2014 December GSOO Stakeholder Presentation

29

2014 December Gas Statement of Opportunities Joachim Tan Senior Analyst, System Capacity Stakeholder Presentation 3 February 2015

-

Upload

joachim-tan -

Category

Business

-

view

50 -

download

1

Transcript of 2014 December GSOO Stakeholder Presentation

2014 December Gas Statement of Opportunities Joachim Tan Senior Analyst, System Capacity Stakeholder Presentation 3 February 2015

2

Forecast context

Findings

Forecasts

Other information

Forecast context

Challenging time to prepare long-term forecasts of gas demand and supply:

• Volatility in oil prices

• Significant fall in the prices of WA commodities

• North West Shelf and related commercial decisions

• Falling Asia Pacific gas prices, making supply to the domestic gas market relatively more attractive

3

Falling oil prices, January 2014 – January 2015 (Brent)

4

$40

$50

$60

$70

$80

$90

$100

$110

$120

US$

/bar

rel

December 2014 GSOO Released

Peak - Brent price US115.19 on 19 June 2014

OPEC 27 November 2014

Decision

Source: EIA, Brent Spot Prices FOB

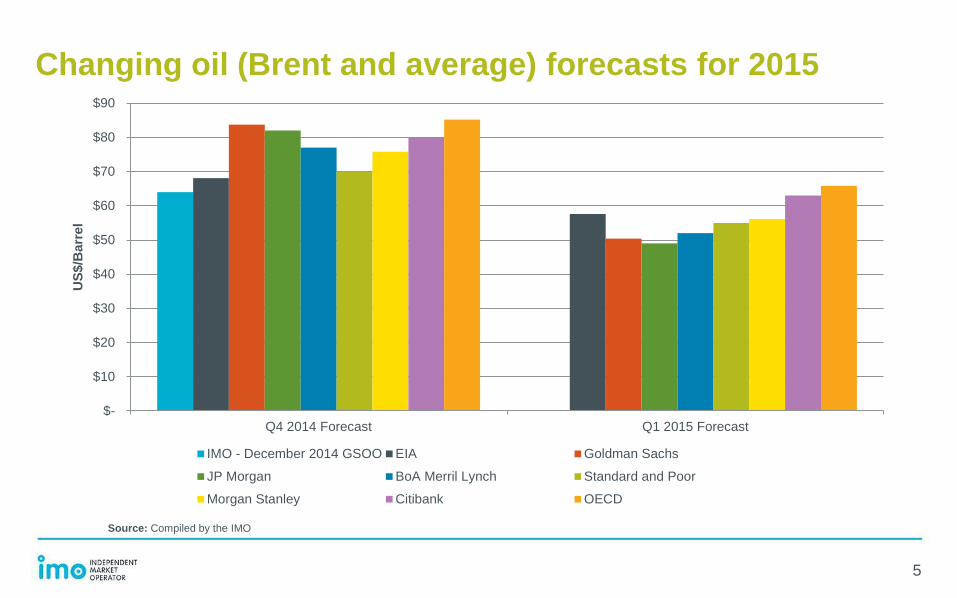

Changing oil (Brent and average) forecasts for 2015

5

Source: Compiled by the IMO

$-

$10

$20

$30

$40

$50

$60

$70

$80

$90

Q4 2014 Forecast Q1 2015 Forecast

US$

/Bar

rel

IMO - December 2014 GSOO EIA Goldman Sachs

JP Morgan BoA Merril Lynch Standard and Poor

Morgan Stanley Citibank OECD

Commodity prices, January 2014 – December 2014

6

0

10

20

30

40

50

60

70

80

90

100

Jan-14 Feb-14 Mar-14 Apr-14 May-14 Jun-14 Jul-14 Aug-14 Sep-14 Oct-14 Nov-14 Dec-14

Inde

x Va

lue

Index of commodity prices; All items US$ Index of commodity prices; Bulk commodities (spot); US$

Source: Reserve Bank of Australia, Base Year = 2012-13

North West Shelf update

NWS and WA Government signed an amendment to the State Agreement on 20 November 2014 (awaiting ratification by WA Parliament) that requires the NWS to:

• adhere to the WA Government’s domestic gas policy – reserve approximately 715 PJ

• upgrade and maintain the NWS domestic gas facilities with sufficient capacity

• diligently market the committed gas quantities to the domestic market

• report to the WA Government annually

While the Agreement Amendment provides more domestic supply certainty, several on going decisions have to be made.

7

North West Shelf update

It now appears likely that some supply will be available from the NWS beyond 2020 but …..

the amendment does not specify :

• the timing or a minimum amount of domestic gas that must be made available beyond 2020

• the minimum level of domestic gas production capacity that must be maintained

The availability of domestic gas from the NWS remains contingent on whether the NWS can profitably and commercially maintain gas supply to the domestic market and multiple investment decisions (beyond Persephone) are yet to be made by the JVs.

However, in the 2015-2024 period, Hess may contract NWS to supply domestic gas (subject to commercial negotiation). Hess announced on 23 December 2014 its intention to develop and toll its WA gas reserves through the NWS processing facilities.

8

9

Forecast context

Findings

Forecasts

Other information

Key findings

• The supply of gas to the domestic market is expected to be adequate to meet demand over the forecast period

• However, with several commercial and investment decisions yet to be made, the extent of any future supply from the NWS is not yet known with certainty, and the supply-demand balance may tighten after 2020

10

Supply – Demand balance

11

900

1,100

1,300

1,500

1,700

1,900

2,100

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024

Qua

ntity

(TJ

per d

ay)

Expected gas demand Lower potential gas supply forecasts

Upper potential gas supply forecasts Total production capacity

Source: NIEIR and IMO Estimates, 2015-2024

Other findings

Gas Demand

• Demand in the non-SWIS areas will grow faster than SWIS

• Rapid growth of total gas demand (domestic & LNG); start-up of Gorgon, Wheatstone and Prelude domestic gas & LNG projects

Resources and Reserves

• Conventional gas reserves is estimated to last between 12 to 37 years, depending on technology (Table 9.4), unconventional reserves (105 years)

• Gas production in WA remain reliant on conventional reserves in the Carnarvon Basin (Table 9.5)

• Exploration of unconventional resources need to be fostered

12

13

Forecast context

Findings

Forecasts

Other information

Gas demand 2015 – 2024

Growth in the early years of the gas demand forecasts is driven by new large gas-consuming projects. These projects include:

• Sub161’s CNG facility at Port Hedland

• the Fortescue River Gas Pipeline

• the Eastern Goldfields Gas Pipeline

And increased gas consumption relating to:

• Alinta Energy’s Newman Power Station which will supply electricity to the Roy Hill mine

• operation of TransAlta’s South Hedland Power Station

• the Pilbara Temporary Power Station

• CITIC Pacific’s Sino Iron’s magnetite mine

14

Domestic gas demand and forecasts 1983 – 2024

15

0

200

400

600

800

1000

1200

140019

8319

8419

8519

8619

8719

8819

8919

9019

9119

9219

9319

9419

9519

9619

9719

9819

9920

0020

0120

0220

0320

0420

0520

0620

0720

0820

0920

1020

1120

1220

1320

1420

1520

1620

1720

1820

1920

2020

2120

2220

2320

24

Qua

ntity

(TJ

per d

ay)

Historical gas consumption Base demand forecast High demand forecast

Source: DMP and IMO Estimates, 2015-2024

IMO and CMEWA WA demand forecasts 2015 – 2023

16

340

350

360

370

380

390

400

410

2015 2016 2017 2018 2019 2020 2021 2022 2023

Qua

ntity

(PJ

per a

nnum

)

CMEWA's forecast NIEIR's forecast

Source: CMEWA, Deloitte Australia and IMO Estimates, 2015-2023

Total gas demand forecasts 2015 – 2024

17

0

1,000

2,000

3,000

4,000

5,000

6,000

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024

Qua

ntity

(PJ

per a

nnum

)

Base scenario High scenario

Source: NIEIR and IMO Estimates, 2015-2024

Forecast prices used in modelling 2015 – 2024

18

$0.0

$2.0

$4.0

$6.0

$8.0

$10.0

$12.0

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024

Pric

e (A

$ pe

r GJ)

December 2014 Base scenario January 2014 GSOO Base scenario

Source: NIEIR and IMO Estimates 2015-2024

Gas supply forecasts 2015 – 2024

19

Source: IMO Estimates 2015-2024

900

1,100

1,300

1,500

1,700

1,900

2,100

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024

Qua

ntity

(TJ/

day)

Lower Potential Gas Supply Forecasts Upper Potential Gas Supply ForecastsTotal Production Capacity

20

Forecast context

Findings

Forecasts

Other information

What’s new in the December 2014 GSOO

Modelling

• Prospective gas projects included in High gas demand scenario

• Improvements to gas consumption estimates of iron magnetite projects

• Improvements to potential gas supply model (considers non-LNG linked facilities)

• LNG feedstock and processing requirements (now considers utilisation rates)

Information

• Greater use of GBB data (more details to come)

• More detailed analysis of demand and its drivers

21

Other information in December 2014 GSOO

Additional Information on:

• Drivers of domestic gas consumption

• Gas production outages

• Gas injection and withdrawals (Mondarra)

• Gas production statistics

• Gas shipping by pipeline

22

Gas demand, August 2013 – November 2014

23

31% 29% 30% 30% 32% 31% 27% 26% 30% 30% 28% 29%

32% 32% 32% 29% 28% 29% 31% 33% 34% 30% 30% 31%

12% 12% 12% 12% 12% 12% 14% 12% 15%

15% 13% 14%

11% 11% 11% 12% 11% 11% 11% 10% 2% 8% 11% 11%

5% 7% 7% 7% 7% 5% 5% 5% 7% 7% 6% 6%

10% 8% 9% 9% 10% 11% 13% 12% 12% 10% 10% 10%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Dec-2013 Feb-2014 Apr-2014 Jun-2014 Aug-2014 Oct-2014

Prop

ortio

n

Minerals processing Electricity Mining Industrial Other Distribution network

Source: IMO GBB

Production facility outages, August 2013 – November 2014

24

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

Prop

ortio

n

Source: IMO GBB

Gas injections and withdrawals (Mondarra), August 2013 – November 2014

25

0

10

20

30

40

50

60

70

80

90

100

Aug-13 Oct-13 Dec-13 Feb-14 Apr-14 Jun-14 Aug-14 Oct-14

Qua

ntity

(TJ

per d

ay)

Gas withdrawn Gas injectedSource: IMO GBB

Gas production statistics, Q4 2013 to Q3 2014

Facility Nameplate capacity (TJ per day)

Peak production October 2013 to September 2014

Day of peak production Average production

Q4 2013 (TJ per day)

Q1 2014 (TJ per day)

Q2 2014 (TJ per day)

Q3 2014 (TJ per day)

Beharra Springs 19.6 19.8 5/10/2013 10.2 9.2 13.9 18.1

Dongara 7 2.5 4/9/2013 2.1 1.8 1.7 1.4

Devil Creek 220 172.5 22/11/2013 135.6 69.6 65.8 76.2

KGP 630 671.9 1/8/2013 443.6 459.2 470.0 493.7

Macedon 200 213.1 10/9/2013 164.5 141.5 142.9 152.3

Red Gully 10 14.7 14/4/2014 7.6 6.0 4.0 7.7

Varanus Island 390 371.7 3/1/2014 272.5 299.4 271.6 234.9

Total 1476.6 1,036.1 986.7 969.9 984.3

26

Source: IMO GBB

Gas production statistics, Q4 2013 to Q3 2014

Facility Nameplate capacity (TJ per day)

Peak production October 2013 to September 2014

Day of peak production Average production

Q4 2013 (TJ per day)

Q1 2014 (TJ per day)

Q2 2014 (TJ per day)

Q3 2014 (TJ per day)

Beharra Springs 19.6 19.8 5/10/2013 10.2 9.2 13.9 18.1

Dongara 7 2.5 4/9/2013 2.1 1.8 1.7 1.4

Devil Creek 220 172.5 22/11/2013 135.6 69.6 65.8 76.2

KGP 630 671.9 1/8/2013 443.6 459.2 470.0 493.7

Macedon 200 213.1 10/9/2013 164.5 141.5 142.9 152.3

Red Gully 10 14.7 14/4/2014 7.6 6.0 4.0 7.7

Varanus Island 390 371.7 3/1/2014 272.5 299.4 271.6 234.9

Total 1476.6 1,036.1 986.7 969.9 984.3

27

Source: IMO GBB

Quantity of gas shipped by pipeline, Q4 2013 to Q3 2014

28

0

10

20

30

40

50

60

70

80

90

100

Q4 2013 Q1 2014 Q2 2014 Q3 2014

Qua

ntity

(PJ)

DBNGP GGP PEP All other pipelinesSource: IMO

Events since publishing December 2014 GSOO • Oil prices (Brent and WTI) falls below US$50/bbl -> Contracted LNG prices falls

below spot (Japan)

• First shipment of LNG leaves Queensland’s QCLNG project

• Shell drops Arrow LNG project

• Quantity of gas reserves relating to Red Gully JV are upgraded

• ACCC commences an inquiry into Woodside’s purchase of Apache Energy’s interests

• Ivernia’s Paroo lead mine placed into care and maintenance (from February 2015)

• TEPCO and Chubu Electric establishing 50/50 JV (to manage all energy assets)

• Proposed Panama Canal charges for LNG carriers released

29