2017 Microsoft Hosting and Cloud study. By 451 Research.

127

Hosting and Cloud Study 2017 Digital Transformation Opportunity for Service Providers: Beyond Infrastructure Survey Data Summary Report

-

Upload

hameed-mohammed -

Category

Technology

-

view

403 -

download

0

Transcript of 2017 Microsoft Hosting and Cloud study. By 451 Research.

Hosting and Cloud Study 2017Digital Transformation Opportunity for Service Providers: Beyond Infrastructure

Survey Data Summary Report

Study OverviewGrand Strategy for Digital Transformation: Partner for Success, is a study Microsoft commissioned through 451 Research. The study is designed to better understand how companies, SMBs, Enterprises etc. are transforming digitally and identify market opportunities for Microsoft’s infrastructure service provider partners to help their customers as they progress along their digital transformation journey. Over 1,700 respondents across 10 geographies participated in this survey study that was fielded between January 30, 2017 to February 22, 2017.

Key findings showed:

The Era of Managed Infrastructure Services: Managed is the New Normal – 62% of Cloud/Hosting Infrastructure Spending Comes Bundled with Value-Added Services

The Next “Beyond Infrastructure” Opportunity: Professional Services for Cloud-Enablement represent 18% of total hosting/cloud spending and 25% of the “Beyond Infrastructure” Opportunity – But Hurry…The Window is Closing Fast!

The Multi-Cloud World Is Real, Tightly Linked to Digital Transformation. 41% of Organizations Are Already On-Board, Driven by Best Execution Venue Considerations, Maximizing On-Premises IT Investments, and Opex-based IT Resource Extension. However, Implementation and Management Challenges Create Service Provider Opportunity --89% of Organizations Are Willing to Pay A Hefty Premium For Assistance

2

Study Overview (Cont.)Key findings showed: (Cont.)

A Majority of Businesses Are Now On-Board the Digital Economy Express, But Skills, Expertise, and Partners Are Lacking, Resulting in A Key Role for Service Providers in Future Digital Transformation Projects • 52% of organizations are on-board with the digital revolution as Market Disruptors, Market Makers or Business

Re-inventors (compared to 46% in 2016)

Half of All Organizations Consider Service Providers As Vital For Future Digital Transformation Projects. 60% of These Look to Service Providers for Sourcing, Implementation and Management and Would Be Willing to Pay a 2X Premium for a “One Throat to Choke” Trusted Advisor Solution

3

Geographic Scope

Worldwide Sample Size n=1,738 10 Countries Represented

USA55%

UK8%

Germany7%

India7%

Brazil5%

Netherlands3%

Turkey3%

Japan4%

Singapore3%

Australia5%

5

HOSTING/CLOUD SERVICES SPENDING (H)

Budgets

41%

39%

42%

41%

39%

40%

30%

36%

30%

30%

32%

32%

16%

13%

16%

16%

17%

16%

13%

12%

12%

14%

12%

12%

MEA (n=47)

LA (n=95)

APAC (n=316)

WE (n=330)

NA (n=950)

Total (n=1738)

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%Average %

2017 IT Budget Allocation by Region

On-PremisesInfrastructure &StaffHosting Services

SaaS

S8b. Using your best guess, approximately what percentage of your total IT budget in 2017 is allocated to: [sum to 100%]

7

Budgets/Spending

8

26%

25%

26%

26%

25%

26%

19%

18%

21%

20%

19%

20%

18%

18%

18%

18%

19%

18%

18%

20%

18%

17%

19%

18%

18%

20%

17%

19%

18%

18%

MEA(n=47)

LA(n=95)

APAC(n=316)

WE(n=330)

NA(n=950)

Total(n=1738)

0% 20% 40% 60% 80% 100%Average %

2017 Hosting/Cloud Services Budget Allocation by Region

InfrastructureHostingApplicationHostingManagedServicesSecurityServicesProfessionalServices

28%

29%

26%

27%

26%

27%

22%

19%

22%

21%

20%

21%

18%

16%

18%

17%

19%

18%

18%

20%

19%

18%

19%

19%

15%

16%

15%

17%

16%

16%

MEA(n=47)

LA (n=95)

APAC(n=316)

WE(n=330)

NA(n=950)

Total(n=1738)

0% 20% 40% 60% 80% 100%Average %

2019 Hosting/Cloud Services Budget Allocation by Region

InfrastructureHostingApplicationHostingManagedServicesSecurityServicesProfessionalServices

H1. Approximately what percent of your HOSTING & CLOUD SERVICES budget in 2016 is allocated to the following services? [Sum to 100%]H2. Now thinking out two years, approximately what percent of your HOSTING & CLOUD SERVICES budget will be allocated to the following services? [Sum to 100%]

INFRASTRUCTURE HOSTING SERVICES AND HYBRID/MULTI-CLOUD (I)

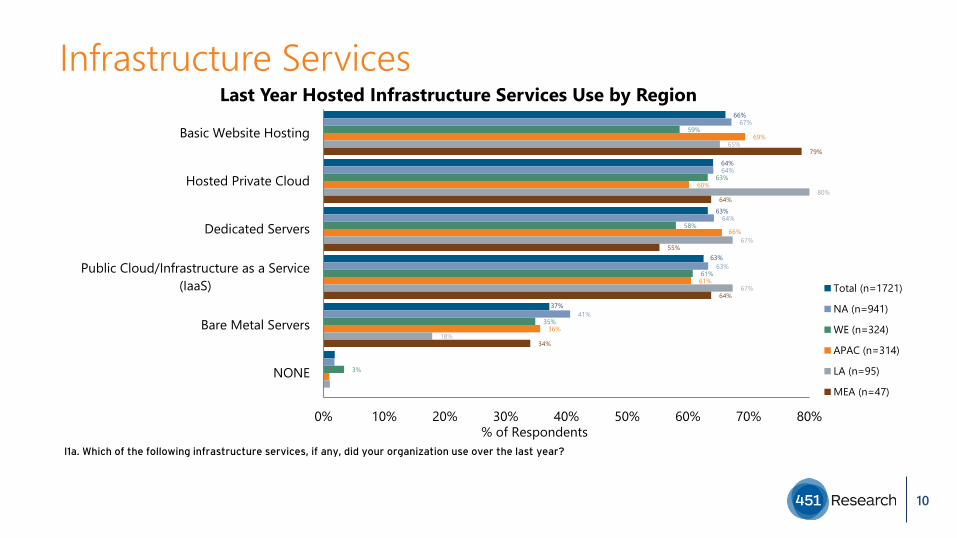

Infrastructure Services66%

64%

63%

63%

37%

67%

64%

64%

63%

41%

59%

63%

58%

61%

35%

3%

69%

60%

66%

61%

36%

65%

80%

67%

67%

18%

79%

64%

55%

64%

34%

0% 10% 20% 30% 40% 50% 60% 70% 80%

Basic Website Hosting

Hosted Private Cloud

Dedicated Servers

Public Cloud/Infrastructure as a Service(IaaS)

Bare Metal Servers

NONE

% of Respondents

Last Year Hosted Infrastructure Services Use by Region

Total (n=1721)

NA (n=941)

WE (n=324)

APAC (n=314)

LA (n=95)

MEA (n=47)

I1a. Which of the following infrastructure services, if any, did your organization use over the last year?

10

Infrastructure Services66%

61%

60%

53%

39%

65%

61%

58%

52%

38%

64%

58%

58%

52%

40%

68%

67%

66%

57%

40%

74%

60%

62%

48%

45%

3%

70%

66%

68%

72%

32%

0% 10% 20% 30% 40% 50% 60% 70% 80%

Hosted Private Cloud

Dedicated Servers

Public Cloud/Infrastructure as a Service(IaaS)

Basic Website Hosting

Bare Metal Servers

NONE

% of Respondents

Coming Year Hosted Infrastructure Services Use by Region

Total (n=1721)

NA (n=941)

WE (n=324)

APAC (n=314)

LA (n=95)

MEA (n=47)

I1b. Which of the following infrastructure services, if any, do you plan to use in the coming year?

11

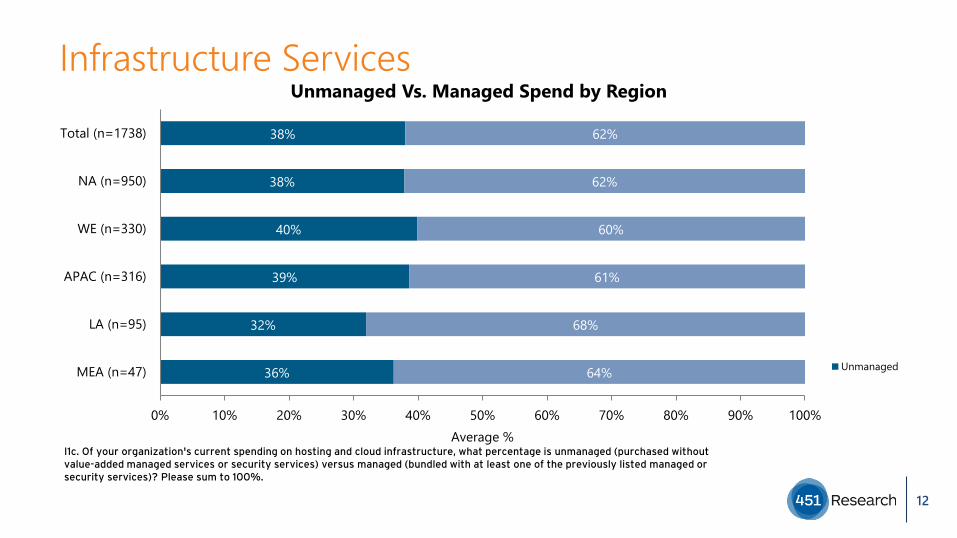

Infrastructure Services

36%

32%

39%

40%

38%

38%

64%

68%

61%

60%

62%

62%

MEA (n=47)

LA (n=95)

APAC (n=316)

WE (n=330)

NA (n=950)

Total (n=1738)

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%Average %

Unmanaged Vs. Managed Spend by Region

Unmanaged

I1c. Of your organization's current spending on hosting and cloud infrastructure, what percentage is unmanaged (purchased without value-added managed services or security services) versus managed (bundled with at least one of the previously listed managed orsecurity services)? Please sum to 100%.

12

Infrastructure Services

48%

43%

47%

47%

45%

46%

52%

57%

53%

53%

55%

54%

MEA (n=47)

LA (n=95)

APAC (n=316)

WE (n=330)

NA (n=950)

Total (n=1738)

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%Average %

Managed Spend by Region

Basicinfrastructure

Managedservices/securityservices

I1d . Thinking about your organization's managed infrastructure spending, what percentage of the spending is allocated to each of the following? Please sum to 100%. [Sum to 100%]

13

Infrastructure Services

16% 14%22% 17%

9%17%

84% 86%78% 83%

91%83%

Total (n=1738) NA (n=950) WE (n=330) APAC (n=316) LA (n=95) MEA (n=47)0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

% o

f Res

pond

ents

Next Engagement by Region

Managed/BundledUnmanaged

I1e. For your organization's next hosting and cloud infrastructure engagement, will the service be unmanaged (purchased without value-added managed services or security services) or managed (bundled with managed or security services)?

14

Infrastructure Services31%

28%

25%

15%

33%

26%

23%

17%

29%

34%

24%

13%

29%

29%

29%

13%

28%

29%

29%

13%

21%

23%

38%

17%

0% 10% 20% 30% 40% 50%

We will focus primarily on a single cloud environment, not multiple clouds

We will have multiple different cloud environments, but there will be little to nointeroperability between the cloud en

We will have multiple cloud environments to migrate workloads or data betweendifferent cloud environments

We will have multiple cloud environments where the delivery of a single businessfunction across the different cloud env

% of Respondents

Cloud Environments Next 2 Years by Region

Total (n=1738)

NA (n=950)

WE (n=330)

APAC (n=316)

LA (n=95)

MEA (n=47)

I2. Which of the following statements best describes how your organization will use different on-premises and off-premises cloudenvironments over the next 2 years?

15

Infrastructure Services

76% 79% 74%67%

78% 77%

19% 16% 19%28%

17% 19%

Total (n=1738) NA (n=950) WE (n=330) APAC (n=316) LA (n=95) MEA (n=47)0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

% o

f Res

pond

ents

Have On-Premise Private Cloud by Region

No

Yes

I3. Does your organization currently have an on-premises private cloud? This is where IT resources in your company owned or operated datacenter are pooled using a cloud platform with policy-based automation and orchestration for delivery.

16

Infrastructure Services64%

57%

55%

49%

18%

16%

65%

59%

63%

51%

18%

15%

64%

54%

38%

42%

11%

10%

61%

59%

56%

57%

22%

18%

56%

50%

38%

24%

24%

29%

71%

53%

35%

53%

24%

35%

0% 10% 20% 30% 40% 50% 60% 70% 80%

On-premises private cloud with a hosted private cloud

On-premises private cloud with a public cloud/IaaS platform

Hosted private cloud with a public cloud/IaaS platform

Public cloud/IaaS platform with a different public cloud/IaaSplatform

Non-cloud environment with a public cloud/IaaS platform

Non-cloud environment with a hosted private cloud

None of the Above

% of Respondents

Cloud Deployment Interoperability

Total (n=554)

NA (n=305)

WE (n=96)

APAC (n=102)

LA (n=34)

MEA (n=17)

Note: Caution is advised when interpreting segments with small sample sizes.

I4. Has your organization configured any of the following cloud deployments for interoperability for the seamless delivery of a business function or to migrate workloads between different cloud environments? Please select all that apply.

17

Infrastructure Services64%

56%

56%

49%

49%

47%

44%

40%

63%

58%

52%

48%

48%

47%

42%

41%

70%

50%

57%

44%

49%

48%

40%

35%

68%

57%

64%

55%

55%

41%

56%

44%

47%

56%

71%

50%

47%

53%

32%

32%

53%

47%

35%

65%

29%

53%

65%

47%

0% 10% 20% 30% 40% 50% 60% 70% 80%

Flexibility and choice: applications/workloads can operate in the mostappropriate IT environment based on security, data residency, application

workload characteristics, end user demand/traffic, etc.

Extend the IT resource capacity of existing on-premises infrastructurewithout capital expense

Maximize return on existing on-premises IT investments for existingapplications/workloads, but use public cloud/IaaS for new

applications/workloads

Establish the right balance between speed/agility/innovation andsecurity/risk

Migrate workloads as needed between private/public cloud and on-premises/off-premises environments

Integrate core business systems and data ("systems of record") to enableinteraction with customer-/end user-facing digital initiatives ("systems of

engagement")

Support the development lifecycle: private cloud for production and publiccloud for development/test

Need for an off-site location for backup /disaster recovery/businesscontinuity

% of Respondents

Adoption Drivers of Hybrid/Multi-Cloud Environments

Total (n=550)

NA (n=303)

WE (n=94)

APAC (n=102)

LA (n=34)

MEA (n=17)

I5. Which of the following factors are driving your organization's adoption/usage of hybrid/multi-cloud environments? Please select all that apply.

Note: Caution is advised when interpreting segments with small sample sizes.

18

Infrastructure Services61%

53%

46%

43%

33%

65%

56%

53%

47%

39%

62%

39%

29%

39%

24%

57%

56%

47%

39%

25%

56%

48%

33%

41%

41%

43%

86%

29%

36%

21%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Microsoft Azure

Google Cloud Platform

Amazon Web Services (AWS)

IBM SoftLayer

VMware vCloud Air

Other

Don't Know

% of Respondents

Public Cloud/IaaS Provider by Region

Total (n=480)

NA (n=262)

WE (n=82)

APAC (n=95)

LA (n=27)

MEA (n=14)

I7. You previously mentioned that you use a public cloud/IaaS platform as part of your hybrid/multi-cloud environment. Which public cloud/IaaS provider(s) are you using? Please select all that apply.

Note: Caution is advised when interpreting segments with small sample sizes.

19

Infrastructure Services41%

30%

16%

13%

44%

28%

16%

11%

34%

35%

10%

20%

28%

36%

19%

16%

56%

19%

26%

64%

7%

14%

14%

0% 10% 20% 30% 40% 50% 60% 70% 80%

Self-built and managed using our own IT staffand hardware/software investments

Service provider-/vendor-built and self-managed

Self-built, but service provider-/vendor managed

Service provider-/vendor-built and managed

Other

% of Respondents

Hybrid/Multi-Cloud Environment Management by Region

Total (n=480)

NA (n=262)

WE (n=82)

APAC (n=95)

LA (n=27)

MEA (n=14)

I8a. How is your organization implementing and managing your hybrid cloud/multi-cloud environment?

Note: Caution is advised when interpreting segments with small sample sizes.

20

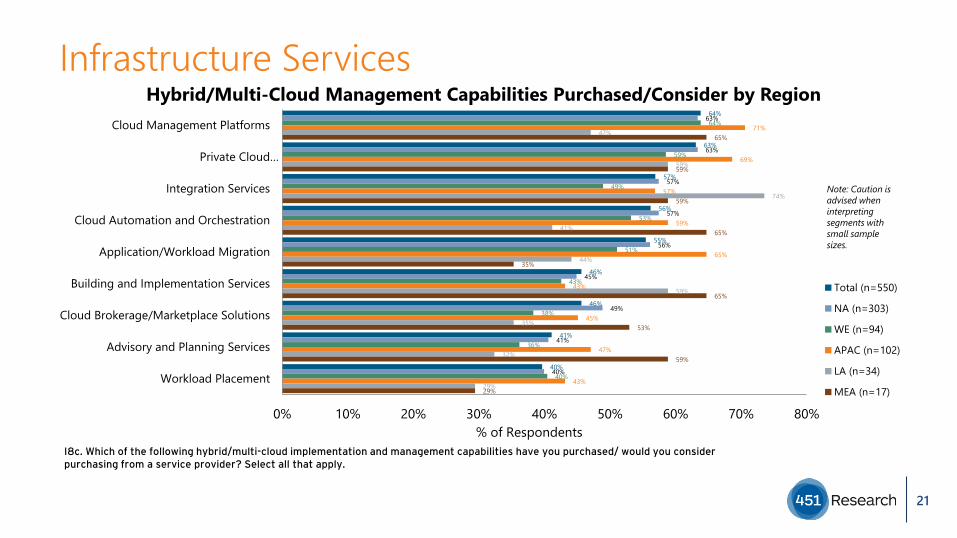

Infrastructure Services64%

63%

57%

56%

55%

46%

46%

41%

40%

63%

63%

57%

57%

56%

45%

49%

41%

40%

64%

59%

49%

53%

51%

43%

38%

36%

40%

71%

69%

57%

59%

65%

43%

45%

47%

43%

47%

59%

74%

41%

44%

59%

35%

32%

29%

65%

59%

59%

65%

35%

65%

53%

59%

29%

0% 10% 20% 30% 40% 50% 60% 70% 80%

Cloud Management Platforms

Private Cloud…

Integration Services

Cloud Automation and Orchestration

Application/Workload Migration

Building and Implementation Services

Cloud Brokerage/Marketplace Solutions

Advisory and Planning Services

Workload Placement

% of Respondents

Hybrid/Multi-Cloud Management Capabilities Purchased/Consider by Region

Total (n=550)

NA (n=303)

WE (n=94)

APAC (n=102)

LA (n=34)

MEA (n=17)

I8c. Which of the following hybrid/multi-cloud implementation and management capabilities have you purchased/ would you considerpurchasing from a service provider? Select all that apply.

Note: Caution is advised when interpreting segments with small sample sizes.

21

Infrastructure Services

89% 91%83%

93%85% 82%

8% 7%14%

3% 12% 12%

Total (n=549) NA (n=302) WE (n=94) APAC (n=102) LA (n=34) MEA (n=17)0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

% o

f Res

pond

ents

Pay Premium for Service Provider Hybrid/Multi Cloud Mgt Services by Region

Don'tknowNo

I8d. Would your organization expect to pay a premium for a service provider's hybrid/multi-cloud implementation and management services?

Note: Caution is advised when interpreting segments with small sample sizes.

22

Infrastructure Services57%

55%

53%

51%

51%

41%

39%

36%

33%

31%

53%

54%

54%

53%

50%

43%

39%

36%

35%

33%

56%

49%

37%

40%

41%

33%

35%

24%

35%

23%

65%

65%

65%

58%

57%

42%

43%

44%

29%

31%

59%

45%

45%

45%

52%

24%

34%

34%

24%

34%

71%

64%

50%

64%

71%

71%

43%

43%

21%

21%

0% 10% 20% 30% 40% 50% 60% 70% 80%

Managed Service Provider (MSP)/Managed Hosting Provider

Public Cloud Infrastructure as a Service (IaaS) Provider

Security Service Provider

Consulting/IT Outsourcing/Systems Integrator

Cloud Enablement and Management Specialist

Hardware Vendor/OEM

Independent Software Vendor (ISV)

Telecommunications Provider

Value Added Reseller (VAR)

Cloud Broker

% of Respondents

Hybrid/Multi-Cloud Management Capabilities Service Providers Consider by Region

Total (n=490)

NA (n=274)

WE (n=78)

APAC (n=95)

LA (n=29)

MEA (n=14)

I8e. What types of service providers does or would your organization look to for hybrid/multi-cloud implementation and management capabilities? Select all that apply.

Note: Caution is advised when interpreting segments with small sample sizes.

23

Infrastructure Services

39%

36%

26%

39%

38%

23%

47%

26%

28%

31%

37%

31%

35%

35%

29%

53%

29%

18%

0% 10% 20% 30% 40% 50% 60% 70%

Individual best-of-breed services purchasedfrom multiple providers/vendors that we

implement and manage ourselves

Integrated multi-vendor solution built andmanaged by a single provider/vendor ('one

throat to choke')

Pre-packaged, pre-configured serviceprovider solution built and managed by a

service provider

% of Respondents

Hybrid/Multi-Cloud Management Capabilities Acquisition Preference by Region

Total (n=549)

NA (n=302)

WE (n=94)

APAC (n=102)

LA (n=34)

MEA (n=17)

I8f. Which of the following best describes how your organization would like to obtain hybrid/multi-cloud implementation and management services?

Note: Caution is advised when interpreting segments with small sample sizes.

24

Infrastructure Services

44%50%

39%28%

50% 50%

28%25%

19% 45%

27%33%

19% 14%

33%

20%19%

17%4% 4% 6% 3%5% 6% 4% 5% 4%

Total (n=442) NA (n=247) WE (n=70) APAC (n=87) LA (n=26) MEA (n=12)0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

% o

f Res

pond

ents

Public Cloud/IaaS Bursting Capability Plans by Region

No plans tousePlan to use in1-2 yearsPlan to use in12 monthsPlan to use in6 monthsCurrently Use

I9. Does your organization currently use or plan to use public cloud/IaaS for bursting capabilities, meaning that an application/workload running in a private cloud or non-cloud environment "bursts" into a public cloud when demand for capacity spikes?

Note: Caution is advised when interpreting segments with small sample sizes.

25

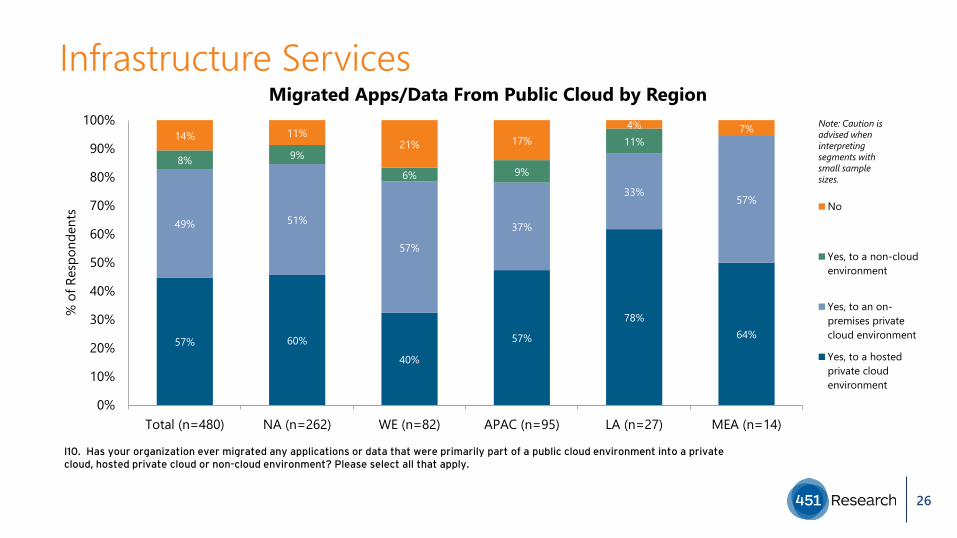

Infrastructure Services

57% 60%

40%

57%

78%64%

49% 51%

57%

37%

33%57%

8% 9%

6% 9%

11%14% 11%21% 17%

4% 7%

Total (n=480) NA (n=262) WE (n=82) APAC (n=95) LA (n=27) MEA (n=14)0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

% o

f Res

pond

ents

Migrated Apps/Data From Public Cloud by Region

No

Yes, to a non-cloudenvironment

Yes, to an on-premises privatecloud environment

Yes, to a hostedprivate cloudenvironment

I10. Has your organization ever migrated any applications or data that were primarily part of a public cloud environment into a private cloud, hosted private cloud or non-cloud environment? Please select all that apply.

Note: Caution is advised when interpreting segments with small sample sizes.

26

Infrastructure Services20%

16%

15%

14%

12%

7%

6%

5%

5%

20%

19%

13%

11%

13%

7%

6%

6%

6%

14%

12%

23%

17%

11%

11%

6%

2%

5%

24%

14%

10%

22%

9%

6%

5%

8%

3%

27%

12%

27%

19%

4%

4%

8%

23%

15%

38%

15%

8%

0% 10% 20% 30% 40%

Security

Part of an IT Centralization…

Better Control

Performance

Enhanced Capabilities/Functionality

We Only use Public Cloud/IaaS for…

Lower Cost

Availability

Customer Service Issues

% of Respondents

Hybrid/Multi-Cloud Management Capabilities Acquisition Preference by Region

Total (n=415)

NA (n=232)

WE (n=65)

APAC (n=79)

LA (n=26)

MEA (n=13)

I11. What was the primary driver for migrating workloads from a public cloud to a private cloud, hosted private cloud or non-cloud environment?

Note: Caution is advised when interpreting segments with small sample sizes.

27

MANAGED SERVICES (M)

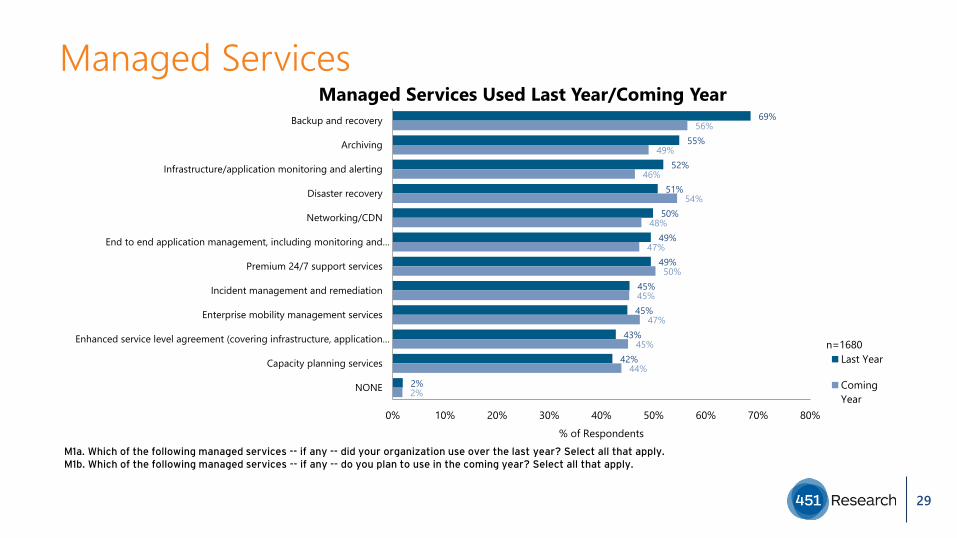

Managed Services69%

55%

52%

51%

50%

49%

49%

45%

45%

43%

42%

2%

56%

49%

46%

54%

48%

47%

50%

45%

47%

45%

44%

2%

0% 10% 20% 30% 40% 50% 60% 70% 80%

Backup and recovery

Archiving

Infrastructure/application monitoring and alerting

Disaster recovery

Networking/CDN

End to end application management, including monitoring and…

Premium 24/7 support services

Incident management and remediation

Enterprise mobility management services

Enhanced service level agreement (covering infrastructure, application…

Capacity planning services

NONE

% of Respondents

Managed Services Used Last Year/Coming Year

Last Year

ComingYear

n=1680

M1a. Which of the following managed services -- if any -- did your organization use over the last year? Select all that apply. M1b. Which of the following managed services -- if any -- do you plan to use in the coming year? Select all that apply.

29

Managed Services

0% 10% 20% 30% 40% 50% 60% 70% 80% 90%

Backup and recovery

Archiving

Infrastructure/application monitoring and alerting

Disaster recovery

Networking/CDN

End to end application management, including…

Premium 24/7 support services

Incident management and remediation

Enterprise mobility management services

Enhanced service level agreement (covering…

Capacity planning services

NONE

% of Respondents

Managed Services Used Last Year by Region

Total (n=1668)

NA (n=920)

WE (n=309)

APAC (n=298)

LA (n=94)

MEA (n=47)

M1a. Which of the following managed services -- if any -- did your organization use over the last year? Select all that apply.

30

Managed Services

0% 10% 20% 30% 40% 50% 60% 70% 80% 90%

Backup and recovery

Disaster recovery

Premium 24/7 support services

Archiving

Networking/CDN

Enterprise mobility management services

End to end application management, including…

Infrastructure/application monitoring and alerting

Incident management and remediation

Enhanced service level agreement (covering…

Capacity planning services

NONE

% of Respondents

Managed Services Used Coming Year by Region

Total (n=1668)

NA (n=920)

WE (n=309)

APAC (n=298)

LA (n=94)

MEA (n=47)

M1b. Which of the following managed services -- if any -- do you plan to use in the coming year? Select all that apply.

31

PROFESSIONAL SERVICES FOR CLOUD ENABLEMENT (Z)

Professional Services63%

56%

53%

48%

7%

60%

58%

54%

53%

5%

0% 10% 20% 30% 40% 50% 60% 70% 80%

Cloud Integration Services

Cloud Migration Services

Cloud Assessment, Readiness and EnablementServices

Cloud Transformation Services

NONE

% of Respondents

Cloud Professional Services Used Last Year/Coming Year

Last Year

Coming Year

n=1599

Z1a. Which of the following cloud professional services does your organization use -- if any -- did your organization use over the last year? Select all that apply.Z1b. Which of the following cloud professional services does your organization use -- if any -- do you plan to use in the coming year? Select all that apply.

33

Professional Services63%

56%

53%

48%

7%

65%

57%

56%

51%

4%

57.0%

54.0%

42.0%

41.3%

11.7%

59%

56%

55%

46%

10%

73%

66%

62%

48%

71%

36%

49%

60%

4%

0% 10% 20% 30% 40% 50% 60% 70% 80%

Cloud Integration Services

Cloud Migration Services

Cloud Assessment, Readiness andEnablement Services

Cloud Transformation Services

NONE

% of Respondents

Cloud Professional Services Used Last Year by Region

Total (n=1599)

NA (n=876)

WE (n=300)

APAC (n=287)

LA (n=91)

MEA (n=45)

Z1a. Which of the following cloud professional services does your organization use -- if any -- did your organization use over the last year? Select all that apply.

34

Professional Services60%

58%

54%

53%

5%

59%

58%

54%

53%

3%

58.3%

53.3%

43.7%

49.0%

8.3%

62%

59%

61%

57%

8%

68%

65%

54%

54%

7%

71%

58%

69%

60%

4%

0% 10% 20% 30% 40% 50% 60% 70% 80%

Cloud Integration Services

Cloud Migration Services

Cloud Assessment, Readiness andEnablement Services

Cloud Transformation Services

NONE

% of Respondents

Cloud Professional Services Use Coming Year by Region

Total(n=1599)NA (n=876)

WE (n=300)

APAC (n=287)

LA (n=91)

Z1b. Which of the following cloud professional services does your organization use -- if any -- do you plan to use in the coming year? Select all that apply.

35

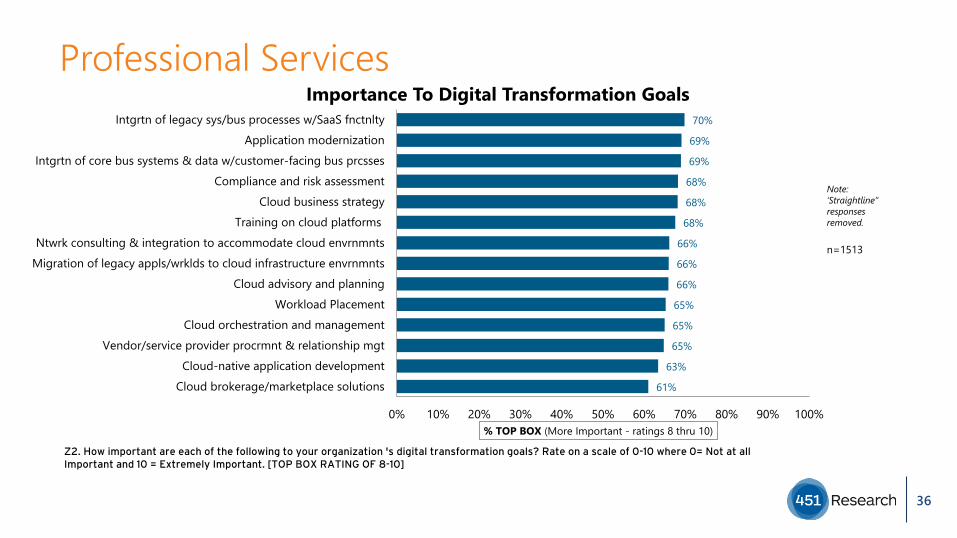

Professional Services70%

69%

69%

68%

68%

68%

66%

66%

66%

65%

65%

65%

63%

61%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Intgrtn of legacy sys/bus processes w/SaaS fnctnltyApplication modernization

Intgrtn of core bus systems & data w/customer-facing bus prcssesCompliance and risk assessment

Cloud business strategyTraining on cloud platforms

Ntwrk consulting & integration to accommodate cloud envrnmntsMigration of legacy appls/wrklds to cloud infrastructure envrnmnts

Cloud advisory and planningWorkload Placement

Cloud orchestration and managementVendor/service provider procrmnt & relationship mgt

Cloud-native application developmentCloud brokerage/marketplace solutions

% TOP BOX (More Important - ratings 8 thru 10)

Importance To Digital Transformation Goals

n=1513

Z2. How important are each of the following to your organization 's digital transformation goals? Rate on a scale of 0-10 where 0= Not at all Important and 10 = Extremely Important. [TOP BOX RATING OF 8-10]

Note: ‘Straightline” responses removed.

36

Professional Services

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Intgrtn of legacy sys/bus processes w/SaaS fnctnltyApplication modernization

Intgrtn of core bus systems & data w/customer-facing bus prcssesCompliance and risk assessment

Cloud business strategyTraining on cloud platforms

Ntwrk consulting & integration to accommodate cloud envrnmntsMigration of legacy appls/wrklds to cloud infrastructure envrnmnts

Cloud advisory and planningWorkload Placement

Cloud orchestration and managementVendor/service provider procrmnt & relationship mgt

Cloud-native application developmentCloud brokerage/marketplace solutions

% TOP BOX (More Important - ratings 8 thru 10)

Importance To Digital Transformation Goals by Region

Total (n=1513)

NA (n=851)

WE (n=274)

APAC (n=262)

LA (n=83)

MEA (n=43)

Z2. How important are each of the following to your organization 's digital transformation goals? Rate on a scale of 0-10 where 0= Not at all Important and 10 = Extremely Important. [TOP BOX RATING OF 8-10]

Note: ‘Straightline” responses removed.

37

Professional Services

12% 15%9% 10% 7% 3%

14%15% 24%

4% 12%13%

16%16%

23%

9%4%

38%

19%19%

19%

19%22%

21%17%

18%

13%

16%

30%

13%11%

10%7%

16%

10%

8%11% 8% 4%

28%

13%5%

Total (n=1282) NA (n=732) WE (n=217) APAC (n=227) LA (n=67) MEA (n=39)0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

% o

f Res

pond

ents

Most Recent Professional Services Cloud Project Spend by Region

$2mil+

$500,000-<$2mil$100,000-$499,999$25,000-$99,999$5,000-$24,999

$1,000-$4,999

<$1,000

Z3. How much did your organization spend on your most recent professional services for cloud enablement project? Please enter a US dollar value. [OPEN NUMERIC]

38

Professional Services

11% 12% 6%13% 11% 12%

22% 24%20%

18% 20% 19%

25% 24%30% 25% 22% 21%

21% 23%23% 19%

16%14%

7% 6% 7%8% 14%

5%

14% 12% 14% 18% 16%30%

Total (n=1391) NA (n=778) WE (n=236) APAC (n=255) LA (n=79) MEA (n=43)0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

% o

f Res

pond

ents

Most Recent Professional Services Cloud Project Duration by Region

More than 24weeks17-24 weeks

9-16 weeks

5-8 weeks

3-4 weeks

1-2 weeks

Average Weeks 13 12 12 14 14 20

Z4. What was the duration (WEEKS) of your organization 's most recent professional services for cloud enablement project? ________ Weeks [OPEN NUMERIC]

39

Professional Services

0% 10% 20% 30%

Public Cloud Infrastructure as a Service (IaaS) Provider

Cloud Enablement and Management Specialist

Managed Service Provider (MSP)/Managed Hosting…

Consulting/IT Outsourcing/Systems Integrator

Security Service Provider

Independent Software Vendor (ISV)

Hardware Vendor/OEM

Telecommunications Provider

Value Added Reseller (VAR)

Cloud Broker

% of Respondents

Total (n=1541)

NA (n=859)

WE (n=279)

APAC (n=269)

LA (n=89)

MEA (n=45)

Most Recent Professional Services Cloud Project Vendor by Region

Z5. Which of the following best describes the type of service provider/vendor your organization used for your most recent professional services for cloud project? Select one.

40

APPLICATION HOSTING (A)

Application Services58%

55%

53%

51%

48%

45%

45%

44%

43%

42%

42%

41%

39%

38%

32%

52%

49%

47%

45%

45%

44%

44%

43%

43%

45%

40%

45%

40%

42%

37%

0% 10% 20% 30% 40% 50% 60% 70%

File storageWebsite hosting and web presence

Database and data warehousingEmail, collaboration & productivity apps for…

CRMData analytics/Business intelligence/Big Data

Industry-specific applicationsApp development (tools, platforms & DevOps)

ERPEcommerce

Media streaming and digital publishingSocial applications

Engineering/R&D/Technical computingVDI and mobility management

Other line of business (LOB) applicationsNONE

% of Respondents

Hosted Applications Used Last Year/Coming Year

Last Year

Coming Year

n=1673

A1a. Which of the following hosted applications - if any -- did your organization use over the last year? Select all that apply. A1b. Which of the following hosted applications -- if any -- do you plan to use in the coming year? Select all that apply.

42

Application Services

0% 10% 20% 30% 40% 50% 60% 70% 80%

File storageWebsite hosting and web presence

Database and data warehousingEmail, collaboration & productivity apps for…

CRMData analytics/Business intelligence/Big Data

Industry-specific applicationsApp development (tools, platforms & DevOps)

ERPEcommerce

Media streaming and digital publishingSocial applications

Engineering/R&D/Technical computingVDI and mobility management

Other line of business (LOB) applicationsNONE

% of Respondents

Hosted Applications Used Last Year by Region

Total (n=1673)

NA (n=911)

WE (n=319)

APAC (n=303)

LA (n=93)

MEA (n=47)

A1a. Which of the following hosted applications - if any -- did your organization use over the last year? Select all that apply.

43

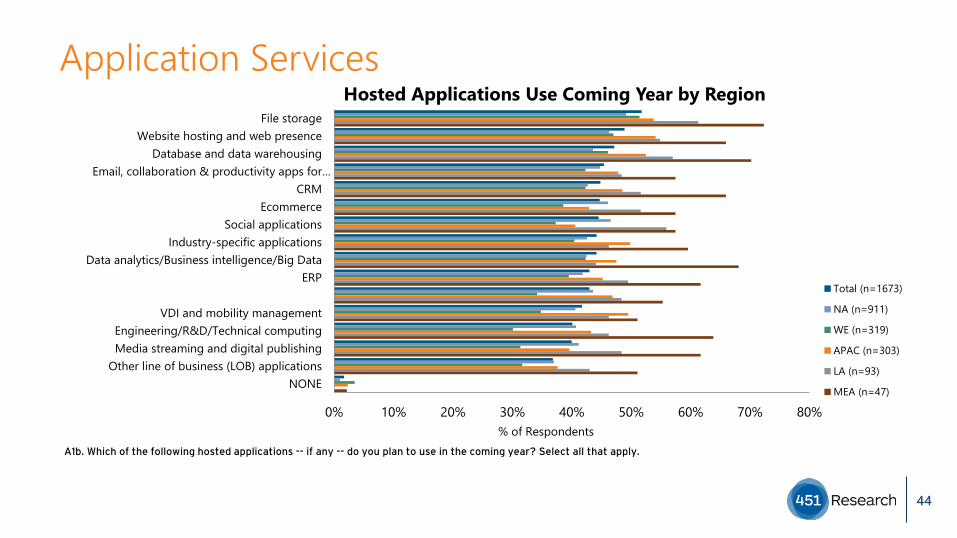

Application Services

0% 10% 20% 30% 40% 50% 60% 70% 80%

File storageWebsite hosting and web presence

Database and data warehousingEmail, collaboration & productivity apps for…

CRMEcommerce

Social applicationsIndustry-specific applications

Data analytics/Business intelligence/Big DataERP

VDI and mobility managementEngineering/R&D/Technical computingMedia streaming and digital publishing

Other line of business (LOB) applicationsNONE

% of Respondents

Hosted Applications Use Coming Year by Region

Total (n=1673)

NA (n=911)

WE (n=319)

APAC (n=303)

LA (n=93)

MEA (n=47)

A1b. Which of the following hosted applications -- if any -- do you plan to use in the coming year? Select all that apply.

44

58%

48%

53%

54%

51%

52%

42%

52%

47%

46%

49%

48%

MEA (n=47)

LA (n=95)

APAC (n=316)

WE (n=330)

NA (n=950)

Total (n=1738)

0% 20% 40% 60% 80% 100%Average %

Application Allocation Today to Third-Party Vs. Internal by Region

Operate/manageinternally

59%

57%

52%

54%

51%

52%

41%

43%

48%

46%

49%

48%

MEA(n=47)

LA (n=95)

APAC(n=316)

WE(n=330)

NA(n=950)

Total(n=1738)

0% 20% 40% 60% 80% 100%

Average %

Application Allocation In 2 Yrs to Third-Party Vs. Internal by Region

Operate/manage internally

Use a ServiceProvider foroperations/management

45

A2a. Thinking about all of your organization's applications, today, what percentage of these would you look to a third-party provider to operate and manage and what percentage would you continue to operate and manage internally? Sum to 100%A2b. Thinking about all of your organization's applications, 2 years from now, what percentage of these would you look to a third-party provider to operate and manage and what percentage would you continue to operate and manage internally?

Application Services

SECURITY SERVICES (E)

Security Services62%

53%

52%

52%

51%

49%

47%

46%

46%

45%

45%

55%

51%

51%

50%

50%

46%

47%

48%

45%

45%

44%

0% 10% 20% 30% 40% 50% 60% 70%

Anti-virus/endpoint security

Web app firewall (WAF)

Data encryption/encryption services

Data loss prevention (DLP)

App security (including patching & firewall mgt)

Advanced anti-malware or advanced persistent threat (APT)…

Security config mgt (including endpoint security)

Vulnerability assessment

Identity and access management (IAM)

IT governance, risk & compliance (GRC) functions

Security info & event mgt (SIEM) & logging/event mgt

NONE

% of Respondents

Security Services Used Last Year/Coming Year

Last Year

Coming Year

n=1673

E1a. Which of the following security services -- if any -- did your organization use over the last year? Select all that apply.E1b. Which of the following security services -- if any -- do you plan to use in the coming year? Select all that apply.

47

Security Services

0% 10% 20% 30% 40% 50% 60% 70% 80% 90%

Anti-virus/endpoint security

Web app firewall (WAF)

Data encryption/encryption services

Data loss prevention (DLP)

App security (including patching & firewall mgt)

Advanced anti-malware or advanced persistent threat (APT)…

Security config mgt (including endpoint security)

Vulnerability assessment

Identity and access management (IAM)

IT governance, risk & compliance (GRC) functions

Security info & event mgt (SIEM) & logging/event mgt

NONE

% of Respondents

Security Services Used Last Year by Region

Total (n=1666)

NA (n=912)

WE (n=311)

APAC (n=301)

LA (n=95)

MEA (n=47)

E1a. Which of the following security services -- if any -- did your organization use over the last year? Select all that apply.

48

Security Services

0% 10% 20% 30% 40% 50% 60% 70% 80%

Anti-virus/endpoint security

Data encryption/encryption services

Web app firewall (WAF)

Data loss prevention (DLP)

App security (including patching & firewall mgt)

Vulnerability assessment

Security config mgt (including endpoint security)

Advanced anti-malware or advanced persistent threat (APT)…

IT governance, risk & compliance (GRC) functions

Identity and access management (IAM)

Security info & event mgt (SIEM) & logging/event mgt

NONE

% of Respondents

Security Services Use Next Year by Region

Total (n=1666)

NA (n=912)

WE (n=311)

APAC (n=301)

LA (n=95)

MEA (n=47)

E1b. Which of the following security services -- if any -- do you plan to use in the coming year? Select all that apply.

49

Transformation (C)

Business Transformation

9% 10% 9% 8% 5% 4%

14%18%

8% 13%

4% 9%

29%29%

27%30%

41%

19%

38% 34%

45%41% 40%

64%

9% 9% 10% 7% 9%4%

Total (n=1738) NA (n=950) WE (n=330) APAC (n=316) LA (n=95) MEA (n=47)0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

% o

f Res

pond

ents

Business Transition Descriptor by Region

Other

Transitioning

Staying theCourseUnderReinventionMarket Maker

MarketDisrupter

C1. Which of the following best describes your organization? (Randomize Select one.)

51

Business Transformation

24 24 23 26 27 30

23 22 23 23 25 20

19 19 20 1919 20

17 18 17 1616 16

16 17 16 16 13 14

Total (n=1738) NA (n=950) WE (n=330) APAC (n=316) LA (n=95) MEA (n=47)

Relative Company Goals

Increaserevenue

Improveproduct orservice qualityLower costs

C3. Allocate 100 points among the following five goals to their relative importance within your company or organization? [Sum to 100]

52

Business Transformation27%

15%

14%

13%

13%

11%

7%

0%

0% 5% 10% 15% 20% 25% 30%

Improve marketing/promotion of products andservices

Compete aggressively to increase market share

Target Cross-sell/Up-sell opportunities within clientbase

Expand geographically

Hire quality staff

Optimize Pricing

Enter into adjacent lines of business

Other

% of Respondents

Most Important Attribute to Increase Revenue by Region

Total (n=1067)

NA (n=555)

WE (n=202)

APAC (n=205)

LA (n=69)

MEA (n=36)

C4. Based on what you have heard, which of the following will be the primary strategy for your organization to increase revenue over the next two years? (Select one)

53

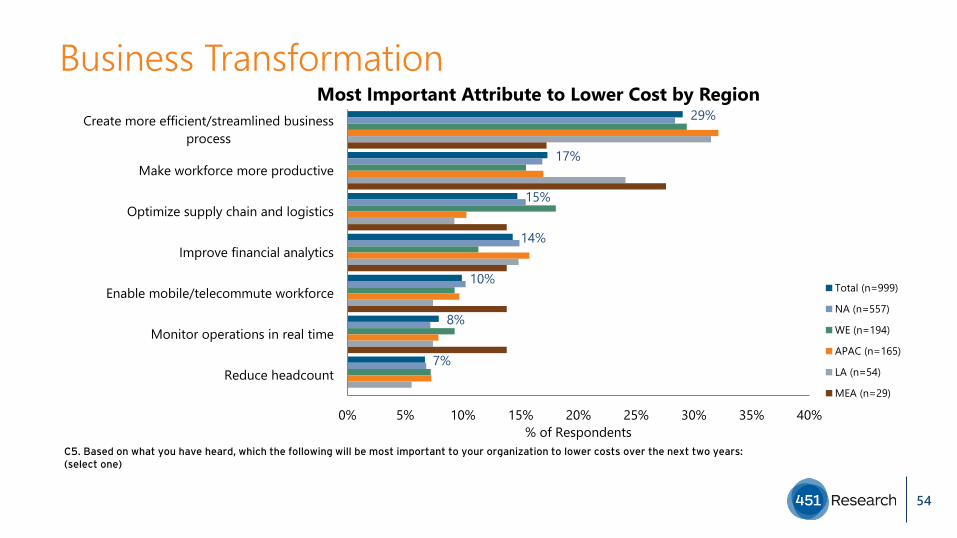

Business Transformation29%

17%

15%

14%

10%

8%

7%

0% 5% 10% 15% 20% 25% 30% 35% 40%

Create more efficient/streamlined businessprocess

Make workforce more productive

Optimize supply chain and logistics

Improve financial analytics

Enable mobile/telecommute workforce

Monitor operations in real time

Reduce headcount

% of Respondents

Most Important Attribute to Lower Cost by Region

Total (n=999)

NA (n=557)

WE (n=194)

APAC (n=165)

LA (n=54)

MEA (n=29)

C5. Based on what you have heard, which the following will be most important to your organization to lower costs over the next two years: (select one)

54

Business Transformation21%

13%

12%

11%

10%

8%

8%

6%6%

5%

0% 5% 10% 15% 20% 25% 30%

Innovate or deliver new products or services

Find, develop and retain talent

Focus on customer convenience

Single customer experience across digital and physical…

Personalize customer experience

Use analytics to predict or recover from errors

Deliver digital products (vs physical products)

Build online communities

Tracking digital identities of customers

Offer self-service products/services

% of Respondents

Most Important Attribute to Improve Product or Service Quality by Region

Total (n=1044)

NA (n=536)

WE (n=207)

APAC (n=204)

LA (n=69)

MEA (n=28)

C6. Based on what you have heard, which the following will be most important to your organization to improve product or service quality over the next two years: (select one)

Note: Caution is advised when interpreting segments with small sample sizes.

55

Business Transformation19%

15%

15%

14%

14%

13%

10%

0% 5% 10% 15% 20% 25% 30%

Improve production processes

Use data to drive strategic decision making

Automate business processes

Encourage knowledge sharing & collaborationamong employees

Invest in research and development

Integrate customer feedback through communitiesor analytics

Cultivate a culture of risk taking (where failure is avalid outcome) to accelerate development

% of Respondents

Most Important Attribute to Speed Time to Market by Region

Total (n=984)

NA (n=570)

WE (n=186)

APAC (n=163)

LA (n=44)

MEA (n=21)

C7. Based on what you have heard, which the following will be most important to your organization to speed time to market over the next two years: (select one)

Note: Caution is advised when interpreting segments with small sample sizes.

56

Business Transformation25%

22%

19%

18%

16%

0% 5% 10% 15% 20% 25% 30% 35% 40%

Identify threats in business exposure orcompetition

Analytics to recognize risks sooner

Focus on reducing Cybersecurity attacks

Minimize risk making decisions with data

Building Digital Trust competencies

% of Respondents

Most Important Attribute to Lower Risk by Region

Total (n=983)

NA (n=559)

WE (n=175)

APAC (n=183)

LA (n=43)

MEA (n=23)

C8. Based on what you have heard, which the following will be most important to your organization to lower risk over the next two years: (select one)

Note: Caution is advised when interpreting segments with small sample sizes.

57

Digital Investment

3% 3% 3% 4% 6%

28% 24%

39% 35%

14%

21%

69% 73%

58% 61%

85%

72%

Total (n=1738) NA (n=950) WE (n=330) APAC (n=316) LA (n=95) MEA (n=47)0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

% o

f Res

pond

ents

Digital Investment Importance by Region

Top Box (MoreImportant:Ratings 8-10)

Middle(Ratings 5-7)

Bottom Box(LessImportant:Ratings 0-4)

C8a. Rate the overall importance of digital investment in achieving your organization's business transformation objectives on a scale of 0 to 10 where 0 is Not at All Important and 10 is Extremely Important.Digital investment here refers to funding for IT and IT-related initiatives. These could be led by IT or by a business unit using technology.

58

Digital Investment

12%

6%

6%

4%

6%

4%

40%

43%

41%

42%

37%

38%

31%

49%

51%

53%

54%

57%

58%

69%

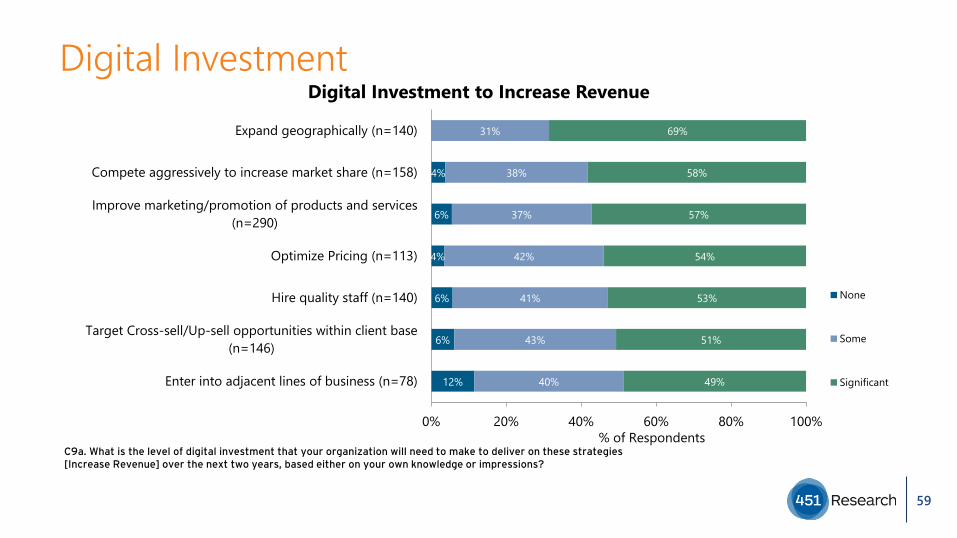

Enter into adjacent lines of business (n=78)

Target Cross-sell/Up-sell opportunities within client base(n=146)

Hire quality staff (n=140)

Optimize Pricing (n=113)

Improve marketing/promotion of products and services(n=290)

Compete aggressively to increase market share (n=158)

Expand geographically (n=140)

0% 20% 40% 60% 80% 100%% of Respondents

Digital Investment to Increase Revenue

None

Some

Significant

C9a. What is the level of digital investment that your organization will need to make to deliver on these strategies [Increase Revenue] over the next two years, based either on your own knowledge or impressions?

59

Digital Investment

10%

9%

5%

3%

3%

49%

39%

42%

42%

39%

38%

37%

40%

52%

53%

55%

58%

59%

60%

Reduce headcount (n=67)

Enable mobile/telecommute workforce (n=99)

Monitor operations in real time (n=79)

Optimize supply chain and logistics (n=147)

Make workforce more productive (n=173)

Improve financial analytics (n=143)

Create more efficient/streamlined business process(n=290)

0% 20% 40% 60% 80% 100%% of Respondents

Digital Investment to Lower Costs

None

Some

Significant

C9b. What is the level of digital investment that your organization will need to make to deliver on these strategies [Lower Costs] over the next two years, based either on your own knowledge or impressions?

60

Digital Investment

4%

4%

5%

3%

3%

3%

52%

49%

42%

42%

39%

41%

39%

38%

32%

28%

46%

47%

55%

56%

56%

57%

59%

59%

66%

70%

Tracking digital identities of customers (n=63)

Offer self-service products/services (n=51)

Use analytics to predict or recover from errors (n=84)

Build online communities (n=66)

Find, develop and retain talent (n=135)

Focus on customer convenience (n=129)

Single cstmr exprnce across digital & physical srvcs/devices/pltfrms…

Personalize customer experience (n=102)

Deliver digital products (vs physical products) (n=79)

Innovate or deliver new products or services (n=224)

0% 20% 40% 60% 80% 100%% of Respondents

Digital Investment to Improve Product or Service Quality

None

Some

Significant

C9c. What is the level of digital investment that your organization will need to make to deliver on these strategies [Improve Product or Service Quality] over the next two years, based either on your own knowledge or impressions?

61

Digital Investment

6%

4%

39%

41%

40%

39%

38%

34%

37%

55%

56%

58%

59%

60%

62%

63%

Cultivate a culture of risk taking...to accelerate development (n=101)

Encourage knowledge sharing & collaboration among employees(n=135)

Invest in research and development (n=133)

Integrate customer feedback through communities or analytics(n=132)

Automate business processes (n=145)

Use data to drive strategic decision making (n=149)

Improve production processes (n=189)

0% 20% 40% 60% 80% 100%% of Respondents

Digital Investment to Speed Time to Market

None

Some

Significant

C9d. What is the level of digital investment that your organization will need to make to deliver on these strategies [Speed Time to Market] over the next two years, based either on your own knowledge or impressions?

62

Digital Investment

42%

41%

38%

36%

27%

56%

58%

60%

62%

71%

Minimize risk making decisions with data (n=177)

Analytics to recognize risks sooner (n=217)

Building Digital Trust competencies (n=162)

Identify threats in business exposure or competition(n=241)

Focus on reducing Cybersecurity attacks (n=186)

0% 20% 40% 60% 80% 100%% of Respondents

Digital Investment to Lower Risk

None

Some

Significant

C9e. What is the level of digital investment that your organization will need to make to deliver on these strategies [Lower Risk] over the next two years, based either on your own knowledge or impressions?

63

Digital Investment

3%

3%

4%

4%

25%

24%

20%

26%

25%

26%

19%

51%

42%

50%

44%

44%

45%

45%

24%

28%

26%

24%

27%

26%

29%

4%

4%

3%

Expand geographically (n=140)

Compete aggressively to increase market share (n=158)

Improve marketing/promotion of products and services(n=290)

Optimize Pricing (n=113)

Target Cross-sell/Up-sell opportunities within client base(n=146)

Enter into adjacent lines of business (n=78)

Hire quality staff (n=140)

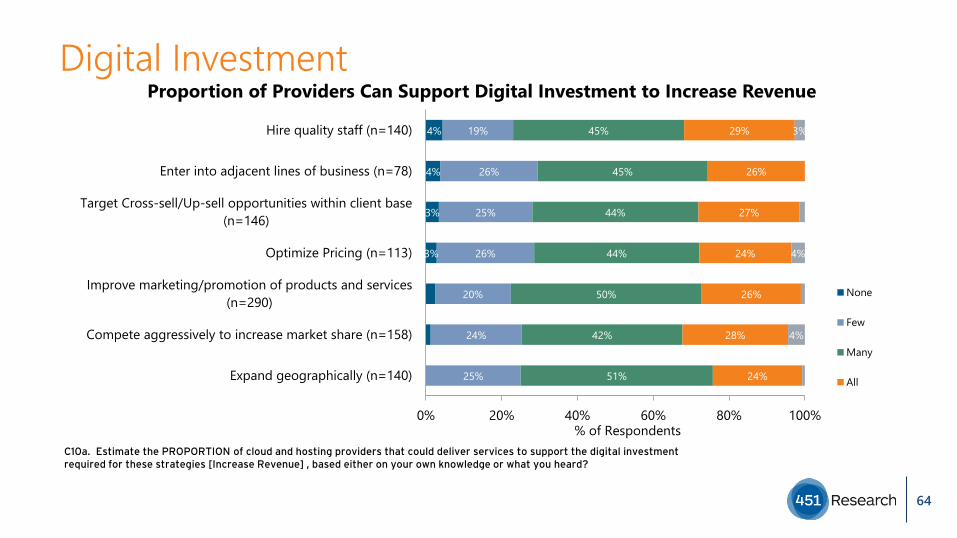

0% 20% 40% 60% 80% 100%% of Respondents

Proportion of Providers Can Support Digital Investment to Increase Revenue

None

Few

Many

All

C10a. Estimate the PROPORTION of cloud and hosting providers that could deliver services to support the digital investment required for these strategies [Increase Revenue] , based either on your own knowledge or what you heard?

64

Digital Investment

3%

9%

13%

23%

20%

21%

24%

24%

28%

45%

52%

52%

48%

46%

44%

28%

42%

23%

26%

25%

28%

26%

28%

3%

5%

6%

Improve financial analytics (n=143)

Monitor operations in real time (n=79)

Create more efficient/streamlined business process(n=290)

Make workforce more productive (n=173)

Optimize supply chain and logistics (n=147)

Enable mobile/telecommute workforce (n=99)

Reduce headcount (n=67)

0% 20% 40% 60% 80% 100%% of Respondents

Proportion of Providers Can Support Digital Investment to Lower Costs

None

Few

Many

All

Don't know

C10b. Estimate the PROPORTION of cloud and hosting providers that could deliver services to support the digital investment required for these strategies [Lower Costs], based either on your own knowledge or what you heard?

65

Digital Investment

3%

5%

14%

15%

19%

18%

17%

18%

15%

17%

20%

21%

55%

48%

57%

50%

46%

50%

39%

52%

50%

46%

29%

36%

24%

29%

36%

26%

43%

27%

26%

24%

3%

5%

4%

Offer self-service products/services (n=51)

Build online communities (n=66)

Tracking digital identities of customers (n=63)

Innovate or deliver new products or services (n=224)

Single customer experience across digital and physical services, devices or platforms…

Use analytics to predict or recover from errors (n=84)

Deliver digital products (vs physical products) (n=79)

Personalize customer experience (n=102)

Focus on customer convenience (n=129)

Find, develop and retain talent (n=135)

0% 20% 40% 60% 80% 100%% of Respondents

Proportion of Providers Can Support Digital Investment to Improve Product or Service Quality

None

Few

Many

All

C10c. Estimate the PROPORTION of cloud and hosting providers that could deliver services to support the digital investment required for these strategies [Improve Product or Service Quality] , based either on your own knowledge or what you heard?

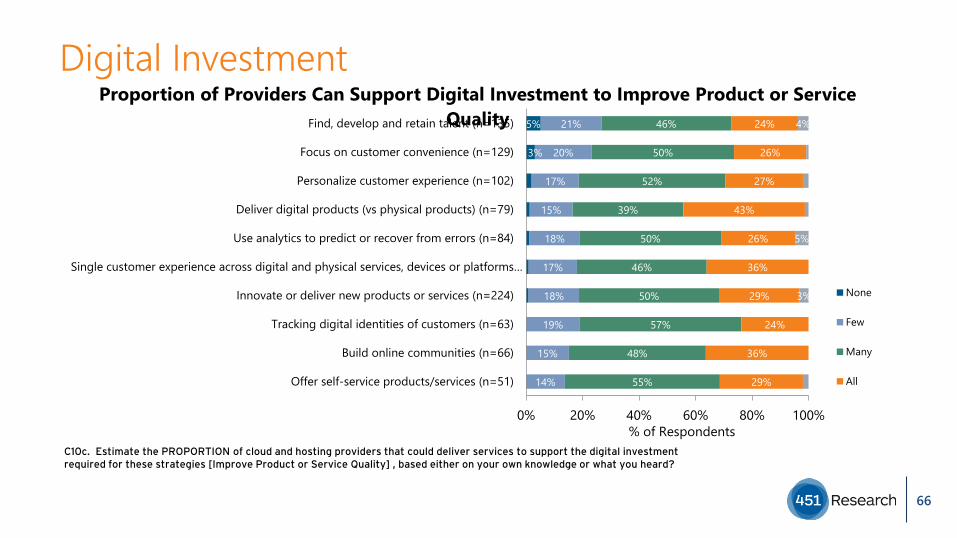

66

5%

14%

15%

19%

18%

17%

18%

15%

17%

20%

21%

55%

48%

57%

50%

46%

50%

39%

52%

50%

46%

29%

36%

24%

29%

36%

26%

43%

27%

26%

24%

3%

5%

4%

Offer self-service products/services (n=51)

Build online communities (n=66)

Tracking digital identities of customers (n=63)

Innovate or deliver new products or services (n=224)

Single customer experience across digital and physical services, devices or platforms (n=111)

Use analytics to predict or recover from errors (n=84)

Deliver digital products (vs physical products) (n=79)

Personalize customer experience (n=102)

Focus on customer convenience (n=129)

Find, develop and retain talent (n=135)

0% 20% 40% 60% 80% 100%% of Respondents

Proportion of Providers Can Support Digital Investment to Improve Product or Service Quality

None

Few

Many

All

Digital Investment

C10c. Estimate the PROPORTION of cloud and hosting providers that could deliver services to support the digital investment required for these strategies [Improve Product or Service Quality] , based either on your own knowledge or what you heard?

67

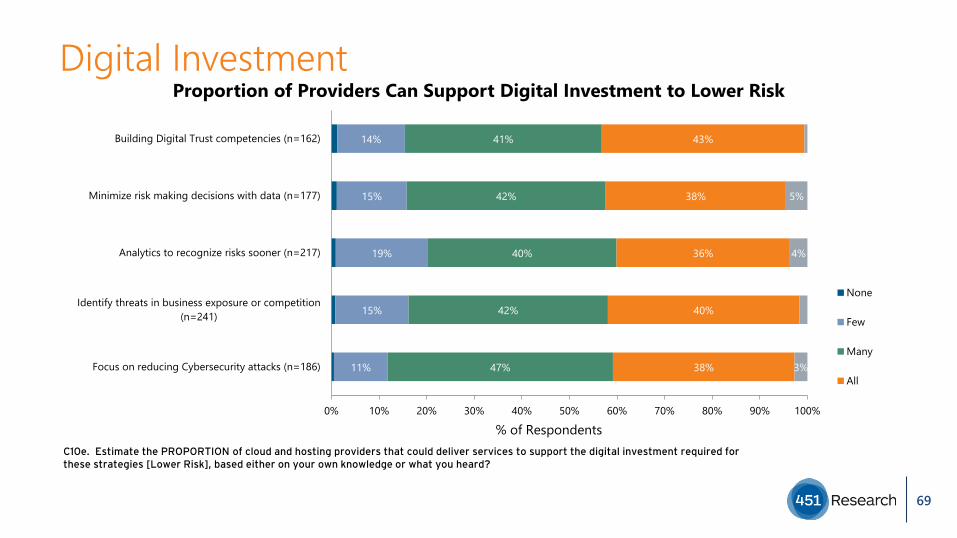

Digital Investment

C10d. Estimate the PROPORTION of cloud and hosting providers that could deliver services to support the digital investment required for these strategies [Speed Time to Market], based either on your own knowledge or what you heard?

17%

15%

15%

14%

20%

12%

19%

54%

54%

58%

51%

50%

51%

50%

26%

30%

26%

33%

30%

33%

28%

3%Automate business processes (n=145)

Use data to drive strategic decision making (n=149)

Integrate customer feedback through communities or analytics(n=132)

Invest in research and development (n=133)

Improve production processes (n=189)

Encourage knowledge sharing & collaboration among employees(n=135)

Cultivate a culture of risk taking...to accelerate development(n=101)

0% 20% 40% 60% 80% 100%% of Respondents

Proportion of Providers Can Support Digital Investment to Speed Time to Market

None

Few

Many

All

68

Digital Investment

C10e. Estimate the PROPORTION of cloud and hosting providers that could deliver services to support the digital investment required for these strategies [Lower Risk], based either on your own knowledge or what you heard?

11%

15%

19%

15%

14%

47%

42%

40%

42%

41%

38%

40%

36%

38%

43%

3%

4%

5%

Focus on reducing Cybersecurity attacks (n=186)

Identify threats in business exposure or competition(n=241)

Analytics to recognize risks sooner (n=217)

Minimize risk making decisions with data (n=177)

Building Digital Trust competencies (n=162)

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

% of Respondents

Proportion of Providers Can Support Digital Investment to Lower Risk

None

Few

Many

All

69

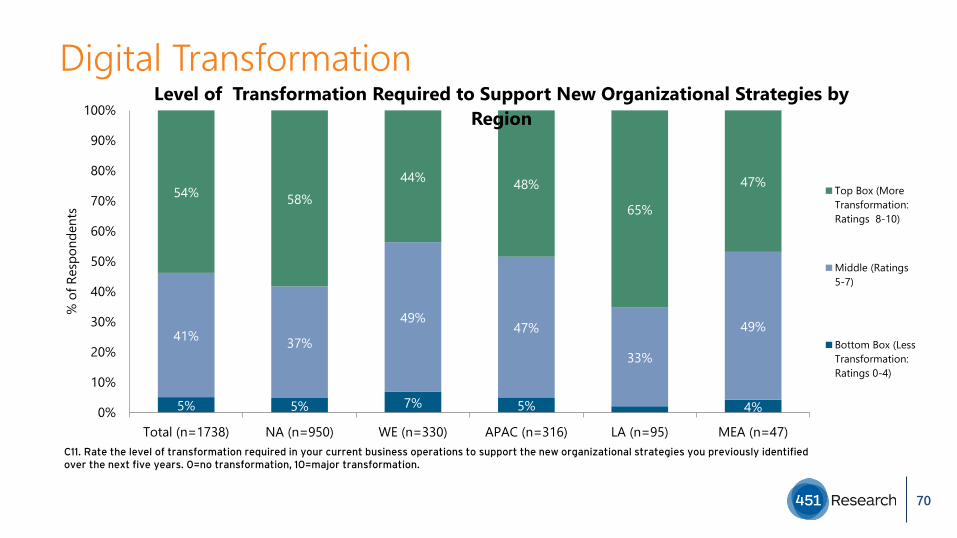

Digital Transformation

5% 5% 7% 5% 4%

41% 37%

49%47%

33%

49%

54% 58%44% 48%

65%

47%

Total (n=1738) NA (n=950) WE (n=330) APAC (n=316) LA (n=95) MEA (n=47)0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

% o

f Res

pond

ents

Level of Transformation Required to Support New Organizational Strategies by Region

Top Box (MoreTransformation:Ratings 8-10)

Middle (Ratings5-7)

Bottom Box (LessTransformation:Ratings 0-4)

C11. Rate the level of transformation required in your current business operations to support the new organizational strategies you previously identified over the next five years. 0=no transformation, 10=major transformation.

70

Digital Transformation

4% 4% 6% 4%

42% 37%

51%47%

41% 45%

54% 59%44% 50%

58% 53%

Total (n=1738) NA (n=950) WE (n=330) APAC (n=316) LA (n=95) MEA (n=47)0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

% o

f Res

pond

ents

Level of Transformation Required in Current IT/Digital Infrastructure Environment by Region

Top Box(MoreTransformation: Ratings 8-10)Middle(Ratings 5-7)

C12. Rate the level of transformation required in your current IT or digital infrastructure environment to support this level of business transformation over the next five years. 0=no transformation, 10=major transformation.

71

Digital Transformation

24% 22% 17%23%

58% 53%

35%32% 43%

40%

21% 34%

41% 46% 40% 37%

21%13%

Total (n=1738) NA (n=950) WE (n=330) APAC (n=316) LA (n=95) MEA (n=47)0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

% o

f Res

pond

ents

Digital Technology Disruption in Your Industry by Region

Top Box(Moredisruption:ratings 8-10)

Middle(Ratings 5-7)

C14. Rate the extent to which digital technology is disrupting your industry over the next 5 years on a 0 to 10 scale where 0 = no disruption and 10 = major disruption.

72

Digital Transformation

C15. What is the level of your organization's commitment to implementing digital/online operations for each of the following business functions? (Randomize) Rate on a scale of 0-10 where 0 = Not at all Committed and 10 = Completely Committed. [TOP BOX RATING OF 8-10]

67%

66%

64%

63%

73%

72%

71%

70%

54%

52%

51%

45%

60%

59%

54%

56%

78%

80%

68%

72%

66%

54%

49%

54%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Customer service/support

Sales

Marketing

Automated internal businessworkflows

% TOP BOX (More Committed - ratings 8 thru 10)

Commitment to Implementing Digital/Online Operation by Region

Total (n=1502)

NA (n=844)

WE (n=271)

APAC (n=265)

LA (n=81)

MEA (n=41)

Note: ‘Straightline” responses removed.

73

Digital Transformation

74

51%

52%

51%

49%

50%

50%

49%

48%

49%

51%

50%

50%

MEA (n=47)

LA (n=95)

APAC (n=316)

WE (n=330)

NA (n=950)

Total(n=1738)

0% 20% 40% 60% 80% 100%Average %

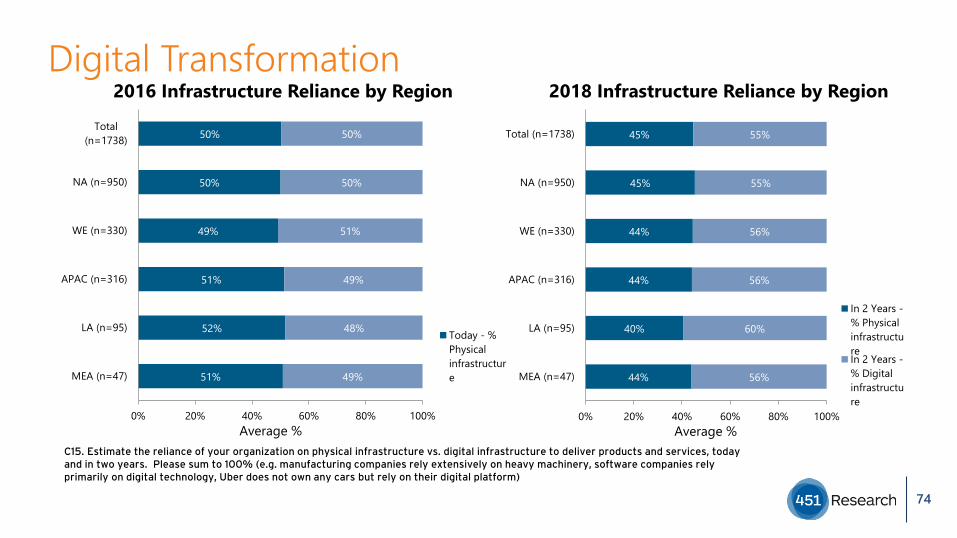

2016 Infrastructure Reliance by Region

Today - %Physicalinfrastructure

C15. Estimate the reliance of your organization on physical infrastructure vs. digital infrastructure to deliver products and services, today and in two years. Please sum to 100% (e.g. manufacturing companies rely extensively on heavy machinery, software companies relyprimarily on digital technology, Uber does not own any cars but rely on their digital platform)

44%

40%

44%

44%

45%

45%

56%

60%

56%

56%

55%

55%

MEA (n=47)

LA (n=95)

APAC (n=316)

WE (n=330)

NA (n=950)

Total (n=1738)

0% 20% 40% 60% 80% 100%Average %

2018 Infrastructure Reliance by Region

In 2 Years -% PhysicalinfrastructureIn 2 Years -% Digitalinfrastructure

Digital Transformation

C16c. How important are each of the following for your organization's digital innovation strategy over the next five years? Rate on a 0-10 scale where 0 = Not at all important and 10 = Extremely Important. (Randomize) [TOP BOX RATING OF 8-10]

72%

72%

65%

63%

79%

78%

72%

70%

62%

63%

50%

48%

62%

59%

57%

58%

81%

82%

81%

68%

74%

77%

49%

58%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Engaging Customers

Optimizing Business Operations

Empowering employees

Transforming Products

% TOP BOX (More Important - ratings 8 thru 10)

Importance to Digital Innovation Strategy by Region

Total (n=1573)

NA (n=870)

WE (n=310)

APAC (n=278)

LA (n=72)

MEA (n=43)

Note: ‘Straightline” responses removed.

75

Digital Transformation: Optimizing Business Operations

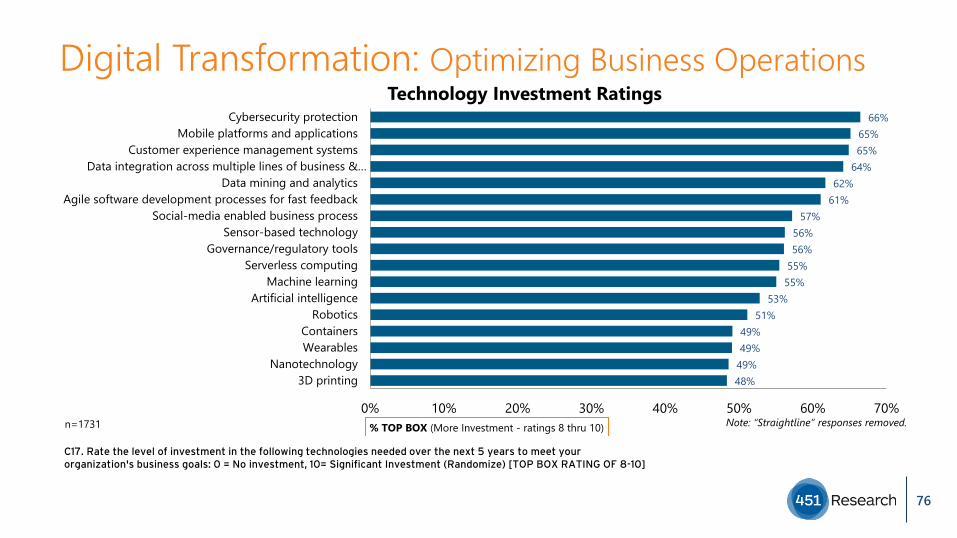

C17. Rate the level of investment in the following technologies needed over the next 5 years to meet your organization's business goals: 0 = No investment, 10= Significant Investment (Randomize) [TOP BOX RATING OF 8-10]

66%65%65%

64%62%

61%57%

56%56%

55%55%

53%51%

49%49%

49%48%

0% 10% 20% 30% 40% 50% 60% 70%

Cybersecurity protectionMobile platforms and applications

Customer experience management systemsData integration across multiple lines of business &…

Data mining and analyticsAgile software development processes for fast feedback

Social-media enabled business processSensor-based technology

Governance/regulatory toolsServerless computing

Machine learningArtificial intelligence

RoboticsContainersWearables

Nanotechnology3D printing

% TOP BOX (More Investment - ratings 8 thru 10)

Technology Investment Ratings

Note: “Straightline” responses removed.n=1731

76

Digital Transformation: Digital Skills

C18. How capable are staff in the following groups at your organization in understanding how digital technologies could transform your business? 0=not at all capable, 10=very capable (Randomize) [TOP BOX RATING OF 8-10]

76%

68%

67%

62%

62%

59%

80%

75%

75%

71%

71%

66%

67%

55%

49%

43%

48%

45%

68%

59%

57%

53%

49%

51%

88%

72%

80%

78%

62%

53%

72%

57%

79%

60%

64%

62%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

IT

Security

Executive team

Line of Business

Support functions: HR, Finance

Legal

% TOP BOX (More Capable - ratings 8 thru 10)

Staff Capability to Understand Digital Technology Transformation by Region

Total(n=1639)NA (n=900)

WE (n=310)

APAC (n=297)

LA (n=85)

77

Digital Transformation: Digital Skills

54% 54% 51%61%

39%

57%

42% 42% 43%33%

58%

43%

5% 4% 6% 6% 3%

Total (n=1738) NA (n=950) WE (n=330) APAC (n=316) LA (n=95) MEA (n=47)0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

% o

f Res

pond

ents

Skill Shortage in Cloud Computing Expertise by Region

Don'tknow

No

C19. Does your organization currently face a skills shortage in cloud computing expertise?

78

Digital Transformation: Digital Skills

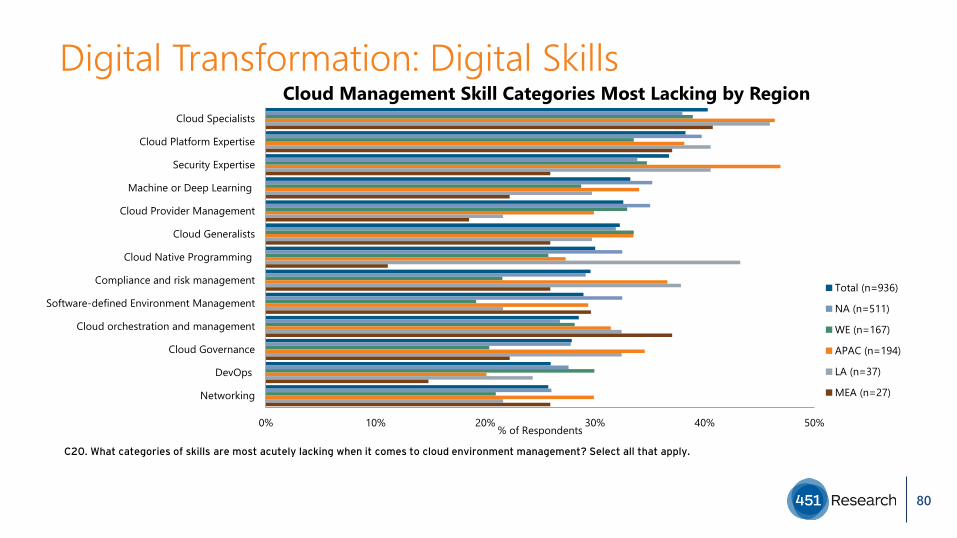

C20. What categories of skills are most acutely lacking when it comes to cloud environment management? Select all that apply.

40%

38%

37%

33%

33%

32%

30%

30%

29%

29%

28%

26%

26%

0% 10% 20% 30% 40% 50%

Cloud Specialists

Cloud Platform Expertise

Security Expertise

Machine or Deep Learning

Cloud Provider Management

Cloud Generalists

Cloud Native Programming

Compliance and risk management

Software-defined Environment…

Cloud orchestration and management

Cloud Governance

DevOps

Networking

% of Respondents

Cloud Management Skill Categories Most Lacking

n=936

79

Digital Transformation: Digital Skills

C20. What categories of skills are most acutely lacking when it comes to cloud environment management? Select all that apply.

0% 10% 20% 30% 40% 50%

Cloud Specialists

Cloud Platform Expertise

Security Expertise

Machine or Deep Learning

Cloud Provider Management

Cloud Generalists

Cloud Native Programming

Compliance and risk management

Software-defined Environment Management

Cloud orchestration and management

Cloud Governance

DevOps

Networking

% of Respondents

Cloud Management Skill Categories Most Lacking by Region

Total (n=936)

NA (n=511)

WE (n=167)

APAC (n=194)

LA (n=37)

MEA (n=27)

80

Digital Transformation: Digital Skills

45% 45% 42%55%

33%21%

50% 50% 54%41%

63%70%

5% 5% 4% 4% 4% 9%

Total (n=1738) NA (n=950) WE (n=330) APAC (n=316) LA (n=95) MEA (n=47)0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

% o

f Res

pond

ents

Lack of Skillset Impeding Digital Transformation Initiatives by Region

Don'tKnow

No

C22. Is there a lack of skillsets in cloud impeding digital transformation initiatives at your organization?

81

Digital Transformation: Digital Culture

4% 3% 3% 8% 3% 6%

33%29%

40%41%

32%36%

63% 69%57%

50%65%

57%

Total (n=1738) NA (n=950) WE (n=330) APAC (n=316) LA (n=95) MEA (n=47)0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

% o

f Res

pond

ents

Level of Agreement by Region

Top Box(More Agree:Ratings 8-10)

Middle(Ratings 5-7)

Our organization has a clear strategy to evolve our digital business

C23. Please rate your level of agreement with this statement where 0=completely disagree, 10=completely agree. Our organization has a clear strategy to evolve our digital business environment over the next five years.

82

Digital Transformation: Digital Culture

C24. Which of the following best describes the key digital transformation leader in your organization, if any?

5%

26%

20%

26%

7%

6%

3%

3%

4%

0% 10% 20% 30% 40%

None: we do not have a digital transfrmtn…

Chief Executive Officer (CEO)

Chief Information Officer (CIO)

Chief Technology Officer (CTO)

Chief Operating Officer (COO)

Chief Digital Officer

Chief Security Officer

Head of Sales

Chief Marketing Officer

% of Respondents

Staff Capability to Understand Digital Technology Transformation by Region

Total (n=1738)

NA (n=950)

WE (n=330)

APAC (n=316)

LA (n=95)

MEA (n=47)

83

DIGITAL TRANSFORMATION CASE STUDY (T)

Digital Transformation

QT1: Is your organization currently undertaking a significant digital transformation project?QT1a: Has your organization completed a significant digital transformation project within the past year?QT1b: Is your organization planning a significant digital transformation project within the next year?

83%

72%

68%

64%

69%

69%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

LA (n=95)

APAC (n=316)

MEA (n=47)

WE (n=330)

NA (n=950)

Total (n=1738)

UndertakingDigitalTransformation - Active

DigitalTransformation - PlansWithin NextYear

85

Digital Transformation

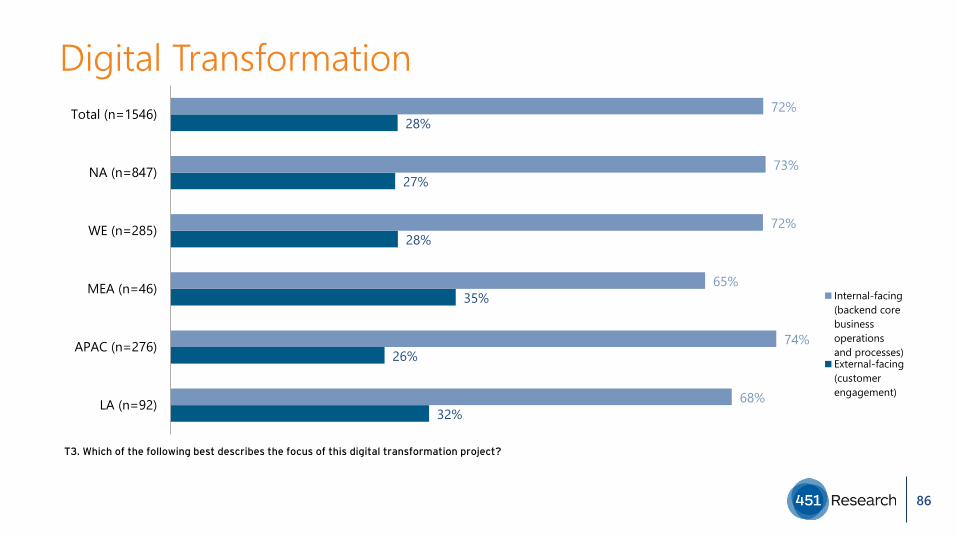

T3. Which of the following best describes the focus of this digital transformation project?

32%

26%

35%

28%

27%

28%

68%

74%

65%

72%

73%

72%

LA (n=92)

APAC (n=276)

MEA (n=46)

WE (n=285)

NA (n=847)

Total (n=1546)

Internal-facing(backend corebusinessoperationsand processes)External-facing(customerengagement)

86

Digital Transformation

T4. What is the primary business purpose of this digital transformation project?

37%

28%

50%

21%

28%

28%

0% 10% 20% 30% 40% 50% 60%

LA (n=92)

APAC (n=276)

MEA (n=46)

WE (n=285)

NA (n=847)

Total (n=1546)

Expand the Business (EnterNew Markets/Lines ofBusiness, Develop NewProducts/Services)Grow the Business (IncreaseRevenue from ExistingBusiness/Products)

Run the Business (OptimizeBusiness Operations)

87

Digital Transformation

T5. Which business processes are being transformed as part of this digital transformation project?

15%

24%

30%

34%

38%

38%

41…

44%

72%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90%

Sales

Customerservice/support

Marketing

Finance

Legal

Human Resources

Line of businessoperations

IT

Productdevelopment/R&D

Total(n=1546)NA (n=847)

WE (n=285)

MEA (n=46)

APAC(n=276)

88

Digital Transformation

T6. At what stage of the digital transformation project was IT brought in?

34%

35%

35%

38%

43%

0% 10% 20% 30% 40% 50% 60% 70%

Infrastructure

Applications/Software

Managed Services

Security Services

Professional Services for CloudEnablement

Total(n=1546)NA (n=847)

WE (n=285)

MEA (n=46)

APAC(n=276)

89

Digital Transformation – IT Service Providers

T7. Please rate the strategic importance of IT service providers for this digital transformation project. [% TOP BOX RATING (More Strategic 8 thru 10)]

77%

61%

63%

60%

71%

67%

LA (n=92)

APAC(n=276)

MEA (n=46)

WE (n=285)

NA (n=847)

Total(n=1546)

90

Digital Transformation – Business Process

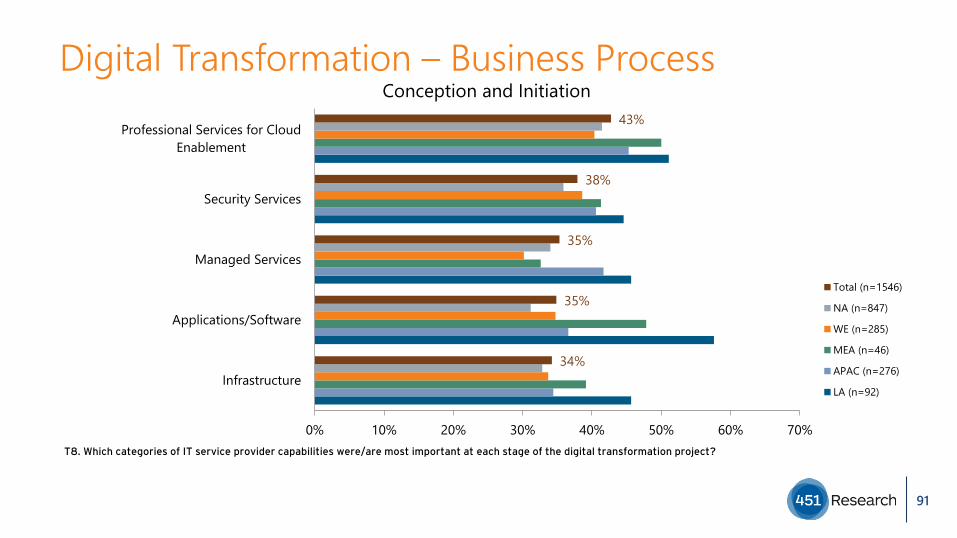

T8. Which categories of IT service provider capabilities were/are most important at each stage of the digital transformation project?

34%

35%

35%

38%

43%

0% 10% 20% 30% 40% 50% 60% 70%

Infrastructure

Applications/Software

Managed Services

Security Services

Professional Services for CloudEnablement

Conception and Initiation

Total (n=1546)

NA (n=847)

WE (n=285)

MEA (n=46)

APAC (n=276)

LA (n=92)

91

Digital Transformation – Business Process

T8. Which categories of IT service provider capabilities were/are most important at each stage of the digital transformation project?

33%

34%

36%

37%

38%

0% 10% 20% 30% 40% 50% 60%

Infrastructure

Applications/Software

Managed Services

Security Services

Professional Services for CloudEnablement

Scoping and Planning

Total (n=1546)

NA (n=847)

WE (n=285)

MEA (n=46)

APAC (n=276)

LA (n=92)

92

Digital Transformation – Business Process

T8. Which categories of IT service provider capabilities were/are most important at each stage of the digital transformation project?

34%

35%

37%

38%

43%

0% 10% 20% 30% 40% 50% 60%

Infrastructure

Applications/Software

Managed Services

Security Services

Professional Services for CloudEnablement

Launch/Execution

Total (n=1546)

NA (n=847)

WE (n=285)

MEA (n=46)

APAC (n=276)

LA (n=92)

93

Digital Transformation – Business Process

T8. Which categories of IT service provider capabilities were/are most important at each stage of the digital transformation project?

32%

33%

34%

37%

39%

0% 10% 20% 30% 40% 50% 60%

Infrastructure

Applications/Software

Managed Services

Security Services

Professional Services for CloudEnablement

Evaluation of Results

Total (n=1546)

NA (n=847)

WE (n=285)

MEA (n=46)

APAC (n=276)

LA (n=92)

94

Digital Transformation – Business Process

T8. Which categories of IT service provider capabilities were/are most important at each stage of the digital transformation project?

37%

37%

38%

40%

40%

0% 10% 20% 30% 40% 50% 60% 70%

Infrastructure

Applications/Software

Managed Services

Security Services

Professional Services for CloudEnablement

Ongoing Operations and Maintenance

Total (n=1546)

NA (n=847)

WE (n=285)

MEA (n=46)

APAC (n=276)

LA (n=92)

95

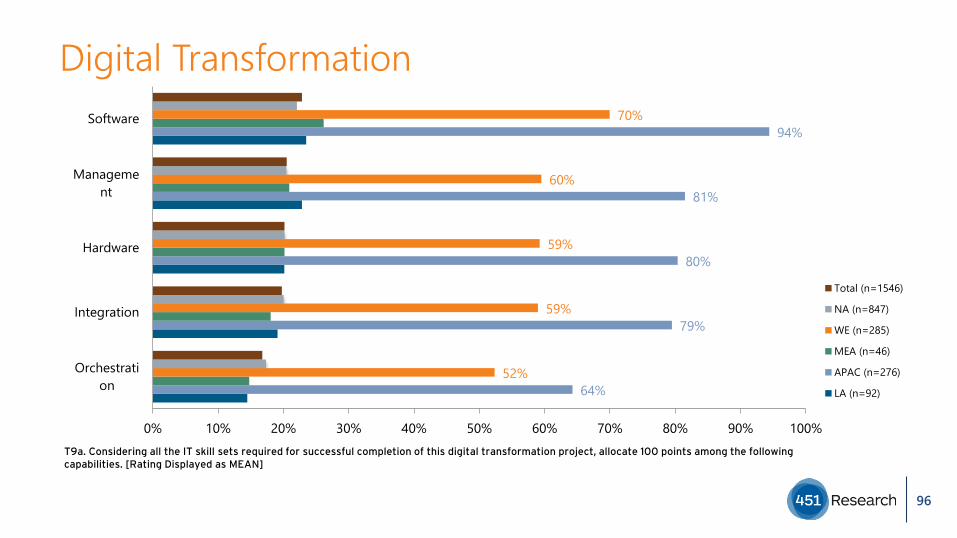

Digital Transformation

T9a. Considering all the IT skill sets required for successful completion of this digital transformation project, allocate 100 points among the following capabilities. [Rating Displayed as MEAN]

64%

79%

80%

81%

94%

52%

59%

59%

60%

70%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Orchestration

Integration

Hardware

Management

Software

Total (n=1546)

NA (n=847)

WE (n=285)

MEA (n=46)

APAC (n=276)

LA (n=92)

96

Digital Transformation

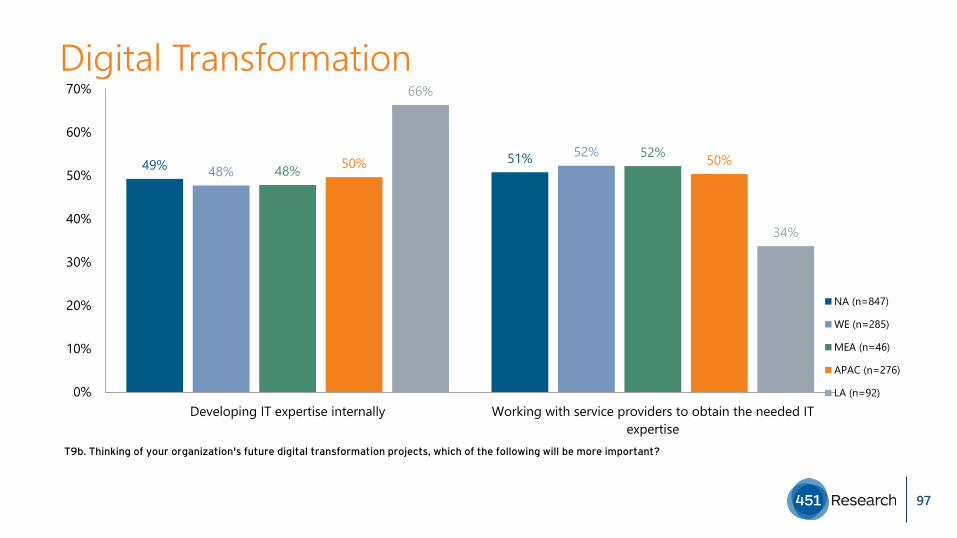

T9b. Thinking of your organization's future digital transformation projects, which of the following will be more important?

49% 51%48%

52%48%

52%50% 50%

66%

34%

0%

10%

20%

30%

40%

50%

60%

70%

Developing IT expertise internally Working with service providers to obtain the needed ITexpertise

NA (n=847)

WE (n=285)

MEA (n=46)

APAC (n=276)

LA (n=92)

97

Hosting/Cloud Service Providers

T10. Which of the following best describes your organization's approach to dealing with hosting/cloud service providers to obtain the IT services needed for digital transformation projects?

27%

34%

36%

0% 10% 20% 30% 40% 50% 60%

Single provider that can offer a broad range of products andservices that it builds and manages