2012 Activity Report Reinventing real economy finance · ” Jean-Paul Chifflet Chairman of the...

43

Reinventing real economy finance 2012 Activity Report

Transcript of 2012 Activity Report Reinventing real economy finance · ” Jean-Paul Chifflet Chairman of the...

Reinventing real economy finance

2012 Activity Report

profileThe Crédit Agricole Group is the market leader in France in UniversalCustomer-Focused Banking and one of the largest banks in Europe.

As the leading financial partner of the French economy and a major European player, the Crédit Agricole Group supports its customers’ projects in France and around the world across the full spectrum of retail banking businesses and related specialised businesses: insurance, asset management, leasing and factoring,consumer finance, corporate and investment banking.

Underpinned by firm cooperative and mutual foundations, 150,000 employees and the 29,000 directors of its Local and RegionalBanks, the Crédit Agricole Group is a responsible and responsive bank serving 51 million customers, 6.9 million mutual shareholders and 1.2 million shareholders.

In its efforts to support the economy, Crédit Agricole also stands out through its dynamic and innovative social and environmental responsibility policy. The Group features in the top 3 of Novethic’s rankings concerning corporate social responsibility and responsible reporting by Europe’s 31 largest banks and insurance companies.

www.credit-agricole.com

51millionclients worldwide

150,000employees

31billionRevenues

€10.6 billionGross operating income

€71billionShareholders’equity - Group share

11.8%*Core Tier One Ratio* pro forma post completion of Emporiki disposal

The Group’s organisation6.9 million mutual shareholders underpin Crédit Agricole’s cooperative organisational structure. They own the capital of the 2,512 Local Banksin the form of mutual shares and they designate their representatives each year.29,000 directors carry their expectations.

The Local Banks own the majority of the Regional Banks’ share capital. The 39 Regional Banks are cooperative Regional Banks that offer their customers a comprehensive range of products and services.The discussion body for the Regional Banks is the Fédération Nationale du Crédit Agricole, where the Group’s main orientations are decided.

Crédit Agricole S.A. owns around 25% of share capital in the Regional Banks (excl. the Regional Bank of Corsica). It coordinates, in relation with its specialist subsidiaries the various business lines’ strategies in France and abroad.

CRédiT AGRiCOle S.A.’S ShARe OwneRShip

56.3%of share capital held by the 39 Regional Banks via holding company SAS Rue La Boétie.

43.4%of share capital held by:

0.3%treasury shares

01 Institutional investors: 27.9%

02 Individual shareholders: 11.1%

03 Employees via employee mutual funds: 4.4%

A Universal Customer-Focused BankThe Credit Agricole Group consists of Crédit Agricole S.A. along with all of the Regional and Local Banks, and together they are developing the Universal Customer-Focused Banking model. This model relies on synergies realised between retail banksand associated specialised business lines.

Savings management

MARKET-LEADING POSITIONS IN FRANCE AND EUROPE• No. 1 in bancassurance in France • No. 2 in asset management in Europe• A key player in private banking in Europe

AN INTERNATIONAL NETWORK IN THE MAIN COUNTRIES OF EUROPE,THE AMERICAS AND ASIA• Financing activities`• Investment banking• Debt optimisation and distribution• Capital markets

Corporateand investmentbanking

• Crédit Agricole Immobilier• Crédit Agricole Capital Investissement & Finance

• Uni-éditions• Crédit Agricole Cards & Payments

Other specialisedsubsidiaries

• No. 1 in factoring in France• A leader in lease fnancing in France• A key player in consumer fnance

Specialised business lines

Retail BankingTHE MARKET LEADER IN FRANCE AND

A KEY PLAYER IN EUROPE, WITH ALMOST 11,300BRANCHES SERVICING 32 MILLION CUSTOMERS

39 CRÉDIT AGRICOLE REGIONAL BANKSCooperative companies and fully-pledged banks with

strong local roots, the Crédit Agricole Regional Banks offer a full range of banking and financial products and services to individual customers, farmers, professionals, businesses,

and public authorities.

LCLLCL is a retail banking network with a strong presence

in urban areas across France, with four main business lines: retailbanking for individual customers, retail banking

for professionals, private banking and corporate banking.

INTERNATIONAL RETAIL BANKINGCrédit Agricole is implementing its Universal

Customer-Focused Banking model internationally and mainly in Europe, in its key mediterranean

countries of operation.

EXPERTIS

E

FINAN

CIAL

USEFULNESS

CONTRIBUTION TO SOCIETY

CUSTOMER-CENTRICITY

OUR LIQUIDITY MANAGEMENT• 5 liquidity centres worldwide

• 21 trading rooms linked up to major international investors

• Innovative solutions to raise cash

OUR TECHNICAL EXPERTISE• Innovative financing for medium-sized companies

• Market solutions helping to economise the Group's capital

• Employee shareholders

• Socially responsible bond issuance

• International assistance for clients of the regional banks

OUR DEEP INSIGHT INTO CORPORATES AND FINANCIAL INSTITUTIONS• In close contact with major clients• Proximity of the French Regions Division with the regional banks

• Capacity to negotiate partnerships with investors

OUR STRONG CSR COMMITMENTS• A team dedicated to social and environmental finance

• Specific sector policies• The Equator principles• Employees committed to solidarity causes

The activities involved in corporate finance and investment banking are used by the entire Crédit Agricole group, and play a concrete role in its corporate project and client relations. Every day, Crédit Agricole CIB works alongside the Group's business lines, offering its expertise, proximity and services in corporate finance and investment banking.

THE CRÉDIT AGRICOLE

GROUP

THE GROUP'S CLIENTS

CRÉDIT AGRICOLE CIB WITHIN THE GROUP

WORKING FOR THE CRÉDIT AGRICOLEGROUP AND ITS CLIENTS EVERYDAY

OUR PRIORITY IS TO HELP THE REGIONAL BANKS

GROW THEIR ACTIVITY WITH MEDIUM-SIZED REGIONALLY-LOCATED

COMPANIES

“

”Jean-Yves HocherChief Executive Officer of Crédit Agricole CIB

CRÉDIT AGRICOLE CIB2012 ACTIVITY REPORT 7

View points of the Chairman and the Chief Executive Officer ........02

Corporate governance ................................................................04

View points of the Executive Management...................................08

Yearbook of achievements..........................................................12

Overview of activity in 2012.......................................................18

Outlook for 2013 .......................................................................24

International network .................................................................28

The new distribution-origination model .......................................32

Focus on infrastructure, rail, real estate......................................38

Focus on bond issuance .............................................................44

Human resources.......................................................................50

Corporate social responsibility ...................................................56

2012 financial report.................................................................61

2012 ACTIVITY REPORT

YearbookDiscover our most

successful achievements

in recent months,p.12 & 13

1,100 corporate clients

500financial institutions

More than

30locations worldwide

4,387million euros

2012 Net Banking Incomefor strategic activities

9,439employees worldwide

Crédit Agricole CIB is the Corporate and Investment Banking arm of the Crédit Agricole group, the world's sixth-largest bank in total assets and Europe's fourth-largest bank by Tier one equity (The Banker, July 2012).

Crédit Agricole CIB offers its clients a large range of products and services.The Corporate and Investment Bank is structured around five major divisions:

• Client Coverage & International Network,

• Global Investment Banking,

• Structured Finance,

• Fixed Income Markets,

• Debt Optimisation and Distribution.

CRÉDIT AGRICOLE CIB SUPPORTING THE REAL ECONOMY

Sources: Crédit Agricole CIB

Under particularly difficultconditions, Crédit Agricole S.A.introduced structural measuresin 2012 to adapt to the neweconomic and regulatory environment. While the 2012"net income group share" was -€6,471 million, this figure should not overshadowthe solidity of our bankingmodel, namely that of a universal customer-focusedbank. Our customer-focusedbanking activity and the relatedbusiness lines are among thestrongest in Europe.

In corporate and investmentbanking, we overhauled CréditAgricole CIB's economic model,centring it around large non-speculative clients with a muchsmaller risk profile. We did thiswhile maintaining a strongcommercial activity. In 2012,Crédit Agricole CIB also reached, often exceeding, all of the targets that had been

set as part of the adaptationplan launched at the end of 2011.

This work included the discontinuation of certain non-priority activities, such asbrokerage. The CA Cheuvreuxand Kepler Capital Marketsmerger and the sale of CLSA by Crédit Agricole CIB to CITICSwere both finalised. All of thiswas undertaken to ensure that Crédit Agricole CIB's expertisecan continue to serve the Groupand that it can continue towork alongside its clients assisting them with their financing projects.

I am aware that 2012 was a demanding, if not difficult, year for Crédit Agricole CIB'semployees. I would like to acknowledge all of their effortsand thank them for their commitment.

“HAVING REFOCUSED ON

OUR STRENGTHS,WE ARE

REASSERTING OUR ROLE IN

SERVICE OF THEREAL ECONOMY

” Jean-Paul ChiffletChairman of the Board of Directors

of Crédit Agricole CIB

Jean-Yves HocherChief Executive Officer of Crédit Agricole CIB

VIEW POINTSOF THE CHAIRMAN ANDTHE CHIEF EXECUTIVE OFFICER

At the end of 2012 we made aloss of €880 million. Althoughthis figure reflects the impactof the financial crisis and the cost of restructuring on our accounts, it should not overshadow the strong sales trend shown by CréditAgricole CIB throughout the year.

For Crédit Agricole CIB, 2012 wasa satisfactory year for at leastthree reasons. Firstly, wesuccessfully completed ourdeleveraging plan, significantlyreducing our risk-weighted assetsand our liquidity consumption.Crédit Agricole CIB alsosucceeded in refocusing on itsbusinesses of excellence, on itsportfolio of strategic clients, i.e.large corporates and financialinstitutions, and on a closer-knitgeographical network. Finally, itwas satisfactory because marketactivity levels were good in 2012.At the same time, our new

distribution-origination modelbegan to show its relevance.

Crédit Agricole CIB was able to maintain its rankings in its businesses of excellence: in project financing it is rankedthird in the world among leadmanagers in the Europe, Middle-East and Africa (EMEA) region, in euro bond issuance it is rankedfourth in the world, in euro bondissuance by financial institutionsit is ranked second in the world,and in loan syndication it isranked the third largestbookrunner in the EMEA region(source: Thomson Reuters).

I believe in our capacity to buildCrédit Agricole CIB's future and to continue our development. In 2013, we plan to strengthen our efforts and, thanks to ourcommercial commitments and rigorous management, to accompany our clients in their projects and fully play our role within the Group.

Jean-Yves HocherChief Executive Officer of Crédit Agricole CIB

Jean-Paul ChiffletChairman of the Board of Directors of Crédit Agricole CIB

CRÉDIT AGRICOLE CIB2012 ACTIVITY REPORT 32

4 CRÉDIT AGRICOLE CIB2012 ACTIVITY REPORT 5

CORPORATE GOVERNANCE

EXECUTIVE COMMITTEEMembers of the Executive Management CommitteeCorporate governance as of April 22, 2013

Jean-François BalaÿDebt Optimisation & Distribution

Francis CanteriniDeputy General

Manager

Thierry SimonClient Coverage

& International Network

Paul de LeusseFinance

Jacques ProstStructured Finance

Catherine DuvaudCompliance

Jean-Yves HocherChief Executive Officer

Pierre CambefortDeputy Chief

Executive Officer

Daniel PuyoRisk

& Permanent Control

Ivana BonnetHuman Resources

Bertrand HugonetCorporate Secretary & Communications

Thomas GadenneCapital Markets

Alix CaudrillierInvestment Banking

Régis MonfrontDeputy Chief

Executive Officer

Pierre DulonInformationTechnology

Frédéric CoudreauOperations

CRÉDIT AGRICOLE CIB2012 ACTIVITY REPORT 76

CORPORATE GOVERNANCE

THE MANAGEMENT COMMITTEEAND THE EXTENDED EXECUTIVE COMMITTEE

BOARD OF DIRECTORS

< EdmondAlphandéryDirector

< Jean-PaulChiffletChairman

< PhilippeBrassacDirector

Stéphane > PallezDirector

Frank >E. Dangeard

Director

< FrançoisThibaultDirector

< MarcDeschampsDirector

< FrançoisImbaultDirector

Jean-Frédéric >DreyfusDirector

Didier >MartinDirector

< MarcKyriacouDirector

< JeanPhilippeDirector

Michel >Mathieu

Director

< DenisGasquetDirector

< FrançoisMacéDirector

< FrançoisVeverkaDirector

Jean-Louis >Roveyaz

Director

Jean-Pierre >PavietDirector

Executive ManagementJean-Yves Hocher Pierre Cambefort Régis Monfront Francis Canterini

FinancePaul de Leusse Adrien CassanetPhilippe CréninLuc GiraudOlivier de KoningPaul MilleliriMichel Robert

Risks & Permanent ControlDaniel Puyo Patricia BogardBoualem BoukaibaGuillaume FaÿGilles GantoisJean-Claude GelhaarEric de LambillyJames Webb

Information Technology Pierre Dulon Pierre-Yves BollardDavid LitotGilles Henri RouxPhilippe Sersot

OperationsFrédéric Coudreau Pascal de MentqueValérie SauvageSerge Moutot

Solutions for Process Improvement Romain JérômeIsabelle Monier-Vinard

Human ResourcesIvana Bonnet Bernard CalvetJean-Paul Kaouza

LegalBruno FontaineFemke BlancquaertDavid Sheldon

Group Internal AuditJean-Pierre Trémenbert Cécile Bennehard

ComplianceCatherine Duvaud Thierry BraultOlivier Godin

Corporate Secretary& CommunicationsBertrand Hugonet Anne Robert

International SupportEric Lechaudel

Capital MarketsThomas Gadenne Eric ChèvreLaurent CoteVincent FleuryTim Hall Arnaud d'IntignanoVincent Leclercq Philippe RakotovaoJames Siracusa Thomas SpitzFrédéric TruchotGraham Williams

Debt Optimisation & DistributionJean-François Balaÿ Gary HerzogAtul Sodhi

Structured FinanceJacques Prost José AbramoviciOlivier AudemardAlexandra BoleslawskiLaurent ChenainOlivier DesjardinsThibaud EscoffierPierre GlauserJ.-F. Grandchamp des RauxJamie MabilatFrançois MartinFrançois PasquierJacques de VillainesNicolas Vix

Investment BankingAlix Caudrillier Jean-Michel BerlingCharles-Hubert de ChaudenayStéphane DucroizetPierre MarlierHatem MasmoudiBertrand Peyrelongue Bernard Vignoles

Distressed AssetsJulian Harris Emmanuel BaptChristine MorisseauBernard Unger

Sourcing & ProcurementHervé Molmy

Client Coverage & International NetworkThierry Simon Emmanuel Bouvier d'YvoireThierry HauretGérald MassenetStéphane PublieAntoine SirgiRenée Talamona

Senior Regional Officer AmericasJean-François Deroche

Senior Regional Officer Asia PacificMarc-André Poirier

Senior Regional OfficerEurope, Middle-Eastand Africa (EMEA) & Senior Country Officer UKArnaud Chupin

Senior Country Officer GermanySylvia Seignette

Senior Country Officer ItalyPhilippe Pellegrin

Senior Country Officer JapanMichel Roy

Senior CountryOfficer RussiaErik Koebe

Senior Country Officer SpainJuan Fabregas

Crédit AgricolePrivate BankingChristophe Gancel

Saudi Fransi BankPatrice Couvègnes

Members of the Extended Executive CommitteeCorporate governance as of April 22, 2013

as possible on our balancesheet. 2012 brought proofthat this model works.

Pierre Cambefort:In concrete terms, the ideais to start thinking aboutdistribution when we areworking on our clients'financial structuring. This involves looking for partners who wish to participate in financingalongside us, or taking the fixed-income path. Our teams workedtogether to understand our clients' needs and offer them appropriatesolutions. We wereparticularly innovative in finding a way for

medium-sized companies,which do not have directaccess to the markets, to finance their growth. We also helped publicauthorities with theirsocially responsible bondissues. Thanks to theexpertise of Crédit Agricole CIB, we offerinnovative financingsolutions to the Group'sclients to accompany theirdevelopment.

HOW DID CRÉDIT AGRICOLE CIBSUCCEED IN MAINTAININGITS ACTIVITY AMID GREATERCONTRAINTS, FINANCIALCRISIS AND NEWREGULATIONS?

Régis Monfront:We dealt with thisessentially in two ways.Firstly, we discontinued the equity derivative and commodity activities,which meant we could off-load risk-weighted assets.Then, by rapidlyimplementing ourdistribution-originationmodel and particularly by signing severalpartnerships withinvestors, we were ableto generate majortransactions for our clients.I think that the rapidity with which our project was executed was adecisive factor inmobilising our teams.

OUR ROLE IS TO PROTECT

THE INTERESTS OF BOTH BORROWER CLIENTS

AND INVESTOR CLIENTS

“

”

CRÉDIT AGRICOLE CIB2012 ACTIVITY REPORT 9

€1.8 billion

in gross operating income from ongoingactivities in 2012*

€1.2 billion

in net income, Group share from ongoing activities

in 2012*

SINCE THE END OF 2011,CRÉDIT AGRICOLE CIB HASTRANSFORMED ITSECONOMIC MODEL ANDROLLED OUT AN ADAPTATIONPLAN FOR ITS BUSINESSLINES. BROADLY SPEAKING,WHAT FOR YOU WERE THEMAIN FEATURES OF 2012?

Jean-Yves Hocher:There were several majoraspects this year. Wesucceeded, despite a veryunstable environment, incompletely transformingour strategic model toreduce our consumption of risk-weighted assetsand liquidity. We soldmarket and creditportfolios under goodconditions to reduce ourconsumption of risk-weighted assets andliquidity. At the same time,we maintained stablerevenue on our strategicactivities with a selection of clients to whom we are looking to proposeall of the Bank's products.Despite a very difficultenvironment for bankfinancing and investment in Europe, we successfullycompleted a majortransformation of CréditAgricole CIB.

Francis Canterini:This scale of changeinvolved significantconstraints that we had tonavigate at several levels. The financial division was able to manage the reduction in liquidityand risk-weighted assets.Given the new regulatoryconstraints, severalsupport functions weremobilised. As regards the employment aspect of the adaptation plan, the human resourcesdivision oversaw thedefinition and successfuldeployment of aheadcount reduction plan,which will concern 1,550people in France andabroad between now andthe end of 2013. Weshifted the Bank to a low-risk profile with, as in 2012, satisfactoryoperating results.

Régis Monfront:This transformation startedout as a sharedobservation: the corporatefinance and investmentbanking model, as we had previously known it,could no longer function in the current Basel IIIenvironment. We thereforedecided in December 2011to adopt what we refer to

as a distribution-originationmodel, which is based on asset distribution viathe bond market,secondary sales andpartnerships withinstitutional investorsupstream of financing. It is a model that allows us to maintain our capacityto provide financing for ourclients while at the sametime keeping as few assets

In one year, Crédit Agricole CIB has accomplished a complete transformation of its economic model.New regulations and financial constraints prompted the Bank to overhaul its entire strategy and organisation. Jean-Yves Hocher, Pierre Cambefort, Régis Monfront and Francis Canterini take a look back over the last year and share their view of the Bank's new line of activity.

VIEW POINTS OF THE EXECUTIVE MANAGEMENT

A NEW MODEL FOR A NEW ENVIRONMENT

8

Jean-Yves HocherChief Executive Officer of Crédit Agricole CIB(since 1 December 2010)

Deputy Chief Executive Officer of Crédit Agricole S.A. and in this regardalso Head of the Private Banking activities. Born in 1955, Mr. Hocher is a graduate of the Institut National Agronomique Paris Grignon and of the École Nationale du Génie Rural, des Eaux et Forêts. He oversees all the support functions.

€4.4 billion

in net banking income from ongoingactivities in 2012*

Francis CanteriniDeputy General Manager of Crédit Agricole CIB(member of the Executive Management since 1 December 2010)

Born in 1947, Mr. Canterini holds a master's degree and a post-graduate diploma in economics. He oversees all of the support functions.

* Excluding private banking and restated for revaluation of own debt issues, loan hedges, adjustment plan impacts, recording of CA Cheuvreux and CL Securities Asia (CLSA) under IFRS 5,

and change in value of goodwill.

25%reduction in liquidity

consumption

Jean-Yves Hocher:Our challenge in the yearsahead is to match the risk-weighted assets (RWA) ofour ongoing activities,which stand at 33% oftotal Crédit Agricole S.A.'sassets, with ourcontribution to CréditAgricole S.A.'s recurringrevenues, which stood at24% at end-2012, withoutit weighing on our revenue.In 2013, we aim toconsolidate what we havealready achieved with ournew model by broadening

our relationship with ourpriority clients and withinvestors who are ready towork with us in financingthese clients. Finally, oneaspect is very important forus: optimising our workwith Crédit Agricole S.A.and its regional banks inorder to help them expandtheir activity withregionally-located medium-sized companies.

OUR AIM IS TO ENSURE A FLUID ORIGINATION PROCESS,

NOTABLY BY ENCOURAGING OUR BORROWER CLIENTS TO LOOK

INCREASINGLY TO THE GLOBAL DEBT MARKETS

“

”

CRÉDIT AGRICOLE CIB2012 ACTIVITY REPORT 11

Jean-Yves Hocher:Within the framework of the Group's strategies,we defined our project forCrédit Agricole CIB: acorporate and investmentbank, with a reduced riskprofile, servicing its clientsand the Group. We tookimmediate decisions, suchas the sale of market riskportfolios, we had to maketough choices, and wetook the time to explainour strategic vision. We aresatisfied that our teamssuccessfully rolled-out this vision in 2012.

WHAT ARE YOUR PRIORITIESFOR 2013? HOW DO YOU SEETHE FUTURE?

Pierre Cambefort:We must work differentlyand strengthen ourcollective approach. With the roll-out of our model, employeesattitudes and behaviourshave changed. We mustnow add an "investor"vision to our client one.This will involveunderstanding investorexpectations in detail in order to coordinatefinancing distributionupstream, at theorigination level. We will of course draw on the Crédit Agricolegroup and produceinnovative solutions for its clients and entities.

Régis Monfront:Our aim in 2013 is toensure a fluid distribution-origination process. Thismeans bringing what weachieved in 2012 toindustrial level in order toroll out a more ambitioussales activity. I know thatwe have the means to dothis: we are very wellpositioned on the eurobond markets, in loansyndication, and infinancing activities. In2013, we plan to boostsales efficiency through oureuro and dollar bondplatform.

Francis Canterini:Our model has changedprofoundly. To reach ourprofitability targets, wemust work on reducingcosts while maintaining thequality of our clientservices and of ourregulatory controls. In themedium term, we arelooking to reduce our fixedcost base by around 15%,notably by accelerating thesale of discontinuingportfolios, potentiallygranting them to externalservice providers, byoutsourcing certainfunctions, by reducingcurrent expenditure and bydeveloping cross-departmental projects. Alot hinges on this.

VIEW POINTS OF THE EXECUTIVE MANAGEMENT

A NEW MODEL FOR A NEW ENVIRONMENT

10

EFFICIENT ACTION ON RARE RESOURCES

Crédit Agricole CIB showed great agility in 2012, which enabled it to adapt its consumption of rare resources andits business scope to the new regulatory environment and establish its distribution-origination activity model.

Its measures concerning rare resources helped to reduce liquidity consumption by more than 25% and its RWA bymore than 20% – based on CRD 4 – in relation to the middle of 2011, thanks to targeted disposals. In additionto these exceptional factors, there was the impact of the sale of CA Cheuvreux, and the impairment of goodwillon Newedge and the corporate and investment bank.

Facing these necessary adjustments, the strategic activities generated a net income, Group share similar tothat of 2011, despite lower consumption of rare resourcesand a difficult economic environment. The rapid roll-out of the new distribution-origination model helped to reducethe final proportion of commitments and the developmentof the fixed-income activities, with an equivalent reductionin financing carried on the Bank's balance sheet.

Pierre CambefortDeputy Chief Executive Officer of Crédit Agricole CIB(since 1 September 2010)

Born in 1964, Mr. Cambefort is a graduate of Stanford University (Master of Science) and of the École Supérieure de Physique et Chimie. He oversees international coverage, investment banking and financing.

Régis MonfrontDeputy Chief Executive Officer of Crédit Agricole CIB(since 15 December 2011)

Born in 1957, Mr. Monfront is a graduate of the HEC (French grande école for management and business studies) and holds a law degree from the Université de Sceaux. He oversees capital markets activities, discontinuing activities, debt optimisation and distribution..

CONTRIBUTION OF CRÉDIT AGRICOLE CIB'S STRATEGIC ACTIVITIES

33%

TO CRÉDIT AGRICOLE S.A.'S NET BANKING INCOME

TO CRÉDIT AGRICOLE S.A.'S RISK-WEIGHTED ASSETS

24%

Source: Crédit Agricole CIB

CRÉDIT AGRICOLE CIB2012 ACTIVITY REPORT 131212

See all of our achievements and follow our news on:www.ca-cib.com or flash this code

OUR GLOBAL PRESENCEAmericas> Argentina> Brazil> Canada> Mexico> United States

Africa> Algeria > Austria

> Belgium> Finland> France> Germany> Greece> Italy> Luxemburg

> Monaco> Netherlands> Norway> Portugal> Spain> Sweden> Switzerland> United Kingdom

Western Europe> RussiaEastern and Central Europe

> Lebanon> Libya> Saudi Arabia> United Arab Emirates

Middle-East> Autralia> China> Hong Kong> India> Japan> Korea> Singapore> Taïwan

Asia Pacific

THE MARGUERITE FUND investsagain in the construction of a solar photovoltaic project with EDF Energies Nouvelles

p.14

APRIL, FRANCE

THE EUROPEAN FINANCIAL STABILITY FUND issued €6 billionto provide aid to the Eurozone

p.16

JUNE, EUROZONE

PETROLEOS MEXICANOSsuccessfully completes a pioneering bond issue

p.22

JULY, MEXICO

THE AFRICAN DEVELOPMENT BANKsources in Japan financing to support the education sector on the continent

p.46

NOVEMBER, AFRICA

AIR LIQUIDE financed its homecareactivity with a socially responsiblebond issue, a first in Europe

p.42

OCTOBER, FRANCE

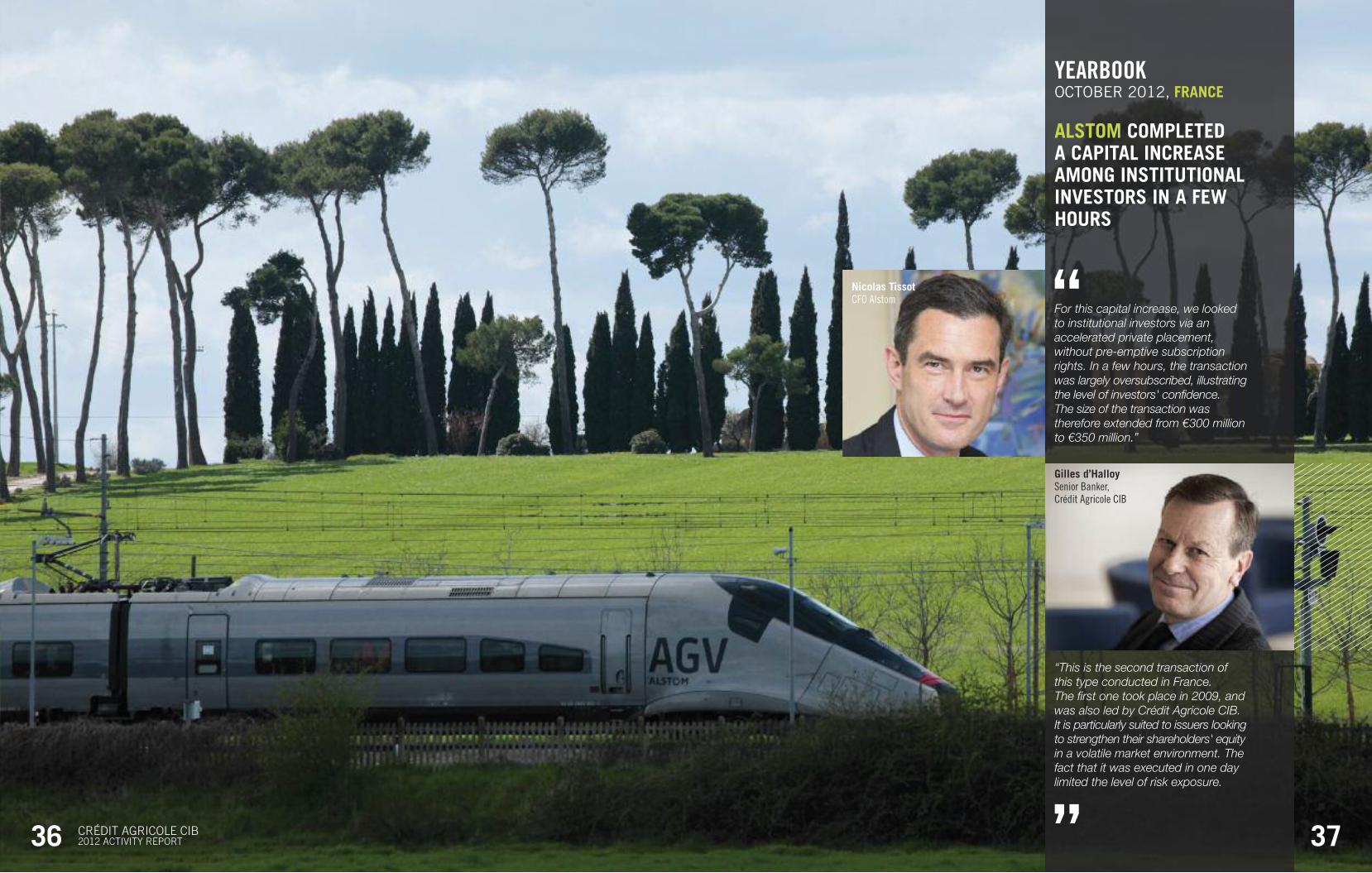

ALSTOM completed a capital increase among institutional investors in a few hours

p.36

OCTOBER, FRANCE

BONDUELLE inaugurates the European private bond placement market

p.26

AUGUST, FRANCE

XCMG, the world's fifth largest manufacturer of construction machinery, with long-term resources for growth

p.30

SEPTEMBER, CHINA

WILLIS LEASE launches the largestaviation ABS offering placed in the market since 2008, and the first aviation ABS in 2012

p.34

SEPTEMBER, USA

INPEX AND TOTAL are writing the future of the energy sector, investing USD 34 billion in the Ichthys LNG project

p.54

JANUARY 2013, AUSTRALIA

ICADE diversified its resources with a €200 million real-estate financing arrangementunderwritten by Allianz France

p.48

DECEMBER, FRANCE

YEARBOOK OF ACHIEVEMENTS

BEING USEFUL EVERY DAY, WORLDWIDE

”Crédit Agricole CIB is pleased to beassisting the Marguerite Fund withthis emblematic project. The Bank’sparticipation bears witness on theone hand to the expertise of its dedicated team and on the otherhand to its unwavering commitmentto sustainable development.

William PiersonManaging Director,Marguerite Adviser S.A. “

”

Renewables is one of our core sectors and we consider that thisproject is a new opportunity to investin a utility-scale solar photovoltaicplant in France. The transaction wasclosed with non-recourse project finance debt raised in a challengingmarket, and closed in a very shortperiod of time."

YEARBOOK APRIL 2012, FRANCE

THE MARGUERITE FUNDINVESTS AGAIN IN THECONSTRUCTION OF A SOLAR PHOTOVOLTAIC PROJECT WITH EDF ENERGIES NOUVELLES

Alexandra BoleslawskiGlobal Head of Power, Utilities and Mines, Crédit Agricole CIB

15CRÉDIT AGRICOLE CIB2012 ACTIVITY REPORT14

“This is the third time that EFSF hasdesignated Crédit Agricole CIB asjoint bookrunner, and it is one of thelargest issues ever conducted byEFSF. This new mandate reflects theexcellent relations that have beendeveloped between the Bank andEFSF over the last two years.“

Christophe FrankelFinance Director,European FinancialStability Fund

Since its creation in 2010, EFSF hasborrowed from investors to provide financial aid to eurozonemember states that request it. Thisbenchmark issue, the largest from asupranational issuer in 2012, is notablefor its efficiency and the diversity of investors, Asian and European notably.

YEARBOOK JUNE 2012, EUROZONE

THE EUROPEAN FINANCIALSTABILITY FUNDISSUED €6 BILLION TO PROVIDE AID TO THE EUROZONE

Henri KuppersSenior Banker, Crédit Agricole CIB

17CRÉDIT AGRICOLE CIB2012 ACTIVITY REPORT16

OVERALL BOND DEAL OF THE YEAR

Euroweek

EUROBOND DEAL OF THE YEAR

SOVEREIGNSSUPRANATIONALS

AGENCIESEuroweek

LIQUIDITY ON THE BALANCE SHEET HAS BEEN REDUCED

The main measure to lighten the balancesheet involved selling portfolios. Almost allof the portfolio of US residential CDOsbooked in the trading book and US RMBSwere sold throughout 2012. The sale ofmarket risks on the credit correlationportfolio to investment fund Blue Mountainwas finalised in February 2012. This transaction helped to reduce our risk-weighted assets by €14 billion.

OUR SCOPE OF ACTIVITY HAS BEEN REFOCUSSED

In 2012, Crédit Agricole CIB disengagedfrom its equity derivative and commodityactivities, which are now managed asdiscontinuing portfolios. Two brokeragesubsidiaries are in the process of beingsold. The sale of CLSA (valued at over€1.25 billion) to CITIC Securities, a Chineseinvestment bank listed in Shanghai andHong Kong, is to be finalised during 2013.The sale of CA Cheuvreux to Kepler CapitalMarkets, a first-rate independent European

financial services group specialised inintermediation and advisory services, is also to be finalised shortly. CréditAgricole CIB's international network has also refocused on around thirtycountries, which account for 85% of globalGDP, after moving out of sixteen countries.

OUR COST BASE HAS BEEN REDUCED

A plan to reduce operating costs has beenimplemented. It includes the voluntarydeparture of 426 employees in France and795 employees abroad. Measures toimprove the operating efficiency ofprocesses have been taken in the businesslines and support functions. In 2013,further work to reduce costs and increaseefficiency will be carried out.

CAPITAL MARKETS ACTIVITY PERFORMED WELL

In 2012, the capital markets activity wasdriven by the strong performance of thefixed-income activities, for which the netbanking income doubled between thefourth quarter of 2011 and the fourthquarter of 2012. Moreover, interest ratederivatives benefited from strong activityparticularly in the fourth quarter with netbanking income up by 87% between thefourth quarter of 2011 and the fourthquarter of 2012.

FINANCING ACTIVITIES ARE RESILIENT

Financing activities were particularlyconcerned by deleveraging, but theyskilfully adapted to the new strategic model in 2012 by refocusing on activitiesthat consume less capital. In this way they maintained most of their competitivepositions.

OUR KNOW-HOW IS WIDELY RECOGNIZED

Our teams received several awards for theirsales performance in 2012: Project FinanceInternational rewarded Crédit Agricole CIBin the category "Global adviser of the year".Global Transportation Finance gave us twoawards: "Airport house of the year" and"Rail house of the year". This is the secondyear in a row that Crédit Agricole CIB has been nominated as the second Most improved bank in covered bonds and best bank for research from Euroweek/The Cover. Finally, in January2013, Crédit Agricole CIB was awarded"European telecoms deal of the year" for the refinancing of ONO by ProjectFinance as part of the "Deals of the year2012" awards.

OUR COMMITMENTS HAVE BEEN METAt the end of 2011, Crédit Agricole group announced an adaptation plan that includedobjectives to reduce liquidity consumption for several of the Group's subsidiaries. For Crédit Agricole CIB, the target reduction in financing needs was set at between €15 billion and €18 billion. To achieve this, three key measures were decided: a reduction in consumption of liquidity on the balance sheet and of risk-weighted assets, a discontinuationof certain activities and the closure of certain locations, and finally a reduction in the cost base.

GOOD PERFORMANCE IN OUR STRATEGIC ACTIVITIES2012 saw a strong sales trend, in particular for the capital markets and financingbusinesses, which succeeded in defending their positions despite a significant fall in liquidity consumption. The impact of deleveraging was therefore well absorbed by the sales activity, excluding exceptional items.

CRÉDIT AGRICOLE CIB2012 ACTIVITY REPORT 19

Crédit Agricole CIB succeeded in completely transforming its strategic model to adapt to a difficult environment and restrictive regulations. The objectives that were set as part of the adaptation planhave been exceeded and the various commercial successes confirm the efficiency and relevance of this new model.

OVERVIEW OF ACTIVITY IN 2012

A SUCCESSFUL TRANSFORMATION

18

AWARDSAND RANKINGS

IN 2012

1st

bookrunner in France for syndication

Thomson Reuters

4thbookrunner in

global convertibleoffering in France

Thomson Reuters

3rdin project finance in EMEA

Thomson Reuters

Rail house of the year

2nd year in a rowGlobal

Transport Finance

4thbookrunner worldwide

in euro bondsThomson Reuters

2ndin ABCP

securitisationin Europe

CP Ware and Banque de France

Aims of the plan

-18

Achievementsat end2012 -33

Aims of the plan

-33

Achievementsat end2012-51

FINANCING REQUIREMENTS(in billions of euros)

RISK-WEIGHTED ASSETS(in billions of euros)

A NEW ECONOMIC MODEL HAS BEEN DEFINED

In this new distribution-origination model, alarge proportion of credit is carried byinvestors: insurance companies, portfoliomanagers and pension funds, as well asbanks with surplus liquidity. Crédit AgricoleCIB will work to reconcile the needs ofthese investors looking for new assetclasses and the needs of clients looking tofinance their development. The Bank willkeep around 20% of lending,demonstrating the quality of the assetsbeing distributed, and will act as arranger(i.e. loan initiator) and loan manager.

PARTNERSHIPS HAVE BEEN ESTABLISHED

During 2012, several partnerships wereestablished with institutional investors:Crédit Agricole Assurances for the firstprivate bond placement on the Europeanmarket by an unrated medium-sizedFrench company, i.e. Bonduelle, AXA tojointly finance Neopost, and Allianz Franceto provide property financing for Icade. Intotal, around thirty partnerships have beeninitiated with institutional investors inFrance and internationally.

A NEW ORGANISATION HAS BEEN ADOPTED

A debt optimisation and distributionbusiness line has been created. Reportingto the general management, it will have atwin role: to identify distribution channelsand placement opportunities, and toincrease assets rotation. In addition, thefollow-up of sales to financial institutionshas been strengthened with the creation ofFinancial Institutions Coverage, as part ofthe capital markets activity.

USING OUR INNOVATIVE CAPACITY TO SERVE THE REAL ECONOMY

In 2012, despite the regulatory constraintsimposed on banks, Crédit Agricole CIB fullyplayed its role as financer of the realeconomy. Along with other Group entities,we proposed innovative bond marketfinancing solutions to local authorities. We offered French unrated medium-sizedcompanies innovative solutions, such as private placements similar to the USmarket. We are proud to have been lead bookrunner for Bonduelle's inaugural bond issue.

ASSISTING THE GROUP IN ITS AREAS OF EXCELLENCE

Within ten years, the Group aims tobecome a benchmark among banks in order to fulfil four challenges for thefuture: the environmental economics,healthcare and Ageing, agriculture andagrifood, and finally Housing. In 2012,Crédit Agricole CIB helped to boost the Group's positions in these areas with a number of transactions such as privatebond placements for Fromageries Bel, abond issue for Sanofi and Caisse deRefinancement de l’Habitat, and thefinancing of an eco-campus for FranceTélécom Orange.

BRINGING OUR VALUES TO LIFE ON A DAILY BASIS

We operate on the basis of the principles ofusefulness, proximity and expertise for thebenefit of our clients and the developmentof our territories. Our ambition is to helpour clients develop through the expertiseand innovative capacity of our teams. Wealso want to strengthen our identity as acorporate and investment bank, a pioneerin the area of sustainable development. For this reason, Crédit Agricole CIBadopted a Corporate Social Responsibilityplan in 2012 as part of the FReD initiativelaunched by Crédit Agricole S.A.. Sectorpolicies were defined to limit operations incertain oil and gas, shale gas, coal-firedthermal energy, hydroelectricity and nuclearenergy sectors. We made strongcommitments to our employees to boostthe gender balance at governance level. Inour areas of expertise, we bring the valuesof the Crédit Agricole group to life, actingon them daily.

Best Uridashi house Capital Market Daily

Global advisor of the year in

project financeProject Finance International

Best bank in covered bonds & best researchEuroweek / The Cover

Environmental bondissue of the year for Ile-de-France

Environmental Finance

European telecomsdeal of the year

for the refinancingof ONO

Project Finance

Deal of the year in Latin AmericaSecuritisation teamGuaranteed ExIm issue for LATAM

Global Transport Finance

CRÉDIT AGRICOLE CIBHAS REFOCUSSED ON ABOUT THIRTYCOUNTRIES TOTALLING85% OF GLOBAL GDP

“

”

A NEW ECONOMIC MODEL TO BUILD THE FUTURESimultaneous to the work to lighten its balance sheet, Crédit Agricole CIB adopted a newdistribution-origination economic model with the aim of continuing to help large priorityclients with our enhanced origination capacity and by drawing on the recognized expertiseof the Crédit Agricole CIB teams.

ONE AMBITION: REINVENTING REAL ECONOMY FINANCEOur identity and our ambitions are profoundly linked to those of the Crédit Agricole group.Our vision for our banking business is simple and structural: to be of use to our clients, to accompany the Group in its areas of excellence and to act on our values each day byrespecting the environment, our clients and our employees.

CRÉDIT AGRICOLE CIB2012 ACTIVITY REPORT 21

OVERVIEW OF ACTIVITY IN 2012

A SUCCESSFUL TRANSFORMATION

20

AWARDSAND RANKINGS

IN 2012

BREAKDOWN OF 2012 NET BANKING INCOME

BY BUSINESS LINE

• Financing activities

• Capital markets & investmentbanking activities

62%

38%

“This issue was the very firstExIm-guaranteed non-aeronauticalsector issuance worldwide.This is an excellent example of howCrédit Agricole CIB is able to draw on the combined skills and expertiseof several teams and products.

Rodolfo Campos VillegasTreasurer, Petroleos Mexicanos “

”

When Crédit Agricole CIB came to us with the idea of adaptingthe Ex-Im guaranteed bond issuestructure used for funding the aircraftindustry, it made sense to us. We were really satisfied with the results of the first issues and expectto use this structure to continue covering part of our financing needsin the future.”

YEARBOOKJULY 2012, MEXICO

PETROLEOS MEXICANOSSUCCESSFULLY COMPLETES A PIONEERING BOND ISSUE

Octavio LievanoSenior Banker & Deputy SCO,Crédit Agricole CIB

23CRÉDIT AGRICOLE CIB2012 ACTIVITY REPORT22

TRADE FINANCEDEAL OF THE YEAR

Latin Finance Magazine

PERSISTENT IMBALANCESWARRANT PRUDENCE

At this level, prudence iscalled for. Academicallyspeaking, the easing ofextreme risks does notmean that the globaleconomic and financialsystem has returned to anormal distribution of risks,where the economic cycleis the beginning and theend of investmentstrategies. There are stilltoo many economic andfinancial imbalances to bereduced and too manypolitical uncertainties to be

dealt with. With regard toimbalances, first andforemost are the persistentlevels of excessive debt, inboth the public and privatesector, in the US and inEurope. Across theAtlantic, private debtreduction is progressingwell; the state (lato sensu)however has barely begun.In Europe, in both casesthere is still a long way togo before normalisation isreached. The conclusionfor growth is clear: thework that remains to bedone will weigh on growthfor another few years.

Where uncertainties areconcerned, a key factor isthe power being wieldedby voters. Going by recentelections in Europeancountries in difficulty, eitherthe intensity of thesovereign debt crisis isvery strong and citizensare voting for pro-European and pro-reformparties, or it is weak andvoters are demonstratingtheir discontent andfavouring an anti-system,anti-European route. Doesthis mean that the crisis ispart of the solution?Clearly, the road to

economic and financialnormalisation is a long oneand undoubtedly full ofpitfalls. Investors must lookfar ahead and watch theirnext step. The current yearwill not buck any trend,and while we must believean improvement is in sight,we must also be preparedfor difficult times. A strategic approach iscalled for: flexibility and lowbreakeven levels will be onthe cards for some time tocome!

Written on April 5, 2013

CRÉDIT AGRICOLE CIB2012 ACTIVITY REPORT 25

GROWTH IS RESUMING INTHE UNITED STATES, WITHCONTROLLED GROWTH INCHINA…

Firstly, there is thesentiment that a positiveeconomic trend is takingshape, in the US notably.Data for residentialproperty and automotivesales show a recovery inactivity, while energy prices(gas in particular) arebecoming morecompetitive in relation tothose applied in many rivalcountries. This will boostgrowth and more thanoffset the negative effect ofinevitable budgetarytightening; particularly in anenvironment of ongoingaccommodative monetarypolicy.

Bearing this in mind, howcan we not heed thepositive message beingsent by the equitymarkets?

The S&P 500 index hasjust broken through thehistorical highs reached in2000 and then in 2007. Isthis not a convincing signof a recovery? China, forits part, is sending out amore reassuring message:fears of a hard landinghave waned and both thebusiness sphere andeconomic policy authoritiesseem satisfied with thecurrent growth rate, whichis slower but is also

perceived as being morestable and sustainable(annual rate no longer of10%(1), but around 6-7%).Given this American andChinese state of affairs,why should we favour aworst-case scenario forEurope? Would it not bebetter to wager on animprovement, albeit a verygradual one, driven byexports to the rest of theworld?

INVESTORS REASSURED BYCENTRAL BANK MEASURES

In addition to this,investors seem happy thatextreme risks, those whichare difficult to apprehendand which have drasticconsequences, have beenreduced considerably byresolute central bankpolicies (US, UK, ECB, andmore recently the Bank ofJapan). This means thatthe capital markets andbanking systems shouldbe able to operatecorrectly; which shouldgive private and publicsectors enough time tocarry out their necessarybalance sheetadjustments.

It is obviously verytempting to mix these twosigns: extreme risks areunder control and themessages from both thereal economy and themarkets are familiar ones:

are we not in the firststages of a classicrecovery, following theusual cyclical trends? If so, investors and moregenerally entrepreneurs,will find their points ofreference, justifying moreaggressive strategies.

The markets are prudently optimistic as regards the current year.Two key factors underlie this more confident stance.

OUTLOOK FOR 2013

A YEAR OF A MORE SUBTLE FORCE

24

9090 14149494 9898 0202 0606 1010

00

55

1010

1515

2020

2525

3030

%%

0000 1212 14140202 0303 0404 0606 0808 1010

-20-20

-15-15

-10-10

-5-5

00

55

1010

1515

2020

400400

800800

1 2001 200

1 6001 600

2 0002 000

2 4002 400%%

Hervé GoulletquerGlobal Head of Markets research

(1) After a long period of annual growth of close to 10%, it may seem paradoxical to say that only a slower rate would now be sustainable. In fact, given the level of growth

that China has now reached, only a slower rate, albeit still a rapid one, is sustainable.

THE ROAD TOECONOMIC AND FINANCIAL

NORMALISATION IS A LONG ONE

“”

UNEMPLOYMENT ON THE RISE IN THE EUROZONE AND ON TOP OF THIS A SIGNIFICANT DIVERGENCE

BETWEEN THE MEMBER COUNTRIES A PROMISING IMPROVEMENT

IN THE US RESIDENTIAL PROPERTY MARKET

• France

• Germany

• Italy

• Spain

• Portugal• Ireland

• Greece• Homes price changes • Housing starts

Source: UE and Crédit Agricole CIB Source: US Dpt of Commerce and Crédit Agricole CIB

“With this first €145 million privateplacement for an unrated company,Crédit Agricole CIB demonstrated itscapacity to finance the economy inan innovative manner, alongside Crédit Agricole Nord de France, inaddition to tradition bank financing.

“

”

The Bonduelle group has increasedthe disintermediation of its debt, andis looking to work with solid, loyaland creative financial partners. CréditAgricole mobilised all of its expertise,business lines and entities, providinginnovative and secure solutions forour financial structure.”

YEARBOOK AUGUST 2012, FRANCE

BONDUELLE INAUGURATES THE EUROPEAN PRIVATE BOND PLACEMENT MARKET

27CRÉDIT AGRICOLE CIB2012 ACTIVITY REPORT26

Grégory SansonCFO Bonduelle Group

Ewa BartmannSenior Banker, Crédit Agricole CIB

Xavier DierickxBusiness Centre Manager,Crédit Agricole Nord de France

BEST SECONDARYTRANSACTION

NYSE Euronext

Arnaud Chupin:In EMEA, we have had todeal with a major crisis: theeurozone crisis which hitus directly. We are, in fact,a European bank whichneeds access to allmarkets to accompany ourclients. Consequently, weswiftly established astrategic response whichinvolved concentrating onour main clients, our primeclients, because we knowthem best and trust in theircapacity to withstand thecrisis. We thereforefavoured clients whooperate in the realeconomy. Secondly, wesought financing solutionsthat go beyond thebanking world. Wefacilitated our clients'access to the bond

markets. While they wereaware of our experience ineuro-denominated issues,we were also able todemonstrated ourexpertise in dollar-denominated transactions.

Jean-François Deroche:In the US, one of ourobjectives was to facilitateaccess for non-Americanborrowers to the dollar-denominated fixed incomemarket. This platform hasseen strong growth in thelast three years: in 2012,20 to 25% of our issueswere for non-Americanissuers, essentiallyEuropean or SouthAmerican players and afew Asian players. We alsoreceived an award for oneof our off-balance sheet

transactions: the ABS(asset-backed securities)refinancing of the Oaxacawind farm project directlyon the capital markets. Atransaction that wereplicated for a pipelineproject.

GOOD KNOWLEDGE OF THECLIENT CREATES CLOSE TIES

AND FACILITATES GOOD STRATEGIC DIALOGUE

“

”

CRÉDIT AGRICOLE CIB2012 ACTIVITY REPORT 29

650prime clients

identified

WHAT WERE CRÉDITAGRICOLE CIB'SINTERNATIONAL OBJECTIVESIN 2012?

Thierry Simon:We showed our clients ourcapacity to accompanythem with theirinternational projects.Through our network, wemaintain close ties with ourclients, wherever they areresident, in France,Europe, Asia and theUnited States, andwherever they are lookingto develop. As an example,we are able to help Lafargeestablish its newinternational sourcingcentre in China. We aremore efficient when wework directly within acountry, withoutnecessarily having tooperate via Paris: a bankerwho is responsible for anoverall client relationship inShanghai or Brazil willwork with bankers in thecountries that are strategicfor that client. It is thesame for our products:when we sell our fixedincome services, whetherthey involve euros, dollarsor renminbi, we operatedirectly at the originationlevel in each zone. This isthe advantage of our neworganisation.

Arnaud Chupin:On the subject of beingclose to the client, it isimportant to know theirsector and their industryvery well. This knowledgeprovides the foundation fora successful relationship,and facilitates goodstrategic dialogue. Theclient knows he is workingwith people whounderstand the sector andits particular positioning.

Thierry Simon:This is the type of closerelationship that we areseeking to establish witharound 650 prime clients,so that we become theirbanking partner in all oftheir international projects.

Marc-André Poirier:This means our teamsmust work cohesivelytogether. As an illustration,when we develop arelationship with a largeinternational group, it is not just a question of oursenior banker working withthe CFO stationed at thecompany's head office.The entire Bank ismobilised around theclient, creating severalpoints of contact within thebusiness lines and in thedifferent countries.

HOW DID 2012 PAN OUTWITHIN EACH REGION?

Marc-André Poirier:Our big challenge in 2012was the liquidity constraint.Asia, a region of highgrowth and wealthaccumulation, brought usthis liquidity. Our aim is toestablish contact between

Asian investors and ourfinancial institutions andlarge corporate clients.Note also that more than70% of our revenue in Asiacomes from clients whoare Asian and operate inEurope or the US, or whoare European or US andoperate in Asia. We havebeen able to transcendborders and promotebusiness flows betweenregions. We plan to securethe success of our neweconomic model by alwaysfinding the most efficientsolutions for our investorand borrower clients.

Crédit Agricole CIB’s newly dimensioned network, as part of the adaptation plan, had its first full year of operation in 2012. This meant a more focused global presence that benefited the Bank in the middle of a liquidity crisis, as related by Thierry Simon, Arnaud Chupin, Jean-François Derocheand Marc-André Poirier.

INTERNATIONAL NETWORK

PROXIMITY ACROSS THE BOARD

28

Thierry Simon Global Head of Client Coverage & International Network

Jean-François DerocheSenior Regional Officer Americas

Arnaud ChupinSenior Regional Officer Europe,Middle-East and Africa (EMEA)

Marc-André PoirierSenior Regional Officer Asia Pacific

13%

38%

31%

CLIENT BREAKDOWNBY GEOGRAPHICAL

LOCATION18%

• Americas

• Asia Pacific

• EMEA

• France

“XCMG's first operation on the syndicated credit market was a success. A loan of €160 millionsparked considerable market interest, obtaining a final subscriptionrate of around 250%.

Jiang Long WUVice Presidentand CFO,XCMG

“

”

XCMG Xuzhou Construction Machinery Group continues to expand, recently acquiring a major world player. A strategic acquisition that justified significantfinancing arrangements, with Crédit Agricole CIB as sole bookrunner of a 18 international and Chinese banks' syndicate.”

YEARBOOK SEPTEMBER 2012, CHINA

XCMG, THE WORLD'S FIFTHLARGEST MANUFACTUREROF CONSTRUCTION MACHINERY, WITH LONG-TERM RESOURCESFOR GROWTH

Didier HONGSenior Banker,Shanghai Branch Manager,Crédit Agricole CIB

31CRÉDIT AGRICOLE CIB2012 ACTIVITY REPORT30

model without significantlytransforming ourorganisation.

Jean-François Balaÿ:What we are seeing is achange in approach ratherthan a change oforganisation. The mostimportant factor is that theclient's approach and theway that we structure andwork have changed.Dedicated operating teamswere set up for eachsolution identified tobroaden our product rangeand our distributionchannels. In this way ourorganisation has adapted.And in this way our newmodel is being deployed.

Thomas Gadenne:We are still a medium-sized bank, with ahuman-sized organisation,

but we are also a leadingplayer in structuredfinancing and fixed incomeproducts, with committedteams working for us. Weare using our excellentrelationships with financialinstitutional clients tointroduce new assetclasses and new types oftransactions that we canwork on.

WHAT IS THE OUTLOOK FOR THE MONTHS AHEAD?

Thomas Gadenne:I think it is encouragingbecause market volumesare still fairly strong andhave even intensified incertain sectors. We sawsignificant volume declinesin the first half of 2012because of the liquiditycrisis, but this is now in the past.

Jean-François Balaÿ:The market at the start of2013 is considerablydifferent to the market atthe start of 2012. Our neworganisation, ourpartnerships and ourposition as a leader in thesyndicated loans marketshould enable us to takegood advantage of thisglobal economicconfiguration. We havebeen a leader for threeyears now.

Jacques Prost:Thanks to this new model,we have been able tomaintain our clientpositions: our dialogue andrelations with our clientshave improved becausewe can offercomprehensive, multi-product financial solutions.This puts us in a goodplace to help them seizebusiness opportunities,notably in theinfrastructure, transport,energy and real estatesectors. On the Frenchmarket, this is also a wayto help boost the economyat a time when banks arereducing their balancesheets.

OUR STRENGTH LIES IN OUR HUMAN SIZE, OUR CAPACITY

TO DEAL WITH ALL SUBJECTS, TO REGULARLY DISCUSS THE

PROGRESS OF THE MARKET AND OUR ANTICIPATIONS

NEW BUSINESS MODEL: THREE

SIGNIFICANT DEALS

“

”

CRÉDIT AGRICOLE CIB2012 ACTIVITY REPORT 33

First private bondplacement on the European marketfor the Bonduelle Groupwith Crédit Agricole

Assurances

Real estate financingfor Icade

with Allianz France

HOW DO YOU SEE THE NEWORIGINATION ANDDISTRIBUTION MODELCHANGING THE WAY YOUOPERATE?

Jacques Prost:Remember firstly that thefinancing, capital marketsand syndication activitieshad already beencooperating on variouslevels. Now, however, wehave more direct andsystematic links betweenour activities. Our loandistribution activity wasbroadened to include newasset classes and a largerbase of investors,including insurancecompanies, assetmanagers, pension fundsand banks with surplusliquidity, notably in Asia.

Jean-François Balaÿ:With this in mind, the newtransversal debtoptimisation anddistribution business linewas created, which reportsto Crédit Agricole CIB'sexecutive management.The teams are organisedinto three global activities:origination and structuring,primary and secondarydistribution, and tradingand optimisation of thefinancing portfolio.

Jacques Prost:In reality, the new model istightening the linksbetween the structuredfinancing, capital marketsand debt optimisation anddistribution businesses.Our aim is that all neworiginated transactionssatisfy the expectations ofour borrower clients andinvestor clients. To achievethis, we bring our teamson board at a very earlystage to find the mostsuitable bond orsecuritisation solution, orto repackage loans for saleto institutional investors.

Thomas Gadenne:This new organisation hasproved its worth this year.We plan to continuebroadening our investorbase, notably with

insurance companieswhich are looking todiversify their investmentsas a result of theconstraints associated withthe new Solvency IIdirective.

FROM THIS PERSPECTIVE,WHAT ARE CRÉDIT AGRICOLE CIB'S STRENGTHS IN RELATION TO ITS COMPETITORS?

Jacques Prost:With this new model, wemade a decision tocapitalise on ourrecognised expertise instructured financing, whichis a part of our DNA. Ouradvantage here is ourhuman-size and ourclosely-knit teams, whichwere quick to apply the

The new distribution-origination model that was applied in 2012 is based on a transversal approachbetween the different business lines. Jean-François Balaÿ, Jacques Prost and Thomas Gadenne,explain how it works.

THE NEW DISTRIBUTION-ORIGINATION MODEL

PARTNERSHIPS AND DIVERSIFICATION:A CHANGE OF APPROACH

32

Jean-François BalaÿHead of Debt Optimisation & Distribution

Thomas GadenneHead of Capital Markets

Jacques ProstHead of Structured Finance

Syndication1ST

BOOKRUNNERIN FRANCE

3RD

BOOKRUNNERIN EMEA

Thomson Reuters

First joint financing

for Neopost with Axa

&

“We were delighted that Willis chose Crédit Agricole Securities to complete this importantmandate which was well received by the market.

Charles F. WillisChairman & CEOWillis Lease FinanceCorporation

“

”

Accessing capital markets isstrategic and important to ourbusiness. The closing of WEST IIprovides us with long-term, low-cost,fixed-rate financing to support andgrow our leasing business for manyyears. The transaction provides Williswith capital to expand our businesswhile improving our cash flowand capital structure."

YEARBOOK SEPTEMBER 2012, USA

WILLIS LEASELAUNCHES THE LARGESTAVIATION ABS* OFFERINGPLACED IN THE MARKETSINCE 2008, AND THEFIRST AVIATION ABSIN 2012

Leo BurellManaging Director,Head of Operating AssetsSecuritization,Crédit Agricole CIB

35CRÉDIT AGRICOLE CIB2012 ACTIVITY REPORT34 * Asset-backed securities

ENGINE DEAL OF THE YEAR

Global Transport Finance

AMERICAS DEAL OF THE YEAR

Airline Economics

ENGINE DEAL OF THE YEAR

Airfinance Journal / Euromoney

“This is the second transaction ofthis type conducted in France. The first one took place in 2009, andwas also led by Crédit Agricole CIB.It is particularly suited to issuers lookingto strengthen their shareholders' equityin a volatile market environment. Thefact that it was executed in one day limited the level of risk exposure.

Nicolas TissotCFO Alstom “

”

For this capital increase, we lookedto institutional investors via an accelerated private placement, without pre-emptive subscriptionrights. In a few hours, the transactionwas largely oversubscribed, illustratingthe level of investors' confidence. The size of the transaction was therefore extended from €300 millionto €350 million.”

YEARBOOKOCTOBER 2012, FRANCE

ALSTOM COMPLETED A CAPITAL INCREASEAMONG INSTITUTIONALINVESTORS IN A FEWHOURS

Gilles d’HalloySenior Banker,Crédit Agricole CIB

37CRÉDIT AGRICOLE CIB2012 ACTIVITY REPORT36

Jamie Mabilat:With the adaptation planand our new strategicmodel, our advisory activityhas seen significantchanges, successfulchanges borne out by thefact that we were named2012 "Global advisor of theyear" by Project FinanceInternational. We also havearound a dozen activeinfrastructure advisorymandates at present. I think it is important to stress here that we owe this success to our first-rate teams in New York, Sydney, Europe,Latin America and Asia.

AND THE OUTLOOK?

Jean-FrançoisGrandchamp des Raux:I see us focusing on fivemain areas in 2013. We willaccompany ourinternational clients in theirdevelopment and in

financing theirinfrastructure. We mustretain our leadershippositions and the top fiveranking that we have heldfor several years in theinfrastructure segment. Wewill continue to work ondistribution and will speedup capital rotation bycreating partnerships withinstitutional investors orthrough infrastructure debtfunds. As Jamiementioned, we will growour advisory activity bydrawing on ourinternational footing.Finally, it is crucial that weposition ourselves so thatwe can take advantage ofthe strong growth in bondissuance.

Jamie Mabilat:

Crédit Agricole CIB'sstrategy is to developpartnerships. Infrastructureare central to this strategybecause our productsparticipate in the long-termfinancing of the realeconomy andconsequently they are idealfor institutional investorspension funds, insurance:companies. This is partlywhy we succeeded inmaintaining a strong levelof activity and in signingmajor contracts in 2012.We are also seeing realgrowth in Debt CapitalMarkets activity.Traditionally, once ourprojects are finished theyare well placed for thebond markets (US,Canada, Europe, Australiaand Asia), and we have a

very active pipeline ofbookrunner mandates in this segment, withseveral major mandates to be completed in 2013.In terms of the deal flow,we expect this to rebound,with volumes recovering in relation to 2012.

ONE OF CRÉDIT AGRICOLEGROUP'S STRENGTHS TODAY

IS ITS CLOSE TIES WITH KEY INFRASTRUCTURE

PLAYERS

“

”

CRÉDIT AGRICOLE CIB2012 ACTIVITY REPORT 39

Matthew NormanStructured Finance,Head of Infrastructure for EMEA

12active

infrastructure advisory mandates

in 2012

WHAT IS THE ACTIVITYSCOPE OF CRÉDIT AGRICOLE CIB'SINFRASTRUCTURE DIVISION?

Jean-FrançoisGrandchamp des Raux:The infrastructure divisioncovers four sectors:transport, i.e. roadways,railways, airports, ports;construction, whichincludes hospitals, prisons,schools and otheradministrative buildings aspart of public-privatepartnerships; theenvironment, whichincludes water and wastetreatment; and finally waterand gas distribution andtransmission networks.

HOW DO YOU ACCOMPANYCRÉDIT AGRICOLE CIB'SCLIENTS?

Jean-FrançoisGrandchamp des Raux:We provide structuredasset financing andstructured financingadvisory services. We alsooffer advice in mergers andacquisitions and finance.

Jamie Mabilat:With the strong support ofour colleagues in DebtCapital Markets, we alsooften finance projects viathe bond market, whichpresently accounts for agrowing share of activity inour sector. As anillustration, for GatwickAirport in London, CréditAgricole CIB had financedGlobal InfrastructurePartners' acquisition of theasset in 2008/2009through a bank loan, and

then contributed to itsrefinancing via successivebond tranches in 2011 and2012. We also contributedto a bond issue by APRRin France in 2012.

Matthew Norman:One of the Crédit AgricoleGroup's strengths today isits close ties with keyinfrastructure players. Inconstruction, for example,we consider ourselves theprivileged partners of ourlargest clients in financingtheir various activities. Theinfrastructure teams offer arange of debt marketadvisory and structuringservices. We work veryclosely with infrastructureinvestment funds, such asGoldman SachsInfrastructure Partners,Global InfrastructurePartners and Antin, whoturn to us first for most oftheir financing needs. It isimportant to stress thatEuropean players (Vinci,Bouygues, Skanska,Hochtief, Strabag, ACS,

etc. but also funds, oftenbased in London andParis) are very active in our segment and alsorepresent a large share of our international activity.

WHAT WERE YOUR MOSTSYMBOLIC ACHIEVEMENTS IN 2012?

Jean-FrançoisGrandchamp des Raux:There was Open GridEurope, the European gasnetwork project, which issymbolic for the Bankbecause we received twoawards for this €2.7 billiondeal, "M&A deal of theyear" from PFI ThomsonReuters and "Oil & Gasdeal of the year" fromProject Finance Magazine.We also contributed to therefinancing of the MacPisto project, which is anoil product storage anddistribution networkbetween Le Havre andParis.

Crédit Agricole CIB's infrastructure division won several major deals worldwide in 2012 and receivedawards for the quality of its mandates. Jean-François Grandchamp des Raux, Jamie Mabilat and Matthew Norman fill us in on a year that brought an abundance of successful transactions.

FOCUS ON INFRASTRUCTURE, RAIL, REAL ESTATE

STIMULATING THE ECONOMY

38

Jean-François Grandchamp des RauxStructured Finance,Global Head of Energy & Infrastructure

Jamie MabilatStructured Finance,Global Head of Infrastructure

&

35%

17%22%

THE INFRASTRUCTUREDIVISION'S ACTIVITY

26%

• Americas

• Asia Pacific

• EMEA

• France

GLOBAL ADVISER

OF THE YEARProject FinanceInternational

&

AIRPORTHOUSE

OF THE YEARGlobal Transport

Finance

innovation. Although manyinsurance companies andpension funds havetraditionally been keeninvestors in real estate, theSolvency II regulationsimpose substantial capitalrequirements. Since theassets that we finance areperceived to be less riskythan equities andsovereign debt, investorsare happy to team up withus as partners to ourfinancing arrangements.They trust us because wefoster good client relationsand because of ourexpertise - we are amongthe leaders in thegeographical areas inwhich we operate. In thisway, we gradually becomethe "natural" intermediariesbetween our clients andnew non-banking partnerswho are economically andfinancially interested inparticipating in thesefinancing arrangementsalongside us.

WHAT IS THE OUTLOOK?

Laurent Chenain:Firstly, there are two realestate markets, theinvestment market and therental market.In investment, as I wassaying, property assets areperceived as a safe haveninvestment and manyclients want to invest inthem. For this reason,there is substantial liquidityavailable. In geographicalterms, in Asia, particularlyHong Kong andSingapore, there has beena slight correction in rentalcompany stocks, whichshows that prices werefairly high. We are seeing arecovery in Japan, strongtrends in Australia and arecovery in the US. In theUK and France, theinvestment market remainsstrong, but there has beena correction of rentalcompany stocks, as aresult of which we areprudent in our choice ofassets and of the financingstructures we recommend.We remain very prudentregarding SouthernEurope.

Olivier Desfontaines: In the rail market, we makea distinction betweenpassenger transportation,which shows a steadyincrease, and freight,which is more cyclical. Inthe US, rail freighttransport has shown anupturn, particularly incertain segments linked tothe development of shalegas. In Europe, the rail

freight market is directlycorrelated to the level ofGerman exports, which areshowing a gradual picking-up. Demand for passengerrail transport is structurallyincreasing, and this wasalso the case during thecrisis, driven by rising fuelprices and external factors(congestion, globalwarming, etc.) related tothe other methods oftransport. The question atstake for Europe is theability to support thisincrease in traffic with newinvestment in infrastructuresand rolling stock.

WE HAVE GENUINE EXPERTISEIN FINANCING STRUCTURES

AND INNOVATION

“”

CRÉDIT AGRICOLE CIB2012 ACTIVITY REPORT 41

Olivier DesfontainesStructured Finance,Asset Finance Group,Head of Rail for Europe

9real estate locations worldwide

€2.4billion

New real estate financing in 2012

WHAT DO YOUR RESPECTIVEACTIVITIES INVOLVE?

Olivier Desfontaines:In the rail sector, we havereached an historicalturning point with the on-going deregulation in Europe. Our missionconsists in accompanyingour clients, public orprivate operators, lessorsand investors in thischanging market, whetherthey look for anacquisition, a financing of rolling stock, or aninvestment in the assetclass. Geographically, our operations are locatedclose to our clients inParis, New York, Frankfurtand Milan.

Laurent Chenain:The Bank operates ninereal-estate entities: inFrance obviously, wherearound 50% of our netbanking income isgenerated, but also inEurope (London, Milan,Madrid), the US, Asia(Hong Kong, Singapore,Tokyo) and Australia.Thanks to our 110 real-estate professionals, wehave been assisting clientsfor decades, financing thebest of their real estate andhotel assets in countrieswhere we have local teamsin place. The Bank's otherbusiness lines also benefitfrom the close relations wemaintain with our clientsand our knowledge ofeach market segment ofthe countries in which weoperate.

Olivier Desfontaines:The sovereign debt crisisled to a sharp reduction ingovernments' ability toprovide public financing forinvestment in the railsector. Fleet renewalrequirements are massiveand a significant level ofemployment for the Frenchand European rail industryis at stake. As anillustration, the averageage of freight locomotivesand railcars in Europe is 30years, compared to a 35years useful life! In Francealone, where recentinvestments were made inthe high-speed train (TGV),another €2 billion ofinvestments are needed aspart of the "Trainsd’Equilibre du Territoire"agreement to replace theTéoz and Intercité trains. Inaddition, furtherinvestments would beneeded in the regions forthe TER trains. In this context, and giventhe reduced amount ofpublic financing available,private financing sourcesneed to bridge the gap.This is good news for newinvestors, notablyinsurance companies, whoare interested in this kindof euro-denominatedasset.

HOW DOES CRÉDIT AGRICOLE CIB STAND OUTFROM THE COMPETITION?

Olivier Desfontaines:Firstly we have built anexperienced team ofspecialists, some of whomhave worked in the railindustry prior to joining theBank. Also, through oursector-based approach,we have been able todevelop very closerelations with our clients,and can propose “one-stop-shop” solutions usingexpertise from the Bank'sother business lines:transportation dedicatedM&A team, specialists inrail financing and in thedebt capital markets. TheBank has been able tocapitalize on its longexperience in assetfinancing, most notably inthe aerospace andshipping sectors, tobecome a leader in the railsector both in Europe andthe US.

Laurent Chenain:Knowing the sectormeans, for example, beingable to talk to an Americanclient investing in Franceabout rental investmenttrends in La Défense. Wehave been very familiarwith this market for a longtime, offering both asset-liability and debt financing,both mortgaged andunguaranteed. We havegenuine expertise infinancing structures and

Leader in the financing of the rail and real-estate sectors, Crédit Agricole CIB maintains its leading position by forging close relationships with its clients, and through its deep sectorial knowledge and innovative skills. Laurent Chenain and Olivier Desfontaines further explain.

FOCUS ON INFRASTRUCTURE, RAIL, REAL ESTATE

STIMULATING THE ECONOMY

40

Laurent ChenainStructured Finance,Asset Finance Group,Global Head of Real Estate

RAIL HOUSE OF THE YEAR

2ND YEAR IN A ROWGlobal

Transport Finance

“For this first SRI transaction by a company in Europe, and as the leading bank for socially responsibleinvestors, Crédit Agricole CIB aimedto succeed. We provided Air Liquidewith an original solution to broadenand diversify its investor base.

Fabienne LecorvaisierVice President, Finance and Operations Control

“

”

To finance our homecare activity, which has a high social impact, we decided to issue a bondaimed at socially responsible investors.Our objective was to mobilise SRI investors who were not yet in thehabit of investing in thematic bonds.Crédit Agricole CIB was able to advise us in this transaction.”

YEARBOOK OCTOBER 2012, FRANCE

AIR LIQUIDE FINANCED ITS HOMECARE ACTIVITYWITH A SOCIALLY RESPONSIBLE BOND ISSUE, A FIRST IN EUROPE

Claire MahouSenior banker,Crédit Agricole CIB

43CRÉDIT AGRICOLE CIB2012 ACTIVITY REPORT42

interests together to be ableto distribute the debt of ourclientscorrectly and at thebest price.

WHAT ARE CRÉDIT AGRICOLE CIB'SADVANTAGES IN THIS CONTEXT?

Philippe Rakotovao:Our main attribute is ourlarge international networkthrough which we arepresent on all continents. Itgives us good proximity toour issuer and investorclients. Also, ourorganisation is tightlyintegrated: we have onemanagement structure,with a continuous link

running from transactionorigination to distributionvia execution and trading.This is a key attribute thathas made Crédit Agricole CIB the world'sfourth largest player on the euro bond market. Anexceptional performance!Another factor that sets usapart is the fact that weare a major player on thedollar bond market,handling more than sixtydollar-denominated issueseach year.

Hugues Delafon:We are also one of thelargest players on the newmarket for euro-denominated privateplacements, a key marketthat will underpin growthon the bond market.Another specific feature isthat we have maintainedour roots in France. Ourglobal platform is availableto all of our French clients,including investors,because France has verylarge investors looking toinvest around the world,and borrowers looking toborrow in dollars, yens,renminbi, etc.

HOW DO THESEINVESTMENTS OPERATE ABROAD?

Philippe Rakotovao:Many of our businessclients operateinternationally and havegrowing investment needsin high-growth areas suchas China, Brazil, Russia,etc. These needs can befinanced through dollar oreuro borrowings, and thenconverted into localcurrency. Our businessclients can also raisemoney directly in the localcurrency. The current trendis for large emergingmarkets to develop theirown capital markets sothat internationalbusinesses, which are ourclients, can raise moneydirectly on these markets,which can but growsignificantly. Our challengeis to accompany themprecisely on those markets.

THE CHALLENGE FOR A BANKLIKE CRÉDIT AGRICOLE CIB

IS TO HAVE ACCESS TO ALL THE DIFFERENT SOURCES OF

SAVINGS IN THE WORLD

“

”

CRÉDIT AGRICOLE CIB2012 ACTIVITY REPORT 45

€900 billion

issued in the

euro bond market*

4thbookrunner worldwide

in eurobonds

Thomson Reuters

WHAT DOES CRÉDITAGRICOLE CIB'S BONDACTIVITY INVOLVE?

Philippe Rakotovao:The bond activity is centralto the Bank because itspurpose is to bring twoclient categories together:clients that borrow capitalto invest and institutionalinvestors. There aredifferent types of borrowerclients. Firstly,governments and similarentities such as publicagencies andsupranational enterprises.Then financial institutions,which also demand highlevels of capital. Finally,commercial and industrialcompanies. In this thirdcategory, a distinction ismade between largebusinesses that enjoy allthe benefits of largeborrowers (rating,reputation) and smallerbusinesses which aregaining increased accessto the capital markets.

Hugues Delafon:Although we have beenoperating on the bondmarket for several years,we are naturally movingwith the trend that hasemerged since the start ofthe crisis: on the one hand,Basel III is forcing bankersto redistribute or reducethe lending they werealready conducting directlywith businesses; and onthe other, businesses arelooking to diversify theirfinancing and to speed updisintermediation by going

directly to the capitalmarkets.

Philippe Rakotovao:One of Crédit Agricole CIB'sbiggest challenges is toaccompany this newmeans of financing theeconomy in Europe. Whilebank borrowing was themain source of financingfor businesses in the past,they now are increasinglymoving towards the capitalmarkets, and the world ofinstitutional investors.

Hugues Delafon:It is already happening.And within this trend,several levels ofdisintermediation cohabit.Large corporations havealready been completely"disintermediated". Today,most of the CAC 40issuers raise almost 100%of their long-term debt onthe capital markets.However, smallercompanies do not havethe same freedom ofaccess to these markets.Their financing needs are

not big enough for thesemarkets, and bank debtremains and will remain asignificant part of theirliability structure. Forexample, Bonduelle's totaldebt amounts to less than€800 million, a relativelylow amount for the bondmarket. Bonduelle's debttherefore is 45% financedvia the capital markets inthe form of privateplacements and 55% viabanks. And Bonduelle isvery comfortable with thisratio.

WHO ARE THE INVESTORS?

Philippe Rakotovao:This is the very subjectunderlying our strategy! Ourinvestors come in manyshapes and sizes. They arenot just domestic in originbut operate from anywhere.They include assetmanagers (mutual funds,investment funds, etc.),banks which manage theirliquidity through the bondmarket, and finally hedgefunds and speculativefunds, which play a majorrole on the governmentbond market and aregradually starting to movetoward the corporate bondmarket. The challenge for abank like Crédit Agricole CIBis to gain access to thedifferent types of savingsthe world has to offer andbring diverse

Corporate financing is being completely transformed and disintermediation is accelerating. Below, Philippe Rakotovao and Hugues Delafon describe the activity's exemplary experience on a bond market that is central to the Bank's strategy.

FOCUS ON BOND ISSUANCE

ACCOMPANYING OUR CLIENTS ON AN EXPANDING MARKET

44

Philippe Rakotovao Global Markets,Head of Corporate & Investor clients division

Hugues DelafonGlobal Markets,Debt Capital MarketsOrigination

*Excluding government borrowing