The New FAR Property Plan Collaboration is Key 2007 Eastern Region Seminar Pat Jacklets, CPPM, CF.

Upload

gabriella-washingtonCategory

view

219download

0

2011 NPMA National Education Seminar

Wayne Norman, CPPM CF Earl Evans, CPPM CF

Northrop Grumman Corp. Northrop Grumman Corp.

AgendaCapital Asset Definition

Capitalization Practices

Responsibility for Capital Assets

Capital Records

Capital Identification

Capital InventoryApproachesRolling Wave

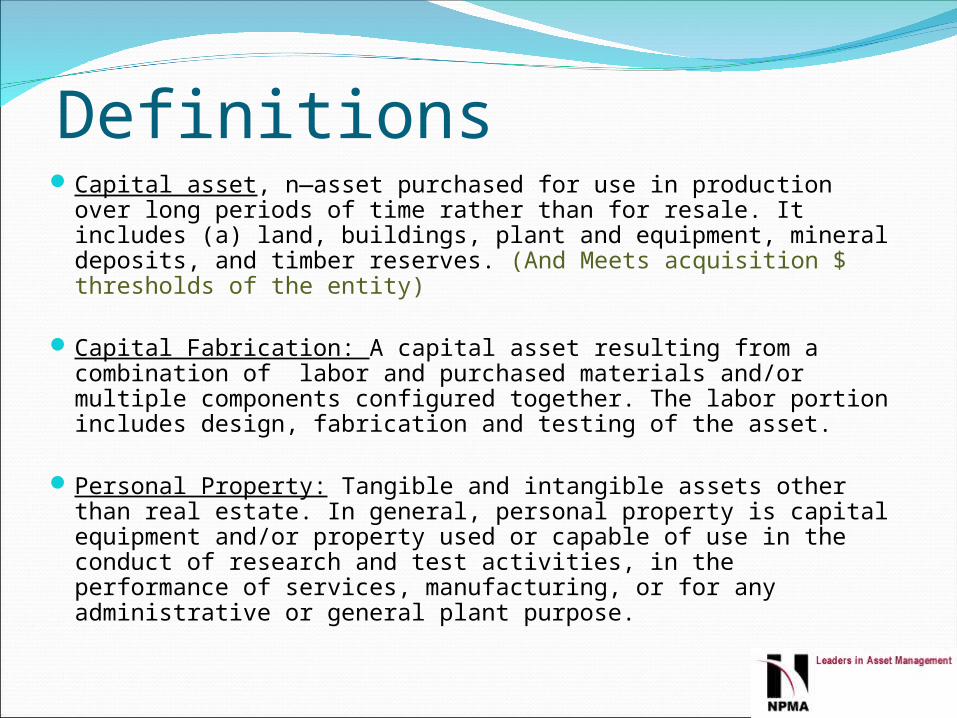

DefinitionsCapital asset, n—asset purchased for use in production over

long periods of time rather than for resale. It includes (a) land, buildings, plant and equipment, mineral deposits, and timber reserves. (And Meets acquisition $ thresholds of the entity)

Capital Fabrication: A capital asset resulting from a combination of labor and purchased materials and/or multiple components configured together. The labor portion includes design, fabrication and testing of the asset.

Personal Property: Tangible and intangible assets other than real estate. In general, personal property is capital equipment and/or property used or capable of use in the conduct of research and test activities, in the performance of services, manufacturing, or for any administrative or general plant purpose.

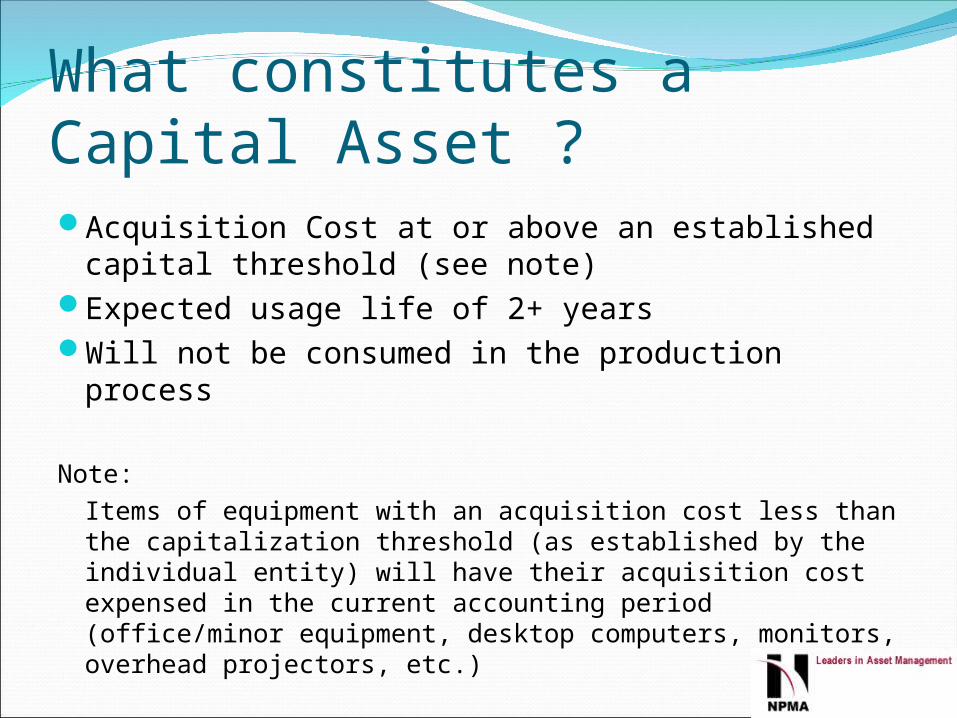

What constitutes a Capital Asset ?Acquisition Cost at or above an established

capital threshold (see note) Expected usage life of 2+ yearsWill not be consumed in the production process

Note:Items of equipment with an acquisition cost less than the capitalization threshold (as established by the individual entity) will have their acquisition cost expensed in the current accounting period (office/minor equipment, desktop computers, monitors, overhead projectors, etc.)

Capitalization thresholdsWhat is in your Entity policy / Disclosure

statement ??Capital Asset = Acquisition value of ??? Typical thresholds - $ 1k , $2k, $5k or more

The trend is higher threshold values Expense more cost in current periodLess pending depreciation and asset balance on

balance sheet (Net Book Value)

InflationLess administration of minor equipment items

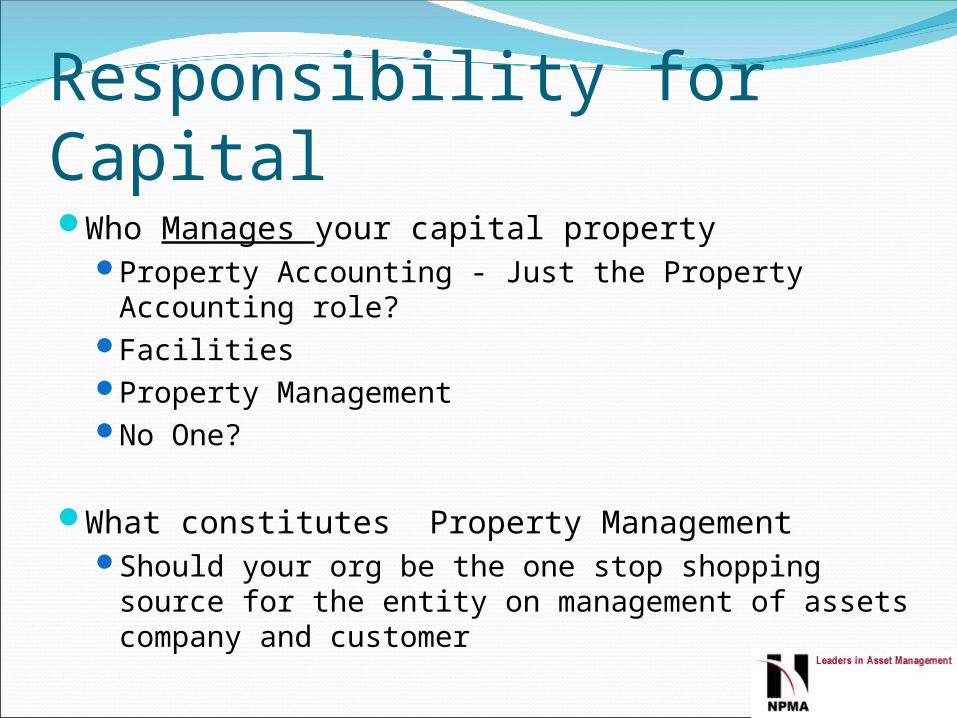

Responsibility for CapitalWho Manages your capital property

Property Accounting - Just the Property Accounting role?

FacilitiesProperty Management No One?

What constitutes Property ManagementShould your org be the one stop shopping source

for the entity on management of assets company and customer

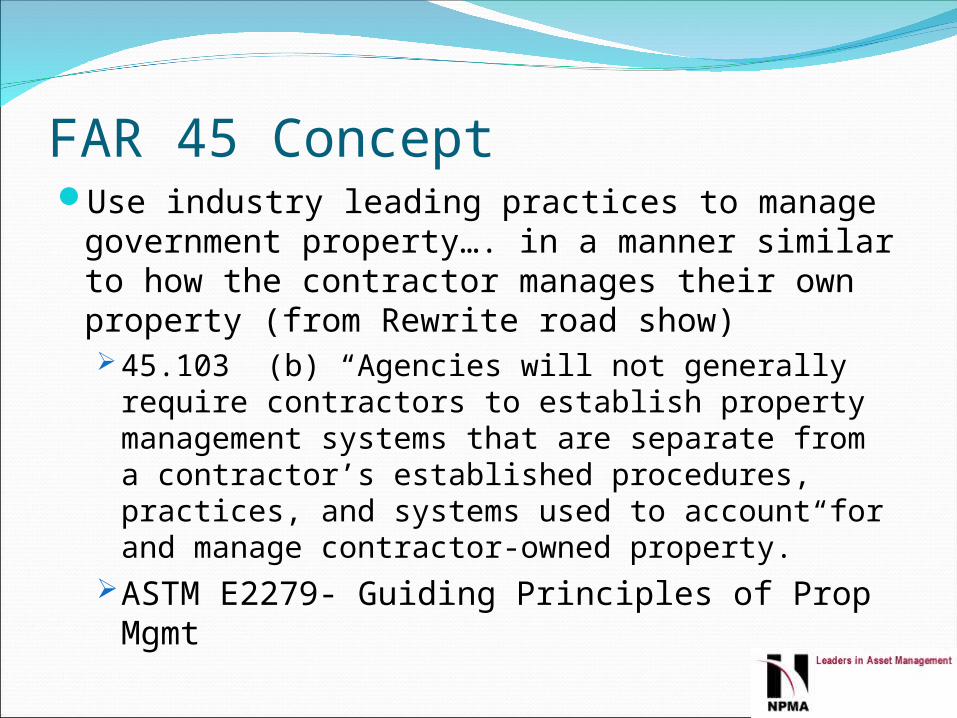

FAR 45 Concept Use industry leading practices to manage

government property…. in a manner similar to how the contractor manages their own property (from Rewrite road show)45.103 (b) “Agencies will not generally require

contractors to establish property management systems that are separate from a contractor’s established procedures, practices, and systems used to account for and manage contractor-owned property.”

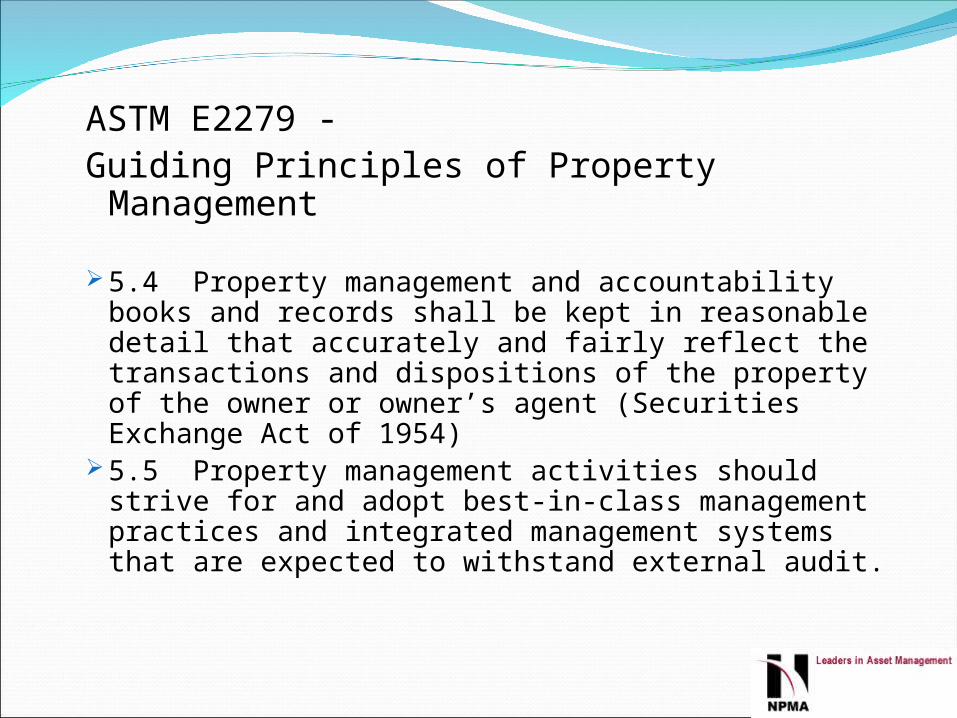

ASTM E2279- Guiding Principles of Prop Mgmt

ASTM E2279 - Guiding Principles of Property

Management

5.4 Property management and accountability books and records shall be kept in reasonable detail that accurately and fairly reflect the transactions and dispositions of the property of the owner or owner’s agent (Securities Exchange Act of 1954)

5.5 Property management activities should strive for and adopt best-in-class management practices and integrated management systems that are expected to withstand external audit.

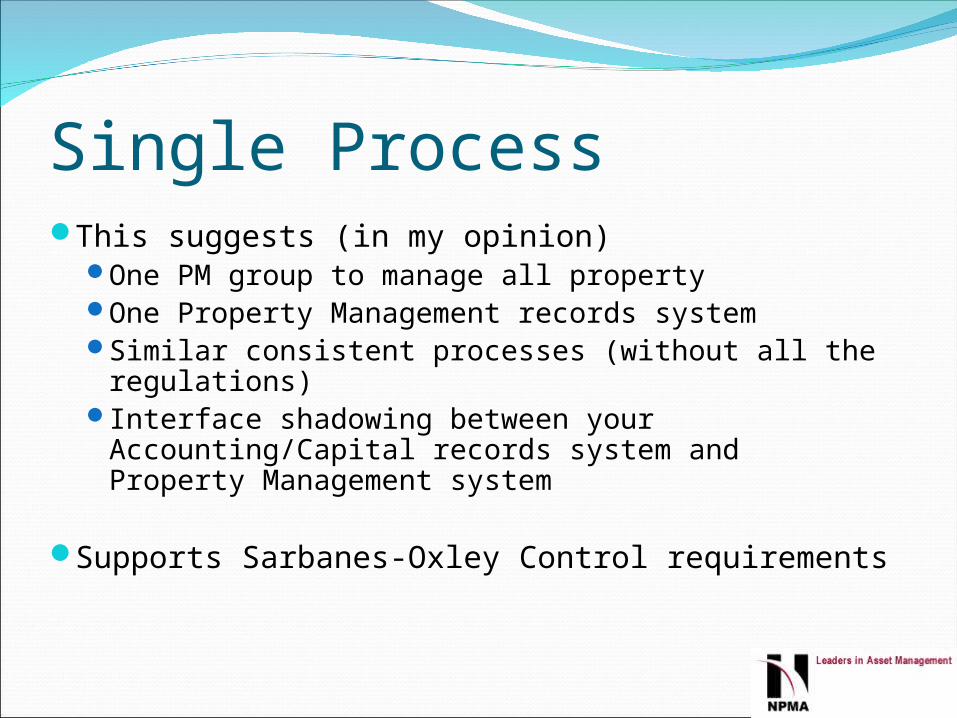

Single ProcessThis suggests (in my opinion)

One PM group to manage all propertyOne Property Management records systemSimilar consistent processes (without all the

regulations)Interface shadowing between your

Accounting/Capital records system and Property Management system

Supports Sarbanes-Oxley Control requirements

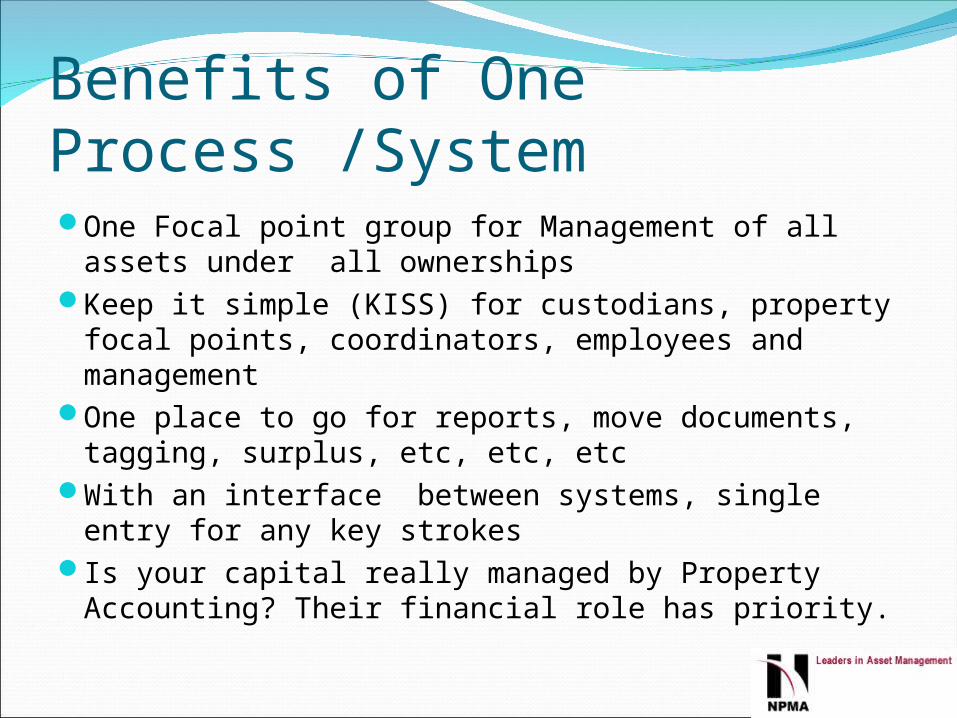

Benefits of One Process /SystemOne Focal point group for Management of all

assets under all ownershipsKeep it simple (KISS) for custodians, property

focal points, coordinators, employees and management

One place to go for reports, move documents, tagging, surplus, etc, etc, etc

With an interface between systems, single entry for any key strokes

Is your capital really managed by Property Accounting? Their financial role has priority.

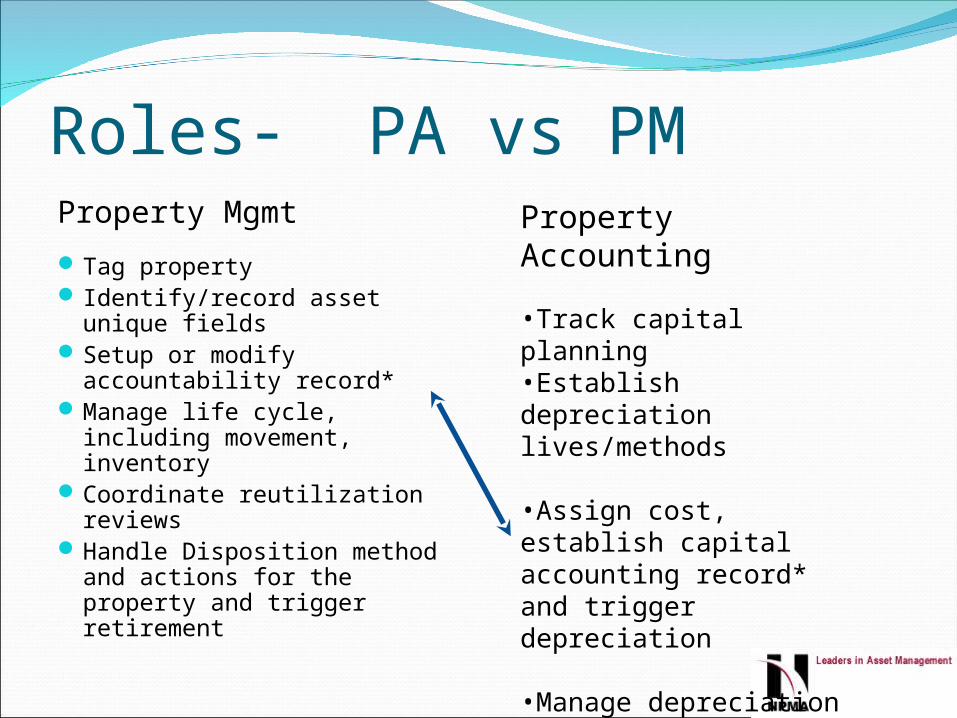

Roles- PA vs PMProperty Mgmt

Tag property Identify/record asset

unique fieldsSetup or modify

accountability record*Manage life cycle, including

movement, inventoryCoordinate reutilization

reviewsHandle Disposition method

and actions for the property and trigger retirement

Property Accounting

•Track capital planning•Establish depreciation lives/methods

•Assign cost, establish capital accounting record* and trigger depreciation

•Manage depreciation and tax

•Retire assets and settle remaining cost

Capital Asset RecordsConsiderations:

What Accounting system are you depreciating assets in?

Does this system provide Property Mgmt functionality?

If not- what is your Customer property system?Why not track your capital in that system too?Consider creating an interface between your

accounting records and property records

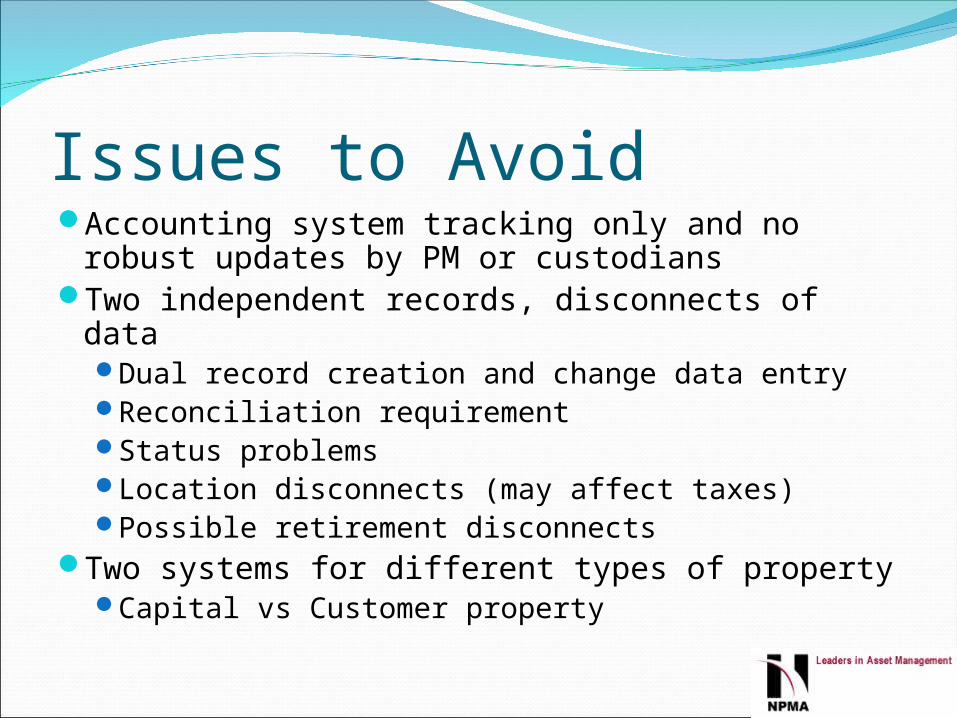

Issues to AvoidAccounting system tracking only and no

robust updates by PM or custodiansTwo independent records, disconnects of

dataDual record creation and change data entryReconciliation requirementStatus problemsLocation disconnects (may affect taxes)Possible retirement disconnects

Two systems for different types of propertyCapital vs Customer property

What to Tag on a Capital ProjectBest Practice concept

Tag items that need to be controlled due to life cycle activities

Property control advantages Asset maintenance and disposition control

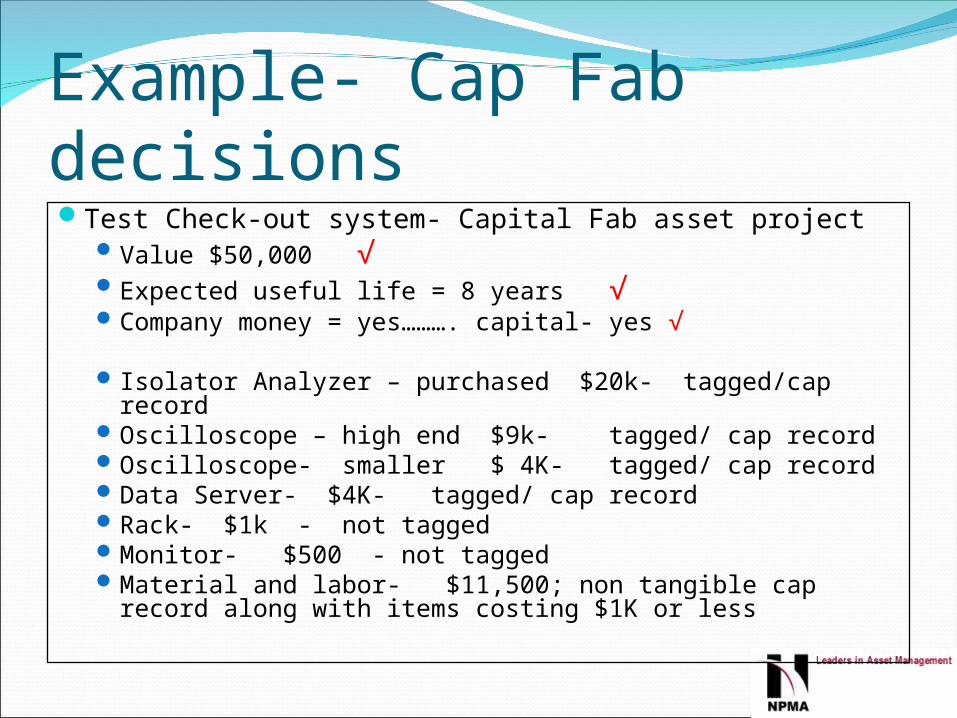

Example- Cap Fab decisionsTest Check-out system- Capital Fab asset project

Value $50,000 √Expected useful life = 8 years √Company money = yes………. capital- yes √

Isolator Analyzer – purchased $20k- tagged/cap recordOscilloscope – high end $9k- tagged/ cap recordOscilloscope- smaller $ 4K- tagged/ cap recordData Server- $4K- tagged/ cap recordRack- $1k - not taggedMonitor- $500 - not taggedMaterial and labor- $11,500; non tangible cap record

along with items costing $1K or less

Current Practice in some placesTest out Equipment- Capital Fab asset project

Value $50,0001 cap record

Issues, all tangible component ignoredSome need to go to calibration, maintenanceSome could be swapped outIdentification issue on the floor for PM processOwnership and trace could be lostComponent sent to surplus, would be hard to

write-down related capital cost

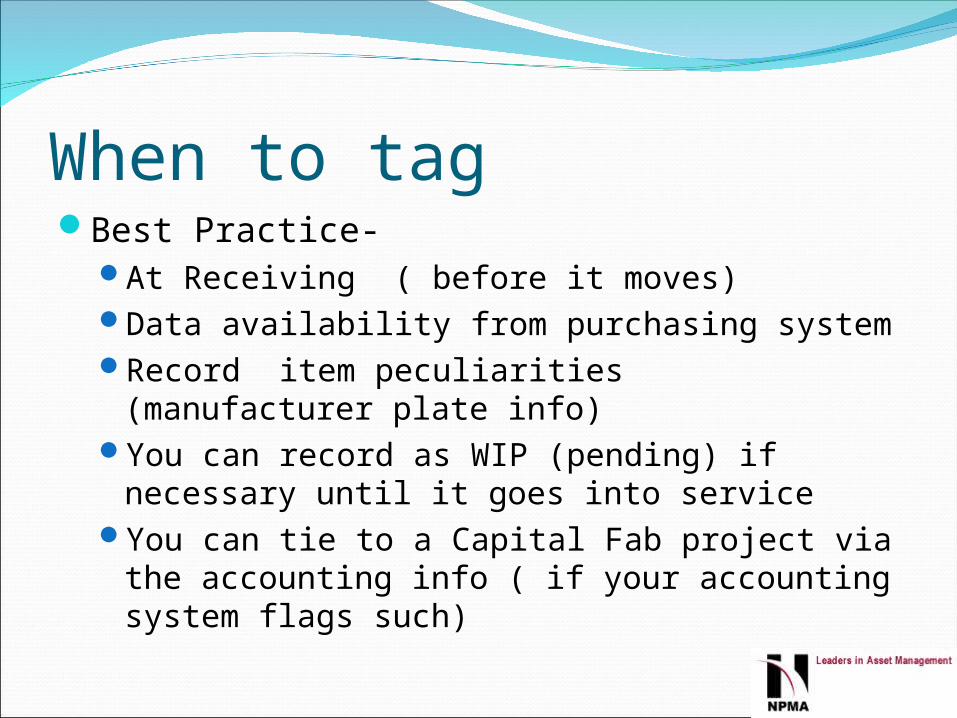

When to tagBest Practice-

At Receiving ( before it moves)Data availability from purchasing systemRecord item peculiarities (manufacturer plate

info)You can record as WIP (pending) if necessary

until it goes into serviceYou can tie to a Capital Fab project via the

accounting info ( if your accounting system flags such)

For Capital Fab taggingSet a rule- no QA buyoff if the item is not

tagged.No Capitalization until PM supplies the tag

data to PAHave a notification form or process for the

Capital process to notify PM when an project is completed and the buyoff is ready to occur

PM then review items for determination of what needs to be tagged

Capital Asset Inventory methodsWall- to- wall (every 1, 2, 3 years)Inventory by exception (every 2, 3 years)

(go find items not otherwise touched during processes which have recorded an inventory touch date)

Situational Inventory- touch all items in certain locations triggered by events (building closures, remodeling events, organizational relocations)

Rolling wave inventory by exception(discussed on next set of slides)

Inventory Rolling WaveCurrent- 2 Year cycle- wait until year two and

touch/validate all our exceptions, perhaps conduct a wall to wall

Proposed- 3 year cycleEverything is touched in some manner every 3

years by exceptionRolling wave-

Each year, the oldest year items are touched if they have not recently been touched (still have an inventory date that will exceed 3 years by current year end)

Every year some those results are turned in Continuous yearly activity

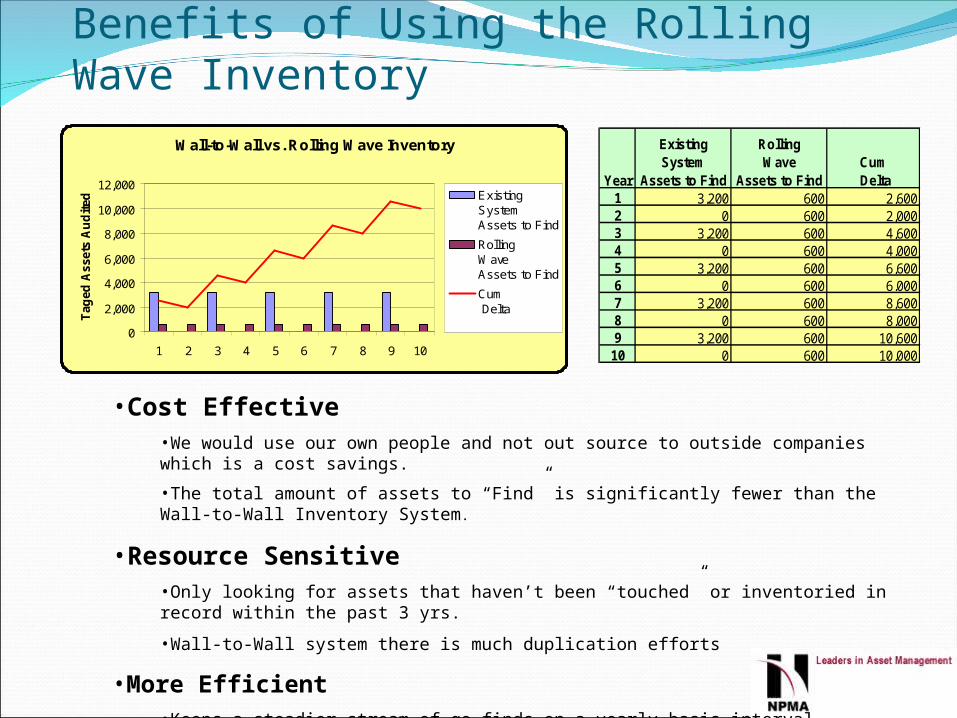

Benefits of Using the Rolling Wave Inventory

Year

ExistingSystem

Assets to Find

RollingWave

Assets to FindCum Delta

1 3,200 600 2,6002 0 600 2,0003 3,200 600 4,6004 0 600 4,0005 3,200 600 6,6006 0 600 6,0007 3,200 600 8,6008 0 600 8,0009 3,200 600 10,60010 0 600 10,000

Wall-to-Wall vs. Rolling Wave Inventory

0

2,000

4,000

6,000

8,000

10,000

12,000

1 2 3 4 5 6 7 8 9 10

Tag

ed A

sset

s A

ud

ited

ExistingSystemAssets to Find

RollingWaveAssets to Find

Cum Delta

•Cost Effective•We would use our own people and not out source to outside companies which is a cost savings.

•The total amount of assets to “Find” is significantly fewer than the Wall-to-Wall Inventory System.

•Resource Sensitive•Only looking for assets that haven’t been “touched” or inventoried in record within the past 3 yrs.

•Wall-to-Wall system there is much duplication efforts

•More Efficient•Keeps a steadier stream of go-finds on a yearly basis interval

•Fewer resources are required to find a smaller amount of assets

22

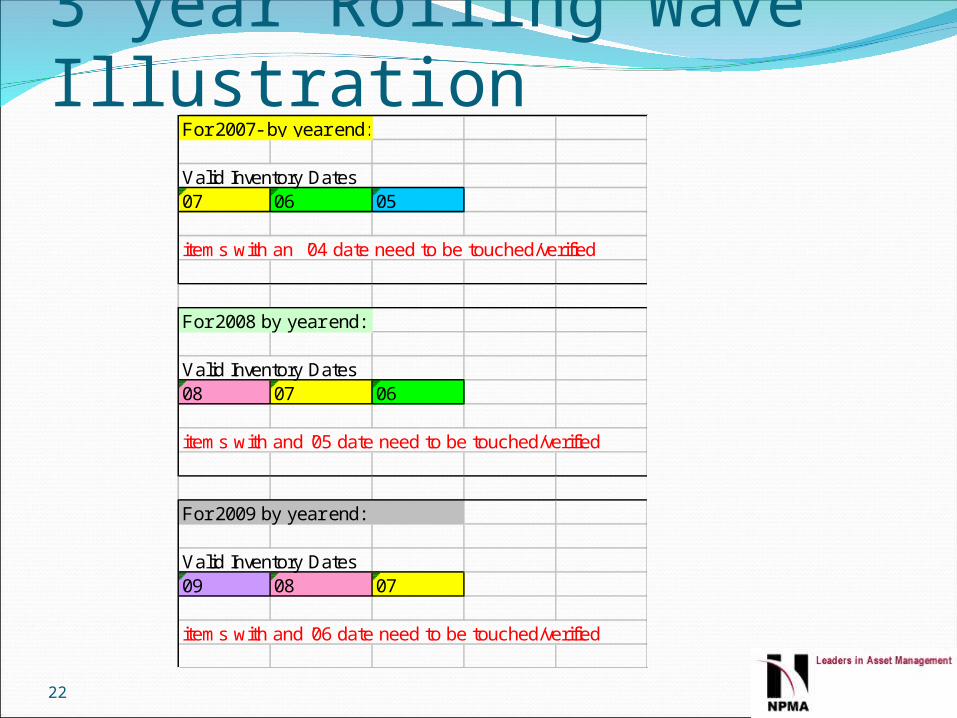

3 year Rolling Wave IllustrationFor 2007- by year end:

Valid Inventory Dates07 06 05

items with an '04 date need to be touched/verified

For 2008 by year end:

Valid Inventory Dates08 07 06

items with and '05 date need to be touched/verified

For 2009 by year end:

Valid Inventory Dates09 08 07

items with and '06 date need to be touched/verified

23

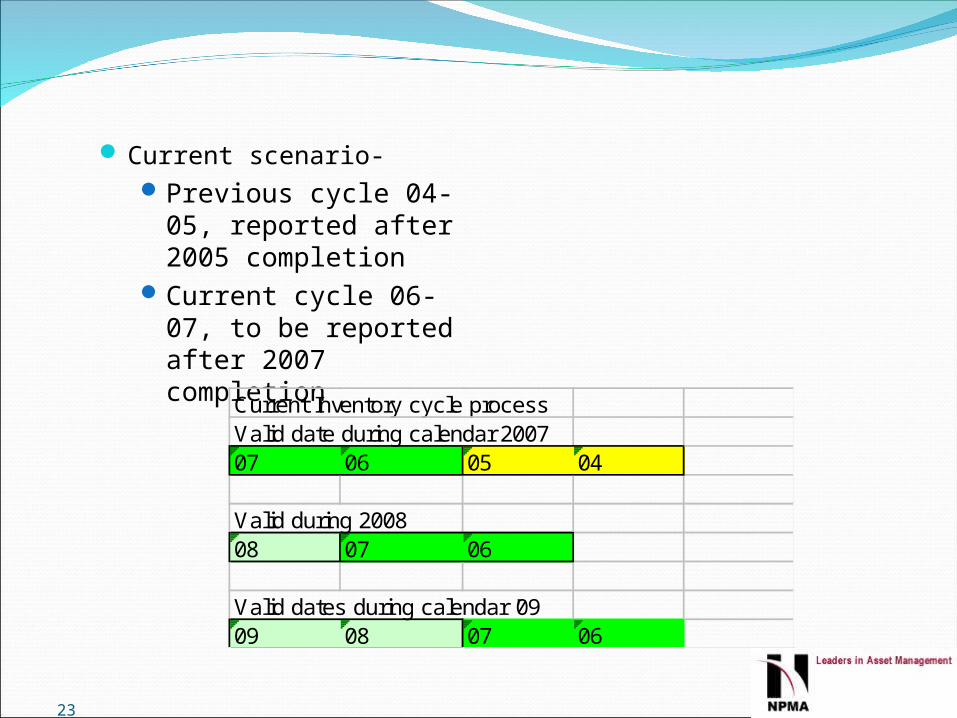

Current scenario-Previous cycle 04- 05,

reported after 2005 completion

Current cycle 06-07, to be reported after 2007 completion

Current Inventory cycle processValid date during calendar 200707 06 05 04

Valid during 200808 07 06

Valid dates during calendar '0909 08 07 06

24

Summary- Rolling WaveReduces disruption to contractor (steady

state)Reduces redundant touchesLevel sets workload over 3 yearsDoes not increase risk to the customerContinual annual feedback- more frequent

partial inventory results.

Questions?