2015.01.21 ACG cup (M&A case competition)

23

RADY ADVISORS TM . OLIVER BINZ | ALLISON NOEL | LAUREN VOLLON | SARAH FELDMAN JANUARY 21, 2015 MEDIACO INVESTMENT OPPORTUNITY

-

Upload

allisonnoel -

Category

Business

-

view

230 -

download

8

Transcript of 2015.01.21 ACG cup (M&A case competition)

RADY ADVISORSTM.

OLIVER BINZ | ALLISON NOEL | LAUREN VOLLON | SARAH FELDMAN JANUARY 21, 2015

MEDIACO INVESTMENT OPPORTUNITY

COMPANY OVERVIEW

Publicly-traded with two reporting units, MediaCo and ApparelCo

Market cap of $550M

Publishes periodicals; operates a website and a TV production company

Slow or no organic growth

Develops, sources, markets, and distributes fashion-forward apparel and accessories

Growing, but margins low due to high SG&A costs

ParentCo

MediaCo

ApparelCo

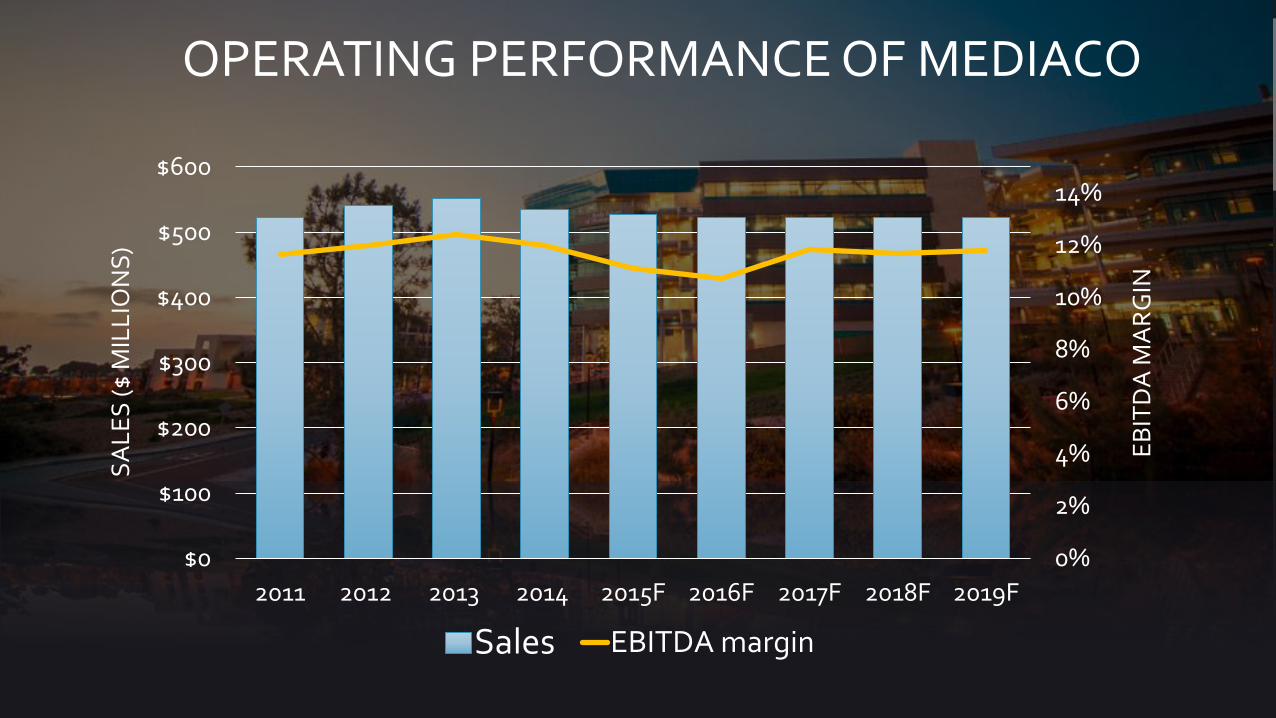

OPERATING PERFORMANCE OF MEDIACO

0%

2%

4%

6%

8%

10%

12%

14%

$0

$100

$200

$300

$400

$500

$600

2011 2012 2013 2014 2015F 2016F 2017F 2018F 2019F

EB

ITD

A M

AR

GIN

SA

LE

S ($

MIL

LIO

NS

)

Sales EBITDA margin

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

$0

$50

$100

$150

$200

$250

$300

$350

2011 2012 2013 2014 2015F 2016F 2017F 2018F 2019F

EB

ITD

A M

AR

GIN

SA

LE

S ($

MIL

LIO

NS

)

Sales EBITDA margin

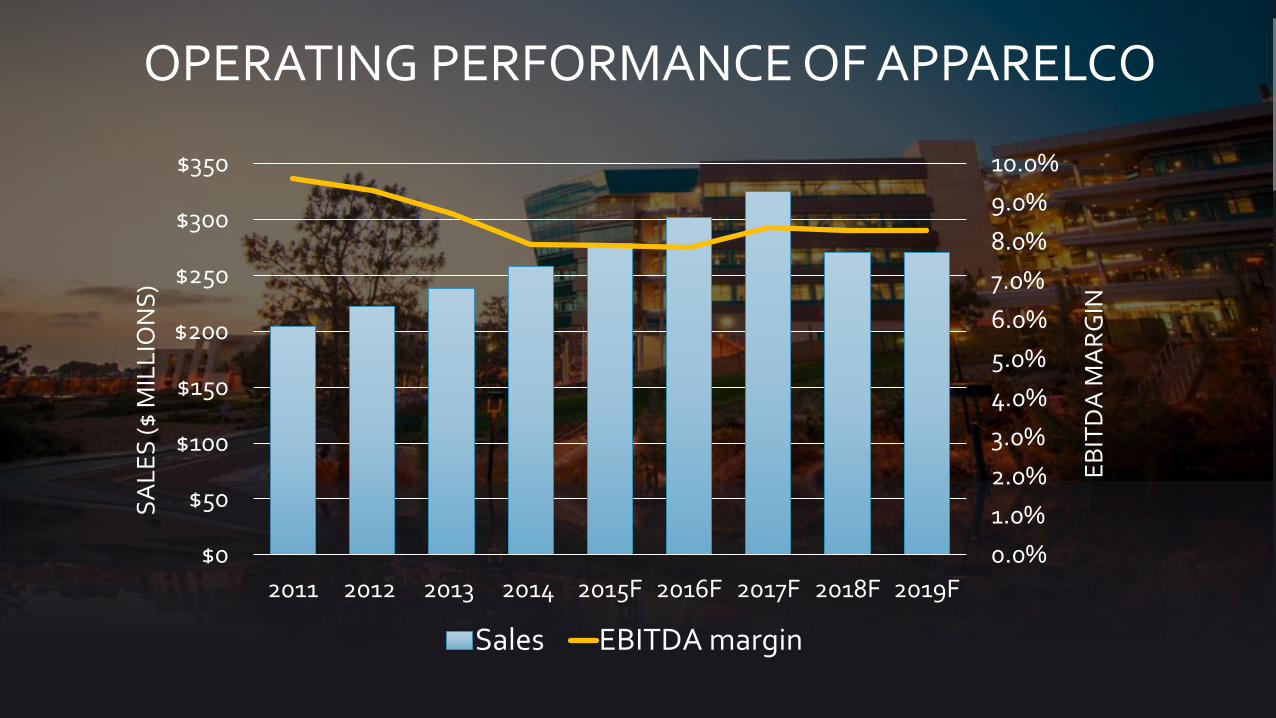

OPERATING PERFORMANCE OF APPARELCO

INDUSTRY OVERVIEW

Media

• Recent consolidation of content publishers

• Little to no revenue growth for the foreseeable future

• Print and TV performing in line with general markets

Fashion

• Highly cyclical

• Comparable company trading multiples cover a wide range

• Growth expected to be in mid-to-low single digits

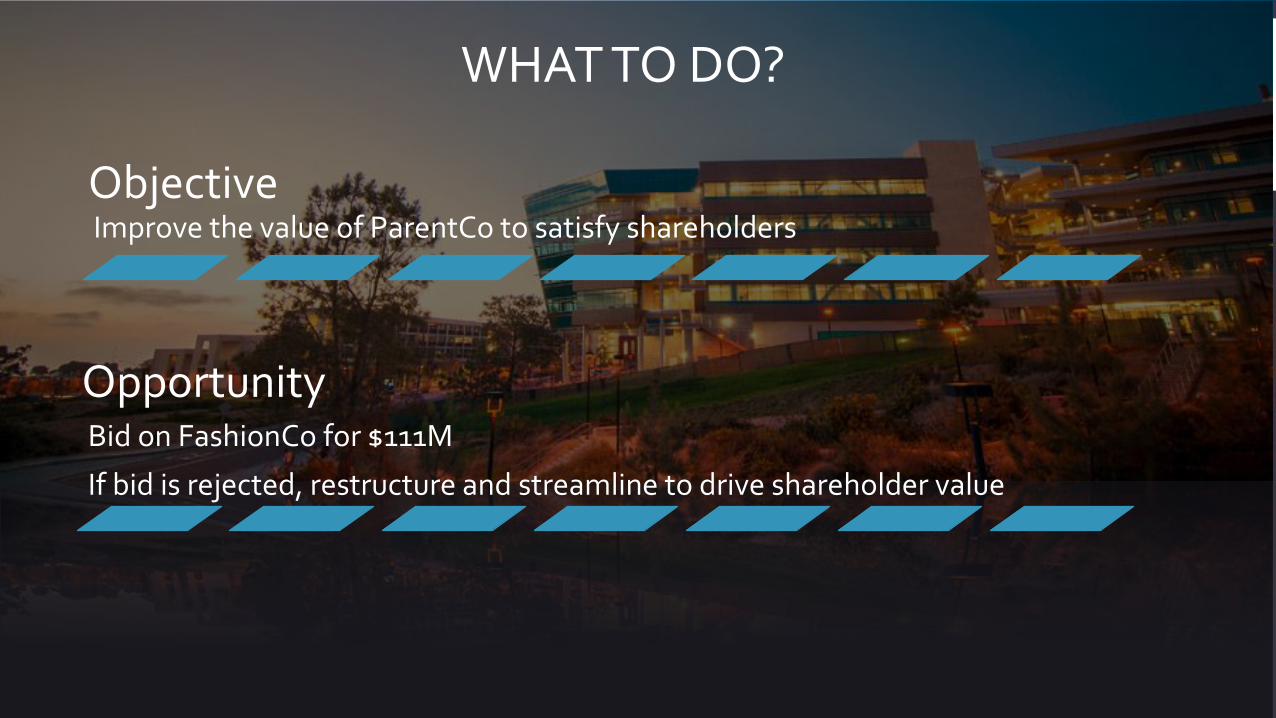

WHAT TO DO?

Improve the value of ParentCo to satisfy shareholdersObjective

OpportunityBid on FashionCo for $111M

If bid is rejected, restructure and streamline to drive shareholder value

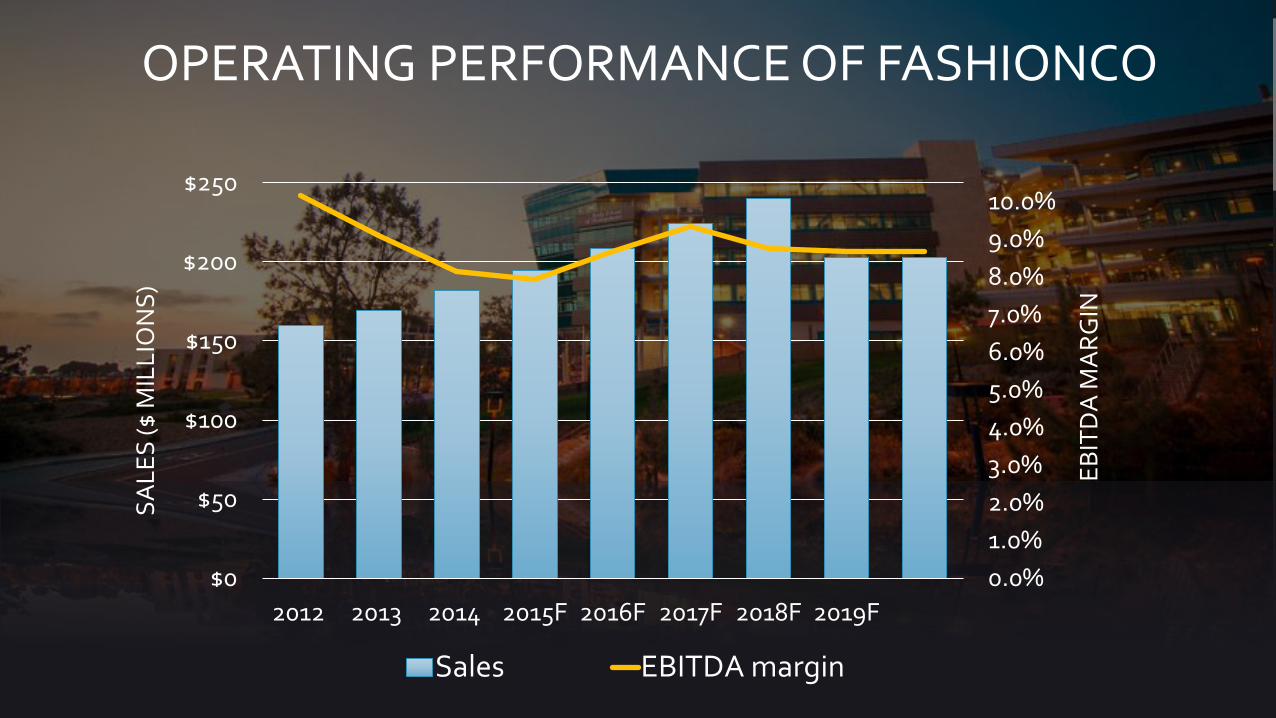

OPERATING PERFORMANCE OF FASHIONCO

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

$0

$50

$100

$150

$200

$250

2012 2013 2014 2015F 2016F 2017F 2018F 2019F

EB

ITD

A M

AR

GIN

SA

LE

S ($

MIL

LIO

NS

)

Sales EBITDA margin

NON-FINANCIAL CONSIDERATIONS

• Balancing interests of all shareholders and board members

• Protecting brand and company images

• Short-term and long-term stability

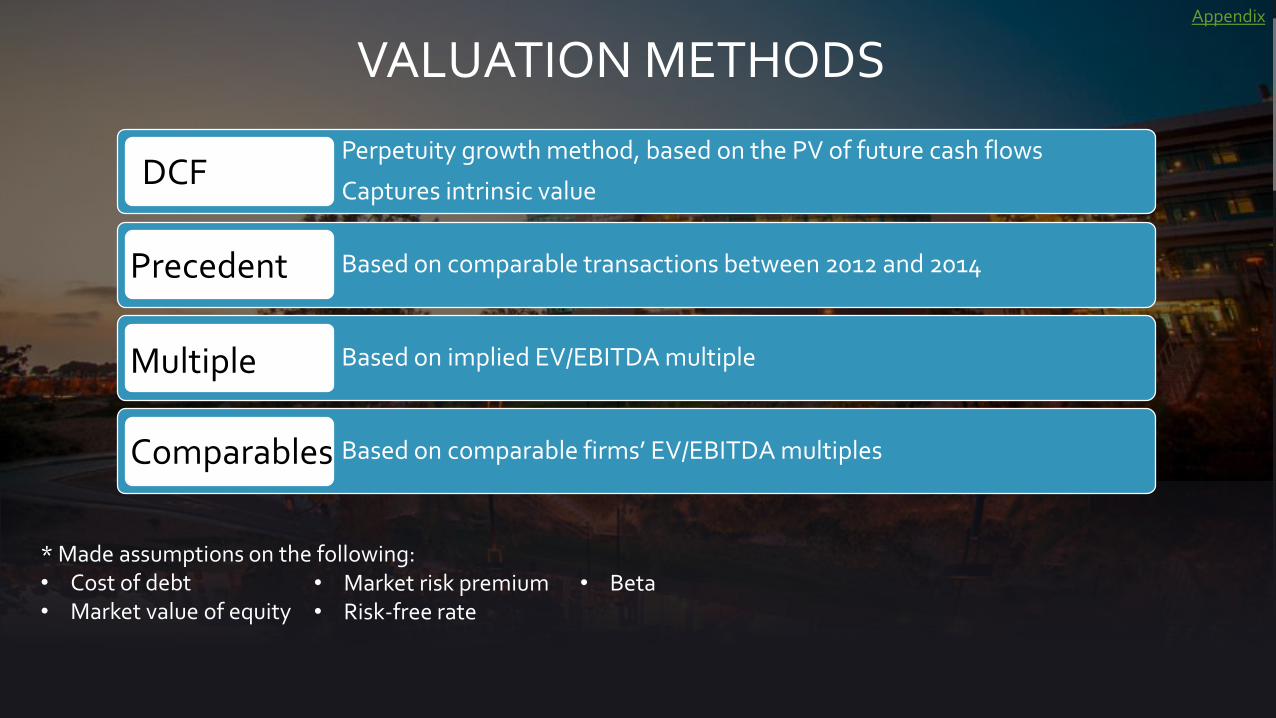

VALUATION METHODS

Perpetuity growth method, based on the PV of future cash flows

Captures intrinsic value

Based on comparable transactions between 2012 and 2014

Based on implied EV/EBITDA multiple

Based on comparable firms’ EV/EBITDA multiples

DCF

Precedent

Comparables

Multiple

Appendix

* Made assumptions on the following:• Cost of debt• Market value of equity

• Market risk premium• Risk-free rate

• Beta

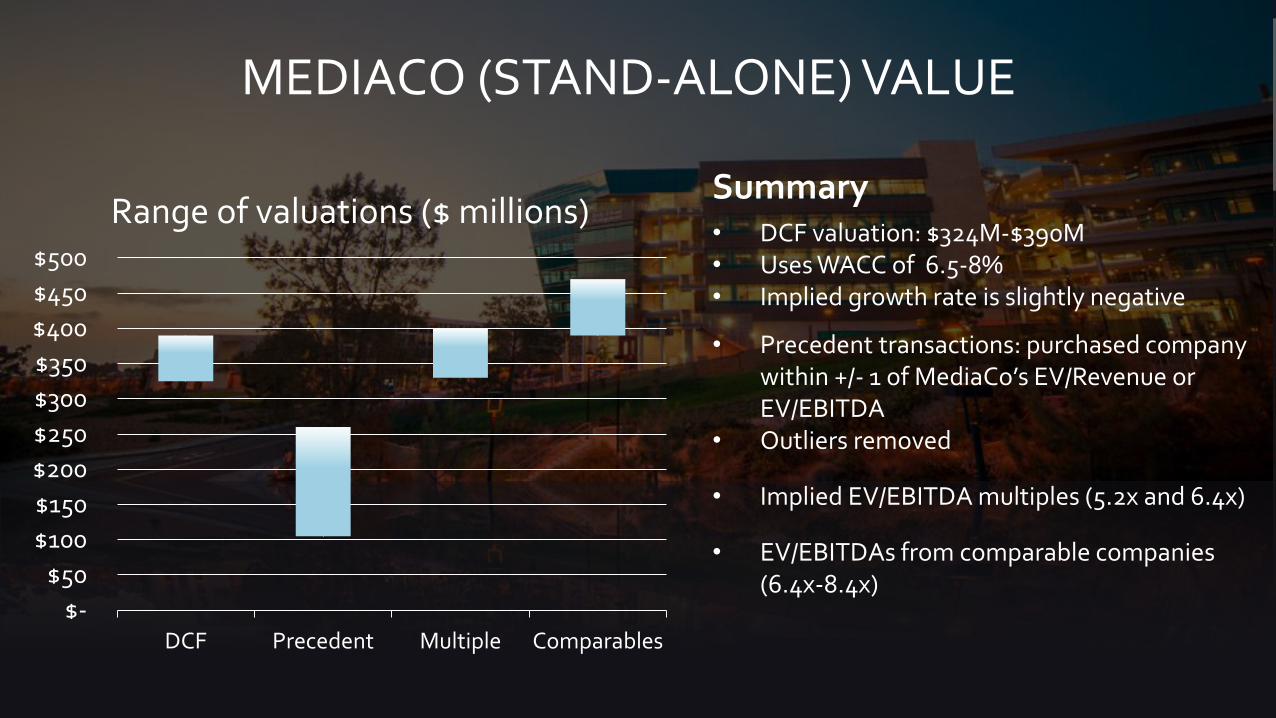

MEDIACO (STAND-ALONE) VALUE

$-

$50

$100

$150

$200

$250

$300

$350

$400

$450

$500

DCF Precedent Multiple Comparables

Range of valuations ($ millions)Summary• DCF valuation: $324M-$390M• Uses WACC of 6.5-8%• Implied growth rate is slightly negative

• Precedent transactions: purchased company within +/- 1 of MediaCo’s EV/Revenue or EV/EBITDA

• Outliers removed

• Implied EV/EBITDA multiples (5.2x and 6.4x)

• EV/EBITDAs from comparable companies (6.4x-8.4x)

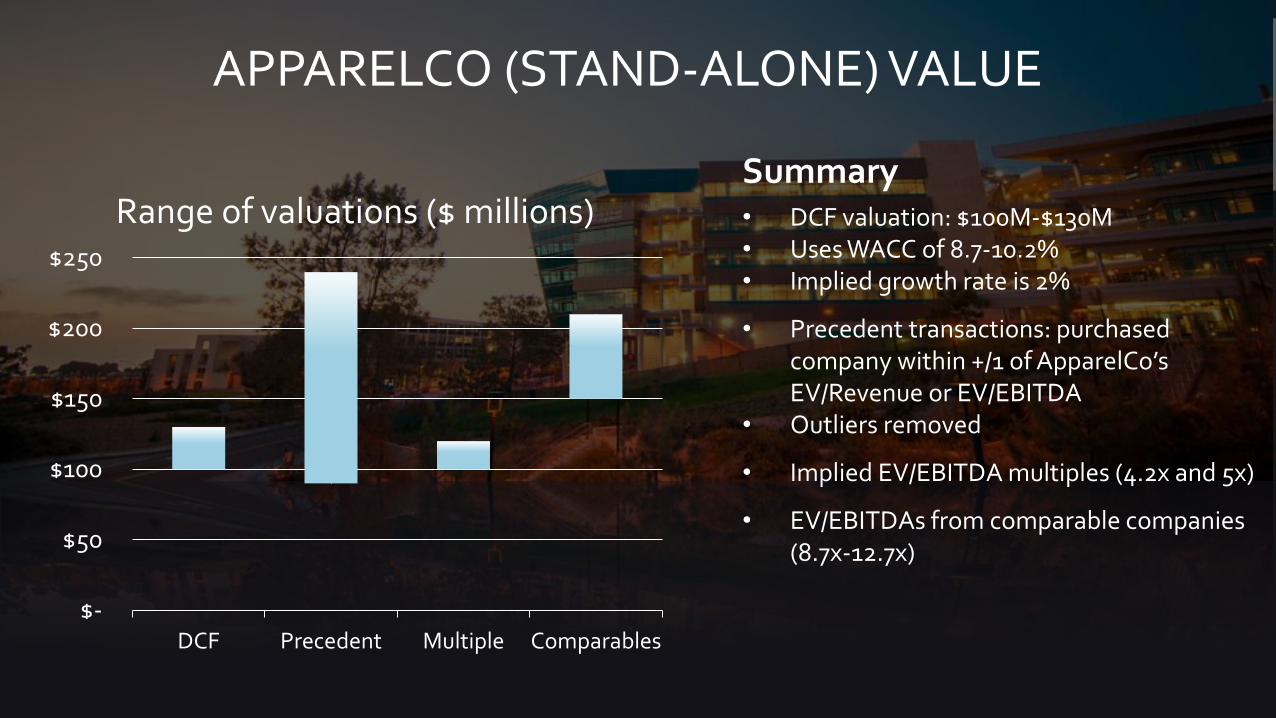

APPARELCO (STAND-ALONE) VALUE

$-

$50

$100

$150

$200

$250

DCF Precedent Multiple Comparables

Range of valuations ($ millions)Summary• DCF valuation: $100M-$130M• Uses WACC of 8.7-10.2%• Implied growth rate is 2%

• Precedent transactions: purchased company within +/1 of ApparelCo’sEV/Revenue or EV/EBITDA

• Outliers removed

• Implied EV/EBITDA multiples (4.2x and 5x)

• EV/EBITDAs from comparable companies (8.7x-12.7x)

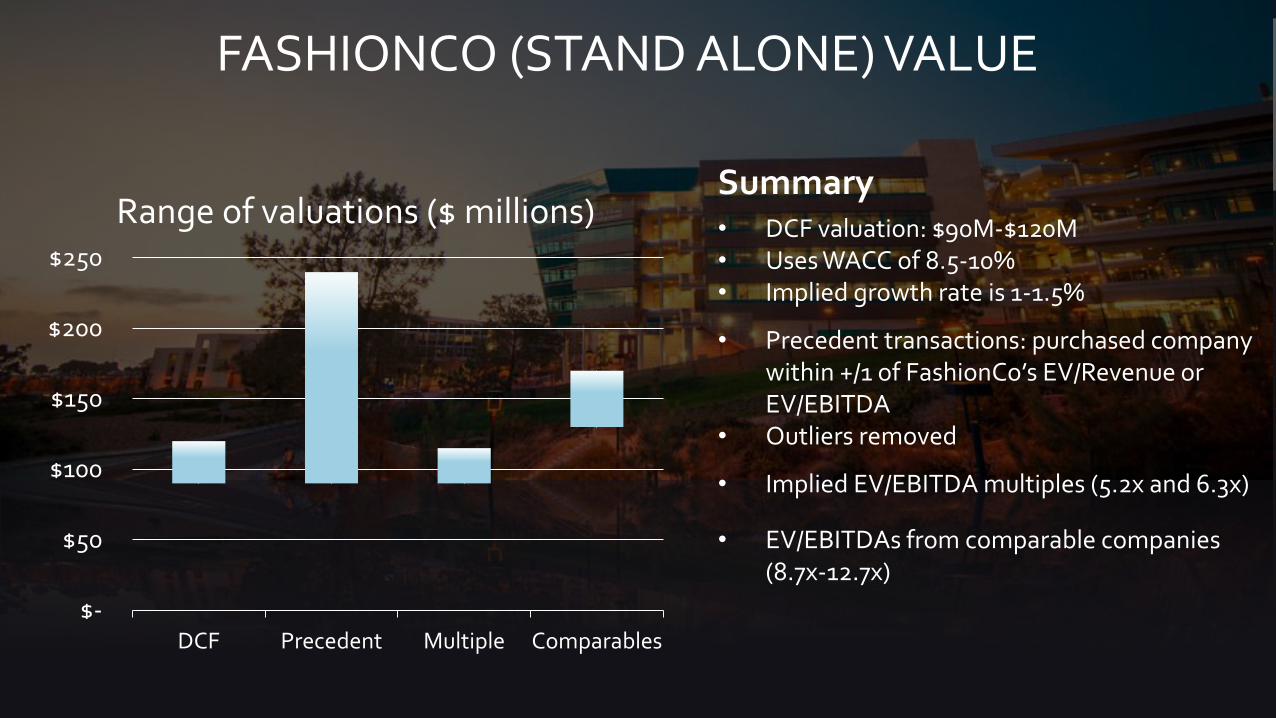

FASHIONCO (STAND ALONE) VALUE

$-

$50

$100

$150

$200

$250

DCF Precedent Multiple Comparables

Range of valuations ($ millions)Summary• DCF valuation: $90M-$120M• Uses WACC of 8.5-10%• Implied growth rate is 1-1.5%

• Precedent transactions: purchased company within +/1 of FashionCo’s EV/Revenue or EV/EBITDA

• Outliers removed

• Implied EV/EBITDA multiples (5.2x and 6.3x)

• EV/EBITDAs from comparable companies (8.7x-12.7x)

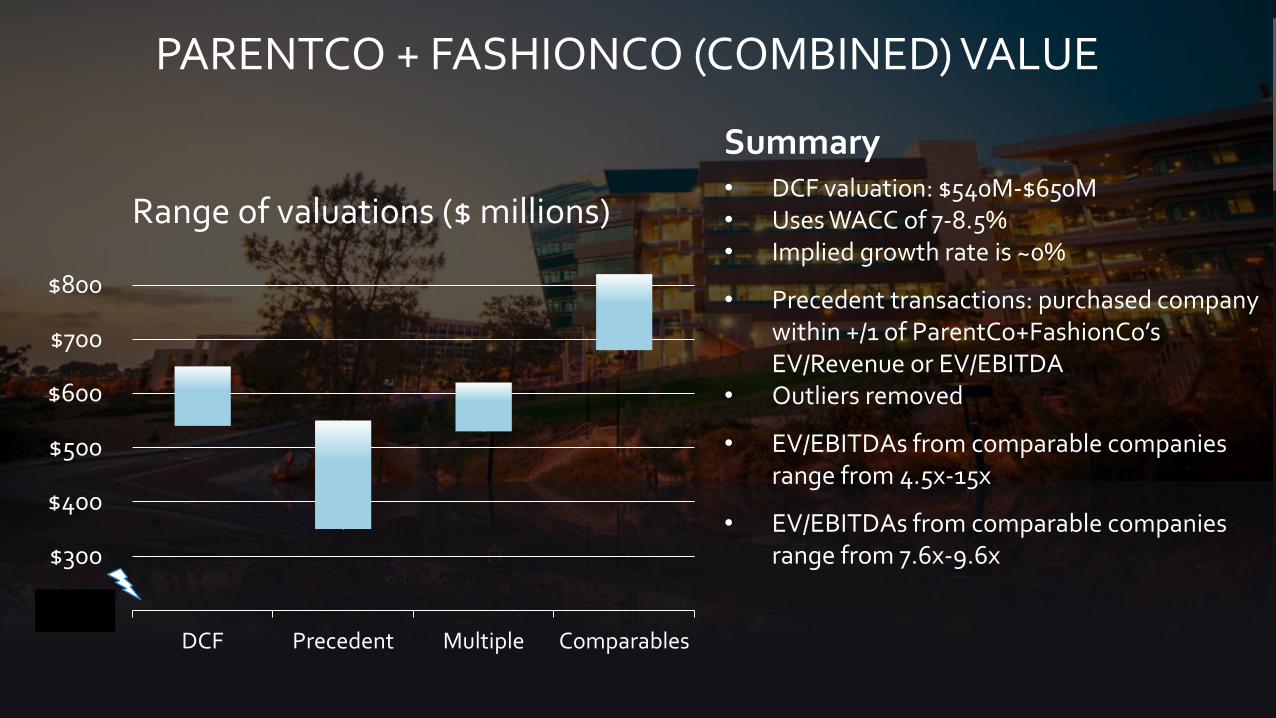

PARENTCO + FASHIONCO (COMBINED) VALUE

$200

$300

$400

$500

$600

$700

$800

DCF Precedent Multiple Comparables

Range of valuations ($ millions)

Summary• DCF valuation: $540M-$650M• Uses WACC of 7-8.5%• Implied growth rate is ~0%

• Precedent transactions: purchased company within +/1 of ParentCo+FashionCo’sEV/Revenue or EV/EBITDA

• Outliers removed

• EV/EBITDAs from comparable companies range from 4.5x-15x

• EV/EBITDAs from comparable companies range from 7.6x-9.6x

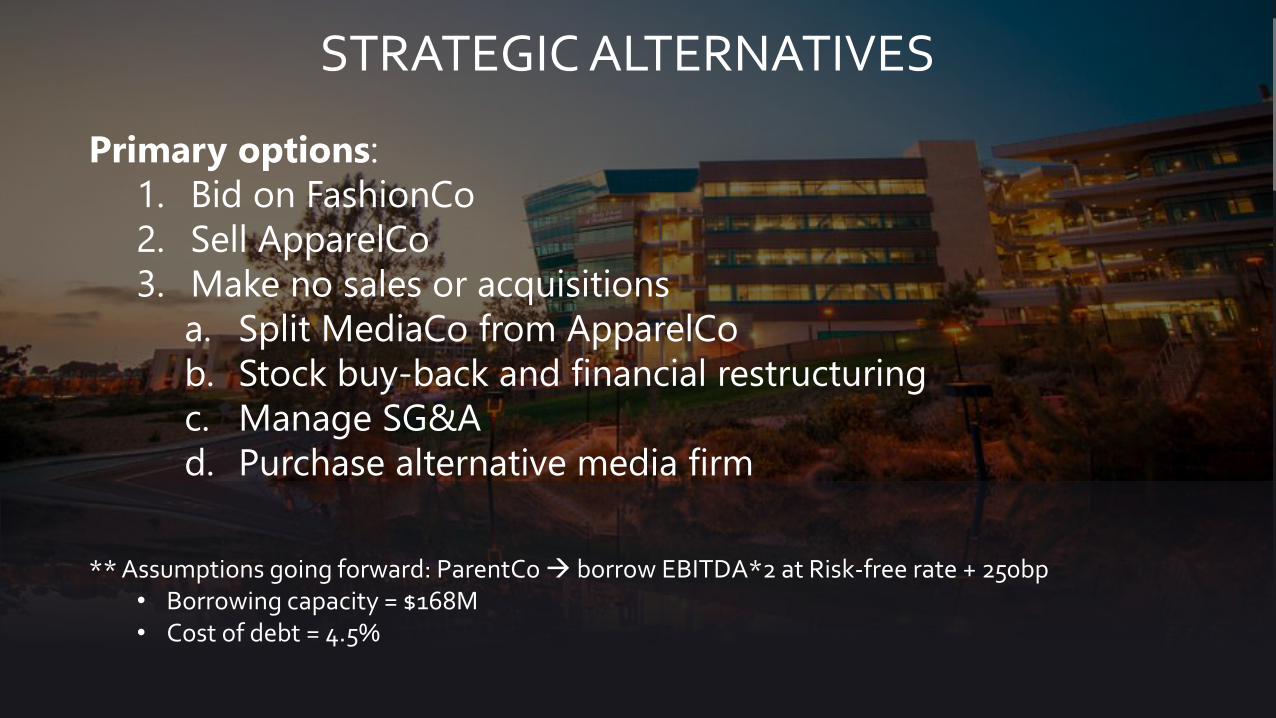

STRATEGIC ALTERNATIVES

Primary options:

1. Bid on FashionCo

2. Sell ApparelCo

3. Make no sales or acquisitions

a. Split MediaCo from ApparelCo

b. Stock buy-back and financial restructuring

c. Manage SG&A

d. Purchase alternative media firm

** Assumptions going forward: ParentCo borrow EBITDA*2 at Risk-free rate + 250bp• Borrowing capacity = $168M• Cost of debt = 4.5%

STRATEGIC ALTERNATIVES

Option 1: Bid on FashionCo for $111M

• Stand-alone value of FashionCo is $90-$120M • Synergies from merging FashionCo with ApparelCo savings of $2M

annually due to SG&A cost reduction• Discount rate of 9.3% (WACC of combined FashionCo and ApparelCo)• Perpetuity valued at $21M (takeover premium)

* Fair Value of buying FashionCo = at least $111M * Walk-away offer: if higher, could make loss

STRATEGIC ALTERNATIVES

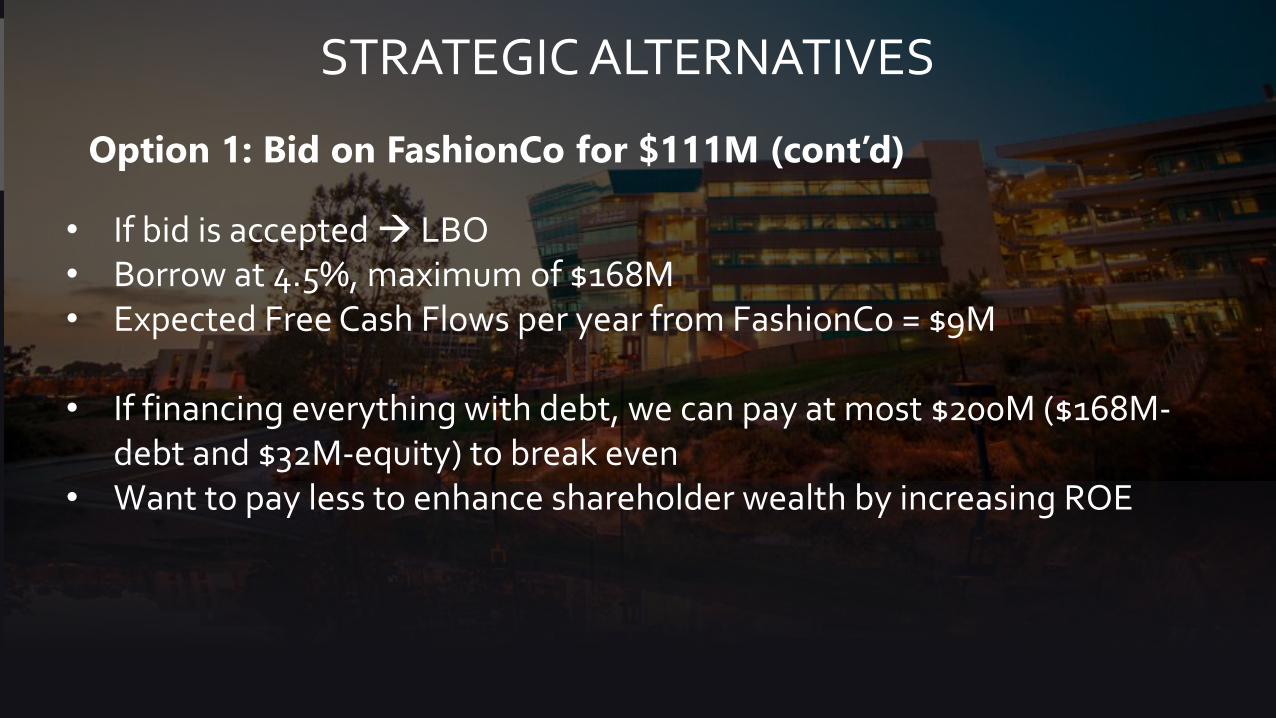

Option 1: Bid on FashionCo for $111M (cont’d)

• If bid is accepted LBO• Borrow at 4.5%, maximum of $168M• Expected Free Cash Flows per year from FashionCo = $9M

• If financing everything with debt, we can pay at most $200M ($168M-debt and $32M-equity) to break even

• Want to pay less to enhance shareholder wealth by increasing ROE

STRATEGIC ALTERNATIVES

Option 2: Sell ApparelCo

• Stand-alone value is $145-$155• Currently under-valued in the market though• Also has grow opportunities in the future• Futhermore, selling would upset the Masterson family!

* Recommendation: keep ApparelCo (ParentCo can increase returns to shareholders in other ways)

STRATEGIC ALTERNATIVES

Option 3: Split ApparelCo and MediaCo

• No synergies between firms*• Set up two separate entities– allocate appropriate share volume to each

shareholder in both firms• Shareholders will be able to diversify efficiently according to their

personal risk preferences

* Merton (1999): Companies shouldn’t diversify their operations when there are no synergies. Shareholders can diversify for idiosyncratic risk more efficiently.

STRATEGIC ALTERNATIVES

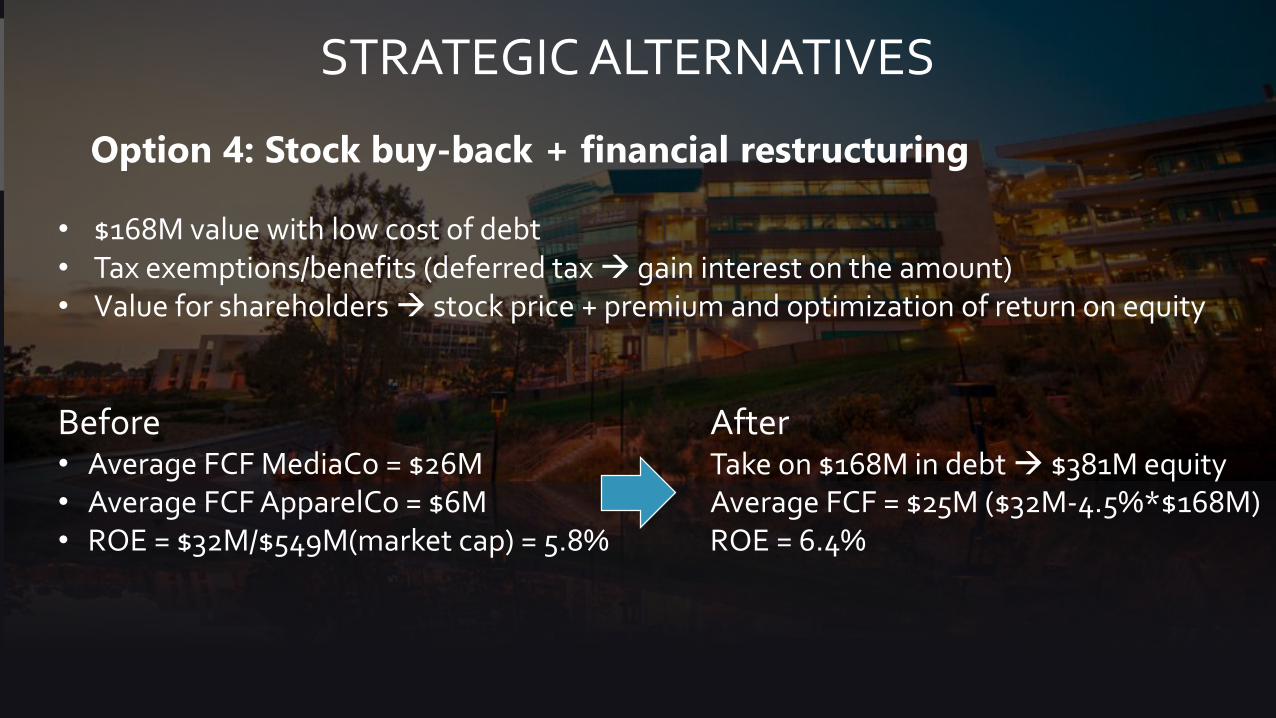

Option 4: Stock buy-back + financial restructuring

• $168M value with low cost of debt• Tax exemptions/benefits (deferred tax gain interest on the amount)• Value for shareholders stock price + premium and optimization of return on equity

Before• Average FCF MediaCo = $26M• Average FCF ApparelCo = $6M• ROE = $32M/$549M(market cap) = 5.8%

AfterTake on $168M in debt $381M equityAverage FCF = $25M ($32M-4.5%*$168M)ROE = 6.4%

STRATEGIC ALTERNATIVES

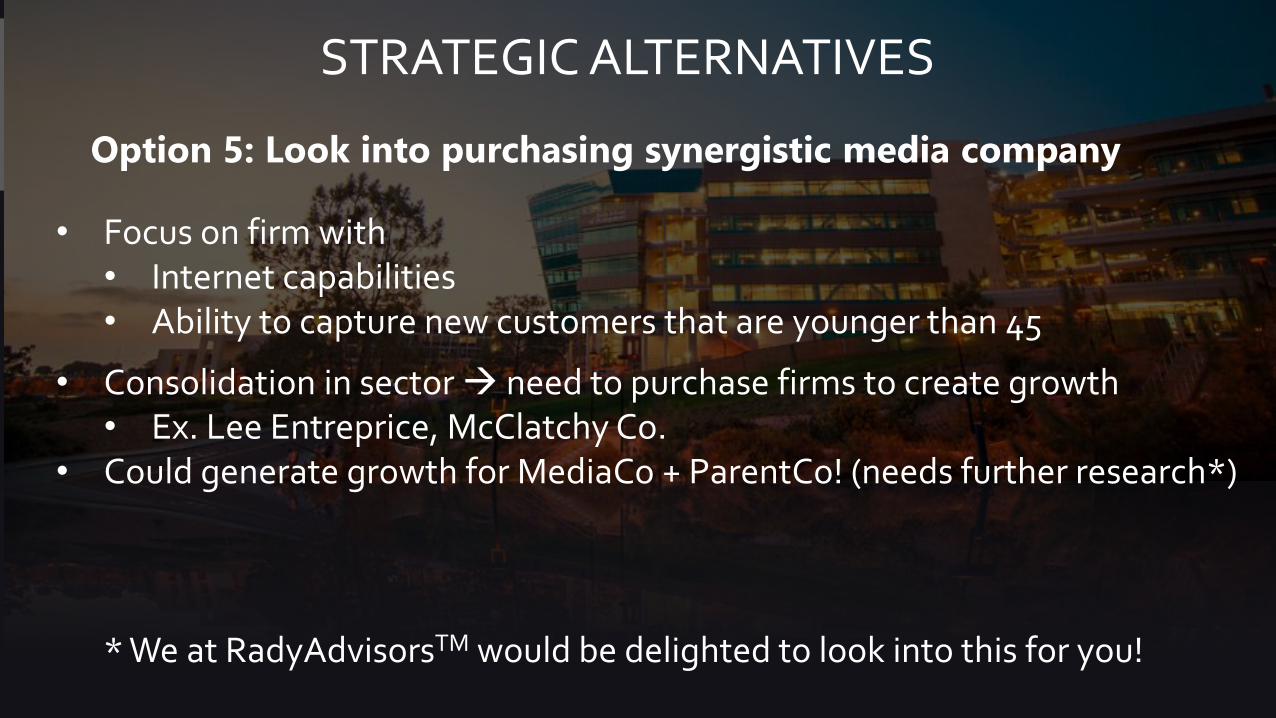

Option 5: Look into purchasing synergistic media company

• Focus on firm with• Internet capabilities• Ability to capture new customers that are younger than 45

• Consolidation in sector need to purchase firms to create growth• Ex. Lee Entreprice, McClatchy Co.

• Could generate growth for MediaCo + ParentCo! (needs further research*)

* We at RadyAdvisorsTM would be delighted to look into this for you!

STRATEGIC ALTERNATIVES

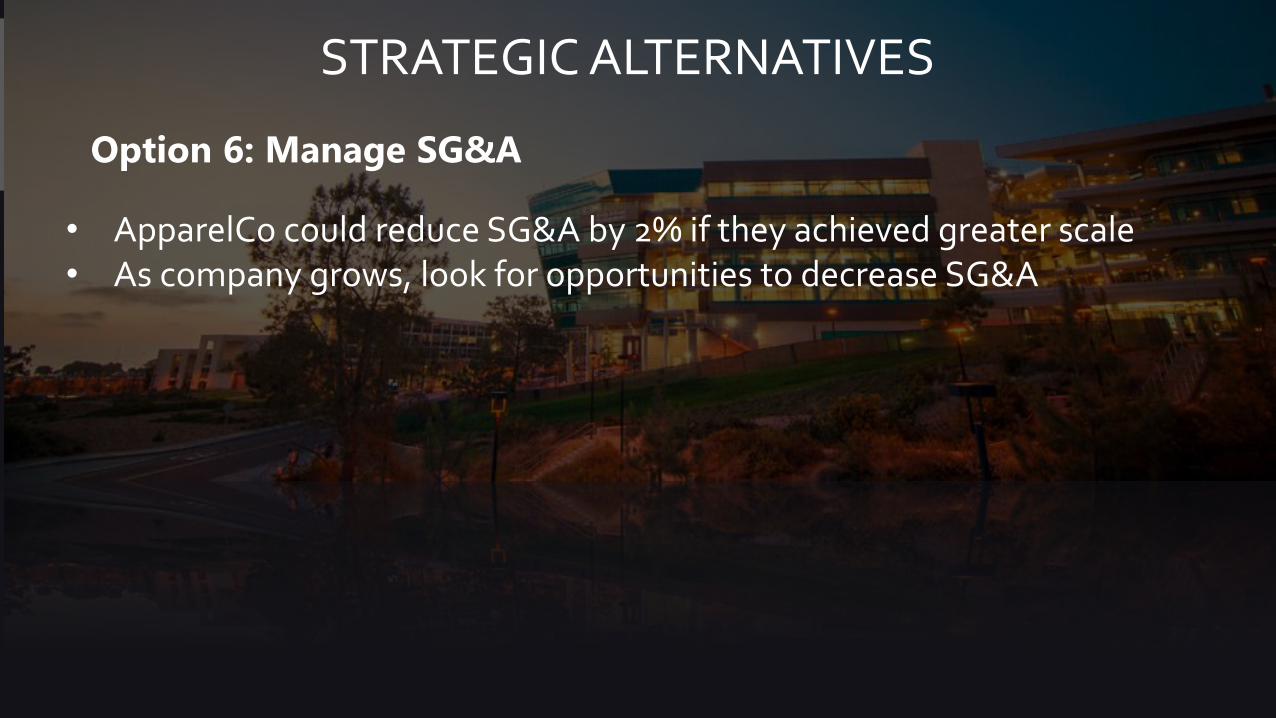

Option 6: Manage SG&A

• ApparelCo could reduce SG&A by 2% if they achieved greater scale• As company grows, look for opportunities to decrease SG&A

NEXT STEPS

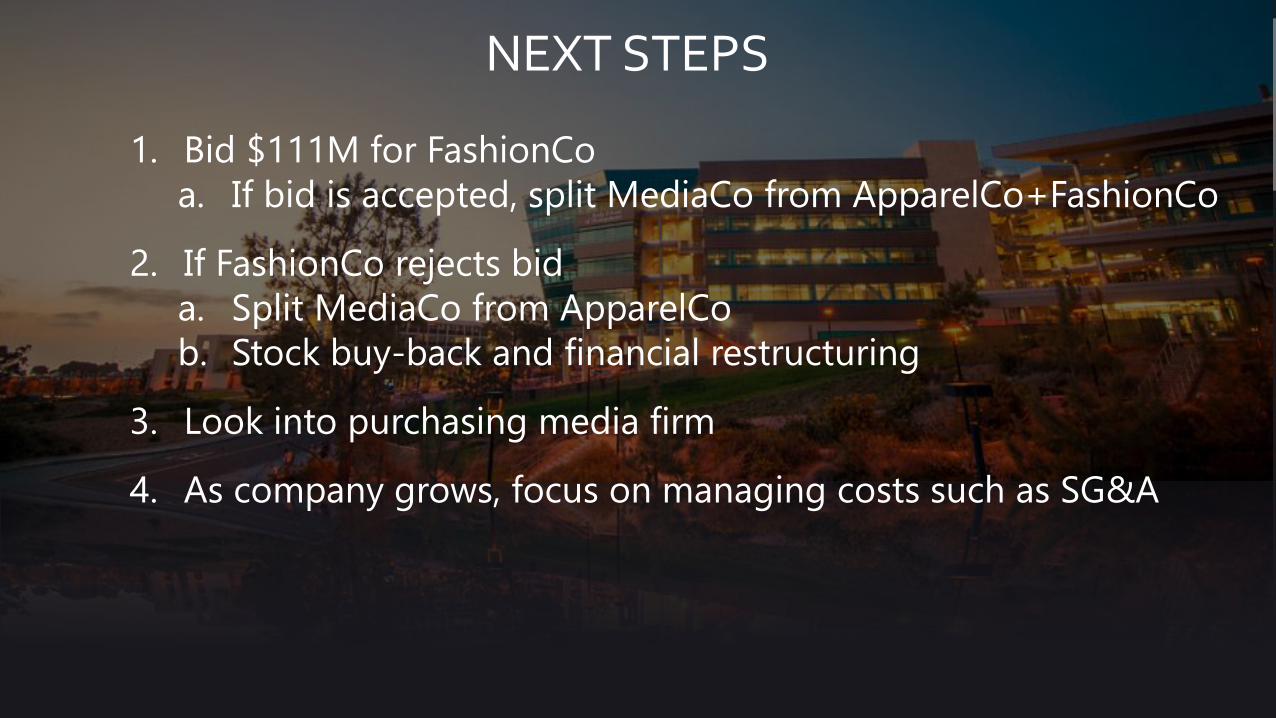

1. Bid $111M for FashionCo

a. If bid is accepted, split MediaCo from ApparelCo+FashionCo

2. If FashionCo rejects bid

a. Split MediaCo from ApparelCo

b. Stock buy-back and financial restructuring

3. Look into purchasing media firm

4. As company grows, focus on managing costs such as SG&A

OLIVER BINZ | ALLISON NOEL | LAUREN VOLLON | SARAH FELDMAN RADY ADVISORSTM

THANK YOU!