2015 CEB Tower Group Mar2015

14

CEB TOWERGROUP | RETAIL BANKING ENTERPRISE FRAUD MANAGEMENT MARKET UPDATE January 2015 Restoring Consumer Confidence Through Enterprise Fraud Management Enterprise Fraud Management Market Update Abstract Prepared For:

-

Upload

ajay-alex -

Category

Technology

-

view

109 -

download

5

Transcript of 2015 CEB Tower Group Mar2015

CEB TOWERGROUP | RETAIL BANKING

ENTERPRISE FRAUD MANAGEMENT MARKET UPDATE

January 2015

Restoring Consumer Confidence Through Enterprise Fraud Management Enterprise Fraud Management Market Update Abstract

Prepared For:

CEB TOWERGROUP | RETAIL BANKING

ENTERPRISE FRAUD MANAGEMENT MARKET UPDATE

EXECUTIVE SUMMARY

While data breaches are hardly the sole driver for fraud and identity theft, recent major retail breaches have put fraud management in the public spotlight like never before. Overall fraud increased, both in the incidences (+4.9%) and total dollar amount (+14.9%), even in regions where fraud management solutions are ubiquitous. There is a constant downward trend in costs per fraud incidence, indicating positive momentum in dealing with fraud even as the numbers grow. We recommend banks take the following actions to get the most out of their fraud management strategies:

1) Establish key metrics on cost per fraud incident. As complex data analysis drives improvements to fraud detection, fraud solutions must also turn analytics inward to improve cost per incidence and other key metrics.

2) Enable development of better tools for consumers. Consumers take little action to address fraud because they lack the tools to do so. This inaction is often mistaken for apathy. Back-office improvements in fraud management should continue to enable better consumer-facing tools.

3)Don’t break down fraud management siloes, but build efficiencies on common processes. While investment in specialized solutions continues, efficiency gains can be made by recognizing commonalities in data and process management.

KEY MARKET TRENDS

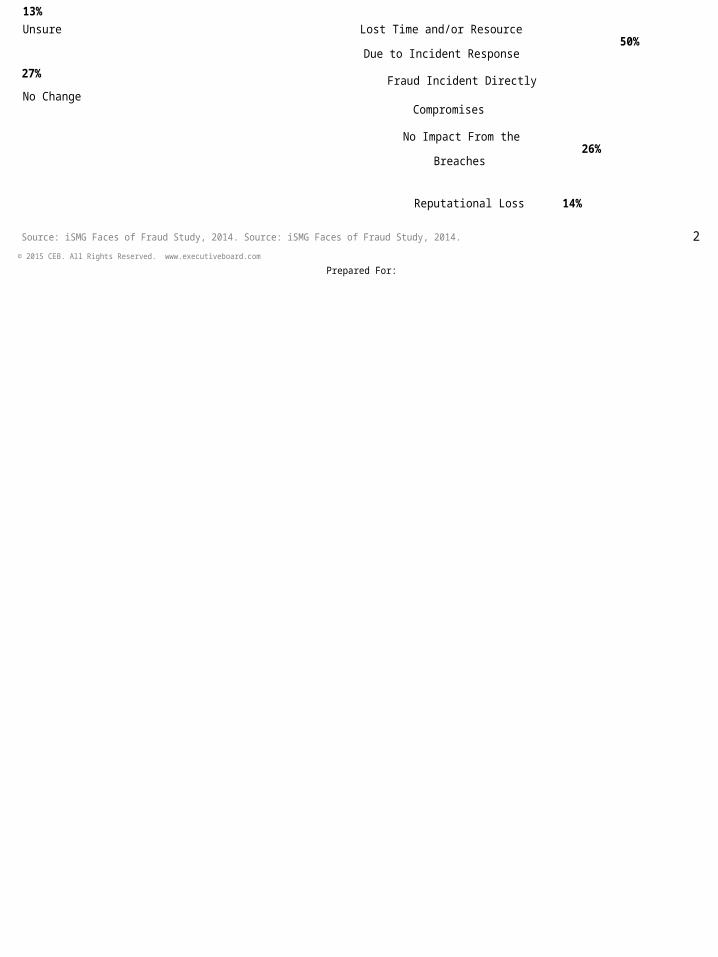

THE FINANCIAL IMPACTS OF FRAUD GO BEYOND THEFT Reported fraud incidences are climbing, and the majority of banks indicate an increase in financial losses over 2014

(Figure 1). There has been a steady beat of high profile data breaches which increase the costs of managing data theft and further damage customer confidence. While difficult to quantify the direct impact fraud has, these breaches combine to undercut the collective confidence in banks’ ability to stem the tide of compromised credentials and their use. The impacts to financial institutions come in the form of measurable effects (reissuing payment cards, lost time and resources from having to respond to fraud incidences), but also the less tangible, but perhaps more alarming impact: the reputational damage incurred by banks (Figure 2).

Figure 1 Figure 2

Financial Losses from Fraud in 2014 Percentage of Respondents

9%

Impact of Data Breaches on Banks and Customers Percentage of Bank Respondents, Multiple Responses Allowed

51%

13%

Unsure

27%

Lost Time and/or Resource50%

Due to Incident Response

Fraud Incident DirectlyNo Change

Compromises

No Impact From the26%

Breaches

Reputational Loss

Source: iSMG Faces of Fraud Study, 2014. Source: iSMG Faces of Fraud Study, 2014.

14%

2

© 2015 CEB. All Rights Reserved. www.executiveboard.com

Prepared For:

CEB TOWERGROUP | RETAIL BANKING

ENTERPRISE FRAUD MANAGEMENT MARKET UPDATE

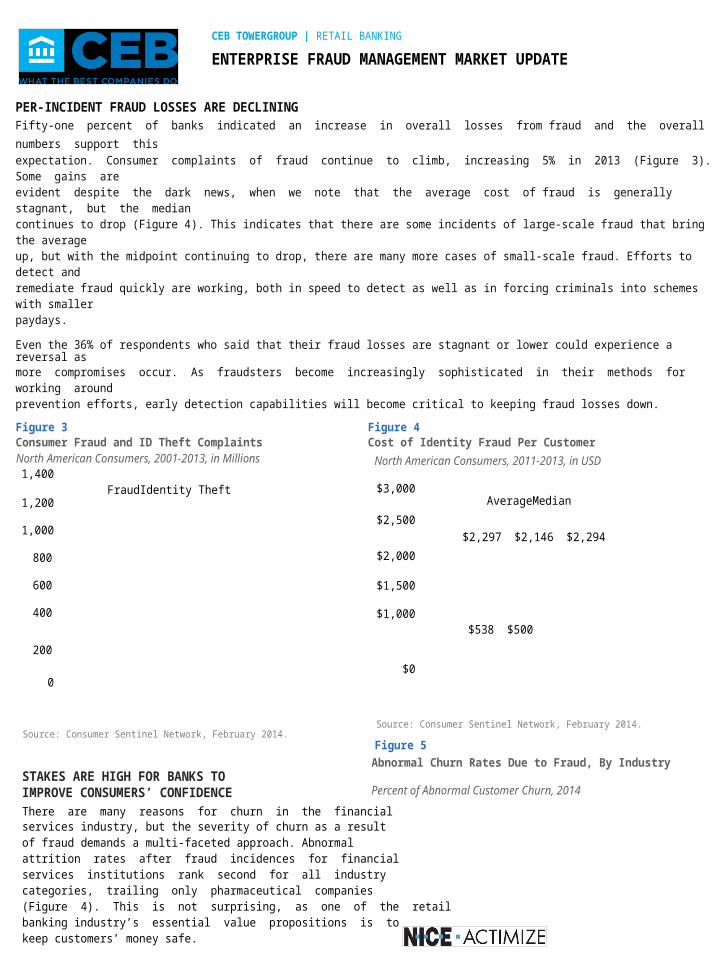

PER-INCIDENT FRAUD LOSSES ARE DECLINING Fifty-one percent of banks indicated an increase in overall losses from fraud and the overall numbers support this expectation. Consumer complaints of fraud continue to climb, increasing 5% in 2013 (Figure 3). Some gains are evident despite the dark news, when we note that the average cost of fraud is generally stagnant, but the median continues to drop (Figure 4). This indicates that there are some incidents of large-scale fraud that bring the average up, but with the midpoint continuing to drop, there are many more cases of small-scale fraud. Efforts to detect and remediate fraud quickly are working, both in speed to detect as well as in forcing criminals into schemes with smaller paydays.

Even the 36% of respondents who said that their fraud losses are stagnant or lower could experience a reversal as more compromises occur. As fraudsters become increasingly sophisticated in their methods for working around prevention efforts, early detection capabilities will become critical to keeping fraud losses down.

Figure 3 Consumer Fraud and ID Theft Complaints North American Consumers, 2001-2013, in Millions

1,400FraudIdentity Theft

1,200

1,000

800

600

400

Figure 4 Cost of Identity Fraud Per Customer

North American Consumers, 2011-2013, in USD

$3,000AverageMedian

$2,500

$2,297 $2,146 $2,294

$2,000

$1,500

$1,000$538 $500

200

$00

Source: Consumer Sentinel Network, February 2014. Source: Consumer Sentinel Network, February 2014.

Figure 5

Abnormal Churn Rates Due to Fraud, By Industry STAKES ARE HIGH FOR BANKS TO IMPROVE CONSUMERS’ CONFIDENCE Percent of Abnormal Customer Churn, 2014

There are many reasons for churn in the financial services industry, but the severity of churn as a result of fraud demands a multi-faceted approach. Abnormal attrition rates after fraud incidences for financial services institutions rank second for all industry categories, trailing only pharmaceutical companies (Figure 4). This is not surprising, as one of the retail banking industry’s essential value propositions is to keep customers’ money safe.

If financial services organizations cannot restore the confidence in their ability to protect consumer information and finances, this churn rate may increase as consumers question whether they need banking services and begin to explore solutions of non-traditional competitors.

CEB TOWERGROUP | RETAIL BANKING

ENTERPRISE FRAUD MANAGEMENT MARKET UPDATE

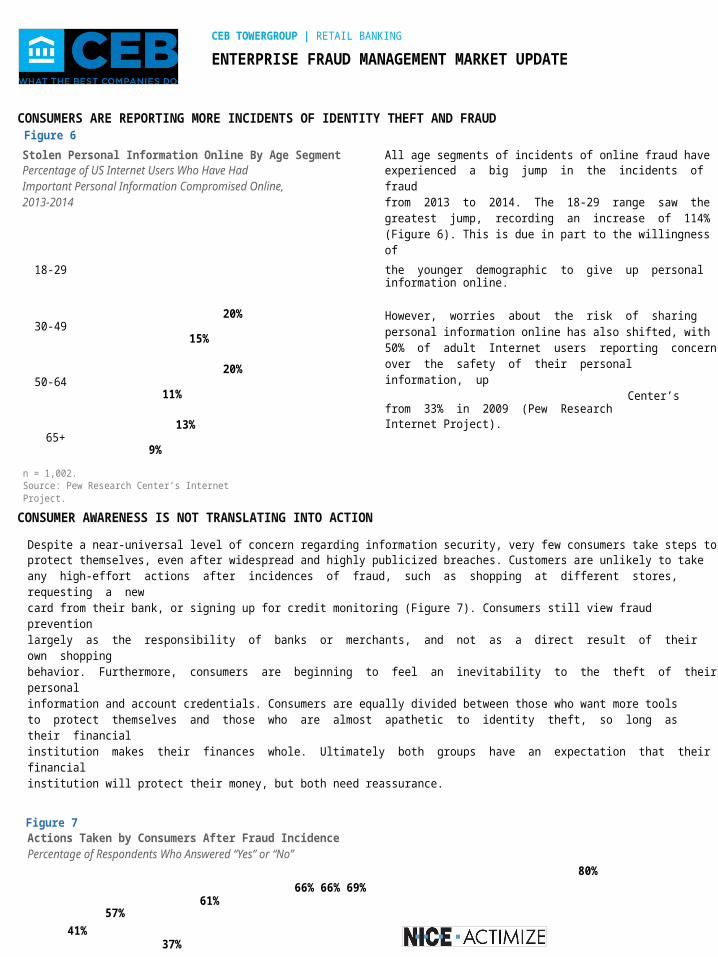

CONSUMERS ARE REPORTING MORE INCIDENTS OF IDENTITY THEFT AND FRAUD Figure 6

Stolen Personal Information Online By Age Segment Percentage of US Internet Users Who Have Had Important Personal Information Compromised Online, 2013-2014

All age segments of incidents of online fraud have experienced a big jump in the incidents of fraud from 2013 to 2014. The 18-29 range saw the greatest jump, recording an increase of 114% (Figure 6). This is due in part to the willingness of

18-29 the younger demographic to give up personal information online.

20% 30-49

15%

20% 50-64

11%

13% 65+

9%

n = 1,002. Source: Pew Research Center’s Internet Project.

However, worries about the risk of sharing personal information online has also shifted, with 50% of adult Internet users reporting concern over the safety of their personal information, up

Center’s from 33% in 2009 (Pew Research Internet Project).

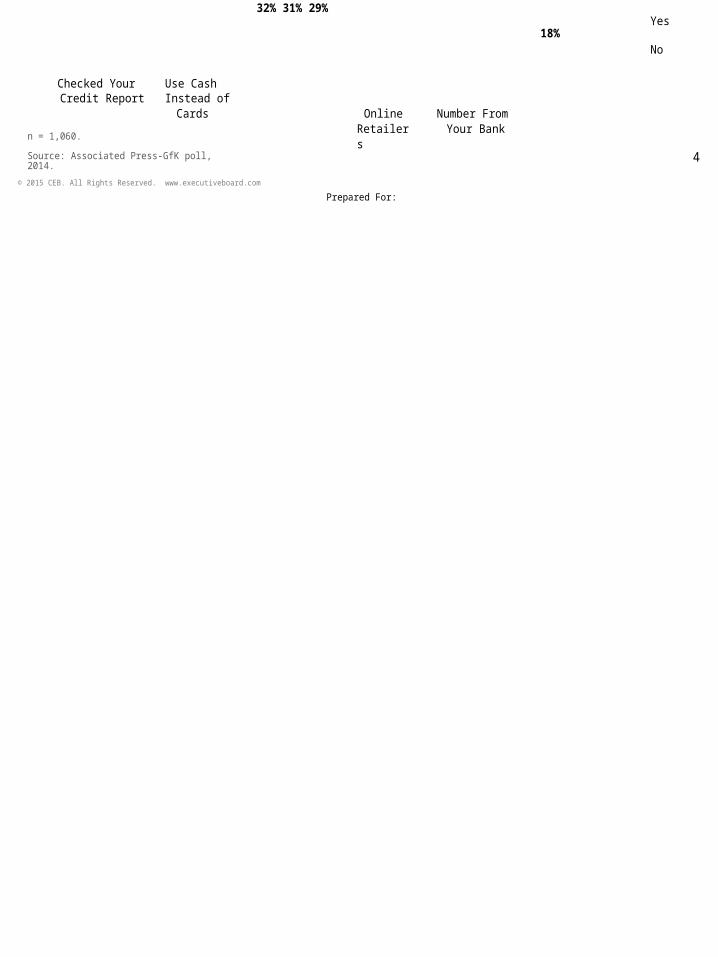

CONSUMER AWARENESS IS NOT TRANSLATING INTO ACTION

Despite a near-universal level of concern regarding information security, very few consumers take steps to protect themselves, even after widespread and highly publicized breaches. Customers are unlikely to take any high-effort actions after incidences of fraud, such as shopping at different stores, requesting a new card from their bank, or signing up for credit monitoring (Figure 7). Consumers still view fraud prevention largely as the responsibility of banks or merchants, and not as a direct result of their own shopping behavior. Furthermore, consumers are beginning to feel an inevitability to the theft of their personal information and account credentials. Consumers are equally divided between those who want more tools to protect themselves and those who are almost apathetic to identity theft, so long as their financial institution makes their finances whole. Ultimately both groups have an expectation that their financial institution will protect their money, but both need reassurance.

Figure 7 Actions Taken by Consumers After Fraud Incidence Percentage of Respondents Who Answered “Yes” or “No”

80%

66% 66% 69% 61%

57%

41% 37%

32% 31% 29% Yes

18% No

Checked YourCredit Report

Cards

n = 1,060.

Use CashInstead of

OnlineRetailers

Number FromYour Bank

Source: Associated Press-GfK poll, 2014. 4 © 2015 CEB. All Rights Reserved. www.executiveboard.com

Prepared For:

CEB TOWERGROUP | RETAIL BANKING

ENTERPRISE FRAUD MANAGEMENT MARKET UPDATE

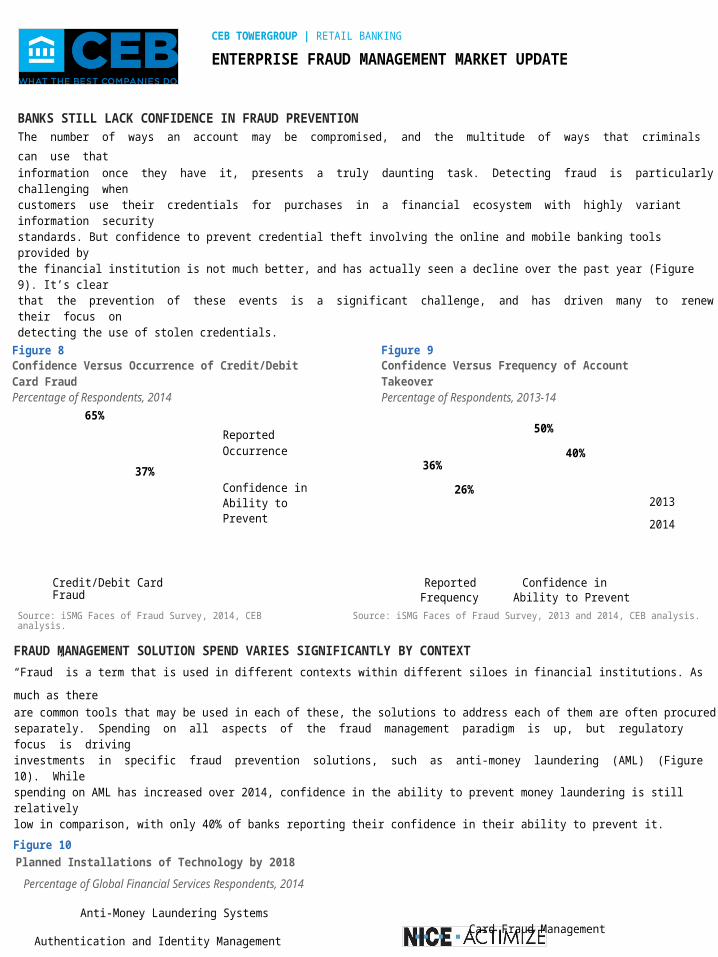

BANKS STILL LACK CONFIDENCE IN FRAUD PREVENTION The number of ways an account may be compromised, and the multitude of ways that criminals can use that

information once they have it, presents a truly daunting task. Detecting fraud is particularly challenging when customers use their credentials for purchases in a financial ecosystem with highly variant information security standards. But confidence to prevent credential theft involving the online and mobile banking tools provided by the financial institution is not much better, and has actually seen a decline over the past year (Figure 9). It’s clear that the prevention of these events is a significant challenge, and has driven many to renew their focus on detecting the use of stolen credentials.

Figure 8 Confidence Versus Occurrence of Credit/Debit Card Fraud Percentage of Respondents, 2014

65%

ReportedOccurrence

37% Confidence inAbility toPrevent

Figure 9 Confidence Versus Frequency of Account Takeover Percentage of Respondents, 2013-14

50%

40% 36%

26% 2013

2014

Credit/Debit Card Fraud ReportedFrequency

Confidence inAbility to Prevent

Source: iSMG Faces of Fraud Survey, 2014, CEB analysis. Source: iSMG Faces of Fraud Survey, 2013 and 2014, CEB analysis.

FRAUD MANAGEMENT SOLUTION SPEND VARIES SIGNIFICANTLY BY CONTEXT

“Fraud” is a term that is used in different contexts within different siloes in financial institutions. As much as there

are common tools that may be used in each of these, the solutions to address each of them are often procured separately. Spending on all aspects of the fraud management paradigm is up, but regulatory focus is driving investments in specific fraud prevention solutions, such as anti-money laundering (AML) (Figure 10). While spending on AML has increased over 2014, confidence in the ability to prevent money laundering is still relatively low in comparison, with only 40% of banks reporting their confidence in their ability to prevent it.

Figure 10

Planned Installations of Technology by 2018

Percentage of Global Financial Services Respondents, 2014

Anti-Money Laundering Systems

Authentication and Identity Management

Card Fraud Management

Fraud Management for Commercial Banks

Fraud Management for Retail Banks

Know Your Customer

n = 39-101. Source: CEB 2013-2014 Technology Adoption & Investment Survey.

41%

21%

30%

34%

22%

32%

5 © 2015 CEB. All Rights Reserved. www.executiveboard.com

Prepared For:

CEB TOWERGROUP | RETAIL BANKING

ENTERPRISE FRAUD MANAGEMENT MARKET UPDATE

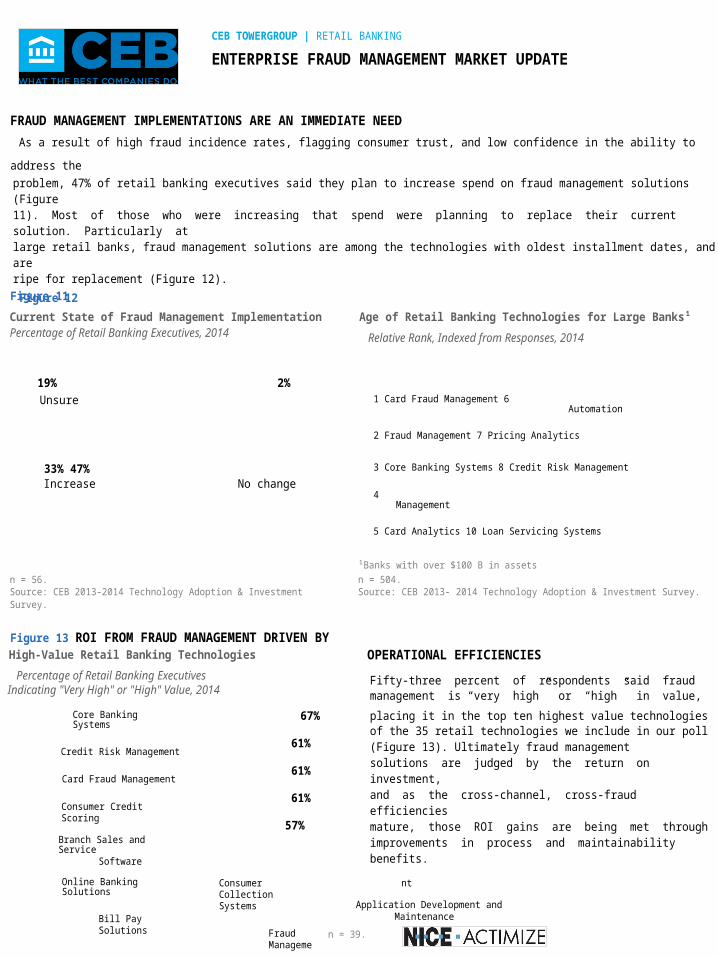

FRAUD MANAGEMENT IMPLEMENTATIONS ARE AN IMMEDIATE NEED

As a result of high fraud incidence rates, flagging consumer trust, and low confidence in the ability to address the

problem, 47% of retail banking executives said they plan to increase spend on fraud management solutions (Figure 11). Most of those who were increasing that spend were planning to replace their current solution. Particularly at large retail banks, fraud management solutions are among the technologies with oldest installment dates, and are ripe for replacement (Figure 12).

Figure 11

Current State of Fraud Management Implementation Percentage of Retail Banking Executives, 2014

Age of Retail Banking Technologies for Large Banks¹

Relative Rank, Indexed from Responses, 2014

Technologies with Oldest Install Dates 19% 2%

Unsure

33% 47%

1 Card Fraud Management 6 Automation

2 Fraud Management 7 Pricing Analytics

3 Core Banking Systems 8 Credit Risk Management

Increase No change 4

Management

5 Card Analytics 10 Loan Servicing Systems

¹Banks with over $100 B in assets

n = 56. Source: CEB 2013-2014 Technology Adoption & Investment Survey.

n = 504. Source: CEB 2013- 2014 Technology Adoption & Investment Survey.

Figure 13 ROI FROM FRAUD MANAGEMENT DRIVEN BY High-Value Retail Banking Technologies

Percentage of Retail Banking Executives Indicating "Very High" or "High" Value, 2014

OPERATIONAL EFFICIENCIES

Fifty-three percent of respondents said fraud management is “very high” or “high” in value,

Core Banking Systems

Credit Risk Management

Card Fraud Management

Consumer Credit Scoring

Branch Sales and ServiceSoftware

67%

61%

61%

61%

57%

placing it in the top ten highest value technologies of the 35 retail technologies we include in our poll (Figure 13). Ultimately fraud management solutions are judged by the return on investment, and as the cross-channel, cross-fraud efficiencies mature, those ROI gains are being met through improvements in process and maintainability benefits.

Online Banking Solutions

Bill Pay Solutions

Consumer Collection Systems

Fraud Management

Application Development andMaintenance

n = 39.

56%

55%

54%

53%

52%

Investment in fraud management solutions is driven primarily by operational considerations, as banks are able to leverage finely tuned scoring rules to reduce analyst time required for fraud monitoring, and significantly reduce the number of false positives.

Source: CEB 2013-2014 Technology Adoption & Investment Survey. 6 © 2015 CEB. All Rights Reserved. www.executiveboard.com

Prepared For:

CEB TOWERGROUP | RETAIL BANKING

ENTERPRISE FRAUD MANAGEMENT MARKET UPDATE

NICE ACTIMIZE – ACTIMIZE INTEGRATED FRAUD MANAGEMENT

KEY STATISTICS Founded: 1999 Company Type: Public Headquarters: New York City, NY (USA) FY 2013 Revenue: $163 million USD Full-Time Employees: 600+

FIRM OVERVIEW NICE Actimize is a technology developer specializing in providing financial crime, enterprise risk, and compliance solutions for financial institutions and government regulators. Actimize was acquired by the Israel-based security technology firm NICE Systems in 2007, becoming a wholly owned independent subsidiary. In addition to its wide range of fraud systems, NICE Actimize’s product offerings also encompass solutions for anti-money laundering, compliance monitoring, and trade surveillance. With major offices in New York, London, Paris, and Hong Kong, the company’s international team of more than 600 professionals serve a global client base.

PRODUCT OVERVIEW NICE Actimize offers Actimize Integrated Fraud Management as a fraud detection software for remote banking, commercial banking, private banking, employee, deposit, and cards. The product provides enterprise-level support to financial institutions in four key areas of fraud and payment expertise, analytics, end-to-end fraud management, and platform adaptability and openness, and provides fraud investigators with the necessary tools to detect and block fraud in real-time.

RECENT UPDATES Financial institutions can enhance fraud detection and risk scoring using Actimize Integrated Fraud Management and several of its new features. The solution utilizes a risk hub framework and open platform that can aggregate data and information from multiple channels, systems, and vendors. Additionally, while the solution includes out-of-the-box analytics models, clients can also choose to apply customized models to their implementations, and support the execution of runtime models with industry standard tools, such as SAAS and SPSS.

CEB TowerGroup View:

CUSTOMER SUCCESS STORY

A top US bank implemented Actimize Integrated Fraud Management to protect their Demand Deposit Account portfolio. The solution provided coverage for:

•Check Deposits •Check Payments •Debit Card activity: ATM, POS, CNP authorizations •Online Banking •Mobile Banking •

IVR and Call Center

The bank benefitted from Actimize’s cross-channel and

customer-centric approach to fraud management, taking advantage of the solution’s self-development capabilities to enhance Actimize’s out-of-the-box logic. The bank provided consumers with new products such as support for card provisioning, usage in mobile wallets, and mobile remote deposit acceptance. The bank is expanding their coverage into the EMEA and APAC regions.

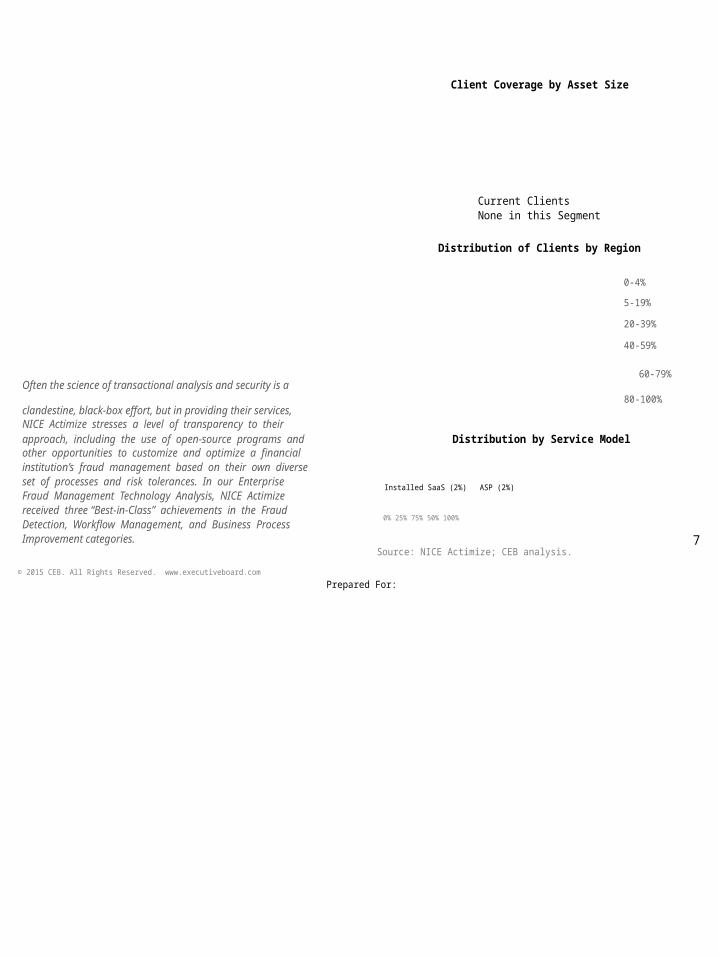

Client Coverage by Asset Size

<$1 B $1-10 B $10-50 B >$50 B

Current Clients None in this Segment

Distribution of Clients by Region

0-4%

5-19%

20-39%

40-59%

60-79% Often the science of transactional analysis and security is a

80-100% clandestine, black-box effort, but in providing their services, NICE Actimize stresses a level of transparency to their approach, including the use of open-source programs and other opportunities to customize and optimize a financial institution’s fraud management based on their own diverse set of processes and risk tolerances. In our Enterprise Fraud Management Technology Analysis, NICE Actimize received three “Best-in-Class” achievements in the Fraud Detection, Workflow Management, and Business Process Improvement categories.

Distribution by Service Model

96%

Installed SaaS (2%) ASP (2%)

0% 25% 75% 50% 100%

7 Source: NICE Actimize; CEB analysis.

© 2015 CEB. All Rights Reserved. www.executiveboard.com

Prepared For:

CEB TOWERGROUP | RETAIL BANKING

ENTERPRISE FRAUD MANAGEMENT MARKET UPDATE

Related Resources CEB TOWERGROUP RETAIL BANKING

Executive Director 2012 Enterprise Fraud

Matt Dixon Management Technology Analysis

Market Drivers

Case Study

Emerging Technology

Diagnostic Anatomy

Feature Audit

Vendor Profiles

Product Rankings

Technology Spending Forecast

Technology Adoption and

Investment Survey

Research Director Jason Malo

QUANTITATIVE INSIGHT TEAM

Project Manager Kevin Wu

Research Analyst Edward MacDonald

VENDOR ASSESSMENT TEAM

Managing Director Jaime Roca

Senior Director Magda Rolfes

Senior Research Analyst Madeline Storck

Specialist Rachel Griffin

Contact CEB TowerGroup +1-866-913-6450

About CEB

CEB is the world’s leading member-based advisory company. We unlock the potential of organizations and leaders by advancing the science and practice of management. CEB equips senior leaders and their teams with insight and actionable solutions to transform operations. This distinctive approach, pioneered by CEB, enables executives to harness peer perspectives and tap into breakthrough innovation without costly consulting or reinvention.

30+ Years of Experience

60+ Countries Represented

6,000+ Participating Organizations

300,000+ Business Professionals 8

© 2015 CEB. All Rights Reserved. www.executiveboard.com

Prepared For: