2010 RBC USA Benefits Overview - experiencerbc-cs.com · Print a copy of the beneficiary...

46

2010 RBC USA Benefits Overview Your Options —Your Choice New Employee/Newly Eligible

Transcript of 2010 RBC USA Benefits Overview - experiencerbc-cs.com · Print a copy of the beneficiary...

2010 RBC USABenefits Overview

Your Options —Your ChoiceNew Employee/Newly Eligible

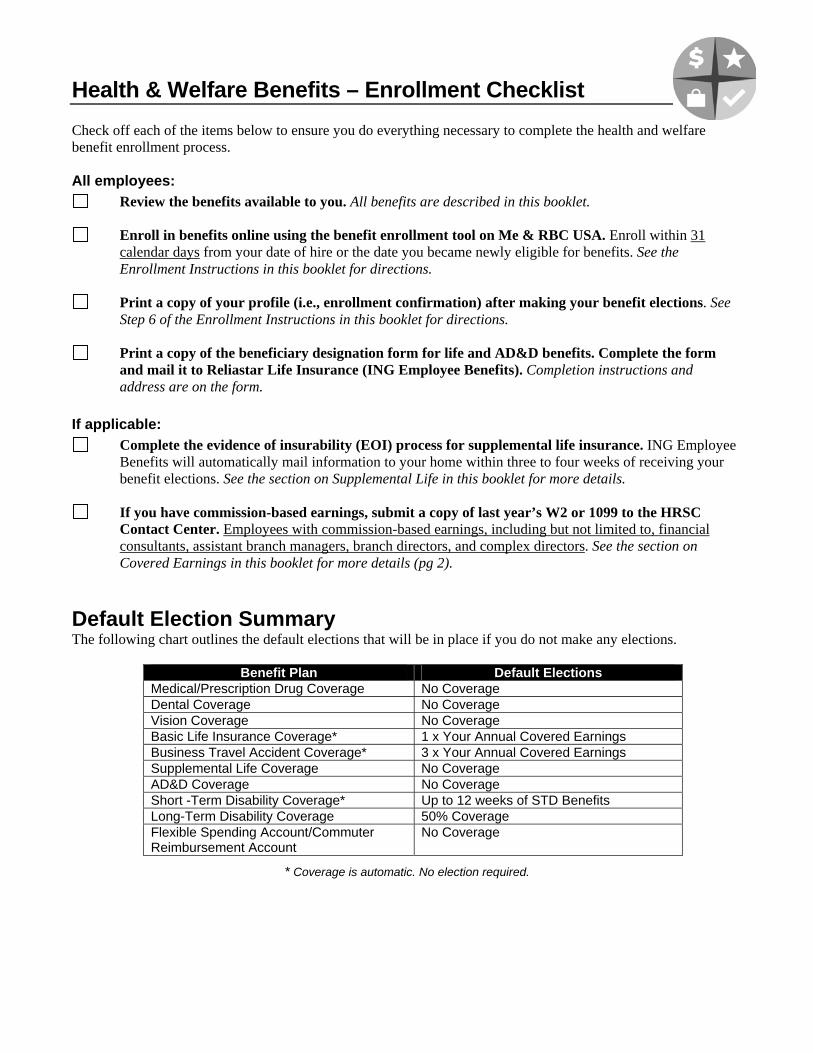

Health & Welfare Benefits – Enrollment Checklist Check off each of the items below to ensure you do everything necessary to complete the health and welfare benefit enrollment process. All employees:

Review the benefits available to you. All benefits are described in this booklet.

Enroll in benefits online using the benefit enrollment tool on Me & RBC USA. Enroll within 31 calendar days from your date of hire or the date you became newly eligible for benefits. See the Enrollment Instructions in this booklet for directions.

Print a copy of your profile (i.e., enrollment confirmation) after making your benefit elections. See Step 6 of the Enrollment Instructions in this booklet for directions.

Print a copy of the beneficiary designation form for life and AD&D benefits. Complete the form and mail it to Reliastar Life Insurance (ING Employee Benefits). Completion instructions and address are on the form.

If applicable:

Complete the evidence of insurability (EOI) process for supplemental life insurance. ING Employee Benefits will automatically mail information to your home within three to four weeks of receiving your benefit elections. See the section on Supplemental Life in this booklet for more details.

If you have commission-based earnings, submit a copy of last year’s W2 or 1099 to the HRSC Contact Center. Employees with commission-based earnings, including but not limited to, financial consultants, assistant branch managers, branch directors, and complex directors. See the section on Covered Earnings in this booklet for more details (pg 2).

Default Election Summary The following chart outlines the default elections that will be in place if you do not make any elections.

Benefit Plan Default Elections

Medical/Prescription Drug Coverage No Coverage Dental Coverage No Coverage Vision Coverage No Coverage Basic Life Insurance Coverage* 1 x Your Annual Covered Earnings Business Travel Accident Coverage* 3 x Your Annual Covered Earnings Supplemental Life Coverage No Coverage AD&D Coverage No Coverage Short -Term Disability Coverage* Up to 12 weeks of STD Benefits Long-Term Disability Coverage 50% Coverage Flexible Spending Account/Commuter Reimbursement Account

No Coverage

* Coverage is automatic. No election required.

Table of Contents

Introduction ................................................................................................................................................................1

Enrollment Instructions ..............................................................................................................................................4

Medical Program ........................................................................................................................................................5

Prescription Drug Coverage .....................................................................................................................................13

Dental Program.........................................................................................................................................................16

Vision Program.........................................................................................................................................................19

Life Insurance Programs...........................................................................................................................................21

Basic Life ....................................................................................................................................................21

Supplemental Life .......................................................................................................................................22

Accidental Death and Dismemberment.......................................................................................................24

Business Travel Accident ............................................................................................................................25

Short-Term Disability...............................................................................................................................................26

Long-Term Disability...............................................................................................................................................27

Flexible Spending Accounts ....................................................................................................................................29

Commuter Reimbursement Accounts.......................................................................................................................31

RBC EmployeeCare Program...................................................................................................................................33

Wellness ...................................................................................................................................................................33

Notice of Privacy Practices ......................................................................................................................................34

Medicare Part D Notice of Creditable Coverage......................................................................................................40

Special Enrollment Rights........................................................................................................................................41

Notice of Rights Under the Women’s Health and Cancer Rights Act ....................................................................42

Notice of Rights Under the Newborns’ and Mothers’ Health Protection Act .........................................................42 Questions?

Call RBC’s U.S. HRSC Contact Center at 1-866-HRSERVE (477-3783) or (612) 313-1112 in the Twin Cities.

CUSTOMER SERVICE CONTACT INFORMATION

Medical Coverage: Blue Cross Blue Shield of Minnesota Customer Service PO Box 64560 St. Paul, MN 55164 Telephone: 1-866-356-2422 or (651) 662-5677 www.bluecrossmn.com/rbc Find a Provider: www.bluecrossmn.com or 800-810-BLUE (1-800-810-2583) Prescription Drug Coverage: Medco Health Solutions, Inc. Member Services PO Box 2187 Lee’s Summit, MO 64063-2187 1-800-716-3219 www.medco.com Dental Coverage: Delta Dental of Minnesota Customer Service P.O. Box 59238 Minneapolis, MN 55459-0238 1-800-448-3815 www.deltadentalmn.org Find a Provider: www.deltadentalmn.org or 1-800-448-3815 Vision Coverage: Superior Vision Services Member Services 11101 White Rock, Suite #150 Rancho Cordova, CA 95670 1-800-507-3800 www.superiorvision.com Find a Provider: www.superiorvision.com or 1-800-448-3815 Short-Term Disability: CIGNA To file a claim: 1-800-36-CIGNA Life Insurance: Reliastar Life Insurance (ING Employee Benefits) & RBC Insurance For Beneficiary Questions: 1-800-955-7736 Flexible Spending Accounts and Commuter Reimbursement Accounts: SHPS, INC. (AKA Carewise Health) Customer Service 11405 Bluegrass Parkway Louisville, KY 40299 1-800-778-0040 Account Information: www.myshps.com RBC EmployeeCare Program (EAP): Ceridian 1-888-267-8126 www.lifeworks.com (User ID: rbc / Password: rbcus)

2010 RBC USA Benefits Enrollment – page 1 Prepared 10/09

2010 RBC USA Benefits Overview The benefits outlined in this booklet apply to employees working for RBC in the USA who are paid through the U.S. payroll. You may participate in the plans and programs outlined in this booklet if you are an active full-time employee, part-time (regularly scheduled to work 20 hours or more per week) employee, or an employee with commission-based earnings (including, but not limited to financial consultants, assistant branch managers, and branch directors).

YOUR OPTIONS, YOUR CHOICE This booklet was designed to be used in conjunction with the 2010 RBC USA Benefits Rate Sheet. Read these materials carefully to learn:

• Information on the programs available; • Coverage options; • Carrier contact information; and • Instructions for making your benefit selections via the online RBC FlexBenefits Enrollment System.

The following chart outlines the tax treatment for the premiums or contributions related to each health and welfare benefit program. For more information, go to the My Benefits section of Me & RBC USA for benefit program details, company policies, summary plan descriptions (SPDs), and certificates of insurance.

Benefit Programs Tax Treatment Medical Choice of 5 plan options Pre-Tax* Dental Choice of 2 plan options Pre-Tax* Vision Choice of 1 plan option Pre-Tax* Basic Life Company provided You will be taxed on coverage amounts

over $50,000 Supplemental Life Optional coverage for you, your spouse,

and your child(ren) After-Tax

Accidental Death & Dismemberment (AD&D)

Optional coverage for you or you and your family

Pre-Tax

Business Travel Accident Company provided N/A Flexible Spending Accounts (FSA)

• Health Care • Dependent Care

Pre-Tax

Commuter Reimbursement Accounts (CRA)

• Mass Transit • Parking

Pre-Tax

Short-Term Disability Company provided N/A Long-Term Disability Choice of 2 plan options • Basic Plan – You will be taxed on the

premiums paid by RBC • Premium Plan – After-Tax

* See the Eligible Dependents section of this booklet for more information about the tax treatment for coverage of Domestic Partners.

Benefit Effective Date With the exception of FSA, CRA, and supplemental life coverage amounts that exceed the Guaranteed Issue (GI), your elected benefits are effective on your first day of employment if you are a new employee, or the date you are reclassified to a benefits-eligible position if you are a newly-eligible employee.

• FSAs and CRAs - Effective on the first day of the pay period following the date you enroll. • Supplemental Life - If you elect to enroll, you and/or your dependent(s) will be asked by the insurer

(ING) to provide evidence of insurability (EOI), for amounts that exceed the Guaranteed Issue (GI) amount. Amounts requiring EOI are subject to insurance company approval. Therefore, elections above the GI are not effective until the insurance company approves coverage.

2010 RBC USA Benefits Enrollment – page 2 Prepared 10/09

Enrollment Deadline If you are a new employee or you are an existing employee newly eligible for benefits, you must enroll within 31 calendar days from your date of hire or the date you become eligible for benefits. If you do not enroll by the enrollment deadline, you will not be enrolled in benefits unless otherwise indicated in this booklet.

Plan Pricing See the 2010 RBC USA Benefits Rate Sheet for a full breakdown of your monthly benefit plan premiums. The amounts vary based on the coverage levels and plan choices you select.**

• If you are paid semi-monthly: Your share of the monthly benefit premiums will be split in half and deducted from each of your semi-monthly paychecks.

• If you are paid monthly: Your share of the monthly benefit premiums will be deducted in full from each paycheck.

Your first deduction will be retroactive to the effective date of your coverage and will include any amounts necessary to bring your deductions current.

RBC uses an income tier approach for the pricing of medical premiums. This approach, which is common within the financial services industry, is a way to keep benefits affordable for all levels of employees. The structure is based on your Covered Earnings (defined below) and includes the following income tiers:

• less than $50,000 • $50,000 to $150,000 • more than $150,000

**The company currently pays the majority of the cost for your medical and dental benefits. Note that actual company contributions are established by the Plan Administrator in its sole discretion. The projected company contribution may change based on plan experience.

Covered Earnings Some of the benefits available to you are based on your “Covered Earnings.” Covered Earnings are defined as your 401(k)-eligible earnings or current base salary (whichever is higher) for the prior 12-month period ending September 30. Earnings are prorated for employees who have worked with the company for less than 12 months. Your 401(k)-eligible earnings include base salary, overtime, short-term incentive and commissions. Your premiums and coverage amounts are automatically updated every year on January 1 in accordance with changes in your Covered Earnings.

Covered Earnings for new employees are determined as follows: • Salaried Employees: Your starting base salary (annualized). • Employees with Commission-Based Earnings (including, but not limited to financial consultants,

assistant branch managers, and branch directors): A default of $30,000 is used. Alternatively, you may provide proof of your prior calendar year earnings (e.g., W2 or 1099) to the HRSC Contact Center. This must be done within 31 calendar days of your hire date. This may increase your life and LTD coverage amounts and your medical, life, and LTD monthly premiums.

Dental Coverage Enrollment in the Dental Program is for two years. All employees are on the same two year enrollment cycle. As a new hire or someone who is newly eligible for benefits, be aware that the enrollment choice you make now cannot be changed until the fall of 2011 with changes effective January 1, 2012, unless you notify RBC’s U.S. HRSC Contact Center within 31 days of an eligible family status change.

2010 RBC USA Benefits Enrollment – page 3 Prepared 10/09

Mid-Year Changes (also referred to as Family Status Changes) With the exception of Commuter Reimbursement Accounts, which can be changed at any time, you can’t make mid-year changes to your benefit elections unless you experience a qualifying family status change that you report to RBC’s U.S. HRSC Contact Center within 31 days of the change. This timeframe is based on IRS regulations for Section 125 Cafeteria Plans. See below for examples of allowable family status changes:

• Marital status changes (marriage, divorce, etc.) • Change in employment status that affects eligibility (spouse gains/loses coverage) • Change in number of dependents (birth, adoption, death, etc.) • Change in dependent eligibility (child graduates from college, etc.)

Important facts to keep in mind with family status changes: • The benefit change you make must be consistent with the family status change. For example, if your

spouse loses medical coverage under their employer’s plan it would be consistent for you to add them to your RBC coverage, but it would not be consistent for you to drop your medical coverage.

• Not all RBC benefit plans recognize the same family status changes. Review the specific SPD for the benefit you want to change.

Eligible Dependents

Some of RBC’s benefit programs allow you to elect coverage on your eligible dependents. When enrolling them in coverage, it is your responsibility to ensure they meet the definition of an eligible dependent. Eligible dependents are broadly defined below. Please refer to each benefit program’s summary plan description for more details.

Dependent Broad Eligibility Definition Spouse Includes both legally married and common-law. Domestic Partner Includes both same and opposite gender.* Children Includes biological, step, and adopted. Eligible to age 19 or to

age 25 if a full-time student. Domestic Partner’s Children Eligible to age 19 or to age 25 if a full-time student.*

*Premiums for this coverage will be deducted from your pay on an after-tax basis. Additionally, RBC’s contributions towards this coverage are treated as taxable income to you.

Helpful Tips As you review this booklet, you will see that RBC offers a wide range of benefits. As you consider what’s best for you, remember:

• You must enroll within 31 days of your hire date. • If both you and your spouse are employees of RBC, you may be covered as either an employee or as a

dependent, but not both. Your eligible dependent children may be covered under either parent’s coverage, but not both.

• If you are rehired within 30 days, you will automatically be enrolled in the same benefit plans and coverage levels you had prior to leaving RBC. If you are rehired more than 30 days after your separation date, you are eligible to make new elections.

Every effort has been made to accurately describe the benefits outlined in this booklet. RBC’s benefit plans are governed by the summary plan descriptions (SPD), carrier contracts and company policies. In the event of a discrepancy between this document and the SPD, contracts or policies, the language in the SPD, contracts or policies will govern. RBC reserves the unilateral right to change, amend or terminate the separate contracts, coverage, and/or policy documents at any time and without prior notice. This right to amend or terminate applies to all current and former employees, including disabled employees, spouses/domestic partners, and dependents.

2010 RBC USA Benefits Enrollment – page 4 Prepared 10/09

ENROLLMENT INSTRUCTIONS Follow the instructions below to make your benefit elections on the RBC USA FlexBenefits Enrollment System. The enrollment system is only accessible from your office computer and cannot be accessed from home. U.S. Insurance agency employees must use their VPN to access the Me & RBC USA site.

I. When you are ready to make your enrollment elections: • Go to Me & RBC USA at http://rbcnet.fg.rbc.com/meandrbcusa. • Under “Employee Toolkit,” select “Benefits Enrollment” on the left side of the page. • Enter your User ID and password (what you use to log in to your work computer every day). • Under “Employee Toolkit,” select “FlexBenefits.”

II. From the homepage of the RBC USA FlexBenefits Enrollment System:

• Review the information and select the “Let’s Get Started” button. • Step 1: Getting Started – Review the information listed and make any necessary updates. This is

the area where you would provide dependent information. When finished, select the “Next Step” button at the bottom of the page.

• Step 2: Enrollment and Eligible Family Status Change Events – Select the “New Employee and Newly Eligible for Benefits” link under the New Enrollment section.

• Step 3: RBC USA FlexBenefits Enrollment System – Make your selections and select the “Next Step” button when you are done.

• Step 4: Assign Dependent(s) – Check the appropriate boxes to assign medical, dental, and vision plan coverage for your dependent(s). If no assignment is required, proceed to Step 5. When finished, select the “Next Step” button to continue.

• Step 5: Review and Submit – Review your elections. Select the “Previous Step” button if you would like to go back and change your elections. Select the “Submit” button when you are done.

• Step 6: Confirm and Print – Print and save a copy of your profile for your records by selecting the “To View or to Print the Current Profile” button.

• Step 7: Print and complete the beneficiary designation form for life and accidental death and dismemberment (AD&D) benefits and mail it to ING Employee Benefits. Complete this form even if you are not electing supplemental life or AD&D coverage, as it also pertains to the Basic Life Insurance plan provided by the company.

You may view your benefits profile anytime.

• Log back into the RBC USA FlexBenefits Enrollment System. • Click the “Let’s Get Started” button. • On step 1: Getting Started – scroll down to the bottom of the page, and click the button “To

View or To Print the Current Profile.” If you see errors, you need to contact the HRSC Contact Center prior to your benefits enrollment deadline (31 calendar days from your hire date). Please note: You will not receive a hard-copy confirmation/profile of your enrollment; you must print your own copy for your records. See Step 6 above for instructions.

Tip: Clicking on the question mark icon provides general information and does not take you to the enrollment system.

2010 RBC USA Benefits Enrollment – page 5 Prepared 10/09

MEDICAL PROGRAM RBC U.S.-based employees may choose from five medical plan options. All options are administered by BlueCross BlueShield of Minnesota. See the plan highlights chart on the following page for more information on each of the options. Medical Plan Options

• EPO

• Premium PPO

• Basic PPO

• Indemnity Plan

• High Indemnity Plan

Plan Pricing See the 2010 RBC USA Benefits Rate Sheet for monthly contribution amounts.**

**The company currently pays the majority of the cost for your medical and dental benefits. Note that actual company contributions are established by the Plan Administrator in its sole discretion. The projected company contribution may change based on plan experience.

Default Election If you do not make a medical plan election you will not be enrolled.

Selecting the Right Medical Plan for You The company’s medical plan is designed to give you maximum flexibility. There’s no single plan that’s right for everyone. That’s why we offer five choices—so you can elect the plan that’s right for you. This section provides a detailed plan comparison chart for you to use when making your selection. Here are a few things to keep in mind while reviewing the chart:

• All the plans cover the same services but may do so at different levels.

• None of the plans exclude pre-existing conditions.

• All plans have the same, combined lifetime coverage maximum.

When comparing plans, you may want to consider:

• Your monthly premium cost (refer to your 2010 RBC USA Benefits Rate Sheet; costs vary by income tier);

• Deductibles;

• Co-pay and co-insurance amounts;

• The network of doctors/hospitals that participate;

• Out-of-network coverage options; and

• Out-of-pocket maximums.

Health Care Cost Calculator The Health Care Cost Calculator is an online tool designed to help you estimate your health care costs for the year and to select the medical plan that best meets your needs. You can use this tool to compare the five different medical plan options and choose the one that best meets your needs. The calculator is available on the BlueCross BlueShield Web site at www.bluecrossmn.com/rbc.

2010 RBC USA Benefits Enrollment – page 6 Prepared 10/09

Medical Plan Highlights This table provides an overview of coverage under the five medical plan options. More details are available in the summary plan description (SPD). Prescription drug coverage is provided by Medco and is outlined on page 13.

Plan Feature EPO Premium PPO Basic PPO Indemnity High Indemnity Network Name Bluecard PPO Bluecard PPO Bluecard PPO Bluecard Traditional Bluecard Traditional Plan deductible In-network:

• Single-$200 • Family-$400

Out-of-network: No Coverage

In-network: • Single-$300 • Family-$900

Out-of-network: • Single-$600 • Family-$1,800

In-network: • Single-$600 • Family-$1,800

Out-of-network: • Single-$1,200 • Family-$3,600

Single-$400 Family-$1200

Single-$200 Family-$400

Out-of-pocket maximum (co-pays do not apply except for the inpatient hospital admission co-pay)

In-network: • Single-$800 • Family-$2,400

Out-of-network: No Coverage

In-network: • Single-$1,100 • Family-$3,300

Out-of-network: • Single-$2,200 • Family-$6,600

In-network: • Single-$1,600 • Family-$4,800

Out-of-network: • Single-$3,200 • Family-$9,600

Single: $2,000 Family: $6,000

Not applicable

In-network benefits

In-network: Covered at 100% after deductible is satisfied (unless otherwise stated)

In-network: Covered at 90% after deductible is satisfied (unless otherwise stated)

In-network: Covered at 85% after deductible is satisfied (unless otherwise stated)

Not applicable Not applicable

Out-of-network benefits

Out-of-network: No out-of-network coverage available except emergencies

Out-of-network: Covered at 70% after deductible is satisfied (unless otherwise stated)

Out-of-network: Covered at 60% after deductible is satisfied (unless otherwise stated)

Covered at 80% after deductible is satisfied (unless otherwise stated)

Covered at 100% after deductible is satisfied (unless otherwise stated)

Responsibility for pre-certifying hospital stays

Member Member Member Member Member

Charges above reasonable & customary

Provider responsibility

In-network: Provider responsibility

Out-of-network: Member responsibility

In-network: Provider responsibility

Out-of-network: Member responsibility

Member responsibility (except when using the BlueCard Traditional Network providers)

Member responsibility (except when using the BlueCard Traditional Network providers)

Primary care referrals for specialists

No referral required (some services require pre-authorization)

No referral required (some services require pre-authorization)

No referral required (some services require pre-authorization)

No referral required (some services require pre-authorization)

No referral required (some services require pre-authorization)

Lifetime maximum (in- and out-of-network benefits and all plans combined)

$3 million $3 million $3 million $3 million $3 million

2010 RBC USA Benefits Enrollment – page 7 Prepared 10/09

Plan Feature EPO Premium PPO Basic PPO Indemnity High Indemnity

Physician Services Office visits (illness / injury)

In-network: $25 co-pay (covers all services provided in physician's office and deductible does not apply)

In-network: $25 co-pay (covers all services provided in physician's office and deductible does not apply)

In-network: $30 co-pay (covers all services provided in physician's office and deductible does not apply)

80% after deductible 100% after deductible

Physician hospital services (some procedures require pre-authorization)

In-network: 100% after $350 per admission co-pay, and deductible

In-network: 90% after deductible

In-network: 85% after deductible

80% after deductible 100% after deductible

Preventive care and well-child care (Covers routine physical exam, one routine vision screen per year, one routine hearing screen per year)

In-network: 100% coverage (deductible does not apply)

In-network: 100% coverage (deductible does not apply)

In-network: 100% coverage (deductible does not apply)

100% coverage (deductible does not apply)

100% coverage (deductible does not apply)

Allergy serum, allergy injections and injectable drugs

In-network: 100% (unless an office visit is charged; if so, a $25 co-pay applies; deductible does not apply)

In-network: 100% (unless an office visit is charged; if so, a $25 co-pay applies; deductible does not apply)

In-network: 100% (unless an office visit is charged; if so, a $30 co-pay applies; deductible does not apply)

80% after deductible 100% after deductible

Lab and x-ray (Provided in physician's office)

In-network: 100% after office visit co-pay of $25 (deductible does not apply)

In-network: 100% after office visit co-pay of $25 (deductible does not apply)

In-network: 100% after office visit co-pay of $30 (deductible does not apply)

80% after deductible 100% after deductible

Lab and x-ray (Provided outside physician's office)

In-network: 100% after deductible

In-network: 90% after deductible

In-network: 85% after deductible

80% after deductible 100% after deductible

2010 RBC USA Benefits Enrollment – page 8 Prepared 10/09

Plan Feature EPO Premium PPO Basic PPO Indemnity High Indemnity

Hospital Services Inpatient coverage

In-network: $350 per admission co-pay, then 100% after deductible

In-network: 90% after deductible

In-network: 85% after deductible

80% after deductible 100% after deductible

Hospital pre-certification requirement (Applies to all inpatient hospital stays)

In-network: Provider responsibility

Out-of-network: No out-of- network coverage

In-network: Provider responsibility

Out-of-network: Member responsibility ($250 penalty if no pre-certification)

In-network: Provider responsibility

Out-of-network: Member responsibility ($250 penalty if no pre-certification)

In-network: Provider responsibility

Out-of-network: Member responsibility ($250 penalty if no pre-certification)

In-network: Provider responsibility

Out-of-network: Member responsibility ($250 penalty if no pre-certification)

Outpatient coverage

In-network: 100% after deductible

In-network: 90% after deductible

In-network: 85% after deductible

80% after deductible

100% after deductible

Emergency care (Facility charge co-pay waived if admitted within 24 hours)

In-network: Facility charge - $100 co-pay; 100% for other services related to the emergency room visit, (not subject to deductible)

Out-of-network: Same as in-network

In-network: Facility charge - $100 co-pay; 90% for other services related to the emergency room visit (not subject to deductible)

Out-of-network: Same as in-network

In-network: Facility charge - $100 co-pay; 85% for other services related to the emergency room visit (not subject to deductible)

Out-of-network: Same as in-network

80% (deductible does not apply)

100% (deductible does not apply)

Ambulance 100%(deductible does not apply)

90% (deductible does not apply)

85% (deductible does not apply)

80% (deductible does not apply)

100% (deductible does not apply)

Medical equipment & supplies (foot orthotics not covered)

In-network: 90%, after deductible

In-network: 90% after deductible

In-network: 85% after deductible

80% after deductible 100% after deductible

Urgent care In-network: $25 co-pay (if billed as physician office visit); $100 co-pay (if billed as a hospital emergency room visit); deductible does not apply)

In-network: $25 co-pay (if billed as physician office visit); $100 co-pay (if billed as a hospital emergency room visit); deductible does not apply

In-network: $30 co-pay (if billed as physician office visit); $100 co-pay (if billed as a hospital emergency room visit); deductible does not apply

80% after deductible 100% after deductible

2010 RBC USA Benefits Enrollment – page 9 Prepared 10/09

Plan Feature EPO Premium PPO Basic PPO Indemnity High Indemnity

Hospital Services Skilled nursing facility (Coverage limited to maximum of 120 days per person per calendar year)

In-network: 100% after deductible

In-network: 90% after deductible

In-network: 85% after deductible

80% after deductible 100% after deductible

Organ and bone marrow transplant (Requires involvement of care management)

Centers of Excellence: 100% of the Transplant Payment Allowance (includes benefits for travel, meals and lodging). Participating BCBS Provider, but not a Center of Excellence: $10,000 co-payment then paid at the in-network hospital benefit level (does not include benefits for travel, meals and lodging). Non-Participating Provider: No coverage.

Maternity Maternity In-network:

Initial office visit-$25 co-pay; (deductible does not apply); All other outpatient services - 100% after deductible

Inpatient: see “Inpatient coverage”

In-network: Initial office visit -$25 co-pay (deductible does not apply); All other outpatient services - 90% after deductible

Inpatient: see “Inpatient coverage”

In-network: Initial office visit -$30 co-pay (deductible does not apply); All other services -85% after deductible

Inpatient: see “Inpatient coverage”

80% after deductible 100% after deductible

Infertility treatment (Lifetime benefit maximum of $10,000 for all options combined)

In-network: Office visit - $25 co-pay (deductible does not apply); all other services 100%, after deductible

In-network: Office visit - $25 co-pay (deductible does not apply); all other services 90% after deductible

In-network: Office visit - $30 co-pay (deductible does not apply); all other services 85% after deductible

80% after deductible 100% after deductible

Home Care Home health care (Annual maximum – 50 visits per person)

In-network: 100% after deductible

In-network: 90% after deductible

In-network: 85% after deductible

80% after deductible 100% after deductible

Home infusion therapy

In-network: 100% after deductible

Out-of-network: No coverage

In-network: 90% after deductible

Out-of-network: Same as in-network

In-network: 85% after deductible

Out-of-network: Same as in-network

80% after deductible 100% after deductible

2010 RBC USA Benefits Enrollment – page 10 Prepared 10/09

Plan Feature EPO Premium PPO Basic PPO Indemnity High Indemnity

Mental Health/Chemical Dependency Mental health care

Outpatient services: In-network professional charges - $25 co-pay (deductible does not apply); 100% for other charges after deductible

Inpatient services: In-network - $350 per admission co-pay; then 100% after deductible

Outpatient services: In-network professional charges - $25 co-pay (deductible does not apply); 90% for other charges after deductible

Inpatient services: In-network - 90% after deductible

Outpatient services: In-network professional charges - $30 co-pay (deductible does not apply); 85% for other charges after deductible

Inpatient services: In-network - 85% after deductible

80% after deductible

100% after deductible

Chemical dependency

Outpatient services: In-network professional charges - $25 co-pay (deductible does not apply); 100% for other charges after deductible

Inpatient services: In-network - $350 per admission co-pay; then 100% after deductible

Outpatient services: In-network professional charges - $25 co-pay (deductible does not apply); 90% for other charges

Inpatient services: In-network - 90% after deductible

Outpatient services: In-network professional charges - $30 co-pay (deductible does not apply); 85% for other charges after deductible

Inpatient services: In-network - 85% after deductible

80% after deductible

100% after deductible

Other Chiropractic coverage (Annual maximum of $1,500 per person)

In-network: Office visits and manipulations -$25 co-pay (deductible does not apply); other services (x-rays, therapies, etc.) -100% after deductible

In-network: Office visits and manipulations -$25 co-pay (deductible does not apply); other services (x-rays, therapies, etc.) -90% after deductible

In-network: Office visits and manipulations -$30 co-pay (deductible does not apply); other services (x-rays, therapies, etc.) -85% after deductible

80% after deductible

100% after deductible

Hospice care In-network: 100% (deductible does not apply)

Out-of-network: Same as in-network

In-network: 90% (deductible does not apply)

Out-of-network: Same as in-network

In-network: 85% (deductible does not apply)

Out-of-network: Same as in-network

80% after deductible

100% after deductible

Physical, occupational, speech therapy

In-network: 100% after deductible

In-network: 90% after deductible

In-network: 85% after deductible

80% after deductible

100% after deductible

2010 RBC USA Benefits Enrollment – page 11 Prepared 10/09

Employee Resources Contacting BlueCross BlueShield Contact BlueCross BlueShield customer service by calling 1-866-356-2422 or at www.bluecrossmn.com/rbc.

Finding a Network Provider To view providers who participate in the BCBS networks:

• Check online by going to www.bluecrossmn.com. Once there, locate “Quick Links” and click on “find a doctor.” Scroll down to “National BlueCard” and click on “search the National BlueCard network.” Read the disclaimer and click “OK.” Click on the blue “Guest Tab” and choose a “Product.” Select “PPO” for the BlueCard PPO Network (for the EPO, Premium PPO, or Basic PPO plans). Select “Traditional” for providers in the BlueCard Traditional Network (for the Indemnity or High Indemnity Plan).

• Call BlueCross BlueShield at 1-800-810-BLUE (1-800-810-2583). ID Cards When you enroll, ID cards will automatically be mailed to you for each covered family member. Additional cards are available by calling customer service or going online at www.bluecrossmn.com/rbc. Present your BCBS ID card when you visit a provider. 24-Hour Nurse Advice Line The 24-Hour Nurse Advice Line is available through BlueCross BlueShield. If you enroll in one of the RBC medical plans, you automatically have this feature available to you. The 24-Hour Nurse Advice Line provides professional medical advice any time day or night and gives you another resource to help you make more informed health care decisions. Telephone advice and the online “symptom advisor” can help you decide where to go for care. With the 24-Hour Nurse Advice Line, you will benefit from:

• 24-hour access to safe, professional health information and advice • Useful online tools to help you make better health care decisions

Care Away From Home In an emergency, call 911 or go to the nearest emergency facility. Then, contact BlueCross BlueShield as soon as possible if you are admitted to the hospital. For other care, call 1-800-810-BLUE (1-800-810-2583) to find a network provider near you. If you plan to travel outside the country, and would like more information on coverage or providers, call BlueCross BlueShield customer service toll-free at 1-866-356-2422. Submitting Claims

• If your provider participates in the BlueCard PPO or Traditional BCBS networks, you do not need to fill out claim forms. Your providers will do it for you.

• If your provider is not a network participant, you are responsible for filing your own claims. If needed, you can request a claim form from BlueCross BlueShield customer service. Complete the form, include any itemized bills that show the diagnosis, services received and dates of service, and submit this information to the address listed on the form.

2010 RBC USA Benefits Enrollment – page 12 Prepared 10/09

Self-Serve Web Site Once you are enrolled, to get the most out of your medical plan, visit BlueCross BlueShield’s self-serve Web site at www.bluecrossmn.com/rbc. Once you register, you will be able to access information including:

• Check claim status; • Learn about your benefits; • View explanation of benefits; • View member information; • Order ID cards; • Find a doctor; and • Contact customer service.

If You Are Covered Under Another Plan – Maintenance of Benefits Today, few plans pay additional benefits if you receive payment from another insurance plan. The only time RBC’s plan pays additional benefits is when the other plan pays lower benefits. In that case, our plan will only pay the difference between what it would normally pay, less any amounts paid by the other plan. For more information on maintenance of benefits (MOB), see the RBC-USA Medical Program SPD available on Me & RBC USA. Understand Your Coverage The single best thing you can do to ensure you get the most out of your plans is to understand the details of your coverage. The plan’s SPD provides complete details and is available on Me & RBC USA. You also can call BlueCross BlueShield customer service toll free at 1-866-356-2422 for more information.

2010 RBC USA Benefits Enrollment – page 13 Prepared 10/09

PRESCRIPTION DRUG COVERAGE This coverage is automatically included with each BlueCross BlueShield medical plan option. The cost is included in your medical premium. You will not receive this benefit unless you elect coverage under the Medical Program. Medical deductibles and out-of-pocket limits do not apply to the prescription drug plan. Prescription drug coverage is provided by Medco, who offers several features to help you control the increasing costs of prescriptions. When filling a prescription, you can choose from a pharmacy in or out of the Medco network. If you choose an “out-of-network” pharmacy, your costs will be higher. For prescriptions taken on a long-term basis—defined as 90 days or more—you are encouraged to use Medco’s mail order service.

Co-Payments Generally, your co-payment is what you pay when you pick up your prescription at a retail pharmacy or place a mail order request. Your co-payment will vary depending on whether a generic versus brand-name drug is requested, whether the prescription is for a preferred or a non-preferred drug, and whether you use a participating pharmacy, non-participating pharmacy or the mail order program. See the table below for details.

Prescription Drug Plan Highlights

Prescription Participating Retail

Pharmacy Non-Participating Retail

Pharmacy Mail Order Pharmacy

When to Use It is recommended that you use this option when purchasing medications taken on a short-term or one-time basis.

It is recommended that you use this option when there is not a network pharmacy available and you are purchasing medications taken on a short-term or one-time basis.

Ideal for long-term needs such as asthma, diabetes, cholesterol, hypertension, arthritis, and birth control. This is the best value. You get 3 months of medication for only 2 ½ months of co-payments.

Generic Drugs $10 co-pay* 50% coinsurance $25 co-pay Preferred Brand-Name Drugs (Listed on the Medco formulary)

$25 co-pay* 50% coinsurance $62.50 co-pay

Non-Preferred Brand-Name Drugs (Not listed on the Medco formulary)

$40 co-pay* 50% coinsurance $100 co-pay

Preferred Brand-Name Drugs (when generic is available)

$25 co-pay* + (brand drug cost, less generic drug cost)

50% coinsurance $62.50 co-pay + (brand drug cost, less generic drug cost)

Non-Preferred Brand-Name Drugs (when generic is available)

$40 co-pay* + (brand drug cost, less generic drug cost)

50% coinsurance $100 co-pay + (brand drug cost, less generic drug cost)

Non-Sedating Antihistamines such as Clarinex, Allegra, Allegra D and Zyrtec

50% coinsurance 50% coinsurance 50% coinsurance

Supply (per co-pay) Up to 30 days Up to 30 days Up to 90 days Claim Filing Not required Required. You pay the full

retail cost when you fill your prescription and submit a claim to Medco for reimbursement.

Not required

* A double co-payment will be charged for long-term medications purchased at retail pharmacies. You can fill a long-term prescription at a participating retail pharmacy 3 times before the double co-pay applies.

2010 RBC USA Benefits Enrollment – page 14 Prepared 10/09

Your prescription drug coverage provides access to approximately 60,000 independently operated and chain pharmacies, including but not limited to, CVS Pharmacy, Eckerd Drugs, Kmart, Wal-Mart, Walgreens and Target, and a convenient prescription-by-mail service for prescriptions you take on a long-term basis.

Making the Most of Your Pharmacy Plan You can get the most out of Medco’s pharmacy benefits by using:

• mail order for long-term medications. • a participating retail pharmacy for one-time or short-term prescriptions. • generic rather than brand-name prescription drugs. • preferred rather than non-preferred prescription drugs.

Generics Every generic drug must undergo the same U.S. Food and Drug Administration (FDA) review as its equivalent branded drug. According to the FDA “a generic drug is a copy that is the same as a brand-name drug in dosage, safety, strength, how it is taken, quality, performance, and intended use.” The color, shape and size of these medications may be different from that used in their brand-name counterparts, but the active ingredients are the same.

Employees who purchase a generic drug instead of a brand-name equivalent maximize their pharmacy benefit. You may want to talk to your doctor about generic drug options where appropriate. If you or your doctor request a brand-name drug when a generic is available and effective in the treatment of your condition, you must pay the price difference in addition to the brand-name drug co-payment.

For example, if a generic costs $46, and the equivalent preferred brand name costs $78, you will pay $57 for the brand name, as the following example shows:

$ 78 cost of brand-name medication - 46 cost of generic medication + 25 co-payment for preferred brand-name medication $ 57 employee’s responsibility

You would only pay a $10 co-payment for the generic. Advantages of Mail Service For Maintenance Medications

• Cost savings: Receive a 90-day supply of most maintenance medications, requiring fewer refills and fewer co-pays, thus saving you money. You can fill long-term prescriptions at retail pharmacies; however, your cost will be significantly higher as shown in the table below.

90-Day Supply of Long-Term Medication Mail Retail Pharmacy

Generic Co-Pay $25 $60 Preferred Brand-Name Co-Pay $62.50 $150 Non-Preferred Brand-Name Co-Pay $100 $240

Note: The amounts above include the double co-pay charged for long-term medications purchased at a participating retail pharmacy (you can fill a long-term prescription at a participating retail pharmacy three times before you have to pay the double co-payment).

• Quality and safety: Your prescription is prepared by a professional registered pharmacist and shipped in an unmarked, weather-resistant package.

• Convenience: Convenient home delivery. Standard delivery through U.S. Postal Service is free and you can check the status of your order at www.medco.com.

2010 RBC USA Benefits Enrollment – page 15 Prepared 10/09

Transferring Prescriptions to Mail Order To transfer a prescription to the mail order program, call your doctor and request a new prescription. The prescription should be written for a 90-day supply with refills for up to a one-year supply. Complete a mail order request form (available from Medco customer service) and mail both back to Medco. Your initial order will be filled and mailed to you within approximately 14 days. Subsequent refills may be ordered by calling Medco or contacting them online. You may also have your doctor fax your prescriptions. Ask your doctor to call 1-888-327-9791 for faxing instructions.

If you need to start taking your maintenance medication right away, have your physician write two prescriptions. Fill one prescription immediately at a participating retail pharmacy. The second prescription should be written for a 90-day supply with refills for up to one year. Submit it to the mail service program. Encourage your physician to write your prescription to allow for generic substitution. This will help minimize your cost. Formulary Changes Medco continuously reviews the medications included on its formulary (list of preferred drugs). The medications covered include generic and brand-name drugs. If your medication is not on the formulary, you will be charged the non-preferred, brand-name drug co-payment. To save money, check with your physician to see if a formulary medication would work for you.

Once you are enrolled in the prescription drug benefits, you can locate the most current formulary by visiting www.medco.com, selecting the “Learn about formularies” section, entering the medication name (up to four letters) and searching for coverage. Until you are enrolled, or if you prefer to call, contact Medco Member Services at 1-800-716-3219 for formulary information.

Employee Resources Contacting Medco Contact Medco by calling member services at 1-800-716-3219 or www.medco.com. ID Cards When you enroll, you will receive a prescription ID card from Medco. Additional cards may be ordered by contacting Medco’s Member Services department at 1-800-716-3219. ID cards should be presented when purchasing prescriptions at participating retail pharmacies. Submitting Claims to Medco (Out of Network Only) When sending a claim to Medco, be sure to include:

• A completed claim form (available on the Medco Web site or through member services); • A receipt for your prescription; • The National Drug Code (NDC) number for your prescription from the pharmacist; and • The 7-digit NCPDP number of the pharmacy.

2010 RBC USA Benefits Enrollment – page 16 Prepared 10/09

DENTAL PROGRAM Employees have two dental options to choose from. Both options are administered by Delta Dental of MN.

Every Other Year Enrollment/Change Window Enrollment in the Dental Program is for two years. All employees are on the same two-year enrollment cycle. The next opportunity to make changes to your dental coverage will be the fall of 2011 with changes effective January 1, 2012, unless you notify RBC’s U.S. HRSC Contact Center within 31 days of an eligible family status change. Dental Plan Options

• Basic Dental • Premium Dental

Plan Pricing See the 2010 RBC USA Benefits Rate Sheet for monthly contribution amounts.** **The company currently pays the majority of the cost for your medical and dental benefits. Note that actual company contributions are established by the Plan Administrator in its sole discretion. The projected company contribution may change based on plan experience. Default Election If you do not make a dental plan election, you will not be enrolled.

Selecting the Right Dental Plan for You Both plans include complete coverage of preventive services, and once you pay your annual deductible, both cover most basic services (except for prosthetic repairs, etc.) at 80 percent of allowable levels. The Premium Option goes one step further. It includes a 50 percent benefit for major services after the deductible has been satisfied, and it also covers orthodontics. In making your choice, you’ll need to balance the cost with the level of benefits you anticipate receiving under the plan. See the plan highlights table for more information on each of the options.

2010 RBC USA Benefits Enrollment – page 17 Prepared 10/09

Dental Plan Highlights Plan Feature Premium Plan Basic Plan

Network Delta Dental Premier Annual Plan deductible $50 per person; $150 per family $50 per person; $150 per family Annual benefit maximum $1,500 per person (excluding

orthodontic benefits) $1,500 per person (excluding orthodontic benefits)

Lifetime maximum orthodontic benefit $1,500 per person Not covered Preventive and Diagnostic Services

Oral Exams (Two per calendar year, includes emergency and specialist exams)

100%, no deductible

100%, no deductible

Prophylaxis (cleaning) (Two per calendar year, includes periodontal maintenance)

100%, no deductible

100%, no deductible

Bitewing x-rays (Two sets per calendar year)

100%, no deductible

100%, no deductible

Full mouth x-rays (Once every 36 months, includes panoramic)

100%, no deductible

100%, no deductible

Fluoride treatment (Two times per calendar year, under age 19)

100%, no deductible

100%, no deductible

Sealants (Permanent molars only, once per lifetime, under age 16)

100%, no deductible

100%, no deductible

Space Maintainers (For extracted primary, posterior teeth only, once per lifetime, for children under age 17)

100%, no deductible

100%, no deductible

Basic Services Restorations (fillings) -- Amalgam -- Resin, front teeth -- Resin, back teeth (Two year replacement limitation)

80% after deductible 80% after deductible 50% after deductible

80% after deductible 80% after deductible 50% after deductible

Endodontics (root canal therapy) 80% after deductible 80% after deductible Periodontics (Non-surgical at two-year intervals; surgical at three-year intervals)

80% after deductible 80% after deductible

Oral surgery (simple and surgical extractions; excision of lesions and bone tissue; and removal of tumors, cysts and neoplasms)

80% after deductible 80% after deductible

Prosthetic repairs and adjustments (bridge, dentures and partial dentures; adjustments, excluding first six months; repairs; relining/rebasing limited to once every six months)

80% after deductible Not covered

Major Services (Premium Plan only) Crowns (includes metallic onlays, crown build-ups, post/cores; Five year replacement limitation)

50% after deductible Not covered

Crown repair (including re-cementing)

50% after deductible Not covered

Bridges, dentures and partial dentures (Five year replacement limitation)

50% after deductible Not covered

Occlusal guards (covered once per lifetime) 50% after deductible Not covered Occlusal adjustments 50% after deductible Not covered

Orthodontics (Premium Plan only) Orthodontic services (adult and child) 50%, no deductible Not covered Appliance therapy 50%, no deductible Not covered Lifetime maximum orthodontic benefit $1,500 per person (does not apply

to annual benefit maximum) Not covered

2010 RBC USA Benefits Enrollment – page 18 Prepared 10/09

Employee Resources Choosing a Network Provider Both plans allow you to use any dentist you choose. Benefit levels are the same whether you choose a dentist who is part of the Delta Dental network or not. However, there are advantages to using an in-network dentist. Both coverage options use Delta Dental’s PPO and Premier Networks.

When you use a dentist in either the PPO or Premier Network, you can eliminate filling out claim forms. These dentists file your claims for you. You may also save money. That’s because these dentists agree to limit their fees to the amount allowed by Delta Dental. Using a dentist in the Delta Dental PPO Network may save you even more money.

To locate providers who participate in the Delta Dental PPO or Premier Networks, you can:

• Check online by going to www.deltadental.com. Once there, click on “Looking for a Dentist?” Select “Delta Dental PPO or Delta Dental Premier” under 1. Product Selection and follow the prompts.

• Call Delta Dental’s customer service at 1-800-448-3815. Out-Of-Network Dentists Dentists who do not participate in the Delta Dental network may charge you more than the amount that Delta allows for that service. You will be responsible for charges over and above Delta’s allowed amount. Out-of-network dentists aren’t required to submit claims on your behalf. If your dentist doesn’t, you’ll need to request reimbursement directly from Delta Dental by completing and filing a claim form.

Claim forms are available from Delta Dental customer service or at www.deltadentalmn.org. From the home page, click on Subscribers > Forms and Publications > Dental Claim Forms. You’ll need to send your completed form to:

Delta Dental of Minnesota P.O. Box 59238 Minneapolis, MN 55459-0238

After processing your claim, Delta Dental will reimburse you directly. When your dentist bills you for services, you are responsible for paying your bill.

ID Cards If you enroll, you will receive a Delta Dental ID card, which you will need to present to your dentist whenever you receive care. Additional cards may be ordered by contacting Delta Dental’s customer service number at 1-800-448-3815 or online at www.deltadentalmn.org.

Self-Serve Web Site To get the most out of your dental plan, visit Delta Dental’s self-service web site at www.deltadentalmn.org. Once you register on the web site, you will be able to quickly access information about your dental plan, including:

• How to find a network dentist; • The ability to view Explanation of Benefits; • Verify benefits and eligibility; • Print educational material; and • Obtain additional ID cards.

If You Are Covered Under Another Plan – Maintenance of Benefits Today, few plans pay additional benefits if you receive payment from another insurance plan. The only time the RBC plan pays additional benefits is when the other plan pays lower benefits. In that case, this plan will only pay the difference between what it would normally pay, less any amounts paid by the other plan. For more information on maintenance of benefits (MOB), see the RBC-USA Dental SPD available on the Me & RBC USA Web site.

2010 RBC USA Benefits Enrollment – page 19 Prepared 10/09

VISION PROGRAM The Vision Program provides coverage for many routine eye care needs, including comprehensive exams, eyeglass frames and lenses or contact lenses at competitive rates. Coverage is administered by Superior Vision Services. Plan Pricing See the 2010 RBC USA Benefits Rate Sheet for monthly contribution amounts. Default Election If you do not make a vision plan election, you will not be enrolled.

Vision Plan Highlights The following chart provides an overview of some of the coverage available through the vision program. See the summary plan description and certificate of insurance for additional information.

Features Benefits In-network providers Out-of-network providers Annual Exam by Ophthalmologist

Covered in full once each calendar year after $15 co-payment

Up to $45 reimbursed each calendar year after a $15 co-payment

Annual Exam by Optometrist

Covered in full once each calendar year after $15 co-payment

Up to $39 reimbursed each calendar year after a $15 co-payment

Frames Up to $125 after $15 co-payment every two calendar years

Up to $62 reimbursed each calendar year after a $15 co-payment

Eyeglass lenses (per pair) Single vision Up to $38 reimbursed each calendar year

after a $15 co-payment Bifocals Up to $53 reimbursed each calendar year

after a $15 co-payment Trifocals Up to $68 reimbursed each calendar year

after a $15 co-payment Lenticular

Standard glass or plastic lenses covered at 100% once each calendar year after you pay your $15 co-payment. Add-on lens options, such as tinting, require payment of an additional amount, but may be eligible for a discount from select providers.

Up to $94 reimbursed each calendar year after a $15 co-payment

Contact lenses Elective/Cosmetic Up to $120 each calendar year Up to $100 reimbursed each calendar year Medically Necessary Covered in full each calendar year Up to $210 reimbursed each calendar year Standard Contact Lens Fitting*

Covered in full after $25 co-payment (separate from comprehensive eye exam co-payment)

No out-of-network benefit

Specialty Contact Lens Fitting*

Covered in full after $25 co-payment up to an allowance of $50 (separate from comprehensive eye exam co-payment)

No out-of-network benefit

Note: There is one $15 co-payment for eyeglass lenses and a frame when purchased together. Out-of-network co-payments are deducted from the out-of-network reimbursement amount. You may receive either eyeglass lenses and frames or contact lenses in a calendar-year benefit period, but not both.

* Standard contact lens fitting fee applies to an existing contact lens user who wears disposable, daily wear, or extended wear lenses only. The specialty contact lens fitting fee applies to new contact lens wearers and/or a member who wears toric, gas permeable, or multifocal lenses. For the specialty fit, the member is responsible for any charges over $50.

2010 RBC USA Benefits Enrollment – page 20 Prepared 10/09

Other Discounts/Benefits Available (certain restrictions apply): • 20% discount on refractive surgery fees from contracted surgeons. • 20% discount to the following add-on charges: lens colors/tints, coatings, special bevels, special

multifocals, and special materials. • 10% - 30% discount on purchases of additional frames, lenses and contact lenses when purchased from

Superior Vision Plan in-network providers who are identified in the provider directory with a “DP” as part of the services they provide under the Plan.

• Discount contact lenses are available for online order at www.svcontacts.com.

Employee Resources Contacting Superior Vision For assistance with claims or questions, call Superior Vision’s member services at 1-800-507-3800. Choosing a Network Provider To get the most out of the Vision Program, always use a network provider. To locate a network provider, visit the Superior Vision Web site at www.superiorvision.com and click on “Locate a Provider” or call member services at 1-800-507-3800. ID Cards Employees who choose this plan will receive ID cards from Superior Vision. ID cards should be presented to your provider whenever you receive care. Additional cards may be ordered by contacting Superior Vision’s customer service at 1-800-507-3800 or online at www.superiorvision.com.

2010 RBC USA Benefits Enrollment – page 21 Prepared 10/09

LIFE INSURANCE PROGRAMS RBC automatically provides basic life insurance coverage and Business Travel Accident (BTA) coverage at no cost to you. The company also offers optional supplemental life insurance and accidental death and dismemberment (AD&D) coverage. Together, these options are designed to give you and your eligible family members flexibility to meet your specific insurance needs. BASIC LIFE RBC provides basic life insurance at no cost to you. You are automatically enrolled. If your coverage exceeds $50,000, the IRS requires that you be taxed on the value of the coverage above $50,000. This is automatically done by payroll. RBC Insurance insures the coverage.

Basic Life Plan Highlights Features Basic Life

Persons Covered Eligible Employees Benefit Amount Equal to one times your annual Covered Earnings*, rounded up to the nearest thousand.

Maximum coverage amount is $300,000. Guaranteed Issue Amount

All coverage is guaranteed. Evidence of insurability is not required.

Beneficiary Designation

All eligible employees must complete a beneficiary designation form (found on Me & RBC USA)

Age Reduction For participants aged 65 and over, insurance amounts are reduced. If any participant reaches age 65, 70 or 75 during a given plan year, the original coverage amount is reduced to the percentage shown below beginning in the next plan year:

65-69: 65% 70-74: 50%

75 and over: 30%

For example, if you turn 65 and your Covered Earnings* are $100,000, your benefit is $65,000 as of January 1 of the following plan year.

*Covered Earnings are defined on Page 2 of this booklet.

2010 RBC USA Benefits Enrollment – page 22 Prepared 10/09

SUPPLEMENTAL LIFE This program gives you and your eligible family members the opportunity to purchase term life insurance at group rates. Reliastar Life Insurance (ING Employee Benefits) insures the coverage. Plan Pricing See the 2010 RBC USA Benefits Rate Sheet for monthly contribution amounts. Default Election If you do not make a supplemental life insurance election, you will not be enrolled.

Supplemental Life Plan Highlights Features Supplemental Life

Persons Eligible for Coverage

Employee, spouse or domestic partner and children, as elected. Children are eligible for coverage until they reach age 19, or age 25 if a full-time student.

Benefit Amounts Employees One to eight times Covered Earnings*, rounded up to the nearest thousand.

Spouse or domestic partner $ 10,000 $ 100,000 $ 750,000 $ 25,000 $ 250,000 $ 1,000,000 $ 50,000 $ 500,000

Children $10,000 per child

Plan Maximum Employees - The lesser of eight times Covered Earnings* or $2,000,000 Spouse or Domestic Partner - $1,000,000 Children - $10,000

Guaranteed Issue Guaranteed issue is the amount of coverage available without needing to provide evidence of insurability. These amounts are available provided coverage is elected during the initial enrollment period (i.e., within 31 days of when you and/or your dependents are first eligible to enroll in this benefit.) Guaranteed issue is no longer available after the initial enrollment period or during future annual enrollment periods, except in some limited cases related to an eligible family status change.

Employees - Lesser of 3 times Covered Earnings* or $1,000,000 Spouse and Domestic Partner - $50,000 Child(ren) - $10,000

Evidence Of Insurability (EOI)

This is a process whereby the insurance company reviews your or your dependent’s health background and determines whether or not to approve the request for coverage. It is required for all amounts applied for during the initial enrollment period that exceed the Guaranteed Issue amounts. It is also required for all increases or new enrollments elected during future annual enrollment periods or following a family status change if coverage was previously available. If coverage elected on you and/or your dependents requires EOI, ING will send information to your home. Premium deductions for amounts requiring EOI begin after ING approves the additional coverage.

EOI is not required for annual changes in Covered Earnings* (automatically updated). Beneficiary Designation

All employees who are newly enrolling must complete a beneficiary designation form (found on Me & RBC USA). Employees are automatically beneficiaries on coverage of spouses, domestic partners and children.

Age Reduction For participants aged 65 and over, insurance amounts are reduced. If any participant reaches age 65, 70 or 75 during a given plan year, the original coverage amount is reduced to the percentage shown below beginning in the next plan year:

Age 65-69: 65% Age 70-74: 50%

Age 75 and over: 30%

For example, if you turn 65, your Covered Earnings* are $100,000, and you elect coverage of one times your Covered Earnings*, your benefit is $65,000 as of January 1 of the next year. Premiums will only be charged for $65,000 of coverage.

*Covered Earnings are defined on page 2 of this booklet.

2010 RBC USA Benefits Enrollment – page 23 Prepared 10/09

Employee Resources Contacting Reliastar Life Insurance (ING Employee Benefits) Contact Reliastar Life Insurance (ING Employee Benefits) customer service for beneficiary questions at 1-800-955-7736. All other questions may be directed to RBC’s HRSC Contact Center at 1-866-HRSERVE (477-3783).

2010 RBC USA Benefits Enrollment – page 24 Prepared 10/09

ACCIDENTAL DEATH & DISMEMBERMENT (AD&D) This program pays a benefit if you lose your life, limb or sight due to an accident. The amount of the benefit varies with the severity of the loss. Reliastar Life Insurance (ING Employee Benefits) insures the coverage.

Plan Pricing See the 2010 RBC USA Benefits Rate Sheet for monthly contribution amounts. Default Election If you do not make an AD&D election, you will not be enrolled.

AD&D Plan Highlights Features AD&D

Persons Eligible for Coverage

Employee or family, as elected.

$10,000 $50,000 $250,000 $750,000 Benefit Amount $25,000 $100,000 $500,000 $1,000,000

You are covered at the elected amount. If you choose family coverage and: • you have no eligible children, your spouse or domestic partner is covered

at 50% of the elected benefit amount. • a spouse or domestic partner is covered and one or more children are

covered, spouses and domestic partners are covered at 40% of the employee amount and children are covered at 10% of the benefit amount.

• no spouse or domestic partner is covered, children are covered at 20% of the elected benefit amount.

For example, if you elect $100,000 of family coverage and your family includes a spouse and two children, you are covered for up to $100,000, your spouse is covered for up to $40,000 and your children are covered for up to $10,000.

Plan Maximum 10 times your annual Covered Earnings*. Evidence Of Insurability

All coverage elected during your initial enrollment period; i.e., when you and/or your eligible dependents are first eligible to enroll in this benefit and during future annual enrollment periods is guaranteed. Evidence of insurability is not required. Evidence of insurability is not required for annual changes in Covered Earnings.

Beneficiary Designation

All employees who are newly enrolling must complete a beneficiary designation form (found on Me & RBC USA). Employees are automatically beneficiaries on coverage of spouses, domestic partners, and children.

*Covered Earnings are defined on page 2 of this booklet.

Employee Resources Contacting Reliastar Life Insurance (ING Employee Benefits) Contact Reliastar Life Insurance (ING Employee Benefits) customer service for beneficiary questions at 1-800-955-7736. All other questions may be directed to RBC’s HRSC Contact Center at 1-866-HRSERVE (477-3783).

2010 RBC USA Benefits Enrollment – page 25 Prepared 10/09

BUSINESS TRAVEL ACCIDENT (BTA) INSURANCE RBC provides BTA coverage at no cost to you if you are a full-time or part-time employee and work at least 15 hours a week. You are automatically enrolled. BTA provides three times your Covered Earnings* if you die as a result of an accidental injury while traveling for business. The maximum benefit is $300,000. Dependents are also covered (amounts vary) if they accompany you on a business trip at the request and expense of RBC and during required travel if you are transferred. This coverage does not apply to travel to and from work as part of your regular commute. RBC Insurance insures the coverage. For full details, review RBC’s Business Travel Accident Policy on Me & RBC USA.

*Covered Earnings are defined on page 2 of this booklet.

2010 RBC USA Benefits Enrollment – page 26 Prepared 10/09

DISABILITY PROGRAMS RBC automatically provides short-term disability coverage to you and also offers two levels of long-term disability coverage. Together, these options are designed to give employees flexibility to meet their specific disability insurance needs. SHORT-TERM DISABILITY (STD) RBC provides STD coverage at no cost to you. You are automatically enrolled. If disabled and your claim is approved, you may be eligible for up to 12 weeks of STD benefits. Under the STD policy, pay is continued at 100%, 60%, or a combination of both pay levels based on your length of service (see chart below for details). Once an STD claim is approved, benefits begin after a required five-day waiting period. STD is a company policy sponsored by RBC. For full details, see the STD policy available on Me & RBC USA.

STD Plan Highlights Features STD

Persons Covered Eligible Employees Qualifying for STD Benefits

To qualify for STD benefits, you must: • be under the direct, ongoing care of a medical doctor; • be certified by the medical doctor as unable to perform job duties for more

than five workdays because of a qualifying disability; • meet all documentation requirements; • meet the five-day waiting period requirement; and • be approved as having a qualifying disability by RBC or RBC’s designated

STD benefits administrator. A qualifying disability is one in which you are unable to perform the material duties of your job solely due to a covered injury or illness, as determined by RBC or RBC’s designated STD benefits administrator.

Waiting Period Once your claim is approved, STD benefits begin after a five-day waiting period. During the waiting period, you may: • use accrued paid time off (PTO)/vacation; • use other paid time off as required by statutory law, such as San Francisco

Sick Leave Ordinance (SFSLO) Sick Leave, or DC Sick and Safe Leave; or • take the time unpaid.

Benefit Amount STD benefits are based on your length of service.

Length of Service (as of the first day of absence)

Weeks of STD at 100% of Pay

Weeks of STD at 60% of Pay

Less than 3 months 0 12 3 months < 12 months 3 9 1 year < 3 years 7 5 3 years < 5 years 9 3 5 or more years 12 0

Childbirth: Following childbirth, an employee can receive up to seven consecutive weeks of maternity-related STD pay after satisfying the five-day waiting period. Benefits may be extended to the 12-week STD maximum, subject to medical documentation, if an employee is: • medically disabled beyond eight weeks following delivery (five-day waiting

period plus seven weeks STD), or • approved for STD benefits due to a maternity-related and medically-

substantiated reason prior to delivery. Maximum Benefit The maximum STD benefit an employee may receive in any 12-month period is 24

weeks regardless of the number of periods of disability and whether or not the cause of the disability periods is related.

2010 RBC USA Benefits Enrollment – page 27 Prepared 10/09

STD Pay Calculation

The STD pay calculation differs depending on whether you receive a salary or commissions. The following amount is used to calculate your STD benefits. • Salaried Employees: Base salary as of the last day worked. • Commission-Based Earnings Employees and Commissioned Sales Agents:

Covered Earnings* up to a maximum of $200,000 Use of Other Paid Time During STD

To supplement STD benefits at the 60% level, you may use accrued PTO/vacation or statutory paid time, such as SFSLO Sick Leave or DC Sick and Safe Leave.

Offsets to STD STD benefits are reduced by other disability or wage replacement payments you receive from other sources, including: • State short-term disability benefits • Workers’ Compensation benefits • Wage replacement plan benefits (i.e., from auto insurance), and • Insurance coverage or other payments (i.e., payment from a third party,

whether voluntarily or as a result of a lawsuit) • RBC paid earnings received during the period of disability, including

commission earnings (applies to Commission-Based Earnings Employees and Commissioned Sales Agents)

Exclusions/ Limitations

• STD benefits must be applied for within 120 days of the qualifying disability. • STD benefits are not payable for an illness or injury directly resulting from an

elective procedure or surgery, unless the procedure or surgery was medically necessary, and covered by the RBC Medical Program.

*Covered Earnings are defined on page 2 of this booklet.

LONG-TERM DISABILITY (LTD) The LTD Plan is designed to provide pay replacement for disabilities lasting longer than 90 days. If you are disabled and the claim is approved, LTD benefits begin after the 90-day waiting period and last as long as an employee remains disabled according to plan provisions. This plan is insured by CIGNA.

Employees have two coverage levels to choose from – the Basic Plan (50% coverage level) and the Premium Plan (60% coverage level). RBC provides the Basic Plan at no cost to you. You are taxed through payroll on the premiums paid by RBC for this coverage. Premiums for the Premium Plan are deducted from your pay on a post-tax basis. By doing so, any LTD benefits paid to you under this program will be considered non-taxable income by the IRS. Plan Pricing See the 2010 RBC USA Benefits Rate Sheet for monthly contribution amounts. Default Election If you do not make an LTD election, you will not be enrolled.

2010 RBC USA Benefits Enrollment – page 28 Prepared 10/09

LTD Plan Highlights Features LTD

Persons Covered Eligible Employees

Benefit Amount • Basic Plan – 50% Coverage (company-paid)

• Premium Plan – 60% Coverage (employee and company-paid) Annual Maximum Covered Earnings* (under both options)

$300,000

Evidence of Insurability

All coverage elected during your initial enrollment period; i.e., when you are first eligible to enroll in this benefit, and during future annual enrollment periods is guaranteed. Evidence of insurability is not required for annual changes in covered earnings.

Pre-Existing Condition Limitation

Applies to disabilities that begin during the first 12 months of coverage for injuries or illnesses diagnosed or treated within the 3 months prior to your coverage effective date. See the Certificate of Insurance for more details.

Benefit Offsets If you are approved for LTD, your LTD benefits may be offset with other income you may receive. Examples of other income benefits include, but are not limited to, government disability and retirement benefits received by you or your dependents, Workers’ Compensation, Unemployment, RBC funded pension plans, proceeds under other group insurance policies, and wages received for work performed. For a complete listing, see the Certificate of Insurance on Me & RBC USA.

Maximum Benefit Period

In addition to meeting other plan requirements, the maximum length of time you may be eligible to receive LTD benefits is determined by your age when your disability begins. See the table below for details.

Age When Disability Begins Maximum Benefit Period

62 or under Your 65th birthday or the date the 42nd monthly benefit is payable, if later.

63 The date the 36th monthly benefit is payable.

64 The date the 30th monthly benefit is payable.

65 The date the 24th monthly benefit is payable.

66 The date the 21st monthly benefit is payable.

67 The date the 18th monthly benefit is payable.

68 The date the 15th monthly benefit is payable.

69 or older The date the 12th monthly benefit is payable.

*Covered Earnings are defined on page 2 of this booklet.

2010 RBC USA Benefits Enrollment – page 29 Prepared 10/09

FLEXIBLE SPENDING ACCOUNTS PROGRAM A Flexible Spending Account (FSA) is an employee benefit program that allows you to set aside money from your pay

• into a special account; • on a pre-tax basis; • to pay many common eligible expenses for you and your eligible dependents.