2016...Terminal Illness / Nursing Home Care Feature If selected, this rider waives the Surrender...

23

SENTINEL SECURITY LIFE INSURANCE COMPANY MYGA & FIA 2016 Annuity Product Kit

Transcript of 2016...Terminal Illness / Nursing Home Care Feature If selected, this rider waives the Surrender...

SENTINEL SECURITY LIFE INSURANCE COMPANY

MYGA & FIA

2016Annuity Product Kit

SENTINEL SECURITY LIFE INSURANCE COMPANY

Personal Choice Annuity

Sentinel Plan® Personal Choice Annuity TM

An a la carte solution for a custom annuity

SSLANBR11-OT REV 06/13

CLIENT BROCHURE

SSLANBR11-FL REV 05/13

Customizable

“Sentinel’s Personal Choice AnnuityTM is great! I was able to choose the features I wanted and build my own single premium deferred annuity to get the best interest rate.”

The Sentinel Personal Choice AnnuityTM was created with the flexibility to meet your needs. First, you have the choice of the duration of the annuity which can be five, seven, or ten years; meaning you will have access to your money when you need it.

Second, Sentinel’s Personal Choice AnnuityTM allows you to determine the optional features, called riders, that fit your needs. In most cases annuities are loaded with riders that you don’t want or need, giving you a lower interest rate during the life of the fully-loaded annuity. With the Personal Choice AnnuityTM you have the option of including only the features that you require, which will allow you to earn a higher interest rate. You have the choice of six different optional riders. You can pick and choose “a la carte” in any combination depending on your needs. You pay only for those features you want.

Finally, the Personal Choice AnnuityTM allows you to add all optional riders at the beginning of the term of the annuity called, the Guarantee Period. You may add the Required Minimum Distribution rider at any time. With Sentinel’s Personal Choice AnnuityTM, the choice is yours!

Personal Choice Annuities are issued by Sentinel Security Life Insurance Company. Annuity contracts, with their charges and limitations, as well as individual features are subject to state regulations and may not be available in all states.

Product specifications vary by state, consult your agent.

SSLANBR11-OT REV 06/13

Personal Choice Annuities are issued by Sentinel Security Life Insurance Company. Annuity contracts, with their charges and limitations, as well as individual features are subject to state regulations and may not be available in all states.

Product specifications vary by state, consult your agent.

Personal Choice Annuities are issued by Sentinel Security Life Insurance Company. Annuity contracts, with their charges and limitations, as well as individual features

are subject to state regulations and may not be available in all states.

*Note - Once an optional rider is selected it may not be removed during the annuity contract.

SSLANBR11-OT REV 06/13

Personal Choice Annuities are issued by Sentinel Security Life Insurance Company. Annuity contracts, with their charges and limitations, as well as individual features

are subject to state regulations and may not be available in all states.

*Note - Once an optional rider is selected it may not be removed during the annuity contract.

Preferred 10% Free WithdrawalIf selected, this rider waives the Surrender Charges and MVA for the first withdrawal per year after the first contract year. The annuitant may withdraw up to the greater of 10% of the account value (as of the last contract anniversary date) or the required minimum distribution (RMD). Surrender charges and MVA may apply if the withdrawal exceeds the greater of 10% or the RMD or there are multiple withdrawals in that contract year.

Required Minimum DistributionIf selected, this rider waives the Surrender Charge and Market Value Adjustment (MVA) on any Required Minimum Distribution (RMD) from tax-qualified plans. This is the only rider that may be added at issue or at the beginning of a subsequent Guarantee Period.

Can be added at issue or the beginning of a Guarantee Period:

ORCan only be added at issue:

Terminal Illness / Nursing Home Care FeatureIf selected, this rider waives the Surrender Charge if the owner is diagnosed with a stroke, heart attack, life-threatening cancer, or any other terminal illness. This feature also waives any Surrender Charge when the owner requires skilled nursing care for more than 90 consecutive days. Age limits and other conditions apply.

Optional Riders*

Death Benefit Feature - (Required for Issue Ages 86-90)If selected, this rider waives the Surrender Charge associated with a lump-sum payment in the case of the death of the Annuitant.

72(t) Free WithdrawalIf selected, this rider waives Surrender Charge and MVA associated with with-drawals made in accordance with Internal Revenue Code Section 72(t).

Accumulated Interest WithdrawalIf selected, this rider waives the Surrender Charge and MVA associated with accumulated interest withdrawals.

NE- Death Benefit will not be less than premium paid regardless if this rider is added.FL- This rider is automatically included with all contracts issued.

SSLANBR11-FL REV 05/13

SSLANBR11-OT REV 06/13

Since 1948, families have counted on Sentinel Security Life Insurance Company during their time of need. The Company was originally established to provide families a way of funding funeral expenses and burial costs. Through our final expense life insurance product, we have been honored to provide peace of mind to families for well over half a century.

Today, Sentinel offers a strong senior market portfolio including Life, Health, and Annuity products. We continue to develop new products and services to better protect our customers.

Sentinel has a long history of financial strength and stability that has afforded us the opportunity to invest wisely in the growth of our company. Our strength lies not only in the quality of our insurance products, but also the level of service we provide to our policyholders, agents, and shareholders. We invite you to learn more about our company by visiting www.sslco.com or by calling 800-247-1423.

Sentinel Plan® Personal Choice Annuity TM

An a la carte solution for a custom annuity

FOR AGENT USE ONLY. NOT A SOLICITATION OR ADVERTISEMENT.

Not all annuities and optional riders are available in all states.

SSLANQS11-OT Rev 02/14

AGENT QUICK SHEET For All States* Except:CA, FL, MN, NV, OK, OR, PA, TX, UT

Policy Year

9% 8% 7% 6% 5% 5% 5% 5% 5% 5%1 2 3 4 5 6 7 8 9 10Year

During renewal guarantee periods the surrender charges for all annuities are 5% unless the contract annuitant has reached an attained age in the table above.Renewal Periods

30 Day Option 30 days prior to the end of any guarantee period Surrender Charges and MVA will not apply.

Attained Age 5% 4% 3% 2% 1%90-93 94 95 96 97Attained

Age 0%98-100

Market Value Adjustment (MVA) The MVA is specified in the contract. The MVA expires at the end of each Guarantee Period and then reinstates when the annuity rolls into a new Guarantee Period.

The following table applies by policy year until the contract annuitant reaches the attained ages in the attained age section below.

Type / MarketIssue Ages / MaturityContribution LimitsMinimum Guaranteed Interest Rate

Single Premium Deferred Annuity / Qualified or Non-Qualified0-90$2,500 to $1 million Qualified or Non-Qualified; over $1 million will require home office approval1.0%

Surrender Charges- Offered in 5, 7, or 10 year variations. Surrender charges will be applied based upon client selection:

Allowed Qualified Funds IRA, Roth IRA, SIMPLE

Sentinel’s Personal Choice AnnuityTM provides flexibility by allowing the selection of optional riders. These riders eliminate possible Surrender Charges or market value adjustments (MVA) in certain situations. The owner selects only the riders that fit his/her needs without paying for features that he/she doesn’t require.

Required Minimum DistributionPreferred 10% Free Withdrawal

Terminal Illness / Nursing Home Care72(t) Free WithdrawalDeath Benefit Feature

0.16%0.08%0.15%0.05%0.35%

0.16%0.08%0.15%0.05%0.35%

0.16%0.08%0.15%

0.05%0.35%

Rate Reductions for Optional Riders:

Accumulated Interest Withdrawal 0.08% 0.08% 0.08%

5 Year 7 Year 10 Year

Sentinel Plan® Personal Choice Annuity TM

An a la carte solution for a custom annuity

FOR AGENT USE ONLY. NOT A SOLICITATION OR ADVERTISEMENT.

Not all annuities and optional riders are available in all states.

SSLANQS11-OT Rev 02/14

AGENT QUICK SHEET For All States* Except:CA, FL, MN, NV, OK, OR, PA, TX, UT

Optional Riders

Required Minimum DistributionIf selected, this rider waives the Surrender Charge and MVA on any Required Minimum Distribution (RMD) from tax-qualified plans. This is the only rider that may be added at issue or at the beginning of a subsequent Guarantee Period.

Can be added at issue or the beginning of a Guarantee Period:

Preferred 10% Free WithdrawalIf selected, this rider waives the Surrender Charges and MVA for the first withdrawal per year starting in the second contract year. The owner may withdraw up to the greater of 10% of the account value (as of the last contract anniversary date) or the required minimum distribution (RMD). Surrender charges and MVA may apply if the withdrawal exceeds the greater of 10% or the RMD or there are multiple withdrawals in that contract year.

Can only be added at issue:

Death Benefit Feature (Required on Issue Ages 86-90)If selected, in case of the death of the annuitant or owner, the Death Benefit will be equal to the total contract value. Any Surrender Charges and MVA will be waived.

Terminal Illness / Nursing Home Care FeatureIf selected, this rider waives the Surrender Charge if the owner is diagnosed with a stroke, heart attack, life-threatening cancer, or any other terminal illness. This feature also waives any Surrender Charge when the annuitant requires skilled nursing care for more than 90 consecutive days. Age limits and other conditions apply.

72(t) Free Withdrawal If selected, this rider waives Surrender Charge and MVA associated with withdrawals made in accordance with Internal Revenue Code Section 72(t).

Accumulated Interest WithdrawalIf selected, this rider waives the Surrender Charge and MVA associated with accumulated interest withdrawals starting in the first contract year.

SENTINEL SECURITY LIFE INSURANCE COMPANY

Summit Bonus IndexSM

SSLIANBR13-OT REV 06/15

Sentinel Plan®

Summit Bonus IndexSM

YOUR CHOICE • YOUR GROWTH • YOUR FUTURE

Client BrochureIL, NC

SSLIANBR13-OT REV 06/15

In today’s challenging financial

environment, many people

are seeking safer investment

opportunities. Fixed indexed

annuities provide the flexibility

to participate in the growth of the

stock market and protect your

principal when the stock market

declines. With the Sentinel Plan®

Summit Bonus IndexSM you

have the ability to enhance your

financial future by selecting from

a variety of indexing strategies.

WHAT AFIXED INDEXED ANNUITY

CAN PROVIDE FOR YOU...

IS A FIXED INDEXED ANNUITY

RIGHTFOR YOU?

CHOICEYou decide how your money grows and how you receive income from your investment.

GROWTHYour money grows with the market without losing value during a downturn.

FUTUREYou will provide for yourself and your beneficiaries.

FACTORS TOCONSIDERFinancial Situation

Retirement Needs

Investment Objectives

Time Horizon

There are many factors to consider when looking into a fixed indexed annuity. Your age, annual income, liquid net worth and financial needs are all important in determining whether or not a fixed indexed annuity can help you reach your financial goals.

Tax DeferralYour annuity earns interest tax-deferred, which

means you do not pay taxes on the interest earned under your contract until you

make a withdrawal. This is a great advantage!

TAX ADVANTAGEWith tax deferral, your PRINCIPAL

will earn interest, and all of your INTEREST will earn interest too!

2

Sentinel Plan® Summit Bonus IndexSM

YOUR CHOICE

YOUR GROWTH

YOUR FUTURE

If you have enough liquid assets

to cover living expenses and emergencies, the fixed indexed annuity is designed

specifically for you.

WHAT AFIXED INDEXED ANNUITY

CAN PROVIDE FOR YOU...

OWNERThe owner makes the initial

investment, selects the indexing strategies and names the annuitant

and beneficiary. The owner can be an individual, trust, or an organization.

The owner also has the right to request withdrawals and income payments.

ANNUITANTThe annuitant is a person named by the owner who will receive payments

under the Maturity Benefit in the policy. In many cases the owner and the annuitant are the same person.

BENEFICIARYThe beneficiary receives the death benefit at the time of

the owner’s death.

WHO’S WHO IN AN ANNUITY?

FACTORS TOCONSIDERFinancial Situation

Retirement Needs

Investment Objectives

Time Horizon

3

SSLIANBR13-OT REV 06/15

*Premium bonus varies by state. Please refer to the website or contact your agent for more details.

Premium Bonus

When you purchase your Sentinel Plan® Summit Bonus IndexSM, you will receive a one-time premium bonus*. The premium bonus is immediately credited to your account which gives you an opportunity to earn additional interest and gives you access to additional funds that you can access subject to your vesting schedule.

FEATURES OF THESENTINEL PLAN® SUMMIT BONUS INDEXSM

AccessibilityThe Sentinel Plan® Summit Bonus IndexSM offers several options to access your money without being subject to surrender charges or market value adjustments. For example:

• During the first policy year, you can withdraw the interest earned on funds allocated to the fixed account or a Required Minimum Distribution;

• After the first policy year, you can withdraw up to 10% of your contract value or a Required Minimum Distribution, whichever is greater;

• After the fifth policy year you can apply the vested value of the policy to purchase a settlement options to provide income. Please refer to page 11 of this brochure for more information on the Settlement Options.

PREMIUM BONUS VESTING SCHEDULE

Excess withdrawals may be subject to the

surrender schedule.

You can take up to two withdrawals in a policy year as long as your accumulation value does not go below $2500. Withdrawals must be at least $250.

Withdrawals other than as listed to the left are subject to applicable surrender charges, premium bonus vesting schedule, and Market Value Adjustments. Withdrawals may also be subject to taxes and penalties.

4

Death Benefit The amount payable if the Owner, or the Annuitant if the Owner is not a Natural Person, dies before annuity payments begin is equal to the ACcumulation Value less the Non-vested Premium Bonus or the Minimum Guaranteed Surrender Value determined as of the date of death, whichever is greater.

Sentinel Plan® Summit Bonus IndexSM

YOUR CHOICE

YOUR GROWTH

YOUR FUTURE

Strategy 4

Strategy 2

SURRENDER CHARGES

SCHEDULE

CapsA cap is the maximum interest rate that is used when calculating the Index Account.

You Have A ChoiceWith the Summit Bonus IndexSM you determine how your investment grows by selecting the crediting strategy that best fits your needs. You can allocate your funds between four Index Strategies, a fixed account, or any combination thereof. You also have the option to adjust your allocations annually, providing you with more control to reach your investment goals.

Fixed AccountThe Fixed Account has a guaranteed minimum interest rate of 1%. Interest is compounded daily, providing steady growth and the comfort of predictability.

• Stability• Annual Rate Guarantee• Earned interest is deposited into your account daily.

Surrender ChargesImportant reminder: If you surrender your policy or request withdrawals above a certain amount, there may be surrender charges. Please discuss the surrender charge schedule with your agent.

Indexing OptionsThe Sentinel Plan® Summit Bonus IndexSM offers four indexing strategies:

• Annual Point to Point• Monthly Sum• Monthly Averaging• Daily Averaging

The indexing strategies are designed to generate interest credits based on the performance of the S&P 500®. The good news is that while you are not investing in the market measured by the S&P 500®, you are able to obtain the benefits of market growth without exposure to market loss. 5

7%

8%

9%

10%

11%

12%

5%

6%

4%

2%

0%

7%

8%

9.5%

9%

3%

4%

1%

2%

0%

6%

5%

ISSUE AGE 0-57

ISSUE AGE 58+

SSLIANBR13-OT REV 06/15

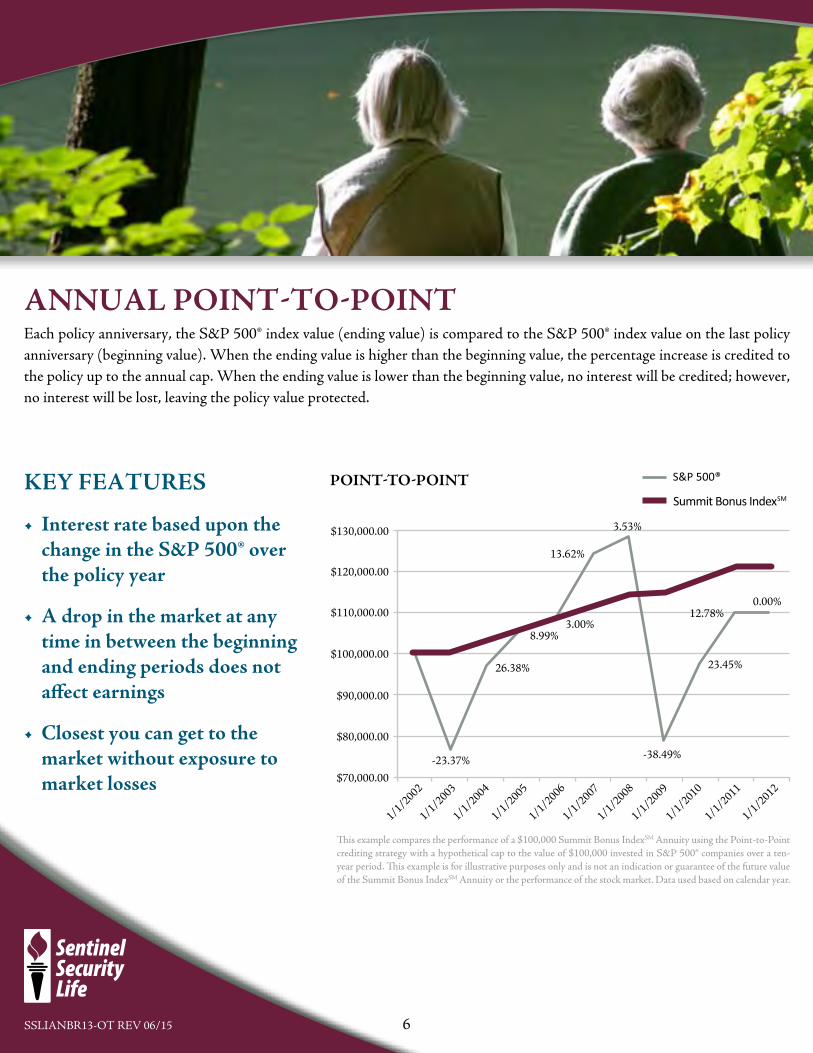

ANNUAL POINT-TO-POINTEach policy anniversary, the S&P 500® index value (ending value) is compared to the S&P 500® index value on the last policy anniversary (beginning value). When the ending value is higher than the beginning value, the percentage increase is credited to the policy up to the annual cap. When the ending value is lower than the beginning value, no interest will be credited; however, no interest will be lost, leaving the policy value protected.

This example compares the performance of a $100,000 Summit Bonus IndexSM Annuity using the Point-to-Point crediting strategy with a hypothetical cap to the value of $100,000 invested in S&P 500® companies over a ten-year period. This example is for illustrative purposes only and is not an indication or guarantee of the future value of the Summit Bonus IndexSM Annuity or the performance of the stock market. Data used based on calendar year.

KEY FEATURES

• Interest rate based upon the change in the S&P 500® over the policy year

• A drop in the market at any time in between the beginning and ending periods does not affect earnings

• Closest you can get to the market without exposure to market losses

6

$130,000.00

POINTTOPOINT

$120,000.00

$110,000.00

$100,000.00

$90,000.00

$80,000.00

-23.37%

26.38%

8.99%3.00%

13.62%

3.53%

12.78%

23.45%

-38.49%

1/1/2002

1/1/2003

1/1/2004

1/1/2005

1/1/2006

1/1/2007

1/1/2008

1/1/2009

1/1/2010

1/1/2011

1/1/2012

0.00%

$70,000.00

Sentinel Plan® Summit Bonus IndexSM

YOUR CHOICE

YOUR GROWTH

YOUR FUTURE

MONTHLY AVERAGINGEach policy anniversary, the monthly S&P 500® index value for the 12 month period since your last anniversary date is averaged (ending value) and compared to the S&P 500® index value on the last policy anniversary (beginning value). When the ending value is higher than the beginning value, the percentage increase is credited to the policy up to the annual cap. When the ending value is lower than the beginning value, no interest will be credited; however, no interest will be lost, leaving the contract value protected.

This example compares the performance of a $100,000 Summit Bonus IndexSM Annuity using the Monthly Averaging crediting strategy with a hypothetical cap to the value of $100,000 invested in S&P 500® companies over a ten-year period. This example is for illustrative purposes only and is not an indication or guarantee of the future value of the Summit Bonus IndexSM Annuity or the performance of the stock market. Data used based on calendar year.

KEY FEATURES

• Interest Rate based upon average of the 12 monthly closing values in S&P 500® over the policy year

• Higher Cap than Annual Point-to-Point

• The Monthly Averaging feature has the potential to yield higher earnings when there is a period of significant market increases.

7

$130,000.00

MONTHY AVERAGE

$120,000.00

$110,000.00

$100,000.00

$90,000.00

$80,000.00

-23.37%

26.38%

8.99%3.00%

13.62%

3.53%

12.78%

23.45%

-38.49%

1/1/2002

1/1/2003

1/1/2004

1/1/2005

1/1/2006

1/1/2007

1/1/2008

1/1/2009

1/1/2010

1/1/2011

1/1/2012

0.00%

$70,000.00

SSLIANBR13-OT REV 06/15

DAILY AVERAGINGEach policy anniversary, the daily S&P 500® index values following the last policy anniversary is averaged (ending value) and compared to the S&P 500® index value on the last policy anniversary (beginning value). When the ending value is higher than the beginning value, the percentage increase is credited to the policy up to the annual cap. When the ending average value is lower, no interest will be credited; however, no interest will be lost, leaving the contract value protected.

This example compares the performance of a $100,000 Summit Bonus IndexSM Annuity using the Daily Averaging crediting strategy with a hypothetical cap to the value of $100,000 invested in S&P 500® companies over a ten-year period. This example is for illustrative purposes only and is not an indication or guarantee of the future value of the Summit Bonus IndexSM Annuity or the performance of the stock market. Data used based on calendar year.

KEY FEATURES

• Interest rate based on the average of the daily closing values of the S&P 500® over the policy year

• Cap is the highest with this feature

• The daily averaging method offsets the impact of large short term market losses.

8

$130,000.00

DAILY AVERAGE

$120,000.00

$110,000.00

$100,000.00

$90,000.00

$80,000.00

-23.37%

26.38%

8.99%3.00%

13.62%

3.53%

12.78%

23.45%

-38.49%

1/1/2002

1/1/2003

1/1/2004

1/1/2005

1/1/2006

1/1/2007

1/1/2008

1/1/2009

1/1/2010

1/1/2011

1/1/2012

0.00%

$70,000.00

Sentinel Plan® Summit Bonus IndexSM

YOUR CHOICE

YOUR GROWTH

YOUR FUTURE

MONTHLY SUMEach policy anniversary, the S&P 500® index value for each month following the last policy anniversary (ending value) for 12 months is compared to the previous month’s S&P 500® index value (beginning value) to determine the percentage change. Monthly percentage increases (up to the monthly cap) are added to monthly percentage decreases (with no cap) for each of the 12 months. When the 12 month total is positive, the full amount is credited to the contract. When the 12 month total is negative, no interest will be credited; however, no interest will be lost, leaving the contract value protected.

This example compares the performance of a $100,000 Summit Bonus IndexSM Annuity using the Monthly Sum crediting strategy with a hypothetical cap to the value of $100,000 invested in S&P 500® companies over a ten-year period. This example is for illustrative purposes only and is not an indication or guarantee of the future value of the Summit Bonus IndexSM Annuity or the performance of the stock market. Data used based on calendar year.

KEY FEATURES

• Interest Rate based upon monthly changes in the S&P 500®

• There is a monthly cap for this account

• Opportunity to earn the highest interest with this option

9

$130,000.00

MONTHY SUM

$120,000.00

$110,000.00

$100,000.00

$90,000.00

$80,000.00

-23.37%

26.38%

8.99%3.00%

13.62%

3.53%

12.78%

23.45%

-38.49%

1/1/2002

1/1/2003

1/1/2004

1/1/2005

1/1/2006

1/1/2007

1/1/2008

1/1/2009

1/1/2010

1/1/2011

1/1/2012

0.00%

$70,000.00

SSLIANBR13-OT REV 06/15

SUMMIT BONUSINDEXSM

INCOMERIDER

PREMIUM BONUSIf you select the Income Rider, we will add 1% of your premium to the total amount of your annuity.

This 1% is in addition to the Premium Bonus you receive on the Base Policy.

That’s a total of TWO Premium Bonuses when you select the Income Rider at policy issue.

We offer an Income Rider that you may select when you purchase the Summit Bonus IndexSM. The Income Rider guarantees that you may withdraw a specified amount from the Summit Bonus IndexSM each year and is available even if the Accumulation Value of your annuity goes to zero after income payments begin.

Income payments under this rider are available as long as you are at least 55 and provided the Policy has been in force for one year. When you elect to receive payments under the Income Rider you have the option to select a single life payout for you or a joint life payout for you and your spouse.

What is the Benefit?Once income benefits begin, you can still receive income even

if the accumulation value of your policy is ZERO.

Withdrawals in addition to your income payments may reduce or eliminate your Lifetime

Annual Income.

Lifetime Annual IncomeYour lifetime annual income will depend on your Income Account Value, your Payout Factor, and if you are required to take out required minimum distributions under federal tax laws.

The Payout Factor is a percentage that is based on whether you elect the Income Rider for you or for you and your spouse. The Payout factor is also based on your age or the age of your spouse.

The Income Account Value is used to calculate the Income Rider payments and the Rider Charge.

10

End of Policy Year

Age Accumulation Value

Income Account

ValuePayout

1 65 $71,173.67 $74,412.002 66 $72,124.81 $78,876.723 67 $73,050.03 $83,609.324 68 $73,945.71 $88,625.885 69 $74,807.95 $93,943.446 70 $75,632.56 $99,580.047 71 $76,415.04 $105,554.848 72 $77,150.60 $111,888.139 73 $77,834.05 $118,601.42

10 74 $78,459.86 $125,717.51 $6,285.8811 75 $72,881.45 $119,431.63 $6,285.8812 76 $67,229.58 $113,145.76 $6,285.8813 77 $61,502.42 $106,859.88 $6,285.8814 78 $55,698.08 $100,574.01 $6,285.8815 79 $49,814.63 $94,288.13 $6,285.8816 80 $43,850.09 $88,002.26 $6,285.8817 81 $37,802.45 $81,716.38 $6,285.8818 82 $31,669.61 $75,430.50 $6,285.8819 83 $25,449.46 $69,144.63 $6,285.8820 84 $19,139.80 $62,858.75 $6,285.8821 85 $12,738.41 $56,572.88 $6,285.8822 86 $6,242.98 $50,287.00 $6,285.8823 87 $0.00 $44,001.13 $6,285.8824 88 $0.00 $37,715.25 $6,285.8825 89 $0.00 $31,429.38 $6,285.88

*Values are not guaranteed and are for a hypothetical scenario. This example assumes an initialpremium of $65,000 allocated to the point-to-point strategy, with an 8% premium bonus and a6% rollup rate. GLWB payments start in year 10.

Sentinel Plan® Summit Bonus IndexSM

YOUR CHOICE

YOUR GROWTH

YOUR FUTURE

Sentinel Plan® Summit Bonus IndexSM

YOUR CHOICE

YOUR GROWTH

YOUR FUTURESETTLEMENT OPTIONSOne of the benefits of the Summit Bonus IndexSM is the ability to choose when you start to receive payments and the period of time you will receive them. The accumulation value and the settlement option you select will determine what payments you receive.

WHEN DO PAYMENTS BEGIN?After the fifth policy anniversary, you may elect to apply the Vested Value of your policy as a single premium to purchase one of the options described above.

LIFE INCOME ONLYWe will pay equal monthly payments for the Annuitant’s remaining lifetime. Payments will end with the payment due just before the annuitant’s death.• A death benefit is not available under this option

LIFE INCOME WITH GUARANTEED PERIOD CERTAINWe will pay equal monthly payments for the Annuitant’s remaining lifetime or the period certain. If the Annuitant dies after payments have been made for the period certain, payments end with the payment due just before the Annuitant’s death.• Payments will continue until the guarantee period ends

PERIOD CERTAIN ONLYWe will pay equal monthly payments for a period certain of not less than 10 years and not more than 20 years.

• Guarantees payments for the time specified between 10-20• Payments under this option can be greater than Life Income Only option

• Death benefit is available

11

Since 1948, families have counted on Sentinel Security Life Insurance Company during their time of need. The Company was originally established to provide families a way of funding funeral expenses and burial costs. Through our final expense life insurance product, we have been honored to provide peace of mind to families for well over half a century.

Today, Sentinel offers a strong senior market portfolio including Life, Health, and Annuity products. We continue to develop new products while improving existing products and services to better protect our customers.

Sentinel has a long history of financial strength and stability that has afforded us the opportunity to invest wisely in the growth of our company. Our strength lies not only in the quality of our insurance products, but also the level of service we provide to our policyholders, agents, and shareholders. We invite you to learn more about our company by visiting www.sslco.com or by calling 800-247-1423.

ABOUT SENTINEL SECURITY LIFE

SENTINEL SECURITY LIFE INSURANCE COMPANYP. O. Box 27248 | Salt Lake City, UT 84127-0478 | (800) 247-1423

The “S&P 500®” is a product of S&P Dow Jones Indices LLC or its affiliates (“SPDJI”) and has been licensed for use by Sentinel Security Life Insurance Company. Standard & Poor’s® and S&P® are registered trademarks of Standard & Poor’s Financial Services LLC (“S&P”) and Dow Jones® is a registered trademark of Dow Jones Trademark Holdings LLC (“Dow Jones”). The trademarks have been licensed to SPDJI and have been sublicensed for use for certain purposes by Sentinel Security Life Insurance Company. Summit Bonus IndexSM is not sponsored, endorsed, sold or promoted by SPDJI, Dow Jones, S&P, any of their respective affiliates (collectively, “S&P Dow Jones Indices”). S&P Dow Jones Indices does not make any representation or warranty, express or implied, to the owners of the Summit Bonus IndexSM or any member of the public regarding the advisability of investing in securities generally or in Summit Bonus IndexSM particularly or the ability of the S&P 500® to track general market performance. S&P Dow Jones Indices only relationship to Sentinel Security Life Insurance Company with respect to the S&P 500® is the licensing of the Index and certain trademarks, service marks and/or trade names of S&P Dow Jones Indices and/or its licensors. The S&P 500® is determined, composed and calculated by S&P Dow Jones Indices without regard to Sentinel Security Life Insurance Company or the Summit Bonus IndexSM. S&P Dow Jones Indices have no obligation to take the needs of Sentinel Security Life Insurance Company or the owners of Summit Bonus IndexSM into consideration in determining, composing or calculating the S&P 500®. S&P Dow Jones Indices is not responsible for and have not participated in the determination of the prices, and amount of Summit Bonus IndexSM or the timing of the issuance or sale of Summit Bonus IndexSM or in the determination or calculation of the equation by which Summit Bonus IndexSM is to be converted into cash, surrendered or redeemed, as the case may be. S&P Dow Jones Indices have no obligation or liability in connection with the administration, marketing or trading of Summit Bonus IndexSM. There is no assurance that investment products based on the S&P 500® will accurately track index performance or provide positive investment returns. S&P Dow Jones Indices LLC is not an investment advisor. Inclusion of a security within an index is not a recommendation by S&P Dow Jones Indices to buy, sell, or hold such security, nor is it considered to be investment advice.

S&P DOW JONES INDICES DOES NOT GUARANTEE THE ADEQUACY, ACCURACY, TIMELINESS AND/OR THE COMPLETENESS OF THE S&P 500® OR ANY DATA RELATED THERETO OR ANY COMMUNICATION, INCLUDING BUT NOT LIMITED TO, ORAL OR WRITTEN COMMUNICATION (INCLUDING ELECTRONIC COMMUNICATIONS) WITH RESPECT THERETO. S&P DOW JONES INDICES SHALL NOT BE SUBJECT TO ANY DAMAGES OR LIABILITY FOR ANY ERRORS, OMISSIONS, OR DELAYS THEREIN. S&P DOW JONES INDICES MAKES NO EXPRESS OR IMPLIED WARRANTIES, AND EXPRESSLY DISCLAIMS ALL WARRANTIES, OF MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE OR USE OR AS TO RESULTS TO BE OBTAINED BY SENTINEL SECURITY LIFE INSURANCE COMPANY, OWNERS OF THE SUMMIT BONUS INDEXSM, OR ANY OTHER PERSON OR ENTITY FROM THE USE OF THE S&P 500® OR WITH RESPECT TO ANY DATA RELATED THERETO. WITHOUT LIMITING ANY OF THE FOREGOING, IN NO EVENT WHATSOEVER SHALL S&P DOW JONES INDICES BE LIABLE FOR ANY INDIRECT, SPECIAL, INCIDENTAL, PUNITIVE, OR CONSEQUENTIAL DAMAGES INCLUDING BUT NOT LIMITED TO, LOSS OF PROFITS, TRADING LOSSES, LOST TIME OR GOODWILL, EVEN IF THEY HAVE BEEN ADVISED OF THE POSSIBILITY OF SUCH DAMAGES, WHETHER IN CONTRACT, TORT, STRICT LIABILITY, OR OTHERWISE. THERE ARE NO THIRD PARTY BENEFICIARIES OF ANY AGREEMENTS OR ARRANGEMENTS BETWEEN S&P DOW JONES INDICES AND SENTINEL SECURITY LIFE INSURANCE COMPANY, OTHER THAN THE LICENSORS OF S&P DOW JONES INDICES.

Agent Quick Sheet BASE POLICY - IL, NC

Sentinel Plan® Summit Bonus IndexSM

A FIXED INDEX ANNUITY

General Overview

Sentinel Plan® Summit Bonus IndexSM is a 10 year, single premium, deferred annuity with four different indexing strategies, in addition to a fixed account. An Income Rider is also available with a rollup that will continue to compound up to 20 years.

Issue Requirements

• Issue Ages: 0-80• Minimum Single Premium: $5,000 (Qualified) and $10,000 (Non-Qualified)• Maximum Single Premium: $1,000,000 (Larger amounts will be considered with Home Office Approval)

Premium Bonus

A one-time bonus equal to 7% of the single premium payment will be credited to the Accumulation Value of the Base Policy on the Policy Date.• 10 year vesting schedule for excess withdrawals and surrenders

Policy Year 1 2 3 4 5 6 7 8 9 10 11+

Vesting % 0% 0% 0% 0% 0% 10% 20% 40% 60% 80% 100%

Interest Crediting

Indexing strategies will be benchmarked against the S&P 500® performance.• Subject to applicable Caps and Minimums (refer to the Rate Sheet for current Caps)• Caps are subject to change on each Policy Anniversary and are guaranteed for that Policy Year• Crediting rate for a particular strategy can never fall below 0%• Available Strategies (refer to brochure SSLIANBR-12-OT for a complete description):

• Annual Point-to-Point • Daily Averaging • Monthly Averaging • Monthly SumFixed Account: Daily crediting with annual rate guarantee

Withdrawal Provisions

• RMD or the interest earned on the Fixed Account is available Penalty Free during the first Policy Year• RMD or up to 10% of the Accumulation Value is available Penalty Free after the first Policy Year• A maximum of two withdrawals are allowed each Policy Year• Minimum withdrawal amount of $250; Minimum account value after withdrawal is $2,500

Surrender Value

The Surrender Value is subject to:• Surrender Charges • Market Value Adjustment (MVA) • Premium Bonus Vesting• Minimum Guarantee Surrender Value required by Standard Non-Forfeiture LawSurrender Charges are calculated according to the following schedule:

Policy Year 1 2 3 4 5 6 7 8 9 10 11+Issue Age 0-57 12% 11% 10% 9% 8% 7% 6% 5% 4% 2% 0%Issue Age 58+ 9.5% 9% 8% 7% 6% 5% 4% 3% 2% 1% 0%

Penalties used to assess the Surrender Value DO NOT apply to Death Benefits, Settlements, or Penalty-Free Withdrawal Amounts

Death Benefit

Settlement

Options

The amount payable if the Owner, or the Annuitant if the Owner is not a Natural Person, dies before annuity payments begin, is equal to the Accumulation Value less the Non-vested Premium Bonus or the Minimum Guaranteed Surrender Value determined as of the date of death, whichever is greater. After the fifth policy year, the entire vested value can be used to purchase one of the Settlement Options. Surrender Charges and the Market Value Adjustment would not apply. • Option 1 - Life Income Only • Option 2 – Life Income with • Option 3 – Period Certain Only Guaranteed Period Certain

SSLIANQS-OT REV 06/15 SENTINEL SECURITY LIFE INSURANCE COMPANY | P. O. Box 27248 | Salt Lake City, UT 84127-0248 | (800) 247-1423

Optional Income RiderThe Income Rider is only available if the Annuitant is an Owner, unless the Owner is not a Natural Person. If the Owner is not a Natural Person, the Annuitant will be treated as the Owner for purposes of this Rider. If the Base Policy has Joint Owners, the Income Rider is only available if the Joint Owners are spouses. The Income rider is subject to a minimum issue age of 45 and benefits may begin anytime after the first Policy Year once the owner has attained age 55.

Charge The GLWB is available for an additional rider charge equal to 1.05% assessed on the Income Account Value and deducted from the Accumulation Value.

Premium Bonus

An additional one-time bonus equal to 1% of the single premium payment will be credited to the Accumulation Value and the Income Account Value on the Policy Date. The total one-time bonus will be equal to 8%.

Income Account

Value

• The Income Account Value is used to calculate the annual GLWB once elected. It is not an amount that may be withdrawn and is not payable on death. The annual GLWB is equal to the Income Account Value multiplied by the Payout Factor corresponding to the attained age of the Owner when income starts.

• Annual Compound Rollup for 10 years- 4.50% for issue ages 45-49- 5.00% for issue ages 50-59- 6.00% for issue ages 60-69- 6.50% for issue ages 70+

• Rollup stops at the earlier of:• The start of GLWBs• The day the oldest Owner, or if the Owner is a Non-natural Person, the Annuitant turns age 85, or• The end of the Initial Roll-up Term Period of 10 years

• Option to renew for an additional 10 years except:• On or after the oldest Owner, or if the Owner is a Non-natural Person, the Annuitant, turns 80• If the Owner previously terminated this rider, or• If the GLWBs have started

• New Rider Fees may apply when rider is renewed

Payout Factors

Rider and features are not available in all states and are subject to change without notice. See annuity contract, agent field guide, rate sheet, and statement of understanding for additional details. All forms are available on the agent portal at www.sslco.com/agents.

The “S&P 500®” is a product of S&P Dow Jones Indices LLC or its affiliates (“SPDJI”), and has been licensed for use by Sentinel Security Life Insurance Company. Standard & Poor’s® and S&P® are registered trademarks of Standard &

Poor’s Financial Services LLC (“S&P”); Dow Jones® is a registered trademark of Dow Jones Trademark Holdings LLC (“Dow Jones”); and these trademarks have been licensed for use by SPDJI and sublicensed for certain

purposes by Sentinel Security Life Insurance Company. Summit Bonus IndexSM is not sponsored, endorsed, sold or promoted by SPDJI, Dow Jones, S&P, or their respective affiliates and none of

such parties make any representation regarding the advisability of investing in such product(s) nor do they have any liability for any errors, omissions, or

interruptions of the S&P 500®.SSLIANQS-OT REV 06/15

Attained Age

Single Life Payout

Joint Life Payout**

Attained Age

Single Life Payout

Joint Life {ayout**

Attained Age

Single Life Payout

Joint Life Payout**

Attained Age

Single Life Payout

Joint Life Payout**

55 4.10% 3.60% 64 5.00% 4.50% 73 5.90% 5.40% 82 6.80% 6.30%56 4.20% 3.70% 65 5.10% 4.60% 74 6.00% 5.50% 83 6.90% 6.40%57 4.30% 3.80% 66 5.20% 4.70% 75 6.10% 5.60% 84 7.00% 6.50%58 4.40% 3.90% 67 5.30% 4.80% 76 6.20% 5.70% 85 7.10% 6.60%59 4.50% 4.00% 68 5.40% 4.90% 77 6.30% 5.80% 86 7.20% 6.70%60 4.60% 4.10% 69 5.50% 5.00% 78 6.40% 5.90% 87 7.20% 6.70%61 4.70% 4.20% 70 5.60% 5.10% 79 6.50% 6.00% 88 7.20% 6.70%62 4.80% 4.30% 71 5.70% 5.20% 80 6.60% 6.10% 89 7.20% 6.70%63 4.90% 4.40% 72 5.80% 5.30% 81 6.70% 6.20% 90+ 7.20% 6.70%

**Based on the Younger Joint Life