2016 first six-months results - IAB2016 first six-months results First six-months and quarterly...

24

IAB internet advertising revenue report 2016 first six-months results www.pwc.com www.iab.net Any trademarks included are trademarks of their respective owners and are not affiliated with, nor endorsed by, PricewaterhouseCoopers LLP.

Transcript of 2016 first six-months results - IAB2016 first six-months results First six-months and quarterly...

PwC

IAB internet advertising revenue report

2016 first six-months results

www.pwc.com

www.iab.net

Any trademarks included are trademarks of their respective owners and are not affiliated with, nor endorsed by, PricewaterhouseCoopers LLP.

PwCPwC

Agenda

2

November 2016

Survey methodology

2016 first six-months results

First six-months and quarterly trends

Advertising formats

Social media

Pricing models

Industry category spending

About PwC

PwCPwC

Survey Methodology

3

November 2016

Survey Scope

The IAB Internet Advertising Revenue Report is part of an ongoing IAB mission to provide an accurate barometer of Internet advertising growth.

To achieve differentiation from existing estimates and accomplish industry-wide acceptance, key aspects of the survey include:

• Obtaining historical data directly from companies generating internet (desktop and mobile) advertising revenues;

• Making the survey as inclusive as possible, encompassing all forms of internet advertising, including websites, consumer online services, ad networks and exchanges, mobile devices; and

• Ensuring and maintaining a confidential process, only releasing aggregate data.

Methodology

Throughout the reporting process, PwC:

• Compiles a database of industry participants selling internet advertising revenues.

• Conducts a quantitative mailing survey with leading industry players, including web publishers, ad networks, commercial online service providers, mobile providers, and other online media companies.

• Requests and compiles several specific data items, including monthly gross commissionable advertising revenue by industry category and transaction.

• Acquires supplemental data through the use of publicly disclosed information.

• Identifies non-participating companies and applies a conservative revenue estimate based on available public sources.

• Analyzes the findings, identifies and reports key trends.

PwCPwC

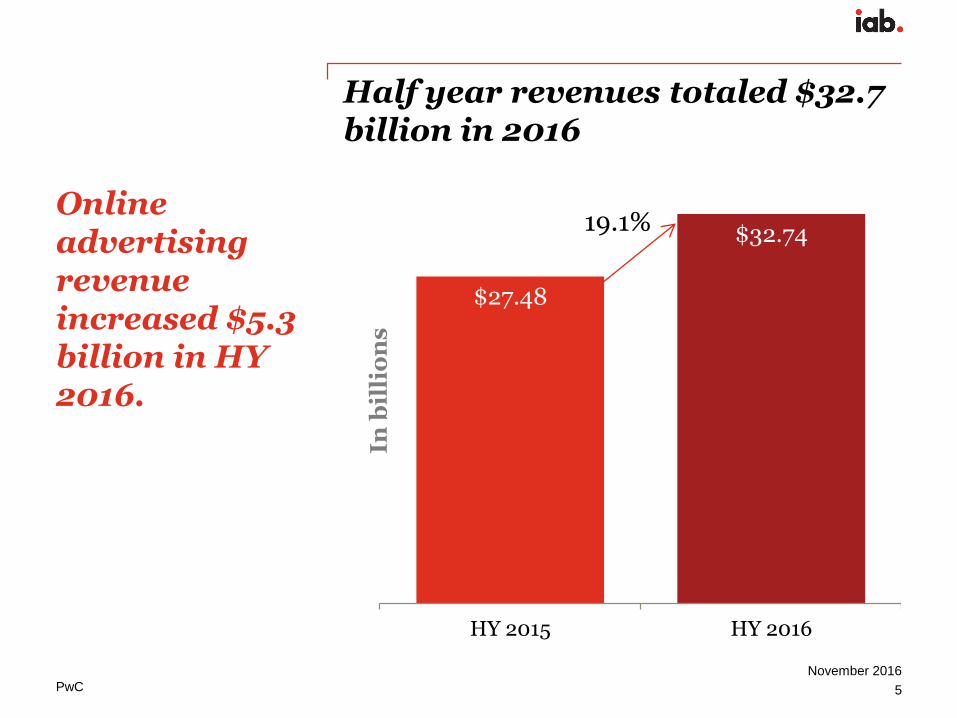

Half year revenues totaled …

4

November 2016

In b

illi

on

s

$27.48

$32.7

HY 2015 HY 2016

PwCPwC 5

November 2016

Half year revenues totaled $32.7billion in 2016

Online advertising revenue increased $5.3 billion in HY 2016.

In b

illi

on

s

$27.48

$32.74

HY 2015 HY 2016

19.1%

PwCPwC 6

November 2016

2016 second quarter revenues totaled ….

In b

illi

on

s

$14.30

$16.9

Q2 2015 Q2 2016

Source: IAB Internet Advertising Revenue Report, HY 2016

PwCPwC 7

November 2016

2016 second quarter revenues totaled $16.89 billion

Revenue in Q2 2016 was $2.6 billion higher than in Q2 2015.

In b

illi

on

s

$14.30

$16.89

Q2 2015 Q2 2016

18.1%

Source: IAB Internet Advertising Revenue Report, HY 2016

PwCPwC 8

November 2016

Strong Growth between Q1 2016 and Q2 2016

In b

illi

on

s

$15.85$16.9

Q1 2016 Q2 2016

Source: IAB Internet Advertising Revenue Report, HY 2016

PwCPwC 9

November 2016

Strong Growth between Q1 2016 and Q2 2016

Revenue in Q2 2016 was $1.0 billion higher than in Q1 2016.

In b

illi

on

s

$15.85$16.89

Q1 2016 Q2 2016

6.6%

Source: IAB Internet Advertising Revenue Report, HY 2016

PwCPwC 10

November 2016

Since 2010, a strong seasonal trend has emerged for internet advertising revenuesQuarterly growth comparison, 1996–HY 2016

In b

illi

on

s

’96

PwCPwC 11

November 2016

First six-months 2016 shows record revenues Historical revenue mix, first half vs. second half

In b

illi

on

s

$3.3 $4.6 $5.8 $7.9 $10.0 $11.5 $10.9 $12.1$14.9 $17.0

$20.1$23.1

$27.5$32.7

$4.0$5.0

$6.8$9.0

$11.2$11.9 $11.8

$13.9

$16.8

$19.5

$22.7

$26.4

$32.1

?

$0

$10

$20

$30

$40

$50

$60

$70

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Last 6 months

First 6 months

* CAGR: Compound Annual Growth Rate

PwCPwC

Industry concentration – the long tail

12

November 2016

Top 10 Companies = 74% of HY 2016 Revenues

Next 15 Companies = 10% of HY 2016 Revenues

Remaining Companies = 16% of HY Revenue

PwCPwC

$8.9 $1.1 $0.9 $15.5 $2.3 $3.4 $0.2 $0.4

-12%

-29%

2%

89%

13%

-10%

-47%

-29%

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

$-

$2

$4

$6

$8

$10

$12

$14

$16

Search Classifieds &Directories

LeadGeneration

Mobile Digital VideoCommercials

Banners Ads Sponsorship Rich Media

HY 2016 Revenue HY 2016 vs. HY 2015 % Growth

$10.1

13

November 2016

Mobile shows the strongest growthAdvertising formats – HY 2016 results and growth rates

In b

illi

on

s

PwCPwC 14

November 2016

Historical trends in internet advertising formatsRevenue share by major ad formats, 2006–HY 2016

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

Search Mobile Banner Ads Digital Video Classifieds LeadGeneration

Sponsorship

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 HY 2016

% o

f to

tal

re

ve

nu

e

Source: IAB Internet Advertising Revenue Report, HY 2016

PwCPwC 15

November 2016

Mobile represents a significant percentage of advertising formats

For the half year in 2016, Mobile revenue totaled $15.5 billion

Source: IAB Internet Advertising Revenue Report, HY 2016

27%

12%

7%

47%

6%

Search Display / BannerVideo MobileOther

48%

39%

10%

3%

Mobile Search

Mobile Display / Banner

MobileVideo

Mobile Other

PwC

Distributing Mobile across formats demonstrates its importance to Search and Display

Formats – HY 2016(Mobile separated)

Formats – HY 2016(Mobile included)

Source: IAB Internet Advertising Revenue Report, HY 2016

27%

12%

7%7%

47%

Search Display Video Other Mobile

50%

31%

12%

8%

Search Display Video Other

PwCPwC 17

November 2016

Ad Formats – Mobile allocated comparison to PYVideo across formats demonstrate strongest growth

50%

31%

9%

10%

HY 2015

Search Display Banner

Display Video Hybrid Other

50%

31%

12%

8%

HY 2016

Search Display Banner

Display Video Hybrid Other

Total – $27.5 billion Total – $32.7 billion

Source: IAB Internet Advertising Revenue Report, HY 2016

PwCPwC

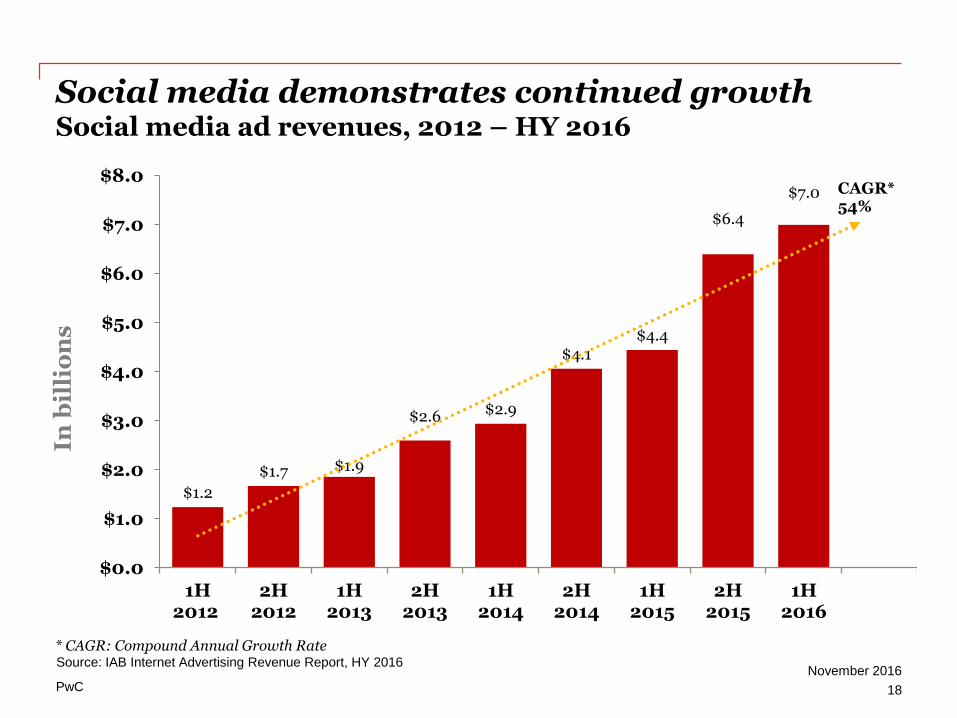

$1.2

$1.7 $1.9

$2.6 $2.9

$4.1$4.4

$6.4

$7.0

$0.0

$1.0

$2.0

$3.0

$4.0

$5.0

$6.0

$7.0

$8.0

1H2012

2H2012

1H2013

2H2013

1H2014

2H2014

1H2015

2H2015

1H2016

CAGR* 54%

Social media demonstrates continued growthSocial media ad revenues, 2012 – HY 2016

18

November 2016

In b

illi

on

s

* CAGR: Compound Annual Growth RateSource: IAB Internet Advertising Revenue Report, HY 2016

PwCPwC 19

November 2016

Pricing modelsInternet ad revenues by pricing model, HY 2015 vs. HY 2016

32%

66%

2%

HY 2015

Impression-based Performance-based

Hybrid

34%

65%

1%

HY 2016

Impression-based Performance-based

Hybrid

Total – $27.5 billion Total – $32.7 billion

Source: IAB Internet Advertising Revenue Report, HY 2016

PwC

Historical pricing model trendsInternet ad revenues by pricing model, 2005–HY 2016

46% 48%

45%

39%37%

33%31% 32% 33% 34%

32%34%

41%

47%

51%

57%59%

62%65% 66% 65% 65% 66% 65%

13%

5% 4% 4% 4% 5% 4%2% 2% 1% 2% 1%

0%

10%

20%

30%

40%

50%

60%

70%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 HY2016

CPM Performance Hybrid

% o

f to

tal

re

ve

nu

e

Note: Pricing model definitions may have changed over the time period depicted both within the survey process and as interpreted by respondents

PwC

Internet ad revenues by major industry category$27.5 B in HY 2015 vs. $32.7 in HY 2016

21%

13%12%

9% 9%

7% 7%

5% 5%4%

21%

13%12%

9%8%

6%7%

6%5%

4%

Retail FinancialServices

Auto Telecom LeisureTravel

PackagedGoods

Tech /Computing

Media Pharma &Healthcare

Entertain-ment

HY 2015 HY 2016

% o

f to

tal

re

ve

nu

e †

† Amounts do not total to 100% as minor categories are not displayed.

PwCPwCNovember 2016

PwC’s Technology and Entertainment, Media, and Communications practices

As business, accounting, and tax advisors to many of the world’s leading Entertainment, Media, and Communications (EMC) and Technology (Tech) companies, PwC (www.pwc.com) has an insider’s view of trends and developments driving the industry. With approximately 1,200 practitioners serving EMC and Tech clients in the United States, PwC is deeply committed to providing clients with industry experience and resources. In recent years, our pioneering work in EMC and Tech has included developing strategies to leverage digital technology, identifying new sources of financing, and marketplace positioning in industries characterized by consolidation and transformation. Our experience reaches across all geographies and segments of the EMC and Tech sectors, including broadband, wireless, the internet, music, film, television, publishing, advertising, gaming, theme parks, computers and networking, and software. With thousands of practitioners around the world, we're always close at hand to provide deep industry knowledge and resources.

Our services include:

• Business assurance services

• Web audience measurement and advertising delivery auditing and advisory

• IAB Measurement Certification Compliance auditing

• Privacy policy structuring, attestation, and compliance advisory

• Mergers & acquisitions assistance

• Tax planning and compliance

• Capital sourcing and IPO assistance

• Marketing & Media operations enablement

22November 2016

PwCPwCNovember 2016

For information, contact one of the following PwC professionals:New York

David SilvermanPartner, Assurance [email protected]

Russ SapienzaPrincipal, Advisory [email protected]

Brian GaffneyManager, Advisory [email protected]

23

Technology and Entertainment, Media, and Communications practicesContacts

PwC

www.pwc.com/e&m

PricewaterhouseCoopers has exercised reasonable care in the collecting, processing, and reporting of this information but has not independently verified, validated, or audited the data to verify the accuracy or completeness of the information. PricewaterhouseCoopers gives no express or implied warranties, including but not limited to any warranties of merchantability or fitness for a particular purpose or use and shall not be liable to any entity or person using this document, or have any liability with respect to this document. This report is for general purposes only, and is not a substitute for consultation with professional advisors.

© 2016 PwC. All rights reserved. PwC refers to the US member firm or one of its subsidiaries or affiliates, and may sometimes refer to the PwC network. Each member firm is a separate legal entity. Please see www.pwc.com/structure for further details.