2010 09 05 AR Mandatory audit firm rotation and audit … Mandatory Audit Firm Rotation and Audit...

63

Mandatory Audit Firm Rotation and Audit Quality: Evidence from the Korean Audit Market Soo Young Kwon Korea University Young Deok Lim University of New South Wales Roger Simnett University of New South Wales November 2010 We are grateful for the insightful comments from Michael Ettredge and participants at the seminars at the University of New South Wales.

Transcript of 2010 09 05 AR Mandatory audit firm rotation and audit … Mandatory Audit Firm Rotation and Audit...

Mandatory Audit Firm Rotation and Audit Quality:

Evidence from the Korean Audit Market

Soo Young Kwon

Korea University

Young Deok Lim

University of New South Wales

Roger Simnett

University of New South Wales

November 2010

We are grateful for the insightful comments from Michael Ettredge and

participants at the seminars at the University of New South Wales.

Mandatory Audit Firm Rotation and Audit Quality:

Evidence from the Korean Audit Market

Abstract

Using a unique database consisting of 12,463 firm-year observations in Korea

between 2000 and 2007, this study examines the effect of mandatory audit firm

rotation on audit hours, audit fees, and audit quality. Since the Korean

government mandated audit firm rotation in 2006, (1) audit hours increased, (2)

audit fees increased, and (3) audit quality (measured as abnormal discretionary

accruals) remained unchanged or decreased slightly. These results, which are

robust to controlling for potential endogeneity between audit hours and earnings

management and to measuring audit quality alternatively, suggest that mandatory

audit firm rotation increases the cost for audit firms and clients while having no

discernable positive effect on audit quality.

Keywords: Mandatory Audit Firm Rotation, Audit Hours, Audit Fees, Audit

Quality

JEL Classifications: M42, M48

Data Availability: Most of the financial data used in the present study are

available from the KIS Value database. The data for audit hours and fees were

drawn from statements of operating results filed with the Financial Supervisory

Services (FSS) in Korea.

1

Mandatory Audit Firm Rotation and Audit Quality:

Empirical Evidence from the Korean Audit Market

1. Introduction

The Korean Financial Supervisory Services (FSS) has mandated audit firm

rotation in 2006. The mandatory audit firm rotation, which requires audit firms to be

rotated every seven years, is intended to reduce auditors’ incentives to develop long-

term relationships with their clients so that their preference for conservative

accounting choices may be induced. This study examines the effect of the mandatory

audit firm rotation in Korea on audit hours, audit fees, and discretionary accruals.

Further, the study explores a forced auditor change setting that allows for a more

direct examination of how audit quality is affected by a mandatory auditor change and

an increase in auditor skepticism.

Whether audit firm rotation should be made mandatory is an issue that has been

debated for almost five decades in the U.S. and around the world. Proponents of

mandatory audit firm rotation have argued that a new auditor would bring to bear

greater skepticism and a fresh perspective that may be lacking in long-standing

auditor-client relationships.1 They have also claimed that when a company has been a

client of an audit firm for a number of years, the client can be viewed as a source of a

perpetual annuity, potentially impairing the auditor’s independence. Conversely,

opponents of mandatory firm rotation have argued that audit quality would suffer

under such a regime because the auditor would lack familiarity with the client and its

industry (AICPA [1992]). Furthermore, opponents have pointed to a higher incidence

of problem audits in the early years of the auditor-client relationship than in the later

years (St. Pierre and Anderson [1984]).

The Enron debacle in late 2001 (and its high-profile collapse) has refocused

attention on the profession’s effectiveness in protecting public interest. The Sarbanes-

Oxley Act [2002] required the General Accounting Office (GAO2) to conduct a study

of the potential effects of requiring the mandatory rotation of auditors registered

under the Act. The GAO’s study concluded that mandatory audit firm rotation might 1 Benson [2002] suggested that institutional investors have focused on this issue and opposed shareholder approval of any audit firm that has been retained by a company for more than five years. 2 Effective July 7, 2004, the GAO changed its name to the Government Accountability Office.

2

not be the most efficient way to strengthen auditor independence. Consequently, the

legislatures settled on the rotation of lead partners. However, the GAO has left open

the possibility of revisiting the mandatory audit firm rotation requirement if the other

requirements of the Sarbanes-Oxley Act do not lead to improved audit quality. Thus,

despite concerns that mandatory rotation could diminish the quality of financial

reporting, the demand for mandatory audit firm rotation has remained.

Because the effects of mandatory firm rotation cannot be analyzed using archival

data, prior research has examined the relation between audit quality and audit firm

tenure. As proxies for audit quality, they employ discretionary accruals, the cost of

debt financing, earnings response coefficients (ERCs), going-concern reports, AAERs

(Accounting and Auditing Enforcement Releases), auditor litigation, and fraud.

Overall, previous studies have suggested that long auditor tenure is not associated

with a decline in audit quality but that short tenure is associated with lower quality

audits (Geiger and Raghunandan [2002], Johnson et. al. [2002], Carcello and Nagy

[2004], Myers et. al. [2003], Ghosh and Moon [2005]). However, no study has

directly examined the effect of mandatory audit firm rotation because all have

examined audit firm rotation in the context of a voluntary change regime. Thus, the

results of prior research may not extend to a mandatory change regime.

Because auditor change is widely known to be endogenously determined, the

association between auditor tenure and audit quality has the self-selection bias (i.e.,

clients with long tenure tend to be good performers with less incentives to manage

earnings). Furthermore, unlike those under a mandatory audit firm rotation regime,

companies under a voluntary change regime are not required to change auditors in

future, and thus, they may still retain bargaining power over successor auditors. To

date, few studies have examined the effect of audit firm rotation in the mandatory

regime context because of the lack of data from a mandatory audit firm rotation

environment.

However, Korea has mandated the audit firm rotation requirement since 2006.

This allows a direct examination of the impact of a forced auditor change on audit

quality under a mandatory audit firm rotation regime. Furthermore, by employing

publicly disclosed data on audit hours and fees to determine the effects of a forced

auditor change on audit hours (auditor effort/cost) and audit fees (cost to clients), this

3

study provides a better understanding of the costs and benefits of mandatory audit

firm rotation.

Using a unique database consisting of 12,463 firm-year observations in Korea

between 2000 and 2007, this study examines the effect of mandatory audit firm

rotation on audit hours, audit fees, and audit quality. Since the Korean government

mandated audit firm rotation in 2006, (1) audit hours increased, (2) audit fees

increased, and (3) audit quality (measured as abnormal discretionary accruals)

remained unchanged or decreased slightly. These results, which are robust to

controlling for potential endogeneity between audit hours and earnings management

and to measuring audit quality alternatively, suggest that mandatory audit firm

rotation increases the cost for audit firms and clients while having no discernable

positive effect on audit quality.

Our study contributes to the literature in several ways. This study explicitly

examines the impact of mandatory audit firm rotation on audit quality under a

mandatory audit firm rotation regime. Previous studies have examined either the

effects of auditor tenure on earnings quality or the characteristics of firms voluntarily

changing auditors on the engagement under a voluntary rotation system, not under a

mandatory system.3 Thus, the results from a voluntary auditor change environment

may not extend to a mandatory auditor change environment if such a requirement is

imposed on public companies.

Second, to the authors’ knowledge, the present study is the first to employ the

rich dataset of audit hours and audit fees to address an important policy question --

the effect of mandatory auditor change on auditor efforts (auditor cost), audit fees

(client cost), and discretionary accruals (audit quality) -- under one study. Prior

studies have employed audit tenure, the auditor’s opinion, or financial statement

restatements to explore the impact of mandatory audit firm rotation. However, they

have not examined the rotation-related costs to clients and audit firms. The present

study has useful implications for regulators, members of the accounting profession,

and financial statement users as they deliberate on the costs and benefits of mandatory

audit firm rotation.

3 One recent study by Ruiz-Barbadillo et al. [2009] examined the impact of mandatory audit firm rotation on auditor behavior in the Spanish context. They used the likelihood of issuing going-concern opinions as a proxy for audit quality and focused on financially distressed firms from 1991~2000.

4

Third, this study provides evidence for the incremental effect of mandatory

auditor changes over voluntary auditor changes on auditor efforts, audit fees, and

discretionary accruals. Further, this study explicitly considers auditors’ responses to

the rule by increasing audit hours; the auditors were expected to change their audit

hours in anticipation of government scrutiny.

The remainder of the paper proceeds as follows. Section 2 provides a review of

the controversy and literature about mandatory rotation. Section 3 develops the

hypotheses, and Section 4 presents the models and key variables. Section 5 describes

the sample and reports the results. Section 6 provides additional analyses, and Section

7 concludes with a summary.

2. Controversy over Mandatory Rotation and Literature Review

2.1 Debate on Mandatory Audit Firm Rotation

2.1.1 Controversy over Mandatory Audit Firm Rotation Among Politicians,

Regulators, and Accounting Practitioners

In their seminal work, Mautz and Sharaf [1961] suggested that extended auditor-

client relationships can have a detrimental effect on auditor independence because an

auditor’s objectivity about a client decreases over time. Further, the Metcalf

Committee indicated that mandatory audit firm rotation is a way to bolster auditor

independence (U.S. Senate [1976]). Regulators have suggested a link between auditor

tenure and reductions in earnings quality and recommended imposing such a

requirement (Commission on Auditors’ Responsibilities [1978]; Division for CPA

firms, [1992]).

The Enron scandal and the Andersen audit failure rekindled the issue of

mandatory audit firm rotation. Mandatory audit firm rotation was advocated in the

congressional testimony by Arthur Levitt, Jr., former chairman of the SEC; Lynn E.

Turner, former SEC chief accountant; and Charles A. Bowsher, a chair of the Public

Oversight Board. They suggested that serious consideration be given to requiring

companies to change their audit firm every 5~7 years to ensure that fresh and

skeptical eyes are always looking at the numbers. Several bills containing provisions

limiting auditor tenure and mandating auditor rotation were proposed in the House

and the Senate as part of an effort to improve financial reporting and protect investors.

5

However, the views expressed above have not been universally accepted. The

Cohen Commission in 1978 concluded that mandatory rotation costs would exceed

the benefits. The auditing profession has argued that mandatory audit firm rotation

would not only decrease audit quality but also increase the cost of an audit (AICPA

[1992]). The 1996 GAO study opposed auditor rotation citing its detrimental impact

on the value of continuity in conducting audits. The AICPA’s Quality Control Inquiry

Committee of the SEC Practice Section analyzed 406 cases of alleged audit failure

between 1979 and 1991 and concluded that allegations of audit failure occurred

almost three times as often when an audit firm was performing its first or second

audit of a given client (AICPA [1992]).

Given the conflicting views on auditor tenure, Congress decided in 2002 not to

require the mandatory rotation of audit firms. Instead, it directed the GAO to conduct

research on the potential effects of mandatory audit firm rotation on audit quality; the

GAO’s 2003 study concluded that mandatory audit firm rotation may not be the most

efficient way to strengthen auditor independence and improve audit quality. As a

result, Congress decided that it was necessary to require mandatory partner rotation

(not mandatory audit firm rotation) every five years to increase audit quality.4

However, the GAO has left open the possibility of revisiting the mandatory audit

firm rotation requirement if the other requirements of the Sarbanes-Oxley Act do not

lead to improved audit quality (GAO [2003, 5]). In addition, several parties including

the GAO [2003, 9], the New York Stock Exchange [2003, 11], the Commission on

Public Trust and Private Enterprise [2003, 3], and TIAA-CREF [2004, 9] suggested

that periodically changing audit firms may enhance audit quality. Therefore, although

mandatory rotation is not required at the present time, regulators, policy makers, and

institutional investors have continued to be interested in this topic.

2.1.2 Pros and Cons of Mandatory Audit Firm Rotation

The most widely used arguments in favor of auditor rotation are as follows. First,

if auditors continue to audit the entity for too long, they risk developing too close a

4 Following the Sarbanes-Oxley Act, the SEC issued its rules on audit partner rotation in 2003; Rule 2-01(c)(6) of Regulation S-X requires the mandatory rotation of the lead partner and the concurring partner every five years in relation to their audit client.

6

relationship with the client and compromising independence.5 Second, periodically

having a new auditor would bring a fresh look to the public company’s financial

reporting and help the auditor appropriately deal with financial reporting issues

because the auditor’s tenure would be limited under mandatory audit firm rotation.

Third, mandatory audit firm rotation would help in the more even development of the

auditing profession, helping smaller and medium-sized audit firms to grow.

There are several arguments against mandatory audit firm rotation. First, new

auditors may miss problems in the period under review because they lack adequate

experience with the client to notice either unusual events or important changes in the

client’s environment.6 Second, there are not enough large audit firms to address the

audit requirements of large companies, making auditor rotation impracticable at the

ground level. Third, mandatory rotation increases audit start-up costs and the risk of

audit failure because the incoming auditor places increased reliance on the client’s

estimates and representations in the initial years of the engagement. Thus, there may

be negative effects on audit quality and effectiveness in the first years following a

change. Fourth, the rotation would only prevent auditors from building in-depth

institutional knowledge of a client and its business.7

It appears that politicians, regulators, analysts, and small audit firms favor

mandatory audit firm rotation as a solution to the perceived lack of objectivity and

independence of auditors. On the other hand, academicians, companies, and large

audit firms tend to be against mandatory audit firm rotation because changing

auditors is costly. It is certainly interesting to observe such different perspectives on

the same issue.

Without empirical evidence, it is neither clear whether mandatory rotation would

really ensure audit quality by strengthening auditor independence nor obvious

whether the rotation rule would hamper audit quality because of insufficient

knowledge of clients.

5 For example, Waste Management, W. R. Grace, and JWP were identified as three cases in which, in the context of a long-term audit relationship, an issue was identified by the auditors but then not resolved (Turner [2001]). 6 The accounting profession has argued that uncertainty about the characteristics of the client increases the potential for audit failures early in the auditor-client relationship (PricewaterhouseCoopers [2002]). 7 Most obviously, the cumulative knowledge of the existing audit team is lost, and the new auditor faces a steep learning curve. The increasing complexity of large groups and the complexities surrounding the financial reporting of their activities suggest that it can take the new auditor several years to fully understand the business (CGAA).

7

The response to mandatory rotation varies from firm to firm. Intel’s audit

committee decided in 2003 to change its auditor regularly in the wake of calls by a

number of advocates for better corporate governance. Intel had been audited by Ernst

& Young since the chipmaker was founded in 1968. However, the audit committee

had decided that Intel might benefit from obtaining a fresh look at its financial

accounting and internal control processes. LESCO also reported in 2003 that its board

of directors appointed KPMG as the company’s independent auditor by replacing

Ernst & Young. LESCO disclosed in a filing with the SEC that there were no

disagreements between the company and Ernst & Young on any matter of accounting

principles or practices, financial statement disclosure, or auditing scope or procedure.

By contrast, DuPont periodically rotated its auditor not only to assure

disinterestedness on the part of the auditor but also to provide the company with a

fresh perspective (Zeff [2003]). However, in 1954, it allowed Price Waterhouse & Co

to remain as the permanent auditor, particularly in view of the increasing size and

complexity of the company and its extensive overseas operations. These two

seemingly conflicting views under the voluntary auditor change setting suggest that

no clear consensus has emerged in favor of or against the concept of auditor rotation.

2.1.3 Trends in Mandatory Audit Firm Rotation Worldwide

In the wake of a number of financial reporting failures (notably in the U.S. but

also in Europe), legislators and regulators have questioned the quality of auditors’

work. The countries that already have an audit rotation system in place are Italy,

Brazil, Malaysia, Singapore, and Korea. Italy has a statutory requirement for audit

firm rotation every nine years. In Brazil, companies have been made to change

auditing firms every three years. In Singapore, banks are required to change audit

firms every five years, but there is no requirement on listed companies. In 2003,

Korea adopted the mandatory rotation rule and required listed firms to rotate their

auditors every six years starting in 2006.

Spain introduced mandatory rotation in 1988 after a maximum period of nine

years but abolished the mandatory rotation requirement in 1995. In 1998, France

considered the reform proposal with a provision to limit the term of the statutory

auditor to six years but dropped the provision from the proposal at the final stage.

8

Similarly, Austria approved a law in 2002 that required audit firm rotation by the end

of six years, but the requirement has been put on hold.

The U.K. concluded that the mandatory rotation of firms was not necessary.

Instead, it decided to increase the frequency of rotation for the lead audit partner to

every five years. Hong Kong also adopted audit partner rotation in 2003 by requiring

lead audit partners to be rotated every five years. Federation des Experts Compatables

Europeans (FEE) recommended in its letter to the European Commission that the

proposed Directive be amended to omit the suggestion that the mandatory rotation of

audit firms should be seen as an alternative to the mandatory rotation of partners.

Accordingly, none of countries in Europe have introduced mandatory audit firm

rotation.

2.2 Literature Review of Mandatory Audit Firm Rotation

Some studies have reported results consistent with the perspective that audit

quality deteriorates as the length of audit tenure increases. Mautz and Sharaf [1961]

suggested that extended client-auditor relationships alone impede auditor

independence. Deis and Giroux [1992] reviewed audit quality letters produced by a

public audit agency and concluded that audit quality declines as audit tenure increases.

Davis et al. [2002] suggested that longer auditor tenure is associated with the use of

discretionary accruals to manage earnings. This argument is reinforced by Bazerman

et al. [2002], who provided evidence of stronger psychological bias with increasing

ties between the auditor and its client. Dopuch et al. [2001] concluded that mandatory

rotation can increase auditor independence because rotation requirements constrain

low-balling in anticipation of potential income from future engagements.

On the other hand, other studies have provided conflicting results. St. Pierre and

Anderson [1984] and Stice [1991] suggested that many audit errors and lawsuits

occur during early years of the client-auditor relationship. Geiger and Raghunandan

[2002] determined that auditors become more efficient at collecting and evaluating

audit evidence as tenure increase. Carcello and Nagy [2004] proposed that the

probability of fraudulent financial reporting is highest early in the audit firm’s tenure

and is not substantially higher for instances of longstanding audit engagements.

Myers et al. [2004] found no evidence of an association between the nature and

severity of the restatement and auditor tenure. Mansi et al. [2004] suggested that

9

longer audit firm tenure is associated with higher bond ratings and a lower cost of

debt. Ghosh and Moon [2005] found that earnings response coefficients increased

with the length of audit firm tenure, suggesting that earnings have a greater influence

on equity prices as auditor tenure increases. Davis et al. [2009] demonstrated that

both short- and long-term auditor engagements were associated with the increased use

of discretionary accruals to meet and beat earnings forecasts in the pre-SOX period

but that the results disappeared following SOX.

A study by the University of Bocconi in Italy, using the number of suspensions

of partners imposed by the Italian nation commission as a proxy for audit quality,

concluded that mandatory auditor rotation was detrimental to audit quality because it

increased start-up costs and caused disruptions in the appointment phase. Ruiz-

Barbadillo et al. [2009] examined the impact of mandatory audit firm rotation on

auditor behavior in the Spanish context and found no evidence that a mandatory

rotation requirement is associated with a higher likelihood of issuing going-concern

opinions.

Overall, prior research on the effect of audit firm tenure on audit quality has

been mixed, although recent studies have tended to support higher audit quality as

auditor tenure increases. However, regardless of whether the results have been in

favor of or against mandatory audit firm rotation, previous studies have not

determined whether mandatory audit firm rotation would improve or hamper audit

quality. They have merely provided evidence that under the system of voluntary audit

firm rotation, audit quality does not appear to decrease with tenure. Therefore, any

generalization of such findings to a regime with mandatory audit rotation should be

implemented with caution.

To better understand the impact of mandatory audit firm rotation, recent studies

have taken two important approaches. The first approach examines the effect of

mandatory audit firm rotation on audit quality under a real mandatory audit firm

rotation regime. Recent studies have taken this approach by investigating the case of

Arthur Andersen (AA), where ex-AA clients were forced to change auditors because

of AA’s failure (Nagy [2005], Blouin et al. [2007]). However, this setting is not a true

mandatory audit firm rotation regime because companies still possessed considerable

amounts of bargaining power in the case of the AA failure.

10

The second approach examines the effect of audit partner rotation on audit

quality (Carey and Simnett [2006], Chi et al. [2009], Chen et al. [2008]).8 However,

audit partner rotation differs considerably from audit firm rotation; although the

former increases the risk of audit failures during a partner’s initial years on an

engagement and brings fresh eyes to an engagement, increasing audit quality, the

extent of the fresh view is less than that of the latter because of the potential

knowledge transfer and staff sharing within the audit firm. Thus, it is not clear

whether the results from these studies can be extended to a mandatory audit firm

rotation setting. Furthermore, Bamber and Bamber [2009] suggested that, compared

with audit firm rotation, audit partner rotation is likely to yield second-order effects.

Thus, audit partner rotation is not likely to have a substantial effect on audit quality.

Despite these attempts, previous studies have been limited by the fact that the

setting remains the voluntary rotation regime. In this regard, the present study

examines the effect of rotation at the time that mandatory rotation occurs, rather than

the effect of auditor tenure. In addition, the study employs audit hours and audit fees

to capture the rotation-related costs to audit firms and their clients; the study also uses

discretionary accruals to measure client managers’ accounting discretion.

3. Institutional Background and Hypotheses Development

3.1 Mandatory Audit Firm Rotation in Korea

The Korean government has initiated many legal and regulatory reforms since

the 1997 financial crisis. In particular, the government has launched bold programs to

improve corporate governance and accounting standards. In the wake of the Sarbanes-

Oxley Act of 2002, which the U.S. enacted in response to the accounting irregularities

of Enron, the Korean government formed a task force composed of experts from both

the public and private sectors, and the group was mandated to formulate robust

8 Carey and Simnett [2006] found that audit quality, proxied by the propensity to issue going-concern opinions and the incidence of just beating (missing) earnings benchmarks, decreased under long partner tenure. By using audit data from Taiwan, Chi, et al. [2009] found no support for the belief that mandatory auditor audit partner rotation enhances audit quality, whereas Chen et al. [2008] found that audit quality increased with partner tenure.

11

reform proposals to further strengthen Korea’s corporate governance and accounting

standards.

In April 2003, Korean regulators proposed an accounting reform bill that would

require listed companies to change auditors periodically. The bill passed through the

National Assembly, marking an epoch in the Korean accounting market; this contrasts

the situation in the U.S., where the implementation of the same scheme failed in 2002.

The mandatory rotation rule, which requires auditor rotation after six consecutive

years of audit engagement, is intended to prevent auditors from compromising their

duty or independence because of financial interests or a long-term relationship with

the same client. The FSS alleged that companies can easily manipulate their financial

statements in connivance with their long-standing auditor because an accounting firm

conducts audits on a listed company for a number of years.

Korea’s adoption of mandatory audit firm rotation provides us with an ideal

setting in which its real impact on costs and audit quality can be examined. The

voluntary setting provides an understanding of one aspect of a mandatory rotation

regime, but it does not truly allow for the examination of the effect that a forced

auditor change has on the level of audit quality. The voluntary setting considers a

company’s choice of an audit firm as exogenous, but in reality, the company is free to

choose any firm it deems appropriate. Thus, this raises the issue of endogeneity

because typically, troubled firms change auditors more often than sound ones.

Furthermore, there seems to be incentives for managers to switch to incompetent

auditors the moment a problem occurs. In this study, the endogeneity issue does not

arise because we deal with the mandatory rotation regime. In addition, we exploit

publicly disclosed audit hours and audit fees data to complement discretionary

accruals.

3.2 The Effect of Mandatory Audit Firm Rotation on Audit Hours

During the first year of a new appointment, more man-hours are necessary,

together with the deployment of more qualified resources than those usually

employed during the auditing of financial statements. Prior studies (Deis and Giroux

[1996], Caramanis and Lennox [2008]) suggested that if a client changes its auditor,

the incoming auditor is more likely to work longer hours because its start-up costs

12

(e.g., assessing the strength of internal controls) are high. Based on this reasoning, we

propose the following hypothesis:

H1-1: An auditor is more likely to spend more audit hours in its initial

audit engagement than in its subsequent audit engagements.

The engagement by mandatory audit firm rotation is a type of initial audit

engagement. However, it differs from the initial engagement because regulators

scrutinize the results of audits from mandatory audit firm rotation. Thus, auditors

under the mandatory auditor regime are more likely to make more audit effort to meet

regulators’ expectations. Furthermore, voluntary auditor change can be motivated by

opinion shopping; thus, a company may end up with a lower quality audit firm. Thus,

an auditor has less incentive to make audit efforts than an auditor under the

mandatory audit firm rotation regime.

On the other hand, low-balling practices to obtain the initial engagement may

result in insufficient audit work being done as auditors try to meet lower budgets. The

2003 GAO study suggested that if intensive price competition occurs, the expected

benefits of mandatory audit firm rotation can be adversely affected if audit quality

suffers as a result of audit fees that do not support an appropriate level of audit work.

In this case, mandatory audit firm rotation is more likely to reduce audit efforts than

the initial audit engagement.

Based on these two conflicting perspectives, we propose the following

hypothesis in an alternate form:

H1-2: An auditor in its initial audit engagement is likely to spend more

audit hours under the mandatory audit firm rotation regime than that

under the voluntary auditor change regime.

3.3 The Effect of Mandatory Audit Firm Rotation on Audit Fees

3.3.1 Without the Inclusion of Audit Hours as Determinants of Audit Fees

Competition among public accounting firms for providing audit services should

affect audit fees to some extent. Firms may be using low bids to obtain their initial

audit engagement. DeAngelo [1981] suggested that the existence of a learning curve

13

in auditing can lead to low-balling (price below cost) when auditors bid to perform a

new engagement. Simon and Francis [1988] suggested that price cutting exists in

early periods and that fee discounting occurs when clients incur considerable

incremental costs when changing auditors. Deis and Giroux [1996] provided

empirical evidence that initial audits are associated with lower audit fees.

Based on these results, we propose the following hypothesis:

H2-1: An auditor is more likely to charge lower audit fees in its initial

audit engagement than in its subsequent audit engagement.

The rule of mandatory external rotation might intensify price competition. In the

case of auditing, which is generally considered as a public interest activity, such

competition may be considered as inappropriate. If this were the case, then audit fees

under the mandatory audit firm rotation regime would be less than those under the

voluntary auditor change regime.

On the other hand, Petty and Cuganesan [1996] argued that auditing fees are

likely to escalate because auditors may be unable to absorb the initial higher costs

associated with the first years of auditing. Engagements through mandatory audit firm

rotation differ from voluntary initial engagements because the former is a case in

which the economic benefits are truncated from an extended period of repeat

engagements. Thus, auditors have fewer incentives to low-ball audit fees in initial

engagements. Furthermore, clients have less bargaining power because of the lack of

auditor choice. Based on these two conflicting views, the following hypothesis is

proposed:

H2-2: Auditors under the mandatory audit firm rotation regime are likely

to charge higher audit fees than those in their initial audit

engagement under the voluntary auditor change regime.

3.3.2 With the Inclusion of Audit Hours As Determinants of Audit Fees

Audit fees are determined by both audit efforts (audit cost) and audit risk. As

discussed above, mandatory audit firm rotation is likely to affect auditors’ efforts

because of regulators’ scrutiny as well as high start-up costs associated with the initial

14

engagement. In this case, it is not clear whether an audit fee increase stems from

compensation for additional work or from mandatory audit firm rotation per se. To

disentangle the effect of mandatory audit firm rotation on audit fees from that of audit

efforts, we further control for auditors’ efforts.

3.4 The Effect of Mandatory Audit Firm Rotation on Earnings Quality

In the voluntary auditor change setting, audit quality is more likely to deteriorate

for two reasons. First, a client is likely to hire an auditor with audit quality not higher

than its outgoing auditor. In the case of resignation, a client has difficulty finding an

auditor that can provide a similar level of audit quality. In the case of dismissal, a

client has an incentive to hire an auditor to get a desired opinion on an accounting

matter or on the financial statements as a whole. Second, the successor auditor under

the voluntary auditor change setting is unfamiliar with the new engagement and faces

a high learning curve. DeFond and Subramanyam [1998] suggested that audit quality

decreases in the initial year of audit engagement.

Thus, we propose the following alternate hypothesis for the initial audit

engagement:

H3-1: Audit quality in the initial audit engagement is lower than that in the

subsequent audit engagements.

Proponents of mandatory audit firm rotation have argued that long-term

relationships between auditors and their clients impede auditor independence. In

addition, they have suggested that decreased auditor independence can lead to

auditors’ support for more aggressive accounting choices that push the boundaries of

GAAP and can ultimately result in a failure to detect material fraud and/or

misstatements. They have argued that mandatory rotation enhances auditor

independence because managers cannot directly threaten auditors with their dismissal

and cannot promise future income arising from their continued appointment.

On the other hand, opponents of such rotation have questioned whether rotation

itself would reduce the incidence of audit failures because new auditors are invariably

unfamiliar with their clients and need time to acquire the relevant information and

know-how to effectively audit firms. They have argued that audit failures typically

15

occur in the first year of a mandate and that an auditor better understands the client’s

business, control risks, and other factors that contribute to audit failures as auditor

tenure increases.

Based on these two conflicting predictions, it is not clear whether an increase in

skepticism can overcome the hazards of a new engagement. Thus, it would be of

interest to empirically test the overall effect of mandatory audit firm rotation on audit

quality. In this regard, we propose the following hypothesis in the alternate form:

H3-2: Audit quality in the initial audit engagement under the mandatory

auditor regime is lower than that under the voluntary auditor change

regime.

The prior discussion assumes that auditors do not respond to the mandatory audit

firm rotation requirement. However, auditors under the mandatory audit firm rotation

regime participate in the bid with full recognition that they need to develop detailed

knowledge of a company’s business, its risks, and its constantly changing external

and internal environment. Auditors accept an audit engagement only if they are

willing to take considerable time to achieve full effectiveness. Thus, auditors are

expected to make additional efforts under the mandatory auditor regime, which

should reduce the adverse effect of mandatory audit firm rotation on audit quality. It

would be of interest to empirically test whether audit quality deteriorates in the

mandatory audit firm rotation regime after controlling for audit efforts.

4. Research Design

4.1 Measures of Audit Hours, Audit Fees, and Discretionary Accruals

4.1.1 Measures of Audit Hours and Audit Fees

The scarcity of empirical findings on audit efforts has been primarily due to the

unavailability of large data sets on audit hours. Prior research has collected data on

audit hours via either questionnaires (Palmrose [1989]; O’Keefe et al. [1994]) or

confidential sources (Davidson and Gist [1989]; Deis and Giroux [1996]). One

exception is Caramanis and Lennox’s [2008] study, which used a database of audit

16

hours from 9,738 audits in Greece between 1994 and 2002. Their study is notable in

that its sample consists of large-scale data on audit hours for a reasonable timeframe

in the private sector.

Until recently, audit fees have been confidential in most countries. Thus, early

studies obtained audit fee data through questionnaires. Simunic [1980], Palmrose

[1986], and Francis and Simon [1987] mailed questionnaires and collected audit fee

data. Maher et al. [1992] obtained data on external audit fees and internal audit costs

from the Michigan database, a collaborative effort by a nonrandom sample of

companies who agreed to participate in a study of internal auditing for 1977 and 1981.

Recent studies (DeFond et al. [2002], Abbott et al. [2003]) have obtained audit fee

data from proxies filed with the SEC since the SEC established a rule requiring fee

disclosure for proxies filed on or after February 5, 2001.

Korea provides a good research setting for collecting and analyzing data on audit

hours and fees. Korean companies are required to disclose such data in the annual

reports filed with the FSS. In this study, we conducted cross-sectional analyses,

employing 5,557 audits in Korea from 2000 to 2007, by using audit hours, audit fees

and earnings quality from annual reports. The data have two merits, clearly

distinguishing the present study from many previous studies. First, we used data on

actual audit hours and fees. This made a survey unnecessary and eliminated potential

problems arising from non-response bias. Second, we used both audit hours and audit

fees in one study, complementing each other in examining the effect of mandatory

audit firm rotation.

4.1.2 Measurement of Discretionary Accruals

Audit quality is typically viewed as compliance with Generally Accepted

Auditing Standards (GAAS). Consistent with prior research, here we posit that higher

quality audits constrain the extreme choices of management in presenting the

financial position of the firm. Accruals have been widely used to identify these

extreme reporting decisions (Becker et al. [1998], Myers et al. [2003]). In this regard,

we document the effect of mandatory audit firm rotation on earnings quality by using

absolute, signed, and raw [unsigned] accrual measures as proxies for earnings quality.

Accruals are defined as the difference between cash flows from operations and

net income. Hribar and Collins [2002] argued that a portion of the changes in balance

17

sheet working capital accounts relates to non-operating events and may erroneously

be shown as accruals under the balance sheet approach, possibly leading to an

erroneous conclusion that earnings management exists when there is none. They

recommend that accruals be measured directly from the cash flow statement as

follows:

ACCCFt = EBXIt –CFOt , (1)

where EBXIt is earnings before extraordinary items and discontinued operations and

CFOt is operating cash flows taken directly from the statement of cash flows.

We used performance-matched discretionary accruals (DA adj ) as the measure for

discretionary accruals. Following Tucker and Zarowin [2005], DA adj was calculated

as a residual from regression (2) as the regression-based approach, as in Kothari et al.

[2005].9 To measure the discretionary portion of accruals, we first estimated the

predicted nondiscretionary accruals by using the cross-sectional adaptation of the

performance-matched modified Jones model and then subtracted these predicted

nondiscretionary accruals from the realized accruals. Specifically, we estimated the

following regressions for a given year by using the control firms in the same two-digit

industry code as the firms in the sample:

jtjtjt

jtjtjtjtjtjtjtjt

TAROA

TAPPETARECREVTATAACC

13

1211101

/

//)(// , (2)

where ACCjt is accruals in year t for firm j; TAjt-1 is total assets in year t-1 for firm j;

REVjt is revenues in year t less revenues in year t-1 for firm j (i.e., change in

revenues); RECjt is receivables in year t less receivables in year t-1 for firm j (i.e.,

change in receivables); PPEjt is property, plant, and equipment in year t for firm j; jt

is the error term in year t for firm j; and ROAjt is the net income in year t for firm j.

We scaled all the variables in regression (2) by total assets in year t-1 to reduce

potential heteroskedasticity. These cross-sectional regressions were re-estimated for

9 Kothari et al. [2005] found that performance-matched discretionary accrual measures enhance the reliability of inferences from earnings management research.

18

each year in the sample period. The nondiscretionary accruals deflated by the total

assets (NDACC) for the sample firms were computed as follows:

13121110 ///)(/ itjtjtjtjtjtjtjtjt TAROAaTAPPEaTARECREVaTAaNDACC

, (3)

where 0a , 1a , 2a , and 3a are the estimated coefficients from regression (3). The

discretionary accruals (DACC) were computed as the difference between realized

accruals scaled by prior-year total assets and NDACC.

4.2 Model Specification

4.2.1 Audit Hours Model

We used the following model to test the hypotheses on audit hours.

LAHjt = + 1INITIALjt + 2INITIALjt MAN_ROTjt + 3LagLAHjt + 4LTAjt

+ 5BIGjt + 6CA_CLjt + 7LEVjt + ejt , (4)

where

LAH = the natural log of audit hours,

INITIAL = 1 if an audit was an initial engagement and 0 otherwise,

MAN_ROT = 1 if a firm changed its auditor as a result of the auditor

rotation requirement and 0 otherwise ,

LagLAH = the log of lag audit hours,

LTA = the natural log of total assets,

BIG = 1 if a firm was audited by one of Big N audit firms and 0

otherwise,

CA_CL = the current ratio (current assets ÷ current liabilities),

LEV = the ratio of long-term liabilities and debt to total assets.

The coefficients of interest were 1, the coefficient of INITIAL, and 2,, the

coefficient of the interaction term between INITIAL and MAN_ROT. We expected

that the coefficient estimate of 1 would be positive. The coefficient estimate of 2

was of primary interest because it allowed the determination of whether there were

19

differential audit efforts for new audit engagements imposed by the mandatory

rotation requirement.

Our model of audit hours is based on O’Keefe et al. [1994] and Caramanis and

Lennox [2008]. They showed that client size is the most important determinant of

audit hours. Thus, we controlled for the log of total assets (LTA). We controlled for

client complexity by using the ratio of current assets to current liabilities, and we

controlled for audit risk by using the leverage ratio (LEV). Finally, we included year

dummies and industry dummies for each two-digit sector.

There is no extant evidence of how actual hours vary across audit firms because

prior research has either obtained data from questionnaires or used internal data from

a single Big audit firm. Thus, we included a dummy variable (BIG), which equals one

if the audit firm is performed by one of the Big N audit firms and zero otherwise. We

also replaced BIG by dummy variables for Ernst & Young (EY),

PricewaterhouseCoopers (PWC), Arthur Andersen (AA), KPMG (KPMG), and

Deloitte & Touche (DT).

4.2.2 Audit Fees Model

We used the following model to test the hypotheses on audit fees. The

multivariate regression is as follows:

LAFjt = β + β1INITIALjt + β2INITIALjt MAN_ROTjt + β3IV_LAHjt + β4LTAjt

+ β5BIGjt + β6SUBjt + β7FRGNjt + β8AR_INVjt + β9ROIjt + β10LOSSjt

+ β11OPINIONjt + β12TELEjt + β13UTILjt + β14IND_SPECjt

+ β15POWERjt + ujt , (5)

where

LAF = the natural log of the audit fee,

IV_LAH = an instrumental variable measured by the natural log of audit

hours estimated from the audit hours model,

SUB = the square root of the number of subsidiaries,

FRGN = the proportion of foreign subsidiaries to total subsidiaries,

AR_INV = the proportion of total assets composed of inventory and

receivables,

ROI = return on investment (net income ÷ total assets),

20

LOSS = 1 if the company reported an operating loss in each of the

past two years and 0 otherwise,

OPINION = an indicator variable equal to 1 if the firm received a going-

concern modification in the prior year and 0 otherwise,

TELE = 1 if a firm operated in a telecommunication industry and 0

otherwise,

UTIL = 1 if a firm operated in an utility industry and 0 otherwise,

IND_SPEC = 1 if an auditor had 25 (33.3) percent or more market share in

an industry in each year and 0 otherwise,

POWER = the natural logarithm of each company’s sales divided by the

sum of industry sales for all firms in the industry audited by

the company’s auditor.

The INITIAL variable was coded as 1 if an audit was an initial engagement and 0

otherwise. Simon and Francis [1988] found that there is a significant fee reduction in

the initial engagement. H2-1 predicts that the coefficient estimate of β1 is negative or

non-positive. The MAN_ROT variable was coded as 1 if an auditor change occurred

as a result of the mandatory rotation requirement and 0 otherwise. MAN_ROT was the

variable of primary interest because it allowed the determination of whether there was

the pricing of new audit engagements imposed by the mandatory rotation requirement.

We included the instrument variable IV_LAH in the full model to address the

endogeneity issue. First, we regressed the log of audit hours at t (LAHjt) with respect

to log-lagged audit hours at t-1 (LAHjt-1) with control variables in the regression. We

expected strong persistence in audit hours, which would make lagged audit hours a

powerful predictor of current audit hours. In addition, LAHjt-1 was expected to be

uncorrelated with ujt. Second, we obtained the predicted (instrumented) log of audit

hours (IV_LAHjt) by using the coefficient estimates in the first regression.

The control variables included in our analysis were drawn from a large body of

research on audit fees (Casterella et al. [2004], Huang et al. [2007]). We included the

LTA variable, the natural log of total assets, because larger client firms were expected

to require more audit effort and consequently higher audit fees. We included the Big

N indicator variable (BIG) to represent the high-quality audit service provided by Big

N auditors, which was expected to influence audit fees (Francis and Simon [1987]).

21

We controlled for client complexity by including the square root of the number of

subsidiaries (SUB) and the proportion of foreign subsidiaries to total subsidiaries

(FRGN). AR_INV measures the proportion of total assets in inventory and accounts

receivable. Because the audit fee is positively related to client size, client complexity,

client-specific risk factors, and high-quality service, we predicted all these

coefficients to be positive.

Prior research has controlled for the client’s financial status and risk profile. We

used an indicator variable (ROI), return on investment, to measure profitability. We

also employed another indicator variable (LOSS) to capture client-specific litigation

risks. LOSS was coded as 1 if the client reported a net loss and 0 otherwise. OPINION

was coded as 1 if the client received a going concern modification in the sample year

and 0 otherwise. We further controlled for industry characteristics by including TELE

(telecommunication industry) and UTIL (utility industry) dummy variables (Huang et

al. [2007]). In addition, auditor industry specialization (IND_SPEC) and client

bargaining power (POWER) were included.

4.2.3 Discretionary Accruals Model

We used the following model to test the hypotheses on audit quality. Our model

specification is as follows:

DAjt = + 1INITIALjt + 2INITIALjt MAN_ROTjt + 3IV_LAHjt + 4LTAjt

+ 5BIGjt + 6AGEjt + 7OCF_TAjt + 8IND_GRWTHjt

+ 9CA_CLjt + vjt , (6)

Where

DA = Discretionary accruals,

AGE = the number of years after establishment,

OCF_TA = the ratio of operating cash flows to total assets,

IND_GRWTH =

N

iitSales

1

/

N

iitSales

11 by two-digit SIC code.

The coefficients of interest were 1, and 2. DeFond and Subramanyam [1998]

found that discretionary accruals are income-decreasing during the last year with the

predecessor auditor. Our key variables were INITIAL, which was coded as 1 if an

22

audit was performed by a predecessor auditor, and MAN_ROT, which was coded as 1

if an initial engagement occurred as a result of the mandatory rotation requirement.

The instrument variable IV_LAH was measured as described in 4.2.2.

The control variables in our analysis were drawn from Myers et al. [2003].

Client size is positively related to abnormal accruals (Becker et al. 1998]. Thus, we

included client size (LTA) as a control variable. We included the Big dummy variable

to control for differences in earnings management between Big N and non-Big N

client firms (Becker et al. 1998). We included AGE because accruals differ with

changes in the firm’s life cycle (Anthony and Ramesh [1992], Dechow et al. [2001],

Myers et al. [2003]). OCF_TA was included because firms with higher cash flows

from operations are more likely to be better performers (Frankel et al. 2002) and

because accruals and cash flows are negatively correlated on average (Dechow [1994],

Sloan [1996], Myers et al. [2003]). We controlled for IND_GRWTH because growth

in the industry should be positively correlated with accruals (Myers et al. [2003]).

Butler, Leone, and Willenborg [2004] found a positive relation between discretionary

accruals and liquidity. Based on their study, we included the current ratio (CA_CL) to

control for liquidity.

5. Empirical Results

5.1 Sample

The sample firms were selected from companies listed on the Korean Stock

Exchange (KSE) and Korea Securities Dealers Automated Quotations (KOSDAQ)

from 2000 to 2007. Initially, a total of 12,463 firm-year observations were obtained

from the KIS value database.10 Non-December year-end firms were excluded because

their tax change effects could have been different. We also excluded 266 financial

and insurance observations from the sample because of differences in financial

characteristics. We further deleted observations if audit fee, audit hour, and financial

data were not available during the sample period. Firms in the industry with less than

eight member firms each year were also excluded because discretionary accruals were

estimated for each industry and each year by using the cross-sectional modified Jones 10 The KIS value database is provided by Korea Investors Service Inc., which is affiliated with

Moody’s.

23

model (Kothari et al. [2005]). These procedures resulted in the final sample

comprising 5,557 firm-year observations (Table 1). There are more observations after

2005 because the disclosure of audit hours and audit fees has stabilized since it was

made mandatory in 2000.

<Insert Table 1 here>

5.2 Descriptive Statistics

5.2.1 Frequency of Observations with Respect to Initial Audit Engagement, Auditor

Change, Industry, and Year

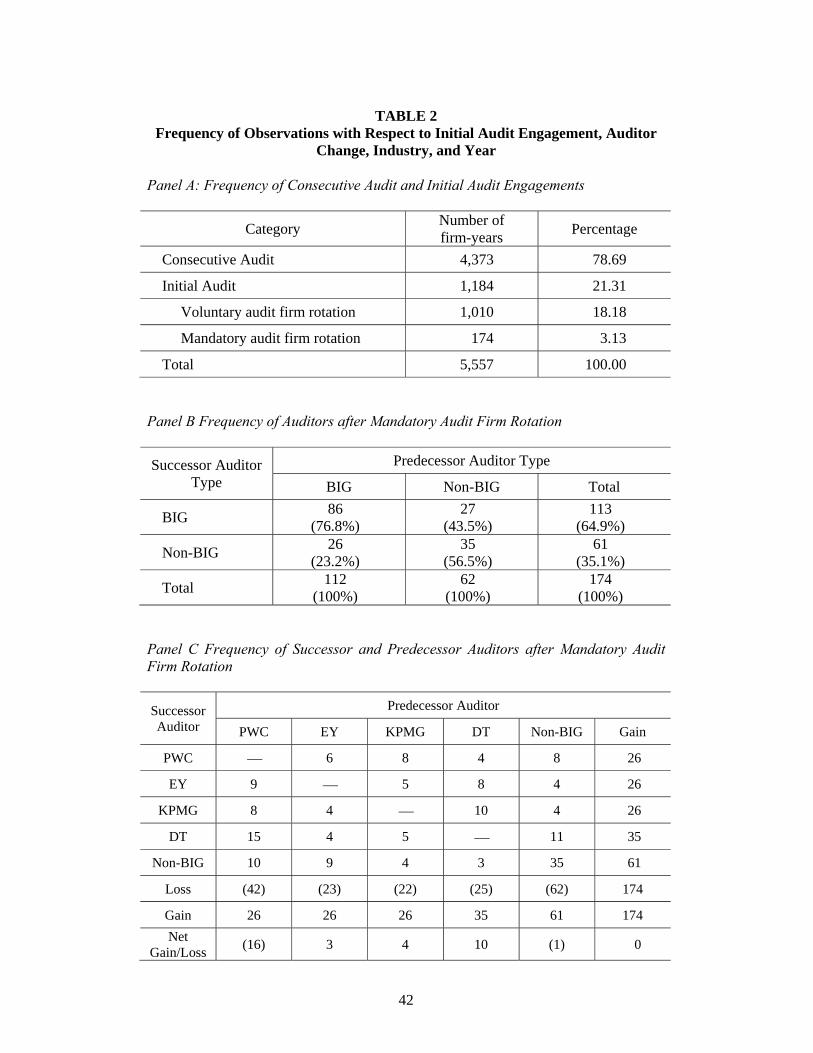

Panel A of Table 2 reports the frequency of observations for the consecutive

audit and initial audit engagements. Out of 5,557 observations, 4,373 (78.7%)

engagements were consecutive audits, and 1,184 (21.3%) were initial audits. Roughly

speaking, one out of five was an initial audit engagement. Of these 1,184 initial

engagements, 1,010 observations were classified as voluntary auditor change. The

remaining 174 engagements were due to auditor change based on the mandatory audit

firm rotation requirement.

Panels B of Table 2 presents the frequency of predecessors and successors for

the 174 engagements. Out of 112 Big audit firm clients, 86 clients (76.8%) chose

another Big audit firm, and the remaining 26 clients (23.2%) chose a non-Big audit

firm. On the other hand, of the 62 non-Big clients, 27 clients (43.5%) switched to a

Big audit firm, and only 35 clients (56.5%) chose a non-Big audit firm. This indicates

the increased concentration of Big N audit firms. This is inconsistent with the recent

argument by Economist [2004] that mandatory audit firm rotation can be a

mechanism to mitigate the dominance of Big N audit firms in the market for public

companies.

Panel C presents the frequency analysis (the net gain or loss of clients for each

audit firm). For example, PWC lost 42 clients but gained 26 clients after the

mandatory audit firm rotation. Thus, PWC experienced 16 losses. Other than PWC,

all the Big audit firms gained clients from the rotation requirement. The biggest

winner was Deloitte Touche, which had a net gain of 10 clients. Non-Big audit firms

lost 62 clients and gained 61 clients, indicating that the effect of mandatory audit firm

rotation on gaining clients was minimal.

24

Panel D of Table 2 shows the industry distribution of our sample firms according

to the 2-digit industry classification code of the Korea National Statistical Office.

Although many firms were concentrated in industries such as chemicals (11.48%),

other machinery (6.75%), computer (6.68%), and basic metals (6.05%), firms were

relatively evenly distributed across all industries, indicating no significant industry

clustering. Panel E of Table 2 exhibits the distribution of the sample by year. There

are more observations since 2005 because the disclosure of audit hours and audit fees

has spiked around this period, even though the disclosure has been required since

2000.

<Insert Table 2 here>

5.2.2 Descriptive Statistics of Study Variables and the Correlation Matrix

Table 3 presents the descriptive statistics for the variables used in our analysis.

The means of INITIAL, VOL_ROT, and MAN_ROT were 0.21, 0.18, and 0.03,

respectively, which were derived from the frequency data in Panel A of Table 2. The

mean and median values of audit hours (AH) were 806 and 516, respectively. The

corresponding values of audit fees (AF) were $73,483 and $50,000, respectively. The

means of both variables were larger than the medians, indicating right-skewed

distributions for both audit hours and audit fees. We then took logarithms of audit

hours and audit fees to normalize the distributions. The mean (median) DA adj was

0.000 (0.000), and the mean (median) Abs_DA adj was 0.08 (0.05). The mean value of

BIG was 0.58, indicating that 58% of the sample was audited by Big N audit firms.

<Insert Table 3 here>

Table 4 reports the correlations among audit hours, audit fees, earnings quality,

and other control variables. The audit hour variable, LAH, was not significantly

correlated with INITIAL but was positively (negatively) correlated with MAN_ROT

(VOL_ROT). This suggests that an auditor is more likely to spend more audit hours in

an initial audit engagement under the mandatory audit firm rotation regime than under

the voluntary audit firm rotation regime. The negative and significant correlation

between LAF and INITIAL suggests that an auditor is likely to charge lower audit fees

25

in an initial audit engagement, which is consistent with H2-1. We did not find a

significant correlation between DA adj and INITIAL, MAN_ROT, and VOL_ROT. This

implies that discretionary accruals neither increased nor decreased in the first year

when auditors changed. DA adj was negatively related to LAH, indicating that the

more the audit effort, the less the discretionary accruals became. The correlations of

BIG with LAH and LAF were significantly positive, but its correlation with DA adj was

significantly negative. This suggests that Big N audit firms make more effort and

receive higher audit fees and constrain clients from managing earnings more than

non-Big firms. The other correlations are consistent with the expectations and the

findings of prior research.

<Insert Table 4 here>

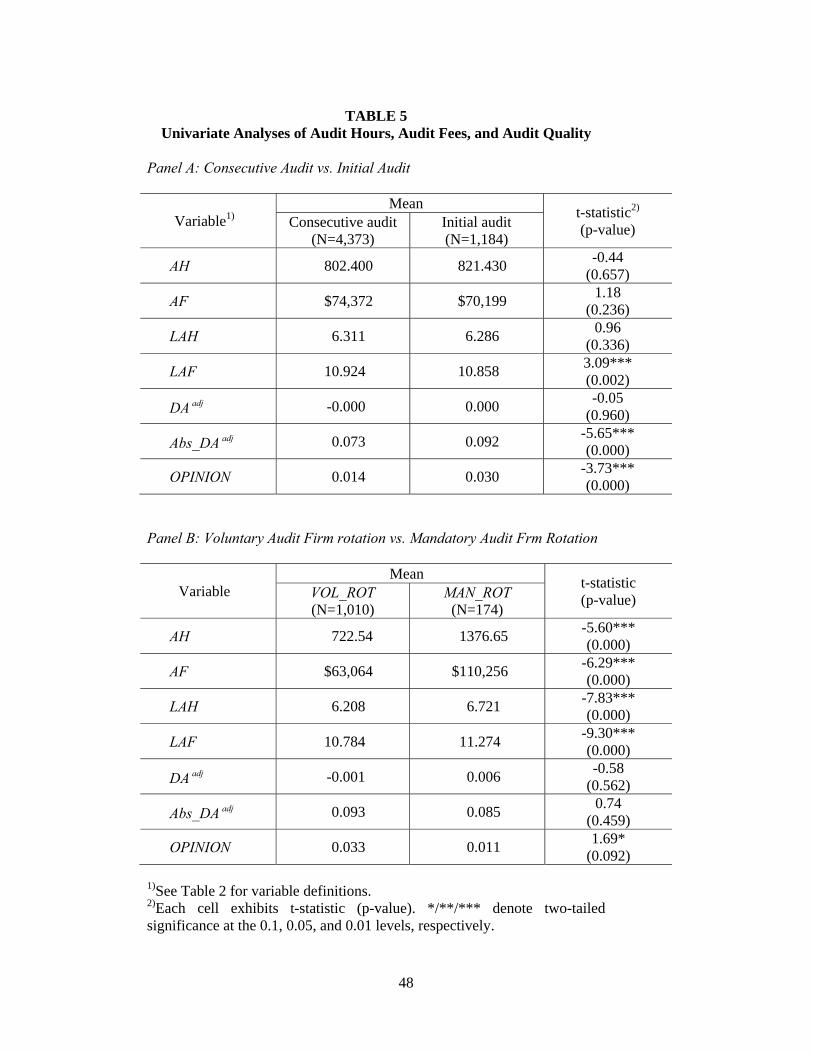

5.2.3 Univariate Analyses of Audit Hours, Audit Fees, and Audit Quality

Panel A of Table 5 presents the univariate analyses between consecutive audit

and initial audit engagements. Initial audits had significantly lower LAF and higher

Abs_DA adj and OPINION than consecutive audits. This suggests that an auditor in an

initial audit engagement is more likely to charge lower audit fees, allow clients to

exercise more discretion, and issue a going-concern opinion than an auditor in

consecutive audits, supporting H2-1 and H3-1.

Panel B compares MAN_ROT with VOL_ROT with respect to audit hours, audit

fees, and audit quality. It shows that MAN_ROT firms had significantly higher AH

and AF than VOL_ROT firms, indicating that an auditor under the mandatory audit

firm rotation is more likely to spend more audit hours and charge higher audit fees

than in an initial auditor under the voluntary auditor change regime. There was no

significant difference in DA adj and Abs_DA adj between MAN_ROT and VOL_ROT

firms. However, MAN_ROT firms had lower OPINION than VOL_ROT firms.

However, it is not clear whether the result that MAN_ROT firms issued a going-

concern opinion less frequently than VOL_ROT firms stemmed from low audit

quality or from high-quality clients that cared less about going-concern issues. Thus,

multivariate analyses are needed to control for client characteristics.

26

<Insert Table 5 here>

5.3 Regression Analyses of the Impact of Mandatory Audit Firm Rotation on

Audit Hours

Table 6 reports the results for the models of audit hours. The coefficient of

INITIAL was positive and significantly associated with audit hours, consistent with

those in Giroux et al. [1995], Deis and Giroux [1996], and Caramanis and Lennox

[2008]. This indicates that auditors invested the additional effort required to audit a

new client. However, the inclusion of the interaction term of INITIAL with

MAN_ROT made the coefficient of INITIAL nonsignificant, whereas the term

INITIAL MAN_ROT was significantly positive. This indicates that the significant

coefficient of the initial engagement was driven by a subset of firms required to rotate

auditors. This was unexpected, given the high set-up costs associated with the first

year’s engagement. This suggests that newly appointed auditors work more hours

than retained incumbent auditors only when they are engaged by the mandatory

rotation requirement.

<Insert Table 6 here>

As expected, the coefficients of LTA (0.287) and BIG (0.248) were significantly

positive. Consistent with O’Keefe et al. [1994], company size and audit firm

size/reputation were all important determinants of audit hours. Therefore, audit hours

were significantly higher for large clients and/or Big N audit firms than for small

clients and non-Big N audit firms. In Model 3, we replaced the BIG variable with

dummy variables for each of the Big N audit firms (PWC, EY, AA, KPMG, and DT).

The coefficients of these Big N dummy variables were all significantly positive

except AA. This indicates that, after controlling for client characteristics such as client

size, all Big N audit firms except Arthur Andersen made more effort than non-Big N

audit firms (Arthur Andersen made less effort than non-Big N audit firms). In model

4, we decomposed INITIAL into MAN_ROT and VOL_ROT and found that the

coefficient of MAN_ROT (0.289) was significant and positive and that the coefficient

of VOL_ROT was nonsignificant.

27

In Model 5, we included the log of the previous year’s audit hours (LagLAH) as

an independent variable to control for persistence in audit hours. The coefficient of

LagLAH was positive and highly significant (t-statistic = 33.56), showing strong

persistence in audit hours. We used the coefficient estimates in Model 5 to obtain the

instrumented log of audit hours (IV_LAH). As IV_LAHjt-1 was a strong predictor of

IV_LAHjt, we were confident that IV_LAHjt was a powerful instrument. We tested

whether IV_LAHjt was a valid (i.e., exogenous) instrument when we estimated the

audit fees and earnings management models. The magnitudes of LTA and BIG

coefficients decreased to a great extent but were still significantly positive. In Model

5, CA_CL and LEV were positive and significant after LagLAH was included.

It is quite evident that the auditee incurs additional costs as a result of the greater

amount of time devoted to interactions with the new audit firm by managers,

personnel, and internal auditors who supply to the audit firm necessary information

on aspects concerning corporate governance, internal control systems, organizational

structure, market position, and so forth. In addition, it seems that mandatory audit

firm rotation imposes an increased financial burden on audit firms while making it

difficult to predict and quantify the potential benefits of mandatory audit firm rotation.

5.4 Regression Analyses of the Impact of Mandatory Audit Firm Rotation on

Audit Fees

The results reported in Table 7 show that the association between the initial

engagement (INITIAL) and audit fees (LAF) was negative but insignificant. It became

significant when we included the interaction term of INITIAL with MAN_ROT. This

is consistent with H2-1. We further decomposed INITIAL into MAN_ROT and

VOL_ROT in Model 2 and found that the coefficient of MAN_ROT was significant

and positive and that the coefficient of VOL_ROT was significant and negative. Our

findings suggest that lower initial audit fees are dominant in VOL_ROT than in

MAN_ROT and that low-balling of initial audit fees do not happen under the

mandatory rotation regime.

<Insert Table 7 here>

28

The coefficient of INITIAL MAN_ROT was positive and significant even when

the instrumented variable of audit hours was included, suggesting that initial

engagements arising from the mandatory rotation requirement fetch higher audit fees.

To the extent that audit fees are competitively determined in the audit market and that

clients are willing to pay additional audit fees for high-quality audits, audit fees can

be used as a proxy for audit quality. From this point of view, the results might suggest

that the mandatory audit firm rotation requirement enhanced audit quality.11

However, it may be premature to make any decisive conclusion because the audit

fee is a noisy proxy for audit quality. High audit fees can be driven by the bargaining

power auditors have under the mandatory rotation regime. Clients are often limited to

choices among the Big 4 firms. The choices can be further restricted because the

accounting profession has become segmented by industry and because a lack of

industry-specific knowledge may preclude some firms from performing audits.12 Thus,

it is difficult to attribute an increase in audit fees for firms under mandatory audit firm

rotation to an increase in audit quality. Thus, we conclude that the mandatory audit

firm rotation increased the audit cost to clients.

The LTA and BIG variables were significantly positive, consistent with prior

studies (e.g., Craswell et al. [1995]). The proxies for operational complexity were

SUB, FRGN, and AR_INV, and those for audit risk were ROI, and LOSS. Some of the

control variables were both significant and in the correct direction. The coefficient of

IND_SPEC was significantly positive, indicating that specialist auditors received

audit premium. The coefficient of POWER was slightly positive but not consistent

with prior research (Casterella et al. [2004], Huang et al. [2007]).13 However, because

the results varied across models, we can place less weight on the significance of the

POWER variable.

11 The relationship between mandatory audit firm rotation and audit quality is addressed in section 5.5. 12 For a company limited to using Big 4 firms, the selection may be limited because an audit firm providing certain non-audit services or serving as a company’s internal auditor is prohibited by independence rules from also serving as that company’s auditor of record. In some cases, a company may also be limited in its choice of firms if an audit firm audits one of the company’s major competitors and the public company decides not to use that firm as its auditor of record (GAO [2003]). 13 Casterella et al. [2004] and Huang et al. [2007] documented a negative association between client bargaining power and audit fees, suggesting that audit fees are lower when clients have greater bargaining power.

29

5.5 Regression Analyses of the Impact of Mandatory Audit Firm Rotation on

Audit Quality

In this section, we document the effect of adopting the mandatory audit firm

rotation requirement on earnings quality. Following prior studies, we employed

discretionary accruals as a proxy for earnings quality. Panel A of Table 8 presents the

results of the OLS regression model estimated with the dependent variable of

abnormal accruals, and Panel B shows the results with the dependent variables of

positive abnormal accruals and negative abnormal accruals.

<Insert Table 8 here>

The INITIAL variable was negative but nonsignificant across models, indicating

that discretionary accruals did not increase in the initial audit engagement year. This

is inconsistent with the concern about poor audit quality in the initial years as a result

of insufficient knowledge of firm-specific risks. The interaction term INITIAL

MAN_ROT was positive but not significant across all models (except the model with

positive abnormal accruals). This result indicates that the forced auditor change under

the mandatory auditor regime did not decrease discretionary accruals; instead, it

increased discretionary accruals when they were income-increasing accruals. This

finding lends some support to no increase or and/or a decrease in audit quality

following a mandatory auditor change. The mandated rotation did not enhance audit

quality; instead, it decreased audit quality while imposing higher audit costs.

The LAH variable and its instrument variable, IV_LAH, were significantly

negative. This is consistent with the results of Caramanis and Lennox [2008] and

suggests that abnormal accruals are more likely to be income-increasing than income-

decreasing accruals when audit hours are low. On the other hand, the audit hour

coefficients were not significantly negative in the models with the dependent variable

of positive abnormal accruals but were significantly negative with that of negative

abnormal accruals. This indicates that less audit effort does not necessarily increase

income-increasing abnormal accruals but that it increases income-decreasing

abnormal accruals. Because audit hours here indicate a raw measure correlated with

other control variables in the regression model, we rely more on the result based on

the IV_LAH variable than that based on the instrument variable IV_LAH.

30

For abnormal accruals, the BIG coefficient was not different from 0. However, for

positive abnormal accruals, the coefficient was significantly negative, indicating that

income-increasing abnormal accruals were significantly smaller for Big N audit firms

than for non-Big N. For negative abnormal accruals, the coefficient was significantly

positive, indicating that income-decreasing abnormal accruals were significantly

larger for Big N audit firms than for non-Big N. This result suggests that Big N audit

firms are effective in constraining extreme abnormal accruals. Noteworthy is that the

coefficient of AA was positive, indicating that firms audited by Arthur Andersen had

more abnormal accruals than non-Big audit firms.

The OCF_TA control variables all had significantly negative coefficients,

implying that financially healthy firms are less likely to manage earnings. On the

other hand, the IND_GRWTH variable was significantly positive. This is consistent

with the view that firms with growth opportunities are more likely to be engaged in

earnings management (Myers et al., 2003). The LEV variable was significantly

negative, suggesting that the higher the debt-to-equity ratio, the less likely the firms

will manage earnings, which is not consistent with the prediction. The TENURE

variable was positive and significant, but the magnitude of the coefficient was so

small that it may have no economic significance. Furthermore, the correlation of

TENURE with the INITIAL and VOL_ROT variables was significantly negative by

construction, indicating that we need to interpret the TENURE coefficient with

caution.

6. Additional Analyses

Several sensitivity tests were performed to check the robustness of our results.

6.1 Alternatives Measures of Audit Quality

Carey and Simnett [2006] used three common measures -- i) the auditor’s

propensity to issue a going-concern opinion for distressed companies, ii) the amount

of abnormal working capital accruals, and iii) the extent to which key earnings targets

are just beaten (missed) -- as proxies for audit quality to determine whether there is a

negative association between long audit partner tenure and audit quality. In this

section, we also test the effect of mandatory audit firm rotation on earnings quality by

31

using the propensity to issue a going-concern opinion for financially distressed

companies and the observations that just beats or misses breakeven as the alternative

earnings quality measures for robustness.

6.1.1 Propensity to Issue a Going-Concern Opinion for Financially Distressed

Companies

We examined the effect of the initial audit and the mandatory audit firm rotation

regime on the propensity to issue a going-concern opinion for financially distressed

companies. Panel A of Table 9 reports the nonsignificant coefficients of INITIAL and

INITIAL MAN_ROT for the regression of both Models 1 and 2, suggesting a

minimal effect of mandatory audit firm rotation on the alternative measure of

earnings quality, which is consistent with Ruiz-Barbadillo et al.’s [2009] results for

Spain.

<Insert Table 9 here>

6.1.2 Observations that Just Beats or Misses Breakeven

We investigated the effect of the initial audit and the mandatory audit firm

rotation regime on the propensity to just beat or miss breakeven. Panel B of Table 10

reports the earnings benchmark frequency and statistics. The results indicate that

MAN_ROT (13.2%) had a slightly higher proportion of just beats (the net profit to

total assets is 0 to 2%) than VOL_ROT (12.3%), but the difference is not significant.

Panel C of Table 10 provides the results of the logistic regression with the dependent

variables of Beats breakeven and Misses breakeven. The coefficients of INITIAL and

INITIAL MAN_ROT for the regression of just beats breakeven and just misses

breakeven were not statistically significant.

To summarize, the findings from the alternative approach indicate that mandatory

audit firm rotation had little significant effect on audit quality, supporting the main

results.

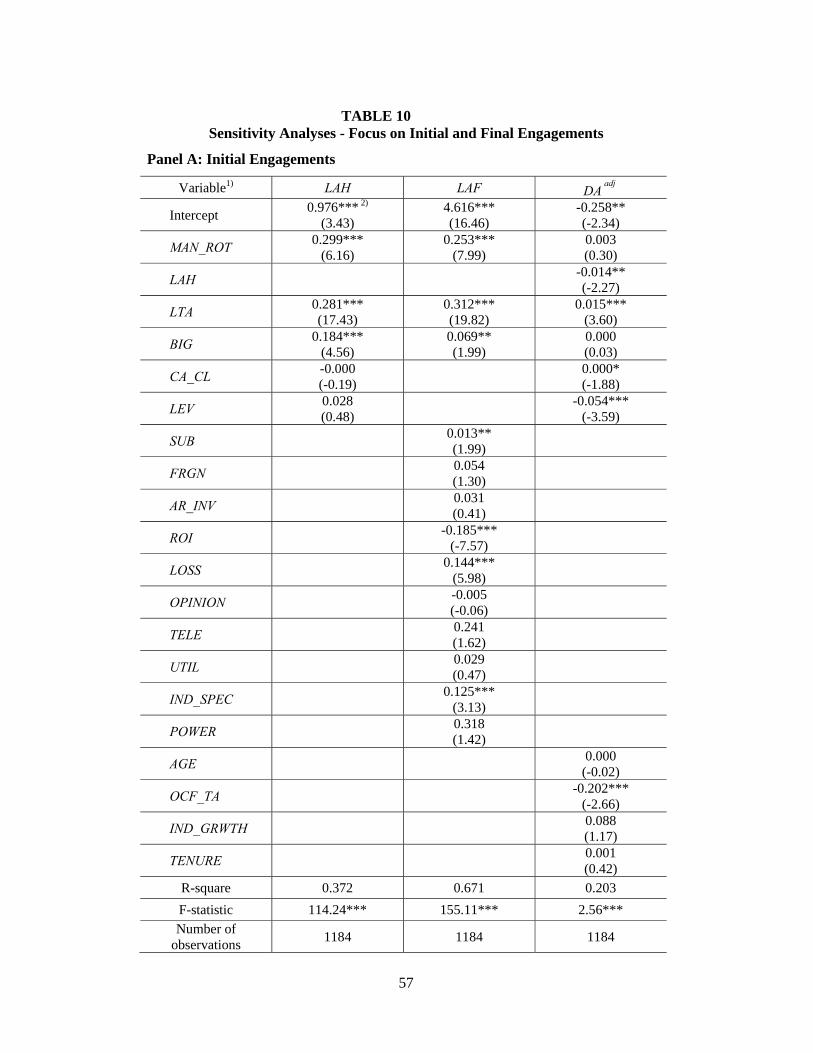

6.2 Focus on the Initial and Final Engagements

6.2.1 Initial Engagement

32

There is an omitted variable problem if the initial audit engagement has certain

characteristics that are correlated with audit hours, audit fees, and audit quality but are

not controlled for in the regression models. Then it is possible to attribute the effect of

mandatory audit firm rotation to the VOL_ROT and/or MAN_ROT variables. Thus, we

tested the impact of mandatory audit firm rotation on audit hours, audit fees, and

earnings quality by focusing on the sample of 1,184 initial audit engagements. Panel

A of Table 10 shows that MAN_ROT had positive coefficients on LAH and LAF but

nonsignificant coefficient on DA adj , which is consistent with the main findings.

<Insert Table 10 here>

6.2.2 Final Engagement

We examined audit hours, audit fees, and accruals in the auditor’s sixth year with

a client. In the old era (2000-2005), the sixth year was just like any other year. In the

new era (2006-2007), the sixth year was the incumbent’s final year before the

mandatory rotation. We investigated whether auditors systematically altered their

efforts and fees in the sixth year by comparing pre- with post- periods. Panel B of

Table 10 shows that the coefficient on LAF was 0.408 (positive and significant),

indicating that in post-periods, the final engagement entailed higher audit fees than

one in pre-periods.

6.3. Control for Structural Change in Voluntary Audit Firm Rotation