2013 Review of Key Trends In Internet and Digital Media - Presentation at IAB

59

Review of Key Trends in Internet/Digital Media November 8, 2013

-

Upload

linda-gridley -

Category

Economy & Finance

-

view

850 -

download

1

Transcript of 2013 Review of Key Trends In Internet and Digital Media - Presentation at IAB

Review of Key Trends in Internet/Digital Media

November 8, 2013

2

I. Setting the Stage

II. Breakdown of Digital Media Sector Activity

III. 2014 Predictions

IV. Quick Gridley Commercial

Agenda

© 2013 Gridley & Company LLC

I. Setting the Stage

4

Broad Market Glance YTD 2013

(60%)

(40%)

(20%)

0%

20%

40%

60%

Jan-08 Sep-08 Jun-09 Feb-10 Nov-10 Jul-11 Apr-12 Jan-13 Sep-13

Source: PriceWaterhouse Coopers; National Venture Capital Association (2013); Capital IQ.

Key Themes in Internet/Digital Media Market Index Performance

© 2013 Gridley & Company LLC

+30.5% YTD

+23.6% YTD

Performance of Internet Bellwethers

YTD Since 2008

44.6% 47.9%

42.0% 284.5%

65.2% 41.4%

4.5% 60.5%

84.5% NA

Strong Market Despite Headwinds

• High unemployment: 7.2% in September

• Fiscal ceiling uncertainty / government

shutdown

• Record amount of cash on corporate balance

sheets

5

Source: PriceWaterhouse Coopers; National Venture Capital Association (2013); Capital IQ.

Ven

ture

Fu

nd

ing

M

&A

Volu

me

VC

M&A

M&A and Venture Funding Volume Since 1995 ($ in billions)

M&A and VC Volume Appear to Be In Line with Prior Years

© 2013 Gridley & Company LLC

$0.0

$20.0

$40.0

$60.0

$80.0

$100.0

$120.0

$140.0

$160.0

$180.0

$200.0

$0.0

$5.0

$10.0

$15.0

$20.0

$25.0

$30.0

$35.0

$40.0

$45.0

6

Billion Dollar Valuations with Little to No Revenue

-Are We in a Bubble?

“Big companies are scarcely growing, and interest rates remain near zero, boosting

zeal for investment opportunities in companies with high-growth potential.” -WSJ

10/27/13

“The price tag… is determined by the market, which right now

is starting to look like the housing bubble of the mid-2000s.

-NYT 10/31/13

LTM Revenue $0 $13 $0 $107 $82 $145 $0 $0 $125

$1,000 $1,100 $966

Instagram Tumblr Waze

$4,000 $3,800 $3,400

Snapchat Pinterest Uber

$1,160

$13,600

$1,062

Rocketfuel Twitter RetailMeNot

Billion Dollar Valuations ($ millions)

M&A Private Placement IPO

Source: Capital IQ, TechCrunch, Wall Street Journal article dated 10/27/2013

© 2013 Gridley & Company LLC

7

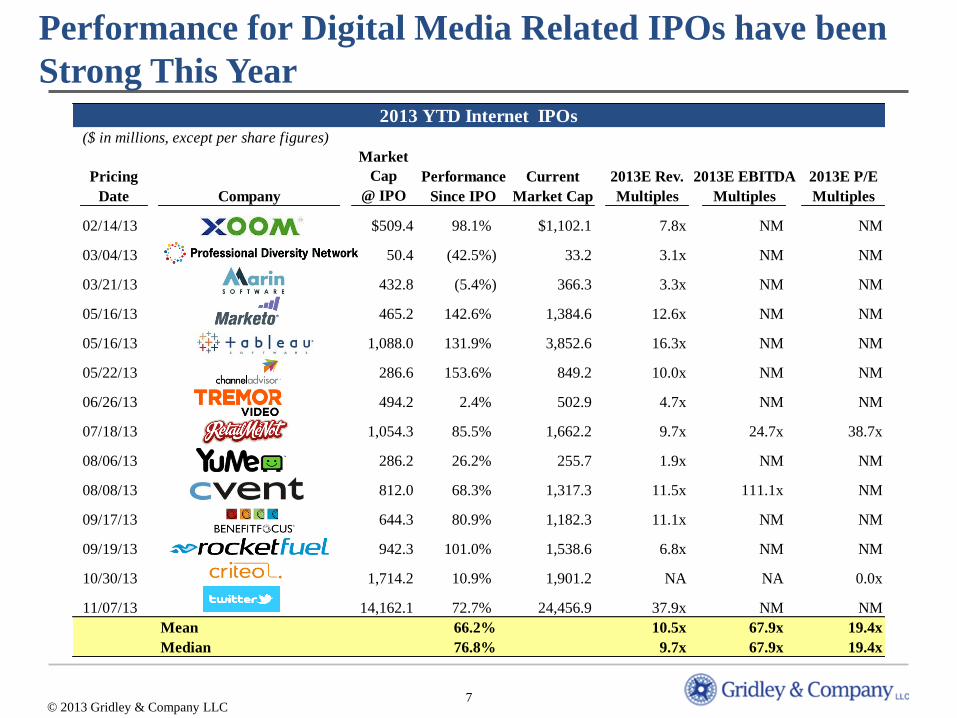

2013 YTD Internet IPOs($ in millions, except per share figures)

Pricing

Market

Cap Performance Current 2013E Rev. 2013E EBITDA 2013E P/E

Date Company @ IPO Since IPO Market Cap Multiples Multiples Multiples

02/14/13 $509.4 98.1% $1,102.1 7.8x NM NM

03/04/13 50.4 (42.5%) 33.2 3.1x NM NM

03/21/13 432.8 (5.4%) 366.3 3.3x NM NM

05/16/13 465.2 142.6% 1,384.6 12.6x NM NM

05/16/13 1,088.0 131.9% 3,852.6 16.3x NM NM

05/22/13 286.6 153.6% 849.2 10.0x NM NM

06/26/13 494.2 2.4% 502.9 4.7x NM NM

07/18/13 1,054.3 85.5% 1,662.2 9.7x 24.7x 38.7x

08/06/13 286.2 26.2% 255.7 1.9x NM NM

08/08/13 812.0 68.3% 1,317.3 11.5x 111.1x NM

09/17/13 644.3 80.9% 1,182.3 11.1x NM NM

09/19/13 942.3 101.0% 1,538.6 6.8x NM NM

10/30/13 1,714.2 10.9% 1,901.2 NA NA 0.0x

11/07/13 14,162.1 72.7% 24,456.9 37.9x NM NM

Mean 66.2% 10.5x 67.9x 19.4x

Median 76.8% 9.7x 67.9x 19.4x

Performance for Digital Media Related IPOs have been

Strong This Year

© 2013 Gridley & Company LLC

8

However, The IPO Market Appears To Be Rational

Relative to 1999

1999 2013 YTD

# of IPOs 368 32

Mean first-day return 87% 26%

Median age of company 4 years 13 years

# that doubled in price on first day 114 1

% with <$50 million LTM Revenue (2005 dollars) 84% 22%

% that were unprofitable LTM 86% 66%

Median ratio of market value to sales, at IPO 26.5x 5.6x

© 2013 Gridley & Company LLC

• Market much more selective vs. 1999 in terms of business model and growth

characteristics

Source: Wall Street Journal article dated 10/27/2013

9

Consumer Monetization Models Today Are More Easily

Understood…

Revenue Jumps When Revenue Models are

“Turned On” Valuation tied to User Adoption

($ in Millions) (Consumers in Thousands)

© 2013 Gridley & Company LLC

1,0005,000

10,000

30,000

100,000

150,000

Dec-

10

Feb

-11

Apr-

11

Jun

-11

Aug

-11

Oct-

11

Dec-

11

Feb

-12

Apr-

12

Jun

-12

Aug

-12

Oct-

12

Dec-

12

Feb

-13

Apr-

13

Jun

-13

Aug

-13

$28

$106

$317

2010 2011 2012

$6

$52

$150

2005 2006 2007

acquisition of

Instragram

10

28.4%

28.9%

33.3%

61.5%

71.6%

102.2%

111.1%

Tremor Video, Inc.

Marin Software Inc.

YuMe, Inc.

Marketo, Inc.

Criteo SA*

Twitter, Inc.

Rocket Fuel Inc.

-15.0%

10.6%

17.2%

21.0%

24.2%

38.5%

76.1%

QuinStreet, Inc.

Bankrate, Inc.

Constant Contact, Inc.

ReachLocal, Inc.

ValueClick, Inc.

ExactTarget, Inc.

Millennial Media Inc.

…And Higher Growth Profiles in Digital Marketing are

Coming to Market

Average : 24.5% Average : 62.4%

* Criteo 2013E revenue growth is based on 2013 1H run rate

Public Comp Universe at End of 2012

’12-’13 Revenue Growth

New Public Comps in 2013

’13-’14 Revenue Growth

© 2013 Gridley & Company LLC

2012

Revenue

Multiple

2013E

Revenue

Multiple

4.8x

3.9x

2.3x

0.6x

2.8x

4.1x

1.0x

6.8x

NM

3.0x

12.6x

2.0x

3.3x

4.7x

Median: 21.0% 2.3x 2.0x Median: 61.5% 3.7x

3.2x

3.9x

2.9x

0.5x

2.5x

4.1x

1.0x

2013E

Revenue

Multiple

11

Key Themes in Strategic M&A and Funding Market

• Consolidation still quiet in fragmented sectors such as Adtech

‒ Complicated cap structures with multiple layers of institutional capital

‒ Investors with different time horizons and priorities on same deals

‒ Lots of strategics holding on to cash

• M&A as a recruiting tool is here to stay – didn’t exist five years ago

‒ Yahoo, Google, Twitter, Facebook all compete with hiring talent

‒ Still primarily a B2C concept, few examples of enterprise software

companies employing this tactic

‒ From banker’s perspective, no company is too small

• VC/PE investors reluctant to triage their portfolios, believe all will be home runs

© 2013 Gridley & Company LLC

12

Digital Leaders Are Known to Overpay into Platform

Shifts

$1,561

NA

$850

NA

$5,000

NA

$745

18.63x(1)

$400

NA

$1,100

73.33x(2)

$966

NA

$350

NA

$1,000

NA

Desktop Chews into

Traditional Media

Consumers Move

to Social Channels

Mobile Overtakes

Desktop for

Consuming Content

Internet Becomes

Scalable Transaction

Medium

$1,433

8.25x

$3,727

NA

$410

NA

1) BuddyMedia rumored LTM revenue is $40MM.

2) Tumblr’s rumored LTM revenue is $15 MM based on 2013 Q1 run rate.

Sale Price

LTM Rev.

Multiple

Sale Price

LTM Rev.

Multiple

Sale Price

LTM Rev.

Multiple

13

Internet Leaders Have and Will Continue to Make

Transformational Business Moves Through M&A

Online shoe and apparel retailer

Online audio entertainment

Online CD and video retailer

Online daily deals

Online baby product retailer

Social book cataloguing

Online seller-bid auction

Digital transactions platform

VOIP and IM client

Online payment system

Digital commerce services provider

Digital payments processer

Pay-per-click advertising

Ad exchange

Job search engine

Web hosting

Microblog and social network

Internet radio

Search solutions provider

Mobile operating system

Online video-sharing website

Handset manufacturing division

Smartphone navigation app

Social media marketing

© 2013 Gridley & Company LLC

14

eBay Has Systematically Built A Multi-Channel

Commerce Capability Through M&A

Discover Pay

In-store

scanner

Nearby

Used, online

Online

retail

Nearby

Used, online

Online retail

Virtual goods

Local Retailers

/ SMB

Any product

Store locator

and location-

based deals

Retailer

At Home

eBay made a series of acquisitions, most notably of PayPal, GSI Commerce, Red Laser, Zong, and Milo,

that enabled eBay to become a front-runner in the race to become the next generation in-store leader

Better

Merchandising

Card-in-cloud

Online social retail

© 2013 Gridley & Company LLC

15

Legend

0%

20%

40%

60%

80%

100%

120%

140%

0.0x 5.0x 10.0x 15.0x 20.0x 25.0x

Adtech

Enterprise

Consumer Internet

Growth and Scale are Primary Factors in Valuations

Today

2013E Revenue Growth Rate vs. 2013E Revenue Multiple

20

13

E R

even

ue G

row

th

Revenue Multiple

$269MM

$615MM

$225MM

$77MM

$706MM

$175MM

$204MM

$10.4BN

$345MM

$243MM

$894MM

$5.2BN

$532MM

$124MM

© 2013 Gridley & Company LLC

II. Sector View of Key Trends and Themes

17

Sector

© 2013 Gridley & Company LLC

AdTech

Mobile

Content

Social

eCommerce

18

AdTech – Gridley was First to Write About It: Sept. 2009

© 2013 Gridley & Company LLC

September 2009

• First to develop an industry overview

based on the premise that the sector

was moving into new phase of growth

and innovation

‒ Just beginning to understand data

‒ Inventory was becoming

biddable

‒ Social was emerging as a new

channel

19

Key Trends in Adtech

• Recent IPOs have brought new life into the Adtech community

‒ Creating urgency to get scale

‒ Establishing clarity around value for high growth advertising stories

• Noise level on Privacy/Cookie debate up; although still very exploratory in

terms of going forward models

• Category leaders getting funding, but otherwise hard market for new capital

‒ Understanding and executing on data is actually very hard!

• Convergence of marketing and advertising technologies not leading to

considerable strategic activity yet

© 2013 Gridley & Company LLC

20

The Shift to Digital is Creating a New Architecture

for the Advertising Buying Process

Traditional Digital

Data

Agency

TV

Data

Agency

Data

Agency

Radio

Data

Agency

Online

Digital

Media

Buyer/Marketer

Data

Video Mobile Site Social

Agency

Consumer

© 2013 Gridley & Company LLC

21

The CMO’s Dilemma – Multiple, Disconnected Channels

Mobile

CMO

• Advertising

• Marketing

• LBS

Display

• Networks

• DSPs

• Direct Sold

• Various capabilities (e.g. retargeting)

Social

• Word of mouth

• Campaigns

• Paid

• Owned

• Earned

• Mass branding

• One-to-one (rules based)

Search

• Google vs. others

• Bid optimization solutions

Video

• Pre vs. post roll

• Networks

• Direct Sold

Capabilities within Digital Channels Continue to Expand

© 2013 Gridley & Company LLC

22

The Buy-side Value Chain – Race to Build Value

Through Use of Data

Execution

Workflow/Mgmt

Value Chain

Planning

Analytics

Data Mgmt

CRM

DSP/Network Social

Publishing Self Serv.

Adserving

Creative Attribution

Modeling Optimization

Warehouse

MRM Ops MAM

Database

Scoring

Normalize Segment

LBS Email

• Strategic value is moving to the middle of the value chain as the value of data

becomes better understood

© 2013 Gridley & Company LLC

23

Notable M&A

Top 2013 Ad Tech M&A and Private Placements

$405MM

$350MM

$261MM

$40MM

$36MM

$75MM

$119MM

$16 MM

Notable Private Financings

Acquirer Target Company

© 2013 Gridley & Company LLC

• Consolidation has been needed in Adtech for

five years, still very fragmented

• Chatter around merger discussions up;

remains to be seen if there is action

$36MM

• Many VCs have moved away from Adtech,

Others are very selective

‒ Clear path to IPO

‒ New data models that create unique

marketer value

Aug. 2013

Sep. 2013

Aug. 2013

Oct. 2013

Feb. 2013

24

(40%)

(20%)

0%

20%

40%

60%

80%

100%

120%

140%

DaysSince

IPO

7 14 21 28 35 42 49 56 63 70 77 84 91 98 105 112 119 126 133 140 147 154

2013 AdTech IPOs

Stock Price Performance

© 2013 Gridley & Company LLC

• Scale and growth clear prerequisites

• Recent success of Criteo and Rocket Fuel have bolstered Tremor and YuMe following their

weaker post IPOs performance earlier this summer

• Overall, mixed public market performance

9.6x LTM Revenue

4.0x LTM Revenue 2.0x LTM Revenue

4.7x LTM Revenue 3.3x LTM Revenue 4.4x 2013E Revenue

1.9x 2013E Revenue 3.0x 2013E Revenue

6.8x 2013E Revenue

3.0x 2013ERevenue

$336 million Market Cap $459 million Market Cap

$1.5 billion Market Cap

$249 million Market Cap $1.9 billion Market Cap

25

Sector

© 2013 Gridley & Company LLC

Ad Tech

Mobile

Content

Social

eCommerce

26

0.0

0.5

1.0

1.5

2.0

2.5

3.0

2009 2010 2011 2012E 2013E 2014E 2015E

Glo

ba

l In

sta

lled

Ba

se (B

illi

on

s)

Desktops+NotebooksSmartphones+Tablets

Mobile Is the Most Important Broad Theme in 2013

Driven by A Rapid Shift in Consumer Behavior

Note: Notebook PCs include Netbooks. Assumes the following lifecycles: Desktop PCs – 5 years: Notebook PCs – 4 years; Smartphones – 2 years; Tablets – 2.5 years.

Source: Morgan Stanley Research, 2012.

Q2:13E: Projected Inflection

Point Smartphones + Tablet

Installed Base > Total PCs

Installed Base

© 2013 Gridley & Company LLC

27

Key Trends in Mobile

• 2013 was the year of mobile from many perspectives

‒ Positive mobile consumption trends, quickly overtaking

desktop

‒ Internet bellwethers have executed multiple large scale M&A

deals

‒ Scaled consumer adoption of vertical specific application such

as Uber and Waze

• Facebook and Twitter are educating the broader market on value of

mobile marketing

• Mobile driving much of the innovation in the payments sector today

‒ Exciting opportunity in the convergence between marketing

and payments

© 2013 Gridley & Company LLC

28

POS – A Major Battleground in Mobile

Market Research /

Data Analytics

Digital Commerce

Account Marketing

Payments

eReceipts

Consumer

© 2013 Gridley & Company LLC

29

$1.0$1.5

$2.2$2.9

$3.6$4.1

$0.7

$1.2

$2.1

$3.1

$4.5

$5.8

2011 2012 2013 2014 2015 2016

National Local

$8.1

$6.0

$4.3

$2.7

$9.9

$1.7

Massive Strategic Opportunity with Mobile + Local

Rise of Localized Mobile Marketing

Sources: BIA Kelsey, “From National to Local: Mobile Advertising Zeroes In,” Jan. 2013; BI Intelligence; Balihoo, “Micro Study:

National Brand Use of Digital in Local Marketing,” Oct. 30, 2012.

41%

58%

Local vs. National Mobile Ad Spend ($ in billions)

Higher Banner Ad CTR for Local Businesses

CTR Lift

40%

CTR Lift

48%

CTR Lift

26%

CTR Lift

5%

<1 Mile 1 to 2 Miles 2 to 5 Miles 5 to 10 Miles

30

Notable M&A

Top 2013 Mobile M&A and Private Placements

$155MM

$225MM

$66MM

$60MM

$361MM

$51MM $100MM

Notable Private Financings

Acquirer Target Company

© 2013 Gridley & Company LLC

• Aggressive VC market across the spectrum

• Continue to see large scale deals as mobile

applications, complimented by tech/team

and tuck in deals

$1.1BN

$350MM

$261MM

Jun. 2013

Sep. 2013

Aug. 2013

Feb. 2013

Apr. 2013

Aug. 2013

Feb. 2013

Jul. 2013

May 2013

Sep. 2013

Large mobile team:

31

Sector

© 2013 Gridley & Company LLC

Ad Tech

Mobile

Content

Social

eCommerce

32

• Originally presented content

sector overview for Business

Insider in 2010. Presented with

update in 2011.

‒ For content to be

successful, businesses need

to think about moving

beyond the simple

browse/consume model

‒ Traditional publishers vs.

new digital publishers –

who can adopt new tools

such as UGC, gaming

mechanics, social, mobile?

© 2013 Gridley & Company LLC

Historical Gridley Views on Content

33

Key Trends in Content

• Healthy valuations in content enablement (e.g. Wordpress) and big

vertical niche properties (e.g. Houzz)

• Ongoing pressure from traditional ad models has force some innovation

in consumer acquisition/retention, revenue models,

integration/coordination across channels

‒ Deeper integration into social channels

‒ New advertising formats such as native advertising

‒ Better mobile consumption experiences

‒ More integrated use of user generated content

• Most traditional media companies still on the sidelines from an M&A

perspective

• Few good public comparable market for digital content businesses

© 2013 Gridley & Company LLC

34

© 2013 Gridley & Company LLC

Change in Content Consumption Behavior Has Been a

Driving Factor in Digital Content Landscape

Browsing and Consuming Behavior

Since the 1950’s… New Content Consumption Model

• The Network

• Science

• Curation

• Incentives

• Location

Tweet

“Like”

Tag

Check-in

• Play

• Watch

• Read

• Converse

• Opine

• Review

• Rank

Revenue Acclaim Loyalty Intelligence

35

Notable M&A

Top 2013 Content M&A and Private Placements

$1.1BN

$68MM

$51MM

$35MM

$750MM

$34MM

Notable Private Financings

Acquirer Target Company

© 2013 Gridley & Company LLC

• Content deal market remains quiet overall

‒ Few buyers in the market for digital

content assets

‒ No material change in behavior in

past 3 years

• Renewed excitement for vertically focused

publishers

‒ Multiple $15mm+ capital raises

• Relatively harder to secure earlier stage

funding vs. other digital segments

May 2013 Jul. 2013

May 2013

Sep. 2013

Jan. 2013

Oct. 2013

36

Sector

© 2013 Gridley & Company LLC

Ad Tech

Mobile

Content

Social

eCommerce

37

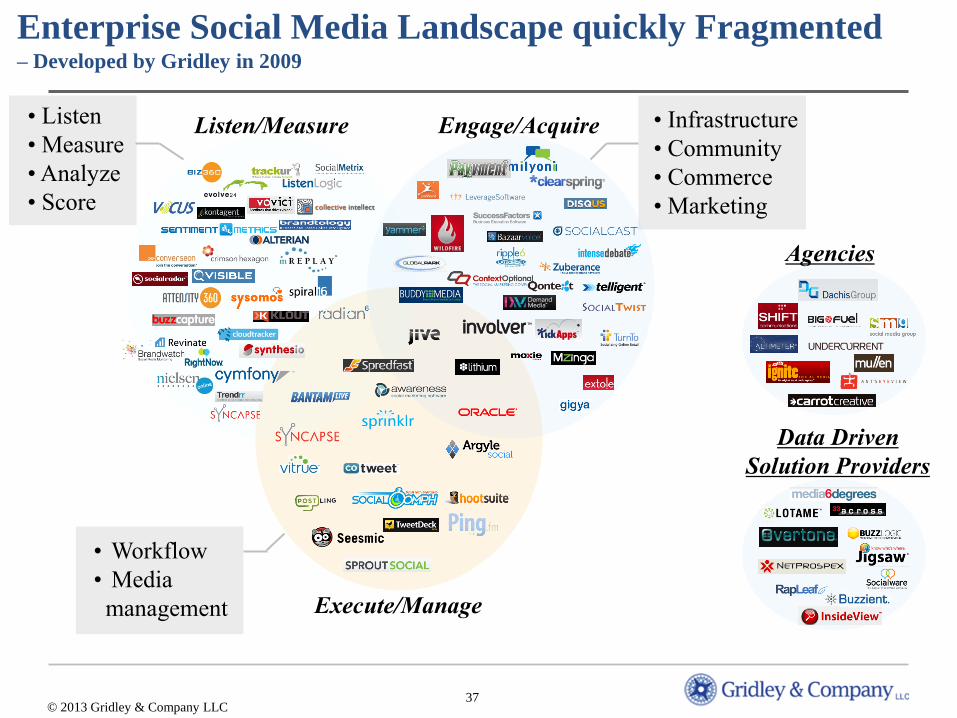

Enterprise Social Media Landscape quickly Fragmented – Developed by Gridley in 2009

Engage/Acquire

Execute/Manage

Agencies

Listen/Measure

Data Driven

Solution Providers

© 2013 Gridley & Company LLC

• Listen

• Measure

• Analyze

• Score

• Workflow

• Media

management

• Infrastructure

• Community

• Commerce

• Marketing

38

Key Trends in Social

• Platform shift to social has created a lot of success stories and exposed a

few vulnerabilities

‒ Positive: Consumer monetization models, value of network effects

‒ Negative: Can a sustainable business be build social media

management?, ecommerce on social doesn’t work, long-term ability

to create a “platform” around users in question

• Fickle users drive consumer businesses, creating new opportunities and

risks

• Social creating positive impact across the digital ecosystem

‒ Content, commerce and mobile big beneficiaries

© 2013 Gridley & Company LLC

39

As the Channel Matured, Social Has Started to Have

Broad Reaching Implications

Social Will Increasingly Play a Role Across the Digital Ecosystem

Commerce

Adv/Mkt. Content

Mobile

• Mobile only

social solutions

are gaining

mass adoption,

bypassing

desktop entirely

• Considerable inventory

controlled by social

platforms opening up

this year

• Social remains a key

strategic channel for

CMOs

• Developing models

that tie social

connectivity into the

path to purchase

• Solving consumer

discovery challenges

via social curation

• Maturing models

around advertising

in user generated

content

© 2013 Gridley & Company LLC

40

Notable M&A

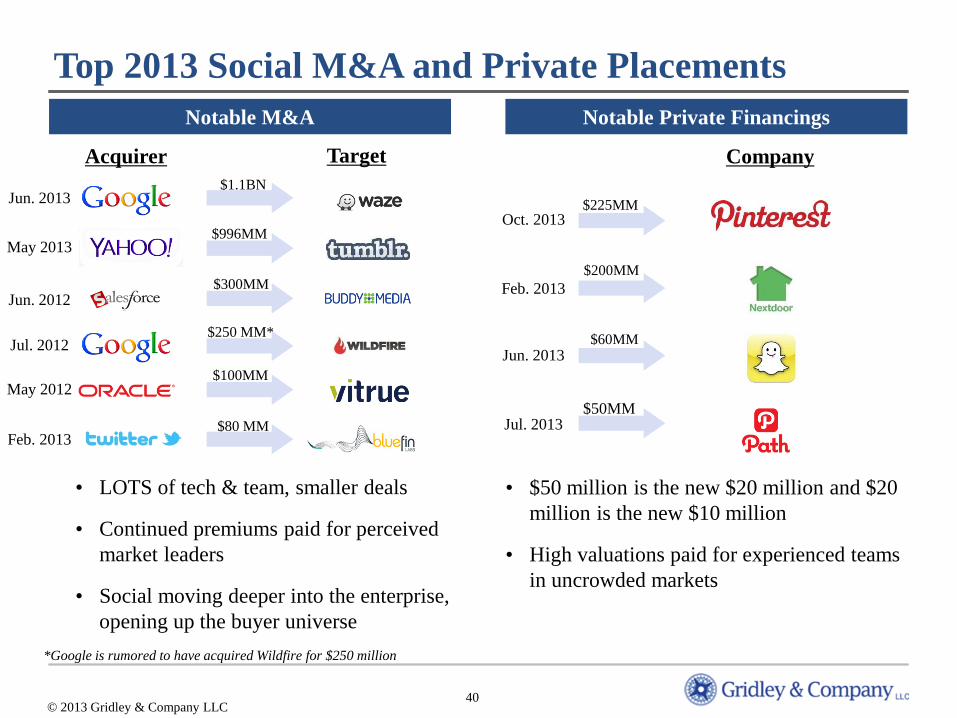

Top 2013 Social M&A and Private Placements

$200MM

$60MM

$50MM

$225MM

Notable Private Financings

Acquirer Target Company

© 2013 Gridley & Company LLC

$1.1BN

$300MM

$100MM

• LOTS of tech & team, smaller deals

• Continued premiums paid for perceived

market leaders

• Social moving deeper into the enterprise,

opening up the buyer universe

• $50 million is the new $20 million and $20

million is the new $10 million

• High valuations paid for experienced teams

in uncrowded markets

$80 MM

$996MM

$250 MM*

*Google is rumored to have acquired Wildfire for $250 million

Jun. 2013

May 2013

Jun. 2012

Jul. 2012

May 2012

Feb. 2013

Oct. 2013

Feb. 2013

Jun. 2013

Jul. 2013

41

Sector

© 2013 Gridley & Company LLC

Ad Tech

Mobile

Content

Social

eCommerce

42

Gridley was One of the First to Write an In-Depth Sector Report

-April 2011

• Developed an industry overview

based on the premise that

innovation was happening at

various levels

‒ New business models such

as flash sales and

subscription commerce

‒ Evolution of back end

technologies that support

new challenges as

ecommerce scaled

‒ Consumer path to purchase

became more complex,

creating greater new to

understand data

© 2013 Gridley & Company LLC

43

Key Trends in eCommerce

• eCommerce is finally strategic as it approaches 10% of all commerce and

is influencing 50% of all purchasing

‒ Decisions being made in the C-suite, transitioning from CTO to

CMO

• Business models still very much in experimental phase

‒ Flash sales, subscription commerce, social commerce, in-store all

developing

‒ Started to see scaleable + sustainable models emerge this year

• Content + Commerce did not pane out across demographics

• Online/Offline convergence still early, but viewed as strategically

important

© 2013 Gridley & Company LLC

44

eCommerce has Very Strong Growth Dynamics

Source: Forrester Reports dated March 13, 2013 and July 25, 2013

© 2013 Gridley & Company LLC

Forecast: US Online Retail Sales 2012 to 2017

eBusinesses are Shifting Spending to

Commerce-Related Technologies

Digital is “10 – 50 – 100”

10%

50%

100%

Source: Kantar Retail “Digital Power 2013” report

• ~10% total retail sales are eCommerce sales

• Development of “omnichannel” experiences open

opportunities in mobile and marketing

• 50% total retail sales are estimated to be influenced

by digital

‒ Showrooming, research, planning

• Digital has an impact on 100% of the modern

shopping experience

45

Notable M&A

Top 2013 eCommerce M&A and Private Placements

$316MM

$180MM

$125MM

$250MM

$170MM

$110MM

$361MM

$98MM

$94MM

$50MM

Notable Private Financings

Acquirer Target Company

dba: NMD Interactive

© 2013 Gridley & Company LLC

• Most M&A focused on B2B as software

companies like IBM and Netsuite expand

retail capabilities into digital

• Continued investor interest in new

commerce models

‒ Rent the Runway, Birchbox, etc

Undisclosed

$206MM

Jul. 2013

Aug. 2013

Feb. 2013

Jun. 2013

Aug. 2013

May 2013

Aug. 2013

Apr. 2013

Jun. 2013

Feb. 2013

Sep. 2013

46

0%

20%

40%

60%

80%

100%

120%

140%

160%

180%

200%

DaysSince

IPO

5 10 15 20 25 30 35 40 45 50 55 60 65 70 75 80 85 90 95 100 105 110 115

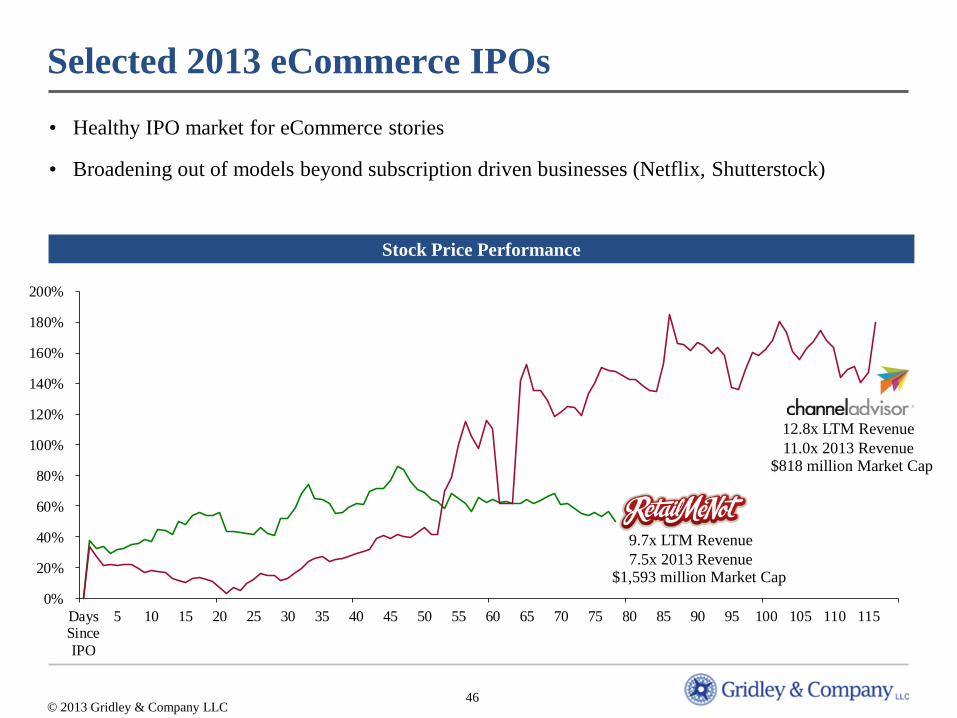

Selected 2013 eCommerce IPOs

Stock Price Performance

© 2013 Gridley & Company LLC

• Healthy IPO market for eCommerce stories

• Broadening out of models beyond subscription driven businesses (Netflix, Shutterstock)

9.7x LTM Revenue

12.8x LTM Revenue

7.5x 2013 Revenue $1,593 million Market Cap

11.0x 2013 Revenue $818 million Market Cap

III. 2014 Predictions

48

IPO Market

VC/PE

Funding

M&A Market

• Valuation bubble needs to show signs of popping

• Big VC investments are squeezing out PE growth opportunities

• Everyone can’t be a billion-dollar company

• Investors get smarter and more exposure in Ad Tech

• Differentiated performance across IPOs

• Quality in Digital Media IPOs will fall

• Continuation of Team & Team deals

• More M&A courage from the New Guys

• Traditional strategic buyers continue to fall behind digital leaders

Exciting Value Creators for 2014

© 2013 Gridley & Company LLC

49

Mobile • Consumer and innovative

“use cases” driving growth

eCommerce • Where Adtech was two years ago,

a lot of M&A expected

Content • Need strategic buyers, watching

out for exciting content tools and

new content models to emerge

Social • First wave of consolidation

happened in 2012; next wave of

innovative products beginning to

emerge

AdTech • More IPOs, and new buyers to help

fuel M&A

• Additional visibility on write offs,

• Programmatic and data driven

growth remains focus of the sector

Key 2014 Sector Themes

V. Quick Gridley Commercial

51

Gridley Overview

Gridley & Company LLC, a New York-based boutique investment bank, provides advisory

services to companies in the Information Services industry

Leading Boutique • Sharp focus provides clients with valuable strategic insights and perspectives

• Specialize in Internet Services, Digital Media & Marketing Services, Data

Services, Financial Technology, and SaaS & Outsourcing Services

• Founded in 2001

• Headquartered in New York, NY

Strong Reputation • Strong industry reputation on assignments led by senior bankers

• Experienced, bulge-bracket trained M&A bankers – The “A” Team

Trusted Advisor • Thoughtful ideas – not just logical combinations

• Deliver value to buyers, sellers, and investors alike

• Broad industry network developed over 25+ years with industry leaders,

emerging growth companies, and senior investors

Gridley & Company LLC

© 2013 Gridley & Company LLC

52

INDEPENDENT ADVICE

INTEGRITY

Gridley’s Differentiated Strategic Approach

Our broad network allows us to discern important trends early in their development, advise

clients on the best strategies to profit from those trends, and execute successful transactions

Strong Network of Relationships

• Split time 1/3, 1/3, 1/3 between

strategics, VC/PE firms, and private

company CEOs

• Built our business by visiting over 400

companies a year annually for 10+ years

• Have set up over 1,000 one-on-one

“meet and greet” meetings at our annual

January conference

INDEPENDENT ADVICE

INTEGRITY

Well-Known Thought Leadership

• Often hired by public company leaders

to advise them on major growth

initiatives

• Approximately 25% of business is

retained, strategic buy-side work for

industry leaders and selected PE

investors

• Use industry overviews to effectively

guide strategic buyers and PE investors

Ability to Strategically Position Companies Impressive Track Record

• Spend more time than our competitors

on the strategic positioning of our

clients

• Work together to optimize market

positioning

• Offer strategic insights based on our

understanding and perspective of the

industry

• Over 25 year history of successfully

completing transactions

• Clients like us and the job we do

• Goal is 100% referencable clients

• “No client gets left behind”

© 2013 Gridley & Company LLC

53

12+ Years of Strategic Thought Leadership

• January Conference

• Summer Networking

Event & Golf Outing

Quarterly Publications

Industry

Guides

Frequent

Industry Speaker

Annual Gridley Hosted

Events

• Highly respected

newsletter about industry

trends and corporate

finance / M&A activity

• In-depth review of the

digital NY ecosystem,

including recent startups

and the firms investing in

them

© 2013 Gridley & Company LLC

54

Host of Leading Annual Industry Conference for

13 years

• Bellwether event focused on our targeted industries

• Approximately 500 senior-level executives from over 300 companies

• Differentiated audience and participants vs. other conferences

• Highly personalized with Gridley arranged “1-on-1”s for clients, presenters, sponsors

• Presentations by approximately 40 private companies and industry panels addressing

timely topics

© 2013 Gridley & Company LLC

January 14, 2014

The Westin New York Grand

Central

(Invitation Only)

55

Event History – Track Record of Finding Highly

Successful Companies Early

• 218 private companies have presented since 2004

• Over 70% have completed liquidity transactions

Selected Past Conference Presenters

© 2013 Gridley & Company LLC

56

Gridley’s Guide to Digital NY

• Unique and comprehensive report for investors, buyers and entrepreneurs looking for one place to quickly

get up to speed on New York’s exciting, explosive digital ecosystem

• We decided to put together this report published originally in Oct. 2011 after people kept asking us about

all of the “digital momentum” in NY. There was a feeling that lots was going on, but people didn’t really

understand just what “it” was and how extensive “it” was. We aim to answer those questions here

• Digital New York report is updated on a quarterly basis and sent to 1,500+ senior executives and investors

• For an “easy to use” website that lays out the information in this report (and more) in a fun, creative way,

visit www.gridleyco.com or www.gridleydigitalny.com

© 2013 Gridley & Company LLC

57

Selected Recent Gridley Transactions

Gridley clients include industry leaders and premier emerging growth companies

© 2013 Gridley & Company LLC

58

Selected Recent Gridley Transactions cont.

© 2013 Gridley & Company LLC

Gridley & Company LLC

10 East 53rd Street, 24th Floor

New York, NY 10022

212.400.9720 tel

212.400.9717 fax

Twitter: @gridleyco

www.gridleyco.com

QUESTIONS?

Linda Gridley

President & CEO

212-400-9710

Pratik Patel

Managing Director

212-400-9712