2008 Annual Report -...

69

Annual Report ~2008~

Transcript of 2008 Annual Report -...

Annual Report~2008~

~ On Our Cover ~

“Apple Butter Season” © 2008 Will Moses

In the painting commissioned for this year’s cover,artist Will Moses, great-grandson of legendary

painter Grandma Moses, transports us to an earlier timeat J. M. Smucker’s Orrville home, where families aregathered to celebrate the goodness of the harvest.

~ Contents ~

Letter to Shareholders 2

Business Overview 6

Recipes 11

Five-Year Summary of Selected Financial Data 14

Summary of Quarterly Results of Operations 15

Stock Price Data 15

Comparison of Five-Year CumulativeTotal Shareholder Return 16

Management’s Discussion and Analysis 17

Report of Management on Internal ControlOver Financial Reporting 27

Report of Independent Registered Public AccountingFirm on Internal Control Over Financial Reporting 28

Report of Independent Registered Public AccountingFirm on the Consolidated Financial Statements 29

Report of Management on Responsibilityfor Financial Reporting 30

Consolidated Financial Statements 31

Notes to Consolidated Financial Statements 36

Directors, Officers, and General Managers 64

Properties 64

Corporate and Shareholder Information 65

Year Ended April 30,

(Dollars in thousands, except per share data) 2008 2007

Net sales $2,524,774 $2,148,017Net income and net income per common share:

Net income $ 170,379 $ 157,219Net income per common share – assuming dilution $ 3.00 $ 2.76

Income and income per common share before restructuringand merger and integration costs: (1)

Income $ 178,881 $ 165,152Income per common share – assuming dilution $ 3.15 $ 2.89

Common shares outstanding at year end 54,622,612 56,779,850Number of employees 3,250 3,025

(1) Reconciliation to net income:Income before income taxes $ 254,788 $ 241,004Merger and integration costs 7,967 61Cost of products sold – restructuring 1,510 9,981Other restructuring costs 3,237 2,120

Income before income taxes, restructuring, and mergerand integration costs $ 267,502 $ 253,166Income taxes 88,621 88,014

Income before restructuring and merger and integration costs $ 178,881 $ 165,152

Financial HighlightsThe J.M. Smucker Company

Why We Are, Who We Are

...Our Culture

A culture of dotting the i’s and crossing the t’s…

Of doing the right things and doing things right…

A culture of growth — individual and as a company.

It’s who we are. It’s because of who we are.

It’s a result of living our Basic Beliefs…

Our Commitment to Each Other. To our customers,

and to our consumers.

As we look to the future of unlimited possibilities,

we recognize the principles that are instrumental

to our success…

A culture deeply rooted in our Basic Beliefs…

Guideposts for decisions at every level...

Why we are who we are.

A culture that encourages commitment to each other…

Clear communication and collaboration…

Vision…A culture of appreciation.

A family-sense of sharing in a job well done…

Where every person makes a difference.

®

®

®®

®

®

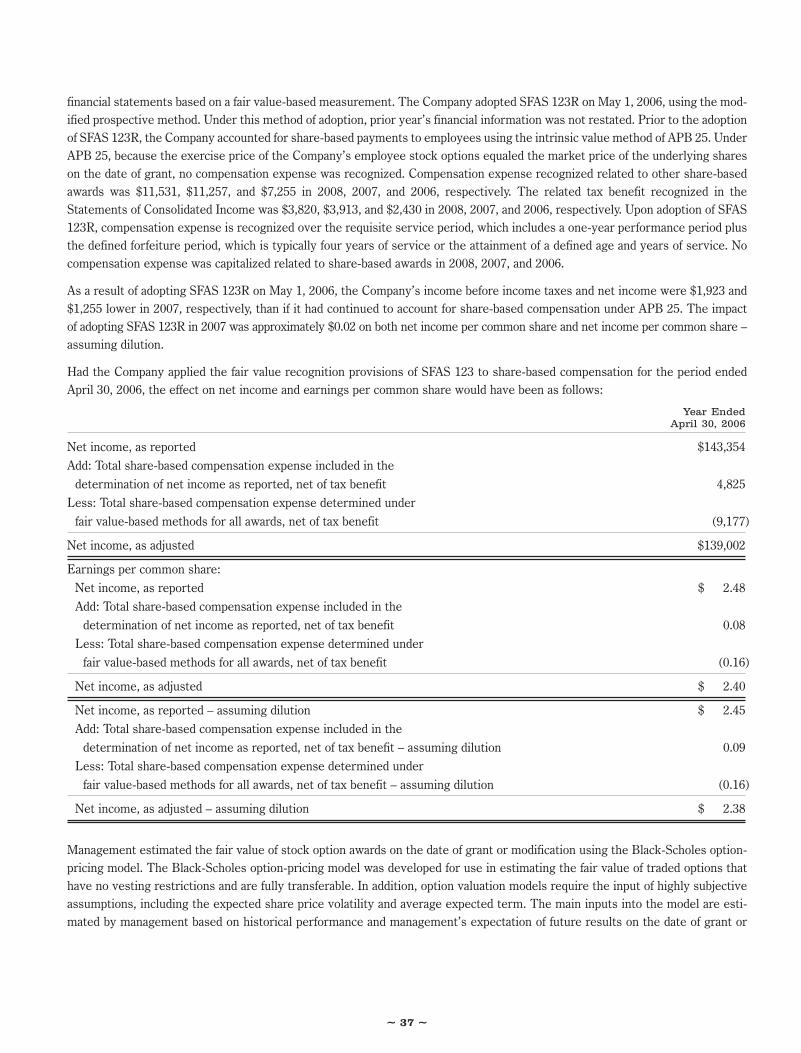

Fiscal 2008 was another record year for The J. M.

Smucker Company. This is especially gratifying in light

of the year’s challenging economic environment and

unprecedented commodity-driven cost increases, which

impacted all of our businesses.

Sales, excluding divested businesses, were up

22 percent, and net income grew eight percent.

Net income per share was $3.00, up from $2.76

last year, a nine percent increase.

Cash flow from operations exceeded $190 million,

allowing for a dividend increase for the 28th time

in the last 31 years.

We attribute our fiscal 2008 success to:

Our loyal consumers and customers, who trust

the Smucker family of brands to deliver on the

promise of quality, taste, and value;

Our talented and dedicated employees, who

continue to focus on our core business, while

embracing change as we grow;

A clear strategy of owning and marketing leading

food brands in North America; and

Our long-term commitment to investing in our

brands, developing new products, and acquiring

strategic businesses.

In fiscal 2008, we repurchased 2.9 million shares, total-

ing almost $150 million. This action demonstrates our

confidence in our Company and is an effective means

for continuing to create shareholder value.

~ Long-Term Performance ~

While we are proud of our fiscal 2008 results, they are

only a snapshot of a single year. We believe that success

is best measured over the long term, and we are pleased

to report that our compounded net sales and earnings

per share grew over the past decade by 16 percent and

10 percent, respectively.

Just as important, we measure success by more than

a financial yardstick. Our long-held values and philoso-

phies tell the true story of who we are—and with whom

you, as a shareholder, have entrusted your investment.

~ Our Purpose and Strategy ~

Our Company, brands, and people are about more

than making and marketing products.

At Smucker, our purpose is to help families share

memorable meals and moments. Key to achieving our

purpose is our strategic vision of owning and marketing

#1 food brands in North America. The Smucker family

of brands is a trusted part of everyday meals, casual

get-togethers, and special occasions—all of which foster

family connections and lasting memories.

Bringing families together is best accomplished by

employees who feel like family themselves. At Smucker,

we maintain a unique family feeling by genuinely living

our Basic Beliefs: Quality, People, Ethics, Growth, and

Independence.

Our purpose is what brings Smucker employees to

work every day. Our strategy is what guides our organi-

zation in a common direction and is the framework for

serving our consumers, customers, employees, suppliers,

communities, and shareholders.

Dear Shareholders and Friends:

~ 2 ~

~ Serving Our Constituents ~

Consumers Meeting consumers’ needs is the heart of

all we do. We always seek to understand what consumers

want and to meet their needs with quality products that

are “good and good for you,” “easy for you,” and that

“make you smile.” That commitment, along with respon-

sible marketing, helps establish a bond between our

brands and consumers. Consumer trust, which takes

years to build, is something we never take for granted.

Customers We strive to satisfy our customers by

delivering outstanding service, offering fair prices, and

creating jointly developed business plans that promise

mutual benefits. Our emphasis on ethics, fairness, and

quality is vital to long-term, productive customer

relationships.

A recent industry initiative called New Ways of Work-

ing Together aims to eliminate business disruptions,

so that—as a team—retailers and manufacturers can

focus more closely on satisfying consumers and grow-

ing business. While this is not a new objective for us,

we have taken a leadership position in this initiative,

because we believe it will benefit everyone: retailers,

manufacturers, and ultimately, consumers.

Employees Smucker employees are quality people,

each of whom brings important talents, perspectives,

and skills to our Company. We believe that every

employee makes a difference.

Suppliers Achieving our strategy depends on dedicated

suppliers and business partners who share our willingness

to go the extra mile in the name of quality and service.

We view our suppliers and business partners as extended

family, and we treat them accordingly. Whether it is the

brokers who stock the retail shelves, the drivers who

deliver our products, the farmers who supply our raw

materials, or the people who create our advertising—

each supplier or partner plays a key role that we

appreciate and acknowledge.

Communities We take seriously our responsibility to

be good environmental stewards. Sustainability, a term

now popular throughout the industry, describes what

we have been doing for many years. We realize that sus-

tainability begins at home—in the 20 North American

communities in which we have offices and manufacturing

plants—and that our local efforts fan out in concentric

circles that ultimately impact the world.

Shareholders In the final analysis, we are confident

that if we do a good job of serving our consumers,

customers, employees, suppliers, and communities, we

will ultimately deliver good returns for our shareholders.

It is clear to us that to achieve lasting, measurable

results, we must serve each of our constituents with

sincerity, trust, creativity, and unwavering dedication to

doing what is right. This is a longstanding commitment

on the part of thousands of thoughtful, capable people,

working with shared purpose in an atmosphere of

collaboration—people who strive every day to help

families create memorable meals and moments together.

All of us at The J. M. Smucker Company thank you for

your continued support and dedication.

Sincerely,

Tim Smucker Richard Smucker

~ 3 ~

Whatever the occasion, we are honored that our brands are included in family meals every day. Our tradi-tional favorites are joined by newly added brands, helping us deliver on

our promise to offer products that are good and good for you, convenient,

and that make you smile.

~ U.S. Retail Segment ~

Sales and profits within our U.S. Retail segment grew

by 21 percent and four percent, respectively, in fiscal

2008. Contributing to this growth were our core busi-

ness, new products, and the first full year of sales and

profits from the Eagle Brand acquisition. We are espe-

cially pleased with the performance of our U.S. Retail

segment, given another year of record-high commodity

costs that impacted all of our businesses.

During uncertain economic times, the Smucker

family of brands steadfastly provides consumers with

highly proven, deeply trusted products. Smucker’s, Jif,

Pillsbury, Crisco, Eagle Brand, Hungry Jack, Martha

White, and White Lily are well-loved parts of the

everyday meals and special occasions that bring

families together.

We are passionate about serving our consumers and

customers, and we always seek better ways to meet

their needs. In January 2008, we appointed Advantage

Sales and Marketing as our single national broker for all

of our grocery business within the U.S. Retail segment.

This decision represents a major milestone in our go-to-

market strategy. It will help us further improve customer

service, realize a number of near-term efficiencies, and

position our Company for future growth.

Fruit Spreads & Peanut Butter Our Smucker’s and Jif

brands delivered record market-share growth in fiscal

2008. Consumers continue to reach for our many fruit

spread varieties and peanut butter products, enjoying

each on its own or

pairing them to create

the “Great American

PB&J.”

Our Smucker’s

Organic fruit

spreads and

Smucker’s Sugar

Free fruit spreads sweetened with Splenda® continue to

perform well and now include even more varieties for

consumers to choose from.

This past year, we reintroduced “The Boys” television

advertising campaign, featuring a young Tim and Richard

Smucker. Through a series of three new television

spots, consumers are reminded of the heritage of the

Smucker’s brand and the quality ingredients we select

for every jar of fruit spread.

Peanut butter, our largest category, sustained impres-

sive growth in fiscal 2008, as increasing numbers of

consumers include this “good for you” and affordable

protein in their pantries. We produced record volumes

of Jif peanut butter to satisfy growing consumer

demand and to help meet customers’ needs as

a result of a competitor’s supply disruption.

In fiscal 2008, we extended the Jif

brand to the snack nuts category.

Just as “choosy moms” and “choosy

dads” have

trusted Jif

peanut butter

for genera-

tions, consum-

ers who crave

the finest-quality peanuts, cashews, and mixed nuts

are drawn to Jif snack nuts. New television advertising

reminds snack nut consumers, “We have to be choosy.

We’re Jif.”

Uncrustables Sandwiches Smucker’s Uncrustables

sandwiches, which offer a convenient and fun way

to enjoy a peanut butter and jelly sandwich, continue

to bring smiles to the faces of consumers. Demand

remains strong, and the introduction this past year of

white whole wheat Smucker’s Uncrustables sandwiches

in strawberry and grape varieties affords consumers

another better-for-you alternative and broadens our

presence in the frozen aisle.

Business Overview

~ 6 ~

Ice Cream Toppings Nothing says “celebration” like

Smucker’s ice cream toppings. The introduction in

fiscal 2008 of Smucker’s Triple Berry topping and

Smucker’s Sugar Free Chocolate and Sugar Free

Caramel Sundae

Syrups heightens

the fun and

further expands

our better-for-

you alternatives

in this category.

Potatoes, Pancakes, and Syrup This past year, we

extended the reach of our Hungry Jack brand by

continuing to focus on new products and expanding

our product distribution and print and radio advertis-

ing. We began testing several products that will offer

consumers even greater convenience. Included are

Hungry Jack refrigerated potatoes, Hungry Jack frozen

biscuits, and Hungry Jack Snack’n Waffles ready-to-eat,

pre-sweetened waffles.

Baking and Oils We continued to strengthen and expand

our U.S. baking aisle leadership position in fiscal 2008.

Through our portfolio of baking brands, including

Pillsbury, Eagle Brand, PET, Martha White, and White

Lily, we offer consumers products that meet nearly all

of their everyday and special-occasion baking needs.

We enjoyed the first full year of sales from

brands that joined our portfolio as part of the Eagle

acquisition. The addition of Eagle Brand sweetened

condensed milk, Eagle Brand evaporated milk,

Eagle Brand dessert

baking mixes, and

Magnolia sweetened

condensed milk

further broad-

ened our cross-

promotional

activities during

the busy fall and spring holiday baking periods.

Consumers often look for something exceptional to

serve to family and friends on special occasions. Our

newly introduced, simple-to-prepare Pillsbury Mint

Chocolate Brownies, Pillsbury Pumpkin Caramel Delight,

and Eagle Brand Magic Cookie Bar and Decadent

Fudge dessert kits answer this desire with impossible-

to-resist convenience.

Consumers continue to respond positively to our

better-for-you baking alternatives, including Pillsbury

Reduced Sugar cake mixes and frostings, Pillsbury

Reduced Sugar brownies, and Martha White whole-

grain muffins and sweet yellow cornbread.

Our Crisco olive oil products, which offer consumers

a trusted brand in the “good for you” olive oil category,

are a growing success. Thanks to ongoing momentum

and expanded distribution, these products will be

offered in the western United States in fiscal 2009.

Our introduction of Crisco Puritan canola oil with

Omega-3 DHA means consumers now have another

smart choice for adding nutritional value to their meals.

Unprecedented soybean, wheat, and milk commodity

costs significantly challenged our

Baking and Oils business in

fiscal 2008. It is expected

that these costs will

continue to rise in the

foreseeable future,

making the always-vital

need for cost and price

management more

critical than ever.

~ 7 ~

We strive to help families share memorable meals and moments.

Great-tasting products from trusted brands make it easier for families to spend time together.

~ Special Markets Segment ~

Our Special Markets segment saw another record

year. Compared to fiscal 2007, sales in this segment,

excluding divested businesses, were up 25 percent.

Profits increased 26 percent.

Canada Excluding divested businesses, our Canadian

business experienced a 35 percent growth in sales in

fiscal 2008. This significant increase was driven largely

by a full year of Eagle Brand sales and our acquisition

of Carnation, the #1 evaporated milk in Canada. Late

in the fiscal year, we also acquired Europe’s Best frozen

fruits and vegetables.

Carnation and Europe’s Best join our already strong

portfolio of #1 brands in Canada, including Smucker’s,

Robin Hood, and Bick’s. The Carnation acquisition

further strengthens our leadership position in the

baking aisle, and Europe’s Best adds premium frozen

fruits and vegetables to our product portfolio.

Adding to a recent string of award-winning innovations

in the baking category, we introduced Robin Hood frozen

muffins this past year. Together, Europe’s Best frozen

fruits and vegetables and Robin Hood frozen muffins

enhance our presence in Canada’s retail freezer aisles.

Foodservice Our Foodservice and Schools business

grew by 27 percent in fiscal 2008. Key contributors

were our core portion control business, Smucker’s

Uncrustables sandwiches, and recent acquisitions

of Eagle Brand and the Snack’n Waffles brand.

Snack’n Waffles ready-to-eat, pre-sweetened waffles

offer consumers a convenient, handheld waffle to

enjoy while away from home.

Beverage Our Beverage group continues to meet

consumer desire for products that are “good and

good for you” and made in a sustainable manner.

This business, driven by our R.W. Knudsen Family

and Santa Cruz Organic brands, grew in sales by nine

percent in fiscal 2008. We introduced new products,

including R.W. Knudsen Family Organic Pomegranate

Nectar, R.W. Knudsen Family Organic Black Currant

Nectar, and Sensible Sippers—juice boxes that provide

parents with a convenient alternative for offering

children organic juice, blended with just the right

amount of water, while at home or on the go.

Our Beverage business is an industry sustainability

leader, receiving the California Waste Reductions

Award for the eighth consecutive year.

International Consumers Consumers in more than

50 countries beyond the United States and Canada con-

tinue to enjoy our brands and products. The International

group remains focused on Mexico and the Caribbean,

with business growing in these markets by six percent

and 66 percent, respectively, in fiscal 2008.

~ 10 ~

We are pleased to welcome these additions to the

Smucker family of brands: Snack’n Waffles ready-

to-eat, pre-sweetened waffles; King Kelly California

Orange Marmalade; and,

in Canada, Carnation

evaporated milk and

Europe’s Best frozen

fruits and vegetables.

Sweet ‘n’ HotSouthwestern DipPrep time: 5 minutesReady in: 2 hoursMakes approximately 2 cups

Orange PecanWaffles with SweetOrange SyrupPrep time: 8 minutesCook time: 10 minutesReady in: 30 minutesMakes 8 waffles

Brownie Bites withCaramel FluffPrep time: 20 minutesBake time: 30 minutesReady in: 1 hour 30 minutesMakes 12 servings

A Touch of OrangeApple PiePrep time: 25 minutesCook time: 45 minutesReady in: 2 hoursMakes 8 servings

Fruit Kabobs withCreamy CherryPeanut Butter DipPrep time: 15 minutesReady in: 15 minutesMakes 8 servings

Mocha Walnut PiePrep time: 30 minutesCook time: 45 minutesReady in: 1 hour 45 minutesMakes 8 servings

Thai Peanut ButterChicken WrapsPrep time: 10 minutesReady in: 10 minutesMakes 4 wraps

Ingredients1 (9-inch) single Classic Crisco® Pie Crust

(recipe available at Crisco.com)2 (1 oz.) squares unsweetened chocolate1/4 cup butter or margarine11/2 tablespoons Kava® Coffee, dissolved in

1/4 cup hot water1 (14 oz.) can Eagle Brand® Sweetened

Condensed Milk2 large eggs, well beaten1 teaspoon vanilla extract1 cup chopped walnuts

Whipped cream or frozen whippedtopping, thawed (optional)

Ingredients1 cup lowfat vanilla yogurt1/4 cup Smucker’s® Creamy Natural

Peanut Butter1/3 cup Smucker’s® Cherry Sugar Free

Preserves or any Smucker’s®

Sugar Free or Low SugarTM flavorof your choice

4 cups fresh fruit such as pineapple chunks,sliced kiwi, melon balls, grapes,assorted whole berries

IngredientsMarinade Juice of 1 lime

2 tablespoons Crisco® Pure Olive Oil1/4 teaspoon salt1/8 teaspoon cayenne pepper1/2 pound fresh sea scallops, 10 to 20 count size1/2 pound fresh tail-on shrimp, 21 to 25 count size1 (6 oz.) package sliced portobello mushrooms

Dressing 1/4 cup balsamic vinegar1/2 teaspoon Dijon mustard

Salt and pepper to taste1 tablespoon chopped fresh herbs (basil,

oregano, thyme)1/2 cup Crisco® Pure Olive Oil

Crisco® Original No-Stick Cooking SpraySalad 12 cups fresh mixed baby greens

1 cup baby grape tomatoes1 medium cucumber, halved lengthwise, sliced1/2 each red and yellow bell peppers,

cut in julienne strips1/4 cup shredded carrots

Freshly grated Parmesan cheese (optional)

IngredientsWaffles 2 cups Hungry Jack® Buttermilk

Complete Pancake & Waffle Mix1/2 cup finely chopped pecans or walnuts1/4 cup Smucker’s® Sweet Orange

Marmalade11/4 cups water1/4 cup Crisco® Pure Vegetable Oil1 large egg

Orange 11/4 cups Smucker’s® Sweet OrangeSyrup Marmalade

1/4 teaspoon ground cinnamon

Whipped cream or frozen whippedtopping, thawed

IngredientsCrisco® Original No-Stick Cooking Spray

1 (12.35 oz.) package Pillsbury®

Reduced Sugar Chocolate FudgeBrownie Mix

1/3 cup Crisco® Pure Vegetable Oil3 tablespoons water1 large egg1/3 cup Smucker’s® Sugar Free

Caramel Topping2 cups sugar free frozen whipped

topping, thawed2 teaspoons mini semi-sweet

chocolate chipsAdditional Smucker’s® Sugar FreeCaramel Topping (optional)

Ingredients1 jar Dickinson’s® Sweet ‘n’ Hot

Pepper & Onion Relish1-2 tablespoons Dickinson’s® Lime Curd1/2 cup mayonnaise1/2 cup sour cream1/2 teaspoon chili powder (optional)

Corn chips or tortilla chips

VARIATIONZesty Pepper ‘n’ Onion DipIngredients1 (8 oz.) package cream cheese, softened1 jar Dickinson’s® Sweet ‘n’ Hot

Pepper & Onion RelishAssorted crackers

Ingredients1/2 cup Jif ® Creamy Peanut Butter

or Jif ® Extra Crunchy Peanut Butter1/2 cup pad thai sauce*1/2 cup chopped green onions4 burrito size tortillas1 (6 oz.) package fully cooked, grilled

chicken breast strips, cut intobite-size pieces or 11/3 cups cookedchicken

2 cups shredded lettuce

*Pad thai sauce is often located inthe Asian foods section of manygrocery stores.

Ingredients1 (9-inch) double Classic Crisco® Pie Crust

(recipe available at Crisco.com)3/4 cup sugar1 tablespoon cornstarch1 teaspoon ground cinnamon1/2 teaspoon grated orange peel1/8 teaspoon salt1/8 teaspoon ground nutmeg7 cups peeled, sliced Granny Smith apples,

about 2 pounds or 7 medium2 tablespoons butter or margarine

MilkSugar

Grilled SeafoodSaladPrep time: 40 minutesCook time: 15 minutesReady in: 1 hourMakes 6 servings

✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥

✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥

✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥

Orange PecanWaffles with Sweet Orange Syrup (Pictured on page 8 )

DirectionsHEAT waffle iron according to manufacturer’s instructions.

COMBINE pancake mix, nuts, 1/4 cup marmalade, water, oil and egg inmedium bowl. Stir until large lumps disappear. Bake in hot waffle ironuntil steaming stops and waffle is golden brown.

PLACE 1 1/4 cups marmalade in microwave-safe bowl. Microwave onHIGH (100% power) 1 minute. Add cinnamon; stir.

SERVE waffles with orange syrup and whipped cream or whippedtopping.

Grilled Seafood Salad (Pictured on page 8 )

DirectionsWHISK together lime juice, oil, salt and cayenne pepper in shallow dish.Add scallops, shrimp and sliced mushrooms; turn to coat. Cover andrefrigerate 30 minutes.

COMBINE vinegar, mustard, salt, pepper and herbs in blender or foodprocessor. Process on high speed until mixture is well blended. With themotor running, carefully pour in olive oil in a steady stream. Set aside.

SPRAY grill pan or sauté pan with no-stick cooking spray; heat tomedium high heat. Remove seafood and mushrooms from marinade;discard marinade. Cook shrimp and scallops 2 to 3 minutes per side oruntil seafood is cooked through and has browned highlights. Removefrom pan; set aside. Add mushrooms to pan; grill 4 to 5 minutes, turn-ing once. Remove from pan.

ARRANGE salad ingredients on medium platter. Top with grilled seafoodand mushrooms. Drizzle dressing as desired over salad. Top withParmesan cheese, if desired.

Fruit Kabobs with Creamy Cherry Peanut Butter Dip (Pictured on page 9 )

DirectionsWHISK together yogurt, peanut butter and preserves in small bowluntil thoroughly mixed. Spoon into small serving dish.

THREAD pieces of fruit onto wooden skewers. Arrange skewers anddip on serving platter.

Mocha Walnut Pie (Pictured on page 8 )

DirectionsPREPARE recipe for single crust pie. Roll out dough; place in 9-inchpie plate. Press to fit without stretching dough. Trim edge of dough,leaving a 3/4-inch overhang. Fold edge under; flute dough as desired.Heat oven to 350ºF.

MELT chocolate and butter in medium saucepan over low heat. Stir indissolved coffee, sweetened condensed milk, eggs and vanilla; mixwell. Pour into pie crust. Top with walnuts.

BAKE 40 to 45 minutes or until center is set. Cool slightly. Serve warmor chilled, topped with whipped cream or whipped topping,if desired.

Sweet ‘n’ Hot Southwestern Dip (Pictured on page 4 )

DirectionsSTIR together all ingredients in small serving bowl.

COVER and chill 2 hours. Serve with corn chips or tortilla chips.

TIP: This is a great sandwich and hamburger spread too!

Zesty Pepper ‘n’ Onion DipDirectionsBEAT cream cheese in medium bowl until smooth. Gradually mixin relish. Spoon into small serving bowl.

COVER and chill at least 1 hour. Serve with crackers.

TIP: For an easier option, unwrap the block of cream cheese and placeon a decorative plate. Pour relish over top. Serve with a small knifeand crackers.

A Touch of Orange Apple Pie (Pictured on page 4 )

DirectionsPREPARE recipe for double crust pie. Roll out dough for bottom crust;place in 9-inch pie plate. Press to fit without stretching dough. Trim evenwith pie plate. Heat oven to 400ºF.

COMBINE sugar, cornstarch, cinnamon, orange peel, salt and nutmeg insmall bowl. Place apples in unbaked pie crust. Sprinkle sugar mixtureover apples. Dot with butter. Moisten pastry edge with water.

ROLL out dough for top crust. Place onto filled pie. Trim 1/2-inch beyondedge. Fold top crust under bottom crust edge to seal. Crimp and fluteedges. Cut slits in top crust or perforate with fork to allow steam to escape.

BAKE 35 minutes. Remove pie from oven. Brush with milk. Sprinkle withsugar. Cover edge of pie with foil, if necessary, to prevent overbrowning.Bake an additional 10 minutes or until filling in center is bubbly andcrust is golden brown. Cool completely on wire rack.

Brownie Bites with Caramel Fluff (Pictured on page 5 )

DirectionsHEAT oven to 350°F. Coat an 8 x 8-inch baking pan lightly withno-stick cooking spray.

COMBINE brownie mix, oil, water and egg in medium bowl.Stir 50 strokes with spoon. Spread evenly in prepared pan.

BAKE 30 to 32 minutes. Cool completely. Cut into cubes. Place halfof cubes in 1 1/2-quart serving dish.

STIR caramel topping in small bowl until smooth. Whisk in whippedtopping until blended. Spread half on top of brownie cubes in dish.Make another layer of remaining brownie cubes and topping.Sprinkle with mini chocolate chips. Drizzle with additional carameltopping, if desired.

Thai Peanut Butter Chicken Wraps (Pictured on page 5 )

DirectionsSTIR together peanut butter, pad thai sauce and green onions inmedium bowl.

PLACE tortilla on microwave-safe plate. Spread 1/4 peanut buttermixture on tortilla to about 1/2-inch of edge. Microwave on HIGH(100% power) 20 seconds.

LAYER with 1/4 chicken; top with 1/2 cup lettuce. Wrap burrito style:Fold one edge of tortilla up about 1 inch over filling; fold right andleft sides over folded edge; roll up, ending with loose edge on bottom.Cut in half diagonally.

REPEAT with remaining tortillas.

©/® The J. M. Smucker Company

©/TM/® The J. M. Smucker Company ©/® The J. M. Smucker Company

©/® The J. M. Smucker Company ©/® The J. M. Smucker Company

©/® The J. M. Smucker Company

©/® The J. M. Smucker CompanyPillsbury is a trademark of The Pillsbury Company, LLC usedunder license.

crisco.comhungryjack.comsmuckers.com

smuckers.com

crisco.comeaglebrand.comkavacoffee.com

crisco.com

dickinsonsfamily.com

crisco.compillsburybaking.com

smuckers.com

crisco.com

jif.com

©/® The J. M. Smucker Company

✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥

✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥

✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥✥

~ 13 ~

Financial Review✷✷✷

Five-Year Summary of Selected Financial Data 14

Summary of Quarterly Results of Operations 15

Stock Price Data 15

Comparison of Five-Year CumulativeTotal Shareholder Return 16

Management’s Discussion and Analysis 17

Report of Management on Internal ControlOver Financial Reporting 27

Report of Independent Registered Public AccountingFirm on Internal Control Over Financial Reporting 28

Report of Independent Registered Public AccountingFirm on the Consolidated Financial Statements 29

Report of Management on Responsibilityfor Financial Reporting 30

Consolidated Financial Statements 31

Notes to Consolidated Financial Statements 36

Directors, Officers, and General Managers 64

Properties 64

Corporate and Shareholder Information 65

~ 14 ~

The following table presents selected financial data for each of the five years in the period ended April 30, 2008. The selectedfinancial data was derived from the consolidated financial statements and should be read in conjunction with “Management’sDiscussion and Analysis of Results of Operations and Liquidity and Capital Resources” and the consolidated financial statementsand notes thereto.

Year Ended April 30,

(Dollars in thousands, except per share data) 2008 2007 2006 2005 2004

Statements of Income:Net sales $2,524,774 $2,148,017 $2,154,726 $2,043,877 $1,369,556Income from continuing operations $ 170,379 $ 157,219 $ 143,354 $ 130,460 $ 111,298Discontinued operations — — — (1,387) 52

Net income $ 170,379 $ 157,219 $ 143,354 $ 129,073 $ 111,350

Financial Position:Total assets $3,129,881 $2,693,823 $2,649,744 $2,635,894 $1,684,125Cash and cash equivalents 184,175 200,119 71,956 58,085 104,551Long-term debt 789,684 392,643 428,602 431,560 135,000Shareholders’ equity 1,799,853 1,795,657 1,728,059 1,690,800 1,210,693

Other Data:Capital expenditures $ 76,430 $ 57,002 $ 63,580 $ 87,576 $ 97,721Common shares repurchased 2,927,600 1,067,400 1,892,100 368,678 —Weighted-average shares 56,226,206 56,432,839 57,863,270 57,086,734 49,816,926Weighted-average shares – assuming dilution 56,720,645 57,056,421 58,425,361 57,748,780 50,395,747Earnings per common share:

Income from continuing operations $ 3.03 $ 2.79 $ 2.48 $ 2.29 $ 2.23Discontinued operations — — — (0.03) 0.01

Net income $ 3.03 $ 2.79 $ 2.48 $ 2.26 $ 2.24

Income from continuing operations –assuming dilution $ 3.00 $ 2.76 $ 2.45 $ 2.26 $ 2.21

Discontinued operations – assuming dilution — — — (0.02) —

Net income – assuming dilution $ 3.00 $ 2.76 $ 2.45 $ 2.24 $ 2.21

Dividends declared per common share $ 1.22 $ 1.14 $ 1.09 $ 1.02 $ 0.94

Five-Year Summary of Selected Financial Data

✷✷✷

~ 15 ~

Summary of Quarterly Results of Operations

The following is a summary of unaudited quarterly results of operations for the years ended April 30, 2008 and 2007.

(Dollars in thousands, except per share data)Earnings per

Net Earnings per Common Share –Quarter Ended Net Sales Gross Profit Income Common Share Assuming Dilution

2008 July 31, 2007 $561,513 $185,984 $40,761 $0.72 $0.71October 31, 2007 707,890 218,488 50,166 0.88 0.87January 31, 2008 665,373 195,453 42,401 0.75 0.75

April 30, 2008 589,998 182,239 37,051 0.68 0.67

2007 July 31, 2006 $526,509 $157,994 $28,724 $0.51 $0.50October 31, 2006 604,955 191,191 45,569 0.80 0.80January 31, 2007 523,081 172,967 40,427 0.72 0.71

April 30, 2007 493,472 179,903 42,499 0.76 0.75

Annual earnings per share may not equal the sum of the individual quarters due to differences in the average number of sharesoutstanding during the respective periods.

Stock Price Data

The Company’s common shares are listed on the New York Stock Exchange – ticker symbol SJM. The table below presents thehigh and low market prices for the shares and the quarterly dividends declared. There were approximately 267,380 shareholdersas of June 17, 2008, of which 78,959 were registered holders of common shares.

Quarter Ended High Low Dividends

2008 July 31, 2007 $64.32 $55.60 $0.30October 31, 2007 58.09 50.79 0.30January 31, 2008 53.70 42.75 0.30

April 30, 2008 52.59 46.84 0.32

2007 July 31, 2006 $47.25 $39.11 $0.28October 31, 2006 49.14 43.00 0.28January 31, 2007 49.98 45.00 0.28

April 30, 2007 57.43 46.97 0.30

✷✷✷

✷✷✷

✷✷✷

~ 16 ~

Comparison of Five-Year Cumulative Total Shareholder Return

April 30,

2003 2004 2005 2006 2007 2008

The J. M. Smucker Company $100.00 $147.38 $142.81 $115.66 $168.57 $154.05S&P 500 100.00 122.88 130.66 150.81 173.79 165.66S&P Packaged Foods & Meats 100.00 129.21 138.28 133.81 159.84 156.94

The above graph compares the cumulative total shareholder return for the five years ended April 30, 2008, for the Company’scommon shares, the S&P 500, and the S&P Packaged Foods and Meats index. These figures assume all dividends are reinvestedwhen received and are based on $100 invested in the Company’s common shares and the referenced index funds on April 30, 2003.

Among The J. M. Smucker Company, the S&P 500 Index, and the S&P Packaged Foods & Meats Index

Copyright © 2008, Standard & Poor’s, a division of The McGraw-Hill Companies, Inc. All rights reserved.

www.researchdatagroup.com/S&P.htm

$180

$160

$140

$120

$100

$80

$60

$40

$20

$0

4/03 4/04 4/05 4/06 4/07 4/08

◆◆

◆

◆◆

• • ••

■■

■

■

■

■ The J. M. Smucker Company

◆ S&P 500

• S&P Packaged Foods & Meats

•

■

~ 17 ~

~ Summary of 2008 ~

The Company realized strong sales growth in 2008 as the

impacts of Eagle and other recent acquisitions, pricing and

volume gains, and favorable foreign currency exchange rates

were realized. Company net sales increased 18 percent to

$2,524.8 million in 2008 from $2,148.0 million in 2007 while

net income increased eight percent to $170.4 million in 2008

from $157.2 million in 2007. Net income per common share –

assuming dilution was $3.00 in 2008, an increase of nine per-

cent from $2.76 in 2007, resulting from the increase in net

income combined with a decrease in common shares outstand-

ing during the year.

~ Net Sales ~

Year Ended April 30,

(Dollars in thousands) 2008 2007 2006

Net sales:U.S. retail market $1,874,547 $1,547,064 $1,484,873

Special markets 650,227 600,953 669,853

Total net sales $2,524,774 $2,148,017 $2,154,726

2008 Compared to 2007. Net sales increased $376.8 million, or

18 percent, in 2008 from 2007. Net sales increased 22 percent

over the same period, excluding the divested Canadian non-

branded, grain-based foodservice and industrial businesses

(“divested Canadian businesses”) sold in September 2006.

The acquired Eagle businesses contributed $236.2 million in

net sales in 2008, accounting for approximately one-half of the

increase in net sales excluding the divested Canadian busi-

nesses, while pricing contributed almost one-third of the

increase. Also contributing to net sales growth in 2008 were

gains in the Smucker’s, Jif, Crisco, and Hungry Jack brands, the

acquired Carnation canned milk business in Canada, and the

impact of favorable foreign exchange rates.

In the U.S. retail market segment, comprised of the Company’s

consumer and consumer oils and baking strategic business

areas, net sales were $1,874.5 million in 2008, up 21 percent

compared to $1,547.1 million in 2007. Net sales in the con-

Executive Summary

✷✷✷

The J. M. Smucker Company (the “Company”), headquartered

in Orrville, Ohio, is the leading marketer and manufacturer of

fruit spreads, peanut butter, shortening and oils, ice cream top-

pings, sweetened condensed milk, and health and natural foods

beverages in North America.

The Company’s strategy is to own and market leading food

brands found in the center of the store and sold throughout

North America. Its family of brands includes Smucker’s, Jif,

Crisco, Pillsbury, Eagle Brand, R.W. Knudsen Family, Hungry

Jack, White Lily, and Martha White in the United States, along

with Robin Hood, Five Roses, Carnation, Europe’s Best, and

Bick’s in Canada. In addition to these brands, the Company

markets products under numerous other brands, including

Dickinson’s, Laura Scudder’s, Adams, Double Fruit (Canada),

and Santa Cruz Organic. The Company is widely known and

trusted for quality food products.

The Company distributes its products through grocery and

other retail outlets, foodservice establishments, schools, spe-

cialty and gourmet shops, health and natural foods stores, and

consumer direct vehicles such as the Internet and a showcase

store in Orrville, Ohio, and markets a wide variety of other

specialty products throughout North America and in many for-

eign countries.

Since 1998, the Company has appeared on FORTUNE maga-

zine’s annual listing of the “100 Best Companies to Work For,”

in the United States, ranking number one in 2004.

Results of Operations

✷✷✷

On May 1, 2007, the Company acquired Eagle Family Foods

Holdings, Inc. (“Eagle”) in a transaction valued at approxi-

mately $248 million. The transaction has been accounted for as

a purchase business combination and the results of Eagle are

included in the Company’s consolidated financial statements

from the date of acquisition.

Management’s Discussion and Analysis

✷✷✷

cent over the same period, excluding the divested Canadian

businesses and the U.S. industrial ingredient business

(“divested businesses”). This net sales growth was led prima-

rily by volume gains in the Jif and Smucker’s brands, strong per-

formance across the businesses in the special markets

segment, and the contribution of approximately $33.4 million

from the White Lily and Five Roses brands acquired during 2007.

Price increases were also taken on most brands during the year.

In the U.S. retail market segment net sales were $1,547.1 mil-

lion in 2007, up $62.2 million, or approximately four percent,

over 2006. Net sales in the consumer strategic business area

were up seven percent for the year. The consumer increase

was led by strong sales of Jif peanut butter, particularly in the

fourth quarter of the fiscal year resulting from increased

demand for the product upon the recall of a competitor’s prod-

ucts. In addition, growth in natural peanut butter, fruit spreads,

toppings, and a 29 percent increase in Smucker’s Uncrustables

sandwiches during the year also contributed. In the consumer

oils and baking strategic business area, sales were flat com-

pared to the prior year as sales gains in retail oils, frosting,

flour, and the contribution of $14.8 million from the White Lily

brand acquired in October 2006 offset declines in baking mixes

and a $14.7 million decrease in sales of industrial oils.

Net sales in the special markets segment were $601.0 million

in 2007, a decrease of 10 percent, compared to 2006.

Excluding divested businesses, special market net sales

increased nine percent for the same period. All strategic busi-

ness areas in special markets contributed to the increase.

Foodservice net sales increased 13 percent, due to a 10 per-

cent increase in sales of traditional portion control products, as

well as a 20 percent increase in Smucker’s Uncrustables sand-

wiches in the schools market. Beverage net sales increased 11

percent in 2007 compared to 2006, as sales of R. W. Knudsen

Family, Santa Cruz Organic, and nonbranded products

increased nine, 21, and 19 percent, respectively. Net sales in

Canada increased five percent driven by the contribution of

approximately $18.6 million from the acquisition of the

~ 18 ~

sumer strategic business area increased nine percent led by

strong sales in peanut butter, fruit spreads, and Smucker’s

Uncrustables sandwiches. Excluding the contribution of $198.9

million from the acquired Eagle business in 2008, net sales in

the oils and baking strategic business area increased eight per-

cent as sales gains were realized in baking mixes and oils.

The special markets segment is comprised of the foodservice,

beverage, Canada, and international strategic business areas.

Net sales in this segment were $650.2 million in 2008, an

increase of eight percent compared to $601.0 million in 2007.

Excluding the divested Canadian businesses, net sales in the

special markets segment increased 24 percent in 2008 com-

pared to 2007. Canada contributed significantly to the increase

in special markets segment net sales due to the impacts of the

acquired Eagle and Carnation canned milk businesses and

favorable foreign exchange rates. The acquisition of Europe’s

Best brand of premium, all natural, frozen fruit and vegetables

during the fourth quarter of 2008 also contributed slightly to

the Canada sales increase. The foodservice strategic business

area net sales increased 27 percent in 2008 compared to 2007,

or 14 percent, excluding the contribution of $21.1 million of

Eagle net sales. Contributing to the foodservice improvement

in 2008 was continued growth of Smucker’s Uncrustables sand-

wiches, which realized a 15 percent increase, and a 12 percent

increase in traditional portion control products, primarily

peanut butter. Net sales in the beverage strategic business

area increased nine percent in 2008 compared to 2007 result-

ing from increases in R.W. Knudsen Family, Santa Cruz

Organic, and nonbranded products of seven, 14, and nine per-

cent, respectively. Net sales in the international strategic busi-

ness area increased two percent in 2008 despite the divestiture

of the Scotland business during the first quarter of 2008, driven

by a 19 percent increase in export sales and a six percent

increase in net sales in Mexico.

2007 Compared to 2006. Net sales in 2007 decreased $6.7 mil-

lion, or less than one percent, from 2006 reflecting the impact

of divestitures. Net sales increased $107.5 million, or five per-

~ 19 ~

Five Roses flour brand during the year and the impact of favor-

able exchange rates. In the international strategic business

area, net sales increased 14 percent primarily due to continued

growth in export markets.

~ Operating Income ~

The following table presents components of operating income

as a percentage of net sales.

Year Ended April 30,

2008 2007 2006

Gross profit 31.0% 32.7% 32.2%Selling, distribution,

and administrative expenses:Advertising 2.2% 2.4% 2.6%Marketing and selling 7.5 7.6 7.4Distribution 3.4 3.5 3.6General and administrative 6.3 7.1 6.7

Total selling, distribution,and administrative expenses 19.4% 20.6% 20.3%

Restructuring and mergerand integration costs 0.4% 0.1% 1.3%

Other operating (income)expense – net (0.1%) 0.2% (0.2%)

Operating income 11.3% 11.8% 10.8%

2008 Compared to 2007. Operating income increased 12 percent

in 2008 to $284.2 million, compared to 2007 while decreasing

as a percentage of net sales from 11.8 percent in 2007 to 11.3

percent in 2008. The impact of the lower margin Eagle busi-

nesses, record costs for soybean oil and wheat, and the mix of

products sold during the year resulted in a decline in gross

profit as a percentage of net sales from 32.7 percent in 2007 to

31.0 percent in 2008. The margin on the Eagle businesses was

impacted by an increase in milk costs and an unfavorable mix

of nonbranded sales during the year and accounted for approx-

imately one-half of the decrease in gross profit as a percentage

of net sales. The impact of price increases taken during the

year across all businesses, while essentially offsetting higher

raw material cost increases of approximately $150 million com-

pared to 2007, was not sufficient to maintain margins.

Selling, distribution, and administrative (“SD&A”) expenses

increased 11 percent from 2007 to $490.7 million in 2008,

resulting from increased marketing spending and additional

costs related to the acquired Eagle businesses. However, cor-

porate overhead expenses increased at a lesser rate than net

sales resulting in SD&A as a percent of net sales improving

from 20.6 percent in 2007 to 19.4 percent in 2008. Higher

restructuring and merger and integration costs in 2008 com-

pared to 2007 also negatively impacted operating income.

Other operating income – net of $3.9 million was recognized in

2008 resulting from a net insurance settlement related to

storm damage at a third-party distribution and warehouse facil-

ity in Memphis, Tennessee. Other operating expense – net of

$2.7 million was recognized in 2007 consisting of losses on dis-

posal of assets.

2007 Compared to 2006. Operating income increased $22.2 mil-

lion in 2007, or 10 percent, compared to 2006, and increased

from 10.8 percent of net sales in 2006 to 11.8 percent in 2007.

The increase in operating income in 2007 was primarily due to

improvements in gross profit and a decrease in merger and

integration costs. Gross profit increased from $692.9 million,

or 32.2 percent of net sales in 2006, to $702.1 million, or

32.7 percent of net sales in 2007. The increase in gross profit

occurred, despite a record high commodity price environment,

due to the divestiture of the lower margin Canadian non-

branded businesses during the second quarter of 2007 and

favorable product mix, particularly in the fourth quarter of

2007. These favorable contributions to gross profit were offset

in part by an increase in restructuring related impairment

charges in 2007 associated with the Canadian divestiture.

Although the Company implemented pricing actions to miti-

gate commodity cost increases totaling approximately $30 mil-

lion during the year, these cost increases were not fully offset

for the year.

~ 20 ~

SD&A expenses increased $4.4 million in 2007, or approximately

one percent, from 2006, and increased from 20.3 percent of net

sales in 2006 to 20.6 percent in 2007 due to costs associated with

the Company’s transition to restricted stock-based compensation

programs and the related impact of adopting Statement of

Financial Accounting Standards No. 123 (revised), Share-Based

Payment. Selling expenses were also up in 2007 compared to

2006. Marketing and distribution expense decreased in 2007

from 2006 as the Company actively managed SD&A costs to help

offset the impact of higher raw material costs.

Other operating expense – net of $2.7 million was recognized

in 2007 consisting of losses on disposal of assets. Other oper-

ating income – net of $3.4 million was recognized in 2006 as

the net gain on the sale of the Salinas facility of $5.6 million

offset losses on disposal of assets during the year.

~ Interest Income and Expense ~

Interest expense increased $18.8 million in 2008 compared to

2007, resulting from the issuance of $400 million in senior

notes on May 31, 2007, a portion of which was used to repay

short-term debt used in financing the Eagle acquisition. The

investment of excess proceeds resulted in an increase in inter-

est income of $4.0 million during 2008 compared to 2007.

Interest expense decreased $0.7 million in 2007 compared to

2006 as a portion of the proceeds from the sale of the Canadian

nonbranded businesses was utilized to pay off balances out-

standing against the Company’s revolving credit facility during

the second quarter of 2007. Also during 2007 interest income

increased $2.6 million compared to 2006, primarily related to

an increase in invested funds during the year resulting from

the Canadian nonbranded businesses sale and an overall

increase in cash generated from operations.

~ Income Taxes ~

Income taxes in 2008 were $84.4 million, up $0.6 million, or

one percent, from 2007. The increase in income taxes that

would have resulted from higher income in 2008 as compared

to 2007 was mostly offset by a decrease in the effective tax rate

from 34.8 percent in 2007 to 33.1 percent in 2008. The lower

effective tax rate for 2008 was primarily attributable to a lower

state tax rate resulting from the favorable resolution of uncer-

tain tax positions.

Income taxes were $83.8 million in 2007, an increase of $11.6

million, or 16 percent, from 2006. The increase is due prima-

rily to an increase in taxable income, combined with an

increase in the effective tax rate from 33.5 percent in 2006 to

34.8 percent in 2007. The effective tax rate in 2006 included

certain one-time benefits of the Company’s legal entity

realignment that did not recur in 2007.

~ Restructuring ~

During 2003, the Company announced plans to restructure cer-

tain operations as part of its ongoing efforts to refine its portfo-

lio, optimize its production capacity, improve productivity and

operating efficiencies, and improve the Company’s overall cost

base as well as service levels in support of its long-term strat-

egy. At the end of 2008, these restructurings were proceeding as

planned.

In conjunction with the restructurings, the Company has

recorded total charges of $58.5 million to date, including $4.7

million in 2008, $12.1 million in 2007, and $10.0 million in 2006.

The majority of these charges related to impairment and accel-

erated depreciation on buildings and machinery and equipment,

system conversion costs, employee separation costs, equipment

relocation expenses, and the disposition of inventories.

~ Subsequent Event ~

On June 4, 2008, the Company entered into a definitive agree-

ment with The Procter & Gamble Company (“P&G”) to merge

P&G’s Folgers coffee business with and into the Company.

Under the terms of the agreement, P&G will distribute the

Folgers business to P&G shareholders in a tax-free transaction,

with a simultaneous merger with and into the Company. In the

merger, current P&G shareholders will receive approximately

~ 21 ~

~ Operating Activities ~

The Company’s working capital requirements are greatest

during the first half of its fiscal year, primarily due to the need

to build inventory levels in advance of the “fall bake” season,

the seasonal procurement of fruit, and the purchase of raw

materials used in the Company’s pickle and relish business in

Canada. The acquisition of the Eagle businesses added further

to the cash requirements during the first half of the year.

Cash provided by operating activities was $191.6 million

during 2008, a decrease of $81.8 million, or 30 percent, over

2007. The decrease in cash from operations was primarily due

to an increase in the cash required to support working capital

requirements. Working capital, excluding cash and cash equiv-

alents, as a percent of net sales increased to 14.0 percent in

2008 from 9.4 percent in 2007 primarily as a result of higher

inventory balances associated with increased raw material costs.

~ Investing Activities ~

Net cash used for investing activities totaled approximately

$262.5 million in 2008, as $220.9 million was used for business

acquisitions, primarily Eagle, the Carnation canned milk busi-

ness in Canada, and Europe’s Best. Capital expenditures were

approximately $76.4 million during 2008, or three percent of

net sales.

~ Financing Activities ~

Net cash provided by financing activities during 2008 consisted

primarily of the Company’s issuance of $400 million in senior

notes on May 31, 2007, offset by the repayment of $148 million

of debt, including $115 million assumed in the Eagle acquisi-

tion, $152.5 million used to finance the repurchases of treasury

shares, and $68.1 million in dividend payments.

The purchase of treasury shares was comprised largely of

2,927,600 common shares, representing approximately five per-

cent of common shares outstanding at the beginning of 2008.

53.5 percent of the Company’s shares and current Company

shareholders will own approximately 46.5 percent of the com-

bined company upon closing. Upon closing, the Company will

have approximately 118 million shares outstanding. As part of

the transaction, the Company will assume an estimated $350

million of Folgers debt. The transaction is expected to be tax

free to both companies and P&G shareholders. In addition,

Company shareholders as of the record date, prior to the

merger, will receive a special dividend of $5 per share. The

record date for the special dividend will be determined by the

Company at a future date.

The transaction is expected to close in the fourth quarter of cal-

endar 2008, subject to customary closing conditions including

regulatory and Company shareholder approvals. The Company

expects to incur approximately $100 million in one-time costs

related to the transaction over the next two fiscal years.

The merger will be accounted for as a purchase business com-

bination. For accounting purposes, the Company will be treated

as the acquiring enterprise.

Liquidity and Capital Resources

✷✷✷

Year Ended April 30,

(Dollars in thousands) 2008 2007 2006

Net cash provided byoperating activities $ 191,577 $273,424 $198,689

Net cash used forinvesting activities 262,486 27,041 16,255

Net cash provided by(used for) financingactivities 49,839 (117,625) (169,129)

The Company’s principal source of funds is cash generated

from operations, supplemented by borrowings against the

Company’s revolving credit facility. Total cash and investments

at April 30, 2008, were $200.2 million compared to $244.2 mil-

lion at April 30, 2007.

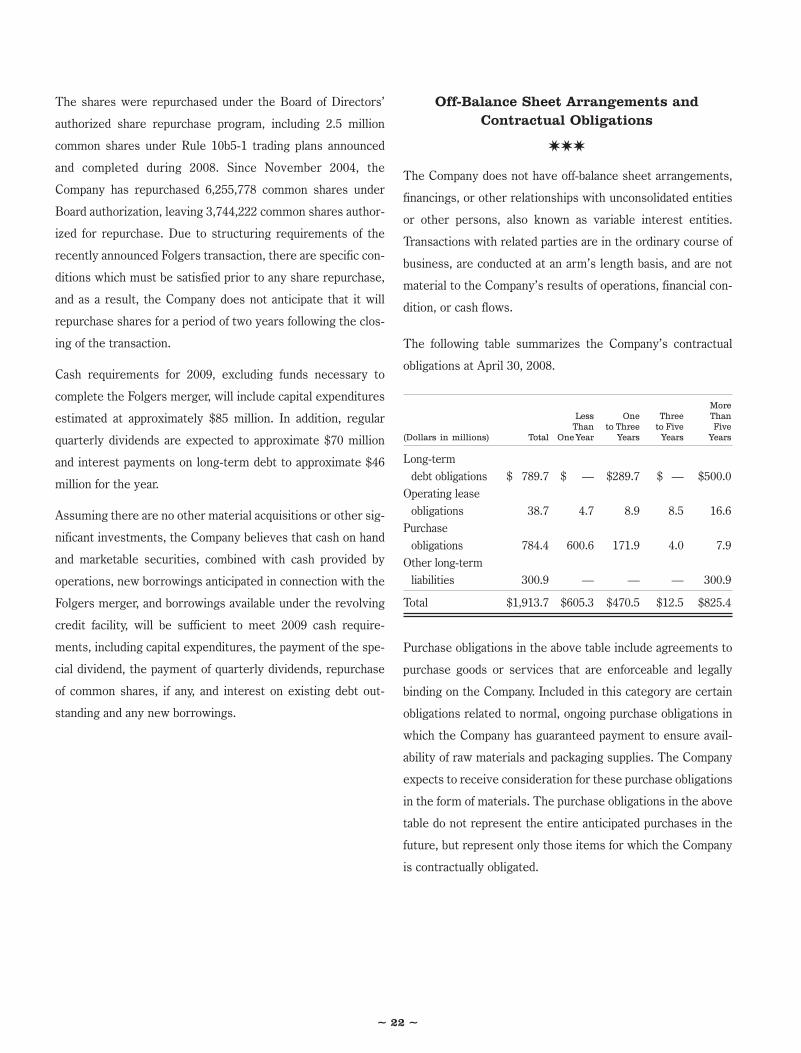

The shares were repurchased under the Board of Directors’

authorized share repurchase program, including 2.5 million

common shares under Rule 10b5-1 trading plans announced

and completed during 2008. Since November 2004, the

Company has repurchased 6,255,778 common shares under

Board authorization, leaving 3,744,222 common shares author-

ized for repurchase. Due to structuring requirements of the

recently announced Folgers transaction, there are specific con-

ditions which must be satisfied prior to any share repurchase,

and as a result, the Company does not anticipate that it will

repurchase shares for a period of two years following the clos-

ing of the transaction.

Cash requirements for 2009, excluding funds necessary to

complete the Folgers merger, will include capital expenditures

estimated at approximately $85 million. In addition, regular

quarterly dividends are expected to approximate $70 million

and interest payments on long-term debt to approximate $46

million for the year.

Assuming there are no other material acquisitions or other sig-

nificant investments, the Company believes that cash on hand

and marketable securities, combined with cash provided by

operations, new borrowings anticipated in connection with the

Folgers merger, and borrowings available under the revolving

credit facility, will be sufficient to meet 2009 cash require-

ments, including capital expenditures, the payment of the spe-

cial dividend, the payment of quarterly dividends, repurchase

of common shares, if any, and interest on existing debt out-

standing and any new borrowings.

Off-Balance Sheet Arrangements andContractual Obligations

✷✷✷

The Company does not have off-balance sheet arrangements,

financings, or other relationships with unconsolidated entities

or other persons, also known as variable interest entities.

Transactions with related parties are in the ordinary course of

business, are conducted at an arm’s length basis, and are not

material to the Company’s results of operations, financial con-

dition, or cash flows.

The following table summarizes the Company’s contractual

obligations at April 30, 2008.

MoreLess One Three ThanThan to Three to Five Five

(Dollars in millions) Total OneYear Years Years Years

Long-termdebt obligations $ 789.7 $ — $289.7 $ — $500.0

Operating leaseobligations 38.7 4.7 8.9 8.5 16.6

Purchaseobligations 784.4 600.6 171.9 4.0 7.9

Other long-termliabilities 300.9 — — — 300.9

Total $1,913.7 $605.3 $470.5 $12.5 $825.4

Purchase obligations in the above table include agreements to

purchase goods or services that are enforceable and legally

binding on the Company. Included in this category are certain

obligations related to normal, ongoing purchase obligations in

which the Company has guaranteed payment to ensure avail-

ability of raw materials and packaging supplies. The Company

expects to receive consideration for these purchase obligations

in the form of materials. The purchase obligations in the above

table do not represent the entire anticipated purchases in the

future, but represent only those items for which the Company

is contractually obligated.

~ 22 ~

~ 23 ~

Critical Accounting Estimates and Policies

✷✷✷

The preparation of financial statements in conformity with

accounting principles generally accepted in the United States

requires management to make estimates and assumptions that

in certain circumstances affect amounts reported in the accom-

panying consolidated financial statements. In preparing these

financial statements, management has made its best estimates

and judgments of certain amounts included in the financial

statements, giving due consideration to materiality. The

Company does not believe there is a great likelihood that mate-

rially different amounts would be reported under different con-

ditions or using different assumptions related to the accounting

policies described below. However, application of these

accounting policies involves the exercise of judgment and use

of assumptions as to future uncertainties and, as a result,

actual results could differ from these estimates.

Revenue Recognition. The Company recognizes revenue when

all of the following criteria have been met: a valid customer

order with a determinable price has been received; the product

has been shipped and title has transferred to the customer;

there is no further significant obligation to assist in the resale

of the product; and collectibility is reasonably assured. A pro-

vision for estimated returns and allowances is recorded as a

reduction of sales at the time revenue is recognized.

Trade Marketing and Merchandising Programs. In order to

support the Company's products, various promotional activities

are conducted through the retail trade, distributors, or directly

with consumers, including in-store display and product place-

ment programs, feature price discounts, coupons, and other

similar activities. The Company regularly reviews and revises,

when it deems necessary, estimates of costs to the Company for

these promotional programs based on estimates of what will be

redeemed by the retail trade, distributors, or consumers. These

estimates are made using various techniques including histori-

cal data on performance of similar promotional programs.

Differences between estimated expense and actual perform-

ance are recognized as a change in management’s estimate in a

subsequent period. As the Company’s total promotional expen-

ditures, including amounts classified as a reduction of net sales,

represent approximately 26 percent of 2008 net sales, the like-

lihood exists of materially different reported results if factors

such as the level and success of the promotional programs or

other conditions differ from expectations.

Income Taxes. The future tax benefit arising from the net

deductible temporary differences and tax carryforwards is

approximately $59.7 million and $63.2 million, at April 30, 2008

and 2007, respectively. Management believes that the

Company’s earnings during the periods when the temporary

differences become deductible will be sufficient to realize the

related future income tax benefits. For those jurisdictions

where the expiration date of tax carryforwards or the projected

operating results of the Company indicate that realization is

not likely, a valuation reserve has been provided.

In assessing the need for a valuation allowance, the Company

estimates future taxable income, considering the viability of

ongoing tax planning strategies and the probable recognition of

future tax deductions and loss carryforwards. Valuation

allowances related to deferred tax assets can be affected by

changes in tax laws, statutory tax rates, and projected future

taxable income levels. Under current accounting rules,

changes in estimated realization of deferred tax assets would

result in either an adjustment to goodwill, if the change relates

to tax benefits associated with a business combination, or an

adjustment to income, in the period in which that determina-

tion is made.

In the ordinary course of business, the Company is exposed to

uncertainties related to tax filing positions and periodically

assesses these tax positions for all tax years that remain sub-

ject to examination, based upon the latest information avail-

able. For uncertain tax positions, the Company has recorded

tax reserves, including any applicable interest and penalty

charges, in accordance with Financial Accounting Standards

Board Interpretation No. 48.

~ 24 ~

Long-Lived Assets. Historically, long-lived assets have been

reviewed for impairment whenever events or changes in cir-

cumstances indicate that the carrying amount of the asset may

not be recoverable. Recoverability of assets to be held and

used is measured by a comparison of the carrying amount of

the assets to future net cash flows estimated to be generated

by such assets. If such assets are considered to be impaired,

the impairment to be recognized is the amount by which the

carrying amount of the assets exceeds the fair value of the

assets. However, determining fair value is subject to estimates

of both cash flows and interest rates and different estimates

could yield different results. There are no events or changes in

circumstances of which management is aware indicating that

the carrying value of the Company’s long-lived assets may not

be recoverable.

Goodwill and Indefinite-Lived Intangible Assets. The annual

evaluation of goodwill and indefinite-lived intangible assets

requires the use of estimates about future operating results for

each reporting unit to determine estimated fair value. Changes

in forecasted operations can materially affect these estimates.

Additionally, other changes in the estimates and assumptions,

including the discount rate and expected long-term growth

rate, which drive the valuation techniques employed to esti-

mate the fair value of the reporting unit could change and,

therefore, impact the assessments of impairment in the future.

Pension and Other Postretirement Benefit Plans. To determine

the Company’s ultimate obligation under its defined benefit

pension plans and other postretirement benefit plans, manage-

ment must estimate the future cost of benefits and attribute

that cost to the time period during which each covered

employee works. Various actuarial assumptions must be made

in order to predict and measure costs and obligations many

years prior to the settlement date, the most significant being

the interest rates used to discount the obligations of the plans,

the long-term rates of return on the plans’ assets, assumed pay

increases, and the health care cost trend rates. Management,

along with third-party actuaries and investment managers,

reviews all of these assumptions on an ongoing basis to ensure

that the most reasonable information available is being consid-

ered. For 2009 expense recognition, the Company will use a

discount rate of 6.6 percent and 6.1 percent, and a rate of com-

pensation increase of 3.8 percent and 4.0 percent, for U.S. and

Canadian plans, respectively. The Company will use an

expected rate of return on plan assets of 7.75 percent for U.S.

plans. For the Canadian plans, the Company will use an

expected rate of return on plan assets of 7.0 percent for the

hourly plan and 7.5 percent for all other plans.

Recovery of Trade Receivables. In the normal course of busi-

ness, the Company extends credit to customers that satisfy

predefined criteria. The Company evaluates the collectibility of

trade receivables based on a combination of factors. When

aware that a specific customer may be unable to meet its finan-

cial obligations, such as in the case of bankruptcy filings or

deterioration in the customer’s operating results or financial

position, the Company records a specific reserve for bad debt

to reduce the related receivable to the amount the Company

reasonably believes is collectible. The Company also records

reserves for bad debt for all other customers based on a vari-

ety of factors, including the length of time the receivables are

past due, historical collection experience, and an evaluation of

current and projected economic conditions at the balance sheet

date. Actual collections of trade receivables could differ from

management’s estimates due to changes in future economic or

industry conditions or specific customers’ financial conditions.

Derivative Financial Instrumentsand Market Risk

✷✷✷

The following discussions about the Company’s market risk

disclosures involve forward-looking statements. Actual results

could differ from those projected in the forward-looking state-

ments. The Company is exposed to market risk related to

changes in interest rates, foreign currency exchange rates, and

commodity prices.

~ 25 ~

Interest Rate Risk. The fair value of the Company’s cash and

short-term investment portfolio at April 30, 2008, approxi-

mates carrying value. Exposure to interest rate risk on the

Company’s long-term debt is mitigated since it is at a fixed rate

until maturity. Market risk, as measured by the change in fair

value resulting from a hypothetical 10 percent change in inter-

est rates, is not material. Based on the Company’s overall

interest rate exposure as of and during the year ended April 30,

2008, including derivative and other instruments sensitive to

interest rates, a hypothetical 10 percent movement in interest

rates would not materially affect the Company’s results of

operations. A hypothetical 100 basis point increase in short-

term interest rates would increase the Company’s interest

expense by approximately $0.1 million. Interest rate risk can

also be measured by estimating the net amount by which the

fair value of the Company’s financial liabilities would change as

a result of movements in interest rates. Based on a hypotheti-

cal, immediate 100 basis point decrease in interest rates at

April 30, 2008, the fair value of the Company’s long-term debt

and interest rate portfolio, in aggregate, would increase by

approximately $41.3 million.

Foreign Currency Exchange Risk. The Company has operations

outside the United States with foreign currency denominated

assets and liabilities, primarily denominated in Canadian cur-

rency. Because the Company has foreign currency denomi-

nated assets and liabilities, financial exposure may result,

primarily from the timing of transactions and the movement of

exchange rates. The foreign currency balance sheet exposures

as of April 30, 2008, are not expected to result in a significant

impact on future earnings or cash flows.

Revenues from customers outside the United States repre-

sented 13 percent of net sales during 2008. Thus, certain rev-

enues and expenses have been, and are expected to be, subject

to the effect of foreign currency fluctuations and these fluctua-

tions may have an impact on operating results.

Commodity Price Risk. Raw materials and other commodities

used by the Company are subject to price volatility caused by

supply and demand conditions, political and economic vari-

ables, and other unpredictable factors. To manage the volatility

related to anticipated commodity purchases, the Company

uses futures and options with maturities generally less than

one year. Certain of these instruments are designated as cash

flow hedges. The mark-to-market gains or losses on qualifying

hedges are included in other comprehensive income to the

extent effective, and reclassified into cost of products sold in

the period during which the hedged transaction affects earn-

ings. The mark-to-market gains or losses on nonqualifying,

excluded, and ineffective portions of hedges are recognized in

cost of products sold immediately.

The following sensitivity analysis presents the Company’s

potential loss of fair value resulting from a hypothetical 10 per-

cent change in market prices.

Year Ended April 30,

(Dollars in thousands) 2008 2007

Raw material commodities:High $13,229 $4,514Low 3,289 1,333Average 8,474 3,105

Fair value was determined using quoted market prices and was

based on the Company’s net derivative position by commodity

at each quarter end during the fiscal year. The calculations are

not intended to represent actual losses in fair value that the

Company expects to incur. In practice, as markets move, the

Company actively manages its risk and adjusts hedging strate-

gies as appropriate. The commodities hedged have a high

inverse correlation to price changes of the derivative com-

modity instrument; thus, the Company would expect that any

gain or loss in fair value of its derivatives would generally be

offset by an increase or decrease in the fair value of the under-

lying exposures.

Forward-Looking Statements

✷✷✷

Certain statements included in this Annual Report contain for-

ward-looking statements within the meaning of federal securi-

ties laws. The forward-looking statements may include

statements concerning the Company’s current expectations,

estimates, assumptions, and beliefs concerning future events,

conditions, plans, and strategies that are not historical fact.

Any statement that is not historical in nature is a forward-look-

ing statement and may be identified by the use of words and

phrases such as “expects,” “anticipates,” “believes,” “will,”

“plans,” and similar phrases.

Federal securities laws provide a safe harbor for forward-look-

ing statements to encourage companies to provide prospective

information. The Company is providing this cautionary state-

ment in connection with the safe harbor provisions. Readers

are cautioned not to place undue reliance on any forward-look-

ing statements as such statements are by nature subject to

risks, uncertainties, and other factors, many of which are out-

side of the Company’s control and could cause actual results to

differ materially from such statements and from the

Company’s historical results and experience. These risks and

uncertainties include, but are not limited to, those set forth

under the caption “Risk Factors” in the Company’s Annual

Report on Form 10-K, as well as the following:

general economic conditions in the U.S.;

the volatility of commodity markets from which rawmaterials are procured and the related impact on costs;

crude oil price trends and its impact on transportation,energy, and packaging costs;

the ability of the Company to successfully implementprice changes;

~ 26 ~

the success and cost of introducing new products andthe competitive response;

the success and cost of marketing and sales programsand strategies intended to promote growth in theCompany’s businesses, and in their respective markets;

general competitive activity in the market, includingcompetitors’ pricing practices and promotional spendinglevels;

the concentration of certain of the Company’s busi-nesses with key customers;

the ability of the Company to manage and maintain keycustomer, supplier, and employee relationships;

the loss of significant customers or a substantial reduc-tion in orders from these customers or the bankruptcyof any such customer;

the ability of the Company to obtain any required financ-ing;

the timing and amount of capital expenditures andrestructuring, and merger and integration costs;