2019 - 2028 TEN-YEAR NETWORK DEVELOPMENT PLAN OF ... 19/TYNDP_en.pdf · -IGI Poseidon () ... –...

85

1 2019 - 2028 TEN-YEAR NETWORK DEVELOPMENT PLAN OF BULGARTRANSGAZ EAD 22 March 2019 Approved with Decision under Protocol No334/18 March 2019 of Bulgartransgaz EAD Management Board meeting

Transcript of 2019 - 2028 TEN-YEAR NETWORK DEVELOPMENT PLAN OF ... 19/TYNDP_en.pdf · -IGI Poseidon () ... –...

1

2019 - 2028 TEN-YEAR

NETWORK DEVELOPMENT PLAN

OF BULGARTRANSGAZ EAD

22 March 2019

Approved with Decision under Protocol No334/18 March 2019 of Bulgartransgaz EAD Management Board meeting

2

T A B L E O F C O N T E N T : D E F I N I T I O N S A N D A B B R E V I A T I O N S . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4

1 T W H = 1 0 0 0 G W H = 1 0 0 0 0 0 0 M W H = 1 0 0 0 0 0 0 0 0 0 K W H . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

S O U R C E S U S E D . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

I N T R O D U C T I O N . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8

B U L G A R T R A N S G A Z E A D P R O F I L E . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

D E S C R I P T I O N O F N A T U R A L G A S T R A N S M I S S I O N A N D . . 1 1

S T O R A G E I N F R A S T R U C T U R E . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1 1

N A T U R A L G A S M A R K E T I N T H E C O U N T R Y A N D T H E R E G I O N . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1 4

1. NATURAL GAS MARKET IN BULGARIA ................................................................... 14

2. NATURAL GAS MARKET IN THE REGION ............................................................... 19

N A T U R A L G A S T R A N S M I S S I O N A N D S T O R A G E . . . . . . . . . . . . . 4 1

1. NATURAL GAS TRANSMISSION COVERING CONSUMPTION IN BULGARIA ................ 41

2. NATURAL GAS TRANSIT TRANSMISSION .............................................................. 42

3. NATURAL GAS STORAGE ..................................................................................... 44

C A P A C I T I E S D E M A N D S C E N A R I O S A N D S O U R C E S T O C O V E R D E M A N D I N T H E C O U N T R Y . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4 6

4. NATURAL GAS DEMAND ...................................................................................... 46

5. SUPPLY SOURCES COVERING DEMAND IN THE COUNTRY ...................................... 47

6. FORECAST ON THE DEMAND OF CAPACITY FOR CROSS-BORDER TRANSMISSION THROUGH BULGARTRANSGAZ EAD EXISTING INFRASTRUCTURE .............................................................................................. 48

S E C U R I T Y O F S U P P L Y . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5 0

2 0 1 9 - 2 0 2 8 G A S I N F R A S T R U C T U R E D E V E L O P M E N T P R O J E C T S . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5 2

1. NATURAL GAS TRANSMISSION AND STORAGE INFRASTRUCTURE DEVELOPMENT PROJECTS IN THE PERIOD 2019-2021 ON WHICH INVESTMENT DECISION HAS BEEN MADE ........................................................................................................ 54

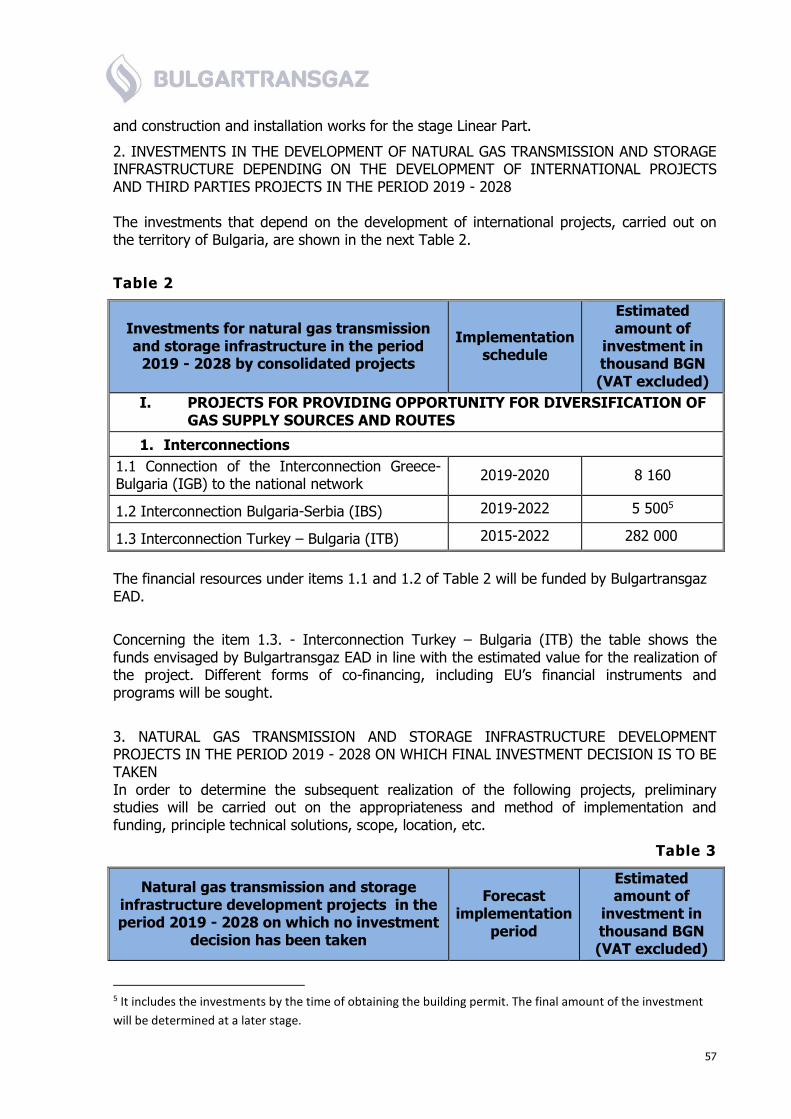

2. INVESTMENTS IN THE DEVELOPMENT OF NATURAL GAS TRANSMISSION AND STORAGE INFRASTRUCTURE DEPENDING ON THE DEVELOPMENT OF INTERNATIONAL PROJECTS AND THIRD PARTIES PROJECTS IN THE PERIOD 2019 - 2028 ........................................................................................................ 57

3. NATURAL GAS TRANSMISSION AND STORAGE INFRASTRUCTURE DEVELOPMENT PROJECTS IN THE PERIOD 2019 - 2028 ON WHICH FINAL INVESTMENT DECISION IS TO BE TAKEN ................................................................................. 57

4. 2019 – 2028 INVESTMENT PROGRAM .................................................................... 58

5. DESCRIPTION OF KEY PROJECTS .......................................................................... 62

3

D E V E L O P M E N T O F T H E C A P A C I T Y O F B U L G A R T R A N S G A Z E A D G A S I N F R A S T R U C T U R E I N T H E P E R I O D 2 0 1 9 - 2 0 2 3 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8 1

C O N C L U S I O N . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8 3

E N C L O S U R E S :

1. DESCRIPTION OF KEY PROJECTS

2. MAP

4

D E F I N I T I O N S A N D A B B R E V I A T I O N S

The following definitions and abbreviations are used for the purposes of this document:

AGRS – Automatic Gas Regulation Station

LNG – Liquefied Natural Gas

GMS – Gas Metering Station

GPB – Gas Pipeline Branch

GRS – Gas Regulation Station

the Company – Bulgartransgaz EAD is an independent combined gas operator in the Republic of Bulgaria

ЕU – European Union

EC– European Commission

EBRD – European Bank for Reconstruction and Development

EIB – European Investment Bank

CEF – Connecting Europe Facility

PCI – Projects of Common Interest

GDC – Gas Distribution Company

ME - Ministry of Energy

MRDPW – Ministry of Regional Development and Public Works

EWRC – Energy and Water Regulatory Commission (formerly SEWRC)

BEH – Bulgarian Energy Holding EAD

VS – Valve Station

EEC – End Energy Consumption

CS – Compressor Station

PF – Pigging Facility

MGP – Main Gas Pipeline

TGP – Transit Gas Pipeline

MPa – Megapascal (unit of pressure)

m³ or cubic meter – unit of volume which in this document for the purposes of determining a natural gas quantity, represents the natural gas quantity in a volume of one cubic meter at 293.15 K (200C) and absolute pressure of 0.101325 MPa.

MW – Megawatt (unit of power)

EIA – Environmental Impact Assessment

Natural Gas Transmission – transport of natural gas through the gas transmission networks owned by Bulgartransgaz EAD

PEC– Primary Energy Consumption

BP – Building Permit

5

CIW – Construction and Installation Works

SMEs – Small and medium-sized enterprises

UGS – Underground Gas Storage

National Gas Transmission Network (NGTN) – gas transmission network the main purpose of which is natural gas transmission to customers in Bulgaria connected thereto and also to interconnection points. The NGTP is owned by Bulgartransgaz EAD and used for performing transmission services;

Gas Transmission Network for Transit Transmission (GTNTT) – gas transmission network with main purpose natural gas transit transmission from the Bulgarian-Romanian border to the borders with Turkey, Greece and Macedonia, used also for natural gas transmission to customers in Bulgaria connected to the network or to interconnection points on the territory of Bulgaria. The GTNTT is owned by Bulgartransgaz EAD and used for performing transmission services;

Bulgartransgaz EAD gas infrastructure – includes the NGTN, the GTNTT and UGS Chiren

ENTSOG – European Network of Transmission System Operators for Gas

CESEC - Central and South Eastern Europe Energy Connectivity - initiative for energy connectivity in Central, Eastern and Southeast Europe;

EASTRING – a project for the construction of a gas transmission infrastructure from Bulgaria through Romania and Hungary to Slovakia;

BRUA – Gas transmission corridor Bulgaria-Romania-Hungary-Austria

IAP – Ionian Adriatic gas pipeline

ТАP – Trans-Adriatic Pipeline

TANAP – Trans-Anatolian Natural Gas Pipeline

The upper calorific value at reference conditions (20/;25) used herein with a view of converting from volumetric units in energy is as follows:

NGTN GTNTT

GCV, kWh/m³ (25⁰C/20⁰C) GCV, kWh/m³ (25⁰C/20⁰C)

2008-2010 10,40 10,40

2011 10,41 10,41

2012 10,45 10,45

2013 10,48 10,48

2014 10,54 10,54

2015 10,64 10,63

2016 10,66 10,66

2017 10,58 10,58

2018 10,56 10,56

For the purposes of forecasting the capacity and volumes, the used calorific value is 1 cu m

=10,57 kWh (25⁰C/20⁰C) 1 TWh=1 000 GWh=1 000 000 MWh = 1 000 000 000 kWh

6

S O U R C E S U S E D

o 2020 Energy Strategy of Bulgaria amended by Council of Ministers Decision № 847 of 22.11.2018 and Decision of the National Assembly of 30.11.2018, promulgated in State Gazette No 101 of 07.12.2018

o Ministry of Energy of the Republic of Bulgaria (www.me.government.bg)

o Energy and Water Regulatory Commission (www.dker.bg)

o National Statistical Institute - GDP, PEC, EEC and other data, (www.nsi.bg)

o Data on natural gas consumption, Eurostat, (www.epp.eurostat.ec.europa.eu)

o National energy balance of the Republic of Bulgaria (www.nsi.bg)

o A list of Projects of Common Interest, webpage of the European Commission,

Directorate-General Energy, (www.ec.europa.eu)

o Reports on the State of the Energy Union (https://ec.europa.eu)

o A Report of the World Bank, Economic Consulting Associates Ltd (ECA) and Infraproject Consult Ltd Bulgaria: Options to Improve Security of Gas Supply

o Public information related to the development of the gas market in the region, published on the following web pages:

– Gazprom (www.gazprom.com)

– Rosneft (www.rosneft.com)

– White Stream (www.white-stream.com)

- IGI Poseidon (www.igi-poseidon.com)

– DESFA S.A. (www.desfa.gr)

– DEPA, S.A. (www.depa.gr)

– Gastrade (www.gastrade.gr)

– Prometheus Gas (www.prometheusgas.gr)

– HRADF (www.hradf.com)

– JP Srbijagas (www.srbijagas.com)

– GAMA AD (www.gama.com.mk)

– LNG Hrvatska (www.lng.hr)

– ICGB AD (www.icgb.еu)

– ITGI (www.edison.it)

– TAP (www.trans-adriatic-pipeline.com)

– Shah Deniz (www.bp.com)

– ANRE - National Energy Regulatory Authority (www.anre.ro)

– Transgaz S.A. (www.transgaz.ro)

– Romgaz (www.romgaz.ro)

– CEPA - Romania’s Energy Crossroads – March 2016 – (www.cepa.org)

– SOCAR – (www.socar.az)

– BOTAS (www.botas.gov.tr)

7

- EMRA – Turkish Natural Gas Market – Report 2017

– Ministry of Foreign Affairs - Turkey's Energy Profile and Strategy (www.mfa.gov.tr)

– World Bank (www.worldbank.org)

– ENTSOG (www.entsog.eu)

– Delek Drilling (www.delekdrilling.co.il)

o Information related to natural gas production in Bulgaria, webpage Petroceltic International Plc (the former Melrose Resources), (www.petroceltic.com)

o Bulgartransgaz EAD 2019-2023 Business Program, approved by decision under Minutes of a meeting No 313/21.12.2018 of Bulgartransgaz EAD Management Board and decision under Minutes No 46/31.12.2018 of Bulgartransgaz EAD Supervisory Board and updated Business Program No 1, approved by decision under Minutes of a meeting No 324/12.02.2019 of Bulgartransgaz EAD Management Board and decision under Minutes No 5/25.02.2019 of Bulgartransgaz EAD Supervisory Board

o Regional Investment Plan 2017-2026 Central and Eastern Europe, (www.entsog.eu)

o Regional Investment Plan 2017-2026 South Corridor (www.entsog.eu)

o Ten-Year Network Development Plan ENTSOG

o GIE – Gas Infrastructure Europe

o IEA - International Energy Agency

o IGU – International Gas Union, Working Committee 2 – UGS (www.igu.org)

o EIA – U.S Energy Information Administration

o IENE – Institute of Energy for South – East Europe

o BP Statistical Review of World Energy 2018

o Turkish Policy Quarterly – 2015 (http://turkishpolicy.com)

o Ministry of Energy and Natural Resources – Republic of Turkey (www.enerji.gov.tr)

o MER JSC Skopje - Macedonian Energy Resources Skopje (www.mer.com.mk)

o Consilium Europa – (www.consilium.europa.eu)

o Platts (www.platts.com)

o Gas in Focus 2017/2018 (www.gasinfocus.com)

o Eustream – Presentation – 21st Annual BBSPA Conference – April, 2015 Wien

o DEPA – Presentation – CEER Workshop – 12 September 2016 – Athens

o DESFA – Presentation – Opening New Routes for Natural Gas in Europe – 2018

o European Commission - Balkan Gas Hub Concept and its Role in the EU's Internal Energy Market – 5 September 2016 – Varna

o Feasibility Study for the Balkan Gas Hub – Interim Results Presentation – 12 June 2018, Brussels

o CESEC Plenary and Working Group, 7 February 2019

o Information from other corporate documents and correspondence with stakeholders

8

I N T R O D U C T I O N

Bulgartransgaz EAD Ten-year plan for development of the natural gas transmission and storage infrastructure has been developed for the period 2019-2028 and sets out the vision for development of the company as an independent transmission operator and storage facility operator. It is consistent with the major European, regional and national priorities, namely increasing the security of natural gas supply, ensuring diversification of natural gas supply sources and routes and creation of sustainable, liberalized and interconnected gas market, and with the „Winter package of measures to safeguard the energy security in the EU”, submitted in February 2016 by the EC.

The priority activities for development of Bulgartransgaz EAD infrastructure in the period 2019 – 2028 are aimed at expansion of the gas transmission infrastructure, improvement and enhancement of the existing main and auxiliary gas transmission infrastructure and the associated equipment, its modernization, rehabilitation and expansion, development of interconnectivity and increase of storage capacity. Their realization will provide Bulgaria with the potential to become an important regional gas distribution centre (gas hub).

The major objective of the TYNDP is to ensure maximum transparency for the future prospects for development of the gas transmission networks and the natural gas storage facility of the Company. It identifies and analyses the trends and factors determining the necessity of the planned investments, as well as their allocation over time. All market participants will thus be informed and this will enable making long-term investment decisions.

The implementation of the investment strategy presented in this TYNDP will provide the opportunity to increase the use of natural gas in the country with the respective economic, social and environmental benefits, and diversify the sources and gas supply routes. It will also promote the establishment of a competitive natural gas market and respectively, lead to a wider choice for its participants. This, in turn, would provide price incentives, being the basis of a liquid natural gas market. Having regard to achieving full transparency and balance between the interests of the TSO and the market participants, the TYNDP is subject to public consultation initiated by Bulgartransgaz EAD based on which the interrelations between the Company's projects and the development plans of the stakeholders can be considered and synchronized in the TYNDP. All motivated proposals will be examined and taken into account.

According to the European legislation, TYNDPs are prepared by the gas transmission operators on the territory of the European Union in line with Art. 22 of Directive (EC) 2009/73. Pursuant to the national legislation, the Bulgarian gas transmission operator Bulgartransgaz EAD develops its TYNDP in line with Art. 81d, para 1 of the Energy Act (EA) published in SG 54 dated 17.07.2012, valid as of 17.07.2012.

The national TYNDPs serve as a basis for development of the Gas Regional Investment Plans (GRIPs), as well as the Community-wide Network Development Plan, developed by the European Network of Transmission System Operators for Gas (ENTSOG).

9

BULGARTRANSGAZ EAD PROFILE

Bulgartransgaz EAD is a sole owner joint stock company, registered on 15.01.2007 at Sofia with a Decision of Sofia City Court. The owner of 100 % of its shares is Bulgarian Energy Holding EAD with principal the Ministry of Energy (ME).

By virtue of Decision of the Energy and Water Regulatory Commission, Bulgartransgaz EAD is certified independent transmission operator in Bulgaria in line with the requirements of Directive 2009/73/ЕC concerning the common rules for the internal market in natural gas, Regulation (ЕC) No 715/2009 on the conditions for access to the natural gas transmission networks and Chapter Eight, (а) of the Energy Act. The Decision was adopted in line with the opinion of the European Commission of 22.04.2015.

The Decision approved by EWRC proves that Bulgartransgaz EAD meets the criteria for certification and the requirements for independence, namely:

- the Management Board of the independent transmission operator is the competent authority responsible for decisions, related to TSO current activity, the management of the network and the activities, required for preparing TYNDP;

- the Independent Transmission Operator has the right to make independent decisions regarding the assets, required for the operation, maintenance and development of the transmission network and the gas regimes control;

- the requirements for professional independence of the members of the Management Board and the members of the Supervisory Board of Bulgartransgaz EAD have been met;

- Bulgartransgaz EAD has at its disposal the necessary resources including human, technical, financial and physical, required to meet its obligations when carrying out the natural gas transport activity;

- the company has its own identity, independent IT systems and equipment, independent premises and security access systems thereto, as well as its own external contractors or external consultants for the access to these systems;

- when carrying out its activity, the Independent Transmission Operator provides services that are non-discriminatory for the different network users and does not restrict, distort or prevent competition in production or gas supply.

In compliance with the provisions of the Energy Act and Directive 2009/73 (EC) of March, 2013 Bulgartransgaz EAD is governed by a two-tier organizational management structure: Supervisory Board and Management Board.

Bulgartransgaz EAD is a combined gas operator carrying out natural gas transmission and storage activities. The company is an owner and operator of the national gas transmission network (NGTN), the gas transmission network for transit transmission (NGTNTT) and the underground gas storage Chiren (UGS Chiren).

The Company is the holder of the following licenses, issued by the State Energy and Water Regulatory Commission (SEWRC):

for natural gas transmission: Licenses No L-214-06 and No L-214-09 of 29.11.2006

for natural gas storage: License No L-214-10 of 29.11.2006

The basic requirements for these activities are regulated by the Energy Act and the by-laws, harmonized with the European legislation in that field.

Bulgartransgaz EAD plays a key role and is responsible for the uniform management, reliable

10

operation and efficient use of the natural gas transmission system, including the gas pipelines, compressor stations and Chiren UGS. The activities include natural gas transmission in compliance with the requirements for gas quality and metering, development of the networks in accordance with the long-term gas sector forecasts and development plans for gas supply and the gas sector in general and, last but not least, maintenance, operation, management and development of the underground gas storage Chiren. All these services are provided to customers on a level playing field. Apart from that, engineering, investment and service activities are carried out in the Company.

The organisational structure of the Company includes a Head office and four operational regions - Northwest operational region Botevgrad, Northeast operational region Valchi dol, Southeast operational region Stara Zagora, Southwest operational region Ihtiman, responsible for the operational management and maintenance of the network on the respective territory, as well as Chiren UGS.

Since its establishment, Bulgartransgaz EAD constantly strives to improve the quality of the offered services and promote the development of the gas market in Bulgaria, an integral part of the corporate policy. As a result of the sustainable business model, the Company shows very good financial results, which reflect the trend of financial stability, with a realistic forecast for its sustainability in the future. All these enable investments in increasing the reliability and development of the natural gas transmission and storage infrastructure. Last but not least, as part of the common European gas network, Bulgartransgaz EAD pursues a policy of transparency, non-discrimination and operates in full compliance with the requirements of the Third Energy Liberalization Package, the European and Bulgarian legislation.

Head office

Chiren UGS

Northwest operational

region Botevgrad Northeast operational

region Valchi dol

Southwest operational region

Ihtiman

Southeast operational region Stara Zagora

11

DESCRIPTION OF NATURAL GAS TRANSMISSION AND

STORAGE INFRASTRUCTURE

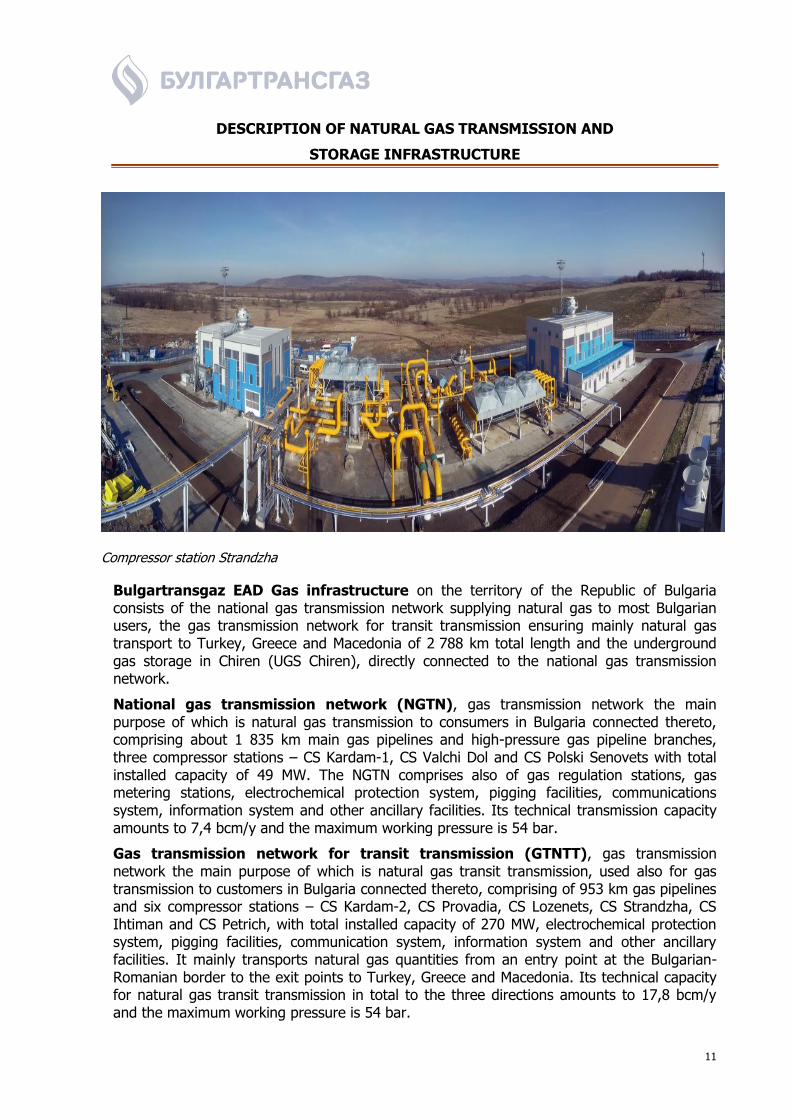

Compressor station Strandzha

Bulgartransgaz EAD Gas infrastructure on the territory of the Republic of Bulgaria consists of the national gas transmission network supplying natural gas to most Bulgarian users, the gas transmission network for transit transmission ensuring mainly natural gas transport to Turkey, Greece and Macedonia of 2 788 km total length and the underground gas storage in Chiren (UGS Chiren), directly connected to the national gas transmission network.

National gas transmission network (NGTN), gas transmission network the main purpose of which is natural gas transmission to consumers in Bulgaria connected thereto, comprising about 1 835 km main gas pipelines and high-pressure gas pipeline branches, three compressor stations – CS Kardam-1, CS Valchi Dol and CS Polski Senovets with total installed capacity of 49 MW. The NGTN comprises also of gas regulation stations, gas metering stations, electrochemical protection system, pigging facilities, communications system, information system and other ancillary facilities. Its technical transmission capacity amounts to 7,4 bcm/y and the maximum working pressure is 54 bar.

Gas transmission network for transit transmission (GTNTT), gas transmission network the main purpose of which is natural gas transit transmission, used also for gas transmission to customers in Bulgaria connected thereto, comprising of 953 km gas pipelines and six compressor stations – CS Kardam-2, CS Provadia, CS Lozenets, CS Strandzha, CS Ihtiman and CS Petrich, with total installed capacity of 270 МW, electrochemical protection system, pigging facilities, communication system, information system and other ancillary facilities. It mainly transports natural gas quantities from an entry point at the Bulgarian-Romanian border to the exit points to Turkey, Greece and Macedonia. Its technical capacity for natural gas transit transmission in total to the three directions amounts to 17,8 bcm/y and the maximum working pressure is 54 bar.

12

Bulgartransgaz EAD had constructed and run in commercial operation two reverse flow stations, metering natural gas quantities between the transit and the national gas transmission networks, GMS Ihtiman and GMS Lozenets and by using them the Operator can transport natural gas quantities to network users of both networks.

The Underground Gas Storage Chiren was built on the lands of Chiren village based on the already depleted gas condensate field. It is equipped with specialized underground and above-ground facilities, required to ensure natural gas storage. Chiren UGS has 24 exploitation wells and a compressor station of approximately 9 МW total installed capacity. The present storage capacity can provide storage of up to 5 813 500 MWh/d natural gas. The withdrawal and injection capacity, according to the formation pressures and other factors, is between 5 500 MWh/d mcm/day (minimum) up to 40 377 MWh/d (maximum) for withdrawal. In an emergency situation, the maximum withdrawal capacity is up to 49 679 MWh/d in case of full gas storage facility and for a short time period (maximum 30 days), and for injection - 5 5 500 MWh/d (minimum) up to 38 253 MWh/d (maximum).

The main entry and exit points of the Company gas transmission network are the following:

Entry/exit interconnection point (IP) Negru Voda 1/Kardam – connection between Bulgartransgaz EAD national gas transmission system and the gas transmission system operated by Transgaz S.A. (Romania) on the Bulgarian-Romanian border in the area of Negru Voda/Kardam;

Entry/exit interconnection point (IP) Negru Voda 2, 3/Kardam – connection between Bulgartransgaz EAD gas transmission system for transit transmission and the gas transmission system operated by Transgaz S.A. (Romania) on the Bulgarian-Romanian border in the area of Negru Voda/Kardam;

Entry-exit interconnection point (IP) Кulata/Sidirocastro – connection between Bulgartransgaz EAD gas transmission network for transit transmission and the gas transmission system operated by DESFA S.A. (Greece), located on the Bulgarian-Greek border in the area of Kulata/Promachonas;

Interconnection point (IP) Strandzha/Malkoclar – an exit point, connection between Bulgartransgaz EAD national gas transmission system for transit transmission and the gas transmission system operated by Botas (Turkey), located on the Bulgarian-Turkish border in the area of the village of Strandzha, Bolyarovo municipality.

Interconnection point (IP) Gueshevo/Jidilovo – an exit point, connection between Bulgartransgaz EAD national gas transmission system for transit transmission and the gas transmission system operated by GA-MA (Macedonia), located on the Bulgarian-Macedonian border in the area of the village of Guyeshevo, Kuystendil municipality.

Entry/exit interconnection point (IP) Ruse/Giurgiu– connection between Bulgartransgaz EAD national gas transmission system and the gas transmission system operated by Transgaz S.A. (Romania) on the Bulgarian-Romanian border in the area of Ruse/Giurgiu.

GMS Ihtiman and GMS Lozenets – reverse flow gas metering stations, physical connections of the gas transmission network for transit transmission and the national gas transmission network, enabling commercial metering of the quantities transferred between both networks, combined in a common entry-exit transfer point between the two networks;

GMS Galata – an entry point from local production of the national gas transmission network;

13

GMS Dolni Dabnik – an entry point from local production of the national gas transmission network;

Entry-exit point GMS Chiren – connection between the national gas transmission network and UGS Chiren.

14

NATURAL GAS MARKET IN THE COUNTRY AND THE REGION

Compressor Station Ihtiman

1. NATURAL GAS MARKET IN BULGARIA

1.1. General Market Overview

Bulgartransgaz EAD transmission and storage activities are regulated and carried out on in line with the licenses issued by the SEWRC. The basic requirements for these activities are regulated by the Energy Act and the by-laws harmonized with the European legislation in that field.

Natural gas consumption in Bulgaria for 2018 was 31 663 GWh, which shows 4.88 % decrease compared to the consumption in 2017 (33 285 GWh). The decrease in consumption is mainly due to the higher average monthly temperatures in 2018 compared to the previous 2017.

Data of the Total Energy Balance of the NSI shows that the natural gas share in the end energy consumption (EEC) was 16.2% for 2017, approximately 1.5% increase compared to 2016 (14.7%). The main natural gas consumers are trade companies from the Energy and Chemistry Sectors, as well as the Distribution System Operators (DSO) as end suppliers.

There is a very high energy dependency in Bulgaria in 2018 regarding natural gas supplies – 99.9%. In 2019 based on forecast data, the import dependency will not change. Local production in the country decreases. In 2019 minor natural gas quantities from local production will be provided by the gas fields Galata and GMS Dolni Dabnik.

15

To date no significant natural gas fields have been found in the Republic of Bulgaria and natural gas consumption in the country is mainly secured through gas imports by one main source – the Russian Federation. Natural gas reaches Bulgaria mainly following the route through the territories of Russia, Moldova, Ukraine and Romania.

Currently our country has one interconnection point (IP) with Greece – Kulata/Sidirocastro. This interconnection serves mainly as an entry point providing natural gas to Greece and during January 2009 crisis physical reverse flow to Bulgaria was carried out through this interconnection. As a result of the Interconnection Agreement (IA) for IP Kulata/Sidirocastro, signed between Bulgartransgaz EAD and DESFA S.A in June 2016 and a Protocol to the Long-term contract for transit transmission with OOO Gazprom Export as of 1 July 2016, an alternative option for natural gas import in the country has been provided via reverse supplies on commercial basis, i.e. backhaul and reverse flow in reverse direction via reverse connection of the modernized CS Petrich.

In 2018, the natural gas quantities by sources of supply are as follows:

No Type of supply Quantity, GWh Percentage

1: Imported natural gas

31.630 99.9 %

2: Local production 33 0.1 %

TOTAL 31,663 100%

The natural gas storage capacity in Chiren UGS and the local production are the main alternatives regarding the security of supply if import from entry point Negru Voda 1/Kardam is suspended, but the storage capacity is insufficient to fully ensure the security of supply if the import (main gas flow) is suspended on a daily basis.

These factors provide for the insufficient level of liberalization and liquidity of the national gas market and a risk regarding the security of supply.

Main participants on the gas market in Bulgaria are the following:

o Bulgartransgaz EAD – combined gas operator licensed to perform natural gas transmission and storage activities;

o Gas distribution companies – performing both natural gas public supply and distribution activities, supply natural gas to customers connected to their networks. It is their obligation to construct and develop the gas distribution networks according to the long-term business plans and conditions approved by the EWRC;

o Bulgargaz EAD – public supplier of natural gas in Bulgaria responsible for ensuring natural gas supply at prices and conditions approved by the EWRC;

o Natural gas traders – make transaction for natural gas supply with the public supplier, end suppliers, users, other natural gas traders, production companies, natural gas storage companies and the combined operator;

o Non-household natural gas customers connected to the gas transmission networks;

o Household and non-household natural gas customers connected to the gas distribution networks.

16

The natural gas distribution and supply activities to customers connected to the distribution networks is carried out by regional and local gas distribution companies – mainly private companies, operating in licence regime and price regulation conditions. Overgas Mrezhi AD, Aresgas AD, Citigas Bulgaria EAD and others have the largest market share. Production companies and two main groups of connected customers - gas distribution companies and non-household users are connected to Bulgartransgaz EAD gas transmission network.

The gas distribution companies carry out the activities of "natural gas distribution" and "natural gas supply from end supplier", supplying natural gas to customers connected to the respective gas distribution networks of the licensed territories. At the end of 2017 two companies were licensed on the territory of the Republic of Bulgaria. They exercise their activity on 35 licensed territories and serve 5 gas distribution regions (Dunav, Zapad, Trakia, Mizia, Dobrudja) and 80 municipalities beyond these regions. According to data of the gas distribution companies, the total number of their customers in 2016 was 87 274, of which 80 705 (92%) – household and 6 569 (8%) – economic entities. Customers of the gas distribution companies are mostly the households, public and administrative customers and small and medium commercial and industrial customers.

The household gas supply share in the country is still very low compared to the EU countries but there is a tendency of increase in the following years, since the required infrastructure for natural gas distribution in the country is under construction. The national Azerbaijani oil company SOCAR continues to study the legal aspects of possible future investments in the gas distribution sector in Bulgaria. The consumption of compressed natural gas also shows an increase.

Regarding the oil and gas exploration permits granted by the Ministry of Energy of the Republic of Bulgaria, there are expectations for increase of the local production share and decrease of the country dependence on natural gas imports. The granted permits include both onshore areas, and territories in the Black Sea shelf and deep waters. Since July 2012, the company Total, in partnership with Repsol and OMV, has a permit for exploration for oil and gas in Block 1-21 Khan Asparuh in the deep water part of Black Sea. In February 2016, a contract for exploration for oil and gas in Block 1-14 Silistar/Khan Kubrat was signed with Shell for 5-year period. Many concessions for natural gas production were awarded in the country, whereas their production is of limited resource and covers no more than 2-3% of the annual consumption. At present, gas field Kavarna-Iztok in Block Galata is a reliable source of local production with proven production reserves of approximately 3 724 - 4 255 GWh of natural gas. In the context of the above, the investment plans of the gas transmission operator Bulgartransgaz EAD will continue to be developed in synergy with the forecasts for the potential incremental quantities of natural gas from local production that will enter in the gas transmission system from new entry points.

1.2 Market potential and development prospects

Bulgartransgaz EAD is an owner and operator of a well-developed natural gas infrastructure, part of the single common European gas network.

The company operates in dynamic, constantly changing world and respectively European energy market. As a transmission operator of an EU member state, Bulgartransgaz EAD operates in accordance with the requirements of the Third Energy Liberalization Package, which are expanded and complemented with the adoption of regulations establishing network codes in the fields regulating the access to gas transmission networks as laid down in Regulation EC 715/2009.

17

As of 1 October, 2017 Bulgartransgaz EAD introduced efficiently the entry-exit pricing method as regards the offered services for access and transport of natural gas.

By virtue of EWRC’s Decision No НГП-01/01.08.2017 the allowed annual revenue and basic pricing parameters for a three-year regulatory period have been approved to Bulgartransgaz EAD. Based on the Decision and the Methodology setting the access and transmission prices through Bulgartransgaz EAD gas transmission network, the company set access and transport prices by entry-exit points for the respective pricing periods.

The main characteristics of the entry-exit model are as follows:

Multi-year price setting model - "Revenue cap" method. Setting the price for access and transmission of natural gas at entry and exit

points/zones;

Recovery by the prices for access and transmission of the required revenues for carrying out the transmission activity, approved by the Commission for each regulatory period;

Ensuring incentives to improve the operator's performance; Level playing field for all transmission network users; Users shall be treated equally

regardless of size, ownership or other factors; Ensuring price stability, transparency of the price setting process; Applying the Matrix approach for costs allocation by entry and exit points/zones; Capability to form a unified exit national zone; Capability to reduce the prices for access to entry and exit points to/from the natural

gas storage facilities;

As of 01.10.2017 an efficient daily balancing regime was introduced in line with the Natural gas market balancing rules and the Daily imbalance charge calculation methodology.

The expectations are in the forthcoming years the number of entry points from where gas enters the gas transmission network to increase significantly as a result of the interconnection projects with Greece, Turkey and Serbia, the commissioned in the end of 2016 new interconnection with Romania and the project for expansion of the infrastructure between the Bulgarian-Turkish and the Bulgarian-Serbian border (Phase 1 of the Balkan gas hub) for which an investment decision has been taken after a successful Phase 3 of the Open Season procedure. These will enable natural gas supply from various sources, which in turn will boost competition and will positively affect natural gas consumers. The new gas interconnections would increase to some degree the entry capacity towards Bulgaria from Greece and Turkey, and on the other hand would provide a possibility for gas supply from LNG terminals from these neighbouring countries. They would significantly contribute to the development of the natural gas market in Bulgaria and the demand for storage capacity.

The realization of the Balkan gas hub is a priority at both national and corporate level as it has the potential to connect all main gas transmission projects of South East Europe and ensure transparent and non-discriminatory access of the European users to a wide range of supply sources. The basic design is supported by the European Commission. In March 2018 a contract for carrying out a feasibility study was signed between Bulgartransgaz EAD and the selected Bulgarian-Swiss consortium АF-ЕMG Consult DZZD. On 12 June 2018 in the European Commission building in Brussels the interim results of the Balkan gas hub Feasibility study were presented. The Final report of the Contractor was approved at the end of November 2018.

Moreover, in implementation of the decisions approved by the Council of Ministers and the National Assembly to amend and supplement 2020 Energy Strategy of the Republic of Bulgaria and having regard to realization of the concept for the construction of a gas

18

distribution centre on the territory of Bulgaria, Bulgartransgaz EAD registered the subsidiary Balkan Gas Hub ЕAD. Currently, 100% of the shares are owned by Bulgartransgaz EAD, where no more than 49% of the shares could at a later stage be provided to other physical and legal entities. This would contribute to realization of the concept for the Balkan gas distribution centre and for increase in liquidity of the natural gas market in Bulgaria and the region of South Eastern Europe.

The company will operate trading platforms servicing the needs of the natural gas markets within the Balkan gas hub. In synergy with the physical infrastructure of the gas distribution centre, the prerequisites required for establishment of the first liquid physical and trading gas hub in the South East Europe region, based in Bulgaria, will be provided.

In line with its objectives, Balkan Gas Hub EAD will establish a liquid gas exchange on the territory of Bulgaria with a bilateral trade segment as well, offering state-of-the-art products and financial services. As a first stage of implementation of the gas exchange, Balkan Gas Hub EAD will provide the participants in the natural gas market in Bulgaria and the region with the opportunity to use a trading platform with all the necessary functionalities, according to the requirements of Art. 10 of Regulation (EU) No 312/2014 establishing a Network Code on Balancing of Gas Transmission Networks.

The following other conceptual gas projects are considered in the region which would affect market development, enhance diversification and security of gas supply: Eastring - a project for construction of gas transmission infrastructure from Bulgaria through Romania and Hungary to Slovakia, BRUA - Bulgaria-Romania-Hungary-Austria gas transport corridor, projects from the Southern Gas Corridor, etc.

Within the framework of the CESEC initiative, a Memorandum signed between the operators of gas transmission systems of Greece, Bulgaria, Romania, Ukraine and Moldova to implement the concept of enabling reverse flow of the Trans-Balkan gas pipeline. The concept involves offer of firm capacity products along the Trans-Balkan gas pipeline in reverse direction, to be offered for booking as of 01.01.2020 as standard short-term products and as of 01.10.2020 as annual products, as follows: In this respect, the capacities at IP Kulata/Sidirocastro and IP Negru Voda 1/Kardam in volumetric units are expected to be, as follows: 1. In flow direction GR - BG: Technical capacity: 4,100 mcm/d (1,01325 bara; 0˚C); 2. In flow direction BG - RO: Technical capacity: 4,100 mcm/d (1,01325 bara; 0˚C); Despite the relatively low share of the final energy consumption, gas is important natural resource with a potential of increasing its share in the total national energy consumption over the next years. The share of gas supplies to households in the country is still low compared to other gas markets, however with a continuous upward trend. Encouraging the gasification by expanding the gas transmission network to new regions and securing access to natural gas by new municipalities, distribution companies and new non-household users, is a priority of Bulgaria’s Energy Strategy, and Bulgartransgaz EAD activity accordingly.

Bulgaria has strategic geographic location, well-developed gas infrastructure and by implementation of the planned new projects which are currently ongoing, the country has

19

the potential to become an important factor in diversifying the natural gas sources and routes for the region.

The described perspectives are in the basis of achieving Bulgartransgaz EAD objectives and investment plans and are reflected in the overall company policy.

2. NATURAL GAS MARKET IN THE REGION

Over the last years, the development of the natural gas market in the region is related to the expected growth of natural gas consumption in Bulgaria's neighbouring countries. On one hand that is based on the long-term existing contracts for natural gas supply from the Russian Federation to the Balkans, and on the other – on market development taking into account the opportunities for natural gas supplies from new sources along the Southern Gas Corridor (including the gas pipelines under construction TAP and TANAP) and the potential of local production. These expectations are in line with the plans for construction of new connections between the gas transmission systems of Bulgaria with Turkey, Greece and Serbia, completion of the infrastructure with Romania, establishing the Balkan gas hub, as well as expansion and modernization of the gas transmission infrastructure of Bulgartransgaz EAD with a view to adapting it to the important projects in the region. Among the Company priorities is the establishment of a gas exchange and in December 2018 a Memorandum of Understanding was signed between the Austrian Central European Gas Hub (CEGH) and Bulgartransgaz EAD with subject "Support for the development of the Balkan gas hub and exchange of information, know-how and best practices in creating a liquid market for natural gas trading in the region."

Existing and planned infrastructure in the region – gas pipelines, LNG terminals and gas storage facilities

Source: Fondation pour la recherché strategique

In addition, natural gas advantages (economic, technological and environmental) resulted in the relatively rapid growth of its consumption in the last thirty years worldwide.

20

This is laid down in 2020 Europe Strategy where the main objectives of the EU 20:20:20 were set in terms of climate and energy. Its main point is promoting the policy of transition to low waste and waste-free technologies. In essence, this is replacement of the energy facilities in most industrial enterprises and those in the chemical industry in order to use more environmentally friendly fuels as certainly natural gas is. The growing need of sustainable development of the transport sector also focuses on the use of natural gas as an alternative fuel. This requires rapid construction of compressor stations on the territory of the Pan-European transport corridors. In recent years, the shipping industry has also focused on the use of liquefied natural gas.

The measures mentioned will contribute to overcoming the consequences of air pollution by reducing the emissions of carbon and nitrogen oxides.

The review of natural gas markets in the neighbouring countries outlines the main trends for development of the regional gas market in terms of diversification and more tangible price competition:

2.1. Greece

As of 1 July 2016, as a result of conclusion of an Interconnection Agreement with DESFA S.A. for IP Kulata/Sidirocastro, a possibility to import gas from Greece was provided.

Natural gas consumption in Greece has been steadily growing and has increased more than twice over the last decade. In 2017 the consumption amounted to 4.8 bcm/y whereas electricity generation still kept a significant share of it.

The consumption was covered by imports of LNG sources in local terminals – 13%; from the gas pipeline connection with Turkey – 21% and the gas pipeline connection with Bulgaria with a source of supply the Russian Federation – 66%.

The Greek company DEPA has three long-term contracts with foreign companies for natural gas supply – with the Russian OOO Gazprom Export – up to 3 bcm/y by 2026, the Algerian Sonatrach (LNG) - up to 0.68 bcm/y by 2021, and the Turkish company Botas – up to 0.75 bcm/y by 2021, and the total supply volume under these contracts does not exceed 4.5 bcm/y. Currently about 90% of the natural gas import in the country is carried out under long-term contracts. Besides Sonatrach, DEPA S.A. has signed a contract with the Italian gas and petroleum company ENI for extraordinary natural gas supplies in case of a crisis or force majeure circumstances. DEPA S.A. follows the plans for expansion of the gas distribution network in the country to meet the constantly increasing number of household customers.

A joint Greek-Russian company Prometheus Gas (50% owned by OОО Gazprom Export and 50 % by Dimitrios Ch. Copelouzos) operates as well on the Greek market, which is increasingly imposing the Russian gas. In order to secure the market by 2016, the company had 3 bcm/y, and for the period beyond 2017 up to 6 bcm/y have been foreseen, but in October 2017 a long-term contract was signed for supply of 1 bcm/y gas for the period from 1 January 2018 until 31 December 2027. The increase in natural gas consumption combined with deregulation on the market contributes favourably to the future development of Prometheus Gas S.A. and their recognition among the leaders on the regional gas market. Its activity is also related to the construction of energy facilities in Greece.

In 2017, Gazprom Export also entered into a contract with one of the leading Greek industrial companies, Mytilineos, under which about 50 mcm of gas were supplied.

In order to satisfy its natural gas needs during growing domestic consumption, Greece has the opportunity to use various supply sources, including the constructed terminal for liquefied natural gas in Revithoussa with capacity of 5 bcm/y which was expanded up to 7 bcm/y in the period 2016/2017. The terminal is still partly used and has a reserve to increase

21

gas storage and supply quantities. At the end of 2018, the storage capacity increased to 225,000 m³, which to a certain extent also relates to the development of the Poseidon Med II project (2015-2020). It basically builds on the Poseidon Med project (COSTA II East) and aims to contribute to the wider use of LNG as an alternative fuel for shipping in order to reduce the negative impacts of heavy fuel use and move towards safe, environmentally friendly and low-carbon fuel to meet the requirements of a number of EU directives on alternative fuels for sustainable future in the shipping industry. The project focuses primarily on maritime transport in the Eastern Mediterranean and is co-funded by the European Union. It includes the Liquified Gas Terminal Revithoussa and covers three countries - Greece, Italy and Cyprus, as well as six European ports (Piraeus, Patras, Lemesos, Venice, Heraklion, Igoumenitsa).

The project for construction of a new LNG terminal in Aegean Sea – Alexandroupolis, announced by the Greek company Gastrade S.A., is in strategic proximity to the gas transmission network of DESFA S.A. and is ranked as a project of common interest (PCI) by the European Commission in the Third list of the EC. In February 2017 one of the biggest international fleets – owner of tankers for LNG transport – Gas Log Ltd. acquired 20% of Gastrade S.A. Interest in the construction of this LNG terminal have expressed DEPA S.A., which confirmed its participation, and until November 2018 the possibility of joint participation of Bulgarian Energy Holding EAD was considered as well. As a result of 2020 Energy Strategy, updated by the National Assembly on November 30, 2018, the Republic of Bulgaria is expected to have 20% shareholding in the project company by the Bulgarian gas transmission operator Bulgartransgaz EAD.

In August 2017 Wood Group signed a contract with Gastrade S.A. for studies and preparation of a technical design for development of a floating facility to receive, store and re-gasify the liquid natural gas (FSRU) in Alexandroupolis. The design annual capacity of the terminal is 6.1 bcm and the storage capacity - 170 000 m3. These natural gas quantities will enable balancing of the needs not only of the local market, but also the Bulgarian, Romanian, Northern Macedonian, Serbian and Hungarian markets. At the end of October 2018, Gastrade S.A. commenced the first non-binding market test for the LNG terminal, in accordance with the LNG Terminal Management and Capacity allocation guidelines under the current Regulation. The test results showed a tremendous interest by 20 companies and requested capacity of 12.2 bcm/y and a binding phase is forthcoming. The companies that participated in this stage of the market test are not only from Southeast Europe, but also large international gas traders. Countries producing LNG such as Algeria, Qatar, the USA, etc. (considering the export capabilities of US LNG exporters - Cheniere LNG и Tellurian LNG), etc. are among the potential sources of supply. Future possible supply option from Cyprus and Israel is also being considered, by using both Egyptian export terminals, which are expected to operate at full capacity in 2020/2021.

The project is considered against the background of the Bulgarian-Greek interconnection under construction and the Trans – Adriatic gas pipeline.

The final investment decision is expected to be taken by the end of 2019, and the terminal to be run into commercial operation in 2021.

The other project Aegean LNG in Kavala region, proposed by DEPA S.A., remained at the conceptual stage and received support by the EC.

In May 2010 Greece signed a non-binding Memorandum of Understanding with Qatar for LNG import, including plans to import Qatari LNG and construction of a € 3.5 billion LNG terminal of 7 bcm/y capacity in Western Greece.

22

Gas transmission infrastructure in Greece

Source: DEPA S.A.

In 2017, a new procedure for privatization of the Greek gas operator DESFA S.A. was announced, following failure of the deal with SOCAR, the state oil company in Azerbaijan, in 2016. According to data from the Greek Privatization Agency (HRADF), the following bidders were approved to present binding offers: a consortium between the Italian gas distribution operator Snam S.p.A, the Spanish Enagas Internacional S.L.U. and Fluxys S.A from Belgium, as well as the consortium of the Italian Regasificador del Noroeste SA, the Romanian Transgaz SA and the European Bank for Reconstruction and Development (EBRD). For sale were announced 31% of HRADF's share in DESFA and 35% of Hellenic Petroleum (HELPE) share in the company. In April 2018, the consortium between Snam, Enagas and Fluxys took control over DESFA. The three companies are also shareholders in the TAP project, which plays a key role in gas transport along the Southern Gas Corridor. The construction of new interconnections is among the priorities that will make supplies to Europe more secure and competitive, relying increasingly on export capacity from the Mediterranean, the Middle East and Central Asia.

In December 2017, Cyprus, Greece, Israel and Italy signed a joint Memorandum of Understanding on the construction of the East Med Gas Pipeline. The project envisages natural gas transportation from the fields in the Eastern Mediterranean to Europe through the island of Crete and the mainland of Greece and via IGI to reach Italy. After detailed technical-economic and financial studies on the gas pipeline infrastructure, in November 2018 an Intergovernmental agreement was signed between the parties. The planned capacity of the East Med gas pipeline is 10 bcm/y with a possibility to increase it by 16 bcm.

The Final Investment Decision is to be taken in the mid of 2021 and the facility construction is scheduled to be completed in 2025. East Med gas pipeline is a PCI for EC in the East

23

Mediterranean and has the prospect of becoming an alternative energy corridor for Europe. So far Bulgaria has held preliminary discussions on the possible future natural gas supplies from Israel and Cyprus from the offshore fields in the East Mediterranean along the possible routes – by the offshore gas pipeline East Med project, LNG, etc.

An Intergovernmental agreement between Cyprus and Egypt was signed in September 2018 on the construction of an offshore gas pipeline connecting the gas transmission systems of Cyprus and Egypt. It provides the political, legal, technical and financial framework for construction of the off-shore gas pipeline, which will connect the first Cyprus gas field Aphrodite with the LNG terminal in Egypt. The future gas pipeline is very important for operation of the Cyprus gas fields and the overall energy development of the Eastern Mediterranean. At the beginning of 2019, the American company Exonn Mobil commenced its exploratory drillings only in the economic area of Cyprus, after Turkey disputed and hindered the drilling activities at the end of last year. The reported results are encouraging in terms of commercial profitability of the open field and according to initial data amount to 142-227 bcm, which was developed jointly by the Cyprus branch of ExxonMobil Exploration Company holding a 60% share and Qatar Petroleum with a 40% share. The fields discovered so far in the Eastern Mediterranean and their assessments open excellent opportunities to cover Europe’s energy needs in the period by 2040. So far Israel has announced availability in the offshore gas fields Tamar - 318 bcm and Leviathan – 605 bcm, and the only Cyprus gas field Aphrodite discovered so far, has a reserve of 120-129 bcm. The leading partners in the biggest Israeli gas fields Noble Energy Inc. and Delek Drilling-LP signed an agreement for gas export with the Egyptian trader Dolphinus Holdings Ltd. under which about 64 bcm of natural gas will be exported from Tamar and Leviathan fields for 10 years. The possibilities of natural gas volumes export to the Egyptian market are to be indicated.

In 2018, the American company Noble Energy Inc. signed a number of agreements in support of natural gas supplies from Leviathan and Tamar fields in Egypt. Noble Energy and its partners (Israeli gas operator Delek Drilling and the Egyptian East Gas) signed agreements for acquisition of a 39% share in East Mediterranean Gas, which manages the inoperative gas pipeline connecting the Israeli and Egyptian gas networks. Upon successful completion of the deal, Noble Energy and its partners will sign an agreement for the gas pipeline operation and provide access to its full capacity. Finalization is scheduled for 2019 and the off-shore gas pipeline will be used primarily to transport natural gas from Leviathan and Tamar to Egypt. Currently Israel has contracts concluded and exports gas to Egypt and Jordan.

The project ITGI Poseidon is part of the Southern Gas Corridor connecting Turkey-Greece-Italy. The initially envisaged capacity is 15 bcm/y. at the Greek-Turkish border and capacity capabilities to increase it to 20 bcm/y. The realization of this project will provide Italy and the European countries with the opportunity of natural gas supply from the Caspian Sea or the Middle East. ITGI Poseidon has submitted an application to the Greek energy regulator RAE for project licensing as an independent gas transmission system and plans to conduct a market test.

The project includes the following gas pipeline sections:

Turkish gas transmission network – to be modernized so in order to ensure transit transmission of natural gas quantities intended for Italy and Greece.

IGB (Interconnection Greece-Bulgaria) upon signing of the final investment decision, an option will be provided for the capacity of the Interconnection with Greece to be increased from the initial 3 bcm/y to 5.0 bcm/y in case of proven economic interest. During the first

24

phase of ICGB market test (joint investment company with shareholding Bulgarian Energy Holding EAD - 50% and IGI Poseidon S.A. - 50%), nine non-binding offers were submitted for about 4.3 bcm/y in total for natural gas transmission from Greece to Bulgaria and approximately 1 bcm/y for firm reverse transmission in Bulgaria-Greece direction. Among the companies that have submitted offers are Bulgarian private gas distribution companies, the Romanian OMV Petrom, Azerbaijani oil company SOCAR (which participates in the development of Shah Deniz II) and others. Binding offers from five companies have been submitted and capacity of 1.57 bcm/y booked out of 2.7 bcm/y of the announced capacity in the second phase. Pursuant to the procedure, the market test was completed by signing agreements for preliminary capacity booking by the participants who have submitted offers. That took place following approval of the respective national regulatory authorities of Greece and Bulgaria. The European Commission has announced the Interconnection Greece-Bulgaria a project of common interest (PCI) in the Third list of the EC.

In 2018, the European Commission considered reasonable the state aid plans of Bulgaria and Greece for construction and run into operation of a gas interconnection in line with EU rules. The total investment costs for project construction amount to € 240 million and are allocated as follows: direct shareholding of EUR 46 million from the shareholders in the joint stock company, EUR 45 million from the European Energy Program for Reconstruction (EEPR), centrally managed by the EC, EUR 110 million loan from the European Investment Bank (EIB) granted to the of Bulgarian Energy Holding (subsequently transferred to ICGB) and direct financial contribution of EUR 39 million from the state budget of Bulgaria through Operational Program "Innovation and Competitiveness 2014-2020".

In August 2018, the national regulators of Greece and Bulgaria took a final joint decision on exemption of the gas pipeline from the requirements of Art. 36 of the Gas Directive 73/2009/EC on Third-party access, regulated tariff and ownership. The decision defines the regulatory framework under which the gas pipeline will operate in commercial operation. The Tariff code was timely submitted on 06.11.2018 and contains the final methodology applicable to IGB tariff calculation under the methodology approved by the regulators upon conduct of the market test for the project. The approval of IGB Tariff code by the national regulators is a precondition for proceeding with the signing of Transport contracts with the traders having booked capacity through IGB. At present, only pre-agreement for booking capacity for the gas pipeline have been signed.

In February, ICGB successfully completed the next step of the process towards certification as an independent gas transmission operator. More than four months prior to the deadline, the project company submitted to the regulators of Bulgaria and Greece the Network code for the IGB Pipeline by 01.07.2019. The Network code contains the rules and procedures for operating the IGB gas transmission system and details on the rights and obligations of the transmission operator and the traders.

In September 2017 the Ministry of Regional Development and Public Works issued the Building permit for the interconnector on Bulgarian territory, and in February 2019 also for the Greek section.

Construction is planned to commence in the mid-2019 and end by the end of 2020.

ITG (Interconnection Turkey-Greece) in operation as of November 2007

IGI Poseidon – offshore section of ITGI through Ionian Sea to connect the gas transmission systems of Greece and Italy where Edison and DEPA S.A. are equal partners. The latest shareholders' concept for Poseidon gas pipeline project is to connect Greece with the Italian, Bulgarian and European gas systems, providing access to gas infrastructure and the available sources of Greece. This also includes connections to the future EastMed gas

25

pipeline and the IGB interconnector, providing Europe with the opportunity to boost price competition and energy security.

According to the intentions of the shareholders, a final investment decision is expected to be taken in the first half of 2019. The main building permits for the Italian section have been obtained and the procedure for issuing permits in Greece is underway.

ITGI Gas Infrastructure

Source: Edison

Actually, implementation of ITGI receded into the background after obtaining final investment decision and construction of the Trans-Adriatic Gas Pipeline (TAP).

TAP is the westward continuation of TANAP. The gas pipeline will be connected to TANAP at the Turkish-Greek border and will cross Greece, Albania, the Adriatic Sea and will reach Southern Italy in its end point. According to the initial notification, 10 bcm will be transported along it. Project’s shareholders are BP (20%), SOCAR (20%), Snam S.p.A. (20%), Fluxys (19%), Enagás (16%) and Axpo (5%).

In March, 2016 the European Commission supported TAP construction and confirmed that the Trans Adriatic gas pipeline complies with all rules for free competition in the EU and will significantly improve energy security. Gazprom has expressed interest in the possibilities to use the market potential to supply Russian gas for Europe via TAP or via the ITGI Poseidon project.

Funding of the gas pipeline final phase was ensured and EBRD, EIB and other loans were confirmed. The first natural gas volumes are planned to be transported in the second half of 2020.

Plans for TAP expansion to the northwest were developed – the Ionian-Adriatic Gas Pipeline (IAP) of 5 bcm/y capacity to supply gas to Albania, Montenegro, Sothern Croatia and Bosnia and Herzegovina, for which TAP consortium has signed a Memorandum of Understanding and cooperation with the TSOs of the respective countries - (BH-gas, Plinacro and Geoplin Plinovodi), and with the Energy Ministries of Albania and Montenegro.

26

Political support for construction of the branch TAP – IAP dates back to May 2013 when the governments of Albania, Bosnia and Herzegovina, Croatia and Montenegro signed a MOU in support of the two gas pipelines. In august 2016 the Parties signed a MOU for the construction of IAP with Azerbaijani state oil and gas company SOCAR. In July 2018, SOCAR announced its intention to set up a new company that will act as a technical consultant and guide the future development of the project.

In February 2017, Montenegro and Albania received a joint grant to the amount of EUR 2.5 mln by the Western Balkans Investment Framework (WBIF) for conceptual design of the project. The building permits for the Croatian section of the Ionian-Adriatic gas pipeline are expected to be obtained in 2019. In the future, Croatia expects to receive up to 2.5 bcm/y.

Of key significance to the gas supplies from Shah Deniz II gas field are both, the existing gas pipeline between Bulgaria and Greece which, in compliance with the requirements of Regulation (EC) 994/2010, as of January 1, 2014 provides the possibility (firm capacity) for gas transmission towards Bulgaria, and the future Interconnector Greece-Bulgaria (IGB), considering the intentions and possibilities for connection between TAP and IGB near the town of Komotini, Greece. In September 2013 the public supplier Bulgargaz EAD and SOCAR on behalf of the Consortium Shah Deniz concluded a supply contract for 1 bcm/y for a term of 25 years, whereas the first gas quantities to the country are expected to be supplied by the end 2018. In May 2018, the completed first stage of the Southern Gas Corridor project was officially opened.

In 2018, the European Union resumed the negotiations with Azerbaijan and Turkmenistan on the implementation of the Trans-Caspian gas pipeline, as part of an expanded Southern Gas Corridor, aimed at diversifying Turkmen gas supplies. The agreement, signed by Azerbaijan, Iran, Kazakhstan, Russia and Turkmenistan, on the Caspian Sea status, which has been a controversial economic zone for more than 20 years, contributed to that.

Planned gas transmission infrastructure connecting Europe with Shah Deniz II gas field

Source: BP

27

2.2 Turkey

Consumption in Turkey in 2017 amounted to 46.03 bcm and is expected to reach 59 bcm by 2020. BOTAS plans to increase the daily capacity of the Turkish gas transmission system in the next years up to 350 - 400 mcm/d compared to the current 200 mcm/d.

The installed capacity, using natural gas for generation of electricity, is used mostly to supply electric generators and plants, industrial and household customers. Demand is expected to continue to increase in the future, as Turkey plans to further develop gas-fired power plants.

Household and industrial consumption are also expected to increase, along with the construction of more distribution gas pipelines and expansion of the existing distribution networks as a result of privatization of the distribution companies.

Turkey produces small amounts of natural gas, covering an insignificant part of domestic consumption (about 1% in 2017). The country imports natural gas mostly from the Russian Federation along two routes – Trans Balkan Gas Pipeline and through Blue Stream gas pipeline. However, the share of the imported Russian gas has been declining in recent years, as Turkey diversifies its gas supply by importing gas from Iran and Azerbaijan, as well as by LNG mostly from Algeria and Nigeria.

The state oil and gas company BOTAS has long-term natural gas supply contracts concluded with:

Algeria (LNG) – 4.4 bcm/y by October 2024;

Nigeria (LNG) – 1.3 bcm/y by October 2021;

Iran – 9.6 bcm/y by July 2026;

Russian Federation (Black Sea) – 16 bcm/y by the end of 2025;

Russian Federation (West Route) – 4 bcm/y by the end of 2021;

Azerbaijan (Phase I) – 6.6 bcm/y by April 2021;

Azerbaijan (Phase II) – 6.0 bcm/y, as of 2018 by 2033;

Azerbaijan – 0.15 bcm/y by 2046.

The remaining large volumes of gas are traded by 10 companies, holding wholesale licenses on the Turkish market.

In 2017 Turkey has imported 55.25 bcm and Botas has re-exported 642 mcm for the same period. In 2017, the imported natural gas quantities through gas pipelines, amount to 80.52 % and are allocated as follows: 6.5 bcm/y (11.85 %) from Azerbaijan, 9.25 bcm/y (16.74%) from Iran, from Russia 28.69 bcm/y - (15.51 bcm/y along Blue Stream, 13.18 bcm/y from Russia via Bulgaria) - 51.93%.

In 2017, 10.76 bcm/y were delivered through the liquefied natural gas terminals. (19.42%) of total imported quantities in the country - from Algeria 4.62 bcm/y (8.36%) from Nigeria 2.08 bcm/y (3.76%). From spot trading the realized quantities are 4.06 bcm/y. (7.36%). The announced actual LNG storage capacity for 2017 was 943 mcm. At the end of 2016 Turkey and Qatar signed an import agreement for 1.2 bcm/y LNG and in September 2017 BOTAS and Qatargas signed a three-year Supply contract. Turkey is one of the countries, which received LNG from the terminal of Cheniere Energy - Sabine Pass in Louisiana as well.

28

Gas pipelines passing through Turkey - existing and planned

Source: Republic of Turkey – Ministry of Energy and Natural Resources

In order to compensate the growing natural gas demand, Turkey will rely on the construction of the Trans-Anatolian gas pipeline (TANAP), intended to natural gas transport from the Azerbaijani field Shah Deniz II from the Georgian-Turkish border to the western border of Turkey (1850 km, DN 1200).

The first stage capacity is 16 bcm/y, of which 10 bcm/y will be transited to the European markets and 6 bcm/y have been negotiated to cover the Turkish domestic consumption.

The project is planned to be developed by progressive capacity increase up to 23 bcm/y by 2023, 31 bcm/y by 2026, reaching 60 bcm/y in its last stage. TANAP shareholding is 58% for the state oil and gas company of Azerbaijan (SOCAR), 30% for the Turkish company BOTAS and 12% for British Petroleum (BP). In January, 2016 the consortium for implementation of the TANAP project identified the composition of the joint venture to build the section on the territory of the Turkish region Eskisehir to the Greek border. TANAP opening ceremony was held on June 19, 2018, and the first natural gas deliveries under the project started on June 30.

Export to Europe is planned to start in 2020.

The projects within the Southern Gas corridor, TAP and TANAP, were included in the Third PCI of the EC.

Following the statements made at political level by Russia on suspension of the South Stream project, on December 1, 2014 OAO Gazprom and the Turkish company BOTAS signed a Memorandum of Understanding on the construction of a new off-shore gas pipeline - TurkStream. The design capacity of the gas pipeline is 31.5 bcm/y. The route passes through the Black Sea offshore from Russia to a receiving terminal on the Turkish coast and consists of two gas pipelines (one for the Turkish market and the other one for the European), each of them of 15.75 bcm/y capacity for which South Stream Transport B.V. (100 % owned by Gazprom) has concluded construction contracts with the Swiss company Allseas group. The Russian company started the construction of TurkStream gas pipeline running on the Black Sea bed in May 2017, whereas Gazprom and the Turkish Ministry of

29

Energy should agree on the on-shore routing of the second pipe of TurkStream on Turkish territory. The two pipelines on the off-shore gas pipeline are scheduled to be completed by the end of 2019.

In September 2017 the Board of Directors of Gazprom approved a 50% shareholding in the joint project company TürkAkım Gaz Taşıma A.Ş. with the Turkish BOTAS, which will construct the on-land section of TurkStream gas pipeline. In the beginning of October, Turkey approved the Environmental Impact Assessment (EIA) of the TurkStream terminal on the Turkish shore, and in the beginning of 2018, together with Petrofac, commenced construction works. One of the leading companies on the construction works market in Turkey, Tekfen, was selected as a contractor. As a result of the accelerated and synchronized works, the gas pipeline is to be run into operation by the end of 2019.

If the other planned new projects are implemented (e.g. a new gas pipeline from Iraq of 10 bcm/y capacity, the Southern Gas Corridor projects and the new LNG terminal on the Southern coast of 10 bcm/y capacity, Turkey will play significant role not only as a transit country of Caspian gas, but also as a supplying country and/or a transporter of additional natural gas quantities to the neighbouring countries in Europe. This will be possible thanks to its favourable geographic location, as it is closely situated to above 70% of the world’s proven natural gas reserves. If the consumption continuously grows, in the near future Turkey will need about 6 -7 bcm active gas, to be stored in underground gas storage facilities. In this respect, the country has been implementing for years an ambitious program for expansion of the operating gas storage facilities and construction of new ones on its own territory, together with the two constructed and operating LNG terminals (Marmara Ereglisi of 8.2 bcm/y capacity following expansion and 18 mcm/d and Aliiaga of 6 bcm/y annual capacity and 16,5 mcm/d), having natural gas storage capacities of 172,2 mcm and 156,8 mcm, respectively. The daily capacity of Marmara Ereglisi is envisaged to reach up to 27 mcm in the next three years. Currently, the total daily capacity of both terminal amount to about 34.5 mcm and efforts will be made to increase it considerably up to 43.5 mcm in the period by the end of 2019.

In 2016 Turkey announced the first floating LNG re-gasification terminal ETKI (LNG), located close to Izmir and developed jointly with the French company ENGIE. The facility has planned annual capacity of 5 bcm, daily capacity of 14 mcm and a capability to store 143 mcm natural gas. It is expected to support the LNG supplies mainly during the winter months.

In order to increase its storage capacity in the situation of growing demand, Turkey has another two LNG floating storage and re-gasification facilities (FSRU at Hatay Dörtyol in the Saros bay). The facility at Hatay Dörtyol has a daily re-gasification capacity of 20 mcm and was commissioned in February 2018. These activities are an important step to increasing the security of supply.

Two gas storages operate on the territory of the country - Sultanhani (Aksaray) and Silivri (Marmara), respectively with capacity of 1.5 and 2.66 bcm, and the total volume of active gas that can be stored in Turkey is currently abound 4.5 bcm. For 2017, the announced actual storage capacity in the underground gas storage facilities was 3.191 bcm. Moreover, Turkey is constructing 3 new gas storage facilities Tuz Golu 1 UGS in salt caverns – 960 mcm, Tuz Golu 2 UGS in salt caverns – 4.2 bcm, Tarsus UGS– 1 bcm. The first stage of Tus Golu UGS was completed in the end of 2017 of 20 mcm/d production capacity, and following completion of the second phase in 2019, the daily capacity will reach up to 40 mcm.

At the end of 2016, the project for gas storage construction was revised, and in 2018 Turkey provided funds in the form of loans from the World Bank and the Asian Infrastructure Investment Bank (AIIB) for expansion of Tuz Golu UGS from 1.2 bcm to 4.2 bcm.

30

Following completion of the expansion activities of Silivri (Marmara) gas storage facility, the storage capacity increased to 2.84 bcm and is planned to subsequently reach 4.6 bcm. The strategic plan of the Ministry of Energy and Natural Resources of Turkey for the period 2015-2019 envisages the storage volume to reach 10 % of the equivalent of the annual natural gas consumption which amounts to about 5.6 bcm by the end of 2019 according to the preliminary estimates. After 2020 the total volume of gas stored in underground gas storages, together with the capacities of the two LNG terminals, is expected to reach about 8.0 bcm. The natural gas storage capacity will continuously increase, and in the time horizon up to 2020 Turkey is expected to increase its annual natural gas storage capacity up to about 11 bcm, and the cumulative storage capacity to amount 20% of the annual gas consumption or about 12% of the natural gas passing through the country.

The storage development program, implemented by Turkey, is in line with securing of the expected additional gas flows which the country will receive from Russia.

North-western Turkey is a major natural gas consumer. At present, the main problem of the gas transmission system of Turkey, is provision of the natural gas quantities requested for the region of Istanbul. The country experiences seasonal natural gas demand and during winter, there is technical capability of providing additional gas quantities from the Balkan direction due to the insufficient storage capacity. According to study of the supply and consumption balance, currently Turkey has no problem in satisfying the demand of natural gas on an annual basis. Despite that, during the winter months, when consumption is high, upon temperatures drop below the seasonal level, consumption might increase to the maximum allowable values and that might cause periodic imbalances.

In addition to the above, there is further potential for expansion of the interconnectivity between Bulgaria and Turkey, therefore MoU was signed in March 2014 between the Ministry of Energy of the Republic of Bulgaria and the Energy and Natural Resources Ministry of the Republic of Turkey. According to a preliminary evaluation, the economically feasible amount of the additional capacity of the Interconnection Turkey-Bulgaria (ITB) is within 3 bcm/y. The realization of this project would contribute significantly to the economic growth of both countries, as Turkey is an important transit hub in gas transportation from the Caspian region, Central Asia and the Middle East.

2.3 Romania