2012 Leadership Conference xxxxxxxxx - Union Pacific 0 50 100 150 200 Fertilizer Demand * Publicly...

9

1 RailTrends November 21, 2014 Brad Thrasher, VP & General Manager Industrial Products 2 7% 1% 4% 4% 9% 11% 13% TOTAL Chemicals Coal Autos Intermodal Industrial Agricultural 2014 vs. 2013 YTD Carloadings 140 150 160 170 180 190 200 210 J F M A M J J A S O N D 7-Day Carloadings 2013 2006 2007 2011 2012 2010 2008 2009 2014 UP Volume 2014 thru October

Transcript of 2012 Leadership Conference xxxxxxxxx - Union Pacific 0 50 100 150 200 Fertilizer Demand * Publicly...

1

RailTrends November 21, 2014

Brad Thrasher, VP & General Manager Industrial Products

2

7%

1%

4%

4%

9%

11%

13%

TOTAL

Chemicals

Coal

Autos

Intermodal

Industrial

Agricultural

2014 vs. 2013 YTD Carloadings

140

150

160

170

180

190

200

210

J F M A M J J A S O N D

7-Day Carloadings

2013

2006

2007

2011

2012 2010

2008

2009

2014

UP Volume 2014 thru October

3

Key Insights • Economy expected to continue

to strengthen

• Improving unemployment and consumer sentiment encouraging

• Economy and population create strong growth foundation

Strengthening U.S. Economy Adds Potential*

*Source: IHS Global Insight: October 2014 Forecast

•

•

•

y

4

North American Manufacturers Becoming More Competitive Globally*

80

85

90

95

100

105

110

115

120

2003 2008 2013

U.S.

Total manufacturing cost indexed against U.S. = 100 Germany France Japan

UK

Canada

Mexico

Russia China Thailand

*Source: Boston Consulting Group

5

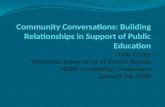

Industrial Production Growing share of GDP*

-14.0

-12.0

-10.0

-8.0

-6.0

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

IP vs. GDP IP GDP

*Source: IHS Global Insight: November 2014 Forecast

IP Lagged GDP Growth

IP Leads GDP Growth

6

Shale Market Impacts

Primary Shale Markets

Complementary Markets

ry SSShhhallle MMMa

Polyethylene Expansions

(C2H4)nH2

Manufacturing Expansions

Fertilizer Production

Refined Petroleum Products

Pipeline Construction

Construction Products

Frac Sand

Drill Pipe

Crude-by-Rail

7

Industrial Expansion

Steel, Pipe, Rock, Trucks

Low Feedstock Costs

Shale Revolution

Low Energy Costs

Demand for Durable Goods

Supporting Rebirth of Manufacturing in North America

8

Global Competitiveness

Low Feedstocks

Low Energy Costs

*Source: Waterborne Energy, Inc. Data in $US/MM Btu Includes information and data supplied by IHS Global Inc. *Source: IHS, Platts, McKinsey Analysis

9

0

50

100

150

200

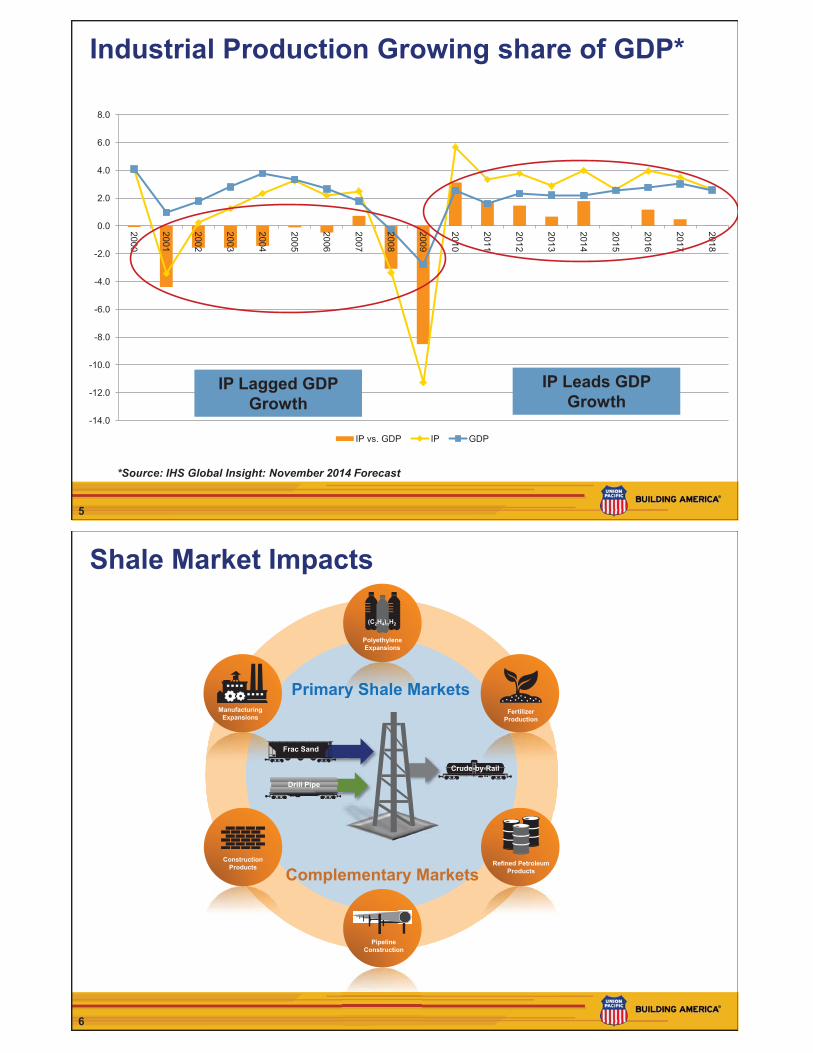

Fertilizer Demand

* Publicly announced

• Phosphates / Nitrogen • Strong Domestic Access • Low Natural Gas Prices • Displacement of Imports

Nitrogen Phosphates Potash

Global Fertilizer Demand* (Million Tons)

*Source: IFA, June 2014

Rock Springs, WY Port Neal, IA

Enid, OK

Freeport, TX Donaldsonville, LA Waggeman, LA

El Dorado, AR

North American Nitrogen Expansions*

Wever, IA

Borger, TX

Spiritwood, ND

E Dubuque, IL Lima, OH

Greene County, TN

10

Point Comfort, TX

Joffre, AB

Sarnia, ON

Coatzacoalcos, VL

Plaquemine, LA

Monaca, PA

Expansions under construction *Publicly announced expansions

Parkersburg, WV

Plaquemine, LA

Odessa, TX

Point Comfort

VL Corpus Christi, TX

Decatur, AL

Montreal, PQ

Badlands NGL LLC North Dakota

La Porte, TX

La Porte, TX

Odessa, TX

La Porte, TX

La Porte, TX

Baytown, TX

Freeport, TX

Sweeny, TX

North American Expansions* Plastic Resin

Lake Charles, LA

Lake Charles, LA

11

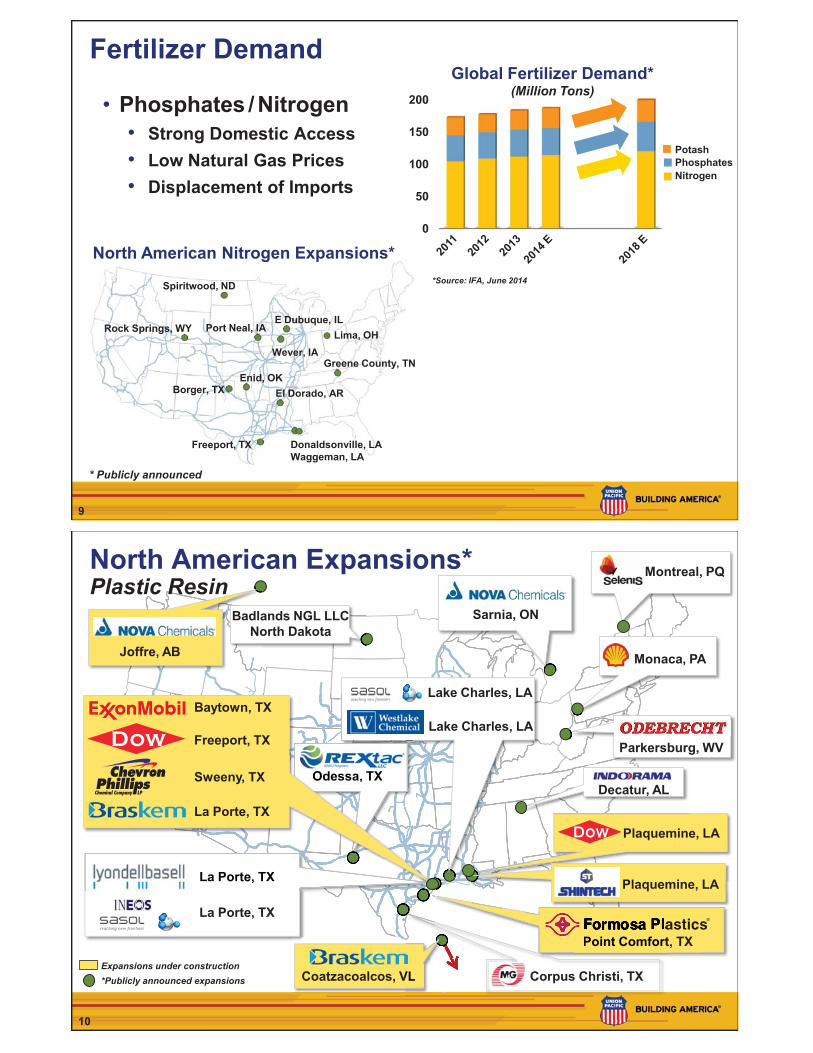

Portland

Oakland

LA

Calexico

Seattle

SLC

Eastport

Brownsville

Twin Cities

Denver

Dallas

Nogales El Paso

Eagle Pass

KC

St. Louis

Duluth

Memphis

Chicago

Laredo

Houston

North American Expansions Steel

New Orleans

12

Foreign Direct Investment in Mexico Important FDI Announcements

*Source: Company public announcements

13

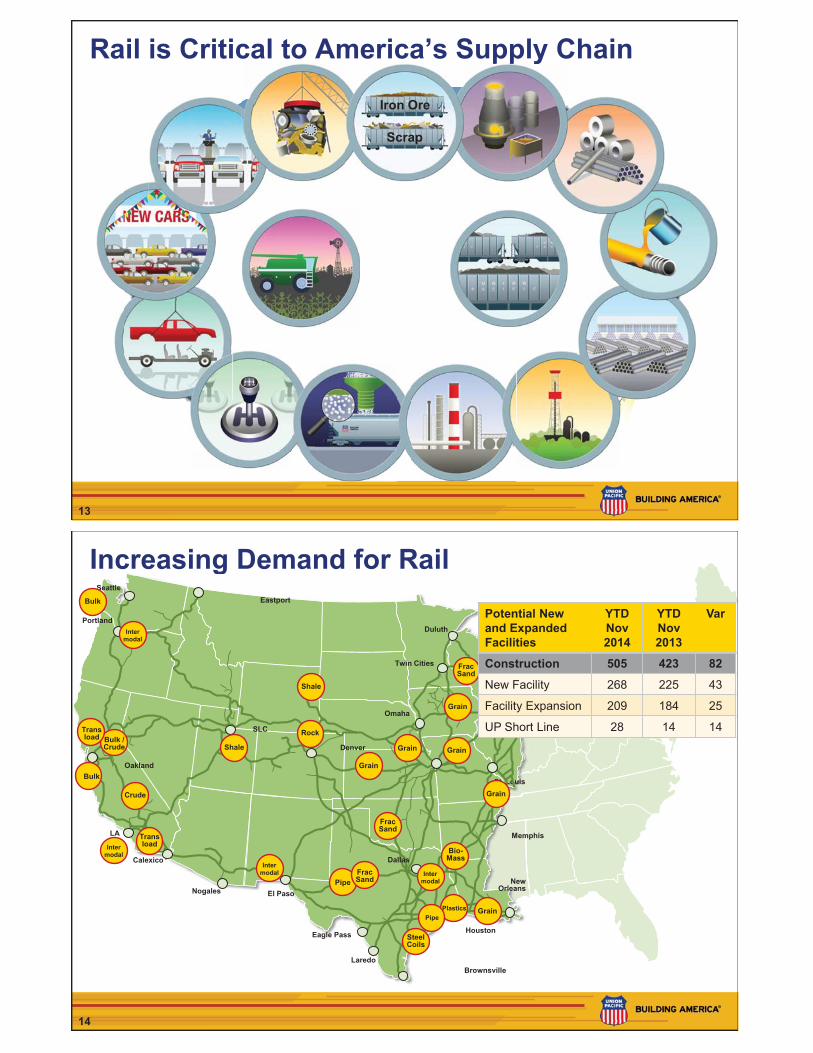

Rail is Critical to America’s Supply Chain

FACILITY

pppppppppppppppppp y

LLLLLLLLLLLLLLLLLLLLLLIIIIIITTTTTTTTTYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAACCCCCCCCCCCCCCCCCCCCCCCCCCCCCCCCCCCCCCCCCCCCCCCCCCCCCCCCCCCCCCCCCCCCCCCCCCCCCCCCCCCCCCCCCCCCCCCCCCCCCCCCCCCCCCCCCCCCCCCIIIIIIIIIIIIIIILLLLLLLLLLLLLLLLLLLLLLLLLLLLLLLLLLLLLLLLLLLLLLLLLLLLLLLLLLLLLLLLLLLLLLLLLLLLLLLLLLLLLLLLLLLLLLLLLLIron Ore

Scrap

14

Increasing Demand for Rail g

St. Louis

Portland

Oakland

LA

Calexico

Nogales El Paso

Seattle

Eagle Pass

SLC

Eastport

Brownsville

Houston

KC

Omaha

Twin Cities

Duluth

Denver

Laredo

Dallas

Memphis

Chicago

New Orleans

Plastics

Bio-Mass

Pipe

Steel Coils

Frac Sand

Frac Sand

Rock

Shale

Shale

Bulk

Crude

Trans load

Bulk / Crude

Bulk

Trans load

Frac Sand

Grain

Grain

Grain

Grain

Grain

Frac Sand

Inter modal

Inter modal

Inter modal

Inter modal

Pipe

Grain

Potential New and Expanded Facilities

YTD Nov 2014

YTD Nov 2013

Var

Construction 505 423 82

New Facility 268 225 43

Facility Expansion 209 184 25

UP Short Line 28 14 14

15

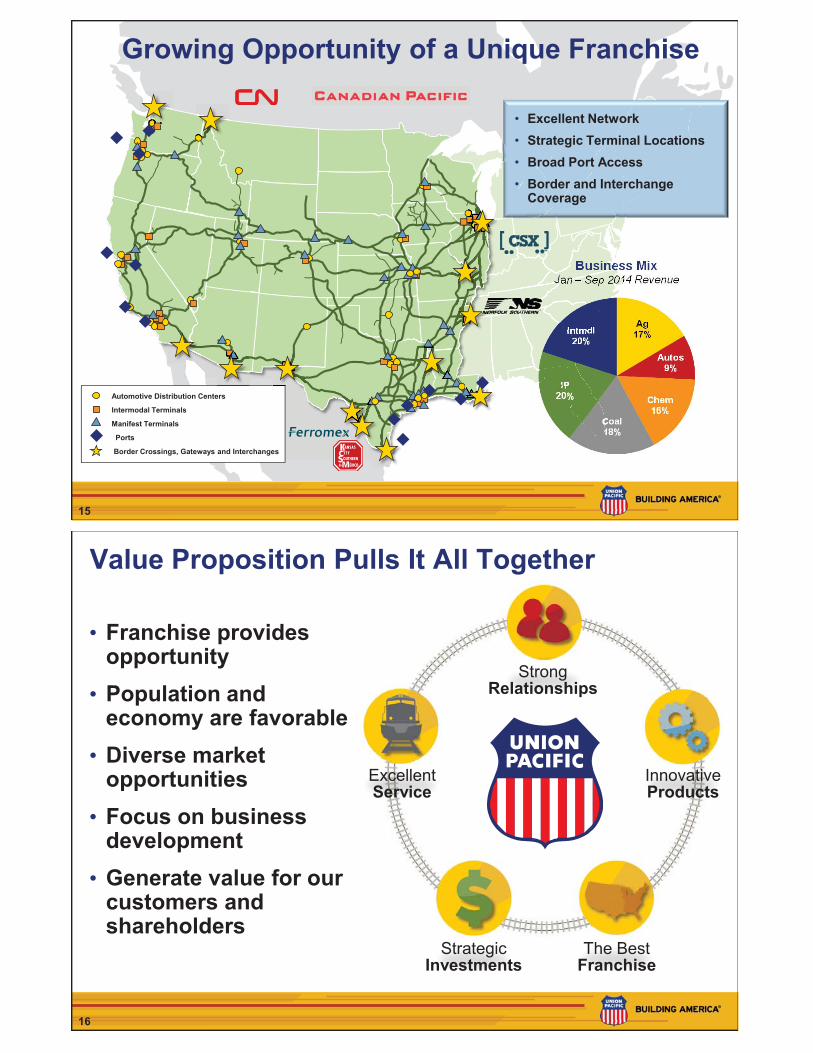

• Excellent Network • Strategic Terminal Locations • Broad Port Access • Border and Interchange

Coverage

Growing Opportunity of a Unique Franchise

Automotive Distribution Centers

Intermodal Terminals

Manifest Terminals

Border Crossings, Gateways and Interchanges

Ports

16

Value Proposition Pulls It All Together

• Franchise provides opportunity • Population and

economy are favorable • Diverse market

opportunities • Focus on business

development • Generate value for our

customers and shareholders

Strategic

Investments The Best

Franchise

Strong Relationships

Innovative Products

Excellent Service

17

RailTrends November 21, 2014

Brad Thrasher, VP & General Manager Industrial Products