2016 Canadian CEO Outlook

36

June 2016 kpmg.ca/CEOoutlook The race is on 2016 Canadian CEO Outlook

-

Upload

stradablog -

Category

Business

-

view

356 -

download

0

Transcript of 2016 Canadian CEO Outlook

© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Contents 4 Overview

7 Executive summary

10 The race is on

15 The ever-changing customer

18 A call for innovation

20 Build, buy, partner

24 Success by the numbers

26 Security in the cyber age

28 A view to talent

33 Conclusion

34 Methodology

32016 Canadian CEO Outlook

© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

75%

98% 92% 92%

82%74%

“ Whether it’s investment strategies, innovation agendas or strategic priorities, we can obtain important insights between Global and Canadian CEOs.”

of CEOs believe the next 3 years will be more critical for their industry than the previous 50

of CEOs indicate innovation is one of the top 3 issues on their personal agenda

Customer loyalty Innovation Economic forces

concerned about the loyalty of their customers

concerned about whether their organization is staying on top of what’s next in services/products

concerned about the impact of the global economy on their company

The complexity of the issues and the need for rapid response is putting significant pressure on CEOs.

of CEOs expect their company to remain mostly the same over the next 3 years

Rob Brouwer, Managing Partner, Clients and Markets, KPMG in Canada

Top 3 concerns for CEOs

The race is on

© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

66%Data & Analytics

of CEOs are using D&A effectively; 62% report using D&A to analyze brand via social media; 58% to aid with maintenance and services; 57% to drive strategy and change

Despite the changes enveloping their organizations, CEOs arelargely confident in their 3-year growth outlook.

Growth confidence is high

13%Cyber

of CEOs feel confident that they are fully prepared for a cyber event; 87% are somewhat prepared. 50% of CEOs use D&A to spot fraud

96% 85% 85% 81%Company Country Industry Global economy

of CEOs areconfident in growth fortheir company over thenext 3 years

confident in theircountry’s growth prospects

confident in theirindustry’s growth prospects

confident in thegrowth of the global economy

“ Canadian CEOs are confident in their ability to outperform the general economic backdrop, and that the next three years will be more important in shaping their industry than the previous 50 years.”Bill Thomas, CEO, KPMG in Canada

Nearly 1,300 CEOs from around the world, including 53 CEOs from Canada, share their perspectives on the unprecedented change forecast for their companies and the world economy.

© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Executive summaryAs CEOs race to secure the talent, innovation, and capabilities for growth in the global digital age, the question is: Are Canadian executives keeping pace?

KPMG conducted a survey of nearly 1,300 around the world, including 53 Canadian CEOs, and the results of that survey provide some interesting insights.

The good news is Canadian leaders are confident in the health of their companies and industries, and optimistic about their growth. They recognize the importance of embracing technology, leveraging data and analytics (D&A), and pursuing innovation; and they are taking steps to connect on a more personal level with today’s ever-evolving (and increasingly fickle) customer.

“What stands out in this report is that CEOs are confident in their ability to outperform the general economic backdrop, and that the next three years will be more important in shaping their industry than the previous 50,” observes Bill Thomas, CEO of KPMG in Canada.

That all sounds promising at first glance, yet our findings suggest we might want to take more cues from our global counterparts. Canadian CEOs, for example,

appear more insular in their thinking. They are less inclined to drive significant business transformation, and more concerned with existing customer loyalties and accessing local talent, than their global counterparts. Meanwhile, they assign a lower priority to innovation, and show less concern for significant external business influences such as geopolitical factors, new disruptors, and competitors.

Interestingly, and perhaps of concern in our globally connected digital world, Canadian CEOs are more

confident when it comes to cyber security and evaluating their organizations’ skills and event readiness at higher levels than their global counterparts.

“Whether related to investment strategies or innovation agendas,

CEO concerns, or strategic game plans, there are key differences between the perspectives of global and Canadian CEOs that are interesting and can generate insights for all of us”, says Rob Brouwer, Managing Partner, Clients and Markets, with KPMG in Canada.

This Canadian CEO Outlook explores why these differences matter, and how learning from them can help position Canadian companies as the leader of the pack.

According to 75 percent of Canadian CEOs, the next three years will be more critical for their industry than the previous 50 years.

72016 Canadian CEO Outlook

© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Canadian CEOs are poised to leave their mark on the global economy. However, with telling differences between them and global CEOs, it is clear there are insights to be gained from their international peers.

Here are some takeaways:

Canadian CEOs are more apprehensive about transformation.While company growth and customer retention are key focuses for Canadian CEOs, they are less likely than global CEOs to undergo a significant transformation over the next three years.

Canadian CEOs are more confident in the growth prospects for their companies and their sector, than for the Canadian economy as a whole, and believe that new customers for existing products, as opposed to new products, markets or channels, will be the most important source of that growth.Interestingly, global CEOs are more outward-looking, with more focus on new geographic markets, new products, and related business model transformation.

Canadian CEOs believe global economic factors, technology, and access to talent will have the most impact on their growth over the next three years.Meanwhile, they believe factors such as current competition, geopolitical factors, and new competitors/disruptors will play a smaller role. Global CEOs agree that global economic factors will have the most impact on growth, but rank domestic economic factors, current competition, and new competitors/disruptors higher than Canadians. These differences suggest Canadian CEOs hold a slightly more insular view when it comes to strategic planning.

Disruptive technologies are a key driver of innovation/transformation.The need to react to disruptive technologies is informing M&A practices, investment strategies, talent development, and overall approaches to innovation.

Canadian CEOs understand the need to innovate, yet not as much as their global peers.A majority of Canadian CEOs say innovation is in their top three priorities, with many planning to drive innovation through the creation of environments that encourage risk taking, partnerships with educational and research institutes, and fostering an overall culture of innovation. However, global CEOs rank innovation higher on their personal agendas.

Customer loyalty is keeping Canadian CEOs up at night.Where Canada was once a leader in loyalty programs, the challenge of changing demographics, disruptive technologies and more customer choice has created new challenges for customer retention. Other CEO concerns include their organization’s ability to keep pace with what customers want in services and products, and the impact of global economic forces on their business.

CEOs are underutilizing their D&A.While customer loyalty is a top concern, less than half of Canadian CEOs use D&A to analyze their existing customers, develop new products or services, or find new customers. Still, they show higher levels of confidence than global CEOs when it comes to the accuracy, effectiveness, security, and ethical use of their D&A.

8 The race is on

© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Cyber risk is not a large concern forCanadian CEOs (but it should be). Canadians feel more confident in their level of preparedness for cyber events than their global counterparts, and only a quarter feel it is a risk (compared to nearly a third of global CEOs and only half use D&A to spot fraud. Certainly, Canadian CEOs are doing their due diligence when it comes to protecting their company and customers from cyber events, however they are not beholden to the same breach notification laws and other cyber regulations in other countries. Therefore, they may not be prioritizing cyber as much as their global peers. This may change as cyber regulations begin rolling out in the second half of 2016.

Canadian CEOs are far more likely to manage skills gaps with outside talent.Compared to global CEOs, Canadian companies are more likely to contract labour, focus on offshoring, and outsource internationally than global CEOs. This will require a stronger talent management strategy.

HR is evolving.With plans to increase their headcount more than global companies over the next three years, and a stronger focus on looking outwards to fill their skills gaps, Canadian HR departments are more critical to all company functions – and busier – than ever before.

92016 Canadian CEO Outlook

© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Innovation, talent, and technology are at the top of Canadian CEOs’ minds as many secure the people and capabilities to compete in the global race.

“Transformation is a word that comes up today more than it ever has before, and both our Canadian CEOs and global CEOs recognize they are going to have to fundamentally transform and evolve who they are, what they do, and how they go to market,” says Jeff Smith, Advisory Managing Partner, KPMG in Canada.

Yet while Canadian CEOs are talking the talk, their outlooks, approaches, and risk assessments differ from their global counterparts in ways that tell a slightly different story. Specifically, 74 percent of Canadian CEOs say their companies will be largely the same in three years, compared to 59 percent globally who believe the same. With a quarter predicting transformation, it’s questionable whether Canadian leaders are as committed to change.

Canadian CEOs are nonetheless optimistic when it comes to forecasting growth for their companies, industries, the country, and the global economy over the next three years. Ninty-six percent foresee company growth (over half predict top-line growth between 2-5 percent), 85 percent have high hopes for their industry, 85 percent are confident in Canada’s growth, and 81 percent express similar optimism for the global economy.

Still, 58 percent of Canadian CEOs recognize that Canada is in a state of slow growth. This is clear evidence that their confidence is tempered by an awareness for domestic speed-bumps such as ongoing oil and gas industry challenges and Canada’s depreciating dollar.

Economic forecasts aside, our data does suggest that Canadian CEOs aren’t fully aligned with their global counterparts when it comes to evaluating the impact that certain external factors and risks will have on their businesses’ growth. When asked what will have the most influence on that growth, Canadian CEOs expressed more concern over technology than global CEOs; whereas the latter were more concerned about their respective domestic economies, and ranked new and current competitors higher than did Canadian CEOs.

Interestingly, Canadian CEOs also identify new customers as the most important source of growth over the next three years, whereas global CEOs rank new markets, new products, and new channels as more important than their Canadian counterparts.

The race is on

10 The race is on

© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Ensuring KPIs are fit for purpose and

accurately measured

Talent development/ management

Responding to short-term

influence of activist shareholders

Stronger client focus Talent development/ management

and implementing disruptive technology

Top strategic priorities

Canada

Global

28% 19% 19%

21% 19% 18%

Loyalty of customers

Impact of global economic forces

on business

Organization’s ability to stay on top of

what’s next in service/products

Top CEO concerns

Canada

98% 92% 92%

Loyalty of customers

Millennials’ wants and needs

impacting business

Impact of global economic forces

on business

Global

88% 88% 86%

Fostering innovation

112016 Canadian CEO Outlook

© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Does this suggest Canadian companies are more inward focused? Brouwer observes, “As Canadians, we appear to be somewhat more insular in our thinking about the future of our businesses, whereas our global counterparts seem more externally focused. As Canadians, we aren’t as focused on new markets, new channels, and new products as much as global CEOs, and that’s a little worrying.”

Other disparities are seen relating to forecasting potential growth in international markets. Over half of Canadian CEOs (51 percent) view India as the region with the most potential for market growth over the next three years, compared to 38 percent of global CEOs. And though both agree China and the United States show equal promise, Canadian CEOs are more confident than anyone else in these regions. This likely reflects the strong economic ties between the Canadian and US economies, and Canada’s increasing focus on China trade. Elsewhere, Canadian CEOs expressed moderate degrees of confidence for increased business in countries like Australia (30 percent), Brazil (28 percent), and Western Europe (26 percent).

Elsewhere, when asked to share their top strategic priorities over the next three years, 19 percent of Canadian CEOs list “responding to short-termism” in their top three – nearly double that of global CEOs. This is also very interesting says Brouwer, who notes, “There has been significant focus in Canada on addressing the perceived impact that activist shareholders, short-sellers, and other market participants with an all-too-often short-term view have had on management decision making and strategic priority setting.”

70% new customers

49%new channels

41%new markets

40%new products

Most important source of growth in next 3 years

12 The race is on

© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

“ Despite all the changes at their doorsteps, corporate leaders around the world are largely confident about their short-term prospects and even more optimistic for the growth of their own companies and the global economy over the next three years.”

Bill Thomas CEO of KPMG in Canada

132016 Canadian CEO Outlook

© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

14 The race is on

© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Keeping up with customers’ needs and wants can be daunting. Today’s customers are more tech-savvy and globally-minded. They crave greater convenience with less hassle, more customization with fewer complexities, and cutting-edge technologies without security risks.

In short: customer loyalty can be tough to pin down, and it’s the companies that effectively embrace D&A, innovative thinking, and flexible strategies that will help them in their corner.

It’s no surprise that 98 percent of Canadian CEOs cite customer loyalty as their number one concern, while 92 percent admit to having sleepless nights over their ability to stay on top of what’s next in services and products, and 53 percent say they are worried about keeping up with customer needs and expectations.

“Canada is a mature market where growth generally comes at the expense of competitors – and re-cently there are many new companies fighting for customer mindshare. It is only natural that this is making CEO’s think more about how win customers and keep them loyal in the face of new choices,” offers Andrea Baldwin, Partner, Management Consulting, KPMG in Canada.

The ever-changing customer

152016 Canadian CEO Outlook

© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

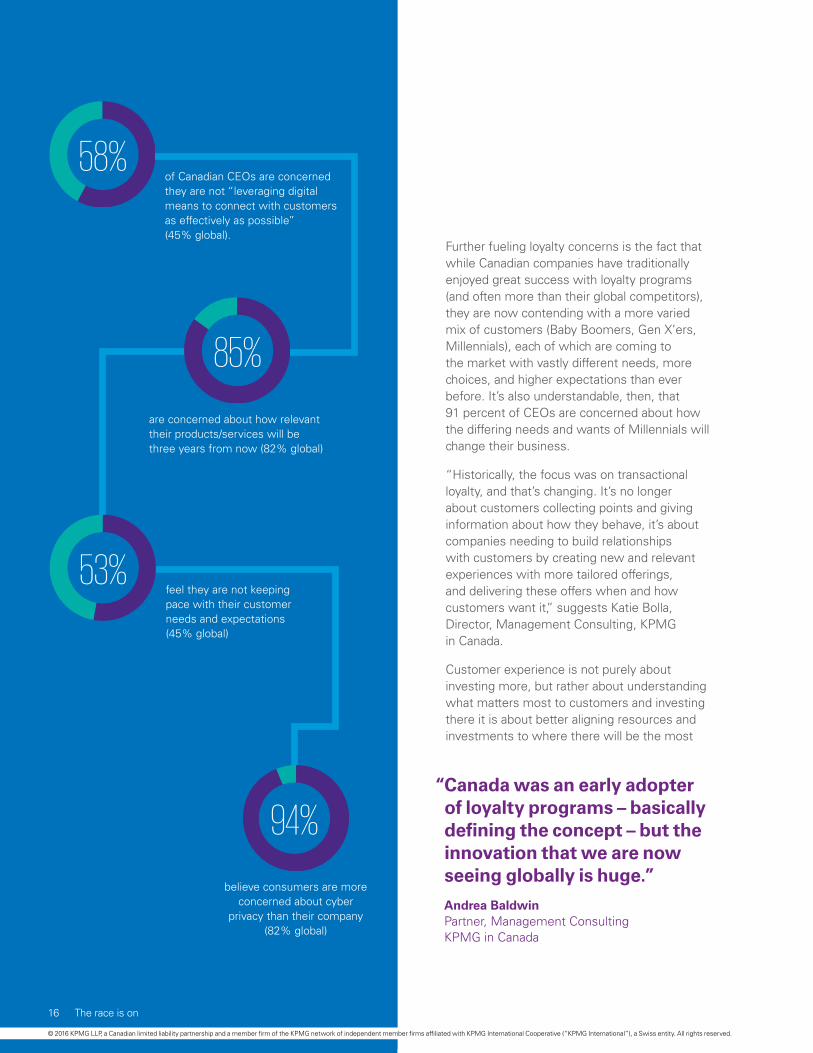

of Canadian CEOs are concerned they are not “leveraging digital means to connect with customers as effectively as possible”(45% global).

are concerned about how relevant their products/services will be three years from now (82% global)

58%

85%

feel they are not keeping pace with their customer needs and expectations (45% global)

believe consumers are more concerned about cyber

privacy than their company (82% global)

53%

94%

Further fueling loyalty concerns is the fact that while Canadian companies have traditionally enjoyed great success with loyalty programs (and often more than their global competitors), they are now contending with a more varied mix of customers (Baby Boomers, Gen X’ers, Millennials), each of which are coming to the market with vastly different needs, more choices, and higher expectations than ever before. It’s also understandable, then, that 91 percent of CEOs are concerned about how the differing needs and wants of Millennials will change their business.

“Historically, the focus was on transactional loyalty, and that’s changing. It’s no longer about customers collecting points and giving information about how they behave, it’s about companies needing to build relationships with customers by creating new and relevant experiences with more tailored offerings, and delivering these offers when and how customers want it,” suggests Katie Bolla, Director, Management Consulting, KPMG in Canada.

Customer experience is not purely about investing more, but rather about understanding what matters most to customers and investing there it is about better aligning resources and investments to where there will be the most

“ Canada was an early adopter of loyalty programs – basically defining the concept – but the innovation that we are now seeing globally is huge.”

Andrea Baldwin Partner, Management Consulting KPMG in Canada

16 The race is on

© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

value to the customer and for the company.

Creating those tailored experiences requires a meaningful approach to how customer data is acquired, interpreted, and used. Still, only half of Canadian CEOs say they use D&A to analyze existing customers, monitor the market, or even assess how their products are being used. And with only 21 percent planning to invest both in data analysis capabilities and the measurement and analysis of their customers’ experience and needs over the next three years, there’s room for greater focus.

“It’s essential for companies to turn their analytics into insights and make data-driven decisions centred around their customers,” suggest Bolla. “Companies that are doing well are ones who know their customers better than the customers know themselves.”

With a third of Canadian CEOs ranking new customers as the most important source of growth over the next three years, companies will need to invest in the capabilities to not only understand their customers’ wants and desired experiences, but develop a strategy for building market share. And while 17 percent of CEOs say being more client-focused is a strategic priority, many are not leveraging technologies and D&A as effectively as they could be to help analyze customer behaviours, target marketing

campaigns, find new customers, and – perhaps most importantly – align resources and investments to create unique customer experiences and to build on their strategy of customer growth.

Meanwhile, as disruptive technologies continue to alter the market, larger companies can find themselves challenged to redirect their IT efforts and pivot as fast as smaller, more flexible competitors.

“Technology is dramatically changing how companies interact with their customers. Progressive IT teams understand this and are changing how they work to become more nimble and responsive to new technology solutions” says Baldwin, adding that this type of culture change can be tough for teams that had previously focused on big investment projects like ERP system implementations.”

It’s the companies that understand the power of D&A, digital engagement, and tailor-made experiences that will have the best shot at customer retention. Still, Canadian CEOs are showing less of an emphasis on innovation or using D&A to understand their customers compared to global CEOs. As such, it’s fair to reason that Canadians can do more with the tools and data at their disposal to fully meet the needs and expectations of today’s constantly-

“ Customers expect security out of the box. They want things like banking apps to be quick and easy, but they also expect full privacy and security around that.”

Paul W. Hanley National Cyber Security Leader KPMG in Canada

172016 Canadian CEO Outlook

© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

A call for innovationThe spirit of Moore’s Law is alive and well, and shaping conversations from the boardroom to the break room. With every passing year comes disruptive technologies that possess the speed and power to change the way companies engage, react, and adapt to their customers. They are the catalyst for innovation, yielding new business models, products, and services; while shifting economic buying power and altering the barriers to entry.

To be sure, disruptive technologies are changing the way both companies and their customers behave. Therefore, staying responsive in a global market affected by near-constant disruptions requires creative thinking and keeping an eye for what’s next.

“Change management will be crucial as organizations intend to match the speed of their customers. This is change management to a degree that people have not witnessed before,” says Brian Miske, Chief Marketing Officer, KPMG in Canada.

While this need is not lost on Canadian CEOs, only 13 percent say innovation is their primary objective on a personal agenda (compared to 23 percent globally). On the upside, 85 percent of Canadian CEOs say it is still within their top three priorities.

As for how Canadian CEOs seek to drive innovation, a majority (83 percent) plan to create environments that encourage risk-taking, while 81 percent intend to foster a culture of innovation and implement formal processes through which innovative ideas can be commercialized or adopted internally.

Collaborating and partnering with universities, research institutes, and other external partnerships is a focus and driver for Canadian companies. Three-quarters of Canadian CEOs plan to drive shareholder value through collaborative growth, compared to 58 percent of global CEOs.

In order to capitalize on the opportunities that exist, it’s clear companies need to be agile and responsive to the constant change. And indeed, 72 percent of Canadian CEOs believe organizational agility and being able to respond quickly to developments, risks, and opportunities is an effective way to drive innovation.

Globally, this is ranked as the most important factor in driving innovation (ranked least important for Canada).

Still, with 60 percent of Canadian CEOs concerned that they are not disrupting business models in their industry, compared to 53 percent of global CEOs, the question is: Are Canadian companies thinking far enough down the road on how they can change the technology landscape?

The focus on innovation is no doubt strong, but our survey suggests Canadian CEOs still lag behind global CEOs when it comes to acknowledging the need to reach new markets with new ideas.

66 percent are concerned they don’t have an effective strategy in place to counter convergence in the market

18 The race is on

© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

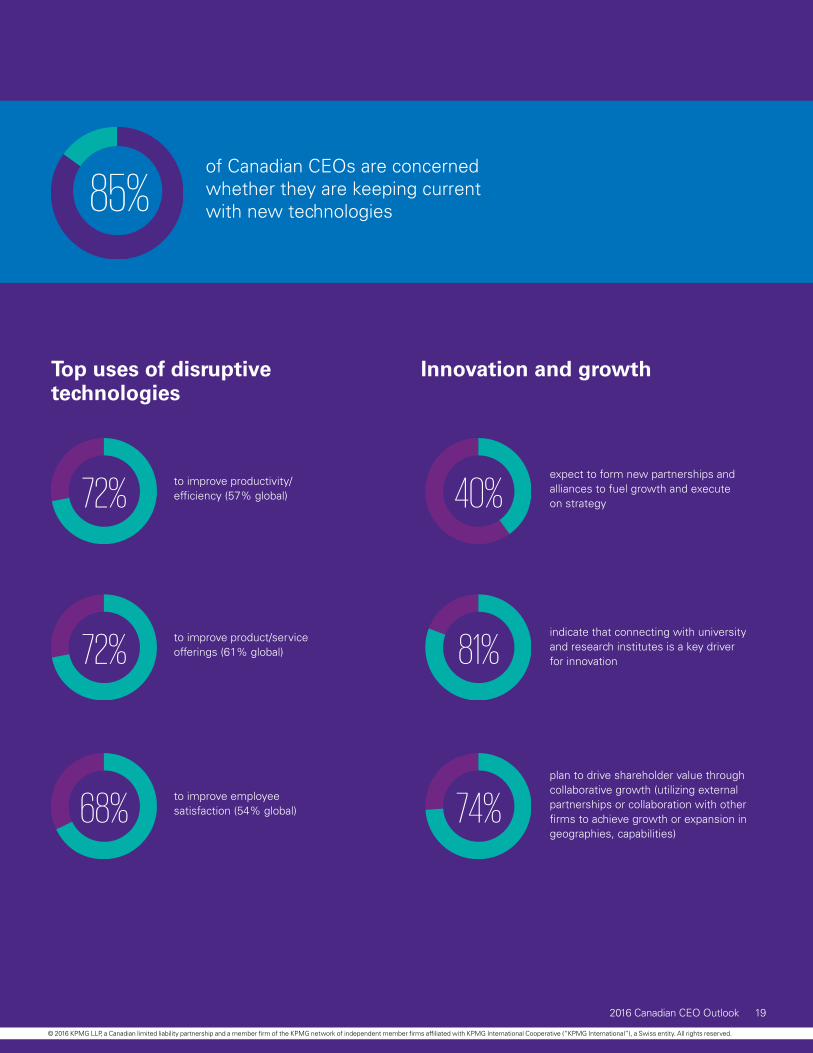

to improve productivity/efficiency (57% global)

Top uses of disruptivetechnologies

72%

of Canadian CEOs are concerned whether they are keeping current with new technologies85%

to improve product/service offerings (61% global)72%

to improve employee satisfaction (54% global)

expect to form new partnerships and alliances to fuel growth and execute on strategy

indicate that connecting with university and research institutes is a key driver for innovation

plan to drive shareholder value through collaborative growth (utilizing external partnerships or collaboration with other firms to achieve growth or expansion in geographies, capabilities)

68%

40%

81%

74%

Innovation and growth

192016 Canadian CEO Outlook

© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Build, buy, partnerNavigating the global market means seizing economic conditions and equipping the right data, capabilities, and talent. It also means capturing the interests (and wallets) of customers whose loyalties can turn at the drop of an app.

Understanding this, forward-thinking companies are aligning themselves with the technologies and capabilities to do just that through acquisitions, mergers, and internal investments. Thirty percent of Canadian CEOs plan to make significant investment in the acquisition of a business, capabilities or assets (18% global), making it one of the top areas of investment for Canadians alongside cyber security solutions.

Interestingly, Canadian CEOs are also approaching M&A as a means to not only enter partnerships that will make them more money, but also open doors to new customer categories, improve their supply chain, or put them in a better position to compete with their innovation agenda.

“A lot of the M&A activity today may not be a traditional straight buy; but instead be companies partnering with firms with the technologies they need. In fact, a lot of the alliances you’re hearing about now are situations where companies are getting into partnerships to see if certain technologies and innovations take off, and if they do, that’s when they’ll go ahead and buy it,” says Matt Tedford, National Leader, Deal Advisory, KPMG in Canada.

20 The race is on

© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

“ If Canadian corporations are going to stay competitive in today’s world, they have to create an environment where risk taking or ‘safe to fail’ is part of their DNA.”

Matt Tedford National Leader, Deal Advisory KPMG in Canada

212016 Canadian CEO Outlook

© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Changing the capital structure through equity

(47% global)

M&A activity over next 3 years

55%

Changing the capital structure with debt/financing

(45% global)

51%

Creating partnerships, joint ventures or collaborative arrangements with other

firms (50% global)

47%

Selling businesses, assets, or capabilities to other

firms (40% global)

38%

Merging with another firm (35% global)

30%

No planned changes(5% global)

0%

Buying businesses, assets, or capabilities from other

firms (41% global)

45%

22 The race is on

© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

This is creating new opportunities for Canadian tech companies that are seeking new partnerships or ways to expand their operations. And certainly, with cross-pollination occurring between high-tech regions such as Toronto, Vancouver, the Waterloo Corridor, and Silicon Valley, Canadians are taking the steps to reinforce their global position.

Surely, the time to evolve is now; M&A strategies within Canada are being driven by a desire to build, buy, or partner their way closer to new assets and capabilities that will fuel their innovation agendas, talent strategies, and technological growth (and, in some cases, with greater intensity than global CEOs). That makes sense, says Tedford, who emphasizes, “Canadian CEOs don’t have the option to sit back; they know that the speed at which things are moving has never been faster.”

“ Globalization continues and the speed at which things are changing is having a considerable impact on how companies are currently making their money. If you look at Canada specifically, there’s no question that our access to capital and our low-interest environment is allowing them affordable capital structures – both in equity and debt – to go ahead and make acquisitions. This is a pretty important time.”

Matt Tedford National Leader, Deal Advisory KPMG in Canada

232016 Canadian CEO Outlook

© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

The future belongs to those that not only collect the data, but wield it effectively. To that end, companies must reposition their approach to D&A from operationally-focused to one that drives innovation and a deep understanding of their customers, suppliers and competitors.

“The most highly valued companies in the world are data-first companies” says Shreeshant Dabir, Partner, KPMG in Canada. “These companies have orchestrated their business around a deep understanding of the interactions and transactions with their customers. CEOs are recognizing the paradigm shift from a digital economy to one where the economy is digital and the number one priority is the customer relationship.”

It’s not enough to own customer data; the advantage is how one uses it. By using advanced analytics, businesses can anticipate individual customer needs and, in response, customize their products and services. Sophisticated techniques, such as machine learning algorithms and cognitive computing, are allowing companies to automatically deliver personalized service at a significantly lower cost.

“Better products, at lower cost points with shorter response times, are the seeds of disruption. Investing in social media analytics is fine, but if Canadian CEOs are truly focused on growth through the customer like they say, they need to be focused on driving strategy and change, researching new products and services, and understanding customer behaviour through advanced analytics”, says Dabir in response to the

fact that a little more than half of Canadian CEOs (57 percent) actually use D&A to drive strategy and growth, while only 55 percent use it to develop new products and services, and fewer (40 percent) leverage D&A to find new customers.

When asked to rank their level of trust in using D&A, an average of 20 percent of Canadian and global CEOs admitted limited or active distrust in the accuracy and effectiveness of the data at their fingertips.

“While CEOs are competent and confident when it comes to reactive analytics – what happened,

how much happened, and when it happened – they need to start focusing on how their businesses will build trust in the forward-looking sophisticated predictive analytics,” says Dabir.

D&A will become even more important in the years to come – especially with the rise of blockchain, which has the potential to create new models of digital commerce, AI, and cognitive analytics to increase the understanding of humans and service by systems, and that more of us will be living in an always-on interconnected world of instant commerce. Companies that hope to make good on their predictions of growth and innovation must therefore assess if they are truly ready to make effective use of data and analytics.

Success by the numbers

of Canadian CEOs have a high level of trust in the ethical use

of their D&A (47% global)

of Canadian CEOs have a high level of trust in the accuracy of

their D&A (41% global)

of Canadian CEOs have a high level of trust in the effectiveness

of their D&A (39% global)

Level of trust in using D&A

53% 34% 34%

Analyzing branding via social media

Driving strategy and change

Aiding with maintenance and services

Improving financial reporting

Developing new products and

services

Analyzing our existing customers

Top uses of D&ACanada

62% 58% 57% 57% 55% 55%

to analyze how products are used

41%

Driving strategy and change

Developing new products and

services

Driving process and cost efficiency

Managing risk Finding new customers

44% 44% 43% 43% 43%

Global

Analytics is no longer optional. It is essential to build trusted intelligence into everyday decisions, products and services.

24 The race is on

© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

of Canadian CEOs have a high level of trust in the ethical use

of their D&A (47% global)

of Canadian CEOs have a high level of trust in the accuracy of

their D&A (41% global)

of Canadian CEOs have a high level of trust in the effectiveness

of their D&A (39% global)

Level of trust in using D&A

53% 34% 34%

Analyzing branding via social media

Driving strategy and change

Aiding with maintenance and services

Improving financial reporting

Developing new products and

services

Analyzing our existing customers

Top uses of D&ACanada

62% 58% 57% 57% 55% 55%

to analyze how products are used

41%

Driving strategy and change

Developing new products and

services

Driving process and cost efficiency

Managing risk Finding new customers

44% 44% 43% 43% 43%

Global

“ The true value from digital comes from the intersection of data, customer, and experience across silos, then simplifying and helping everyone within the organization to see the potential.”

Brian Miske Chief Marketing Officer KPMG in Canada

252016 Canadian CEO Outlook

© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Security in the cyber ageIt’s impossible to talk about D&A, online strategies, and cutting-edge technologies without addressing the digital elephant in the room: cyber security.

Canadian CEOs exhibit a heightened sense of confidence (or perhaps unawareness) when it comes to cyber security. Eighty-seven percent say they are somewhat prepared for a cyber attack compared to 69 percent globally; and only a quarter perceive it as a top risk, compared to 30 percent of global CEOs.

“Things are certainly different here in Canada compared to Europe or the US when it comes to the perception of cyber risk, and that comes down primarily to legislation,” explains Paul W. Hanley, National Cyber Security Leader, KPMG in Canada.

That legislation includes data breach notification laws and privacy acts which are applicable within countries in Europe, and have motivated CEOs therein to enhance their focus on cyber defenses. Canada has some controls in place, but not to the extent of its international colleagues.

“If you look at the reason Canadian CEOs may be feeling comfortable with their cyber capabilities, it is likely the same reason why a lot of hackers feel comfortable with executing cyber crime within Canada. It just comes down to the lack of focus on legislation and litigation,” offers Kevvie Fowler, National Cyber Response Leader, KPMG in Canada.

“ There is this view in Canada that we’re a friendly nation and less likely to be hit than other nations, but that’s just not true.”

Paul W. Hanley National Cyber Security Leader KPMG in Canada

26 The race is on

© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

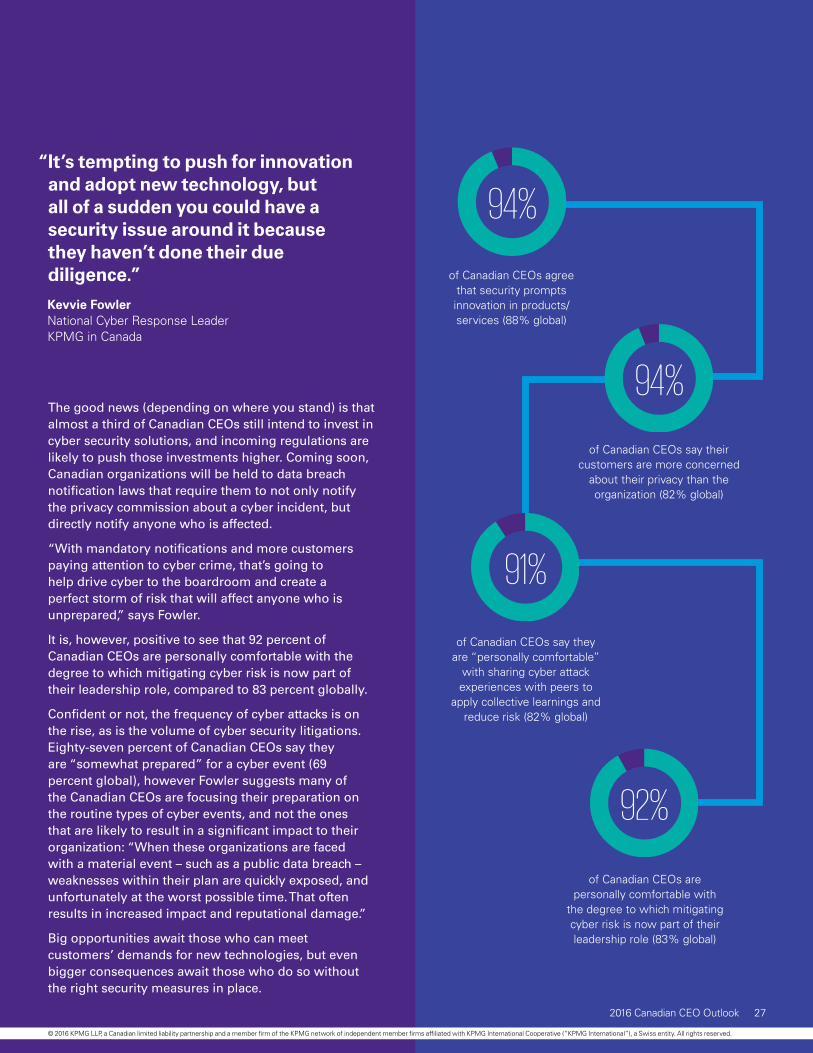

of Canadian CEOs agree that security prompts innovation in products/services (88% global)

of Canadian CEOs say their customers are more concerned

about their privacy than the organization (82% global)

of Canadian CEOs say they are “personally comfortable”

with sharing cyber attack experiences with peers to

apply collective learnings and reduce risk (82% global)

of Canadian CEOs are personally comfortable with

the degree to which mitigating cyber risk is now part of their leadership role (83% global)

94%

91%

94%

92%

The good news (depending on where you stand) is that almost a third of Canadian CEOs still intend to invest in cyber security solutions, and incoming regulations are likely to push those investments higher. Coming soon, Canadian organizations will be held to data breach notification laws that require them to not only notify the privacy commission about a cyber incident, but directly notify anyone who is affected.

“With mandatory notifications and more customers paying attention to cyber crime, that’s going to help drive cyber to the boardroom and create a perfect storm of risk that will affect anyone who is unprepared,” says Fowler.

It is, however, positive to see that 92 percent of Canadian CEOs are personally comfortable with the degree to which mitigating cyber risk is now part of their leadership role, compared to 83 percent globally.

Confident or not, the frequency of cyber attacks is on the rise, as is the volume of cyber security litigations. Eighty-seven percent of Canadian CEOs say they are “somewhat prepared” for a cyber event (69 percent global), however Fowler suggests many of the Canadian CEOs are focusing their preparation on the routine types of cyber events, and not the ones that are likely to result in a significant impact to their organization: “When these organizations are faced with a material event – such as a public data breach – weaknesses within their plan are quickly exposed, and unfortunately at the worst possible time. That often results in increased impact and reputational damage.”

Big opportunities await those who can meet customers’ demands for new technologies, but even bigger consequences await those who do so without the right security measures in place.

“ It’s tempting to push for innovation and adopt new technology, but all of a sudden you could have a security issue around it because they haven’t done their due diligence.”

Kevvie Fowler National Cyber Response Leader KPMG in Canada

272016 Canadian CEO Outlook

© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

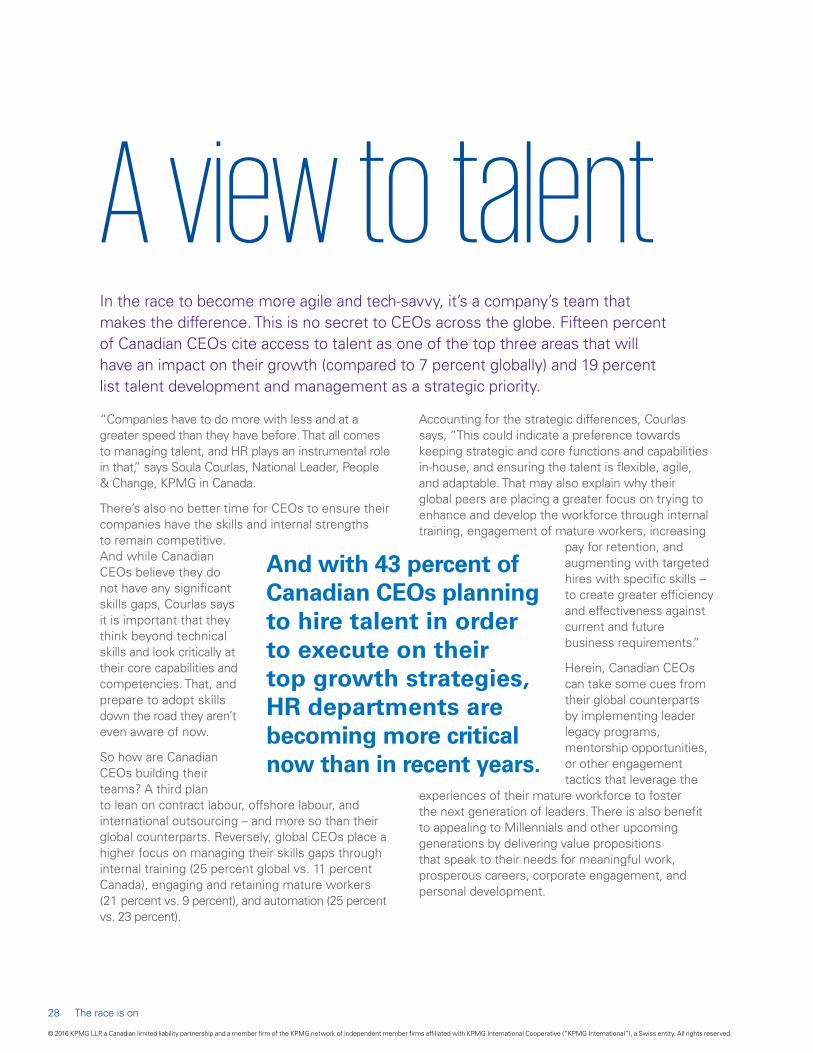

A view to talentIn the race to become more agile and tech-savvy, it’s a company’s team that makes the difference. This is no secret to CEOs across the globe. Fifteen percent of Canadian CEOs cite access to talent as one of the top three areas that will have an impact on their growth (compared to 7 percent globally) and 19 percent list talent development and management as a strategic priority.

“Companies have to do more with less and at a greater speed than they have before. That all comes to managing talent, and HR plays an instrumental role in that,” says Soula Courlas, National Leader, People & Change, KPMG in Canada.

There’s also no better time for CEOs to ensure their companies have the skills and internal strengths to remain competitive. And while Canadian CEOs believe they do not have any significant skills gaps, Courlas says it is important that they think beyond technical skills and look critically at their core capabilities and competencies. That, and prepare to adopt skills down the road they aren’t even aware of now.

So how are Canadian CEOs building their teams? A third plan to lean on contract labour, offshore labour, and international outsourcing – and more so than their global counterparts. Reversely, global CEOs place a higher focus on managing their skills gaps through internal training (25 percent global vs. 11 percent Canada), engaging and retaining mature workers (21 percent vs. 9 percent), and automation (25 percent vs. 23 percent).

Accounting for the strategic differences, Courlas says, “This could indicate a preference towards keeping strategic and core functions and capabilities in-house, and ensuring the talent is flexible, agile, and adaptable. That may also explain why their global peers are placing a greater focus on trying to enhance and develop the workforce through internal training, engagement of mature workers, increasing

pay for retention, and augmenting with targeted hires with specific skills – to create greater efficiency and effectiveness against current and future business requirements.”

Herein, Canadian CEOs can take some cues from their global counterparts by implementing leader legacy programs, mentorship opportunities, or other engagement tactics that leverage the

experiences of their mature workforce to foster the next generation of leaders. There is also benefit to appealing to Millennials and other upcoming generations by delivering value propositions that speak to their needs for meaningful work, prosperous careers, corporate engagement, and personal development.

And with 43 percent of Canadian CEOs planning to hire talent in order to execute on their top growth strategies, HR departments are becoming more critical now than in recent years.

28 The race is on

© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

“ There’s no better time for the role that HR can serve than now, particularly since business leaders are becoming more performance focused than ever and HR is being drawn in as a strategic business partner in driving that performance.”

Soula Courlas National Leader, People & Change KPMG in Canada

292016 Canadian CEO Outlook

© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Financial incentives (e.g. pay, bonuses)

Non-financial incentives (benefits,

vacation time)

Opportunities to learn, develop, and work with leaders

in the field

The chance to innovate and work

in an entrepreneurial or collaborative environment

Non-financial incentives (benefits,

vacation time)

Financial incentives (e.g. pay, bonuses)

Top strategies for attracting talentCanada

47% 42% 40% 37% 36% 35%

Opportunities to learn, develop, and work with leaders

in the field

Non-financial incentives (benefits,

vacation time)

Flexible work assignments

Non-financial incentives (benefits,

vacation time)

Financial incentives (e.g. pay, bonuses)

The chance to innovate and work

in an entrepreneurial or collaborative

environment/promotion opportunities

Top strategies for retaining talent Canada

51% 49% 38% 39% 37% 36%

Global

Global

30 The race is on

© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

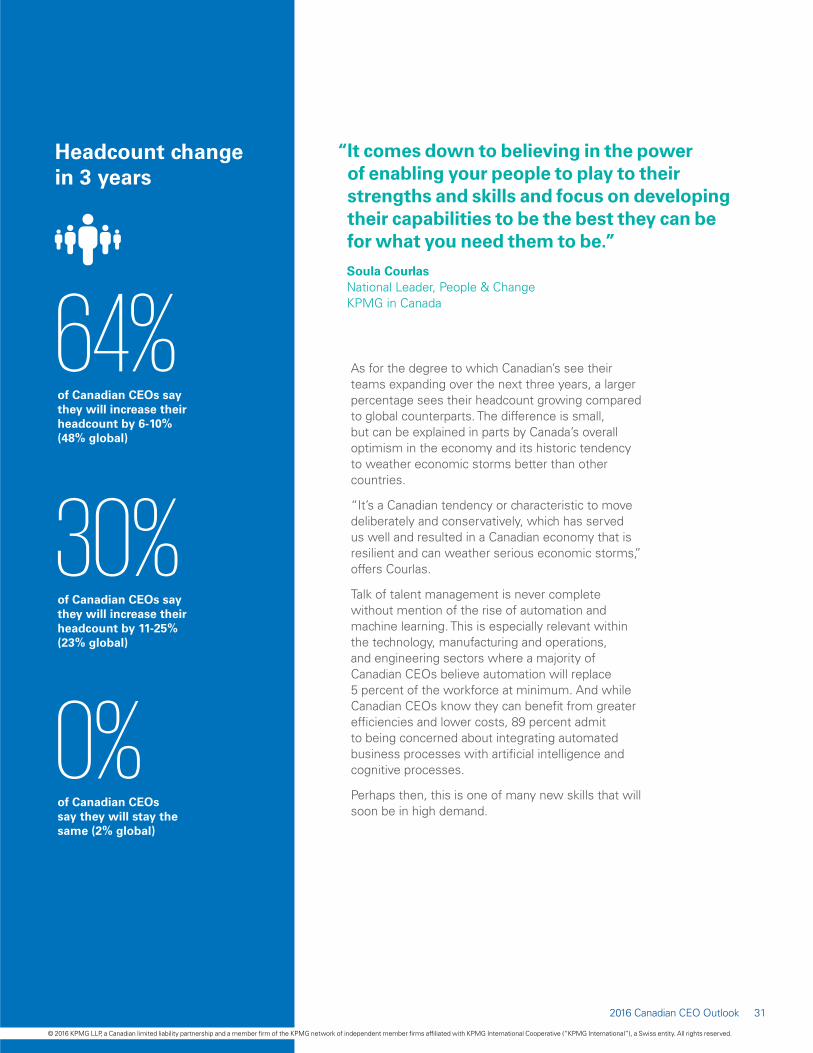

“ It comes down to believing in the power of enabling your people to play to their strengths and skills and focus on developing their capabilities to be the best they can be for what you need them to be.”

Soula Courlas National Leader, People & Change KPMG in Canada

As for the degree to which Canadian’s see their teams expanding over the next three years, a larger percentage sees their headcount growing compared to global counterparts. The difference is small, but can be explained in parts by Canada’s overall optimism in the economy and its historic tendency to weather economic storms better than other countries.

“It’s a Canadian tendency or characteristic to move deliberately and conservatively, which has served us well and resulted in a Canadian economy that is resilient and can weather serious economic storms,” offers Courlas.

Talk of talent management is never complete without mention of the rise of automation and machine learning. This is especially relevant within the technology, manufacturing and operations, and engineering sectors where a majority of Canadian CEOs believe automation will replace 5 percent of the workforce at minimum. And while Canadian CEOs know they can benefit from greater efficiencies and lower costs, 89 percent admit to being concerned about integrating automated business processes with artificial intelligence and cognitive processes.

Perhaps then, this is one of many new skills that will soon be in high demand.

64%of Canadian CEOs say they will increase their headcount by 6-10% (48% global)

30%of Canadian CEOs say they will increase their headcount by 11-25% (23% global)

0%of Canadian CEOs say they will stay the same (2% global)

Headcount change in 3 years

Financial incentives (e.g. pay, bonuses)

Non-financial incentives (benefits,

vacation time)

Opportunities to learn, develop, and work with leaders

in the field

The chance to innovate and work

in an entrepreneurial or collaborative environment

Non-financial incentives (benefits,

vacation time)

Financial incentives (e.g. pay, bonuses)

Top strategies for attracting talentCanada

47% 42% 40% 37% 36% 35%

Opportunities to learn, develop, and work with leaders

in the field

Non-financial incentives (benefits,

vacation time)

Flexible work assignments

Non-financial incentives (benefits,

vacation time)

Financial incentives (e.g. pay, bonuses)

The chance to innovate and work

in an entrepreneurial or collaborative

environment/promotion opportunities

Top strategies for retaining talent Canada

51% 49% 38% 39% 37% 36%

Global

Global

312016 Canadian CEO Outlook

© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

32 The race is on

© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

ConclusionGoing the distance in a global digital market requires a strong team, the willingness to innovate, and having a deep understanding of the customers in play. And while Canadian CEOs can match the pace of their competition, it will take meaningful transformation to pull ahead.

Promisingly, Canadian leaders are confident in their ability to achieve growth over the next few years. However, their areas of focus, strategic priorities, and overall reluctance towards transformation suggest they maintain a more insular view than global CEOs. Here’s where Canadian CEOs can benefit from sharing their global peers’ heightened considerations for external factors like geopolitical influences, new and existing competitors and disruptors, cyber security risks, and the need to make innovation their top priority.

Canadian CEOs can also take greater steps towards addressing their number one concern: customer loyalty. This includes using data and analytics more effectively and delivering tailor-made experiences to customers with the digital tools at their disposal. No doubt, in an age of instant communication and online lifestyles, the onus is on companies to find new and meaningful ways of attracting today’s ever-evolving customer.

The way forward is not without its challenges. Nevertheless, by expanding their global perspective and aligning with the partners and technologies that can give them an edge, Canadian CEOs can build on their domestic successes to claim a greater stake in the world market.

332016 Canadian CEO Outlook

© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

MethodologyThis survey includes perspectives from 53 Canadian CEOs, and is part of a global KPMG study including nearly 1,300 international CEOs. A majority of the Canadian CEOs who responded (87 percent) represent publicly-owned companies and over half of which report revenues between $1.3 billion and $12 billion (28 percent earning $13 billion or more, and 19 percent between $668 million and $1.2 billion). Of the respondents, 79 percent have held their position for a minimum of 6 years and 43 percent of which have been with their company for over 15 years.

The study represents CEOs of companies from a wide range of industries, the top three being banking, energy and utilities, and infrastructure. CEOs from retail, automotive, manufacturing, insurance, telecom, technology, investment management, and life sciences sectors were also represented.

34 The race is on

© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

kpmg.ca/CEOoutlook

The information contained herein is of a general nature and is not intended to address the circumstances of any particular individual or entity. Although we endeavor to provide accurate and timely information, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No one should act on such information without appropriate professional advice after a thorough examination of the particular situation.

© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 13091

The KPMG name and logo are registered trademarks or trademarks of KPMG International.

Contact usBill ThomasCEO, KPMG in CanadaT: 416-777-8144 E: [email protected]

Rob BrouwerManaging Partner, Clients and Markets, KPMG in CanadaT: 416-777-8542 E: [email protected]