20150307 Budget 2015

25

SRD L SRD L SRD L SRD L E E EGAL GAL GAL GAL Union Budget 2015-16 Sanjay Dwivedi Advocate Mumbai – March 07, 2015 SRD L SRD L SRD L SRD L E E EGAL GAL GAL GAL

-

Upload

sanjay-dwivedi -

Category

Documents

-

view

13 -

download

0

description

Presentation on Union Budget 2015

Transcript of 20150307 Budget 2015

SRD LSRD LSRD LSRD LEEEEGALGALGALGAL

Union Budget 2015-16

Sanjay Dwivedi Advocate Mumbai – March 07, 2015

SRD LSRD LSRD LSRD LEEEEGALGALGALGAL

SRD LSRD LSRD LSRD LEEEEGALGALGALGAL

Both Education Cesses exempted

Duty Old rate New rate Remarks

Basic Excise Duty 12% 12.5%

Education Cess 2% Nil Exempted vide Notification

no. 14/2015-CE

Sec. & Higher Ed.

Cess

1% Nil Exempted vide Notification

no. 15/2015-CE

Total Effective rate 12.36% 12.5%

SRD LSRD LSRD LSRD LEEEEGALGALGALGAL

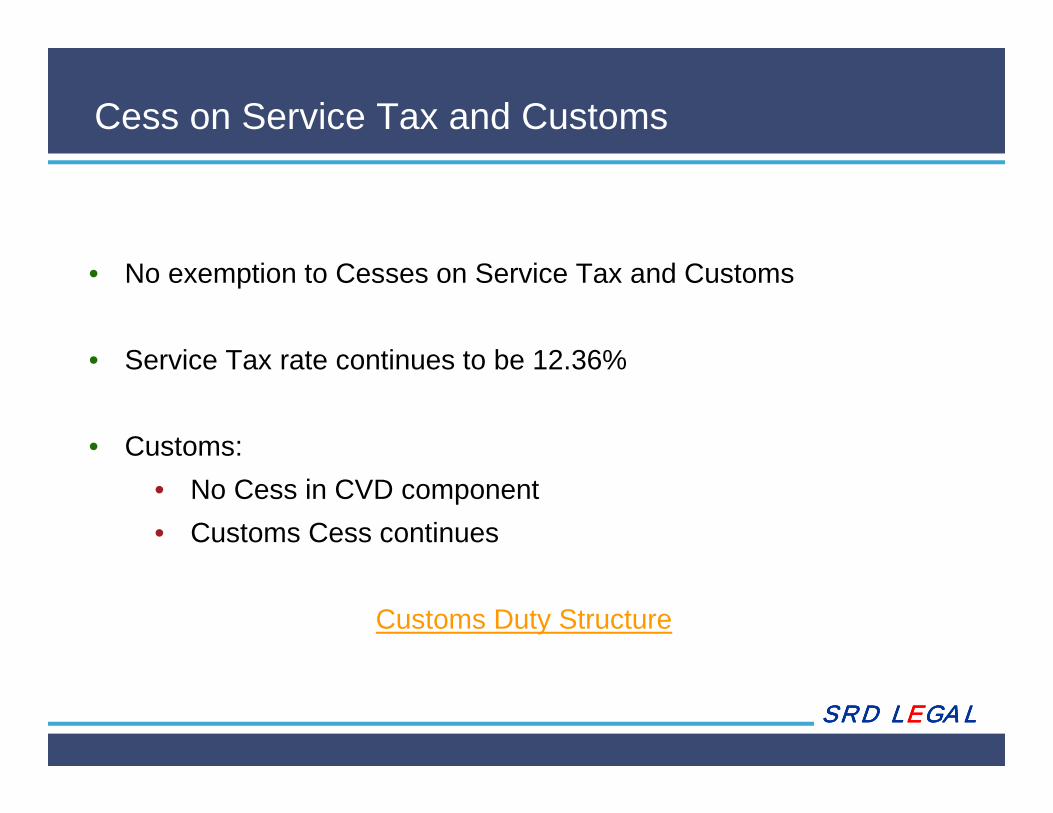

Cess on Service Tax and Customs

• No exemption to Cesses on Service Tax and Customs

• Service Tax rate continues to be 12.36%

• Customs:

• No Cess in CVD component

• Customs Cess continues

Customs Duty Structure

SRD LSRD LSRD LSRD LEEEEGALGALGALGAL

Issues awaiting clarification

• Credit balance of Cess (P.L.A. and Cenvat Credit a/c)

• Fresh credit of cess on old stock being received

• Method of payment of duty on removal of goods as such [rule 3(5)]

• Receipt and removal of goods under rule 16

SRD LSRD LSRD LSRD LEEEEGALGALGALGAL

Cenvat Credit – Time Limit extended

• Cenvat Credit can be availed within one year from the date of the invoice/ Bill of Entry etc.

• This applies to credits on ‘inputs’ as well as ‘input services’

• Does not apply to credit of ‘Capital Goods’

(w.e.f. 01/03/2015)

SRD LSRD LSRD LSRD LEEEEGALGALGALGAL

Cenvat Credit – Direct delivery to Job-worker

Credit available immediately on receipt of goods by job-worker

Proof:

• Acknowledgment by the job-worker • Entry in records of the job-worker • Transport documents

SRD LSRD LSRD LSRD LEEEEGALGALGALGAL

Invoicing

• When the buyer and the consignee are different we must mention details of the both in our invoice.

• Importer sending goods directly from port (or other place of import) to the buyer’s premises – should put such remark on his invoice.

SRD LSRD LSRD LSRD LEEEEGALGALGALGAL

Digital Signature

• Invoices can be digitally signed but a hard copy of the ‘duplicate copy’ attested by the manufacturer must accompany the goods.

• Electronic Maintenance of records is permissible – but each page must be digitally signed.

• This applies to C. Excise as well as Service Tax

SRD LSRD LSRD LSRD LEEEEGALGALGALGAL

Recovery of Wrong Credits

• Credit taken but not utilized

• Credit recoverable;

• Interest not payable

• Penalty to be imposed

• Credit taken and utilized: Credit + Interest + Penalty

• Utilization sequence:

� Opening Balance

� Admissible Credits

� Inadmissible Credits

SRD LSRD LSRD LSRD LEEEEGALGALGALGAL

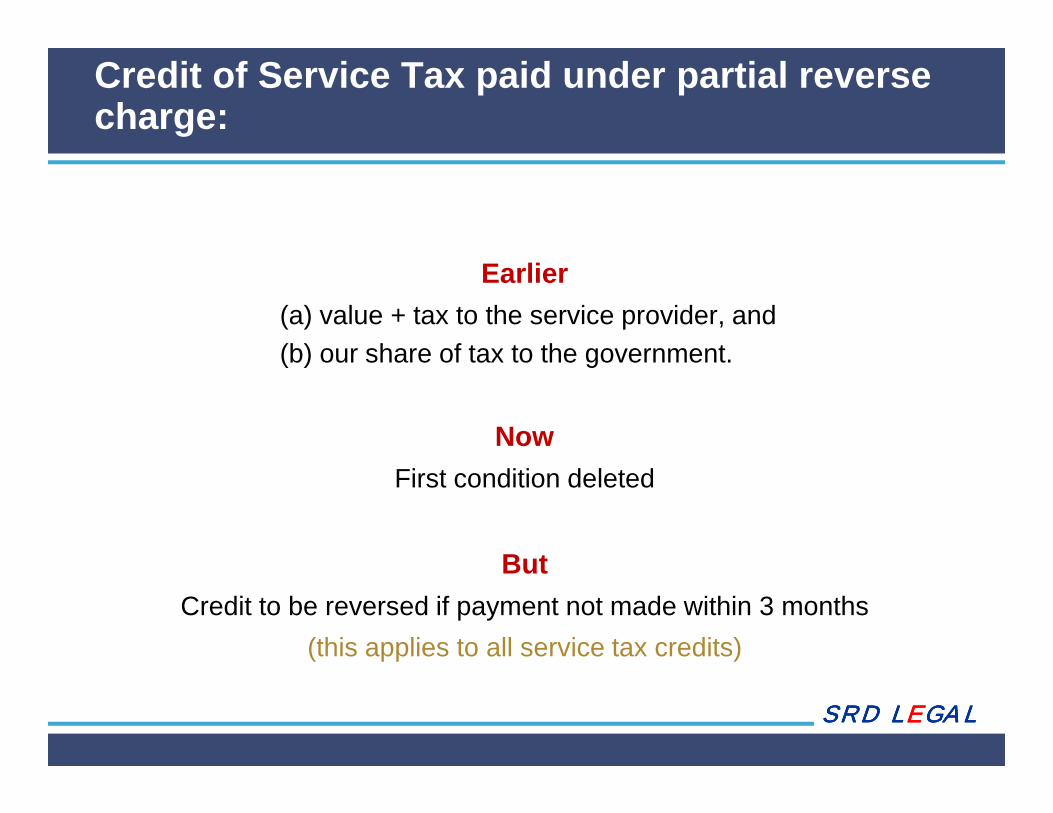

Credit of Service Tax paid under partial reverse charge:

Earlier (a) value + tax to the service provider, and (b) our share of tax to the government.

Now First condition deleted

But

Credit to be reversed if payment not made within 3 months

(this applies to all service tax credits)

SRD LSRD LSRD LSRD LEEEEGALGALGALGAL

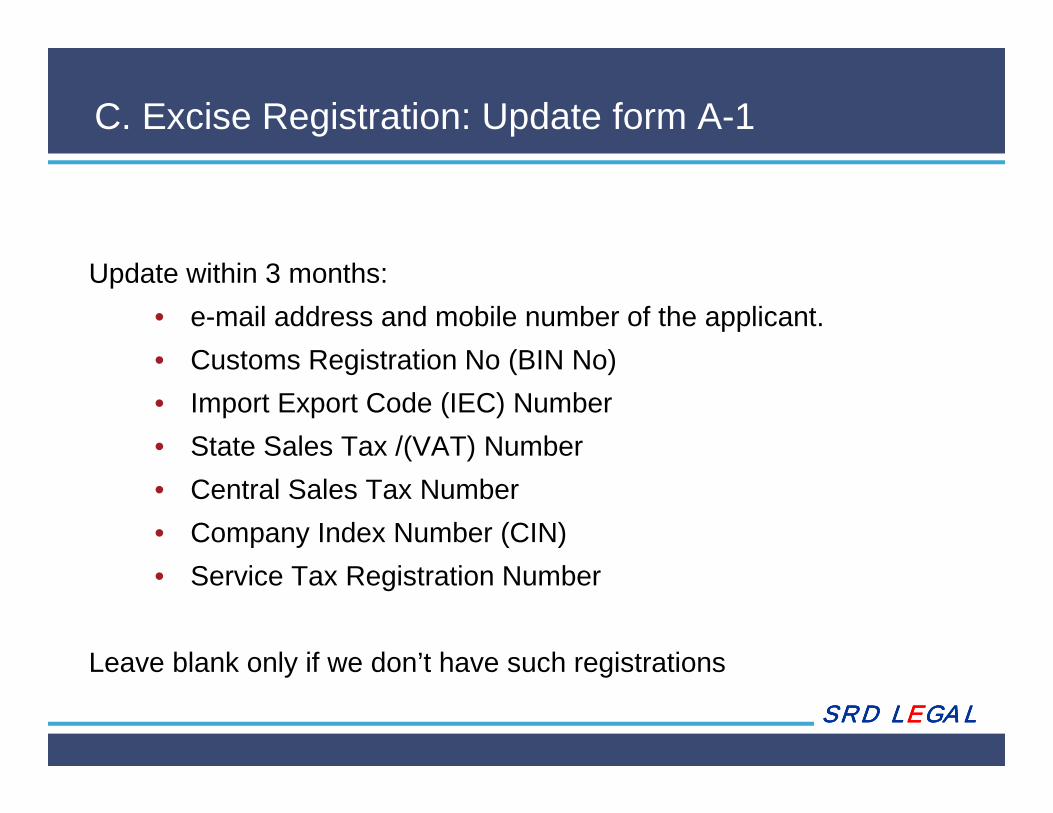

C. Excise Registration: Update form A-1

Update within 3 months:

• e-mail address and mobile number of the applicant.

• Customs Registration No (BIN No)

• Import Export Code (IEC) Number

• State Sales Tax /(VAT) Number

• Central Sales Tax Number

• Company Index Number (CIN)

• Service Tax Registration Number

Leave blank only if we don’t have such registrations

SRD LSRD LSRD LSRD LEEEEGALGALGALGAL

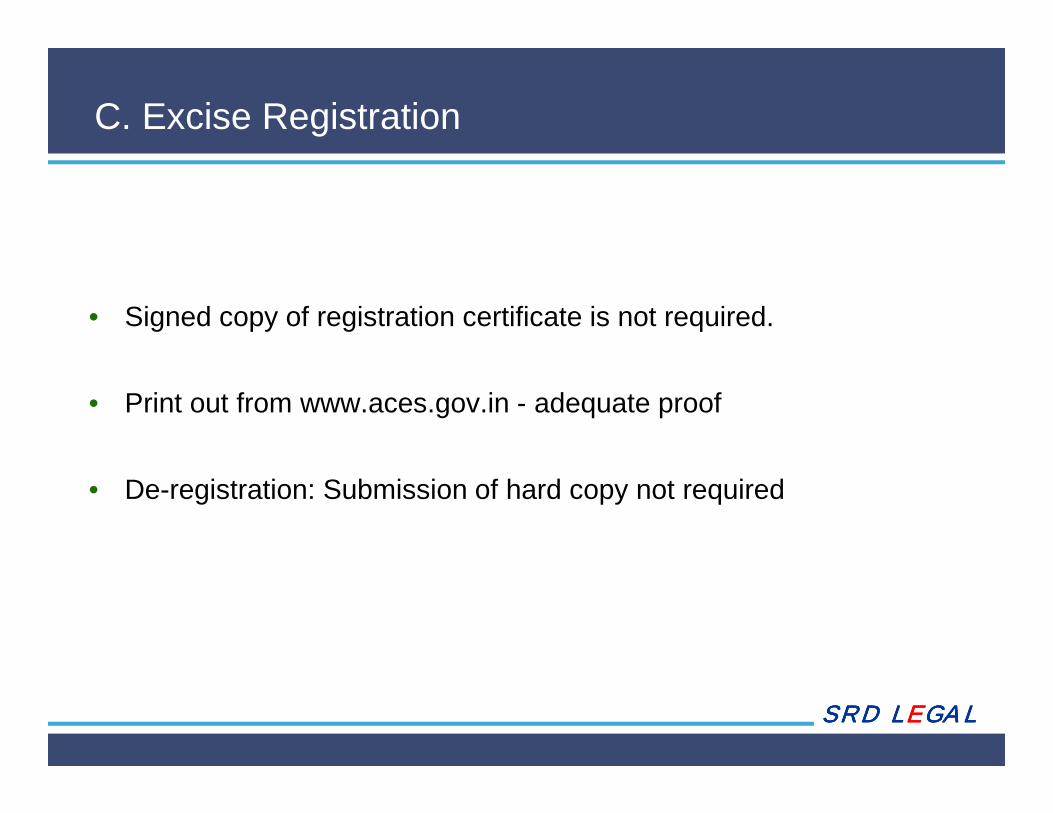

C. Excise Registration

• Signed copy of registration certificate is not required.

• Print out from www.aces.gov.in - adequate proof

• De-registration: Submission of hard copy not required

SRD LSRD LSRD LSRD LEEEEGALGALGALGAL

Penal Provisions-1 (after enactment of bill)

No fraud, collusion, suppression of facts

• Penalty equal to 10% of the duty or 5000 (whichever is higher)

• If duty + interest paid before SCN or within 30 days of SCN – no penalty – all proceedings deemed to be concluded.

• If duty + Interest + Penalty is paid within 30 days of order – penalty = 25% of penalty imposed [i.e. 2.5%].

(Nil ----- 2.5% ----- 10%)

SRD LSRD LSRD LSRD LEEEEGALGALGALGAL

Penal Provisions-2 (after enactment of bill)

Evasion by fraud, or collusion or suppression of facts etc.

• Penalty equal to duty

• If Duty + interest + penalty paid within 30 days of SCN – penalty = 15% of duty – all proceedings deemed to be concluded.

• If Duty + interest + penalty paid within 30 days of order – penalty = 25% of duty – all proceedings deemed to be concluded.

(15% ------ 25% ------ 100%)

SRD LSRD LSRD LSRD LEEEEGALGALGALGAL

Penalty – Late filing of C. Excise returns

Rs. 100/- per day

Maximum: Rs. 20,000/-

SRD LSRD LSRD LSRD LEEEEGALGALGALGAL

Supply of goods to SEZ units/ developers

• Rebate not available (rule 18 of C. Excise Rules, 2002)

• Refund of accumulated Cenvat Credit – Not available (rule 5 of Cenvat Credit Rules, 2004)

SRD LSRD LSRD LSRD LEEEEGALGALGALGAL

SERVICE TAX

SRD LSRD LSRD LSRD LEEEEGALGALGALGAL

Services by Government

All services provided by government to Business Entity have become taxable: (earlier only ‘support services’ + following 3 were taxable)

• Normal charge in case of following 4 services: • Dept of Post (speed post, express parcel, life insurance,

agency) • Aircraft/ vessel • Transport of Passengers • Renting of immovable property

• Reverse Charge for all other services (the Business Entity receiving the service, would take registration, pay tax, file returns etc.)

SRD LSRD LSRD LSRD LEEEEGALGALGALGAL

Exemptions withdrawn w.e.f. 01st April 2015

Construction Industry (entries deleted from 25/2012-ST)

Sr. 12

(a) a civil structure or any other original works meant predominantly for use other than for commerce, industry, or any other business or profession;

(c) a structure meant predominantly for use as (i) an educational, (ii) a clinical, or (iii) an art or cultural establishment;

(f) a residential complex predominantly meant for self-use or the use of their employees or other persons ……

SRD LSRD LSRD LSRD LEEEEGALGALGALGAL

Exemptions withdrawn w.e.f. 01st April 2015

Sr. 14(a) (amended)

Exemption withdrawn on services by way of construction, erection, commissioning, or installation of original works pertaining to airport or port

Exemption continues to railways, including monorail or metro

SRD LSRD LSRD LSRD LEEEEGALGALGALGAL

Exemption Exemptions withdrawn w.e.f. 01st April 2015

Job-work in case of ‘alcoholic liquors for human consumption’ – no more exempted [sr 30 (c) of 25/2012-ST amended]

SRD LSRD LSRD LSRD LEEEEGALGALGALGAL

Fresh Exemption granted (w.e.f. 01/04/2015)

• Operation of common effluent treatment plant (sr. 43)

• Services by way of pre-conditioning, pre-cooling, ripening, waxing, retail packing, labelling of fruits and vegetables which do not change or alter the essential characteristics of the said fruits or vegetables; (sr. 44)

SRD LSRD LSRD LSRD LEEEEGALGALGALGAL

GTA – Abatement reduced

• Abatement is reduced from 75% to 70%

• W.e.f. 01/04/2015 – Tax payable on 30% of the bill amount

SRD LSRD LSRD LSRD LEEEEGALGALGALGAL

Reverse Charge Mechanism (w.e.f. 01/04/2015)

100% tax payable by service receiver in case of

� Manpower Supply; and

� Security Service

• If service receiver is a body corporate; and

• Service provider is NOT a body corporate

[Earlier the liability was shared as 75% & 25%]

SRD LSRD LSRD LSRD LEEEEGALGALGALGAL

Thank You Sanjay Dwivedi Advocate 9320 456 555 [email protected]

SRD LSRD LSRD LSRD LEEEEGALGALGALGAL

Advocates & Consultants

C. Excise • Service Tax • Customs • Foreign Trade