Harley -Davidson, Inc. - marketscreener.com fileHarley -Davidson, Inc. - marketscreener.com

2017 Interim Results

August 2017

2

Cautionary Statements Regarding Forward-Looking Statement

To the extent any statements made in this presentation containing information that is not historical are essentially

forward-looking. These forward-looking statements include but are not limited to projections, targets, estimates and

business plans that the Company expects or anticipates will or may occur in the future. These forward-looking

statements are subject to known and unknown risks and uncertainties that may be general or specific. Certain

statements, such as those including the words or phrases "potential", "estimates", "expects", "anticipates",

"objective", "intends", "plans", "believes", "will", "may", "should", and similar expressions or variations on such

expressions may be considered forward-looking statements.

Readers should be cautioned that a variety of factors, many of which may be beyond the Company's control, affect

the performance, operations, and results of the Company, and could cause actual results to differ materially from the

expectations expressed in any of the Company's forward-looking statements. These factors include but are not

limited to exchange rate fluctuations, market shares, competition, environmental risks, changes in legal, financial

and regulatory frameworks, international economic and financial market conditions, and other risks and factors

beyond our control. These and other factors should be considered carefully, and readers should not place undue

reliance on the Company's forward-looking statements. In addition, the Company undertakes no obligation to

publicly update or revise any forward-looking statement that is contained in this presentation as a result of new

information, future events, or otherwise. None of the Company, or any of its employees or affiliates is responsible

for, or is making, any representation concerning the future performance of the Company.

Contents

3

Overview

Customer Development

Business Review

Financial Review

4

Overview Financial

Review

Customer

Development Business Review

Overview

Chairman and CEO Peter Ma

5

Ping An's strategy: A World-leading Personal

Financial Services Provider

World-leading

Personal Financial Services Provider

Pan Financial Assets Pan Health Care

Financial

Services

Ecosystem

Real Estate

Finance

Ecosystem

Auto

Services

Ecosystem

Health

Care

Ecosystem

Two

Focuses

One

Positioning

Four Service

Ecosystems

6

Financial Review

Group CFO Jason Yao

Overview Financial

Review

Customer

Development Business Review

7

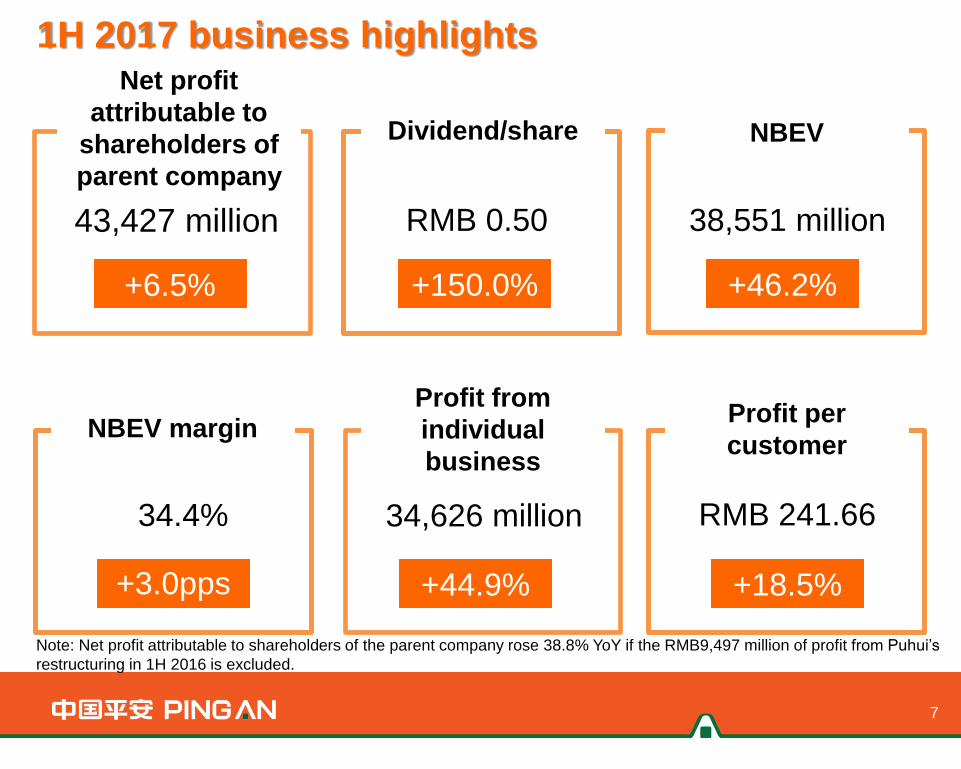

1H 2017 business highlights

Dividend/share

43,427 million

+6.5% +46.2% +150.0%

+18.5% +44.9%

Profit from

individual

business

34.4%

+3.0pps

NBEV

Profit per

customer NBEV margin

Net profit

attributable to

shareholders of

parent company

38,551 million RMB 0.50

34,626 million RMB 241.66

Note: Net profit attributable to shareholders of the parent company rose 38.8% YoY if the RMB9,497 million of profit from Puhui’s

restructuring in 1H 2016 is excluded.

Sustained business growth

Revenue Net Profit attributable to shareholders

of the parent company/EPS

8

23.4%

7.2%

6.5%

11.0%

407,828

503,143 40,776 43,427

2.28 2.43

10.6% 11.6%

5,576,903 5,978,688

425,780 383,449

(in RMB million/in RMB)

Dec 31, 2016 Jun 30, 2017

1H 2016 1H 2017

Dec 31, 2016/

1H 2016

Jun 30, 2017/

1H 2017

1H 2016 1H 2017

Note: Revenues are reported under the International Financial Reporting Standards (IFRS).

Total assets Equity attributable to shareholders of the

parent company/ROE(not annualized)

9

Profit contribution by business lines

Property and casualty

insurance 0.4

The Group

Banking business

Securities business

Life and health insurance 36.7

2.1

(3.1)

Trust business 152.0

Other asset management

15.8

100.0

16.8

2.6

54.3

5.2

8.2 92.0

6.5

6,861

43,427

7,281

1,142

23,576

2,260

3,557

Internet finance (94.7)

Others & elimination

0.9

(3.8) (26.2)

420

(1,670)

1H 2017 (in RMB million)

YoY change(%)

Notes: (1) In 1H2017, the Company redefined its business segments to provide clear and concise information.

(2) The other asset management business represents subsidiaries such as Ping An Asset Management and Ping An Financial Leasing. Elimination

includes offsets against cross-shareholding among business lines.

(3) If the RMB9,497 million of profit from Puhui’s restructuring in 1H 2016 is excluded, the profit contributed by the internet finance business

increased sharply, and the Group’s profit rose 38.8% YoY.

Proportion(%)

1H 2016

6,834

40,776

7,130

1,178

17,243

897

1,853

7,905

(2,264)

10

1H 2017 net assets and ROE of business lines

Property and casualty

insurance (0.8)

The Group

Banking business

Securities business

Life and health insurance 2.6

(1.2)

(0.4)

Trust business 6.5

Other asset management

15.7

100.0

28.8

5.9

33.2

4.8

11.6 1.8

(1.0)

66,869

425,780

122,643

25,210

141,308

20,560

49,442

Internet finance (44.1)

Others & elimination

4.8

(4.8) NA

20,291

(20,543)

Amount Proportion(%)

10.5

10.6

6.2

4.6

18.1

11.5

7.2

1.2

NA

Not annualized

(%)

Net assets attributable to

parent company YoY change

(pps)

ROE

(in RMB million)

11

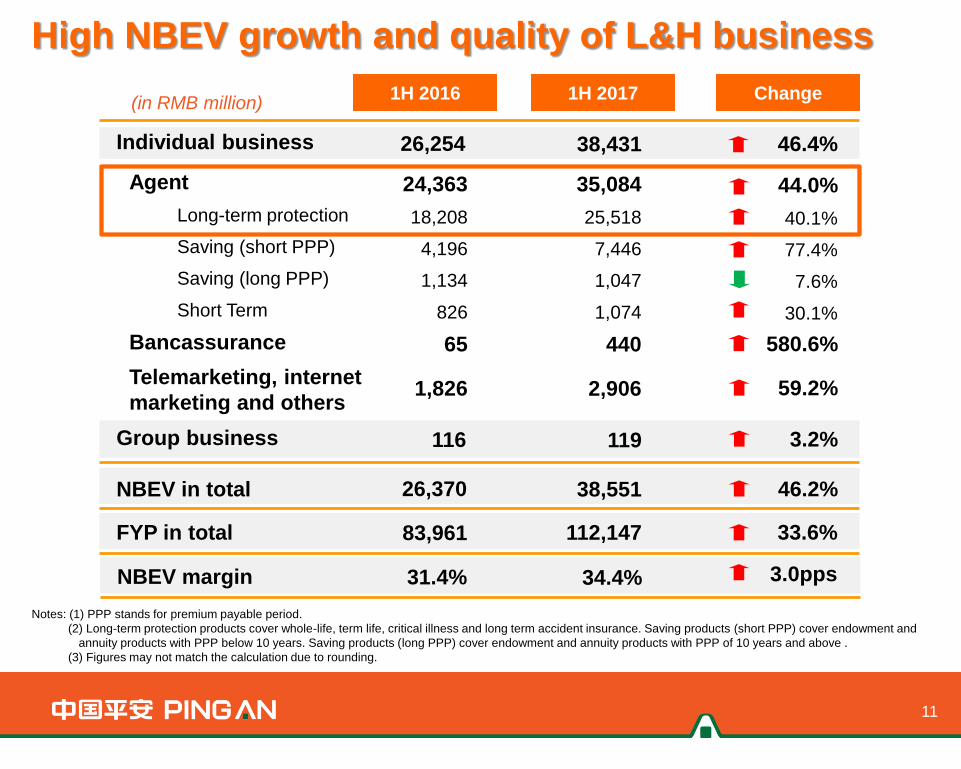

3.2% 116 119 Group business

(in RMB million)

Agent

Long-term protection

Saving (short PPP)

Saving (long PPP)

Short Term

Bancassurance

Telemarketing, internet

marketing and others

24,363

18,208

4,196

1,134

826

65

1,826

1H 2016

26,254 38,431 46.4% Individual business

1H 2017 Change

35,084

25,518

7,446

1,047

1,074

440

2,906

44.0%

40.1%

77.4%

7.6%

30.1%

580.6%

59.2%

26,370 38,551 46.2% NBEV in total

83,961 112,147 33.6% FYP in total

31.4% 34.4% 3.0pps NBEV margin

Notes: (1) PPP stands for premium payable period.

(2) Long-term protection products cover whole-life, term life, critical illness and long term accident insurance. Saving products (short PPP) cover endowment and

annuity products with PPP below 10 years. Saving products (long PPP) cover endowment and annuity products with PPP of 10 years and above .

(3) Figures may not match the calculation due to rounding.

High NBEV growth and quality of L&H business

NBEV growth driven by agent force and productivity

Note: The reason why above average agent force*6*new policies per agent per month*premium income per policy is slightly higher than total

first-year premium in the agent channel is that premiums generated from policies of the internet channel but sold by agents are accounted in

other channels.

Delivered increases in both

agent force and productivity

12

26,370

NBEV

38,551

35,084

24,363

Agent channel’s

NBEV

Other channels’

NBEV

3,467

2,007

First-year premium

NBEV margin

41.5%

42.9%

Average agent force

(’000 persons)

940

1,170

New policies per

agent per month

1.39

1.32

7,984

8,964

Premium income

per policy (in RMB)

44.0%

46.2%

72.8%

24.5%

5.3%

12.3%

1.4

pps

84,596

56,771

49.0%

(in RMB million)

1H 2016

1H 2017

Steady growth of Group EV

739,144

278,639

460,505

15.9%

21.0%

13.1%

230,363

407,340

637,703

739,144

446,600

292,544

15.9%

23.9%

5.5%

360,312

277,391

637,703

13

Embedded Value per Share @ Dec 31, 2016 = RMB 34.88

Embedded Value per Share @ Jun 30, 2017 = RMB 40.43

Value of in-

force

business

Adjusted

net asset

value

Life and health

insurance

business

Other

businesses

Dec 31, 2016 Jun 30, 2017 Jun 30, 2017 Dec 31, 2016

(in RMB million)

Group operating ROEV (not annualized): 15.4%

736,209 739,144

637,703 17,641

48,544 12,469 19,851 12,990 (10,054)

End-2016

Group EV

Expected

return on

EV

Operating

contribution

and others

of L&H

2017

interim

Group EV

EV operating profit of the Group: RMB 98,506 million

Value

generation

of new

business

Notes: (1) Value generation of new business includes NBEV and risk diversification effects.

(2) Operating contribution and others of L&H include operating assumptions and model changes(RMB90 million), operating variances

and others of life and health insurance business(RMB12,380 million).

(3) Investment variances and others include economic assumption changes, market value adjustments and investment variances.

Group EV

before non-

operating

variances

14

Investment

variances

and others

Dividend

paid

Net profit of

other

businesses

(in RMB million)

+15.4%

L&H operating ROEV (not annualized): 21.8%

438,966 446,600

360,312 17,641

48,544 12,469

13,856 (6,223)

End-2016

L&H EV

Expected

return on

EV

Operating

contribution

and others

2017

interim L&H

EV

EV operating profit of L&H: RMB 78,654 million

Value

generation

of new

business

L&H EV before

non-operating

variances

15

Dividend

paid

+21.8%

(in RMB million)

Notes: (1) Value generation of new business includes NBEV and risk diversification effects.

(2) Operating contribution and others include operating assumptions and model changes(RMB90 million), operating variances and

others of life and health insurance business(RMB12,380 million).

(3) Investment variances and others include economic assumption changes, market value adjustments and investment variances.

Investment

variances

and others

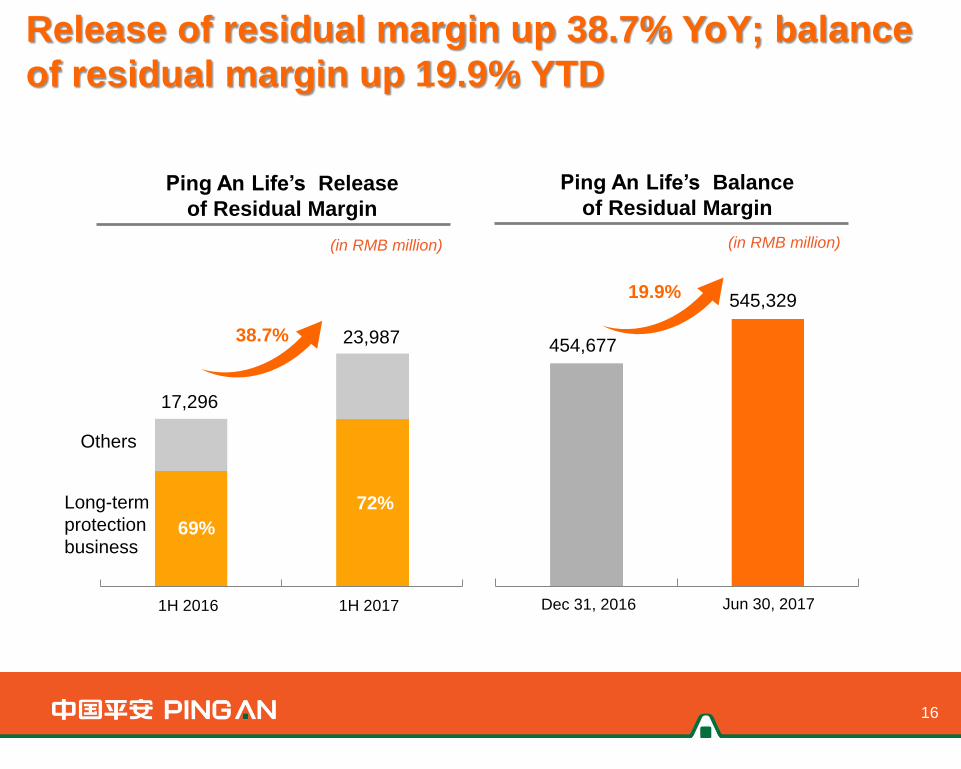

69%

72%

Release of residual margin up 38.7% YoY; balance

of residual margin up 19.9% YTD

Ping An Life’s Release

of Residual Margin

16

(in RMB million)

Ping An Life’s Balance

of Residual Margin

Others

Long-term

protection

business

38.7% 23,987

17,296

545,329

454,677

19.9%

1H 2016 1H 2017 Dec 31, 2016 Jun 30, 2017

(in RMB million)

267.3%

210.0%

Dec 31, 2016 Jun 30, 2017

225.9%

11.53%

245.4%

211.1%

232.6%

11.23%

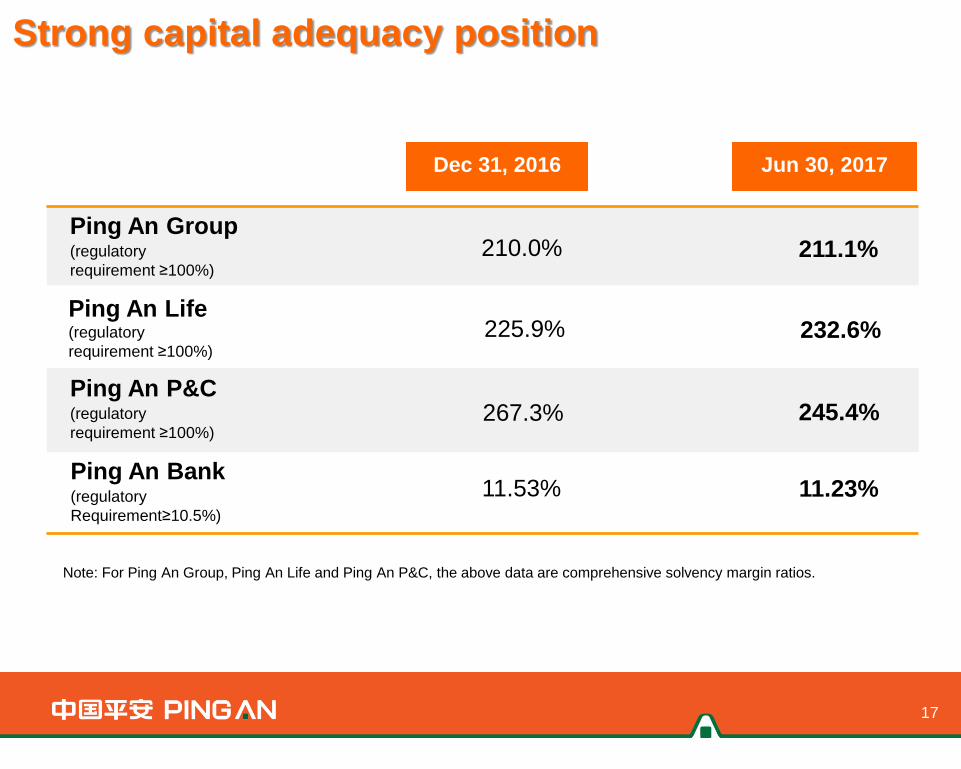

Strong capital adequacy position

17

Ping An Group (regulatory

requirement ≥100%)

Ping An P&C (regulatory

requirement ≥100%)

Ping An Life (regulatory

requirement ≥100%)

Ping An Bank (regulatory

Requirement≥10.5%)

Note: For Ping An Group, Ping An Life and Ping An P&C, the above data are comprehensive solvency margin ratios.

18 18

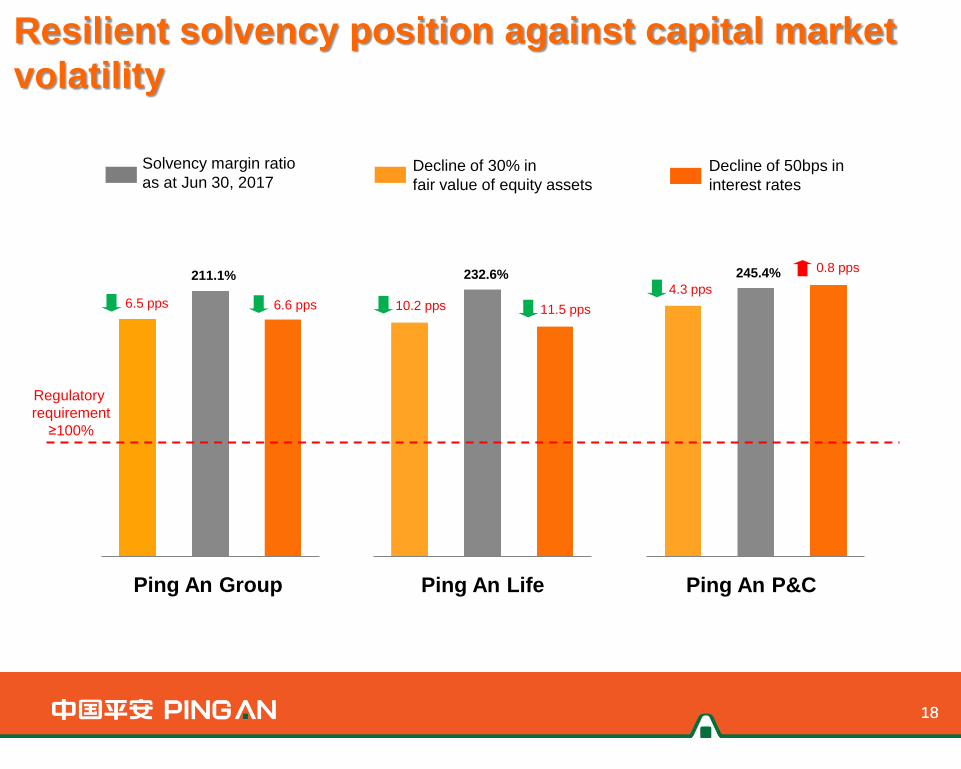

Ping An Group

Regulatory

requirement

≥100%

Ping An Life Ping An P&C

Solvency margin ratio

as at Jun 30, 2017 Decline of 30% in

fair value of equity assets

Decline of 50bps in

interest rates

Resilient solvency position against capital market

volatility

211.1%

6.5 pps

232.6% 245.4%

6.6 pps 10.2 pps 11.5 pps

4.3 pps

0.8 pps

Interim dividend: up 150% year on year

(in RMB million)

19

Profit size Business growth Capital

requirements

Sustainability of distribution

policy

RMB 0.50/share

RMB 0.20/share

Dividend

payout

ratio: 21.0%

Dividend

payout

ratio: 9.0%

We decided to increase dividends

given improving core profitability

coupled with strong solvency

position.

2017 interim dividend distribution

plan: to pay a cash dividend of RMB

0.50 per share, totaling RMB 9,140

million, up 150% year on year. 1H 2016 1H 2017

150%

3,656

9,140

20

Customer Development

Group CFO Jason Yao

Overview Financial

Review

Customer

Development Business Review

1H 2016/Jun 30, 2016

1H 2017/Jun 30, 2017

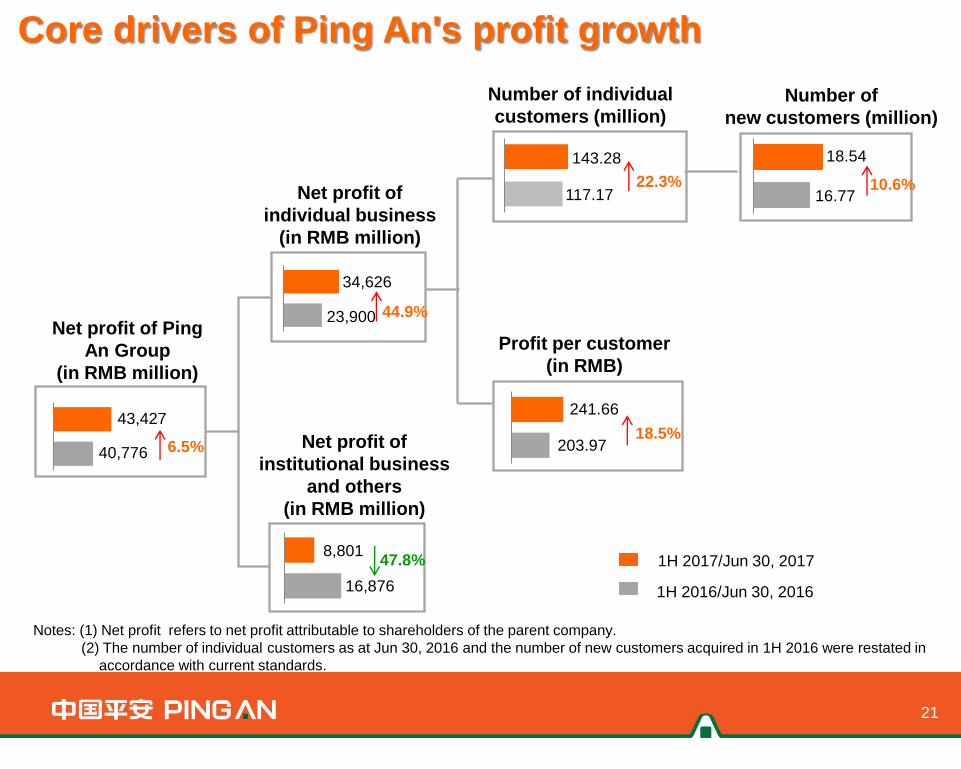

Core drivers of Ping An's profit growth

21

Notes: (1) Net profit refers to net profit attributable to shareholders of the parent company.

(2) The number of individual customers as at Jun 30, 2016 and the number of new customers acquired in 1H 2016 were restated in

accordance with current standards.

Net profit of Ping

An Group

(in RMB million)

Net profit of

individual business

(in RMB million)

Net profit of

institutional business

and others

(in RMB million)

Number of individual

customers (million)

Profit per customer

(in RMB)

143.28

117.17 22.3%

18.5% 6.5%

44.9%

34,626

23,900

43,427

40,776

8,801

16,876

241.66

203.97

47.8%

Number of

new customers (million)

16.77

18.54

10.6%

Stable growth in customer base, profit per customer,

and contracts per customer

22

Dec 31, 2016

Jun 30, 2017

18.5%

1H 2016

1H 2017

143.28 million

131.07 million

2.28 3.2%

9.3%

2.21 Dec 31, 2016

Jun 30, 2017 Contracts

per

customer

Profit per

customer

Number of

customers

RMB 241.66

RMB 203.97

23

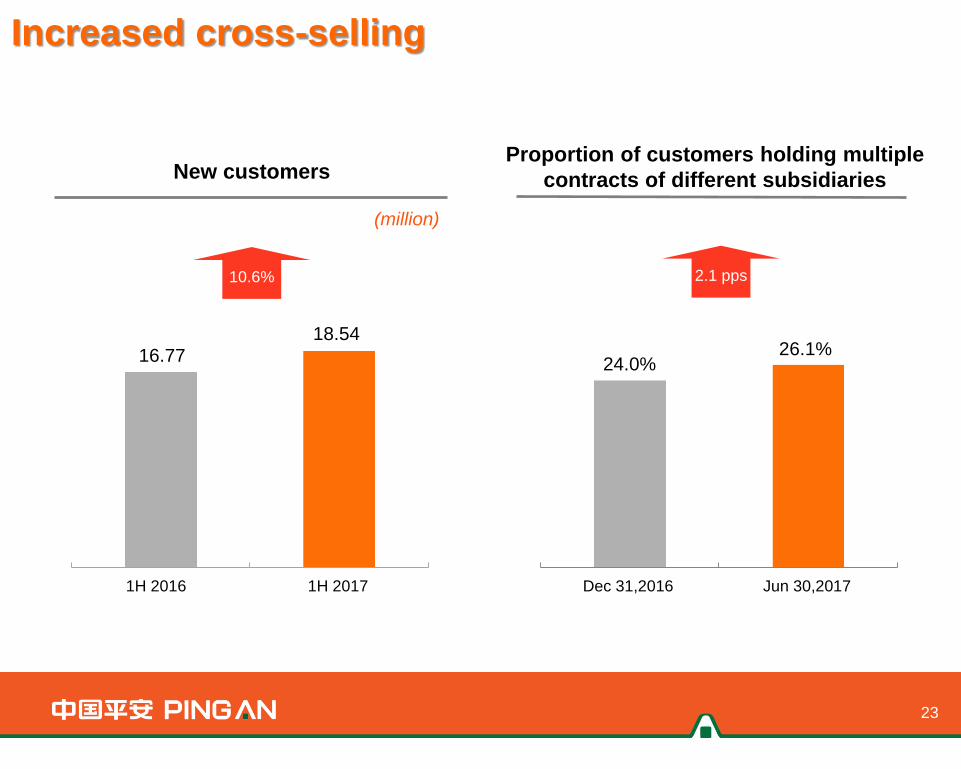

Increased cross-selling

New customers Proportion of customers holding multiple

contracts of different subsidiaries

2.1 pps

(million)

10.6%

16.77 18.54

1H 2016 1H 2017 Dec 31,2016 Jun 30,2017

24.0% 26.1%

Dec 31, 2016

Jun 30, 2017

76.1%

Jun 30, 2016

Jun 30, 2017

403 million

346 million

67.4%

4.1 pps

16.4%

Booming user base and growing user stickiness

65.31 million

37.08 million

24

Dec 31, 2016

Jun 30, 2017 71.5% Proportion

of app

users

Monthly

active

users

Number of

users

Note: Monthly active users refers to the monthly average of active users for 12 months by the end of the reporting period, where

active users are those who logged on at least once in the month.

25

Business Review

Group President Alex Ren

Overview Financial

Review

Customer

Development Business Review

26

L&H insurance: NBEV increased by 46.2% year on

year, with an increase of 44.0% of the agent channel.

The number of sales agents exceeded 1.30 million;

productivity increased by 18.2%, and their income

rose by 14.0% year on year.

Lufax Holding’s wealth management transaction

volume increased by 65.0% year on year;

institutional trading volume grew by 45.4%.

Finance One Account now has 203 million

registered users, and has cooperated with 406

banks and 1,493 non-bank financial and quasi-

financial institutions.

Ping An Securities developed differential

advantages; net profit slightly declined by 2.6%

year on year, better than industry average.

Ping An Asset Management’s AUM rose to about

RMB 2.49 trillion, up 10.0% YTD.

Results of business lines

Ping An Bank realized a net profit of RMB

12,554 million; its cost-to-income ratio

decreased by 4.04 pps year on year to 24.76%.

Retail business accounted for 40% of its total

revenue, up 11 pps year on year. P&C insurance: The premium income

reached RMB103.4billion, up 23.5% year on

year; the combined ratio was 96.1%; the

unannualized ROE was 10.5%.

27

Insurance Business

Overview Financial

Review

Customer

Development

Business Review

- Insurance

185,728

250,031

12,393

9,805

275,717

207,537

2016年 2017年

76,211 105,603

131,326

170,114

2015年 2016年

218,192

287,116

(in RMB million)

Written premium by business type

Group

business

Renewal

business

38.6%

31.6%

L&H Insurance: fast-growing written premium

29.5%

Individual

business

New

business

28

1H 2016 1H 2017

(in RMB million)

Written premium of individual

business by channel

Agent channel 34.6%

32.9%

Bancassurance

channel

Telemarketing,

internet

marketing and

other channels

1H 2016 1H 2017

1H 2016

Steady growth in agent force and productivity

29

26.7%

Agents’ productivity Number of agents

1,325,477

Jun 30, 2017 Jun 30, 2016

1,045,813

18.2%

(RMB/person/month)

Agents’ income

7,218

6,333

1H 2017 1H 2016

14.0%

(RMB/person/month) (person)

10,522

12,438

1H 2017

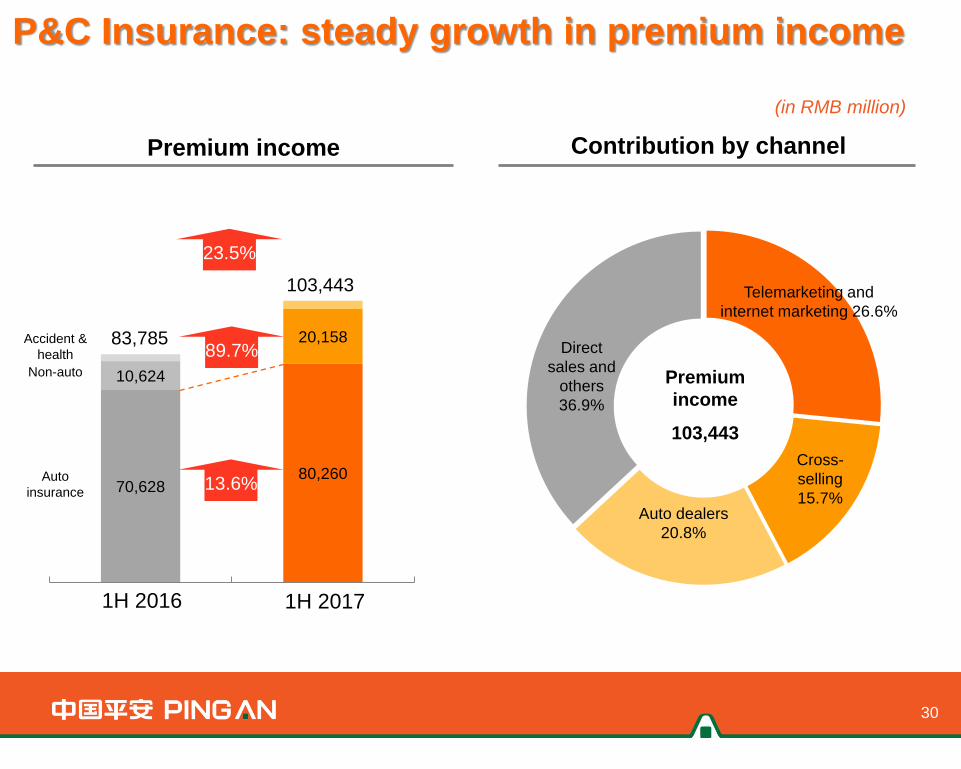

P&C Insurance: steady growth in premium income

Premium income

(in RMB million)

70,628 80,260

10,624

20,158

103,443

83,785

1H 2016 1H 2017

Contribution by channel

Direct

sales and

others

36.9%

Cross-

selling

15.7% Auto dealers

20.8%

Telemarketing and

internet marketing 26.6%

Premium

income

103,443

13.6%

89.7%

23.5%

30

Accident &

health

Non-auto

Auto

insurance

31

P&C Insurance: excellent combined ratio

Combined ratio

54.9% 58.8%

40.4% 37.3%

1H 2016 1H 2017

95.3% 96.1%

0.8

pps

Breakdown of premium income and

combined ratio

Expense

ratio

Loss

ratio

Guarantee insurance 9,515

Premium income

Corporate property insurance

Accidental injury insurance

91.5%

Combined ratio

Auto insurance 80,260 97.1%

69.7% 2,578

91.9% 3,100

Liability insurance 3,126 89.3%

(in RMB million)

32

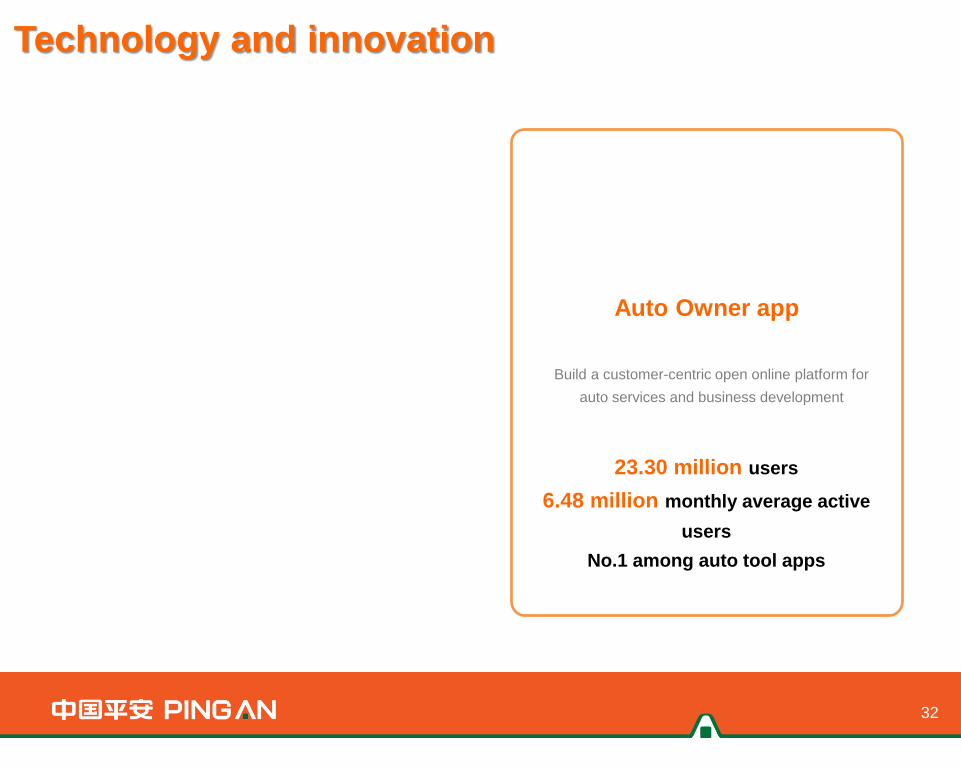

Technology and innovation

Auto Owner app

Build a customer-centric open online platform for

auto services and business development

23.30 million users

6.48 million monthly average active

users

No.1 among auto tool apps

Jin Guan Jia app

Diversify scenarios on the Jin Guan Jia app; promote

customer development and meet various demands

Over 120 million registered users

Over 23 million monthly average active

users

33

Banking Business

Overview Financial

Review

Customer

Development

Business Review

- Banking

1H 2016 1H 2017

Dec 31, 2016 Jun 30, 2017 Dec 31, 2016 Jun 30, 2017

Dec 31, 2016 Jun 30, 2017

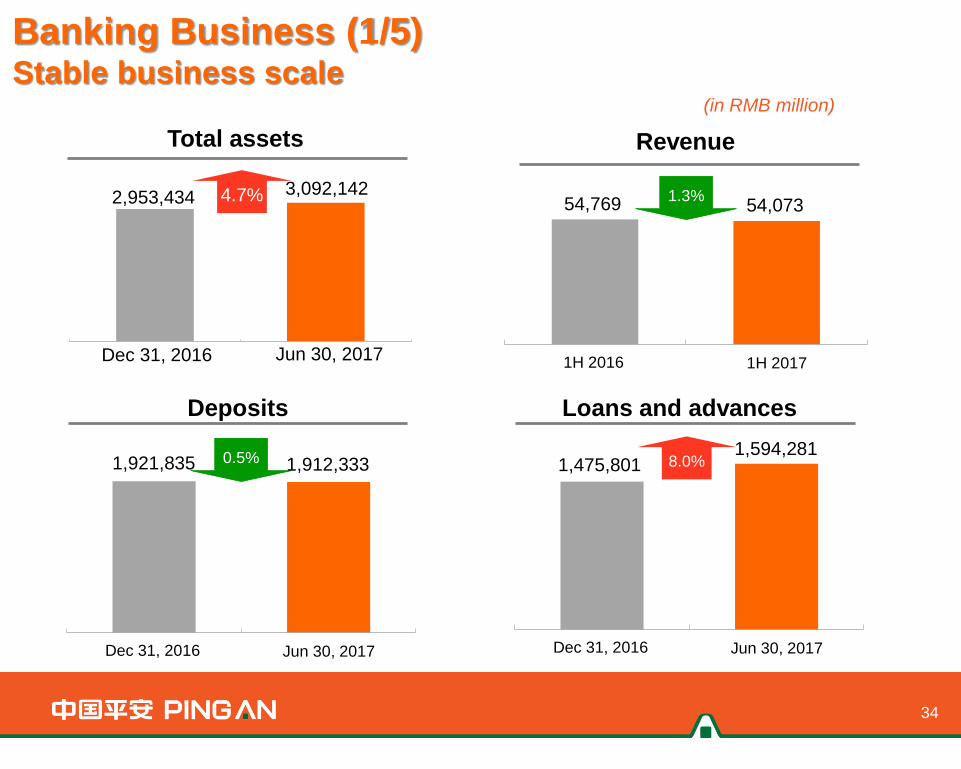

2,953,434 4.7%

(in RMB million)

Total assets

3,092,142

34

0.5% 1,921,835 1,912,333 1,594,281

1,475,801 8.0%

Banking Business (1/5) Stable business scale

Revenue

54,073 54,769 1.3%

Deposits Loans and advances

1H 2016 1H 2017

(in RMB million)

1H 2016 1H 2017

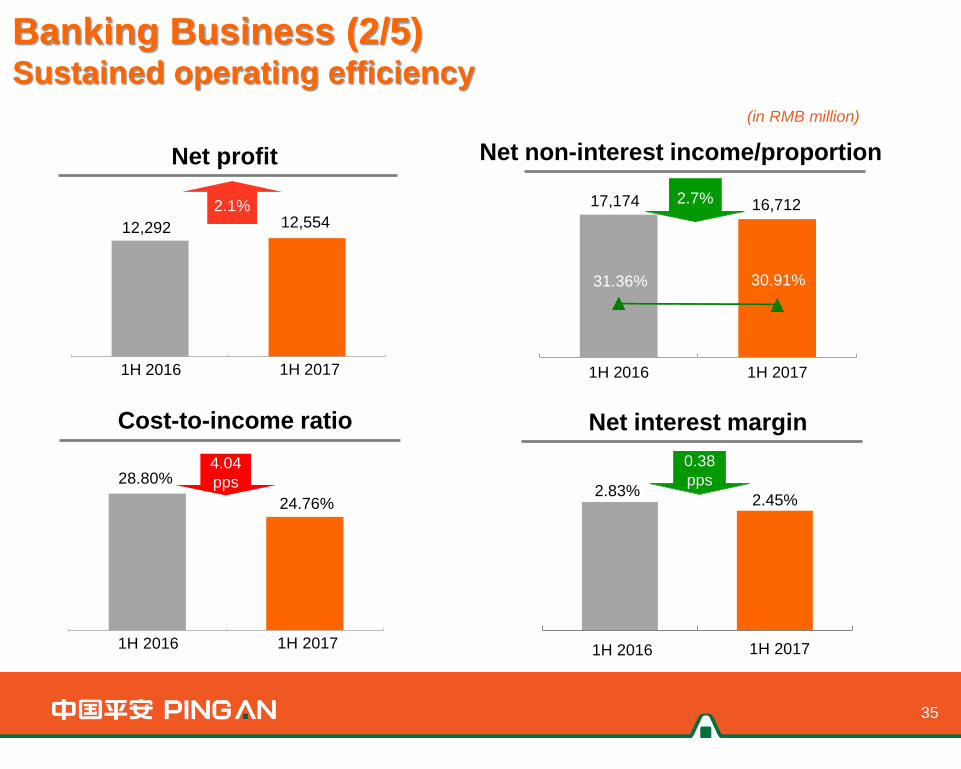

24.76%

28.80% 4.04

pps

Cost-to-income ratio

Net non-interest income/proportion

17,174 16,712

31.36% 30.91%

Net interest margin

2.45%

1H 2016 1H 2017

0.38

pps 2.83%

35

2.7%

Banking Business (2/5) Sustained operating efficiency

1H 2016 1H 2017

12,554 12,292

2.1%

Net profit

Dec 31, 2016

Jun 30, 2017

Personal assets

under

management

Number of retail

customers

58.43 million

52.39 million

RMB 951

billion 19.2%

11.5%

RMB 797.6 billion

36

Number of customers

holding products from

other subsidiaries of

Ping An Group

24.40 million

20.15 million Dec 31, 2016

Jun 30, 2017

Dec 31, 2016

Jun 30, 2017

Banking Business (3/5) Transformation towards retail banking

21.1%

Note: Retail customers include debit card customers and credit card customers, with duplication removed; the number of retail customers

as at the end of 2016 has been restated accordingly.

37

Banking Business (4/5) Encouraging signs from retail strategic transformation

(in RMB million)

% of

revenue

from

retail 29%

40% % of profit

before tax

from retail

29%

64%

Growth of

retail

deposits

Growth of

retail loans

16%

+43,051

-0.5%

21.5%

3.5%

+15,591

16,029

21,769

4,709

10,597

1H 2017

-1,366

1H 2016

1H 2017

1H 2016

1H 2017

1H 2016

1H 2017

1H 2016

+116,091

38

Banking Business (5/5) Asset quality snapshot

Dec 31, 2016 Change

1,475,801 8.0% Total loans and advances

1.74% +0.02 pps NPL ratio

4.11% +0.03 pps Proportion of special

mention loans

39,932 13.3% Loan loss provision balance

155.37% +5.95 pps Provision coverage ratio

98.51% +6.16 pps Provision coverage ratio of

loans overdue >= 90 days

Jun 30, 2017

1,594,281

1.76%

4.14%

45,229

161.32%

104.67%

(in RMB million)

39

Asset Management

Business

Overview Financial

Review

Customer

Development

Business Review –

Asset Management

Net investment income(1) 59,752 61,829

Net realized and unrealized gains(2) (21,277) (2,515)

Impairment loss (447) (239)

Total investment income 38,028 59,075

Annualized net investment yield(3) 5.7% 5.0%

Annualized total investment yield(3) 4.4% 4.9%

Investment returns on insurance funds

40

(in RMB million) 1H 2016 1H 2017

Notes: (1) Includes deposit interest income, bond interest income, dividends from equity investments, and rents from

investment properties.

(2) Includes capital gains from securities investments and profits/losses from fair value changes.

(3) Net foreign currency gains/losses on investment assets denominated in foreign currencies are excluded from the

above investment incomes. Average investment assets used as the denominator are computed in line with principles

of the Modified Dietz method.

Proportions Dec 31, 2016 Jun 30, 2017 Change (pps)

Fixed-income investments 74.6% 73.0% 1.6

Term deposits 10.5% 7.2% 3.3

Bond investments 46.2% 48.1% 1.9

Debt plan investments 6.9% 6.0% 0.9

Wealth management products(1) 6.3% 7.1% 0.8

Other fixed-income investments(2) 4.7% 4.6% 0.1

Equity investments 16.9% 20.4% 3.5

Stocks and equity funds 8.4% 11.8% 3.4

Preferred stocks 3.8% 3.2% 0.6

Bond funds 0.7% 0.4% 0.3

Wealth management products(1) 2.1% 3.1% 1.0

Unlisted equity investments 1.9% 1.9% -

Investment properties 2.2% 2.2% -

Cash, cash equivalents and others 6.3% 4.4% 1.9

Total investment assets (in RMB million) 1,971,798 2,219,658

Investment portfolio of insurance funds

41

Notes: (1) Wealth management products include trust plans from trust companies and wealth management products from commercial banks.

(2) Other fixed-income investments include financial assets purchased under agreements to resell, policy loans, and statutory deposits for insurance operations.

Proportion of non-

standard debts:

Dec 31, 2016: 13.2%

Jun 30, 2017: 13.1%

Structure of the non-standard debt portfolio

42

Real estate development 6.28 11.3 3.76

Investment

proportion (%)

5.97 Total 100.0

Real estate 6.37 12.3 3.73

Urban construction 20.2 6.03 5.06

Others 3.1 6.26 2.50

Expressway 19.2 6.03 6.60

5.40

Infrastructure 56.9 5.93 5.29

Electric power 8.0 5.63 3.49

Coal mining 4.5 6.09 3.17

Others 5.0 5.48 5.93

Others 1.0 7.46 3.42

Non-bank FIs 27.7 5.83 6.71

Remaining

maturity (year)

Nominal yield

(%)

43

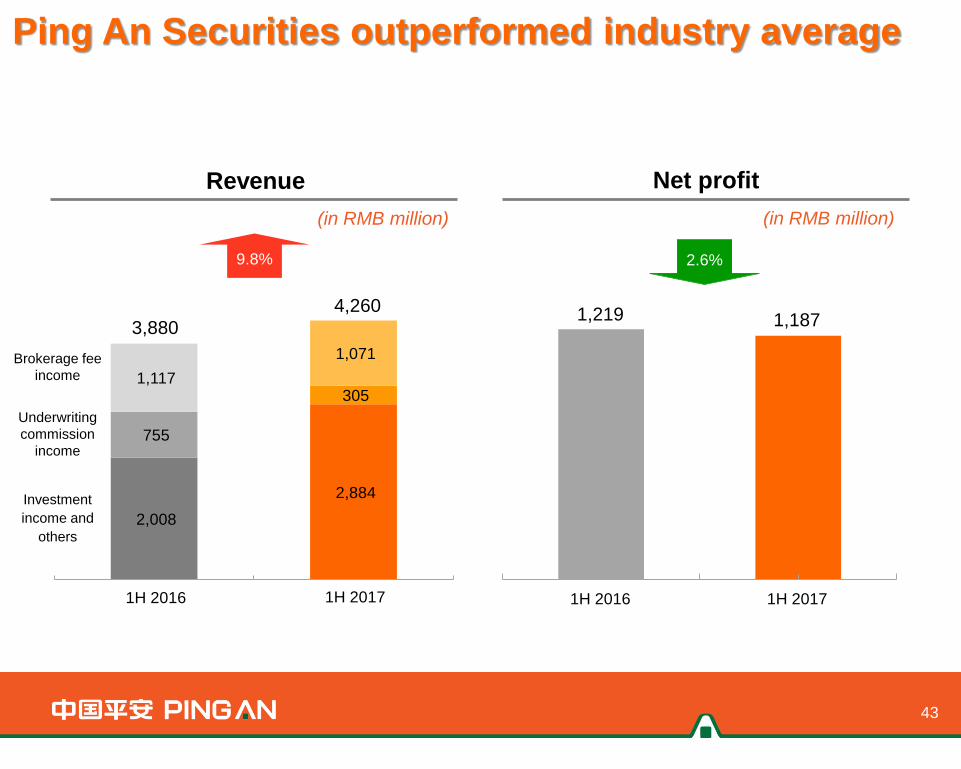

2016年1-6月 2017年1-6月

Net profit

1,219 1,187

Ping An Securities outperformed industry average

Revenue

Investment

income and

others

Underwriting

commission

income

Brokerage fee

income

(in RMB million) (in RMB million)

2.6%

1H 2016 1H 2017

2,008

2,884

755

305 1,117

1,071

3,880

4,260

9.8%

1H 2016 1H 2017

44

Increasing number and activity of brokerage

customers

Number of brokerage customers Daily average active customers

(in thousand) (in thousand)

11.1% 50.6%

Dec 31, 2016 Jun 30, 2017

1,009 1,121

10,090

11,210

Jun 30, 2017 Dec 31, 2016

870

1,310

391,095 348,773

144,815 150,476

141,311 133,392

2016年12月31 2017年6月30日

52,500

65,500

2016年12月31 2017年6月30日 Dec 31, 2016

Ping An Trust enhanced risk management

Active wealth management customers Assets under management

677,221 632,641

24.7% 6.6%

(person) (in RMB million)

Jun 30, 2017 Dec 31, 2016 Jun 30, 2017

45

Administrative

category

Financing

category

Investment

category

46

Internet Finance Business

Overview Financial

Review

Customer

Development

Business Review -

Internet Finance

47

Technology-powered business transformation

Ping An is transforming from a traditional capital-powered model to a technology-powered model,

and is building core infrastructure platforms with innovative technologies such as AI, big data,

blockchain and cloud computing to support transformation of its core business activities

Scenarios

Connected 70% of core

business systems into

Ping An FinCloud

Data Speed A I

Exploring 12 blockchain-

based financial and

health care scenarios

Applied face recognition

to over 80 scenarios

within the Group

Big data platform’s

data size: 8.5PB

20,000 data labels for

single users

Help 2,200 institutions to

manage risks with credit

reference technology

Ping An FinCloud: a

proprietary financial

cloud platform

developed by Ping An

89% of product/ system

updates can be completed

within 30 days

Perception AI Accuracy rate of face

recognition: 99.8%

Accuracy rate of voiceprint

recognition:

text-dependent 99%

text-independent 93%

Prediction AI Joint R&D of the world’s first

“AI + big data” flu prediction

model

Prescription AI Increased the loss verification

speed of auto insurance by

4,000 times

Its basic environment can

be deployed within 150

seconds, allowing an

institution to finish

deployment jobs within

one day

59% of product/ system

updates can be

completed within 14 days

2016年12月31 2017年6月30日 Jun 30,2017

2,536.0 3,687.3

665.9

1,098.5

2016年1-6月 2017年1-6月 1H 2016 1H 2017

Lufax Holding achieved fast business growth

Up by 3.5% YTD Up by 46.9% YTD

31.23 million

registered

users

Up by 10.0% YTD

7.66 million

active investor

users

5.54 million

borrowers

with Puhui

(in RMB billion)

Transaction volume

49.5%

48

(in RMB billion)

Balance of loans under management

53.5%

3,201.9

4,785.8

146.6

225.1

Wealth

management

Institutional

trading

Dec 31,2016

49

Ping An Good Doctor and Finance One Account

Ping An Good Doctor: build a

comprehensive O2O health

care ecosystem

• Nearly 1,000 in-house doctors

• Over 60,000 external contracted doctors

• Nearly 2,300 hospitals

• 700 checkup centers

• Over 160 million users

• A peak number of 20 million monthly active

users

• A peak number of 460,000 queries per day

Finance One Account:

develop an open financial

services ecosystem

• Account, wealth, credit and lifestyle management

services

• 203 million users, up 9.7% from the beginning

of the year

• Sales of financial products rose to RMB 36.8

billion, up by 111.5% year on year

• Partnered with 406 banks and 1,493 non-bank

financial and quasi-financial institutions

• RMB 2.62 trillion of interbank trading volume

• Over 356 million credit inquiries

Individual customers:

Institutional clients:

User base:

Doctor network:

Partners:

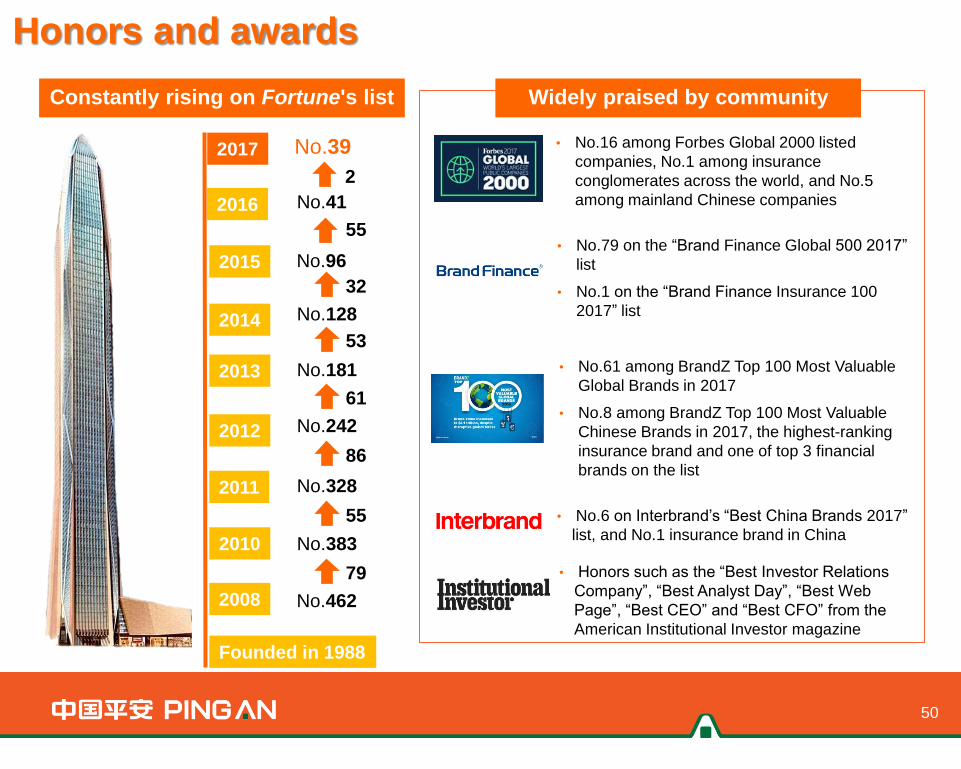

Honors and awards

Widely praised by community Constantly rising on Fortune's list

• No.6 on Interbrand’s “Best China Brands 2017”

list, and No.1 insurance brand in China

• Honors such as the “Best Investor Relations

Company”, “Best Analyst Day”, “Best Web

Page”, “Best CEO” and “Best CFO” from the

American Institutional Investor magazine

• No.16 among Forbes Global 2000 listed

companies, No.1 among insurance

conglomerates across the world, and No.5

among mainland Chinese companies

• No.79 on the “Brand Finance Global 500 2017”

list

• No.1 on the “Brand Finance Insurance 100

2017” list

50

No.462

No.383

No.328

No.242

No.181

No.128

No.41

2015

2014

2013

2012

2011

2010

2008

Founded in 1988

No.96

79

55

86

61

53

32

2017

55

2016

No.39

2

• No.61 among BrandZ Top 100 Most Valuable

Global Brands in 2017

• No.8 among BrandZ Top 100 Most Valuable

Chinese Brands in 2017, the highest-ranking

insurance brand and one of top 3 financial

brands on the list

Q&A