Axel Leijonhufvud Economics of the Crisis and the Crisis of Economics

Upload

peregrine-littleCategory

view

216download

0

2008 Credit Crisis

Its connection to subprime mortgage crisis

By Supriya Sarnikar, J.D., Ph.D. (economics)

Asst. ProfessorEconomics and Management Department

Westfield State College

The Beginnings of the Crisis

• You have heard that the current credit crisis began in the housing market.

• We will look at the basics of the mortgage market to understand how it affected the financial markets.

• But first, we will look at the meaning of some financial terms that you will encounter in this presentation.

Some Terminology

• Mortgage – to pledge property as security for a loan

• Collateral – the property that is pledged

• Liquidity – ease of conversion of an asset into cash

• Security – A certificate (paper or electronic) that gives certain rights to the lender.

• Securitization – process involving pooling loans and creating securities backed by the loans.

• Bonds/Debt instrument – A security that gives the holder a right to receive a fixed amount (called “face value”) on a fixed date in the future (date of maturity) and right to receive periodic interest payments (called the “coupon rate” ).

Conventional Mortgage Process…

• …begins when a buyer wishing to buy a house, approaches a bank/financial institutions for a loan.

• Bank/Financial Institution checks borrower’s credit history, income, other financial data (such as other debts owed), and then decides whether to make the loan.

• Once the loan is made, the bank’s money is tied up for the duration of the loan (typically 30 years). This made traditional real estate loans very illiquid.

• Securitization of mortgages was meant to turn these illiquid loans into more liquid assets..

What is Securitization of Mortgages

• Mortgage securitization is the process in which several real estate loans are pooled together and then broken up into smaller pieces to be sold to investors.

• Just like stock ownership makes it possible for each one of us (no matter how wealthy or not wealthy) to own a piece of a company (instead of the whole), and enjoy shares of the profits, mortgage securitization, in theory, makes it possible for investors to hold a piece of the mortgage and enjoy shares of the interest (and principal) payments.

Securitization can be a good thing..

• ..because it allows money to flow from the savers (and investors who are willing to bear the risk), to the borrowers who do not have the money but want to use it.

• Obviously, the bank (or other financial institution) that made the original loan is also already performing this function. So why the securitization?• Answer: The bank may not be willing to make too many real

estate loans if its money will be tied up for such long durations. By breaking the loans into pieces and selling it to investors, the bank turns an illiquid loan into a liquid asset. The money that is now freed up can be used to fund other productive activities..

Mortgage Securitization is not new..

• In 1968, GNMA (Ginnie May) was first authorized by Congress to issue Mortgage backed Securities to finance its home loans.

• FNMA (Fannie May) and FHMC (Freddie Mac) have been issuing Mortgage backed securities since the 1980s.

• The mortgage backed securities created with pools of subprime loans are thought to be the culprits in the current financial crisis and these were issued starting in the mid-1990s.

• Source: “Credit Crunch of 2008,” by Paul Mizen in Federal Reserve Bank of St. Louis Review, September/October 2008, 90(5), pp. 531-567.

Mortgages Conventional Vs. Jumbo, Alt-A, and Subprime

• Conventional Mortgages adhered to certain standards. •Borrowers must have good credit rating•Income documentation required•Down payment required (typically 20%)•Principal balance could not be higher than a certain amount ($729,750 in 2008)

• Jumbo Loans•Made to borrowers with good credit (i.e., prime borrowers) but the principal balance is larger than the Agency (Fannie and Freddie) limits (729,750 in 2008).

• Alt-A Loans•Made to prime borrowers but lax on other standards such as income documentation or down payment requirements

• Subprime Loans•Made to borrowers with bad credit ratings. Other standards may also be relaxed.

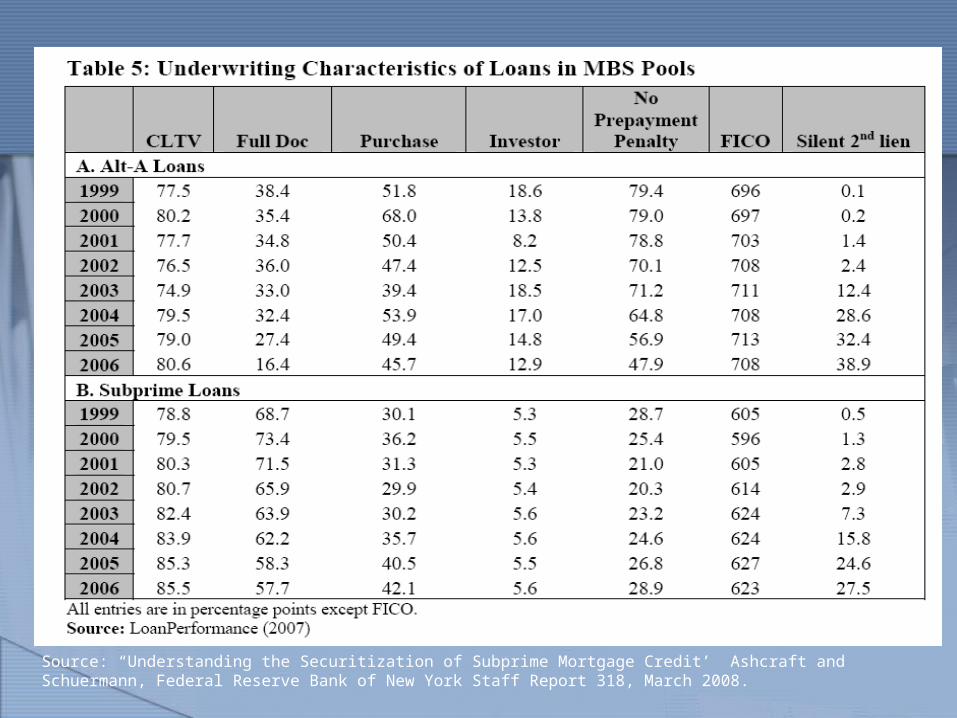

Source: “Understanding the Securitization of Subprime Mortgage Credit’” Ashcraft and Schuermann, Federal Reserve Bank of New York Staff Report 318, March 2008.

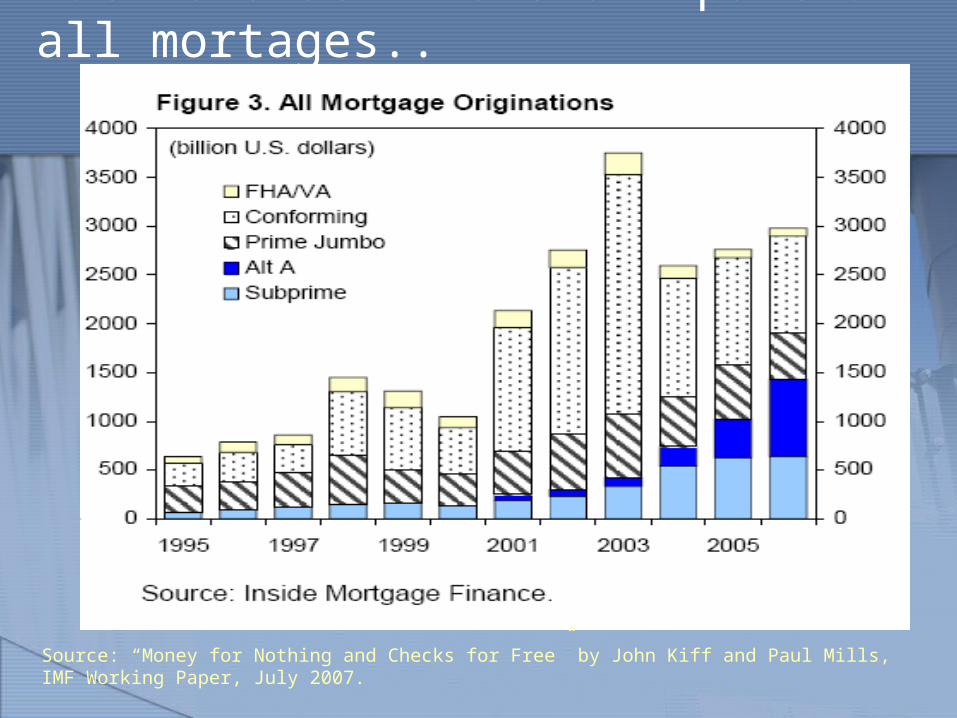

Subprime loans increased dramatically…

Source: “Money for Nothing and Checks for Free” by John Kiff and Paul Mills, IMF Working Paper, July 2007.

But were still a small part of all mortages..

Source: “Money for Nothing and Checks for Free” by John Kiff and Paul Mills, IMF Working Paper, July 2007.

The Subprime Mortgage Securitization Process

Mortgagor(Borrower)

Bank/Financial Institution(Originator)

Requests loan

Provides loan

Arranger/Issuer

Loan sold

Investors

issues securities

Warehouse Lender(makes short term loans to Issuer for purchase of mortgages)

Credit Rating Agency

SPV(Trust)

Loans pooled and sold to Trust

Servicer(is employed by Trust to collect loan payments etc.)

Makes loan payments

Remits loan payments to Trust and advances unpaid interest payments.

Provides customer service to borrower

Adapted from: “Understanding the Securitization of Subprime Mortgage Credit’” Ashcraft and Schuermann, Federal Reserve Bank of New York Staff Report 318, March 2008.

Source: “Understanding the Securitization of Subprime Mortgage Credit’” Ashcraft and Schuermann, Federal Reserve Bank of New York Staff Report 318, March 2008.

Source: “Understanding the Securitization of Subprime Mortgage Credit’” Ashcraft and Schuermann, Federal Reserve Bank of New York Staff Report 318, March 2008.

Source: “Money for Nothing and Checks for Free” by John Kiff and Paul Mills, IMF Working Paper, July 2007.

Creation of the M.B.Securities- A Highly Simplified illustration..

• Originator makes, lets say, a 100 loans adding up to, say, $80 million. The expected payback is $80 million (Principal) plus the interest payments of, say, $5million (assuming no defaults).

• The originator pools the 100 loans and sells to the Arranger for, say, $82 million. (The Arranger is willing to pay more than $80 million because it expects to receive some interest payments).

• The Arranger then divides up the $80 million into several smaller pieces. Let’s say 1000 bonds each with a face value of 80,000 and some interest rate (called a coupon rate). Now it wants to sell these bonds to investors.

Securitization creates a distance between the investor and the borrower..

• So how can an investor know whether the mortgages that secure its investment are healthy?

• Several checks and balances exist but also many problems also exist at each stage of the securitization process.

• Investors relied heavily on credit ratings provided by the Rating Agencies.

The Role of Credit Rating Agencies

• Credit rating agencies, such as Moody’s, Standard & Poor, and Fitch, are paid by financial institutions to provide easy to read/understand ratings of the risk associated with various debt instruments.

• Each Agency has its own scale of indicators and own models to determine default risk

A sample scale of ratings• AAA – extremely safe, very low risk• AA – very strong credit, low risk• A – strong credit• BBB – Good credit• BB – good credit but vulnerable to economic conditions

Role of credit Rating Agencies- contd.

• In rating Mortgage Backed Securities (MBS), the rating agencies relied on information provided by the Issuer/Arranger.

• Their rating models were publicly available and Issuers often consulted with the rating agencies when constructing the loan pools and creating the MBS.

• The models used by the rating agencies relied on historical data (typically, 1992-2000) of mortgage default and foreclosure frequency rates. But the type of loans made during 2001-2007 were very different from the types of loans made during 1992-2000. The later loans were much more risky.

Source: “Credit Crunch of 2008,” by Paul Mizen in Federal Reserve Bank of St. Louis Review, September/October 2008, 90(5), pp. 531-567.

Structuring the Deal- the Devil in the Details

• The potential investors in these mortgage backed securities were mainly institutions that were restricted by regulation to buying investment grade bonds. (Typically these are bonds that are rated BBB or better).

• So, for an Arranger to sell these mortgage backed bonds, a rating of BBB or better was essential.

• Working in consultation with the credit rating agencies, the deals were structured in a way that would give most of the bonds AAA (safe) rating.

Structured Deals – Converting Subprime Loans into AAA bonds• To convert a pool of loans to AAA securities, the Issuer had to provide

Credit Enhancements (CE) in the form of

• Over Collateralization: For example, $80 million loans are backed by real estate that is valued at more than $80 million. Or, more typically, the collective face value of the MBS is less than the underlying loan.

• Excess Spread: The weighted average of the coupon rates on the MBS is less than the interest rate on the underlying home loan.

• Subordination: In our example, the 1000 securities are divided into tranches (groups)- senior, mezzanine, equity, and residual tranches. Typically, about 80% of the bonds were designated senior tranche and were rated AAA, the rest were rated A, BBB and lower. The mezzanine, equity, and residual tranches are “subordinated” to the senior tranche. That means any money repaid by the borrower is first applied to the AAA tranche before any money is paid to the mezzanine, equity, and residual tranches.

• Additionally, the investors were assured of the safety of the bonds by the insurance provided by monoline insurers such as AMBAC, MBIA etc.

Source: “Money for Nothing and Checks for Free” by John Kiff and Paul Mills, IMF Working Paper, July 2007.

Collateralized Debt Obligations (CDOs)

• No natural market for BB and C rated MBS.

• Repackaged into CDOs with other collateralized loans such as car loans.

• No natural market for lower tranches of CDOs. These are repackaged into CDO2. Lower tranches of CDO2 are repackaged into CDO3.

Source: “Money for Nothing and Checks for Free” by John Kiff and Paul Mills, IMF Working Paper, July 2007.

Structured Deals – Each MBS and CDO is unique..

• For any given pool of loans the rating agency, (or its publicly available rating model), told the Issuer how much credit enhancement would be necessary for the MBS tranches to receive AAA rating.

• The Issuers often bundled car loans and credit card loans with subprime mortgages to get the desired credit enhancements (especially for the CDOs).

• This turned the previously standardized MBS market (with virtually no chance of default) into a market with high risk. And, especially, into a market with risk that was very difficult to price.

• Compounding the risk pricing problems, were falling housing prices and several incentive and information problems at each stage of the securitization process.

Incentive Problems in the Securitization Process

Mortgagor(Borrower)

Originator(gets closing costs, points paid by borrower PLUS sale proceeds of loan)Makes warranties to Arranger

Predatory Borrowing

Predatory Lending

Arranger/Issuer (gets fees paid by investors plus any premium paid over the par value)

Mortgage Fraud

Investors

Principal Agent problem

Warehouse Lender(Makes short term loans to Issuer for funding mortgage purchases)

Credit Rating Agency

SPV(Trust)

Adverse Selection

Servicer(gets paid fixed fee based on outstanding loan value)

Moral Hazard

Adverse Selection

Moral Hazard

Model Error

Adapted from: “Understanding the Securitization of Subprime Mortgage Credit’” Ashcraft and Schuermann, Federal Reserve Bank of New York Staff Report 318, March 2008.

Source: “Understanding the Securitization of Subprime Mortgage Credit’” Ashcraft and Schuermann, Federal Reserve Bank of New York Staff Report 318, March 2008.

Source: “Understanding the Securitization of Subprime Mortgage Credit’” Ashcraft and Schuermann, Federal Reserve Bank of New York Staff Report 318, March 2008.

What triggered the credit crunch?

• Falling housing prices increased defaults.• Investors began to exercise “put back” options that

put the Originators on the hook for the bad loans.• High leverage meant that a small loss on subprime

loans translated into huge losses of capital.• The run on the banks started a chain reaction that

resulted in the failure of several stand-alone (monoline) banks and insurers.

• Doubts about the extent of losses suffered by each institution created large scale uncertainty that froze the credit market.

What Now?

• Credit Crisis is real. But what is the solution?

• Is a bailout necessary? If so, what should a good bailout do?• Depends on whether the credit crisis is

due to • Inadequate capital, or• Lack of confidence, or• Both inadequate capital and lack of confidence

The current bailout/rescue plan

• Mainly addresses the problem of lack of confidence. Seeks to restore confidence by:• Govt. buying up the “toxic” assets

• Critical question is “at what price?”• Seeks to find the price through a reverse

auction.

Reverse Auctions

• Problems with using reverse auctions in this case• Each “toxic” asset is different. The CDOs

and MBS are not all alike.• Asymmetric Information - Banks know more

about the quality of the securities than the government.

• Adverse Selection - Banks are likely to offer the worst securities for sale at the auction and keep the good (more valuable, profitable) ones to themselves.

Alternatives to bailout plan

• Why not simply help the homeowners who are in foreclosure?• Curing current foreclosures is not enough. • Future defaults will have to be picked up by taxpayers as

well for this to work. • Estimated $6 trillion of potentially problematic loans made.

Very expensive to bailout homeowners..• Moral hazard issue – more are likely to default is

government bails out. This is also a problem with current plan to directly help banks.

• Problematic loans were made in other markets (car loans, credit cards) as well. Curing defaults in housing markets may not be enough to avert deeper recession.

Alternatives to Bailout plan

• Demanding stock (share in profits) in return for providing capital to troubled banks.

• Good idea from taxpayer’s perspective but not likely to help if bankers do not participate.

No easy answers..

• Rules of auction and other details of bailout are critical for • preventing a deeper and longer recession, as well

as,• Not enriching banks at the expense of tax payers.

Treasury Secretary has 45 days to come up with the details of the plan to buy toxic assets.

Watch for more details..Meanwhile, time is running out as evidenced

by the deepening of the crisis.