2015 Annual CRR Market Results Report - California ISO is based on the theory of spot pricing and is...

22

2015 Annual CRR Market Results Report March 9, 2015 ISO Market Services

Transcript of 2015 Annual CRR Market Results Report - California ISO is based on the theory of spot pricing and is...

2015 Annual CRR Market Results

Report

March 9, 2015

ISO Market Services

Market Services –California ISO 2015 Annual CRR Market Results Report

Market Services/CRR Team Page 2 of 22

Executive Summary

This report on the Congestion Revenue Rights (CRR) market concerns those annual

markets that were associated with the 2015 annual CRR processes, which include the

2015 tier 1 (Priority Nomination Process), tier 2, tier 3 and long-term allocation markets

as well as the 2015 annual auction market.

Empirical Results of 2015 annual processes

The annual allocation awarded to LSEs an average of 9,611 MW and 8,315 MW of CRRs

in on-peak and off-peak periods, respectively, which was approximately 42 percent of

what they nominated across all tiers. The volume of CRR awards in the 2015 annual

auction increased to 335,981 MW from 286,923 MW in the 2014 annual auction.

Further, the revenues from the 2015 annual auction were $66.62 million, an increase of

59 percent with respect to the revenues of $41.82 million from the 2014 annual auction.

Market Services –California ISO 2015 Annual CRR Market Results Report

Market Services/CRR Team Page 3 of 22

Acronyms

BPM Business Practice Manual

CRR Congestion Revenue Right

DA Day Ahead

IFM Integrated Forward Market

LAP Load Aggregation Point

LMP Locational Marginal Price

LT Long Term

LSE Load Serving Entity

MCC Marginal Congestion Component

MSS

NERC

OBAALSE

Meter Sub-System

North American Electric Reliability Corporation

Out of Balancing Authority Area Load Serving Entity

RT Real Time

SRS Secondary Registration System

ST Short Term

TOU

WECC

Time of Use

Western Electricity Coordinating Council

Market Services –California ISO 2015 Annual CRR Market Results Report

Market Services/CRR Team Page 4 of 22

List of Figures

Figure 1: Number of Different Paths Cleared in Annual ST CRR Allocations ..................... 10 Figure 2: Volume of Awards in Annual CRR Allocations –On Peak .................................... 11 Figure 3: Volume of Awards in Annual CRR Allocations –Off Peak ................................... 11 Figure 4: Volumes of LT CRR in Annual Allocations -On Peak .......................................... 12 Figure 5: Volumes of LT CRR in Annual Allocations -Off Peak.......................................... 13 Figure 6: Total Volumes of CRRs Released in Annual Allocations –On Peak ..................... 14 Figure 7: Total Volumes of CRRs Released in Annual Allocations –Off Peak .................... 14 Figure 8: Number of Participants in Annual CRR Auctions ................................................... 15 Figure 9: Number of Bids in Annual CRR Auctions .............................................................. 16 Figure 10: Number of Different Paths Cleared in Annual Auctions ....................................... 17 Figure 11: Bid-in Volume in Annual CRR Auctions .............................................................. 18 Figure 12: Volume of Awards in Annual CRR Auctions ....................................................... 19 Figure 13: Volume of Bids and Awards in Annual CRR Auctions ........................................ 19 Figure 14: Annual Auction Prices Organized by Price Range –On Peak ............................... 20 Figure 15: Annual Auction Prices Organized by Price Range –Off Peak .............................. 20 Figure 16: Revenues Collected in Annual CRR Auctions ..................................................... 21 Figure 17: Net Revenues Collected in Annual CRR Auctions ............................................... 22

Market Services –California ISO 2015 Annual CRR Market Results Report

Market Services/CRR Team Page 5 of 22

Table of Contents

Executive Summary ................................................................................................................... 2 Empirical Results of 2015 annual processes .................................................................... 2

Acronyms .................................................................................................................................. 3 List of Figures ............................................................................................................................ 4 Table of Contents ...................................................................................................................... 5 Introduction .............................................................................................................................. 6 Allocation Processes ................................................................................................................. 9

CRR Paths .............................................................................................................................. 9 Annual Allocation of Short-Term (ST) CRRs ........................................................................ 10 Annual Allocation of LT CRRs .............................................................................................. 12

Auctions .................................................................................................................................. 15 Participation ....................................................................................................................... 15 Market Bids ......................................................................................................................... 16 CRR Paths ............................................................................................................................ 16 Annual Volumes .................................................................................................................. 17 Auction Prices ..................................................................................................................... 20 Auction Revenues ............................................................................................................... 21

Market Services –California ISO 2015 Annual CRR Market Results Report

Market Services/CRR Team Page 6 of 22

Introduction

This report covers the ISO’s CRR annual market for 2015. The nodal market’s LMP

approach is based on the theory of spot pricing and is the natural extension of the

classical market equilibrium theory. LMPs reflect the locational value of power which

depends not only on the generation costs but also on the transmission system

characteristics and the willingness of demand to pay. The essence of an LMP-based

market is that all operational decisions are made by an independent system operator and

that energy is traded at LMPs. As a by-product of this pricing process, the marginal cost

of transmission is just the price difference between locations, which amounts to the price

differential of congestion and losses. Since congestion is inherently volatile, so are

congestion costs. In order to hedge volatile congestion costs, a natural complement to the

LMP-based markets is a transmission rights market. At the ISO, the energy market is

supplemented with a Congestion Revenue Rights (CRR) market. CRRs are financial

instruments that the ISO has put in place to provide participants a means to manage the

variability of congestion charges that arise under the congestion management protocol of

the Integrated Forward Market (IFM). CRRs hedge only congestion costs, not losses.

Also, only congestion costs from the DA market are hedged with CRRs. There is no

hedging mechanism for congestion costs in RT.

A CRR is defined by a MW quantity, term (i.e. season or month), time of use (TOU),

source and sink. For each term, a CRR can have one of two TOU periods: on- or off-

peak. The TOU definition is consistent with the Western Electricity Coordinating

Council (WECC) and the North American Electric Reliability Corporation (NERC)

guidelines. CRRs have a term consistent with the markets for which they have been

awarded. Each CRR is awarded through either the monthly, annual or long-term market

processes. The monthly and annual markets have both an allocation and auction

component, while the long term market is only available for the allocation. Monthly

CRRs are valid for a specific TOU for the month, while annual CRRs are valid for a

specific TOU for one of four seasons/quarters. Through the long term allocation any

awarded CRRs are valid for one of the seasons/quarters for an additional 9 years beyond

the annual market term. This effectively provides LSEs with the ability to hedge a

particular position for ten years, the annual term plus nine years associated with the long

term allocation. There may also be CRRs associated with merchant transmission projects

that may have a life term of up to 30 years.

Market Services –California ISO 2015 Annual CRR Market Results Report

Market Services/CRR Team Page 7 of 22

As noted above, the CRR market is organized in annual and monthly processes, and each

process is composed of allocations and auctions. CRRs are released on a seasonal basis

during the annual processes. There are two distinct phases in the annual allocation,

Short-Term (ST) phase for the upcoming calendar year, which consists of three separate

tiers and Long-Term (LT) phase, which is a nine year extension of awards received in tier

1 of the ST annual allocation process. In the ST annual process, up to 75 percent of the

transmission capacity is released. The remaining 25 percent of the capacity is released in

the monthly processes. For the LT allocation process 60 percent of the transmission

capacity is released. Although two types of products can be found in the ISO’s CRR

market: obligations and options; only obligation CRRs are released in the standard

allocation and auction markets. Option CRRs are only made available through the

Merchant Transmission allocation process or through the conversion of TOR rights to

CRRs, referred to as MT_TOR CRRs. The allocation and auction processes release as

much transmission capacity as is determined by the simultaneous feasibility of all CRR

portfolios. Even though market participants can nominate up to a certain volume of

CRRs in the allocation process, there is no guarantee that all of their nominations can be

allocated, due to the simultaneous feasibility constraint.

Obligation CRRs can be obtained through both annual and monthly allocations and

auctions. Entities with load-serving obligations are generally entitled to receive CRRs at

no cost in the allocation process with an upper bound set in proportion to the LSE’s load

serving obligation. A special class of LSE, the Out of Balancing Authority Area LSE

(OBAALSE), is required to prepay the respective Wheeling Access Charge (WAC) in

order to participate in the allocation process. The maximum volume of CRRs for

nomination is determined by the load serving entities (LSEs) historical load, and in tier 1

(Priority Nomination Process - PNP) of the annual allocation the CRR paths they can

nominate are restricted by a predefined set of sources and sinks. For all subsequent

allocation tiers the LSEs can nominate to any valid source, but the LSEs are always

limited to the sink location where the load is actually scheduled. Sources can be

generators, trading hubs and scheduling points. Sinks are restricted to Default Load

Aggregation Points (DLAPs), Sub-LAPs, Custom LAPs and scheduling points external to

the LSEs areas, for OBAALSEs.

The very first CRR market run was the 2008 annual market and the 2009-2017 LT CRR

market. These markets were run in the summer of 2007 when the new nodal market

(Market Redesign and Technology Upgrade – MRTU) was initially planned to go live in

2008. Since MRTU did not go live until April 1, 2009 only the CRRs awarded in the

2009-2017 LT CRR market for seasons 2-4 were kept. For the 2009 annual process, run

in 2008, the ISO released 2009 seasonal ST CRRs for seasons 2 to 4 after the launch of

Market Services –California ISO 2015 Annual CRR Market Results Report

Market Services/CRR Team Page 8 of 22

the new market on April 1, 2009, and 2010-2018 LT CRRs for all four seasons. The

2010 annual process, run in 2009, released 2010 ST CRRs and 2011-2019 LT CRRs for

all four seasons. The 2011 annual process, run in 2010, released 2011 ST CRRs and

2012-2020 LT CRRs for all four seasons. The 2012 annual process, run in 2011, released

2012 ST CRRs and 2013-2021 LT CRRs for all four seasons. The 2013 annual process,

run in 2012, released 2013 ST CRRs and 2014-2022 LT CRRs for all four season. The

2014 annual process, run in 2013, released 2014 ST CRRs and 2015-2023 LT CRRs for

all four season. In the summer of 2014, the ISO started the 2015 annual process with the

allocation and auction processes completing in November of 2014 with the release of

2015 ST CRRs (allocation and auction) and 2016-2024 LT CRRs (allocation only) for all

four seasons. Furthermore, each monthly process is started approximately one month

ahead with two allocation tiers and one auction round to release monthly CRRs for each

TOU, although this report focuses only on the 2015 annual CRR allocation and auction

market results.

This report provides metrics and analysis only related to the annual CRR markets,

including 2015 and 2014 annual processes.

Market Services –California ISO 2015 Annual CRR Market Results Report

Market Services/CRR Team Page 9 of 22

Allocation Processes

Only (candidate) CRR holders that are LSEs or qualified Out of Balancing Authority

Area Load Serving Entities (OBAALSEs) can participate and obtain CRRs through the

CRR allocations. The CRR eligible quantity is the starting point for calculating an LSE’s

nomination limits. CRR eligible quantities for the annual CRR allocations are based on

the LSE’s historical load. The reference period for historical load includes the most

recent and full calendar year. The historical load data is then grouped by season and

TOU to derive a load duration curve. The LSE’s seasonal CRR load metric for each

season and TOU period is the MW level of load that is exceeded only in 0.5 percent of

the hours based on the LSE’s historical load data. With the participants’ nominations

available, the ISO runs a simultaneous feasibility test to release CRRs to fulfill CRR

nominations as fully as possible while enforcing all transmission constraints defined in

the full network model of the transmission system. To the extent that nominations are not

simultaneously feasible, the nominations are reduced in accordance with the CRR

allocation optimization formulation until simultaneous feasibility is achieved. The CRR

Allocation optimization formulation, which utilizes a weighted least squares objective

function that applies reductions in flows on a binding constraint based on the squares of

the power transfer distribution factor of each CRR nomination for the binding constraint

while applying a weighting factor based on bid in volumes. In the annual process, up to

75 percent of transmission capacity is available. Annual allocations are organized in four

different tiers, with one tier releasing LT CRRs, as explained in the BPM for CRRs.

CRR Paths

The definition of a CRR includes the path from source to sink points. For the allocation

process, CRR nominations are restricted to a predefined set of sources and sinks. Sources

can be generation PNodes, trading hubs or scheduling points. Sinks are restricted to

default LAPs, sub-LAPs, custom LAPs and scheduling points external to the LSE’s areas

(for OBAALSEs). CRR paths for the allocation can only be from a source to a sink

(where the LSE schedules load) and cannot be in the counter-flow direction. The

expectation is that the CRR paths for the allocation will be positively valued because they

resemble supply-to-load patterns.

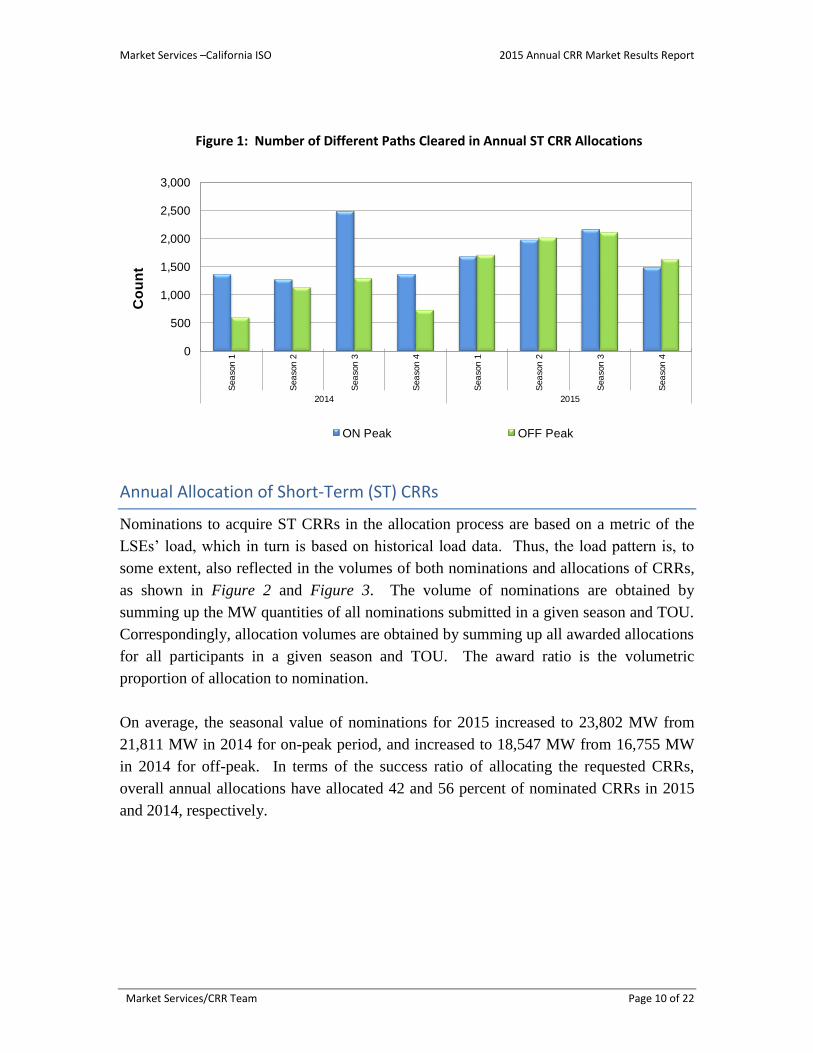

Figure 1 represents the count of different ST CRR paths awarded in the annual

allocations, organized by year, season and TOU. The number of different paths in the

2015 allocation averaged 1855, while it averaged 1293 in the 2014 annual process.

Market Services –California ISO 2015 Annual CRR Market Results Report

Market Services/CRR Team Page 10 of 22

Figure 1: Number of Different Paths Cleared in Annual ST CRR Allocations

0

500

1,000

1,500

2,000

2,500

3,000

Sea

son

1

Sea

son

2

Sea

son

3

Sea

son

4

Sea

son

1

Sea

son

2

Sea

son

3

Sea

son

4

2014 2015

Co

un

t

ON Peak OFF Peak

Annual Allocation of Short-Term (ST) CRRs

Nominations to acquire ST CRRs in the allocation process are based on a metric of the

LSEs’ load, which in turn is based on historical load data. Thus, the load pattern is, to

some extent, also reflected in the volumes of both nominations and allocations of CRRs,

as shown in Figure 2 and Figure 3. The volume of nominations are obtained by

summing up the MW quantities of all nominations submitted in a given season and TOU.

Correspondingly, allocation volumes are obtained by summing up all awarded allocations

for all participants in a given season and TOU. The award ratio is the volumetric

proportion of allocation to nomination.

On average, the seasonal value of nominations for 2015 increased to 23,802 MW from

21,811 MW in 2014 for on-peak period, and increased to 18,547 MW from 16,755 MW

in 2014 for off-peak. In terms of the success ratio of allocating the requested CRRs,

overall annual allocations have allocated 42 and 56 percent of nominated CRRs in 2015

and 2014, respectively.

Market Services –California ISO 2015 Annual CRR Market Results Report

Market Services/CRR Team Page 11 of 22

Figure 2: Volume of Awards in Annual CRR Allocations –On Peak

0%

17%

33%

50%

67%

83%

100%

0

6

12

18

24

30

36

Sea

son

1

Sea

son

2

Sea

son

3

Sea

son

4

Sea

son

1

Sea

son

2

Sea

son

3

Sea

son

4

2014 2015

Aw

ard

Ra

tio

MW

(T

ho

usan

ds)

Nomination Allocation Award Ratio

Figure 3: Volume of Awards in Annual CRR Allocations –Off Peak

0%

20%

40%

60%

80%

100%

0

5

10

15

20

25

Sea

son

1

Sea

son

2

Sea

son

3

Sea

son

4

Sea

son

1

Sea

son

2

Sea

son

3

Sea

son

4

2014 2015

Aw

ard

Ra

tio

MW

(T

ho

us

an

ds

)

Nomination Allocation Award Ratio

Market Services –California ISO 2015 Annual CRR Market Results Report

Market Services/CRR Team Page 12 of 22

Annual Allocation of LT CRRs

LT CRRs are released in only one of the four allocation tiers each year, and are defined

by season and TOU as well. The CRRs that are awarded in the LT tier are a subset and,

effectively, an extension of CRRs received in tier 1 of the corresponding annual

allocation. As LT CRRs have a term of nine years, and are required to be a subset of the

CRRs awarded in tier 1 of the annual allocation CRR holders who receive LT CRRs will

hold CRRs having an effective term of 10 years. The total quantity of ST CRRs that an

LSE can nominate as LT CRRs is up to 50 percent of their adjusted load metric. Figure 4

and Figure 5 show both the volumes of nominations and allocations for LT CRRs in the

latest three annual processes, and the percentage of the nomination volume that was

awarded.

Figure 4: Volumes of LT CRR in Annual Allocations -On Peak

0%

20%

40%

60%

80%

100%

0

3

6

9

12

15

Sea

son

1

Sea

son

2

Sea

son

3

Sea

son

4

Sea

son

1

Sea

son

2

Sea

son

3

Sea

son

4

Sea

son

1

Sea

son

2

Sea

son

3

Sea

son

42014- 2022 2015- 2023 2016- 2024

Aw

ard

Ra

tio

MW

(T

ho

usan

ds)

Nomination Allocation Award Ratio

Compared with the volumes of LT CRRs allocated in the annual process of 2013 (LT

2014-2022) and 2014 (LT 2015-2023), the volumes of LT CRRs allocated in the annual

process of 2015 (LT 2016-2024) dropped significantly. One contributing factor to these

decreases was associated with two constraints which were heavily de-rated by the

application of the break-even methodology. In addition, since all previously awarded LT

markets become fixed CRRs for the subsequent markets it would be expected that the

total awards would decrease until the first LT market expires. Compared with the

volumes of LT CRRs allocated in the annual process of 2014 (LT 2015-2023), the

seasonal average in the 2015 (LT 2016-2024) annual process dropped to 2,358 MW from

6,165 MW for on-peak, and to 1,850 MW from 7,785 MW for off-peak.

Market Services –California ISO 2015 Annual CRR Market Results Report

Market Services/CRR Team Page 13 of 22

Figure 5: Volumes of LT CRR in Annual Allocations -Off Peak

0%

25%

50%

75%

100%

0

1

2

3

4

5

6

7

8

9

10

Sea

son

1

Sea

son

2

Sea

son

3

Sea

son

4

Sea

son

1

Sea

son

2

Sea

son

3

Sea

son

4

Sea

son

1

Sea

son

2

Sea

son

3

Sea

son

4

2014- 2022 2015- 2023 2016- 2024

Aw

ard

Ra

tio

MW

(T

ho

us

an

ds

)

Nomination Allocation Award Ratio

Since nominations for LT CRRs are based on CRRs that are already simultaneously

feasible in Tier 1 of the annual allocation, nominations for LT CRRs usually have a

higher success ratio than the ST CRRs. It is worth mentioning that previously awarded

LT CRR allocations are modeled as fixed in the current LT allocation process and,

therefore, the awarded volumes of LT CRRs are only for the left over transmission

capacity. With this configuration, and given the fact that the allocations of LT CRRs are

implicitly limited by their nominations, with some participants nominating as much as

possible in the early releases, allocation volumes of LT CRRs are expected to gradually

diminish over the years, until the first increase of capacity in 2018, when the first LT

market (2009-2017) expires.

Given the extended time span of LT CRRs, various allocations of LT CRRs will overlap

with the corresponding ST CRR allocations in any given year. Figure 6 and Figure 7

show the total volume of CRRs allocated in a given year from ST allocation markets and

all LT markets for the latest three years. The volumes are organized by year, season and

TOU. Since CRRs from allocations are defined from supply-type sources to load-type

sinks, the total volumes may represent the load that is actually being hedged with CRRs

from annual allocations. Similar to 2014, season 3 has the maximum volume hedged in

2015, with 20,673 MW for on-peak and 20,761 MW for off-peak. However, the volume

in season 2 and season 3 are very close for on-peak in 2015, unlike in 2014. From the

total volume of CRRs released in the annual allocations, the volume hedged with LT

CRRs increased to 48 percent in 2015 from 41 percent in 2014.

Market Services –California ISO 2015 Annual CRR Market Results Report

Market Services/CRR Team Page 14 of 22

Figure 6: Total Volumes of CRRs Released in Annual Allocations –On Peak

0

5

10

15

20

25

30

Sea

son

1

Sea

son

2

Sea

son

3

Sea

son

4

Sea

son

1

Sea

son

2

Sea

son

3

Sea

son

4

Sea

son

1

Sea

son

2

Sea

son

3

Sea

son

4

2014 2015 2016

MW

(T

ho

us

an

ds

)

ST Annual All LTs

Figure 7: Total Volumes of CRRs Released in Annual Allocations –Off Peak

0

5

10

15

20

25

Sea

son

1

Sea

son

2

Sea

son

3

Sea

son

4

Sea

son

1

Sea

son

2

Sea

son

3

Sea

son

4

Sea

son

1

Sea

son

2

Sea

son

3

Sea

son

4

2014 2015 2016

MW

(T

ho

us

an

ds

)

ST Annual All LTs

Market Services –California ISO 2015 Annual CRR Market Results Report

Market Services/CRR Team Page 15 of 22

Auctions

CRR auctions are available in both annual and monthly processes. In these one-tier

auctions, each TOU is treated independently as a market.

Participation

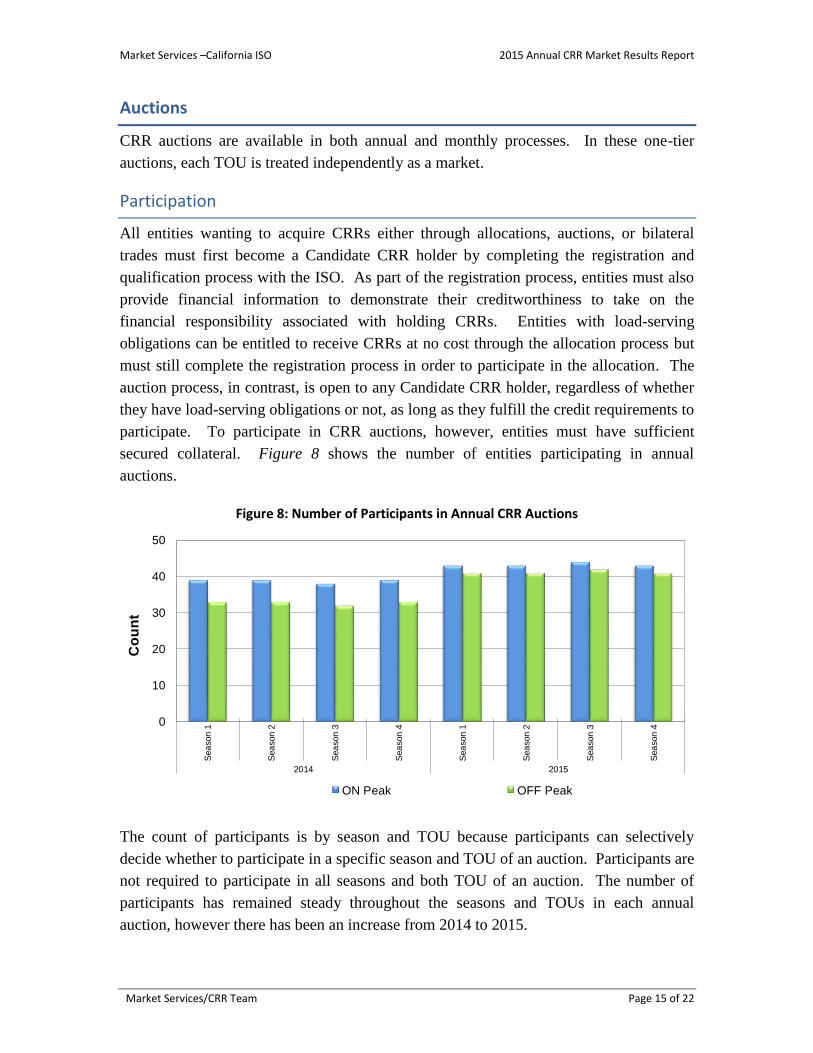

All entities wanting to acquire CRRs either through allocations, auctions, or bilateral

trades must first become a Candidate CRR holder by completing the registration and

qualification process with the ISO. As part of the registration process, entities must also

provide financial information to demonstrate their creditworthiness to take on the

financial responsibility associated with holding CRRs. Entities with load-serving

obligations can be entitled to receive CRRs at no cost through the allocation process but

must still complete the registration process in order to participate in the allocation. The

auction process, in contrast, is open to any Candidate CRR holder, regardless of whether

they have load-serving obligations or not, as long as they fulfill the credit requirements to

participate. To participate in CRR auctions, however, entities must have sufficient

secured collateral. Figure 8 shows the number of entities participating in annual

auctions.

Figure 8: Number of Participants in Annual CRR Auctions

0

10

20

30

40

50

Sea

son

1

Sea

son

2

Sea

son

3

Sea

son

4

Sea

son

1

Sea

son

2

Sea

son

3

Sea

son

4

2014 2015

Co

un

t

ON Peak OFF Peak

The count of participants is by season and TOU because participants can selectively

decide whether to participate in a specific season and TOU of an auction. Participants are

not required to participate in all seasons and both TOU of an auction. The number of

participants has remained steady throughout the seasons and TOUs in each annual

auction, however there has been an increase from 2014 to 2015.

Market Services –California ISO 2015 Annual CRR Market Results Report

Market Services/CRR Team Page 16 of 22

Market Bids

In general, any bid point (quantity, price) is allowed in CRR auctions. Since participants

can bid positive or negative bid curves it is possible to buy or sell through the CRR

auction. Each CRR bid must have an associated season and TOU, source(s) and sink(s),

and a set of bid points, quantity-price, that conforms to a monotonically non-increasing

piecewise linear bid curve. One salient feature of the CRR market is that multi-segment

bids are allowed, up to 20 segments. This adds great flexibility for participants to build a

bid with different levels of willingness to pay, and may avoid the submission of multiple

bids of a single segment that would be needed to attain the same result. Figure 9 shows

the number of bids submitted in the annual auctions, counted by season, TOU and year

for the latest two years. A bid is counted as a single bid regardless of how many price

segments the bid contains. The number of bids almost doubled in the 2015 annual

auction with respect to the 2014 annual auction.

Figure 9: Number of Bids in Annual CRR Auctions

0

5

10

15

20

25

Sea

son

1

Sea

son

2

Sea

son

3

Sea

son

4

Sea

son

1

Sea

son

2

Sea

son

3

Sea

son

4

2014 2015

Co

un

t (T

ho

us

an

ds

)

ON Peak OFF Peak

CRR Paths

CRR bids in auctions are open to all CRR paths that can be defined between any valid

points, such as generation PNodes, trading hubs, LAPs, MSS-LAPs, sub-LAPs and

scheduling points. This flexibility gives participants an opportunity to bid for counter-

flow CRRs, which have an expectation of a negative revenue stream. Figure 10 shows

the number of different CRR paths cleared in annual auctions. The number of different

paths cleared increased 61% in the 2015 auction with respect to the 2014 auction.

Market Services –California ISO 2015 Annual CRR Market Results Report

Market Services/CRR Team Page 17 of 22

Figure 10: Number of Different Paths Cleared in Annual Auctions

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

Sea

son

1

Sea

son

2

Sea

son

3

Sea

son

4

Sea

son

1

Sea

son

2

Sea

son

3

Sea

son

4

2014 2015

Co

un

t

ON Peak OFF Peak

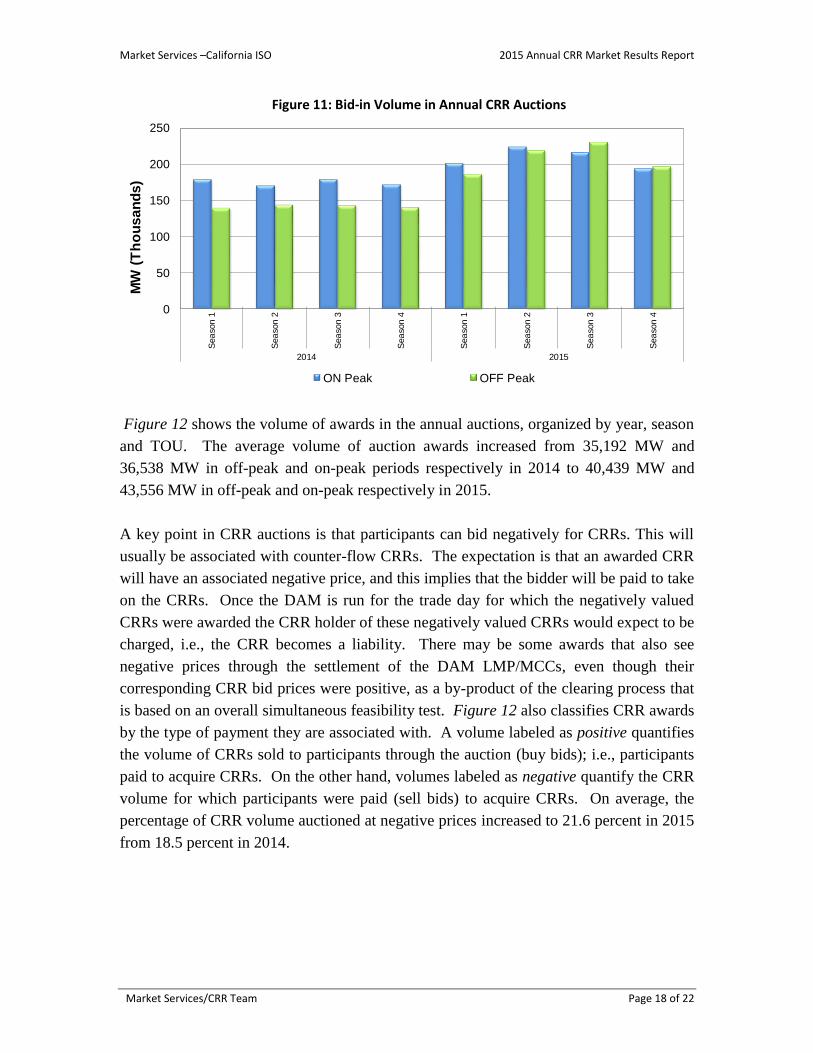

Annual Volumes

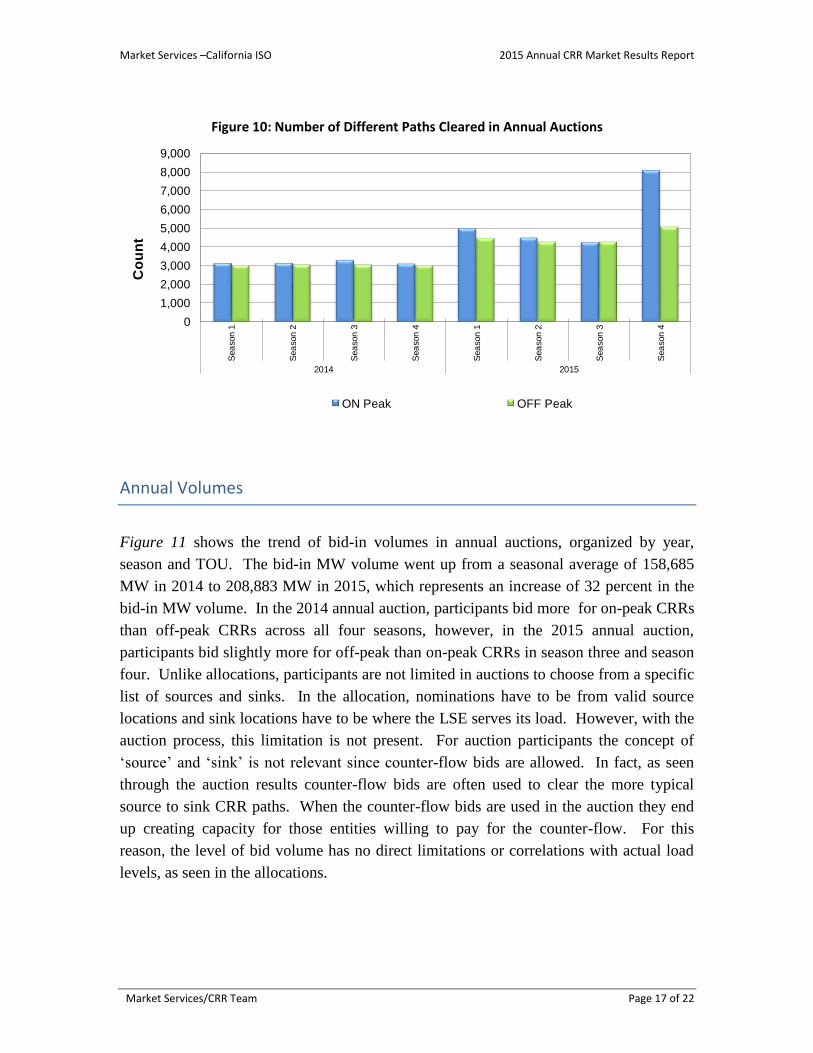

Figure 11 shows the trend of bid-in volumes in annual auctions, organized by year,

season and TOU. The bid-in MW volume went up from a seasonal average of 158,685

MW in 2014 to 208,883 MW in 2015, which represents an increase of 32 percent in the

bid-in MW volume. In the 2014 annual auction, participants bid more for on-peak CRRs

than off-peak CRRs across all four seasons, however, in the 2015 annual auction,

participants bid slightly more for off-peak than on-peak CRRs in season three and season

four. Unlike allocations, participants are not limited in auctions to choose from a specific

list of sources and sinks. In the allocation, nominations have to be from valid source

locations and sink locations have to be where the LSE serves its load. However, with the

auction process, this limitation is not present. For auction participants the concept of

‘source’ and ‘sink’ is not relevant since counter-flow bids are allowed. In fact, as seen

through the auction results counter-flow bids are often used to clear the more typical

source to sink CRR paths. When the counter-flow bids are used in the auction they end

up creating capacity for those entities willing to pay for the counter-flow. For this

reason, the level of bid volume has no direct limitations or correlations with actual load

levels, as seen in the allocations.

Market Services –California ISO 2015 Annual CRR Market Results Report

Market Services/CRR Team Page 18 of 22

Figure 11: Bid-in Volume in Annual CRR Auctions

0

50

100

150

200

250

Sea

son

1

Sea

son

2

Sea

son

3

Sea

son

4

Sea

son

1

Sea

son

2

Sea

son

3

Sea

son

4

2014 2015

MW

(T

ho

us

an

ds

)

ON Peak OFF Peak

Figure 12 shows the volume of awards in the annual auctions, organized by year, season

and TOU. The average volume of auction awards increased from 35,192 MW and

36,538 MW in off-peak and on-peak periods respectively in 2014 to 40,439 MW and

43,556 MW in off-peak and on-peak respectively in 2015.

A key point in CRR auctions is that participants can bid negatively for CRRs. This will

usually be associated with counter-flow CRRs. The expectation is that an awarded CRR

will have an associated negative price, and this implies that the bidder will be paid to take

on the CRRs. Once the DAM is run for the trade day for which the negatively valued

CRRs were awarded the CRR holder of these negatively valued CRRs would expect to be

charged, i.e., the CRR becomes a liability. There may be some awards that also see

negative prices through the settlement of the DAM LMP/MCCs, even though their

corresponding CRR bid prices were positive, as a by-product of the clearing process that

is based on an overall simultaneous feasibility test. Figure 12 also classifies CRR awards

by the type of payment they are associated with. A volume labeled as positive quantifies

the volume of CRRs sold to participants through the auction (buy bids); i.e., participants

paid to acquire CRRs. On the other hand, volumes labeled as negative quantify the CRR

volume for which participants were paid (sell bids) to acquire CRRs. On average, the

percentage of CRR volume auctioned at negative prices increased to 21.6 percent in 2015

from 18.5 percent in 2014.

Market Services –California ISO 2015 Annual CRR Market Results Report

Market Services/CRR Team Page 19 of 22

Figure 12: Volume of Awards in Annual CRR Auctions

0

10

20

30

40

50

Sea

son

1

Sea

son

2

Sea

son

3

Sea

son

4

Sea

son

1

Sea

son

2

Sea

son

3

Sea

son

4

2014 2015

Th

ou

sa

nd

s

ON Positive ON Negative OFF Positive OFF Negative

Figure 13 shows the total MW volume of bids and awards for each year and season.

Volumes of both TOUs are aggregated, and the ratio of award volume to the total bid

volume is represented by square markers. On average, the ratio of awards decreased to

20.2 percent in 2015, from 22.6 percent in 2014. It is interesting to note that even though

the award ratio dropped from 2014 to 2015 the total for both bid in volumes and award

volumes increased.

Figure 13: Volume of Bids and Awards in Annual CRR Auctions

0%

10%

20%

30%

40%

50%

0

80

160

240

320

400

480

Sea

son

1

Sea

son

2

Sea

son

3

Sea

son

4

Sea

son

1

Sea

son

2

Sea

son

3

Sea

son

4

2014 2015

Aw

ard

Ra

tio

MW

(T

ho

us

an

ds

)

Bid Award Award Ratio

Market Services –California ISO 2015 Annual CRR Market Results Report

Market Services/CRR Team Page 20 of 22

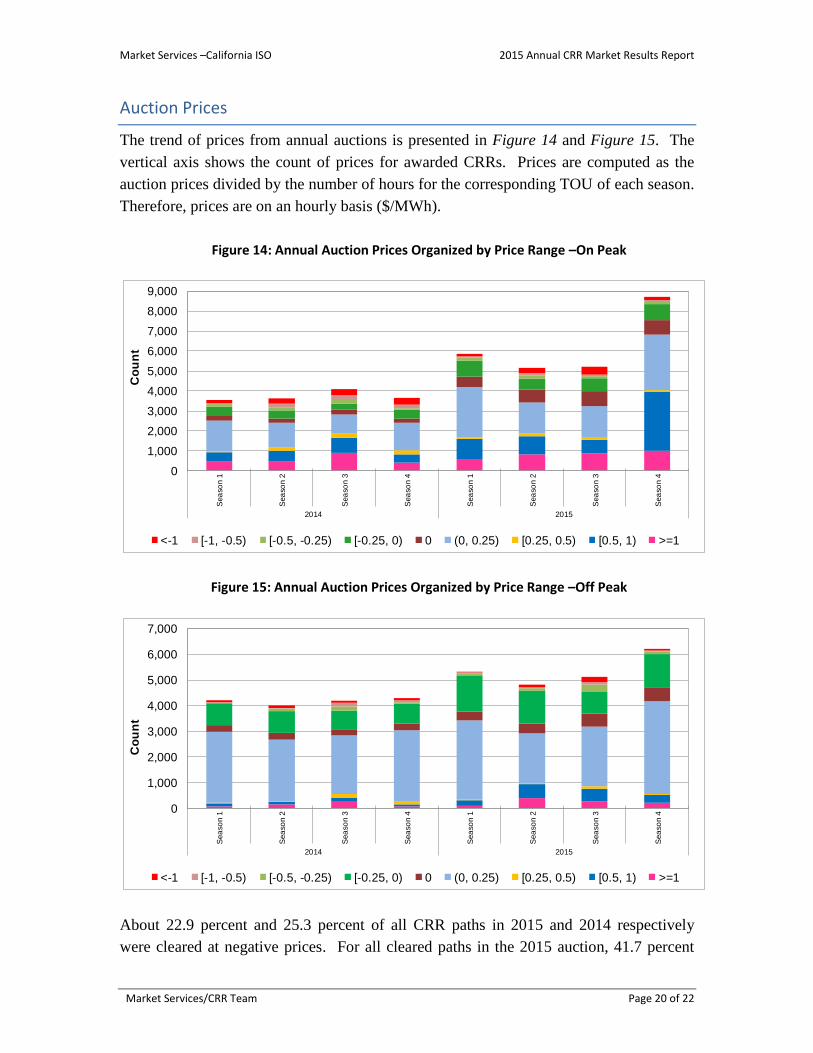

Auction Prices

The trend of prices from annual auctions is presented in Figure 14 and Figure 15. The

vertical axis shows the count of prices for awarded CRRs. Prices are computed as the

auction prices divided by the number of hours for the corresponding TOU of each season.

Therefore, prices are on an hourly basis ($/MWh).

Figure 14: Annual Auction Prices Organized by Price Range –On Peak

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

Sea

so

n 1

Sea

son 2

Sea

son 3

Sea

so

n 4

Sea

son 1

Sea

son 2

Sea

so

n 3

Sea

son 4

2014 2015

Co

un

t

<-1 [-1, -0.5) [-0.5, -0.25) [-0.25, 0) 0 (0, 0.25) [0.25, 0.5) [0.5, 1) >=1

Figure 15: Annual Auction Prices Organized by Price Range –Off Peak

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

Sea

son 1

Sea

son 2

Sea

son 3

Sea

son 4

Sea

son 1

Sea

son 2

Sea

son 3

Sea

son 4

2014 2015

Co

un

t

<-1 [-1, -0.5) [-0.5, -0.25) [-0.25, 0) 0 (0, 0.25) [0.25, 0.5) [0.5, 1) >=1

About 22.9 percent and 25.3 percent of all CRR paths in 2015 and 2014 respectively

were cleared at negative prices. For all cleared paths in the 2015 auction, 41.7 percent

Market Services –California ISO 2015 Annual CRR Market Results Report

Market Services/CRR Team Page 21 of 22

were at prices between 0 and 0.25 $/MWh and 9.6 percent were at prices 0 $/MWh, while

they were 48.5 percent and 6.1 percent in the 2014 auction.

Auction Revenues

Participants in CRR auctions pay or are paid to acquire CRRs1. Participants receiving

CRRs at positive prices pay the amount of the CRR clearing price multiplied by the

awarded volume, with the expectation that the revenue stream from the IFM marginal

congestion component prices will at least offset this cost. Conversely, participants

acquiring CRRs at negative prices are paid the amount of the CRR clearing price

multiplied by the awarded volume, with the expectation that such CRRs will be a liability

with an associated charge that the CRR Holder will have to pay when settled with the

associated IFM marginal congestion component prices. Negative auction revenues are

funded with positive revenues, meaning no negative valued CRRs are awarded unless

there is a counter-party willing to pay for the associated counter-flow. The net balance is

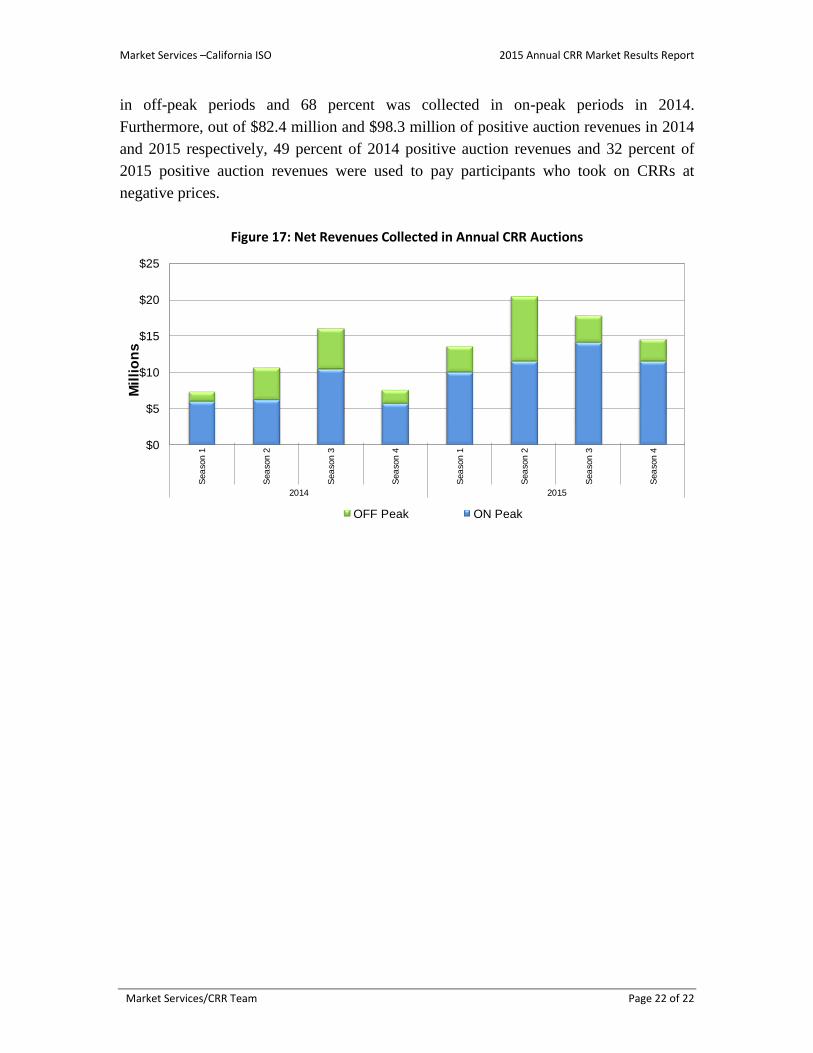

the CRR auction revenues collected by the ISO. Figure 16 shows the auction revenues

organized by positive and negative revenues in each TOU, while Figure 17 shows the net

auction revenues collected by the ISO by TOU.

Figure 16: Revenues Collected in Annual CRR Auctions

-$20.0

-$15.0

-$10.0

-$5.0

$0.0

$5.0

$10.0

$15.0

$20.0

$25.0

$30.0

$35.0

Sea

son

1

Sea

son

2

Sea

son

3

Sea

son

4

Sea

son

1

Sea

son

2

Sea

son

3

Sea

son

4

2014 2015

Mil

lio

ns

ON Peak OFF Peak

The auction revenues in 2015 increased 59 percent to $66.62 million from $41.82 million

in 2013. Out of the total auction revenues, 29 percent was collected in off-peak periods

and 71 percent was collected in on-peak periods in 2015, while 32 percent was collected

1 Some CRRs may also be acquired at zero prices.

Market Services –California ISO 2015 Annual CRR Market Results Report

Market Services/CRR Team Page 22 of 22

in off-peak periods and 68 percent was collected in on-peak periods in 2014.

Furthermore, out of $82.4 million and $98.3 million of positive auction revenues in 2014

and 2015 respectively, 49 percent of 2014 positive auction revenues and 32 percent of

2015 positive auction revenues were used to pay participants who took on CRRs at

negative prices.

Figure 17: Net Revenues Collected in Annual CRR Auctions

$0

$5

$10

$15

$20

$25

Sea

son

1

Sea

son

2

Sea

son

3

Sea

son

4

Sea

son

1

Sea

son

2

Sea

son

3

Sea

son

4

2014 2015

Mil

lio

ns

OFF Peak ON Peak