28pp105766 C&W_Troyes_MacArthurGlen_inv2

28

Leading Designer Outlet Centre Investment Troyes Designer Outlet France

-

Upload

squeeze-design -

Category

Documents

-

view

215 -

download

1

description

Leading Designer Outlet Centre Investment France 18 Planning 20 Tenancies 06 Location 27 Proposal 16 Description 25 McArthurGlen Designer Outlets 12 Situation 08 Socio Economic Profile 22 Major Asset Management Initiatives 10 Outlet Centre Retailing

Transcript of 28pp105766 C&W_Troyes_MacArthurGlen_inv2

Leading Designer Outlet Centre Investment

Troyes Designer OutletFrance

Contents05 Investment Summary

06 Location

08 Socio Economic Profile

10 Outlet Centre Retailing

12 Situation

16 Description

18 Planning

19 Tenure

20 Tenancies

22 Major Asset Management Initiatives

25 McArthurGlen Designer Outlets

27 Proposal

Troyes Designer Outlet

TrO

yes

Des

Ign

er O

UTL

eT

03

Defensive asset class with excellent tenant line-up.

Over 200 designer and high street brands at discounts of up to 70% in an attractive ‘village’ environment.

Circa 3 million visitors each year.

Total sales for the first 5 months of 2009 up 9.6% and like for like sales up 4.2%.

France’s largest designer outlet in a market where per capita provision is one of the lowest in Europe and new developments are limited.

Troyes Designer OutletMall 1

Decathlon‘Oxylane Village’ site

Adidas

Mall 2

Fidia site

D610 Rocade

N77

To Troyes Centre Ville

To Paris

To Dijon / Reims

■■ A rare opportunity to acquire one of France’s leading

designer outlet centres.

■■ Well located and easily accessible from Paris, Reims and

Dijon in the scenic Champagne-Ardenne region. Recent

road improvements have enhanced accessibility.

■■ over 200 brands in 117 stores and catering outlets

totalling 30,000 sq m.

■■ Developed and managed for over 14 years by

McArthurGlen - market leader in the outlet sector.

■■ Circa 3 million customers enjoying designer and high

street brands at discounts of up to 70% in an attractive

and safe village environment.

■■ France’s largest designer outlet - successful phase IV

extension completed in 2007/08 with 26 new stores

including: Calvin Klein, swarovski, Lindt, Geox, Zadig &

Voltaire, Gerard Darel, swatch, Guess, and Mango.

■■ Defensive asset class and excellent security of income

spread across a high number of dominant retailers.

■■ 2009 first five months total sales up 9.60% and like for like sales

up 4.24% against last year.

■■ High occupancy and strong income growth - rents linked

to tenant turnover with a minimum base subject to annual

indexation.

■■ Low turnover rent percentage relative to new agreements in

phase IV (Mall 1) offering excellent opportunity for improved

lease terms.

■■ Real and significant scope for future value growth from asset

management including proposals to extend and provide a

more coherent link between Mall 1 and 2.

Investment Summary

TrO

yes

Des

Ign

er O

UTL

eT

05

Troyes

Lyon

Paris

troyes Designer outlet is the dominant scheme in a town

considered to be the centre of outlet shopping in France.

troyes is capital of the Aube département, within the

Champagne-Ardenne region of north-eastern France.

Located on the seine river the town is 120 km south of Reims,

160 km north of Dijon and 150 km south-east of central

Paris. Aube is one of the 100 départements of France with

a population in excess of 300,000 and is a popular tourist

destination particularly for those living in the Paris region.

troyes is a medieval town of timber framed houses, narrow

streets and a beautifully preserved historical centre - it boasts

a gothic cathedral, some marvellous churches, a system of

boulevards shaped like a champagne cork, a Université de

technologie, and some excellent shopping opportunities.

Rising from a strong link with the textile industry there

are currently still close to 150 companies in the troyes

area linked to the textile trade including a specialised

research centre (ItF Maille). Major troyes brands include

Lacoste, DD, Absorba, Petit Bateau and Gil.

Locationthe town has excellent access located at the junction of the A5

and A26 motorways. one of the main routes out of Paris the A5

leads east from troyes towards Dijon and nancy. the A26 joins

the A5 just south of troyes and provides a direct link to Reims

in the north. troyes also has good rail connections with regular

services direct to central Paris (Gare de l’est) of 1hr 25 minutes.

Troyes designer ouTleTVoIe DU BoIs10150 Pont De sAInte MARIe+33 (0)3 25 70 47 10WWW.MCARtHURGLen.CoM

Troyes

Paris Nancy

Dijon

Lille

Reims

Strasbourg

Lyon

MarseilleToulouse

Bordeaux

Nantes

Rennes

Excellent transport links - easy to reach by the A26 and A5 motorways.

TrO

yes

Des

Ign

er O

UTL

eT

07

Strategic location in the heart of the scenic Champagne region within easy reach of Paris, Reims and Dijon.

tRoYes DesIGneR oUtLet

tRoYestRoYes

Approximately 3.1 million people live within a 90 minute drive time of the property

rising to 14.9 million within 120 minutes (source: CACI Ltd, 2009). Detailed statistics

indicate a positive and relatively affluent catchment profile for the 90 minute drive time:

Socio-Economic Profile

Purchasing power is ahead of the national average and increases

to 15% per capita above base for the 120 minute catchment.

Retail spend also receives an extra boost by the significant

number of tourists estimated to visit the region each year.

the continued success of troyes Designer outlet is due

to the rare, high quality and attractive retailing offer

provided by the centre. A new phase IV extension to Mall 1

has increased provision in the scheme to 30,000 sq m

generating a dominant and significant critical mass.

there is little question that troyes Designer outlet together

with the wider town itself draws on a considerable catchment

as a result of the strength and depth of its retail offer. A

proposed oxylane Village (Decathlon) on a site just north

of the property will strengthen the location further.

2007 Population by euro ACOrn Profile Troyes France

Highest spenders 19.1% 15.9%

Comfortable Families and Couples 15.5% 12.1%

Families with Children 22.8% 21.2%

Young Low Income with Children 28.4% 29.0%

older Low Income 14.2% 21.8%

Car Ownership Troyes France

number of cars per household 1.24 1.18

Troyes Designer Outlet attracts circa 3 million visitors each year.

source: CACI Ltd, 2009

Chålons-en-Champagne

Vitry-le-François

Chaumont

Saint-Dizier

Pont-a-Mousson

Bar-le-Duc

Nancy

Metz

Bessançon

Reims

Dole

BeauneBeaune

Romilly-sur-Seine

Provins

Montereau-Fault-Yonne

Sens

Auxerre

Cosne-Cours-sur-Loire

Gien

Amilly

Nemours

AvonEtampes

Mennecy

LucéNogent-le-Rotrou

Châteaudun

Vendõme

Blois

Eveux

Louviers

Beauvais

Coulommiers

Meaux

Cháteau-Thierry

Crépy-en-Valois

Tergnier

Laon

Soissons

Epernay

Clergy

Paris

Troyes

Dreux

Amboise

Rouen

Tours

Orléans

Nevers

Bourges

Dijon

A6

A5

A5

A4

A4

A1

A31

A31

A26

A19

A11

A10

A10

A71

A13

N77

A31

Luxembourg

Drive time contours120 minutes 14,944,835

90 minutes 3,090,240

60 minutes 689,378

TrO

yes

Des

Ign

er O

UTL

eT

09

The centre draws on a strong Paris catchment increasing by 5% in 2007 and 9.4% in 2008.

Outlet Centre Retailing

troyes Designer outlet is one of europe’s strongest outlet centres

with limited competition and an excellent line-up of dominant

retailers and brands.

second in europe by overall number of outlets the level of

provision per capita in France is lower than Italy, Austria, spain

and approximately half that of the UK.

the main attraction of designer outlet centres to consumers is summarised as follows:

■■ Value for money relative to traditional retailing

■■ Designer labels and high street brands at discounted prices

■■ Wide product range and brands in a single location

■■ easily accessible with free car parking

the popularity of outlets is created by a mixture of manufacturer

needs and consumer requirements. Manufacturers need reliable

channels of distribution for surplus stock and discounted

prices make the brand available to a wider consumer market.

shoppers may convert to full price customers over time whilst

manufacturers are able to control their own brand identity.

Designer outlets are symbolic of a defensive asset class.

they appeal to price conscious consumers and become of even

greater importance in times of economic difficulty. At troyes

Designer outlet new development means retail provision is at its

highest ever level, footfall numbers over recent months are up,

and spend per visitor is increasing.

the 2009 relaxation of French legislation on dual pricing now also

gives outlet centre retailers the ability to advertise discounted

goods against the original full price. this will help strengthen the

distinction of outlet centres and improve consumer marketing.

troyes Designer outlet has the widest brand offering and largest

floorspace of any outlet in France. Add to this the fact that current

planning legislation in France is very ‘tight’ and we believe troyes

Designer outlet should improve its current dominant status over

the medium term.

Designer labels and high street brands at discounted prices in a single location.

TrO

yes

Des

Ign

er O

UTL

eT

11

France’s largest designer outlet in a market where per capita provision is one of the lowest in Europe and new developments are limited.

Situation

l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l lllll

llll

lll l

l ll l

l ll l

l ll l

l ll l

l ll l

l ll l

l ll l

l ll l

l ll l

l ll l

l ll l

l ll l

l ll l

lll l

l ll l

l lll

lll l

l ll l

l ll l l

l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l ll l

l ll l

l ll l

l ll l

l ll l

l ll l

l ll l

l ll l

l ll l

l ll

l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l

llllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllllll

l llll l l l l l l ll l l l l

l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l ll l

l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l l lll

l ll l l l l l

l ll l

l ll l

l ll l

l ll l

l lll

llll

lll

A26

D610

D677

D960

D610

D610

D141

D619

D619

A26

A5

N77

N77

A5

Pont-Sainte-MarieLa Chapelle-Saint-Luc

LKes Noës-prés-Troyes

Sainte-Savine

Saint-Julien-les-Vilas

La Moline

Saint-Parres-aux-Tertres

Saint-André-les-Vergers

La Riviére-de-Corps

Creney-prés-Troyes

Villechétif

Troyes

Troyes Designer Outlet

Pont-Sainte-MarieLa Chapelle-Saint-Luc

LKes Noës-prés-Troyes

Sainte-Savine

Saint-Julien-les-Vilas

La Moline

Saint-Parres-aux-Tertres

Saint-André-les-Vergers

La Riviére-de-Corps

Creney-prés-Troyes

Villechétif

Troyes

Troyes Designer Outlet

the property is situated in the Pont-sainte Marie area, 10 minutes

north of the town centre, in a mixed retail and commercial area.

the scheme is just south of the D610 Rocade which has recently

been upgraded to dual carriageway status and now provides a

direct link between the A5 and A26 motorways creating a fully

orbital ring road for the town.

the property can be accessed from two roads: the Route national

77 (D677) connecting troyes with Châlons-en-Champagne to

the north and Auxerre to the south; and the D960 Route de

Brienne leading east towards Piney and the natural Regional

Parc de la Forêt d’orient. Both roads provide a direct link

between the Rocade and A26 motorway just 4 km to the east.

Decathlon received CDeC retail consent in october 2008 for their

successful ‘oxylane Village’ concept on a site immediately north

of the property. the building permit is currently under review and

includes a first phase 6,000 sq m Decathlon store, 800 parking

spaces and 20 acre “terrain des sports” with football pitches, cycle

tracks, golf driving range etc. Accessed off the same n77/D610

junction with a direct link into the new phase IV entrance, the

development will significantly enhance the offer of the location.

Unquestionably the dominant outlet offer for the catchment in a strengthening location.

TrO

yes

Des

Ign

er O

UTL

eT

13

Excellent location easily accessible from Troye’s recently upgraded ring road.

Merchandising Mix

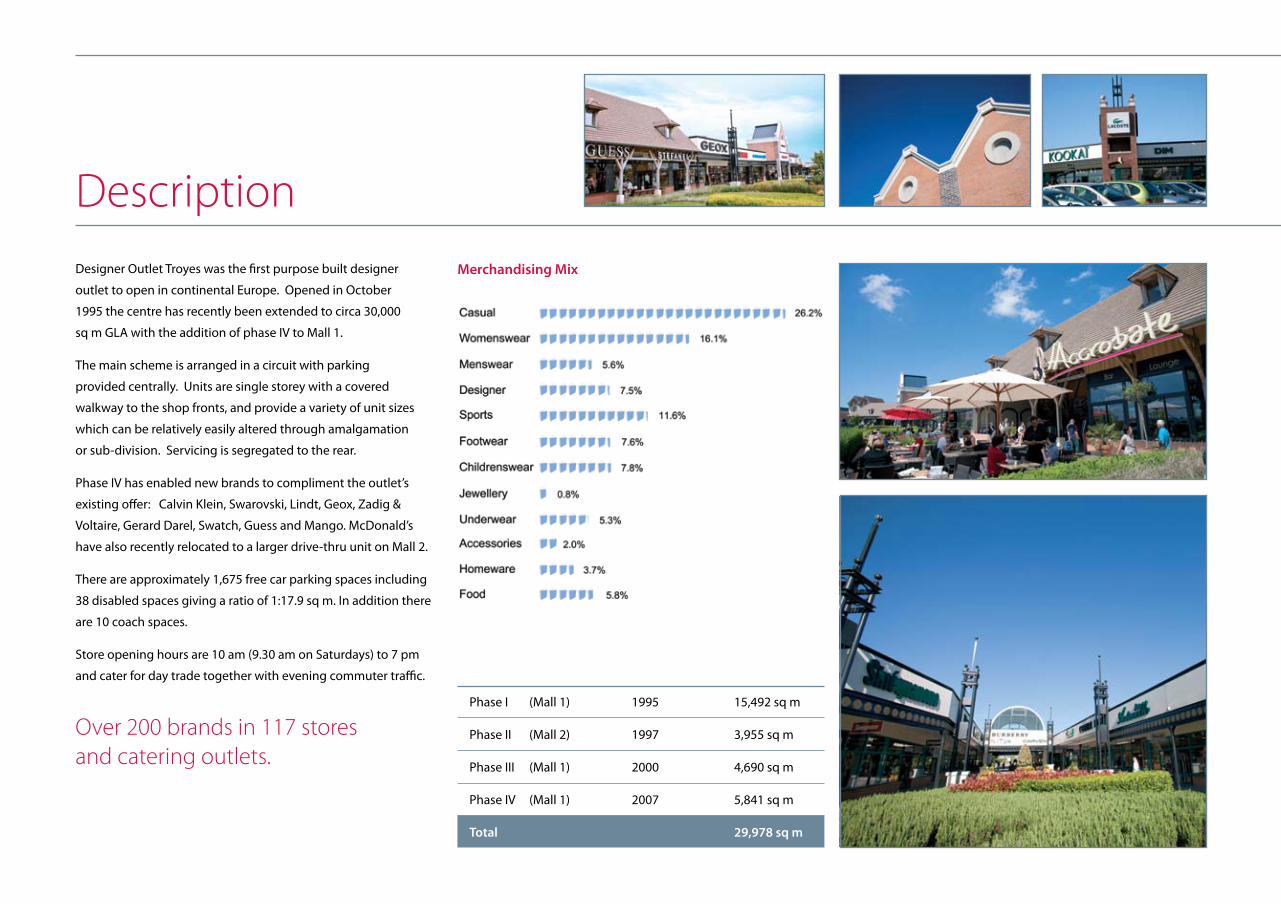

DescriptionDesigner outlet troyes was the first purpose built designer

outlet to open in continental europe. opened in october

1995 the centre has recently been extended to circa 30,000

sq m GLA with the addition of phase IV to Mall 1.

the main scheme is arranged in a circuit with parking

provided centrally. Units are single storey with a covered

walkway to the shop fronts, and provide a variety of unit sizes

which can be relatively easily altered through amalgamation

or sub-division. servicing is segregated to the rear.

Phase IV has enabled new brands to compliment the outlet’s

existing offer: Calvin Klein, swarovski, Lindt, Geox, Zadig &

Voltaire, Gerard Darel, swatch, Guess and Mango. McDonald’s

have also recently relocated to a larger drive-thru unit on Mall 2.

there are approximately 1,675 free car parking spaces including

38 disabled spaces giving a ratio of 1:17.9 sq m. In addition there

are 10 coach spaces.

store opening hours are 10 am (9.30 am on saturdays) to 7 pm

and cater for day trade together with evening commuter traffic.

Phase I (Mall 1) 1995 15,492 sq m

Phase II (Mall 2) 1997 3,955 sq m

Phase III (Mall 1) 2000 4,690 sq m

Phase IV (Mall 1) 2007 5,841 sq m

Total 29,978 sq m

Over 200 brands in 117 stores and catering outlets.

Mall 1

Mall 2

N

this

pla

n is

pub

lishe

d fo

r the

con

veni

ence

of i

dent

ifica

tion

only

. Any

site

bou

ndar

ies

are

indi

cativ

e on

ly a

nd s

houl

d be

che

cked

aga

inst

titl

e D

eeds

.

TrO

yes

Des

Ign

er O

UTL

eT

17

The scheme offers flexible accommodation, free car parking and a modern safe environment. First class design, layout and retail offer including Nike, Burberry, Kenzo, Polo Ralph Lauren and Lacoste.

Planningthe centre has undergone significant change and development

since the original phase I authorisation to open to the public was

granted on 9 october 1995.

subsequent phases and extensions have received the necessary

authorisation by the relevant public authority to be used as an

outlet centre.

Further information is

available on request.

Tenure

TrO

yes

Des

Ign

er O

UTL

eT

19

the property is held Freehold

comprising three main sites.

Additional land surrounding the scheme

has been bought-in to enable possible

future extension / advertising space, or give

control over adjoining site development.

Tenanciestroyes Designer outlet is currently let to 111 occupiers with a further

three units under offer. new in 2007/08 phase IV comprising 26 units

is fully let and brings global occupancy to 97% plus.

All tenants pay turnover rent calculated as a percentage of trading

performance, subject to a Minimum Base Rent (MBR) reviewed on the

1 January each year upward only to:

■■ the previous year’s base rent plus indexation; or

■■ a percentage (typically 80%) of the previous year’s turnover rent.

the budget estimate for 2009/10, including units under offer, shows a

full year gross income of €8,673,260. the average total rent (turnover

plus base) of €291.33 per sq m is up 5.98% on last year reflecting a

mixture of: indexation; improved leasing terms; letting of vacant

units; and the annualisation of new tenants in 2008/09.

some 15 tenancies include steps on base rent and/or turnover

percentages. the budgeted gross income figure includes a

vendor top-up for contractual steps occurring up to 31 March

2010 totalling €44,962. Additional steps worth in excess of €60,000

per annum will improve the income profile further over the next

two to three years.

existing tenancies have a low turnover rent percentage relative

to new agreements in phase IV (7.80% compared to 9.06%) and

therefore we believe offers excellent opportunity for improved

lease terms on renewal or expiry.

500,000

2009

2013

2017

2011

2015

2019

2010

2014

2018

2012

2016

2020

1,000,000

1,500,000

2,000,000

2,500,000

Inco

me

(€ E

uros

)

Lease Expiry (year ended 31 March)

the property has excellent security of income spread across a high

number of tenants, dominated by well known national multiple

retailers and high-end brands. the average unexpired term is 6.00

years (or 6.35 years weighted by income).

40 out of 46 tenants (87%) that were invited to renew since

2005/06 have done so, either within the original unit or in one of a

different size.

sour

ce: M

cArt

hurG

len,

200

9

Tenant Trading and sales Density

In 2009 the centre has performed well with total sales for the first

five months of the year up 9.60% whilst like for like sales are up

4.24% against last year.

the average 2008/09 sales density for full year tenants in Mall 1 was

€3,287 per sq m rising to €7,000–€9,000 per sq m for the best performing

retailers. Phase IV is beginning to increase the scheme average showing

a 39.7% increase on last year and 13.6% like for like.

the top ten tenants have reported sales up 8.9% on last year

including: Burberry, Lancel, Black & Decker, Lacoste, eden Park,

Polo Ralph Lauren, Guess, La City, Geox and salomon.

High occupancy and strong income growth – rents linked to turnover with a minimum base subject to annual indexation.

TrO

yes

Des

Ign

er O

UTL

eT

21

2009/10 turnover is expected to increase as a consequence of:

■■ full trading year of new tenants (4.40%);

■■ leasing up units (3.69%); and

■■ 3% like for like increase on phases I–III and

6% on phase IV (3.80%).

service Charge and Marketing

Both service charge and marketing budgets are fully

recoverable from tenants, with the exception of:

■■ tenant caps (current total €115,270); and

■■ landlord contribution on vacant space (which at 3%

totals €102,525).

the current tenant re-charge rates for 2009/10 are €59.50 per sq m

for service charge and €54.50 per sq m for marketing.

Total sales for the first 5 months of 2009 up 9.6% with like for like sales up 4.2%.

2005/6 2006/7 2007/8 2008/91 2009/10 Budget2

total GLA (sq m) 23,453 23,453 29,593 29,593 29,978

Average occupancy 97.9% 97.2% 86.3% 91.1% 97.1%

turnover (€) 72,256,000 71,654,000 83,008,000 83,648,000 93,601,000

Density (€ per sq m) 3,147 3,143 3,250 3,103 3,216

Gross Income (€) 5,647,000 5,707,800 6,935,000 7,575,300 8,673,2603

Rent(€ per sq m) 236.56 242.71 266.54 274.89 291.33

1. Due to calendar variations 2008/09 was a 52 rather than 53 week sales year and also excluded easter. 2. Includes full year effect of 2009/10 asset management moves, and vendor top-up for contractural steps occurring up to 31/03/10 (totalling €44,962). 3. We estimate the current gross income as at June 2009 (ignoring steps and units under offer) is €8,260,760. 84% of the rent from retail units comprises the minimum base rent. MBR on units under offer and the vendor top-up for contractual steps amounts to an additional €267,533.

troyes Designer outlet has real and significant scope for further

value growth driven forward by a number of opportunities across

the scheme:

Tenant mix and asset management of under-performing tenants

the tenant mix is constantly under review and a number

of tenants have been identified as suitable for downsizing

to maximise sales per sq m. there is also strong demand

from tenants for representation on the scheme.

renewal of leases on improved terms

together with improvements in tenant mix we firmly believe

there is upwards pressure on rents that can be exploited in

the short to medium term. Phase IV is fully let with 26 new

agreements creating further evidence for improved lease terms:

■■ average minimum base rents of €269 per sq m against

€232 per sq m on existing.

■■ average turnover rent percentage of 9.06% against 7.80% on the

remaining 91 units.

removal of tenant caps

there are 20 lease agreements with tenant caps on either

service charge and/or marketing. A number of these are

now historic offering good potential to renegotiate on

renewal or be bought out. the total potential saving

based on the 2009/10 budget is €115,270 per annum.

Dual Pricing

the 2009 relaxation of French legislation on dual pricing enables

consumers to understand the outlet centre concept more clearly.

Retailers now have greater freedom on advertising whilst centre

marketing can now directly promote the offer of designer and high street

brands at discounts of up to 70%.

some retailers have already started to take advantage of the

new legislation but there is now also potential to market this

consistently across the centre. Initial feedback from consumers

has been positive which we believe will feed through to higher

future visitor numbers and turnover densities for the scheme.

Link to Decathlon ‘Oxylane Village’ scheme

Potential to improve retailing synergy with surrounding

development and create new access direct from phase IV into

the proposed ‘oxylane Village’ scheme.

Major Asset Management Initiatives

Commercialisation

We believe there is excellent opportunity to increase the

amount of additional ‘mall income’ which is currently behind

levels achieved on other comparable schemes. Possible

initiatives include new kiosks, advertising boards, vending

machines, car stands, promotions and temporary stalls. TrO

yes

Des

Ign

er O

UTL

eT

23

Real and significant scope for future value growth.

N

Mall 2

Mall1

Phase V

Addional Phase Vextension land/car parking

FIDIA factory site and potential for phase V

Discussions are currently ongoing to buy-in the FIDIA factory site

– a parcel of land around 10,000 sq m connecting Mall 1 and 2.

A new 15 unit (2,500 sq m) phase V extension with 550 sq m

anchor could be added. this will provide a greater link and

significantly boost value for Mall 2 which is currently split from the

principal retail offer.

the extension of troyes Designer outlet and proposed new

phase is backed by the local authority who we understand are

willing to use statutory powers available to ensure its success.

Further information is available on request.

Major Asset Management Initiatives

McArthurGlen is the leading developer, owner and manager

of designer outlet villages in europe.

the group has a portfolio of 18 designer outlets totalling

400,000 sq m and is opening a further five centres totalling

170,000 sq m in Berlin, naples, salzburg and Athens by the

end of 2010.

Partnering with more than 750 top brands McArthurGlen

currently manage outlets near London, Rome, Venice, Milan,

Dusseldorf, Florence, edinburgh, York and Vienna amongst

others.

McArthurGlen developed and has actively managed troyes

Designer outlet for over 14 years. Consequently the centre

is maintained to an excellent standard, whilst turnover

performance is constantly monitored to ensure all retailers

are trading to their optimum.

the current management agreement is for a term of 12

years from 31 January 2004 subject to earlier termination.

McArthurGlen would be delighted to continue to manage

troyes Designer outlet.

McArthurGlen Designer Outlets

TrO

yes

Des

Ign

er O

UTL

eT

25

offers are invited for the freehold interest in the property.

troyes Designer outlet is currently held by a French sARL

with a Luxembourg company parent offering flexibility of

ownership and potential transfer of existing debt and tax

saving on acquisition.

Proposal

TrO

yes

Des

Ign

er O

UTL

eT

27

Graham Collisont: +44 (0) 20 7152 5140F: +44 (0) 20 7152 5381e: [email protected]

Patrick Knapmant: +44 (0) 20 7152 5019F: +44 (0) 20 7152 5381e: [email protected]

Antoine Grignont: +33 (0) 153 769 298F: +33 (0) 153 760 525e: [email protected]

Olivier Gerardt: +33 (0) 153 769 574F: +33 (0) 153 760 525e: [email protected]

ContactsFor further information please contact:

Misrepresentation Act 1967 and Property Misdescriptions Act

Cushman & Wakefield LLP for themselves and for vendors or lessors of this property whose agents they are, give notice that :

1 the particulars are produced in good faith, are set out as a general guide only and do not constitute any part of a contract.

2 no person in the employment of the agent(s) has any authority to make or give any representation or warranty whatever in relation to this property.

3 this property is offered subject to contract and, Floor areas, measurements or distances given are approximate and unless otherwise stated, all rents are quoted exclusive of VAt.

4 nothing in these particulars should be deemed to be a statement that the property is in good condition or that any services or facilities are in working order.

5 Unless otherwise stated, no investigations have been made regarding pollution or potential land, air or water contamination. Interested parties are advised to carry out their own investigations if required.

6. Plans are published for convenience of identification. Any site boundaries shown are indicative only and should be checked against title Deeds.

www.cushmanwakefield.com

Troyes, France | MacArthur Glen Troyes Outlet | June 09 | Ref: 105766