2012 ICF Global Coaching Study - Results...

34

2012 ICF Global Coaching Study www.pwc.com The Business of Coaching: Fee and Revenue Drivers ICF Global Conference 2012 4 October2012

Transcript of 2012 ICF Global Coaching Study - Results...

2012 ICF Global Coaching Study

www.pwc.com

The Business of Coaching: Fee and Revenue DriversICF Global Conference 2012

4 October2012

How the ICF plays an important role in the area of coaching research….

• ICF members and global chapter network creates the unique capacity to complete these studies

• Collaborative alliances with other coaching organizations ensure

PwC2012

Slide 22012 ICF Global Coaching Study - Key headlines

• Collaborative alliances with other coaching organizations ensure that results are representative of the global profession

• Serves as a resource for providing valuable data to a variety of stakeholders

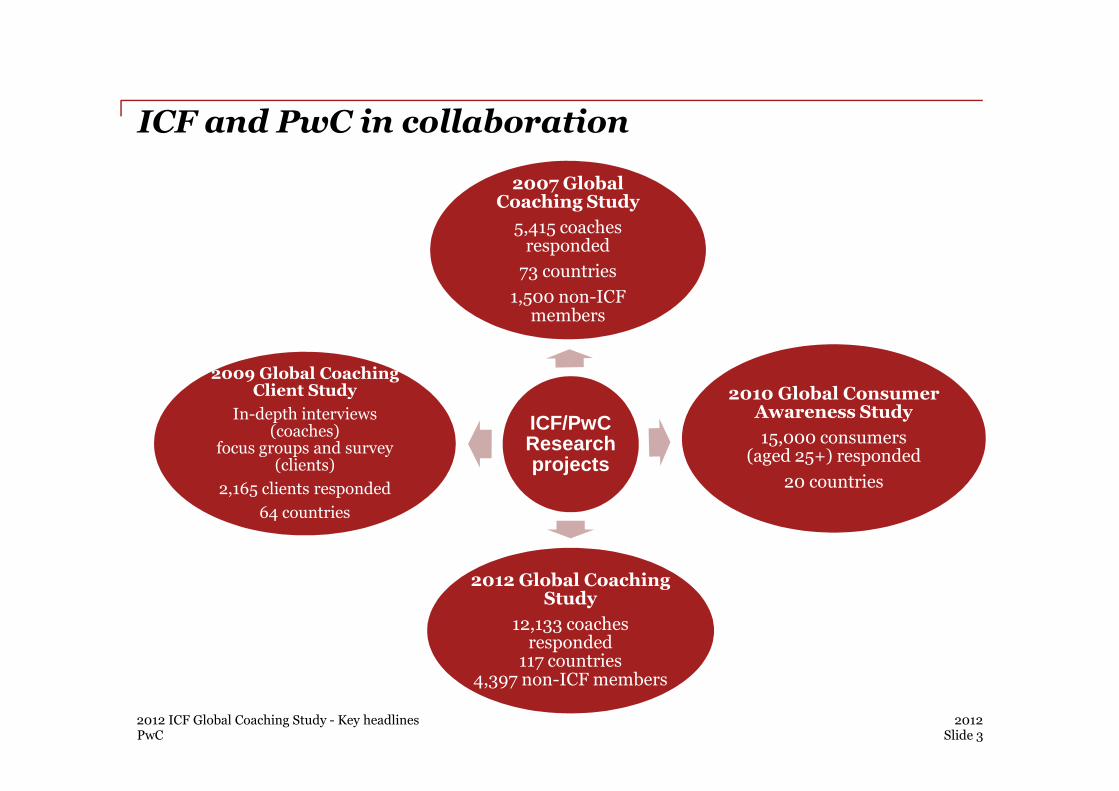

ICF and PwC in collaboration

2007 Global Coaching Study

5,415 coaches responded

73 countries

1,500 non-ICF members

2010 Global Consumer 2009 Global Coaching

Client Study

PwC2012

Slide 32012 ICF Global Coaching Study - Key headlines

ICF/PwC Research projects

2010 Global Consumer Awareness Study

15,000 consumers(aged 25+) responded

20 countries

2012 Global Coaching Study

12,133 coaches responded

117 countries4,397 non-ICF members

Client Study

In-depth interviews (coaches)

focus groups and survey (clients)

2,165 clients responded

64 countries

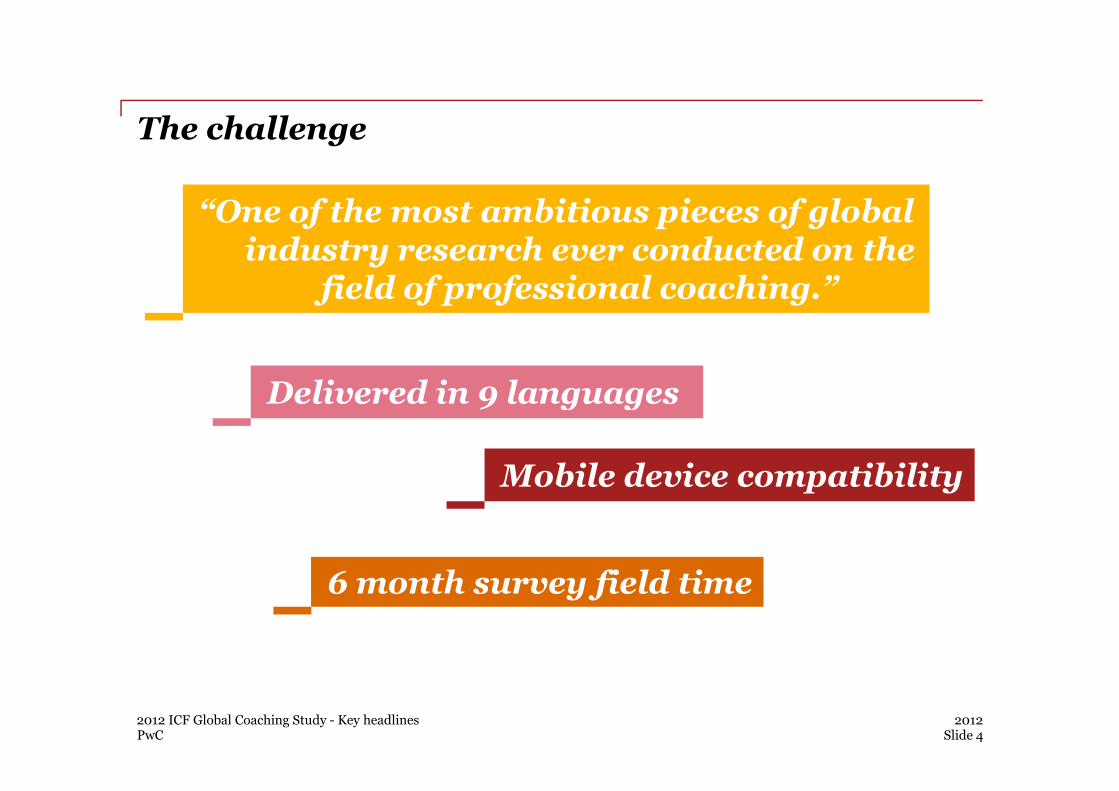

The challenge

Delivered in 9 languages

“One of the most ambitious pieces of global industry research ever conducted on the

field of professional coaching.”

PwC2012

Slide 42012 ICF Global Coaching Study - Key headlines

Delivered in 9 languages

Mobile device compatibility

6 month survey field time

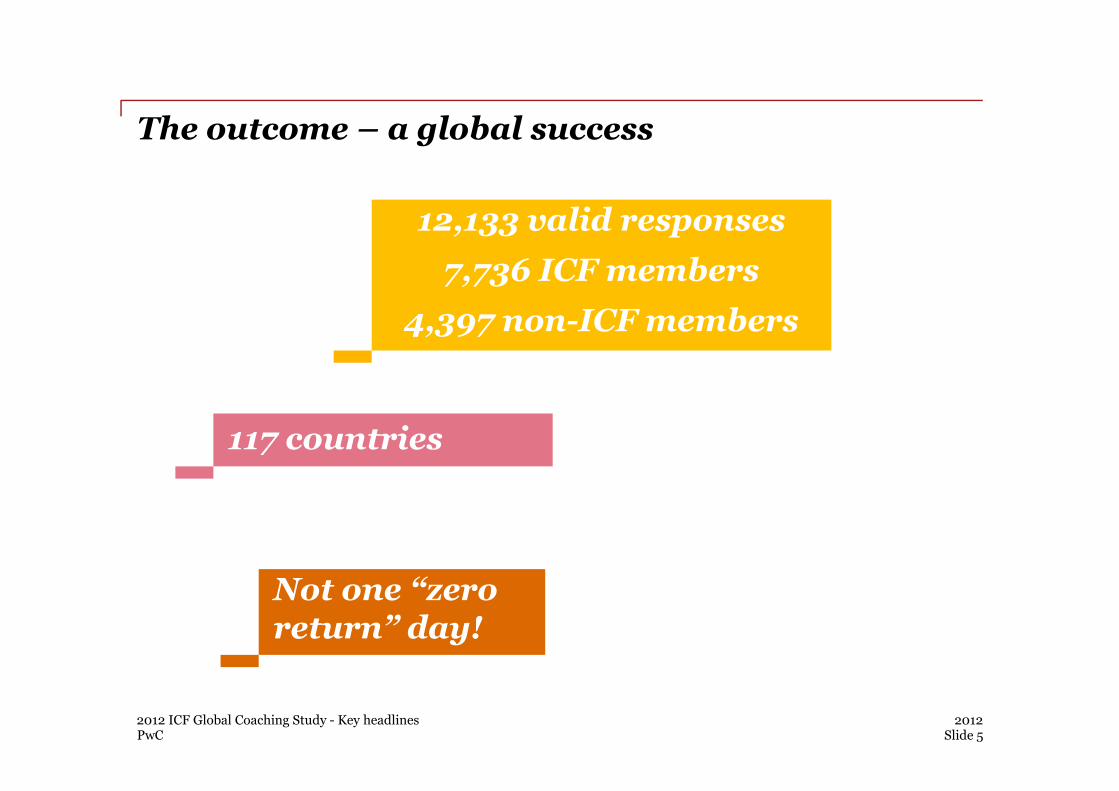

The outcome – a global success

12,133 valid responses

7,736 ICF members

4,397 non-ICF members

PwC2012

Slide 52012 ICF Global Coaching Study - Key headlines

Not one “zero return” day!

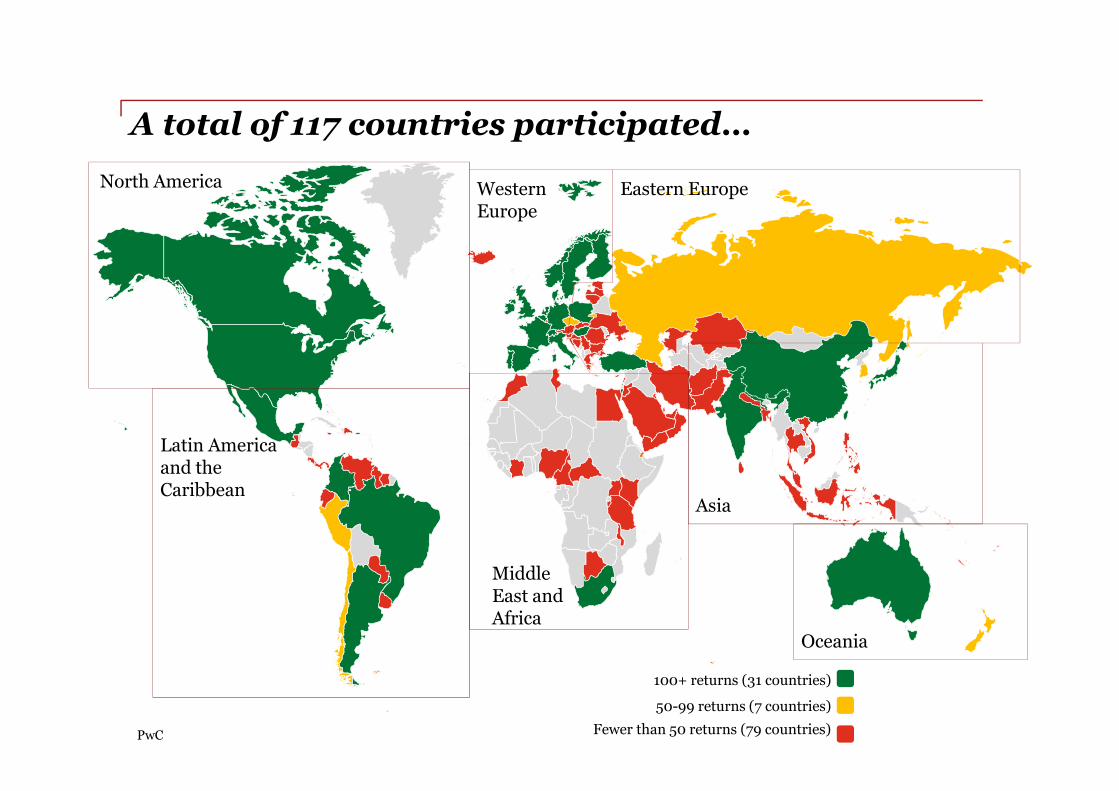

117 countries

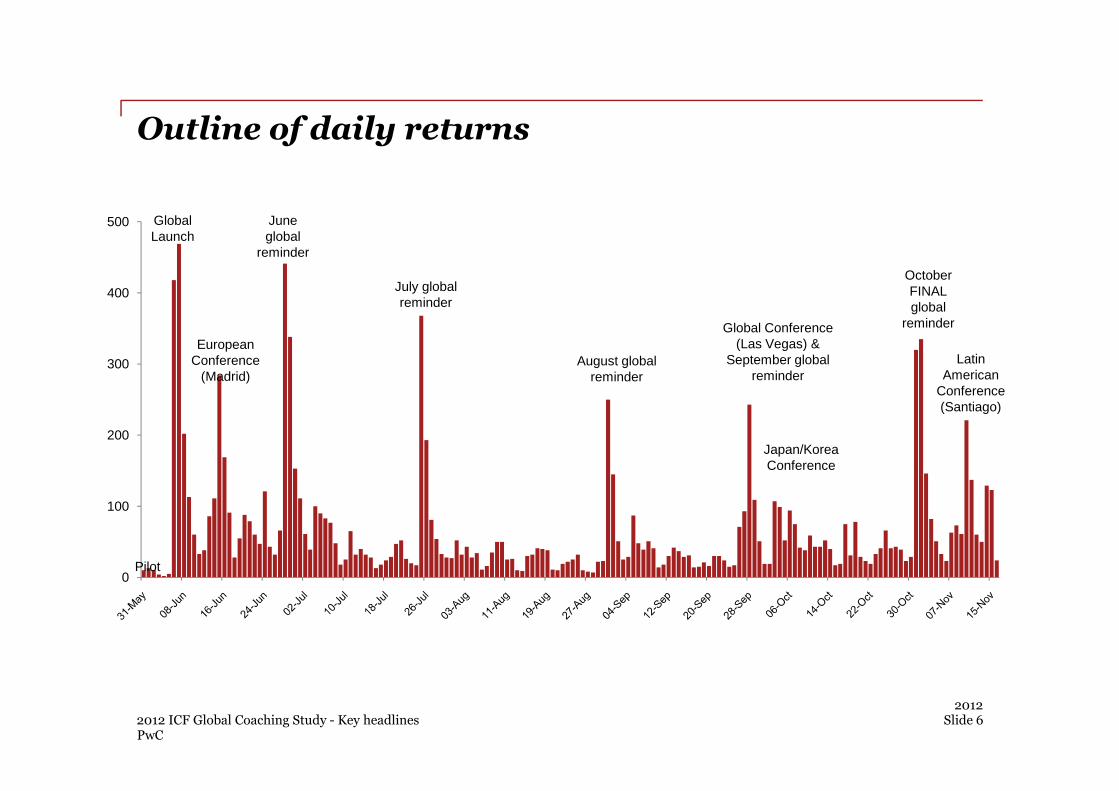

Outline of daily returns

300

400

500 GlobalLaunch

European Conference

(Madrid)

June global

reminder

July global reminder

August global reminder

Global Conference (Las Vegas) &

September global reminder

October FINAL global

reminder

Latin American

Conference

PwC

2012Slide 6

0

100

200

Pilot

2012 ICF Global Coaching Study - Key headlines

Conference (Santiago)

Japan/Korea Conference

North America Eastern EuropeWestern Europe

A total of 117 countries participated…

PwC

100+ returns (31 countries)

50-99 returns (7 countries)

Fewer than 50 returns (79 countries)

Oceania

Latin America and the Caribbean

Middle East and Africa

Asia

Main findings

The Size of the Profession

PwC20122012 ICF Global Coaching Study - Key headlines

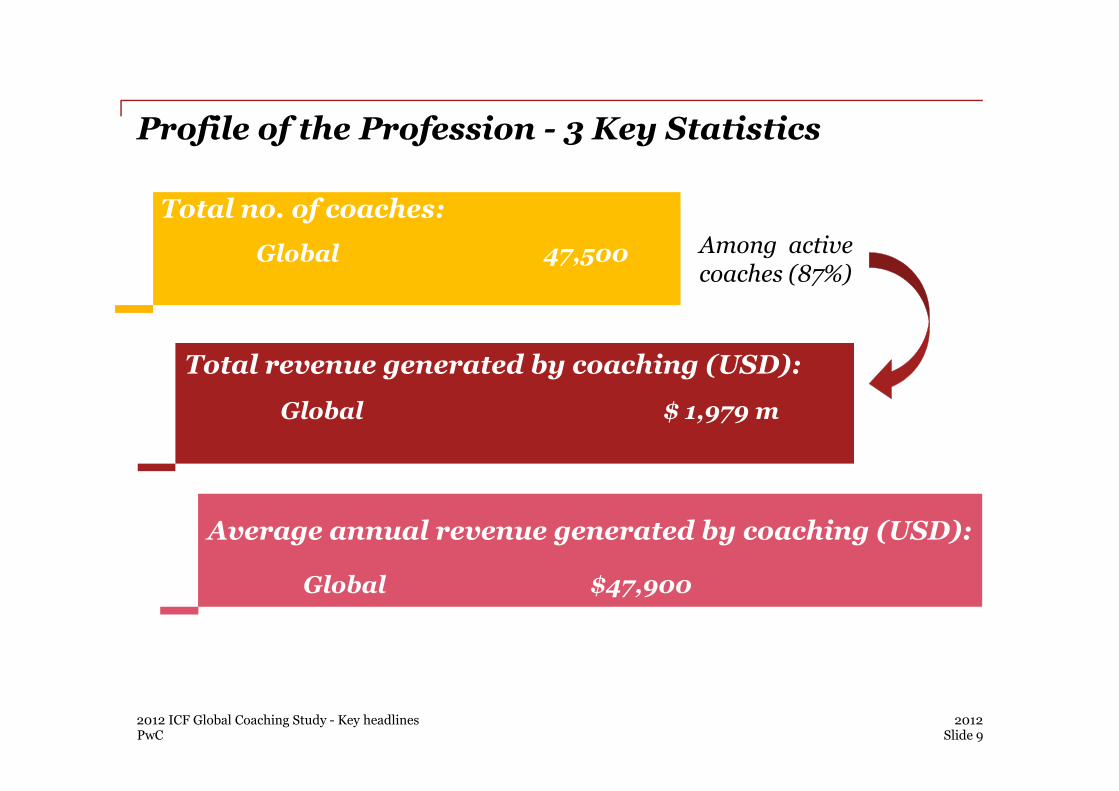

Profile of the Profession - 3 Key Statistics

Total no. of coaches:

Global 47,500

Total revenue generated by coaching (USD):

Among active coaches (87%)

PwC2012

Slide 92012 ICF Global Coaching Study - Key headlines

Global $ 1,979 m

Average annual revenue generated by coaching (USD):

Global $47,900

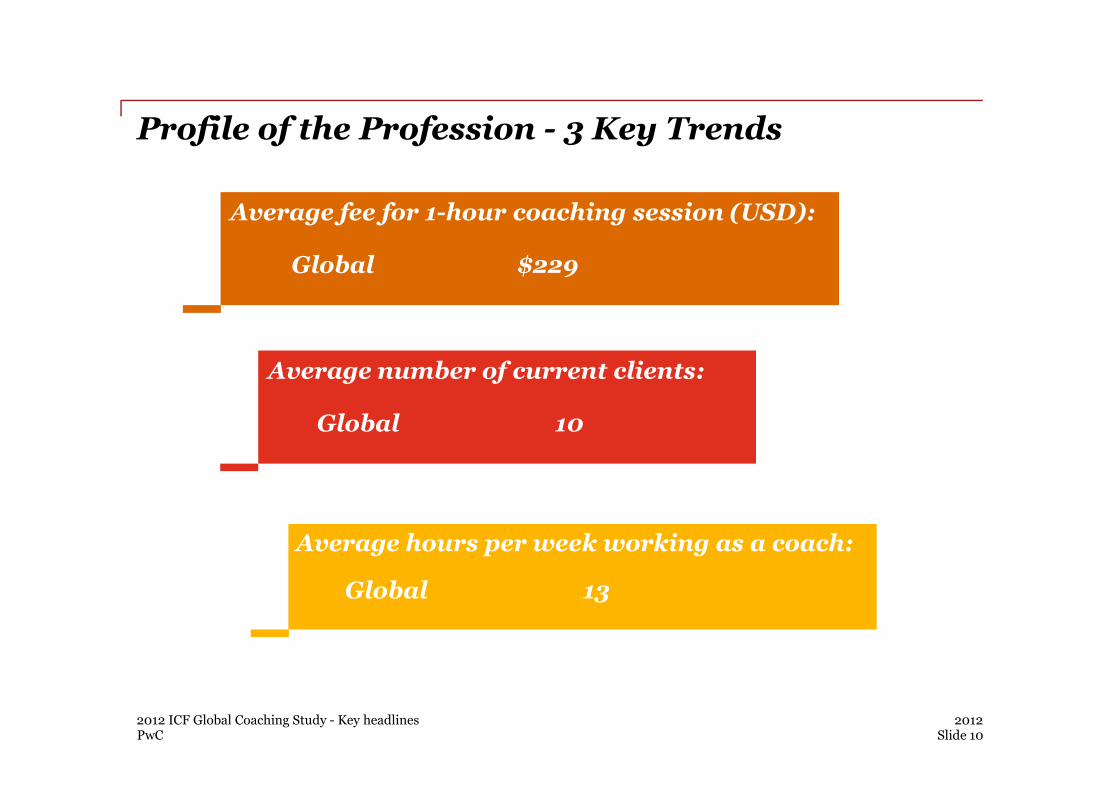

Average fee for 1-hour coaching session (USD):

Global $229

Profile of the Profession - 3 Key Trends

Average number of current clients:

PwC2012

Slide 102012 ICF Global Coaching Study - Key headlines

Global 10

Average hours per week working as a coach:

Global 13

Main findings

About You - The Coach

PwC20122012 ICF Global Coaching Study - Key headlines

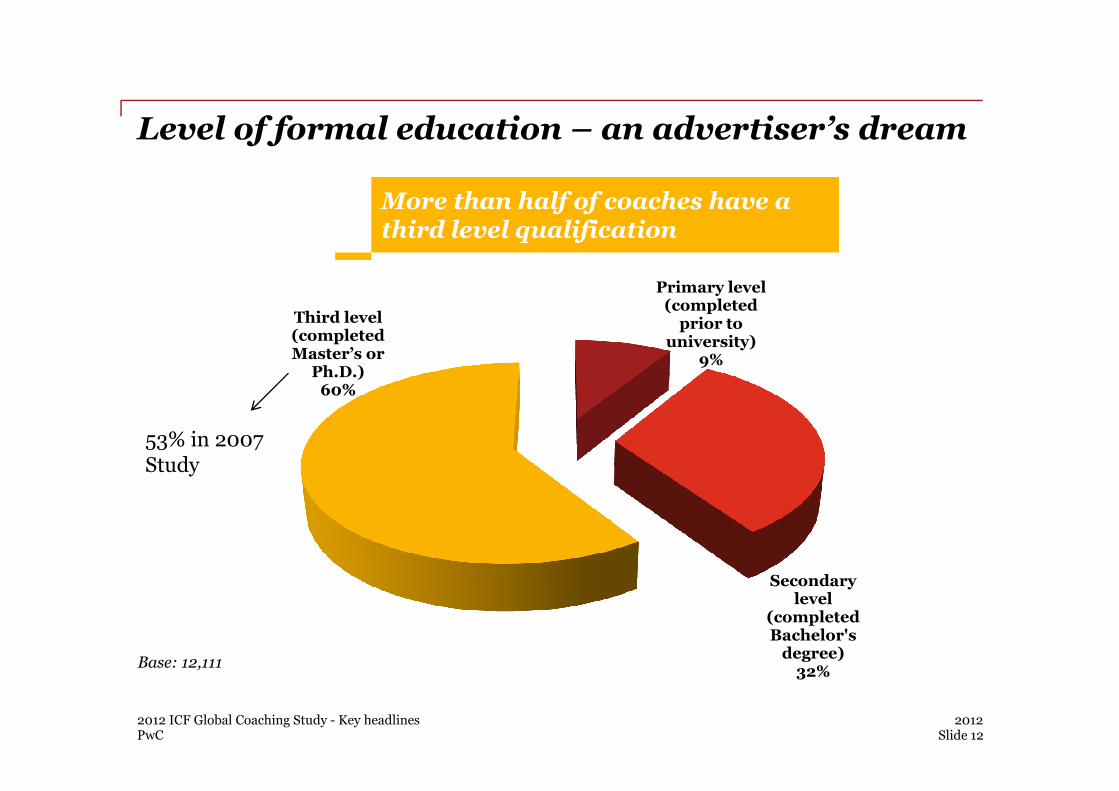

Level of formal education – an advertiser’s dream

Primary level (completed

prior to university)

9%

Third level (completed Master’s or

Ph.D.)60%

More than half of coaches have a third level qualification

PwC

Secondary level

(completed Bachelor's degree)

32%

60%

Base: 12,111

2012Slide 12

2012 ICF Global Coaching Study - Key headlines

53% in 2007 Study

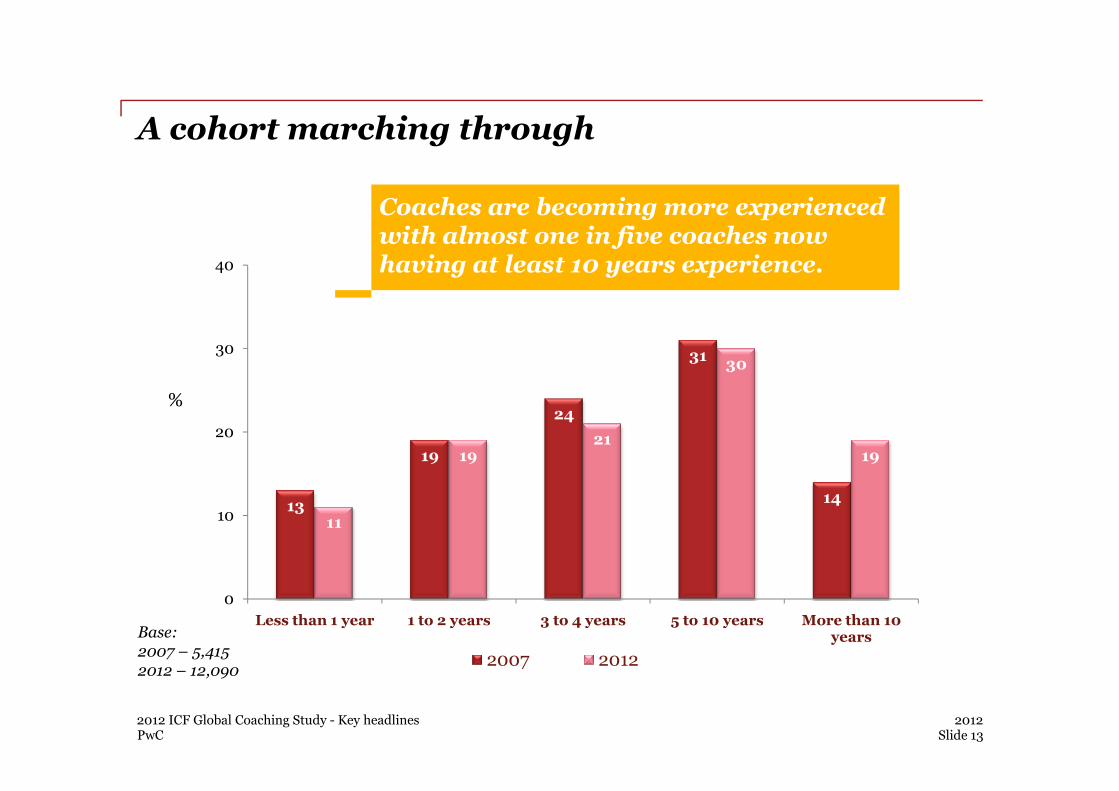

A cohort marching through

3130

30

40

%

Coaches are becoming more experienced with almost one in five coaches now having at least 10 years experience.

PwC

13

19

24

14

11

1921

19

0

10

20

Less than 1 year 1 to 2 years 3 to 4 years 5 to 10 years More than 10 years

2007 2012

%

Base:2007 – 5,4152012 – 12,090

2012Slide 13

2012 ICF Global Coaching Study - Key headlines

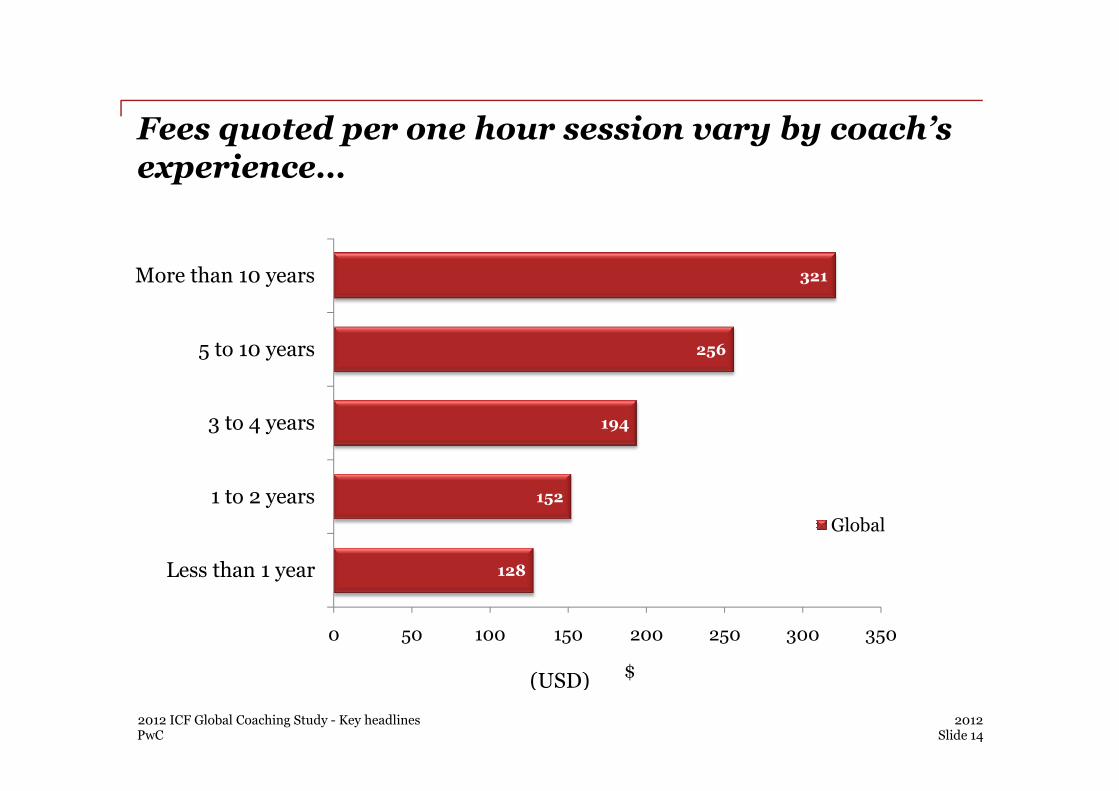

Fees quoted per one hour session vary by coach’s experience…

256

321

5 to 10 years

More than 10 years

PwC2012

Slide 14

$

2012 ICF Global Coaching Study - Key headlines

128

152

194

0 50 100 150 200 250 300 350

Less than 1 year

1 to 2 years

3 to 4 years

Global

(USD)

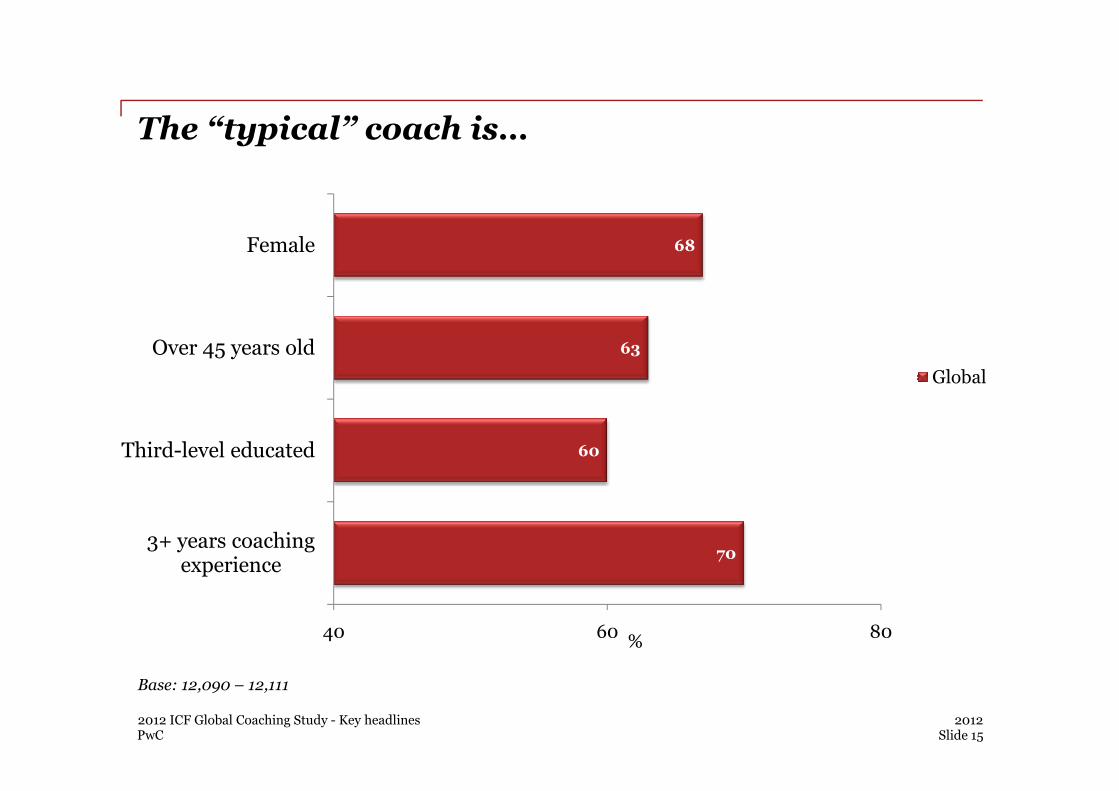

The “typical” coach is…

63

68

Over 45 years old

Female

Global

PwC

Base: 12,090 – 12,111

2012Slide 15

%

2012 ICF Global Coaching Study - Key headlines

70

60

40 60 80

3+ years coaching experience

Third-level educated

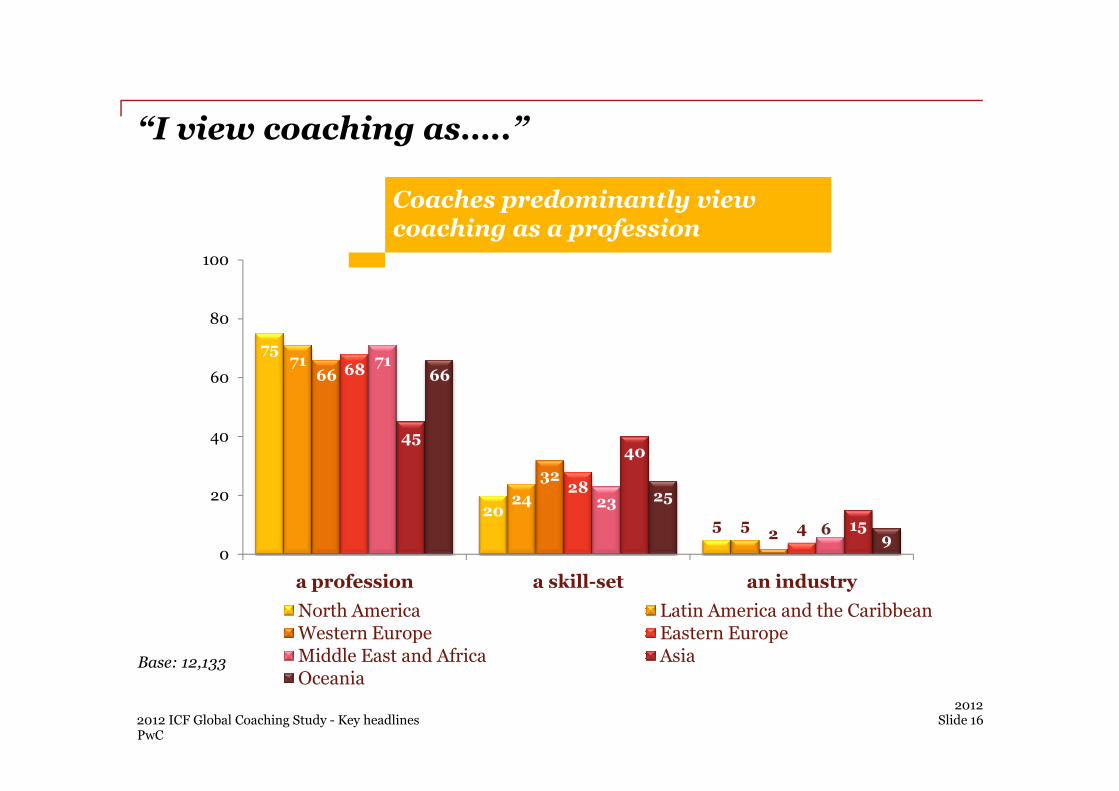

“I view coaching as…..”

Coaches predominantly view coaching as a profession

7571

66 6871

6660

80

100

PwC

Base: 12,133

2012Slide 162012 ICF Global Coaching Study - Key headlines

205

24

5

32

2

28

4

23

6

4540

15

25

90

20

40

a profession a skill-set an industry

North America Latin America and the CaribbeanWestern Europe Eastern EuropeMiddle East and Africa AsiaOceania

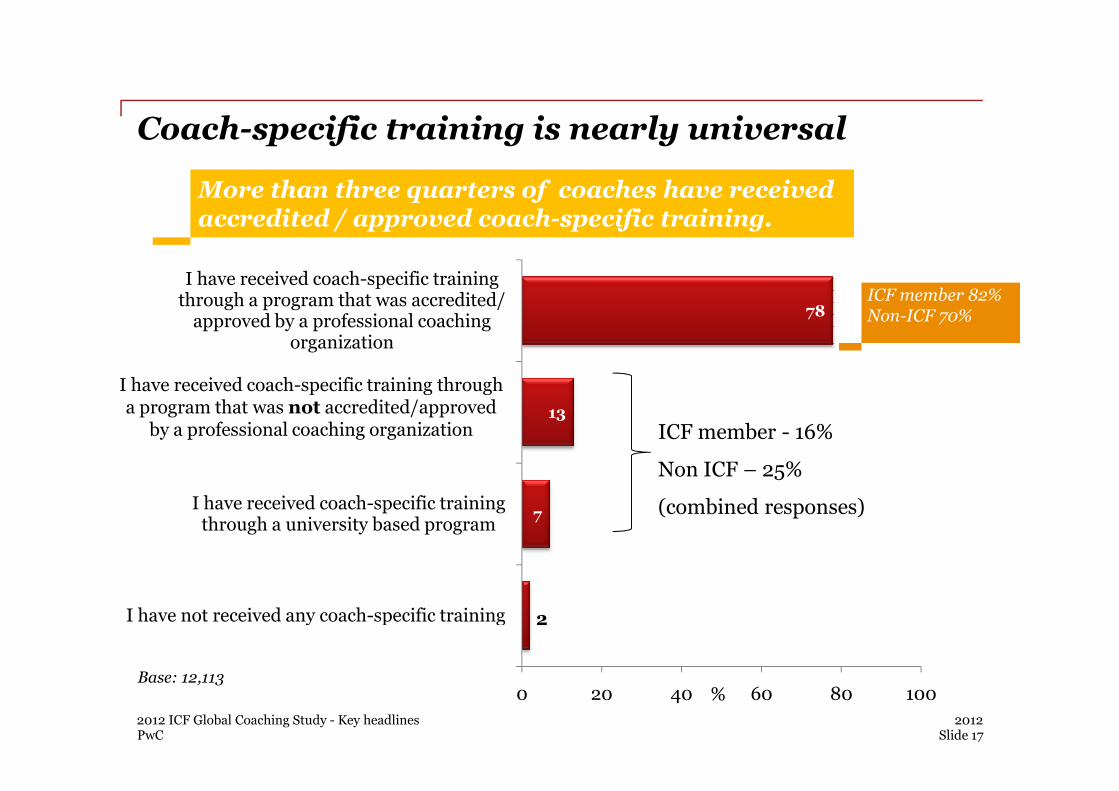

Coach-specific training is nearly universal

78

I have received coach-specific training through a program that was not

I have received coach-specific training through a program that was accredited/ approved by a professional coaching

organization

More than three quarters of coaches have received accredited / approved coach-specific training.

I have received coach-specific training through

ICF member 82%Non-ICF 70%

PwC

2

7

13

0 20 40 60 80 100

I have not received any coach-specific training

I have received coach-specific training through a university based program

through a program that was not accredited/approved by a professional

coaching organization

Base: 12,113%

2012Slide 17

2012 ICF Global Coaching Study - Key headlines

ICF member - 16%

Non ICF – 25%

(combined responses)

a program that was not accredited/approved by a professional coaching organization

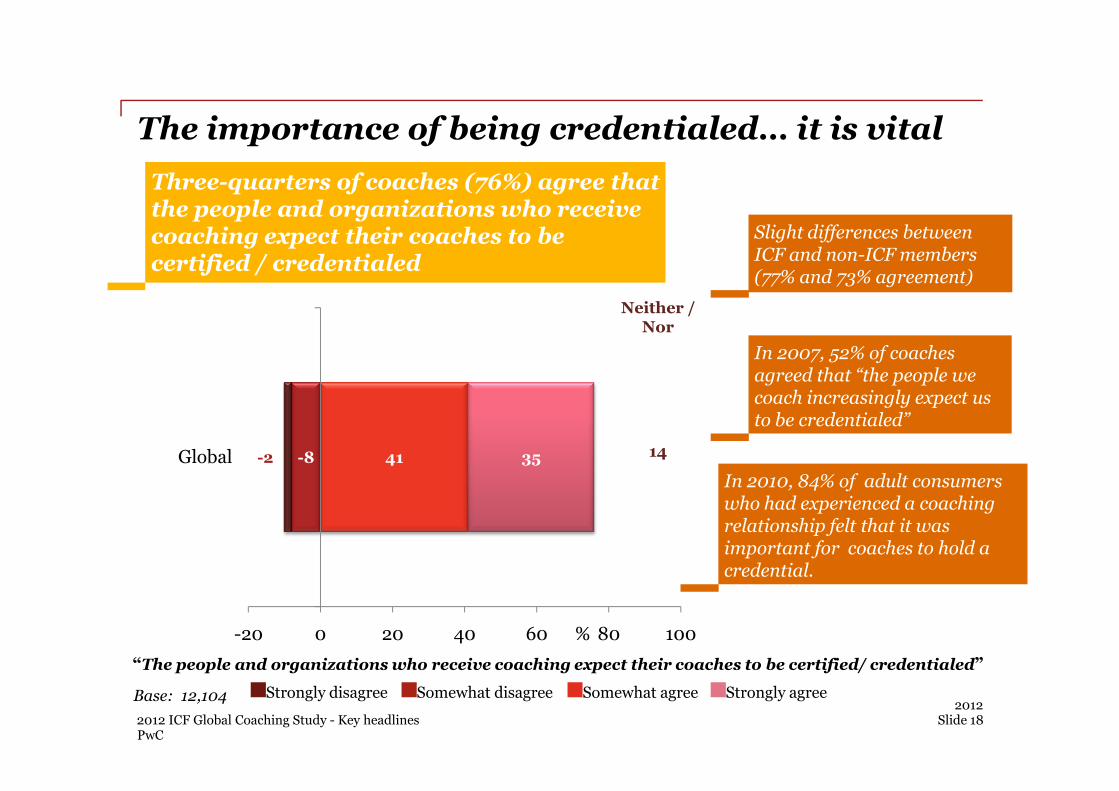

The importance of being credentialed… it is vital

In 2007, 52% of coaches agreed that “the people we coach increasingly expect us

Neither / Nor

Three-quarters of coaches (76%) agree that the people and organizations who receive coaching expect their coaches to be certified / credentialed

Slight differences between ICF and non-ICF members (77% and 73% agreement)

PwC

Base: 12,104

-8-2 41 35

-20 0 20 40 60 80 100

Global

coach increasingly expect us to be credentialed”

“The people and organizations who receive coaching expect their coaches to be certified/ credentialed”

Strongly disagree Somewhat disagree Somewhat agree Strongly agree

In 2010, 84% of adult consumers who had experienced a coaching relationship felt that it was important for coaches to hold a credential.

%

2012Slide 182012 ICF Global Coaching Study - Key headlines

14

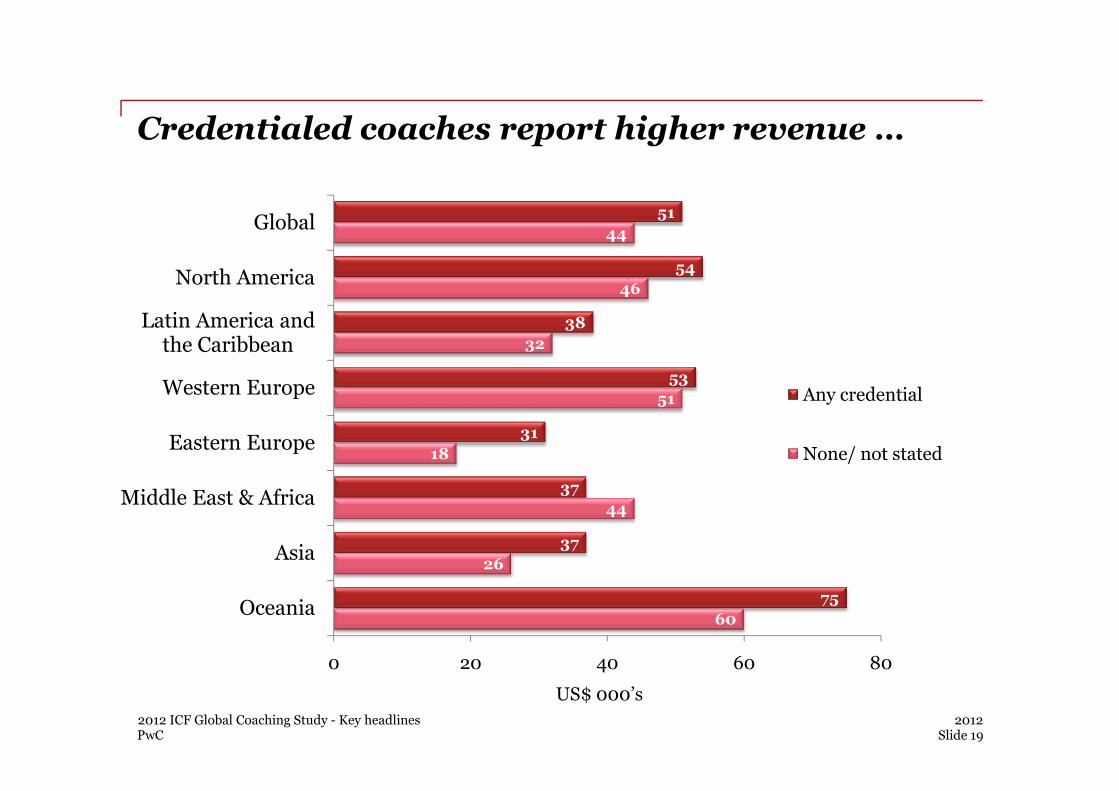

Credentialed coaches report higher revenue …

51

32

46

44

53

38

54

51

Western Europe

Latin America and the Caribbean

North America

Global

Any credential

PwC2012

Slide 19

US$ 000’s

2012 ICF Global Coaching Study - Key headlines

60

26

44

18

51

75

37

37

31

0 20 40 60 80

Oceania

Asia

Middle East & Africa

Eastern Europe

Western Europe Any credential

None/ not stated

Main findings

Key Issues Facing the Profession -Past/Future Trends

PwC20122012 ICF Global Coaching Study - Key headlines

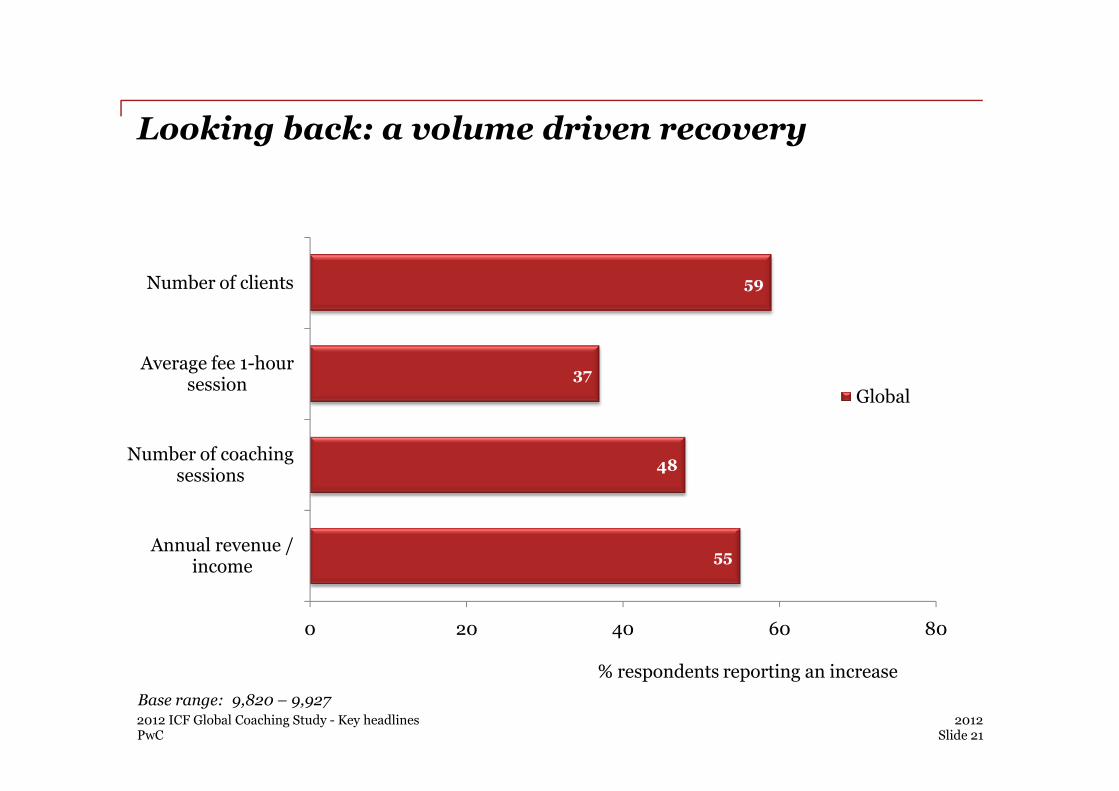

Looking back: a volume driven recovery

37

59

Average fee 1-hour session

Number of clients

Global

PwC

55

48

0 20 40 60 80

Annual revenue / income

Number of coaching sessions

Global

Base range: 9,820 – 9,927

% respondents reporting an increase

2012Slide 21

2012 ICF Global Coaching Study - Key headlines

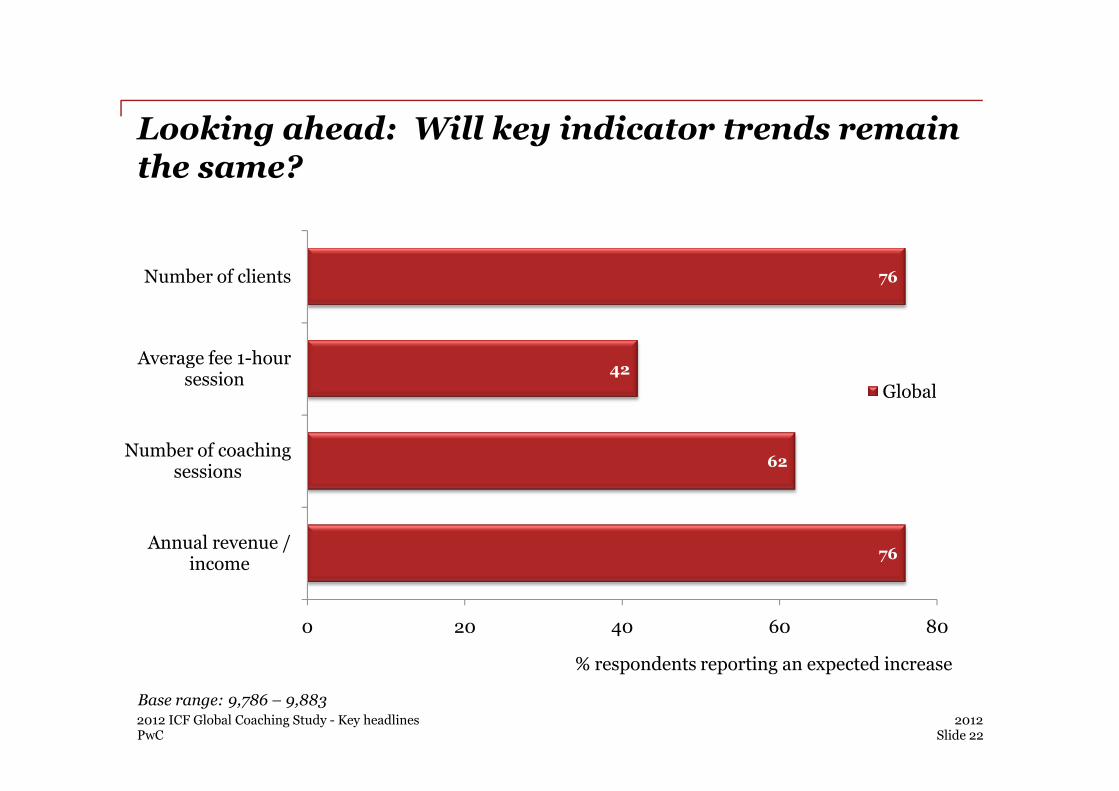

Looking ahead: Will key indicator trends remain the same?

42

76

Average fee 1-hour session

Number of clients

Global

PwC

76

62

0 20 40 60 80

Annual revenue / income

Number of coaching sessions

Global

% respondents reporting an expected increase

2012Slide 22

2012 ICF Global Coaching Study - Key headlines

Base range: 9,786 – 9,883

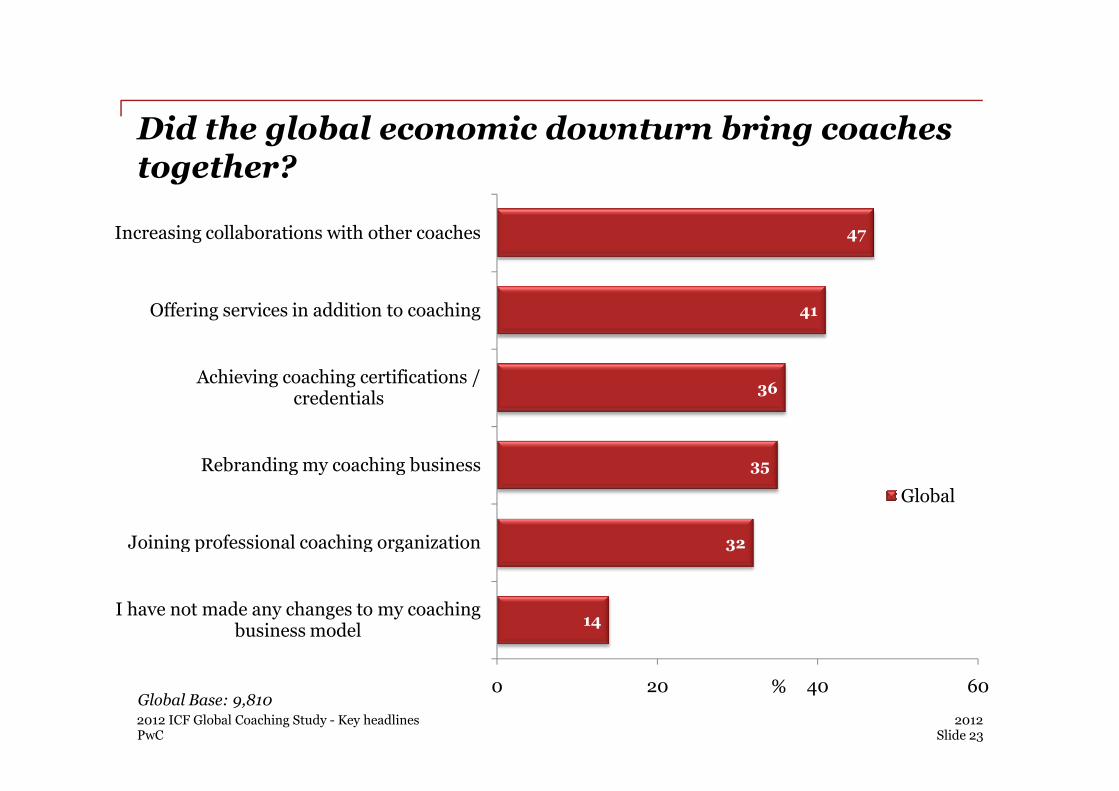

36

41

47

Achieving coaching certifications / credentials

Offering services in addition to coaching

Increasing collaborations with other coaches

Did the global economic downturn bring coaches together?

PwC

14

32

35

36

I have not made any changes to my coaching business model

Joining professional coaching organization

Rebranding my coaching business

credentials

0 20 40 60

Global

Global Base: 9,810%

2012Slide 23

2012 ICF Global Coaching Study - Key headlines

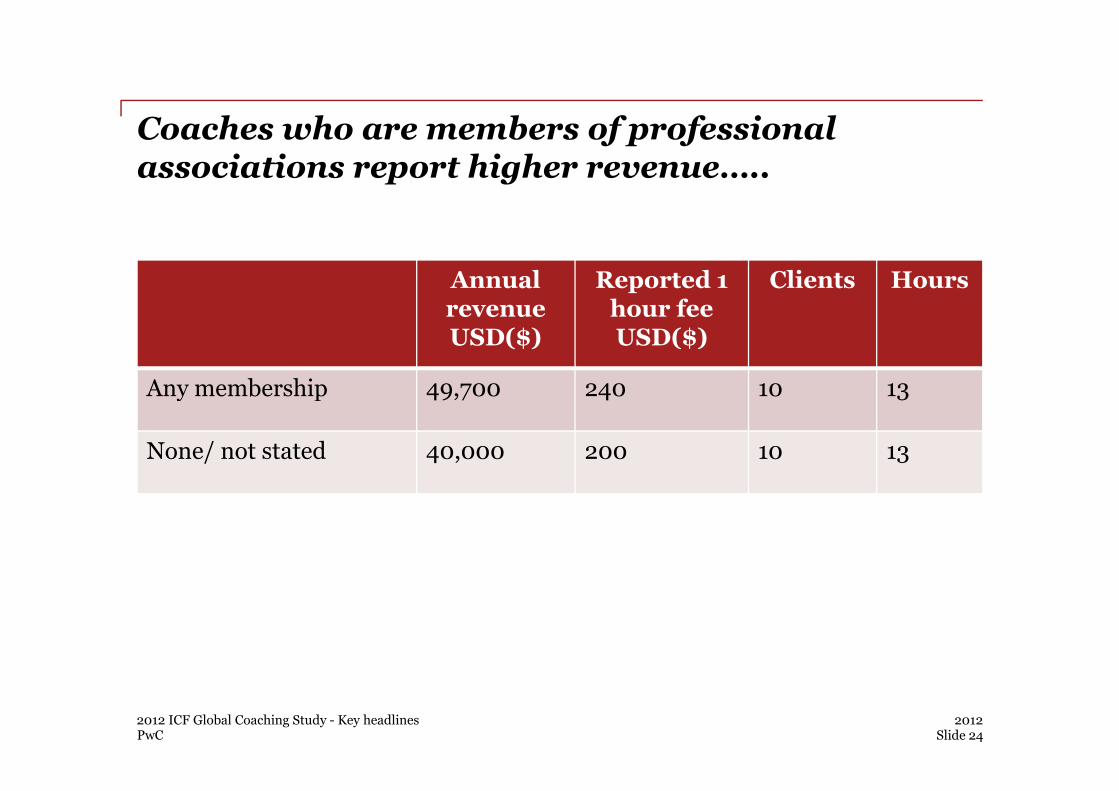

Coaches who are members of professional associations report higher revenue…..

Annual revenueUSD($)

Reported 1 hour fee USD($)

Clients Hours

Any membership 49,700 240 10 13

PwC2012

Slide 242012 ICF Global Coaching Study - Key headlines

Any membership 49,700 240 10 13

None/ not stated 40,000 200 10 13

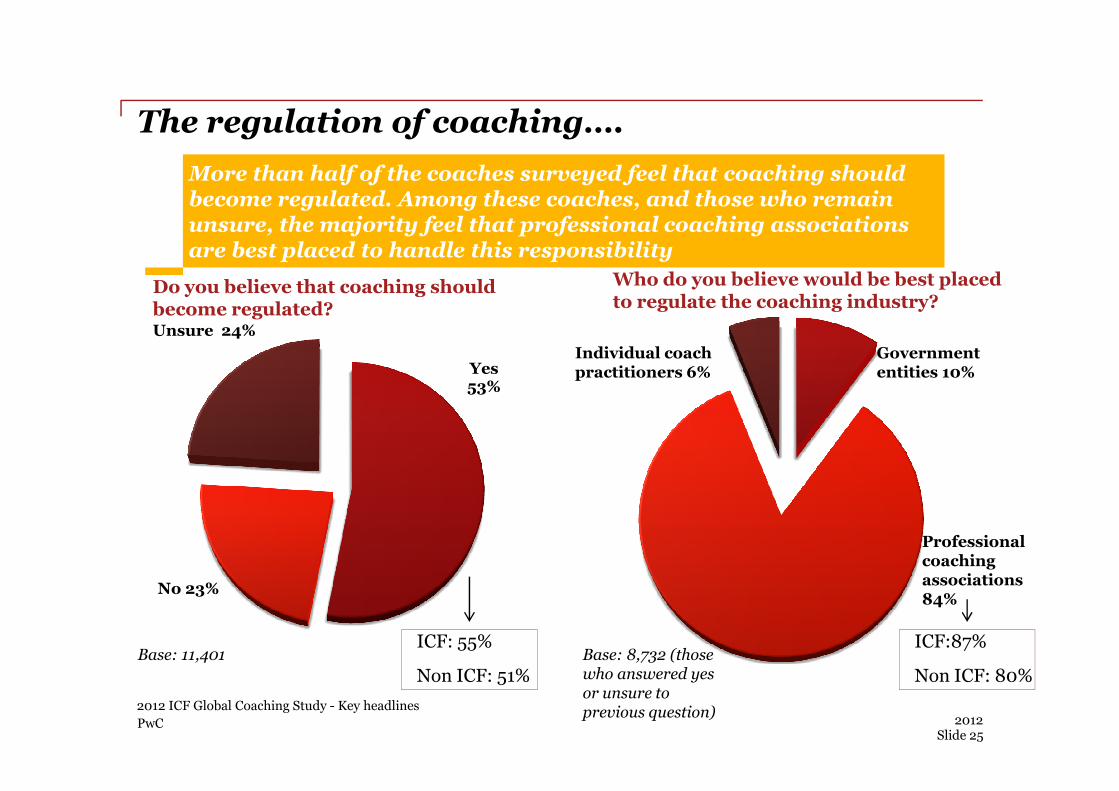

Do you believe that coaching should become regulated?

Who do you believe would be best placed to regulate the coaching industry?

The regulation of coaching….

Yes 53%

Government entities 10%

Individual coach practitioners 6%

Unsure 24%

More than half of the coaches surveyed feel that coaching should become regulated. Among these coaches, and those who remain unsure, the majority feel that professional coaching associations are best placed to handle this responsibility

PwC

Base: 11,401

No 23%

Base: 8,732 (those who answered yes or unsure to previous question)

Professional coaching associations 84%

2012Slide 25

2012 ICF Global Coaching Study - Key headlines

ICF: 55%

Non ICF: 51%

ICF:87%

Non ICF: 80%

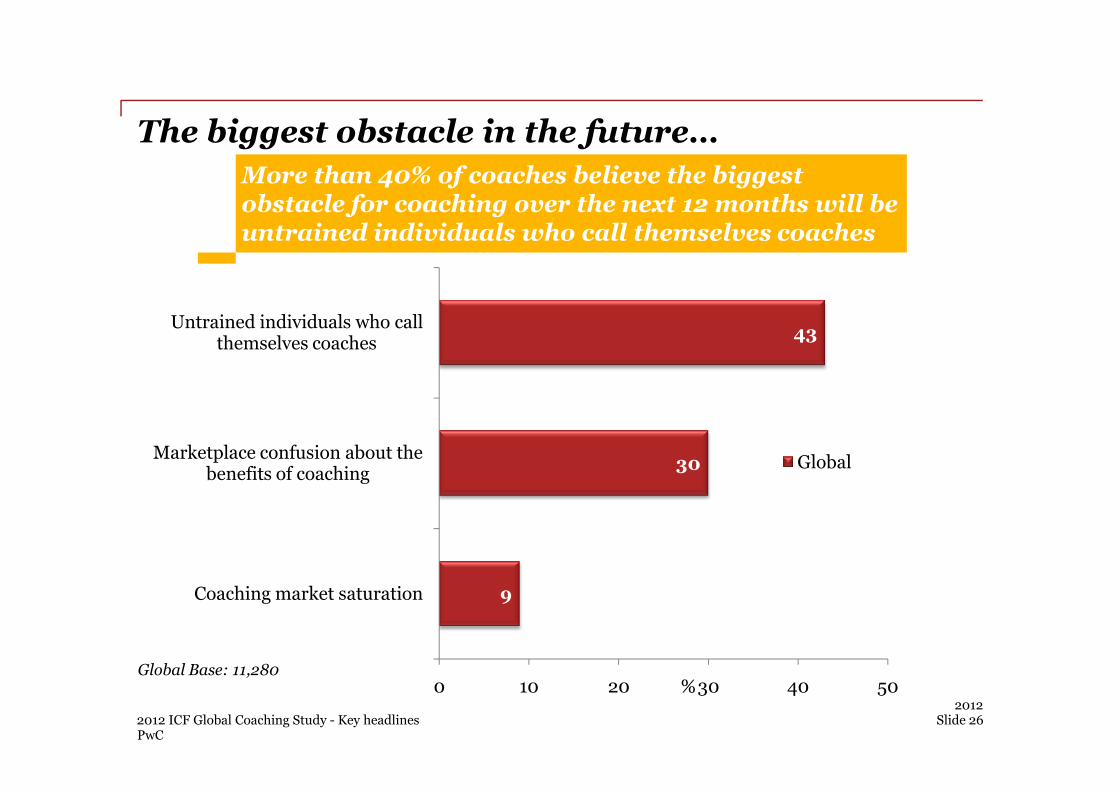

43Untrained individuals who call

themselves coaches

The biggest obstacle in the future…

More than 40% of coaches believe the biggest obstacle for coaching over the next 12 months will be untrained individuals who call themselves coaches

PwC

9

30

0 10 20 30 40 50

Coaching market saturation

Marketplace confusion about the benefits of coaching

Global

Global Base: 11,280%

2012Slide 262012 ICF Global Coaching Study - Key headlines

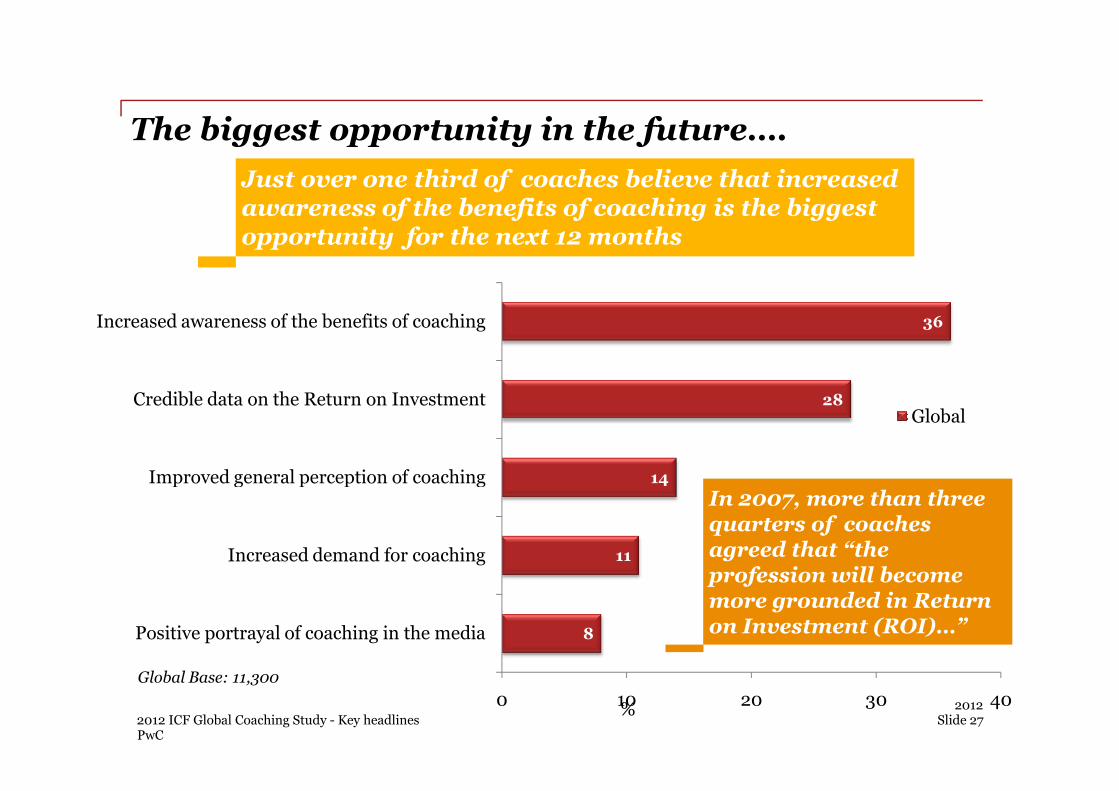

The biggest opportunity in the future….

28

36

Credible data on the Return on Investment

Increased awareness of the benefits of coaching

Just over one third of coaches believe that increased awareness of the benefits of coaching is the biggest opportunity for the next 12 months

PwC

Global Base: 11,300

8

11

14

28

0 10 20 30 40

Positive portrayal of coaching in the media

Increased demand for coaching

Improved general perception of coaching

Credible data on the Return on InvestmentGlobal

In 2007, more than three quarters of coaches agreed that “the profession will become more grounded in Return on Investment (ROI)…”

% 2012Slide 272012 ICF Global Coaching Study - Key headlines

Key drivers for coaching fees and revenue

• Experience/ years as a coach

• Credential

• Membership

• Position of the client

PwC20122012 ICF Global Coaching Study - Key headlines

Slide 28

• Position of the client

• Duration of the engagement

• Number of methods used to evaluate coaching

What’s next?

PwC20122012 ICF Global Coaching Study - Key headlines

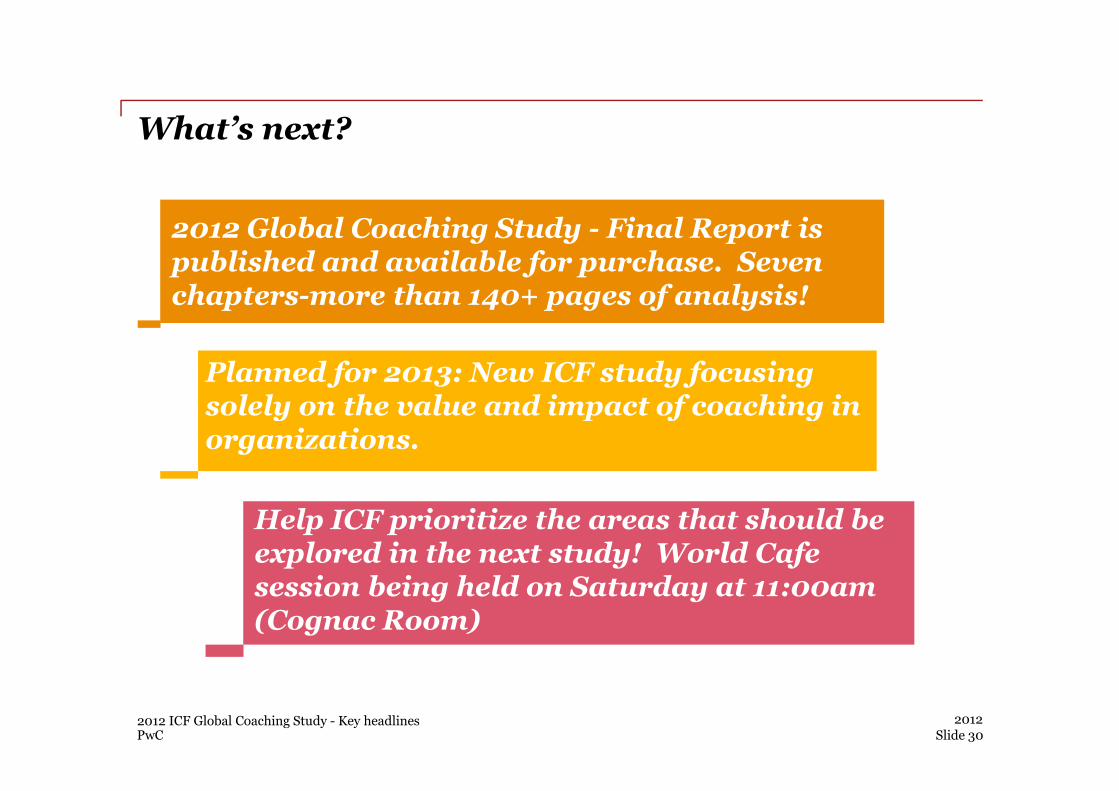

2012 Global Coaching Study - Final Report is published and available for purchase. Seven chapters-more than 140+ pages of analysis!

What’s next?

Planned for 2013: New ICF study focusing solely on the value and impact of coaching in

PwC20122012 ICF Global Coaching Study - Key headlines

Slide 30

solely on the value and impact of coaching in organizations.

Help ICF prioritize the areas that should be explored in the next study! World Cafe session being held on Saturday at 11:00am (Cognac Room)

Thank-you!

www.coachfederation.org/coachingstudy2012/

This publication has been prepared for general guidance on matters of interest only, and does not constitute professional advice. You should not act upon the information contained in this publication without obtaining specific professional advice. No representation or warranty (express or implied) is given as to the accuracy or completeness of the information contained in this publication, and, to the extent permitted by law, PricewaterhouseCoopers LLP, its members, employees and agents do not accept or assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance on the information contained in this publication or for any decision based on it.

© 2012 PricewaterhouseCoopers LLP. All rights reserved. In this document, “PwC” refers to PricewaterhouseCoopers LLP (a limited liability partnership in the United Kingdom) which is a member firm of PricewaterhouseCoopers International Limited, each member firm of which is a separate legal entity.

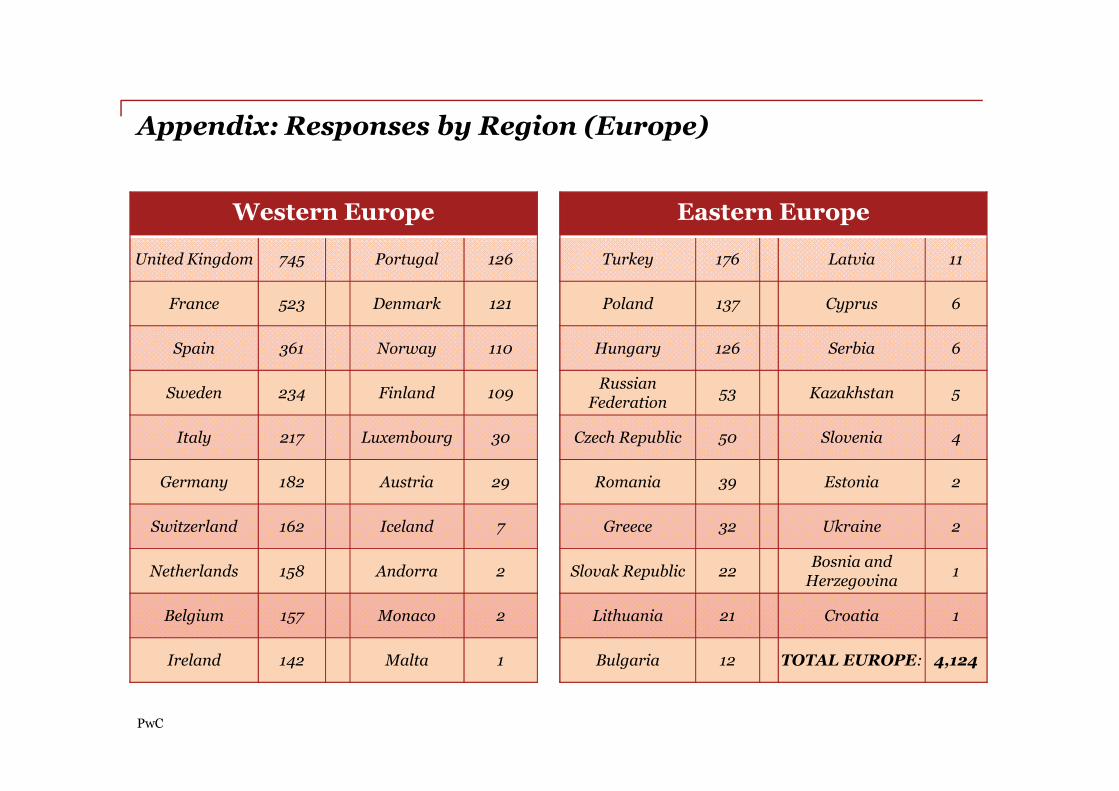

Appendix: Responses by Region (Europe)

Western Europe

United Kingdom 745 Portugal 126

France 523 Denmark 121

Spain 361 Norway 110

Sweden 234 Finland 109

Eastern Europe

Turkey 176 Latvia 11

Poland 137 Cyprus 6

Hungary 126 Serbia 6

Russian Federation

53 Kazakhstan 5

PwC

Sweden 234 Finland 109

Italy 217 Luxembourg 30

Germany 182 Austria 29

Switzerland 162 Iceland 7

Netherlands 158 Andorra 2

Belgium 157 Monaco 2

Ireland 142 Malta 1

Federation53 Kazakhstan 5

Czech Republic 50 Slovenia 4

Romania 39 Estonia 2

Greece 32 Ukraine 2

Slovak Republic 22Bosnia and Herzegovina

1

Lithuania 21 Croatia 1

Bulgaria 12 TOTAL EUROPE: 4,124

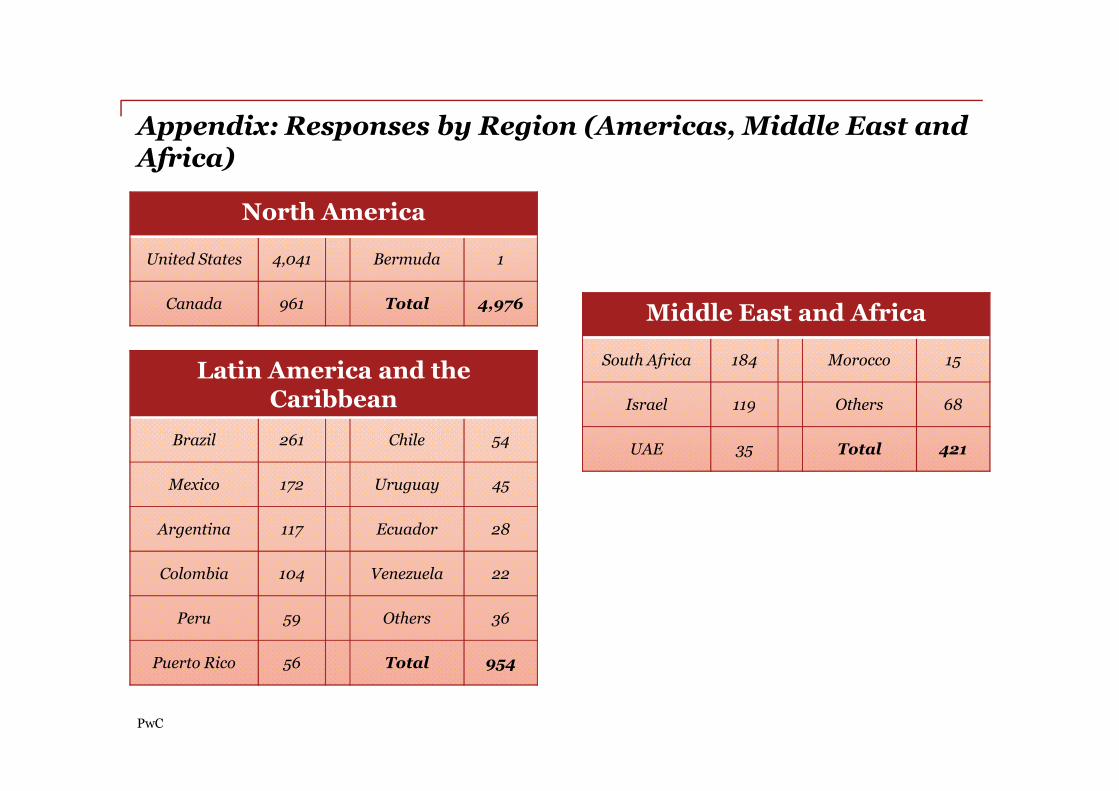

Appendix: Responses by Region (Americas, Middle East and Africa)

North America

United States 4,041 Bermuda 1

Canada 961 Total 4,976

Latin America and the Caribbean

Middle East and Africa

South Africa 184 Morocco 15

Israel 119 Others 68

PwC

Caribbean

Brazil 261 Chile 54

Mexico 172 Uruguay 45

Argentina 117 Ecuador 28

Colombia 104 Venezuela 22

Peru 59 Others 36

Puerto Rico 56 Total 954

Israel 119 Others 68

UAE 35 Total 421

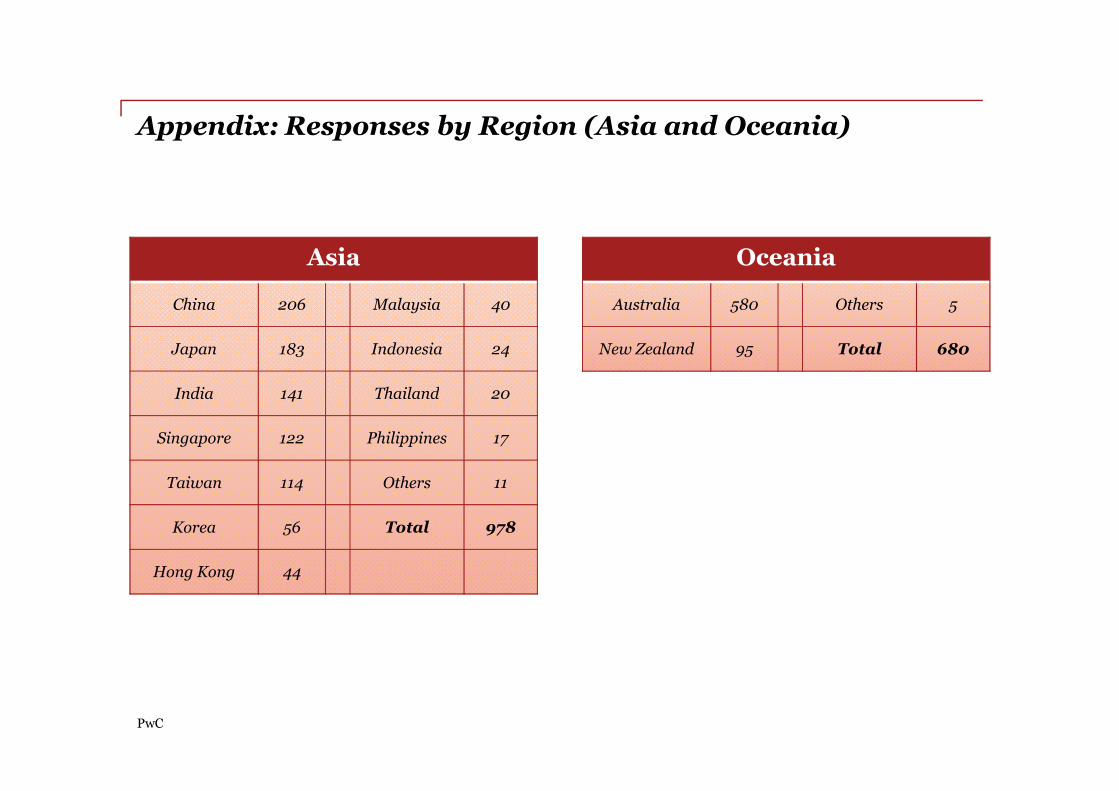

Appendix: Responses by Region (Asia and Oceania)

Asia

China 206 Malaysia 40

Japan 183 Indonesia 24

India 141 Thailand 20

Oceania

Australia 580 Others 5

New Zealand 95 Total 680

PwC

India 141 Thailand 20

Singapore 122 Philippines 17

Taiwan 114 Others 11

Korea 56 Total 978

Hong Kong 44