2010 SITE REVIEW REPORT WORKPAPERS - SBDCNet · transactions, which were chosen ... The...

24

1 2010 SITE REVIEW REPORT WORKPAPERS Center Name: Review Date: Center Director: Host Institution: Review By: FINANCIAL REVIEW Objective: To obtain an understanding of the internal controls used by the center and its host, to ensure the accuracy of reported financial and management information, and assess whether costs incurred and claimed for reimbursement and accounted for as match were reasonable, allowable, and allocable. Financial Review Overview The financial review consists of a cursory review of regional center reports and financial detail submitted to the state office, and Q&A with the center director, budget officer and other key personnel for the center. Questions are asked to gain an understanding of the internal controls of the center and host institution to ensure the safeguarding of federal and state funding and to ensure proper authorization of those funds. The financial review also consists of a sampling of program transactions, which were chosen from the year-end financial transaction reports submitted with the center’s year-end cost share report (i.e. final reimbursement invoice). The reviewer’s findings and notes relating to this portion of the review are included below.

Transcript of 2010 SITE REVIEW REPORT WORKPAPERS - SBDCNet · transactions, which were chosen ... The...

1

2010 SITE REVIEW REPORT WORKPAPERS

Center Name: Review Date: Center Director: Host Institution: Review By:

FINANCIAL REVIEW

Objective: To obtain an understanding of the internal controls used by the center and its host, to ensure the accuracy of reported financial and management information, and assess whether costs incurred and claimed for reimbursement and accounted for as match were reasonable, allowable, and allocable. Financial Review Overview The financial review consists of a cursory review of regional center reports and financial detail submitted to the state office, and Q&A with the center director, budget officer and other key personnel for the center. Questions are asked to gain an understanding of the internal controls of the center and host institution to ensure the safeguarding of federal and state funding and to ensure proper authorization of those funds. The financial review also consists of a sampling of program transactions, which were chosen from the year-end financial transaction reports submitted with the center’s year-end cost share report (i.e. final reimbursement invoice). The reviewer’s findings and notes relating to this portion of the review are included below.

2

CURSORY REVIEW PERFORMED BY STATE OFFICE PRIOR TO THE ONSITE REVIEW

The following pre-review tasks should be completed by the state office at least 30-days prior to the scheduled onsite review. 1) Review final cost share report to determine if year-end federal, state and grantee

match (i.e. cash, in-kind and indirect) are supported by ledger and journal detail. This function must take place prior to the submission of the final cost share report (i.e. invoice) for final payment.

Tasks Completed:

Yes No

Reviewers Comments:

2) Record final line item expenditure totals reported in final cost share report and compare year-end actual results to the planned budget provided in the centers contract. Note discrepancies and prepare discussion notes for onsite visit.

SBDC Budget BUDGET ACTUAL VARIANCE A. Personnel $ $ $ % B. Fringe $ $ $ % C. Travel $ $ $ % D. Equipment $ $ $ % E. Supplies $ $ $ % F. Contractual $ $ $ % G. Consultants $ $ $ % H. Other Direct $ $ $ % I. Indirect $ $ $ % TOTAL BUDGET (ACTUAL) $ $ $ 100%

Tasks Completed: Yes No

Reviewers Comments:

3

3) Scan general ledgers and general journals for transactions that appear questionable, improper or extraordinary in nature for sample selection. Questionable, improper or extraordinary samples may include: abstract transaction descriptions, unrecognizable employees or consultants, items in extraordinary cost categories, expenditures large in amount, charges to equipment or out-of-state/country travel, or transaction dates outside of the program year. Select all questionable samples for review. In lieu of such transactions, randomly select samples to insure adequate representation (10 – 20). Tasks Completed:

Yes No

Reviewers Comments:

4) Record the transaction details of the samples selected and provide a copy to the

center director and center budget officer for compilation of support documentation. Use the “Master Sample Selection Worksheet” to record sample detail. Attach a copy of sample selections to onsite review work papers.

Tasks Completed:

Yes No

Reviewers Comments:

5) Review financial findings from previous financial review and list below.

FINDINGS # Description

Reviewers Comments:

4

CURSORY REVIEW PERFORMED BY REGIONAL CENTER PRIOR TO THE ONSITE REVIEW

The following pre-review tasks should be completed by the regional center director and provided to the state office at least 30-days prior to the scheduled onsite review.

1) Describe the degree of autonomy the SBDC regional director has within the host

organization to allocate/expend committed (budgeted) program resources, i.e. state award and match resource, to accomplish contractual milestones and further the objectives of the SBDC program.

Director’s Comments:

2) Describe who, besides the regional director, is authorized to expend SBDC program

award or match funds. List the name, title and organization or host unit of all individuals with such authority, and describe what level of authority they have and if prior approval of the SBDC regional director is required. SBDC Program Authorized Delegates:

Name Title Organization/Unit

Director’s Comments:

3) Describe, if applicable, hosts or SBDC policies covering approval authority for

program financial transactions. Do the policies include guidelines for controlling expenditures include such as general purchasing and voucher payment authorizations, equipment purchases, or travel authorizations?

Director’s Comments:

4) Describe the general processes and procedures required to expend SBDC program

funds. Describe how and who prepares requisitions/purchase orders, reviews and handles invoices and vouchers for payment, and processes and signs checks for payment. Describe if there is a policy regarding business purchases made with cash or credit cards from personal accounts.

Director’s Comments:

5

5) Describe the accounting system used to manage SBDC program funds. Does the

director have direct access to the system to review SBDC accounts? Describe any financial statements or reports that are prepared and distributed to the regional director for review. How often are these reports distributed and reviewed?

Director’s Comments:

6) Attach a copy of a chart of accounts for the SBDC. Include a listing of the SBDC’s

accounts (i.e. cost centers for each SBDC account) for the program year being reviewed.

Director’s Comments:

6

ONSITE REVIEW WORKPAPERS

The following are the state office’s detailed workpapers for an SBDC onsite review. These are internal documents that assist the examiner in being responsive to each area included in an onsite review. These notes are not intended to be distributed to outside parties who do not have direct knowledge, experience, or authority with the MnSBDC.

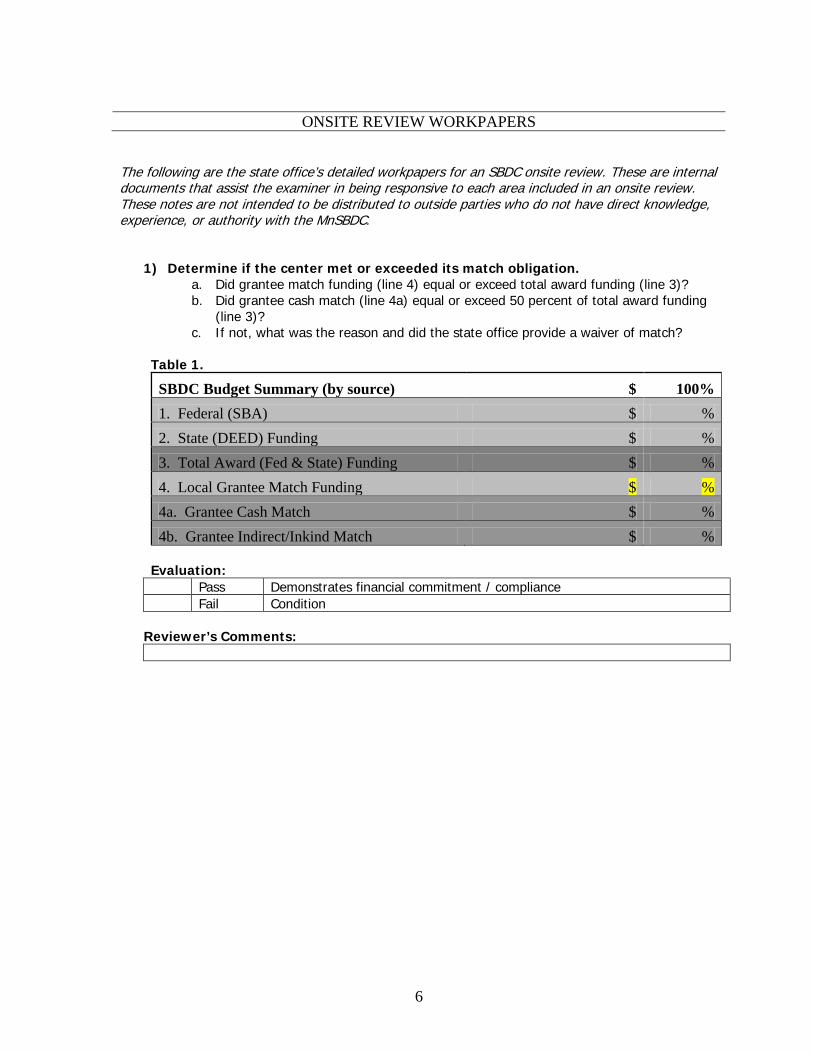

1) Determine if the center met or exceeded its match obligation. a. Did grantee match funding (line 4) equal or exceed total award funding (line 3)? b. Did grantee cash match (line 4a) equal or exceed 50 percent of total award funding

(line 3)? c. If not, what was the reason and did the state office provide a waiver of match?

Table 1.

SBDC Budget Summary (by source) $ 100% 1. Federal (SBA) $ % 2. State (DEED) Funding $ % 3. Total Award (Fed & State) Funding $ % 4. Local Grantee Match Funding $ % 4a. Grantee Cash Match $ % 4b. Grantee Indirect/Inkind Match $ %

Evaluation:

Pass Demonstrates financial commitment / compliance Fail Condition

Reviewer’s Comments:

7

2) Determine if the center managed its financial resources as planned.

a. Was the budget an accurate representation actual spending? b. Were there significant variances (over 10%) in any line item? Which? c. What were the extraordinary circumstances that accounted for significant variances? d. Did the center have unspent award funding for the year? If yes, did the center

execute a grant amendment to reallocate resources to another center? Table 2.

SBDC Budget BUDGET ACTUAL VARIANCE A. Personnel $ $ $ % B. Fringe $ $ $ % C. Travel $ $ $ % D. Equipment $ $ $ % E. Supplies $ $ $ % F. Contractual $ $ $ % G. Consultants $ $ $ % H. Other Direct $ $ $ % I. Indirect $ $ $ % TOTAL $ $ $ 100%

Evaluation:

Pass Demonstrates financial management / compliance Fail Condition

Reviewer’s Comments:

3) Determine if the center had previous financial findings and if those findings were resolved.

a. What financial findings were identified in the centers last review? (note below) b. What corrective action was taken to resolve previous findings? c. Describe in detail what new procedures or internal controls were instituted. d. Describe any unresolved issues and recommended appropriate corrective action.

Evaluation:

Pass Demonstrates control / compliance Fail Condition

Reviewer’s Comments:

Previous Findings

# Description

8

Corrective Actions (if any):

4) Determine whether cost share reports (i.e. invoices) followed state invoicing policy guidelines.

a. How often were invoices submitted for reimbursement? b. If less frequently than quarterly, what was the reason? c. Did the center utilize the state prepared invoice form worksheets? d. Who prepared reimbursement invoices for submission? e. Were invoices prepared correctly or did they require frequent correction? f. How were invoices prepared, i.e. what support was used to prepare invoices? g. Who reviewed invoices before submission for reimbursement? h. Were invoices signed by the regional director and other appropriate parties?

Evaluation:

Pass Demonstrates control / compliance Fail Condition

Reviewer’s Comments:

5) Describe year-end allocation procedures.

a. How was year-end cut-off procedures completed? b. Who performs / reviews these procedures? c. Are new accounts / cost center numbers assigned each program year? d. How are misallocations resolved if they occur?

Evaluation:

Pass Demonstrates control Fail Condition

Reviewer’s Comments:

6) Describe any services provided to clients that require a fee being charged. a. If any, what services are provided to clients for a fee? b. How are the fees determined? c. How were the revenues and cash receipts accounted for? d. Who was responsible for making deposits? e. Who was responsible for tracking program income? f. Review appropriate program income items for comparison.

Evaluation:

Pass Demonstrates control / does not apply Fail Condition

Reviewer’s Comments:

9

7) Determine if the center director has control of the SBDC budget as prescribed by

state policy. a. Who, besides the regional director, is authorized to accrue expenditures using

program resources? b. What level of authority do they have to disburse funds? c. Do they require the prior approval of the center director? d. Are periodic financial management reports prepared? Describe the reports provided. e. How often are reports provided and reviewed by the center director? f. How are discrepancies in reports resolved?

Evaluation:

Pass Demonstrates control / compliance Fail Condition

Reviewer’s Comments:

8) Determine whether cash match committed was allowable and met the special terms and conditions of the grant contract.

a. Verify the center’s Sources of Cash Match Report and determine if contributions were from allowable non-federal sources.

b. If applicable, review bank statements or electronic fund transfer (EFT) reports for proof of receipt and deposit of grant funds to SBDC accounts.

c. Summarize major cash match contributions.

Cash Match Contributions ($2,500 or more): Amount ($) Organization Primary POC

$ $ $ $

Evaluation:

Pass Demonstrates control / compliance Fail Condition

Reviewer’s Comments:

9) Determine if cash match contributions were appropriately managed and protected.

a. Who is the dedicated financial manager/budget officer for the SBDC program? b. Who processes purchase orders/requisitions for the center? c. Who is responsible for the receipt of ordered merchandise? d. Who receives invoices for goods ordered by the center? e. Who reviews invoices/vouchers before payment? f. Are payments to external entities for goods or services ever made by cash? g. How are inter-agency transfers (i.e. charge backs) determined and processed? h. Do invoices/vouchers require the signature of the center director? If not, who is

required to sign them?

10

i. What is the name of the account system used to manage SBDC finances? Does the regional director have direct access to the system to review SBDC accounts?

Evaluation:

Pass Demonstrates control and segregation of duties Fail Condition

Reviewer’s Comments:

10) Determine if in-kind contributions were accurately calculated and justified. a. Are there any conflicts of interest in the sources of in-kind contributions? b. Are amounts claimed reasonable, allowable and allocable? c. Is there adequate supporting documentation for amounts claimed? (e.g., signed and

dated time sheets, non-SBDC customer invoices, log and market rate of supplies received, comparable lease property invoices, etc.)

Evaluation:

Pass Demonstrates compliance / does not apply Fail Condition

Reviewer’s Comments:

11) Determine if indirect contributions were accurately calculated and justified. a. Verify that the center has an indirect rate agreement that is current or that a

provisional rate is allowed. b. Verify that only those costs allowed are included in the indirect base in accordance

with the indirect rate agreement. c. Verify that indirect costs reported are less than or equal to the Federal indirect cost

rate agreement allowed.

Evaluation: Pass Demonstrates compliance / does not apply Fail Condition

Reviewer’s Comments:

12) Determine if the organization’s procedures are adequate to account for program

income. a. Verify documentation and usage of program income according to federal regulation. b. Was there program income carried forward from the previous period? c. Are attendee list maintained from events that produced program income and are fees

paid by attendees recorded in the program income ledger? d. How were cash receipts received and managed? e. Was program income accurately reported to the lead center? f. Discuss how program income was used to further program objectives.

11

Evaluation: Pass Demonstrates control / does not apply Fail Condition

Reviewer’s Comments: 13) Review sample financial data selected. Report findings below.

a. Personnel i. Are all center personnel full-time? If no, what personnel were part-time and

what was the percentage of time allocated to the SBDC. ii. What other programs did the employee allocate time, if any? iii. Does the timesheet / time and effort report support employee’s effort?

b. Fringe Benefits i. Is there a written policy / employment contract outlining fringe benefits or

fringe rate? ii. Are fringe expenditures in accordance with policy?

c. Travel i. Are travel costs attributed to an employees’ effort on behalf of the SBDC? ii. Are the costs attributed to out-of-state travel? If yes, what was the purpose

of the travel? iii. Was the travel approved in the proposal or by prior approval? If not, why?

d. Equipment i. Does the equipment purchased meet the definition of equipment (i.e.

tangible property greater than $500 in value per single item)? ii. Was the equipment approved in the proposal or by prior approval? iii. Was the equipment detail recorded in the Equipment Inventory Record and

provided to the lead center. e. Supplies

i. Are the supplies charged reasonable, allowable, and allocable to the center? ii. Is the expenditure appropriately categorized as supplies?

f. Contractual/Consultant i. Is the organization/consultant included in the regional proposal budget? ii. If no, how was the organization/consultant selected? iii. Does a contract between the center and organization/consultant exist? iv. Was the contract executed prior to delivery of service? v. Do contracts contain the necessary terms described in the grant agreement? vi. Does the consulting hours delivered agree in terms (i.e. hours and rate) to

budget and consulting report detail from the MIS? g. Other Direct

i. Are expenditures reasonable, allowable, and allocable to the center? ii. Are expenditures in excess of historical trends? If yes, why? iii. Is the expenditure appropriately categorized?

h. Program Income i. Verify that the revenue sources were from allowable activities. ii. Were there controls in place to manage and track cash receipts? iii. Were expenses appropriate, i.e. did they further the objectives of the

program? iv. Were receipts and expenses allocable to the appropriate period?

Findings: Sample# Category Finding

12

Reviewer’s Comments:

13

PROGRAMMATIC REVIEW

Objective: To ensure the safeguarding of client confidentiality and compliance with program policies, operating procedures, and applicable laws and regulations pursuant to the Cooperative Agreement. Programmatic Review The Programmatic review consists of Q&A with the center director, program coordinator and selects consultants for the SBDC. The programmatic review questions are asked to gain an understanding of the internal controls of the SBDC and to ensure the safeguarding of the SBDC and its clients. The programmatic review also consisted of the review of client and consultant records, consulting narratives, and observation of center facilities, include client safe guards. The reviewer’s findings and notes relating to this portion of the review are included below. PERFERMANCE MEASUREMENT

1) Determine if the center director is managing center assets to accomplish performance expectations.

a. How is the center director managing the centers assets to accomplish goals? b. What tools or reports are used to monitor progress toward accomplishing goals? c. How often is performance accomplishment reviewed by the director? d. What are the biggest obstacles in accomplishing goals? e. How are these obstacles, if any, managed? f. Did the center accomplish its goals in each key performance area? g. If not, how does the director plan to respond to the centers shortfalls? h. If the center exceeds its goals, what is directors’ insight to the reasons why?

CONTRIBUTION TO JOB CREATION AND RETENTION

OUTPUT GOAL ACTUAL

Existing, In-Business Client Hrs. (#)

Existing, In-Business Client Hrs. (%) 70%

OUTCOME GOAL PROJECTED

Jobs Created and Saved (G=.25)

CONTRIBUTION TO CAPITAL ACCESS FOR BUSINESS INVESTMENT

OUTPUT GOAL ACTUAL

Financing and Capital Access Consulting Hrs (#)

Financing and Capital Access Hrs (%) 30%

OUTCOME GOAL ACTUAL

Loan Capital Accessed (G=$10,000/hr)

14

CONTRIBUTION TO BUSINESS WEALTH CREATION AND GROWTH

OUTPUT GOAL ACTUAL

Marketing and Business Plan Consulting Hrs (#)

Marketing and Business Plan Consulting Hrs (%) 50%

OUTCOME GOAL PROJECTED

Bus Wealth in Sales Rev Increased (G=$5,000/hr)

Tax Revenues Generated (G=$1,500/hr)

CONTRIBUTION TO NEW BUSINESS STARTS

OUTPUT GOAL ACTUAL

Start-up Assistance Consulting Hours (#)

Start-up Assistance Consulting Hours (%) 10%

OUTCOME GOAL PROJECTED

New Businesses Started (G=1 per 30 start-up hrs)

Evaluation: Pass Demonstrates control to manage assets effectively Fail Condition / Needs attention

Reviewer’s Comments:

Recommendation:

2) Determine the centers knowledge of customers and stakeholders needs and expectations.

a. How does the center monitor what services its small business community needs? b. Does the center conduct its own survey to determine needs? If so, how often? c. How does the center assess key stakeholder expectations? d. What are key stakeholder expectations? How does the center manage those

expectations? e. Are there other formal or informal tools the center uses to determine needs?

Evaluation:

Pass Center utilizes formal and informal resources to manage needs and expectations

Fail Condition / Needs attention

Reviewer’s Comments:

15

Recommendation:

3) Determine how the center manages satisfaction and quality of service delivery?

a. What is the centers current level of client satisfaction from the last state survey? b. What other formal and informal tools does the center use to measure satisfaction? c. How does (or would) the center respond to complaints and dissatisfied clients? d. How does the center measure the quality of services delivered? e. Does the center have a process for reviewing client files and consulting narratives?

How, how often and by who? f. How are non-compliant client files or consulting narrative handled? g. How does (or would) the center respond to issues related to low-quality?

Evaluation:

Pass Demonstrates management of satisfaction and quality of service Fail Condition / Needs attention

Reviewer’s Comments:

Recommendation:

4) Determine if the center is deploying a marketing strategy to attract targeted

clients and support from key stakeholders and funders. a. How does the center market to prospective targeted clients? b. How does the center market and report results to current and funding partners?

Prospective funding partners? c. Does the center director regularly engage with host leadership? d. Does the center market to local elected officials? Who? How often? Results? e. What tools does the center use to market? f. Does the center use the states unified image, identity and message in its marketing

efforts? g. Do the materials used follow State Graphic Standard guidelines? h. Obtain samples of advertising/reporting material.

Evaluation:

Pass Demonstrates ability to market SBDC strategically Fail Condition / Needs attention

Reviewer’s Comments:

Recommendation:

5) Describe the centers strengths and weakness in services delivery.

a. How does the center define its most important product and service offerings? b. How do the centers most important services link to the state’s strategic objectives? c. What are the centers core competency strengths and weaknesses?

16

d. What strategies can the center deploy to respond to its weaknesses? What resources are needed?

e. How does the center share its strengths with other centers? If it doesn’t, how can they be leveraged or duplicated in other centers?

Evaluation:

Pass Demonstrates ability to deliver, manage and improve services Fail Condition / Needs attention

Reviewer’s Comments:

Recommendation:

6) Determine if the center has adequate human capital, resources and support to accomplish expectations and deliver results.

a. Has there been turnover in the regional director, program coordinator or key consultant positions over the past three years?

b. How long has the regional director and program coordinator been employed? c. What is the current job classification of the regional director? Program coordinator? d. How many employee consultants does the center employ? Active private consultants? e. Are host faculty engaged with the SBDC? How? f. Does the center utilize under-graduate or graduate students? How? g. Could the center utilize faculty or students more effectively? How? h. Does center workforce (employees and consultants) activity participate in the state’s

annual professional development conference? If no, why? i. Do the regional director and program coordinator attend the ASBDC annual

conference? If no, why? j. What other professional development does the center or workforce employ? k. What motivates center workforce to contribute to the network’s success?

Evaluation: Pass Center has committed leadership to achieve high performance Fail Condition / Needs attention

Reviewer’s Comments:

Recommendation:

7) Determine if the procedures regarding the solicitation of private consultants

meets state standards. a. Does the center utilize private consultants? b. If yes, were all the consultants utilized included in the proposal budget? c. If not, how were the consultants not included in the proposal selected? d. Did the center advertise/issue and RFP? Where? e. What selection standards were used? f. How did the center determine which consultants receive contracts? g. Obtain a sample of advertising material, if applicable

17

Evaluation:

Pass Demonstrates compliance with guidelines / Does not apply Fail Condition / Needs attention

Reviewer’s Comments: Recommendation: 8) Determine if the center is employing review procedures for personnel, including

private consultants. a. What criteria are used to evaluate personnel performance? Private consultants? b. How often are personnel performance reviews performed? Private consultants? c. How are personnel rewarded/penalized for work performance? Private consultants?

Evaluation:

Pass Demonstrates use of formal procedures Fail Condition / Needs attention

Reviewer’s Comments: Recommendation: 9) Review two center employee files. Employee files should include, at a minimum,

the following: a. Current Code of Ethics

Employee (1): [Name]

A Signed [date]

Employee (2): [Name] A Signed [date]

Reviewer’s Comments:

10) Review two private consultant files. Consultant files should include, at a

minimum, the following: a. Current contract b. Current Code of Ethics c. Current Debarment Certification

Consultant (1): [Name]

A Signed [date] B Signed [date]

18

C Signed [date]

Consultant (2): [Name] A Signed [date] B Signed [date] C Signed [date]

Reviewer’s Comments:

11) Determine if the center has adequate facilities to fulfill the mission of the SBDC? a. Is the facility on or off campus? b. Is there adequate parking available? c. Is the facility ADA compliant? d. Is the center adequately equipped and secured to meet the needs of clients and

protect client confidentiality? e. Does the center have a library and resource center available to the general public? f. Does the centers signage comply with state standards?

Evaluation:

Pass Center facility meets minimum standards Fail Condition / Needs attention

Reviewer’s Comments: Recommendation: 12) Review five client records. Select five of the top ten clients that received the

greatest number of consulting hours during the program year. Each client record should include, at a minimum, a scanned copy of the following:

a. Signed “Request for Services” form; signed before the client initial session. b. Signed engagement letter (contract for services) describing the expectations of the

client of the SBDC and the expectations of the SBDC of the client. c. Any key publications, studies, reports, research or documentation prepared or

gathered for the benefit of the client. d. The most current version of financial documentation prepared (spreadsheets,

proformas, and loan documentation) for the client. Financial documents prepared by the SBDC must include the appropriate financial disclaimer.

Client ID: [number]

A Signed [date]; initial session [date] B Signed [date] C D

Client ID: [number]

A Signed [date]; initial session [date]

19

B Signed [date] C D

Client ID:

A Signed [date]; initial session [date] B Signed [date] C D

Client ID:

A Signed [date]; initial session [date] B Signed [date] C D

Client ID:

A Signed [date]; initial session [date] B Signed [date] C D

Evaluation:

Pass Client records reviewed were in compliance with policy Fail Condition / Needs attention

Reviewer’s Comments:

13) Review five client consulting narrative records for the entire program year. Each consulting narrative record should be appropriately categorize and support the time recorded. Each prep-only consulting narrative session should thoroughly describe the work completed by the consultant. Each contact consulting narrative session record should include the following:

a. An analysis of the client’s problem. b. A summary of the consultants observations and recommendations. c. A description of follow-up required by the consultant and client. d. Any other documentation deemed appropriate by the consultant.

CLIENT ID HOURS FINDINGS

Consultant(s) ID: # of Sessions: None. Notes were of sufficient detail.

Consultant(s) ID: # of Sessions: None. Notes were of sufficient detail.

20

Consultants(s) ID: # of Sessions: None. Notes were of sufficient detail.

Consultants(s) ID: # of Sessions: None. Notes were of sufficient detail.

Consultants(s) ID: # of Sessions: None. Notes were of sufficient detail.

Evaluation: Pass Consulting narratives complied with policy Fail Condition / Needs attention

Reviewer’s Comments:

Recommendations: 14) Review three training packets. Each training packet should include the following:

a. A “Management Training Report” (SBA Form 888). b. A roster of attendees. c. Training event promotional materials, with appropriate logos and disclaimer. d. Cosponsorship agreement, if applicable, signed by all cosponsors. e. Completed training evaluations.

Conference:

A Completed and signed by regional director [date] B Roster attached and includes conference attendee signatures. C Promotion material included and complete; special needs disclaimer included D Cosponsorship agreement included and signed by appropriate parties E Training evaluations on file and tallied correctly

Conference:

A Completed and signed by regional director [date] B Roster attached and includes conference attendee signatures. C Promotion material included and complete; special needs disclaimer included D Cosponsorship agreement included and signed by appropriate parties E Training evaluations on file and tallied correctly

Conference:

A Completed and signed by regional director [date] B Roster attached and includes conference attendee signatures. C Promotion material included and complete; special needs disclaimer included D Cosponsorship agreement included and signed by appropriate parties E Training evaluations on file and tallied correctly

21

Evaluation:

Pass Training packets reviewed indicate compliance with policy Fail Condition

Reviewer’s Comments:

22

STRATEGIC REVIEW

Objective: To ensure the continual growth and development in accomplishing the objectives of the program and to provide for continuous improvement. Strategic Review The Strategic Review consists of comparison of center accomplished strategic objectives versus state strategic objectives, and Q&A of the center director, program coordinator and key personnel for the SBDC. Strategic review questions are asked to assure the center understands state strategic objectives and the implementation plan to accomplish them. The reviewer’s findings and notes relating to this portion of the review are included below.

1) Describe how the state strategic plan goals and objectives are integrated throughout all levels of the organization.

a. How are the goals and objectives of the state strategic plan integrated in to planning and center operations?

b. How is progress towards accomplishing the plans objectives monitored? c. Who receives a copy of the state strategic plan in the center? d. How are the roles to accomplishing the plans objectives communicated to each

center employee and consultant? How?

Evaluation: Pass Demonstrates knowledge, monitoring and communication of strategic

objectives Fail Condition / Needs attention

Director’s Response: Reviewer’s Recommendation: 2) Describe how program resources are allocated to meet strategic objectives.

a. What are the centers primary objectives? b. Do they differ from primary state strategic objectives? If so, how? c. How were center objectives determined? d. Describe how an increase in program resources (i.e. increase in award or cash

match) would be utilized to further or expand program objectives.

Evaluation: Pass Demonstrates management Fail Condition

Director’s Response: Reviewer’s Recommendation:

23

3) Discuss the strategic planning process. a. Does the center participate in the annual strategic planning process? If so, who

participates? b. Does the current strategic planning process and action planning still have value? If

so, how? If not, what might it be changed? c. What should be the focus of the next strategic planning meeting? d. How should the meeting be conducted? Facilitated?

Evaluation:

Pass Demonstrates consensus and value of strategic planning Fail Condition

Director’s Response: Reviewer’s Recommendation:

CONSULTANT QUESTIONNAIRE

4) Determine if the consultant understands the role they have in accomplishing the mission and vision of the SBDC?

a. Have you participated in the state’s strategic planning process? b. Have you received a copy of the state strategic plan? c. Has the strategic plan been discussed or reviewed with you? d. Has your role in accomplishing the plans objectives been described to you? When? e. What is your primary driver (motivation) when determining the level of service you

offer a new client?

Evaluation: Pass Demonstrates communication and understanding Fail Condition / Needs attention

Reviewer’s Comments: Recommendation:

5) Determine the consultants approach to a new client engagement.

a. Describe an initial meeting with a new client. b. What is initially discussed? c. Do you go over the “Request for Services” form and disclaimers? d. Do you complete an engagement letter or agreement? e. Do you discuss client expectations (who will do what)?

Evaluation:

Pass Demonstrates adequate process Fail Condition

Reviewer’s Comments:

24

Recommendation: 6) Discuss a current high-hour, high-impact client project.

a. What is the scope of the project? b. How long have you been working on the project? c. When do you expect the project to be complete? d. What is the expected economic impact?

Evaluation:

Pass Demonstrates communication and understanding Fail Condition

Reviewer’s Comments: Recommendation: