20141212 inside bitcoinsseoul_zennonkapron_final

20

China & Digital Currencies Today: Opportunities and Challenges Zennon Kapron December 12 th , 2014

-

Upload

mecklermedia -

Category

Economy & Finance

-

view

51 -

download

0

Transcript of 20141212 inside bitcoinsseoul_zennonkapron_final

China & Digital Currencies Today: Opportunities and Challenges

Zennon Kapron December 12th, 2014

Overview

• China Today • Macroeconomic Issues • Moving Mobile • Mobile Payments • NFC • P2P Lending • Opportunities for Digital Currencies / Digital Technology • Challenges • Conclusions

14-12-16 2

Macroeconomic / Financial Industry Development

• GDP Slowing • Shadow Lending • Increased focus on changing the industry

– Private Banks – Loose regulations around internet finance

China economy still strong, but growth has slowed / structural issues creeping in

14-12-16 3

6

8

10

12

Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2

GDP Growth: ChinaQ1 2010 - Q3 2014 Y-o-Y growth (%)

2010 2011 2012 2013 2014

10.3

9.6 9.8 9.7 9.59.1

8.9

8.1

7.6 7.47.9 7.7

7.57.8 7.7

7.3 7.57.3

Mobile Uptake

Mobile payments in China are increasing rapidly as more and more users start to use smartphones and payment options increase.

14-12-16 4

7.47 8.59

9.86 11.12

12.29 12.35

56 64

74

83 91 92

0

10

20

30

40

50

60

70

80

90

100

0

2

4

6

8

10

12

14

2009 2010 2011 2012 2013 2014Q1

China Mobile Phone Users and Mobile Phone Penetration: Unit 100 Million, Percentage

China Mobile Phone User Mobile Phone Penetration

Smartphone Penetration

Increased availability of faster data-services through 3G and 4G has supported an already strong shift to smartphones.

224 266 390 449

30%

65%

88% 90%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0

50

100

150

200

250

300

350

400

450

500

2011 2012 2013 2014

Smartphone sales volume and % of Overall Mobile Phone sales 2011-2014 (Unit: Millions & %)

Mobile Phone Sales Volume Smart Phones as % of Overall Mobile Phone Sales

5 14-12-16

Mobile Internet Usage

Continued growth and availability of data and smart phones has driven mobile internet usage setting the stage for increased e-commerce and mobile payments

233 303 356 420 500

60.80% 66.20% 69.30%

74.50% 81%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

0

100

200

300

400

500

600

2009 2010 2011 2012 2013

Mobile internet users and Mobile Internet Usage as % of Overall Internet Usage

Number of Mobile Internet Users Percentage of Mobile Internet Usage

6 14-12-16

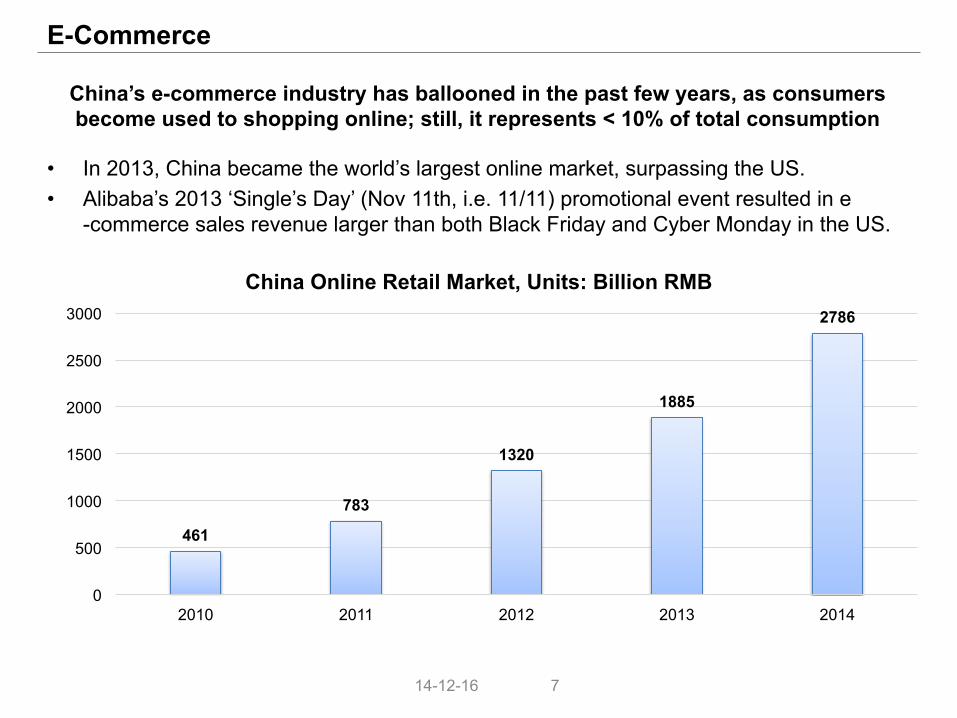

E-Commerce

• In 2013, China became the world’s largest online market, surpassing the US. • Alibaba’s 2013 ‘Single’s Day’ (Nov 11th, i.e. 11/11) promotional event resulted in e

-commerce sales revenue larger than both Black Friday and Cyber Monday in the US.

China’s e-commerce industry has ballooned in the past few years, as consumers become used to shopping online; still, it represents < 10% of total consumption

461

783

1320

1885

2786

0

500

1000

1500

2000

2500

3000

2010 2011 2012 2013 2014

China Online Retail Market, Units: Billion RMB

7 14-12-16

Mobile E-Commerce

Increasingly, Mobile shopping represents a growing share of overall e-commerce

98.50% 95.20% 90.90% 86.90% 83.60% 80.10% 75.90%

1.50% 4.80% 9.10% 13.10% 16.40% 19.90% 24.10%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2011 2012 2013 2014e 2015e 2016e 2017e

Breakdown of e-commerce purchasing Channels in China

Mobile

PC

Source: MOFCOM, iResearch, Kapronasia Analysis 8 14-12-16

E-commerce in China

E-commerce in China is eclipsing that of the west

14-12-16 9

Comparison of China's Singles Day to America's Cyber Monday and Black Friday US$Billion

Source: Kapronasia, company reports

Singles Day Black Friday Cyber Monday

0

2

4

6

8

10

201420132012

5.75

9.34

2.29

1.2

2.65

1.513.04 1.04

1.98

Mobile Payment Transaction Volume

• E-commerce was specifically mentioned in the 12th five-year plan with mobile payment being a crucial aspect of that.

• Development of information and communication technology (ICT) is also a measurement of the performance of local governments

As measured by value and volume, mobile payments are growing very quickly in China

1.18 2.47

5.35

16.74

6.59 77.80%

109.32% 116.46%

212.86% 232.20%

0%

50%

100%

150%

200%

250%

0 2 4 6 8

10 12 14 16 18

2010 2011 2012 2013 2014Q1

China Mobile Payment Transaction Volume and Growth Rate: Unit 100 Million

Completed Transactions Completed Transactions Growth Rate

10 14-12-16

Mobile Payment Preferences Promoted by Alipay, “Mobile bundled card” payments where a payment card is semi-permanently linked to a payment platform, have become the most popular methods of payment while NFC payments are gradually gaining attention.

0.8%

1.9%

2.9%

4.0%

4.3%

11.7%

17.9%

27.5%

29.2%

0% 5% 10% 15% 20% 25% 30% 35%

Others

Plug-In Reader

NFC Payment

Bar Code Payment

QR Code

Mobile Phone Bundled Card

Mobile Web Payment

SMS Payment

Mobile App Payment

Source: iResearch

2012 2014

Source: Kapronasia Primary Research, 2014

0.2%

1.5%

3.7%

8.7%

9.9%

18.0%

26.2%

31.7%

0% 10% 20% 30% 40%

Others

Plug-in Card Reader Payment

Barcode Payment

NFC Payment

Mobile Web Payment

SMS Payment

Mobile App

Mobile Phone Bundled Card Payment (Quick Pay)

Question: What type of mobile payment method do you prefer to use?

NB: Kapronasia does not know the sample set or specific methodology that iResearch used for collecting 2012, and so 2012 vs. 2014 data should be used as a broad / general comparison only and should not be compared directly.

11 14-12-16

NFC

• Development of NFC standards in China (and globally) stymied by disagreement on standards

• Agreement in 2013 has led to increased focus from all players • Mobile Network Operators (MNOs), China Unionpay, Banks and • Overview of key efforts • Apple and China Unionpay tie-up for iTunes • Apple Pay in China • Android Pay

Near Field Communications (NFC) standards have been set => China may be ahead of other markets

14-12-16 12

Source: Kapronasia Primary Research, 2014

NFC – Preferences and Reasons for Using NFC

Metric

Would Pick NFC

1

Likely to Pick NFC

2

No Impact 3

Likely to Pick Other Mobile

Payment Method

4

Would Pick Other Mobile

Payment method

5

Notes

Transaction Speed

Convenience of Bundle w/ bankcard

Example: Quickpay

Convenience of wallet functionality

Current SIM-NFC solutions often have multiple cards in a single mobile wallet

Simplified Operation

Perception that NFC payment simplifies payment

Higher Security NFC payments’ generally seen as safer

Widely Known and Used

NFC marketing has helped awareness

Broad Usage Available solutions in the market

Try New Payments

Curious about new payment methods

Used Currently for Payment

Many users are used to their current payment method, so there seems to be stickiness.

2.33

2.50

2.24

2.42

2.22

2.65

2.42

2.13

2.83

13 14-12-16

3rd Party Payment Companies

China’s large internet services have also provided social ‘hubs’ with integrated payment functions, completely avoiding the need to work with MNOs and Banks

• Wechat, an online chat app from Tencent, has become incredibly popular in China.

• Functionality – Book taxis – Pay friends – Buy movie / show tickets – Pay bills – Mobile top-up

• Increasingly, the more successful payment models are the ones that adapt to China users needs.

• May be potential to cooperate with 3rd

party companies for SanDisk

14 14-12-16

Peer to Peer (P2P) Lending

• Small and medium enterprises have been starved of cash • Online P2P lending has been in existence since 2007, really only gained traction in

previous 4 years • The lending solves a problem => allowed by the government

The tacit acceptance of the government of P2P has allowed the industry to grow rapidly

14-12-16 15

Check Point China

• Economy is not in the best of shape, but still better than most • Consumers are getting online and getting mobile – mainly on smartphones • As more people are mobile, shopping and payments are following • Younger generation is increasingly used to doing everything online • Regulators are pushing change – 2013-2016 reforms:

– Direct Banks Implemented – Private Banks on the way – P2P lending continuing w/o regulation – HK / Shanghai connect – Deposit Insurance – Stock Options – Financial Futures – Interest Rate Liberalization – Online Finance – Growth Enterprise Board – Negotiable Deposit Certificates – NFC Standards – Credit Asset Securitization – Bankruptcy Provisioning

An increasingly online / mobile user base is enabling a massive shift to online payments and finance.

14-12-16 16

And the list goes on…..

Opportunities for Digital Currencies / Digital Technology

• Younger generation, and increasing the older generation are used to new technology • QQ coins have been around for ages => population is used to virtual goods • Solutions that focus on making something easier • Chinese government’s attitude towards Bitcoin

• Will they regulate further? • Law targeting virtual currency in 2009; forbade virtual currency for purchase of real

items. • Focused on Q Coin, paid for online services such as games. However, it seemed to

be easily applied to Bitcoin • Unlike Q coin, the Ministry of Commerce and the Ministry of Culture can’t target a

company or entity to regulate or to submit the circulation and transaction volumes of Bitcoin.

• Is the government happy enough with the status quo? Not much has changed, what were they unhappy about before?

China’s financial industry is still relatively immature => scope for providing new and innovative solutions

14-12-16 17

Challenges

• P2P Lending allowed as fits with reform and helps the industry by reducing risk • Bitcoin was speculation => didn’t solve any issues in the market • Too many business models for too few users => demand needs to increase • Crypto is a solution searching for a problem

• Current Bitcoin business models don’t fix much in China: – Merchant fees are low with CUP cards – Security no longer seems to be a concern for users – Real time domestic payments through banks or 3rd party platforms – Exists on its own – not tied into social

However, solutions need to fit with the government’s path for the economy and reform

14-12-16 18

Conclusions

• We will look back at China’s financial industry in 5 years as the most innovative globally • Crossing the river by feeling the stones => path to reform • Government is not anti-bitcoin, they are just anti-risk • Think of business models that help rather than hurt the industry • Stop pitching ‘RMB to whatever’ business models. It’s illegal no matter how you spin it.

14-12-16 19

![[Chuyên đề] - docview1.tlvnimg.comdocview1.tlvnimg.com/tailieu/2014/20141212/whynot_whynot/wn12... · Email: huongdt1@msb.com.vn Giấy phép xuất bản số: 95/GP-XBBT In](https://static.fdocuments.net/doc/165x107/5a7e03f47f8b9ae9398e1d69/chuyn-de-huongdt1msbcomvn-giay-php-xuat-ban-so-95gp-xbbt-in.jpg)