2015 Credit Slides Final - Ford – New Cars, Trucks, SUVs, … · 2018-07-18 · economic cycles...

67

CREDIT UNIVERSITY March 13, 2015

Transcript of 2015 Credit Slides Final - Ford – New Cars, Trucks, SUVs, … · 2018-07-18 · economic cycles...

CREDIT UNIVERSITY

March 13, 2015

SLIDE 1

CREDIT UNIVERSITY

Outline

• Ford Credit Strategic Value, Virtuous Circle and Value Proposition

• Scope of Operations

• Ford Credit Business Model and the Drivers of the Business– Originate: Buy it Right– Service: Operate Efficiently, Collect Effectively– Fund: Fund Efficiently, Manage Risk

• Ford Credit Profit Reporting

Anything else is just credit.

Ford Credit Strategic Value, Virtuous Circle and Value Proposition

SLIDE 3

SLIDE 4

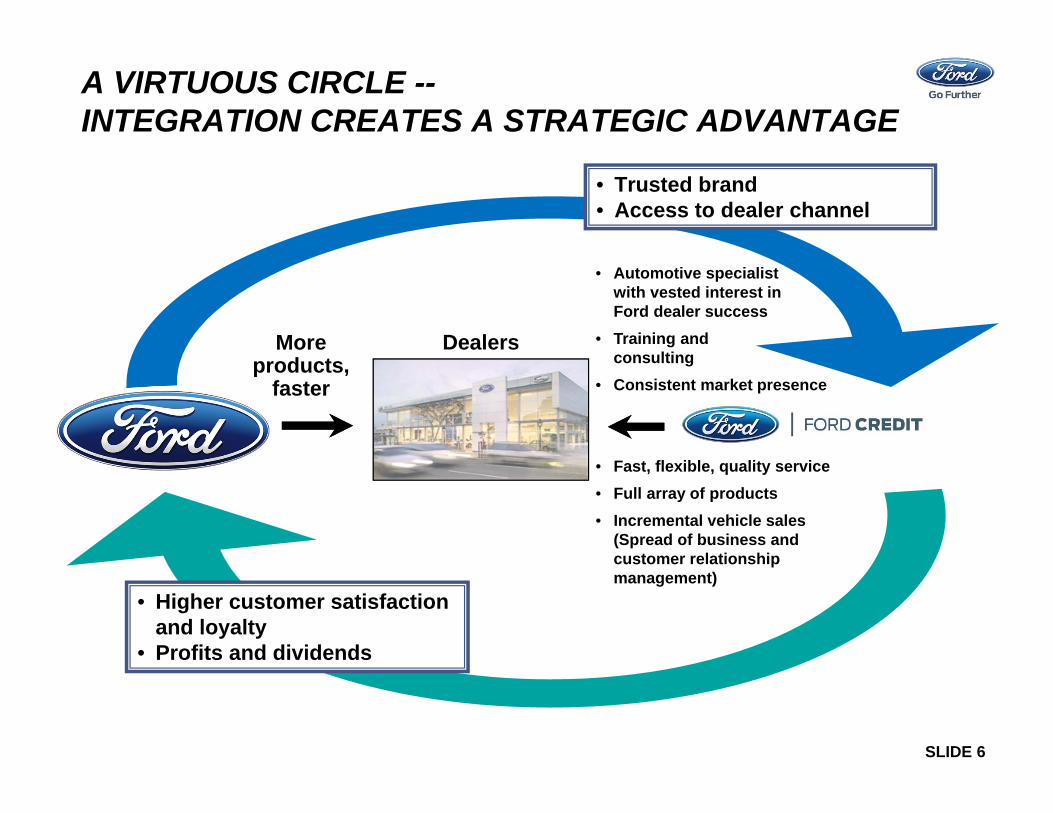

FORD CREDIT STRATEGIC VALUE

• Profitably support Ford, its dealers and customers through economic cycles

• Strategic value delivered through:– More than 55 years of automotive financing experience– Consistent vehicle inventory financing, supporting automotive

production plans and dealer inventory requirements– Exclusive Ford and Lincoln retail and lease consumer

financing products; integrated marketing strategies

SLIDE 5

FORD CREDIT STRATEGIC VALUE

• Ford Credit is integrally tied to Ford Motor Company

• Our profitability is based on competitive leverage and return targets

• We have a relentless focus on driving value based on:– A competitive funding structure– A world-class operating cost structure– A world-class risk management organization

• Our comprehensive customer relationship management process enhances the sales and service experience, and drives repeat business for Ford and Lincoln

• Ford Credit’s processes and focus create the “Virtuous Circle”

SLIDE 6

A VIRTUOUS CIRCLE --INTEGRATION CREATES A STRATEGIC ADVANTAGE

• Automotive specialist with vested interest in Ford dealer success

• Training and consulting

• Consistent market presence

• Fast, flexible, quality service• Full array of products• Incremental vehicle sales

(Spread of business and customer relationship management)

More products,

faster

• Higher customer satisfaction and loyalty

• Profits and dividends

• Trusted brand• Access to dealer channel

Dealers

SLIDE 7

FORD CREDIT VALUE PROPOSITION --CUSTOMER LOYALTY TO FORD

Customers Who Finance With Ford Credit Are More Loyal To Ford Compared With Customers Who Finance With Other Lenders

25%

35%

45%

55%

65%

75%

2010 2011 2012 2013 2014

U.S. ‐ % Loyal to Ford & Lincoln

Ford Credit Dealer Arranged Customer Arranged

25%

35%

45%

55%

65%

75%

2009 2010 2011 2012 2013

Europe (Big 5 Markets) ‐ % Loyal to Ford*

Ford Credit Dealer Arranged Customer Arranged

Source: Maritz New Vehicle Customer Survey 2010-2014 Source: Internal* 2014 European Data will be available in 2Q 2015

17 ppts.

27 ppts.

SLIDE 8

FORD CREDIT VALUE PROPOSITION --U.S. CUSTOMER SATISFACTION WITH DEALER-ARRANGED FINANCING

40%

90%

Customers Are More Satisfied With Ford Credit Than Other Dealer-Arranged Financing

Ford Credit FinancingOther Dealer-Arranged Financing

6 ppts.

Source: Maritz New Vehicle Customer Survey 2010–2014

2010 2011 2012 2013 2014

SLIDE 9

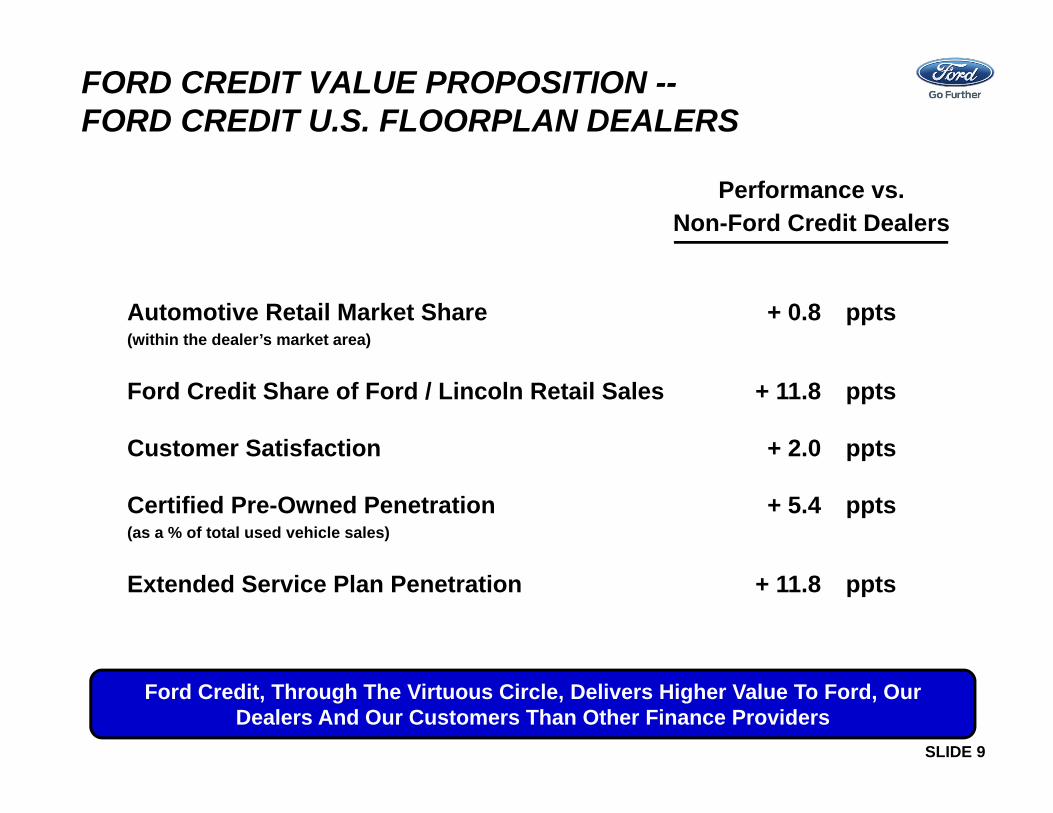

Automotive Retail Market Share + 0.8 ppts(within the dealer’s market area)

Ford Credit Share of Ford / Lincoln Retail Sales + 11.8 ppts

Customer Satisfaction + 2.0 ppts

Certified Pre-Owned Penetration + 5.4 ppts(as a % of total used vehicle sales)

Extended Service Plan Penetration + 11.8 ppts

FORD CREDIT VALUE PROPOSITION --FORD CREDIT U.S. FLOORPLAN DEALERS

Performance vs. Non-Ford Credit Dealers

Ford Credit, Through The Virtuous Circle, Delivers Higher Value To Ford, Our Dealers And Our Customers Than Other Finance Providers

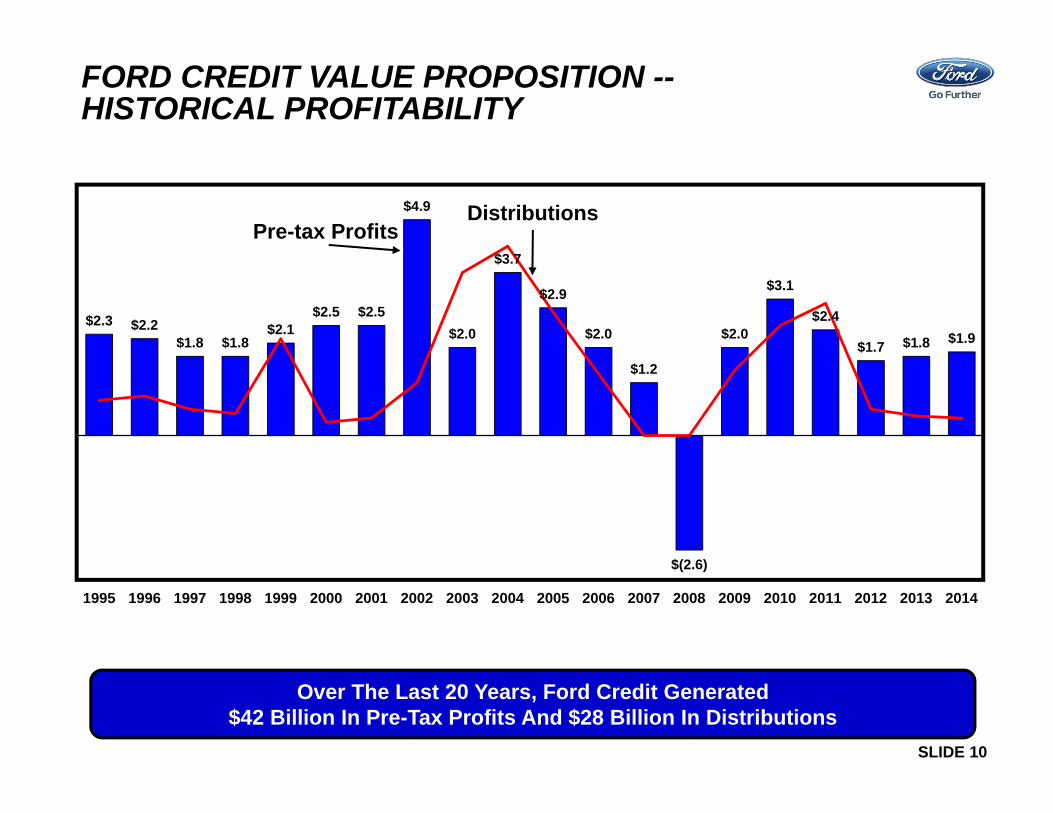

SLIDE 10

Pre-tax Profits

FORD CREDIT VALUE PROPOSITION --HISTORICAL PROFITABILITY

Over The Last 20 Years, Ford Credit Generated $42 Billion In Pre-Tax Profits And $28 Billion In Distributions

$2.3 $2.2 $1.8 $1.8

$2.1 $2.5 $2.5

$4.9

$2.0

$3.7

$2.9

$2.0

$1.2

$(2.6)

$2.0

$3.1

$2.4

$1.7 $1.8 $1.9

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Distributions

Scope of Operations

SLIDE 12

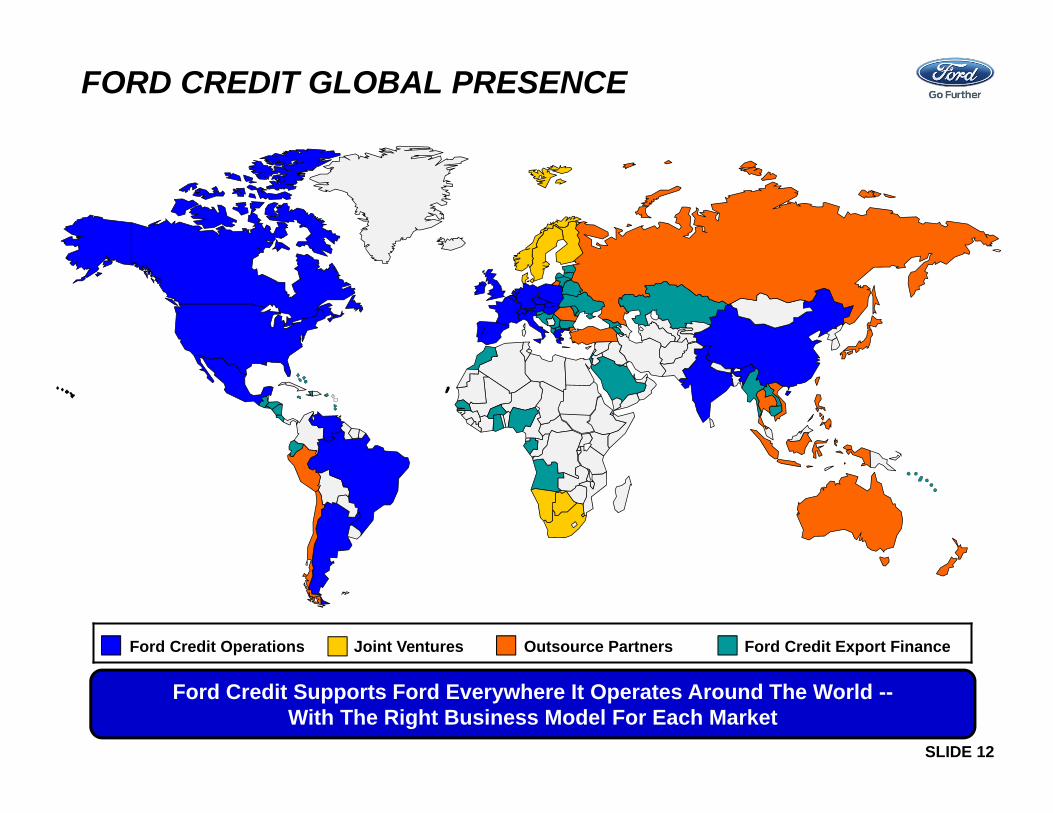

FORD CREDIT GLOBAL PRESENCE

Ford Credit Supports Ford Everywhere It Operates Around The World --With The Right Business Model For Each Market

Ford Credit Operations Joint Ventures Outsource Partners Ford Credit Export Finance

SLIDE 13

SIZE AND SCOPE OF OPERATIONS

• Ford indirectly owns 100% of Ford Credit

• Ford Credit offers a wide variety of automotive financing products to and through automotive dealers around the world

• Ford Credit has about 6,500 full-time employees and provides financing in approximately 100 countries

• As of year-end 2014, Ford Credit was financing worldwide:– About 5,200 Ford and Lincoln dealers– About 4.2 million customer contracts

• Ford Credit generates about 100 million customer touch points every year through websites, calls, e-mails, preapprovals, and invoices

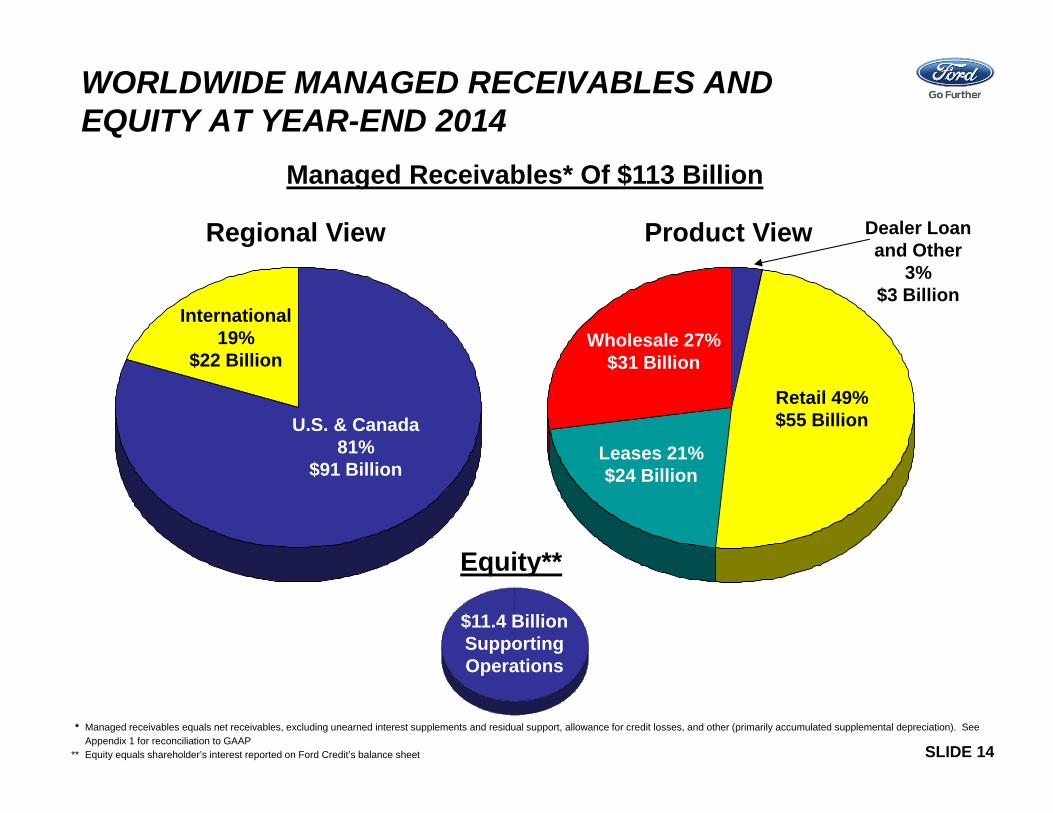

SLIDE 14

WORLDWIDE MANAGED RECEIVABLES AND EQUITY AT YEAR-END 2014

* Managed receivables equals net receivables, excluding unearned interest supplements and residual support, allowance for credit losses, and other (primarily accumulated supplemental depreciation). See Appendix 1 for reconciliation to GAAP

** Equity equals shareholder’s interest reported on Ford Credit’s balance sheet

U.S. & Canada 81%

$91 Billion

International 19%

$22 Billion

Regional View

Retail 49% $55 Billion

Wholesale 27%$31 Billion

Leases 21% $24 Billion

Product View Dealer Loan and Other

3% $3 Billion

$11.4 BillionSupporting Operations

Equity**

Managed Receivables* Of $113 Billion

SLIDE 15

RELATIONSHIP AGREEMENT WITH FORD

• Any extension of credit to Ford will be on arm’s-length terms and will be enforced in a commercially reasonable manner

• Ford Credit will not guarantee more than $500 million of indebtedness of, or make equity investments in any of, Ford or its automotive affiliates

• Ford Credit can require Ford to make a capital contribution if Ford Credit’s managed leverage is greater than 11.5 to 1

• Ford Credit will not be required to accept credit or residual risk beyond what it would be willing to accept acting in a prudent and commercially reasonable manner

• Ford and Ford Credit are separate, legally distinct companies and will continue to maintain separate books, accounts, assets and liabilities

• Up to $2 billion of borrowing capacity under Ford’s revolving credit facility allocated to Ford Credit

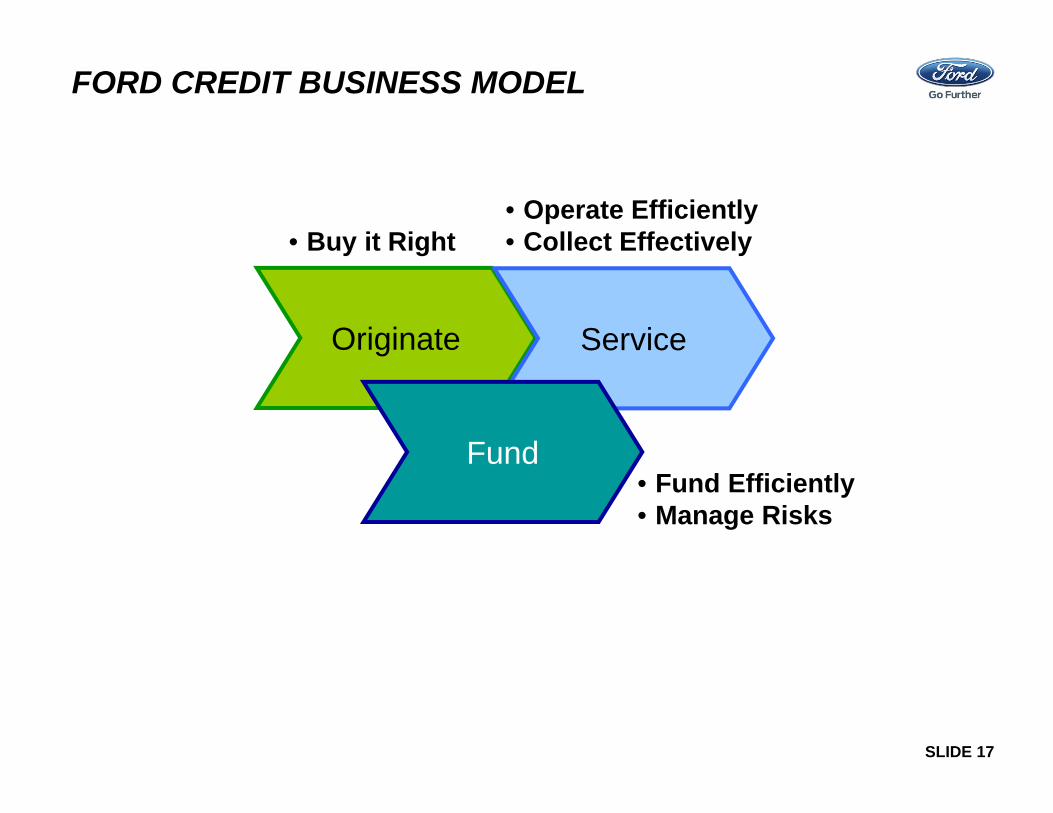

Ford Credit Business Model and the Drivers of the Business

SLIDE 17

• Buy it Right• Operate Efficiently• Collect Effectively

• Fund Efficiently• Manage Risks

Originate

FORD CREDIT BUSINESS MODEL

Service

Fund

SLIDE 18

ORIGINATIONS STRATEGY

• Support Ford Motor Company brands• Build strong relationships with dealers• Segment credit applications and price appropriately for risk• Use robust credit evaluation and verification process• Ensure efficient use of capital

• Buy it Right• Operate Efficiently• Collect Effectively

• Fund Efficiently• Manage Risks

ServiceOriginate

Fund

Technology And Judgment Combine To Buy It Right

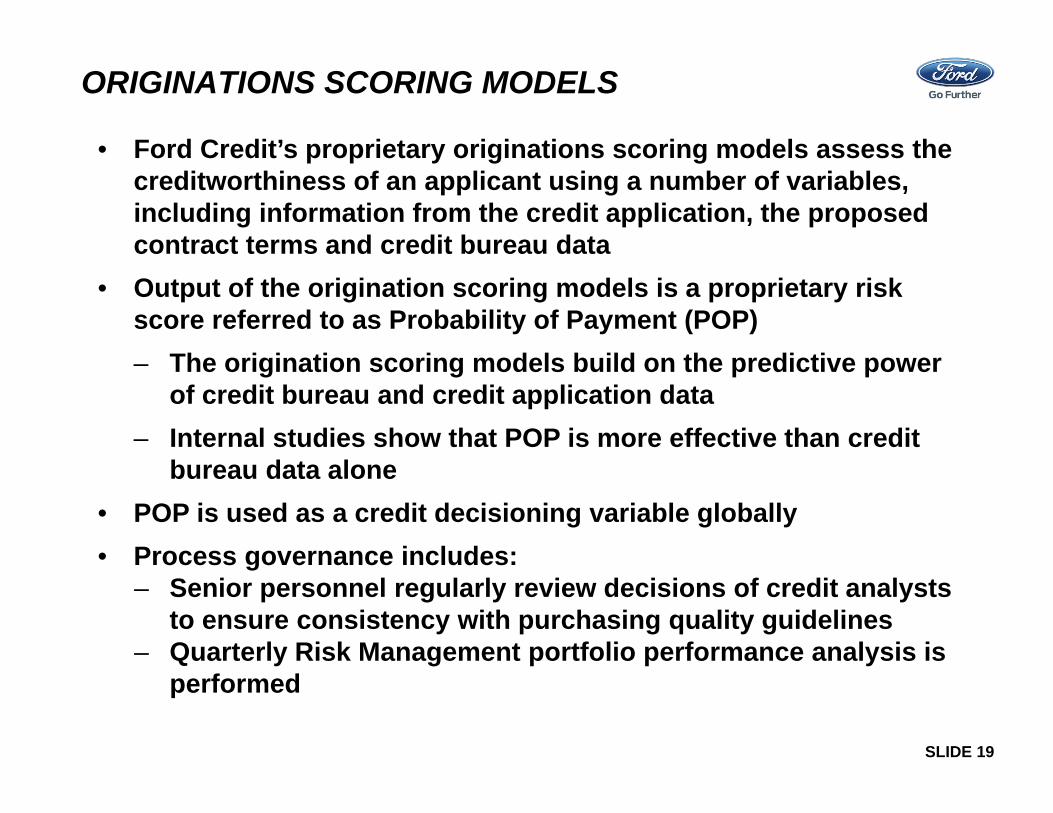

SLIDE 19

• Ford Credit’s proprietary originations scoring models assess the creditworthiness of an applicant using a number of variables, including information from the credit application, the proposed contract terms and credit bureau data

• Output of the origination scoring models is a proprietary risk score referred to as Probability of Payment (POP) – The origination scoring models build on the predictive power

of credit bureau and credit application data – Internal studies show that POP is more effective than credit

bureau data alone• POP is used as a credit decisioning variable globally • Process governance includes:

– Senior personnel regularly review decisions of credit analysts to ensure consistency with purchasing quality guidelines

– Quarterly Risk Management portfolio performance analysis is performed

ORIGINATIONS SCORING MODELS

SLIDE 20

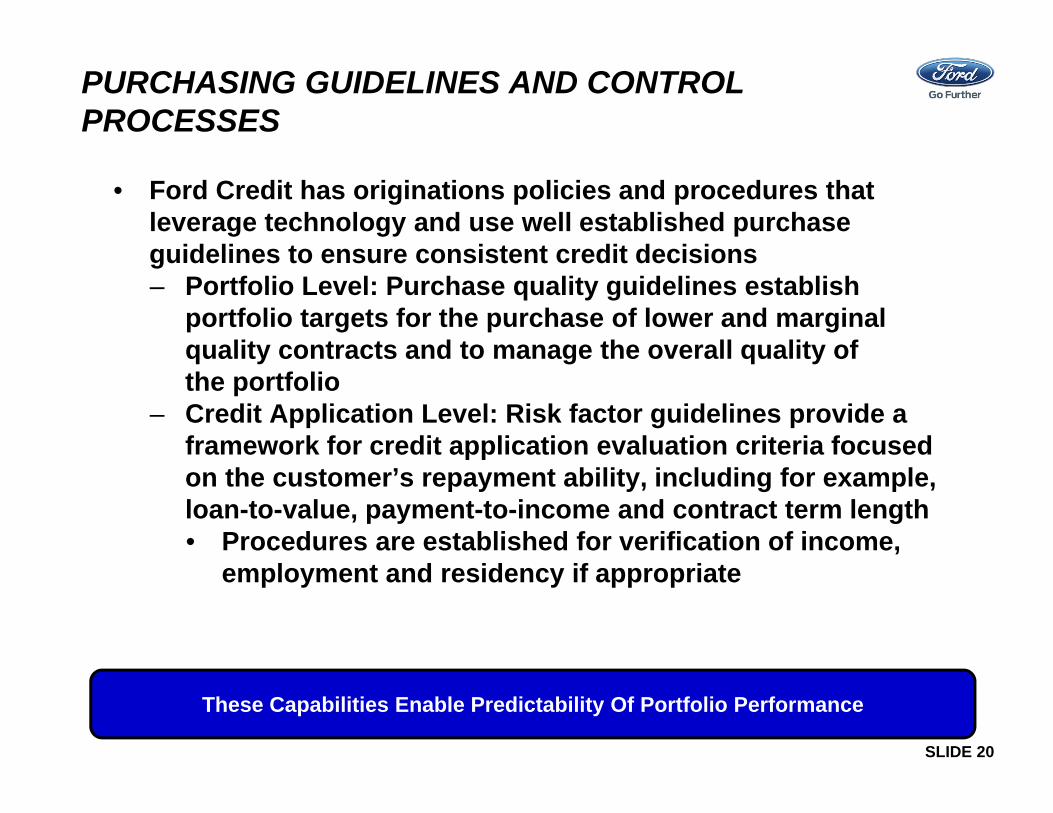

PURCHASING GUIDELINES AND CONTROL PROCESSES

• Ford Credit has originations policies and procedures that leverage technology and use well established purchase guidelines to ensure consistent credit decisions – Portfolio Level: Purchase quality guidelines establish

portfolio targets for the purchase of lower and marginal quality contracts and to manage the overall quality of the portfolio

– Credit Application Level: Risk factor guidelines provide a framework for credit application evaluation criteria focused on the customer’s repayment ability, including for example, loan-to-value, payment-to-income and contract term length• Procedures are established for verification of income,

employment and residency if appropriate

These Capabilities Enable Predictability Of Portfolio Performance

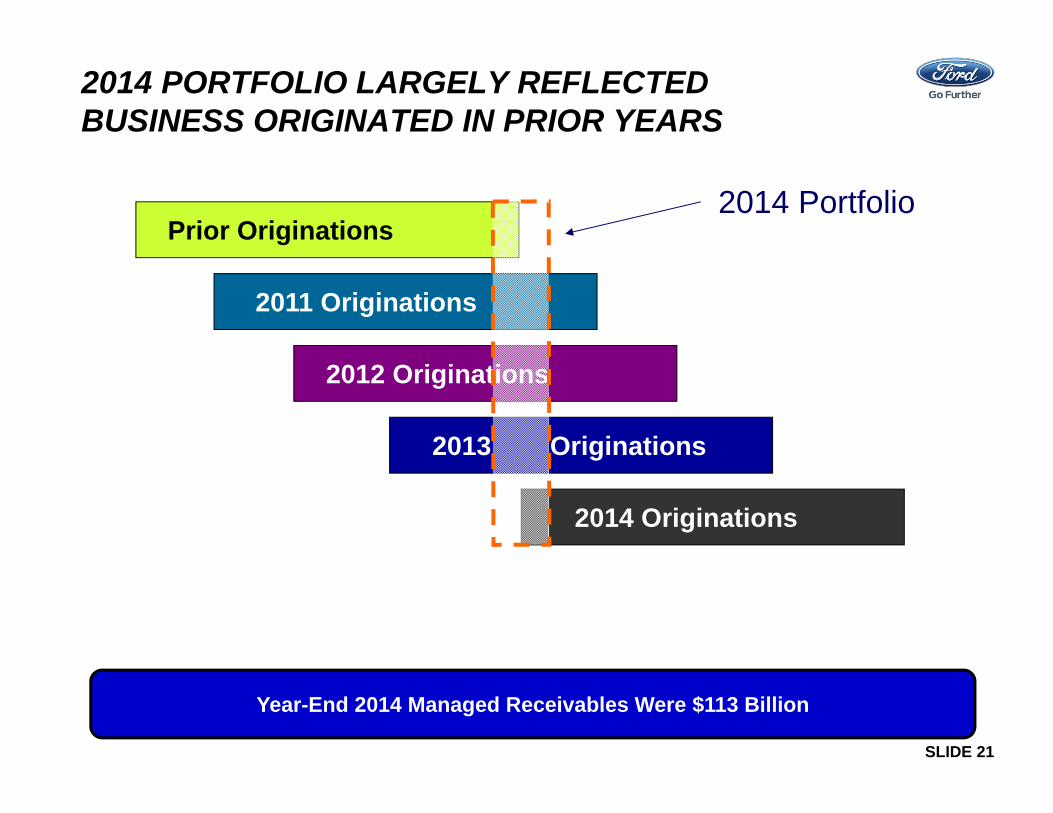

SLIDE 21

Prior Originations

2011 Originations

2012 Originations

2013 Originations

2014 Originations

2014 Portfolio

2014 PORTFOLIO LARGELY REFLECTEDBUSINESS ORIGINATED IN PRIOR YEARS

Year-End 2014 Managed Receivables Were $113 Billion

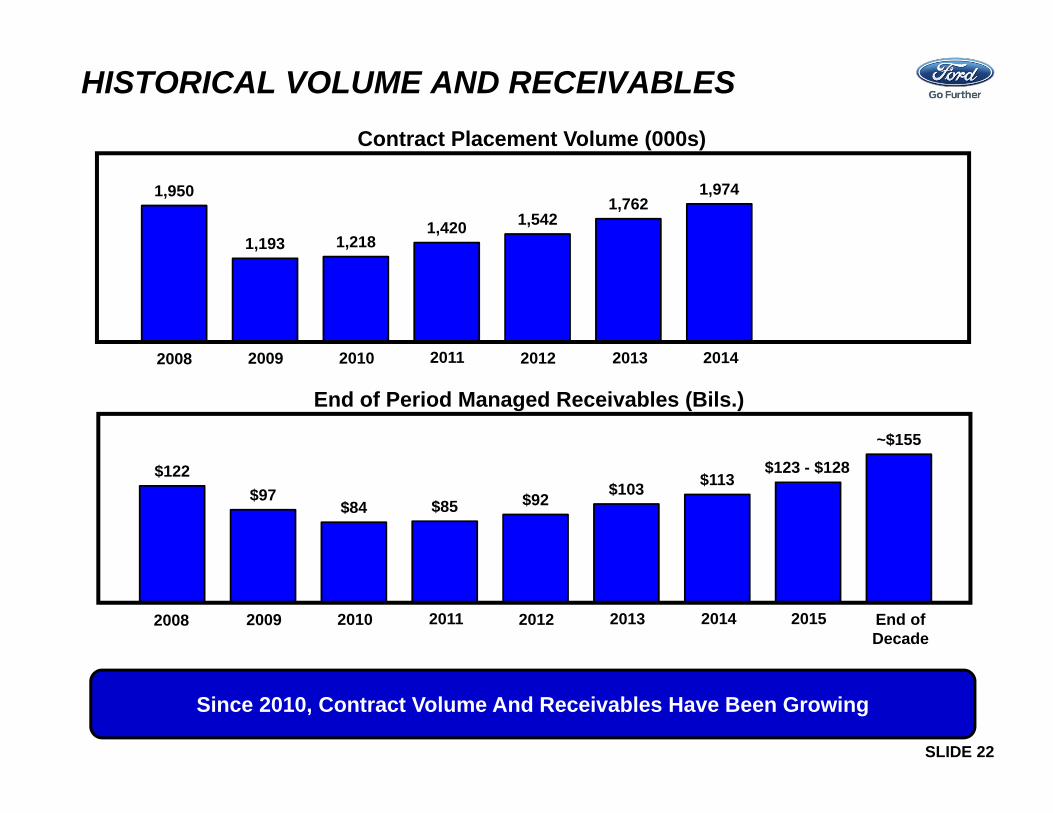

SLIDE 22

End of Period Managed Receivables (Bils.)

Contract Placement Volume (000s)

$122 $97

$84 $85 $92 $103 $113 $126

~$155

2008 2009 2010 2011 2012 2013 2015

HISTORICAL VOLUME AND RECEIVABLES

1,950

1,193 1,218 1,420 1,542

1,762 1,974

2008 2009 2010 2011 2012 2013

2014

Since 2010, Contract Volume And Receivables Have Been Growing

2014

$123 - $128

End of Decade

SLIDE 23

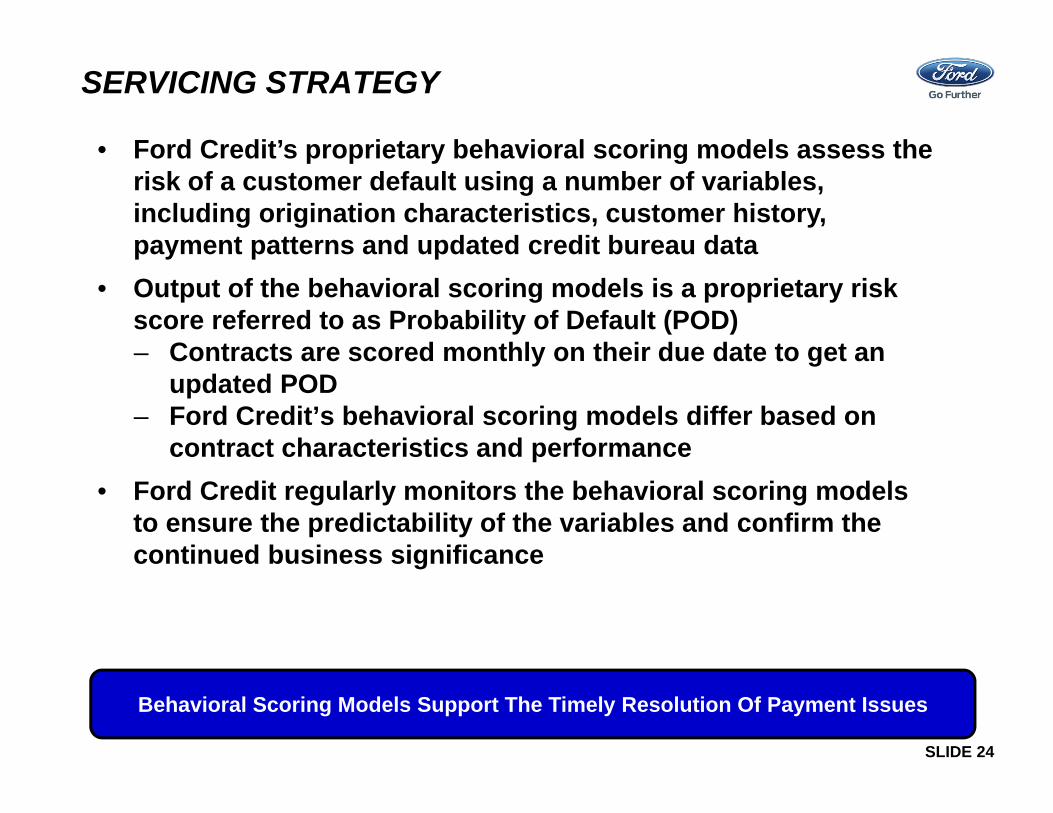

SERVICING STRATEGY

• Buy it Right• Operate Efficiently• Collect Effectively

• Fund Efficiently• Manage Risks

ServiceOriginate

Fund

• Ford Credit has a world-class servicing organization• Credit losses are an expected part of the business• The objective is to collect within the portfolio loss expectation while

managing costs • Customer and dealer satisfaction is critical

Technology And Judgment Combine To Minimize Credit Losses

SLIDE 24

SERVICING STRATEGY

• Ford Credit’s proprietary behavioral scoring models assess the risk of a customer default using a number of variables, including origination characteristics, customer history, payment patterns and updated credit bureau data

• Output of the behavioral scoring models is a proprietary risk score referred to as Probability of Default (POD) – Contracts are scored monthly on their due date to get an

updated POD – Ford Credit’s behavioral scoring models differ based on

contract characteristics and performance • Ford Credit regularly monitors the behavioral scoring models

to ensure the predictability of the variables and confirm the continued business significance

Behavioral Scoring Models Support The Timely Resolution Of Payment Issues

SLIDE 25

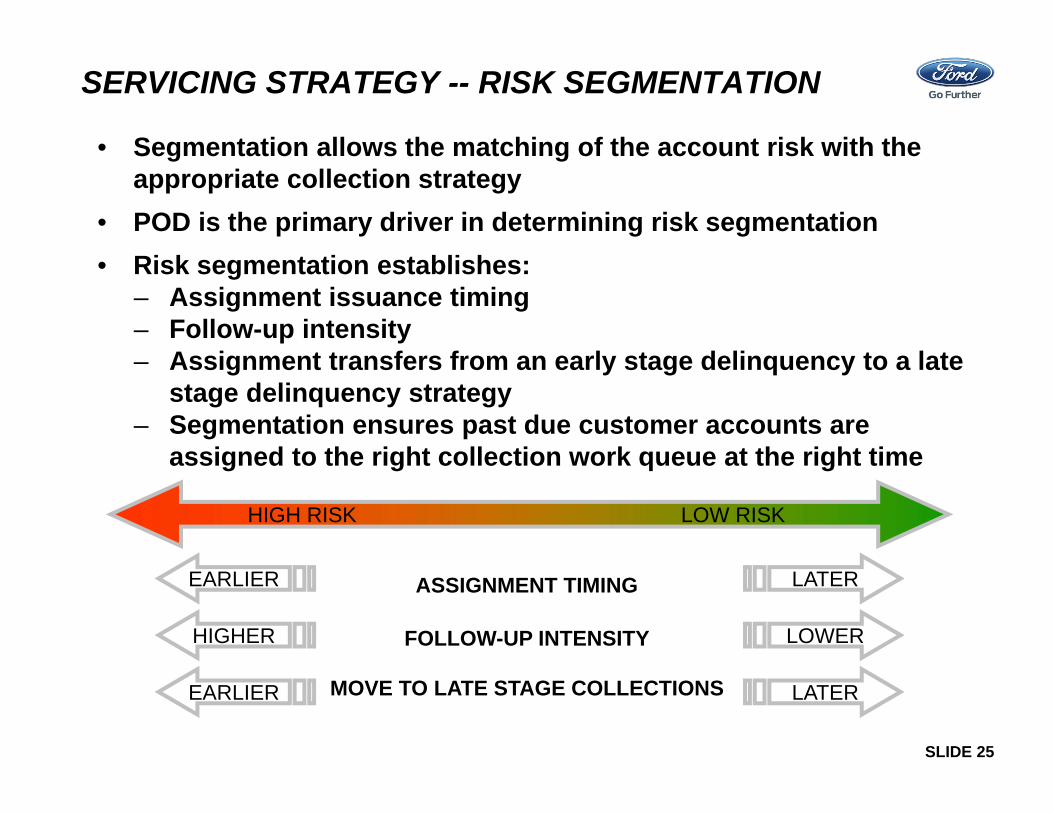

SERVICING STRATEGY -- RISK SEGMENTATION

• Segmentation allows the matching of the account risk with the appropriate collection strategy

• POD is the primary driver in determining risk segmentation• Risk segmentation establishes:

– Assignment issuance timing– Follow-up intensity– Assignment transfers from an early stage delinquency to a late

stage delinquency strategy– Segmentation ensures past due customer accounts are

assigned to the right collection work queue at the right time

HIGH RISK LOW RISK

ASSIGNMENT TIMING

FOLLOW-UP INTENSITY

MOVE TO LATE STAGE COLLECTIONS

LATER

LOWER

LATER

EARLIER

HIGHER

EARLIER

SLIDE 26

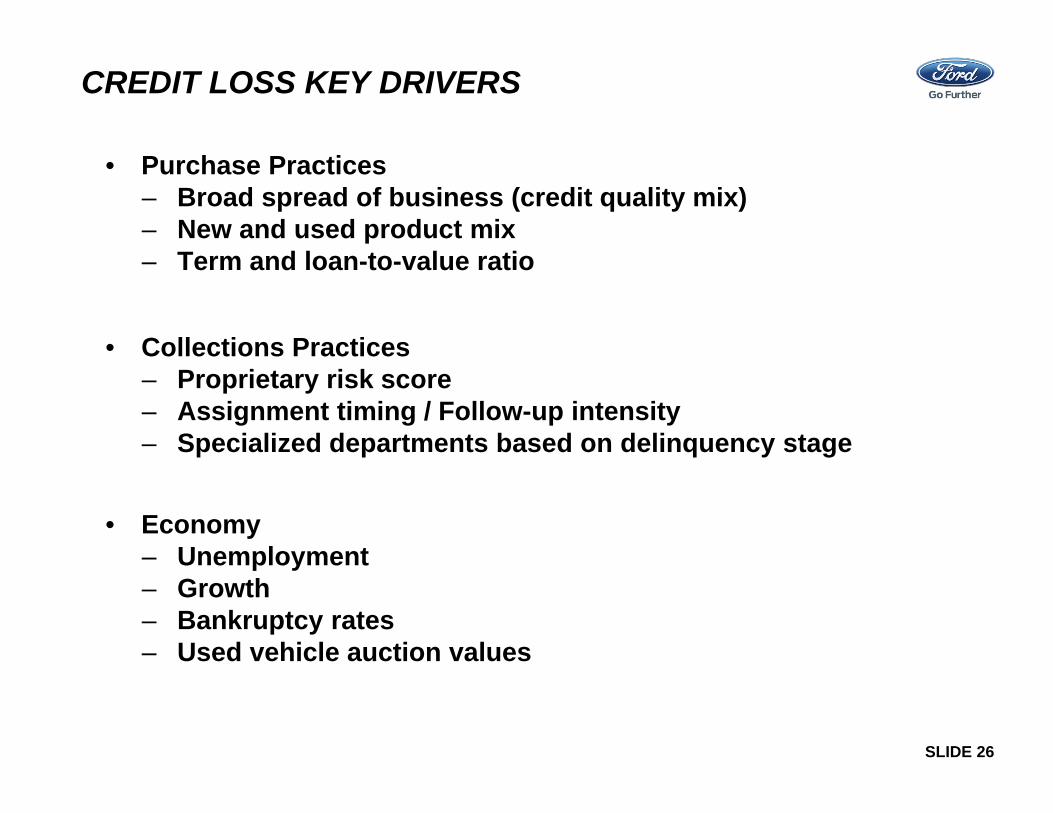

CREDIT LOSS KEY DRIVERS

• Purchase Practices– Broad spread of business (credit quality mix)– New and used product mix– Term and loan-to-value ratio

• Collections Practices– Proprietary risk score – Assignment timing / Follow-up intensity– Specialized departments based on delinquency stage

• Economy– Unemployment– Growth– Bankruptcy rates– Used vehicle auction values

SLIDE 27

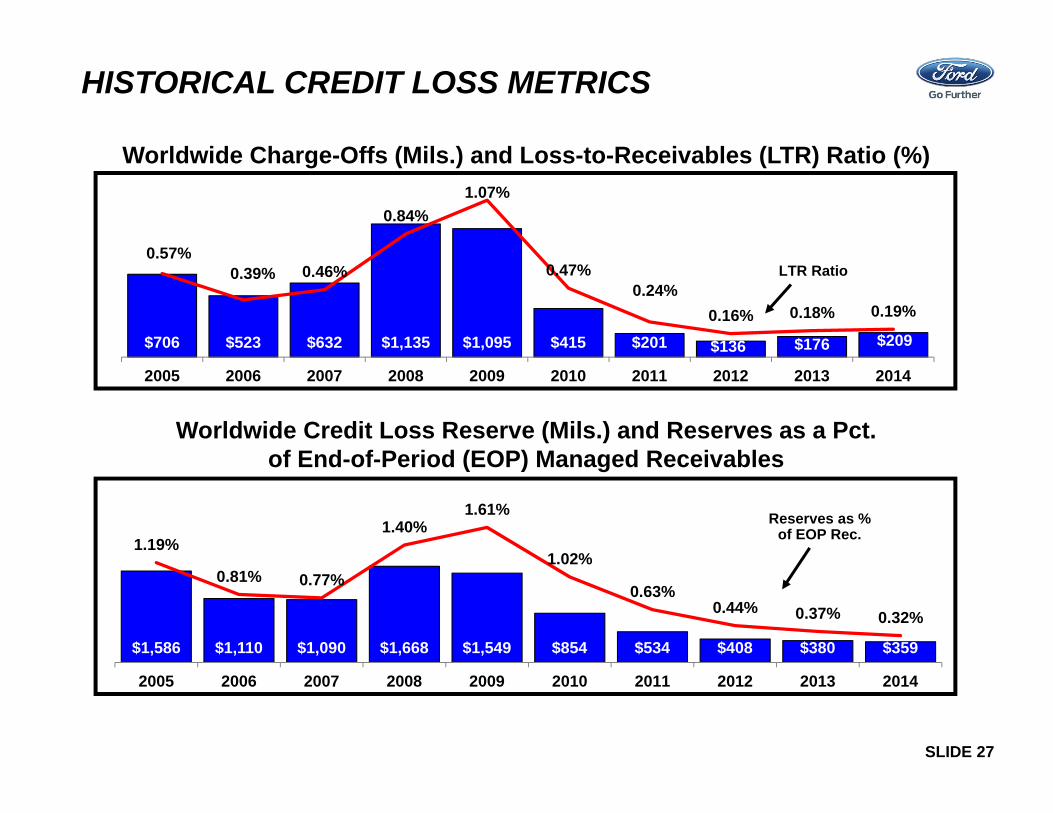

HISTORICAL CREDIT LOSS METRICS

$706 $523 $632 $1,135 $1,095 $415 $201 $136 $176 $209

0.57%0.39% 0.46%

0.84%1.07%

0.47%0.24%

0.16% 0.18% 0.19%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Worldwide Charge-Offs (Mils.) and Loss-to-Receivables (LTR) Ratio (%)

LTR Ratio

$1,586 $1,110 $1,090 $1,668 $1,549 $854 $534 $408 $380 $359

1.19%

0.81% 0.77%

1.40%1.61%

1.02%

0.63%0.44% 0.37% 0.32%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Reserves as % of EOP Rec.

Worldwide Credit Loss Reserve (Mils.) and Reserves as a Pct. of End-of-Period (EOP) Managed Receivables

SLIDE 28

109

82 74 8194

6445

32 29 28

2.30%1.94%

1.89%

2.30%

3.01%

2.41%

1.86%

1.35%1.18% 1.06%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

0.15% 0.16%0.19%

0.24% 0.24%

0.15% 0.14% 0.15% 0.15% 0.14%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

715 710 714 719726 730

738 737 738 741

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Average Placement FICO Score

Repossessions (000)Repo. Ratio

Charge-Offs (Mils.) and LTR (%)

Over-60-Day Delinquencies

HISTORICAL U.S. RETAIL AND LEASE CREDIT LOSS DRIVERS*

* Includes Ford, Lincoln and Mercury

Memo: New Bankruptcy Filings (000)84 21 27 37 47 42 31 23 17 14

Memo: Severity$6,100 $6,300 $7,400 $9,900 $8,300 $6,900 $6,500 $6,900 $7,600 $7,900

$433

$309$431

$775

$635

$280

$144 $100 $127 $146

0.79%0.56%

0.74%

1.36% 1.32%

0.68%

0.36%0.23%

0.26% 0.27%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

LTR

SLIDE 29

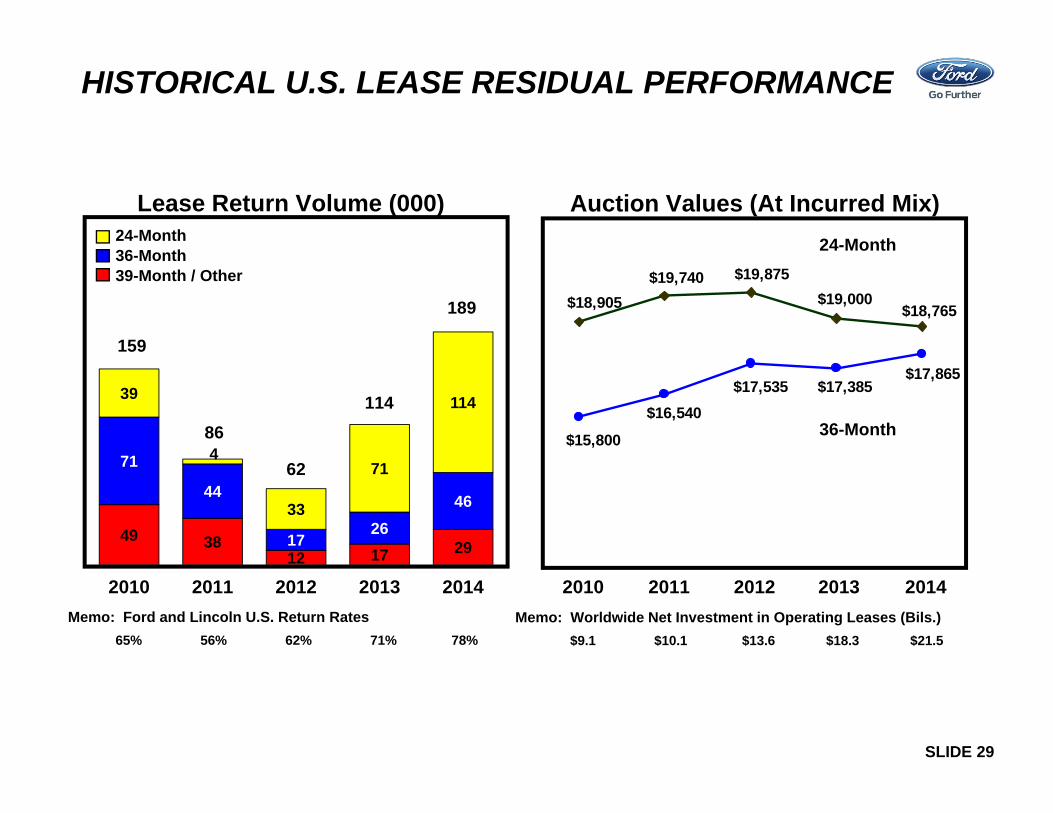

HISTORICAL U.S. LEASE RESIDUAL PERFORMANCE

Memo: Ford and Lincoln U.S. Return Rates 65% 56% 62% 71% 78%

49 3812 17 29

71

44

1726

46

39

4

33

71

114

2010 2011 2012 2013 2014

Lease Return Volume (000)

Memo: Worldwide Net Investment in Operating Leases (Bils.) $9.1 $10.1 $13.6 $18.3 $21.5

24-Month36-Month39-Month / Other

159

62

86

189 $18,765$19,000

$19,875

$18,905$19,740

$17,865$17,385$17,535

$16,540

$15,800

Auction Values (At Incurred Mix)

114

2013 20142010 2011 2012

24-Month

36-Month

SLIDE 30

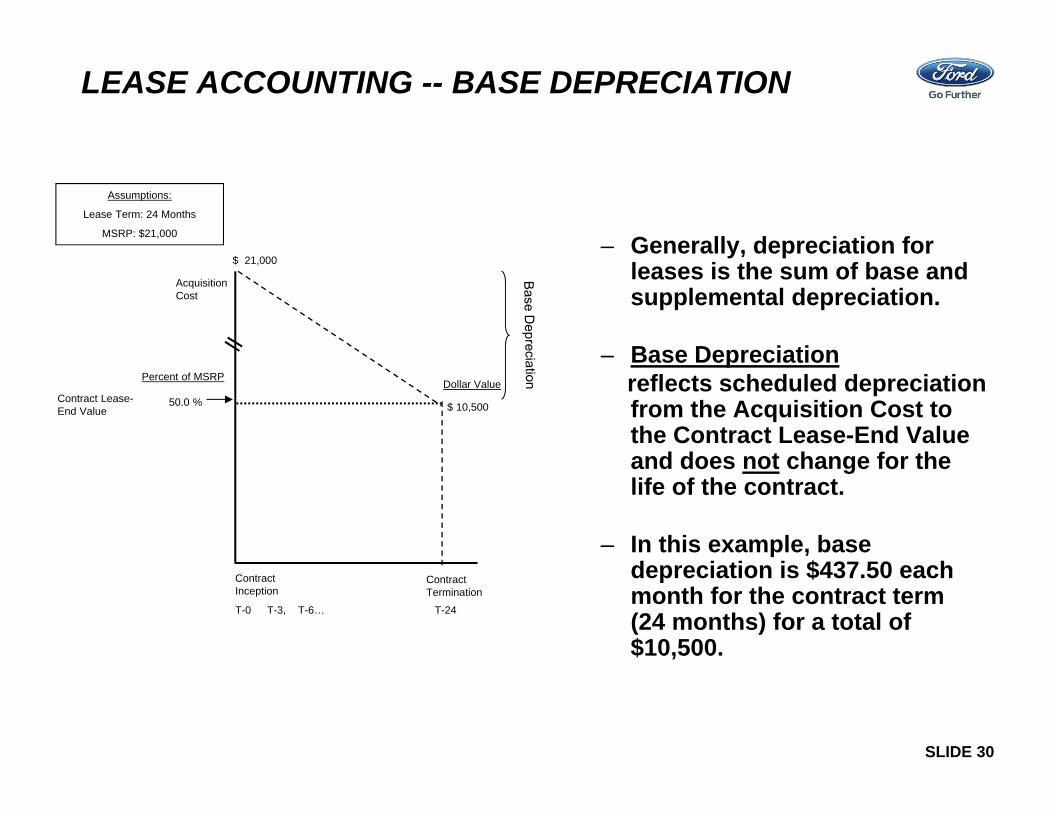

LEASE ACCOUNTING -- BASE DEPRECIATION

– Generally, depreciation for leases is the sum of base and supplemental depreciation.

– Base Depreciationreflects scheduled depreciation from the Acquisition Cost to the Contract Lease-End Value and does not change for the life of the contract.

– In this example, base depreciation is $437.50 each month for the contract term (24 months) for a total of $10,500.

Assumptions:

Lease Term: 24 Months

MSRP: $21,000

Acquisition Cost

Contract Lease-End Value

Percent of MSRP

50.0 %

ContractTermination

Dollar Value

$ 10,500

$ 21,000

ContractInception

T-0 T-3, T-6… T-24

SLIDE 31

LEASE ACCOUNTING --SUPPLEMENTAL DEPRECIATION

– Supplemental Depreciationreflects additional depreciation to achieve expected actual residual (i.e., auction) values for the leased vehicles.

– Supplemental depreciation can change based on expectations and it is assessed quarterly.

– It can be negative, however, it can never “un-depreciate” above base depreciation.

– In this example, supplemental depreciation is $40 each month for remaining term (21 months) for a total of $840.

Book Value

Contract Lease-End Value

Expected Actual Residual (i.e., Auction) Value at Lease ContractTermination

Percent of MSRP

50.0 %

46.0 %

ContractTermination

Dollar Value

$ 10,500

Additional Credit Co.SupplementalDepreciationExpense

$ 9,660

$ 19,687.50

ContractInception

T-0 T-3, T-6… T-24

Acquisition Cost $ 21,000

Assumptions:

Lease Term: 24 Months

MSRP: $21,000

SLIDE 32

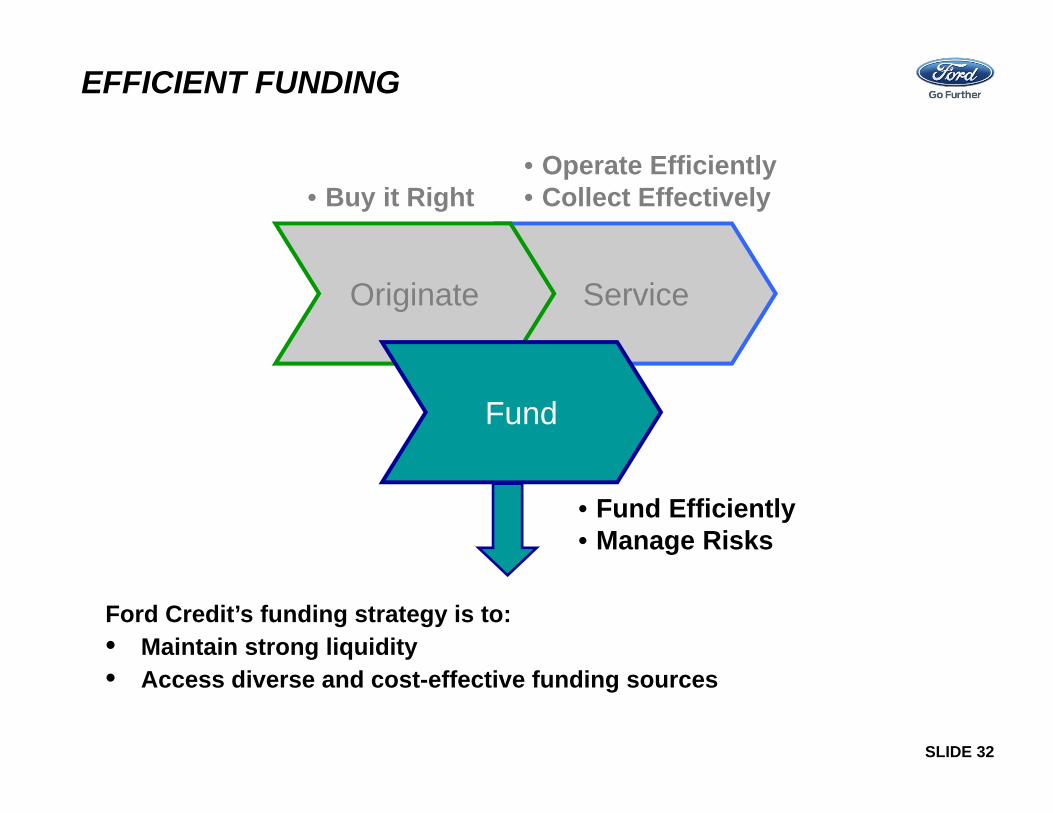

EFFICIENT FUNDING

• Buy it Right• Operate Efficiently• Collect Effectively

• Fund Efficiently• Manage Risks

ServiceOriginate

Fund

Ford Credit’s funding strategy is to:• Maintain strong liquidity• Access diverse and cost-effective funding sources

SLIDE 33

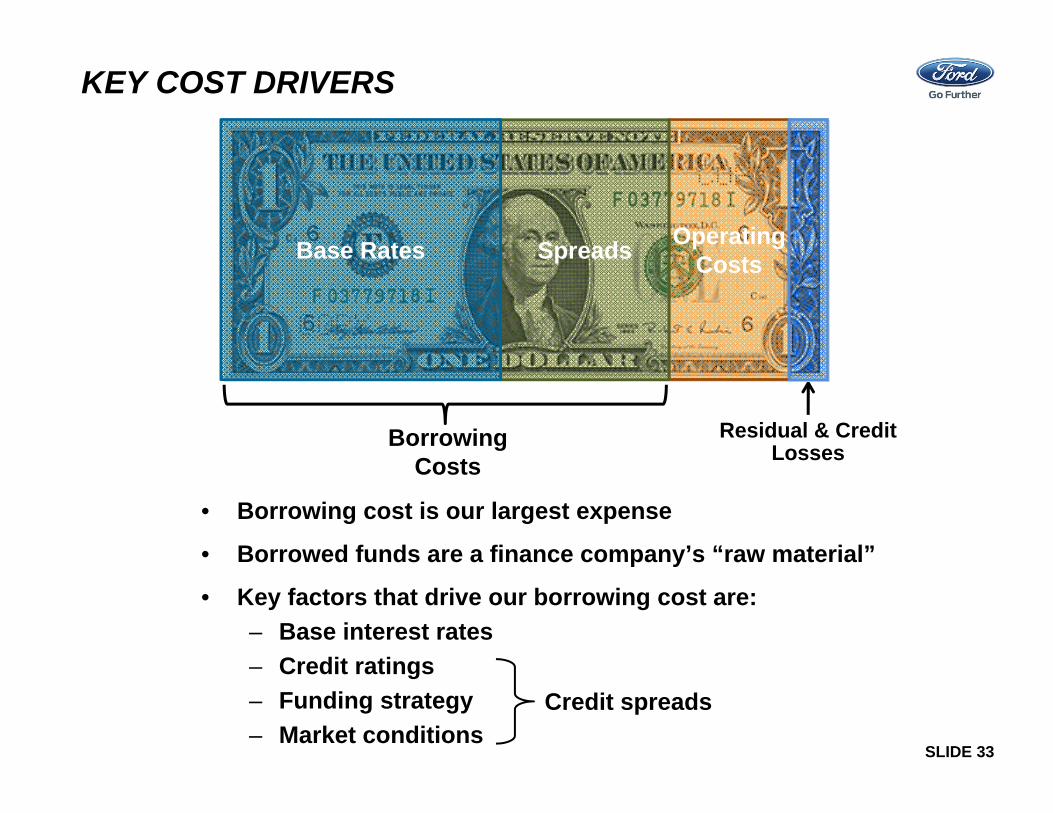

KEY COST DRIVERS

• Borrowing cost is our largest expense

• Borrowed funds are a finance company’s “raw material”

• Key factors that drive our borrowing cost are:– Base interest rates– Credit ratings– Funding strategy– Market conditions

Credit spreads

OperatingCostsSpreadsBase Rates

Residual & Credit LossesBorrowing

Costs

SLIDE 34

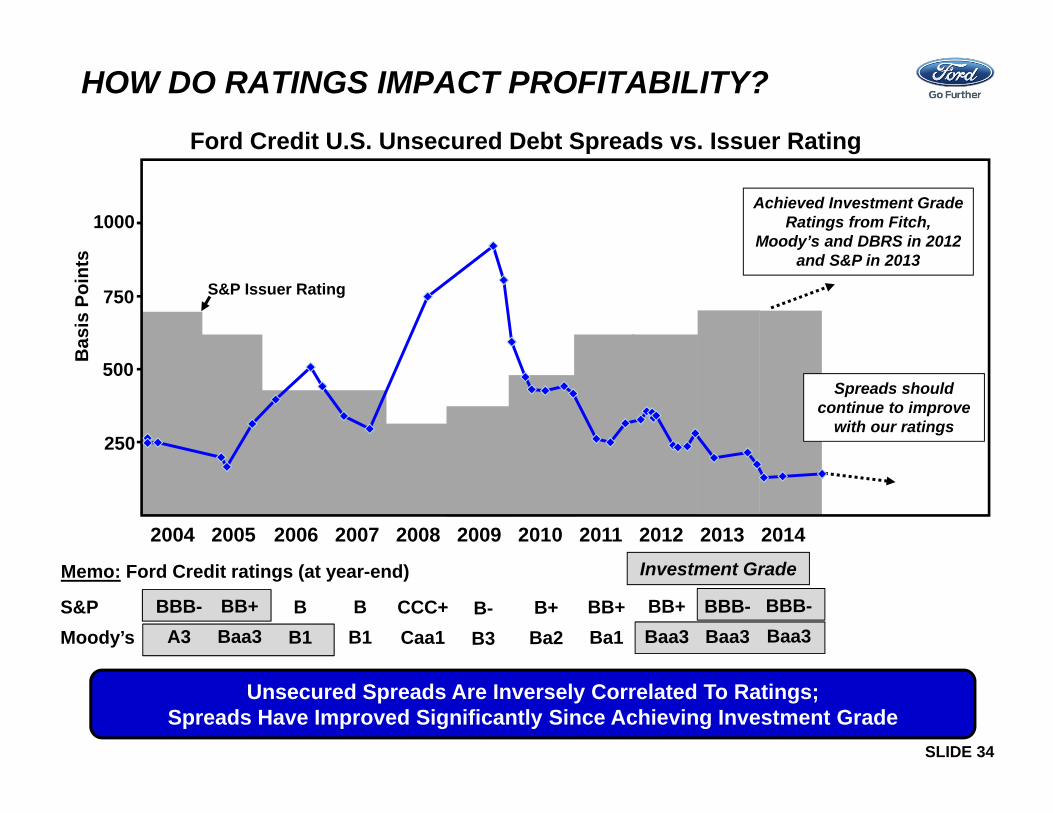

250

500

1000

HOW DO RATINGS IMPACT PROFITABILITY?

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

750

Ford Credit U.S. Unsecured Debt Spreads vs. Issuer Rating

S&P Issuer Rating

Bas

is P

oint

s

Achieved Investment Grade Ratings from Fitch,

Moody’s and DBRS in 2012 and S&P in 2013

Memo: Ford Credit ratings (at year-end)

BB+Ba1

B+Ba2

B-B3

CCC+Caa1

BB1

BB1

BB+Baa3

BBB-A3

BB+Baa3

S&PMoody’s

BBB-Baa3

Spreads should continue to improve

with our ratings

Investment Grade

Unsecured Spreads Are Inversely Correlated To Ratings; Spreads Have Improved Significantly Since Achieving Investment Grade

BBB-Baa3

SLIDE 35

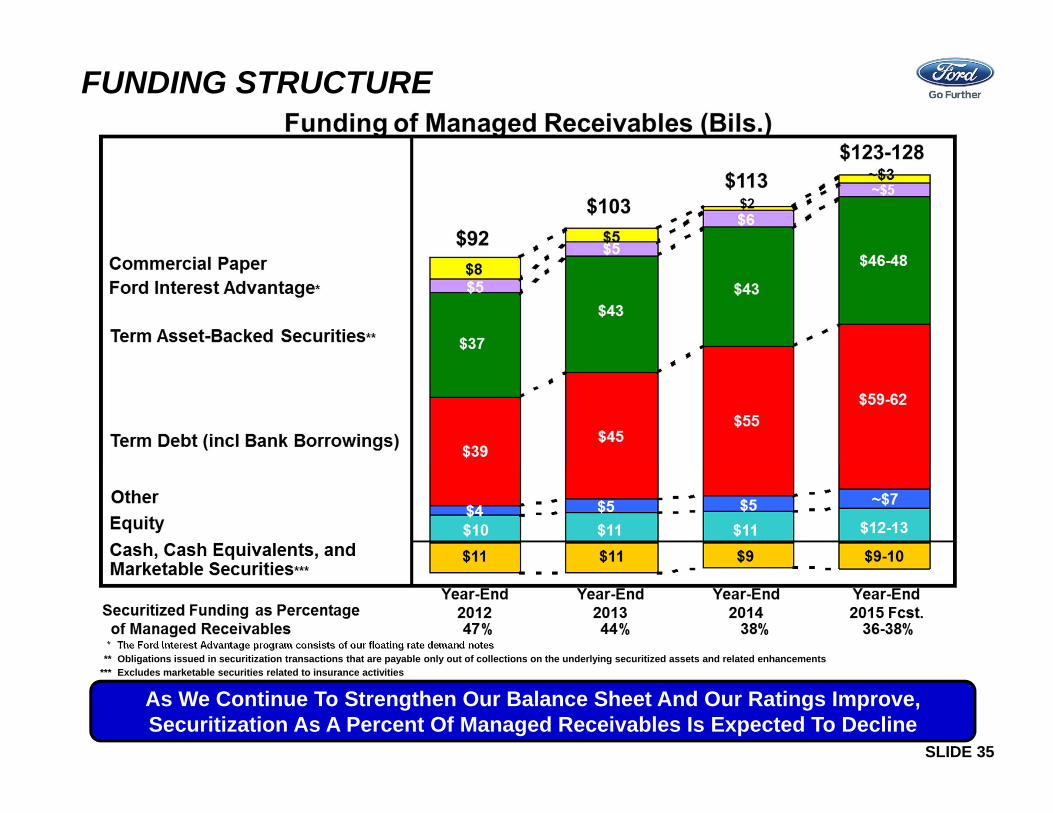

FUNDING STRUCTURE

* The Ford Interest Advantage program consists of our floating rate demand notes** Obligations issued in securitization transactions that are payable only out of collections on the underlying securitized assets and related enhancements

*** Excludes marketable securities related to insurance activities

As We Continue To Strengthen Our Balance Sheet And Our Ratings Improve, Securitization As A Percent Of Managed Receivables Is Expected To Decline

SLIDE 36

PUBLIC TERM FUNDING PLAN

Unsecured $ 9 $ 11 $ 13 $ 12 – 15

Securitizations* 14 14 15 13 – 16

Total $ 23 $ 25 $ 28 $ 25 – 31

2012 Actual(Bils.)

2013 Actual(Bils.)

2014Actual(Bils.)

2015Forecast

(Bils.)

* Includes Rule 144A offerings

Projected 2015 Public Issuance Largely Consistent With 2014; Continue To Maintain A Significant Presence In Both Unsecured And Securitization Markets

SLIDE 37

2014 LIQUIDITY PROGRAMS

Committed Capacity$37.3 billion

Available Liquidity Remains Strong At $26.5 Billion

* Cash, cash equivalents, and marketable securities (excludes marketable securities related to insurance activities)** Committed ABS lines are subject to availability of sufficient assets and ability to obtain derivatives to manage interest rate risk

*** Used only to support on-balance sheet securitization transactions**** Adjustments include other committed ABS lines in excess of eligible receivables and certain cash within FordREV available through future sales of receivables

SLIDE 38

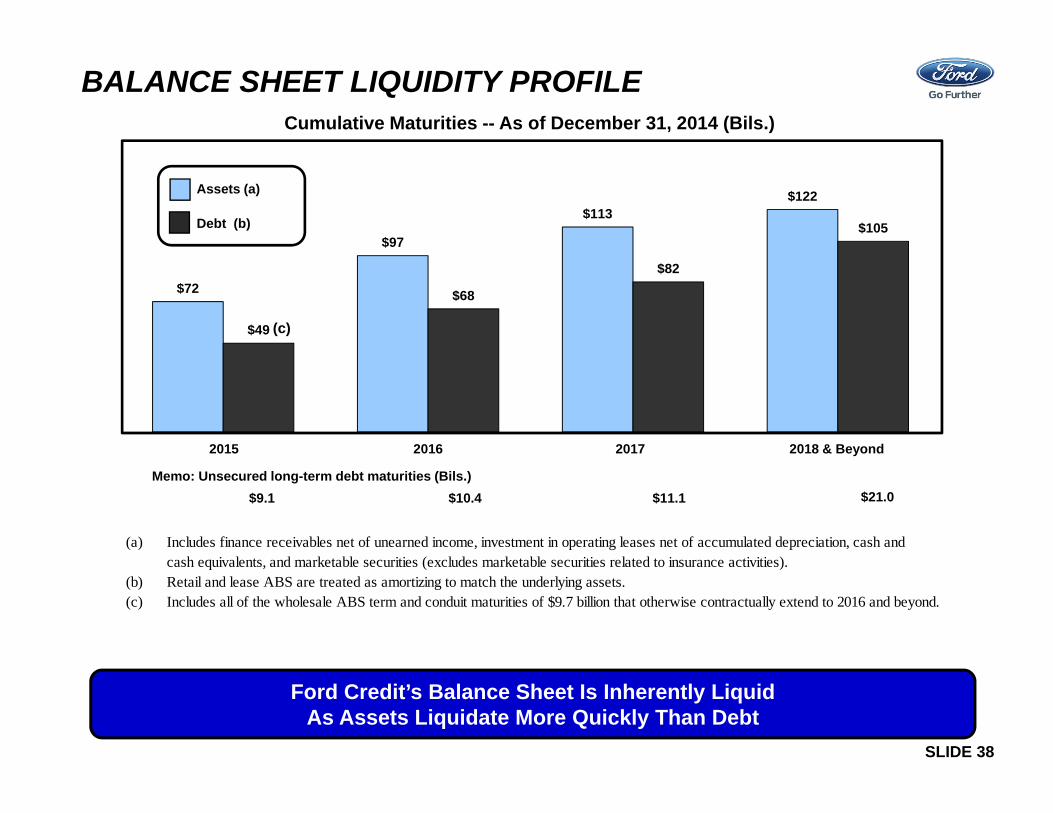

BALANCE SHEET LIQUIDITY PROFILECumulative Maturities -- As of December 31, 2014 (Bils.)

Ford Credit’s Balance Sheet Is Inherently Liquid As Assets Liquidate More Quickly Than Debt

(a) Includes finance receivables net of unearned income, investment in operating leases net of accumulated depreciation, cash andcash equivalents, and marketable securities (excludes marketable securities related to insurance activities).

(b) Retail and lease ABS are treated as amortizing to match the underlying assets.(c) Includes all of the wholesale ABS term and conduit maturities of $9.7 billion that otherwise contractually extend to 2016 and beyond.

$72

$97

$113$122

$49

$68

$82

$105

Assets (a)

Debt (b)

(c)

Memo: Unsecured long-term debt maturities (Bils.)

2015 2016 2017 2018 & Beyond

$9.1 $10.4 $11.1 $21.0

SLIDE 39

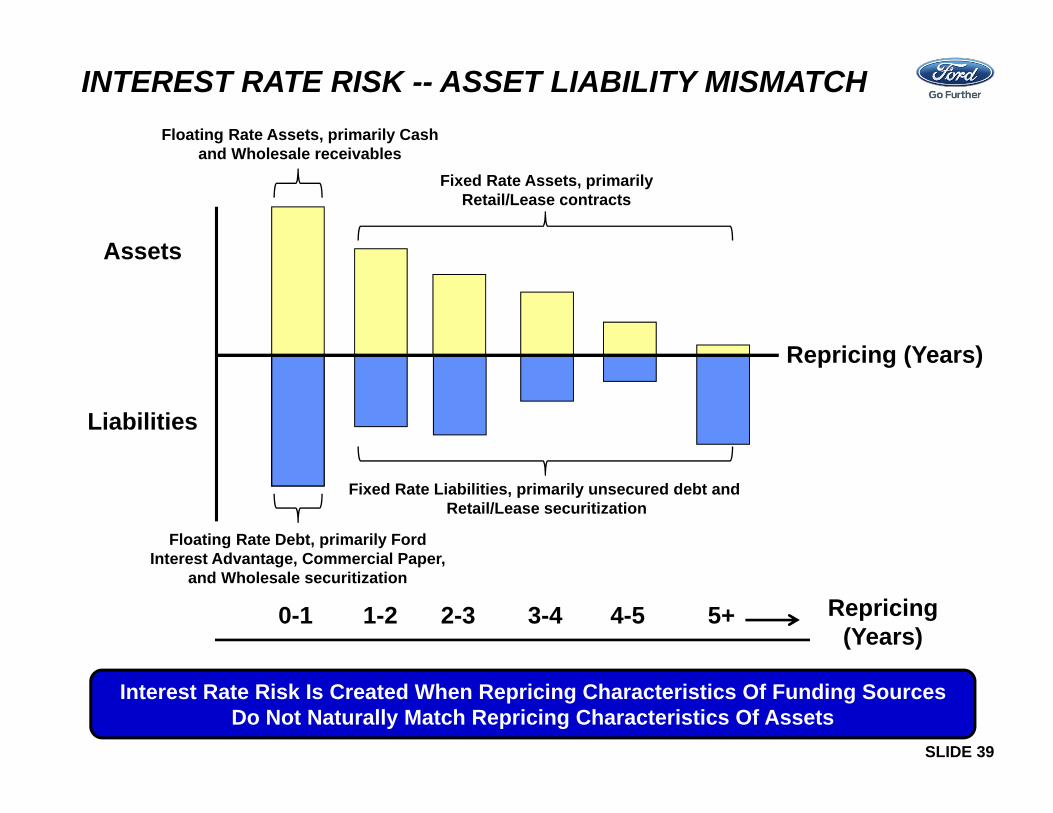

INTEREST RATE RISK -- ASSET LIABILITY MISMATCH

0-1 1-2 2-3 3-4 4-5 5+

Assets

Liabilities

Repricing (Years)

Repricing (Years)

Floating Rate Assets, primarily Cash and Wholesale receivables

Fixed Rate Assets, primarily Retail/Lease contracts

Floating Rate Debt, primarily Ford Interest Advantage, Commercial Paper,

and Wholesale securitization

Fixed Rate Liabilities, primarily unsecured debt and Retail/Lease securitization

Interest Rate Risk Is Created When Repricing Characteristics Of Funding Sources Do Not Naturally Match Repricing Characteristics Of Assets

SLIDE 40

Step 1:Excess long-term fixed rate debt is swapped to floating rate debt

Assets

Liabilities, Derivatives

& Equity

0-1 1-2 2-3 3-4 4-5 5+ Repricing (Years)

Step 2:Excess floating rate debt is swapped to fixed rate debt to match asset repricing profile in line with risk tolerance

0-1 1-2 2-3 3-4 4-5 5+ Repricing (Years)

Assets

INTEREST RATE RISK -- ASSET LIABILITY MISMATCH

Liabilities, Derivatives

& Equity

Swaps Are Used To Manage Our Interest Rate Exposure In Line With Risk Management Strategy And Tolerances

SLIDE 41

FORD CREDIT DERIVATIVE NOTIONAL

Despite The Significant Derivative Notional Balance, Ford Credit’s Derivatives Had A Minimal Impact On Total Profit

2013 2014(Bils.) (Bils.)

Interest Rate DerivativesPay-fix swaps 17$ 15$ Pay-float swaps 30 36 Securitization swaps 42 29

Subtotal interest rate derivatives $ 89 $ 80

Other DerivativesCross-currency swaps 3 2 Foreign currency forwards 2 2

Total derivative notional 94$ 84$

Memo:Non-designated derivative notional (Bils.) 75$ 61$ Income/(loss) from Unallocated Risk Management (Mils.) (53)$ (6)$ Income/(Loss) as a % of non-designated notional (Pct.) (0.07) % (0.01) %

SLIDE 42

FUNDING A STRONG FORD CREDIT BALANCE SHEET• Expanding and diversifying our funding programs globally

– Increasing mix of term debt, reducing annual financing requirements– Developing innovative funding platforms in mature and growth markets

• Maintaining strong liquidity to protect against funding disruptions– Targeting total liquidity of $25 billion +

• Delivering around 10% return on equity with sustainable distributions– Maintaining leverage between 8 and 9 to 1

• Targeting single-A credit rating profile

Strong Funding and Liquidity Profile Supports Growth in Receivables

Ford Credit Profit Reporting

SLIDE 44

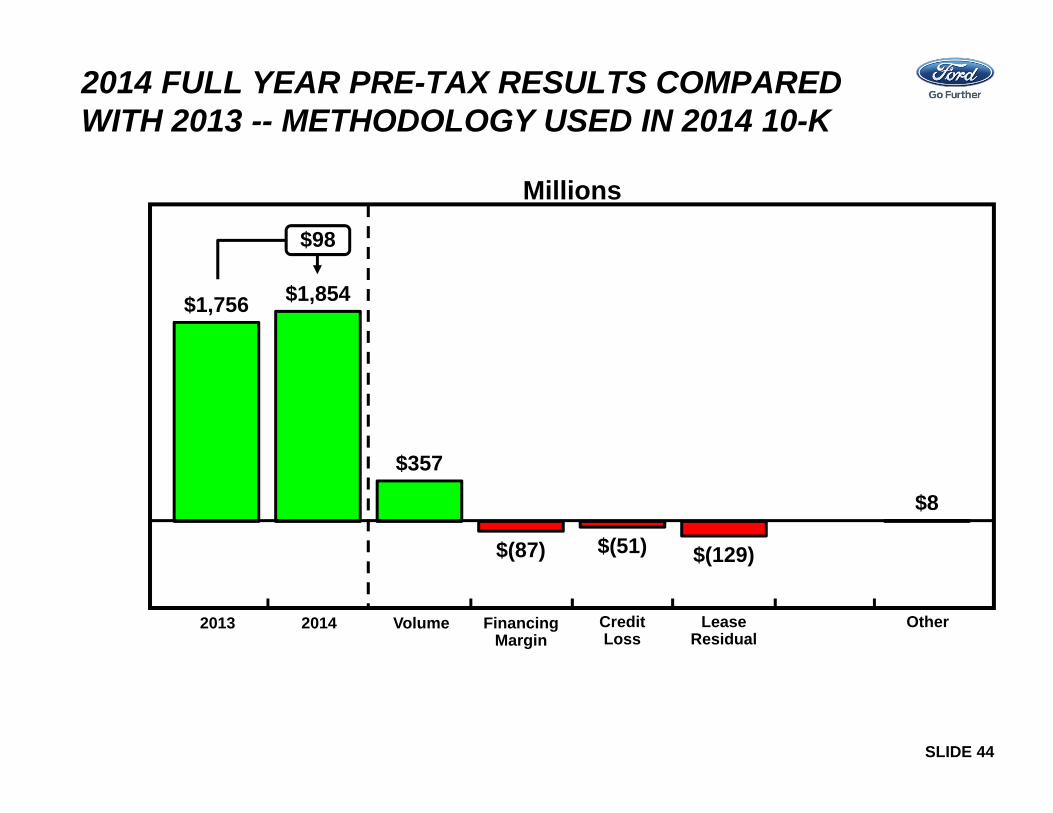

$1,756 $1,854

$357

$(87) $(51) $(129)

$8

Millions

$98

LeaseResidual

Volume20142013 CreditLoss

FinancingMargin

Other

2014 FULL YEAR PRE-TAX RESULTS COMPARED WITH 2013 -- METHODOLOGY USED IN 2014 10-K

SLIDE 45

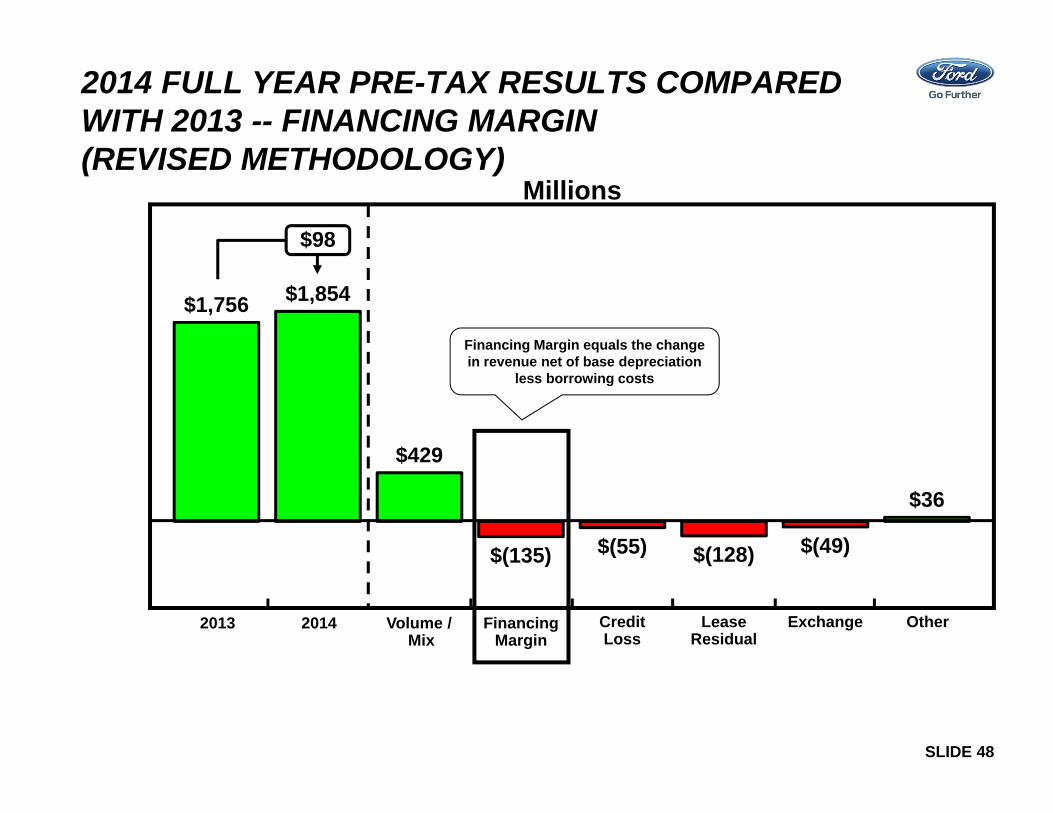

2014 FULL YEAR PRE-TAX RESULTS COMPARED WITH 2013 -- REVISED METHODOLOGY

$1,756 $1,854

$429

$(135) $(55) $(128) $(49)

$36

Millions

$98

LeaseResidual

Volume / Mix

20142013 CreditLoss

FinancingMargin

OtherExchange

• New variance category to isolate changes in pre-tax profit driven by changes in exchange rates

• Previously, pre-tax profit effect of changes in exchange rates was reflected in each causal factor

• Added Mix to the Volume category

• Previously, Mix (by default) was included in Financing Margin

SLIDE 46

2014 FULL YEAR PRE-TAX RESULTS COMPARED WITH 2013 -- VOLUME (REVISED METHODOLOGY)

$1,756 $1,854

$429

$(135) $(55) $(128) $(49)

$36

Millions

$98

LeaseResidual

20142013 CreditLoss

FinancingMargin

OtherExchange

• Volume represents the change in average receivables multiplied by the prior period financing margin yield at prior period exchange rates

• Mix represents changes in net financing margin driven by changes in the composition of our average managed receivables by product and by country or region

Volume / Mix

SLIDE 47

$92 $103

$113 $103

$113

VOLUME AND MIX PROFIT VARIANCES

Memo: Average Receivables at Incurred Exchange Rates

$96.4 $108.4 ~$119

Average Receivables at Prior Year Exchange Rates$108.9 ~$122

Managed Receivables (Bils.)Beginning of PeriodEnd of Period

2014 20152013

Volume and Mix Variances

$123-128

2014 Compared with 2013Volume

2014 Average Receivables at 2013 Exchange Rates (Bils.) 108.9$ 2013 Average Receivables 96.4 Increase / (Decrease) in Receivables 12.5$

Average 2013 Financing Margin ~ 2.80 %

Volume Variance (Mils.) ~ 350$

Mix (Primarily Higher Leases and China Receivables) ~ 79 Total Volume and Mix 429$

Directional 2015 Compared with 2014Volume

2015 Average Receivables at 2014 Exchange Rates (Bils.) ~ 122.0$ 2014 Average Receivables 108.4 Increase / (Decrease) in Receivables ~ 13.6$

Average 2014 Financing Margin (similar to 2014) ~ 2.80 %

Volume Variance (Mils.) ~ 380$

Mix (similar to 2014) ~ 80 Total Volume and Mix ~ 460$

SLIDE 48

2014 FULL YEAR PRE-TAX RESULTS COMPARED WITH 2013 -- FINANCING MARGIN (REVISED METHODOLOGY)

$1,756 $1,854

$429

$(135) $(55) $(128) $(49)

$36

Millions

$98

LeaseResidual

20142013 CreditLoss

FinancingMargin

OtherExchangeVolume / Mix

Financing Margin equals the change in revenue net of base depreciation

less borrowing costs

SLIDE 49

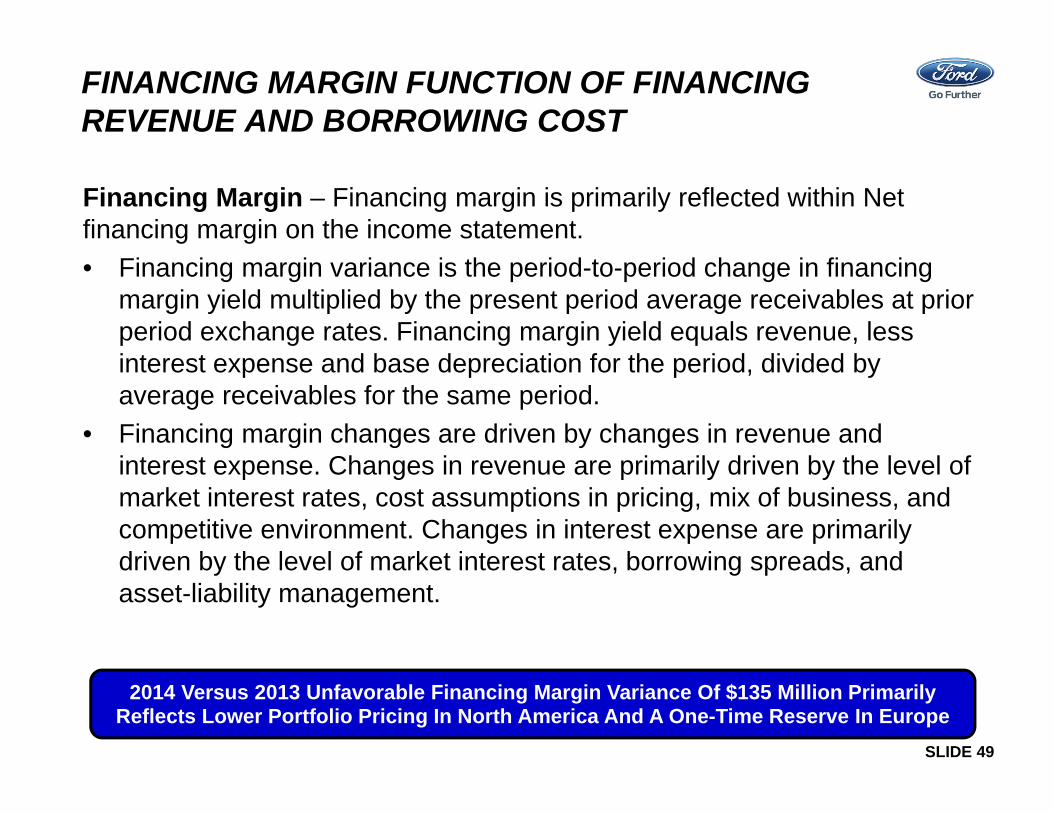

FINANCING MARGIN FUNCTION OF FINANCING REVENUE AND BORROWING COST

Financing Margin – Financing margin is primarily reflected within Net financing margin on the income statement.• Financing margin variance is the period-to-period change in financing

margin yield multiplied by the present period average receivables at prior period exchange rates. Financing margin yield equals revenue, less interest expense and base depreciation for the period, divided by average receivables for the same period.

• Financing margin changes are driven by changes in revenue and interest expense. Changes in revenue are primarily driven by the level of market interest rates, cost assumptions in pricing, mix of business, and competitive environment. Changes in interest expense are primarily driven by the level of market interest rates, borrowing spreads, and asset-liability management.

2014 Versus 2013 Unfavorable Financing Margin Variance Of $135 Million Primarily Reflects Lower Portfolio Pricing In North America And A One-Time Reserve In Europe

SLIDE 50

2014 FULL YEAR PRE-TAX RESULTS COMPARED WITH 2013 -- CREDIT LOSSES (REVISED METHODOLOGY)

$1,756 $1,854

$429

$(135) $(55) $(128) $(49)

$36

Millions

$98

LeaseResidual

20142013 CreditLoss

FinancingMargin

OtherExchangeVolume / Mix

Credit Loss equals the change in:• Charge-offs, plus• Changes in the Allowance for Credit

LossesAt prior period exchange rates

SLIDE 51

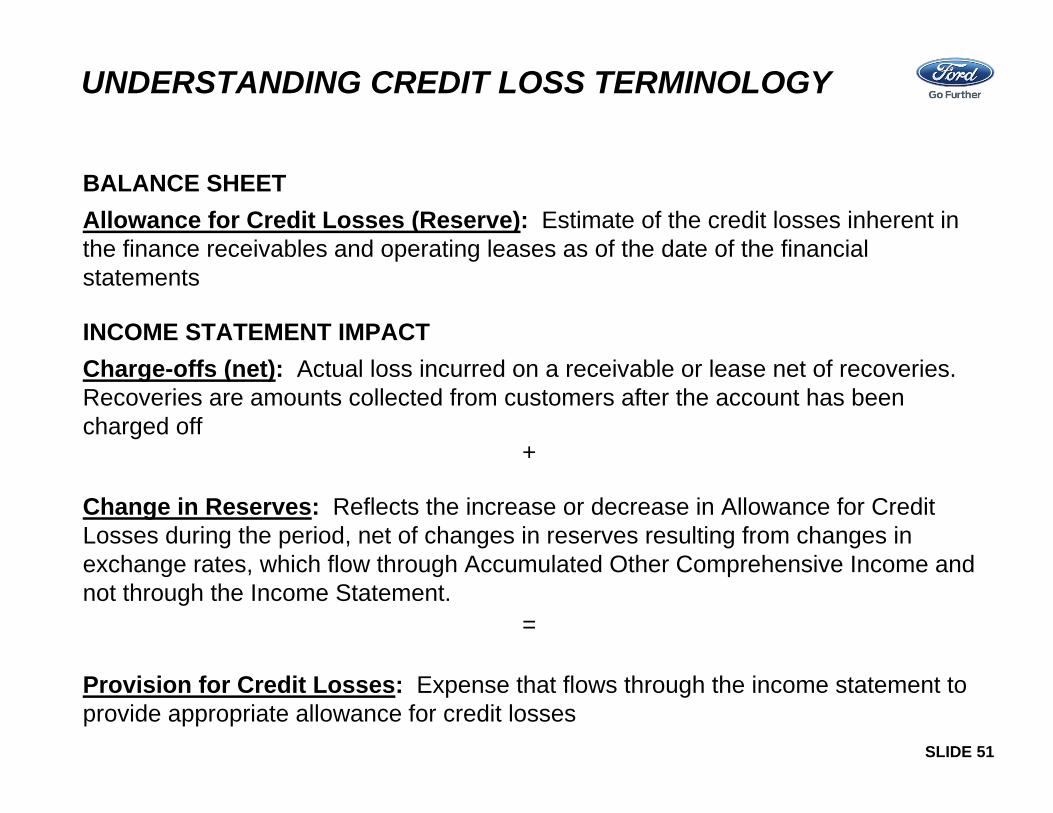

UNDERSTANDING CREDIT LOSS TERMINOLOGY

BALANCE SHEETAllowance for Credit Losses (Reserve): Estimate of the credit losses inherent in the finance receivables and operating leases as of the date of the financial statements

INCOME STATEMENT IMPACTCharge-offs (net): Actual loss incurred on a receivable or lease net of recoveries. Recoveries are amounts collected from customers after the account has been charged off

+

Change in Reserves: Reflects the increase or decrease in Allowance for Credit Losses during the period, net of changes in reserves resulting from changes in exchange rates, which flow through Accumulated Other Comprehensive Income and not through the Income Statement.

=

Provision for Credit Losses: Expense that flows through the income statement to provide appropriate allowance for credit losses

SLIDE 52

$136 $176 $209

$408 $380 $359

Worldwide On-Balance Sheet Charge-Offs and Allowance for Credit Losses (Bils.)

$28 $21

$(33)

$(7)

2014 FULL YEAR CREDIT LOSS VARIANCE EXPLANATION (REVISED METHODOLOGY)

Charge-Offs

20132012 2014

Reserves

MEMO: LTR (%) 0.16% 0.18% 0.19%

Profit Impact 2014 (Mils.)

Change in Reserves $ (7)Exchange Rate Impact on Reserves* (11)

Change in Reserves Variance $ (18)

Charge-Offs (33) Exchange Rate Impact on Losses (4)

Total Credit Loss Variance $ (55)

* In the absence of a stronger dollar, Reserves would have been about $370 million -- $11 million higher.

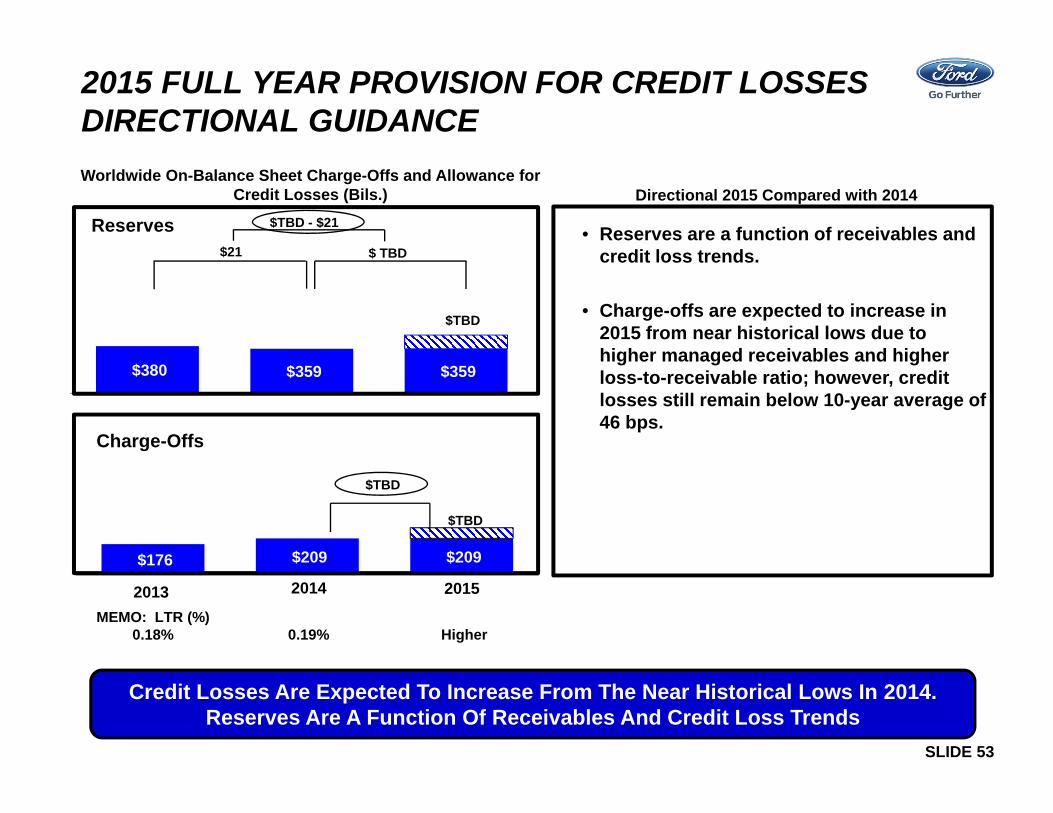

SLIDE 53

$380 $359 $359

$176 $209 $209

Worldwide On-Balance Sheet Charge-Offs and Allowance for Credit Losses (Bils.)

2015 FULL YEAR PROVISION FOR CREDIT LOSSES DIRECTIONAL GUIDANCE

• Reserves are a function of receivables and credit loss trends.

• Charge-offs are expected to increase in 2015 from near historical lows due to higher managed receivables and higher loss-to-receivable ratio; however, credit losses still remain below 10-year average of 46 bps.

Directional 2015 Compared with 2014

$21

$TBD - $21

$ TBD

$TBD

Charge-Offs

20142013 2015

Reserves

$TBD

MEMO: LTR (%) 0.18% 0.19% Higher

$TBD

Credit Losses Are Expected To Increase From The Near Historical Lows In 2014. Reserves Are A Function Of Receivables And Credit Loss Trends

SLIDE 54

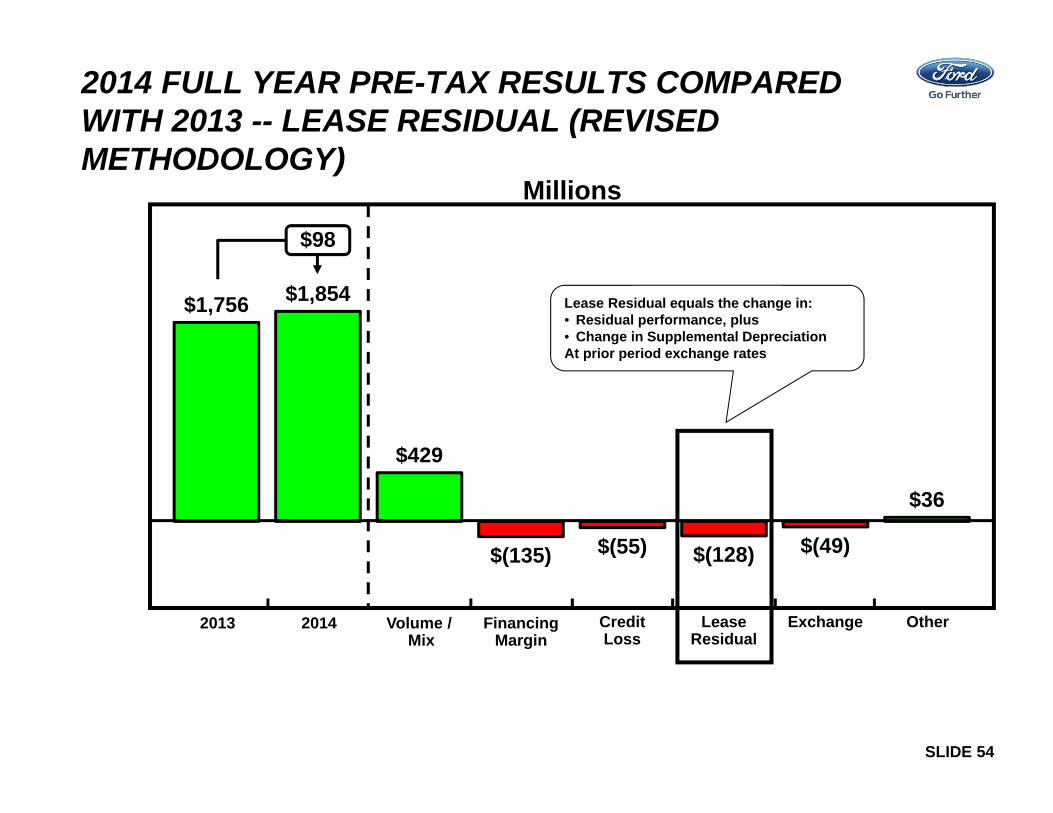

2014 FULL YEAR PRE-TAX RESULTS COMPARED WITH 2013 -- LEASE RESIDUAL (REVISED METHODOLOGY)

$1,756 $1,854

$429

$(135) $(55) $(128) $(49)

$36

Millions

$98

LeaseResidual

20142013 CreditLoss

FinancingMargin

OtherExchangeVolume / Mix

Lease Residual equals the change in:• Residual performance, plus• Change in Supplemental DepreciationAt prior period exchange rates

SLIDE 55

UNDERSTANDING LEASE RESIDUAL TERMINOLOGY -- INCOME STATEMENTRESIDUAL PERFORMANCE IN THE FINANCIAL STATEMENTSLease residual performance is included in depreciation in our financial statements, which is part of Net Financing Margin. For analytical purposes, we move the residual performance portion of depreciation from Net Financing Margin into its own category

RESIDUAL PERFORMANCESupplemental Depreciation: Reflects the increase or decrease in depreciation as a result of changes in the projected residual values beyond base depreciation at prior period exchange rates

+Residual Gains / Losses: Reflects the difference between the auction value and the depreciated value (base + supplemental depreciation) at prior period exchange rates

+Impairment (Rarely Used): Reflects a decrease in the book value of a lease due to significant decline in the value of the vehicles

=Lease Residual: The sum of the change in supplemental depreciation, residual gains or losses, and impairment for the period

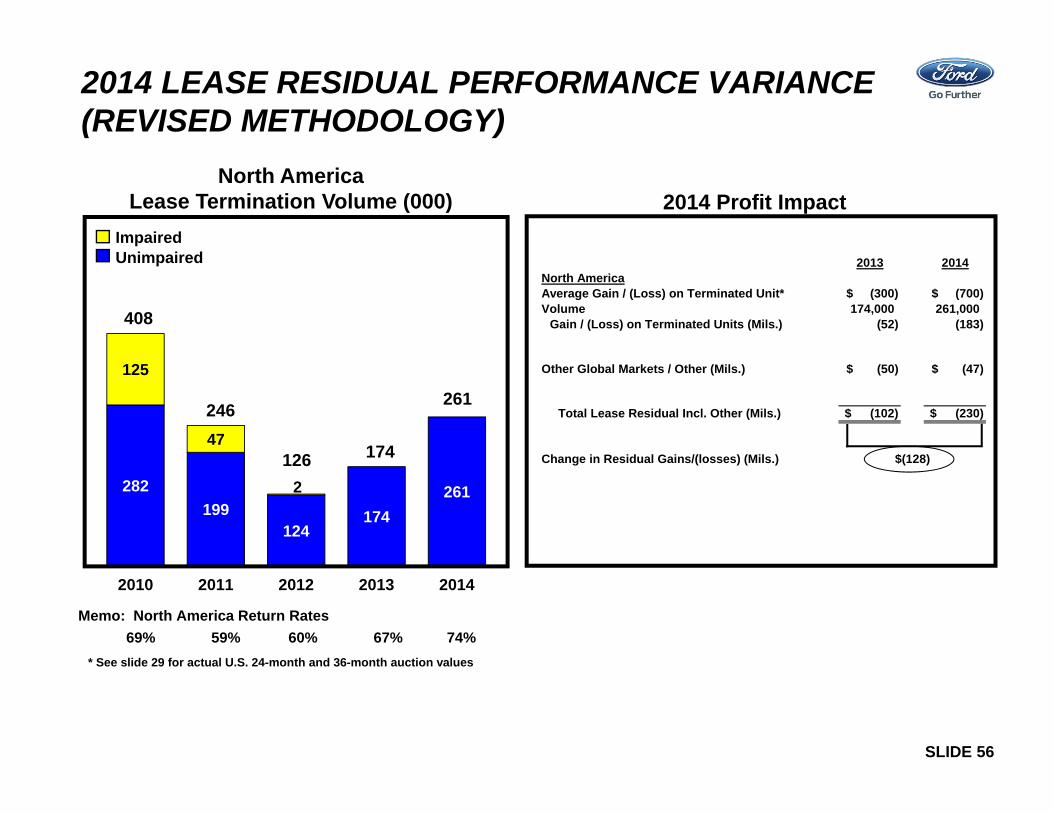

SLIDE 56

2014 LEASE RESIDUAL PERFORMANCE VARIANCE (REVISED METHODOLOGY)

282199

124174

261

125

47

2

2010 2011 2012 2013 2014

North America Lease Termination Volume (000)

ImpairedUnimpaired

246

126

408

2014 Profit Impact

* See slide 29 for actual U.S. 24-month and 36-month auction values

Memo: North America Return Rates 69% 59% 60% 67% 74%

174

261

2013 2014North AmericaAverage Gain / (Loss) on Terminated Unit* (300)$ (700)$ Volume 174,000 261,000

Gain / (Loss) on Terminated Units (Mils.) (52) (183)

Other Global Markets / Other (Mils.) (50)$ (47)$

Total Lease Residual Incl. Other (Mils.) (102)$ (230)$

Change in Residual Gains/(losses) (Mils.) $(128)

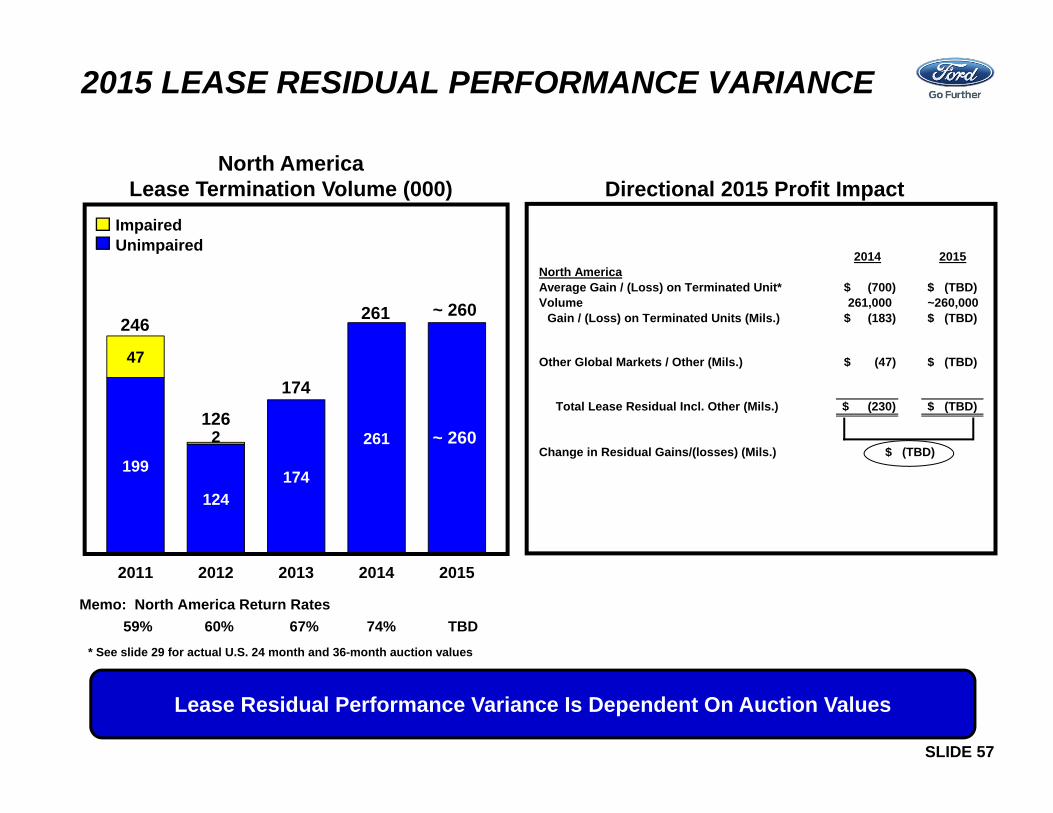

SLIDE 57

199

124174

261

47

2

2011 2012 2013 2014 2015

246

126

174

2015 LEASE RESIDUAL PERFORMANCE VARIANCE

ImpairedUnimpaired

Directional 2015 Profit Impact

Memo: North America Return Rates 59% 60% 67% 74% TBD

* See slide 29 for actual U.S. 24 month and 36-month auction values

Lease Residual Performance Variance Is Dependent On Auction Values

261 ~ 260

~ 260

North America Lease Termination Volume (000)

2014 2015North AmericaAverage Gain / (Loss) on Terminated Unit* (700)$ $ (TBD)Volume 261,000 ~260,000

Gain / (Loss) on Terminated Units (Mils.) (183)$ $ (TBD)

Other Global Markets / Other (Mils.) (47)$ $ (TBD)

Total Lease Residual Incl. Other (Mils.) (230)$ $ (TBD)

Change in Residual Gains/(losses) (Mils.) $ (TBD)

SLIDE 58

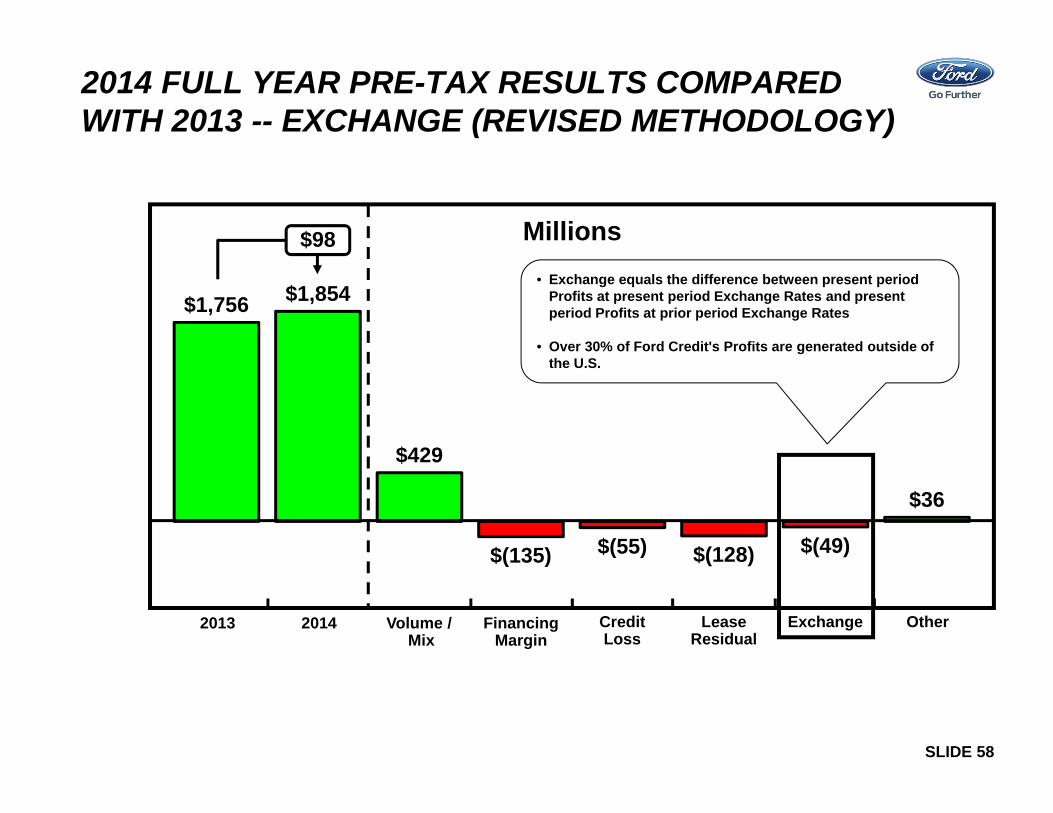

2014 FULL YEAR PRE-TAX RESULTS COMPARED WITH 2013 -- EXCHANGE (REVISED METHODOLOGY)

$1,756 $1,854

$429

$(135) $(55) $(128) $(49)

$36

Millions$98

LeaseResidual

20142013 CreditLoss

FinancingMargin

OtherExchangeVolume / Mix

• Exchange equals the difference between present period Profits at present period Exchange Rates and present period Profits at prior period Exchange Rates

• Over 30% of Ford Credit's Profits are generated outside of the U.S.

SLIDE 59

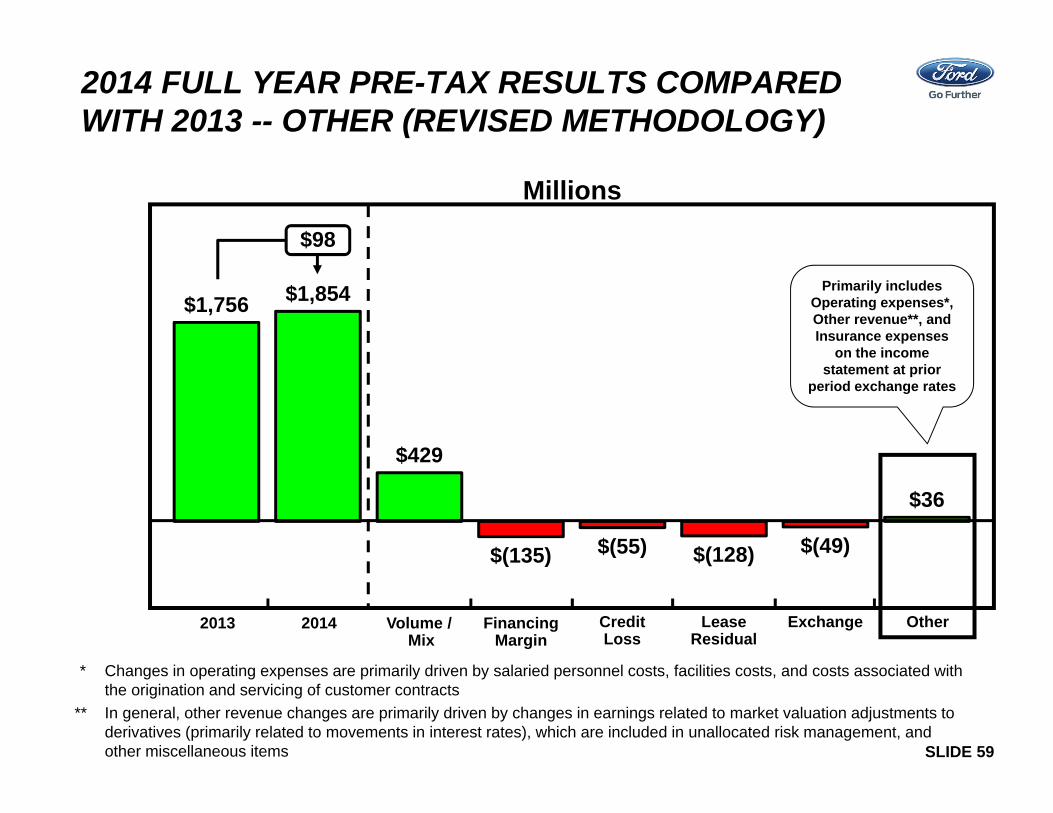

2014 FULL YEAR PRE-TAX RESULTS COMPARED WITH 2013 -- OTHER (REVISED METHODOLOGY)

$1,756 $1,854

$429

$(135) $(55) $(128) $(49)

$36

Millions

$98

LeaseResidual

20142013 CreditLoss

FinancingMargin

OtherExchangeVolume / Mix

Primarily includes Operating expenses*, Other revenue**, and Insurance expenses

on the income statement at prior

period exchange rates

* Changes in operating expenses are primarily driven by salaried personnel costs, facilities costs, and costs associated with the origination and servicing of customer contracts

** In general, other revenue changes are primarily driven by changes in earnings related to market valuation adjustments to derivatives (primarily related to movements in interest rates), which are included in unallocated risk management, and other miscellaneous items

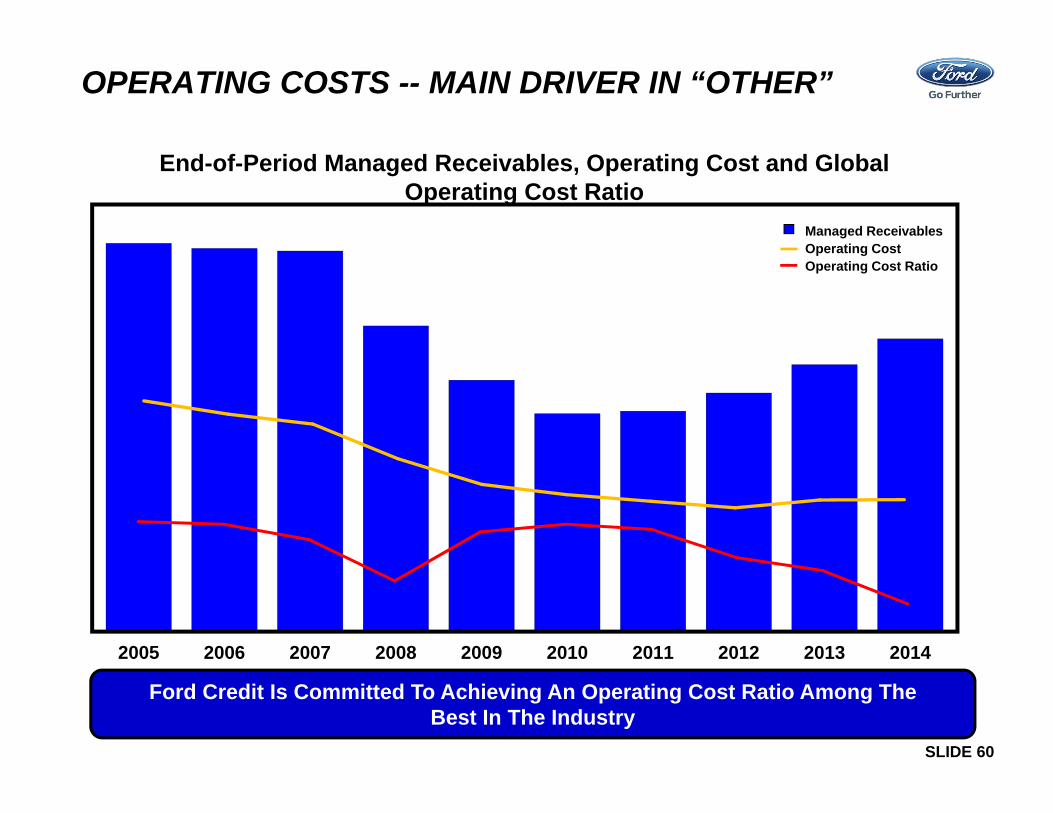

SLIDE 60

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

OPERATING COSTS -- MAIN DRIVER IN “OTHER”

End-of-Period Managed Receivables, Operating Cost and Global Operating Cost Ratio

Ford Credit Is Committed To Achieving An Operating Cost Ratio Among The Best In The Industry

Managed ReceivablesOperating CostOperating Cost Ratio

SLIDE 61

• Decline in industry sales volume, particularly in the United States, Europe, or China, due to financial crisis, recession, geopolitical events, or other factors;• Decline in Ford’s market share or failure to achieve growth;• Lower-than-anticipated market acceptance of Ford’s new or existing products;• Market shift away from sales of larger, more profitable vehicles beyond Ford’s current planning assumption, particularly in the United States;• An increase in or continued volatility of fuel prices, or reduced availability of fuel;• Continued or increased price competition resulting from industry excess capacity, currency fluctuations, or other factors;• Fluctuations in foreign currency exchange rates, commodity prices, and interest rates;• Adverse effects resulting from economic, geopolitical, or other events;• Economic distress of suppliers that may require Ford to provide substantial financial support or take other measures to ensure supplies of components or materials and

could increase costs, affect liquidity, or cause production constraints or disruptions;• Work stoppages at Ford or supplier facilities or other limitations on production (whether as a result of labor disputes, natural or man-made disasters, tight credit markets or

other financial distress, production constraints or difficulties, or other factors);• Single-source supply of components or materials;• Labor or other constraints on Ford’s ability to maintain competitive cost structure;• Substantial pension and postretirement health care and life insurance liabilities impairing liquidity or financial condition;• Worse-than-assumed economic and demographic experience for postretirement benefit plans (e.g., discount rates or investment returns);• Restriction on use of tax attributes from tax law “ownership change;”• The discovery of defects in vehicles resulting in delays in new model launches, recall campaigns, or increased warranty costs;• Increased safety, emissions, fuel economy, or other regulations resulting in higher costs, cash expenditures, and/or sales restrictions; • Unusual or significant litigation, governmental investigations, or adverse publicity arising out of alleged defects in products, perceived environmental impacts, or otherwise; • A change in requirements under long-term supply arrangements committing Ford to purchase minimum or fixed quantities of certain parts, or to pay a minimum amount to

the seller (“take-or-pay” contracts); • Adverse effects on results from a decrease in or cessation or clawback of government incentives related to investments; • Inherent limitations of internal controls impacting financial statements and safeguarding of assets; • Cybersecurity risks to operational systems, security systems, or infrastructure owned by Ford, Ford Credit, or a third-party vendor or supplier;• Failure of financial institutions to fulfill commitments under committed credit and liquidity facilities; • Inability of Ford Credit to access debt, securitization, or derivative markets around the world at competitive rates or in sufficient amounts, due to credit rating downgrades,

market volatility, market disruption, regulatory requirements, or other factors; • Higher-than-expected credit losses, lower-than-anticipated residual values, or higher-than-expected return volumes for leased vehicles; • Increased competition from banks, financial institutions, or other third parties seeking to increase their share of financing Ford vehicles; and • New or increased credit, consumer, or data protection or other regulations resulting in higher costs and/or additional financing restrictions.

Statements included or incorporated by reference herein may constitute “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. Forward-looking statements are based on expectations, forecasts, and assumptions by our management and involve a number of risks, uncertainties, and other factors that could cause actual results to differ materially from those stated, including, without limitation:

We cannot be certain that any expectation, forecast, or assumption made in preparing forward-looking statements will prove accurate, or that any projection will be realized. It is to be expected that there may be differences between projected and actual results. Our forward-looking statements speak only as of the date of their initial issuance, and we do not undertake any obligation to update or revise publicly any forward-looking statement, whether as a result of new information, future events, or otherwise. For additional discussion, see "Item 1A. Risk Factors" in our Annual Report on Form 10-K for the year ended December 31, 2014, as updated by our subsequent Quarterly Reports on Form 10-Q and Current Reports on Form 8-K.

RISK FACTORS

APPENDIX

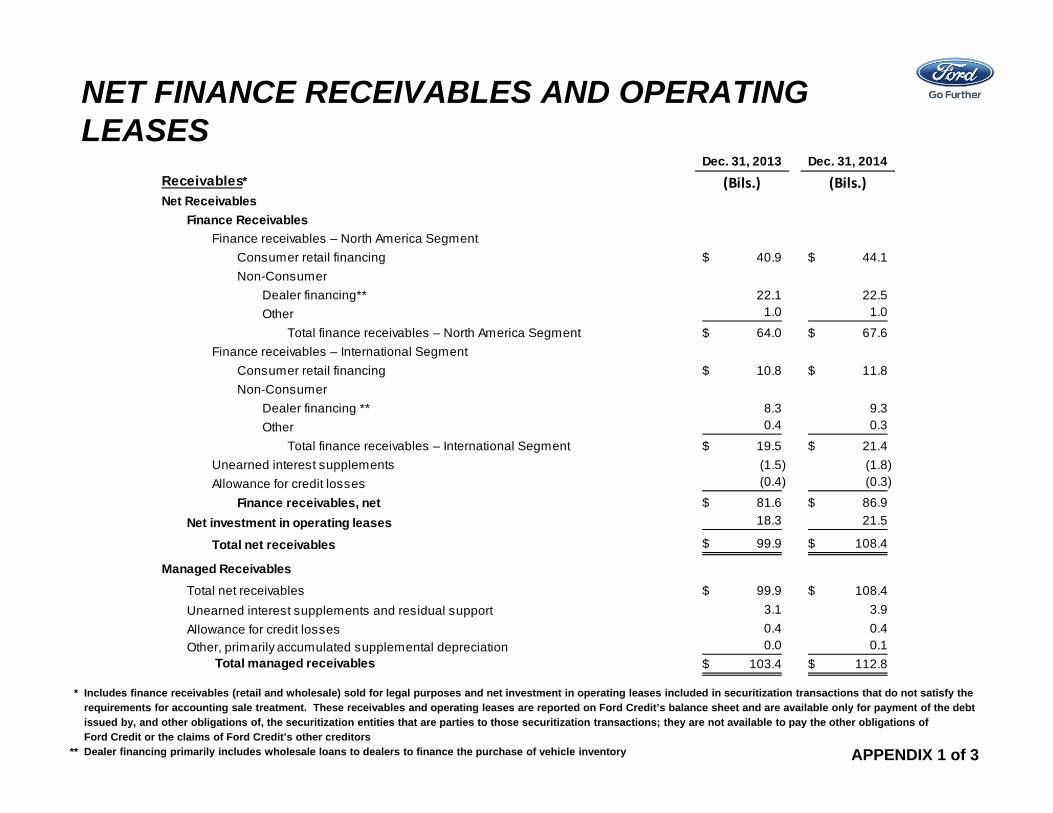

NET FINANCE RECEIVABLES AND OPERATING LEASES

APPENDIX 1 of 3

Dec. 31, 2013 Dec. 31, 2014Receivables* (Bils.) (Bils.)Net Receivables

Finance ReceivablesFinance receivables – North America Segment

Consumer retail financing 40.9$ 44.1$ Non-Consumer

Dealer financing** 22.1 22.5 Other 1.0 1.0

Total finance receivables – North America Segment 64.0$ 67.6$ Finance receivables – International Segment

Consumer retail financing 10.8$ 11.8$ Non-Consumer

Dealer financing ** 8.3 9.3 Other 0.4 0.3

Total finance receivables – International Segment 19.5$ 21.4$ Unearned interest supplements (1.5) (1.8) Allowance for credit losses (0.4) (0.3)

Finance receivables, net 81.6$ 86.9$ Net investment in operating leases 18.3 21.5

Total net receivables 99.9$ 108.4$

Managed ReceivablesTotal net receivables 99.9$ 108.4$ Unearned interest supplements and residual support 3.1 3.9 Allowance for credit losses 0.4 0.4 Other, primarily accumulated supplemental depreciation 0.0 0.1

Total managed receivables 103.4$ 112.8$

* Includes finance receivables (retail and wholesale) sold for legal purposes and net investment in operating leases included in securitization transactions that do not satisfy the requirements for accounting sale treatment. These receivables and operating leases are reported on Ford Credit’s balance sheet and are available only for payment of the debt issued by, and other obligations of, the securitization entities that are parties to those securitization transactions; they are not available to pay the other obligations of Ford Credit or the claims of Ford Credit’s other creditors

** Dealer financing primarily includes wholesale loans to dealers to finance the purchase of vehicle inventory

RECONCILIATION OF MANAGED LEVERAGE TO FINANCIAL STATEMENT LEVERAGE

APPENDIX 2 of 3

2013 2014Dec. 31 Dec. 31(Bils.) (Bils.)

Leverage Calculation Total Debt* $ 98.7 $ 105.0 Adjustments for Cash, Cash Equivalents, and Marketable Securities** (10.8) (8.9)Adjustments for Derivative Accounting*** (0.2) (0.4)

Total Adjusted Debt $ 87.7 $ 95.7

Equity**** $ 10.6 $ 11.4 Adjustments for Derivative Accounting*** (0.3) (0.4)

Total Adjusted Equity $ 10.3 $ 11.0

Financial Statement Leverage (to 1) 9.3 9.2 Managed Leverage (to 1)***** 8.5 8.7

* Includes debt reported on Ford Credit's balance sheet that is issued in securitization transactions and payable only out of collections on the underlying securitized assets and related enhancements. Ford Credit holds the right to receive the excess cash flows not needed to pay the debt issued by, and other obligations of, the securitization entities that are parties to those securitization transactions

** Excludes marketable securities related to insurance activities*** Primarily related to market valuation adjustments to derivatives due to movements in interest rates. Adjustments to debt are related to designated fair value hedges

and adjustments to equity are related to retained earnings**** Shareholder's interest reported on Ford Credit's balance sheet

***** Equals total adjusted debt over total adjusted equity

IMPACT OF ON-BALANCE SHEET SECURITIZATION

Impact of On-Balance Sheet Securitization – receivables include finance receivables (retail and wholesale) sold for legal purposes and net investment in operating leases included in securitization transactions that do not satisfy the requirements for accounting sale treatment. These receivables and operating leases are reported on Ford Credit’s balance sheet and are available only for payment of the debt issued by, and other obligations of, the securitization entities that are parties to those securitization transactions; they are not available to pay the other obligations of Ford Credit or the claims of Ford Credit’s other creditors. Total debt includes debt reported on Ford Credit’s balance sheet that is issued in securitization transactions and payable only out of collections on the underlying securitized assets and related enhancements. Ford Credit holds the right to receive the excess cash flows not needed to pay the debt issued by, and other obligations of, the securitization entities that are parties to those securitization transactions.

APPENDIX 3 of 3

SLIDE 66

FURTHER INFORMATION

Ford Investor Relations Contacts:Fixed Income Investors:

Stephen Dahle (U.S.-based)[email protected]

Information on Ford:• www.shareholder.ford.com• 10-K Annual Reports• 10-Q Quarterly Reports• 8-K Current Reports• Ford University• 2013/2014 Sustainability Report

– www.corporate.ford.com/microsites/sustainability-report-2013-14/default.html

Information on Ford Motor Credit Company:• www.fordcredit.com/investor-center• 10-K Annual Reports• 10-Q Quarterly Reports• 8-K Current Reports• Ford Credit University