2016 - SC Department of Revenue · 2016 (Rev. 9/19/14) 7037. 1 PROPERTY TAX TIMETABLE INFORMATION...

36

To Be Used By The Following Property Types: Manufacturing Mining Corporate Headquarters Corporate Offices Facilities Distribution Facilities Research and Development Facilities Leased Utilities Leased Transportation For Hire Fee In Lieu of Tax Properties This Package Contains: PT-300 Instructions Schedules A, B, C, D, E, F, S and T Schedule X Schedule Z Schedule Instructions Property Tax and Fee In Lieu Schedules and Instructions For PT-300 State of South Carolina Department of Revenue 2016 (Rev. 9/19/14) 7037

Transcript of 2016 - SC Department of Revenue · 2016 (Rev. 9/19/14) 7037. 1 PROPERTY TAX TIMETABLE INFORMATION...

To Be Used By The Following Property Types:ManufacturingMining Corporate HeadquartersCorporate Offices FacilitiesDistribution FacilitiesResearch and Development FacilitiesLeased UtilitiesLeased Transportation For HireFee In Lieu of Tax Properties

This Package Contains:PT-300 InstructionsSchedules A, B, C, D, E, F, S and TSchedule XSchedule ZSchedule Instructions

Property Tax and Fee In LieuSchedules and Instructions

For PT-300

State of South CarolinaDepartment of Revenue

2016

(Rev. 9/19/14) 7037

1

PROPERTY TAX TIMETABLE

INFORMATION

Location: 300A Outlet Pointe Blvd.Columbia, South Carolina 29210

REMINDERS

CHECK THE FOLLOWING ITEMS BEFORE MAILING YOUR RETURN.* SID number included on all forms.* SCHEDULE SUMMARY completed with information from attached schedules.* SCHEDULE X attached to the associated schedule.* SCHEDULE Z attached after page 2 of PT-300.* POLLUTION detail list attached to the associated schedule.* POLLUTION detail list (copy) maintained at the plant site.* RETURNS signed by taxpayer and preparer.* RETURNS not filed timely may result in penalties, estimates and loss of an exemption.

Mailing Address:

South Carolina Department of RevenueManufacturing SectionColumbia, South Carolina 29214-0302

Telephone Number: (803) 898-5055

* Accounting Closing Date - "When Are Returns Required To Be Filed?", page 4.* Return Due Date - Returns are due on or before the last day of the fourth month following the taxpayer's accounting

closing date.* Notice of Assessment - Taxpayers are notified of assessments and exemptions in August of each year.* Appeal Period - Ninety (90) day appeal period. (See page 3)* Tax Bills - Assessments are furnished to counties, local millage rate applied and tax bills issued in the fall.

Websites: Department of Revenue: www.dor.sc.govAssociation of Counties: www.sccounties.org

FREQUENTLY ASKED QUESTIONS

Who is required to file this return? .................................................................................................................................. 4When are taxpayers required to file? ............................................................................................................................... 4Which tax year return to file? ........................................................................................................................................... 4Are extensions granted? ................................................................................................................................................. 4Are amended returns accepted? ...................................................................................................................................... 4

Forms: (803) 898-5320(800) 768-3676

2

TABLE OF CONTENTS

1

33

7, 134, 10

67355

4, 107, 13

945

445

111111121213

6865

4, 105

1414

143

4, 1011

104

1047

4, 10

912

9124

Accounting Closing Date .........................................................Change in ..............................................................................Airline companies ............................................................... Amended Returns ................................................................Annual Returns ........................................................................Appeal Procedure ...................................................................Assessment Notice Date .......................................................... Building and Land Improvements ...........................................Cable Television Companies .............................................Carlines ..............................................................................Classification Guidelines .........................................................Computer Hardware and Software ..........................................Corporate Headquarters or Offices

Classification Guidelines ................................................Who Is Required To file? ................................................

Depreciation RateSchedules A, E, F and S

Gross Cost less depreciation .......................................Schedules B, C, D and T

Net Book ......................................................................Due Date, Return ..................................................................... Estimates - Failure to file ......................................................... Exemptions

Application for ...............................................................Code Section ................................................................

Evasion of Property Tax and Assessment ...............................Extensions ...............................................................................Failure to File ...........................................................................Fee In Lieu of Tax (FILOT)

Classification Guidelines ................................................Schedule S .....................................................................Who Is Required To File?................................................

Final Return .............................................................................Forms and Information ............................................................Furniture and Office Equipment ............................................... Gross Cost, definition ..............................................................Idle Property ............................................................................Initial Return ......................................................................... Jobs Created ............................................................................

12-37-220B (32) ............................................................Land .........................................................................................Land Improvements ................................................................ Leased Property

Who Is Required To File? ..............................................Schedule Z .....................................................................

Leasehold Improvements .........................................................Machinery and Equipment ..................................................Mailing Address ......................................................................Manufacturing

Definition ........................................................................Classification Guidelines ................................................

MiningDefinition .........................................................................Classification Guidelines .................................................

NAICS Code..............................................................................Net Book, definition ..................................................................No Longer Reporting Assets ....................................................Office Facility

Classification Guidelines .................................................Ownership, change in ..........................................................

Payment Date ........................................................................... Penalties

Late Filing .......................................................................Late Payment ..................................................................

Personal Property-Defined ................................................. Pipeline Companies ............................................................ Plant/operation name ................................................................ Pollution Control ....................................................................... Power of Attorney ..................................................................... Preprinted returns ..................................................................... PT-300 Instructions ................................................................... Railway Companies ............................................................ Real Property Improvements .............................................. Research and Development

Classification Guidelines .................................................Who Is Required To File? ...............................................

Return Filing Status .................................................................. Sale of Property

After Closing Date ...........................................................Before Closing Date ........................................................Final Return ....................................................................

SC Code Sections12-37-220A(7) ...............................................................12-37-220A(8) ...............................................................12-37-220B(32) .............................................................12-37-220B(34) .............................................................12-37-220(C) .................................................................

SC Property Tax Regulations 117-105 .................................... Schedule Instructions

A, B, C, D E, F ................................................................S, T, X, Z ........................................................................

Schedule Number ..................................................................... Schedule Summary ................................................................... Sewer Companies ............................................................... SID Number .............................................................................. Social Security Privacy Act .................................................... Tax Bill ......................................................................................Tax Year ................................................................................... Taxpayer Bill of Rights ........................................................... Taxpayer Representative .......................................................... Telephone Companies ........................................................ Telephone Numbers ................................................................. Timetable ..................................................................................Transportation for Hire

Classification Guidelines ..............................................Who Is Required To File? ..............................................

Utility PropertiesClassification Guidelines ...............................................Who Is Required To File? ...............................................

Vehicles, licensed ..................................................................... Water Companies ............................................................... Warehouse Facility

Classification Guidelines ..................................................Definition .........................................................................

Wholesale Distribution FacilitiesClassification Guidelines .................................................Definition ........................................................................Who Is Required To File? ...............................................

54, 5

4, 104, 5

331

134, 104, 10

97

94

7

743

1211343

9645

1577

124, 5

7117

13

487

7, 1315

39

39676

95,12

3

TAXPAYER REPRESENTATIVEForm SC2848, Power of Attorney and Declaration of Representative, must be signed by the taxpayer and the representative in orderto authorize an individual to represent a taxpayer. Authorization has been restricted to attorneys, CPAs and enrolled agents. Thetaxpayer should consider indicating on the Power of Attorney that the representative has the authority to represent the taxpayer inproperty tax matters as well as income tax matters as they relate to property tax. Authorization may be extended to registered, licensedor certified real estate appraisers in questions of real property value only.

Any taxpayer aggrieved by a new or amended value, assessment or fee may appeal by filing a "written protest" within ninety (90)days of the date of the "PROPERTY ASSESSMENT NOTICE". The valuation for the property under appeal shall be adjusted to eightypercent (80%) upon acceptance of the appeal by the Department of Revenue, pending resolution. Any valuation greater than eightypercent (80%) agreed to in writing by the taxpayer may be accepted pending resolution of the appeal. Interest at a rate establishedunder SC Code Section 12-54-25 shall be added for the unpaid portion. Penalties may be appealed in accordance with SC RevenueProcedure #98-3.

APPEAL PROCEDURES

MANUFACTURING AND MINING DEFINEDA Manufacturer is every person engaged in making, fabricating or changing things into new forms or in refining, rectifying or combiningdifferent materials. Manufacturing and mining is further defined by the classifications set out in Sectors 21, 31, 32 and 33 of the mostrecent North American Industrial Classification System Manual, with the exception of publishers of newspapers, books and periodicalswhich do not actually print their publications. In accordance with SC Code Section 12-43-335.

EXEMPTION/ESTIMATESSee application for exemption and SC Code Sections 12-37-220(A)(7), (A)(8), (B)(32), (B)(34) and 12-37-220(C) on pages 11 and 12.

FAILURE TO FILEFailure to file in a timely manner may result in an estimated assessment, the loss of exemptions and late filing penalties, in accordancewith SC Code Section 12-37-800.

EVASION OF PROPERTY TAX OR ASSESSMENTCivil and Criminal penalties and damages can be found under SC Code Sections 12-54-43 and 44.

PENALTIESLate Filing penalties may be appealed in writing in accordance with SC Revenue Procedure #98-3.

Late Payment penalties are applied by the local county and should be appealed to the County Auditor. Telephone numbers and mailingaddresses for all county officials are on the Association of Counties website.

MILLAGE RATES or tax levies are applied by the local county auditors. Telephone numbers for all county auditors are available on theAssociation of Counties website.

A "written protest" must be filed within ninety (90) days and containing the following:1) Property owner's name, address, and telephone number.2) SID number as shown on the assessment notice.3) Date of assessment notice appealing.4) Tax year appealing.5) Identify the plant operation schedule identification number (SCHD A00001).6) Indicate any combination of the following as the matter(s) under appeal for each schedule:

a) Real Property Value/Assessment/Feeb) Personal property Value/Assessment/Feec) Exemption Assessmentd) Penalty Assessment/Fee

7) All reasons or grounds by which the taxpayer disagrees with the valuation/assessment/fee.8) The valuation and assessment which the taxpayer deems to be the fair market value and assessment of the property under

appeal.9) Name and telephone of a contact person.

10) Power of Attorney and Declaration of Representative form SC2848 must be completed and filed as a part of the appeal forall taxpayer representatives. The taxpayer should consider indicating on the Power of Attorney that the representative has theauthority to represent the taxpayer in property tax matters as well as income tax matters as they relate to property tax.This is important since many property tax issues require reference to information filed on the income tax return. If this power isnot granted, we will not be able to discuss these issues with the representative. (See SC Code Section 12-60-90)

11) Agreed upon percentage valuation, assessment or fee in excess of eighty percent (80%). See information above.

GENERAL INFORMATION

4

The PT-300 is designed to be used for all property types listedbelow under "Who is Required to File?" and should be used forany RETURN FILING STATUS from the initial return to the finalreturn. A separate return is required for each property location.Once the property has been registered with the Property Divisionof the South Carolina Department of Revenue, the taxpayer willbe issued annual returns preprinted with identification andschedule information. The taxpayer should review all preprinteditems for accuracy and enter all items not preprinted on thereturn. The taxpayer is responsible for completing and attachingthe appropriate plant/operation schedules. When filing an initialreturn or adding a new plant/operation, refer to theCLASSIFICATION GUIDELINES on page 9 to determine theappropriate schedules to file. For due date information, refer to"When are taxpayers required to file?". All code references comefrom the 1976 Code of Laws of South Carolina, as amended.

Who is required to file this return?The owners of all real and/or personal property of which a Fee InLieu of Tax agreement has been negotiated with the county.

The owners of all real and/or personal property owned, used, orleased* by the following businesses:(1) Manufacturing(2) Mining(3) Industrial Development Projects assessed under "Fee in lieu

of tax" agreements under SC Code Sections 4-29-67,4-29-69 and 12-44

(4) The following facilities that qualify for an exemption under SCCode Sections 12-37-220B(32) of 12-37-220B(34):

(a) Corporate Headquarters(b) Corporate Office Facilities(c) Distribution Facilities(d) Research and Development Facilities

The owners of all real and/or personal property used by orleased* to the following utility and transportation for hirecompanies:(1) Water, Heat, Light and Power(2) Telephone(3) Cable Television(4) Sewer (5) Railway(6) Private Carline(7) Airline(8) Pipeline

*All leased property should be reported by the owner. Whenleased property is capitalized by the lessee for income taxpurposes, the lessee is considered the owner, in accordance withSC Revenue Ruling #93-11.

Which tax year return to file?Property taxes are based on the status of the property as of thetaxpayer's accounting closing date of the previous year. Thetaxpayer's 2003 tax year return should be based on the 2002accounting closing date. For example, a taxpayer filing a returnbased on his March 2002 accounting closing date, should file hisTAX YEAR 2003 return, due on or before July 31, 2002.

When are taxpayers required to file?Returns are required to be filed not less than once each calendaryear, in accordance with SC Code Section 12-37-970. Returnsare normally due on or before the last day of the fourth monthfollowing the taxpayers accounting closing date used for incometax purposes. The following exceptions apply:

Initial return: The initial return is required to be filed for the firstcalendar year in business based on the taxpayers accountingclosing date or December 31, whichever comes first. Example: Ataxpayer that starts operation in July, after his June accountingclosing date, should file based on assets as of Dec 31.

Change in account closing date: When a taxpayer changes hisaccounting closing date, within a calendar year, he must file areturn for each accounting closing date. The Department ofRevenue will determine the assessment from each return and usethe highest assessment.

Property sold after the seller's account closing date: A returnis required by the seller, based on the seller's accounting closingdate. The purchaser is not required to file a return as of thepurchaser's accounting closing date during the calendar year ofthe sale.

Property sold before the seller's account closing date: Aninitial return is required by the purchaser, based on thepurchaser's accounting closing date or Dec 31, whichever comesfirst, after the purchase of the property.

Are extensions granted?Extensions are not granted for filing of property tax returns.Extensions granted for income tax purposes do not apply toproperty tax returns. SC Code Section 12-37-980 providing forproperty tax extensions was repealed.

Are amended returns accepted?Amended returns may be accepted up to the due date of thereturn. Amended returns, filed after the due date, may beaccepted or rejected by the Department of Revenue, inaccordance with SC Code Section 12-37-975.

PT-300 INSTRUCTIONS

5

Please type or print all items requested. Round all entries to thenearest dollar. Returns must be signed and dated by both thetaxpayer and the preparer. To determine the due date of thereturn, refer to "When are taxpayers required to file?", page 4.

Preprinted returns are issued for all property locations registeredwith the Property Division of the Department of Revenue. Thesereturns are preprinted with your account information. To avoiderrors and duplicate assessments, taxpayers are encouraged touse the preprinted returns when available. Preprinted returnsmay be requested by contacting the Property Division.

When filing on the preprinted return, the taxpayer should verify allpreprinted items. All changes, corrections and additional entriesare to be reported in the change field to the right of the item beingchanged. When filing on a blank return, the taxpayer is requiredto complete all items on the return.

SID NUMBEREnter your SINGLE IDENTIFICATION NUMBER (SID), asassigned by the Department of Revenue. The first seven (7) digitsis a unique number used for all tax types. The next three (3)digits indicate a separate location for each tax type and the lastdigit is a check digit. Please refer to the entire eleven (11) digitnumber on all correspondence.

COUNTYEnter the name of the county in which the property is located.

RETURN FILING STATUSEnter the filing status of this return. (Check one).

* Initial ReturnAn initial return is required your first calendar year in businessbased on your accounting closing date or Dec. 31, whichevercomes first.

* Annual ReturnAn annual return is required each calendar year after your initialreturn, based on your accounting closing date.

* Amended ReturnAn amended return may be filed to correct a previously filedreturn. A three year statute of limitations exists for theabatement or refund of property taxes. This is in accordancewith SC Code Sections 12-37-975 and 12-54-85.

* Returns Due to Change in Accounting Closing DateWhen a taxpayer changes his accounting closing date within acalendar year, he must file a return for each accounting closingdate. The Department of Revenue will determine theassessment from each return and use the highest assessment.Only the return reporting the new accounting closing dateshould be filed under this filing status. The return for the originalaccounting closing date should be filed under the "annual" or"initial" filing status. For the additional filing, a preprinted returnmay be requested by contacting the Property Division.

*Final ReturnA final return is required after all operations have ceased or theproperty is sold. The filing of a final return will initiate a review ofthe property prior to closure. (Note: If still in operation on youraccounting closing date, the "annual" return filing status should beused.) If the final return is the result of a change in ownership,complete the change in ownership section on the form PT-300.Also, complete the appropriate plant/operation schedule reportingthe reason and the date of occurrence.

OWNER NAME AND MAILING ADDRESSEnter the property owner's name and mailing address. Name andaddress changes or spelling corrections should be reported in thecorrections area. For corporations, only name corrections orchanges that have been recorded with the Secretary of Stateshould be reported. Name changes resulting from a change inownership should be reported under CHANGE IN OWNERSHIP.The OWNER MAILING ADDRESS reported on this return will beused for all future correspondence including assessment noticesand tax bills issued by the county. The attention line of theaddress may be used for additional mailing or routing informationsuch as "Attn: Bill Smith, Property Tax Department".

ACCOUNT DATA

Federal EI or SSNEnter the taxpayer's Federal Employer Identification (FEI) numberor Social Security Number (SSN).

Property LocationEnter the exact property location information (street address, city,zip code and phone number).

Accounting Closing DateEnter the taxpayer's accounting closing date used for income taxpurposes (month/year).

Start Up DateEnter the date that the operation started at this location(month/day/year).

Contact PersonEnter the name of a contact person.

Contact Person Phone NumberEnter the contact person's telephone number.

Name Used To File Income TaxIf you are filing a consolidated income tax return or for any otherreason filing under another name, enter the name and FEI orSSN used to file that return.

CHANGE IN OWNERSHIPIf there has been a change in ownership of this facility, pleasecomplete this portion of the return. The purchaser of an existingfacility should review SC 12-37-220(C) and Application forExemption on page 12. Seller and purchaser should review"When are taxpayers required to file?" on page 4.

6

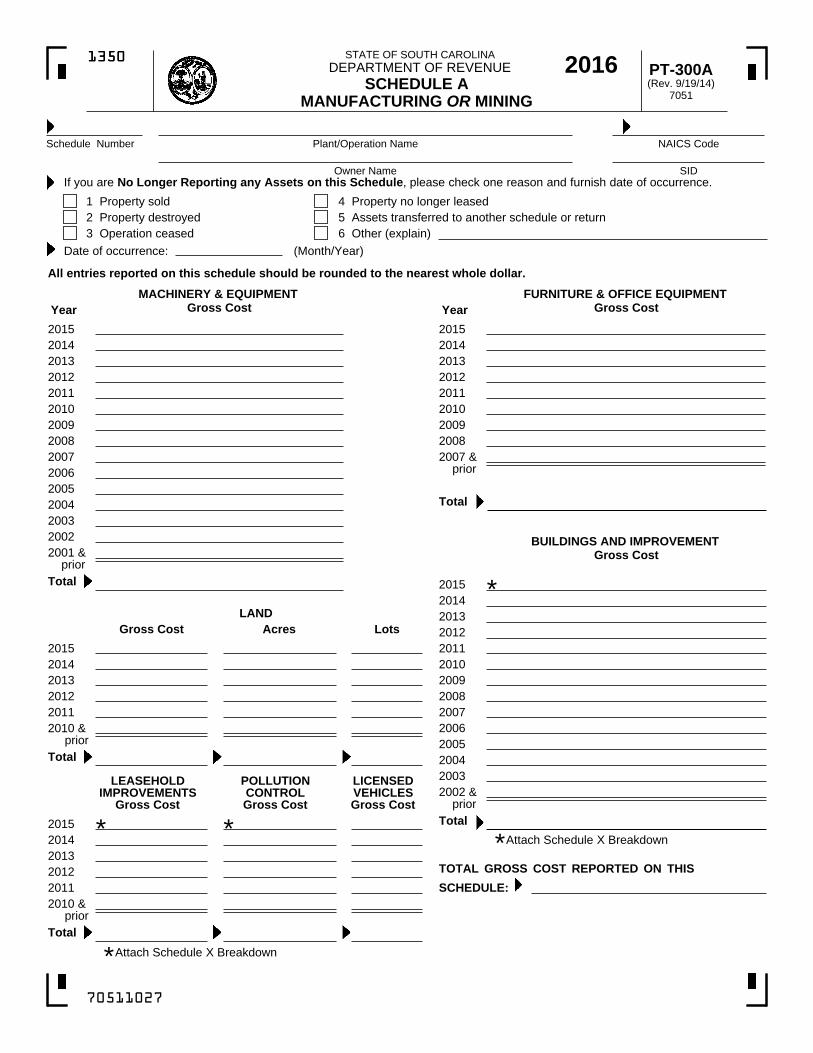

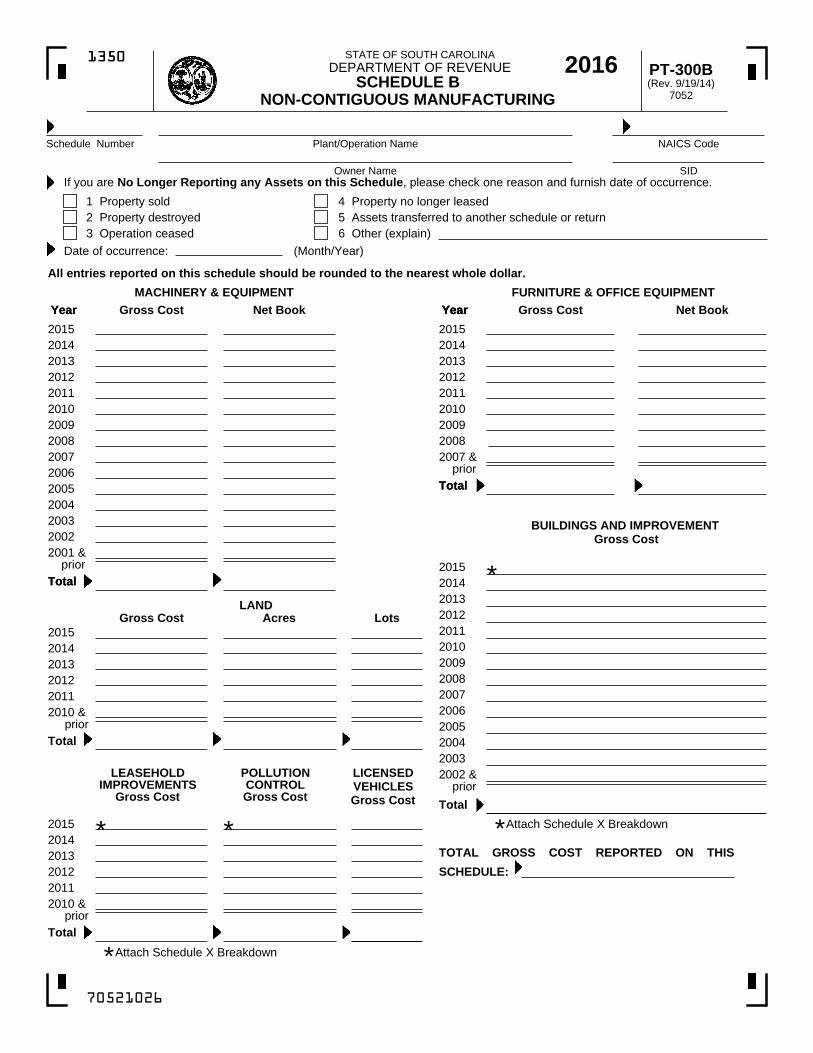

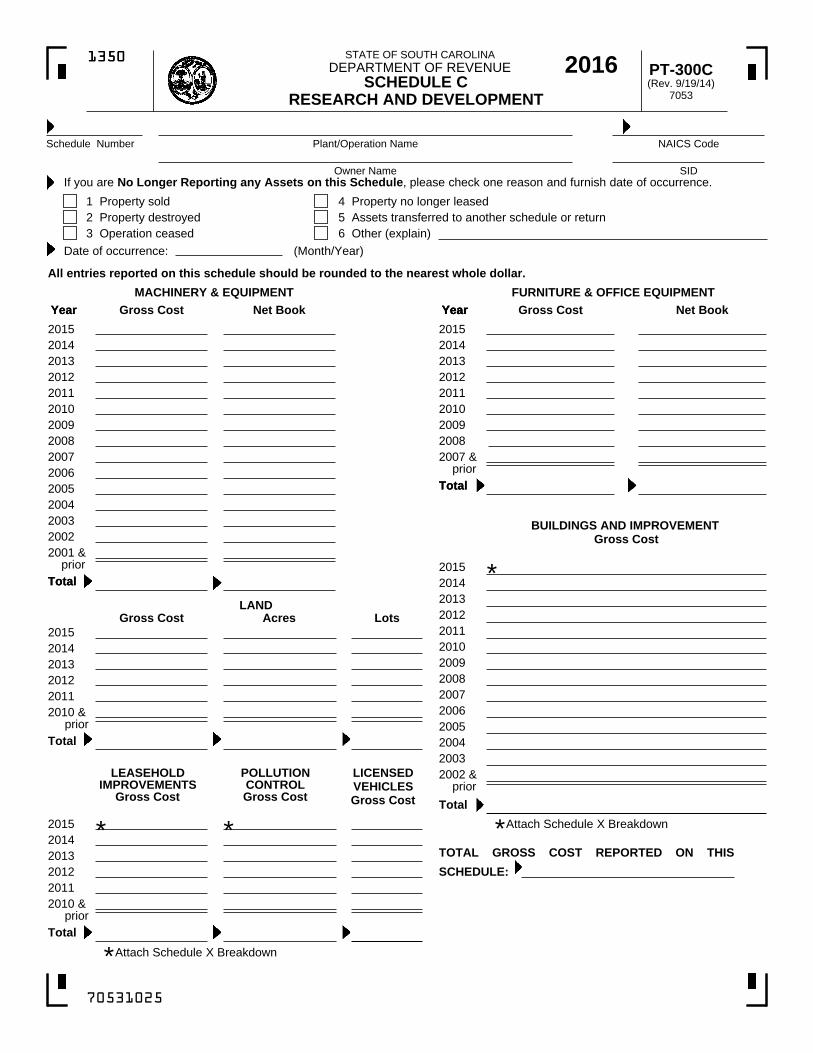

A schedule is required for each plant/operation reporting the fixedassets at that location. Preprinted returns for existing accountshave the required schedule(s) listed in the SCHEDULESUMMARYon the form PT-300. New operations should refer tothe CLASSIFICATION GUIDELINES to determine the appropriateschedule(s) (see page 9). If the property location has multipleoperations that fall into more than one classification, separateplant/operation schedules should be filed for each. DO NOTsubmit ledgers or computer printouts in lieu of appropriateschedule.

Only one copy of each schedule is included in this booklet. Ifadditional schedules are needed, copies will be accepted. Youmay contact the Department of Revenue or visit our website foradditional schedules.

The items covered in the following instructions are not required onall schedules. Only the items specifically requested on eachschedule are required. For example, net book value is onlyrequired on Schedules B, C, D and T.

SCHEDULE NUMBERThe SCHEDULE NUMBER is used to designate multipleschedules for a given classification of property.

When filing your initial return or adding a new schedule to anexisting account, leave this area blank. The schedule number willbe assigned by the Department of Revenue as eachplant/operation is registered. When subsequent annual returnsare preprinted each year, the schedule letter and assignedschedule number will be printed in the schedule summary. Pleasemaintain a record of the schedule letter and number assigned toeach plant/operation as a reference for future correspondenceand assessment notices. If you have multiple "Fee in Lieu of Tax"agreements, a separate schedule should be completed for eachagreement.

PLANT/OPERATION NAMEThe PLANT/OPERATION NAME is assigned by the taxpayerwhen filing his initial return or adding a new schedule. Theplant/operation name must be unique for each taxpayerstatewide. The name on each schedule should correspond to the

SCHEDULES A, B, C, D, E, F, S AND TPLANT/OPERATION SCHEDULE INSTRUCTIONS

SCHEDULE SUMMARY

This portion of the return is a summary of all plant/operationschedules filed as a part of this return. Complete each scheduleaccording to the Plant/Operation instructions below. Enter theschedule letter, schedule number, plant/operation name and thetotal gross capitalized cost reported on each schedule. If you areno longer reporting assets on a schedule previously reported, filethe schedule stating the reason for no assets. Enter a zero (0) forthe total gross capitalized cost on the plant/operation scheduleand the SCHEDULE SUMMARY. If you are filing an initial returnor adding new schedules to an existing account, do not enter aschedule number. The schedule number will be assigned by theDepartment of Revenue as each operation is registered.

ADDITIONAL SCHEDULESSCHEDULE XCheck box when Schedule X is attached reporting the breakdownof real property, leasehold and pollution control improvements.

SCHEDULE ZCheck box when Schedule Z is attached reporting additionalleases. Leases currently on our records are listed on page 2 ofthe form PT-300.

SIGNATURE AND DATEAll returns must be signed and dated by the preparer and thetaxpayer or an officer of the company. Property tax returns mustbe mailed separately from the income tax or any other type taxreturn filed with the Department of Revenue.

plant/operation name in the SCHEDULE SUMMARY on the formPT-300. Space is limited to forty (40) alpha and/or numericcharacters. Examples of plant/operation names are:

Plant No 13Corporate HeadquartersSmith Inc Fiber Plant Spartanburg

NAICS CODE Enter your North American Industrial Classification System code.NAICS codes have been published for all fields of economicactivity by the Executive Office of the President, Office ofManagement and Budget. (replaces the Standard IndustrialClassification system)

OWNER NAME Enter the property owner's name as reported on the form PT-300. SIDEnter the SINGLE IDENTIFICATION NUMBER as reported on theform PT-300. If you are setting up a new account, a SID will beassigned when the return is processed.

NO LONGER REPORTING ANY ASSETSIf you are no longer reporting any assets on a given schedule,check one of the reasons and enter the month and year of theoccurrence. When reporting no assets on a schedule, enter zero(0) as the TOTAL GROSS COST on the schedule and in theSCHEDULE SUMMARY on the form PT-300.

PROPERTY LISTINGSWhen completing the plant/operation schedule, enter by year ofacquisition, the gross capitalized cost and net book value, whenapplicable, for all fixed assets as shown by the taxpayer's recordsfor income tax purposes. Round all entries to the nearest dollar.The years listed represent the year in which the accounting periodended and that entry should include all assets acquired for thataccounting year. The last year listed for each property typeshould include all assets acquired for that year and all prior years.Adjustments for disposals should be made by reducing theinvestment by the amount of the disposal for the year ofacquisition.

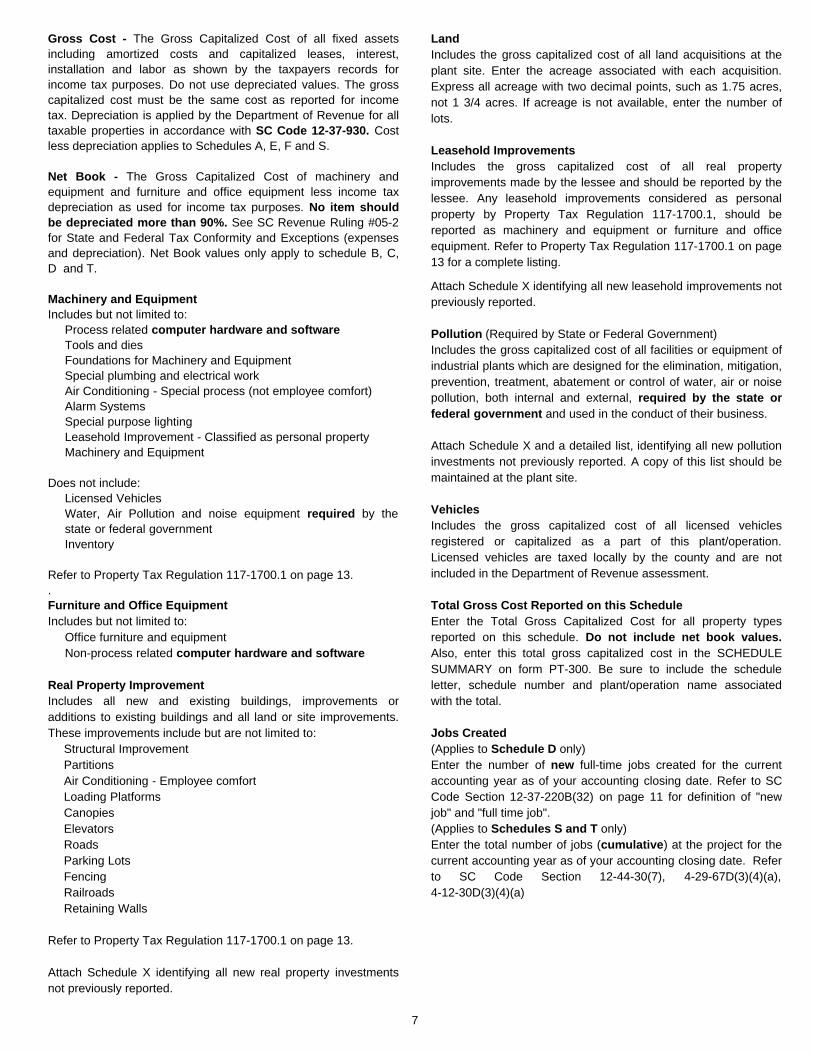

Gross Cost - The Gross Capitalized Cost of all fixed assetsincluding amortized costs and capitalized leases, interest,installation and labor as shown by the taxpayers records forincome tax purposes. Do not use depreciated values. The grosscapitalized cost must be the same cost as reported for incometax. Depreciation is applied by the Department of Revenue for alltaxable properties in accordance with SC Code 12-37-930. Costless depreciation applies to Schedules A, E, F and S.

Net Book - The Gross Capitalized Cost of machinery andequipment and furniture and office equipment less income taxdepreciation as used for income tax purposes. No item shouldbe depreciated more than 90%. See SC Revenue Ruling #05-2for State and Federal Tax Conformity and Exceptions (expensesand depreciation). Net Book values only apply to schedule B, C,D and T.

Machinery and EquipmentIncludes but not limited to:

Process related computer hardware and softwareTools and diesFoundations for Machinery and EquipmentSpecial plumbing and electrical workAir Conditioning - Special process (not employee comfort)Alarm SystemsSpecial purpose lightingLeasehold Improvement - Classified as personal propertyMachinery and Equipment

Does not include:Licensed VehiclesWater, Air Pollution and noise equipment required by thestate or federal governmentInventory

Refer to Property Tax Regulation 117-1700.1 on page 13..Furniture and Office EquipmentIncludes but not limited to:

Office furniture and equipmentNon-process related computer hardware and software

Real Property ImprovementIncludes all new and existing buildings, improvements oradditions to existing buildings and all land or site improvements.These improvements include but are not limited to:

Structural ImprovementPartitionsAir Conditioning - Employee comfortLoading PlatformsCanopiesElevatorsRoadsParking LotsFencingRailroadsRetaining Walls

Refer to Property Tax Regulation 117-1700.1 on page 13.

Attach Schedule X identifying all new real property investmentsnot previously reported.

7

Attach Schedule X identifying all new leasehold improvements notpreviously reported.

Pollution (Required by State or Federal Government)Includes the gross capitalized cost of all facilities or equipment ofindustrial plants which are designed for the elimination, mitigation,prevention, treatment, abatement or control of water, air or noisepollution, both internal and external, required by the state orfederal government and used in the conduct of their business.

Attach Schedule X and a detailed list, identifying all new pollutioninvestments not previously reported. A copy of this list should bemaintained at the plant site.

VehiclesIncludes the gross capitalized cost of all licensed vehiclesregistered or capitalized as a part of this plant/operation.Licensed vehicles are taxed locally by the county and are notincluded in the Department of Revenue assessment.

Total Gross Cost Reported on this ScheduleEnter the Total Gross Capitalized Cost for all property typesreported on this schedule. Do not include net book values.Also, enter this total gross capitalized cost in the SCHEDULESUMMARY on form PT-300. Be sure to include the scheduleletter, schedule number and plant/operation name associatedwith the total.

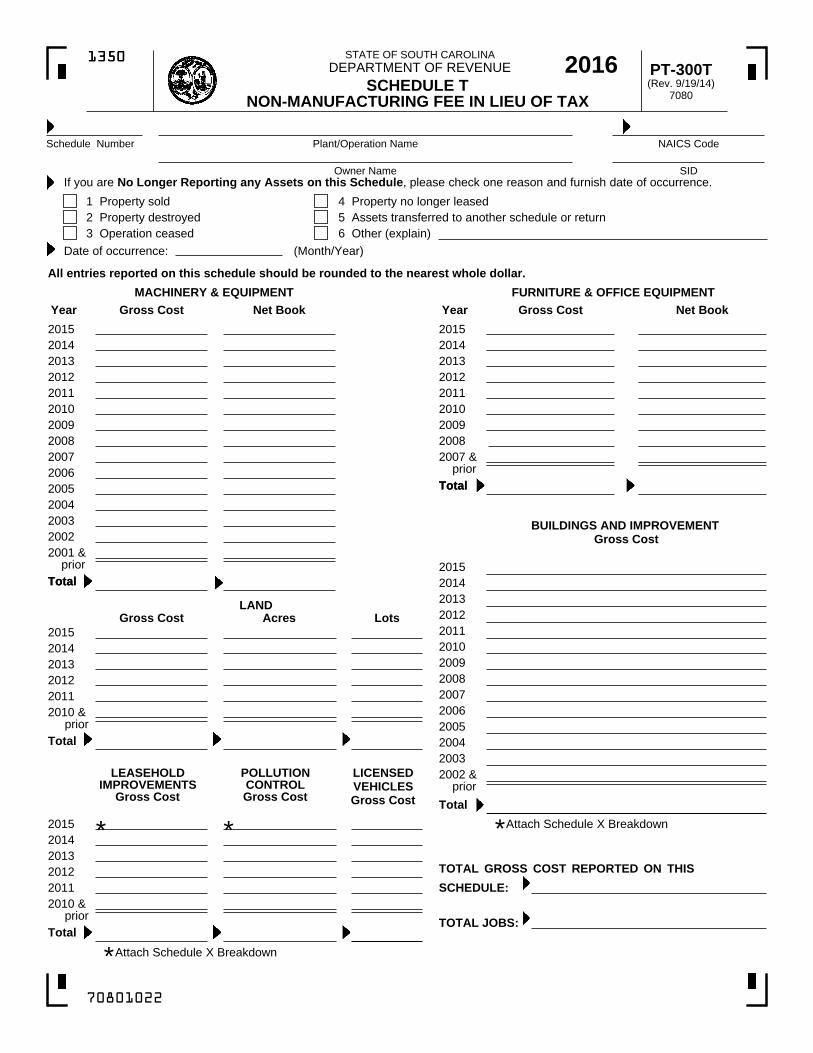

Jobs Created(Applies to Schedule D only)Enter the number of new full-time jobs created for the currentaccounting year as of your accounting closing date. Refer to SCCode Section 12-37-220B(32) on page 11 for definition of "newjob" and "full time job". (Applies to Schedules S and T only)Enter the total number of jobs (cumulative) at the project for thecurrent accounting year as of your accounting closing date. Referto SC Code Section 12-44-30(7), 4-29-67D(3)(4)(a),4-12-30D(3)(4)(a)

LandIncludes the gross capitalized cost of all land acquisitions at theplant site. Enter the acreage associated with each acquisition.Express all acreage with two decimal points, such as 1.75 acres,not 1 3/4 acres. If acreage is not available, enter the number oflots.

Leasehold ImprovementsIncludes the gross capitalized cost of all real propertyimprovements made by the lessee and should be reported by thelessee. Any leasehold improvements considered as personalproperty by Property Tax Regulation 117-1700.1, should bereported as machinery and equipment or furniture and officeequipment. Refer to Property Tax Regulation 117-1700.1 on page13 for a complete listing.

Attach Schedule X Breakdown

Schedule Number NAICS Code

Owner Name

Plant/Operation Name

SIDIf you are No Longer Reporting any Assets on this Schedule, please check one reason and furnish date of occurrence.

3 Operation ceased(Month/Year)

5 Assets transferred to another schedule or return4 Property no longer leased

6 Other (explain)2 Property destroyed

Date of occurrence:

Total

Total

Year

2011

2015

LICENSEDVEHICLESGross Cost

LEASEHOLDIMPROVEMENTS

Gross Cost

POLLUTIONCONTROLGross Cost

LotsGross Cost AcresLAND

MACHINERY & EQUIPMENT Gross Cost

1 Property sold

Total

YearFURNITURE & OFFICE EQUIPMENT

Gross Cost

2001 & prior

Total

BUILDINGS AND IMPROVEMENT Gross Cost

TOTAL GROSS COST REPORTED ON THIS

SCHEDULE:

Attach Schedule X Breakdown

*

*

*

* *

2014

2010 & prior

2013

2010

Total

SCHEDULE AMANUFACTURING OR MINING

2007

20152014

All entries reported on this schedule should be rounded to the nearest whole dollar.

70511027

STATE OF SOUTH CAROLINADEPARTMENT OF REVENUE 201613501350

2003

2013

2006

2010

2013

2015

2009

2005

2012

2004

2008

2011

2009

2012

2014

2012

2011

2008

2014

2015

201320122011

2007 & prior

2002 & prior

2010 & prior

2015

20102009

2004

20082007

20142013

2005

2012

20032002

2006

2011

PT-300A(Rev. 9/19/14)

7051

SCHEDULE BNON-CONTIGUOUS MANUFACTURING

Schedule Number NAICS Code

Total

Total

All entries reported on this schedule should be rounded to the nearest whole dollar.

Total

Total

Total

YearYear

BUILDINGS AND IMPROVEMENT Gross Cost

LICENSEDVEHICLESGross Cost

LEASEHOLDIMPROVEMENTS

Gross Cost

POLLUTIONCONTROLGross Cost

LotsGross Cost AcresLAND

Total

MACHINERY & EQUIPMENT Gross Cost Net Book

TOTAL GROSS COST REPORTED ON THIS

SCHEDULE:

Gross Cost

Total

Year Net BookFURNITURE & OFFICE EQUIPMENT

Plant/Operation Name

SIDIf you are No Longer Reporting any Assets on this Schedule, please check one reason and furnish date of occurrence.

3 Operation ceased(Month/Year)

5 Assets transferred to another schedule or return4 Property no longer leased

6 Other (explain)2 Property destroyed

Date of occurrence:

*

*

*

* *

1 Property sold

YearYear

Attach Schedule X Breakdown

Attach Schedule X Breakdown

70521026

STATE OF SOUTH CAROLINADEPARTMENT OF REVENUE 201613501350

Owner Name

2011

2015

2010

2013

2009

2014

2012

20082007 & prior

2001 & prior

2015

20102009

2004

20082007

20142013

2005

2012

20032002

2006

2011

2013

2007

20152014

2003

2006

20102009

2005

2012

2004

2008

2011

2002 & prior

2014

2010 & prior

2013

2015

PT-300B(Rev. 9/19/14)

7052

20122011

20142013201220112010 & prior

2015

SCHEDULE CRESEARCH AND DEVELOPMENT

Schedule Number NAICS Code

Total

Total

All entries reported on this schedule should be rounded to the nearest whole dollar.

Total

Total

Total

YearYear

BUILDINGS AND IMPROVEMENT Gross Cost

LICENSEDVEHICLESGross Cost

LEASEHOLDIMPROVEMENTS

Gross Cost

POLLUTIONCONTROLGross Cost

LotsGross Cost AcresLAND

Total

MACHINERY & EQUIPMENT Gross Cost Net Book Gross Cost

Total

Year Net BookFURNITURE & OFFICE EQUIPMENT

Plant/Operation Name

TOTAL GROSS COST REPORTED ON THIS

SCHEDULE:

SID

3 Operation ceased(Month/Year)

5 Assets transferred to another schedule or return4 Property no longer leased

6 Other (explain)2 Property destroyed

Date of occurrence:

*

*

*

* *

1 Property sold

YearYear

Attach Schedule X Breakdown

Attach Schedule X Breakdown

70531025

If you are No Longer Reporting any Assets on this Schedule, please check one reason and furnish date of occurrence.

STATE OF SOUTH CAROLINADEPARTMENT OF REVENUE 201613501350

Owner Name

2011

2015

2010

2013

2009

2014

2012

20082007 & prior

2001 & prior

2015

20102009

2004

20082007

PT-300C(Rev. 9/19/14)

7053

20142013

2005

2012

20032002

2006

2011

2014

2010 & prior

2013

2015

20122011

2013

2007

20152014

2003

2006

20102009

2005

2012

2004

2008

2011

2002 & prior

20142013201220112010 & prior

2015

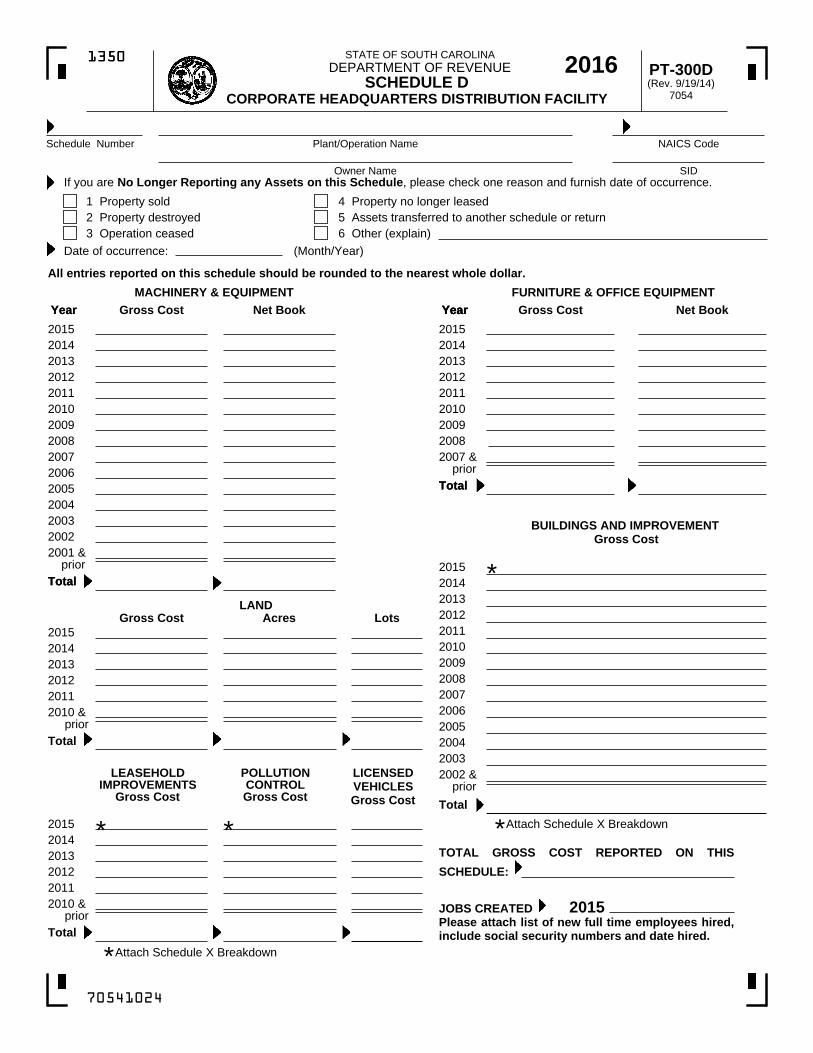

SCHEDULE DCORPORATE HEADQUARTERS DISTRIBUTION FACILITY

Schedule Number NAICS Code

Total

Total

All entries reported on this schedule should be rounded to the nearest whole dollar.

Total

Total

Total

YearYear

BUILDINGS AND IMPROVEMENT Gross Cost

TOTAL GROSS COST REPORTED ON THIS

SCHEDULE:

LICENSEDVEHICLESGross Cost

LEASEHOLDIMPROVEMENTS

Gross Cost

POLLUTIONCONTROLGross Cost

LotsGross Cost AcresLAND

JOBS CREATED 2015Please attach list of new full time employees hired,include social security numbers and date hired.

Total

MACHINERY & EQUIPMENT Gross Cost Net Book Gross Cost

Total

Year Net BookFURNITURE & OFFICE EQUIPMENT

Plant/Operation Name

SIDIf you are No Longer Reporting any Assets on this Schedule, please check one reason and furnish date of occurrence.

3 Operation ceased(Month/Year)

5 Assets transferred to another schedule or return4 Property no longer leased

6 Other (explain)2 Property destroyed

Date of occurrence:

*

*

* *

1 Property sold

YearYear

Attach Schedule X Breakdown

Attach Schedule X Breakdown

70541024

STATE OF SOUTH CAROLINADEPARTMENT OF REVENUE 2016 PT-300D

(Rev. 9/19/14)7054

13501350

Owner Name

2011

2015

2010

2013

2009

2014

2012

20082007 & prior

2001 & prior

2015

20102009

2004

20082007

20142013

2005

2012

2003

*

2002

2006

2011

2014

2010 & prior

2013

2015

20122011

2013

2007

20152014

2003

2006

20102009

2005

2012

2004

2008

2011

2002 & prior

20142013201220112010 & prior

2015

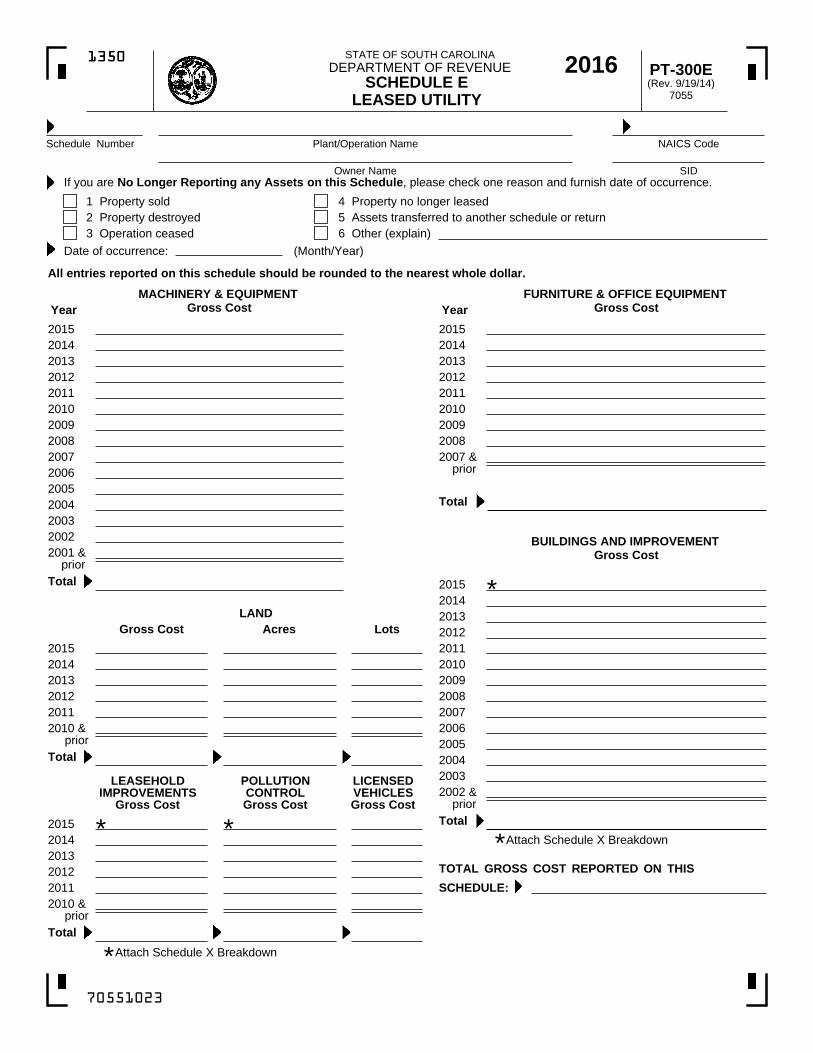

SCHEDULE ELEASED UTILITY

Attach Schedule X Breakdown

Schedule Number NAICS CodePlant/Operation Name

3 Operation ceased(Month/Year)

5 Assets transferred to another schedule or return4 Property no longer leased

6 Other (explain)2 Property destroyed

Date of occurrence:

Total

Total

Year

LICENSEDVEHICLESGross Cost

LEASEHOLDIMPROVEMENTS

Gross Cost

POLLUTIONCONTROLGross Cost

LotsGross Cost AcresLAND

MACHINERY & EQUIPMENT Gross Cost

1 Property sold

Total

YearFURNITURE & OFFICE EQUIPMENT

Gross Cost

Total

BUILDINGS AND IMPROVEMENT Gross Cost

TOTAL GROSS COST REPORTED ON THIS

SCHEDULE:

Attach Schedule X Breakdown

*

*

*

* *

Total

All entries reported on this schedule should be rounded to the nearest whole dollar.

70551023

If you are No Longer Reporting any Assets on this Schedule, please check one reason and furnish date of occurrence.

STATE OF SOUTH CAROLINADEPARTMENT OF REVENUE 201613501350

Owner Name SID

PT-300E(Rev. 9/19/14)

7055

2001 & prior

2015

20102009

2004

20082007

20142013

2005

2012

20032002

2006

2011 2011

2015

2010

2013

2009

2014

2012

20082007 & prior

2013

2007

20152014

2003

2006

20102009

2005

2012

2004

2008

2011

2002 & prior

2014

2010 & prior

2013

2015

20122011

20142013201220112010 & prior

2015

Attach Schedule X Breakdown

Schedule Number

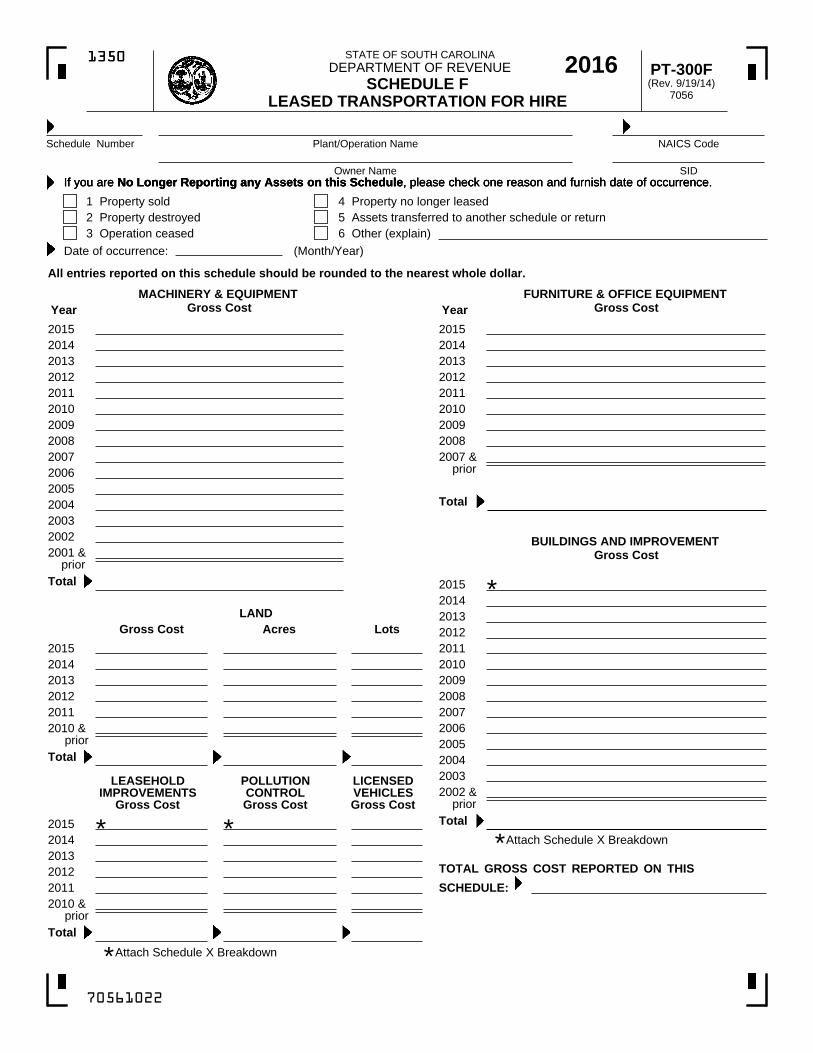

SCHEDULE FLEASED TRANSPORTATION FOR HIRE

NAICS CodePlant/Operation Name

3 Operation ceased(Month/Year)

5 Assets transferred to another schedule or return4 Property no longer leased

6 Other (explain)2 Property destroyed

Date of occurrence:

Total

Total

Year

LICENSEDVEHICLESGross Cost

LEASEHOLDIMPROVEMENTS

Gross Cost

POLLUTIONCONTROLGross Cost

LotsGross Cost AcresLAND

MACHINERY & EQUIPMENT Gross Cost

1 Property sold

Total

YearFURNITURE & OFFICE EQUIPMENT

Gross Cost

Total

BUILDINGS AND IMPROVEMENT Gross Cost

TOTAL GROSS COST REPORTED ON THIS

SCHEDULE:

Attach Schedule X Breakdown

*

*

*

* *

Total

All entries reported on this schedule should be rounded to the nearest whole dollar.

70561022

If you are No Longer Reporting any Assets on this Schedule, please check one reason and furnish date of occurrence.If you are No Longer Reporting any Assets on this Schedule, please check one reason and furnish date of occurrence.If you are No Longer Reporting any Assets on this Schedule, please check one reason and furnish date of occurrence.

STATE OF SOUTH CAROLINADEPARTMENT OF REVENUE 2016 PT-300F

(Rev. 9/19/14)7056

13501350

Owner Name SID

2001 & prior

2015

20102009

2004

20082007

20142013

2005

2012

20032002

2006

2011 2011

2015

2010

2013

2009

2014

2012

20082007 & prior

2013

2007

20152014

2003

2006

20102009

2005

2012

2004

2008

2011

2002 & prior

2014

2010 & prior

2013

2015

20122011

20142013201220112010 & prior

2015

SCHEDULE SMANUFACTURING FEE IN LIEU OF TAX

Attach Schedule X Breakdown

3 Operation ceased(Month/Year)

5 Assets transferred to another schedule or return4 Property no longer leased

6 Other (explain)2 Property destroyed

Date of occurrence:

Total

Total

LICENSEDVEHICLESGross Cost

LEASEHOLDIMPROVEMENTS

Gross Cost

POLLUTIONCONTROLGross Cost

LotsGross Cost AcresLAND

MACHINERY & EQUIPMENT Gross Cost

1 Property sold

Total

FURNITURE & OFFICE EQUIPMENT Gross Cost

Total

BUILDINGS AND IMPROVEMENT Gross Cost

TOTAL GROSS COST REPORTED ON THIS

SCHEDULE:

Attach Schedule X Breakdown

*

*

*

* *

Total

All entries reported on this schedule should be rounded to the nearest whole dollar.

70611025

STATE OF SOUTH CAROLINADEPARTMENT OF REVENUE 201613501350

If you are No Longer Reporting any Assets on this Schedule, please check one reason and furnish date of occurrence.

Schedule Number NAICS CodePlant/Operation Name

Owner Name SID

PT-300S(Rev. 9/19/14)

7061

YearYear

2001 & prior

2015

20102009

2004

20082007

20142013

2005

2012

20032002

2006

2011 2011

2015

2010

2013

2009

2014

2012

20082007 & prior

2013

2007

20152014

2003

2006

20102009

2005

2012

2004

2008

2011

2002 & prior

2014

2010 & prior

2013

2015

20122011

20142013201220112010 & prior

2015

TOTAL JOBS:

SCHEDULE TNON-MANUFACTURING FEE IN LIEU OF TAX

Schedule Number NAICS Code

Total

Total

All entries reported on this schedule should be rounded to the nearest whole dollar.

Total

Total

Total

BUILDINGS AND IMPROVEMENT Gross Cost

LICENSEDVEHICLESGross Cost

LEASEHOLDIMPROVEMENTS

Gross Cost

POLLUTIONCONTROLGross Cost

LotsGross Cost AcresLAND

Total

MACHINERY & EQUIPMENT Gross Cost Net Book Gross Cost

Total

Net BookFURNITURE & OFFICE EQUIPMENT

Plant/Operation Name

3 Operation ceased(Month/Year)

5 Assets transferred to another schedule or return4 Property no longer leased

6 Other (explain)2 Property destroyed

Date of occurrence:

*

*

* *

1 Property sold

Year

Attach Schedule X Breakdown

Attach Schedule X Breakdown

70801022

STATE OF SOUTH CAROLINADEPARTMENT OF REVENUE 2016 PT-300T

(Rev. 9/19/14)7080

13501350

If you are No Longer Reporting any Assets on this Schedule, please check one reason and furnish date of occurrence.Owner Name SID

2011

2015

2010

2013

2009

2014

2012

20082007 & prior

2001 & prior

2015

20102009

2004

20082007

20142013

2005

2012

20032002

2006

2011

2014

2010 & prior

2013

2015

20122011

2013

2007

20152014

Year

2003

2006

20102009

2005

2012

2004

2008

2011

2002 & prior

20142013201220112010 & prior

2015

TOTAL GROSS COST REPORTED ON THIS

SCHEDULE:

TOTAL JOBS:

SCHEDULE X IMPROVEMENT SCHEDULE

LEASEHOLD IMPROVEMENTS

Gross Cost

SIDOwner Name

Enter the breakdown of improvements for each plant/operation, reporting investments not previously reported. Enter theschedule letter, schedule number and plant/operation name associated with the improvements. A separate Schedule X isrequired for each plant/operation and should be attached to the associated plant/operation schedule.

ScheduleNumber

2. Interior renovations/repair1. Change in square footage

Plant/Operation Name

9. Other (specify)

3. Roof repair/replacement

7. Site/yard improvements8. Tanks

1. Land2. Building

1. All personal property

2. Interior renovations/repair1. Change in square footage

6. Other (specify)

3. Roof repair/replacement

6. Lighting

4. Heating and air conditioning5. Sprinklers

Attach a detailed list identifying all new pollution control investments, item by item.Only investments required by state or federal governments qualify.

PERSONAL PROPERTY POLLUTION

ScheduleLetter

Gross CostREAL PROPERTY IMPROVEMENTS

Gross Cost

POLLUTION CONTROL IMPROVEMENTS

6. Other (specify)

3. Site/yard improvements4. Sedimentation ponds5. Dykes/retention ponds

Gross CostREAL PROPERTY POLLUTION

4. Site/yard improvements5. Tanks

70571021

STATE OF SOUTH CAROLINADEPARTMENT OF REVENUE 2016 PT-300X

(Rev. 9/19/14)7057

13501350

STATE OF SOUTH CAROLINADEPARTMENT OF REVENUE 2016 PT-300Z

(Rev. 9/19/14)7058

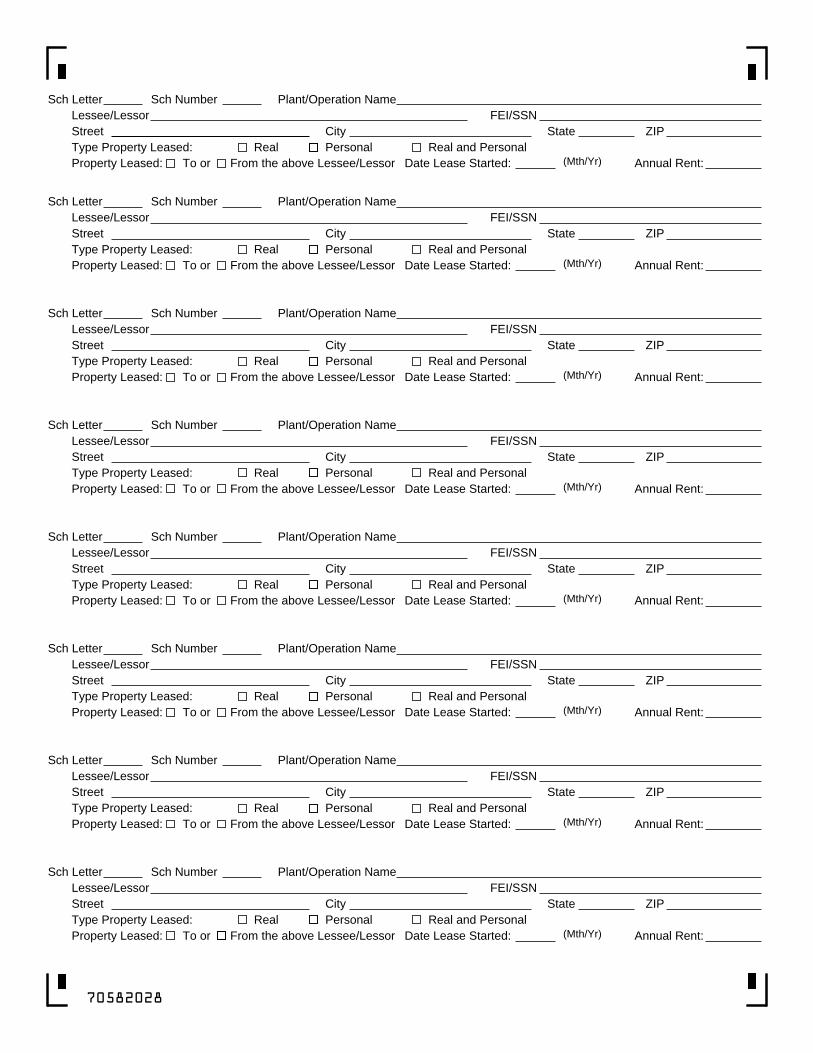

SCHEDULE ZLEASE SCHEDULE

Please furnish the following information for all leases not previously reported. Indicate the schedule letter, schedulenumber and plant/operation name associated with each lessee/lessor. Attach Schedule Z behind page two of the PT-300.

SIDOwner Name

Additional Space on Back.

13501350

70581020

Sch Number Plant/Operation NameSch LetterLessee/Lessor

To or

Street

Property Leased: From the above Lessee/LessorReal

Date Lease Started:

CityFEI/SSN

ZIPType Property Leased: Real and PersonalPersonal

(Mth/Yr) Annual Rent:

State

Sch Number Plant/Operation NameSch LetterLessee/Lessor

To or

Street

Property Leased: From the above Lessee/LessorReal

Date Lease Started:

CityFEI/SSN

ZIPType Property Leased: Real and PersonalPersonal

(Mth/Yr) Annual Rent:

State

Sch Number Plant/Operation NameSch LetterLessee/Lessor

To or

Street

Property Leased: From the above Lessee/LessorReal

Date Lease Started:

CityFEI/SSN

ZIPType Property Leased: Real and PersonalPersonal

(Mth/Yr) Annual Rent:

State

Sch Number Plant/Operation NameSch LetterLessee/Lessor

To or

Street

Property Leased: From the above Lessee/LessorReal

Date Lease Started:

CityFEI/SSN

ZIPType Property Leased: Real and PersonalPersonal

(Mth/Yr) Annual Rent:

State

Sch Number Plant/Operation NameSch LetterLessee/Lessor

To or

Street

Property Leased: From the above Lessee/LessorReal

Date Lease Started:

CityFEI/SSN

ZIPType Property Leased: Real and PersonalPersonal

(Mth/Yr) Annual Rent:

State

Sch Number Plant/Operation NameSch LetterLessee/Lessor

To or

Street

Property Leased: From the above Lessee/LessorReal

Date Lease Started:

CityFEI/SSN

ZIPType Property Leased: Real and PersonalPersonal

(Mth/Yr) Annual Rent:

State

Sch Number Plant/Operation NameSch LetterLessee/Lessor

To or

Street

Property Leased: From the above Lessee/LessorReal

Date Lease Started:

CityFEI/SSN

ZIPType Property Leased: Real and PersonalPersonal

(Mth/Yr) Annual Rent:

State

Sch Number Plant/Operation NameSch LetterLessee/Lessor

To or

Street

Property Leased: From the above Lessee/LessorReal

Date Lease Started:

CityFEI/SSN

ZIPType Property Leased: Real and PersonalPersonal

(Mth/Yr) Annual Rent:

State

Sch Number Plant/Operation NameSch LetterLessee/Lessor

To or

Street

Property Leased: From the above Lessee/LessorReal

Date Lease Started:

CityFEI/SSN

ZIPType Property Leased: Real and PersonalPersonal

(Mth/Yr) Annual Rent:

State

Sch Number Plant/Operation NameSch LetterLessee/Lessor

To or

Street

Property Leased: From the above Lessee/LessorReal

Date Lease Started:

CityFEI/SSN

ZIPType Property Leased: Real and PersonalPersonal

(Mth/Yr) Annual Rent:

State

Sch Number Plant/Operation NameSch LetterLessee/Lessor

To or

Street

Property Leased: From the above Lessee/LessorReal

Date Lease Started:

CityFEI/SSN

ZIPType Property Leased: Real and PersonalPersonal

(Mth/Yr) Annual Rent:

State

Sch Number Plant/Operation NameSch LetterLessee/Lessor

To or

Street

Property Leased: From the above Lessee/LessorReal

Date Lease Started:

CityFEI/SSN

ZIPType Property Leased: Real and PersonalPersonal

(Mth/Yr) Annual Rent:

State

Sch Number Plant/Operation NameSch LetterLessee/Lessor

To or

Street

Property Leased: From the above Lessee/LessorReal

Date Lease Started:

CityFEI/SSN

ZIPType Property Leased: Real and PersonalPersonal

(Mth/Yr) Annual Rent:

State

Plant/Operation NameLessee/Lessor

To or Real

CityFEI/SSN

ZIPReal and Personal

(Mth/Yr) Annual Rent:

Sch NumberSch Letter

Street

Property Leased: From the above Lessee/Lessor Date Lease Started:Type Property Leased: Personal

State

70582028

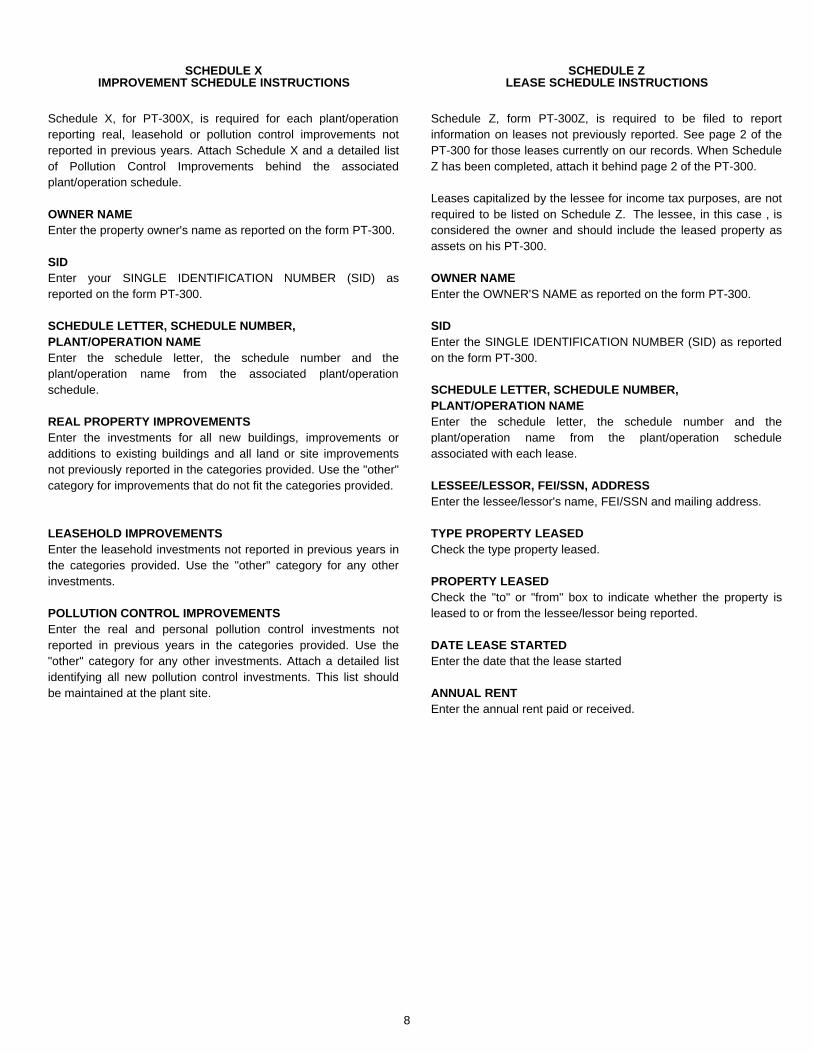

SCHEDULE ZLEASE SCHEDULE INSTRUCTIONS

Schedule Z, form PT-300Z, is required to be filed to reportinformation on leases not previously reported. See page 2 of thePT-300 for those leases currently on our records. When ScheduleZ has been completed, attach it behind page 2 of the PT-300.

Leases capitalized by the lessee for income tax purposes, are notrequired to be listed on Schedule Z. The lessee, in this case , isconsidered the owner and should include the leased property asassets on his PT-300.

OWNER NAMEEnter the OWNER'S NAME as reported on the form PT-300.

SIDEnter the SINGLE IDENTIFICATION NUMBER (SID) as reportedon the form PT-300.

SCHEDULE LETTER, SCHEDULE NUMBER,PLANT/OPERATION NAMEEnter the schedule letter, the schedule number and theplant/operation name from the plant/operation scheduleassociated with each lease.

LESSEE/LESSOR, FEI/SSN, ADDRESSEnter the lessee/lessor's name, FEI/SSN and mailing address.

TYPE PROPERTY LEASEDCheck the type property leased.

PROPERTY LEASEDCheck the "to" or "from" box to indicate whether the property isleased to or from the lessee/lessor being reported.

DATE LEASE STARTEDEnter the date that the lease started

ANNUAL RENTEnter the annual rent paid or received.

LEASEHOLD IMPROVEMENTSEnter the leasehold investments not reported in previous years inthe categories provided. Use the "other" category for any otherinvestments.

POLLUTION CONTROL IMPROVEMENTSEnter the real and personal pollution control investments notreported in previous years in the categories provided. Use the"other" category for any other investments. Attach a detailed listidentifying all new pollution control investments. This list shouldbe maintained at the plant site.

SCHEDULE XIMPROVEMENT SCHEDULE INSTRUCTIONS

8

Schedule X, for PT-300X, is required for each plant/operationreporting real, leasehold or pollution control improvements notreported in previous years. Attach Schedule X and a detailed listof Pollution Control Improvements behind the associatedplant/operation schedule.

OWNER NAMEEnter the property owner's name as reported on the form PT-300.

SIDEnter your SINGLE IDENTIFICATION NUMBER (SID) asreported on the form PT-300.

SCHEDULE LETTER, SCHEDULE NUMBER,PLANT/OPERATION NAMEEnter the schedule letter, the schedule number and theplant/operation name from the associated plant/operationschedule.

REAL PROPERTY IMPROVEMENTSEnter the investments for all new buildings, improvements oradditions to existing buildings and all land or site improvementsnot previously reported in the categories provided. Use the "other"category for improvements that do not fit the categories provided.

9

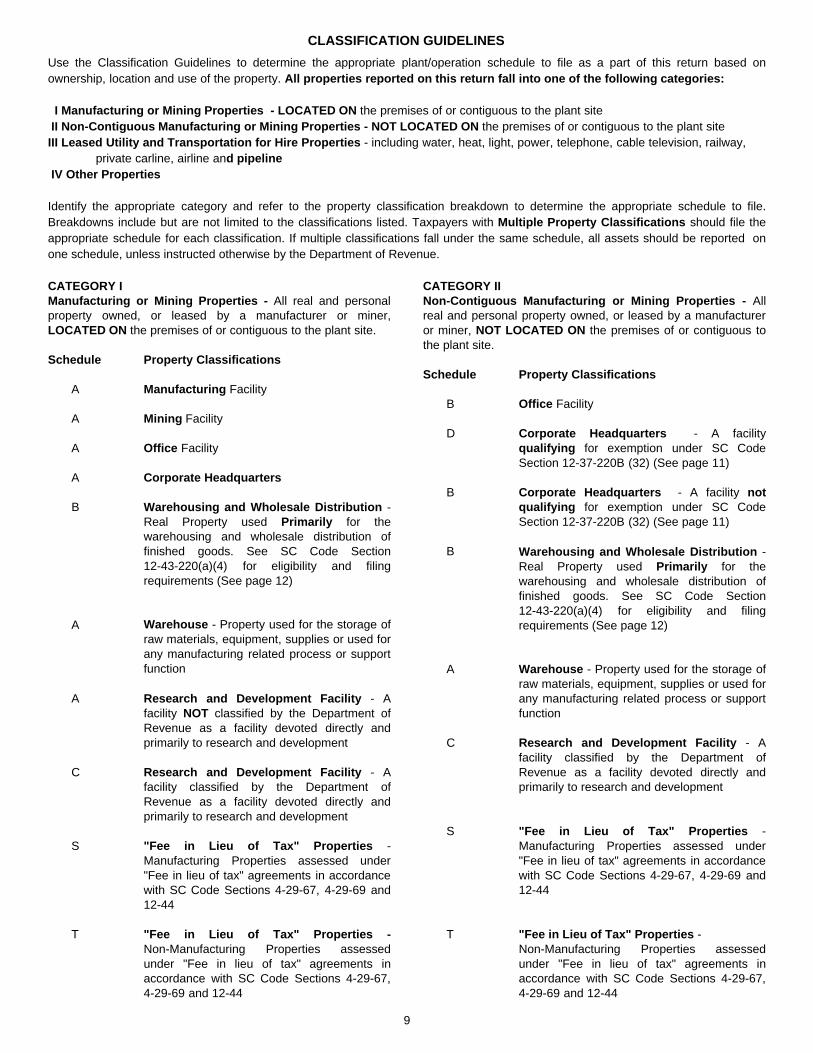

Use the Classification Guidelines to determine the appropriate plant/operation schedule to file as a part of this return based onownership, location and use of the property. All properties reported on this return fall into one of the following categories:

I Manufacturing or Mining Properties - LOCATED ON the premises of or contiguous to the plant siteII Non-Contiguous Manufacturing or Mining Properties - NOT LOCATED ON the premises of or contiguous to the plant siteIII Leased Utility and Transportation for Hire Properties - including water, heat, light, power, telephone, cable television, railway,

private carline, airline and pipeline IV Other Properties

Identify the appropriate category and refer to the property classification breakdown to determine the appropriate schedule to file.Breakdowns include but are not limited to the classifications listed. Taxpayers with Multiple Property Classifications should file theappropriate schedule for each classification. If multiple classifications fall under the same schedule, all assets should be reported onone schedule, unless instructed otherwise by the Department of Revenue.

CLASSIFICATION GUIDELINES

CATEGORY IINon-Contiguous Manufacturing or Mining Properties - Allreal and personal property owned, or leased by a manufactureror miner, NOT LOCATED ON the premises of or contiguous tothe plant site.

Schedule Property Classifications

B Office Facility

D Corporate Headquarters - A facilityqualifying for exemption under SC CodeSection 12-37-220B (32) (See page 11)

B Corporate Headquarters - A facility not

qualifying for exemption under SC CodeSection 12-37-220B (32) (See page 11)

B

A

C Research and Development Facility - A

facility classified by the Department ofRevenue as a facility devoted directly andprimarily to research and development

S "Fee in Lieu of Tax" Properties -Manufacturing Properties assessed under"Fee in lieu of tax" agreements in accordancewith SC Code Sections 4-29-67, 4-29-69 and12-44

T "Fee in Lieu of Tax" Properties -Non-Manufacturing Properties assessedunder "Fee in lieu of tax" agreements inaccordance with SC Code Sections 4-29-67,4-29-69 and 12-44

CATEGORY IManufacturing or Mining Properties - All real and personalproperty owned, or leased by a manufacturer or miner,LOCATED ON the premises of or contiguous to the plant site.

Schedule Property Classifications

A Manufacturing Facility

A Mining Facility

A Office Facility

A Corporate Headquarters B

A

A Research and Development Facility - A

facility NOT classified by the Department ofRevenue as a facility devoted directly andprimarily to research and development

C Research and Development Facility - A

facility classified by the Department ofRevenue as a facility devoted directly andprimarily to research and development

S "Fee in Lieu of Tax" Properties -

Manufacturing Properties assessed under"Fee in lieu of tax" agreements in accordancewith SC Code Sections 4-29-67, 4-29-69 and12-44

T "Fee in Lieu of Tax" Properties -

Non-Manufacturing Properties assessedunder "Fee in lieu of tax" agreements inaccordance with SC Code Sections 4-29-67,4-29-69 and 12-44

Warehouse - Property used for the storage ofraw materials, equipment, supplies or used forany manufacturing related process or supportfunction Warehouse - Property used for the storage of

raw materials, equipment, supplies or used forany manufacturing related process or supportfunction

Warehousing and Wholesale Distribution -Real Property used Primarily for thewarehousing and wholesale distribution offinished goods. See SC Code Section12-43-220(a)(4) for eligibility and filingrequirements (See page 12)

Warehousing and Wholesale Distribution -Real Property used Primarily for thewarehousing and wholesale distribution offinished goods. See SC Code Section12-43-220(a)(4) for eligibility and filingrequirements (See page 12)

10

CATEGORY IVOther Properties - All real and personal property NOT owned,used, or leased by a manufacturer, miner or utility company.

Schedule Property Classifications

D Corporate Headquarters or CorporateOffice Facility

D Distribution Facility

C Research and Development Facility - A

facility classified by the Department ofRevenue as a facility devoted directly andprimarily to research and development

T "Fee in Lieu of Tax" Properties - Non-Manu-

facturing Properties assessed under "Fee inlieu of tax" agreements in accordance with SCCode Sections 4-29-67, 4-29-69 and 12-44

CATEGORY IIILeased Utility and Transportation For Hire Properties - All realand personal property used or leased to (a) utility companiesincluding water, heat, light, power, telephone, cable televisionand sewer companies and (b) transportation for hire companiesincluding railway, private carline, airline and pipelinecompanies. This category excludes property owned by utilitycompanies.

Schedule Property Classifications

E Utilities Properties - Water, Heat, Light, Power,Telephone, Cable Television and SewerCompanies

F Transportation For Hire Properties - Railway,

Private carline, Airline and PipelineCompanies

D Corporate Headquarters of a Utility Company- A facility qualifying for exemption under SCCode Section 12-37-220B(32) (See page 11)

E Corporate Headquarters of a Utility Company

- A facility not qualifying for exemption underSC Code Section 12-37-220B(32) (See page 11)

D Corporate Headquarters of a Transportation

For Hire Company - A facility qualifying forexemption under SC Code Section12-37-220B(32) (See page 11)

F Corporate Headquarters of a TransportationFor Hire Company - A facility not qualifying forexemption under SC Code Section12-37-220B(32) (See page 11)

D Distribution Facility - A facility qualifying for

exemption under SC Code Section12-37-220B(32) (See page 11)

E Distribution Facility of a Utility Company - A

facility not qualifying for exemption under SCCode Section 12-37-220B(32) (See page 11)

F Distribution Facility of a Transportation For

Hire Company - A facility not qualifying forexemption under SC Code Section12-37-220B(32) (See page 11)

C Research and Development Facility - A facility

classified by the Department of Revenue as afacility devoted directly and primarily to researchand development

T "Fee in Lieu of Tax" - Non-ManufacturingProperties assessed under "Fee in lieu of tax"agreements in accordance with SC Code Section4-29-67, 4-29-69 and 12-44

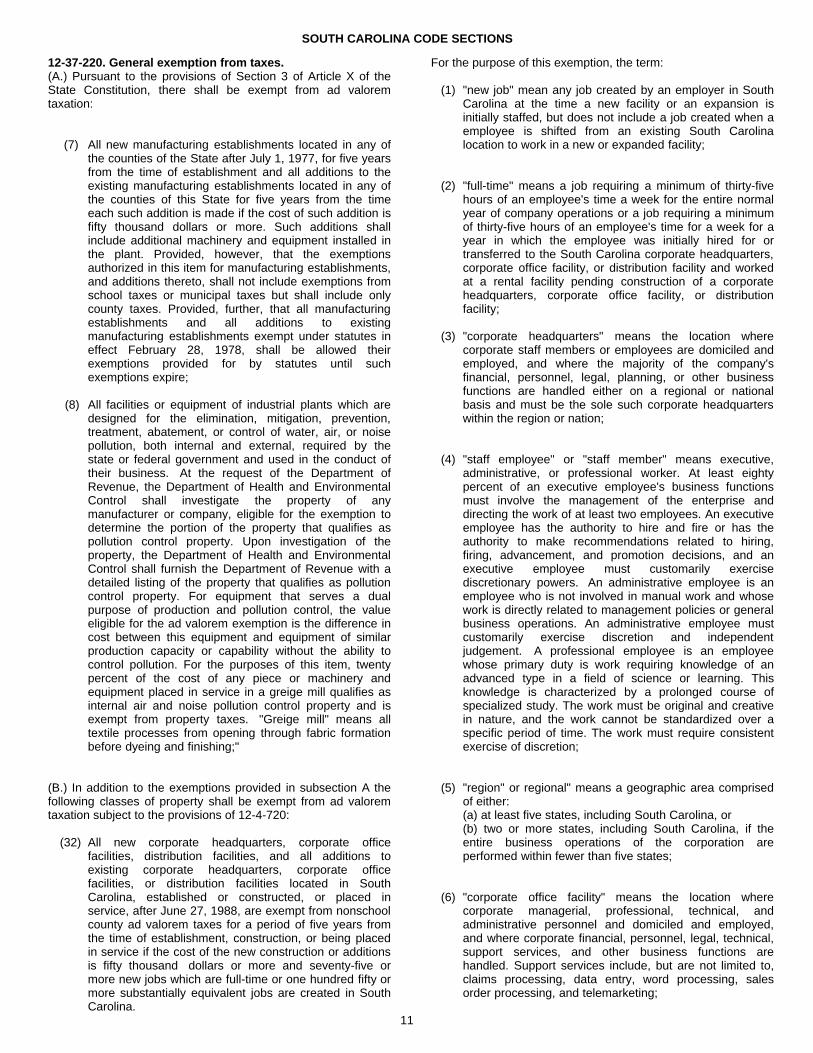

12-37-220. General exemption from taxes.(A.) Pursuant to the provisions of Section 3 of Article X of theState Constitution, there shall be exempt from ad valoremtaxation:

(7) All new manufacturing establishments located in any ofthe counties of the State after July 1, 1977, for five yearsfrom the time of establishment and all additions to theexisting manufacturing establishments located in any ofthe counties of this State for five years from the timeeach such addition is made if the cost of such addition isfifty thousand dollars or more. Such additions shallinclude additional machinery and equipment installed inthe plant. Provided, however, that the exemptionsauthorized in this item for manufacturing establishments,and additions thereto, shall not include exemptions fromschool taxes or municipal taxes but shall include onlycounty taxes. Provided, further, that all manufacturingestablishments and all additions to existingmanufacturing establishments exempt under statutes ineffect February 28, 1978, shall be allowed theirexemptions provided for by statutes until suchexemptions expire;

(8) All facilities or equipment of industrial plants which aredesigned for the elimination, mitigation, prevention,treatment, abatement, or control of water, air, or noisepollution, both internal and external, required by thestate or federal government and used in the conduct oftheir business. At the request of the Department ofRevenue, the Department of Health and EnvironmentalControl shall investigate the property of anymanufacturer or company, eligible for the exemption todetermine the portion of the property that qualifies aspollution control property. Upon investigation of theproperty, the Department of Health and EnvironmentalControl shall furnish the Department of Revenue with adetailed listing of the property that qualifies as pollutioncontrol property. For equipment that serves a dualpurpose of production and pollution control, the valueeligible for the ad valorem exemption is the difference incost between this equipment and equipment of similarproduction capacity or capability without the ability tocontrol pollution. For the purposes of this item, twentypercent of the cost of any piece or machinery andequipment placed in service in a greige mill qualifies asinternal air and noise pollution control property and isexempt from property taxes. "Greige mill" means alltextile processes from opening through fabric formationbefore dyeing and finishing;"

(B.) In addition to the exemptions provided in subsection A thefollowing classes of property shall be exempt from ad valoremtaxation subject to the provisions of 12-4-720:

(32) All new corporate headquarters, corporate officefacilities, distribution facilities, and all additions toexisting corporate headquarters, corporate officefacilities, or distribution facilities located in SouthCarolina, established or constructed, or placed inservice, after June 27, 1988, are exempt from nonschoolcounty ad valorem taxes for a period of five years fromthe time of establishment, construction, or being placedin service if the cost of the new construction or additionsis fifty thousand dollars or more and seventy-five ormore new jobs which are full-time or one hundred fifty ormore substantially equivalent jobs are created in SouthCarolina.

SOUTH CAROLINA CODE SECTIONS

11

For the purpose of this exemption, the term:

(1) "new job" mean any job created by an employer in SouthCarolina at the time a new facility or an expansion isinitially staffed, but does not include a job created when aemployee is shifted from an existing South Carolinalocation to work in a new or expanded facility;

(2) "full-time" means a job requiring a minimum of thirty-fivehours of an employee's time a week for the entire normalyear of company operations or a job requiring a minimumof thirty-five hours of an employee's time for a week for ayear in which the employee was initially hired for ortransferred to the South Carolina corporate headquarters,corporate office facility, or distribution facility and workedat a rental facility pending construction of a corporateheadquarters, corporate office facility, or distributionfacility;

(3) "corporate headquarters" means the location wherecorporate staff members or employees are domiciled andemployed, and where the majority of the company'sfinancial, personnel, legal, planning, or other businessfunctions are handled either on a regional or nationalbasis and must be the sole such corporate headquarterswithin the region or nation;

(4) "staff employee" or "staff member" means executive,administrative, or professional worker. At least eightypercent of an executive employee's business functionsmust involve the management of the enterprise anddirecting the work of at least two employees. An executiveemployee has the authority to hire and fire or has theauthority to make recommendations related to hiring,firing, advancement, and promotion decisions, and anexecutive employee must customarily exercisediscretionary powers. An administrative employee is anemployee who is not involved in manual work and whosework is directly related to management policies or generalbusiness operations. An administrative employee mustcustomarily exercise discretion and independentjudgement. A professional employee is an employeewhose primary duty is work requiring knowledge of anadvanced type in a field of science or learning. Thisknowledge is characterized by a prolonged course ofspecialized study. The work must be original and creativein nature, and the work cannot be standardized over aspecific period of time. The work must require consistentexercise of discretion;

(5) "region" or regional" means a geographic area comprisedof either:(a) at least five states, including South Carolina, or(b) two or more states, including South Carolina, if theentire business operations of the corporation areperformed within fewer than five states;

(6) "corporate office facility" means the location wherecorporate managerial, professional, technical, andadministrative personnel and domiciled and employed,and where corporate financial, personnel, legal, technical,support services, and other business functions arehandled. Support services include, but are not limited to,claims processing, data entry, word processing, salesorder processing, and telemarketing;

engaged in research and development are exempt fromad valorem taxation in the same manner and to the sameextent as the exemption allowed pursuant to item (7) ofsubsection A of Section 12-37-220 of the 1976 Code.These additions include machinery and equipmentinstalled in an existing manufacturing or research anddevelopment facility. For purposes of this section,facilities of enterprises engaged in research anddevelopment activities are facilities devoted directly andexclusively to research and development in theexperimental or laboratory sense for new products, newuses for existing products, or for improving existingproducts. To be eligible for the exemption allowed by thissection, the facility or its addition must be devotedprimarily to research and development as defined in thissection. The exemption does not include facilities used inconnection with efficiency surveys, management studies,consumer surveys, economic surveys, advertising,promotion, or research in connection with literary,historical, or similar projects.

(C.) Upon approval by the governing body of the county, thefive-year partial exemption allowed pursuant to subsections(A)(7), (B)(32) and (B)(34) is extended to an unrelated purchaserwho acquires the facilities in an arms-length transaction andwho preserves the existing facilities and existing number of jobs.The partial exemption applies for the purchaser for five years ifthe purchaser otherwise meets the exemption requirements.

12

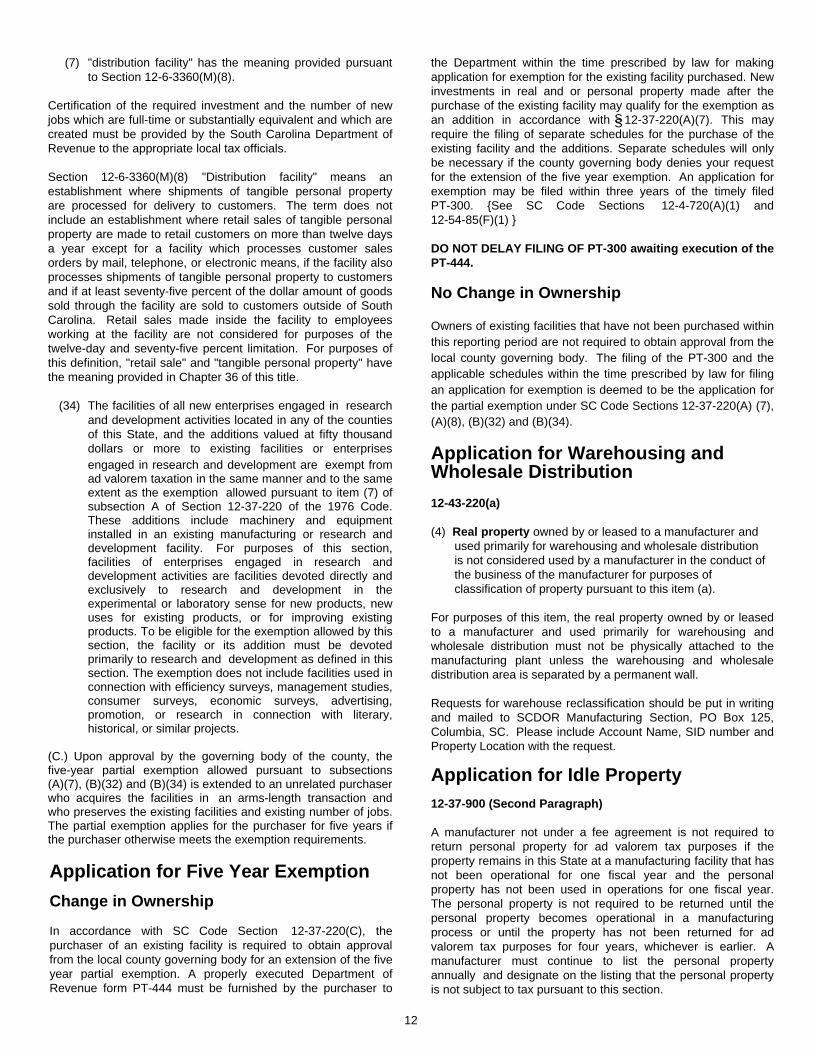

(7) "distribution facility" has the meaning provided pursuantto Section 12-6-3360(M)(8).

Certification of the required investment and the number of newjobs which are full-time or substantially equivalent and which arecreated must be provided by the South Carolina Department ofRevenue to the appropriate local tax officials.

Section 12-6-3360(M)(8) "Distribution facility" means anestablishment where shipments of tangible personal propertyare processed for delivery to customers. The term does notinclude an establishment where retail sales of tangible personalproperty are made to retail customers on more than twelve daysa year except for a facility which processes customer salesorders by mail, telephone, or electronic means, if the facility alsoprocesses shipments of tangible personal property to customersand if at least seventy-five percent of the dollar amount of goodssold through the facility are sold to customers outside of SouthCarolina. Retail sales made inside the facility to employeesworking at the facility are not considered for purposes of thetwelve-day and seventy-five percent limitation. For purposes ofthis definition, "retail sale" and "tangible personal property" havethe meaning provided in Chapter 36 of this title.

(34) The facilities of all new enterprises engaged in researchand development activities located in any of the countiesof this State, and the additions valued at fifty thousanddollars or more to existing facilities or enterprises

Application for Five Year Exemption

12-43-220(a)

(4) Real property owned by or leased to a manufacturer and used primarily for warehousing and wholesale distribution is not considered used by a manufacturer in the conduct of the business of the manufacturer for purposes of classification of property pursuant to this item (a).

For purposes of this item, the real property owned by or leasedto a manufacturer and used primarily for warehousing andwholesale distribution must not be physically attached to themanufacturing plant unless the warehousing and wholesaledistribution area is separated by a permanent wall.

Requests for warehouse reclassification should be put in writingand mailed to SCDOR Manufacturing Section, PO Box 125,Columbia, SC. Please include Account Name, SID number andProperty Location with the request.

No Change in Ownership

Owners of existing facilities that have not been purchased withinthis reporting period are not required to obtain approval from thelocal county governing body. The filing of the PT-300 and theapplicable schedules within the time prescribed by law for filingan application for exemption is deemed to be the application forthe partial exemption under SC Code Sections 12-37-220(A) (7),(A)(8), (B)(32) and (B)(34).

Change in Ownership

In accordance with SC Code Section 12-37-220(C), thepurchaser of an existing facility is required to obtain approvalfrom the local county governing body for an extension of the fiveyear partial exemption. A properly executed Department ofRevenue form PT-444 must be furnished by the purchaser to

SS

Application for Warehousing andWholesale Distribution

Application for Idle Property12-37-900 (Second Paragraph)

A manufacturer not under a fee agreement is not required toreturn personal property for ad valorem tax purposes if theproperty remains in this State at a manufacturing facility that hasnot been operational for one fiscal year and the personalproperty has not been used in operations for one fiscal year.The personal property is not required to be returned until thepersonal property becomes operational in a manufacturingprocess or until the property has not been returned for advalorem tax purposes for four years, whichever is earlier. Amanufacturer must continue to list the personal propertyannually and designate on the listing that the personal propertyis not subject to tax pursuant to this section.

the Department within the time prescribed by law for makingapplication for exemption for the existing facility purchased. Newinvestments in real and or personal property made after thepurchase of the existing facility may qualify for the exemption asan addition in accordance with 12-37-220(A)(7). This mayrequire the filing of separate schedules for the purchase of theexisting facility and the additions. Separate schedules will onlybe necessary if the county governing body denies your requestfor the extension of the five year exemption. An application forexemption may be filed within three years of the timely filedPT-300. {See SC Code Sections 12-4-720(A)(1) and12-54-85(F)(1) }

DO NOT DELAY FILING OF PT-300 awaiting execution of thePT-444.

Cold Storage Refrigeration Equipment - PersonalControl Booth - PersonalConveyor or Housing, Structure or Tunnels - RealConveyor Unit Including Belt and Drives - PersonalCoolers - portable walk-in coolers - PersonalCooling Towers - Primary use of manufacture - PersonalCooling Towers - Primary use for building - RealCrane - Moving crane - PersonalCrane Runways Including Supporting Columns or

Structure - Inside or outside of building - RealCrane Runways - Bolted to or hung on tresses - PersonalDock Levelers - PersonalDrying Rooms Structure - RealDrying Rooms Heating Systems - PersonalDust Catchers - PersonalFarm Equipment - PersonalFire Alarm System - PersonalFire Walls - Masonry - RealFoundations for Machinery and Equipment - PersonalFurniture and Fixtures of Commercial Establishments