2016 RACV Annual Report Financial · Changes in the fair value of available for sale financial...

49

FINANCIAL STATEMENTS 2016

-

Upload

nguyenthuy -

Category

Documents

-

view

212 -

download

0

Transcript of 2016 RACV Annual Report Financial · Changes in the fair value of available for sale financial...

FINANCIAL STATEMENTS2016

RACV 2016 ANNUAL REPORT | 19

CONTENTS OF FINANCIAL STATEMENTSCONSOLIDATED INCOME STATEMENT 20CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME 21CONSOLIDATED BALANCE SHEET 22CONSOLIDATED STATEMENT OF CASH FLOWS 23CONSOLIDATED STATEMENT OF CHANGES IN EQUITY 24

NOTES TO THE FINANCIAL STATEMENTSWORKING CAPITAL MANAGEMENT 251. CASH AND CASH EQUIVALENTS 252. RECEIVABLES 263. TRADE AND OTHER PAYABLES 274. INVENTORIES 27

OTHER ASSETS AND LIABILITIES 275. PROPERTY, PLANT AND EQUIPMENT 276. INTANGIBLE ASSETS 297. INVESTMENT PROPERTIES 308. PROVISIONS 319. UNEARNED INCOME 31

FINANCIAL INSTRUMENTS AND RISK MANAGEMENT 3210. AVAILABLE FOR SALE FINANCIAL ASSETS 3211. INTEREST BEARING LIABILITIES 3212. OTHER FINANCIAL LIABILITIES 3313. FINANCIAL RISK MANAGEMENT 3414. FAIR VALUE MEASUREMENT 38

TAXATION 4115. INCOME TAX EXPENSE 4116. DEFERRED TAX ASSETS 42

REMUNERATION AND BENEFITS 4317. KEY MANAGEMENT PERSONNEL 4318. SUPERANNUATION BENEFITS 43

GROUP STRUCTURE 4519. SUBSIDIARIES 4520. BUSINESS COMBINATIONS 4621. INVESTMENTS ACCOUNTED FOR USING

THE EQUITY METHOD 4722. PARENT ENTITY FINANCIAL INFORMATION 49

OTHER INFORMATION 5023. MEMBERS’ EQUITY 5024. RELATED PARTY TRANSACTIONS 5125. AUDITOR’S REMUNERATION 5226. DEED OF CROSS GUARANTEE 5227. SIGNIFICANT ACCOUNTING POLICIES 54

UNRECOGNISED ITEMS AND UNCERTAIN EVENTS 6228. COMMITMENTS AND CONTINGENCIES 6229. SUBSEQUENT EVENTS 62

DIRECTORS’ DECLARATION 63

AUDITOR’S REPORT 64

CORPORATE DIRECTORY 65

20 | RACV 2016 ANNUAL REPORT

CONSOLIDATED INCOME STATEMENTFor the year ended 30 June 2016 Royal Automobile Club of Victoria (RACV) Limited

Notes2016

$m2015

$m

RevenueSubscription and entrance fee income 189.0 180.5Commission income 102.8 98.3Club and resorts trading income 140.1 129.7Sale of goods and other trading income 82.6 71.9Interest on loans and leases 25.8 26.4Trust distributions 28.5 39.4Rental income 9.3 9.4Other income 2.7 –Interest income 2.0 3.7Fair value adjustment to assets 1.5 0.6Profit on sale of plant and equipment 0.5 0.1Total revenue 584.8 560.0

ExpensesEmployee benefits expense (233.1) (219.6)Depreciation and amortisation expense (40.6) (41.9)Impairment of property, plant and equipment 5 (39.0) –Reversal of previously impaired property, plant and equipment 5 18.8 6.5Provision for property development 8 (15.5) –Impairment of intangible assets 6 (12.1) (1.7)Doubtful debts expense (0.9) (1.6)Computer and telecommunications expense (47.7) (41.4)Advertising expense (45.3) (42.0)External fees expense (55.9) (50.9)Property expense (29.5) (26.9)Consumables expense (64.9) (58.4)Interest expense and other finance costs (20.3) (21.1)Other expenses (21.5) (19.0)Total expenses (607.5) (518.0)

Share of net profit of equity accounted investments 21(b) 83.1 104.3

Profit before net (loss)/gain on available for sale financial assets and income tax 60.4 146.3

Net (loss)/gain on available for sale financial assetsNet (loss)/gain on available for sale financial assets sold (6.1) 2.3Impairment of available for sale financial assets (0.9) (5.3)

Profit before income tax 53.4 143.3

Income tax expense 15 (6.7) (16.8)

Profit after income tax 46.7 126.5

Profit after income tax is attributable to:Members of RACV Group 45.8 126.1Non-controlling interests 0.9 0.4

46.7 126.5

The above Consolidated Income Statement should be read in conjunction with the accompanying notes.

RACV 2016 ANNUAL REPORT | 21

Notes2016

$m2015

$m

Profit after income tax 46.7 126.5

Other comprehensive incomeItems that may be reclassified to profit or loss:

Changes in the fair value of available for sale financial assets, net of tax 23(a) (10.8) (4.2)

Items that will not be reclassified to profit or loss:(Loss)/gain on revaluation of land and buildings, net of tax 23(a) (3.0) 1.8Superannuation plan remeasurements, net of tax 23(c) (8.5) 3.6Change in associate retained earnings, net of tax 23(c) (0.2) 1.0

Other comprehensive (loss)/income for the year, net of tax (22.5) 2.2

Total comprehensive income for the year 24.2 128.7

Total comprehensive income for the year is attributable to:Members of RACV Group 23.2 128.3Non-controlling interests 1.0 0.4

24.2 128.7

The above Consolidated Statement of Comprehensive Income should be read in conjunction with the accompanying notes.

CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOMEFor the year ended 30 June 2016

Royal Automobile Club of Victoria (RACV) Limited

22 | RACV 2016 ANNUAL REPORT

Notes2016

$m2015

$m

ASSETS

Current assetsCash and cash equivalents 1 73.0 100.3Receivables 2 130.6 120.3Available for sale financial assets 10 20.5 49.0Inventories 4 3.1 2.9Prepayments and accrued income 60.9 16.0Total current assets 288.1 288.5

Non-current assetsReceivables 2 224.6 198.5Available for sale financial assets 10 469.5 442.9Investments accounted for using the equity method 21 243.9 217.3Property, plant and equipment 5 617.1 573.7Intangible assets 6 117.3 131.3Investment properties 7 42.1 47.6Deferred tax assets 16 93.4 87.3Total non-current assets 1,807.9 1,698.6Total assets 2,096.0 1,987.1

LIABILITIES

Current liabilitiesTrade and other payables 3 81.8 71.8Interest bearing liabilities 11 218.8 129.7Current tax payable 1.8 1.3Provisions 8 62.1 41.7Unearned income 9 125.4 115.4Total current liabilities 489.9 359.9

Non-current liabilitiesInterest bearing liabilities 11 57.0 114.0Other financial liabilities 12 – 0.3Superannuation benefits 18 22.2 9.3Provisions 8 7.7 7.4Total non-current liabilities 86.9 131.0Total liabilities 576.8 490.9Net assets 1,519.2 1,496.2

EQUITY

Member reserves 23(a) 47.9 63.3Retained earnings 23(c) 1,466.2 1,429.1

Equity attributable to members of RACV Group 1,514.1 1,492.4

Non-controlling interests 5.1 3.8

Total equity 1,519.2 1,496.2

The above Consolidated Balance Sheet should be read in conjunction with the accompanying notes.

CONSOLIDATED BALANCE SHEETAs at 30 June 2016 Royal Automobile Club of Victoria (RACV) Limited

RACV 2016 ANNUAL REPORT | 23

Notes2016

$m2015

$m

Cash flows from operating activities

Subscription and entrance fee income received 217.5 208.5Club and resorts trading income received 155.2 144.4Commission income received 112.0 108.9Sale of goods and other trading income received 93.8 89.4Payments to suppliers and employees (552.8) (511.1)Net cash outflow from loans and leases (34.4) (16.0)Dividends received from equity accounted investments 57.7 132.2Interest received 29.0 30.9Interest paid (9.6) (10.6)Income tax paid (1.7) –Net cash inflow from operating activities 1 66.7 176.6

Cash flows from investing activities

Trust distributions received 24.0 36.4Proceeds from sale of property, plant and equipment 0.5 0.4Proceeds from sale/maturity of available for sale financial assets 40.8 26.5Proceeds from disposal of controlled entity – 5.0Purchase of available for sale financial assets (91.8) (279.3)Purchase of property, plant and equipment (68.0) (35.1)Purchase of intangibles (13.3) (9.5)Payment for business acquisitions, net of cash acquired (15.5) –Investment in equity accounted investments (2.7) –Net cash outflow from investing activities (126.0) (255.6)

Cash flows from financing activities

Proceeds from/(repayment of) issue of borrowings/secured notes 5.0 2.7Proceeds from subscription agreement 26.7 19.7Repayment of loans – (1.9)Transactions with non-controlling interests 0.3 0.3Net cash inflow from financing activities 32.0 20.8

Net decrease in cash and cash equivalents (27.3) (58.2)

Cash and cash equivalents at beginning of financial year 100.3 158.5Cash and cash equivalents at end of financial year 1 73.0 100.3

The above Consolidated Statement of Cash Flows should be read in conjunction with the accompanying notes.

CONSOLIDATED STATEMENT OF CASH FLOWSFor the year ended 30 June 2016

Royal Automobile Club of Victoria (RACV) Limited

24 | RACV 2016 ANNUAL REPORT

Attributable to members of RACV GroupNon-

controlling interests

$m

Total equity

$mNotes

Member reserves

$m

Retained earnings

$m

Total members’

equity $m

Balance at 1 July 2014 60.4 1,298.4 1,358.8 3.4 1,362.2

Profit after income tax – 126.1 126.1 0.4 126.5Other comprehensive income (2.4) 4.6 2.2 – 2.2Total comprehensive income for the year (2.4) 130.7 128.3 0.4 128.7

Contribution of equity – non-controlling interests – – – 0.3 0.3Transactions with non-controlling interests 5.3 – 5.3 (0.3) 5.0Balance at 30 June 2015 23 63.3 1,429.1 1,492.4 3.8 1,496.2

Profit after income tax – 45.8 45.8 0.9 46.7Other comprehensive (loss)/income (13.9) (8.7) (22.6) 0.1 (22.5)Total comprehensive income for the year (13.9) 37.1 23.2 1.0 24.2

Contribution of equity – non-controlling interests – – – 0.3 0.3Transactions with non-controlling interests (1.5) – (1.5) – (1.5)Balance at 30 June 2016 23 47.9 1,466.2 1,514.1 5.1 1,519.2

The above Consolidated Statement of Changes in Equity should be read in conjunction with the accompanying notes.

CONSOLIDATED STATEMENT OF CHANGES IN EQUITYAs at 30 June 2016 Royal Automobile Club of Victoria (RACV) Limited

RACV 2016 ANNUAL REPORT | 25

WORKING CAPITAL MANAGEMENT

1. CASH AND CASH EQUIVALENTS

2016 $m

2015 $m

Cash at bank and on hand 73.0 100.3

Cash at bank earns interest at floating rates based on daily bank deposit rates. The Group has a combined net bank overdraft facility of $5.6 million (2015: $5.6 million). After adjusting for cash balances and unpresented cheques the Group net bank overdraft amounted to $nil (2015: $nil).

Reconciliation of net cash inflow provided by operating activities to net profit after income tax

Net profit after income tax 46.7 126.5

Add/(less) items classified as investing/financing activities:(Increase)/decrease in equity accounted investments (25.4) 26.6Net profit on sale of plant and equipment (0.5) (0.1)Net profit on realisation of investments – (2.3)Trust distributions received (24.0) (36.4)Discount on business acquisition (2.7) –

Add/(less) non-cash items:Depreciation and amortisation 40.6 41.9Allowance for doubtful debts 0.9 1.6Amortisation of loan and lease receivables 1.2 0.8Fair value adjustments to liabilities – 0.2Superannuation – defined benefit expense 0.5 1.7Fair value adjustments to assets (1.5) (0.6)Impairment/(reversal of impairment) of assets 33.2 0.5Provision for property development 15.5 –

Changes in operating assets and liabilities:Increase in receivables (33.3) (16.2)(Increase)/decrease in inventories (0.2) 0.1Increase in prepayments and accrued income (8.5) (2.2)Increase in payables 4.5 3.8Increase in unearned income 10.1 10.7Increase in provisions 4.9 3.4Decrease in net deferred tax balances 4.7 16.6

Net cash provided by operating activities 66.7 176.6

NOTES TO THE FINANCIAL STATEMENTS30 June 2016

Royal Automobile Club of Victoria (RACV) Limited

26 | RACV 2016 ANNUAL REPORT

NOTES TO THE FINANCIAL STATEMENTS30 June 2016 Royal Automobile Club of Victoria (RACV) Limited

2. RECEIVABLES

2016 $m

2015 $m

CurrentLoan receivables 70.2 66.1Lease receivables 37.5 35.3Trade receivables 21.0 17.5

128.7 118.9Provision for doubtful debts (0.5) (0.8)

128.2 118.1Other receivables 2.4 2.2

130.6 120.3

Non-currentLoan receivables 156.7 142.6Lease receivables 68.7 56.5

225.4 199.1Provision for doubtful debts (0.8) (0.6)

224.6 198.5

Movement in provision for doubtful debts

Loan and lease receivables

$m

Trade receivables

$mTotal

$m

2016Opening balance 1.0 0.4 1.4Provision raised during the year 0.8 0.1 0.9Bad debts written off during the year (0.6) (0.4) (1.0)Closing balance 1.2 0.1 1.3

2015Opening balance 0.9 0.4 1.3Provision raised during the year 0.7 0.2 0.9Bad debts written off during the year (0.6) (0.2) (0.8)Closing balance 1.0 0.4 1.4

Refer note 11(a) for information on non-current assets pledged as security by R.A.C.V. Finance Limited.

(a) Accounting estimates, assumptions and judgements: Provision for impairment of loan and lease receivables

Loan and lease receivables are carried at amortised cost less a provision for impairment. The provision for impairment is established when there is objective evidence that the Group will not be able to collect all amounts due according to the original terms of the receivable. In calculating the provision for impairment, the Group has assumed that the historical loss experience, including loss rates and loss events such as default payments, arrears and dishonour payments are applicable to the current portfolio. To mitigate the estimation uncertainty, the historical loss rates are updated and the loss events are reviewed at each reporting period. In addition, all loans and leases are subject to regular management review.

RACV 2016 ANNUAL REPORT | 27

3. TRADE AND OTHER PAYABLES

2016 $m

2015 $m

CurrentTrade payables 75.2 60.1Other payables 6.6 11.7

81.8 71.8

4. INVENTORIES

CurrentFinished goods and hospitality supplies 3.1 2.9

Inventories recognised as an expense totalled $41.1 million (2015: $28.3 million) for the Group.

OTHER ASSETS AND LIABILITIES

5. PROPERTY, PLANT AND EQUIPMENT

Freehold land and

improvements $m

Buildings $m

Plant and equipment

$m

In course of construction

$mTotal

$m

2016

Year ended 30 June 2016Opening net book amount 135.3 386.7 41.0 10.7 573.7Additions 4.0 15.3 6.3 60.1 85.7Disposals – – (0.2) – (0.2)Transfers 19.9 17.1 7.0 (38.3) 5.7Revaluation (decrement)/increment (5.7) 1.6 – – (4.1)Impairment (4.9) (18.6) – (15.5) (39.0)Reversal of impairment (1.1) 19.9 – – 18.8Depreciation (1.2) (13.1) (9.2) – (23.5)Closing net book amount 146.3 408.9 44.9 17.0 617.1

At 30 June 2016Cost or fair value 149.0 440.5 112.3 17.0 718.8Accumulated depreciation and impairment (2.7) (31.6) (67.4) – (101.7)Net book amount 146.3 408.9 44.9 17.0 617.1

NOTES TO THE FINANCIAL STATEMENTS30 June 2016 Royal Automobile Club of Victoria (RACV) Limited

28 | RACV 2016 ANNUAL REPORT

5. PROPERTY, PLANT AND EQUIPMENT (CONTINUED)Freehold land and

improvements $m

Buildings $m

Plant and equipment

$m

In course of construction

$mTotal

$m

2015

Year ended 30 June 2015Opening net book amount 119.2 368.4 52.5 14.5 554.6Additions 4.4 1.3 3.7 25.8 35.2Disposals – – (0.4) – (0.4)Transfers 11.5 20.7 (3.0) (29.6) (0.4)Revaluation increment 1.1 2.2 – – 3.3Reversal of impairment 0.1 6.4 – – 6.5Depreciation (1.0) (12.3) (11.8) – (25.1)Closing net book amount 135.3 386.7 41.0 10.7 573.7

At 30 June 2015Cost or fair value 137.4 412.0 103.6 10.7 663.7Accumulated depreciation and impairment (2.1) (25.3) (62.6) – (90.0)Net book amount 135.3 386.7 41.0 10.7 573.7

(a) Valuations of land and buildingsThe basis of the valuation of land and buildings is fair value, being the price for which the properties could be sold in an orderly transaction between market participants at the measurement date. Information about the valuation of land and buildings is provided in note 14(b).

(b) In course of construction assetsThe carrying amount of in course of construction assets includes capital costs associated with the Cape Schanck Resort redevelopment and improvements to amenities at the Cobram and Hobart resort properties.

The previous year’s carrying amount of in course of construction assets includes capital costs associated with the Cape Schanck Resort redevelopment and golf course development at Royal Pines Resort.

(c) Carrying amounts that would have been recognised if land and buildings were stated at costIf freehold land and buildings were stated on the historical cost basis, the amounts would be as follows:

2016 $m

2015 $m

Freehold land and improvementsCost 147.2 123.1Accumulated depreciation (7.8) (6.2)Net book amount 139.4 116.9

BuildingsCost 519.1 487.5Accumulated depreciation (116.4) (102.4)Net book amount 402.7 385.1

(d) Accounting estimates, assumptions and judgements: Property developmentsThe Group assesses annually whether property development costs have suffered any impairment in accordance with the accounting policy stated in note 27(f). The completed works to date are impaired to the extent their carrying amount exceeds their recoverable amount. A property development provision is also recognised for the unavoidable future contractual obligations in excess of recoverable amount on completion.

RACV 2016 ANNUAL REPORT | 29

6. INTANGIBLE ASSETS

Goodwill $m

Customer contracts

$mSoftware*

$m

Software in development

$mTotal

$m

2016

Year ended 30 June 2016Opening net book amount 11.4 8.8 109.1 2.0 131.3Additions 0.2 – 4.8 8.9 13.9Transfers – – 4.4 (3.2) 1.2Impairment – (1.0) (11.1) – (12.1)Amortisation – – (17.0) – (17.0)Closing net book amount 11.6 7.8 90.2 7.7 117.3

At 30 June 2016Cost 11.6 13.9 186.6 7.7 219.8Accumulated amortisation and impairment – (6.1) (96.4) – (102.5)Net book amount 11.6 7.8 90.2 7.7 117.3

2015

Year ended 30 June 2015Opening net book amount 11.4 10.4 111.7 7.4 140.9Additions – – 5.0 3.5 8.5Transfers – – 9.3 (8.9) 0.4Impairment – (1.6) (0.1) – (1.7)Amortisation – – (16.8) – (16.8)Closing net book amount 11.4 8.8 109.1 2.0 131.3

At 30 June 2015Cost 11.4 13.9 177.4 2.0 204.7Accumulated amortisation and impairment – (5.1) (68.3) – (73.4)Net book amount 11.4 8.8 109.1 2.0 131.3

* Software includes $68.7 million (2015: $84.5 million) relating to an internally developed web-based business system with a remaining weighted average amortisation period of 9.4 years (2015: 10.2 years).

NOTES TO THE FINANCIAL STATEMENTS30 June 2016 Royal Automobile Club of Victoria (RACV) Limited

30 | RACV 2016 ANNUAL REPORT

6. INTANGIBLE ASSETS (CONTINUED)

(a) Impairment tests for goodwill, customer contracts and software in development A cash-generating unit (CGU) to which goodwill, customer contracts or software in development is allocated is tested for impairment annually. Goodwill, customer contracts and software in development are allocated to the Group’s CGUs identified according to business units. Software in development is attributed to the Information, Communications and Technology, Membership and Motoring & Mobility business units (2015: Human Resources, RACV Salary Solutions, Membership and Motoring & Mobility business units). Goodwill and customer contracts are attributed to the RACV Salary Solutions business unit. As at 30 June 2016, the recoverable amount of the RACV Salary Solutions business unit was $30.6 million (2015: $21.4 million).

The recoverable amount of each CGU is determined based on value in use calculations and in some circumstances, independent assessments performed by external valuers. The value in use calculations use cash flow projections based on financial forecasts prepared by management covering a 5 to 11 year period (2015: 5 to 11 year period).

The key assumptions used in these calculations are as follows:

2016 %

2015 %

Discount rate 7.8–12.5 8.4–13EBITA margin 7–18 15–22Terminal growth rate 2.5 2.5

The calculations also take into account market conditions and investment market returns. These assumptions have been determined by reference to historical company experience, industry benchmarks sourced externally and publicly available data. Whenever the CGU is impaired, the carrying amounts of goodwill, customer contracts and software in development are written down to their recoverable amount.

(b) Accounting estimates, assumptions and judgements: Estimated impairment of goodwill, customer contracts and software in development

The Group tests whether goodwill, customer contracts and software development costs not yet ready for use have suffered any impairment in accordance with the accounting policy stated in note 27(m). The recoverable amounts of CGU’s have been determined based on value in use calculations which incorporate the use of assumptions and estimates.

7. INVESTMENT PROPERTIES

2016

$m2015

$m

Opening balance 47.6 47.6Additions – 0.1Transfers (6.9) –Net gain/(loss) from fair value adjustments 1.4 (0.1)Net book amount 42.1 47.6

(a) Amounts recognised in Income Statement for investment propertiesRental income 4.1 4.2Direct operating expenses from property that generated rental income (1.1) (1.1)Fair value gain/(loss) recognised in other income 1.4 (0.1)

4.4 3.0

(b) Valuation basisThe basis of the valuation of investment properties is fair value, being the price for which the properties could be sold in an orderly transaction between market participants at the measurement date. Information about the valuation of investment properties is provided in note 14(b).

RACV 2016 ANNUAL REPORT | 31

8. PROVISIONS

Employee benefits

$m

Property development

$mOther

$mTotal

$m

2016Opening balance 41.1 – 8.0 49.1Additional provisions recognised 21.7 15.5 3.0 40.2Payments/provision of economic benefits (18.3) – (1.2) (19.5)Closing balance 44.5 15.5 9.8 69.8

Current 2016 37.8 15.5 8.8 62.1Non-current 2016 6.7 – 1.0 7.7

44.5 15.5 9.8 69.8

Current 2015 34.9 – 6.8 41.7Non-current 2015 6.2 – 1.2 7.4

41.1 – 8.0 49.1

Property developmentProvision is made for the estimated loss on the development of the RACV Cape Schanck Resort contracts whereby the unavoidable costs of meeting the future obligations under these contracts exceed the economic benefit expected to be received. The anticipated future economic benefits to be received are based on an assessment of recoverable amount of the development on completion.

9. UNEARNED INCOME

2016 $m

2015 $m

CurrentSubscriptions in advance 7.5 7.2Unearned income 113.2 103.2Other 4.7 5.0

125.4 115.4

NOTES TO THE FINANCIAL STATEMENTS30 June 2016 Royal Automobile Club of Victoria (RACV) Limited

32 | RACV 2016 ANNUAL REPORT

FINANCIAL INSTRUMENTS AND RISK MANAGEMENT

10. AVAILABLE FOR SALE FINANCIAL ASSETS

2016 $m

2015 $m

CurrentUnit trusts – unlisted 20.5 49.0

Non-currentUnit trusts – unlisted 469.5 442.9

(a) Accounting estimates, assumptions and judgements: Estimate of impairment revaluation charge on available for sale financial assets

The Group assesses annually whether there is objective evidence, as a result of past events, that an available for sale financial asset or group of available for sale financial assets is impaired. An equity investment is impaired if it has been below its cost for a minimum of 12 months or if the market value of the investment is more than 30% below its accounting cost.

11. INTEREST BEARING LIABILITIES

2016 $m

2015 $m

CurrentSecured notes 127.9 129.7Subscription agreement 90.9 –

218.8 129.7

Non-currentSecured notes 57.0 49.8Subscription agreement – 64.2

57.0 114.0

(a) Secured notesSecured notes are issued at a fixed rate for periods between six months and four years. Secured notes are initially recorded at their fair value and subsequently measured at amortised cost. Interest expense is recognised using the effective interest method and is payable on a quarterly, six monthly or annual basis depending upon the notes selected.

Secured notes are secured by a first floating charge over the assets of R.A.C.V. Finance Limited under a Debenture Stock and Unsecured Notes Supplemental and Consolidated Trust Deed (“Trust Deed”) dated 4 May 2000. On 9 June 2015, the Trust Company (Australia) Limited replaced the original Trustee under and for the purpose of the Trust Deed. All other terms of the Trust Deed remain unchanged.

R.A.C.V. Finance Limited assets pledged as security are as follows:

2016 $m

2015 $m

Floating chargeCash assets 2.3 3.5Receivables – Current 108.2 101.2Receivables – Non-current 224.6 198.5Intangibles 0.2 0.3Other assets 0.2 0.1Total R.A.C.V. Finance Limited assets pledged as security 335.5 303.6

RACV 2016 ANNUAL REPORT | 33

Under the terms of the Trust Deed, R.A.C.V. Finance Limited may in certain circumstances give charges over its assets wherever situated, ranking equally with or in priority to the security constituted by the charges under the Trust Deed, subject to borrowing limits which require:

(i) secured liabilities to not exceed 85% of the tangible assets of R.A.C.V. Finance Limited and any guarantor bodies;

(ii) prior secured liabilities to not exceed 10% of the tangible assets of R.A.C.V. Finance Limited and any guarantor bodies; and

(iii) external liabilities to not exceed 93.75% of the tangible assets of R.A.C.V. Finance Limited and any guarantor bodies.

R.A.C.V. Finance Limited has a commitment from RACV Limited for an increase in its capital base by $10 million should the secured liabilities to tangible assets ratio reach 83.5%.

(b) Subscription agreementThe subscription agreement is a secured borrowing facility carried at amortised cost and bears interest at market rates.

On 31 March 2014, an existing facility with the National Australia Bank (NAB) was renewed with a Second Amendment Deed to increase the funding limit to $100 million with a number of changes made to terms and conditions. The facility can be drawn for periods up to six calendar months and expires on 31 March 2017.

As at 30 June 2016, $90.9 million of the $100 million facility was drawn (2015: $64.2 million of the $100 million facility was drawn). This facility has been secured by secured notes. The individual drawdown amounts bear fixed interest rates with rollover dates and interest rates as shown below:

Principal amount $m

Interest rate (payable at rollover)

% p.a. Rollover date

June 2016 2.0 2.95 8 July 201666.4 2.94 22 July 20161.0 2.96 26 July 2016

14.0 2.96 26 July 20161.5 2.96 26 July 20164.0 2.91 8 September 20162.0 2.92 8 September 2016

June 2015 1.4 3.26 10 July 201558.3 3.05 17 July 20153.0 3.04 29 July 20151.5 3.11 25 August 2015

Under the NAB subscription agreement, R.A.C.V. Finance Limited has a financial undertaking to ensure that its gearing ratio is less than or equal to 0.85 times. This ratio is calculated as interest bearing liabilities divided by interest bearing liabilities plus equity. The gearing ratio as at 30 June 2016 was 0.84 times (2015: 0.83 times). The Company was in compliance with its capital requirements throughout the whole financial year.

12. OTHER FINANCIAL LIABILITIES

2016 $m

2015 $m

Non-currentLoans from external entities – 0.3

NOTES TO THE FINANCIAL STATEMENTS30 June 2016 Royal Automobile Club of Victoria (RACV) Limited

34 | RACV 2016 ANNUAL REPORT

13. FINANCIAL RISK MANAGEMENT

The Group holds the following financial instruments:

Notes2016

$m2015

$m

Financial assetsCash and cash equivalents 1 73.0 100.3Trade and other receivables 2 23.3 19.3Loan receivables 2 225.8 207.7Lease receivables 2 106.1 91.8Available for sale financial assets 10 490.0 491.9

918.2 911.0

Financial liabilitiesTrade and other payables 3 81.8 71.8Secured notes 11 184.9 179.5Subscription agreement 11 90.9 64.2Loans from external entities 12 – 0.3

357.6 315.8

The Group’s activities expose it to a variety of financial risks such as credit risk, liquidity risk and market risk. The Group’s overall risk management program seeks to minimise potential adverse effects on the financial performance of the Group. Risk management is carried out by the Group’s management under policies approved by the Board of Directors. The Group uses different methods to measure different types of risk to which it is exposed. These methods include monthly cash flow projections for liquidity risk and ageing analysis for credit risk.

The Group’s material risks are disclosed below:

(a) Credit riskThe maximum exposure to credit risk on financial assets of the Group is the carrying amount of those assets as indicated in the Balance Sheet. Credit risk arises from cash and cash equivalents, receivables and committed transactions. Cash and cash equivalents are held with independently rated banks with a minimum rating of ‘A’ (2015: ‘A’). In relation to receivables, which consist largely of loans and leases, the Group manages credit risk by ensuring the portfolio is well diversified across a large number of customers.

Credit risk also arises in relation to financial guarantees given to certain parties (refer note 13(a)(iii)). Such guarantees are only provided in exceptional circumstances and are subject to specific Board approval. Trade and other receivables are well diversified across a large number of customers and do not expose the Group to significant credit risk. Credit risk exposures relating to loans, leases and financial guarantees are disclosed below in more detail.

(i) Credit risk in relation to loan and lease receivables Credit risk is managed by using a prudent risk assessment process for all customers with the intention of seeking minimum exposure at all times and assessing the borrower’s capacity to repay the loan or lease. Credit risk is assessed similarly for each loan or lease based on the borrower’s credit worthiness, credit history and the collateral being provided. Internal policies provide guidance on the acceptable mix of risk categories associated with the receivables portfolio.

Collateral held as security and other credit enhancements

Credit risk on loan and lease receivables is mitigated by obtaining security over the underlying asset. The majority of consumer loan receivables are secured with a motor vehicle and the security registered on the Personal Property Security Register. The vehicle can be repossessed if the counterparty is in default under the terms of agreement. Where there is a shortfall in security held over the motor vehicle, a caveat may be placed over real estate property of the borrower or treated as unsecured.

RACV 2016 ANNUAL REPORT | 35

For novated lease agreements and business loans (goods mortgage and commercial hire purchase agreements), the motor vehicle remains the property of the Group until all payments and the residual are repaid. The following table shows the extent to which mortgage over motor vehicles (for consumer loans) and ownership of property (for novated leases and business loans) mitigate credit risk:

Maximum exposure to credit risk

$m

Market value* of collateral held at

reporting date $m

Secured %

June 2016Loan receivables 226.9 184.0 81Lease receivables 106.2 88.9 84

June 2015Loan receivables 208.7 169.3 81Lease receivables 91.8 78.7 86

* Value of motor vehicles as quoted in the Glass’s Guide vehicle pricing guide.

All loans 61 days overdue are issued with a default notice and reported to the Credit Reporting Agency. Steps are taken to repossess the collateral if the overdue payment is not made within 35 days of the notice. Repossessed collateral is sold at a public auction. The carrying amount of repossessed vehicles as at 30 June 2016, representing the foreclosed collateral obtained through the enforcement of security was $50,000 (2015: $7,000).

Customers are also offered Credit Protection Insurance and Autosure Insurance. Credit Protection Insurance covers loan repayments if customers are unable to meet payment commitments because of illness, injury or unemployment. Autosure Insurance covers the shortfall between the comprehensive motor vehicle insurance payout and any amount still owing to R.A.C.V. Finance Limited in the event the motor vehicle is declared a total loss.

Concentrations of credit risk in relation to loan and lease receivables

The Group minimises concentrations of credit risk in relation to loan receivables by diversification. This is achieved by undertaking transactions with a large number of customers over many sectors and industries. A prudent risk assessment process for all customers is used to manage the credit risk on loan receivables.

Concentration of risk on leases and commercial hire purchases is minimised by the spread of transactions with a large number of customers. Credit risk is minimised through prudent assessment policies and ensuring final balloon repayment amounts are in line with estimated asset values at the end of the repayment term.

The categories of credit risk exposure and the maximum exposure for each concentration are as follows:

2016 %

2015 %

2016 $m

2015 $m

CategorySecured loans 68 69 226.3 207.9Unsecured loans – – 0.6 0.8Leases 32 31 106.2 91.8Total receivables 100 100 333.1 300.5

(ii) Credit quality The level of risk associated with a loan or lease receivable is a measure of its credit quality. The prudent risk assessment process discussed previously assesses the risk associated with a loan or lease receivable. The following information shows the risk profile of loan and lease receivables that are neither past due nor impaired at reporting date and loan and lease receivables that are past due but not impaired at the reporting date.

NOTES TO THE FINANCIAL STATEMENTS30 June 2016 Royal Automobile Club of Victoria (RACV) Limited

36 | RACV 2016 ANNUAL REPORT

13. FINANCIAL RISK MANAGEMENT (CONTINUED)

(a) Credit risk (continued)(ii) Credit quality (continued)

Loan receivablesLoan receivables neither past due nor impaired

2016 %

2015 %

Low-risk loan receivables 99 99High-risk loan receivables 1 1

100 100

The low-risk loans relate to customers with good credit history, capacity to repay the loan and sufficient collateral to minimise exposure. The high-risk loans relate to customers who have had a poor credit history but are now considered to have the capacity to repay the loan.

Loan receivables past due but not impaired

As at 30 June 2016, loan receivables of $0.3 million (2015: $0.5 million) were past due but not impaired. The ageing analysis of payments in arrears on these loan receivables is as follows:

2016 $m

2015 $m

Up to 1 month 0.1 0.1Longer than 1 month and not longer than 3 months 0.1 0.1Longer than 3 months 0.1 0.3

0.3 0.5

Lease receivablesLease receivables neither past due nor impairedSince the launch of the lease product, losses of less than 1% of the portfolio have occurred to date (2015: less than 1%). As at 30 June 2016, 0.3% of the portfolio is in arrears (2015: 0.2%).

Lease receivables past due but not impairedAs at 30 June 2016, lease receivables of $0.4 million (2015: $0.3 million) were past due but not impaired. The ageing analysis of payments in arrears on these lease receivables is as follows:

2016 $m

2015 $m

Up to 1 month 0.3 0.3Longer than 1 month and not longer than 3 months 0.1 –Longer than 3 months – –

0.4 0.3

(iii) Financial guaranteesCross guarantees are given by RACV and each of its wholly owned subsidiaries within the Closed Group as described in note 26. No deficiencies of assets exist in the Closed Group. No liability was recognised by the Group in respect of these guarantees.

(b) Liquidity risk Prudent liquidity risk management implies maintaining sufficient cash assets and the availability of funding through an adequate amount of committed credit facilities and on using the most cost effective means of finance. The Group manages liquidity risk by continuously monitoring of budget and actual cash flows and reporting liquidity projections to the Board. The Group monitors its liquidity position on a monthly basis with the aim of maintaining a liquidity target between 0.3 and 0.6 of one month’s operating expenses (2015: between 0.3 and 0.6 of one month’s operating expenses). The average liquidity position for the Group was 0.6 months (2015: 0.6 months). Due to the dynamic nature of the underlying businesses, the Group aims to maintain flexibility in funding by keeping committed credit lines available.

RACV 2016 ANNUAL REPORT | 37

(i) Financing arrangementsThe Group had access to the following net undrawn borrowing facilities at the reporting date:

2016 $m

2015 $m

Floating rateExpiring within 1 year (bank overdraft) 5.6 5.6Expiring within 1 year (subscription agreement) 9.1 –Expiring within 2 years (subscription agreement) – 35.8

14.7 41.4

(ii) Maturities of financial liabilitiesThe table below analyses the Group’s financial liabilities. The amounts disclosed in the table are the contractual undiscounted cash flows.

Up to 1 month

$m

1 year or less $m

Over 1 to 5 years

$m

Total contractual cash flows

$m

Carrying amount

$m

June 2016Non-interest bearing 81.8 – – 81.8 81.8Fixed interest rate 15.3 203.5 57.0 275.8 275.8

97.1 203.5 57.0 357.6 357.6

June 2015Non-interest bearing 71.8 – 0.3 72.1 72.1Fixed interest rate 14.0 113.1 116.6 243.7 243.7

85.8 113.1 116.9 315.8 315.8

(c) Market risk(i) Price riskThe Group is exposed to unit trust price risk. This arises from investments held by the Group and classified as available for sale financial assets. The Group diversifies its portfolio to manage its price risk arising from investments in unit trusts. Diversification of the portfolio is done in accordance with the limits set by the Group.

The following table summarises the impact of increases/decreases in market price on the Group’s post-tax profit and on equity. The analysis is based on the assumption that the market price of all investments within a specified asset class has moved by the same percentage with all other variables held constant.

2016 2015

Change in value

%

Impact on post-tax

profit $m

Impact on other

components of equity

$m

Change in value

%

Impact on post-tax

profit $m

Impact on other

components of equity

$m

Asset classAustralian equities –/+ 9.5 – –/+ 8.7 –/+ 9.5 – –/+ 7.9Global equities –/+ 9.5 – –/+ 10.2 –/+ 9.5 – –/+ 13.5Inflation linked bonds –/+ 5.0 – –/+ 2.0 –/+ 5.0 – –/+ 2.1Australian bonds –/+ 4.5 – –/+ 1.9 –/+ 4.5 – –/+ 1.7Global bonds –/+ 4.5 – –/+ 1.0 –/+ 4.5 – –/+ 0.5Alternatives –/+ 9.0 – –/+ 7.3 –/+ 9.0 – –/+ 6.7Cash –/+ 0.0 – – –/+ 0.0 – –

Where the fair value of an investment would not be significantly below cost or cost less any impairment loss, no impairment loss would be recognised in the Income Statement as a result of the decrease in the market price.

NOTES TO THE FINANCIAL STATEMENTS30 June 2016 Royal Automobile Club of Victoria (RACV) Limited

38 | RACV 2016 ANNUAL REPORT

13. FINANCIAL RISK MANAGEMENT (CONTINUED)

(c) Market risk (continued)(ii) Interest rate riskThe Group’s interest rate risk exposure results primarily from repricing risk or differences in the repricing characteristics of its financial assets and liabilities. An instrument’s repricing period is a term used to describe how an interest rate sensitive instrument responds to changes in interest rates. It refers to the time it takes an instrument’s interest rate to reflect a change in market interest rates. For fixed rate instruments, the repricing period is equal to the maturity of the instrument’s principal, because the principal is considered to reprice only when reinvested in a new instrument. For floating rate instruments, the repricing period is the period of time before interest rates adjust to the market value.

The Group’s financial assets consist primarily of cash, available for sale financial assets, fixed rate loan receivables with maturities ranging from 12 to 84 months and fixed rate lease receivables with maturities ranging from 6 to 60 months.

The financial liabilities funding these receivables consist primarily of fixed rate secured notes with maturities ranging from 6 to 48 months and fixed rate borrowings on the subscription agreement with maturities up to 180 days that renew automatically at the option of the Group during the term of the subscription agreement.

Due to the mismatch in the maturities of its receivables and the financial liabilities funding these receivables, the Group is exposed to repricing risk. The impact on equity and pre-tax profit of reasonably possible changes in the interest rate over the next 12 months, with all other variables held constant is -/+ $0.1 million (2015: -/+ $0.2 million).

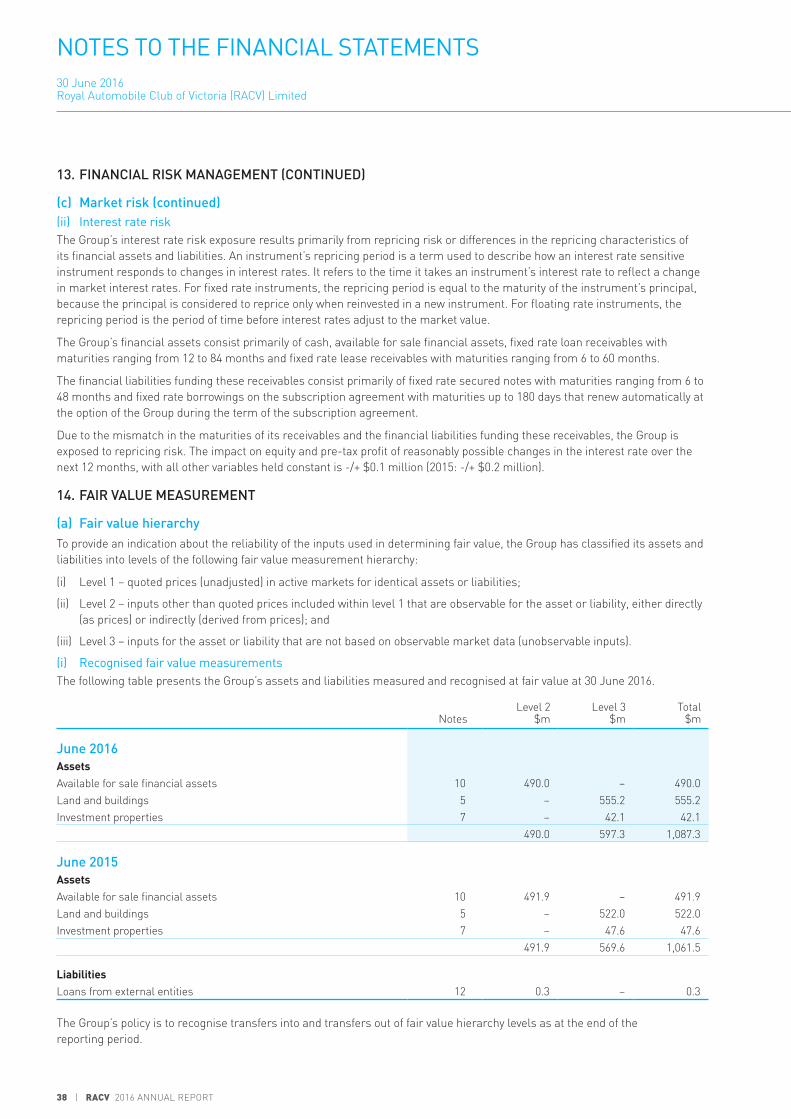

14. FAIR VALUE MEASUREMENT

(a) Fair value hierarchyTo provide an indication about the reliability of the inputs used in determining fair value, the Group has classified its assets and liabilities into levels of the following fair value measurement hierarchy:

(i) Level 1 – quoted prices (unadjusted) in active markets for identical assets or liabilities;

(ii) Level 2 – inputs other than quoted prices included within level 1 that are observable for the asset or liability, either directly (as prices) or indirectly (derived from prices); and

(iii) Level 3 – inputs for the asset or liability that are not based on observable market data (unobservable inputs).

(i) Recognised fair value measurementsThe following table presents the Group’s assets and liabilities measured and recognised at fair value at 30 June 2016.

NotesLevel 2

$mLevel 3

$mTotal

$m

June 2016AssetsAvailable for sale financial assets 10 490.0 – 490.0Land and buildings 5 – 555.2 555.2Investment properties 7 – 42.1 42.1

490.0 597.3 1,087.3

June 2015AssetsAvailable for sale financial assets 10 491.9 – 491.9Land and buildings 5 – 522.0 522.0Investment properties 7 – 47.6 47.6

491.9 569.6 1,061.5

LiabilitiesLoans from external entities 12 0.3 – 0.3

The Group’s policy is to recognise transfers into and transfers out of fair value hierarchy levels as at the end of the reporting period.

RACV 2016 ANNUAL REPORT | 39

(ii) Disclosed fair valuesThe Group also has the following assets and liabilities which are not measured at fair value but for which fair values are disclosed in the notes:

• the carrying amount of loan and lease receivables, secured notes and subscription agreement approximates their fair value as the impact of discounting is not significant;

• the carrying amount of trade receivables and payables approximates their fair value due to their short term nature.

(b) Valuation techniques and inputs used to derive level 2 and level 3 fair valuesThe fair value of available for sale financial assets is based on exit price which is determined by using valuation techniques. The Group uses a variety of methods and makes assumptions that are based on market conditions existing at each reporting date. Quoted market prices of the underlying instruments are used to estimate fair value of all available for sale financial assets (2015: all available for sale financial assets).

Fair value of land and buildings and investment properties is based on independent assessments made by members of the Australian Property Institute. The Group obtains independent valuations for each property on a rolling basis at least every five years. The most recent external valuations of selected land and buildings were made as at 3 May 2016 (2015: 28 February 2015). The most recent external valuations of selected investment properties were made as at 29 February 2016 (2015: 28 February 2013).

Primary valuation techniques supporting the external valuations are the capitalisation approach and the discounted cash flow approach. The capitalisation approach uses cash flow projections based on a property’s estimated net market income and a capitalisation rate derived from an analysis of market evidence. The discounted cash flow approach is based on projected net income and a projected terminal value discounted at an appropriate rate.

The discount rate applied is based on investors’ current return expectations. The resulting valuations are compared to current sales prices in an active market for similar properties in the same location and condition. The fair value of loans from external entities is calculated as the present value of the estimated future cash flows.

NOTES TO THE FINANCIAL STATEMENTS30 June 2016 Royal Automobile Club of Victoria (RACV) Limited

40 | RACV 2016 ANNUAL REPORT

14. FAIR VALUE MEASUREMENT (CONTINUED)

(c) Fair value measurements using significant unobservable inputs (level 3)The following table presents changes in level 3 recurring fair value measurements:

Land and buildings

$m

Investment properties

$mTotal

$m

June 2016Opening balance 1 July 2015 522.0 47.6 569.6Additions 19.3 – 19.3Disposals – – –Transfers 37.0 (6.9) 30.1Depreciation and impairment (19.0) – (19.0)Revaluation (decrement)/increment (4.1) 1.4 (2.7)Closing balance 30 June 2016 555.2 42.1 597.3

Total loss for the period recognised in the Consolidated Income Statement in impairment of property, plant and equipment* (35.7) – (35.7)

Total loss for the period recognised in the Consolidated Statement of Comprehensive Income (4.1) – (4.1)

June 2015Opening balance 1 July 2014 487.6 47.6 535.2Additions 5.7 0.1 5.8Disposals – – –Transfers 32.2 – 32.2Depreciation and impairment (6.8) (0.1) (6.9)Revaluation increment 3.3 – 3.3Closing balance 30 June 2015 522.0 47.6 569.6

Total gain for the period recognised in the Consolidated Income Statement in impairment of property, plant and equipment* 5.3 – 5.3

Total gain for the period recognised in the Consolidated Statement of Comprehensive Income 2.6 – 2.6

* Represents unrealised (loss)/gain recognised in the Consolidated Income Statement attributable to assets held at the end of the reporting period.

(d) Valuation processes Information about the valuation of land and buildings and investment property is provided in note 14(b). Where land and buildings and investment properties are not externally valued in a given year, fair value is re-assessed by considering factors such as significant changes to the property, material changes to the local conditions and major macro-economic shocks. Valuation outcomes are reported to the Audit and Compliance Committee at least annually.

RACV 2016 ANNUAL REPORT | 41

TAXATION

15. INCOME TAX EXPENSE

2016 $m

2015 $m

(a) Income taxCurrent tax expense (2.4) (1.3)Deferred tax expense (refer note 16) (6.7) (14.7)Over/(under) provided in prior years 2.4 (0.8)Income tax expense (6.7) (16.8)

(b) Reconciliation of prima facie income tax

The assessable income of RACV for income tax purposes comprises only certain income deemed to be derived from non-member activities. Conversely, allowable deductions for income tax purposes are limited to certain expense and statutory deductions.

The prima facie tax on operating profit differs from the income tax provided in the accounts as follows:

Profit before income tax 53.4 143.3

The prima facie tax expense on operating profit before income tax @ 30% (16.0) (43.0)

Tax effect of amounts which are not taxable/(deductible) in calculating income tax:Over/(under) provision for tax from previous year 2.4 (0.8)Profit/(loss) attributable to activities for the mutual benefit of members 1.3 (0.2)Share of net profit of equity accounted investments 24.6 31.3Capital gains (1.7) (4.7)Sundry items 2.9 0.6Prior year tax losses derecognised (20.2) –

Income tax expense attributable to operating profit (6.7) (16.8)

(c) Tax expense relating to items of other comprehensive income

Aggregate current and deferred tax arising in the reporting period and not recognised in net profit or loss but directly debited or credited to other comprehensive income:

Net deferred tax credited directly to other comprehensive income (refer note 16) 7.9 (0.5)

(d) Tax consolidationRACV and its wholly owned subsidiaries are parties to a tax sharing agreement and a tax funding agreement. The tax sharing agreement, in the opinion of the Directors, limits the joint and several liability of the wholly owned subsidiaries in the case of default by RACV.

Under the tax funding agreement, the wholly owned subsidiaries fully compensate RACV for any current tax payable assumed and are compensated by RACV for any current tax receivable and deferred tax assets relating to unused tax losses or unused tax credits that are transferred to RACV under the tax consolidation legislation. The funding amounts will be determined by reference to the amounts recognised in the wholly owned subsidiaries’ financial statements.

(e) Income tax contributionsRACV continues to contribute significantly to Australia’s tax base across all applicable federal and state taxes. With respect to income tax, a major component of RACV’s profit comes from its investments in associates where the dividend income is received on a fully franked basis meaning income tax is paid at source. The amount of income tax paid on RACV’s dividend component was over $24.7 million during the financial year (2015: $58.1 million).

NOTES TO THE FINANCIAL STATEMENTS30 June 2016 Royal Automobile Club of Victoria (RACV) Limited

42 | RACV 2016 ANNUAL REPORT

16. DEFERRED TAX ASSETS

2016 $m

2015 $m

The balance comprises temporary differences attributable to:

Amounts recognised in profit or lossProperty, plant and equipment 23.6 14.1Employee benefits 7.3 7.4Superannuation plan (2.5) (2.6)Unearned income 3.0 3.8Available for sale financial assets 5.5 5.6Finance leases (3.2) (2.3)Intangible assets (13.7) (16.2)Tax losses and credits 65.5 79.7Other 3.8 (0.1)

89.3 89.4

Amounts recognised directly in other comprehensive incomeRevaluation of property (5.6) (3.6)Superannuation plan 9.1 5.4Available for sale financial assets 0.6 (3.9)

4.1 (2.1)

Net deferred tax assets 93.4 87.3

MovementsOpening balance 87.3 103.0Under/(over) provision from prior year 3.1 (0.6)Debited to the Consolidated Income Statement (6.7) (14.7)Credited/(debited) to equity 7.9 (0.5)Deferred tax impact of business acquisition 1.9 –Other (0.1) 0.1Closing balance 93.4 87.3

(a) Accounting estimates, assumptions and judgements: Income taxesThe Group assesses the recoverability of deferred tax assets based on detailed financial forecasts. When assessing the recoverability of the deferred tax assets, the Directors consider the expected profitability of non-mutual activities, prevailing economic conditions and investment return rates.

The Group has recognised deferred tax liabilities for capital gains under the Capital Gains Tax regime on unrealised tax gains that would arise on disposal of its available for sale financial assets at current tax rates. This is in accordance with the accounting policy stated in note 27(d).

In addition, the Group has recognised deferred tax assets relating to carried forward capital and tax losses to the extent there are sufficient future tax liabilities and taxable temporary differences (deferred tax liabilities) relating to the same taxation authority. However, utilisation of the tax losses also depends on the ability of the Group to satisfy certain tests at the time the losses are recouped.

If the Group fails to satisfy these tests, carried forward tax losses of $52.6 million and capital losses of $12.9 million that are currently recognised as deferred tax assets would have to be recognised as income tax expense (2015: carried forward tax losses of $61.7 million and capital losses of $18 million).

RACV 2016 ANNUAL REPORT | 43

REMUNERATION AND BENEFITS

17. KEY MANAGEMENT PERSONNEL

Key management personnel compensation comprises:2016

$’0002015

$’000

Short-term benefits 10,502 10,005Post-employment benefits 670 657Long-term benefits 1,363 1,271Termination benefits (contractual entitlements) 1,958 –

14,493 11,933

Key management personnel of the Group

The key management personnel of the Group comprise all Directors of RACV and the executives having authority and responsibility for planning, directing and controlling the activities of the Group. At 30 June 2016, in addition to the 11 Directors, 15 executives were included as key management personnel (30 June 2015: 11 Directors, 17 executives).

Transactions with key management personnel of the wholly owned Group

The key management personnel of RACV have normal business transactions with various controlled entities including the use of various facilities available to them as members and reimbursement of travelling expenses. These transactions include insurance, secured note investments and finance loans and leases with the wholly owned Group’s finance company and minor sales of products and services. All these transactions are conducted on a commercial basis on conditions no more beneficial than those available to members or employees.

18. SUPERANNUATION BENEFITS

Upon joining the Group, new employees are able to choose whether to join the defined contribution section of the RACV Superannuation Fund (Plan) or an alternative fund. All members of the Plan are entitled to benefits on resignation, retirement, ill health, disability or death.

The Plan has both a defined benefit section and a defined contribution section. The defined benefit section provides defined benefits based on years of membership and final average salary for those members employed prior to 1 March 1998 and who elected to remain defined benefit members. The defined contribution section receives fixed contributions from Group companies and the Group’s legal or constructive obligation is limited to these contributions for this section of the Plan.

Plan assets are held in trust which is subject to supervision by the prudential regulator. Funding levels are reviewed regularly. Where assets are less than vested benefits, being those payable upon exit, a management plan must be formed to restore the coverage to at least 100%.

Responsibility for governance of the Plan, including investment decisions and plan rules rests with the Board of Trustees of the Plan. Contribution levels are also the responsibility of the trustee, although these are usually set in consultation with the employer. Disclosures for the Plan are shown below:

2016 $m

2015 $m

Fair value of superannuation Plan assets 194.6 200.5Present value of the defined benefit obligation (74.6) (61.4)Present value of the defined contribution obligation (142.2) (148.4)Superannuation Plan liability in the Balance Sheet (22.2) (9.3)

NOTES TO THE FINANCIAL STATEMENTS30 June 2016 Royal Automobile Club of Victoria (RACV) Limited

44 | RACV 2016 ANNUAL REPORT

18. SUPERANNUATION BENEFITS (CONTINUED)

2016 $m

2015 $m

(a) ReconciliationsMovement in the present value of the defined benefit obligation:Opening present value 61.4 61.8Current service cost 1.6 1.7Interest expense 2.2 1.9Actuarial loss/(gain) arising from changes in financial assumptions 11.6 (33.6)Actuarial loss arising from changes in demographic assumptions – 28.0Actuarial loss arising from liability experience – 2.8Contributions by Plan participants 0.3 0.3Benefits, administrative costs and tax paid (2.5) (1.5)Closing present value 74.6 61.4

Movement in the fair value of Plan assets (including defined contribution plan):Opening fair value 200.5 197.5Interest income 2.0 1.6Actuarial return on Plan assets, less interest (expense)/income (0.6) 2.4Contributions by employer 1.2 0.3Contributions by Plan participants 0.3 0.3Benefits, administrative costs and tax paid (2.5) (1.5)Movement in vested benefits in respect of defined contribution members (6.3) (0.1)Closing fair value 194.6 200.5

(b) Amounts recognised in the Consolidated Income StatementCurrent service cost 1.6 1.7Net interest expense 0.3 0.3Total included in employee benefits expense 1.9 2.0

(c) Amounts recognised in the Consolidated Statement of Comprehensive IncomeRemeasurements:Actual return on Plan assets, less interest expense/(income) 0.6 (2.4)Actuarial loss/(gain) incurred during the year 11.6 (2.7)Total amount recognised in the Consolidated Statement of Comprehensive Income 12.2 (5.1)

RACV 2016 ANNUAL REPORT | 45

GROUP STRUCTURE

19. SUBSIDIARIES

Equity interest held by the consolidated entity

2016 %

2015 %

Royal Automobile Club of Victoria (RACV) Ltd.* − RACV Holdings Pty. Ltd. 100 100

− R.A.C.V. Investment Company Pty. Ltd. 100 100 − RACV Centre Pty Ltd 100 100

− RACV Centre Holdings Pty. Ltd. 100 100 − RACV Centre Finance Pty. Ltd. 100 100 − RACV Centre Building Pty. Ltd. 100 100

− RACV Sales & Marketing Pty. Ltd. 100 100 − R.A.C.V. Finance Limited* 100 100 − RACV Insurance Services Pty. Ltd.* 100 100 − Direct Salary Packaging Pty. Ltd. 100 100 − C.E. Aitken Pty. Ltd. 100 100 − RACV Road Service Pty. Ltd. 100 100

− Intelematics Australia Pty Limited* 90 90 − RACV Investment Holdings Pty. Ltd. 100 100

− Club Home Assistance Holdings Pty Ltd 100 100 − Club Resort Holdings Pty Ltd 100 100

− National Roads & Motorists Association & N.R.M.A of Victoria Pty. Ltd. 100 100 − Automobile Association & A.A of Victoria Pty. Ltd. 100 100 − RACV Security Pty. Ltd. 100 100 − RACV Country Club Pty. Ltd. 100 100 − RACV Property Investments Pty. Ltd. 100 100 − Access 24 Holdings Pty Ltd 100 100 − RACV Commercial Holdings Pty. Ltd 100 100 − RACV Group Services Pty. Ltd. 100 100 − National Response Pty. Ltd 100 100 − RACV Services Pty. Ltd. 100 100 − EPAC Group Pty Ltd 100 100

− Carfleet Pty Ltd 100 100 − Carlease Pty Ltd 100 100 − EPAC Innovation Pty Ltd 100 100 − EPAC Salary Solutions Pty Ltd 100 100

− EPAC WA Pty Ltd 100 100 − Club Tasmania Holdings Pty Ltd* 90 90 − Club Home Response Pty Ltd* 51 51

Sub-controlled entities are indented.* These controlled entities have not been granted relief from the necessity to prepare financial reports in accordance with Class Order 98/1418 issued by the

Australian Securities and Investments Commission (ASIC).

NOTES TO THE FINANCIAL STATEMENTS30 June 2016 Royal Automobile Club of Victoria (RACV) Limited

46 | RACV 2016 ANNUAL REPORT

20. BUSINESS COMBINATIONS

On 5 November 2015, RACV Limited acquired the land, building and chattels used in operating the Novotel Forest Resort in Creswick, Victoria for a total consideration of $15.5 million. The facility is a four-star rated property which commenced operation in 2008 and currently operates as RACV Goldfields Resort. The acquisition complements the Group’s existing resorts portfolio.

The acquired business contributed revenue of $4.7 million and operating loss of ($4.1) million to the Group during the 2016 financial year. If the acquisition had occurred on 1 July 2015, consolidated revenue and operating loss for the year ended 30 June 2016 would have been $8.2 million and ($3.0) million respectively. These amounts have been calculated using the Group’s accounting policies applied from 1 July 2015.

Details of the purchase consideration, the net assets acquired and discount on business acquisition are as follows:

$m

Purchase consideration (refer (i) below):Cash paid 15.5

Total purchase consideration 15.5Less: fair value of net identifiable assets acquired (refer (ii) below) (18.2)Discount on business acquisition1 (2.7)

1 Discount on business acquisition is attributable to the deferred tax impact of the acquisition.

(i) Purchase consideration

Outflow of cash on purchase of the business, working capital and chattels, net of cash acquired:Cash consideration 15.5

Outflow of cash 15.5

Acquisition related costs

Acquisition related costs of $0.9 million were included in other expenses in the Consolidated Income Statement and in payments to suppliers and employees in the Consolidated Statement of Cash Flows.

(ii) Assets and liabilities acquiredThe assets and liabilities arising from the acquisition are as follows:

Carrying amount

$mFair value

$m

Receivables 0.1 0.1Freehold land and improvements 4.1 4.1Buildings 11.7 11.7Plant and equipment 1.1 1.1Deferred tax asset – 1.9Payables (0.3) (0.3)Employee benefit provisions (0.3) (0.4)Net identifiable assets acquired 16.4 18.2

There were no acquisitions during the year ended 30 June 2015.

RACV 2016 ANNUAL REPORT | 47

21. INVESTMENTS ACCOUNTED FOR USING THE EQUITY METHOD

(a) Carrying amountsAll associates are measured using the equity method and have a reporting date of 30 June. The country of incorporation is also their principal place of business. The proportion of ownership interest is the same as the proportion of voting rights held.

Name Principal activityPlace of Business

Ownership interest Consolidated carrying amount2016

%2015

%2016

$m2015

$m

AssociatesInsurance Manufacturers of Australia Pty Limited (IMA)

General insurance Australia 30 30 217.2 195.8

Australian Motoring Services Pty Ltd (AMS)

Assistance services Australia 24 24 2.3 2.0

Club Assets Pty Ltd (Club Assets) Assistance services Australia 501 501 20.3 18.2

239.8 216.0

Joint ventures Intelematics North America, LLC (INA)

Telematics services United States of America

452 452 2.7 1.3

Intelematics Europe Limited (IEU) Telematics services United Kingdom

293 – 1.4 –

243.9 217.3

1 For the purposes of this disclosure, the 50% ownership interest in Club Assets is equivalent to a beneficial 30% ownership interest in the net assets of the underlying investment.

2 The 45% ownership interest represents RACV’s share of Intelematics Australia Pty Limited 50% ownership interest in the net assets of INA.

3 The 29% ownership interest represents RACV’s share of Intelematics Australia Pty Limited 32% ownership interest in the net assets of IEU.

Associates and joint ventures are strategic investments for the Group and complement the services provided by the general insurance and emergency roadside assistance businesses.

2016 $m

2015 $m

(b) Movements in carrying amount of investments in associates and joint venturesOpening balance 217.3 242.9Increase in investment in associates and joint ventures 1.4 1.3Share of profits after income tax 83.1 104.3Dividend received/receivable (57.7) (132.2)Changes to retained earnings (0.2) 1.0Closing balance 243.9 217.3

NOTES TO THE FINANCIAL STATEMENTS30 June 2016 Royal Automobile Club of Victoria (RACV) Limited

48 | RACV 2016 ANNUAL REPORT

21. INVESTMENTS ACCOUNTED FOR USING THE EQUITY METHOD (CONTINUED)

(c) Summarised financial information for associates The table below presents summarised financial information for associates that are material to the Group. The information disclosed reflects the amounts presented in the financial statements of the relevant associates.

IMA AMS Club Assets1

2016 $m

2015 $m

2016 $m

2015 $m

2016 $m

2015 $m

Balance Sheet Total assets 3,605.8 3,498.0 34.0 33.2 89.4 113.6

Total liabilities 2,881.2 2,845.2 24.5 24.9 22.8 52.8Net assets 724.6 652.8 9.5 8.3 66.6 60.8

Reconciliation to carrying amountOpening net assets 1 July 652.8 743.1 8.3 8.7 60.8 59.8Profit after tax for the period 258.3 338.1 1.2 2.7 12.6 7.6Other comprehensive (loss)/income (2.5) 2.4 – – – –Dividends paid (184.2) (430.5) – (3.1) (8.0) (8.0)Share of reserves movement charged to retained earnings

(0.4) (0.3) – – 2.1 1.4

Closing net assets 30 June 724.0 652.8 9.5 8.3 67.5 60.8

Group’s share in % 30% 30% 24% 24% 30%1 30%1

Group’s share in $ 217.2 195.8 2.3 2.0 20.3 18.2Carrying amount 30 June 217.2 195.8 2.3 2.0 20.3 18.2

Statement of Comprehensive IncomeRevenue 2,806.4 2,686.2 42.1 39.5 294.9 251.2

Profit after tax for the period 258.3 338.1 1.2 2.7 12.6 7.6Other comprehensive (loss)/income (2.5) 2.4 – – – –Total comprehensive income 30 June 255.8 340.5 1.2 2.7 12.6 7.6

1 For the purposes of this disclosure, the ownership interest in Club Assets is equivalent to a beneficial 30% ownership interest in the net assets of the underlying investment.

RACV 2016 ANNUAL REPORT | 49

22. PARENT ENTITY FINANCIAL INFORMATION

(a) Summary financial informationThe individual financial statements for Royal Automobile Club of Victoria (RACV) Limited, the parent entity, show the following aggregate amounts:

RACV2016

$m2015

$m

Profit for the year 10.6 16.8

Total comprehensive income 19.1 20.9

Balance SheetCurrent assets 1,312.1 1,221.3Total assets 1,586.2 1,468.2

Current liabilities 988.1 886.9Total liabilities 1,013.9 898.0

Members’ equityAsset revaluation reserve 1.3 1.3Retained earnings 571.0 568.9

Total members’ equity 572.3 570.2

(b) Financial guarantees entered into by Royal Automobile Club of Victoria (RACV) LimitedCross guarantees are provided by RACV and each of its wholly owned subsidiaries within the Closed Group as described in note 26. No deficiencies of assets exist in the Closed Group.

R.A.C.V. Finance Limited has a commitment from RACV Limited for an increase in its capital base by $10 million should the secured liabilities to tangible assets ratio reach 83.5% as described in note 11(a).

No liability was recognised by the Group or RACV in respect of these guarantees.

(c) Contingent liabilities of Royal Automobile Club of Victoria (RACV) LimitedRACV has agreed to support various Group subsidiaries to ensure their debts are paid as and when they fall due (refer to note 26).

(d) Contractual commitments for the acquisition of property, plant and equipmentAs at 30 June 2016, Royal Automobile Club of Victoria (RACV) Limited had contractual commitments for the acquisition of property, plant and equipment totalling $0.7 million (2015: $5.9 million). These commitments relate to Cobram Resort redevelopment (2015: Cobram Resort redevelopment).

NOTES TO THE FINANCIAL STATEMENTS30 June 2016 Royal Automobile Club of Victoria (RACV) Limited

50 | RACV 2016 ANNUAL REPORT

OTHER INFORMATION

23. MEMBERS’ EQUITY

2016 $m

2015 $m

(a) Members’ reserves Asset revaluation reserve 45.6 48.7Fair value reserve – available for sale financial assets (1.5) 9.3Transactions with non-controlling interests 3.8 5.3

47.9 63.3

Movements:

Asset revaluation reserveOpening balance 48.7 46.9Revaluation – gross (4.1) 2.6Deferred tax 0.9 (0.8)Non-controlling interests share in revaluation 0.1 –Closing balance 45.6 48.7

Fair value reserve – available for sale financial assets Opening balance 9.3 13.5Revaluation – gross (13.5) (10.6)Transfer of realised gains to net profit – gross (2.8) (0.8)Impairment of available for sale investments – gross 0.9 5.3Deferred tax 4.6 1.9Closing balance (1.5) 9.3

(b) Nature and purpose of reserves

Asset revaluation reserve

The asset revaluation reserve is used to record increments and decrements on the revaluation of properties as described in note 27(k).

Fair value reserve – available for sale financial assets

This reserve is used to record movements in the fair value of available for sale financial assets as described in note 27(h). Amounts are recognised in the Income Statement when the associated assets are sold or impaired.

Transactions with non-controlling interests

This reserve is used to record changes in the ownership interest in a subsidiary company that do not result in a loss of control.

(c) Retained earningsOpening balance 1,429.1 1,298.4Net profit attributable to members of RACV for the year 45.8 126.1Superannuation plan remeasurements (12.2) 5.1Deferred tax on superannuation plan 3.7 (1.5)Change in associate retained earnings (0.2) 1.0Closing balance attributable to members of RACV 1,466.2 1,429.1

RACV 2016 ANNUAL REPORT | 51

(d) Capital risk management The Group’s objective when managing members’ equity (capital) is to protect the financial viability and sustainability of the Group and to ensure sufficient funds continue to be available to deliver member services and carry out business plans and initiatives. The Group’s capital management is focused on monitoring balance sheet strength and flexibility using liquidity projections (refer to note 13(b)) and detailed budgeting processes.

(e) Membership

Number of members2016 2015

Membership categoryOrdinary (Club) 26,293 26,306Service 1,457,636 1,451,227Total voting members 1,483,929 1,477,533

Relationship members 597,915 616,010Associate Corporate and Honorary members 3,874 3,774Total members 2,085,718 2,097,317

RACV operates as a company limited by guarantee with the liability of any member not exceeding $6.30. The number of voting members represents the total number of members who are entitled to a vote.

In accordance with the Articles of Association, Service members and Ordinary (Club) members are entitled to vote in a Service election whilst only Ordinary (Club) members are entitled to vote in an Ordinary (Club) election. Associate Corporate and Honorary Club members and Relationship members are not entitled to a vote under the Articles.

24. RELATED PARTY TRANSACTIONS

The Royal Automobile Club of Victoria (RACV) Limited is the ultimate controlling entity.

(a) The following related party transactions occurred during the financial year:

Transactions with related parties within the wholly owned Group

Administrative and other service charges are made within the Group on commercial terms and conditions. All material transactions with associate companies are made on commercial terms and conditions.

Transactions with other related parties

Aggregate amounts included in the determination of operating profit before income tax that resulted from transactions with each class of other related parties:

2016 $’000

2015 $’000

Commission and other revenueIMA 83,936 80,540Club Assets 1,835 2,479

Subscription and other revenueAMS 7,326 6,473

Superannuation expensesRACV Superannuation Fund 11,038 10,640

Current receivablesIMA 7,590 6,849

Current payablesIMA 4,058 3,894

(b) Ownership interests in related partiesInterests held in the following classes of related parties are set out in the following notes:

(i) Subsidiaries – note 19(ii) Associates – note 21(iii) Joint ventures – note 21

NOTES TO THE FINANCIAL STATEMENTS30 June 2016 Royal Automobile Club of Victoria (RACV) Limited

52 | RACV 2016 ANNUAL REPORT

25. AUDITOR’S REMUNERATION

2016 $’000

2015 $’000

During the year, the following fees were paid or payable to the auditor:

PricewaterhouseCoopersAudit and review of consolidated financial reports of RACV and the financial reports of its subsidiaries 631 552 Other services 88 88

Total remuneration 719 640

It is RACV’s policy to employ PricewaterhouseCoopers on assignments additional to their statutory audit duties where PricewaterhouseCoopers’ expertise and experience with RACV are important. These assignments are principally audit and other services, or where PricewaterhouseCoopers is awarded assignments on a competitive basis. It is RACV’s policy to seek competitive tenders for all major consulting projects.

26. DEED OF CROSS GUARANTEE

RACV and each of its wholly owned subsidiaries indicated in note 19, excluding RACV Insurance Services Pty. Ltd. and R.A.C.V. Finance Limited, are parties to a Deed of Cross Guarantee (Deed) under which each company guarantees the debts of the others. By entering into the Deed, these wholly owned subsidiaries have been relieved from the requirement to prepare a financial report and Directors’ report under Class Order 98/1418 (as amended by Class Order 98/2017) issued by ASIC.

These companies represent a ‘Closed Group’ for the purposes of the Class Order and, as there are no other parties to the Deed that are controlled by RACV, they also represent the ‘Extended Closed Group’. Set out below is a condensed consolidated Income Statement, Statement of Comprehensive Income, summary of movements in retained earnings and a Balance Sheet of the Closed Group, after eliminating all transactions between parties to the Deed.

Closed Group2016

$m2015

$m

Condensed Income Statement

Profit from ordinary activities before income tax 50.9 144.4Income tax expense (4.7) (13.8)Profit from ordinary activities after income tax 46.2 130.6

Condensed Statement of Comprehensive Income

Profit from ordinary activities after income tax 46.2 130.6Other comprehensive (loss)/income (24.5) 1.6Total comprehensive income for the year 21.7 132.2

Movement in retained earnings

Opening balance 1,361.5 1,210.5Revocation of Intelematics Australia Pty Limited from the ‘Closed Group’ – 15.8Profit from ordinary activities after income tax 46.2 130.6Superannuation plan actuarial (loss)/gain (12.2) 5.1Deferred tax on superannuation plan actuarial (loss)/gain 3.7 (1.5)Change in associate retained earnings (0.3) 1.0Retained earnings at the end of the financial year 1,398.9 1,361.5

RACV 2016 ANNUAL REPORT | 53

Closed Group2016

$m2015

$m

Balance Sheet

Current assetsCash and cash equivalents 33.2 65.9Receivables 27.1 23.0Inventories 3.0 2.8Available for sale financial assets 21.7 49.0Prepayments and accruals 57.0 14.5Total current assets 142.0 155.2

Non-current assetsAvailable for sale financial assets 520.7 491.3Investments accounted for using the equity method 240.0 216.1Property, plant and equipment 583.2 545.7Investment properties 42.1 47.6Intangible assets 79.3 93.1Deferred tax assets 99.9 93.3Total non-current assets 1,565.2 1,487.1Total assets 1,707.2 1,642.3

Current liabilitiesTrade and other payables 67.6 60.4Provisions 58.2 38.7Unearned income 106.8 103.3Total current liabilities 232.6 202.4

Non-current liabilitiesSuperannuation benefits 22.2 9.3Provisions 6.6 6.5Total non-current liabilities 28.8 15.8Total liabilities 261.4 218.2Net assets 1,445.8 1,424.1

Members’ equityMember reserves 46.9 62.6Retained earnings 1,398.9 1,361.5Total members’ equity 1,445.8 1,424.1

NOTES TO THE FINANCIAL STATEMENTS30 June 2016 Royal Automobile Club of Victoria (RACV) Limited

54 | RACV 2016 ANNUAL REPORT

27. SIGNIFICANT ACCOUNTING POLICIES

The principal accounting policies adopted in the preparation of the financial report are set out below. These policies have been consistently applied to all the years presented, unless otherwise stated. The financial report is for the consolidated entity (the Group) consisting of Royal Automobile Club of Victoria (RACV) Limited (“RACV”) and its subsidiaries.

(a) Basis of preparationThis general purpose financial report has been prepared in accordance with Australian Accounting Standards and Interpretations issued by the Australian Accounting Standards Board (AASB) and the Corporations Act 2001. The Group is a for-profit entity for the purpose of preparing the financial statements.

Compliance with IFRS

The consolidated Financial Statements of the Group also comply with International Financial Reporting Standards (IFRS) as issued by the International Accounting Standards Board (IASB).

Historical cost convention

These consolidated Financial Statements have been prepared under the historical cost convention, as modified by the revaluation of available for sale financial assets and liabilities, certain classes of property, plant and equipment and investment property.

Functional and presentation currency

The consolidated Financial Statements are presented in Australian dollars, which is the functional and presentation currency of the Group.

Accounting estimates, assumptions and judgements

In preparing these consolidated Financial Statements management has made judgements, estimates and assumptions that affect the application of the Group’s accounting policies and the reported amounts of assets, liabilities, income and expenses. Actual results may differ from these estimates.

Estimates and judgements are continually evaluated and are based on historical experience and other factors, including expectation of future events that may have a financial impact on the Group and that are believed to be reasonable under the circumstances.

The areas involving a higher degree of judgement or complexity, or areas where assumptions and estimates are significant to the consolidated Financial Statements are disclosed in the following notes:

• Provision for impairment of loan and lease receivables – refer note 2(a);

• Property developments – refer note 5(d);

• Estimated impairment of goodwill, customer contracts and software in development – note 6(b);

• Estimate of impairment revaluation charge on available for sale financial assets – note 10(a); and

• Income taxes – refer note 16(a).

Reclassification of prior year amounts

Where material, comparative amounts have been reclassified to ensure consistency with the current reporting period.

New and amended standards adopted by the Group

There are no new accounting standards or interpretations impacting the Group in the financial year commencing 1 July 2015.

Early adoption of standards

The Group has not elected to apply any pronouncements before their operative date in the annual reporting period beginning 1 July 2015.

(b) Principles of consolidation

Subsidiaries

The consolidated Financial Statements incorporate the assets and liabilities of all subsidiaries of RACV as at 30 June 2016 and the results of all subsidiaries for the year then ended. RACV and its subsidiaries together are referred to in this financial report as the Group or the consolidated entity.