2017 IRP Advisory Group - Puget Sound Energy · Overview February 3, ... Overview of Resource...

69

2017 IRP Advisory Group February 3, 2017 IRPAG

Transcript of 2017 IRP Advisory Group - Puget Sound Energy · Overview February 3, ... Overview of Resource...

2017 IRP Advisory Group

February 3, 2017 IRPAG

2

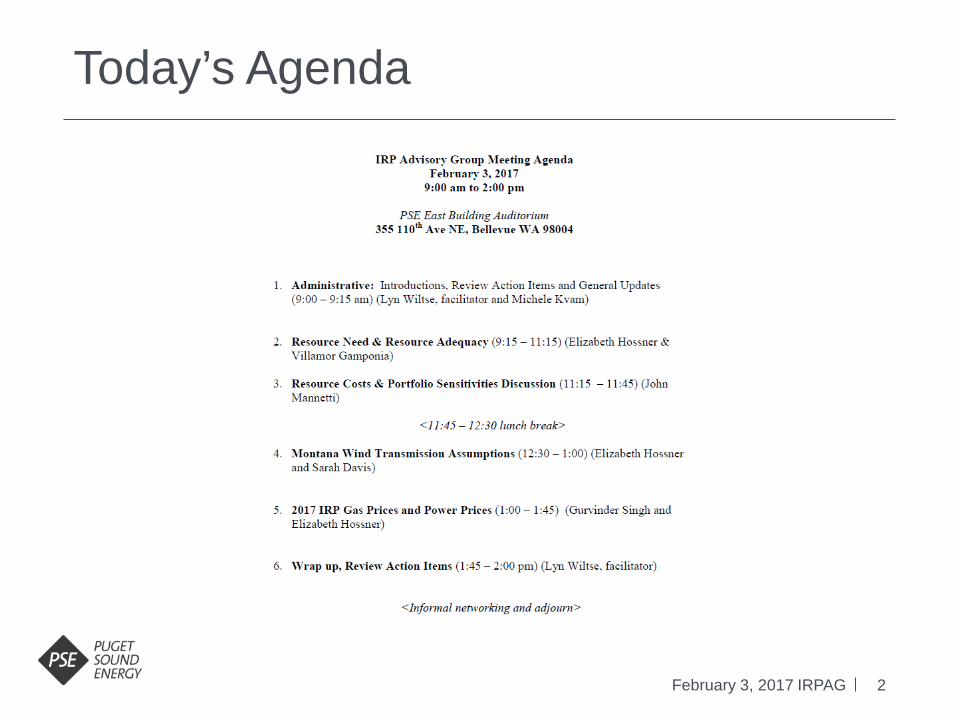

Today’s Agenda

February 3, 2017 IRPAG

3

Purpose of IRP

February 3, 2017 IRPAG

WAC 480-100-238 Integrated resource planning.

• (1) Purpose. Each electric utility regulated by the commission has the responsibility to meet its system demand with a least cost mix of energy supply resources and conservation. In furtherance of that responsibility, each electric utility must develop an "integrated resource plan."

4

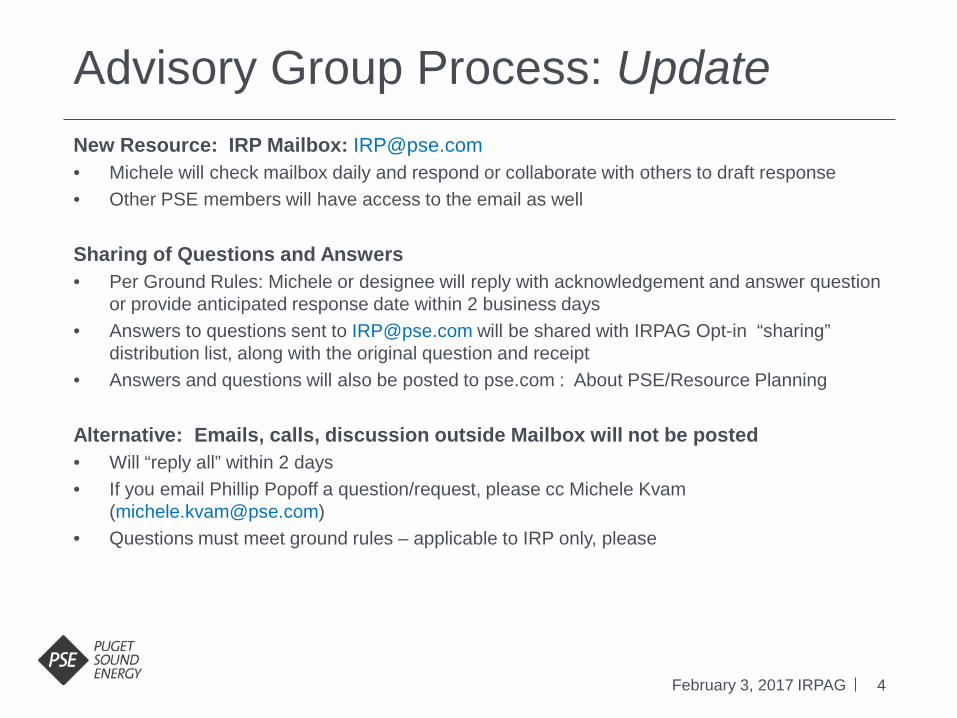

Advisory Group Process: Update

February 3, 2017 IRPAG

New Resource: IRP Mailbox: [email protected] • Michele will check mailbox daily and respond or collaborate with others to draft response • Other PSE members will have access to the email as well

Sharing of Questions and Answers • Per Ground Rules: Michele or designee will reply with acknowledgement and answer question

or provide anticipated response date within 2 business days • Answers to questions sent to [email protected] will be shared with IRPAG Opt-in “sharing”

distribution list, along with the original question and receipt • Answers and questions will also be posted to pse.com : About PSE/Resource Planning

Alternative: Emails, calls, discussion outside Mailbox will not be posted • Will “reply all” within 2 days • If you email Phillip Popoff a question/request, please cc Michele Kvam

([email protected]) • Questions must meet ground rules – applicable to IRP only, please

5

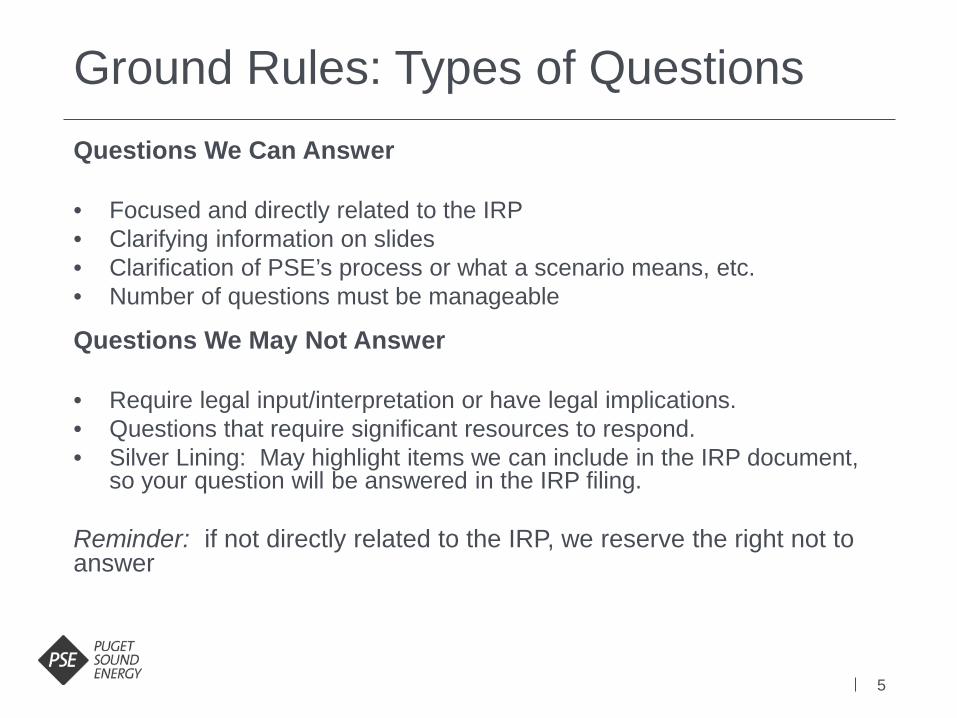

Ground Rules: Types of Questions Questions We Can Answer • Focused and directly related to the IRP • Clarifying information on slides • Clarification of PSE’s process or what a scenario means, etc. • Number of questions must be manageable

Questions We May Not Answer • Require legal input/interpretation or have legal implications. • Questions that require significant resources to respond. • Silver Lining: May highlight items we can include in the IRP document,

so your question will be answered in the IRP filing.

Reminder: if not directly related to the IRP, we reserve the right not to answer

Resource Need & Resource Adequacy

February 3, 2017 IRPAG

7

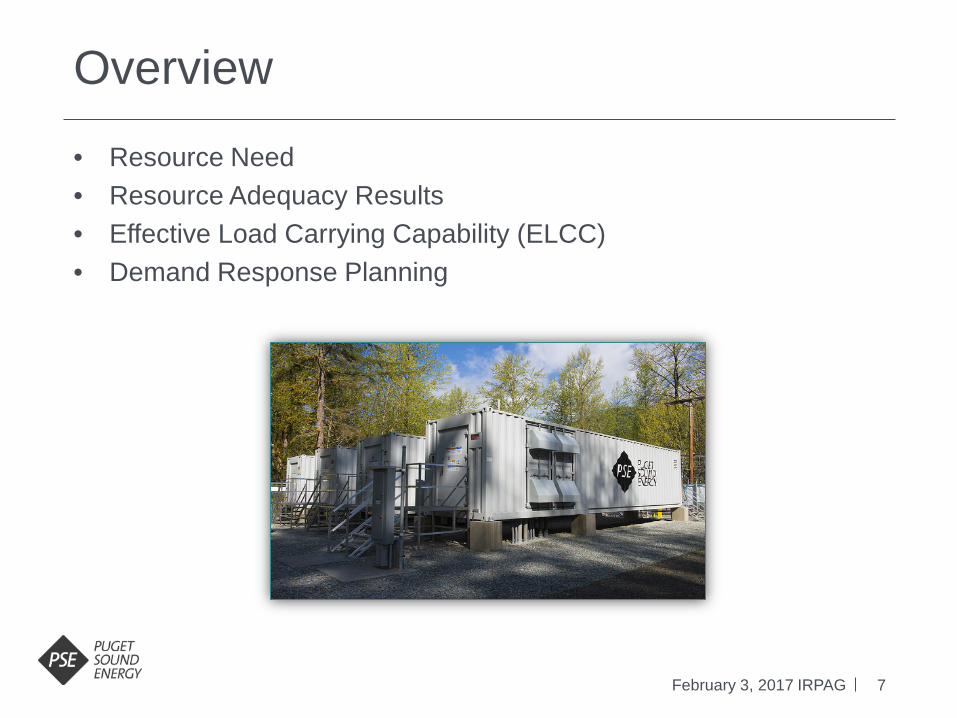

Overview

February 3, 2017 IRPAG

• Resource Need • Resource Adequacy Results • Effective Load Carrying Capability (ELCC) • Demand Response Planning

8

Calculating the Resource Need

February 3, 2017 IRPAG

December 2020 w/ Colstrip 1&2

Peak Demand 5,227 MW

Planning Margin 13.6%

Normal Peak Load + PM 5,927 MW

Operating Reserves 408 MW

Total Capacity Need 6,334 MW

Total Resources (No DSR) (4,357) MW

Available Mid-C Transmission (1,722) MW

Total 256 MW

Operating reserves on new resources 8 MW

Total Resource Deficit/(surplus)* 263 MW

*Resource need before demand side resources (DSR)

9

December Peak Capacity Deficit/(Surplus)

February 3, 2017 IRPAG

-5

12

-60

-19

286

293

314 41

5

788

828

838 91

1 990

1,31

4

1,38

0

1,44

8

1,51

7

1,59

5

1,61

0

1,69

1

108

223

263 38

2

758 825 90

6 1,06

4

1,46

7

1,53

7

1,57

8

1,67

6

1,78

2 2,14

7

2,24

8

2,34

9

2,45

0

2,55

6

2,59

6

2,70

4

-500

0

500

1,000

1,500

2,000

2,500

3,000

2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 2031 2032 2033 2034 2035 2036 2037

MW

Total Need after 2015 IRP DSR

2017 IRP Total Need Before DSR

10

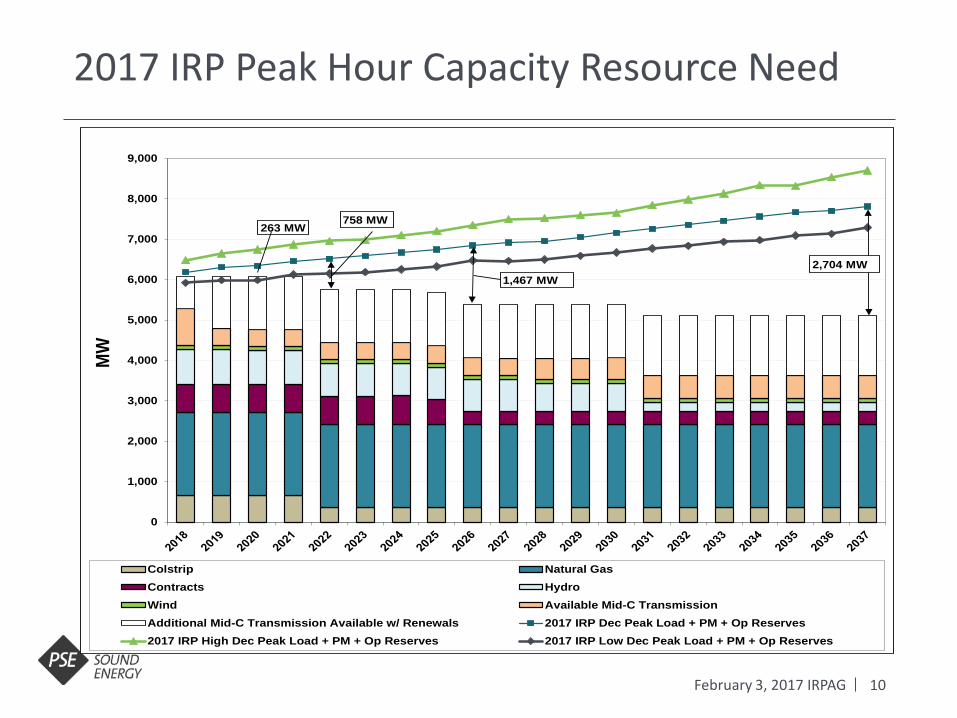

2017 IRP Peak Hour Capacity Resource Need

February 3, 2017 IRPAG

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

MW

Colstrip Natural GasContracts HydroWind Available Mid-C TransmissionAdditional Mid-C Transmission Available w/ Renewals 2017 IRP Dec Peak Load + PM + Op Reserves2017 IRP High Dec Peak Load + PM + Op Reserves 2017 IRP Low Dec Peak Load + PM + Op Reserves

2,704 MW1,467 MW

758 MW263 MW

11

Overview

February 3, 2017 IRPAG

• Resource Need • Resource Adequacy Results • Effective Load Carrying Capability (ELCC) • Demand Response Planning

12

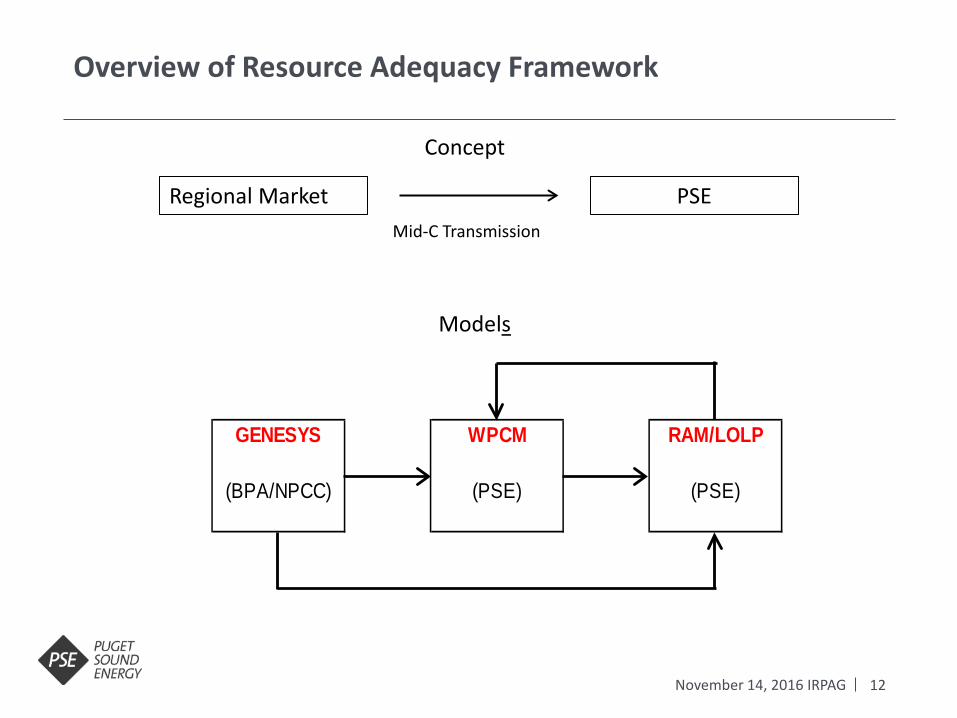

Overview of Resource Adequacy Framework

November 14, 2016 IRPAG

GENESYS WPCM RAM/LOLP

(BPA/NPCC) (PSE) (PSE)

Regional Market PSE Mid-C Transmission

Concept

Models

13

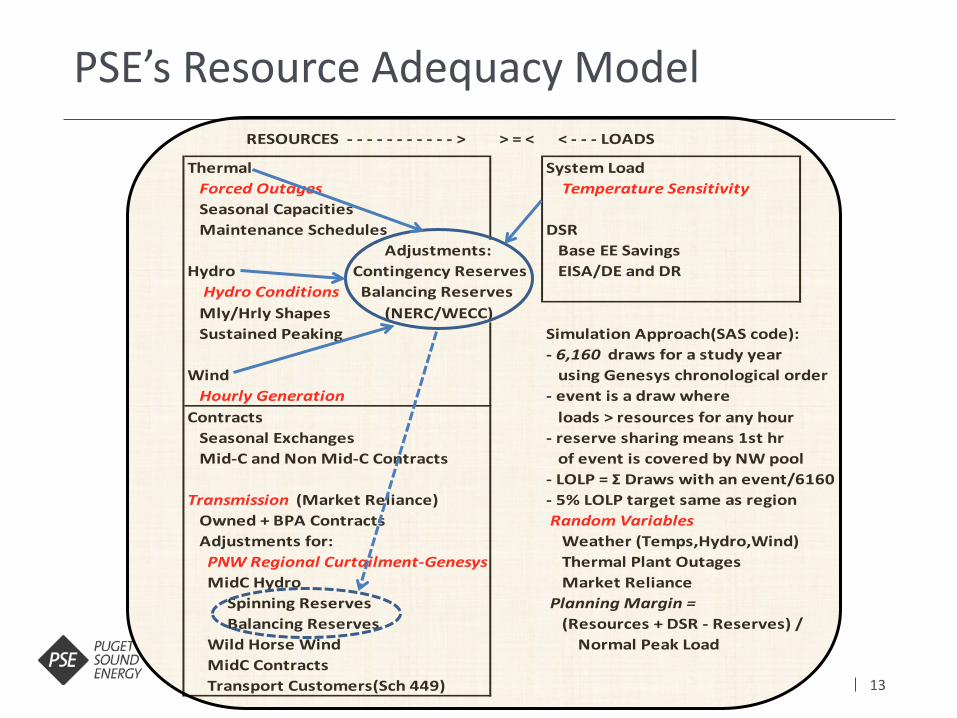

PSE’s Resource Adequacy Model > = <

Thermal System Load Forced Outages Temperature Sensitivity Seasonal Capacities Maintenance Schedules DSR

Adjustments: Base EE SavingsHydro Contingency Reserves EISA/DE and DR Hydro Conditions Balancing Reserves Mly/Hrly Shapes (NERC/WECC) Sustained Peaking Simulation Approach(SAS code):

- 6,160 draws for a study yearWind using Genesys chronological order Hourly Generation - event is a draw whereContracts loads > resources for any hour Seasonal Exchanges - reserve sharing means 1st hr Mid-C and Non Mid-C Contracts of event is covered by NW pool

- LOLP = Ʃ Draws with an event/6160Transmission (Market Reliance) - 5% LOLP target same as region Owned + BPA Contracts Random Variables Adjustments for: Weather (Temps,Hydro,Wind) PNW Regional Curtailment-Genesys Thermal Plant Outages MidC Hydro Market Reliance Spinning Reserves Planning Margin = Balancing Reserves (Resources + DSR - Reserves) / Wild Horse Wind Normal Peak Load MidC Contracts Transport Customers(Sch 449)

RESOURCES - - - - - - - - - - - > < - - - LOADS

14

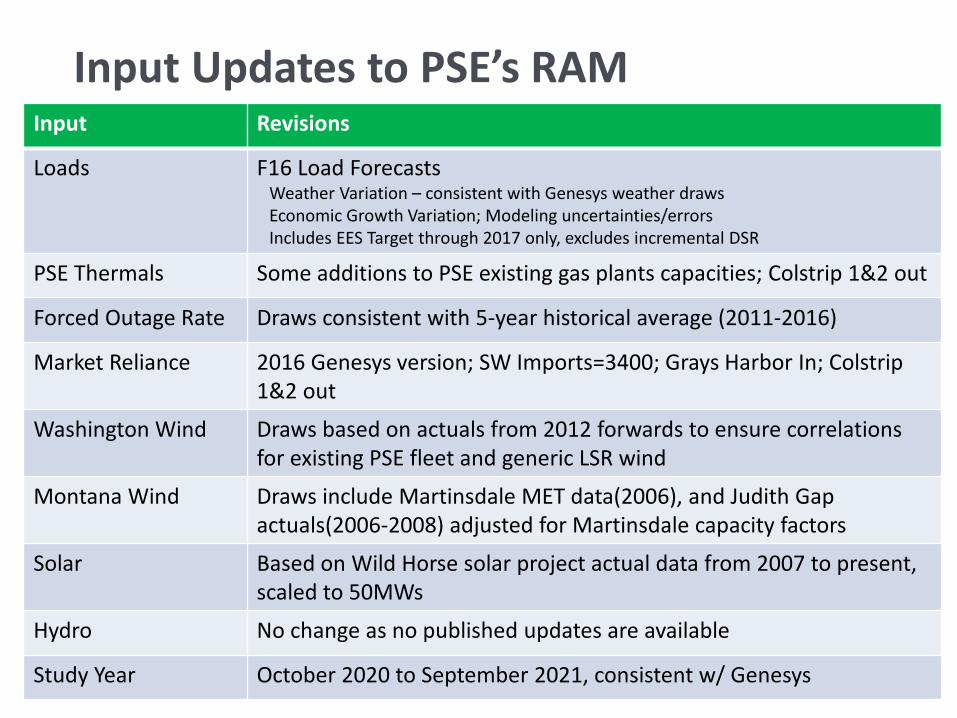

Input Updates to PSE’s RAM

February 3, 2017 IRPAG

Input Revisions

Loads F16 Load Forecasts Weather Variation – consistent with Genesys weather draws Economic Growth Variation; Modeling uncertainties/errors Includes EES Target through 2017 only, excludes incremental DSR

PSE Thermals Some additions to PSE existing gas plants capacities; Colstrip 1&2 out

Forced Outage Rate Draws consistent with 5-year historical average (2011-2016)

Market Reliance 2016 Genesys version; SW Imports=3400; Grays Harbor In; Colstrip 1&2 out

Washington Wind Draws based on actuals from 2012 forwards to ensure correlations for existing PSE fleet and generic LSR wind

Montana Wind Draws include Martinsdale MET data(2006), and Judith Gap actuals(2006-2008) adjusted for Martinsdale capacity factors

Solar Based on Wild Horse solar project actual data from 2007 to present, scaled to 50MWs

Hydro No change as no published updates are available

Study Year October 2020 to September 2021, consistent w/ Genesys

15

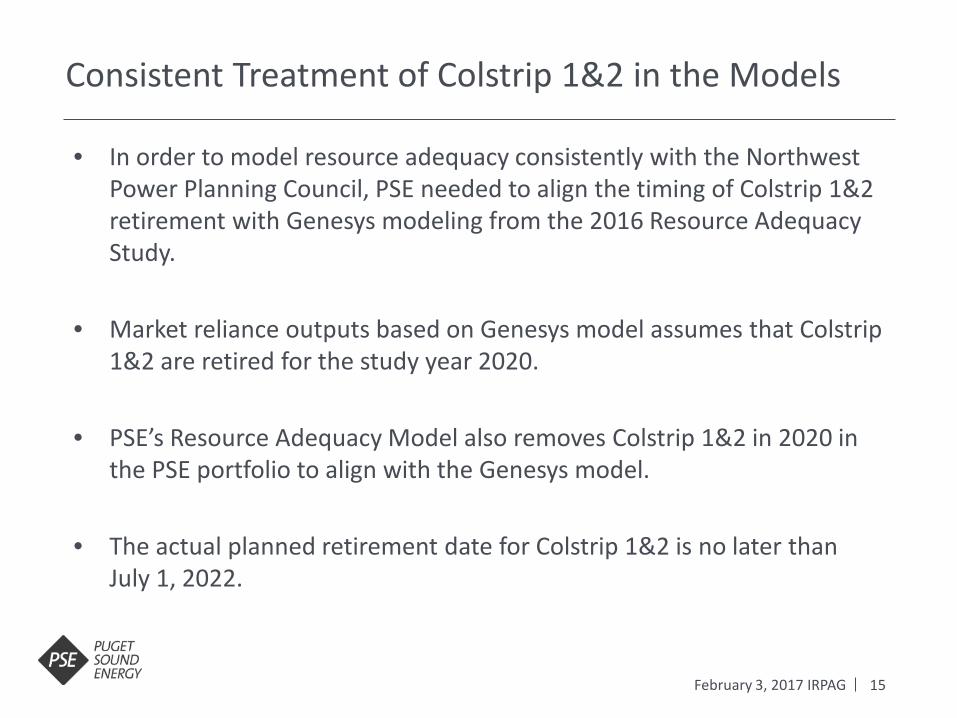

Consistent Treatment of Colstrip 1&2 in the Models

February 3, 2017 IRPAG

• In order to model resource adequacy consistently with the Northwest Power Planning Council, PSE needed to align the timing of Colstrip 1&2 retirement with Genesys modeling from the 2016 Resource Adequacy Study.

• Market reliance outputs based on Genesys model assumes that Colstrip 1&2 are retired for the study year 2020.

• PSE’s Resource Adequacy Model also removes Colstrip 1&2 in 2020 in the PSE portfolio to align with the Genesys model.

• The actual planned retirement date for Colstrip 1&2 is no later than July 1, 2022.

16

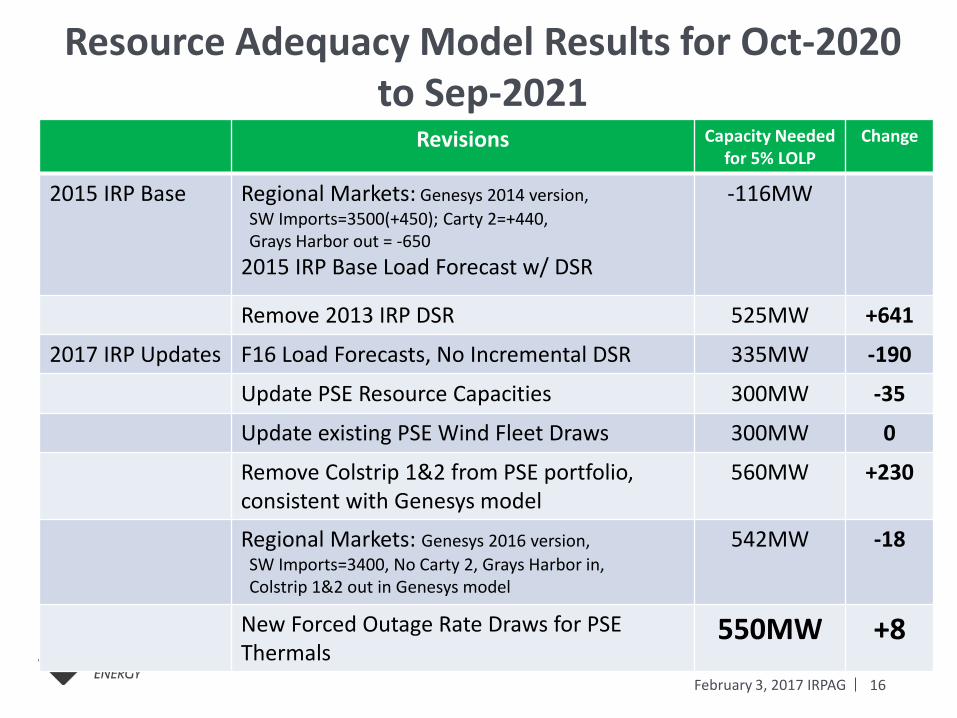

Resource Adequacy Model Results for Oct-2020 to Sep-2021

February 3, 2017 IRPAG

Revisions Capacity Needed for 5% LOLP

Change

2015 IRP Base Regional Markets: Genesys 2014 version, SW Imports=3500(+450); Carty 2=+440, Grays Harbor out = -650 2015 IRP Base Load Forecast w/ DSR

-116MW

Remove 2013 IRP DSR 525MW +641

2017 IRP Updates F16 Load Forecasts, No Incremental DSR 335MW -190

Update PSE Resource Capacities 300MW -35

Update existing PSE Wind Fleet Draws 300MW 0

Remove Colstrip 1&2 from PSE portfolio, consistent with Genesys model

560MW +230

Regional Markets: Genesys 2016 version, SW Imports=3400, No Carty 2, Grays Harbor in, Colstrip 1&2 out in Genesys model

542MW -18

New Forced Outage Rate Draws for PSE Thermals

550MW +8

17

Calculating the Resource Need

February 3, 2017 IRPAG

December 2020 w/ Colstrip 1&2

Peak Demand 5,227 MW

Planning Margin 13.6%

Normal Peak Load + PM 5,927 MW

Operating Reserves 408 MW

Total Capacity Need 6,334 MW

Total Resources (No DSR) (4,357) MW

Available Mid-C Transmission (1,722) MW

Total 256 MW

Operating reserves on new resources 8 MW

Total Resource Deficit/(surplus)* 263 MW

*Resource need before demand side resources (DSR)

December 2020 w/o Colstrip 1&2

5,227 MW

13.6%

5,927 MW

399 MW

6,325 MW

(4,058) MW

(1,717) MW

550 MW

17 MW

567 MW

18

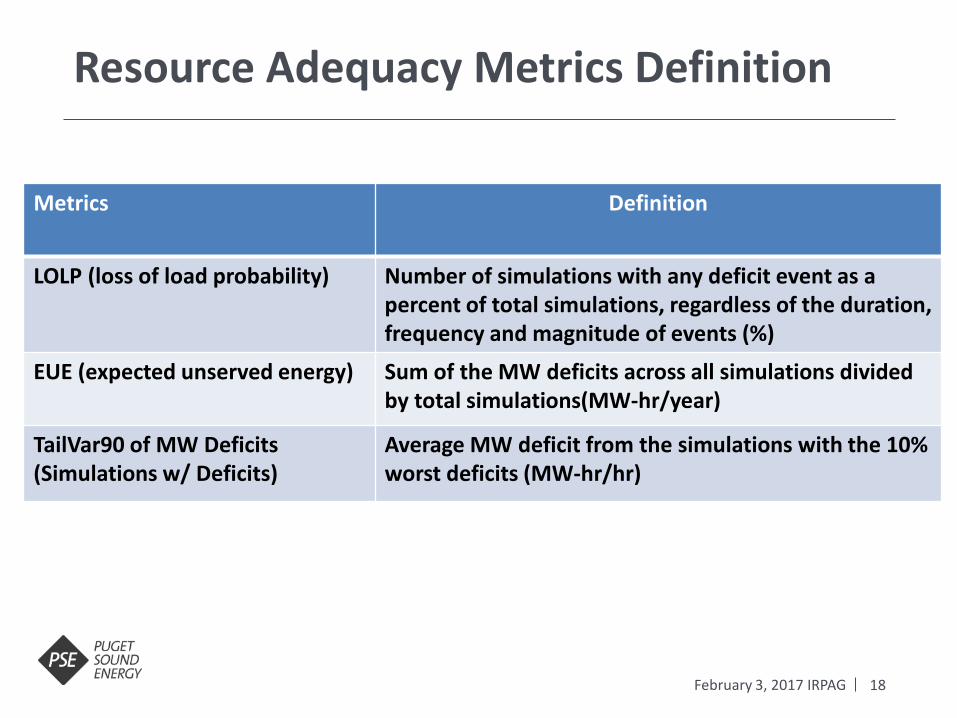

Resource Adequacy Metrics Definition

February 3, 2017 IRPAG

Metrics Definition

LOLP (loss of load probability) Number of simulations with any deficit event as a percent of total simulations, regardless of the duration, frequency and magnitude of events (%)

EUE (expected unserved energy) Sum of the MW deficits across all simulations divided by total simulations(MW-hr/year)

TailVar90 of MW Deficits (Simulations w/ Deficits)

Average MW deficit from the simulations with the 10% worst deficits (MW-hr/hr)

19

Resource Adequacy Model 2017IRP Metrics

February 3, 2017 IRPAG

MW peaker needed or EUE are inputs into the peak capacity credit calculations

Peak capacity credit approach used is ELCC (effective load carrying capability) defined as the equivalent peaker capacity change to get the same LOLP or EUE as a percent of the resource capacity added or removed from portfolio

PSE Portfolio for Study Year: Oct-2020 to Sep-2021 5% LOLP

MW Capacity Needed 550 MW

EUE (expected unserved energy) 34.6 MW-hr/year

TailVar90 of MW Deficit (Simulations w/ Deficit Events) 460 MW-hr/hr

20

Overview

February 3, 2017 IRPAG

• Resource Need • Resource Adequacy Results • Effective Load Carrying Capability (ELCC) • Demand Response Planning

21

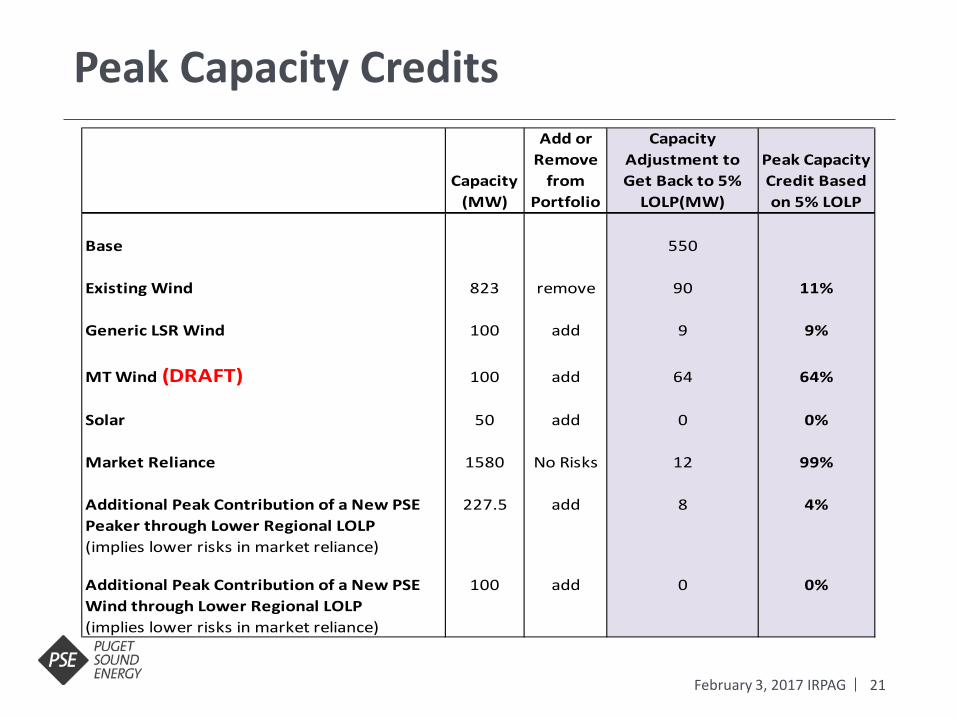

Peak Capacity Credits

February 3, 2017 IRPAG

Capacity(MW)

Add or Remove

from Portfolio

Capacity Adjustment to Get Back to 5%

LOLP(MW)

Peak Capacity Credit Based on 5% LOLP

Base 550

Existing Wind 823 remove 90 11%

Generic LSR Wind 100 add 9 9%

MT Wind (DRAFT) 100 add 64 64%

Solar 50 add 0 0%

Market Reliance 1580 No Risks 12 99%

Additional Peak Contribution of a New PSE 227.5 add 8 4%Peaker through Lower Regional LOLP(implies lower risks in market reliance)

Additional Peak Contribution of a New PSE 100 add 0 0%Wind through Lower Regional LOLP(implies lower risks in market reliance)

22

Peak Capacity Credit for Battery

February 3, 2017 IRPAG

Capacity(MW)

Add or Remove

from Portfolio

Capacity Adjustment to Get Back to 5%

LOLP(MW)

Peak Capacity Credit Based on 5% LOLP

EUE @ 5% LOLP

Capacity Adjustment to Get EUE @ 5%

LOLP(MW)

Peak Capacity Credit Based on EUE @ 5%

LOLPFinal EUE

Base 550 34.6Battery Lithium Ion, 2Hr, 25MW max per hr 25 add 24 96% 36.3 15 60% 34.5 Lithium Ion, 4Hr, 25MW max per hr 25 add 24 96% 35.0 22 88% 34.7 Lithium Ion, 2Hr, 50MW max per hr 50 add 50 100% 34.5 50 100% 34.5 Flow Battery, 4Hr, 25MW max per hr 25 add 24 96% 35.5 19 76% 34.6 Flow Battery, 6Hr, 25MW max per hr 25 add 24 96% 35.3 20 80% 34.5

LOLP Does: Count New Simulations That Experience a Resource Deficiency LOLP Does Not: Reflect Making Deficiencies Worse in an Event That Was Already Short

23

Overview

February 3, 2017 IRPAG

• Resource Need • Resource Adequacy Results • Effective Load Carrying Capability (ELCC) • Demand Response Planning

24

Demand Response Planning

February 3, 2017 IRPAG

Determine The Characteristics Needed from Demand Response • What we need versus what we can have • What characteristics should a DR program have to adequately displace a

peaker of a given size? • Focused on load that needs to be carried, rather than the load that

can be carried by a specific program

Key Question • LOLP: Only focuses on new simulations that experience a resource • LOLP Does Not: Address bad simulations where events are made worse

in frequency, duration, and magnitude • Question: Shouldn’t we be concerned about making already bad

simulations worse?

25

How to Estimate Reliability Needed From Demand Response

February 3, 2017 IRPAG

The equivalent DR program is described by the difference before and after removing a peaker based on: duration of deficit events by hour, event frequency(number of events in a year), and magnitude of deficits in MWs time between deficit events

26

Approach to Describing the Need

Case 1: Start at 5% LOLP Case 2: Remove X MW of Peaker Capacity Compare: Difference Between Case 1 and Case 2 Identifies the Impact:

– PSE’s RAM Allows a Simulation-by-Simulation Comparison – Additional simulations that will experience resource deficiency(ies) – Magnitude of Deficiencies in bad simulations – Frequency of resource deficiencies within a “bad” simulation – Duration of resource deficiencies within a “bad” simulation – Time between resource deficiencies

27

Using a Layered Approach

February 3, 2017 IRPAG

The Greater the Capacity Need to Fill, the Larger the “Hole” • In capacity, but also possibly frequency, duration, and time between resource

deficiencies

Examining Layers Avoids Over-Specifying What Would be Needed from DR • Avoids possibly over-stating the capacity, frequency, and duration • Therefore avoids overstating the cost of DR required

Approach • A 200 MW DR resource can be broken down into smaller, possibly more cost

effective steps.

Steps • Started with portfolio at 5% LOLP • Subtract 25 MW Peaker: Compare with above

– Impact on frequency, duration, and time between deficiencies • Subtracted additional 25 MW (50 MW Total): Compare with above • Subtracted additional 70 MW (120 MW Total): Compare with above • Subtracted additional 80 MW (200 MW Total): Compare with above

28

Summary of Results

February 3, 2017 IRPAG

LOLP Only: DR calls at most 2x a year for a maximum of 2 hour duration

LOLP + EUE: DR calls at most 6x a year for a maximum of 5-8 hour duration

Scenarios LOLP Only Duration (hours)

LOLP Only Frequency

LOLP+EUE Duration (hours)

LOLP+EUE Frequency

Base less 25MW 2 1 5 6 Base less 25 MW more(-50MW) 2 2 6 6 Base less 70 MW more(-120MW) 2 2 7 6 Base less 80 MW more(-200MW) 2 2 8 6

If All We Cared About Was LOLP

If We Needed to Make Portfolio

Whole

29

Analysis Approach

February 3, 2017 IRPAG

Assumes DR is dispatchable, peaker has a 3% forced outage rate

DR programs are stackable based on size

From a base portfolio where 5% LOLP is achieved, reduce peaker capacity by some MWs incrementally

Examine the characteristics of incremental deficits created by the reduction in peaker capacity

LOLP EUE Simulations with Deficits

Number of Deficit Events

Base 5% 34.6 306 522

Base less 25MW 5.4% 39.7 335 (+29) 592 (+70)

Base less 50MW 6.1% 44.4 376 (+41) 667 (+75)

Base less 120MW 7.2% 64.0 441 (+65) 837 (+170)

Base less 200MW 8.9% 95.6 550 (+109) 1129 (+292)

30

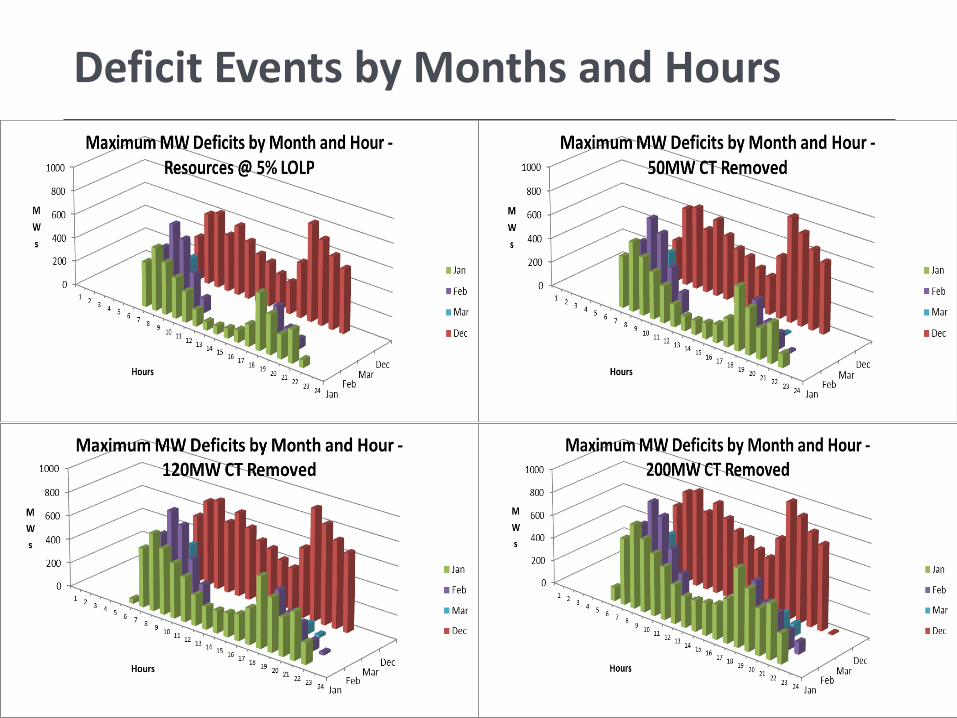

Deficit Events by Months and Hours

31

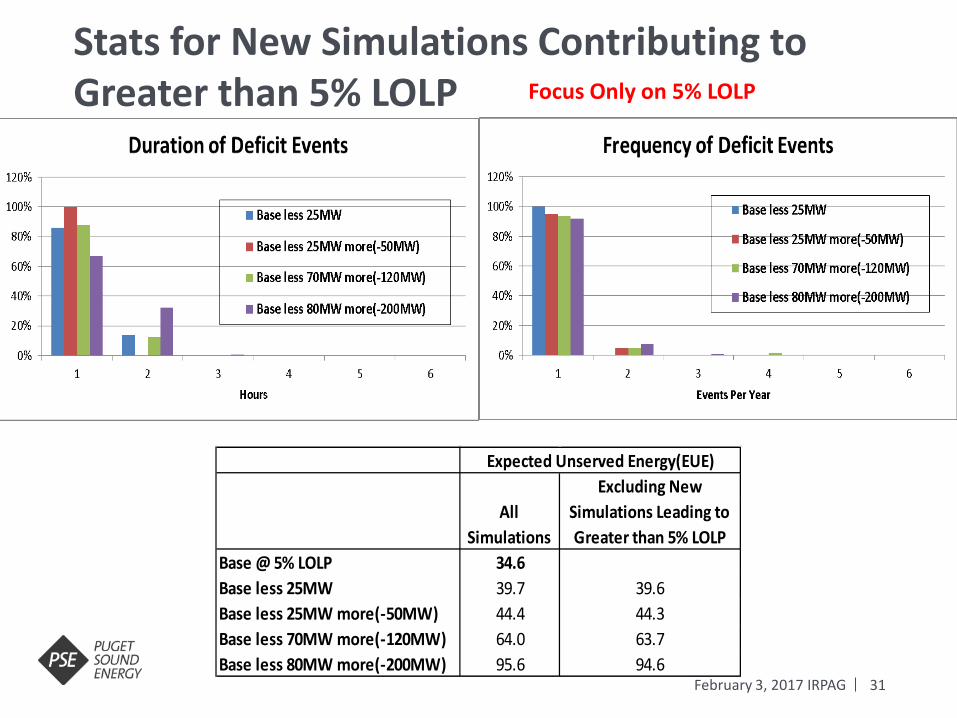

Stats for New Simulations Contributing to Greater than 5% LOLP

February 3, 2017 IRPAG

Excluding NewAll

SimulationsSimulations Leading to Greater than 5% LOLP

Base @ 5% LOLP 34.6Base less 25MW 39.7 39.6Base less 25MW more(-50MW) 44.4 44.3Base less 70MW more(-120MW) 64.0 63.7Base less 80MW more(-200MW) 95.6 94.6

Expected Unserved Energy(EUE)

Focus Only on 5% LOLP

32

Duration of Deficit Events for all Simulations With Deficit (Incremental Impact Only)

Make Portfolio Whole

33

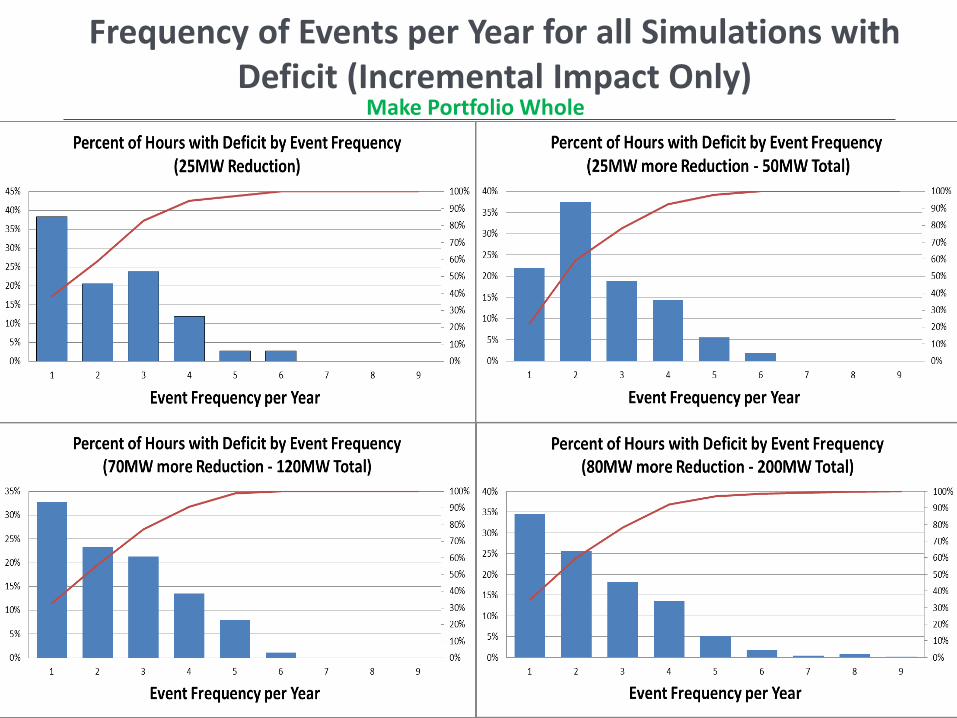

Frequency of Events per Year for all Simulations with Deficit (Incremental Impact Only)

Make Portfolio Whole

34

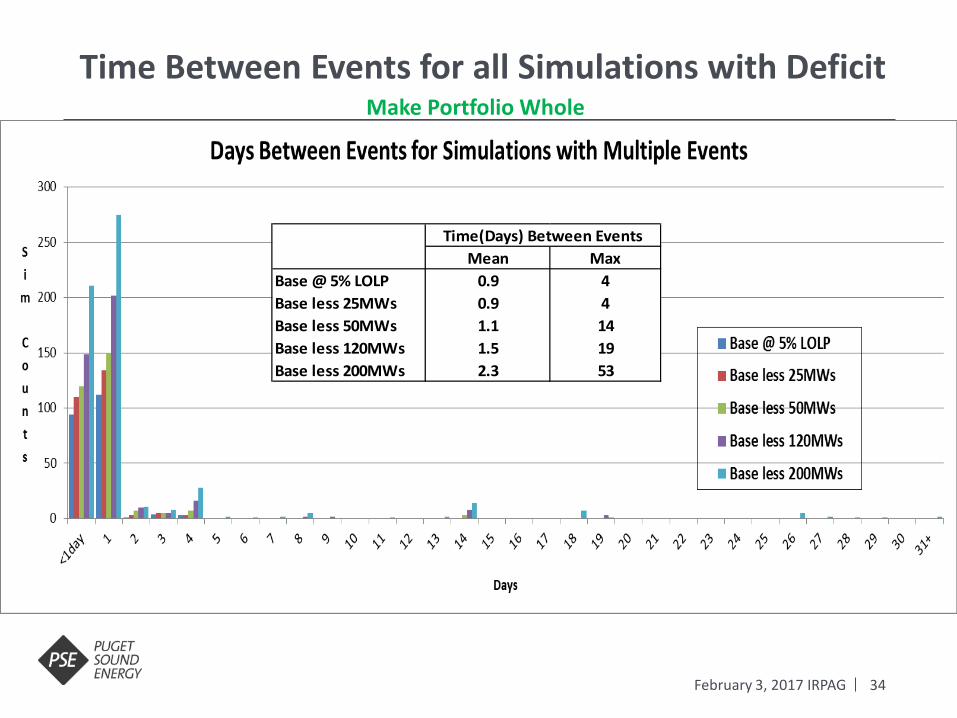

Time Between Events for all Simulations with Deficit

February 3, 2017 IRPAG

Mean MaxBase @ 5% LOLP 0.9 4Base less 25MWs 0.9 4Base less 50MWs 1.1 14Base less 120MWs 1.5 19Base less 200MWs 2.3 53

Time(Days) Between Events

Make Portfolio Whole

35

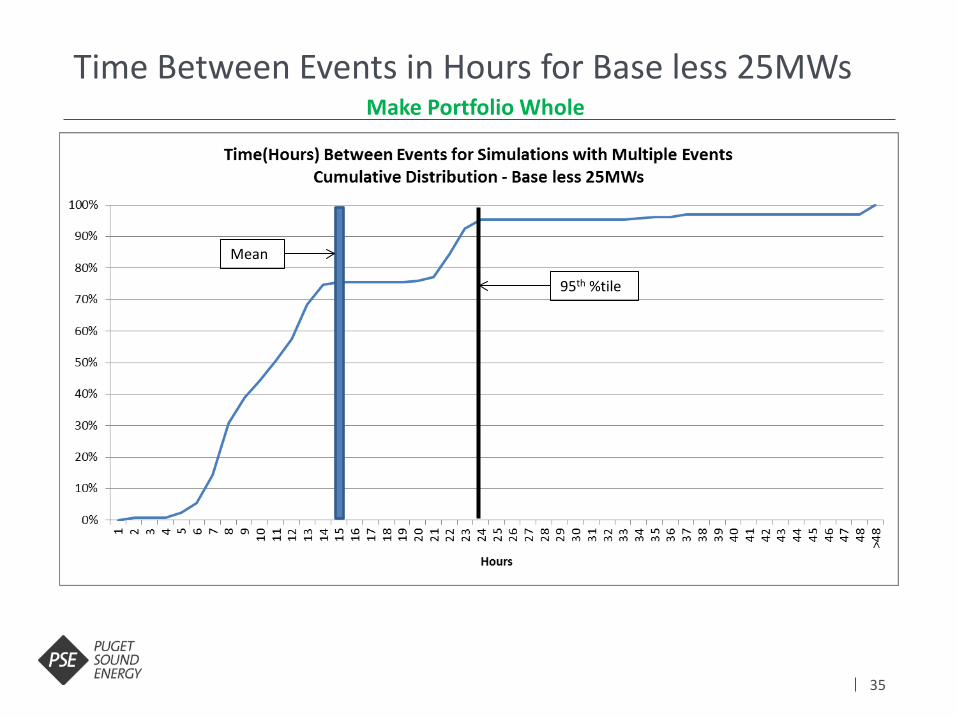

Time Between Events in Hours for Base less 25MWs Make Portfolio Whole

Mean

95th %tile

36

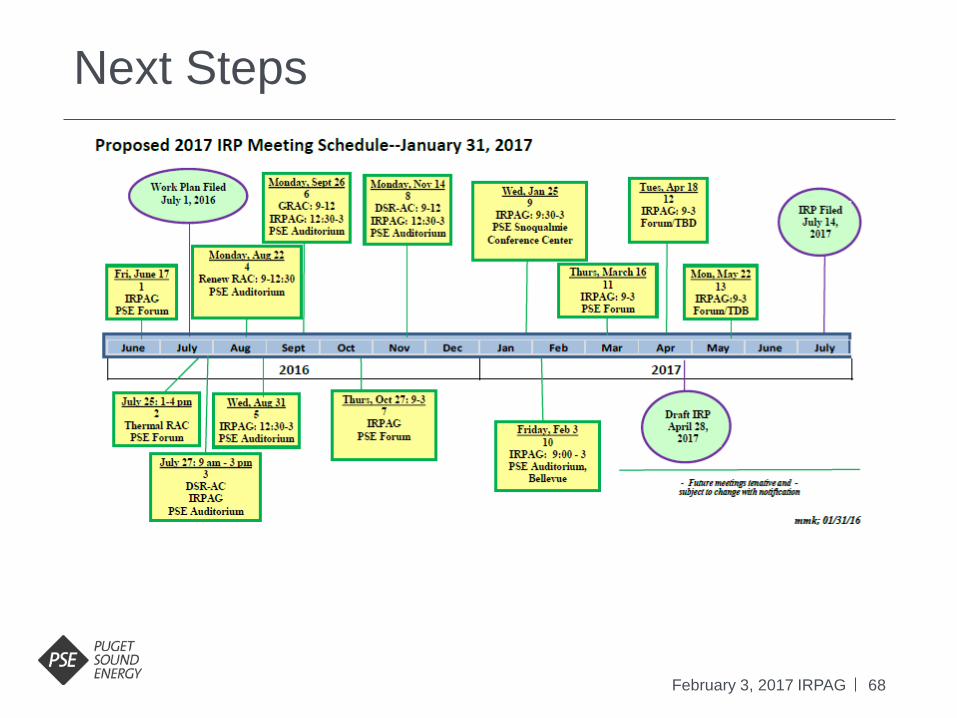

Next Steps

February 3, 2017 IRPAG

Refine analysis of time between deficiencies to hourly rather than daily

Examine tradeoff between duration and time between deficiencies • Example, a 6 hour DR event might cover multiple deficiencies

Consider working with Navigant to refine potential assessment to shape DR to fit PSE’s resource need. Consider just estimating the ELCC of a 4-hour, once a day or twice a day demand response resource of a given MW magnitude, or variations thereof. Next IRP: Examine the ELCC implications of day-ahead demand response • Not effective for covering resource deficiencies created by forced

outages…or not totally effective.

Resource Costs & Portfolio Sensitivities Discussion

February 3, 2017 IRPAG

38

Purpose of Generic Resources

February 3, 2017 IRPAG

• Resource decisions are not made in the IRP. Acquisition decisions are made in a separate process as detailed in WAC 480-107.

• In the acquisition process, generic resource costs for near-term decisions are replaced with actual resource alternatives.

• Generic resource costs in the IRP are helpful just to let participants in the acquisition process know the range of what PSE thinks it may see for new resources, however, bidders will compete against each other with a PSE self-build as a back-stop.

• The alternatives evaluated in the RFP do not compete against the generic resources assumed in PSE’s IRP

39

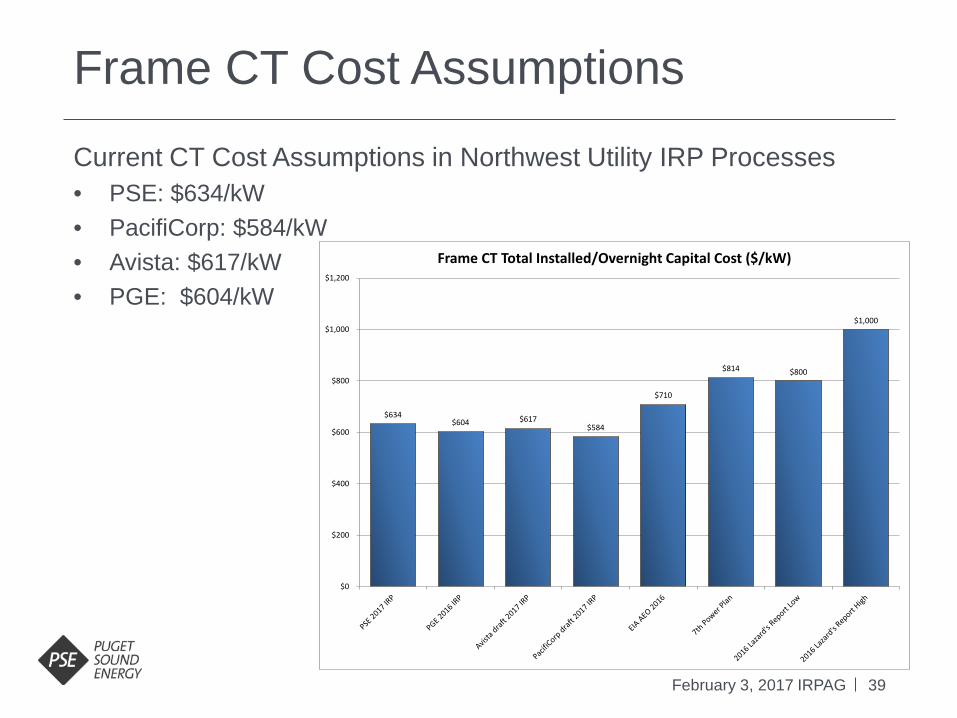

Frame CT Cost Assumptions

February 3, 2017 IRPAG

Current CT Cost Assumptions in Northwest Utility IRP Processes • PSE: $634/kW • PacifiCorp: $584/kW • Avista: $617/kW • PGE: $604/kW

$634 $604 $617

$584

$710

$814 $800

$1,000

$0

$200

$400

$600

$800

$1,000

$1,200

Frame CT Total Installed/Overnight Capital Cost ($/kW)

40

Other Thermal Plant Input

February 3, 2017 IRPAG

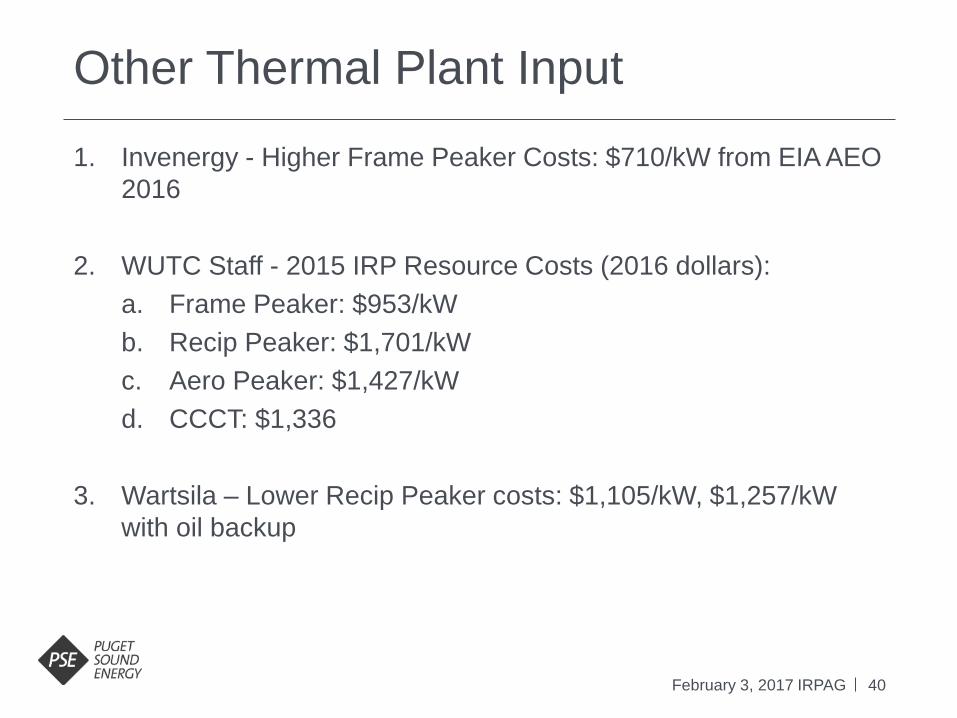

1. Invenergy - Higher Frame Peaker Costs: $710/kW from EIA AEO 2016

2. WUTC Staff - 2015 IRP Resource Costs (2016 dollars): a. Frame Peaker: $953/kW b. Recip Peaker: $1,701/kW c. Aero Peaker: $1,427/kW d. CCCT: $1,336

3. Wartsila – Lower Recip Peaker costs: $1,105/kW, $1,257/kW

with oil backup

41

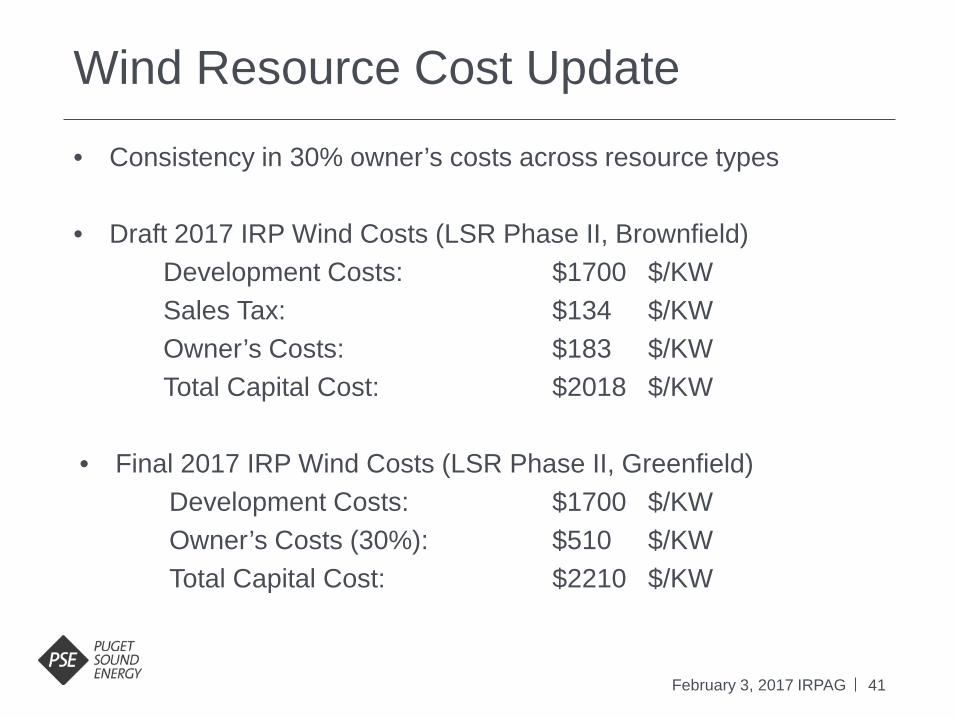

Wind Resource Cost Update

February 3, 2017 IRPAG

• Consistency in 30% owner’s costs across resource types • Draft 2017 IRP Wind Costs (LSR Phase II, Brownfield)

Development Costs: $1700 $/KW Sales Tax: $134 $/KW Owner’s Costs: $183 $/KW Total Capital Cost: $2018 $/KW

• Final 2017 IRP Wind Costs (LSR Phase II, Greenfield) Development Costs: $1700 $/KW Owner’s Costs (30%): $510 $/KW Total Capital Cost: $2210 $/KW

42

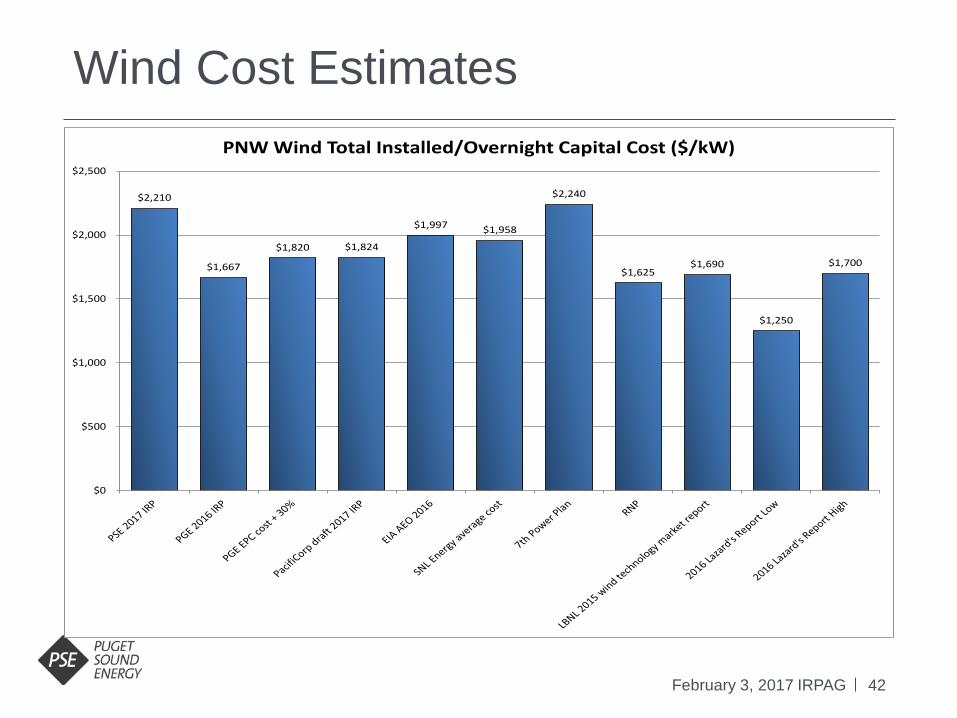

Wind Cost Estimates

February 3, 2017 IRPAG

$2,210

$1,667

$1,820 $1,824

$1,997 $1,958

$2,240

$1,625 $1,690

$1,250

$1,700

$0

$500

$1,000

$1,500

$2,000

$2,500

PNW Wind Total Installed/Overnight Capital Cost ($/kW)

43

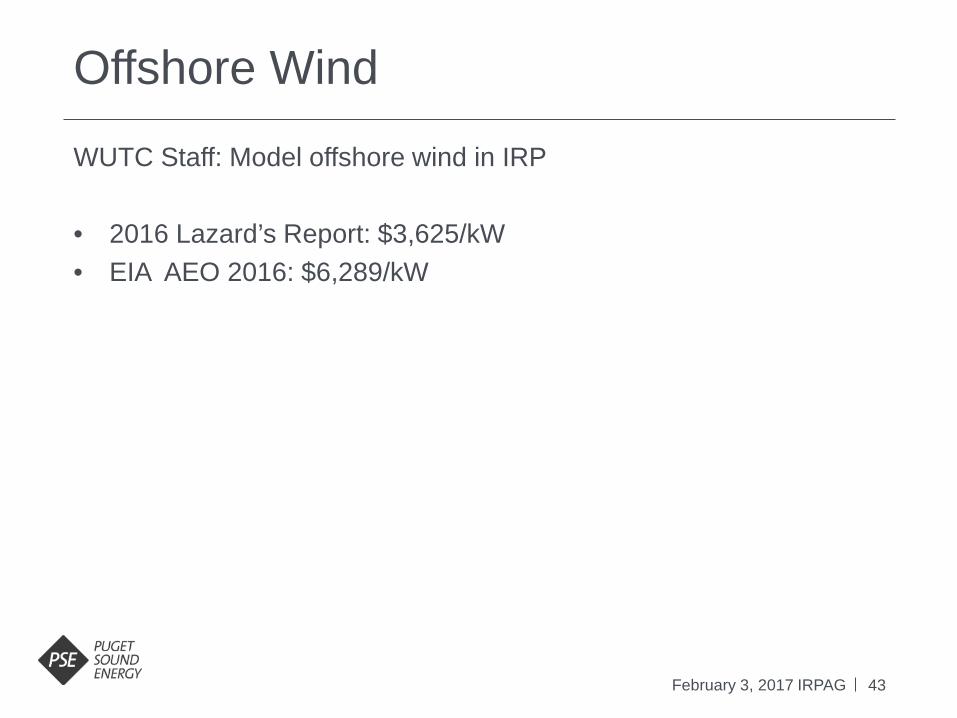

Offshore Wind

February 3, 2017 IRPAG

WUTC Staff: Model offshore wind in IRP • 2016 Lazard’s Report: $3,625/kW • EIA AEO 2016: $6,289/kW

44

Portfolio Sensitivities

February 3, 2017 IRPAG

Sensitivity Alternatives Analyzed A Colstrip

How do different retirement dates affect decisions about replacing Colstrip resources?

Baseline – Colstrip units 1&2 retire mid-2022, units 3&4 remain in service 1. Retire units 1&2 in 2018 2. Retire units 3&4 in 2030

B Demand-side Resources (DSR) How much does DSR reduce cost, risk and emissions?

Baseline – All cost-effective DSR per RCW 19.285 requirements 1. No DSR. All future needs met with supply-side resources.

C Thermal Mix How does changing the mix of resources affect portfolio cost and risk?

Baseline – Frame peakers selected as lowest cost addition in the Base Scenario deterministic portfolio 1. All CCCT additions 2. Mix of CCCT and frame peaker additions

D Gas Plant Location What if gas plants were built in eastern Washington instead of PSE service territory?

Baseline – Gas plants located in PSE Service territory 1. Model gas plants with gas transport costs and transmission costs from eastern Washington.

Highlighted sensitivities indicate stakeholder suggestions

45

Portfolio Sensitivities

February 3, 2017 IRPAG

Sensitivity Alternatives Analyzed E Gas Transport/Oil Backup for Peakers

What if peakers cannot rely on oil for backup fuel and must have firm gas supply instead?

Baseline – No firm pipeline capacity with 48 hours of oil backup 1. 100% firm pipeline capacity with no oil backup

F Energy Storage What is the cost difference between a portfolio with and without energy storage?

Baseline – Batteries and pumped hydro included only if chosen economically 1. Add X MW battery in 2022 instead of economically chosen peaker. 2. Add X MW pumped hydro storage in 2022 instead of economically chosen peaker.

G Montana Wind What if Montana wind was an RPS-eligible resource?

Baseline – Montana wind is not an RPS-eligible resource 1. Montana wind is an RPS-eligible resource

H Stakeholder-requested alternate resource costs and assumptions

Baseline – PSE cost estimate for generic supply-side resources 1. Lower Recip Peaker Cost 2. Higher thermal resource costs 3. Lower wind development cost 4. More aggressive cost curve for solar

Highlighted sensitivities indicate stakeholder suggestions

46

Portfolio Sensitivities

February 3, 2017 IRPAG

Sensitivity Alternatives Analyzed I No New Thermal

What would it cost to fill all future resources needs without new carbon emitting resources

Baseline – Gas-fired generation is an option in the optimization model 1. Remove carbon emitting resource alternatives to examine how this would affect the least-cost mix of resources.

J Renewable Resources + Energy Storage Does bundling renewable resources with energy storage change resource decisions?

Baseline – Renewable resources and energy storage evaluated as individual resources in the analysis 1. Bundle 200 MW battery + 200 MW wind

K Expanded Conservation Potential Baseline: Retrofit programs fully captured within 10-year accelerated ramp based on conservation potential assessment. 1. Assumes new, unforecasted efficiency measures are developed, such that the 10-year ramp continues for the full 20-year horizon.

Highlighted sensitivities indicate stakeholder suggestions

47

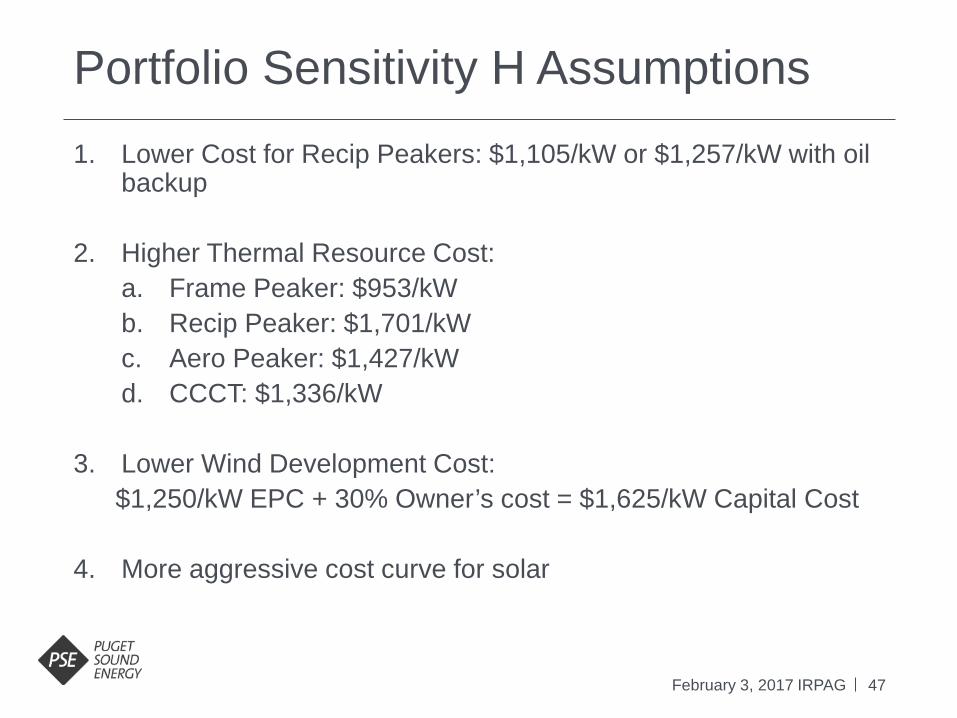

Portfolio Sensitivity H Assumptions

February 3, 2017 IRPAG

1. Lower Cost for Recip Peakers: $1,105/kW or $1,257/kW with oil backup

2. Higher Thermal Resource Cost: a. Frame Peaker: $953/kW b. Recip Peaker: $1,701/kW c. Aero Peaker: $1,427/kW d. CCCT: $1,336/kW

3. Lower Wind Development Cost: $1,250/kW EPC + 30% Owner’s cost = $1,625/kW Capital Cost

4. More aggressive cost curve for solar

48

Resource Assumptions Matrix

February 3, 2017 IRPAG

Montana Wind Transmission Assumptions

February 3, 2017 IRPAG

50

MT Wind Transmission Scenarios

February 3, 2017 IRPAG

• MT Wind Scenarios A. 75 Miles from Broadview with existing transmission B. 75 Miles from Colstrip with existing transmission C. 75 Miles from Broadview with transmission upgrades

51

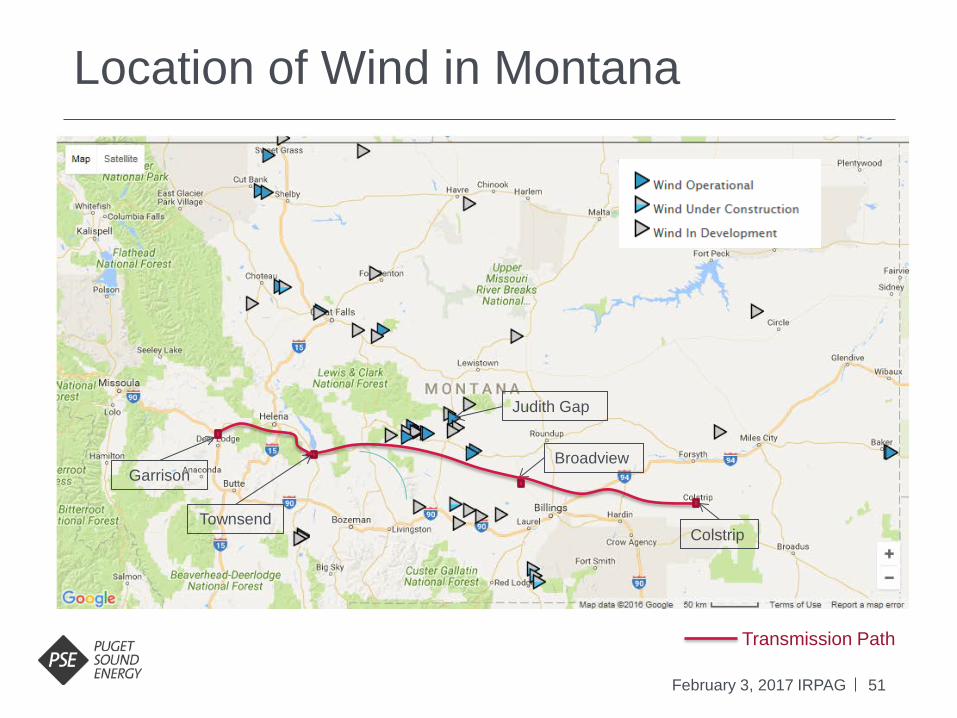

Location of Wind in Montana

February 3, 2017 IRPAG

Colstrip

Judith Gap

Broadview

Townsend

Garrison

Transmission Path

52 February 3, 2017 IRPAG

le.g.end - BPA, Losses = 1.9% +Formula losses on Townsend-Garrison

PSEI, LosS<>s ·= 2.7% • • • • Wind Project, Assume Losses : 2. 7%

Garrison

@ Judith Gap

o© ~ : ; :~ ~.' fl! • ,

Broadview Colstrip

Esti mates of lnte:rconnection Costs and Transmission Rates Options Interconnection Costs Transmission Rates ($/KW-Year)

A - Colstrip 1&2 Retired, 300MW, 75 Mi les Away to Broadview Sub $ B - Colstrip 1&2 Ret ired, 300MW, 75 Ml les Away to Colstrip Sub $ C - Colstrip 1&2 Retired, Above 300MW Wind, 75 Miles Away to Broadview Sub $

Assumpt ions and Scope of Est imates:

• Transmission capacity freed up by reti r ing Colst rip 1&2 is currently unknow n.

• Costs to mitigate transmission impacts of ret ir ing Colstrip 1&2 are currently unknown.

• Interconnection costs and t ransmission faci l ities costs are estimates based on previous

NorthWestern Energy {NWE) studies t hat assume Colstrip 1&2 ar·e not retfred.

• Costs exclude costs to bui ld generation.

• Costs exclude overheads.

52,200,000 $ 80.16

51,800,000 $ 80.16

52,200,000 S 80.16 +llmpactofcapacfty Increase on Rate

Wind Site Statistks Estimated Wind Capacity Percentage

MT Wind Capacity Factor 46.00% Loss Factor 7.30% Wind Capacity Net of Losses 42..64%

Transmission Rate Breakdown Transmission Rates $/KW-Year ~~~~~~~~~~~~

Colstrip to Townsend (PSEI) $ 31.83

Townsend to Garrison (BPA) $ 7.36 Garrison ito PSEI (BPA)1 $ 21 .62

Estimated Wind Integration Costs2 $ 19.34

Impact of Capacity Increase on Rate $ Uncertain 1 Rates from BP-18 Initial Proposal 2 201£ year a..erage of NWMT Energy Imbalance Prices

2017 IRP Gas Prices & Power Prices

February 3, 2017 IRPAG

54

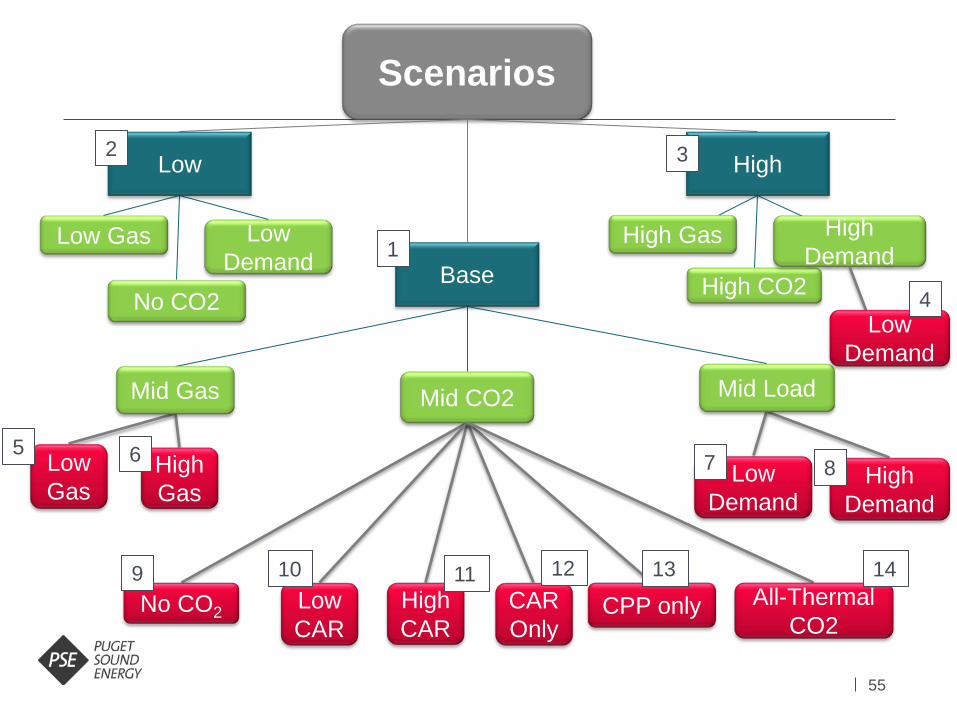

2017 IRP Scenarios

February 3, 2017 IRPAG

Scenario Demand Gas Price CO2 Regulation 1 Base Mid Mid Mid CAR to 2022, then CPP

2 Low Low Low Low CAR to 2022

3 High High High High CAR to 2022, then CPP

4 Low Demand + High Gas & CO2 Low High High CAR to 2022, then CPP

5 Base + Low Gas Price Mid Low Mid CAR to 2022, then CPP

6 Base + High Gas Price Mid High Mid CAR to 2022, then CPP

7 Base + Low Demand Low Mid Mid CAR to 2022, then CPP

8 Base + High Demand High Mid Mid CAR to 2022, then CPP

9 Base + No CO2 Mid Mid None

10 Base + Low CAR CO2 Mid Mid Low CAR to 2022, then CPP

11 Base + High CAR CO2 Mid Mid High CAR to 2022, then CPP

12 Base w/ CAR Only (electric only) Mid Mid Mid CAR indefinitely

13 Base w/ CPP Only (electric only) Mid Mid CPP in 2022

14 Base + All-Thermal CO2 (electric only)

Mid Mid CO2 price applied to all thermal resources in the WECC (baseload and peakers)

CAR: WA Clean Air Rule CPP: EPA Clean Power Plan

55

Scenarios

Low Gas

Mid Gas Mid CO2 Mid Load

Low Gas

High Gas

High CAR

No CO2

Low Demand

High Demand

Low High

Base

Low CAR

CAR Only

2

1

3

5 6 7 8

9 10 12 11 CPP only All-Thermal

CO2

No CO2

14

High CO2

Low Demand

High Gas High Demand

Low Demand

4

13

56

2017 IRP Gas prices

February 3, 2017 IRPAG

• Base 2018-2021: 3 month average forward marks from Sep 23 thru Dec 27, 2016 (65 business days) 2022-2037: Wood Mackenzie Fall 2016 long term fundamentals forecast

• Low

2018-2037: Wood Mackenzie long term low forecast

• High 2018-2037: Wood Mackenzie long term high forecast

57

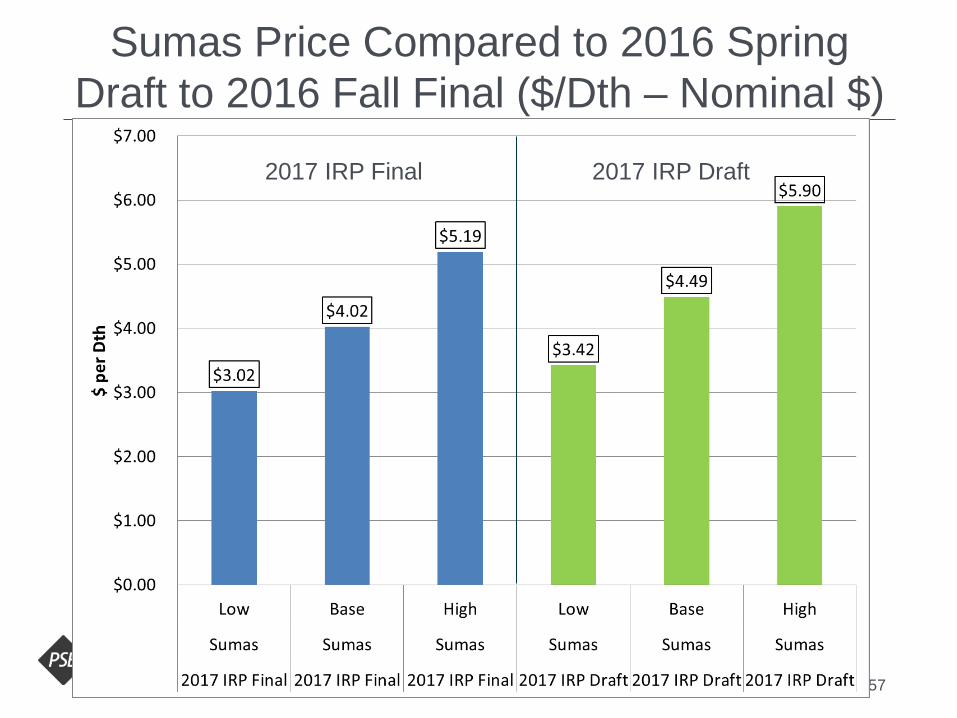

Sumas Price Compared to 2016 Spring Draft to 2016 Fall Final ($/Dth – Nominal $)

2017 IRP Final 2017 IRP Draft

58

Levelized Sumas Price ($/Dth – Nominal $)

59

Sumas Price Compared to Past IRPs

$7

.85 $1

0.01

$7.3

5

$8.0

8

$6.0

6

$5.3

7

$4.0

2

$0.3

6

$3.0

4

$3.0

4

$1.4

6

$3.11

$0.00

$2.00

$4.00

$6.00

$8.00

$10.00

$12.00

$14.00

2007 IRP 2009 IRP 2009 IRP Update 2011 IRP 2013 IRP 2015 IRP 2017 IRP

(2008-2027) (2010-2029) (2010-2029) (2012-2031) (2014-2033) (2016-2035) (2018-2037)

$ pe

r Dth

CO2 priceBase gas price

60

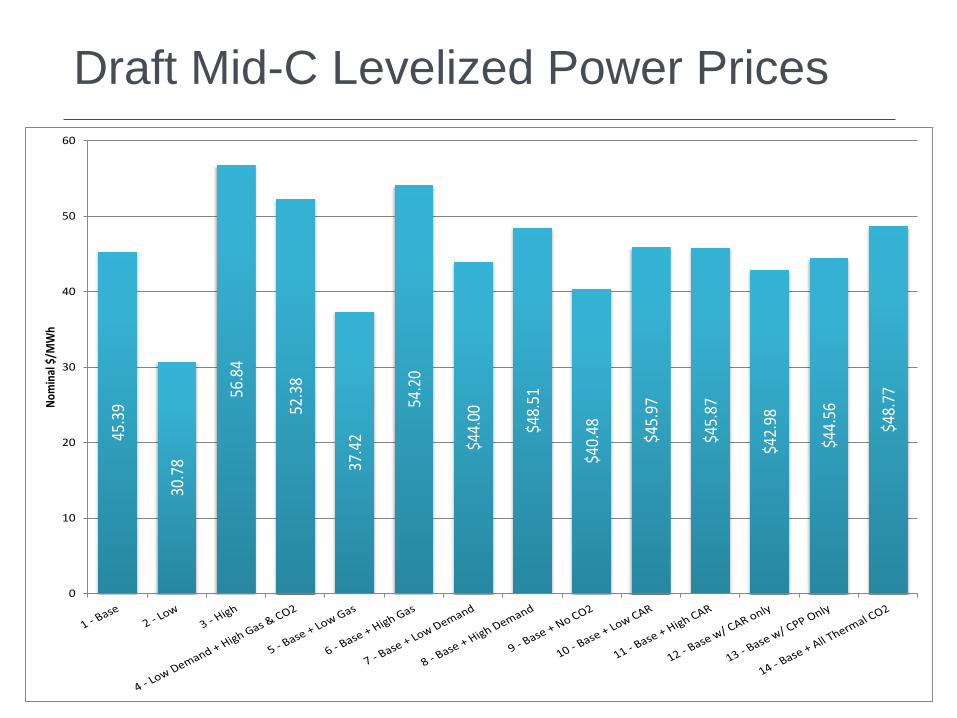

Draft Mid-C Levelized Power Prices

45

.39

30.7

8

56.8

4

52.3

8

37.4

2

54.2

0

$44.

00

$48.

51

$40.

48

$45.

97

$45.

87

$42.

98

$44.

56

$48.

77

0

10

20

30

40

50

60

Nom

inal

$/M

Wh

61

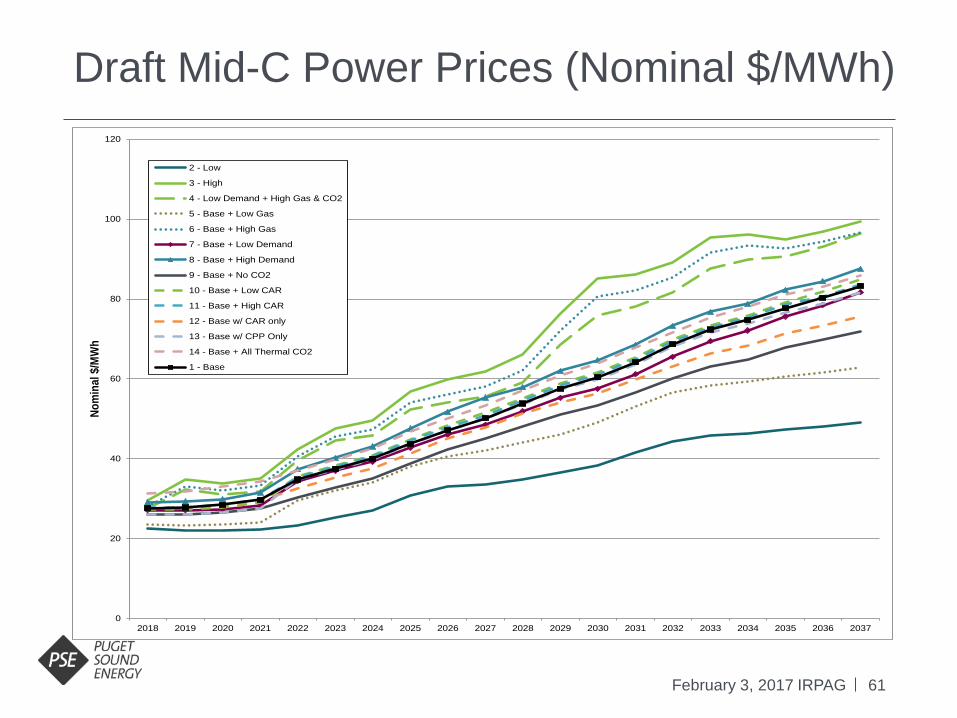

Draft Mid-C Power Prices (Nominal $/MWh)

February 3, 2017 IRPAG

0

20

40

60

80

100

120

2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 2031 2032 2033 2034 2035 2036 2037

Nom

inal

$/M

Wh

2 - Low

3 - High

4 - Low Demand + High Gas & CO2

5 - Base + Low Gas

6 - Base + High Gas

7 - Base + Low Demand

8 - Base + High Demand

9 - Base + No CO2

10 - Base + Low CAR

11 - Base + High CAR

12 - Base w/ CAR only

13 - Base w/ CPP Only

14 - Base + All Thermal CO2

1 - Base

62

Draft 2017 IRP Mid-C Prices vs. 2015 IRP

February 3, 2017 IRPAG

0

20

40

60

80

100

120

140

160

2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 2031 2032 2033 2034 2035 2036 2037

Nom

inal

$/M

Wh

2015 IRP Base2015 IRP Low2015 IRP High2017 IRP Base2017 IRP Low2017 IRP High

63

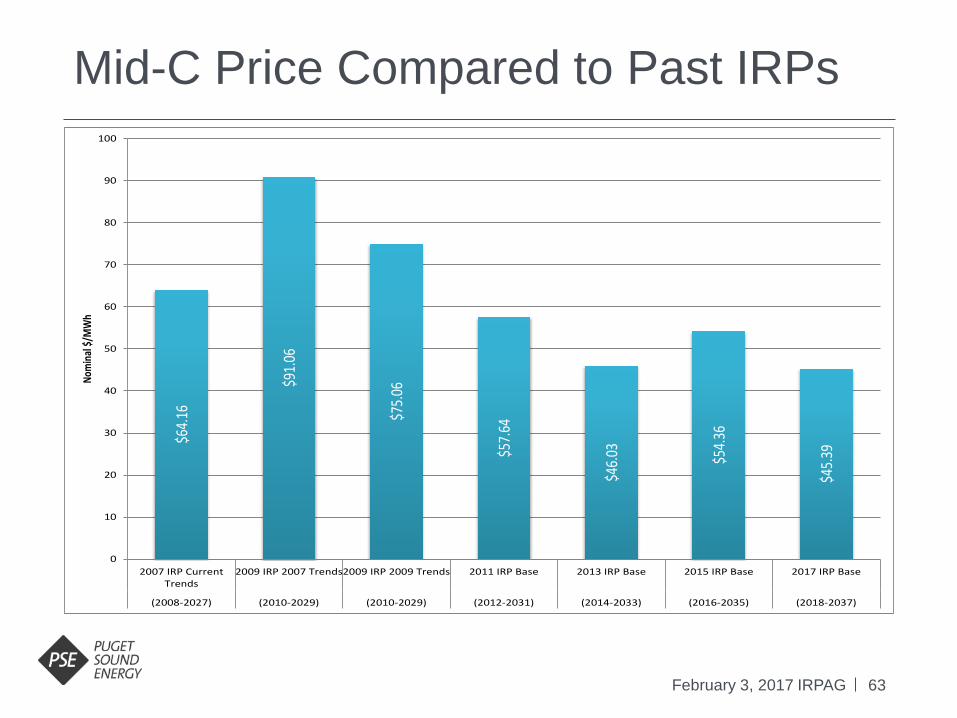

Mid-C Price Compared to Past IRPs

February 3, 2017 IRPAG

$64.1

6

$91.0

6

$75.0

6

$57.6

4

$46.0

3

$54.3

6

$45.3

9

0

10

20

30

40

50

60

70

80

90

100

2007 IRP CurrentTrends

2009 IRP 2007 Trends2009 IRP 2009 Trends 2011 IRP Base 2013 IRP Base 2015 IRP Base 2017 IRP Base

(2008-2027) (2010-2029) (2010-2029) (2012-2031) (2014-2033) (2016-2035) (2018-2037)

Nom

inal

$/M

Wh

64

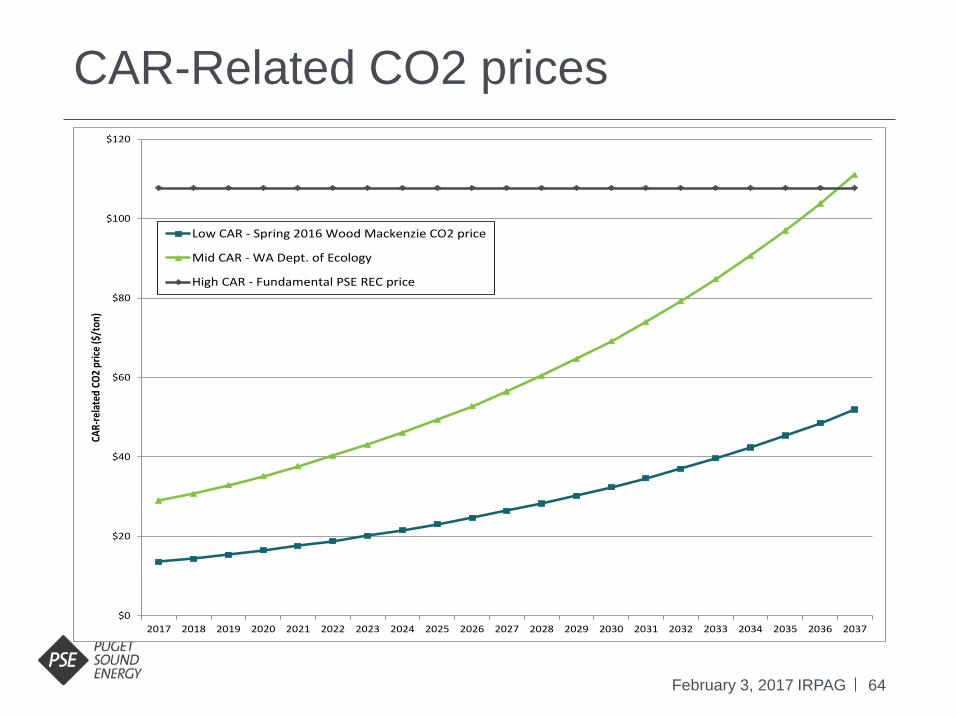

CAR-Related CO2 prices

February 3, 2017 IRPAG

$0

$20

$40

$60

$80

$100

$120

2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 2031 2032 2033 2034 2035 2036 2037

CAR-

rela

ted

CO2

price

($/t

on)

Low CAR - Spring 2016 Wood Mackenzie CO2 price

Mid CAR - WA Dept. of Ecology

High CAR - Fundamental PSE REC price

65

Electric CO2 price scenarios

February 3, 2017 IRPAG

$0

$20

$40

$60

$80

$100

$120

2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 2031 2032 2033 2034 2035 2036 2037

CO2

price

($/t

on)

High, Base + High CAR

Base + No CPP (WA only)

Base

Base + Low CAR

Low

Base + No CAR

WA CAR WECC CO2

66

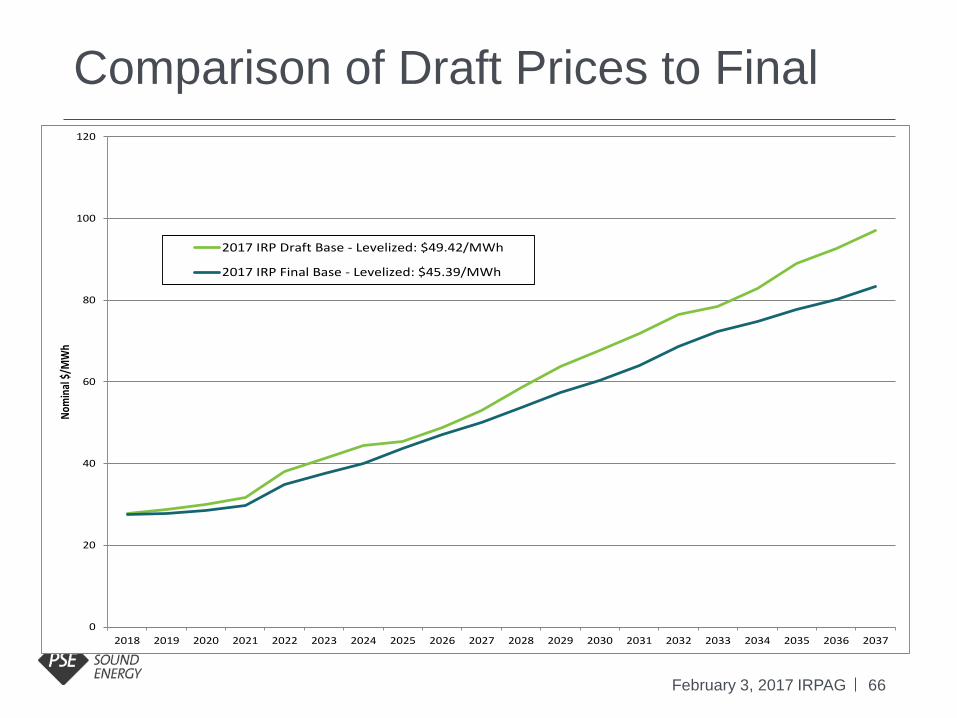

Comparison of Draft Prices to Final

February 3, 2017 IRPAG

0

20

40

60

80

100

120

2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 2031 2032 2033 2034 2035 2036 2037

Nom

inal

$/M

Wh

2017 IRP Draft Base - Levelized: $49.42/MWh

2017 IRP Final Base - Levelized: $45.39/MWh

Wrap-up/Review

February 3, 2017 IRPAG

68

Next Steps

February 3, 2017 IRPAG

69

THANK YOU

February 3, 2017 IRPAG