2009 Eldon D. Foote Lecture in International Business · 2009 Eldon D. Foote Lecture in...

38

1 2009 Eldon D. Foote Lecture in International Business Dr. Daniel Trefler, The Rotman School, CIFAR, Institute for Competitiveness and Prosperity Of Dragons and Elephants: Responding to the Rise of China and India I was told that what I’d have to do is bring you something unique, and I hope that what I’m doing will fit the bill here. I will be trying to go beyond the hyperbola for this talk on what globalization really means, and try to do what most of us do best, and that is to muster facts. It’s really to say of globalization, “it’s an interesting hypothesis, but is it supported by facts?” Currently, and popularly, when you look at what’s happening in China and in India, it’s overwhelming―I mean in the sense that Canada will be overtaken and become a backwash, and it won’t be long at all before we’ll be darning the socks of visiting Chinese businessmen because that’s about all we’ll be good for. So, I want to try to put something into perspective, and this is not easy to do, because it involves understanding the Chinese economy, the Indian economy, and the Canadian economy. It’s not just a trade issue to be sorted through, it’s a matter of understanding the structure of three economies, and that’s vast, as probably everyone understands. I think you can get a sense of the extent of the hyperbola tied up with all this talk of outsourcing to China and India, from this slide which I took off an airplane magazine, offering to “outsource your personal life” through dating for business professionals. It’s an example of the hype over outsourcing which has so permeated the way we think about the world, that to my mind, it’s past the point of absurdity. So, to understand what I think is really going on, there are three things you really need to know. There is what I call the “dragon myth,” the notion that everything that we buy is made in China. Well, if everything is made in China, how can we possibly have any money left for what we produce? Still, when China finally produces that last manufacturing widget which it doesn’t already produce, we must eventually become impoverished...This is how the dragon myth runs. So, first thing, we need to do is to get past it. The second thing to do is to return to basics. And “basics” here is to return to competition. There are two types of competition in this world: there’s low-cost competition, where you manage your processes, keep your costs down as much as possible, and worry about productivity. Then there is innovation-based competition, in which what you’re trying to do is not to manage costs, but, of course, to find [unintelligible]. The Chinese and the Indians both tell us that they’ve completely crossed over, and that what they’re doing now is extraordinarily good, innovative products and services. I’m going to cast extreme skepticism on that claim. Not to take away from what China and India are doing―it’s something historically extraordinary―but they’ve hardly broken into OECD innovation levels…as of yet.

Transcript of 2009 Eldon D. Foote Lecture in International Business · 2009 Eldon D. Foote Lecture in...

1

2009 Eldon D. Foote Lecture in International Business

Dr. Daniel Trefler, The Rotman School, CIFAR, Institute for Competitiveness and

Prosperity

Of Dragons and Elephants: Responding to the Rise of China and India

I was told that what I’d have to do is bring you something unique, and I hope that what

I’m doing will fit the bill here. I will be trying to go beyond the hyperbola for this talk on

what globalization really means, and try to do what most of us do best, and that is to

muster facts. It’s really to say of globalization, “it’s an interesting hypothesis, but is it

supported by facts?”

Currently, and popularly, when you look at what’s happening in China and in India, it’s

overwhelming―I mean in the sense that Canada will be overtaken and become a

backwash, and it won’t be long at all before we’ll be darning the socks of visiting

Chinese businessmen because that’s about all we’ll be good for. So, I want to try to put

something into perspective, and this is not easy to do, because it involves understanding

the Chinese economy, the Indian economy, and the Canadian economy. It’s not just a

trade issue to be sorted through, it’s a matter of understanding the structure of three

economies, and that’s vast, as probably everyone understands.

I think you can get a sense of the extent of the hyperbola tied up with all this talk of

outsourcing to China and India, from this slide which I took off an airplane magazine,

offering to “outsource your personal life” through dating for business professionals. It’s

an example of the hype over outsourcing which has so permeated the way we think about

the world, that to my mind, it’s past the point of absurdity. So, to understand what I think

is really going on, there are three things you really need to know. There is what I call the

“dragon myth,” the notion that everything that we buy is made in China. Well, if

everything is made in China, how can we possibly have any money left for what we

produce? Still, when China finally produces that last manufacturing widget which it

doesn’t already produce, we must eventually become impoverished...This is how the

dragon myth runs. So, first thing, we need to do is to get past it.

The second thing to do is to return to basics. And “basics” here is to return to

competition. There are two types of competition in this world: there’s low-cost

competition, where you manage your processes, keep your costs down as much as

possible, and worry about productivity. Then there is innovation-based competition, in

which what you’re trying to do is not to manage costs, but, of course, to find

[unintelligible]. The Chinese and the Indians both tell us that they’ve completely crossed

over, and that what they’re doing now is extraordinarily good, innovative products and

services. I’m going to cast extreme skepticism on that claim. Not to take away from what

China and India are doing―it’s something historically extraordinary―but they’ve hardly

broken into OECD innovation levels…as of yet.

2

What I’m going to argue as well is that Canada, as much as it likes to think that it has an

innovation-based economy, is sitting on the fence, surprisingly, between low-cost and

innovation-based competition, and that positioning is what’s going to hurt us more than

anything else. It’s not what’s happening in China and India that will hurt us, but what will

happen here, and that’s what worries me more than anything.

The third thing that I want you to understand is what I call the innovation tipping point.

Innovation is spurred on by a number of things, including the presence of sophisticated,

affluent consumers who are driving producers to produce new and innovative products.

And there may, no, there will come a time when consumers in Shanghai and Mumbai are

sufficiently affluent that they are going to be driving such innovation in their own

domestic markets. Their own domestic producers would then become so savvy that they

are going to start churning out the products that we all want to buy. And when that time

comes, China and India will make all of us quake in our boots, in terms of our ability to

survive this manufacturing onslaught. That’s one view of what will happen when we pass

the innovation tipping point. I don’t think that’s quite the right story, but I’ll tell you what

I think is the right story as we go along.

Let us go back to those three pillars―the dragon myth; making sure we know the

difference between low-cost competition and innovation-based competition; and making

sure we understand this innovation tipping point. With those three in place, I think we

can go quite far.

1. The Dragon Myth

DescriptionImports Share (% of total

imports from China)Imports per capita (C$)

Laptop and Accessories 9% 110

Telephone and Accessories 4% 56

Table Games 4% 45

Monitors and Projectors 3% 42

Toys 2% 31

Furniture 2% 30

Seats 2% 26

Sweaters 2% 22

Leather Bags 2% 21

Women/Girls Suits 2% 21

3

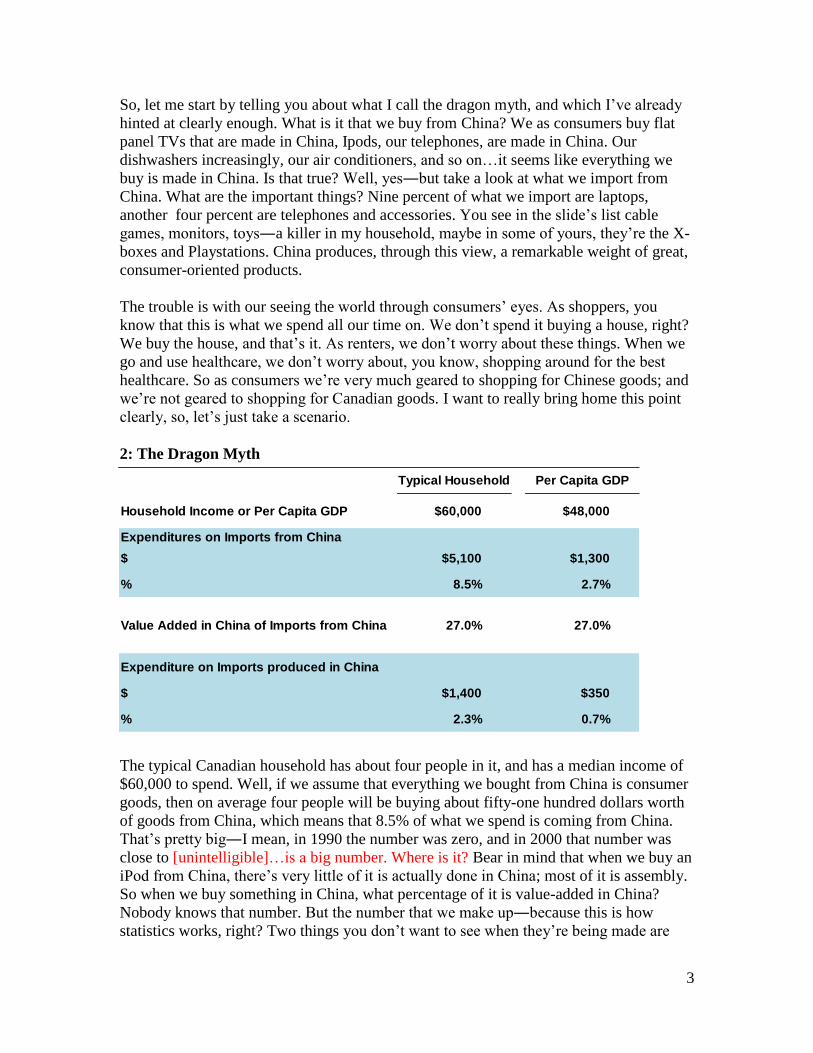

So, let me start by telling you about what I call the dragon myth, and which I’ve already

hinted at clearly enough. What is it that we buy from China? We as consumers buy flat

panel TVs that are made in China, Ipods, our telephones, are made in China. Our

dishwashers increasingly, our air conditioners, and so on…it seems like everything we

buy is made in China. Is that true? Well, yes―but take a look at what we import from

China. What are the important things? Nine percent of what we import are laptops,

another four percent are telephones and accessories. You see in the slide’s list cable

games, monitors, toys―a killer in my household, maybe in some of yours, they’re the X-

boxes and Playstations. China produces, through this view, a remarkable weight of great,

consumer-oriented products.

The trouble is with our seeing the world through consumers’ eyes. As shoppers, you

know that this is what we spend all our time on. We don’t spend it buying a house, right?

We buy the house, and that’s it. As renters, we don’t worry about these things. When we

go and use healthcare, we don’t worry about, you know, shopping around for the best

healthcare. So as consumers we’re very much geared to shopping for Chinese goods; and

we’re not geared to shopping for Canadian goods. I want to really bring home this point

clearly, so, let’s just take a scenario.

2: The Dragon Myth

The typical Canadian household has about four people in it, and has a median income of

$60,000 to spend. Well, if we assume that everything we bought from China is consumer

goods, then on average four people will be buying about fifty-one hundred dollars worth

of goods from China, which means that 8.5% of what we spend is coming from China.

That’s pretty big―I mean, in 1990 the number was zero, and in 2000 that number was

close to [unintelligible]…is a big number. Where is it? Bear in mind that when we buy an

iPod from China, there’s very little of it is actually done in China; most of it is assembly.

So when we buy something in China, what percentage of it is value-added in China?

Nobody knows that number. But the number that we make up―because this is how

statistics works, right? Two things you don’t want to see when they’re being made are

Typical Household Per Capita GDP

Household Income or Per Capita GDP $60,000 $48,000

Expenditures on Imports from China

$ $5,100 $1,300

% 8.5% 2.7%

Value Added in China of Imports from China 27.0% 27.0%

Expenditure on Imports produced in China

$ $1,400 $350

% 2.3% 0.7%

4

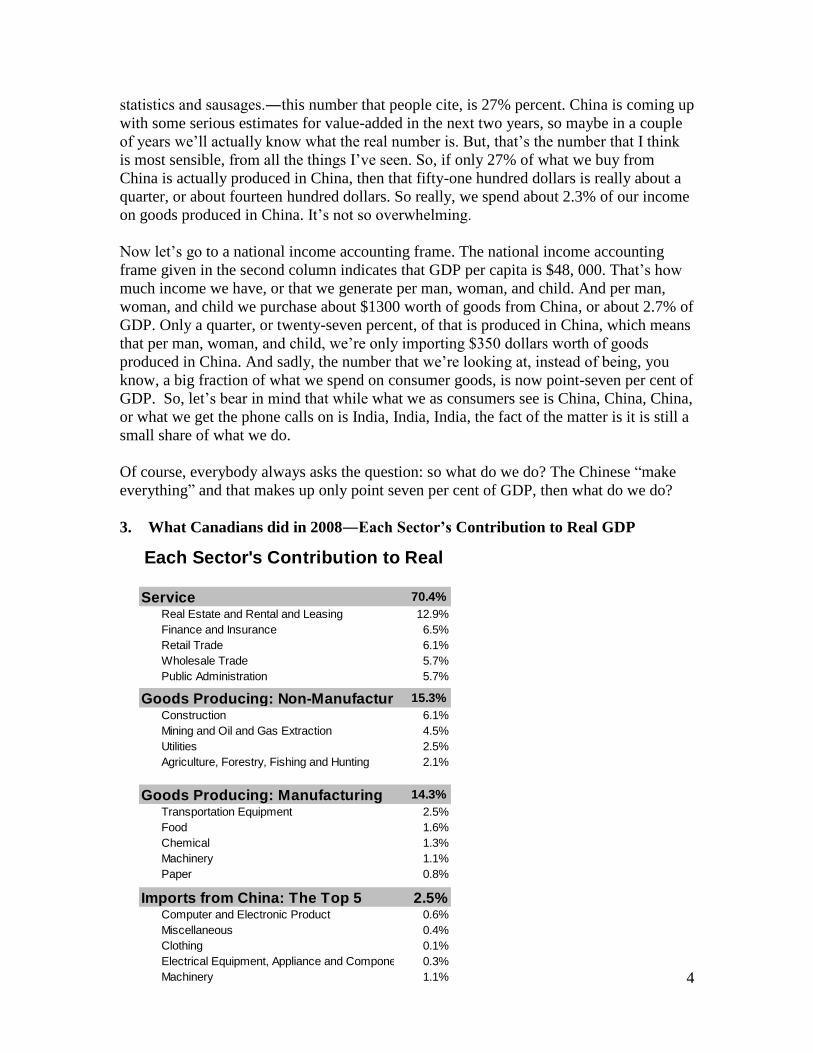

statistics and sausages.―this number that people cite, is 27% percent. China is coming up

with some serious estimates for value-added in the next two years, so maybe in a couple

of years we’ll actually know what the real number is. But, that’s the number that I think

is most sensible, from all the things I’ve seen. So, if only 27% of what we buy from

China is actually produced in China, then that fifty-one hundred dollars is really about a

quarter, or about fourteen hundred dollars. So really, we spend about 2.3% of our income

on goods produced in China. It’s not so overwhelming.

Now let’s go to a national income accounting frame. The national income accounting

frame given in the second column indicates that GDP per capita is $48, 000. That’s how

much income we have, or that we generate per man, woman, and child. And per man,

woman, and child we purchase about $1300 worth of goods from China, or about 2.7% of

GDP. Only a quarter, or twenty-seven percent, of that is produced in China, which means

that per man, woman, and child, we’re only importing $350 dollars worth of goods

produced in China. And sadly, the number that we’re looking at, instead of being, you

know, a big fraction of what we spend on consumer goods, is now point-seven per cent of

GDP. So, let’s bear in mind that while what we as consumers see is China, China, China,

or what we get the phone calls on is India, India, India, the fact of the matter is it is still a

small share of what we do.

Of course, everybody always asks the question: so what do we do? The Chinese “make

everything” and that makes up only point seven per cent of GDP, then what do we do?

3. What Canadians did in 2008―Each Sector’s Contribution to Real GDP

Service 70.4%

Real Estate and Rental and Leasing 12.9%

Finance and Insurance 6.5%

Retail Trade 6.1%

Wholesale Trade 5.7%

Public Administration 5.7%

Goods Producing: Non-Manufacturing15.3%

Construction 6.1%

Mining and Oil and Gas Extraction 4.5%

Utilities 2.5%

Agriculture, Forestry, Fishing and Hunting 2.1%

Goods Producing: Manufacturing 14.3%

Transportation Equipment 2.5%

Food 1.6%

Chemical 1.3%

Machinery 1.1%

Paper 0.8%

Imports from China: The Top 5 2.5%Computer and Electronic Product 0.6%

Miscellaneous 0.4%

Clothing 0.1%

Electrical Equipment, Appliance and Component 0.3%

Machinery 1.1%

Each Sector's Contribution to Real

GDP

5

Remembering back to 1900, when we talked about agriculture we said that agriculture

was the backbone of the economy, the farmers bore the economy on their shoulders, food

was essential for life, and without it, we’re nothing. Well, today agriculture is two per

cent of GDP. Manufacturing is also trending down fast. In the ‘fifties it was about 25% of

GDP, and now we’re quickly heading towards 10%. Why? It’s because of productivity.

[we’re getting good at time] Just like we got good at producing food, now we’re getting

good at producing manufactured goods. So, manufacturing is shrinking, and that’s not

what we do anymore. Then, what do we do in Canada? Much of it now, 70%, is services.

If you’re my dad you’ll say, “That’s not producing anything really, Dan.” Well, when I

bought my house that real estate agent really did help me. When I go for healthcare,

public administration really does help me. When I buy my iPod, which costs $300 and I

pay $150 of that in wholesale-retail markup, somebody’s providing me a service. I

certainly don’t want to travel to China to buy an iPod. So, these are important things.

When you look into non-manufacturing—building my house, for example, is a big part of

what I’ve spent in my lifetime―it’s 6.1% of the economy. Mining, and oil and gas

extraction is huge, they’re four and a half percent of the economy. That’s all Alberta: it’s

amazing, it’s actually crazy. Manufacturing is14% of the economy, and of course, the

killer, transportation equipment, is two and half percent. That’s all Ontario, or was

Ontario. It’s interesting to note that despite the fact that Ontario has been killed on

transportation equipment, transportation equipment is not on our top five list of goods we

buy from China. We don’t buy from China anything much to do with automobiles.

Alright, so we’ve talked about this dragon myth, and I’d like next to talk about this issue

of low-cost versus innovation-based competition, to bring out the distinction between

them. So let’s take a look at what China produces, and at what Canada imports and

exports, so you can get a sense of where we stand on this front.

4. Competition

Low-cost

Competition

• Focus on

Productivity • Managing Costs

6

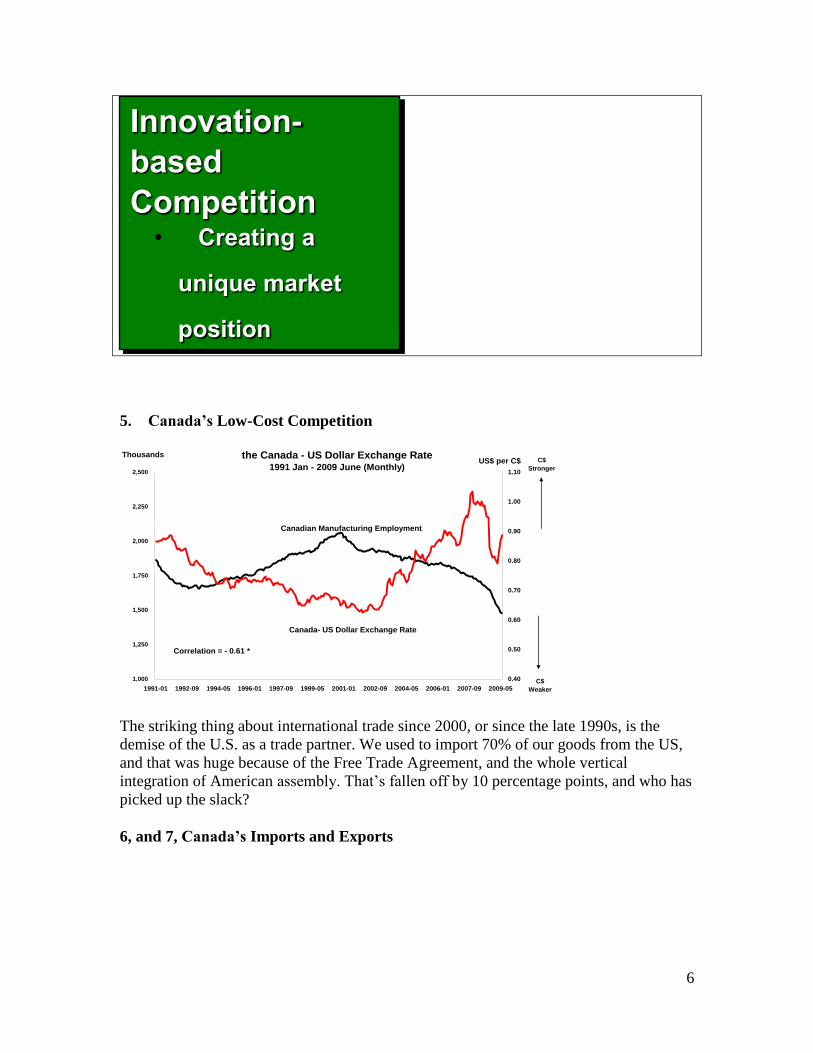

5. Canada’s Low-Cost Competition

The striking thing about international trade since 2000, or since the late 1990s, is the

demise of the U.S. as a trade partner. We used to import 70% of our goods from the US,

and that was huge because of the Free Trade Agreement, and the whole vertical

integration of American assembly. That’s fallen off by 10 percentage points, and who has

picked up the slack?

6, and 7, Canada’s Imports and Exports

1,000

1,250

1,500

1,750

2,000

2,250

2,500

1991-01 1992-09 1994-05 1996-01 1997-09 1999-05 2001-01 2002-09 2004-05 2006-01 2007-09 2009-05

0.40

0.50

0.60

0.70

0.80

0.90

1.00

1.10

Canadian Manufacturing Employment

Canada- US Dollar Exchange Rate

ThousandsUS$ per C$

Canadian Manufacturing Employment and

the Canada - US Dollar Exchange Rate1991 Jan - 2009 June (Monthly)

Note: * significant at 1%.

Source: Institute for Competitiveness & Prosperity analysis based on data from Statistics Canada and Bank of Canada.

C$

Stronger

C$

Weaker

Correlation = - 0.61 *

Innovation-

based

Competition

• Creating a

unique market

position

7

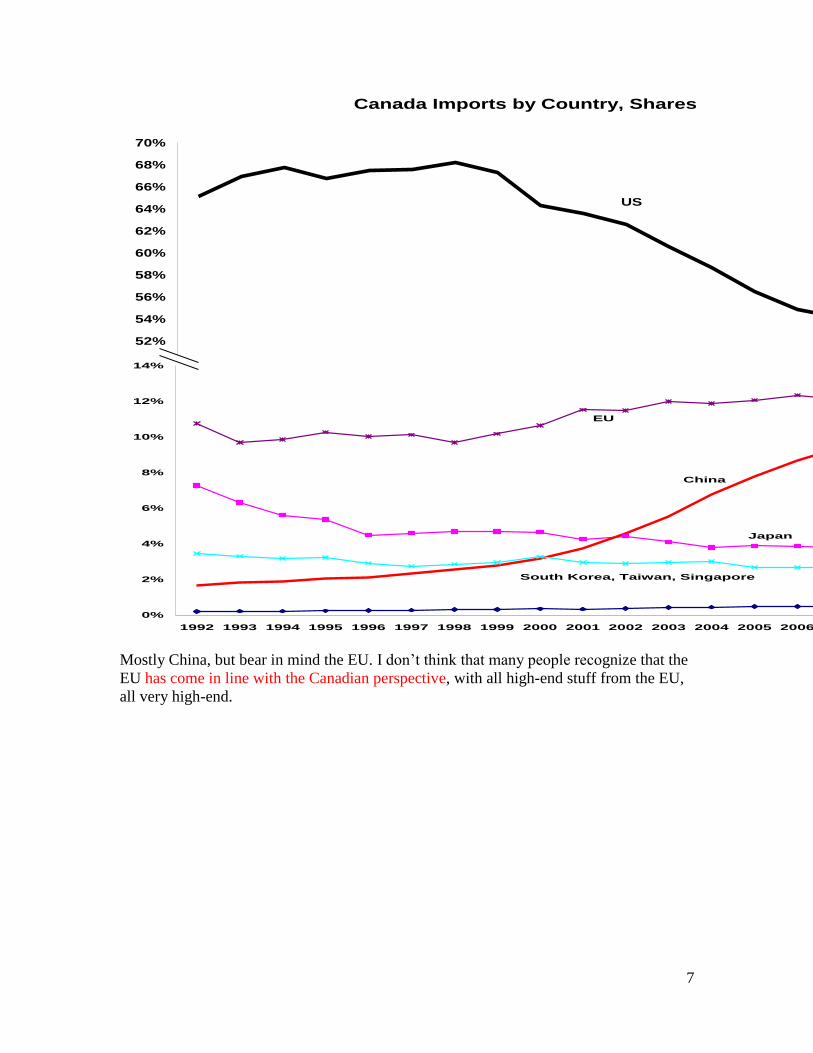

Mostly China, but bear in mind the EU. I don’t think that many people recognize that the

EU has come in line with the Canadian perspective, with all high-end stuff from the EU,

all very high-end.

Canada Imports by Country, Shares

0%

2%

4%

6%

8%

10%

12%

14%

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Japan

China

South Korea, Taiwan, Singapore

EU

India

Canada Imports by Country, Shares

40%

42%

44%

46%

48%

50%

52%

54%

56%

58%

60%

62%

64%

66%

68%

70%

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

US

8

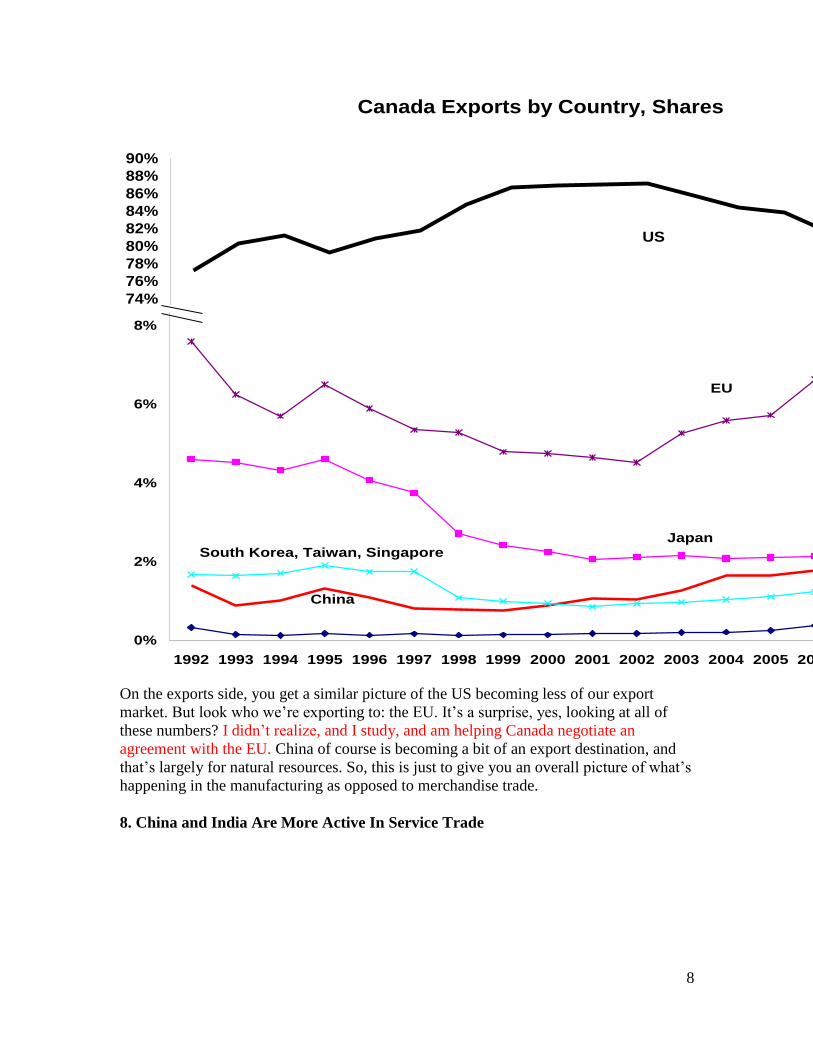

On the exports side, you get a similar picture of the US becoming less of our export

market. But look who we’re exporting to: the EU. It’s a surprise, yes, looking at all of

these numbers? I didn’t realize, and I study, and am helping Canada negotiate an

agreement with the EU. China of course is becoming a bit of an export destination, and

that’s largely for natural resources. So, this is just to give you an overall picture of what’s

happening in the manufacturing as opposed to merchandise trade.

8. China and India Are More Active In Service Trade

Canada Exports by Country, Shares

0%

2%

4%

6%

8%

10%

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Japan

China

South Korea, Taiwan, Singapore

EU

India

Canada Exports by Country, Shares

40%

42%

44%

46%

48%

50%

52%

54%

56%

58%

60%

62%

64%

66%

68%

70%

72%

74%

76%

78%

80%

82%

84%

86%

88%

90%

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

US

9

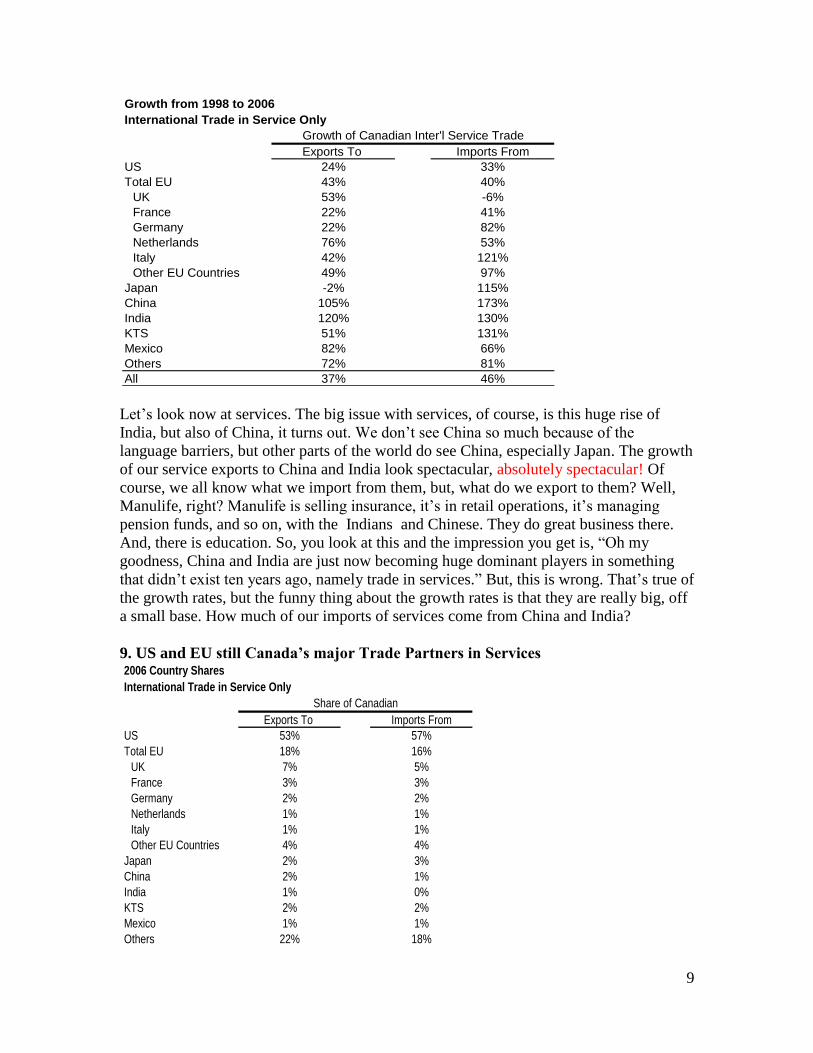

Let’s look now at services. The big issue with services, of course, is this huge rise of

India, but also of China, it turns out. We don’t see China so much because of the

language barriers, but other parts of the world do see China, especially Japan. The growth

of our service exports to China and India look spectacular, absolutely spectacular! Of

course, we all know what we import from them, but, what do we export to them? Well,

Manulife, right? Manulife is selling insurance, it’s in retail operations, it’s managing

pension funds, and so on, with the Indians and Chinese. They do great business there.

And, there is education. So, you look at this and the impression you get is, “Oh my

goodness, China and India are just now becoming huge dominant players in something

that didn’t exist ten years ago, namely trade in services.” But, this is wrong. That’s true of

the growth rates, but the funny thing about the growth rates is that they are really big, off

a small base. How much of our imports of services come from China and India?

9. US and EU still Canada’s major Trade Partners in Services

Growth from 1998 to 2006

International Trade in Service Only

Growth of Canadian Inter'l Service Trade

Exports To Imports From

US 24% 33%

Total EU 43% 40%

UK 53% -6%

France 22% 41%

Germany 22% 82%

Netherlands 76% 53%

Italy 42% 121%

Other EU Countries 49% 97%

Japan -2% 115%

China 105% 173%

India 120% 130%

KTS 51% 131%

Mexico 82% 66%

Others 72% 81%

All 37% 46%

2006 Country Shares

International Trade in Service Only

Share of Canadian

Exports To Imports From

US 53% 57%

Total EU 18% 16%

UK 7% 5%

France 3% 3%

Germany 2% 2%

Netherlands 1% 1%

Italy 1% 1%

Other EU Countries 4% 4%

Japan 2% 3%

China 2% 1%

India 1% 0%

KTS 2% 2%

Mexico 1% 1%

Others 22% 18%

10

Something looks a little bit wrong with the numbers, but the point is that for sure [the

total is] under 3%. Now, China and India remain inconsequential. 80% of what we buy

and sell in the way of services internationally, is with OECD countries, mostly with the

US, though the UK is a big destination as well.

9. “Much Ado about Nothing”

So, let’s not kid ourselves about having spectacular growth rates

impact so far. Runjuan Liu and I have a paper which talks about

what the stats and the impacts from Indian Inc. are: they’re what we

call, “Much Ado about Nothing.” We generated systematic analyses

of what the labor market impacts have been of offshoring services

to China and India, and the impact at the end is zero, and that’s

precisely estimated, for those of you who are statisticians.

I want to make one quick note and that is that Canada is also a major exporter of services.

10. The American “Dis”

We are a major exporter of services, but the fact is, if you look at the composition of what

we export, it is actually surprisingly low end. Manulife is a great example, but I can give

you many more examples of things that look like call centres in the Atlantic provinces.

So, we are much more on the low cost side of competition when it comes to our service

exports.

11. Canada: Wrong End of the Value Chain?

U.S. Imports of Offshored Services

All Offshored Services Royalties & License Fees

United Kingdom 20% Japan 26%

Bermuda 11% Germany 11%

Canada 10% Switzerland 10%

Germany 9% United Kingdom 8%

Japan 6% Netherlands 8%

France 5% Bermuda 7%

Switzerland 5% France 7%

Mexico 3% Canada 5%

Netherlands 3% Mexico 1%

Export-oriented FDI Projects Worldwide, 2002-2003

Country

Low Value

Added Country

High Value

Added

India 60 India 168

Canada 56 UK 144

UK 43 USA 108

China 30 China 102

Ireland 29 Singapore 79

Germany 20 Germany 57

Australia 19 Australia 53

Singapore 16 China & HK 51

USA 15 Ireland 48

China & HK 2 Canada 42

11

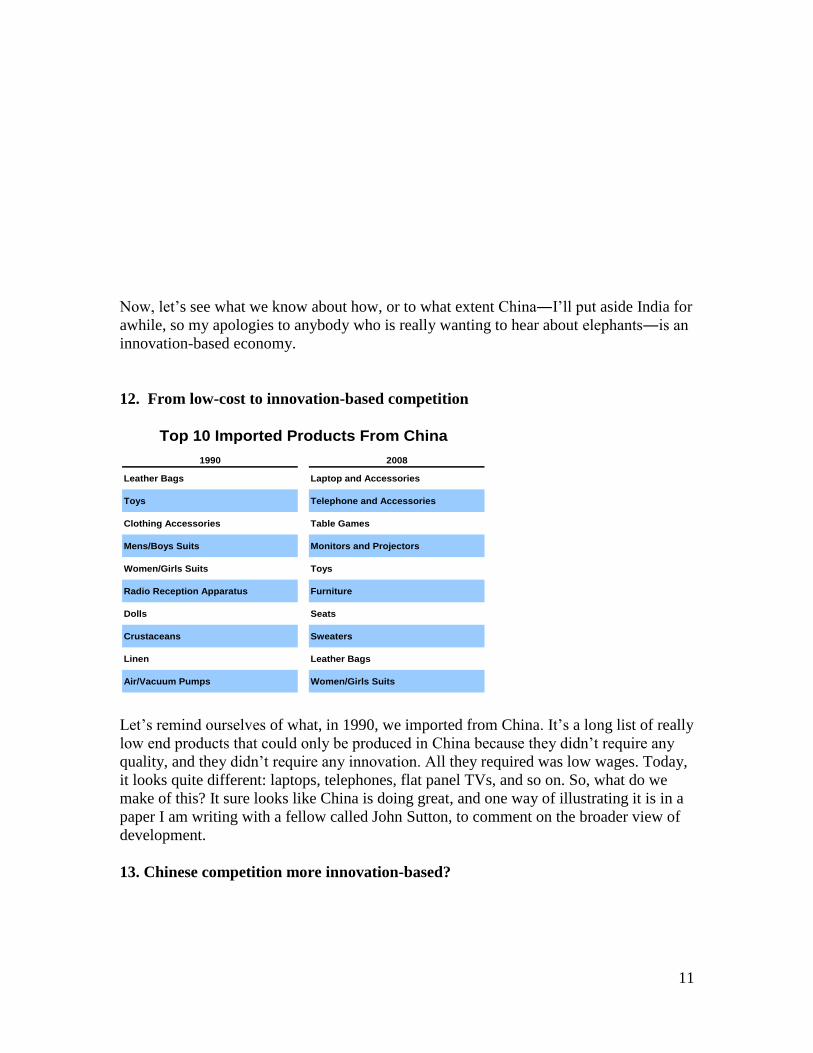

Now, let’s see what we know about how, or to what extent China―I’ll put aside India for

awhile, so my apologies to anybody who is really wanting to hear about elephants―is an

innovation-based economy.

12. From low-cost to innovation-based competition

Let’s remind ourselves of what, in 1990, we imported from China. It’s a long list of really

low end products that could only be produced in China because they didn’t require any

quality, and they didn’t require any innovation. All they required was low wages. Today,

it looks quite different: laptops, telephones, flat panel TVs, and so on. So, what do we

make of this? It sure looks like China is doing great, and one way of illustrating it is in a

paper I am writing with a fellow called John Sutton, to comment on the broader view of

development.

13. Chinese competition more innovation-based?

1990 2008

Leather Bags Laptop and Accessories

Toys Telephone and Accessories

Clothing Accessories Table Games

Mens/Boys Suits Monitors and Projectors

Women/Girls Suits Toys

Radio Reception Apparatus Furniture

Dolls Seats

Crustaceans Sweaters

Linen Leather Bags

Air/Vacuum Pumps Women/Girls Suits

35% of Total Imports from China 32% of Total Imports from China

Top 10 Imported Products From China

12

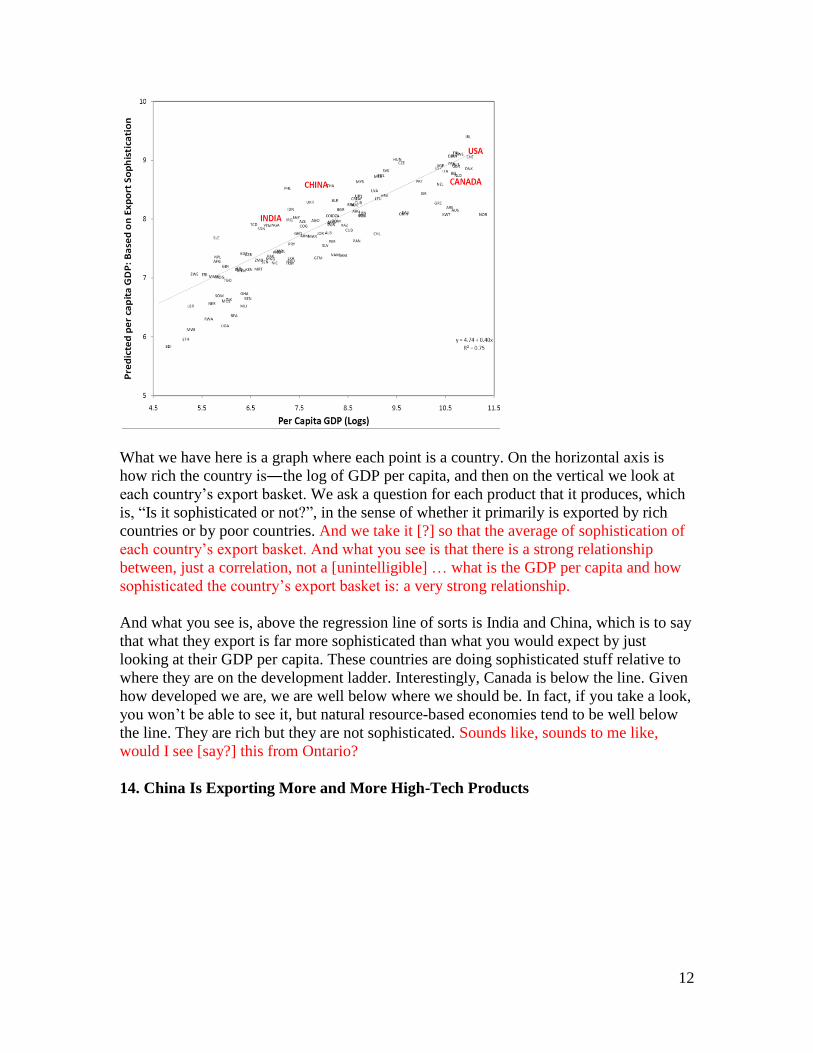

What we have here is a graph where each point is a country. On the horizontal axis is

how rich the country is―the log of GDP per capita, and then on the vertical we look at

each country’s export basket. We ask a question for each product that it produces, which

is, “Is it sophisticated or not?”, in the sense of whether it primarily is exported by rich

countries or by poor countries. And we take it [?] so that the average of sophistication of

each country’s export basket. And what you see is that there is a strong relationship

between, just a correlation, not a [unintelligible] … what is the GDP per capita and how

sophisticated the country’s export basket is: a very strong relationship.

And what you see is, above the regression line of sorts is India and China, which is to say

that what they export is far more sophisticated than what you would expect by just

looking at their GDP per capita. These countries are doing sophisticated stuff relative to

where they are on the development ladder. Interestingly, Canada is below the line. Given

how developed we are, we are well below where we should be. In fact, if you take a look,

you won’t be able to see it, but natural resource-based economies tend to be well below

the line. They are rich but they are not sophisticated. Sounds like, sounds to me like,

would I see [say?] this from Ontario?

14. China Is Exporting More and More High-Tech Products

13

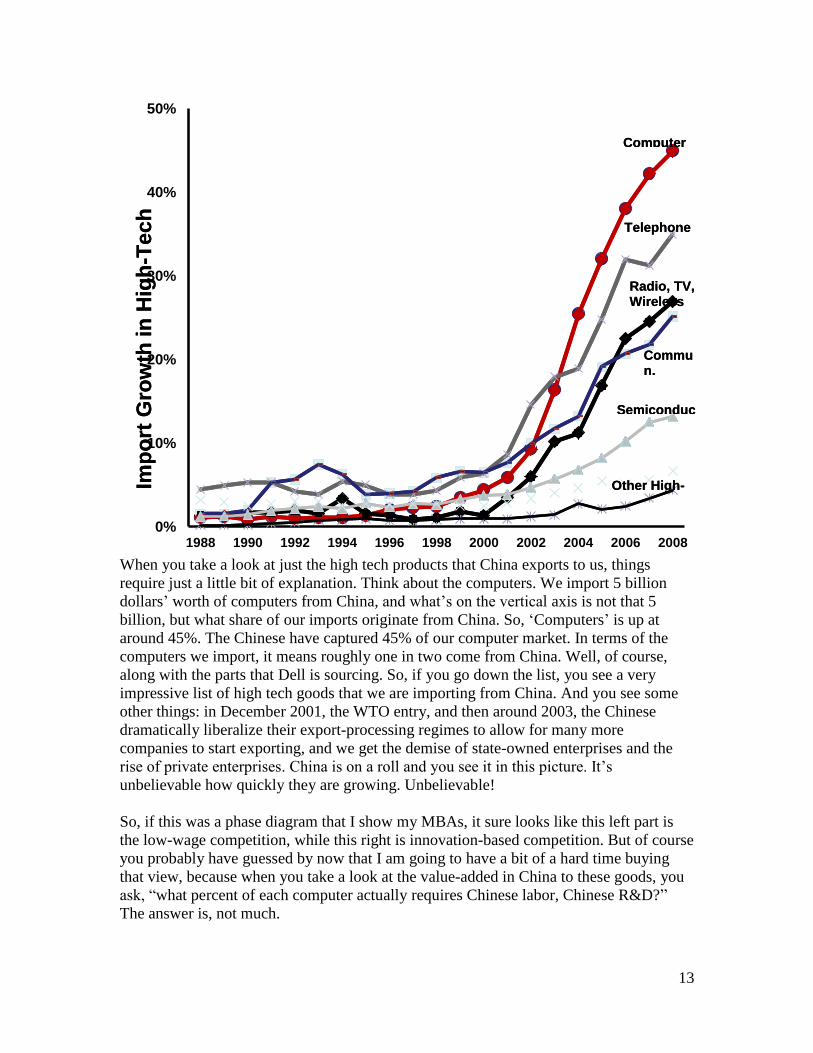

When you take a look at just the high tech products that China exports to us, things

require just a little bit of explanation. Think about the computers. We import 5 billion

dollars’ worth of computers from China, and what’s on the vertical axis is not that 5

billion, but what share of our imports originate from China. So, ‘Computers’ is up at

around 45%. The Chinese have captured 45% of our computer market. In terms of the

computers we import, it means roughly one in two come from China. Well, of course,

along with the parts that Dell is sourcing. So, if you go down the list, you see a very

impressive list of high tech goods that we are importing from China. And you see some

other things: in December 2001, the WTO entry, and then around 2003, the Chinese

dramatically liberalize their export-processing regimes to allow for many more

companies to start exporting, and we get the demise of state-owned enterprises and the

rise of private enterprises. China is on a roll and you see it in this picture. It’s

unbelievable how quickly they are growing. Unbelievable!

So, if this was a phase diagram that I show my MBAs, it sure looks like this left part is

the low-wage competition, while this right is innovation-based competition. But of course

you probably have guessed by now that I am going to have a bit of a hard time buying

that view, because when you take a look at the value-added in China to these goods, you

ask, “what percent of each computer actually requires Chinese labor, Chinese R&D?”

The answer is, not much.

0%

10%

20%

30%

40%

50%

1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008

Other High-

ComputerIm

po

rt G

row

th in

Hig

h-T

ech

Radio, TV, Wireless

Semiconduc

Telephone

Commun.

Other High-

ComputerIm

po

rt G

row

th in

Hig

h-T

ech

Radio, TV, Wireless

Semiconduc

Telephone

Commun.

14

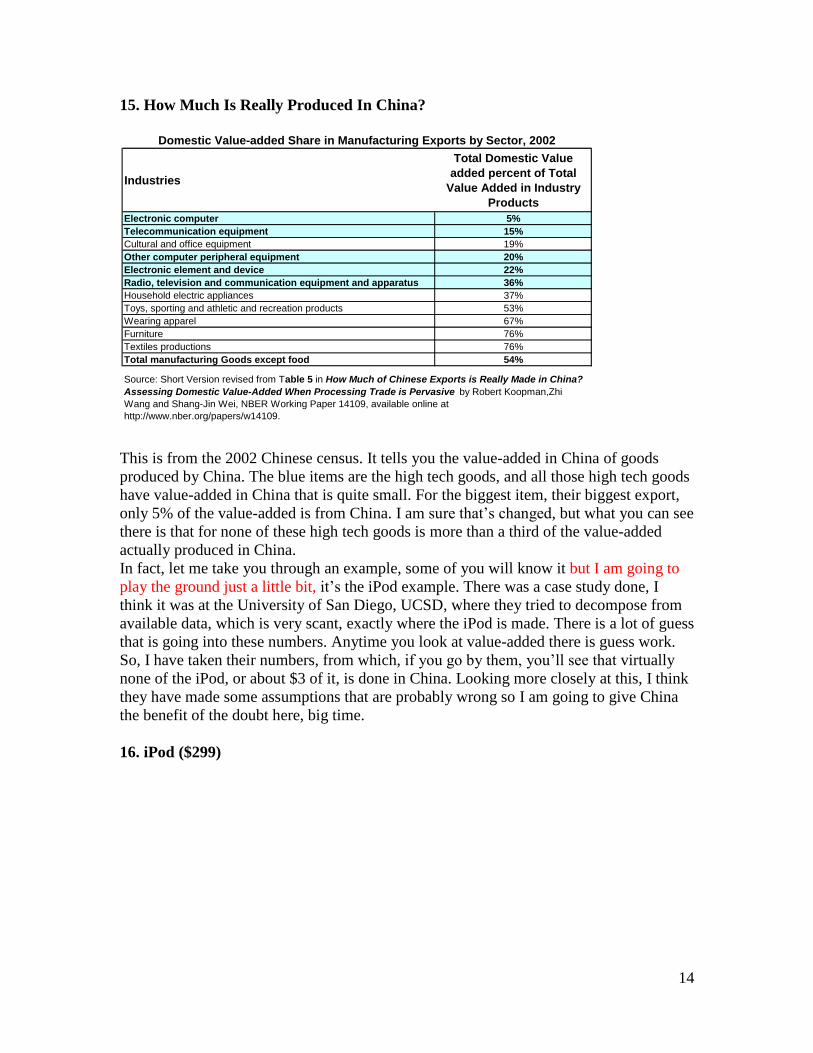

15. How Much Is Really Produced In China?

This is from the 2002 Chinese census. It tells you the value-added in China of goods

produced by China. The blue items are the high tech goods, and all those high tech goods

have value-added in China that is quite small. For the biggest item, their biggest export,

only 5% of the value-added is from China. I am sure that’s changed, but what you can see

there is that for none of these high tech goods is more than a third of the value-added

actually produced in China.

In fact, let me take you through an example, some of you will know it but I am going to

play the ground just a little bit, it’s the iPod example. There was a case study done, I

think it was at the University of San Diego, UCSD, where they tried to decompose from

available data, which is very scant, exactly where the iPod is made. There is a lot of guess

that is going into these numbers. Anytime you look at value-added there is guess work.

So, I have taken their numbers, from which, if you go by them, you’ll see that virtually

none of the iPod, or about $3 of it, is done in China. Looking more closely at this, I think

they have made some assumptions that are probably wrong so I am going to give China

the benefit of the doubt here, big time.

16. iPod ($299)

Industries

Total Domestic Value

added percent of Total

Value Added in Industry

Products

Electronic computer 5%

Telecommunication equipment 15%

Cultural and office equipment 19%

Other computer peripheral equipment 20%

Electronic element and device 22%

Radio, television and communication equipment and apparatus 36%

Household electric appliances 37%

Toys, sporting and athletic and recreation products 53%

Wearing apparel 67%

Furniture 76%

Textiles productions 76%

Total manufacturing Goods except food 54%

Source: Short Version revised from Table 5 in How Much of Chinese Exports is Really Made in China?

Assessing Domestic Value-Added When Processing Trade is Pervasive by Robert Koopman,Zhi

Wang and Shang-Jin Wei, NBER Working Paper 14109, available online at

http://www.nber.org/papers/w14109.

Domestic Value-added Share in Manufacturing Exports by Sector, 2002

15

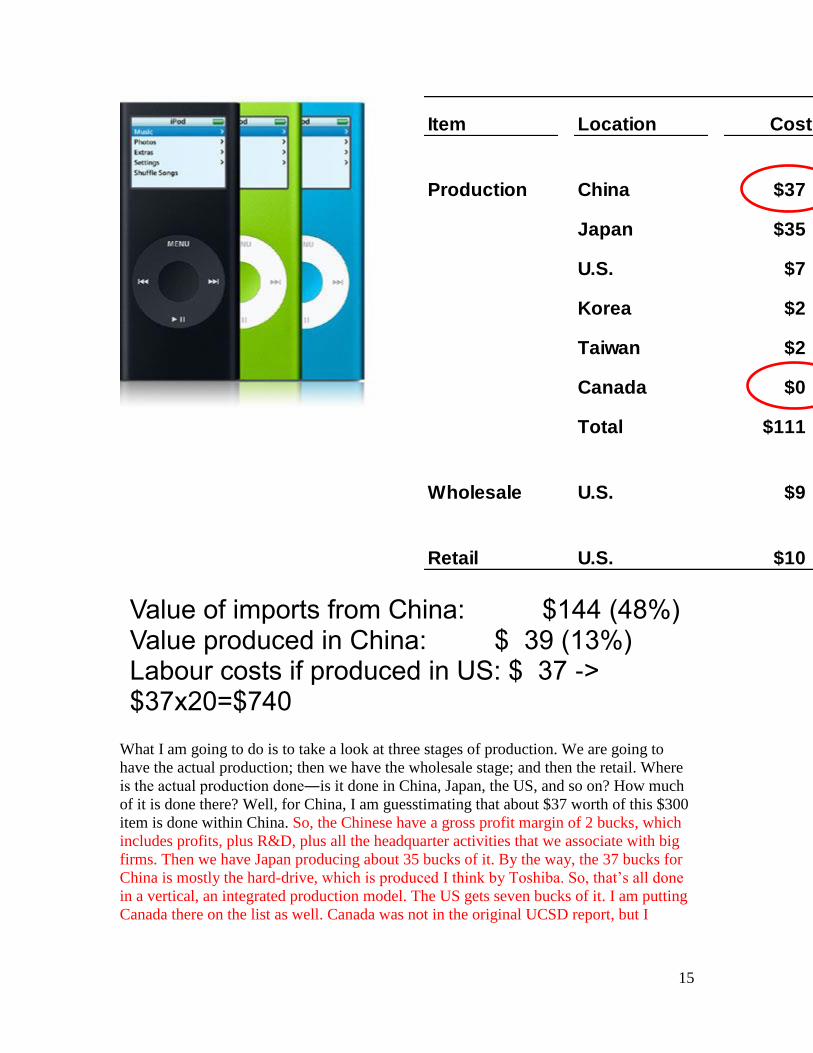

What I am going to do is to take a look at three stages of production. We are going to

have the actual production; then we have the wholesale stage; and then the retail. Where

is the actual production done―is it done in China, Japan, the US, and so on? How much

of it is done there? Well, for China, I am guesstimating that about $37 worth of this $300

item is done within China. So, the Chinese have a gross profit margin of 2 bucks, which

includes profits, plus R&D, plus all the headquarter activities that we associate with big

firms. Then we have Japan producing about 35 bucks of it. By the way, the 37 bucks for

China is mostly the hard-drive, which is produced I think by Toshiba. So, that’s all done

in a vertical, an integrated production model. The US gets seven bucks of it. I am putting

Canada there on the list as well. Canada was not in the original UCSD report, but I

Value of imports from China: $144 (48%) Value produced in China: $ 39 (13%)

Labour costs if produced in US: $ 37 -> $37x20=$740

Item Location Cost Gross Profit

Production China $37 $2

Japan $35 $24

U.S. $7 $7

Korea $2 $1

Taiwan $2 $0

Canada $0 $0

Total $111 $33

Wholesale U.S. $9 $71

Retail U.S. $10 $65

16

thought it worthwhile just mentioning what Canada’s contribution to the iPod

was―absolutely zip.

Okay, then we move to the wholesale and retail margins, and of course that’s where the

big bucks are, where Apple makes its money. So, there are a few points that I want you to

take away from this. The first one comes in the production cost, you see it is $111 per

$33? So that $144, that means that when we import this good from China, it shows up in

our trade statistics as if we bought $144 from China. In fact, we bought $39 from China,

$37 plus $2. So, while it looks like the Chinese are sophisticated, because we are buying

an iPod made in China, almost none of it was made in China. Not even the outer casing,

which was designed by Taiwanese firms.

The second thing I want you to think about is the following: suppose that the US had

closed off its borders and said, “You have to make this iPod with American labour, in

particular, anything that you previously did in China, you’ve got to do in the United

States?” Chinese manufacturing wages are about $1 an hour, maybe a buck-50. So, $37 is

about equal to 37 hours. In the US, 37 hours times 20 bucks an hour is $740. We’ve just

jacked up the cost of iPods to roughly $1,000. If this was produced in the United States or

Canada, we are talking about something that is close to $1,000. Is anybody going to buy

an iPod for $1000? I’d rather carry a laptop on my back. So we can whine about the rise

of low cost destinations like China, but the fact is it allows us to do things that we

couldn’t have done without it. It is a big welfare loss for American workers, but not as

big as you think, because some of the stuff just wouldn’t happen otherwise. There would

never be American jobs producing an iPod, it just would not be.

So, yes, there are implications for American and Canadian workers and I don’t minimize

that in the least. But there are also things that happen for consumers, and that has to be

balanced against the cost to workers.

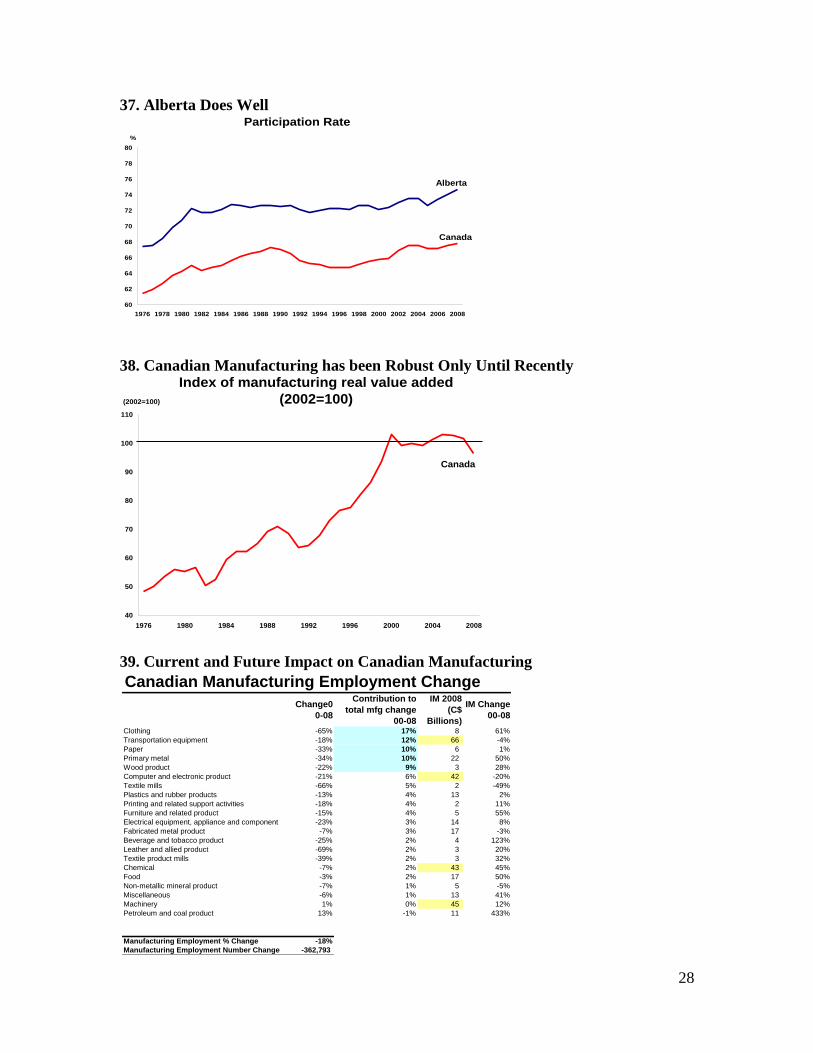

17. Canadian Manufacturing Value Added

17

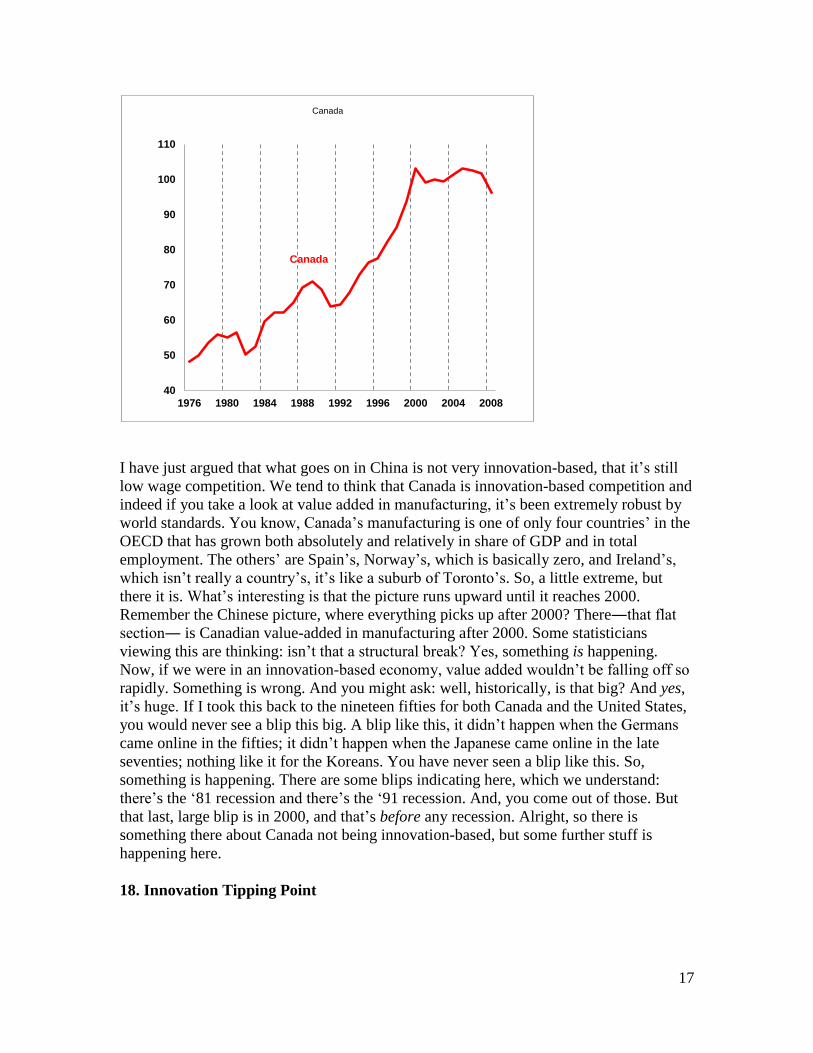

I have just argued that what goes on in China is not very innovation-based, that it’s still

low wage competition. We tend to think that Canada is innovation-based competition and

indeed if you take a look at value added in manufacturing, it’s been extremely robust by

world standards. You know, Canada’s manufacturing is one of only four countries’ in the

OECD that has grown both absolutely and relatively in share of GDP and in total

employment. The others’ are Spain’s, Norway’s, which is basically zero, and Ireland’s,

which isn’t really a country’s, it’s like a suburb of Toronto’s. So, a little extreme, but

there it is. What’s interesting is that the picture runs upward until it reaches 2000.

Remember the Chinese picture, where everything picks up after 2000? There―that flat

section― is Canadian value-added in manufacturing after 2000. Some statisticians

viewing this are thinking: isn’t that a structural break? Yes, something is happening.

Now, if we were in an innovation-based economy, value added wouldn’t be falling off so

rapidly. Something is wrong. And you might ask: well, historically, is that big? And yes,

it’s huge. If I took this back to the nineteen fifties for both Canada and the United States,

you would never see a blip this big. A blip like this, it didn’t happen when the Germans

came online in the fifties; it didn’t happen when the Japanese came online in the late

seventies; nothing like it for the Koreans. You have never seen a blip like this. So,

something is happening. There are some blips indicating here, which we understand:

there’s the ‘81 recession and there’s the ‘91 recession. And, you come out of those. But

that last, large blip is in 2000, and that’s before any recession. Alright, so there is

something there about Canada not being innovation-based, but some further stuff is

happening here.

18. Innovation Tipping Point

40

50

60

70

80

90

100

110

1976 1980 1984 1988 1992 1996 2000 2004 2008

Canada

Canada

18

So, let me come to the innovation tipping point. I

want to emphasize, the innovation tipping point says

that there is a number of drivers of innovation.

Institutions matter, you are protecting property

rights, protecting private contracts, preventing the

firms from being expropriated by local government,

so there is all sort of things that are important for

investor protections.

Another driver, and from a business school perspective, one we tend to emphasize, is this

sort of proletarian idea of sophisticated consumers, who are providing pressure to

innovate, and sophisticated input suppliers who are providing the support for that

innovation. And there will come a time when China is going to be a sophisticated

innovator. What is my prediction of what will happen when that does come?

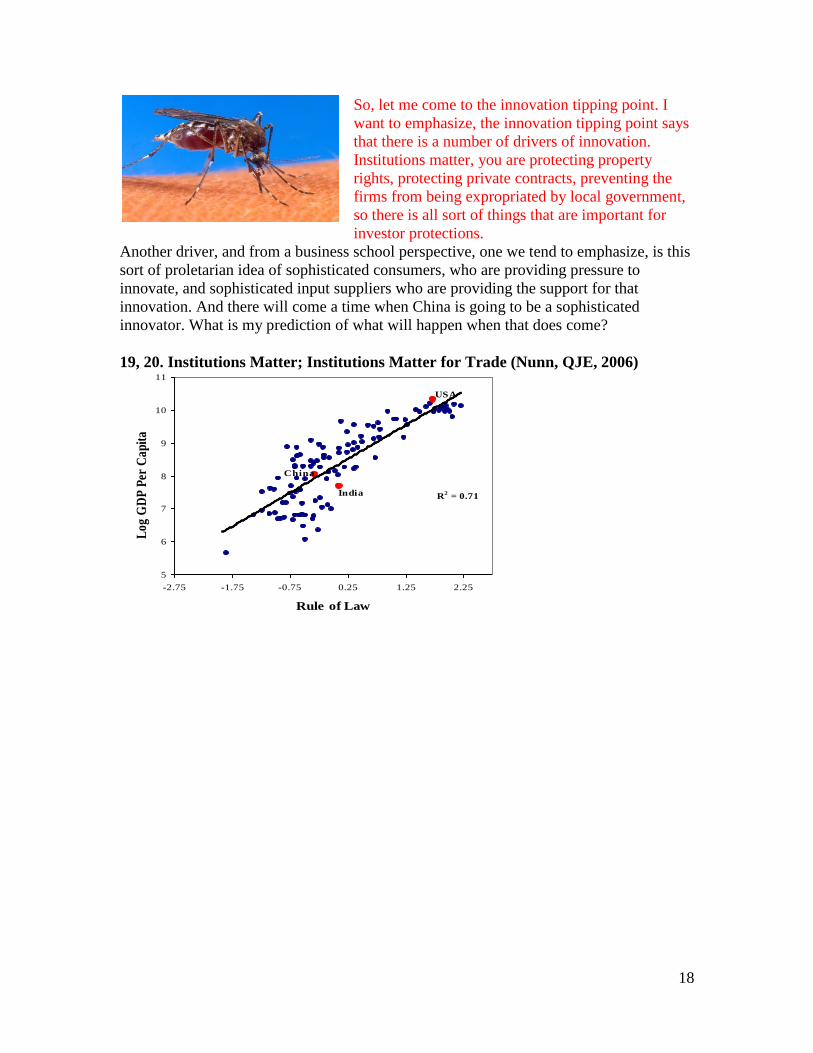

19, 20. Institutions Matter; Institutions Matter for Trade (Nunn, QJE, 2006)

R2 = 0.71

5

6

7

8

9

10

11

-2.75 -1.75 -0.75 0.25 1.25 2.25

Rule of Law

Lo

g G

DP

Per

Ca

pit

a

India

China

USA

19

First of all, how long is it going to take? Well, for it to happen, institutions in China and

India would have to improve dramatically, and I would love to talk about that at length,

but the bottom line is that no country has ever changed its core institutions rapidly. Hong

Kong did something remarkable in the sixties, but you can look across the almost two

hundred countries in existence on the planet, and none of them have transformed their

institutions in anything other than what could be called a glacial pace in history. So, for

China and India to change their institutions to promote innovation, we are talking about

decades― twenty years, thirty years. But the time will come when they join the

innovation club.

What will happen when that occurs? Well, the same thing will happen when they join as

happened when Japan, another low wage economy in the ‘fifties, joined; or when Korea,

a further low wage economy with a devalued currency, joined; or when Taiwan,

Singapore, and so on, joined. There were ripples, and then we adjusted. China would take

us a little bit longer to adjust to, because they have a policy of keeping the Yuan heavily

devalued. Korea did the same thing, but China is taking it to new lengths. So, there will

come a tipping point, but only when it comes. First, it’s going to be far off. And, it will

not do anything dramatic to the world economy. China will be another player in the

innovation game, just as other low wage economies have become other players.

What worries me more is that Canada is losing its position as an innovator, not because

of China or India, but because of government policies and business attitudes towards

innovation which are, frankly, second class. So, I want to show you a series of slides

Standardized Complex, Contract-Intensive

Qu

ality

of

a

Co

un

try’s

Type of Good Exported

= 0.40

t = 6.37

20

which tell us that what’s going on in China and India is not nearly as dramatic as you

think, by looking at R&D, looking at numbers of engineers, looking at patents.

21. China outperforms Canada in BERD in 2007

What’s going on is not nearly what you think either, but, what is going on in Canada is

probably more depressing than what’s going on in China. So, let’s start with R&D. I want

to focus on business R&D because that’s where Canada is really, really pathetic. So, the

black lines are 1997, the blue lines are 2007. In 2007, Japan is the world leader in

business R&D, and companies like Toyota are treading [?spending?] buckets. The United

States, Germany, the countries you would expect, are the big leaders in R&D. Whereas in

Canada, we are sitting: we are spending 1.1% of GDP on business R&D, compared to a

sort of world class standard of 2 %, almost twice that. And we remain stagnant out there,

not going anywhere. There is one country here that has changed dramatically, going from

nowhere to Canadian levels, and that is China. So, something is happening in China that

should be embarrassing to Canada. There is no reason why we should be at 1.1%.

22. Laughing Stock of the OECD

We can look now rather at all R&D, not just business R&D. Let’s consider government

R&D and university R&D, which is huge in Canada―thank goodness for the federal

government. You still see that Canada is what I call the laughing stock of the OECD. I

wrote a report for this for the Canadian government and I was told that I had to take that

terminology out, the minister wouldn’t like it. But, the minister needs to hear it, frankly; I

BERD as a percentage of GDP

1.1%

0.0

0.5

1.0

1.5

2.0

2.5

3.0

Japa

n

Unite

d Sta

tes

Ger

man

y

Franc

e

Belgium

Austra

lia

Unite

d Kin

gdom

EU27

China

Can

ada

Net

herla

nds

Italy

1997

%

2007

Israel

Sweden

Finland

Japan

Korea

Switzerland

Iceland

United States

Taiwan

Germany

Denmark

Austria

Singapore

France

Canada

China

Ireland

1.0% 2.0% 3.0% 4.0%

Israel

Sw eden

Finland

Japan

Korea

Sw itzerland

Iceland

United States

Taiw an

Germany

Denmark

Austria

Singapore

France

Canada

China

Ireland

21

should have said no, that is exactly what needs to be said. We are 15th

in the world in

terms of R&D expenditures per capita, and it’s an embarrassment. China is quickly

catching up with us.

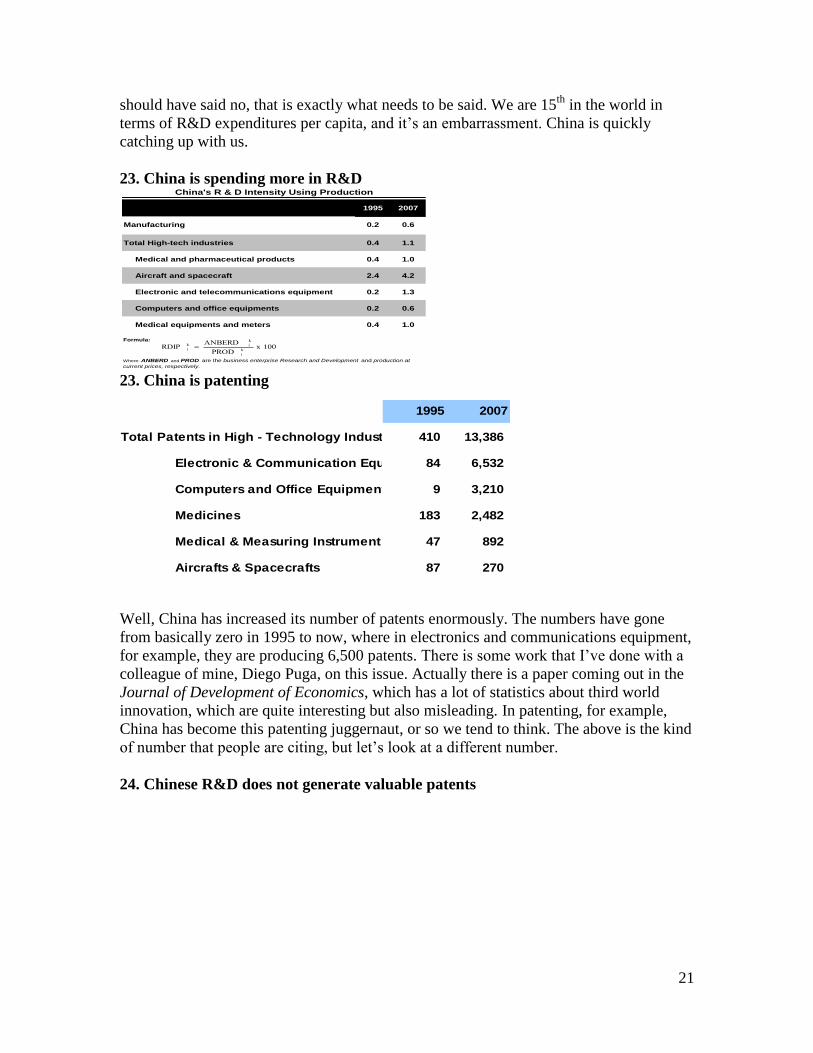

23. China is spending more in R&D

23. China is patenting

Well, China has increased its number of patents enormously. The numbers have gone

from basically zero in 1995 to now, where in electronics and communications equipment,

for example, they are producing 6,500 patents. There is some work that I’ve done with a

colleague of mine, Diego Puga, on this issue. Actually there is a paper coming out in the

Journal of Development of Economics, which has a lot of statistics about third world

innovation, which are quite interesting but also misleading. In patenting, for example,

China has become this patenting juggernaut, or so we tend to think. The above is the kind

of number that people are citing, but let’s look at a different number.

24. Chinese R&D does not generate valuable patents

1995 2007

Manufacturing 0.2 0.6

Total High-tech industries 0.4 1.1

Medical and pharmaceutical products 0.4 1.0

Aircraft and spacecraft 2.4 4.2

Electronic and telecommunications equipment 0.2 1.3

Computers and office equipments 0.2 0.6

Medical equipments and meters 0.4 1.0

Formula:

China's R & D Intensity Using Production

Where: ANBERD and PROD are the business enterprise Research and Development and production at

current prices, respectively.

100 x k

i

k

ik

i PROD

ANBERD=RDIP

1995 2007

Total Patents in High - Technology Industries 410 13,386

Electronic & Communication Equipment84 6,532

Computers and Office Equipment 9 3,210

Medicines 183 2,482

Medical & Measuring Instrument 47 892

Aircrafts & Spacecrafts 87 270

22

We know that the vast majority of patents are junk, right? A very cursory way of

checking whether a patent is worth anything, and this is sort of a minimum criteria, is that

you had better have taken the patent out in Japan, the EU and US. Because, if you haven’t

taken it out in all three of those locations, it’s probably not worth anything. So, let’s just

look at the patents that have been taken out in all three locations. When you do that, each

point is then a country and the horizontal axis is how much R&D that country is doing

and inputting into patenting. Then, over here on the vertical axis is how many patents are

listed in all three patent offices. And, what you see is that China is way off the trend.

They are doing lots of R&D, they’re doing lots of patenting, but they are not doing lots of

patenting that warrants being listed on all three markets, in all three offices. And in fact,

I’ve read through every patent that China has taken out in the United States. It’s

extraordinary how many of them are literally better mouth traps, or can openers, a better

design for a light fixture―just complete nonsense.

So, don’t let the patent numbers scare you, and don’t let the engineering numbers scare

you either. Let me take you through these, because people really misunderstand the

engineering numbers.

25. Is This Turning Point Happening in China?

23

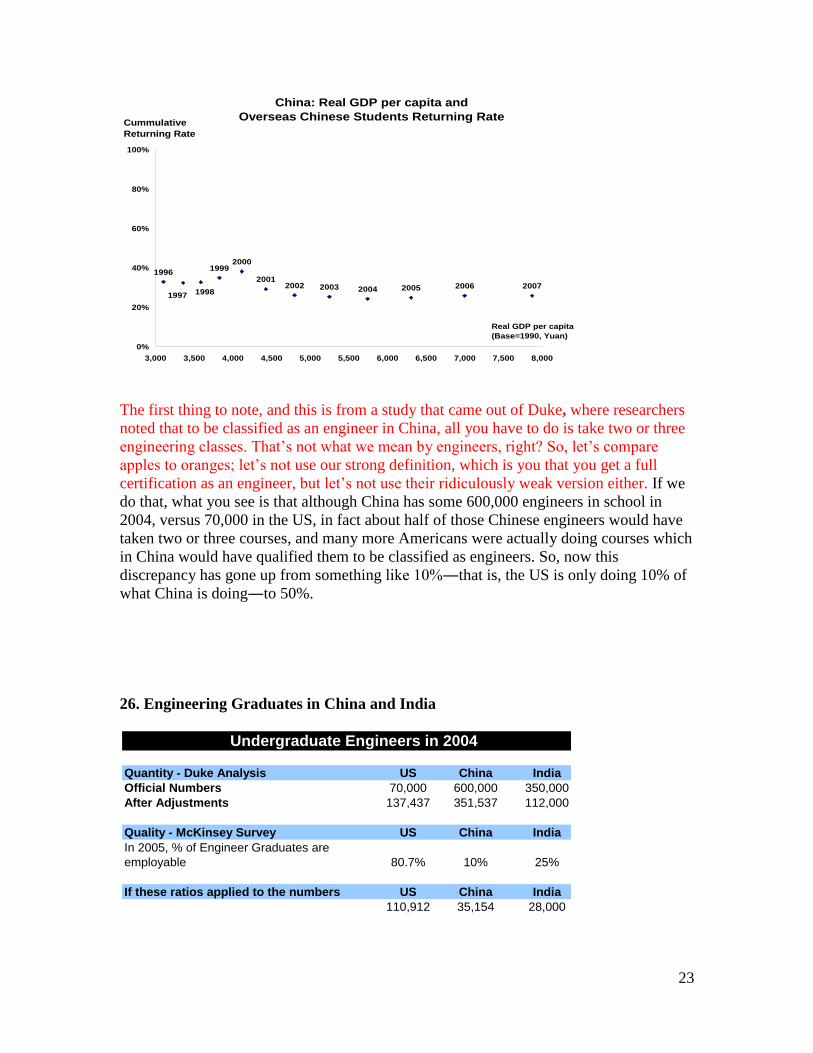

The first thing to note, and this is from a study that came out of Duke, where researchers

noted that to be classified as an engineer in China, all you have to do is take two or three

engineering classes. That’s not what we mean by engineers, right? So, let’s compare

apples to oranges; let’s not use our strong definition, which is you that you get a full

certification as an engineer, but let’s not use their ridiculously weak version either. If we

do that, what you see is that although China has some 600,000 engineers in school in

2004, versus 70,000 in the US, in fact about half of those Chinese engineers would have

taken two or three courses, and many more Americans were actually doing courses which

in China would have qualified them to be classified as engineers. So, now this

discrepancy has gone up from something like 10%―that is, the US is only doing 10% of

what China is doing―to 50%.

26. Engineering Graduates in China and India

China: Real GDP per capita and

Overseas Chinese Students Returning Rate

1996

1997 1998

19992000

20012002 2003 2004 2005 2006 2007

0%

20%

40%

60%

80%

100%

3,000 3,500 4,000 4,500 5,000 5,500 6,000 6,500 7,000 7,500 8,000

Cummulative

Returning Rate

Real GDP per capita

(Base=1990, Yuan)

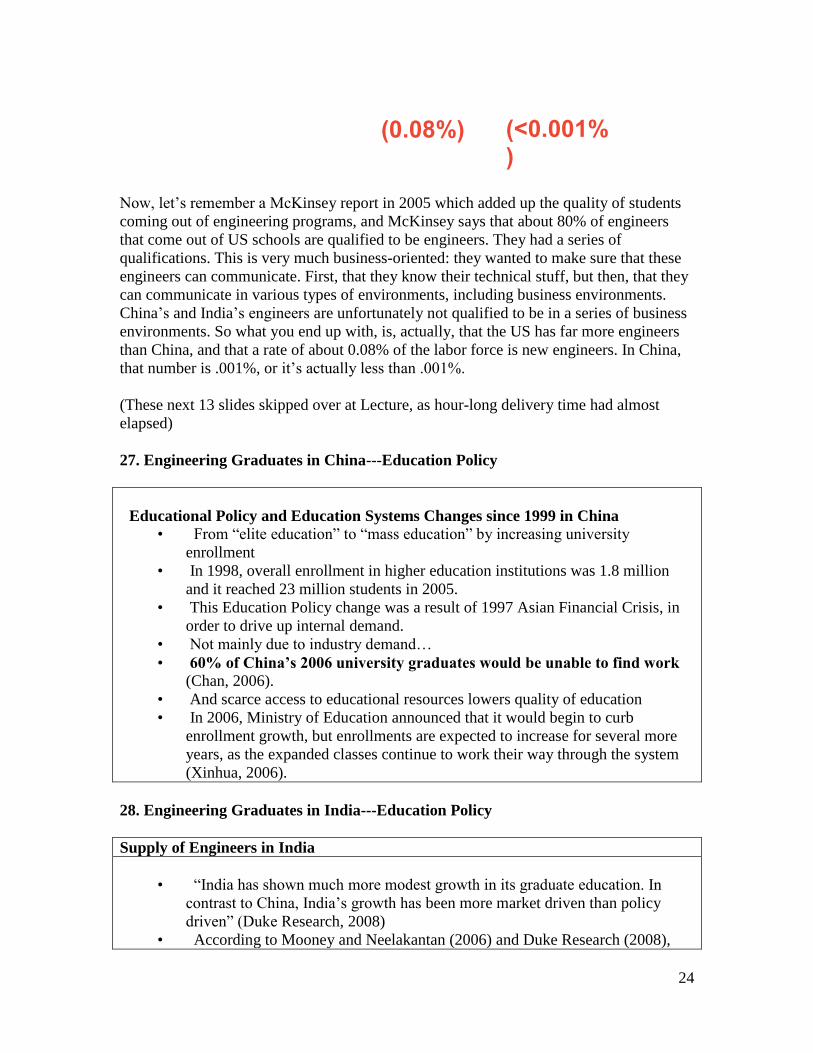

Quantity - Duke Analysis US China India

Official Numbers 70,000 600,000 350,000

After Adjustments 137,437 351,537 112,000

Quality - McKinsey Survey US China India

In 2005, % of Engineer Graduates are

employable 80.7% 10% 25%

If these ratios applied to the numbers US China India

110,912 35,154 28,000

Undergraduate Engineers in 2004

24

Now, let’s remember a McKinsey report in 2005 which added up the quality of students

coming out of engineering programs, and McKinsey says that about 80% of engineers

that come out of US schools are qualified to be engineers. They had a series of

qualifications. This is very much business-oriented: they wanted to make sure that these

engineers can communicate. First, that they know their technical stuff, but then, that they

can communicate in various types of environments, including business environments.

China’s and India’s engineers are unfortunately not qualified to be in a series of business

environments. So what you end up with, is, actually, that the US has far more engineers

than China, and that a rate of about 0.08% of the labor force is new engineers. In China,

that number is .001%, or it’s actually less than .001%.

(These next 13 slides skipped over at Lecture, as hour-long delivery time had almost

elapsed)

27. Engineering Graduates in China---Education Policy

Educational Policy and Education Systems Changes since 1999 in China • From “elite education” to “mass education” by increasing university

enrollment

• In 1998, overall enrollment in higher education institutions was 1.8 million

and it reached 23 million students in 2005.

• This Education Policy change was a result of 1997 Asian Financial Crisis, in

order to drive up internal demand.

• Not mainly due to industry demand…

• 60% of China’s 2006 university graduates would be unable to find work (Chan, 2006).

• And scarce access to educational resources lowers quality of education

• In 2006, Ministry of Education announced that it would begin to curb

enrollment growth, but enrollments are expected to increase for several more

years, as the expanded classes continue to work their way through the system

(Xinhua, 2006).

28. Engineering Graduates in India---Education Policy

Supply of Engineers in India

• “India has shown much more modest growth in its graduate education. In

contrast to China, India’s growth has been more market driven than policy

driven” (Duke Research, 2008)

• According to Mooney and Neelakantan (2006) and Duke Research (2008),

(<0.001%)

(0.08%)

25

India has nearly one million unemployed engineers.

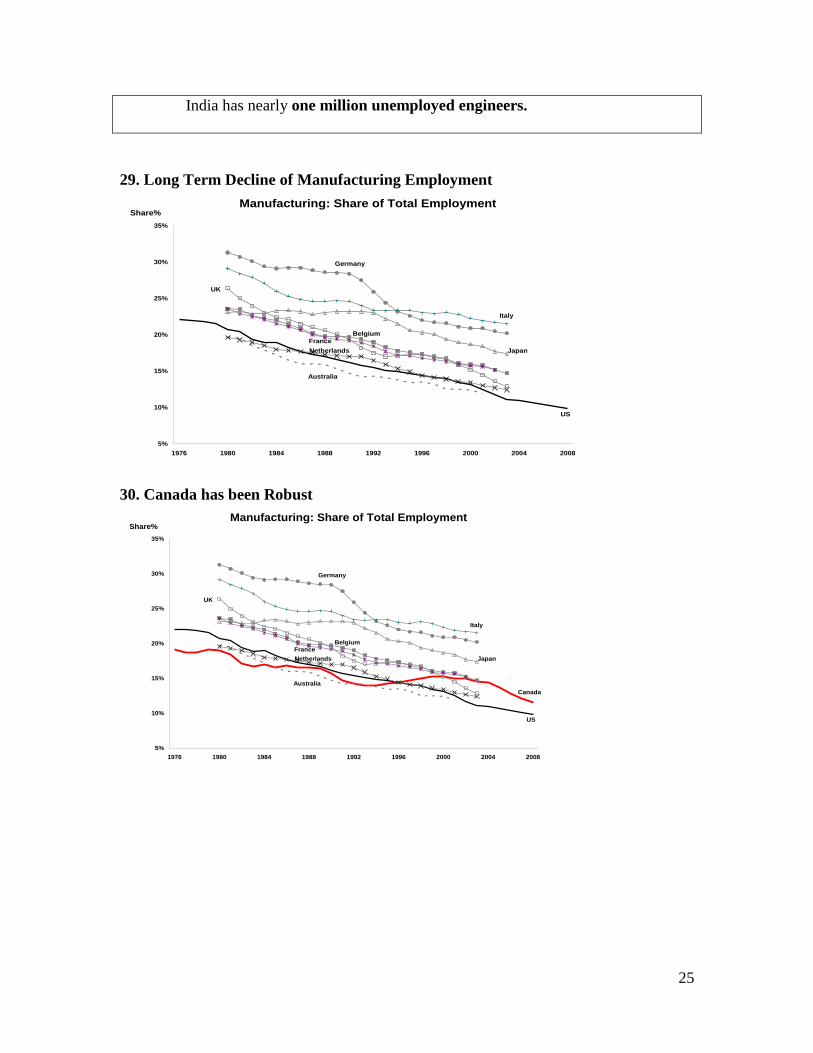

29. Long Term Decline of Manufacturing Employment

30. Canada has been Robust

Manufacturing: Share of Total Employment

5%

10%

15%

20%

25%

30%

35%

1976 1980 1984 1988 1992 1996 2000 2004 2008

US

Australia

Germany

Italy

Japan

UK

BelgiumFrance

Share%

Netherlands

Manufacturing: Share of Total Employment

5%

10%

15%

20%

25%

30%

35%

1976 1980 1984 1988 1992 1996 2000 2004 2008

Canada

US

Australia

Germany

Italy

Japan

UK

BelgiumFrance

Share%

Netherlands

26

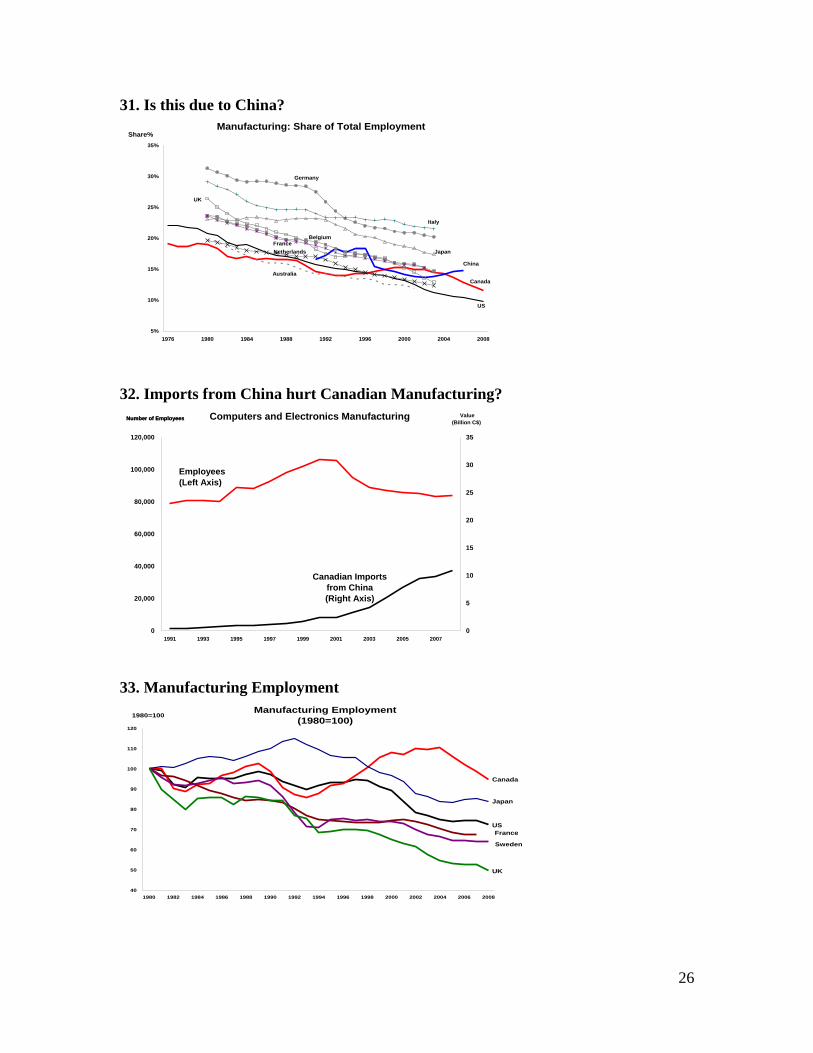

31. Is this due to China?

32. Imports from China hurt Canadian Manufacturing?

33. Manufacturing Employment

Manufacturing: Share of Total Employment

5%

10%

15%

20%

25%

30%

35%

1976 1980 1984 1988 1992 1996 2000 2004 2008

Canada

US

Australia

Germany

Italy

Japan

UK

BelgiumFrance

Share%

Netherlands

China

Computers and Electronics Manufacturing

0

20,000

40,000

60,000

80,000

100,000

120,000

1991 1993 1995 1997 1999 2001 2003 2005 2007

0

5

10

15

20

25

30

35

Number of Employees Value

(Billion C$)

Employees

(Left Axis)

Canadian Imports

from China

(Right Axis)

Number of Employees

Manufacturing Employment

(1980=100)

40

50

60

70

80

90

100

110

120

1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008

1980=100

US

Canada

UK

Japan

Sweden

France

27

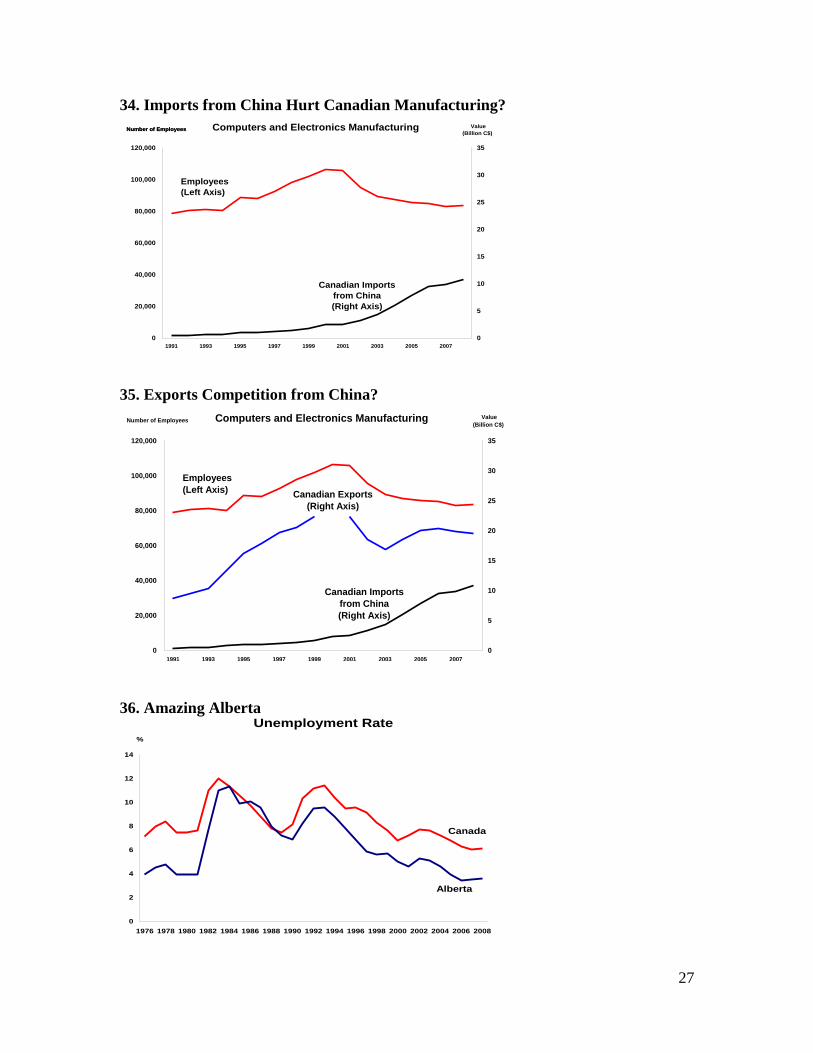

34. Imports from China Hurt Canadian Manufacturing?

35. Exports Competition from China?

36. Amazing Alberta

Computers and Electronics Manufacturing

0

20,000

40,000

60,000

80,000

100,000

120,000

1991 1993 1995 1997 1999 2001 2003 2005 2007

0

5

10

15

20

25

30

35

Number of Employees Value

(Billion C$)

Employees

(Left Axis)

Canadian Imports

from China

(Right Axis)

Number of Employees

Computers and Electronics Manufacturing

0

20,000

40,000

60,000

80,000

100,000

120,000

1991 1993 1995 1997 1999 2001 2003 2005 2007

0

5

10

15

20

25

30

35

Canadian Exports

(Right Axis)

Number of Employees Value

(Billion C$)

Employees

(Left Axis)

Canadian Imports

from China

(Right Axis)

Unemployment Rate

0

2

4

6

8

10

12

14

1976 1978 1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008

Canada

Alberta

%

28

37. Alberta Does Well

38. Canadian Manufacturing has been Robust Only Until Recently

39. Current and Future Impact on Canadian Manufacturing

Participation Rate

60

62

64

66

68

70

72

74

76

78

80

1976 1978 1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008

Canada

Alberta

%

40

50

60

70

80

90

100

110

1976 1980 1984 1988 1992 1996 2000 2004 2008

Index of manufacturing real value added

(2002=100)

Canada

(2002=100)

Change0

0-08

Contribution to

total mfg change

00-08

IM 2008

(C$

Billions)

IM Change

00-08

Clothing -65% 17% 8 61%

Transportation equipment -18% 12% 66 -4%

Paper -33% 10% 6 1%

Primary metal -34% 10% 22 50%

Wood product -22% 9% 3 28%

Computer and electronic product -21% 6% 42 -20%

Textile mills -66% 5% 2 -49%

Plastics and rubber products -13% 4% 13 2%

Printing and related support activities -18% 4% 2 11%

Furniture and related product -15% 4% 5 55%

Electrical equipment, appliance and component -23% 3% 14 8%

Fabricated metal product -7% 3% 17 -3%

Beverage and tobacco product -25% 2% 4 123%

Leather and allied product -69% 2% 3 20%

Textile product mills -39% 2% 3 32%

Chemical -7% 2% 43 45%

Food -3% 2% 17 50%

Non-metallic mineral product -7% 1% 5 -5%

Miscellaneous -6% 1% 13 41%

Machinery 1% 0% 45 12%

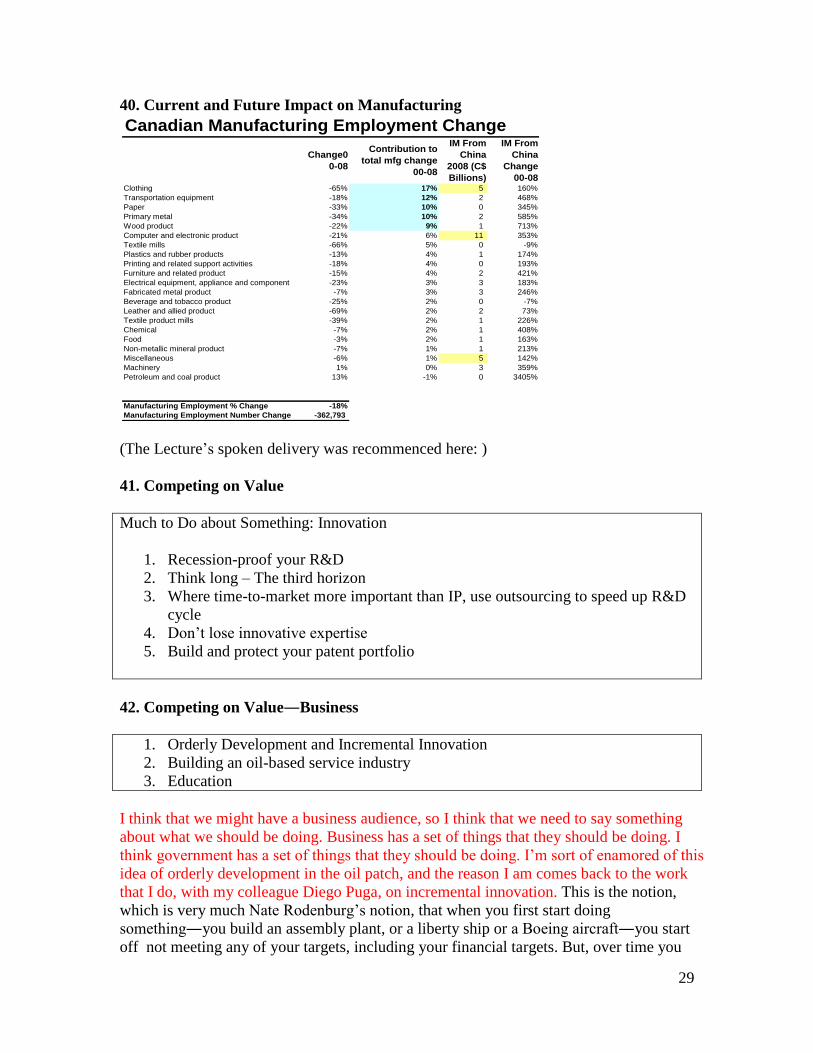

Petroleum and coal product 13% -1% 11 433%

Manufacturing Employment % Change -18%

Manufacturing Employment Number Change -362,793

Canadian Manufacturing Employment Change

29

40. Current and Future Impact on Manufacturing

(The Lecture’s spoken delivery was recommenced here: )

41. Competing on Value

Much to Do about Something: Innovation

1. Recession-proof your R&D

2. Think long – The third horizon

3. Where time-to-market more important than IP, use outsourcing to speed up R&D

cycle

4. Don’t lose innovative expertise

5. Build and protect your patent portfolio

42. Competing on Value―Business

1. Orderly Development and Incremental Innovation

2. Building an oil-based service industry

3. Education

I think that we might have a business audience, so I think that we need to say something

about what we should be doing. Business has a set of things that they should be doing. I

think government has a set of things that they should be doing. I’m sort of enamored of this

idea of orderly development in the oil patch, and the reason I am comes back to the work

that I do, with my colleague Diego Puga, on incremental innovation. This is the notion,

which is very much Nate Rodenburg’s notion, that when you first start doing

something―you build an assembly plant, or a liberty ship or a Boeing aircraft―you start

off not meeting any of your targets, including your financial targets. But, over time you

Change0

0-08

Contribution to

total mfg change

00-08

IM From

China

2008 (C$

Billions)

IM From

China

Change

00-08Clothing -65% 17% 5 160%

Transportation equipment -18% 12% 2 468%

Paper -33% 10% 0 345%

Primary metal -34% 10% 2 585%

Wood product -22% 9% 1 713%

Computer and electronic product -21% 6% 11 353%

Textile mills -66% 5% 0 -9%

Plastics and rubber products -13% 4% 1 174%

Printing and related support activities -18% 4% 0 193%

Furniture and related product -15% 4% 2 421%

Electrical equipment, appliance and component -23% 3% 3 183%

Fabricated metal product -7% 3% 3 246%

Beverage and tobacco product -25% 2% 0 -7%

Leather and allied product -69% 2% 2 73%

Textile product mills -39% 2% 1 226%

Chemical -7% 2% 1 408%

Food -3% 2% 1 163%

Non-metallic mineral product -7% 1% 1 213%

Miscellaneous -6% 1% 5 142%

Machinery 1% 0% 3 359%

Petroleum and coal product 13% -1% 0 3405%

Manufacturing Employment % Change -18%

Manufacturing Employment Number Change -362,793

Canadian Manufacturing Employment Change

30

look at all the bugs, and if you’re really good, you design your assembly so that you can

work out the bugs on the fly. Boeing knew, when it produced the 747, that it was going to

stretch its plane; it knew that it was going to double its capacity even before it put out its

first one. So you “design-in” the notion that you’ll improve over time. But where the

trouble comes in with orderly development is when you start building, say, four upgraders

at once. I don’t if that is the number for upgraders, I’m winging it here, but when you start

doing everything at once, you’re not gaining the benefits of seeing what had been the

previous state of the art. Everybody’s replicating, and you’re losing an enormous

opportunity for incremental innovation. Incremental innovation is the heart and soul of

innovation, vastly more important by all estimates than lab-coated technicians coming up

with brilliant ideas. It’s the day-to-day shop floor activities that matter for producing

productivity gains. “Disorderly development” is perhaps too emotive of a term, but the

current rapid pace of development precludes, locks you in ways that prevent you, from

benefitting from that incremental innovation. And that is a way for government― to try to

force firms to internalize what is essentially an externality.

43. Public Spending on Education in Canada Lags

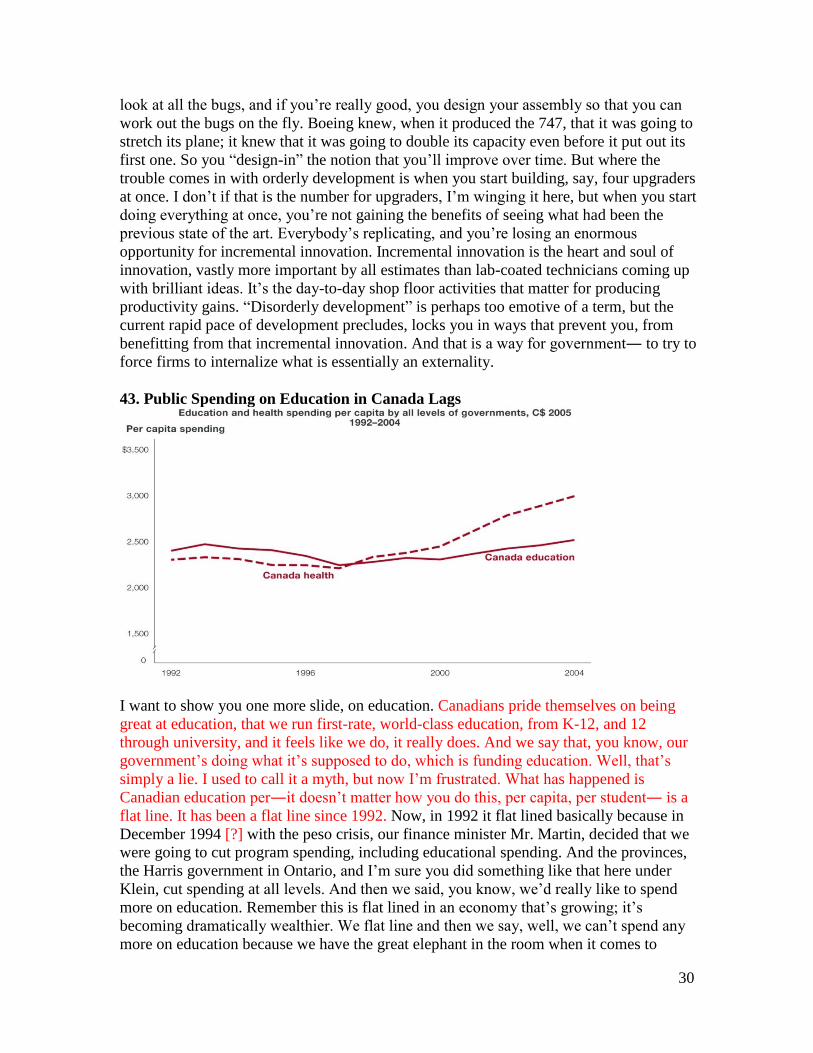

I want to show you one more slide, on education. Canadians pride themselves on being

great at education, that we run first-rate, world-class education, from K-12, and 12

through university, and it feels like we do, it really does. And we say that, you know, our

government’s doing what it’s supposed to do, which is funding education. Well, that’s

simply a lie. I used to call it a myth, but now I’m frustrated. What has happened is

Canadian education per―it doesn’t matter how you do this, per capita, per student― is a

flat line. It has been a flat line since 1992. Now, in 1992 it flat lined basically because in

December 1994 [?] with the peso crisis, our finance minister Mr. Martin, decided that we

were going to cut program spending, including educational spending. And the provinces,

the Harris government in Ontario, and I’m sure you did something like that here under

Klein, cut spending at all levels. And then we said, you know, we’d really like to spend

more on education. Remember this is flat lined in an economy that’s growing; it’s

becoming dramatically wealthier. We flat line and then we say, well, we can’t spend any

more on education because we have the great elephant in the room when it comes to

31

budgeting, and that is healthcare. Healthcare’s eating up all our resources. That’s what

we’re told over and over again, but it’s a lie. It’s a choice. It is governments that have

said we don’t care about our kids, we don’t care about future productivity, elect us

because we’re going to help spend on your healthcare, and nothing else. That’s what

you’re voting for, your politicians. I’ve never heard them say that quite clearly, but that’s

what they’re asking us to vote them into office for.

44. Public Spending on Education in Canada Lags

What about the Americans, the big bad, ugly Americans, right? Obama has to come in

and say, “Get your act together, we need to spend more on education. Get the healthcare

system in order, because we need to spend more on healthcare.” The big, bad Americans,

and they’re not dissing. Obama’s are actually accurate statements. Even with those

statements, what have the Americans done? They’ve ramped up education spending

faster than Canada, and they’ve ramped up public expenditures on healthcare. So, as bad

as the Americans think of themselves on these two items, they’re better than Canadians.

We should be frustrated, we should be angry. This is just completely unacceptable. It’s

only going to get worse, because if Obama can get his educational reform together, the

Americans are going to do a heck of a lot better. Somebody has to say it’s actually quite

sound, based on current research on education policy.

45. Competing on Value―Governments

1. Orderly Development and Incremental Innovation

2. Building an oil-based service industry

3. Develop an EU relationship

4. Education

5. Invest in building tomorrow’s productivity, reduce current consumption

32

The main message then, for what governments can do—it’s not what firms can do, but

what governments can do―is keep on task, and “on task” means to keep investing in

productivity, keep finding other tax incentives, or ways of encouraging people to get

higher levels of educational attainment, and so on. Invest in future productivity, stop

thinking about consuming current prosperity. That’s what governments can do.

And so, just to conclude, I said that there are three things that prevent people from

understanding what I believe is the right perspective on China and India. The first thing is

the dragon myth. It sure looks like they’re producing everything and we’re producing

nothing. But that’s because we see the world as consumers, and that’s not the right way to

see the world. That’s one leg on the elephant, you’ve got to see the whole elephant.

The second thing is, you’ve got to see where we really are in the spectrum between low-

cost and innovation-based competition. I don’t think the Chinese are nearly so far along

as they advertise, and I think that Canadians—I don’t want to say that we’re regressing,

but we’re stagnating in a world in which everybody else is doing more. The second thing

you have to understand is that that’s the thing we should be worried about. We can

control that, and we’ve chosen to let it get out of control.

The third thing that we have to remember is the innovation tipping point. It will come,

but it’s going to come at a glacial pace. We’re talking about decades...twenty, thirty

years, and when it does come, it’s actually not as threatening as it seems. There’ll be

another member in the world innovation class. Innovation is good for the world, and

we’re going to benefit from it. The only question is whether we’re going to be part of the

innovation club in twenty or thirty years, because of the things that we’re choosing to do,

and not because of things that the Chinese are doing.

33

Questions from the Foote Lecture audience:

Question: [not clear]

DT: They spend 17%, we spend 11% of GDP.

Question:

Yes, you didn’t really have time to compare or talk much about India. What about, say,

two things that we should be thinking about concerning India?

DT: I think my starting point would be: what is it that’s new here? The newness that

people are worried about, I think, is that for the first time ever, skilled workers in North

America are being exposed to low-wage competition. It’s never happened before. So

suddenly, an educated person in Hyderabad can compete with an educated person here.

So that’s the context in which this is something really new to my mind. It’s also cool

technologically that we can do these things, but that doesn’t really make it fundamentally

new. So the research I’ve done with Runjuan Liu tells me that that turns out not to be a

big issue, despite the hype by people like Alan Blinder that, you know, it’s going to be a

steamroller. So, that’s the first point I’d make. The second point I’d make is the same

point I’ve made about China: there’s a debate about how sophisticated what India does in

its sphere of activity. Is it really, you know, high-end management consulting, high-end

custom designed computer software, etc? Or, is it really pre-packaged software and you

know, payrolls of a dollar per client. And there’s quite a few people who have made an

articulate argument about the value-added data that came out of India, that in fact it’s

much closer to, you know, routinized payroll software than anything like, say Microsoft

or Broadcom produces. And, the third thing to bear in mind is that, suppose India really

did take off? And in many ways I think that India is more likely to take off than China.

The reason for that is—I didn’t talk about it—but it is institutions. You know, you ask

what do you do need, for good institutions, and you need something that looks like

Western intellectual property protections, rule of law, and so on. You know, remove the

appropriation risk problem by sovereign [unintelligible]. I mean, why is Shanghai so

important to China? What’s Shanghai’s history, that puts it in so central a position? Well,

the answer is: not only was it one of about twenty-three customs-free zones that the

British conquered in the 19th

century, but it’s the one that the British came to do business

at, more than any other place. Once the British came to do business, and to start

developing a legal system to deal with internal contract law between, you know, the

many expats in there, who started to arrive? The Chinese. And the Chinese start to do

business in Shanghai precisely because it allowed them to escape a legal system which

was dysfunctional, and a political system which was increasingly dysfunctional,

fragmenting, the center of gravity from Beijing had all but disappeared. You come to

Shanghai to do business, you buy a piece of property, you know it’s not going to be

expropriated by a local landlord, and you have a contract it’s going to be adjudicated in a

British court. That’s the history of Shanghai.

Fortunately for India, things that really matter—banking, and a legal system—are

actually surprisingly good by the standards of the country at that level of development.

And the Indians are working hard at making transparency in financial markets clearer,

improving the banking system, making it more stable in terms of reserve requirements.

34

You know, compare that to what’s going on in China with state-owned banks and central

interference in the balance sheets of these banks---just a nightmare, a huge overhang of

debts that will never be repaid from the state-owned enterprises. The Chinese banking

system has serious problems but added to that the Indian banking system is looking much

better, and their legal system is going through a series of reforms to try and get it out of

the volume exit bottleneck[?] it’s currently in. But the foundations are there and the

questions is to get rid of the bottleneck. So, I’m very optimistic about India.

Question: unclear

DT: So let me preface it by saying I know very little about the oil patch. I’m a Toronto-

boy, so bear that in mind. But there’s a certain obvious place to look, and that is Houston,

which ran out of oil fifty years ago. So the question is: what can you leverage

permanently out of the oil patch? Where is the big value-added that you can try and get?

Is it transportation? Is it pipelines? Trying to, you know, corner the pipeline nexus in

North America? That sounds sort of dumb, but, you know, there are people in Canada

who are trying to build a for hire port on the West coast, right? Where, you can say if my

goods come through your port, then my competitor’s goods do not. I mean, you can think

strategically about infrastructure. Then services. What service expertise are we gaining

from it? Maybe it’s financial expertise. You know, when a banker’s looking at a proposal

that comes out of the oil patch, that banker in Calgary—I’m assuming Edmonton, too—

knows a lot about the industry, knows the appropriate benchmarks, knows how things

work. That’s expertise that doesn’t just, it can be used not just here. It can be used in, you

know, in a calmer Congo, or in Ecuador, or wherever. How can we leverage this

knowledge, these abilities, take it abroad and do well. That’s what I have in mind.

Question: unclear

DT: Unfortunately, if I...the easiest thing to do is to go to government and ask about tax

rates. And do I have to say, the last five years, both, you know, sides of the aisle have

done quite well in trying to get down marginal effective tax rates. You know, you’re

harmonizing the capital gains, the machinery-equipment tax, the capital surcharge, so

you’re doing pretty good on that front. Really at some point, business has to step up to

the plate, because at the end of the day, it’s business R&D where Canada is weakest. So,

we have, you know, to think up ways. I’m never going to be up here picking winners, so

how do you avoid picking winners? You avoid picking winners by funding industry

associations, never by funding individual companies. Right, figuring out, you know,

identifying...In Toronto, the board of trade, it’s practically a corpse. Where is its civic

initiative? Where’s its sense of pride in trying to promote business, entrepreneurial spirit

in Toronto? I don’t see it. So I think that if I were connected in the business community,

or if I could find—and I know we could find people who are connected in the business

community who share this view—that’s where I would push. And perhaps I would push

it hardest in Quebec, which is really a drag on the Canadian economy, and Quebecers

know it.

Question: unclear

35

DT: Yeah, we know all the R&D level, numbers, probably to 2007. China’s now the, in

absolute terms, it’s the second largest spender on R&D in the world behind the US. So

they’re continuing to ramp up, ramp up. And maybe the day will come, for instance

when actually there’s a biotech patent out of Beijing that’s worth anything. I don’t know.

Uh, but you know, they’re doing great guns in all sorts of areas. But you know you keep

seeing the same points. Microchip fear, you know, they’re going to take over all of the

microchips the way the Japanese did RAMS back in the ‘90s. And yet, that’s not where

the action is. That’s all commodity chips. All the boutique stuff, that’s still all happening

in the US.

Question: unclear.

DT: That’s exactly what I’m saying. Why would it happen? Because, no matter where

you invent the good, you’re still going to...we’ve already seen, manufacturing is just a

small piece of the whole picture. The money, the value-added is when you need market

positions from the idea, right? So, whether you’re inventing in the US, you’re inventing

in China, you’re still going to be producing in China. There is no cost advantage on the

manufacturing side...these are all contract manufacturers, right? Does Voxcon care who

invented it? They’re still going to be producing it. So, by the time China gets to the point

where it’s a real innovation juggernaut, you think that these innovators are going to be

earning $3 an hour? I don’t think so. I mean, Runjuan, you just told me the other day that

salaries for business professors in one university is $150,000, and that’s before PPP

conversion, right? You know, I just don’t see how they’re going to be beating us on costs

that we can’t take advantage of. We can take advantage of the same costs they do.

Question: unclear

DT: Okay, there’s a lot of questions there. And you’re asking a question which is near

and dear to my heart, so I’ll probably end up with an hour-long conversation on that. Let

me make some very brief comments about that. First of all, if you break down...uh, sort

out medium public universities in the US—so, let’s forget about M.I.Ts and Stanfords,

and so on, because you’ve just got no apples compared them with here—you’ll see that

their revenue sources in every single category that you can imagine, are vastly higher

than ours, including government contributions that are not defense-related.

They out-fund their universities, their middle public universities at every possible level,

okay? So, it is not a defense story. The defense story is for Stanfords and M.I.Ts, not

exclusively but... The next one is where should the money go? To me the money should

not just go, if we’re talking about education, universities. If we’re talking about R&D, to

universities is great, but Canada already spends a lot on R&D in universities, so I think

we’re doing great on that front. If we’ve got to spend on education at all levels, where

would I start? I’d start at age three. In fact, I’d put in...I have a paper that’s coming out in

Pediatrics and Healthcare, which is Canada’s big pediatrics journal, on why we should

be investing in children.Which you all know, and you’ve all heard, and I subscribe to

thoroughly. I think the government should be spending another $15 billion a year funding

K-6. And I think that answers all of the questions that you asked me.

Question: unclear

36

DT: I’m much less concerned that you are about dumping US bonds. The US dollar is

here for another long, long time, in my view, but let’s not argue about that. The thing

to...that I think is the most important is actually long-term. Long-term, China is going to

be intransigent on devaluing against the US dollar, which means that the burden—the

massive burden of adjustment, since the US must export more—falls on the rest of the

world, and particularly it falls on Japan, EU, and Canada. So in this...yet again Canada’s

going to find itself in the midst...it’s going to be the collateral damage in a US battle on

international trade issues. We got hammered with the EU-US battles with their

agriculture, we’ll get hammered with the US-China battles, over structural adjustment.

And that means long-term Canadian currency is going to stay high because that’s the only

way the US is going to get rid of its trade imbalances. China won’t let them do anything

else. So we should be really frustrated at being collateral victims of China’s

intransigence.

Question: unclear

DT: So here’s the thing, here’s to me what is a huge puzzle: that view has been expressed

a number of times and I clearly bought into it, but what makes me pause is the Ontario

Task Force on competitiveness. We actually spent piles of money, it’s embarrassing, to

get a first-rate consulting firm to do a large-scale survey of business attitudes among US

businessmen, Canadian businessmen, and Canadian public. We asked them a gazillion

questions about you know, do businessmen deserve the rewards that they get; should we

have higher taxes; are businessmen taking up, you know, the whole slew of questions,

question after question after question. It was a large scale survey, over a thousand people

on each sides of the border. Question after question, we found no differences in responses

to anything. You know, would you be willing to work weekends? Would, you know...It’s

not in innovation, there were no innovation questions where you are, but on all sorts

about other questions that reflect cultural attitudes, no difference, except for one. And

that was, we asked businessmen on both sides of the border: what level of education do

you need, in order to be a successful businessman? In the US, more than half said you

need a university degree; and in Canada, it was less than a quarter.

So what you’re saying is very...makes total sense, but I just haven’t...we’ve looked and

looked in the data to see if we could find something in the date which is a smoking gun.

We just haven’t been able to find it; it doesn’t show up in the data. Casual empiricism, I

agree, it looks like it’s there.

Question: unclear.

DT: The OECD has been on our case for years, saying that we’re way too generous with

small and medium-sized enterprises. Just to bear in mind, one thing to bear in mind,

though, uhm, Canadian, small Canadian firms export in far greater numbers than is the

norm in all the OECD countries for which we have numbers. So they’re actually pretty

good exporters. Why that is, I don’t know. I’ve never taken the time to do cross-country

comparisons. But you’re absolutely right. The tax system’s gone way overboard, way

overboard. But don’t dis them completely.

Question: unclear.

37

DT: This is...Roger first showed me this slide probably about, oh, what year? Probably

about five years ago. This has been, this has been a big issue now, and we’ve been

pushing that for years.

Question: