

(17.7%) has risen 36.7% since the end of 2015. Below

we show a chart of it back to 2011.

A clear floor became established at 500 and the recent

sharp rise has cut the downtrend. Some work will

though be needed to get through major resistance in the

800 region. However, clearly, a buy on dips. We also

show a chart of the FTSE 100 index which is

diametrically opposed and is a clear sell on rallies.

GOLD – DAILY CHART WITH COT

(COMMITMENT OF TRADERS INDICATOR)

Gold rose further than we were expecting last month,

but as can be seen from the wide divergence in net

positions of Hedge Funds (large specs) and the

producers (commercials), a downward reaction is now

likely. As to how far it could react is, as ever, not an

easy task. However, it should at least drop back into the

David Kerly’s - Gold-Silver-Shares-Markets - Unique - Insightful - Independent 29 February 2016

US$1160 to US$1180 support zone from the

August/October top areas and quite possibly beyond

that to the 50% and 61.8% retracement levels at

US$1155 and US$1129. We should though get some

strong clues from the price action and the COT position

when a base or reaction low has been established.

Though we cannot say with certainty how long this may

take, we suspect that given the significant overextension

above the 200 day moving average, which has only just

turned up, that it may take longer than the gold bulls

among us would prefer. It’s a bit like the financial

prudence needed after blowing ones monthly salary on

a new bike or the new Microsoft surface book laptop!

SILVER – DAILY CHART WITH COT

(COMMITMENT OF TRADERS INDICATOR)

Silver broke above resistance from the early December

high of US$14.66 sooner than expected. This completed

a near three month base pattern, meeting and exceeding

our target of US$15.30, the 61.8% retracement level and

the base target of US$15.62 to reach US$15.92 before

retreating. Silver was unable to extend anywhere as far

above the 200 day moving average that gold did and is

now in danger of dropping well back into the underlying

near three month base area. In fact we would not be

surprised to see short positions being aggressively built

up in anticipation of even a test of the December lows

around US$13.62-US$13.66. Such is the volatile nature

of silver though, that we would again not be surprised

to see a sharp recovery once a fresh floor had been

established. Here too, some advance warning should be

evident in the price action and COT position.

STOCK MARKET RALLIES FOLLOW FIVE

WAVE DECLINES

The sharp falls in stock markets during the opening half

of January and February were waves three and five,

completing the down legs from the early December

highs. We have labelled the waves on the five stock

market charts shown.

The MACD for the S&P 500 Index is very similar to

that seen in September/October when a bear market

rally followed. This time the rally has scope to test the

2025-2050 supply area before selling pressure reverses

the market to the downside for a fresh bear leg.

The FTSE 100 has oscillated around the key long term

pivotal level of 6000 since September, but still shows a

completed Elliott five wave move at the 5500 February

low. Potentially the current rally could extend towards

a test of the falling 200 day moving average near 6325,

though resistance around 6200 could provide the

ceiling. Thereafter, the next down leg should begin.

David Kerly’s - Gold-Silver-Shares-Markets - Unique - Insightful - Independent 29 February 2016

The German DAX Index (bottom of previous page)

does not look quite as weak as the FTSE 100 Index on

a longer term chart (see our 01 February newsletter- last

page), though it has fallen the most (29.7%) from last

years high. It needs to break the pivotal 8170 level to

really set the bear market on its way. Near term, the

completed five waves from the December high

signalled the current rally. This may extend into the

10,000-10,250 region but probably falling short of the

200 day moving average now at 10549, before the

downtrend resumes.

France’s CAC 40 Index saw its fifth wave bottom just

over two weeks ago at 3892. The latest rally just tests

the falling 50 day moving average also close to the

August/September lows. Clearing the top of wave 4

near 4100 should open a further rally but probably no

more than 4500-4600 before selling pressure returns.

Japan’s Nikkei 225 Index looks to have the weakest

pattern of the five indices since last autumn, though has

not fallen (29%) quite as far as the DAX Index. Rally

scope looks confined to below the top of wave four at

17,905 before fresh weakness returns later on.

Thereafter the risk would be for a test of the 2014 low

at 13885.

TWO YEAR HEAD AND

SHOULDERS TOP IN FTSE

ALL WORLD STOCK

MARKET INDEX

The plunge in World stock markets in January through

a 245-250 neckline completed a large two year head and

shoulders top pattern, signalling the onset of a major

bear market in global stocks. A fall of 20.8% from the

May 2015 peak of 292.79 (just beyond a 20% drop)

officially confirmed a bear market. This has in our

opinion only just begun, though a further near term

rally, but to probably no more than to the 260 area

(+5%), may follow to further unwind a recent oversold

condition. The target (which is of course only a

minimum) from the H & S is the 200 area. That would

represent a decline of 31.7% from last year’s record

high.

MEXICO AND BRAZIL ARE FURTHER INTO

THEIR RALLIES

David Kerly’s - Gold-Silver-Shares-Markets - Unique - Insightful - Independent 29 February 2016

The Mexican stock market completed its five wave

bear leg in January, one month earlier than US, UK,

European and Japanese bourses. Consequently it has

already rallied 10% from the recent low and may now

be in wave three (of a corrective three) or in effect an

A-B-C as we have labelled on the chart (shown on the

previous page at the bottom). A lot of overhead supply

is evident between current levels and 45,700 and we

would expect the market to reverse to the downside

before long.

The Brazilian Bovespa Index has been in a bear market

since the end of 2010, just over five years. The decline

to this January’s low of 37,000 represents a near 50%

fall from the 2010 peak of 73,100, or an 11% drop from

last May’s high. Given that the 50% level (36,550) is a

potential prime rebound level (37,000 is pretty close),

we should be on the lookout for more than just a bear

market rally, as currently appears to be underway now.

A daily close, at least to 46,000, clearing a pivotal

resistance area at 44,000 to 45,000 and a 10 month

(purple) trend line would suggest further upside, rather

than the risk, along with world stock markets, of fresh

downside later on. We would add that commonality, in

terms of the main trend with other markets, would be

more likely given the bearish look to the long term

chart.

BREXIT ? OR NOT FROM THE EU?

Whether the UK decides in June to stay in or leave the

Eurozone is to some extent an academic exercise. The

UK and German stock markets are already officially in

bear markets (down 22.8% and 29.7% from last year’s

peaks) and have further to fall. If we leave, the positives

and negatives will probably cancel each other out.

One of the main positives to being out would hand back

the right for us to control our own borders. Thus,

immigration could be controlled. Hmm, whether it

would is a topic for debate given that historically the

UK has always been regarded as a “soft touch” in that

regard. It would though potentially make it harder for

terrorists to enter the UK. Though once again that is also

open to debate given the persistence of such

organisations or individual’s intent on inflicting harm.

What would be a benefit is the elimination of social

security payments to family members of immigrants

still in their own countries.

On the one hand some trade deals between UK and EU

companies require both to be in the EU vis a vis being

eligible for the necessary documentation and other

requirements, though we suspect that the rules could be

bent if vested interests were strong enough. However,

not being in could be viewed negatively in this

particular aspect. A recent prime ministers question

time provided us with an amusing analogy to the

negative camp. Lack of an appropriate suit and tie as far

as Jeremy Corbyn is concerned could prevent him from

being admitted to a select Gentlemen’s Club. Do they

still exist?

“DERIVATIVES ARE FINANCIAL WEAPONS

OF MASS DESTRUCTION” – WARREN

BUFFETT

Germany’s largest bank, DeutscheBank had as at 31

December 2014 (as shown in its 2014 annual report and

accounts) an exposure of 52 Trillion euro’s to

derivatives, over 15 times larger than the GDP of

Germany, over 4 times the size of the GDP of the

Eurozone or not far short of the entire GDP of the world

in 2014 (Euro’s 71 Trillion or US$77.6 Trillion). Derivatives can be big money spinners for large

banking institutions when trading conditions remain

fairly stable. However, when market conditions are

volatile and markets move further than anticipated and

in unexpected directions, then these derivative

instruments can very rapidly expose banks and indeed

the entire financial system to massive risks. The long

term capital management (LTCM) disaster in 1998

which would have taken the entire financial system

down was averted by the Federal Reserve bail out. LTCM failed because the volatility that ensued in stock

markets and bonds after Russia declared it was

devaluing its currency and basically defaulting on its

bonds, was beyond the regular range that LTCM, who

used derivatives, had counted on. Also, the wild

derivative exposure that grew up out of US sub-prime

mortgage lending in 2005 and 2006 which would have

also taken down the entire financial system in 2008 was

averted by central banks once again. However, in the

next disaster, which we believe has already been

written, central banks have said that they will not step

in this time to save too big to fail institutions. The risk

falls on to the shoulders of shareholders and bank

creditors, e.g. current account holders. Cypress and

Greece were warnings!

David Kerly’s - Gold-Silver-Shares-Markets - Unique - Insightful - Independent 29 February 2016

It doesn’t stop there as DeutscheBank is not the only big

player in derivatives. Four of the largest US banks, J P

Morgan, CitiBank, Goldman Sachs and Bank of

America have combined derivatives exposure of

US$175 Trillion, between two and three times the entire

GDP of the World economy. Also, as of 30 September

2015 the total exposure of the 25 largest US banks was

US$191.7 Trillion.

Below we show the stock price charts for the five

banks that have the most exposure to derivatives.

The least bad is JP Morgan, which may or may not be

due to the fact that you could argue that their derivative

exposure is to some extent “hedged” by the largest ever

hoard of silver amassed in history. However, at current

prices that is still only worth between US$5billion to

US$6 billion.

The chart of DeutscheBank goes back beyond the

2008/2009 lows of 18.39 which were recently taken out,

the shares reaching 14.78. They have since rallied to

17.32, still under the lows of seven years ago, but the

chart is very bearish and any further rally may be hard

pushed to exceed the low 20’s.

J P Morgan has met support from the late 2014/early

2015 lows at US$52.50 and has rallied to near

US$60.00 so far. It could get to US$62.00-US$63, but

an eventual break of US$50.00 opens the risk of a

significant decline.

Citigroup (Citibank) completed a very wide (35 month)

top pattern on January’s break of key neckline support

at US$45. That US$45 level should prove to be a very

solid ceiling and the top pattern calls for a later

downside target of US$30, ahead of the 2012 lows

around US$25.

David Kerly’s - Gold-Silver-Shares-Markets - Unique - Insightful - Independent 29 February 2016

Goldman Sachs completed a 17 month Head and

Shoulders top pattern in January on the loss of US$170

neckline support. A return rally towards the neckline

may follow, but the risk is for renewed weakness to a

minimum H & S target of US$125 (US$140 seen

already) and possibly US$110 to US$120 where a band

of support is evident, mostly formed during 2012.

Bank of America completed a 27 month top pattern,

also in January, and has already met the minimum target

of around US$11.00. The top area is not so “high” as

most of the others but ultimately the width of the pattern

should be able to force a lower target of US$8.60 to

US$9.80, the upper region of the trading activity in

2012.

THE WORLD’S FINANCIAL SYSTEM IS A

TICKING TIME BOMB

The derivatives markets have been largely unregulated

for the last 15 years and most derivatives are traded over

the counter (OTC). That is to say seller direct to buyer

and vice versa. As of 30 September 2015 OTC

derivatives by the top 25 US banks accounted for 93.5%

of the US$191.7 Trillion exposure. The total global

market for derivates traded in unregulated fashion

(OTC) is a mind boggling US$630 Trillion (31

December 2014), or eight times World GDP. This is

without doubt a ticking time bomb of epic proportions.

By now it should have become abundantly clear why

gold, and also silver, are the preferred assets to hold

looking immediately forward and some years hence.

In a 2015 Q3 bulletin by the Bank of England, entitled

OTC derivatives, central clearing and financial stability,

the author, Arshadur Rahman, states that “When OTC

derivatives are traded bilaterally, they involve the risk

that a counterparty fails to meet their obligations under

the contract” This of course is what happened around

the time of the Lehman Bros collapse in 2008. “This

risk can be mitigated by using a CCP (central

counterparty) to centrally clear the transaction. The

CCP acts as buyer to every seller, and seller to every

buyer, simplifying the network of exposures within the

system.”

“Central clearing is therefore recognised as a key way

to manage systemic risk. Following the financial crisis

of 2007–09, G20 leaders agreed to reform the structure

of OTC derivatives markets, requiring that contracts

which are sufficiently standardised be centrally cleared.

The United States and Japan have already implemented

this ‘clearing obligation’ for certain interest rate and

credit derivative contracts. The European Union is

scheduled to do so in 2016. Approximately 50% of

interest rate contracts and 20% of credit derivative

contracts outstanding globally are now centrally

cleared.”

Interest rate and foreign exchange derivatives

accounted for 76.7% and 16.7%, respectively of

derivative contracts either regulated or OTC. The

remainder are mainly Credit derivatives (4.3%), the

ones which blew up in 2008. Figures as at 30 September

2015. With the unusually currently low interest rate

environment and some even going negative, the

potential for derivative “shocks” could be rising. Also,

the risk for a derivate “upset” in the Foreign Exchange

markets has perhaps got to be greater, particularly with

“currency wars” between countries on the rise. This

time around credit derivatives may not be the future

“problem”.

Also we note that in the bulletin it says that:

“According to data collected by the Bank for

International Settlements (BIS), the United Kingdom is

the single largest global venue for OTC derivatives

activity: it accounts for almost half of all global activity

in interest rate derivatives, and over a third of global

activity in foreign exchange derivatives contracts

(Chart 3).(1) The United Kingdom is also a major

centre for the central clearing of OTC derivatives

contracts: it is home to four CCPs, which between them

account for most of the cleared activity in OTC interest

rate derivatives globally, and a substantial proportion of

the cleared activity in the other asset classes.(2)

David Kerly’s - Gold-Silver-Shares-Markets - Unique - Insightful - Independent 29 February 2016

RISKS TO THE UK FINANCIAL SYSTEM

“The size of the UK market and the systemic

importance of some of the CCPs within it make it

essential for the Bank of England to understand and

monitor the risks arising from this sector. The Bank is

the supervisor of UK CCPs, and in fulfilling this

function it works closely with other authorities in

regulatory colleges (see Supervisory co-operation

section later). The Bank’s Financial Policy Committee

(FPC) considers risks to the UK financial system more

broadly, including from outside the core banking

system. It intends to conduct an in-depth analysis of the

derivatives market during 2016.”

This “spider web” chart looks rather complex and

potentially financially catastrophic. It may not be.

However, can anyone be so sure it is not?

POTENTIAL ADVERSE EFFECTS OF CCP

POLICIES

“As CCPs become more central to OTC derivatives

markets, the risk increases that they could take actions

which have the effect of imposing stress on other parts

of the financial system. For example, under the CPMI-

IOSCO Principles, CCPs are expected to consider the

potentially adverse effects of the models they use to

calculate clearing member margin requirements. This

includes in particular the impact of procyclicality,

whereby margin requirements may increase rapidly

during periods of market stress. In such situations,

CCPs may require their clearing members to post

more margin due to worsening market conditions,

but these conditions themselves may make it more

difficult to source that additional margin, and also

further reduce the value of the margin already

posted, thus driving up margin requirements even

more. Procyclicality can cause liquidity stress,

because clearing members posting margin might

have to find additional liquid assets precisely at

times when they are least able to do so.”

IAMGOLD Corp +2.1% in Jan 201

At this pivotal point in the global economic, stock market, currency and interest rate markets cycles, the

extremely excessive exposure of the global banking system to derivatives is in our view a totally stupid, crazy

and downright irresponsible situation for the world to be in because of the unbridled greed of huge

investment banking organisations. This is going to end badly – Warren Buffett is right.

David Kerly’s - Gold-Silver-Shares-Markets - Unique - Insightful - Independent 29 February 2016

In February the 21 UK listed gold and silver

producers that we follow from a fundamental and

technical standpoint rose by an average of 31.3%

during February. Charts with analysis and technical

commentary will in future be posted on our soon to

be finished unique website.

These are the individual shares in descending order of

performance last month.

1 Trans-Siberian Gold + 116.4%

2 Avocet Mining + 90.6%

3 Aureus Mining + 61.9%

4 Anglo Asian Mining + 46.5%

5 Hochschild Mining + 42.6%

6 Fresnillo + 37.6%

7 ASA Resources + 33.3%

8 Patagonia Gold + 33.3%

9 Centamin + 32.1%

10 Randgold Resources + 29.0%

11 Petropavlosk + 24.5%

12 Highland Gold Mining + 22.0%

13 Pan African Resources + 20.9%

14 Acacia Mining + 19.3%

15 Serabi Gold + 18.2%

16 Caledonia Mining + 14.6%

17 Orosur Mining + 14.2%

18 Polymetal International + 13.0%

19 Griffin Mining + 1.5%

20 Shanta Gold - 5.0%

21 Vast Resources - 8.9%

US DEBT & DEBT LIMIT vs GOLD since 2000

Here we can see how up until 2011 gold rose in the same

direction as US debt (red line) and the US debt limit

(black staircase trend). Since then however, an apparent

anomaly is evident. The gold price has fallen back

significantly. This can be explained by a combination of

(A) a market which had in 2011 got ahead of itself and

was in need of a correction and (B) large vested interests

using the trend change to exploit the market to their

advantage while other diametrically opposed markets,

namely stock indices were being forced higher by

similar vested interests. This of course is nothing new

in the gold market, a market whose small relative size

to stock markets makes it ripe for such “manipulation

“and whose exchange traded demand is inversely

correlated with such financial instruments. The longer

term chart of gold vs US federal debt since 1970

demonstrates this amply.

Clearly, the potential now is for gold to play “catch up”

with US debt, the other side of the equation which is, at

present, unlikely to fall to close the gap.

200 YEARS OF THE DOW/GOLD RATIO

This very long term chart of the Dow Jones Industrial

Average relative to gold in US dollars shows that since

the formation of the Federal Reserve in 1913 the ratio

has seen very wild swings. This is in essence the boom

and bust cycle, which since the involvement of the Fed

has been more violent and thus has created greater

opportunities for profit or loss within the capitalist

system.

The last big upswing from 1980 was the boom cycle and

from the year 2000, the bust cycle which favours gold

over stocks has been underway. This has yet to

completely to run its course. Our take on that is shown

on the same chart but with annotations, trend lines and

arrows.

David Kerly’s - Gold-Silver-Shares-Markets - Unique - Insightful - Independent 29 February 2016

The latest four year rise in the ratio we think is akin to

the two year rise that occurred between 1974 and 1976

when gold fell from US$197 to US$103.50. The fall in

gold from the 2011 high of US$1920 is coincidentally

about ten times the 1974 high and also about ten times

(US$1046) the low seen in 1976. The two declines are

virtually the same also at around 46% to 47%.

So what some would say! Well, taken on its own we

would have to agree with them. However, this is not the

only reason to suggest that this is more than just a

coincidence. Then as now, the world was undergoing

great changes in the global economy. Inflation began to

take off in the second half of the 1970’s as soaring oil

prices and the loss of control over economic conditions

by central banks led to a runaway gold price.

The situation as far as inflation is concerned is reversed.

The risk now is for deflation to gather pace as Q/E and

zero/negative interest rates fail to attract demand from

heavily indebted consumers and corporates whose only

means to growth has been in record values of Merger

and Acquisition activity and share buy backs. Cost

cutting in newly acquired businesses will also help to

kick start a rise in unemployment from historically low

levels and thus further feed a deflationary environment.

Falling oil prices have also contributed to the

deflationary trends.

While the likelihood of making long term targets that

pan out as forecast is not great and indeed perhaps of

dubious value given that most will have forgotten what

the target was, or indeed that a target was even made, in

this instance we feel that such a major change in global

markets that we see ahead warrants an attempt at least.

The similarity with 1974-1976 continues with the

location on the chart. That is the two respective lows

(1974 and 2011) appear about the same extent below the

bottom of the green confidence band and the highs

(1976 and 2015) near or towards the rising dark green

centre trend line.

Widening red boundary lines since 1929 and 1933 puts

the lower red boundary towards the 0.8 level. Whether

the ratio gets as low as that is open to debate. If it

eventually does that would also mean a greater

percentage decline than seen in the move to the 1980

low (gold high/Dow low). However, given the potential

for a major bear market in stocks, which we argue is

already underway, then a fall in the DJIA back to its

2009 lows around 6470 is quite feasible. Probable, only

time will tell. For the ratio to get to 0.8 that would imply

a gold price of just over US$8000 per ounce. We have

David Kerly’s - Gold-Silver-Shares-Markets - Unique - Insightful - Independent 29 February 2016

had that figure in our heads for some time, but it does

make sense, particularly if a return to some form of gold

standard takes place in the years ahead because of

currency debasement. However, we could well be way

out, in which case the folly of making long term targets

will become apparent, assuming that any one will

remember them in the years to follow!

FINALLY A CHART THAT SPEAKS VOLUMES

ABOUT THE LEVEL OF THE UK HOUSING

MARKET

I am grateful to a client of Fuller Treacy Money, who

saw one of my newsletters posted on this excellent

website, for reminding me of this chart. I worked for

David Fuller and Anne Whitby back in the days of Chart

Analysis and learnt a lot from these great masters and

enjoyed my 4 years there immensely.

For fans of Elliott wave analysis this has to be a classic.

It is very clear and has five waves, the last of which is

also made up of five waves. So this market, UK average

house prices is finally approaching a grand top, some 45

years or so from its bull market beginnings around

1970. It also ties in with the ratio of average earnings

to average house prices. This is now around 5.69, just

under the 2007 peak of 5.83, and is thus actually

showing bear divergence with the average UK house

price.

Also, the chancellor’s imposition from 6th April of a 3%

levy on buy to let has already led to a final surge in

prices, a trend ending characteristic, also seen at the end

of wave 1 in 1988/1989 when multiple mortgage

interest relief ended. The stage is now set for a very

significant fall in UK house prices in the years ahead.

DISCLAIMER

Gold-Silver-Shares-Markets expresses our views and

opinions on precious metals, shares and other financial

markets and are subject to change without notice. Trading or

investing in stocks or any other financial market carries a high

degree of risk and it is possible that an investor may lose part

or all of their investment. The information in this newsletter

is expressed in good faith, but is not guaranteed. A market

service that is completely accurate100% of the time does not

exist. Please ask your broker or investment advisor to explain

the risks involved before making any trading and investing

decisions.

![INVESTOR FACT SHEET - Denver Gold Group Resources Fact...Shareholding [1] (shares in millions) Public Float 161.7 Silver Standard Shares 17.0 Total Issued & Outstanding Shares 178.8](https://static.fdocuments.net/doc/165x107/5e7178c6fb707741215015b0/investor-fact-sheet-denver-gold-group-resources-fact-shareholding-1-shares.jpg)